slide 1 corporate...

TRANSCRIPT

Corporate PresentationSlide 1

Corporate PresentationSlide 2

Except for historical information, the matters discussed in thispresentation are forward-looking statements that are subject to certain risks and uncertainties which could cause the actual results to differ materially from those projected, including industry trends, the timing and strength of the Company's or competitors’ new product and service offerings, the mix of product and service revenues, changes in the Company's or competitors’ business or pricing strategies, changes in the prevailing political and regulatory framework in which the Company operates or in economic or technological trends or conditions, including currency fluctuations, inflation and consumer confidence, on a global, regional or national basis and other risks detailed from time to time in the Company’s SEC reports. The Company assumes no obligation to update the information herein contained.

PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995 SAFE HARBOR

Disclaimer

Corporate PresentationSlide 3

WHO ARE WE?

Orbotech is a world leader in providing yield and productivity enhancement solutions to the electronics industry

Orbotech’s dedicated worldwide team ensures that it delivers the most innovative technologies

Virtually every electronic device in the world is produced using Orbotech systems

Corporate PresentationSlide 4

THE INDUSTRIES WE SERVE

Bare PCB Production5500 systems installed

PCB Assembly1600 systems installed

FPD Manufacturing500 systems installed

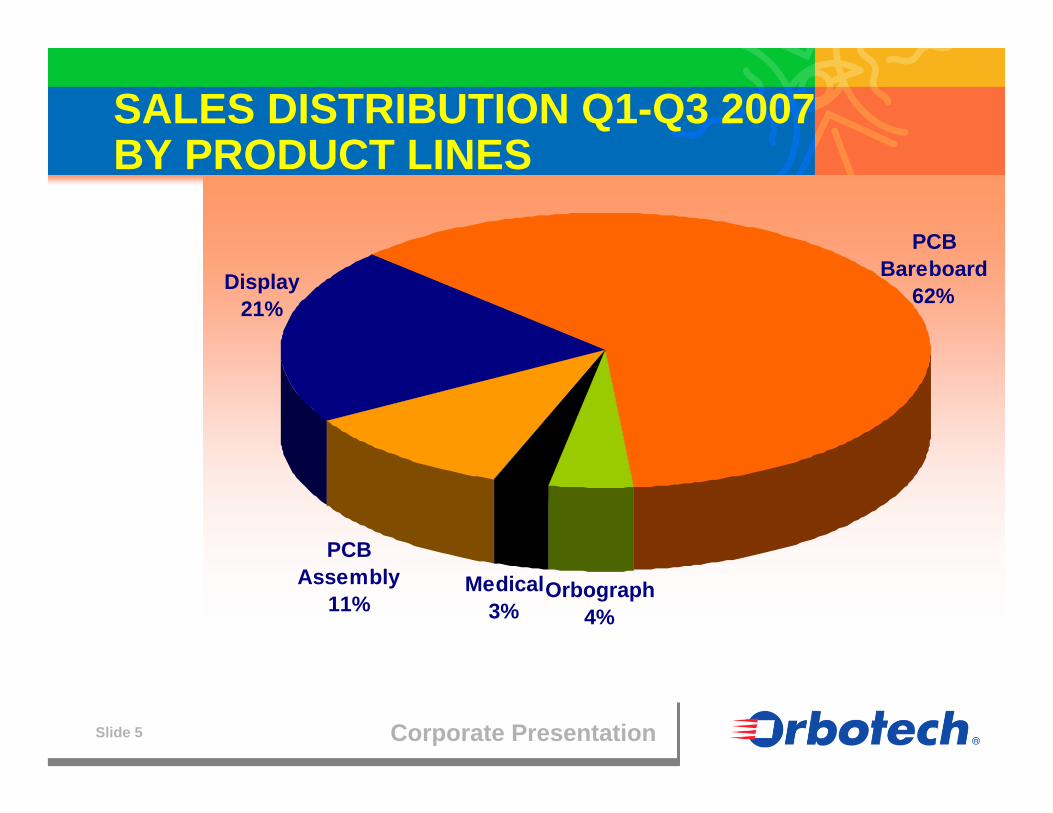

Corporate PresentationSlide 5

Medical3%

Orbograph4%

PCB Bareboard

62%Display21%

PCB Assembly

11%

SALES DISTRIBUTION Q1-Q3 2007 BY PRODUCT LINES

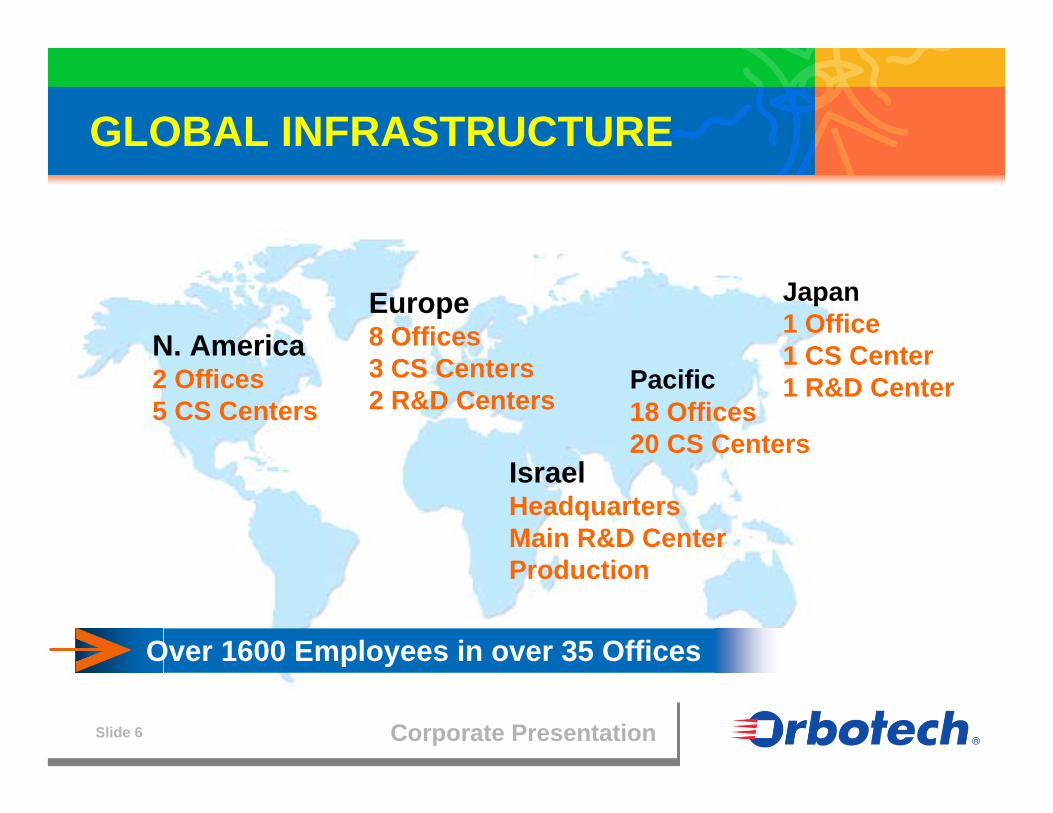

Corporate PresentationSlide 6

GLOBAL INFRASTRUCTURE

IsraelHeadquartersMain R&D CenterProduction

Europe8 Offices 3 CS Centers2 R&D Centers

N. America2 Offices 5 CS Centers

Japan1 Office1 CS Center 1 R&D CenterPacific

18 Offices 20 CS Centers

Over 1600 Employees in over 35 Offices

Corporate PresentationSlide 7

Europe11%

North America

15%Other

1%

Korea14%

Taiwan18%

Japan10%

China31%

SALES DISTRIBUTION Q1-Q3 2007 BY REGION

Corporate PresentationSlide 8

90% of current product sales are from products introduced over the last 24 monthsOver 400 Scientists and EngineersOver $60M annual R&D budget

R&D INVESTMENT

Corporate PresentationSlide 9

GROWTH STRATEGY

Bare PCB Production

Corporate PresentationSlide 11

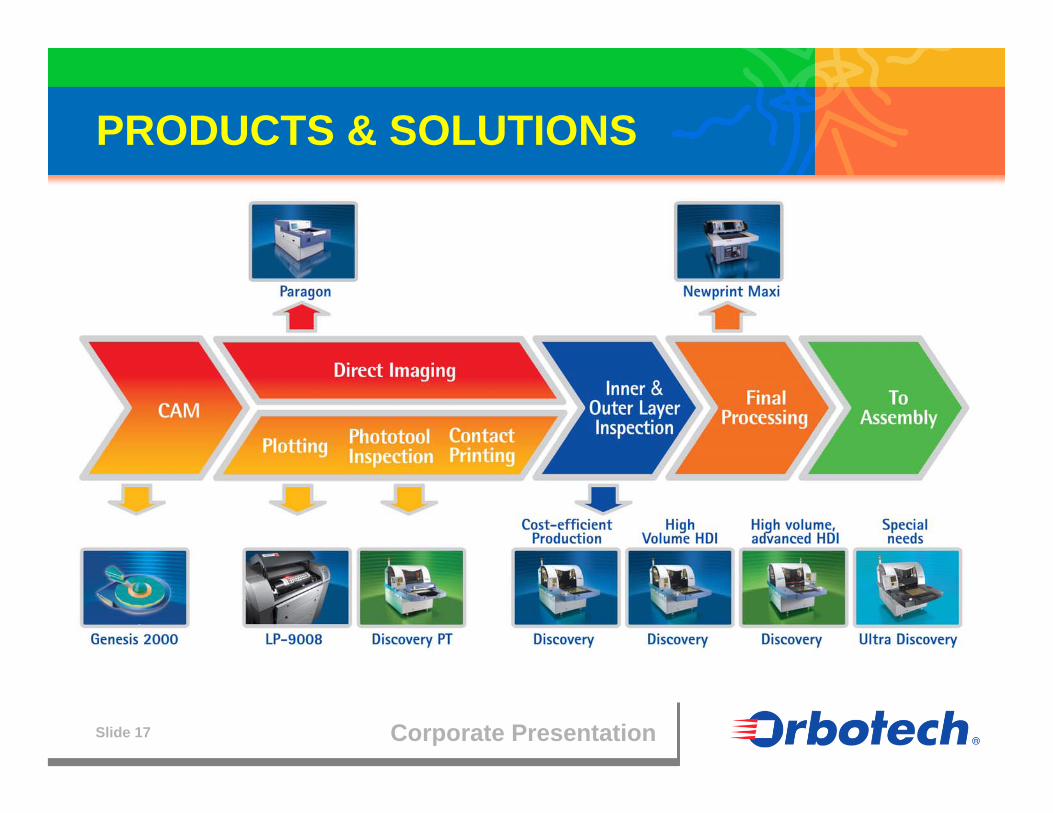

BARE PCB PRODUCTION

Automated Optical Inspection (AOI)

