services trade in nepal: a comparative case study of banking and insurance...

TRANSCRIPT

Services Trade in Nepal: A Comparative Case Study of Banking and Insurance Sectors

D. R. KhanalInstitute for Policy Research and Development

(IPRAD)

Scope of the StudyBriefly assess the liberalization policies perused in the banking and insurance sectors especially since 1990s, Examine the strengths and weaknesses of the banking and insurance sector liberalization in the light of their contribution in raising efficiency and competitiveness,Make comparative assessment on the role of joint venture, private and government owned banks and insurance companies promoting business and enhancing access to credit with special focus on gender dimension, Explore the possibility of enhancing the role of banking and insurance services in the Nepalese economy and chalk out strategies to be appropriate in the preferential trade agreements especially to the LDC countries like Nepal.

Methodology an analytical approach for examining the features of banking and insurance sector liberalization and reviewing their strengths and weaknesses,quantitative analysis for assessing the efficiency of banking and insurance sectors as well as examining the effect on access to services and employment creation, a case study of banking sector (one each from government owned, domestically private sector owned and joint venture banks) to look into the impact on efficiency, access to credit and employment in a comparative way.

Financial Sector Liberalization: Driving Forces and Present Status

Driving ForcesUnilateral Regional Commitments Multilateral Routes (WTO)

Although, prior to the accession to the WTO in April 2004, Nepal’s financial liberalization was carried out by the government unilaterally, donors were mainly instrumental. The first phase of financial liberalization which began in mid 1980 was influenced by the conditions laid down in the Structural Adjustment Program (SAP) of the WB and IMF. The second phase of wide ranging liberalization which began in the early 1990s was driven by the conditions incorporated in the Enhanced Structural Adjustment Facility (ESAF) Program of the IMF. Wave of liberalization including liberalization in India also contributed to the liberalization drive in Nepal.

Some of the major reforms carried out before accession to the WTO include

Interest rate deregulationPermission to establish banks and insurance companies in the private sector including foreign equity participation up to 66 percent in banks and 100 percent in insurance sector in a case by case basis. Phasing out of private sector lending by 2007.Enactment of various laws including Nepal Rastra Bank Act 2002, Debt Recovery Act 2002 and now Bank and Financial Institutions Act 2006 aimed primarily at enhancing prudential rules and regulations in the financial institutions and raising competitive strength.

So far no major commitments under SAFTA and BIMESTC. However, SAARC member countries have decided to include service trade within the free trading framework and a decision on this respect is expected in coming month. More importantly, Nepal has made certain commitments under WTO membership obligation having far reaching implications on further opening up the banking and insurance sector. Accordingly, Nepal must allow foreign wholesale banking and insurance by 1st January, 2010.

Some Specific Policy MeasuresRules on Ownership

In general, at least 51 percent ownership should be occupied by promoters to establish any bank and financial institutions. At least 30 percent shares of total paid up capital should be allocated for general public.

Rules on LocationTo establish a commercial bank operating all over Nepal, the paid up capital must be at least Rs 1 billion. For outside the Kathamdnu paid up capital must be Rs. 320 million.

Legal FormsBanks to be established with foreign promoters' participation have also to be registered fulfilling all the legal processes prescribed by the prevalent Nepal laws. For the establishment of Joint Venture Bank, the share capital of foreign joint venture bank should be at least 20 percent and it can't exceed 75 percent ( banks which are already operating in Nepal, otherwise two third at the most) of total paid up capital.

Branching The Commercial banks established with a head office in Kathmandu are authorized to open a main branch office in the Valley initially and thereafter one more branch in Kathmandu Valley and then only branches outside Kathmandu Valley.

Rules on EmploymentThere are no specific rules and regulations that are required to be incorporated in the rules of employment. For employment to the foreigners separate technical agreement is required.

Prudential RegulationsRules and regulation directives of the central bank. Which include (I) Maintenance of capital adequacy, (ii) Loan classification & loan loss provisioning, (iii) Limit of credit exposure and facilities to single borrower, group of related borrowers and single sector of the economy, (iv) Accounting policies and formats of financial statements, (v) Minimization of risk, (vi) Corporate governance, (vii) Time-frame for implementation of regulatory directives issued in connection with inspection & supervision of the banks, (viii) Investment in shares & securities, (ix) Statistical reporting by commercial banks to NRB and (x) Sale and transfer of promoters share (xi) Provision related with Consortium financing (xii) Provision for blacklisting (xiii) Maintenance of Cash reserve ratio (xiv) Provisions for bank branches (xv) Provisions relating interest rate (xvi) Provisions related with financial resource collection.

Off-Site Inspection Special InspectionOn-Site Inspection

InsuranceThe Insurance Act, 1992 and Insurance Regulation, 1993 are the main guidelines for the administration of the insurance industry in Nepal. There is no restriction on pattern of ownership, location of business inside the country and in legal forms. However, in case of foreign joint venture, 20 percent of the share should be issued to the public for general subscription. The insurer is not allowed to operate life insurance and non-life insurance business side by side through the same organization. There is a provision in the Insurance Act, 1992 that the Insurance Board may cancel the registration of an insurance company in thecircumstances if the head office of the insurance business of any foreign insurer is situated out side Nepal, and in case it is felt that Nepalese insurer has not obtained equal facilities while operating in the foreign countries as enjoyed by the foreign insurer pursuant to the prevailing law of such country.

OperationsThe insurer may operate life insurance business under (a) whole life insurance (b) endowment life insurance and (c) term life insurance The foreign investor making an investment in foreign currency shall be entitled to repatriate share of equity, profit or dividend, and also principal and interest on foreign loan. The Insurance Board formulates policies for systematizing, regulating, developing and controlling insurance business.

Exchange Rate PolicyNepal constantly is following two sets of policies regarding the exchange rate-one for the IC and another for convertible currencies. The liberalization of the exchange rate gained momentum after India introduced partial convertibility of the current account in 1993. Nepal accepted the Article VIII of the IMF in 1993 and thereby fully liberalized the current account. Now convertible currency rate is market determined. However, Nepal has not been able to liberalize exchange rate with India despite misalignment of the prices hurting business competitiveness of Nepal.

