session 1: introduction - university of warwick in economics from trinity college dublin msc, mres...

TRANSCRIPT

Session 1: Introduction

Michael McMahon

University of Warwick

McMahon (University of Warwick) Introduction 1 / 22

To Cover

1 The Abouts2 Syllabus3 Assignments and Grading4 Some philosophical points about Economics

McMahon (University of Warwick) Introduction 2 / 22

The Abouts

About you and about me

About the course in general

Resources

McMahon (University of Warwick) Introduction 3 / 22

The AboutsAbout you and about me

Dr. Michael McMahon

Biographical information:

IrishBA in Economics from Trinity College DublinMSc, MRes and PhD in Economics from London School of EconomicsWorked as a professional economist for the Bank of England, ECB, andCentral Bank of IrelandTaught for Warwick, LSE, NYU and University of Chicago.

Your name, your area of work, your economics and statisticsbackground, and your chance to ask me any questions about me.

McMahon (University of Warwick) Introduction 4 / 22

The AboutsAbout the course

1 Lectures (40%)2 Class Discussion of Relevant Literature and current situation (40%)3 Computer Based Work (20%)

McMahon (University of Warwick) Introduction 5 / 22

The AboutsAbout the course

Economist Article....the measure of your learning.

McMahon (University of Warwick) Introduction 6 / 22

The AboutsAbout the course

There are 3 main themes to be covered in the course:

1 Macroeconomic Theory;2 Money, banking and the �nancial system (including the current crisisand policy responses);

3 Macroeconomic indicators and an introduction to the use of statisticsin macroeconomics.

McMahon (University of Warwick) Introduction 7 / 22

The AboutsAbout the timetable - Day 1

The Basic Real Business Cycle Model (Theme 1)

Introducing the RBC modelDiscussing the costs of business cycles and the argument forstabilisation policyMeasuring business cycles using data (computer based work)Understanding and interpreting macroeconomic indicators

The economics of sectoral diversi�cation (Theme 1)

Bene�ts of diversi�ed economiesHow di¤erent sectors behave over the business cycle and economicadjustment across sectors

A brief introduction to forecasting and factor models (Theme 3)

the eurocoin indicator of the CEPR

McMahon (University of Warwick) Introduction 8 / 22

The AboutsAbout the timetable - Day 2

Evening / Overnight Problem: Full problem set details to beprovided but expected to be done in 30 - 90 minutes.

Money and Banking (Theme 2)

The basics of the �nancial system including the main instrumentsWhy the current crisis? Focus on the concept of leverage and balancesheet e¤ects.Fiscal policy response including a discussion of how �scal policyoperates in the economy.A brief discussion of monetary policy including models of monetarypolicyClass discussion of the liquidity trap, the zero nominal bound oninterest rates and �quantitative easing�

McMahon (University of Warwick) Introduction 9 / 22

The AboutsAbout the timetable - Day 3

Evening / Overnight Problem: To be decided - likely to considerthe issues of oil and monetary unions (full problem set details to beprovided but expected to be done in 30 - 90 minutes).Basic approaches to the labour market (Theme 1)

Search and Matching Models of the Labour MarketE¤ects of labour market regulation

The Macroeconomic E¤ects of Oil (Theme 1)How oil a¤ects the economyAnalysing the e¤ects of oil in the US and EUThe e¤ects of oil in oil-exporting countries

The Economics of Customs Unions (Theme 1)The bene�ts of customs unionsA brief introduction to the new economic geography (Krugman andVenables)Discussion of the GCC

McMahon (University of Warwick) Introduction 10 / 22

The AboutsResources

Lectures

Course pack

http://www2.warwick.ac.uk/fac/soc/economics/staff/faculty/mcmahon/adced_course

Macroeconomic data

The Economist magazine, The FT, WSJ, etc...

McMahon (University of Warwick) Introduction 11 / 22

Grading

Students will be assessed on 5 criteria:

Understanding of the theoretical components of the course

Understanding of the practical components of the course

Ability to combine the theoretical and practical elements of the coursein answers/project;

Communication of ideas � these should be both concise and clear;

Attitude to fellow students and the lecturer.

McMahon (University of Warwick) Introduction 12 / 22

GradingGrade expectations

Top Marks: The student has an excellent understanding of the materialcovered within the lectures of the course. Moreover, the student has shownan ability to think beyond the basic material and to relate the sessions toone another in a highly perceptive way. Moreover, this student understandsthe limitations of the analytical tools developed in the course. The studentpresents ideas, both written and orally, in a clear and concise manner. Inboth class participation and also other interactions with the student, (s)hedisplays an excellent attitude; receptive to comments and eager to learn.

McMahon (University of Warwick) Introduction 13 / 22

GradingGrade expectations

Middle Grade: Good understanding with some lack of clarity on eithertheoretical or empirical issues. Presentation of ideas may be moreambiguous or less well structured. Nonetheless, the student is clearlymotivated and works well within the course.

McMahon (University of Warwick) Introduction 14 / 22

GradingGrade expectations

Lower Grade: The student has only partial understanding of some areasof the course. This leads to greater ambiguities in his/her presentation ofideas.

McMahon (University of Warwick) Introduction 15 / 22

Grading

Each participant will be individually assessed via the following:

1 Two "within course" problem sets (20 points)

these short problems will involve the use of data from large databasessuch as FRED database at the St. Louis Fed, IMF and World Bankdatabases, or ILO data.each problem will be submitted by individual participants and will beworth up to 10 points.

2 2-week individual research exercise (80 points)

Assignment provided at the end of the course

McMahon (University of Warwick) Introduction 16 / 22

Basics Concepts You Must Be Aware OfGDP - Real versus Nominal Concepts

Nominal GDP in year t =N

∑i=1pit .qit (1)

Real GDP (year K prices) in year t =N

∑i=1piK .qit (2)

De�ning the price level as a de�ator

Base Z de�atort =nominal GDPt

(real GDP in year Z prices)t(3)

Calculating growth

Growth between t and t + 1 =

�Xt+1Xt

� 1�

(4)

� lnXt+1 � lnXtMcMahon (University of Warwick) Introduction 17 / 22

Philosophical Points about Economics

Economics is a way of thinking - not a set of laws and rules

This framework for thinking can then be applied to many topics

Freakonomics

Empirical work is very tricky

LSE (my alma mater!) - motto is "Rerum Cognoscere Causas"

The following material is just for fun, but the frame of mind that theexercise highlights is all important for economics.

McMahon (University of Warwick) Introduction 18 / 22

Philosophical Points about Economics

McMahon (University of Warwick) Introduction 19 / 22

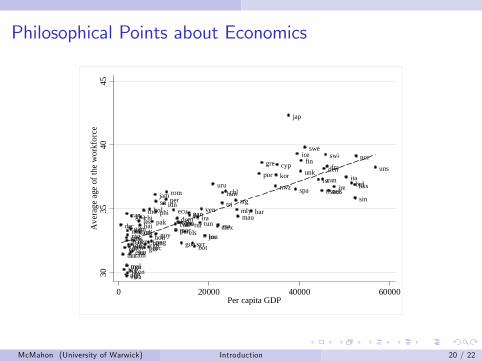

Philosophical Points about Economics

drc

tan

bur

eth

ngr

mlw

maluga

mad

car

rwa

nigmoz

bur

togben

gam

zam

ken

sil

cha

gha

angsennepcam

lescdihaichi

ind

guizimbannic

bol

honpng

pak

jam

phisri

guy

idnperrom

ecu

colmorpar

domegycos

gua

thaels

panfijtur

syrbot

iratun

ven

jorbra

uru

mexrsa

trihunchl

argmlymau

bar

por

gre

nwzkorcyp

jap

spa

ice

unkfin

swe

isrost

canden

swi

fra

netausireita

belhks

sin

nor

uns

3035

4045

Ave

rage

age

of t

he w

orkf

orce

0 20000 40000 60000Per capita GDP

McMahon (University of Warwick) Introduction 20 / 22

Questions?

McMahon (University of Warwick) Introduction 21 / 22

END

McMahon (University of Warwick) Introduction 22 / 22

Session 2: Business Cycle Theory

Michael McMahon

University of Warwick

McMahon (University of Warwick) Business Cycles 1 / 53

To Cover

1 Measuring business cycles using data2 Introducing the business cycle theory3 Discussing the costs of business cycles and the argument forstabilisation policy

4 Understanding and interpreting macroeconomic indicators.

McMahon (University of Warwick) Business Cycles 2 / 53

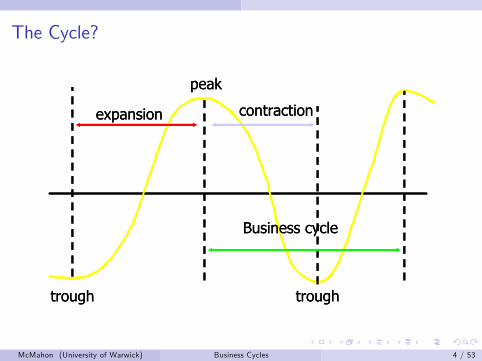

Business Cycles

De�nitionCycle is made of an expansion (boom) and a contraction (recession).During the expansion all good things (GDP, employment, productivity,. . . )tend to go up, or grow faster than �normal,� and bad things(unemployment) tend to fall. During the contraction good things go downand bad things go up.

To be contrasted with economic growth.

McMahon (University of Warwick) Business Cycles 3 / 53

The Cycle?

trough

peak

trough

expansion contraction

Business cycle

trough

peak

trough

expansion contraction

Business cycle

McMahon (University of Warwick) Business Cycles 4 / 53

Features of Business Cycles I

1 Business cycles are NOT regular: They do not behave anything likesine waves. This is important because it tells us that they are not dueto some regular underlying component.

2 Expansions tend to be long and mild. They are measured in years.The 1990�s expansion and the most recent expansion = the longestever (my PhD).

3 Recessions tend to be short but more dramatic. They are measured inmonths.

4 However, in recessions the decline per period is relatively large.

McMahon (University of Warwick) Business Cycles 11 / 53

Features of Business Cycles II

Series St. Dev Rel. Dev Autocorrelation Corr. with GDPY 1.49 1.00 0.58 1.00C 1.59 1.06 0.73 0.68I 6.69 4.48 0.68 0.74G 1.50 1.00 0.63 0.15NX 0.90 0.60 0.51 �0.16Hours 1.60 1.07 0.70 0.58Employ 1.05 0.70 0.77 0.39

YE 1.43 0.95 0.34 0.40P 2.1 1.45 0.88 �0.57M1 3.11 2.05 0.74 0.33

McMahon (University of Warwick) Business Cycles 12 / 53

Business Cycle Dating Game

ProblemAnswer the following:

1 How would you identify periods of recession in the US economy since1940?

2 What criteria would you use to de�ne the periods?3 Apply this criteria to the data on US GDP and US GDP growth (andother important variables) using Excel.

McMahon (University of Warwick) Business Cycles 5 / 53

Should We Care About Business Cycles?

McMahon (University of Warwick) Business Cycles 13 / 53

Should We Care About Business Cycles?

Picture suggests that business cycles are minor blips and not worth muchattention. However:

1 What would level of GDP be without business cycles?

Some average of what we observe now?Or by eliminating recessions something that is on average higher?

2 Although GDP doesn�t do �much� in a recession, this doesn�t meansome �rms and individuals are not hurt (e.g. bankruptcies are verycyclical)

3 Business cycles could a¤ect growth rates

McMahon (University of Warwick) Business Cycles 14 / 53

Business Cycle v. Output GapsDe�nitionOutput gap - A measure of the di¤erence between actual activity andpotential activity.