Laser Direct Imaging (LDI)

Laser Plotting

Computer Aided Manufacturing (CAM)

Orbotech is the world leader in

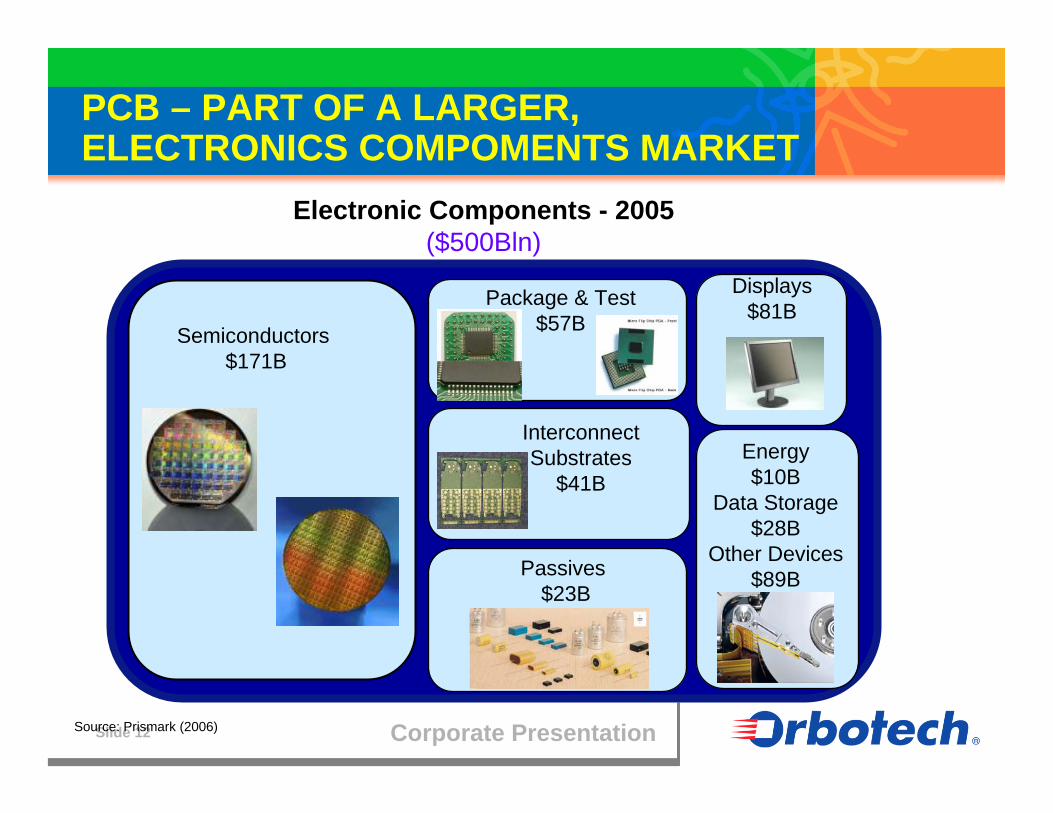

Corporate PresentationSlide 12

Electronic Components - 2005($500Bln)

Semiconductors $171B

Package & Test $57B

Passives $23B

Displays $81B

Energy $10B

Data Storage $28B

Other Devices $89B

Interconnect Substrates

$41B

PCB – PART OF A LARGER, ELECTRONICS COMPOMENTS MARKET

Source: Prismark (2006)

Corporate PresentationSlide 13

Expected growth of 5-7% in next few years

Over 80% of the market in the Far East

- China is world’s largest PCB producer

Aggressive expansion plans

Cell phones driving the industry

- Over 1BN phones in 2007

Fastest growing segments: microvia, IC substrates, flex

BARE PCB MARKET SUMMARY

Corporate PresentationSlide 14

STRONG GROWTH IN HIGH END SEGMENTS

PCB Value by Segment [$M]

0 2000 4000 6000 8000 10000 12000 14000 16000

SS+DS

4-& 6-layer

MLB

Microvia

Si platform

Flex

20072011

High end

Low end

30%

33%

34%

28%

17%

14%

Source: Prismark (08/’07)

Corporate PresentationSlide 15

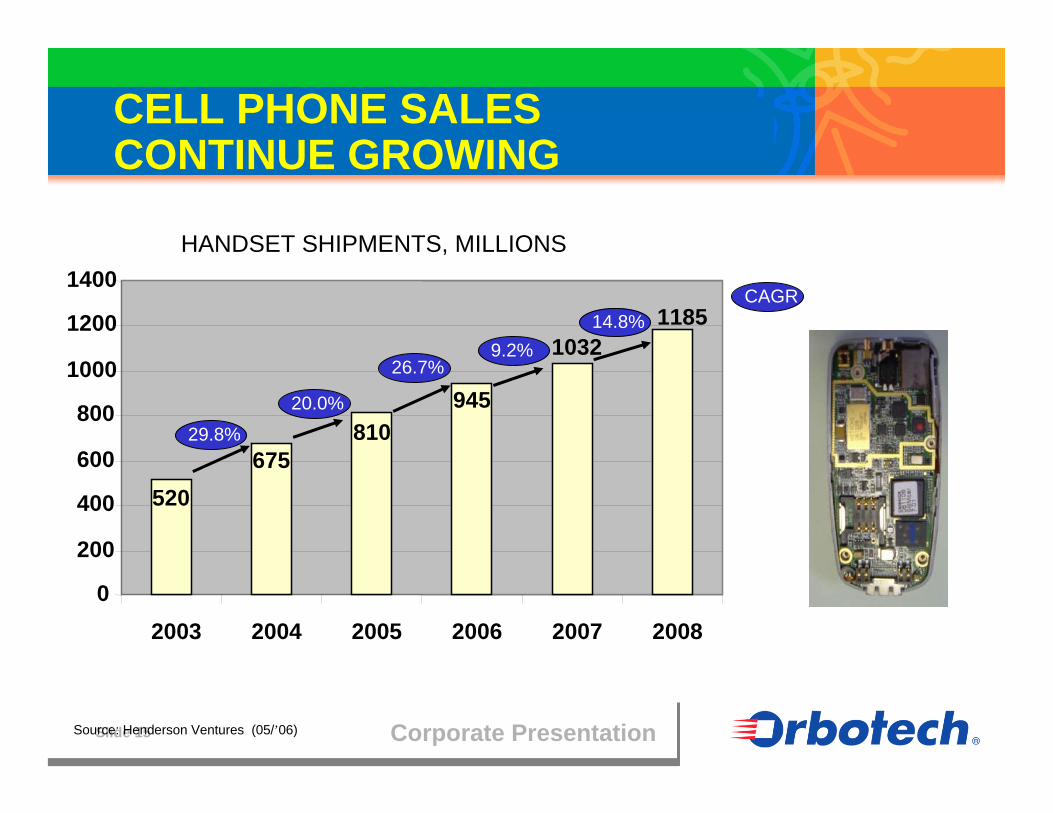

CELL PHONE SALES CONTINUE GROWING

520675

810945

10321185

0

200

400

600

800

1000

1200

1400

2003 2004 2005 2006 2007 2008

29.8%

20.0%

26.7%9.2%

14.8%

HANDSET SHIPMENTS, MILLIONS

Source: Henderson Ventures (05/’06)

CAGR

Corporate PresentationSlide 16

ONE iPhone, TWO MAIN PCBs, SEVERAL FLEX, MANY IC SUBSTRATES

Wireless board Application board

Source: Prismark (06/’07)

Corporate PresentationSlide 17

PRODUCTS & SOLUTIONS

Corporate PresentationSlide 18

DISCOVERY™

Industry’s Best Selling AOI

Simple with Push-to-Scan™- The easiest AOI solution in the industry

Intelligent with Visual Intelligence™- Detect all you want and only what you want

Powerful impact with new AOI economics- Maximum output with maximum availability

Over 1000 sold worldwide

Corporate PresentationSlide 19

PARAGON™

Industry’s Only Field Proven Laser Direct Imaging (LDI) SystemEnabling technology for complex and advanced applicationsIncreased adoption for high-end mainstream applicationsUsed in all segments including packaging and solder maskFuture direction: high resolution, high throughput

