session 3: drug insurance pooling - member | soa · session 3: drug insurance pooling ... •claims...

TRANSCRIPT

Session 3: Drug Insurance Pooling

Presented by:

Kathy Seliga, FSA, FCIA, Sun Life Financial Tom Strickland, FSA, FCIA, RBC Insurance

David Willows, Green Shield

2016 SOA Health SeminarSession 3: Drug Insurance PoolingKATHY SELIGA

TOM STRICKLAND

M AY 2 4 , 2 0 1 6

DAVID WILLOWS

• Canadian Drug Insurance Pooling Corporation (CDIPC)• What is it?

• How did pooling work before CDIPC?

• Plan Sponsor view of CDIPC

• Risk sharing under CDIPC

• What groups are ineligible (and what happens to ineligible groups)

• CDIPC Regional Pools

• How does CDIPC work with the Quebec provincial drug pool?

• Common misperceptions

• Positive outcomes of the CDIPC

• Experience to date

• Where do we go from here?

2

AGENDA

CDIPC – WHAT IS IT?

• CDIPC is an insurance industry-wide drug pool for annually recurring high cost drugs

• Insurers get pooling protection against volatility from very high cost drugs

• Insurers required to follow certain rules meant to improve insurance accessibility and affordability for groups with large drug claims for specific individuals

• All Canadian Group insurers have joined CDIPC

3

HOW DID POOLING WORK BEFORE CDIPC?

• Before CDIPC, insurers set up Large Amount Pooling (LAP) for high cost drug claims • Most common pooling threshold $10,000 per individual – but many

alternatives (per certificate, drug only versus all Health benefits, other dollar levels)

• “Base” renewal pricing only includes amounts under the threshold (non-pooled claims)

• Pooling charge added to the non-pooled rate at the end to cover claim costs over the threshold

• No clear rules on what could/could not be done in pricing for large drug claims or methods to limit anti-selection

4

CDIPC CHANGES – PLAN SPONSOR VIEW

• The basic pooling structure does not change under CDIPC from the Plan Sponsor’s point of view

• Insurer provides very similar pooling coverage under CDIPC –but now the “LAP” has a new name – EP3 (Extended Health Care or Drug Policy Protection Plan)

• CDIPC is “behind the scenes”, but…• Insurers must follow CDIPC rules when pricing EP3s – better protection

for the Plan Sponsor• Key rule – Insurer must provide pooling that meets the minimum EP3

requirements and pooled rates must follow a standard methodology for all groups in a given pool (ignoring the individual group’s pooled claims)

• Companies quoting on a CDIPC eligible group must follow CDIPC rules (but they can decline to quote)

• CDIPC also establishes consistent methodology to limit anti-selection for new groups entering the Industry pool

5

RISK SHARING UNDER CDIPCWhen Does CDIPC Pool Claims?

• As of 2016, CDIPC pools claims for certificates (the whole family, if family coverage) that have exceeded $65,000 (the “initial threshold”) for two consecutive calendar years

• Once two years above $65,000 have been satisfied, in the second and later years, the CDIPC pool covers amounts above $32,500 (the “ongoing threshold”)

• Pooling of amounts above the ongoing threshold continues for that certificate until it has two consecutive years of claims below the ongoing threshold

• The initial and ongoing threshold levels are subject to change from year to year