Is the economy under-performing or over-performing?

The two concepts are related but conceptually distinct.

The economy could be in a statistical recession without thiscorresponding to an output gap - e.g. natural disaster.Likewise, the economy could be in a boom but still beunder-performing.Output gap may be more useful as a concept but it is much harder tomeasure - one way is the production function technique:

Yt = AtLαtK

1�αt

McMahon (University of Warwick) Business Cycles 15 / 53

Growth Accounting Framework

Using the production function:

Yt = AtLαtK

1�αt

Combined with data on inputs and income shares...

we can decompose GDP growth into its driving forces:

Contributions to Aggregate GrowthY TFP K L

1970s 1.55 0.56 0.89 0.111980s 2.58 1.77 0.76 0.071990s 2.39 1.56 0.74 0.092000s 2.41 1.42 0.84 0.15

McMahon (University of Warwick) Business Cycles 16 / 53

A Basic Business Cycle TheoryAS-AD Model

A simple diagrammatic exposition to examine the behaviour of outputand in�ation.

Contains 2 elements:1 Aggregate demand curve - captures the national income identity:

AD = C + I + G + X �M

2 Aggregate supply curve - captures the total quantity supplied at everyprice level.

The aim is to examine the interaction of these two relationships andto develop a framework to think about the causes of business cycles.

McMahon (University of Warwick) Business Cycles 17 / 53

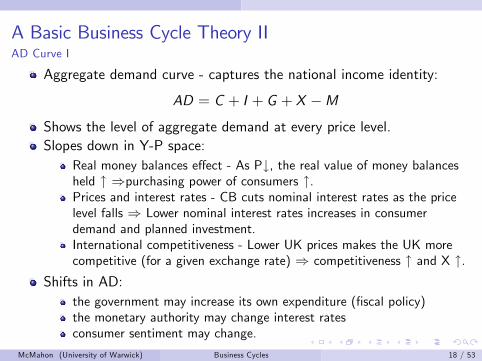

A Basic Business Cycle Theory IIAD Curve I

Aggregate demand curve - captures the national income identity:

AD = C + I + G + X �MShows the level of aggregate demand at every price level.Slopes down in Y-P space:

Real money balances e¤ect - As P#, the real value of money balancesheld " )purchasing power of consumers ".Prices and interest rates - CB cuts nominal interest rates as the pricelevel falls ) Lower nominal interest rates increases in consumerdemand and planned investment.International competitiveness - Lower UK prices makes the UK morecompetitive (for a given exchange rate) ) competitiveness " and X ".

Shifts in AD:the government may increase its own expenditure (�scal policy)the monetary authority may change interest ratesconsumer sentiment may change.

McMahon (University of Warwick) Business Cycles 18 / 53

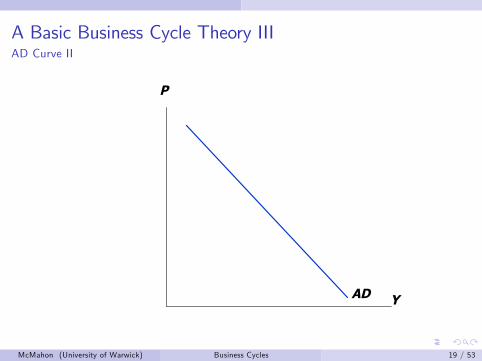

A Basic Business Cycle Theory IIIAD Curve II

Y

P

AD

McMahon (University of Warwick) Business Cycles 19 / 53

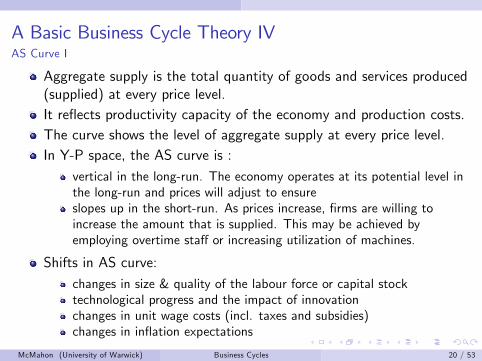

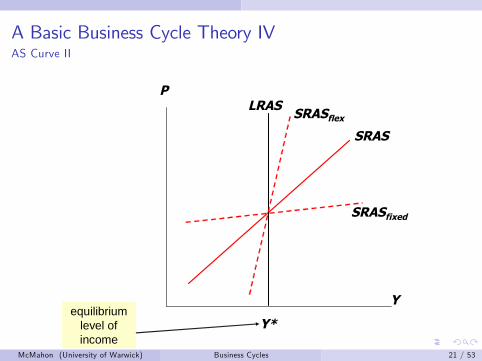

A Basic Business Cycle Theory IVAS Curve I

Aggregate supply is the total quantity of goods and services produced(supplied) at every price level.It re�ects productivity capacity of the economy and production costs.The curve shows the level of aggregate supply at every price level.In Y-P space, the AS curve is :

vertical in the long-run. The economy operates at its potential level inthe long-run and prices will adjust to ensureslopes up in the short-run. As prices increase, �rms are willing toincrease the amount that is supplied. This may be achieved byemploying overtime sta¤ or increasing utilization of machines.

Shifts in AS curve:changes in size & quality of the labour force or capital stocktechnological progress and the impact of innovationchanges in unit wage costs (incl. taxes and subsidies)changes in in�ation expectations

McMahon (University of Warwick) Business Cycles 20 / 53

A Basic Business Cycle Theory IVAS Curve II

Y

P

SRAS

equilibriumlevel ofincome

LRAS

Y*

SRASflex

SRASfixed

McMahon (University of Warwick) Business Cycles 21 / 53

Price Adjustment is Key

Why don�t �rms adjust prices immediately - the Classical School (AScurve is vertical):

1 Most �rms seem to revise prices only occasionally (perhaps as rarelyas once a year). This means that some �rms will delay price revisionby as long as one year.

2 Firms are concerned with their market share: even those whose turn isto revise prices will do so slowly if they know many others are notrevising any time soon.

3 May be uncertain about nature of shock (is it only me or is iteveryone?) and reactions of competitors.

4 Wages are often �xed for long periods (annual contracts). Somarginal cost fairly stable. In competitive markets price cannot movetoo far from marginal cost.

McMahon (University of Warwick) Business Cycles 22 / 53

Frequency of Price Reviews

More than 12 512 34 2 1 00

5

10

15

20

25

30

35

40

McMahon (University of Warwick) Business Cycles 23 / 53

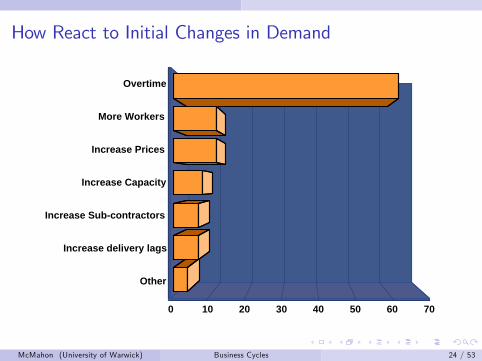

How React to Initial Changes in Demand

0 10 20 30 40 50 60 70

Overtime

More Workers

Increase Prices

Increase Capacity

Increase Subcontractors

Increase delivery lags

Other

McMahon (University of Warwick) Business Cycles 24 / 53

Price Adjustment is Key

But eventually:

More and more �rms get chance to revise prices, meaning thataggregate prices creep up

Workers get a chance to renegotiate wages, meaning that costs startincreasing, and �rms need to increase prices

Also, start running out of unemployed workers, which also pusheswages and hence prices upwards

McMahon (University of Warwick) Business Cycles 25 / 53

A Basic Business Cycle Theory VEquilibrium

Y

P

SRAS

ADequilibrium

level ofincome

LRAS

Y*

McMahon (University of Warwick) Business Cycles 26 / 53

What causes business cycles?

Economy humming along its long-run growth path but constantly bu¤etedby:

Demand Shocks: changes in demand for good and services;

Supply Shocks: essentially changes in �rms�costs of production;

Both demand and supply shocks can generate �uctuations.

McMahon (University of Warwick) Business Cycles 27 / 53

Demand Shock IShifts in the AD curve:

Consumption

Investment

Government spending

Exports

Changes in desired amounts of all these a¤ect the demand faced by �rms

1 Say initial shock pushes demand up;2 Firms�initial response is to leave prices unchanged, and accommodatethe surge in demand by producing more (GDP, investment,employment go up). This is the boom.

3 In a second stage �rms begin to increase prices and reduce output.GDP etc. return to their long-run trend.

And a recession is the same thing in reverse.McMahon (University of Warwick) Business Cycles 28 / 53

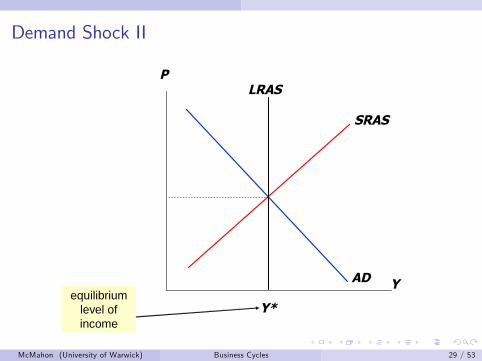

Demand Shock II

Y

P

SRAS

ADequilibrium

level ofincome

LRAS

Y*

McMahon (University of Warwick) Business Cycles 29 / 53

Demand Shock II

Y

P

SRAS

equilibriumlevel ofincome

LRAS

Y*

AD’

Y1

McMahon (University of Warwick) Business Cycles 29 / 53

Demand Shock II

Y

P

equilibriumlevel ofincome

LRAS

Y*

AD’

Y1

SRAS’’

McMahon (University of Warwick) Business Cycles 29 / 53

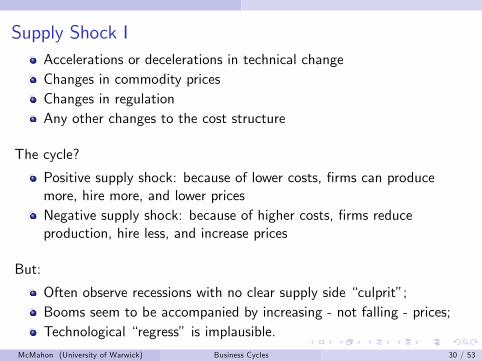

Supply Shock IAccelerations or decelerations in technical changeChanges in commodity pricesChanges in regulationAny other changes to the cost structure

The cycle?

Positive supply shock: because of lower costs, �rms can producemore, hire more, and lower pricesNegative supply shock: because of higher costs, �rms reduceproduction, hire less, and increase prices

But:

Often observe recessions with no clear supply side �culprit�;Booms seem to be accompanied by increasing - not falling - prices;Technological �regress� is implausible.

McMahon (University of Warwick) Business Cycles 30 / 53

Supply Shock II - Temporary

Y

P

SRAS

ADequilibrium

level ofincome

LRAS

Y*

McMahon (University of Warwick) Business Cycles 31 / 53

Supply Shock II - Temporary

Y

P

equilibriumlevel ofincome

LRAS

Y*

AD

Y1

SRAS’’

McMahon (University of Warwick) Business Cycles 31 / 53

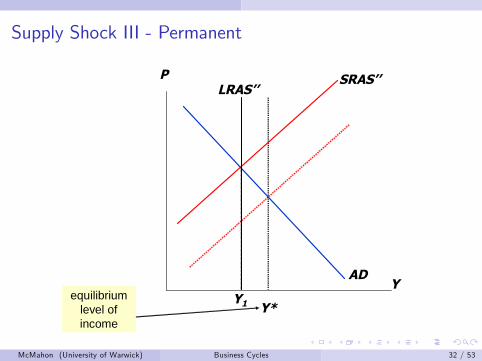

Supply Shock III - Permanent

Y

P

SRAS

ADequilibrium

level ofincome

LRAS

Y*

McMahon (University of Warwick) Business Cycles 32 / 53

Supply Shock III - Permanent

Y

P

equilibriumlevel ofincome

LRAS’’

Y*

AD

Y1

SRAS’’

McMahon (University of Warwick) Business Cycles 32 / 53

Propagation of Shocks - I

Above we have thought about business cycles in terms of demand andsupply shocks. This is informative but does not answer following question:

How do shocks to the economy become transmitted over time?