Over 285 LDI systems sold worldwide

Corporate PresentationSlide 20

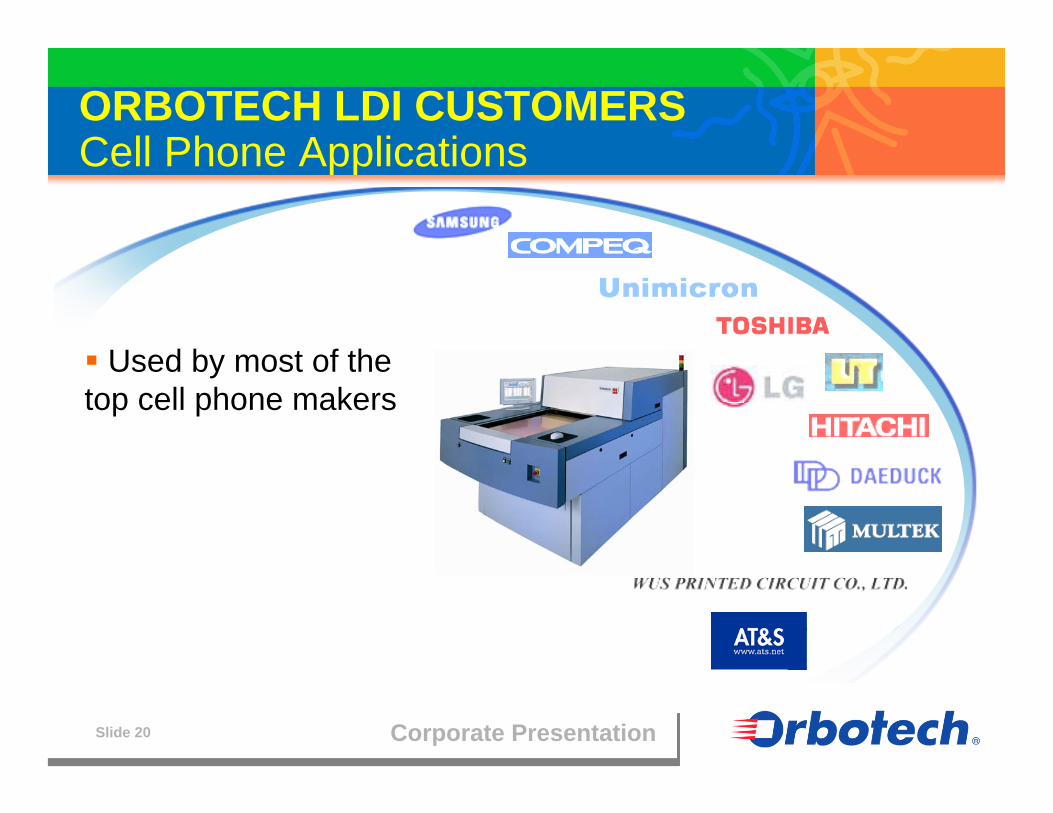

ORBOTECH LDI CUSTOMERS Cell Phone Applications

Used by most of the top cell phone makers

Corporate PresentationSlide 21

NEW SYSTEM

Founded in 1993 - Privately owned company, Headquarters in Gorizia, Italy

13 years of ground-breaking expertise in inkjet for PCB

Unique, leading edge technology

In house, “hands-on” capability across all aspects of inkjet technology for the electronics industry

Main market: Legend inkjet printing in Europe and USA

Corporate PresentationSlide 22

Strategic Level- Acquire world class inkjet know-how and expertise- Provide opportunity for developing future products and markets

Market- Quick entry into inkjet for PCB: Legend, Etch & future products- Complementary to our DI for PCB- Synergetic with inkjet for other industries

Technology- Leading, proprietary technology (UV-based) for PCB- Design-to-cost, “good enough” machines- Complementary to our technologies (panel & data handling, front end, multiple head designs)

ORBOTECH ITALY (NEW SYSTEM) Business & Technology Opportunity

Corporate PresentationSlide 23

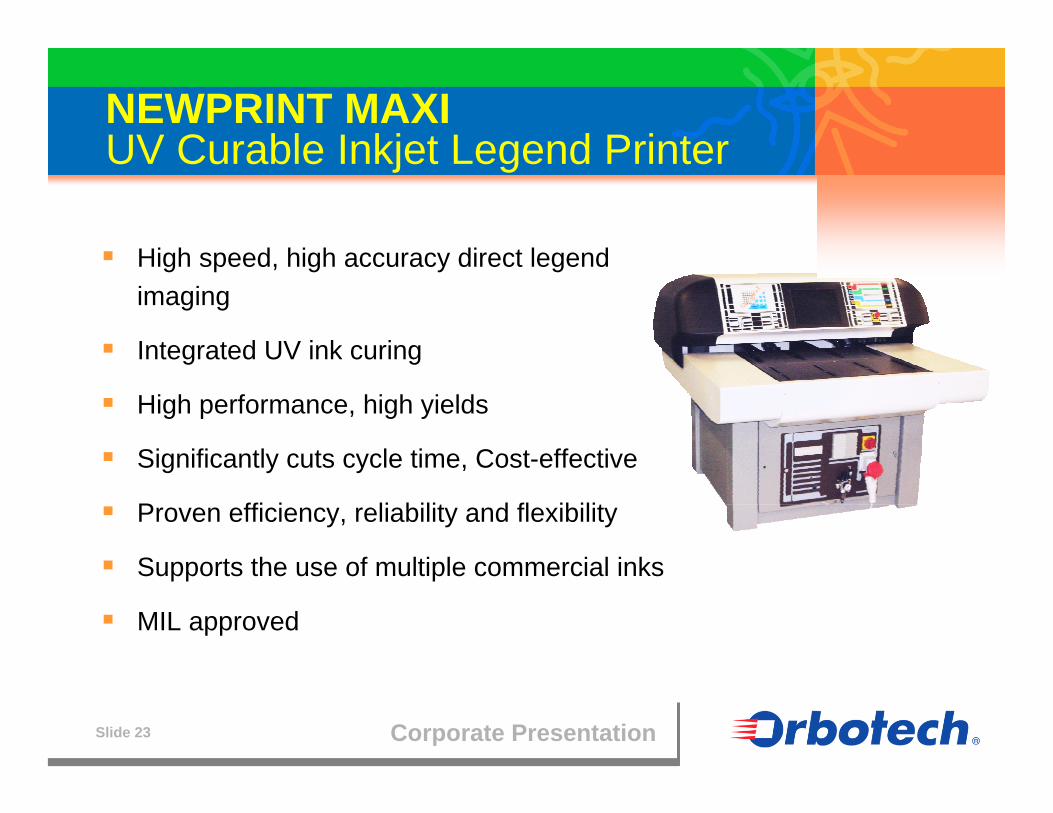

NEWPRINT MAXIUV Curable Inkjet Legend Printer

High speed, high accuracy direct legend imaging

Integrated UV ink curing

High performance, high yields

Significantly cuts cycle time, Cost-effective

Proven efficiency, reliability and flexibility

Supports the use of multiple commercial inks

MIL approved

PCB Assembly

Corporate PresentationSlide 25

PCB ASSEMBLY

Orbotech is a leading provider of

Automated Optical Inspection

Process Control Software

Corporate PresentationSlide 26

MARKET SUMMARY

EMS and ODM market will reach $227B (TFI 10/2005), high growth > 12% from outsourcing

Volume production will continue to concentrate in China

Low volume & automotive will continue to be in Europe, USA and Japan

Overall AOI market > $470M in 2008 (PRG 9/2005)

Corporate PresentationSlide 27

ASSEMBLY AOI DRIVERS

Smaller components, finer pitch- Impossible to control by visual inspection- Multiple stage inspection is required

Limited access for electrical test

Traceability- Component version and warranties control- Production information and process control

Outsourcing trend (safety margin when not manufactured by OEM)

Corporate PresentationSlide 28

ASSETS & CHALLENGES

Advanced, 3-D technology platform - Simple, cost-effective, high performance

Complete, integrated solution- AOI for all inspection stages & applications- Closed loop process control & yield management tools