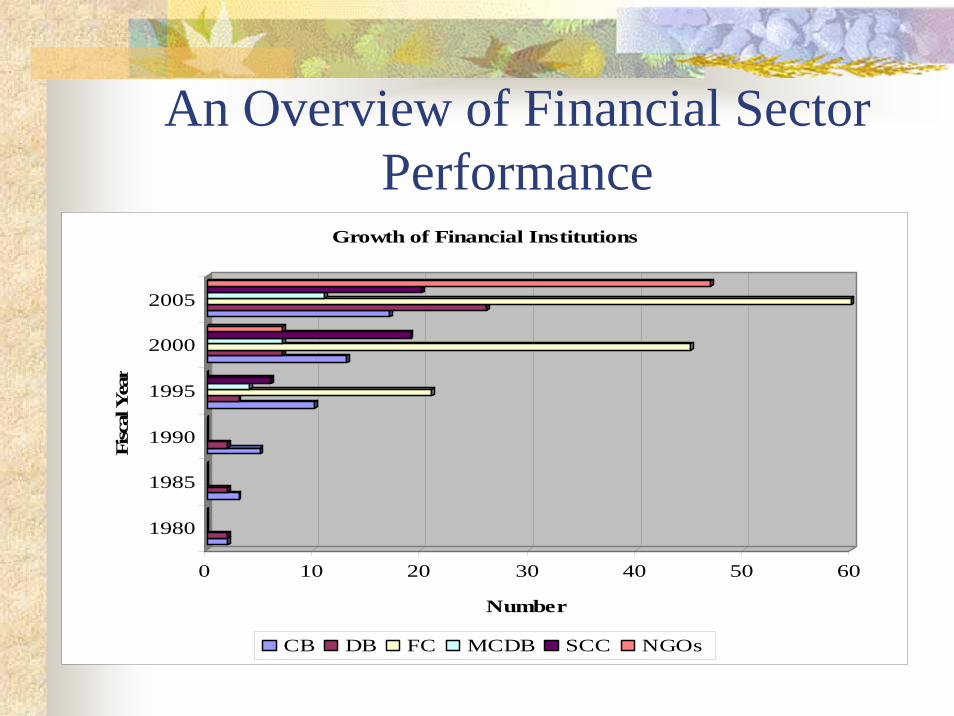

An Overview of Financial Sector Performance

0 10 20 30 40 50 60

Number

1980

1985

1990

1995

2000

2005

Fisc

al Y

ear

Growth of Financial Institutions

CB DB FC MCDB SCC NGOs

Total Assets of Financial Institutions (Mid- July 2005)

CB87%

Others(Cooperatives and NGOs)

1%MCDB1%

DB5%

FC6%

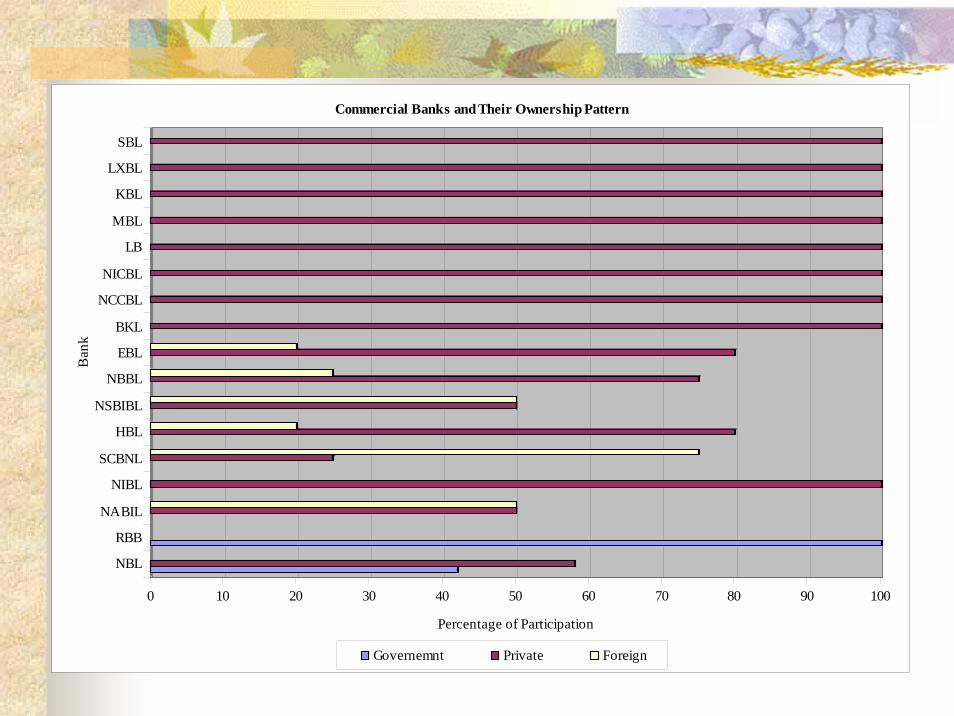

0 10 20 30 40 50 60 70 80 90 100

Percentage of Participation

NBL

RBB

NABIL

NIBL

SCBNL

HBL

NSBIBL

NBBL

EBL

BKL

NCCBL

NICBL

LB

MBL

KBL

LXBL

SBL

Ban

k

Commercial Banks and Their Ownership Pattern

Governemnt Private Foreign

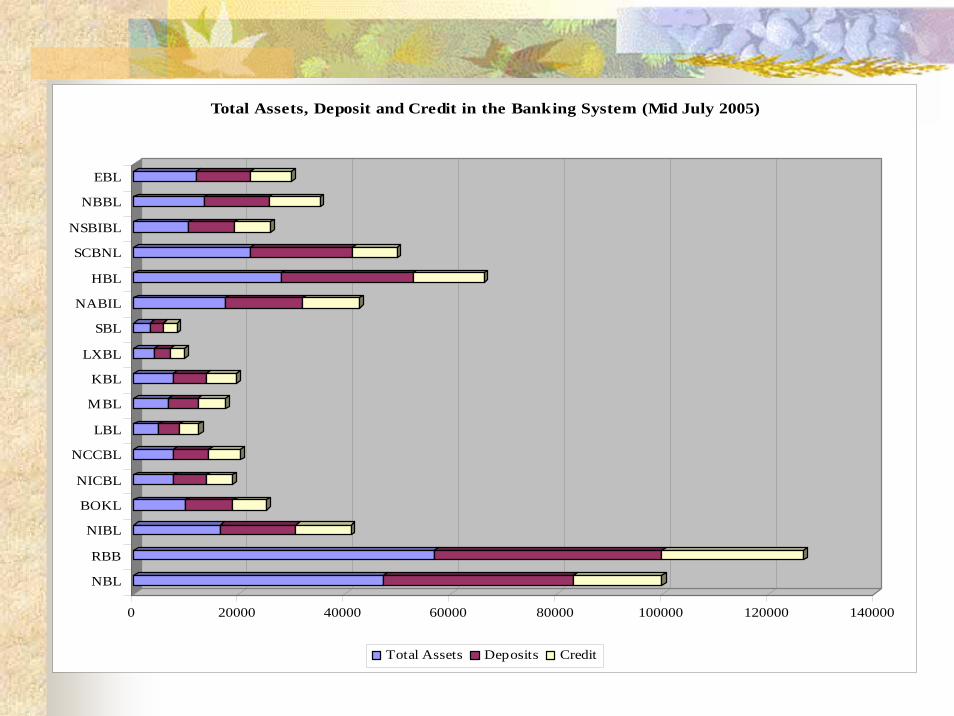

0 20000 40000 60000 80000 100000 120000 140000

NBL

RBB

NIBL

BOKL

NICBL

NCCBL

LBL

MBL

KBL

LXBL

SBL

NABIL

HBL

SCBNL

NSBIBL

NBBL

EBL

Total Assets, Deposit and Credit in the Banking System (Mid July 2005)