Remember that business cycles have a duration of 4-10 years, so the factthat the �uctuations are persistent is a key feature.

To think about this, it is useful to consider a distinction between the initialshock to the economy �the impulse �and the mechanism that transmitsshocks over time � the propagation mechanism.

McMahon (University of Warwick) Business Cycles 33 / 53

Propagation of Shocks - II

ImpulseImpulse PropagationMechanismPropagationMechanism

BusinessCycles

BusinessCycles

If there was no propagation mechanism, impulses would quickly dieout unless the impulses are repeated over time.

Propagation mechanisms are aspects that gives rise to persistente¤ects.

McMahon (University of Warwick) Business Cycles 34 / 53

Propagation of Shocks - III

Propagation mechanisms:

investment and capital accumulation. e.g. credit markets;

intertemporal substitution in consumption and labor supply

nominal rigidities

Neoclassical economists stress the �rst two.

Keynesian economists stress the last.

McMahon (University of Warwick) Business Cycles 35 / 53

Propagation of Shocks - IVImpulse Response Functions

Suppose that we are in equilibrium

Allow there to be a once-occurring shock (e.g. technology shock)

Impulse-response functions tell you how the variables of the modeladjust over time.

McMahon (University of Warwick) Business Cycles 36 / 53

Propagation of Shocks - V

2 0 2 4 6 8 10 12 14 16 18100

100.5

101

101.5Response of TFP (% of SS)

2 0 2 4 6 8 10 12 14 16 1898

100

102

104Response of GDP (% of SS)

2 0 2 4 6 8 10 12 14 16 1899

100

101Response of Consumption (% of SS)

2 0 2 4 6 8 10 12 14 16 1890

100

110Response of Investment (% of SS)

2 0 2 4 6 8 10 12 14 16 1899

100

101Response of Capital (% of SS)

2 0 2 4 6 8 10 12 14 16 1898

100

102Response of Hours (% of SS)

2 0 2 4 6 8 10 12 14 16 181

0

1Response of Inventory Investment ( ∆ from SS (% of GDP))

2 0 2 4 6 8 10 12 14 16 1895

100

105Response of Inventories (% of SS)

2 0 2 4 6 8 10 12 14 16 1880

100

120Response of ι (% of SS)

2 0 2 4 6 8 10 12 14 16 181

0

1Response of Storage (% of SS)

Model 0 (RBC)Model 2 (Baseline)

McMahon (University of Warwick) Business Cycles 37 / 53

The Timeline of Modern Macroeconomic Theory

The basic framework we have examined is useful as a framework to thinkabout macroeconomics, but modern macroeconomics is more complex.

It is also an ever evolving �eld:

Traditional Keynesian models (60�s)

RBC models (early 80�s onwards)

New-Keynesian Economics (mid/late 80�s onwards)

DSGE models (mid 90�s onwards)

McMahon (University of Warwick) Business Cycles 38 / 53

The DSGE Model IThe RBC model was the �rst of a class of models now known as DSGE:

D Dynamic - we look at variables over timeS Stochastic - the model is subject to random shocksGE General Equilibrium - everything e¤ects everything else (if

households work more, the wage rate is driven down)

The RBC model assumes:Perfect competitionno market imperfectionfully �exible nominal prices

Saving determines capital accumulationTechnology shocks and their propagation create �uctuations aroundthe equilibrium of all macro variablesThe model is fully microfoundedFluctuations re�ect optimal reactions to shocks

McMahon (University of Warwick) Business Cycles 39 / 53

The DSGE Model IIContributions of the basic RBC model:

Combines growth and business cycles

Uses a relatively simple model and can capture the key features ofbusiness cycles

Hugely important methodological contribution

Objections to the RBC model:

Ignores demand shocks which are known to contribute to output�uctuations

Needs very persistent exogenous shocks to generate reasonable output�uctuation persistence

Cannot generate the highly variable employment numbers, unless weassume very high elasticity of labour supply (not true)

Weak propagation mechanism

McMahon (University of Warwick) Business Cycles 40 / 53

The DSGE Model IIIBasic Equilibrium

Equilibrium in DSGE models is given by rational expectations.

Need to combine:

Optimality conditions for equilibrium consumption, savings and laboursupply from household�s maximisation problemOptimality conditions for equilibrium prices of production factors(rental and wage rate) from �rm�s maximisation problemMarket clearing conditions (GE)

Households derive utility from consumption and from leisure and so itfaces a trade-o¤:

Need to work (provide labour) to earn labour income for current andfuture consumptionNeed to have some leisure

Will have a set of equilibrium conditions which will determine theevolution of all variables over time

McMahon (University of Warwick) Business Cycles 41 / 53

The DSGE Model IVFrom RBC to alternative DSGE models I

1 Capital market imperfections / Credit Frictions2 Externalities, multiple equilibria and self-ful�lling expectations(Farmer)

3 Sticky information (Mankiw-Reis, Mackowiak-Wiederholt)4 Bounded rationality

McMahon (University of Warwick) Business Cycles 42 / 53

The DSGE Model IVFrom RBC to alternative DSGE models II

Capital market imperfections / Credit Frictions

RBC models assume perfect capital markets

But borrowers are better informed than lenders about the risk andreturns on their projects (information asymmetries)

Lenders guard themselves against this extra risk by:

requiring an external �nance premium that is negatively related to thevalue of the borrowers�collateral (Bernanke-Gertler-Gilchrist)limiting the amount of lending to a fraction of the value of thecollateral (Kiyotaki-Moore)

Both lead to a ��nancial accelerator�.

McMahon (University of Warwick) Business Cycles 43 / 53

The DSGE Model IVFrom RBC to alternative DSGE models III

Bounded rationality

=) expectations are not always and completely rational

Agents need to �nd out what is going on by learning (Evans &Honkapohja)

While learning, bounded rationality may amplify business cycle andgenerate asymmetric e¤ects (Giannitsarou)

While a reasonable assumption, non-rationality could be anything -too many ways to model bounded rationality

McMahon (University of Warwick) Business Cycles 44 / 53

The DSGE Model VIThe future?

Good modelling idea in principleBut these models get very complicated and di¢ cult to solve

Must resort to approximate solutions which are often computationallycomplicated

Assumption of rational expectations and representative agent is oftencriticised (see recent Economist article).

My View:Existing approaches are not perfect, and are certainly not de�nitivetheories of business cyclesHowever, we have gone a long way in explaining lots of things andshown that the methodology is �exible enough to deal with a lot ofthe current challenges:

though they will be hard from a computational point of view

A very exciting and challenging area of current research!McMahon (University of Warwick) Business Cycles 45 / 53

Macroeconomic Indicators

Di¤erent countries have a large (and varied) range of macroeconomicindicators apart from GDP statistics:

Industrial Production Indexes

Prices series

Money Aggregates

Interest Rates

Financial Variables

Demand Indicators (such as retail sales, auto sales, etc)

Surveys (Industrial, Construction, Consumer)

Trade Variables

Labour Market Series

Daily stock markets series

McMahon (University of Warwick) Business Cycles 46 / 53

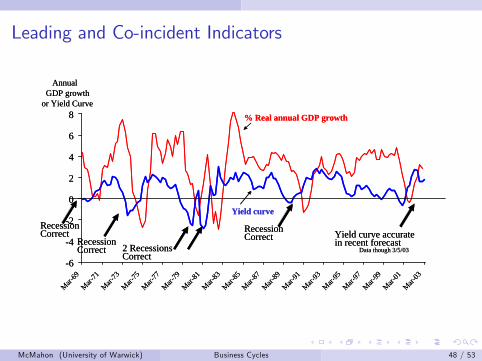

Leading and Co-incident IndicatorsIdentifying business cycles is important information for the public. But:High quality data become available only with a delay �nobody knowsexactly what current GDP is due both to revisions and to delay in datacollection.

For that reason leading and co-incident indicators are valuable:

Leading indicators: Indicators that have predictive power for businesscycle turning points and phases.

The spread between the yield on short and long bonds; New privatehousing starts; Un�lled orders in manufacturing; Number of people onpart-time work.

Co-incident indicators: Indicators that have predictive power forcurrent state of the economy.

Industrial production; Real personal sector income; Real manufacturingtrade and sales; Total non-agricultural payroll and hours

McMahon (University of Warwick) Business Cycles 47 / 53

Leading and Co-incident Indicators

6

4

2

0

2

4

6

8

Mar69

Mar71

Mar73

Mar75

Mar77

Mar79

Mar81

Mar83

Mar85

Mar87

Mar89

Mar91

Mar93

Mar95

Mar97

Mar99

Mar01

Mar03

% Real annual GDP growth

Yield curve

RecessionCorrect 2 Recessions

Correct

RecessionCorrect Yield curve accurate

in recent forecast

RecessionCorrect

AnnualGDP growth

or Yield Curve

Data though 3/5/03

6

4

2

0

2

4

6

8

Mar69

Mar71

Mar73

Mar75

Mar77

Mar79

Mar81

Mar83

Mar85

Mar87

Mar89

Mar91

Mar93

Mar95

Mar97

Mar99

Mar01

Mar03

% Real annual GDP growth

Yield curve

RecessionCorrect 2 Recessions

Correct

RecessionCorrect Yield curve accurate

in recent forecast

RecessionCorrect

AnnualGDP growth

or Yield Curve

Data though 3/5/03

McMahon (University of Warwick) Business Cycles 48 / 53

Surveys I

Many bodies (o¢ cial and uno¢ cial) conduct surveys in order to gatherinformation on the economy:

They are very timely - often can get them within the period of interest

Expectations of agents matter

But:

there is an issue of how to interpret them

we need to be careful

they can be volatile and may not be representative

sample size is important

McMahon (University of Warwick) Business Cycles 49 / 53

Surveys IIEuropean Surveys

All EU countries conduct a common survey of manufacturers, servicecompanies, construction �rms, retailers and consumer:

survey has both backward-looking and forward-looking components;

most questions asked monthly (some quarterly);

respondents choose from a menu of qualitative answers:,

�+ +�(most positive answer)�+�(positive answer)�=�(neutral answer)�-� (negative answer)�- -� (most negative answer)�Don�t know".

Some surveys are combined to give "Economic Sentiment Indicator"

McMahon (University of Warwick) Business Cycles 50 / 53

Surveys IIIEuropean Surveys

Example from consumer survey:

1 How do you expect the general economic situation in this country todevelop over the next 12 months? It will...

+ + get a lot better+ get a little better= stay the same- get a little worse- - get a lot worseN don�t know.

Answer is reported as a balance between positives and negativeswhere ++ is worth double +.

�Don�t knows�are discarded.

Often compare to long-term average.