Extensive global infrastructure and local support

Expert AOI know-how and experience

Fragmented market, highly competitive AOI landscape

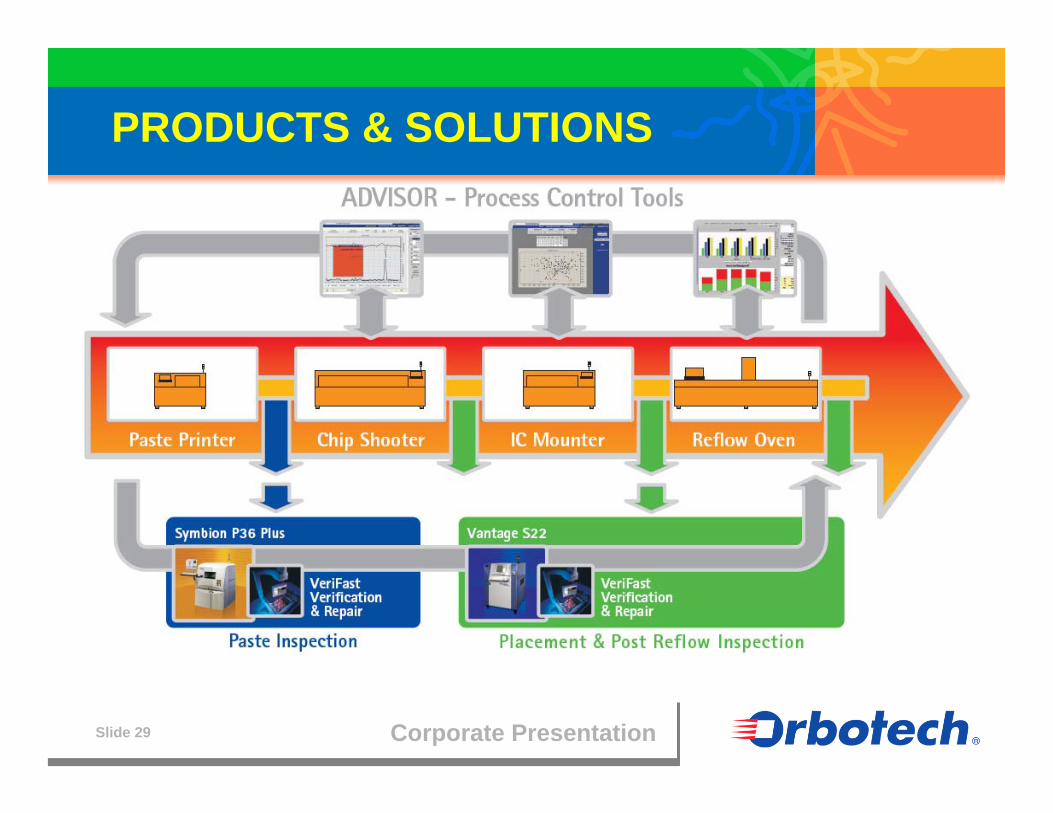

Corporate PresentationSlide 29

PRODUCTS & SOLUTIONS

Corporate PresentationSlide 30

SYMBION™ SERIES

New generation solder paste and post-reflow AOI systems

Specialized 3-D & 2-D detection

Very simple operation

Ultra-fast speed

Integrated process control software

Over 230 new generation systems sold worldwide

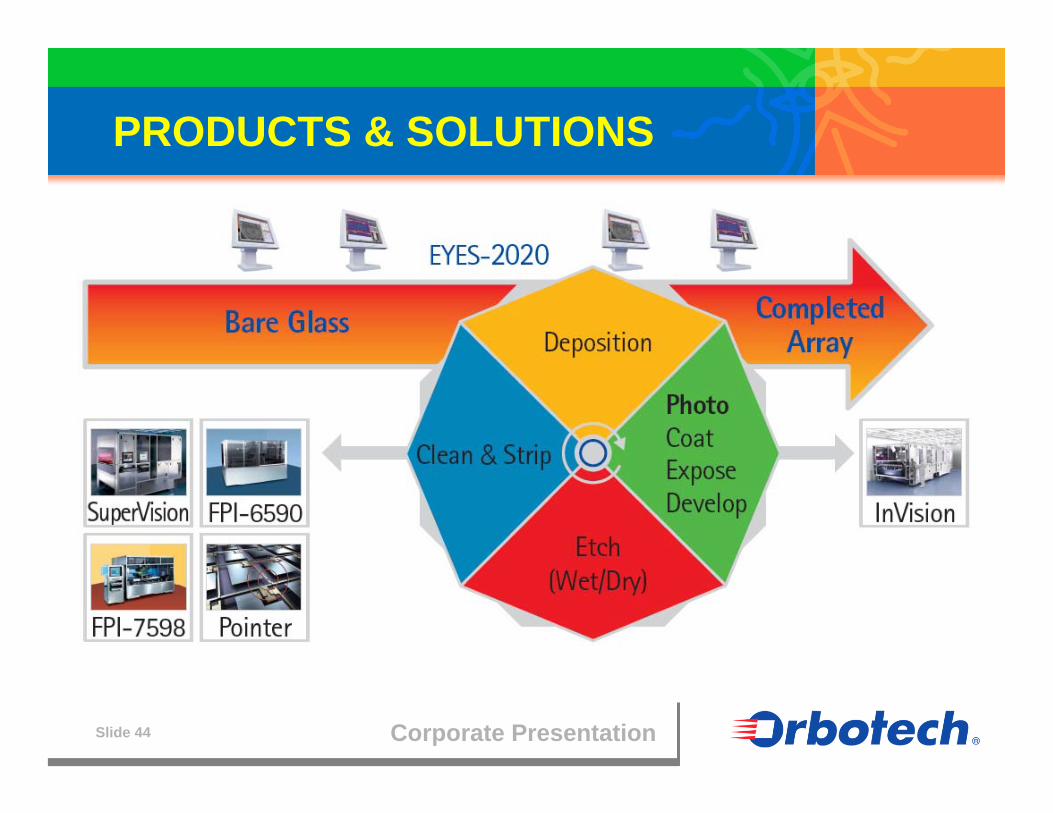

Flat Panel Display Manufacturing

Corporate PresentationSlide 32

FPD MANUFACTURING

Orbotech is the world’s leading provider of

Yield Management

Automated Optical Inspection

Corporate PresentationSlide 33

ORBOTECH PRESENCE

Presence at all LCD fabs

Proven solutions for all generations

Future-proof technology: OLED, plastic-based & other specialties

Corporate PresentationSlide 34

INDUSTRY OUTLOOK

FPTV industry outlook - Market will be expanded by 2015 till 200M units for LCD-TV

Significant movement recently- Major brands are to focus on LCD for 40” and up which has:

Very positive impact on LCDNegative impact on the PDP industry

CAPEX impact - Positive outlook – new investments are being announced - Materialize mainly as of H2 ‘08

Long term- New manufacturing technologies are being researched for and

implemented for:Improving panel qualityCost reduction purposes

Corporate PresentationSlide 35

TFT LCD LARGE AREA APPLICATIONS(Units)

Source: DisplaySearch Q3’07 Quarterly Worldwide FPD Forecast Report

TVs grow 32% CAGR from 28.5M in 2005 to 155.2M in 2011Notebook CAGR = 20%, Desktop Monitor CAGR = 11%

0

50,000

100,000

150,000

200,000

250,000

2 0 0 5 2 0 0 6 2 0 0 7 2 0 0 8 2 0 0 9 2 0 1 0 2 0 1 1

Uni

ts

LCD TV Notebook PC Desktop Monitor

Corporate PresentationSlide 36

TV DEMAND FORECAST BY TECHNOLOGY

Corporate PresentationSlide 37

2008-10 NEW 30KG/m FABS FORECAST

Investment plans for the next 3 years are: ~42 new a-Si Fabs~5 new S/M Fabs

Decisions of 2 leading companies have a major impact on the equipment marketThe number of new Fabs is inline with the glass demand for LCD FPD productsSimilar number of Fabs is expected for CF

Corporate PresentationSlide 38

SHARP 108” LCD TV:How far LCD manufacturing technology has come

53”

134cm

94”

239cm

Corporate PresentationSlide 39

THIS IS REAL SIZE

Corporate PresentationSlide 4022366812282424363350x3900G12

2223668121824242950x3450G11

2222368101518242850x3050G10

112223681012182400x2800G9

1122238810152200x2500G8.5

1122238810152160x2460G8

12223688121950x2250G7.5

11223668101870x2200G7

12233681500x1850G6

1222361300x1500G5.5

122231100x1300G5

118"105"95"85"75"65"57"46"42"37"32"Glass Size

16:9Aspect ratio

Generation

SUBSTRATE SIZE – The Way To Reach The Price & Size Goals

Source: ADR Nov., 2006

Corporate PresentationSlide 41

IMPLICATIONS OF LARGE-SIZE TV

TV Market

Image Quality

Cheaper

Larger

Yield Management

More & NewTest Methods

Rigorous QA& Repair

Cost-EffectiveProcess Control

FPD product strategy requires an integrated, multi-function yield management solution

Manufacturing

Complex Design

MinimizeHandling

HugeGlass

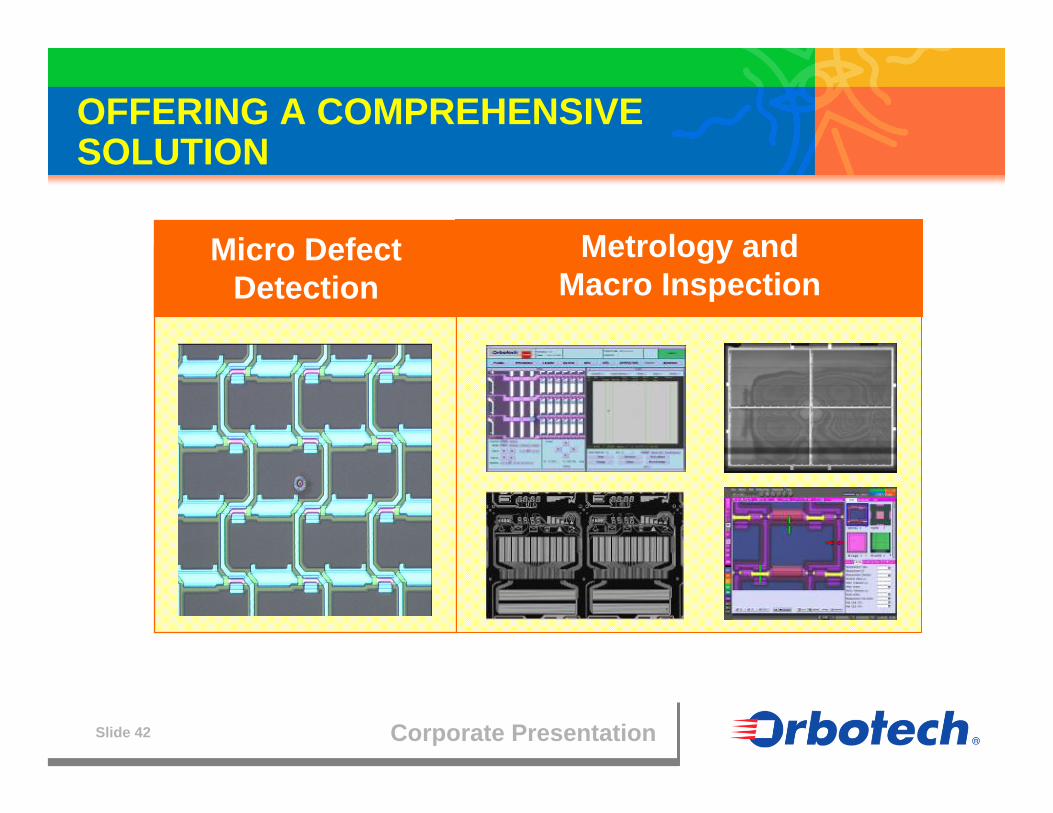

Corporate PresentationSlide 42

Micro Defect Detection

Metrology and Macro Inspection

OFFERING A COMPREHENSIVE SOLUTION

Corporate PresentationSlide 43

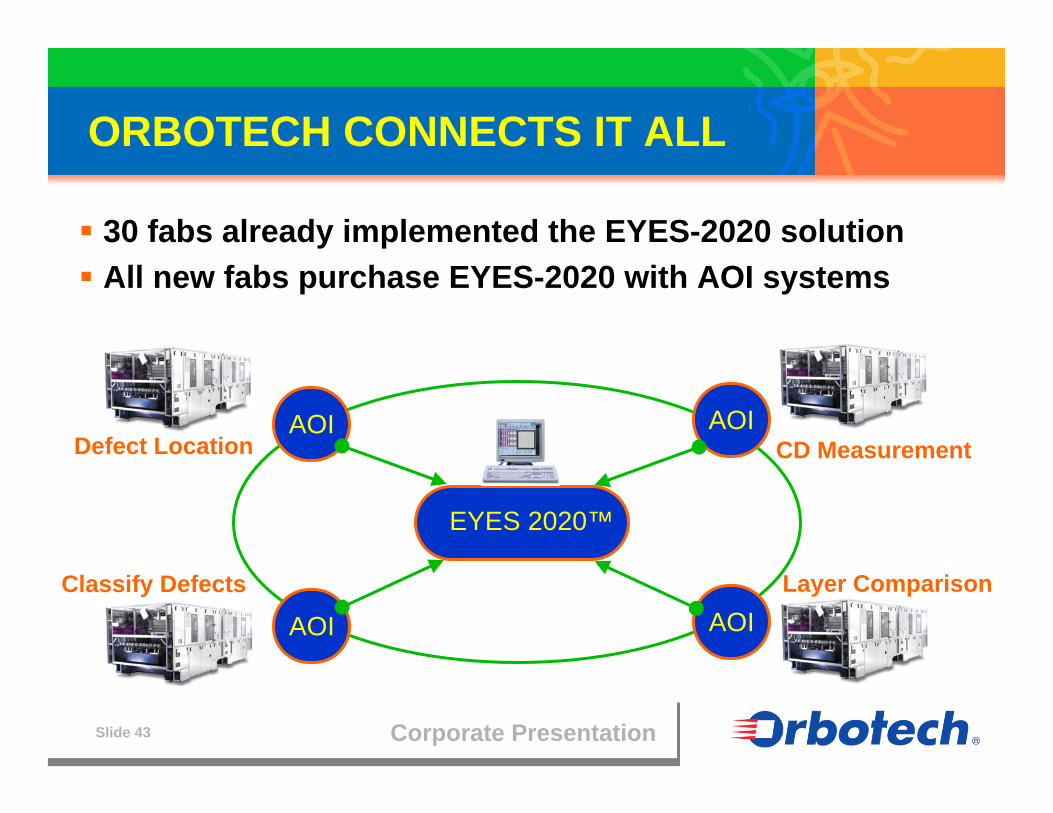

ORBOTECH CONNECTS IT ALL

30 fabs already implemented the EYES-2020 solutionAll new fabs purchase EYES-2020 with AOI systems