Total Assets Deposits Credit

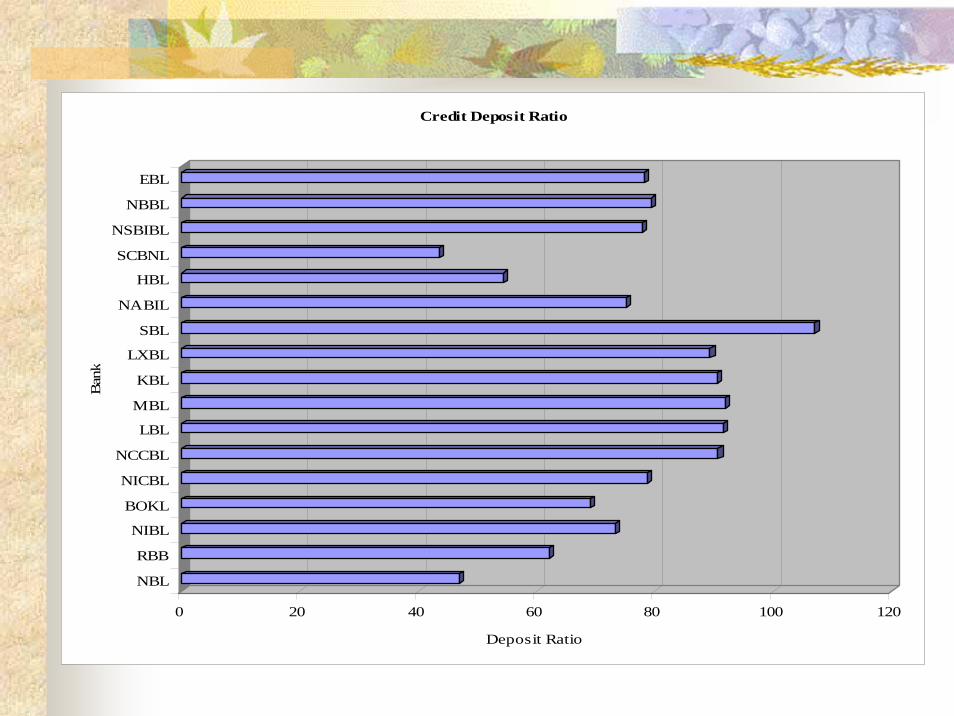

0 20 40 60 80 100 120

Deposit Ratio

NBL

RBB

NIBL

BOKL

NICBL

NCCBL

LBL

MBL

KBL

LXBL

SBL

NABIL

HBL

SCBNL

NSBIBL

NBBL

EBL

Ban

kCredit Deposit Ratio

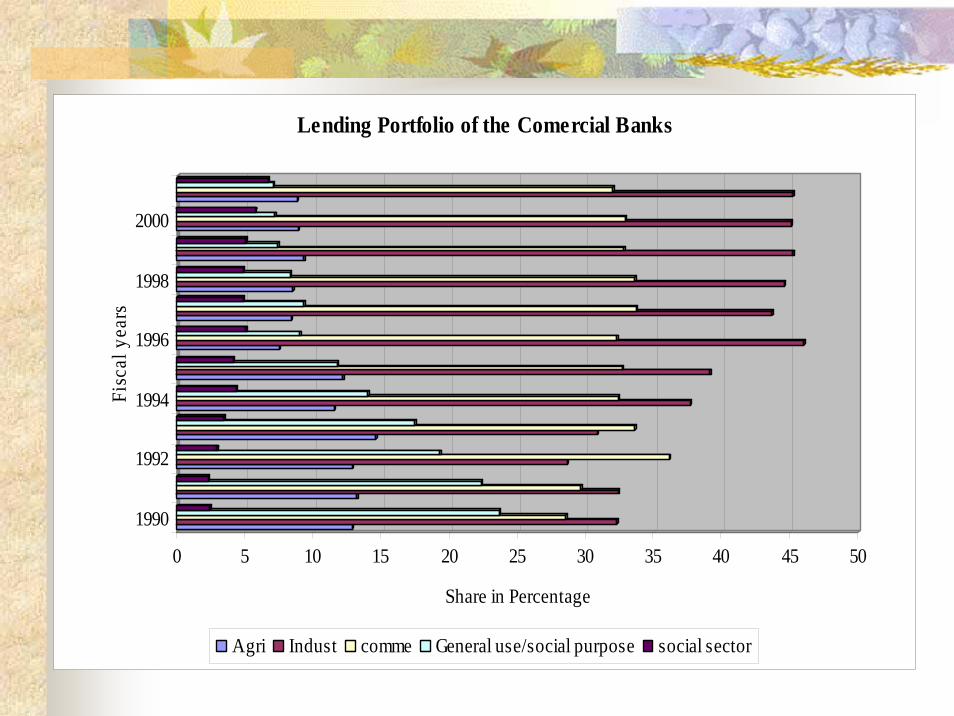

0 5 10 15 20 25 30 35 40 45 50

Share in Percentage

1990

1992

1994

1996

1998

2000

Fisc

al y

ears

Lending Portfolio of the Comercial Banks

Agri Indust comme General use/social purpose social sector

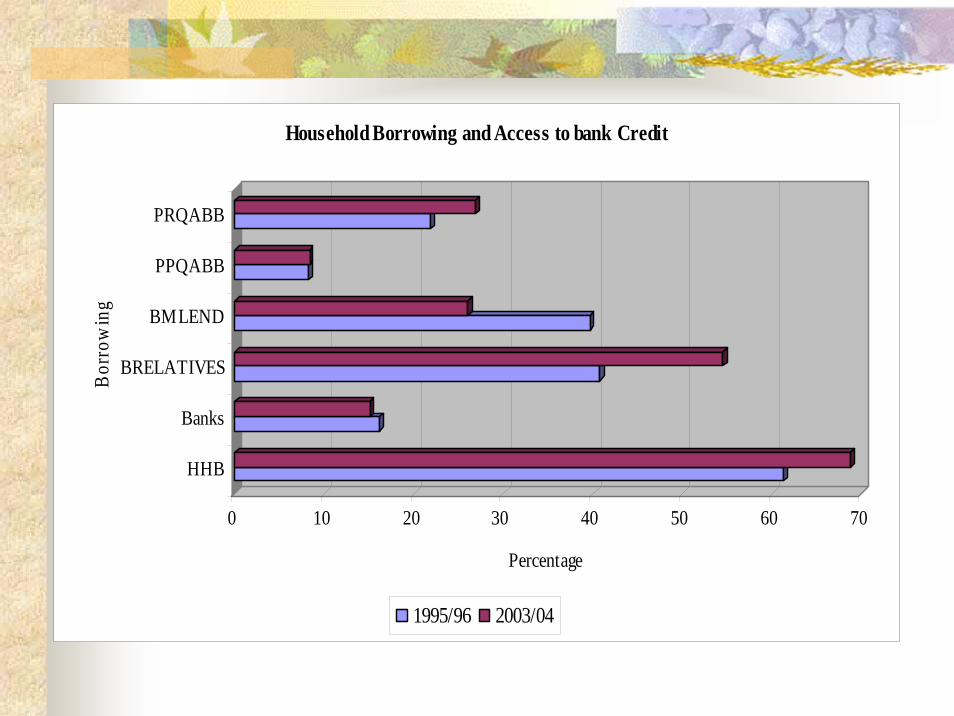