6

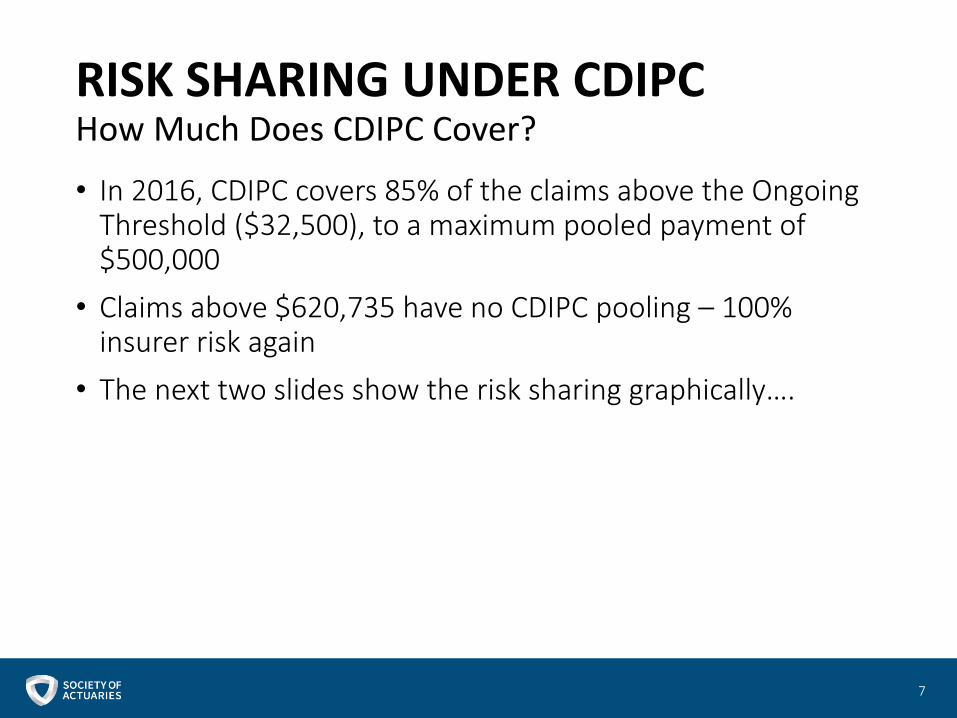

RISK SHARING UNDER CDIPCHow Much Does CDIPC Cover?

• In 2016, CDIPC covers 85% of the claims above the Ongoing Threshold ($32,500), to a maximum pooled payment of $500,000

• Claims above $620,735 have no CDIPC pooling – 100% insurer risk again

• The next two slides show the risk sharing graphically….

7

RISK SHARING UNDER CDIPCBasic Overview

The BASIC overview when claims exceed the CDIPC maximum

8

Insurer’s Large Amount (EP3) Pooling Threshold

Industry Ongoing Pooling Threshold

Industry Pooling Maximum

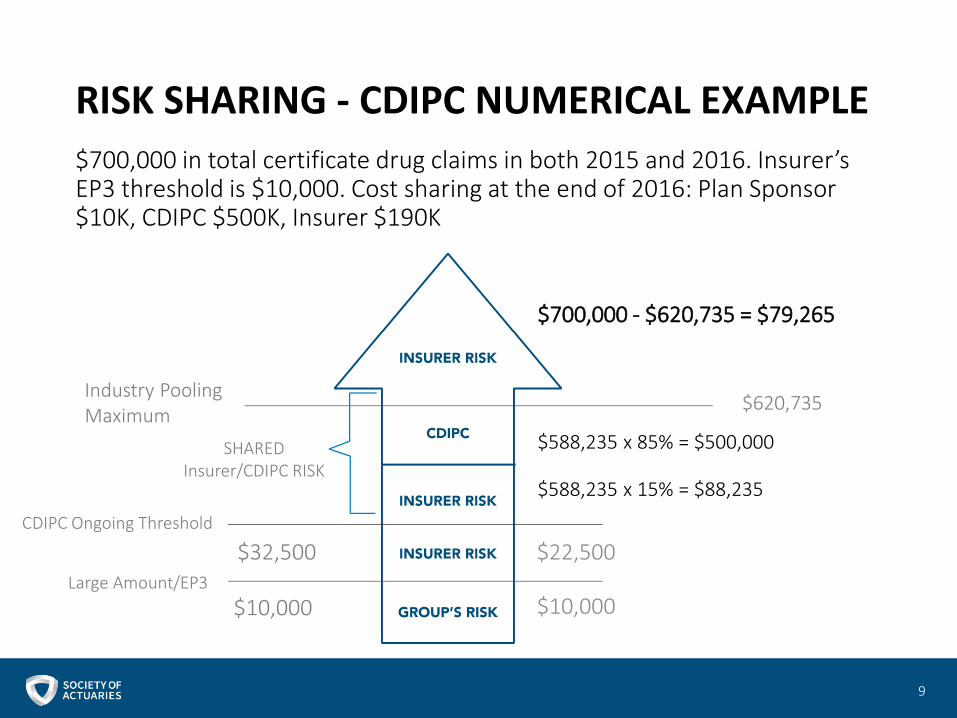

RISK SHARING - CDIPC NUMERICAL EXAMPLE

$700,000 in total certificate drug claims in both 2015 and 2016. Insurer’s EP3 threshold is $10,000. Cost sharing at the end of 2016: Plan Sponsor $10K, CDIPC $500K, Insurer $190K

9

$700,000 - $620,735 = $79,265

$620,735

$588,235 x 15% = $88,235

$588,235 x 85% = $500,000

$22,500

$10,000

Industry Pooling Maximum

SHARED Insurer/CDIPC RISK

CDIPC Ongoing Threshold

Large Amount/EP3

$32,500

$10,000

INELIGIBLE GROUPS

• Ineligible Groups for CDIPC (2016 values):• Non-insured funding types

• Administrative Services Only

• Refund Accounting

• Cost Plus/Health Care Spending

• Fully Reinsured (e.g. multi-national pooling)

• Drug maximums under $32,500 per individual (Ongoing Threshold) or $65,000 per certificate (Initial Threshold)

• High deductible plans (more than $1,100 single, $2,200 family, $35 per DIN)

• Voluntary plans (simple spousal opt-outs are okay)

10

WHAT HAPPENS TO INELIGIBLE GROUPS?