EYES 2020™

AOIAOI

AOIAOI

Defect Location

Classify Defects

CD Measurement

Layer Comparison

Corporate PresentationSlide 44

PRODUCTS & SOLUTIONS

Corporate PresentationSlide 45

SAMSUNG AWARD

In appreciation of Orbotech’s dedication and improved performance

Customer Support

Corporate PresentationSlide 47

CUSTOMER SUPPORT

Strategic & necessary for customer relationships

Differentiating factor vs. our competition

20% of our revenue

Source of recurring revenue

Consistent contributor to profitability

On-going presence at customer sites

Corporate PresentationSlide 48

CUSTOMER SUPPORT INFRASTRUCTURE

Over 500 employees in 35 countries

Supporting over5500 AOI systems,650 Plotters, 285 LDI and 4000 CAM stations

5 response centers, 5 customer training centers

Corporate PresentationSlide 49

CUSTOMER SUPPORT SERVICES

Response centersTraining centersRemote accessSoftware upgrades & ECOsSpare parts inventoriesApplication supportConsulting and site auditsPreventive maintenanceLocal satellite officesLocal adaptation

Corporate PresentationSlide 50

CUSTOMER SUPPORT EXAMPLE:RESPONSE CENTERS

Convenient, efficient “hotline”Expert-level staffRemote diagnostic capabilitiesMany calls closed over the phoneDispatched calls for on-site service with diagnostic information

Increases customer satisfaction and our profitability

Medical Imaging

Corporate PresentationSlide 52

Medical Imaging Equipment Market

Synergy with Orbotech’s imaging technology

Large market with continuous high growth

Market paying premiums for differentiating & unique imaging technologies

ENTERING NEW MARKETS

Corporate PresentationSlide 53

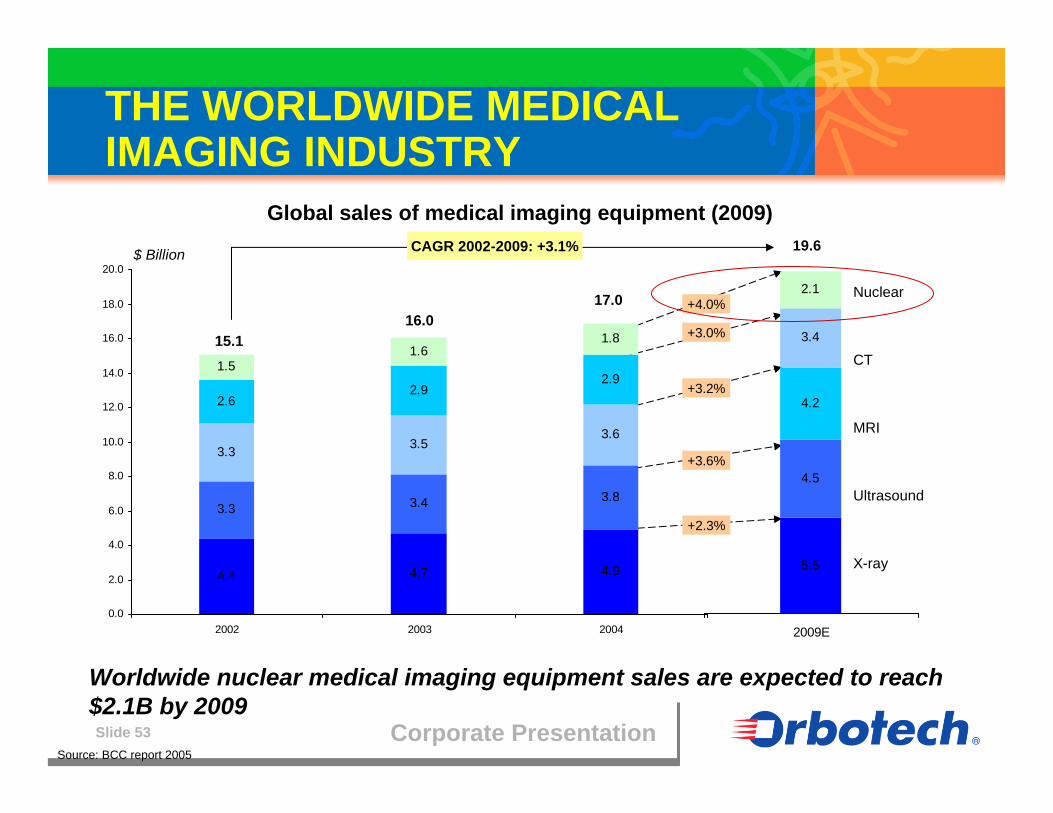

5.5

4.5

4.2

3.4

2.1

2009E

4.4 4.7 4.9

3.3 3.4 3.8

3.3 3.53.6

2.62.9

2.91.5

1.61.8

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

2002 2003 2004

Global sales of medical imaging equipment (2009)

X-ray

Ultrasound

MRI

CT

Nuclear

19.6

+2.3%

+3.6%

+3.2%

+3.0%

+4.0%

Worldwide nuclear medical imaging equipment sales are expected to reach $2.1B by 2009

15.116.0

17.0

$ Billion

Source: BCC report 2005

CAGR 2002-2009: +3.1%

THE WORLDWIDE MEDICAL IMAGING INDUSTRY

Corporate PresentationSlide 54

EXPECTED GLOBAL SALES OF NUCLEAR IMAGING EQUIPMENT (2009)

5.5

4.5

4.2

3.4

2.1

2009E

X-ray

Ultrasound

MRI

CT

Nuclear

19.6

0.8

1.3

Source: BCC report 2005

0.80

0.36

0.12

USA

ROW

Standalone SPECT

SPECT/CT

PET,PET/CT

2.1$ Billion 1.30

The standalone SPECT segment represents $120M from an end-user price standpoint

Corporate PresentationSlide 55

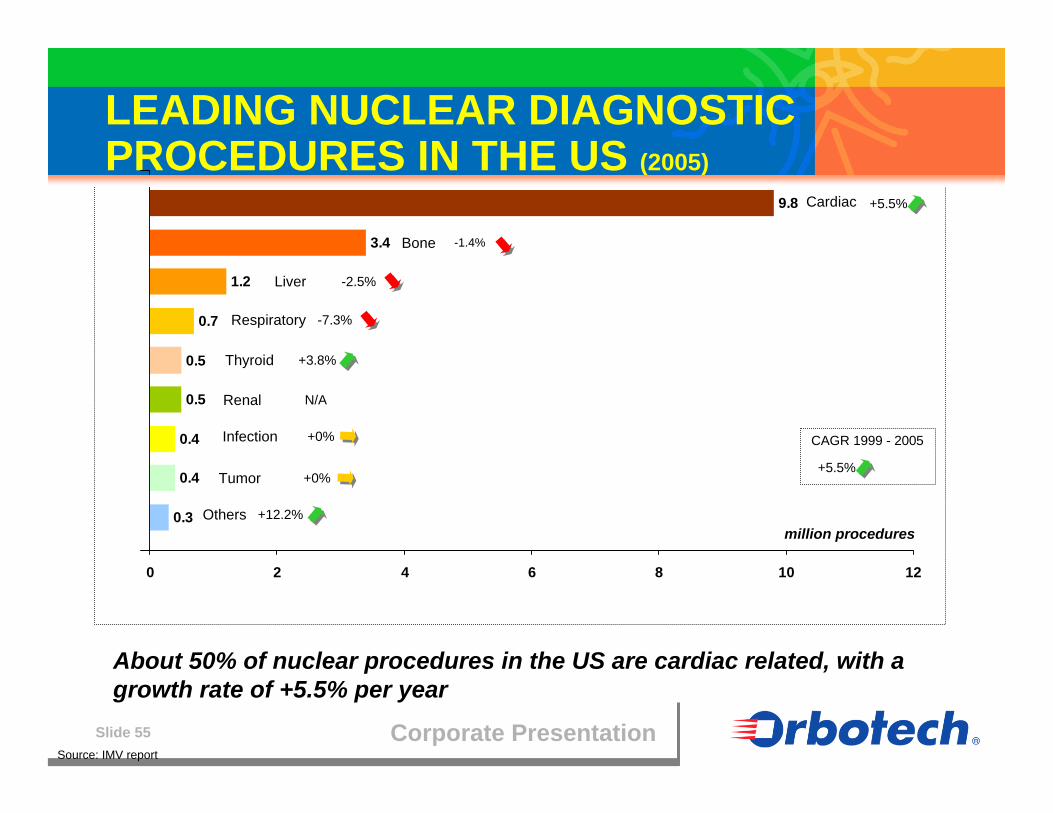

LEADING NUCLEAR DIAGNOSTIC PROCEDURES IN THE US (2005)