0 10 20 30 40 50 60 70

Percentage

HHB

Banks

BRELATIVES

BMLEND

PPQABB

PRQABB

Bor

row

ing

Household Borrowing and Access to bank Credit

1995/96 2003/04

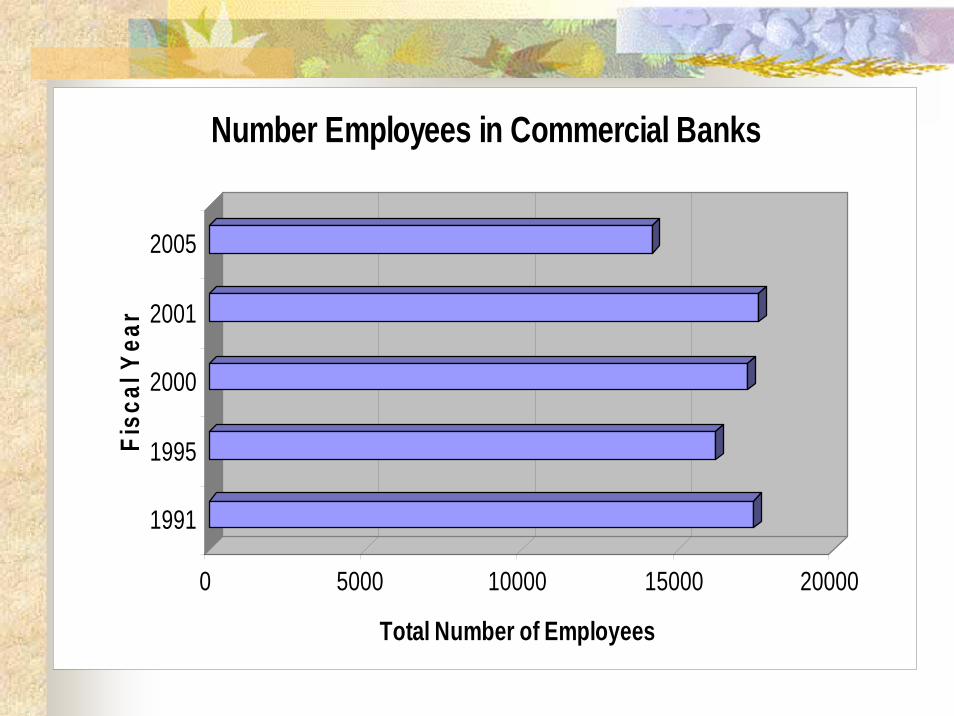

0 5000 10000 15000 20000

Total Number of Employees

1991

1995

2000

2001

2005

Fisc

al Y

ear

Number Employees in Commercial Banks

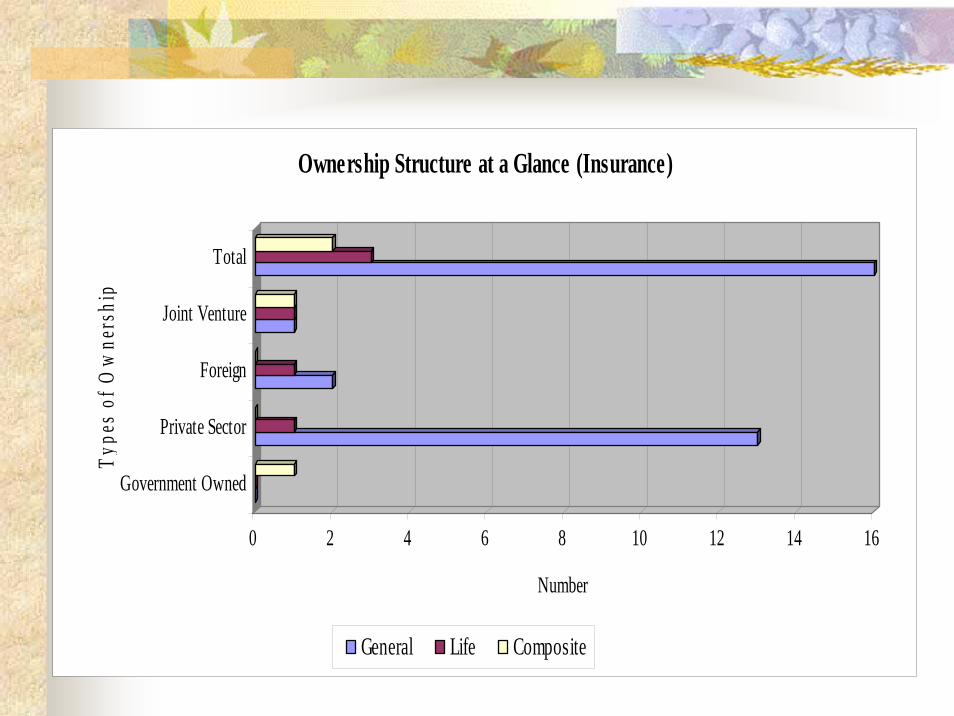

0 2 4 6 8 10 12 14 16

Number

Government Owned

Private Sector

Foreign

Joint Venture

Total

Type

s of

Ow

ners

hip

Ownership Structure at a Glance (Insurance)