McMahon (University of Warwick) Business Cycles 51 / 53

Final Comments on Indicators

When looking at macroeconomic indicators, two additional issues need tobe considered:

1 Seasonal adjustment2 Revisions to statistics

McMahon (University of Warwick) Business Cycles 52 / 53

END

McMahon (University of Warwick) Business Cycles 53 / 53

Session 3: Economic Diversi�cation

Michael McMahon

University of Warwick

McMahon (University of Warwick) Diversi�cation 1 / 18

To Cover

1 Di¤erent Economic Sectors2 How di¤erent sectors are a¤ected by the business cycle3 The bene�ts of diversi�cation

McMahon (University of Warwick) Diversi�cation 2 / 18

Di¤erent Economic Sectors

We have discussed how GDP can be split into di¤erent expenditurecomponents (C, I, etc...)

But we can also look at how di¤erent industries contribute to nominalGDP:

GDPt = Ind1t + Ind2t + Ind

3t ...+ Ind

Nt

where Ind jt is the contribution of industry j to nominal GDP (which"adds up").

We cannot just use industry output as the contribution - we must usea concept called "Gross Value Added (GVA)".

this avoids any double-counting of industry output

McMahon (University of Warwick) Diversi�cation 3 / 18

Gross Value Added - An Example I

Consider an economy that has 2 sectors

1 Manufacturing sector:

Imports raw materials from abroad and then creates output from that.

2 Retail and Distribution sector:

Buys the output from manufacturers and sells the goods to consumers.

GVAt = Outputt � intermediate_inputst

McMahon (University of Warwick) Diversi�cation 4 / 18

Gross Value Added - An Example IIIntermediate goods Output SalesDomestic Imported Intermed. Final

Manufacturing 0 50 100 100 0Retail & Dist. 100 0 150 0 150

1 Expenditure Approach

GDP(E ) = C + I + G + X �M= 150+ 0+ 0+ 0� 50= 100

2 GVA - must yield the same as expenditure approach

GDP(VA) = VAman + VAret

= (100� 50) + (150� 100)= 100

McMahon (University of Warwick) Diversi�cation 5 / 18

Adding Up Real GDP

It is not possible to simply "add up" real values

Real GDP is often simply reported as an index

Calculation of real GDP uses a method called "chain-weighting"

Following Jorgensen, we calculate real GDP (gYt ) growth as aTornqvist index of growth in each sector:

gYt = ∑i

vi ,t .gVAi ,t (1)

where vi ,t =12

�pi ,0.qi ,0

∑ipi ,0.qi ,0

+ pi ,t .qi ,t∑ipi ,t .qi ,t

�is the average nominal share of

sector i in periods t and t � 1.The main implication of this is that we cannot take real shares - wemust calculate nominal shares.

McMahon (University of Warwick) Diversi�cation 6 / 18

Overnight Problem

ProblemContinuing to look at the overnight problem - discussion of the issuesencountered and some time to work on the data with my help.

McMahon (University of Warwick) Diversi�cation 7 / 18

What is Diversi�cation?

De�nitionDiversi�cation is the process whereby an economy expands:

1 the range of sectors it produces in;2 the markets that are served; and/or3 its sources of income.

The objective is to create a stable and sustainable level of income at a(relatively) high level.

Economic diversi�cation is a structural transformation and is oftenaccompanied by economic development.

McMahon (University of Warwick) Diversi�cation 8 / 18

Why Diversi�cation?

There are well-known e¢ ciency bene�ts from specialization...

..but also risks of too little diversi�cation.

The reasons for diversi�cation typically discussed in the literature (seeZhang) are:

1 Trends in terms of trade2 Price instability in primary commodity markets3 Depletion of mineral resources4 Economies of scale and external economies especially associated withmanufacturing

5 Reduction of portfolio risk

McMahon (University of Warwick) Diversi�cation 9 / 18

How to Measure Diversi�cation? I

1 share of sector in nominal GDP2 share of sector in exports3 the % of the labour force employment in the sector

McMahon (University of Warwick) Diversi�cation 10 / 18

How to Measure Diversi�cation? II

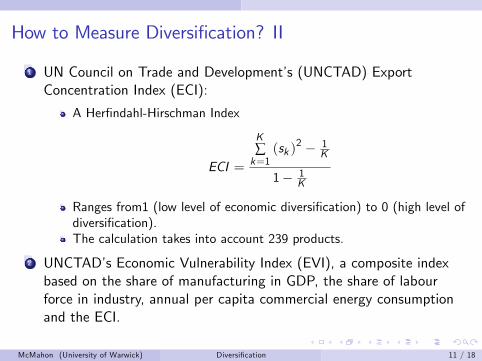

1 UN Council on Trade and Development�s (UNCTAD) ExportConcentration Index (ECI):

A Her�ndahl-Hirschman Index

ECI =

K∑k=1

(sk )2 � 1

K

1� 1K

Ranges from1 (low level of economic diversi�cation) to 0 (high level ofdiversi�cation).The calculation takes into account 239 products.

2 UNCTAD�s Economic Vulnerability Index (EVI), a composite indexbased on the share of manufacturing in GDP, the share of labourforce in industry, annual per capita commercial energy consumptionand the ECI.

McMahon (University of Warwick) Diversi�cation 11 / 18

How do Countries Encourage Diversi�cation?

Foreign-direct investment

creating �nancial incentives for foreign investmentfavourable legislationsidenti�cation of investment opportunities and marketing theopportunities

privatization of industries

may lead to greater e¢ ciency and thus expansion of marketsAbu Dhabi utilities

liberalization of �nancial markets

use of subsidies

other industrialization policies

education and training capacities.

McMahon (University of Warwick) Diversi�cation 12 / 18

Diversi�cation in the GCC I

Many of the GCC economies stress the need for economicdiversi�cation

E¤ort has been made with:

downstream industries (such as petrochemicals, fertilizers and metals)agriculture (albeit at a high cost in subsidies)services (in the form of �nancial institutions and tourism).

There are problems associated with the diversi�cation process - e.g.the scarcity of water resources in agriculture

Success has followed with reliance on oil falling

McMahon (University of Warwick) Diversi�cation 13 / 18

Diversi�cation in the GCC II

Diversi�cation does not only mean new industries in the GCC:

GCC countries have natural advantages in solar, wind, geothermal,hydropower and biomass energies:

Existing infrastructure can be adapted for other energy purposes;training may be easier for existing energy workers

These sectors are less vulnerable than oil:

renewable�green�

Thus, measuring just energy sector share does not capture the fullextent of possible diversi�cation

McMahon (University of Warwick) Diversi�cation 14 / 18

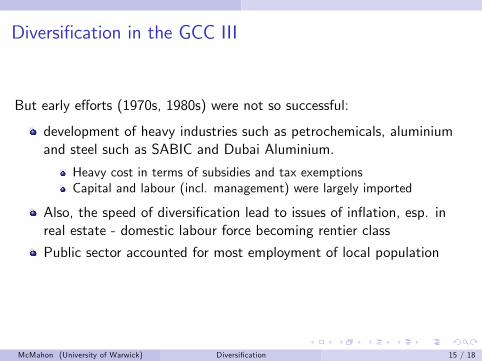

Diversi�cation in the GCC III

But early e¤orts (1970s, 1980s) were not so successful:

development of heavy industries such as petrochemicals, aluminiumand steel such as SABIC and Dubai Aluminium.

Heavy cost in terms of subsidies and tax exemptionsCapital and labour (incl. management) were largely imported

Also, the speed of diversi�cation lead to issues of in�ation, esp. inreal estate - domestic labour force becoming rentier class

Public sector accounted for most employment of local population

McMahon (University of Warwick) Diversi�cation 15 / 18

Diversi�cation in the GCC IV

Now:

Additional focus on new services such as IT and tourism

diversi�cation within energy sector (lique�ed natural gas)

Creation of further free zones

Real estate ownership opening to nonresidents (e.g. Dubai)

Opening-up the economy to private sector FDI

Encouraging domestic enterprise

Structural and institutional reforms

McMahon (University of Warwick) Diversi�cation 16 / 18

Diversi�cation in the GCC VSuccess - Non-oil GDP in Nominal GDP (%)

McMahon (University of Warwick) Diversi�cation 17 / 18

END

McMahon (University of Warwick) Diversi�cation 18 / 18

Session 4: An Introduction to Forecasting

Michael McMahon

University of Warwick

McMahon (University of Warwick) Forecasting 1 / 22

To Cover

1 Basic Statistics and Regression2 Forecasting3 euro-coin indicator

McMahon (University of Warwick) Forecasting 2 / 22

Probability and Classical StatisticsRandom Variables and Probability Distribution I

De�nitionA random variable (RV) is a function that associates a unique numericalvalue with every outcome of an experiment. The value of the randomvariable will vary from trial to trial as the experiment is repeated. Arandom variable, which can be either continuous or discrete, has anassociated probability distribution.

For example:

a toss of a coin (discrete RV)

resultt =�heads w .p. 12tails w .p. 12

a roll of a dice

McMahon (University of Warwick) Forecasting 3 / 22

Probability and Classical StatisticsRandom Variables and Probability Distribution II

A common probability distribution is the normal distribution:

Xvalues0

Probability

Try the repeated coin toss game.McMahon (University of Warwick) Forecasting 4 / 22

Probability and Classical StatisticsRandom Variables and Probability Distribution III

Any observation on a RV is the outcome of a statistical experiment:

Occasionally we know enough about the experiment to predict thefrequency of di¤erent outcomes.Usually, we observe a sample of outcomes, and try to infer the natureof the underlying experimental mechanism from this sample.In both cases we cannot predict the exact outcome of an individualexperiment.

We can imagine two types of economic experiments:1 using a set of characteristics (e.g. wage, education, experience, sex) foran individual unit (e.g. an employee) selected at random from a muchlarger population.

2 analysing an economic time series (e.g. GDP, or individual �rm sales)

McMahon (University of Warwick) Forecasting 5 / 22

Probability and Classical StatisticsRandom Variables and Probability Distribution IV

Economics is not like other science experiments:

We do not (usually) control any of the observed characteristics(unlike a physicist who might control the temperature of a reaction)

we need to adopt statistical methods which cope with situations wheremany characteristics vary simultaneously.

We cannot measure all the relevant characteristics precisely (e.g. wecannot directly observe risk aversion)

we have to assume that the e¤ects of the unobserved characteristicscan be represented by a random disturbance.Therefore, �averaging�over many observations will eliminate theire¤ects and allow us to make inferences about how the observedcharacteristics a¤ect individual behaviour.

McMahon (University of Warwick) Forecasting 6 / 22

Statistics and ProbabilityRegression - The Basics I

You want to model the e¤ect of X on Y where the true relationship is:

Yt = α+ βXt + εt (1)

Yt �! variable to explain (dependent variable)

α �! constant

β �! regression coe¢ cient

Xt �! explanatory variable

εt �! economic shocks in the relationship.

McMahon (University of Warwick) Forecasting 7 / 22

Statistics and ProbabilityRegression - The Basics II

But we don�t know the true relationship so we estimate it using the datathat we have:

Yt = α+ βXt + et (2)

Yt �! variable to explain (dependent variable)

α �! estimated constant

β �! estimated regression coe¢ cient

Xt �! explanatory variable

et �! estimated residuals in the relationship.

The aim of Least Squares regression is to make the line �t as best aspossible (minimise the square of the errors).