0.4

0.5

0.5

0.7

1.2

3.4

9.8

0.3

0.4

0 2 4 6 8 10 12

Source: IMV report

Others

Cardiac

Bone

Liver

Respiratory

Thyroid

Renal

Infection

Tumor

About 50% of nuclear procedures in the US are cardiac related, with a growth rate of +5.5% per year

million procedures+12.2%

-1.4%

+5.5%

-2.5%

-7.3%

+3.8%

N/A

+0%

+0%+5.5%

CAGR 1999 - 2005

Corporate PresentationSlide 56

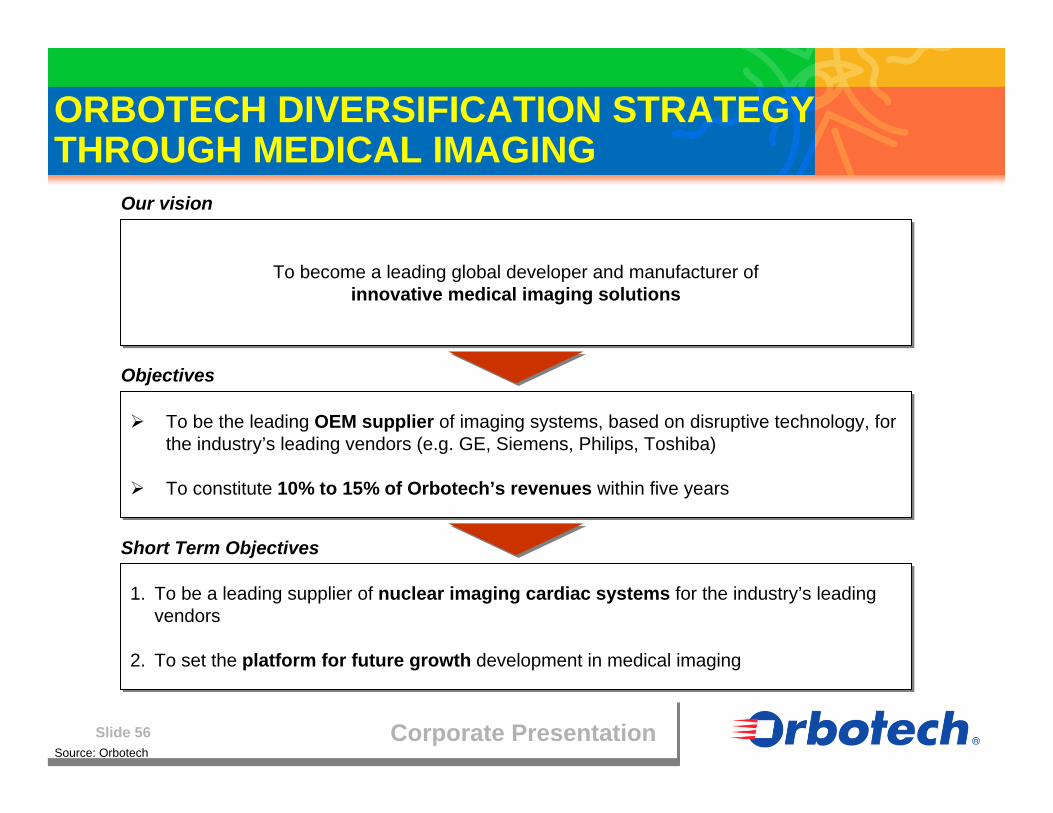

Objectives

Short Term Objectives

To be the leading OEM supplier of imaging systems, based on disruptive technology, for the industry’s leading vendors (e.g. GE, Siemens, Philips, Toshiba)

To constitute 10% to 15% of Orbotech’s revenues within five years

To be the leading OEM supplier of imaging systems, based on disruptive technology, for the industry’s leading vendors (e.g. GE, Siemens, Philips, Toshiba)

To constitute 10% to 15% of Orbotech’s revenues within five years

To become a leading global developer and manufacturer ofinnovative medical imaging solutions

To become a leading global developer and manufacturer ofinnovative medical imaging solutions

1. To be a leading supplier of nuclear imaging cardiac systems for the industry’s leading vendors

2. To set the platform for future growth development in medical imaging

1. To be a leading supplier of nuclear imaging cardiac systems for the industry’s leading vendors

2. To set the platform for future growth development in medical imaging

ORBOTECH DIVERSIFICATION STRATEGY THROUGH MEDICAL IMAGING

Our vision

Source: Orbotech

Corporate PresentationSlide 57

Founded in 1987 by Kai Lange, a prominent figure in the medical imaging industry

Employees: 42 (July 2007)

Headquarters in Hoersholm (Copenhagen), Denmark

Previously owned by: Axcel, Denmark’s largest private equity company

Estimated revenues in 2007: ~$30M

NUCLEAR MEDICAL IMAGING: DANISH DIAGNOSTIC DEVELOPMENT A/S (DDD)

DDD is the leading manufacturer of dedicated imaging equipment for the Nuclear Cardiology segment

Corporate PresentationSlide 58

DDD - BUSINESS DESCRIPTION

DDD mainly sells dedicated medical imaging equipment for nuclear cardiology (~$100M market)

DDD is the leading OEM supplier of dedicated nuclear medicine gamma camera in the US

DDD has the largest installed base (IB) of cardiac cameras worldwide (1,600 units out of 2,400 total IB)

DDD is a supply partner to two out of three major OEMs worldwide (Philips and Siemens)

DDD has a pipeline of new products expected in 2008/09, offering long-term growth potential