General Life Composite

0 5 10 15 20 25 30 35

Percentage

1996

1997

1998

1999

2000

2001

2002

2003

Fisc

al y

ears

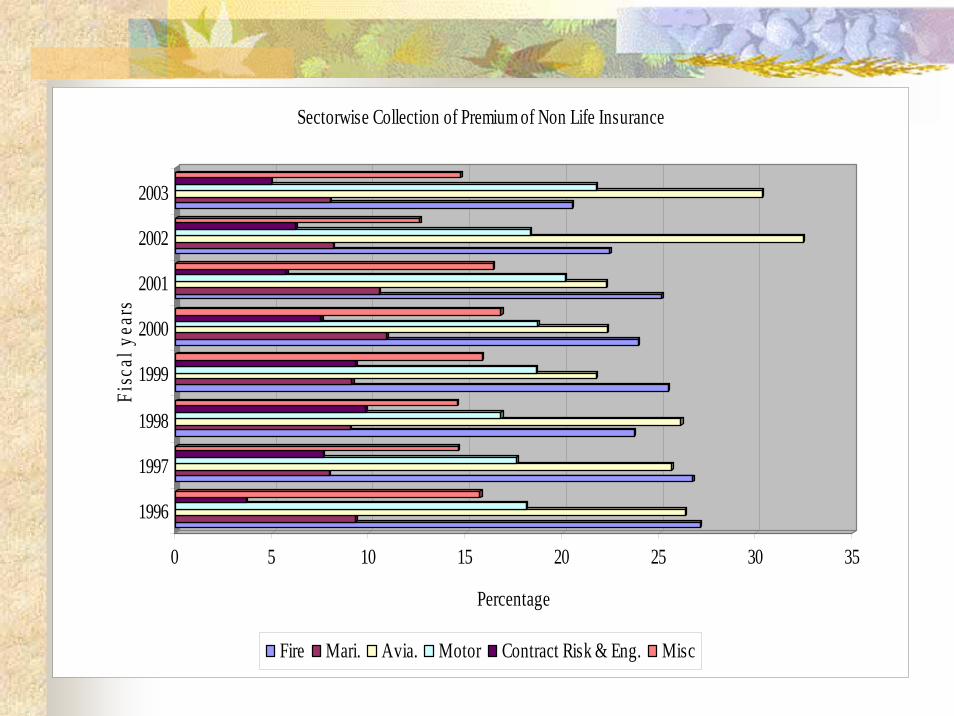

Sectorwise Collection of Premium of Non Life Insurance

Fire Mari. Avia. Motor Contract Risk & Eng. Misc

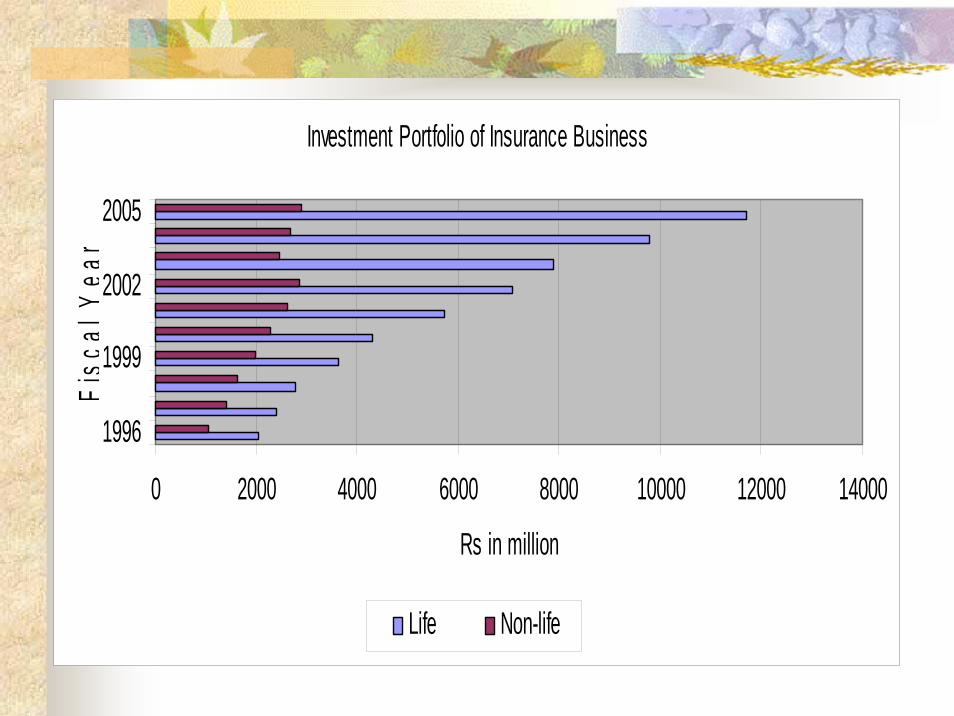

Investment Portfolio of Insurance Business

0 2000 4000 6000 8000 10000 12000 14000

1996

1999

2002

2005

Fisc

alY

ear

Rs in million

Life Non-life

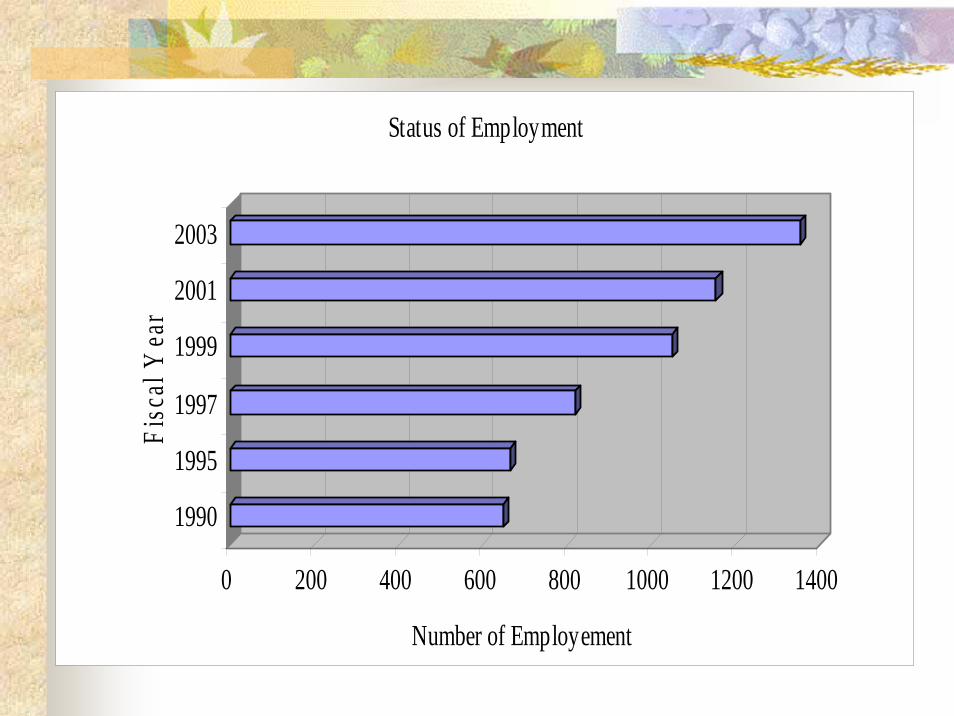

0 200 400 600 800 1000 1200 1400

Number of Employement

1990

1995

1997

1999

2001

2003

Fisc

al Y

ear