McMahon (University of Warwick) Forecasting 8 / 22

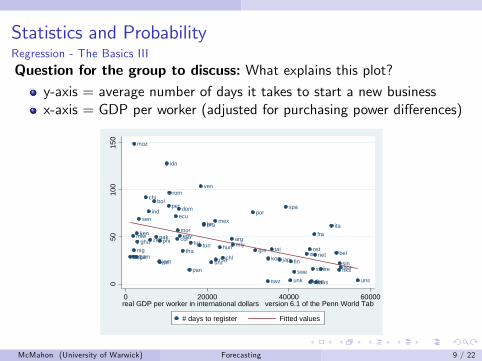

Statistics and ProbabilityRegression - The Basics III

Question for the group to discuss: What explains this plot?y-axis = average number of days it takes to start a new businessx-axis = GDP per worker (adjusted for purchasing power di¤erences)

arg

aus

bel

bol

bra

can

chi

chl

col

den

domecu

egy

fin

fragha

gre

hks

hun

idn

ind

ire

isr

ita

jam jap

jor

ken

kor

mex

mlwmly

mor

moz

netnig

nor

nwz

ost

pak

pan

per

phi

por

rom

rsa

sen

sin

spa

sri

swe swi

taitan

thatuntur

uga

unk uns

uru

ven

zam

zim

050

100

150

0 20000 40000 60000real GDP per worker in international dollars version 6.1 of the Penn World Tab

# days to register Fitted values

McMahon (University of Warwick) Forecasting 9 / 22

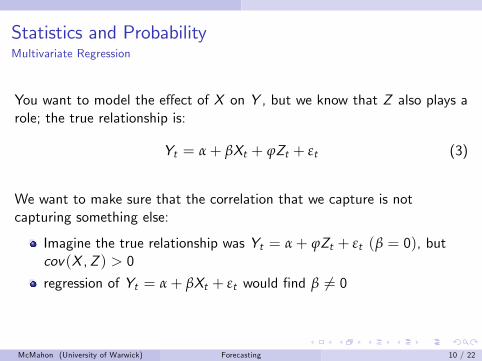

Statistics and ProbabilityMultivariate Regression

You want to model the e¤ect of X on Y , but we know that Z also plays arole; the true relationship is:

Yt = α+ βXt + ϕZt + εt (3)

We want to make sure that the correlation that we capture is notcapturing something else:

Imagine the true relationship was Yt = α+ ϕZt + εt (β = 0), butcov(X ,Z ) > 0

regression of Yt = α+ βXt + εt would �nd β 6= 0

McMahon (University of Warwick) Forecasting 10 / 22

Statistics and ProbabilityA Closer Look At Residuals

The residual term (et) captures everything not explained by X :Using equations (2), we get:

et = Yt � α� βXt

If the true relationship is (1):

et = α+ βXt + εt � α� βXt= εt + (α� α) +

�β� β

�Xt

which means that so long as our coe¢ cients are unbiased, then theestimated residuals match up with the economic shocks.But if the true relationship is (3):

et = α+ βXt + ϕZt + εt � α� βXt= εt + ϕZt + (α� α) +

�β� β

�Xt

which means that the omitted variable turns up in the residual.

McMahon (University of Warwick) Forecasting 11 / 22

Statistics and ProbabilityCare with Statistical Analysis

As already discussed, you must be careful with how you interpret simplestatistics:

Selection bias - see below

Omitted variable bias - wrongly attribute e¤ects to X rather than to Z

Measurement error

Speci�cation error - we have been talking about linear models, whatabout non-linear models?

McMahon (University of Warwick) Forecasting 12 / 22

Selection Bias

Consider again the regression hospitalization on health outcomes:

y = α+ βD + ε

Using 12,000 + German households in 1994, where health is a measurefrom 1 (ill�health) to 5 (best health), we get the following results:

health = 2.52 � 0.58 �Hospital(0.09) (0.03)

=) Hospital makes people sicker!

=) Need to Randomise our experiment.

McMahon (University of Warwick) Forecasting 13 / 22

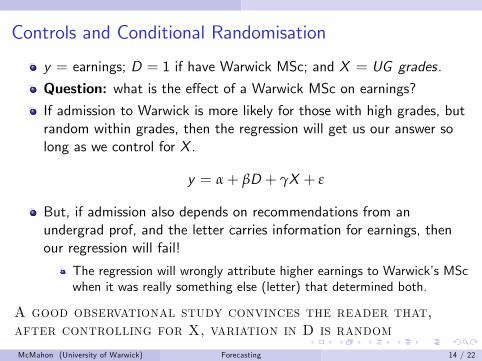

Controls and Conditional Randomisation

y = earnings; D = 1 if have Warwick MSc; and X = UG grades.

Question: what is the e¤ect of a Warwick MSc on earnings?If admission to Warwick is more likely for those with high grades, butrandom within grades, then the regression will get us our answer solong as we control for X .

y = α+ βD + γX + ε

But, if admission also depends on recommendations from anundergrad prof, and the letter carries information for earnings, thenour regression will fail!

The regression will wrongly attribute higher earnings to Warwick�s MScwhen it was really something else (letter) that determined both.

A good observational study convinces the reader that,after controlling for X, variation in D is random

McMahon (University of Warwick) Forecasting 14 / 22

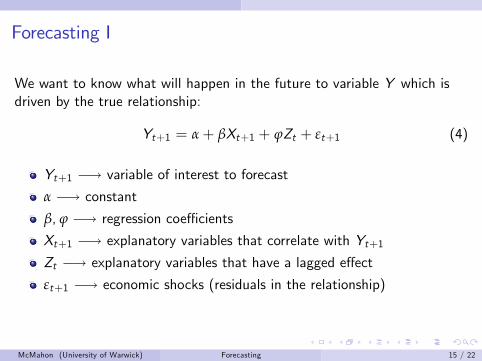

Forecasting I

We want to know what will happen in the future to variable Y which isdriven by the true relationship:

Yt+1 = α+ βXt+1 + ϕZt + εt+1 (4)

Yt+1 �! variable of interest to forecast

α �! constant

β, ϕ �! regression coe¢ cients

Xt+1 �! explanatory variables that correlate with Yt+1Zt �! explanatory variables that have a lagged e¤ect

εt+1 �! economic shocks (residuals in the relationship)

McMahon (University of Warwick) Forecasting 15 / 22

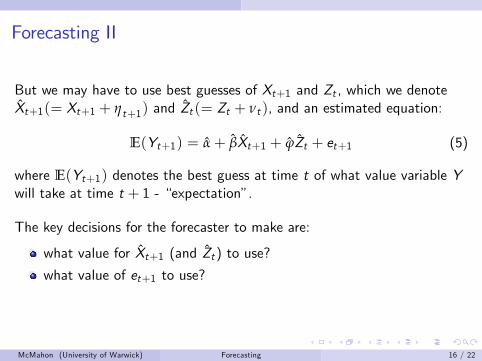

Forecasting II

But we may have to use best guesses of Xt+1 and Zt , which we denoteXt+1(= Xt+1 + ηt+1) and Zt (= Zt + νt ), and an estimated equation:

E(Yt+1) = α+ βXt+1 + ϕZt + et+1 (5)

where E(Yt+1) denotes the best guess at time t of what value variable Ywill take at time t + 1 - �expectation�.

The key decisions for the forecaster to make are:

what value for Xt+1 (and Zt) to use?

what value of et+1 to use?

McMahon (University of Warwick) Forecasting 16 / 22

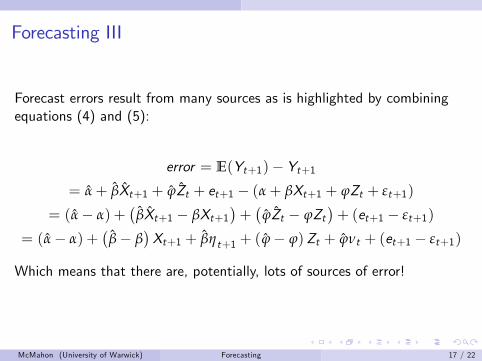

Forecasting III

Forecast errors result from many sources as is highlighted by combiningequations (4) and (5):

error = E(Yt+1)� Yt+1= α+ βXt+1 + ϕZt + et+1 � (α+ βXt+1 + ϕZt + εt+1)

= (α� α) +�

βXt+1 � βXt+1�+�

ϕZt � ϕZt�+ (et+1 � εt+1)

= (α� α) +�

β� β�Xt+1 + βηt+1 + (ϕ� ϕ)Zt + ϕνt + (et+1 � εt+1)

Which means that there are, potentially, lots of sources of error!

McMahon (University of Warwick) Forecasting 17 / 22

Forecasting IV

4

3

2

1

0

1

2

3

4

5

6

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

Per centResiduals from a US Business Investment Equation

4

3

2

1

0

1

2

3

4

5

6

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

Per centResiduals from a US Business Investment Equation

What next?

McMahon (University of Warwick) Forecasting 18 / 22

Forecasting IV

4

3

2

1

0

1

2

3

4

5

6

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

Per centResiduals from a US Business Investment Equation

4

3

2

1

0

1

2

3

4

5

6

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

Per centResiduals from a US Business Investment Equation

4

3

2

1

0

1

2

3

4

5

6

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

Per centResiduals from a US Business Investment Equation

Choices to make...

McMahon (University of Warwick) Forecasting 18 / 22

Eurocoin - A "Nowcasting" tool

De�nitione-coin is a real-time, monthly estimate of area-wide underlying GDPgrowth, computed each month by the sta¤ of the Banca d�Italia.It provides a single number summarizing the current economic outlook forthe Euro area.e-coin is obtained by collecting a large set of statistics (such as industrialproduction, surveys, stock market and �nancial data, demand indicators )and extracting from it the information that is relevant to forecast futureGDP trend.It tracks GDP growth anticipating o¢ cial GDP releases by several months.It is a �smooth version�of GDP growth...

McMahon (University of Warwick) Forecasting 19 / 22

Eurocoin - Macroeconomic Indicators UsedThe database uses 141 data series:

industrial Production Indexes (41 series)

Prices (24)

Money Aggregates (8)

Interest Rates (11)

Financial Variables (6)

Demand Indicators (14)

Surveys (25)

Trade Variables (9)

Labour Market Series (7)

Daily stock markets series

See other slides for (i) what it does, (ii) its real-time performance, and (iii)why use so much data.McMahon (University of Warwick) Forecasting 20 / 22

Eurocoin - Recent Performance

McMahon (University of Warwick) Forecasting 21 / 22

END

McMahon (University of Warwick) Forecasting 22 / 22

Money, Banking, the Current Crisis and the PolicyResponse

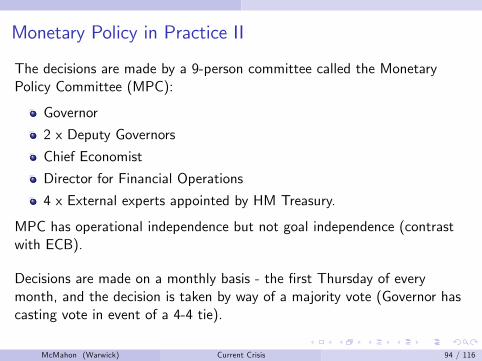

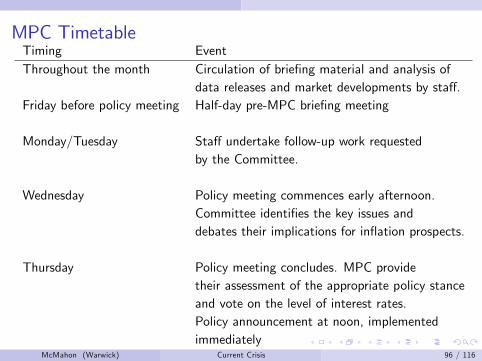

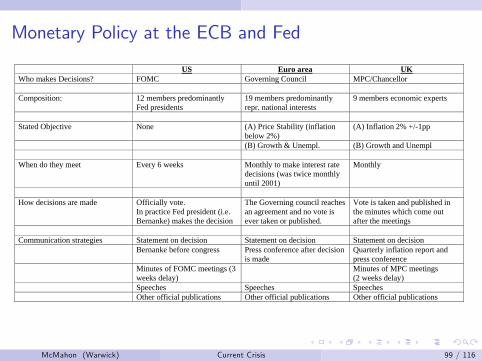

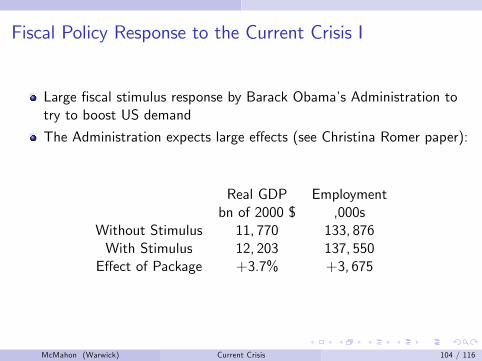

Michael McMahon

McMahon () Current Crisis 1 / 116

Money, Banking, the Current Crisis and the PolicyResponse

The basics of the �nancial system including the main instruments

Why the current crisis? Focus on the concept of leverage and balancesheet e¤ects.