• Ineligible groups are in the same position as before CDIPC:• Insurers free to offer pooling parameters of their choice

(as before)

• Insurers free to price and limit anti-selection as they see fit (as before)

11

CDIPC ANTI-SELECTION CONTROLS

• CDIPC rules mandate risk controls to limit anti-selection when an employer enters the CDIPC pool by:• A virgin group taking out coverage

• Changing from ineligible to eligible funding arrangement (e.g. ASO to fully insured)

• Plan design change (e.g. $10,000 drug maximum to unlimited maximum)

12

WHAT ARE THE ANTI-SELECTION CONTROLS?

• When a group enters the CDIPC industry pool, the insurer reviews the claims by certificate to see if any certificate has claims exceeding the Ongoing Threshold ($32,500 in 2016)

• If claims are available from prior carrier or insurer’s own data, check the claims before entering the industry pool

• If claims are not available at issue, first 12 months claims after issue are reviewed

• If a certificate’s claims exceed the Ongoing Threshold, they become an “excluded certificate” • Must be excluded from CDIPC pool and insurer EP3 pool pricing• Insurer may still pool the claim in a non-EP3 pool• If excluded from all insurer pools, claims for that certificate included in

the “non-pooled” claims for renewal pricing purposes• “Excluded certificate” claims are still paid by the insurer to the

employee – excluded just refers to their treatment in renewal pricing

13

WHAT ARE THE ANTI-SELECTION CONTROLS?

• All groups in the CDIPC industry pool receive an “EP3 statement” from the insurer at least annually

• Key information on the EP3 statement:• Current EP3 pooling arrangement (e.g. $10,000 per

individual)• If part of the group is ineligible for CDIPC (e.g. one class

has a $5,000 drug maximum) – describe what is/is not eligible

• State whether there are any excluded certificates (no details due to confidentiality)

• A subsequent insurer will get (confidentially) details of excluded certificates, and continue to exclude them

14

CDIPC REGIONAL POOLS

• There are three industry pools based on differences in provincial drug programs:

• Pool 1 – Residents of Alberta, Ontario, Nova Scotia, New Brunswick, Newfoundland and Labrador, Prince Edward Island, Yukon, North West Territories and Nunavut

• Pool 2 – Residents of Quebec for costs not covered under the Quebec Drug Insurance Pooling Corporation

• Pool 3 – Residents of British Columbia, Manitoba and Saskatchewan

• The total pooled drug claims are shared by all participating insurers based on each participating insurer’s market share of total paid drug claims for all insured business in the applicable provinces for that pool.

15

CDIPC AND QUEBEC RAMQ DRUG POOLING

• For Quebec certificates, RAMQ is the “first payor” pooling mechanism

• CDIPC pays any cost it would normally pay that the Quebec pool has not already paid, e.g.• Claims between the CDIPC threshold and the RAMQ

threshold, where RAMQ is higher

• Non-Quebec certificates in a Quebec group

16

CDIPC – COMMON MISPERCEPTIONS

• “CDIPC will lower pooling costs”• CDIPC is only a mechanism to share the high drug claim

risk among insurers

• CDIPC does not remove the risk – insurers will charge EP3 pooling rates to cover all their costs above the EP3 threshold, including the average cost of claims above the CDIPC threshold

• Addition of many new high cost drugs will continue to increase the pooling charge as a percentage of total drug cost

17

EXPERIENCE TO DATE

• Industry Drug Pool took effect January 1, 2013

• January 1, 2012 is the date that drug claims were eligible to begin accumulating toward the initial threshold (remember it’s a recurring, two year requirement)

• Through 2012 and 2013 certificates’ drug claims accumulated towards the initial threshold (which was $50,000 at that time)

• Claims incurred in 2013 were the first claims submitted to the industry pool based on the ongoing threshold ($25,000 at that time)

• In 2014 carriers submitted any eligible claims to the industry drug pool, based on 2013 calendar year claims over the ongoing threshold