Status of Employment

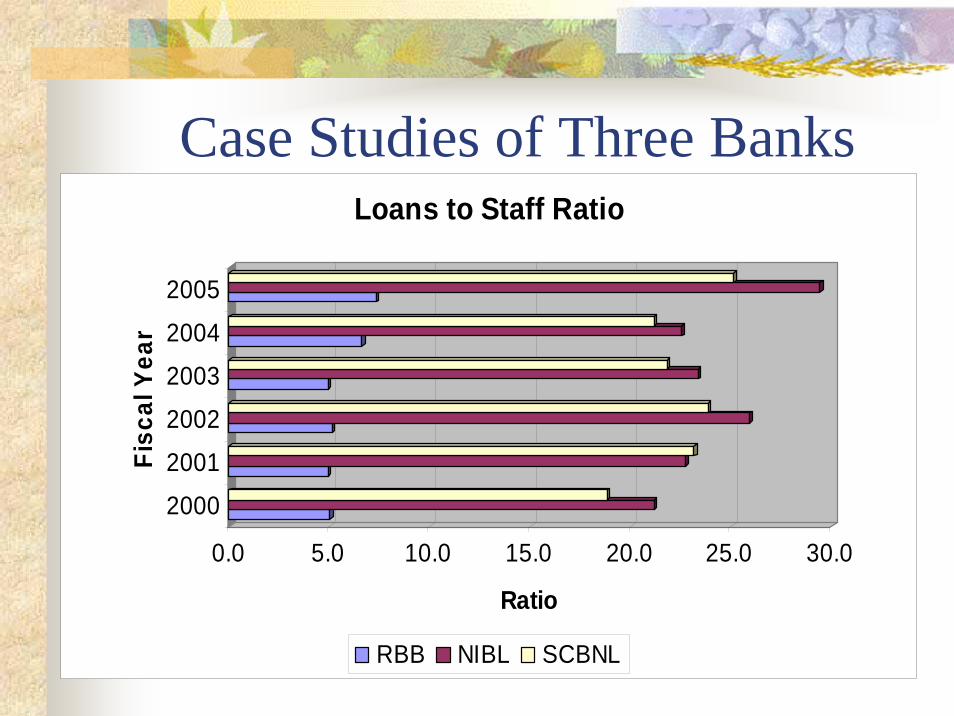

Case Studies of Three Banks

0.0 5.0 10.0 15.0 20.0 25.0 30.0

Ratio

2000

2001

2002

2003

2004

2005

Fisc

al Y

ear

Loans to Staff Ratio

RBB NIBL SCBNL

0 10 20 30 40 50 60 70

Percentage

2000

2001

2002

2003

2004

2005

Yea

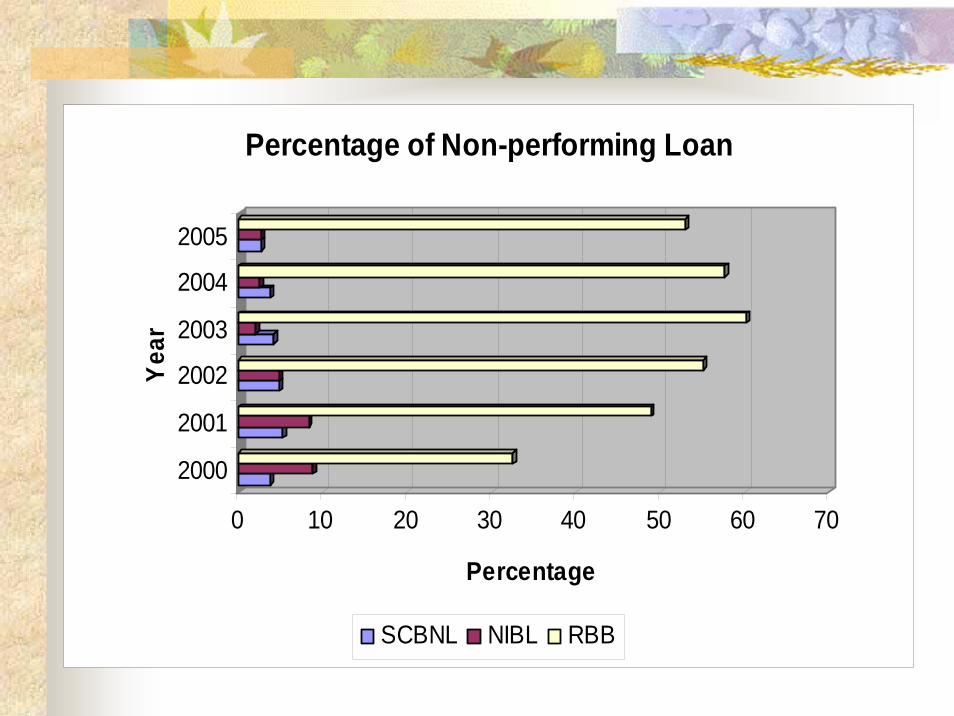

rPercentage of Non-performing Loan

SCBNL NIBL RBB

0 20 40 60 80 100

2000

2001

2002

2003

2004

2005

Fisc

al Y

ear

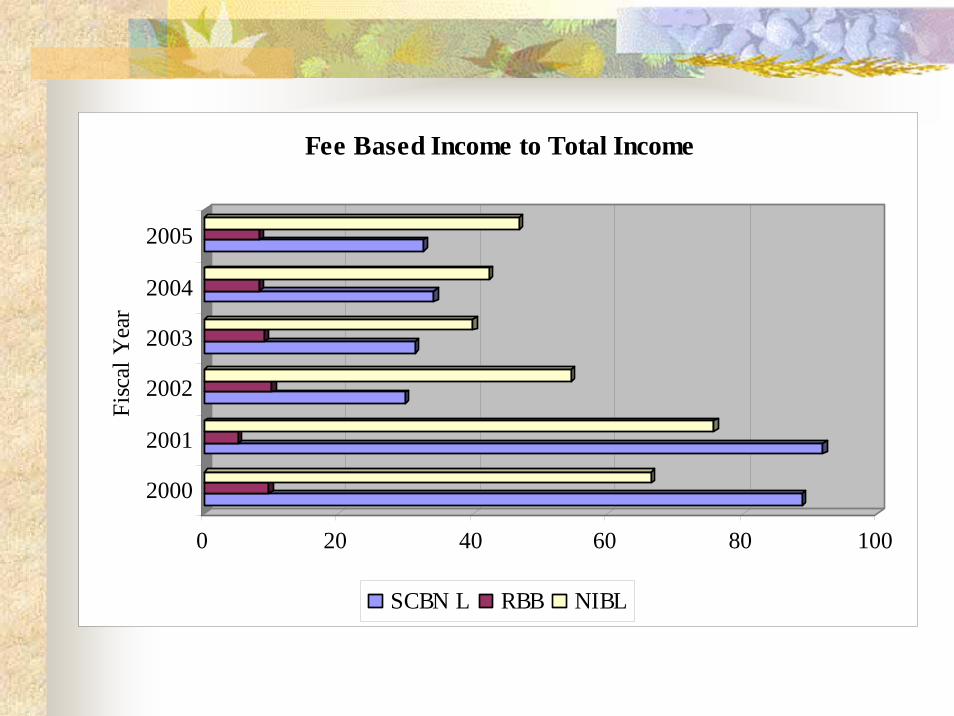

Fee Based Income to Total Income

SCBN L RBB NIBL

0 1 2 3 4

2000

2001

2002

2003

2004

2005

Fisc

al Y

ear