A brief discussion of monetary policy including models of monetarypolicy

Class discussion of the liquidity trap, the zero nominal bound oninterest rates and �quantitative easing�

Fiscal policy response including a discussion of how �scal policyoperates in the economy.

A discussion of exchange rate policy

McMahon (Warwick) Current Crisis 2 / 116

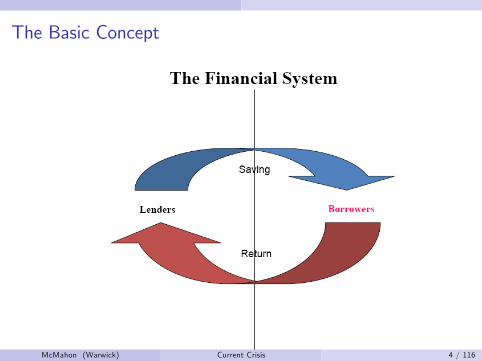

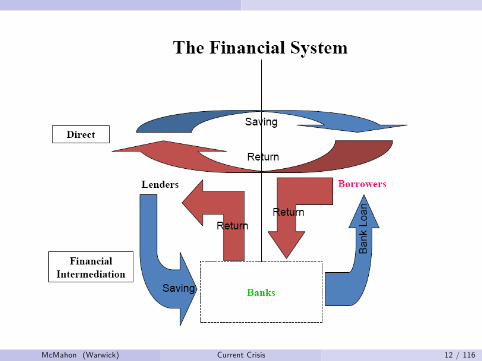

The Basic Concept

De�nitionA �nancial system is de�ned as a set of markets for �nancial instruments,and the individuals and institutions who trade in those markets, togetherwith the regulators and supervisors of the system.[Howells and Bain, 2003]

The basic function of the �nancial system is to transfer resources fromthose with excess funds for investment, to those who require more fundsfor investment.

McMahon (Warwick) Current Crisis 3 / 116

The Basic Concept

McMahon (Warwick) Current Crisis 4 / 116

The PeopleBorrowers

Firms

Households

The government

Foreigners - varies

McMahon (Warwick) Current Crisis 5 / 116

The PeopleLenders

Households

The government

Firms

Foreigners - varies

Same people - but usually in a di¤erent order.

McMahon (Warwick) Current Crisis 6 / 116

Why do Lenders Lend?

Lenders will worry about:

the return that they can get.

the risk surrounding this return:

default risk;income risk;capital risk;in�ation risk;

liquidity

If we wish to encourage more lending, one way is to increase the returnwhich we o¤er to lenders.

McMahon (Warwick) Current Crisis 7 / 116

What determines borrowers behaviour?

Borrowers will worry about:

the return that they must pay to get the funds;

the terms of this return;

for example, debt is not state-contingent while equity is.

the length and �exibility of the borrowing;

�rms will not wish to have debts which are too easily recalled.

McMahon (Warwick) Current Crisis 8 / 116

The Financial Account

Like in double-entry book-keeping, all de�cits (borrowing) must have ano¤setting surplus (lender)In the national accounts, it is possible to look at the �nancial accounts ofdi¤erent sectors over time.In Europe:

Private Non-Financial Corporations (PNFCs)

Monetary and Financial Institutions (MFIs)

Government

Households (and NPISH)

Foreigners - this is the current account

McMahon (Warwick) Current Crisis 9 / 116

The Financial Account

8.0

6.0

4.0

2.0

0.0

2.0

4.0

6.0

8.0

1999 2000 2001 2002 2003 2004 2005 2006

Households PNFCsMFI GovtNet with ROW

% of GDP

McMahon (Warwick) Current Crisis 10 / 116

How the Matches Occur

Lending can be:

1 Completely direct - lenders seeking out other agents who need toborrow.

2 Direct lending through a market.3 Through �nancial intermediation:

direct; orthrough a market.

McMahon (Warwick) Current Crisis 11 / 116

McMahon (Warwick) Current Crisis 12 / 116

The Di¤erent Types of Market

There are di¤erent �nancial markets for each di¤erent type of instrument

Primary versus secondary markets

OTC versus exchange markets

Dealers versus Brokers

Money-market versus capital market (maturity)

McMahon (Warwick) Current Crisis 13 / 116

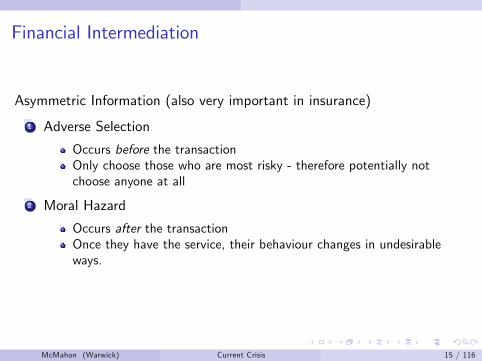

Financial Intermediation

De�nitionInstitutions that borrow funds from people who have saved and in turnmake loans to others. [Mishkin, p.7]

So �nancial intermediates include banks, but will also include pensionfunds, insurance companies, etc...Why go through a �nancial intermediate:

Reduced transaction costs

Risk diversi�cation

Maturity transformation

Reduce Asymmetric Information

Adverse SelectionMoral Hazard

McMahon (Warwick) Current Crisis 14 / 116

Financial Intermediation

Asymmetric Information (also very important in insurance)

1 Adverse Selection

Occurs before the transactionOnly choose those who are most risky - therefore potentially notchoose anyone at all

2 Moral Hazard

Occurs after the transactionOnce they have the service, their behaviour changes in undesirableways.

McMahon (Warwick) Current Crisis 15 / 116

The Di¤erent Types of Instruments

The main two instruments to distinguish are:

Equity

May get an annual share of pro�ts as dividendOwns part of the company )voting rightPrice varies depending on supply and demand

Debt

Contractually �xed return

per period interestprincipal at maturity date

Preferential debtorNo voting right

McMahon (Warwick) Current Crisis 16 / 116

No Single Interest RateThere is NOT 1 single interest rate:

0

5

10

15

20

25

Apr71 Apr81 Apr91 Apr01

Fed funds Nominal 10yearAAA BAAState & local Mortgage

%

McMahon (Warwick) Current Crisis 17 / 116

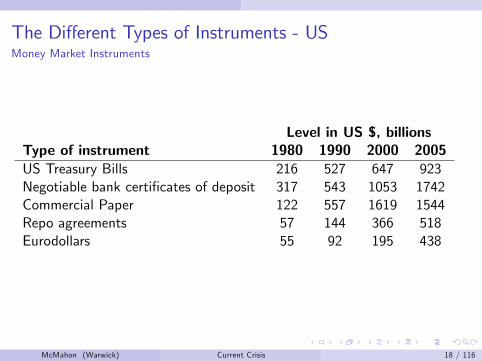

The Di¤erent Types of Instruments - USMoney Market Instruments

Level in US $, billionsType of instrument 1980 1990 2000 2005US Treasury Bills 216 527 647 923Negotiable bank certi�cates of deposit 317 543 1053 1742Commercial Paper 122 557 1619 1544Repo agreements 57 144 366 518Eurodollars 55 92 195 438

McMahon (Warwick) Current Crisis 18 / 116

The Di¤erent Types of Instruments - USMoney Market Instruments

Level (% of GDP)Type of instrument 1980 1990 2000 2005US Treasury Bills 8 9 7 7Negotiable bank certi�cates of deposit 11 9 11 14Commercial Paper 4 10 16 12Repo agreements 2 2 4 4Eurodollars 2 2 2 4

McMahon (Warwick) Current Crisis 19 / 116

The Di¤erent Types of Instruments - USCapital Market Instruments

Level (% of GDP)Type of instrument 1980 1990 2000 2005Corporate Stocks 57 71 180 144Residential Mortgages 40 50 56 76Commercial and Farm Mortgages 13 14 12 15Corporate Bonds 13 17 23 24Government Bonds 18 22 29 36Consumer Loans 13 14 12 15

McMahon (Warwick) Current Crisis 20 / 116

Regulation

Financial services are a highly regulated industry (and have been for a longtime). But why do we regulate �nancial services?

Banking relies on con�dence of public

fractional reserves systemliquidity mismatch between assets and liabilities

Contagion...

Consumer protection...not caveat emptor!

McMahon (Warwick) Current Crisis 21 / 116

Regulation

Problems because of regulation:

Moral hazard

Compliance costs

Costs of entry and exit are higher - more monopoly power!

McMahon (Warwick) Current Crisis 22 / 116

The Macroeconomic E¤ects of Financial Markets

ProblemWhy might the �nancial system have macroeconomic e¤ects?

McMahon (Warwick) Current Crisis 23 / 116

How Banking Works - The Bank Balance Sheet

McMahon (Warwick) Current Crisis 25 / 116

Bank Balance Sheets

Assets LiabilitiesReserves 4% Checkable Deposits 7%Securities 23% Time Deposits 59%Loans 66% Borrowings 26%Other assets (e.g. physical capital) 7% Bank Capital 8%

decreasing liquidity

Basic idea is to make more on the assets than you pay on the liabilities

) pro�ts

McMahon (Warwick) Current Crisis 26 / 116

Bank T-accounts

New account opened with cash (£ 100)

Assets LiabilitiesReserves +£ 100 Checkable Deposits +£ 100

If opened with a cheque from another bank, pretty much the same - cashin process of collection.

McMahon (Warwick) Current Crisis 27 / 116

Bank T-accounts

What if the new account holder then wrote a cheque for £ 50?

Assets LiabilitiesReserves -£ 50 Checkable Deposits -£ 50

.