18

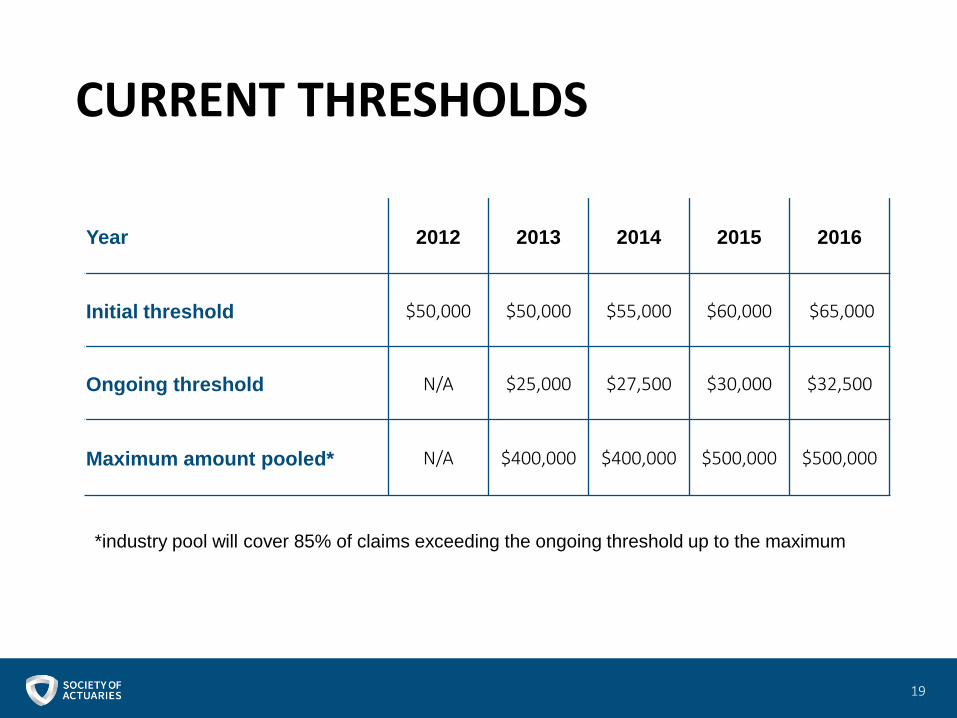

CURRENT THRESHOLDS

19

Year 2012 2013 2014 2015 2016

Initial threshold $50,000 $50,000 $55,000 $60,000 $65,000

Ongoing threshold N/A $25,000 $27,500 $30,000 $32,500

Maximum amount pooled* N/A $400,000 $400,000 $500,000 $500,000

*industry pool will cover 85% of claims exceeding the ongoing threshold up to the maximum

2014 POOLING RESULTS AT A GLANCE

20

2013 & 2014 CERTIFICATES WITH CLAIMS COVERED BY CDIPC,Banded by Amount Covered

21

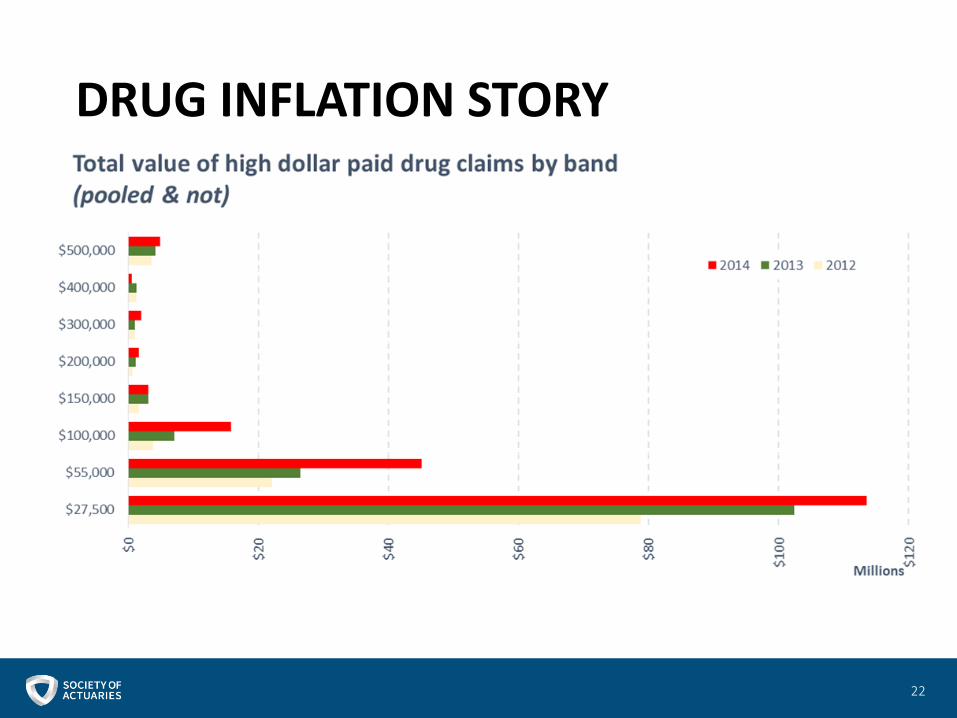

DRUG INFLATION STORY

22

INFLATIONARY DRIVERS

• 118 new certificates (claims) represent $6.7M (51% of total pool).• Many are for