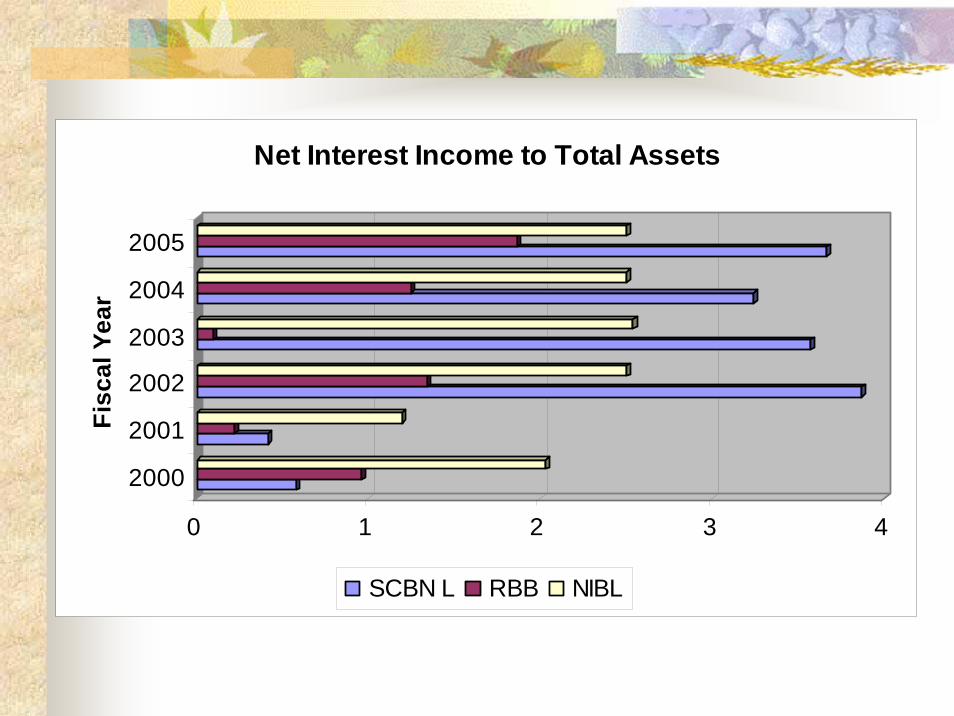

Net Interest Income to Total Assets

SCBN L RBB NIBL

0 5 10 15 20 25 30 35 40 45 50

2001

2003

2005

Fisc

al y

ear

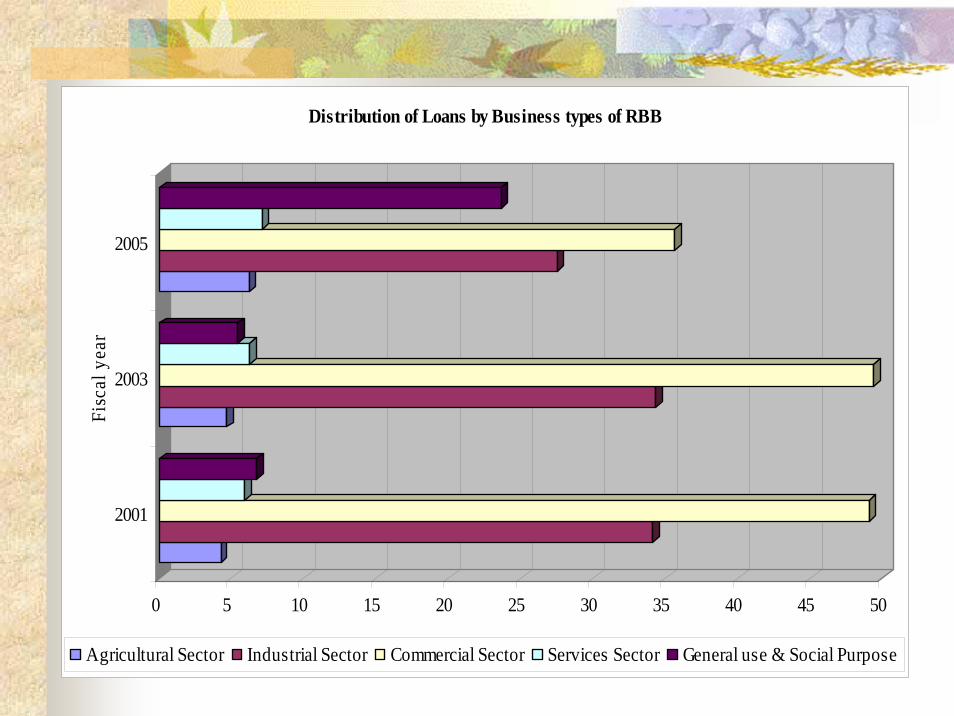

Distribution of Loans by Business types of RBB

Agricultural Sector Industrial Sector Commercial Sector Services Sector General use & Social Purpose

0 5 10 15 20 25 30 35 40 45

Share

2001

2003

2005

Fisc

al y

ear

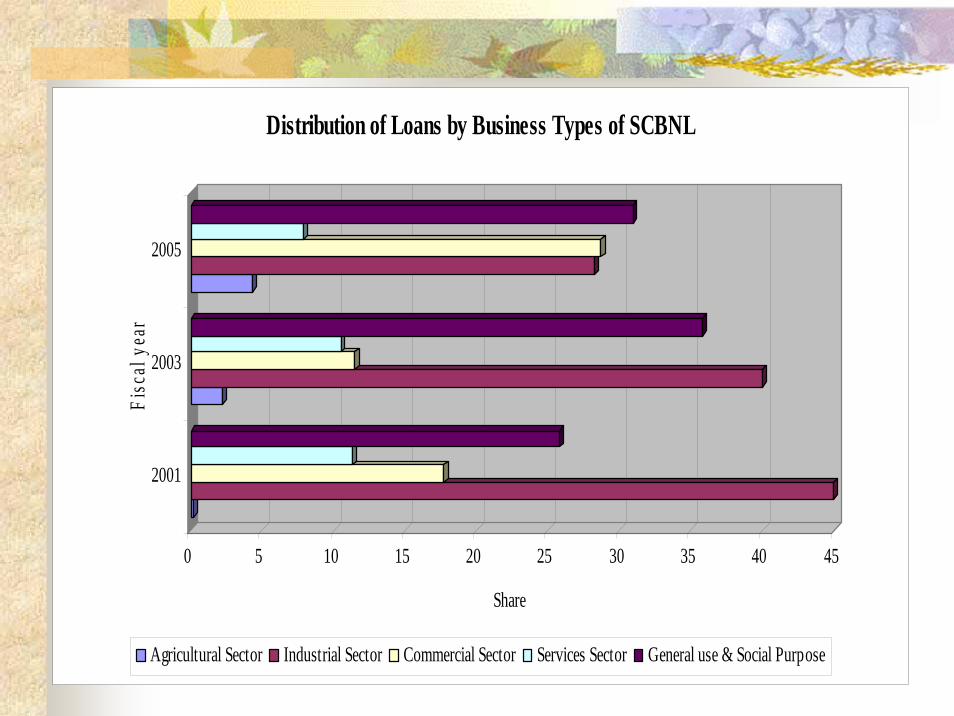

Distribution of Loans by Business Types of SCBNL

Agricultural Sector Industrial Sector Commercial Sector Services Sector General use & Social Purpose