McMahon (Warwick) Current Crisis 28 / 116

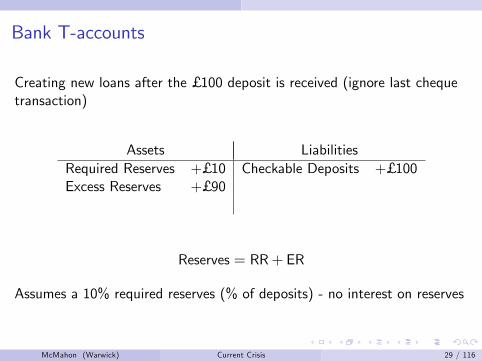

Bank T-accounts

Creating new loans after the £ 100 deposit is received (ignore last chequetransaction)

Assets LiabilitiesRequired Reserves +£ 10 Checkable Deposits +£ 100Excess Reserves +£ 90

Reserves = RR+ ER

Assumes a 10% required reserves (% of deposits) - no interest on reserves

McMahon (Warwick) Current Crisis 29 / 116

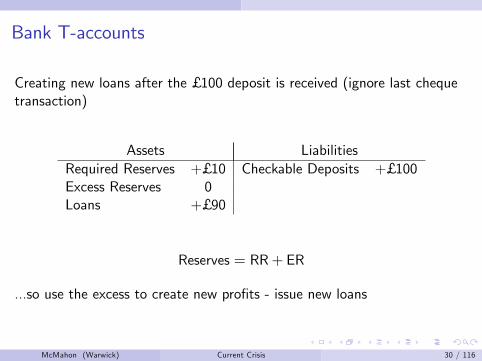

Bank T-accounts

Creating new loans after the £ 100 deposit is received (ignore last chequetransaction)

Assets LiabilitiesRequired Reserves +£ 10 Checkable Deposits +£ 100Excess Reserves 0Loans +£ 90

Reserves = RR+ ER

...so use the excess to create new pro�ts - issue new loans

McMahon (Warwick) Current Crisis 30 / 116

Bank T-accounts

Creating new loans after the £ 100 deposit is received (ignore last chequetransaction)

Assets LiabilitiesRequired Reserves +£ 10 Checkable Deposits +£ 100Excess Reserves 0Loans 0Securities +£ 90

Reserves = RR+ ER

...so use the excess to create new pro�ts - issue new loans (or could buysecurities).

McMahon (Warwick) Current Crisis 31 / 116

Bank Management (brie�y)

1 Liquidity and Reserve management2 Asset and liability management3 Capital adequacy - trade-o¤

Capital prevents failures (cushion against drop in value of assets);Capital lowers return to shareholders;

4 Credit risk and interest rate risk

McMahon (Warwick) Current Crisis 32 / 116

Liquidity and Reserve management

Consider the Bank which created the £ 90 of extra loans and kept noexcess reserves (assume this is the whole balance sheet of the �rm):

Assets LiabilitiesRequired Reserves £ 10 Checkable Deposits £ 100Excess Reserves 0Loans £ 90

If there is a (relatively small) £ 10 withdrawal of deposits, deposits drop by£ 10 and reserves would be exhausted (-£ 10). The Bank is about to fail -they have a reserve shortage of £ 9...

McMahon (Warwick) Current Crisis 33 / 116

Liquidity and Reserve management

Consider the Bank which created the £ 90m of extra loans and kept noexcess reserves (assume this is the whole balance sheet of the �rm):

Assets LiabilitiesRequired Reserves £ 0 Checkable Deposits £ 90Excess Reserves 0Loans £ 90

They need to:

Borrow the required reserves, at a cost, from other banks (borrowingliabilities +£ 9, reserves +£ 9);Borrow the required reserves, at the discount rate, from the CB;Try to recall loans worth £ 9 and put the money into reserves;If they had other assets (securities or even physical capital), theycould also try to sell £ 9m of this.McMahon (Warwick) Current Crisis 34 / 116

Bank Management (brie�y)

1 Liquidity and Reserve management2 Asset and liability management3 Capital adequacy - trade-o¤

Capital prevents failures (cushion against drop in value of assets);Capital lowers return to shareholders;

4 Credit risk and interest rate risk

McMahon (Warwick) Current Crisis 35 / 116

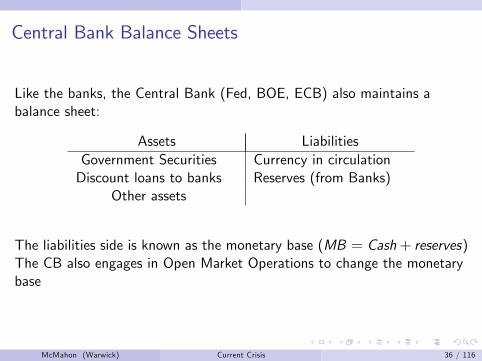

Central Bank Balance Sheets

Like the banks, the Central Bank (Fed, BOE, ECB) also maintains abalance sheet:

Assets LiabilitiesGovernment Securities Currency in circulationDiscount loans to banks Reserves (from Banks)

Other assets

The liabilities side is known as the monetary base (MB = Cash+ reserves)The CB also engages in Open Market Operations to change the monetarybase

McMahon (Warwick) Current Crisis 36 / 116

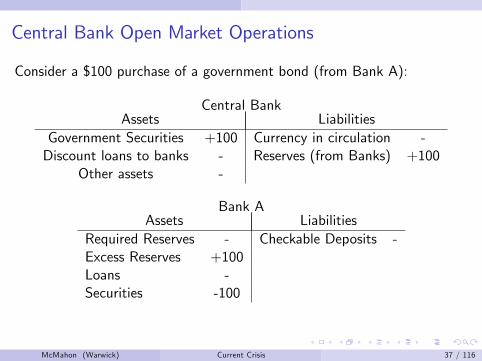

Central Bank Open Market Operations

Consider a $100 purchase of a government bond (from Bank A):

Central BankAssets Liabilities

Government Securities +100 Currency in circulation -Discount loans to banks - Reserves (from Banks) +100

Other assets -

Bank AAssets Liabilities

Required Reserves - Checkable Deposits -Excess Reserves +100Loans -Securities -100

McMahon (Warwick) Current Crisis 37 / 116

The Subprime and Financial Crisis

McMahon (Warwick) Current Crisis 38 / 116

The Subprime and Financial Crisis IUS House Prices Since 1890 (adjusted for in�ation)

Source: S&P, CaseShiller Index

McMahon (Warwick) Current Crisis 39 / 116

The Subprime and Financial Crisis IIUS House Prices and Equity Markets Have Fallen Sharply

McMahon (Warwick) Current Crisis 40 / 116

The Subprime and Financial Crisis IIIUS House Prices and Equity Markets Have Fallen Sharply

McMahon (Warwick) Current Crisis 41 / 116

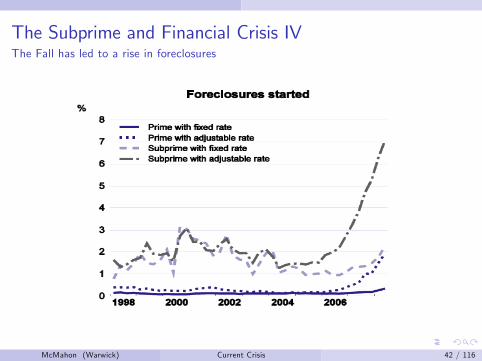

The Subprime and Financial Crisis IVThe Fall has led to a rise in foreclosures

McMahon (Warwick) Current Crisis 42 / 116

The Subprime and Financial Crisis V

But bank losses due to mortgages in this crisis are relatively small

approximately US$1,000 mnthis is equivalent to a 3% fall in the stock market (at end 2006 prices)In October 1987, the S&P 500 fell 20 % in a single month with almostno macroeconomic repercussions

Therefore, we need to understand how the shock got transmitted tobecome the large scale, global crisis that we have seen in the last 2years.

I will focus here on the idea of leverage.

McMahon (Warwick) Current Crisis 43 / 116

Leverage and the US Banking Crisis I

Leverage =assetscapital

Assets LiabilitiesReserves Checkable DepositsSecurities Time DepositsLoans BorrowingsOther assets (e.g. physical capital) Bank Capital

McMahon (Warwick) Current Crisis 44 / 116

Leverage and the US Banking Crisis II

Leverage =assetscapital

= 10

Assets LiabilitiesAssets 100 Debt 90

Bank Capital 10

McMahon (Warwick) Current Crisis 45 / 116

Leverage and the US Banking Crisis II

Leverage =assetscapital

= 9.18

Assets LiabilitiesAssets 101 Debt 90

Bank Capital 11

If debt constant, leverage is inversely proportional to asset values:

assets # ) leverage "

Holding debt constant ) counter-cyclical leverage

McMahon (Warwick) Current Crisis 46 / 116

Leverage and the US Banking Crisis IIIHouseholds

McMahon (Warwick) Current Crisis 47 / 116

Leverage and the US Banking Crisis IVPNFCs

McMahon (Warwick) Current Crisis 48 / 116

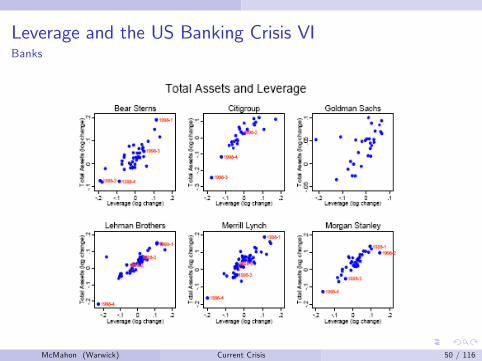

Leverage and the US Banking Crisis VBanks

McMahon (Warwick) Current Crisis 49 / 116

Leverage and the US Banking Crisis VIBanks

McMahon (Warwick) Current Crisis 50 / 116

Leverage and the US Banking Crisis VIIImplications of Asset Price Fall with Procyclical Leverage

Leverage =assetscapital

= 10 = TARGET

Assets LiabilitiesAssets 100 Debt 90

Bank Capital 10

Pro-cyclical leverage means that as asset prices go up, we increaseleverage by buying even more assets using debt.

But buying more assets pushes the value of assets " ) circular

When prices start to fall, we get a �resale of assets.

McMahon (Warwick) Current Crisis 51 / 116

Leverage and the US Banking Crisis VIIImplications of Asset Price Fall with Procyclical Leverage

Leverage =assetscapital

= 11

TARGET = 9 (falls)

Assets LiabilitiesAssets 99 Debt 90

Bank Capital 9

McMahon (Warwick) Current Crisis 51 / 116

Leverage and the US Banking Crisis VIIImplications of Asset Price Fall with Procyclical Leverage

Leverage =assetscapital

= 11

NEW TARGET = 9 (falls)

Assets LiabilitiesAssets 81 Debt 72

Bank Capital 9

To achieve new target the bank must sell o¤ assets and use theproceeds to pay down debt

1% fall in asset prices ) 18% sale of assets which puts furtherpressure on prices.

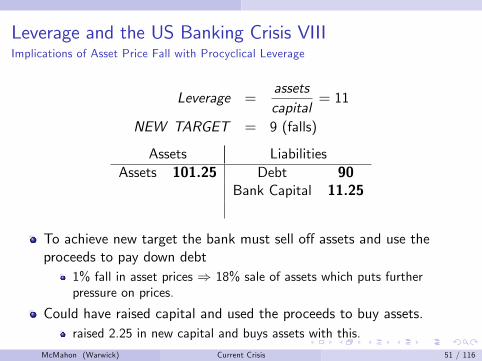

McMahon (Warwick) Current Crisis 51 / 116

Leverage and the US Banking Crisis VIIIImplications of Asset Price Fall with Procyclical Leverage

Leverage =assetscapital

= 11

NEW TARGET = 9 (falls)

Assets LiabilitiesAssets 101.25 Debt 90

Bank Capital 11.25

To achieve new target the bank must sell o¤ assets and use theproceeds to pay down debt

1% fall in asset prices ) 18% sale of assets which puts furtherpressure on prices.

Could have raised capital and used the proceeds to buy assets.raised 2.25 in new capital and buys assets with this.