Source: Orbotech

Corporate PresentationSlide 59

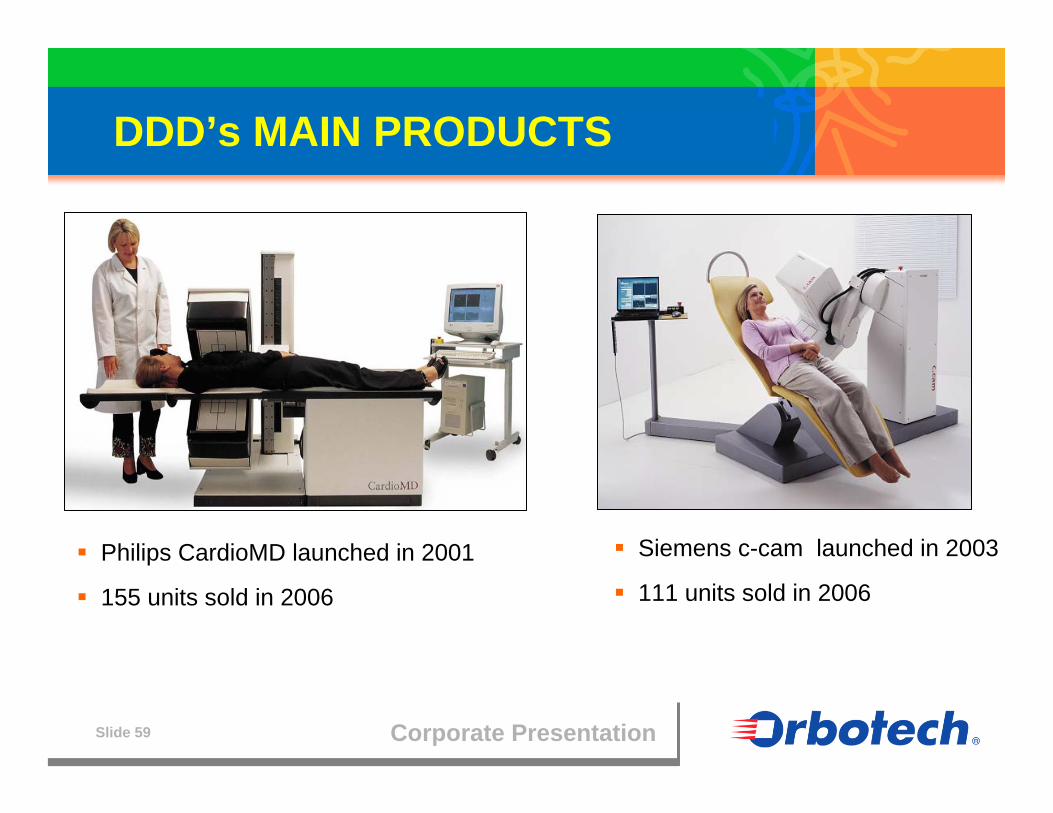

DDD’s MAIN PRODUCTS

Philips CardioMD launched in 2001

155 units sold in 2006

Siemens c-cam launched in 2003

111 units sold in 2006

Corporate PresentationSlide 60

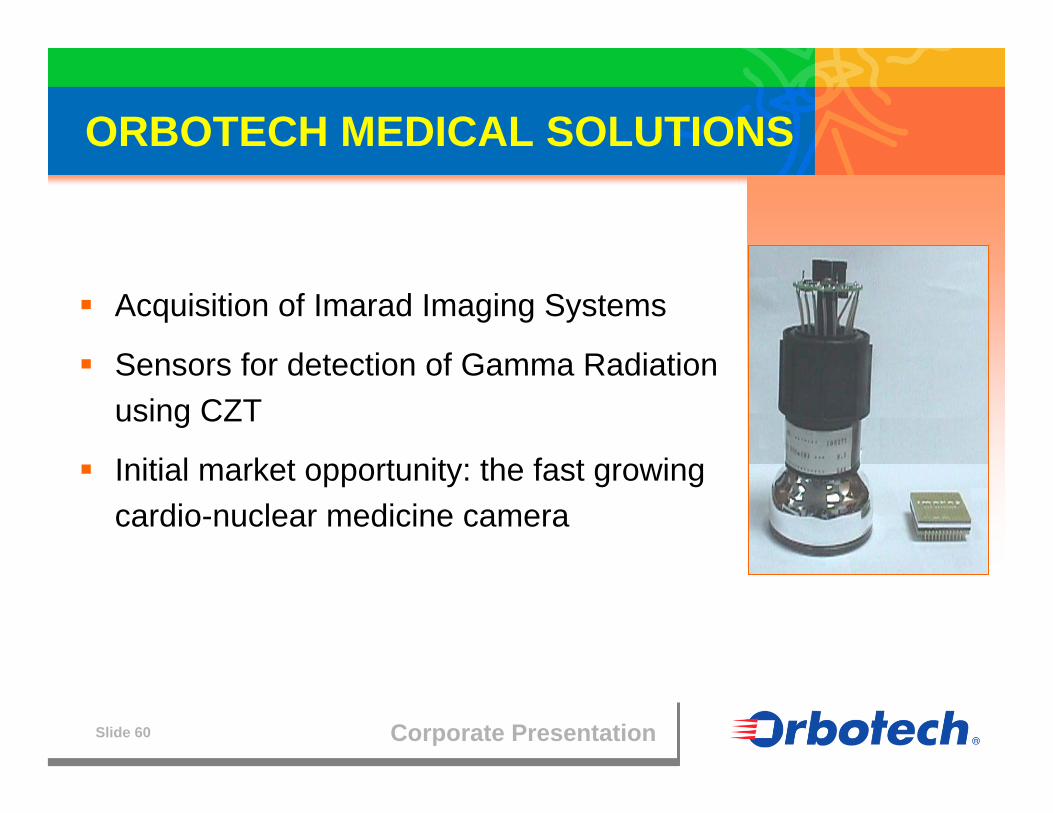

ORBOTECH MEDICAL SOLUTIONS

Acquisition of Imarad Imaging Systems

Sensors for detection of Gamma Radiation using CZT

Initial market opportunity: the fast growing cardio-nuclear medicine camera

Orbograph

Corporate PresentationSlide 62

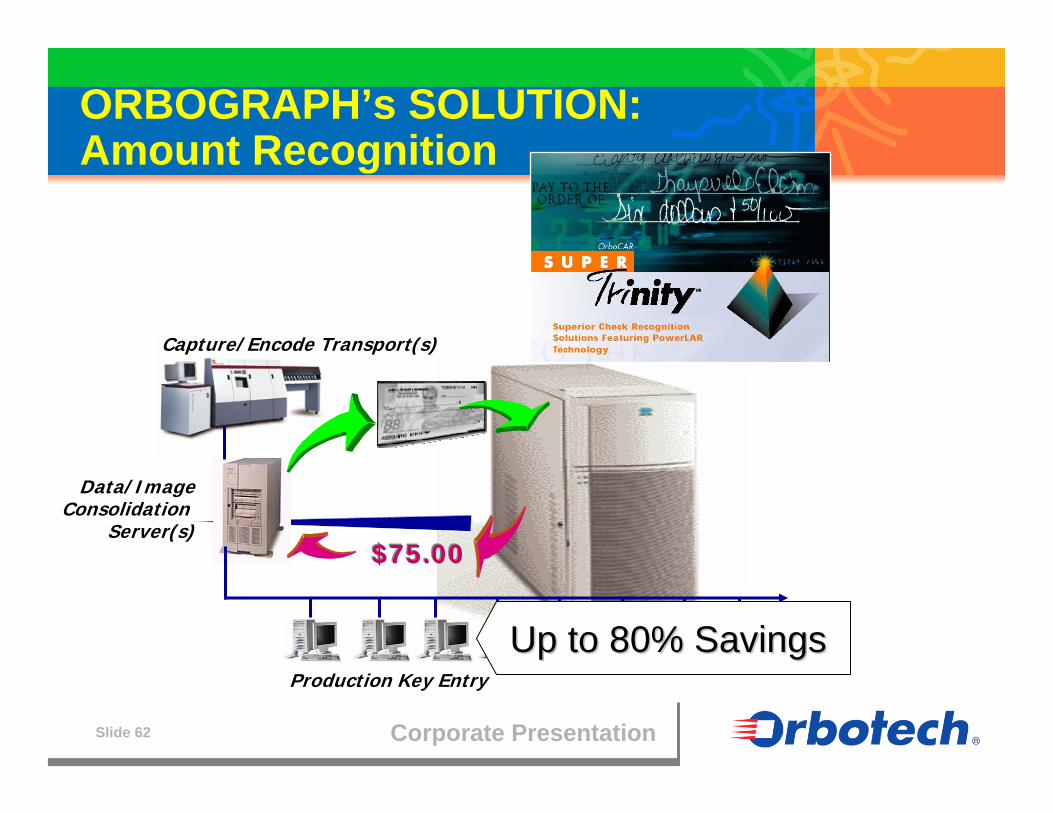

ORBOGRAPH’s SOLUTION: Amount Recognition

Data/ImageConsolidation

Server(s)$75.00$75.00

Production Key Entry

Up to 80% SavingsUp to 80% Savings

Capture/Encode Transport(s)

Corporate PresentationSlide 63

RECO PRODUCT LINE

Amount recognition for checks (Orbocar)

Field recognition (payer, payee, MICR)

Image quality and field usability (IQUA)

Image-based fraud detection

PNV

Forgery

Counterfeit

Data mining for marketing

Corporate PresentationSlide 64

THE KEY-PAY® CONCEPT

Highly-skilled,performance-driven

workforce

Check Image

Document Image(Unstructured, structured

semi-structured)

Audio File

?Image, video, etc.

Digital Objector Source

Secure InternetConnection

Key-PayHubR-BOX

Remote Data Completion

Personnel

Web-based, DistributedHuman Completion providers

AutomatedConversion App.

Corporate PresentationSlide 65

KEY-PAY® PRODUCT LINE

Products:

APEX for checks processing

CONVENE for forms processing

Sales model:

Recurring service revenues (by click charge)

Offer turnkey solution or Infrastructure only

Financials

Corporate PresentationSlide 67

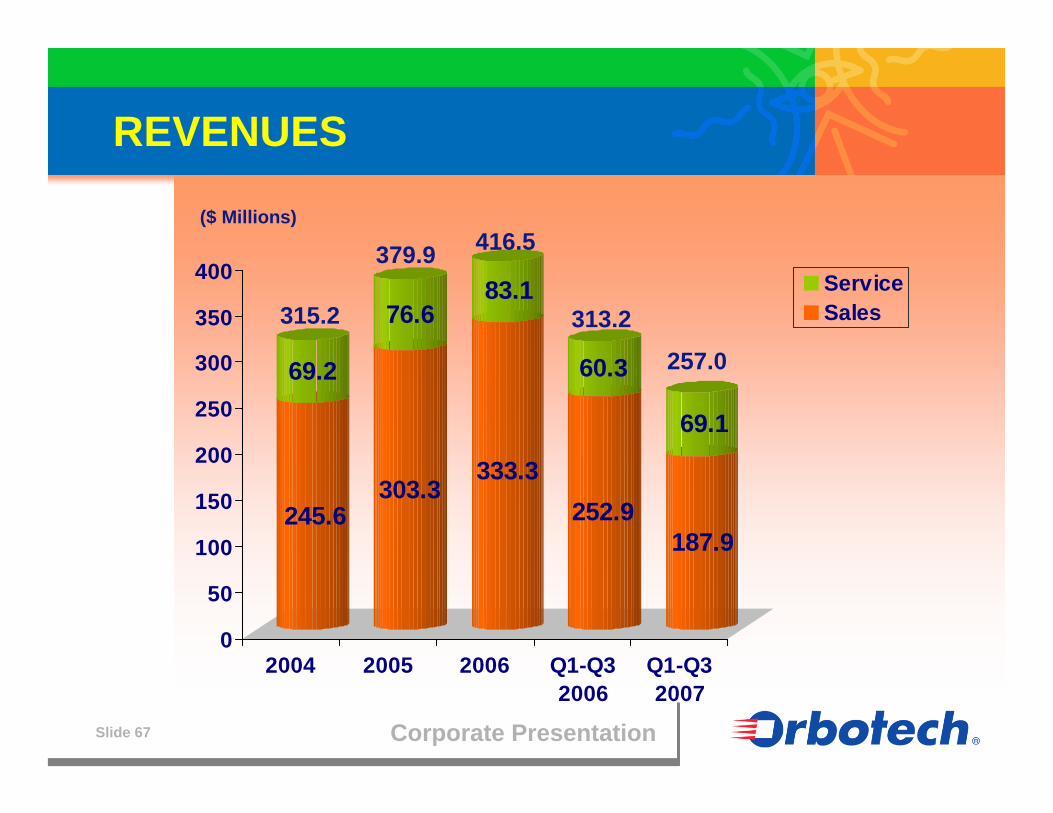

REVENUES

($ Millions)

245.6

69.2

303.3

76.6

333.3

83.1

252.9

60.3

187.9

69.1

0

50

100

150

200

250

300

350

400

2004 2005 2006 Q1-Q32006

Q1-Q32007

ServiceSales315.2

379.9 416.5

313.2

257.0

Corporate PresentationSlide 68

REVENUES BY QUARTER

($ Millions)