0 10 20 30 40 50 60 70

Share

2001

2003

2005

Fisc

al Y

ear

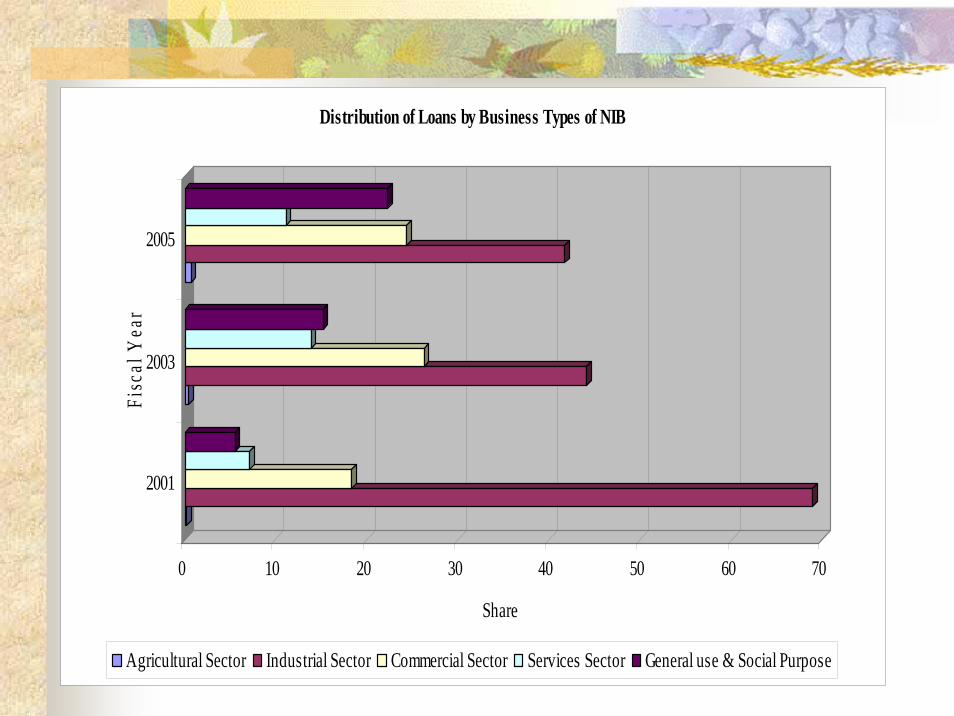

Distribution of Loans by Business Types of NIB

Agricultural Sector Industrial Sector Commercial Sector Services Sector General use & Social Purpose

InnovationBanks are engaged in developing new products and services. Most of the banks now use swift and Epabx for speedy banking transactions. Banks are also providing limited Internet banking facilities. Further extension will take place after the introduction of Cyber law in Nepal. Auto loan, home loan, education loan, employment loan, debit card, VISA and Master Card are increasingly becoming popular products of the commercial banks.

Internet Transactions vs Other the CounterBanks have started to make certain banking transactions through internet banking. Mobile banking is used for balance enquiry, statement of transactions, alert notice etc. In general more than 98 percent of banking transactions are made over the counter. Now banks have started providing services of ATM, payment of electricity bill, telephone bill etc.

Risk Management in Commercial BankVery few banks have developed consumer scoring model on their own but it is not a major criteria for the purpose of providing loans or provisioning the loan losses. The advanced form of loan grading and credit portfolio management models are not used in the commercial banks. Only very few banks do have their internal risk based provisioning model. The risk based provisioning model is not used in Nepal.

Conclusions and Implication for Managing Change

ConclusionBoth industry and trade have been beneficiary of banking and insurance sector liberalization. Profitability ratio, margins, spread rate, fee based income to total income ratio, interest income to total assets ratio and labor productivity in the form of loan to labor ratio indicate that efficiency of the private and joint venture banks has greatly enhanced. They have employed a large number of people overtime. However, an assessment of the entire banking system by including two government owned banks gives completely a different but disappointing picture. Studies show that these twobanks became technically insolvent in 2002 as the share of non-performing assets in these banks reached about 60 percent of thetotal assets. The huge negative net worth and profitability has had very severe adverse effect on the entire financial system.

Although after contracting out the two banks to the foreign companies some improvements in their performance has taken place, adverse employment implication has been very large. The deepening crisis in these banks has undermined the good performance demonstrated by the private domestic and joint venture banks. Access to the credit among the rural populous has decreased over times. Similarly, the private domestic and foreign joint venture banks have almost confined their investment in the urban center with priority on lucrative business. As a result, despite huge expansion in their investment the productive areas have been least benefited. This is true in case of insurance companies also. The investment portfolio of such companies reveals that most of their funds are kept in fixed deposit.

Implications for Policy Design and ImplementationUnilateral move under the external influence without rigorous domestic analysis examining the pros and cons would have very adverse effect on enhancing competition and ensuring healthy development of the financial sector. Particularly, enactment of laws, development of institutional capacity both in central and concerned banks in terms of strengthening regulatory system would be a key in this respect. One important implication from the policy design perspective is that unless excessive influence of the state in government run banks or insurance companies is stopped and restructuring is started simultaneously that would have negative spill over effect on theentire financial system. As the multilateral route through WTO compels to introduce various acts in the course of meeting WTO obligations, it would help enhancing institutional and technical capacity. Hence, the multilateral route could be more viable and effective.

Managing ChangeStrong curative as well as preventive measures for improving the performance of the two banks is warranted. While introducing measures, restructuring of two commercial banks at a faster pace along with strong steps to reduce NPAs will need top most priority. Likewise, bank capitalization, implementation of regulations effectively, improvement in risk management, better governance including rules to promote transparency and strengthening the capacity of the supervisory authority would be essential. Accountability, transparency and strict financial discipline are critically important in the whole reform and or restructuring process. Introduction of new products and diversification of financial services will also be essential to improve the financial health of the banking system.

Reduction of transaction cost is necessary. For this efficiency not only in business service but also in the physical infrastructure and other support services would be essential. There is a necessity of timely fulfillment of the WTO commitments. Strengthening of financial laws by promulgating bank rules, banking fraud control laws, Asset Securitization law and Trustee law, among others would be essential. Nepal has to allow foreign wholesale banking by 2010. On the other; the problems are magnifying in the banking system. Therefore, Nepal’s experience so far indicates that either review of deadline or some support measures would be essential.

In view of access to credit among the rural populous decreasing on the one hand and restructuring of banks making very adverse effects on employment on the other, consideration of some safeguard measures in the international trade forums for the LDCs like Nepal would be essential. WTO obligations insurance sector needs various reforms like; (i) strengthening of legal, regulatory and supervisory frameworks, (2) maintenance of soundness in operational and management of insurance institutions, (3) introduction of dispute settlement mechanism and strengthening of capital base, (4) exploration of reinsurance business (5) deepening of service reach to the general masses, (6) capacity enhancement and integration among the insurance companies and (7) reforms in activities of state owned insurance institutions.

THANK YOU.