McMahon (Warwick) Current Crisis 51 / 116

Leverage and the US Banking Crisis IXA Game of Two Halves

In the beginning of the crisis (up until August 2008), banks tried to coverthe declines in the values of their assets (marked-to-market) and reducethe �resale activity by raising new capital:

Source: Bloomberg

($Bn)

CitigroupWachoviaMerril LynchWashington MutualBank of America

UBSIKB DeutscheCredit SuisseDeutsche BankCredit Agricole

HSBCRBSBarclaysHBOSLloyds TSB

Mizuho FGNomura HoldingsBank of ChinaMitsubishi UFJBank Hapoalim

333.3

170.4

62.824.2

235.4

118.6

58.122.2

0

50

100

150

200

250

300

350

North America Continental Europe UK Asia

Sum of Writedown & Loss Sum of Capital Raised

McMahon (Warwick) Current Crisis 52 / 116

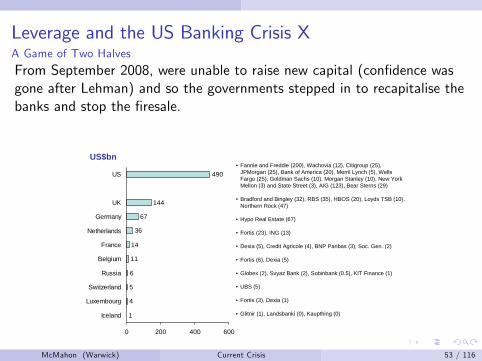

Leverage and the US Banking Crisis XA Game of Two Halves

From September 2008, were unable to raise new capital (con�dence wasgone after Lehman) and so the governments stepped in to recapitalise thebanks and stop the �resale.

1

4

5

6

11

14

36

67

144

490

0 200 400 600

Iceland

Luxembourg

Switzerland

Russia

Belgium

France

Netherlands

Germany

UK

US•Fannie and Freddie (200), Wachovia (12), Citigroup (25),

JPMorgan (25), Bank of America (20), Merril Lynch (5), WellsFargo (25), Goldman Sachs (10), Morgan Stanley (10), New YorkMellon (3) and State Street (3), AIG (123), Bear Sterns (29)

•Bradford and Bingley (32), RBS (35), HBOS (20), Loyds TSB (10),Northern Rock (47)

•Hypo Real Estate (67)

•Fortis (23), ING (13)

•Dexia (5), Credit Agricole (4), BNP Paribas (3), Soc. Gen. (2)

•Fortis (6), Dexia (5)

•Globex (2), Svyaz Bank (2), Sobinbank (0.5), KIT Finance (1)

•UBS (5)

•Fortis (3), Dexia (1)

•Glitnir (1), Landsbanki (0), Kaupthing (0)

US$bn

McMahon (Warwick) Current Crisis 53 / 116

Leverage and the US Banking Crisis XIA Game of Two Halves

Seems to be working.

Interest rate at which banks are willing to lend to each other

McMahon (Warwick) Current Crisis 54 / 116

Northern Rock - A slightly di¤erent problem

ProblemFrom the provided articles, can you develop an understanding of why theNorthern Rock crisis occurred? What were the primary failings of thebank? What was the policymakers response?

McMahon (Warwick) Current Crisis 55 / 116

Monetary and Fiscal Policy

McMahon (Warwick) Current Crisis 62 / 116

Monetary Policy

Interest rates are discussed everyday in the papers and in �nancialmarkets...Why?

Monetary policy is important because interest rates determine:

The interest rate is the cost of borrowing;

It a¤ects investment decisions by �rms;

It determines consumption decisions by families;=) it a¤ects aggregate demand.

In a recession. . . if aggregate demand is low, can stimulate economy bylowering interest rates.In a boom. . . booms driven by unusually high aggregate demand tend tolead to in�ation (overheating) and we can prevent this in�ation by reigningin aggregate demand through higher interest rates.

McMahon (Warwick) Current Crisis 63 / 116

Monetary Policy - contd

Ideal: Be �Tight� in booms and �Loose� in recessions

But:

�Long and variable lags� faced by Central Bankers;

Only get clear picture of where economy is after the fact (recognitionlag);

Takes time for interest rate changes to work their way into aggregatedemand and prices;

Very hard to tell if you are being �too loose,��too tight,� or �justright�at any particular moment;

Not always clear whether cycle is driven demand or supply shock

e.g. oils shocks of the 1970s lead to a �supply-side� recession;�stag�ation�.

McMahon (Warwick) Current Crisis 64 / 116

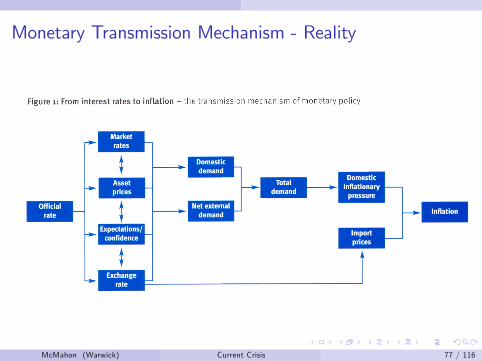

Monetary Transmission Mechanism

De�nitionThe monetary transmission mechanism describes how policy-inducedchanges...in the short-term nominal interest rate impact on real variablessuch as aggregate output and employment. Speci�c channels of monetarytransmission operate through the e¤ects that monetary policy has oninterest rates, exchange rates, equity and real estate prices, bank lending,and �rm balance sheets.

We do not know exactly what the size of each channel is (with anycertainty), but we do have good ideas about which are the main channels.

"Monetary Policy acts with long and variable lags" - MiltonFriedman

McMahon (Warwick) Current Crisis 65 / 116

Monetary Transmission Mechanism - Reality

McMahon (Warwick) Current Crisis 66 / 116

Starting at the End - Consumer Price In�ation(CPI)

%∆CPIt =N

∑i=0wi .%∆pi ,t

where wi is the weight of good i in the consumers basket of goods, and%∆pi ,t is the change in prices of the ith good.

Splitting the N goods into:

domestically produced - determined more directly by domesticdevelopments/producers;

imported goods - determined by foreign producers, but also:

the exchange rate (directly) - e.g. price of a $10 book in UK £ ifexchange rate is $1=£ 1 versus if $2=£ 1?relative price shocks - e.g. oil prices.

McMahon (Warwick) Current Crisis 67 / 116

Domestically Generated In�ation - Role of the Output GapDe�nitionWhen there is a positive (negative) output gap, i.e. demand is greater(lower) than the potential output measure, then there will be upward(downward) or in�ationary (de�ationary) pressures on prices.

What can monetary policy do:

Monetary policy a¤ects the demand side of the economy (AD curve);Policymakers will need to try to �gure out where the AS curve is - itis constantly changing.

"It is plain that if you are trying to hit an in�ation target, youhave to form a judgment about the level of demand in theeconomy relative to potential supply and how it is likely to move.This must, among other things, involve making judgments aboutgrowth prospects, not for their own sake but because they arevital when it comes to understanding the prospects for in�ation."

McMahon (Warwick) Current Crisis 68 / 116

How Monetary policy a¤ects AD

AD = C + I + G + (X � Z )where C is �nal consumption by individuals and families mainly, I isinvestment in gross �xed capital (by �rms and households), G isgovernment spending, (X � Z ) is the trade balance (X is exports and Z isimports).We can broadly assume the G is not a¤ected too much by monetarypolicy- although there is some e¤ect from the business cycle on G .The other 3 will depend on how the interest rates a¤ect:

1 market interest rates;2 asset prices (equities, house prices, etc...);3 the exchange rate;

For all 3 e¤ects, expectations and how the move is interpreted plays a keyrole.

McMahon (Warwick) Current Crisis 69 / 116

How Monetary policy a¤ects ADMarket interest rates

As we already saw, the short rate will closely follow the policy rate andthen the longer term rates will depend on the expectations of futureinterest rates.

If the interest rate is increased, people might think:

interest rates in the future will be higher (better growth prospects);

lower future interest rates.

Therefore, it is necessary to understand how decisions will be interpretedand how expectations will change (see later).

McMahon (Warwick) Current Crisis 70 / 116

How Monetary policy a¤ects ADAsset Prices

If interest rates increase, and so bond yields also increase, bond prices willfall:=) this can generate a wealth e¤ect.=) this can also cause the cost of �rms investment and �nancing toincrease.

A similar thing may happen with equities - if the future is discounted witha higher interest rate, then equities decline with interest rate increases...but what if the policy is interpreted as signalling better growth prospects?

House prices, as a result of higher interest rates, may fall because lesspeople can a¤ord to take out large loans.

McMahon (Warwick) Current Crisis 71 / 116

How Monetary policy a¤ects ADExchange Rates

When the interest rate increases, then the exchange rate should, ceterisparibus, appreciate:

Foreigners will get a higher return on savings in the UK thanelsewhere - money �ows into the UK;

UK residents will rather save at home rather than abroad - less money�ows out;=) higher demand for the pound means that it will increase in valuerelative to other currencies.

The exchange rate is simply the price of one country�s money in terms ofanother country�s money.

McMahon (Warwick) Current Crisis 72 / 116

How Monetary policy a¤ects ADConsumption

The e¤ect on consumption comes through:

1 Market interest rates

depends on net position!depends on how quickly the interest rates are changed;depends on whether interest rates are �xed or �oating;depends on country of borrowing;

2 Asset prices and wealth e¤ects

Poorer people spend less.

McMahon (Warwick) Current Crisis 73 / 116

How Monetary policy a¤ects ADInvestment and Net Trade

The e¤ect on investment will come through:

1 the e¤ect on market interest and other �nancing costs;2 the e¤ects on demand.

The e¤ect on net trade is driven:

1 the exchange rate

appreciation lowers (X � Z ) as foreign goods seem cheaper (Z ") andforeigners will sell more of the home produced good (X #).

McMahon (Warwick) Current Crisis 74 / 116

Monetary Policy in Action

ProblemUsing the AS-AD framework developed yesterday, answer and explain eachof the following questions:

1 Can monetary policy can o¤set a reduction in consumption spending(perhaps related to uncertainty)?

2 How might monetary policy lead to �stag�ation�by wronglyresponding to an oil price increase?

McMahon (Warwick) Current Crisis 75 / 116

Second Round E¤ects and ExpectationsE¤ects described so far are �rst round e¤ects - directly the result ofchanges in the interest rate. We must also consider the second rounde¤ects:

Price shocks (such as oil) feeding into the wage setting process;

First round e¤ects of GDP leading to other changes in demand in theeconomy - explains the widespread e¤ects of interest rates on allsectors.

While the central bank can do nothing about the �rst round e¤ects ofsupply shocks, they can deal with the second round e¤ects.How the policy decisions are interpreted can have a key e¤ect on theeconomy:

In�ation expectations are particular important

Role in wage-setting to determine in�ation;Real interest rate is key = int.rate � πe

McMahon (Warwick) Current Crisis 76 / 116

Monetary Transmission Mechanism - Reality

McMahon (Warwick) Current Crisis 77 / 116

Long and Variable Lags

McMahon (Warwick) Current Crisis 78 / 116

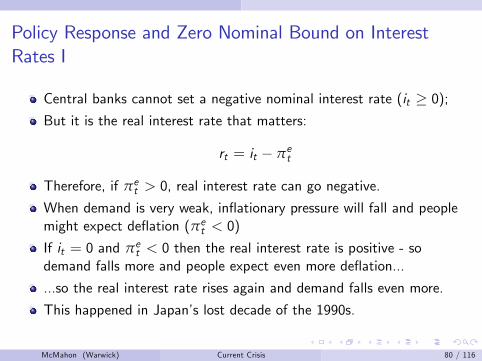

Policy Response and Zero Nominal Bound on InterestRates I