• Remicade which grew by $1.4M and 28 certificates• Kuvan which grew by $578K and 6 certificates• Revlmid which grew by $476 and 7 certificates

• 17 drugs new to 2014 pooling represent $2.22 M (17% of total pool)• Kalydeco with 6 certificates totalling $1.55M is a major

contributor.• On market November 2012 so would not show up in 2013 pooling.• Treatment of patients age two years and older who have a

designated mutation in the Cystic Fibrosis Transmembrane conductance Regulator (CFTR) gene.

23

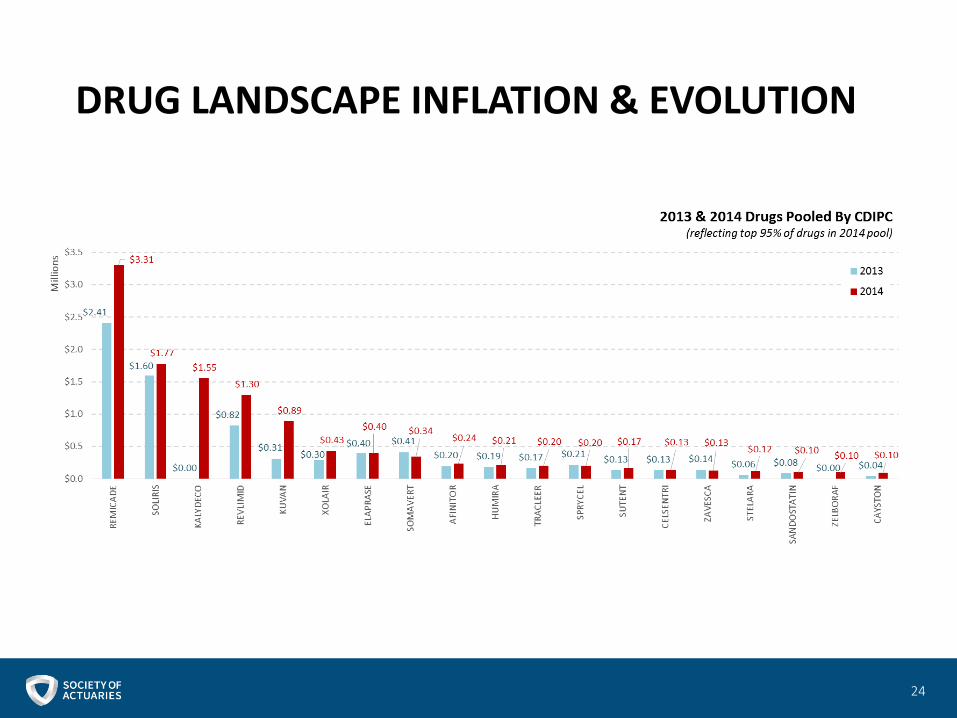

DRUG LANDSCAPE INFLATION & EVOLUTION

24

CDIPC – POSITIVE OUTCOMES

• CDIPC has delivered on the following key principles:

• Availability – All currently fully insured groups in Canada should be able to continue to purchase/renew group extended healthcare coverage to meet their needs

• Affordability – All currently fully insured groups should be able to purchase group extended health care coverage at a reasonable price. Plan sponsors are not subject to experience rating due to the presence of a recurring claim from one of their members or dependents

• Viability – both large and small participating insurers should be able to abide by the principles and continue to offer health insurance products

• Participative – Any sustainable solution should be available to all interested eligible insurance companies

• Competitive – In its current form the CDIPC is pro-competitive and continues to encourage active and vigorous competition in the market

25

WHERE DO WE GO FROM HERE?

• There are no immediate plans for significant changes to the CDIPC framework

• Quebec drug pooling started out as insured plans only, then later included non-insured business –CDIPC could consider that in the future

• Annual updates required for Initial Threshold, Ongoing Threshold and Maximum Pooled Amount

26

QUESTIONS?