100.5101.4

86.1 89.3

104.9

88.693.7

106.9

82.3

96.4103.3

0

20

40

60

80

100

120

Q1 Q2 Q3 Q4

200520062007

Corporate PresentationSlide 69

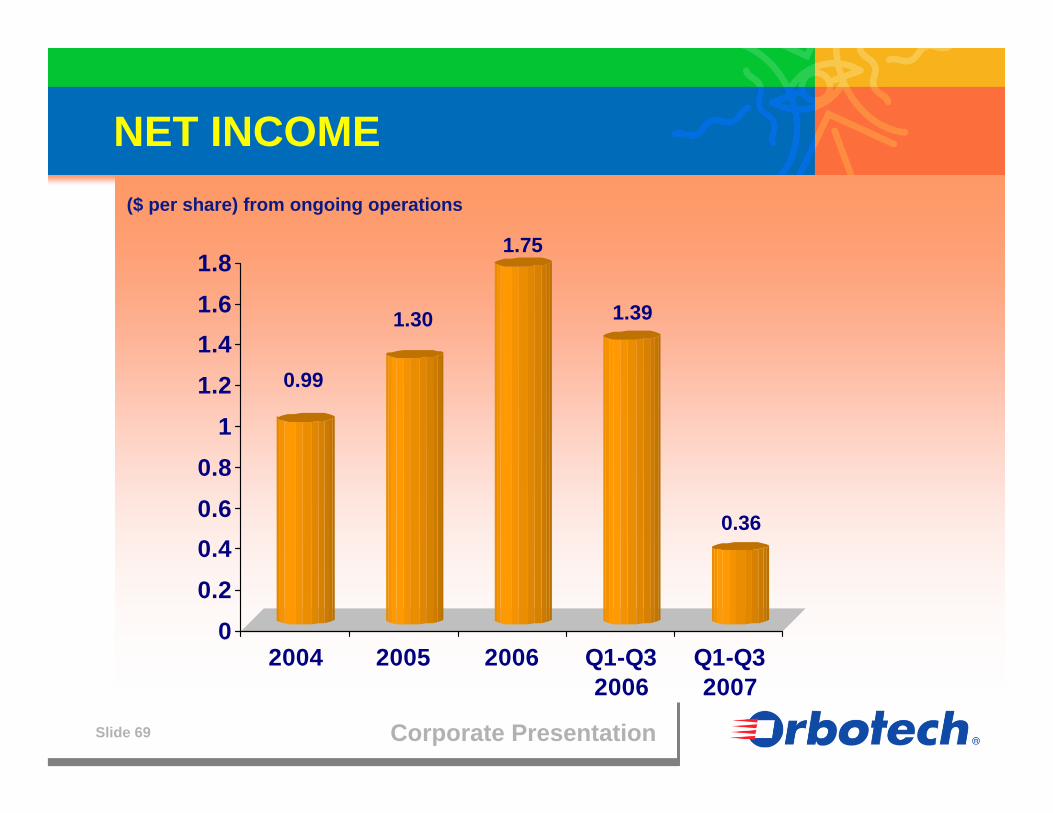

NET INCOME

0.99

1.30

1.75

1.39

0.36

00.20.40.60.8

11.21.41.61.8

2004 2005 2006 Q1-Q32006

Q1-Q32007

($ per share) from ongoing operations

Corporate PresentationSlide 70

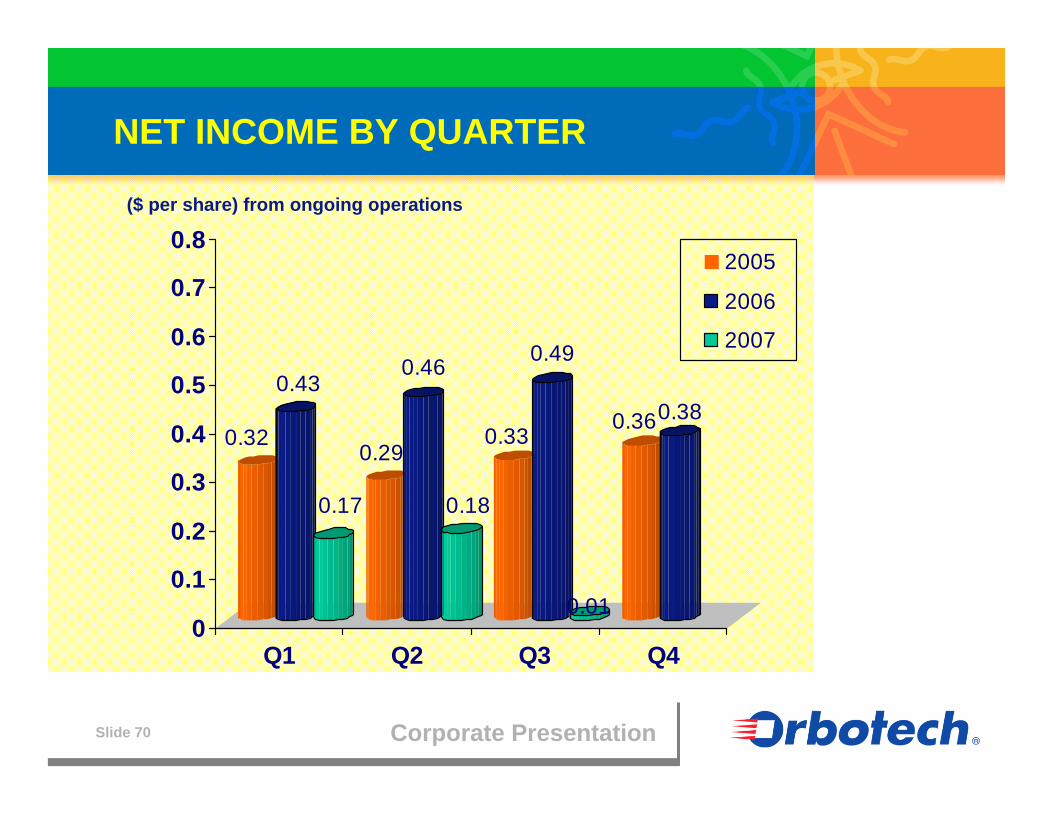

NET INCOME BY QUARTER

($ per share) from ongoing operations

0.32

0.43

0.17

0.29

0.46

0.18

0.33

0.49

0.01

0.360.38

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Q1 Q2 Q3 Q4

2005

2006

2007

Corporate PresentationSlide 71

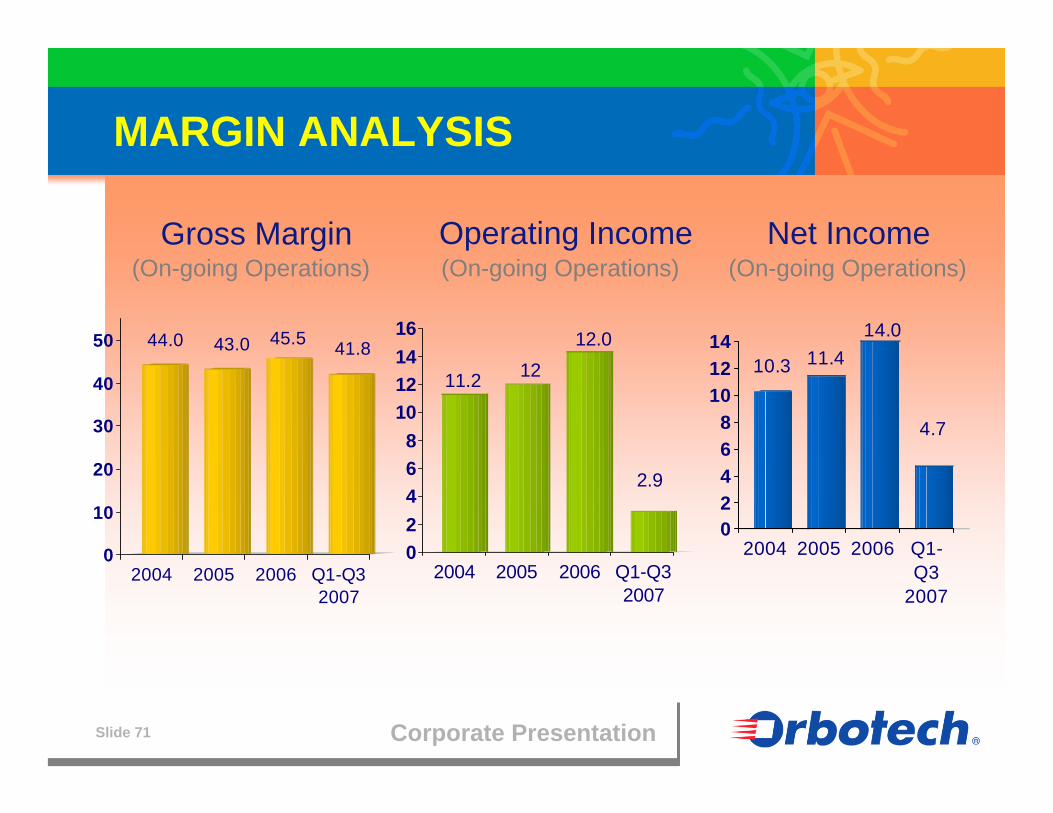

MARGIN ANALYSIS

44.0 43.0 45.5 41.8

0

10

20

30

40

50

2004 2005 2006 Q1-Q32007

11.2 1212.0

2.9

02468

10121416

2004 2005 2006 Q1-Q32007

10.3 11.414.0

4.7

02468

101214

2004 2005 2006 Q1-Q3

2007

Gross Margin(On-going Operations)

Operating Income(On-going Operations) (On-going Operations)

Net Income

Corporate PresentationSlide 72

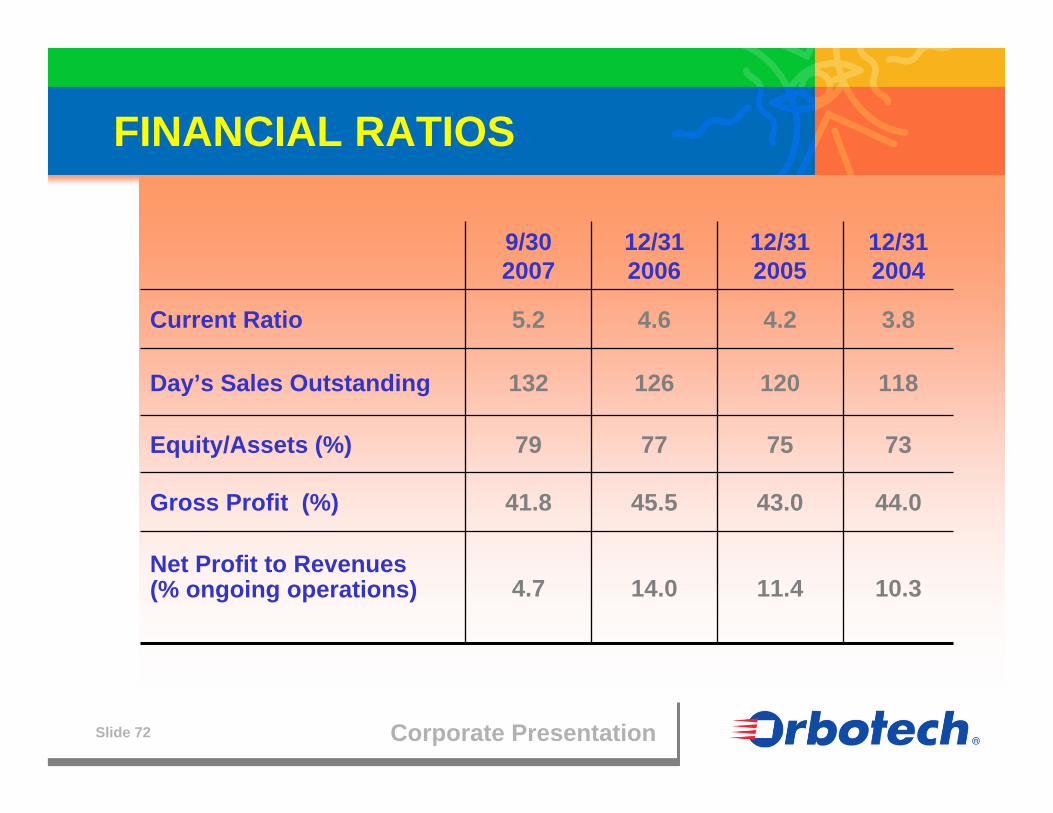

14.0

45.5

77

126

4.6

12/312006

10.3

44.0

73

118

3.8

12/312004

11.4

43.0

75

120

4.2

12/31 2005

4.7Net Profit to Revenues(% ongoing operations)

41.8Gross Profit (%)

79Equity/Assets (%)

132Day’s Sales Outstanding

5.2Current Ratio

9/302007

FINANCIAL RATIOS

Corporate PresentationSlide 73