slides developed by: pamela l. hall, western washington university risk and return chapter 8

TRANSCRIPT

Slides developed by:Pamela L. Hall, Western Washington University

Risk and Return

Chapter 8

2

Why Study Risk and Return?

Returns to equity investments (stock) have historically been much higher than the return to debt investments Equity returns averaged more than 10% while debt

returns average between 3% and 4%• Inflation also averaged about 3% during the same time

period

Returns on equity investments are much more volatile than the returns on debt instruments in the short-run

3

Why Study Risk and Return?

Since equity earns a much higher return but with higher risk, it would be nice if we could invest and earn a high return but reduce the risk associated with such investments Investing in portfolios of securities can help manage

risk• A portfolio is a collection of financial assets by investors

We wish to capture the high average returns of equity investing while limiting the associated risk as much as possible

4

The General Relationship Between Risk and Return Risk in finance is defined as the probability of

losing some or all of the money invested in a deal Generally investments that offer higher returns

involve higher risks Suppose you could invest in a stock that would

either return you 15% or a loss of everything (-100%) Also, suppose the chance of losing everything is 1%

and the chance of earning 15% is 99% The risk associated with this investment is the 1%

chance of losing everything

5

The General Relationship Between Risk and Return Investors more or less expect to receive a

positive return but they realize that there is risk associated with these investments and the chance that they can lose their money

Stocks offering a higher likely return also have higher probabilities of total loss

It is difficult to determine how much risk is associated with a given level of return Need to define risk in a measurable way

• The definition has to include all the probabilities of loss Have to relate that measurement to return

6

Portfolio Theory—Modern Thinking about Risk and Return Portfolio theory defines investment risk in

a measurable way and relates it to the expected level of return from an investment

Has had major impact on practical investing activities

7

The Return on an Investment

The rate of return allows an investment's return to be compared with other investments

One-Year Investments The return on a debt investment is

• K = interest paid loan amount• A return is what the investor receives divided by what is

invested

The return on a stock investment is • K = D1 + (P1 – P0) P0

8

Returns, Expected and Required The expected return on a stock is the

return investors feel is most likely to occur based on currently available information Anticipated return based on the dividends

expected as well as the future expected price No rational person makes any investment

without some expectation of return

9

Returns, Expected and Required The required return on a stock is the minimum

rate at which investors will purchase or hold a stock based on their perceptions of its risk People will only invest in an asset if they believe the

expected return is at least equal to the required return• Different people have different levels of both expected and

required return• Significant investment in a stock occurs only if the expected

return exceeds the required return for a substantial number of investors

10

Risk—A Preliminary Definition

A preliminary definition of investment risk is the probability that return will be less than expected This definition includes both positive and negative returns that

are lower than expected

Feelings About Risk Most people have negative feelings about bearing risk Risk averse investors prefer lower risk when expected returns

are equal Most people see a trade-off between risk and return However risk isn't to be avoided, but higher risk investments

must offer a higher expect return to encourage investment

11

Portfolio Theory

Review of the Concept of a Random Variable In statistics a random variable is the outcome

of a chance process and has a probability distribution

Discrete variables can take only specific variables

Continuous variables can take any value within a specified range

12

Review of the Concept of a Random Variable The Mean or Expected Value

The most likely outcome for the random variable

For symmetrical probability distributions the mean is the center of the distribution

Statistically it is the weighted average of all possible outcomes

n

i ii=1

X = XP X

13

Portfolio Theory

Variance and Standard Deviation Variability relates to how far a typical observation of

the variable is likely to deviate from the mean• There's is a great deal of difference in variability around the

mean for different distributions• Telephone poles don't vary much in height from pole to pole—

actual pole heights are closely clustered around the mean

• Office buildings do vary a great deal in terms of height—widely dispersed around the mean

• The standard deviation gives an indication of how far from the mean a typical observation is likely to fall

14

Portfolio Theory

Variance and Standard Deviation Variance Formula

n 22

x i ii=1

Var X X X P X

n 2

X x i ii=1

SD X X P X

• Variance is the average squared deviation from the mean

Standard deviation formula

15

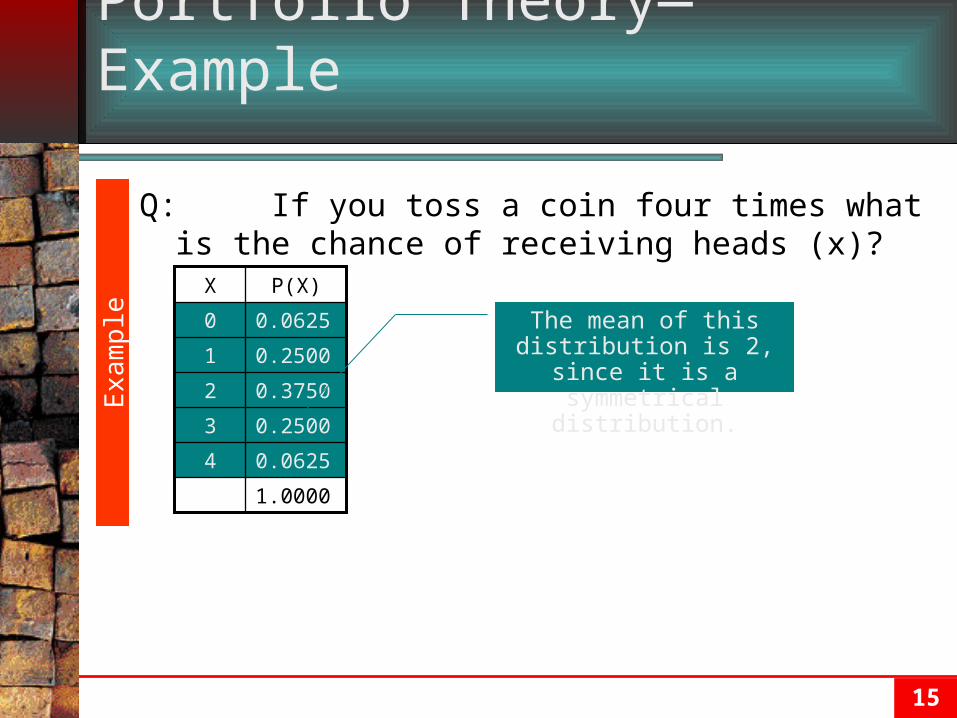

Portfolio Theory—Example

1.0000

0.06254

0.25003

0.37502

0.25001

0.06250

P(X)X

The mean of this distribution is 2, since it is a symmetrical distribution.

Exa

mpl

e

Q:If you toss a coin four times what is the chance of receiving heads (x)?

16

Portfolio Theory—Example

1.00SD X =

1.00Var X =

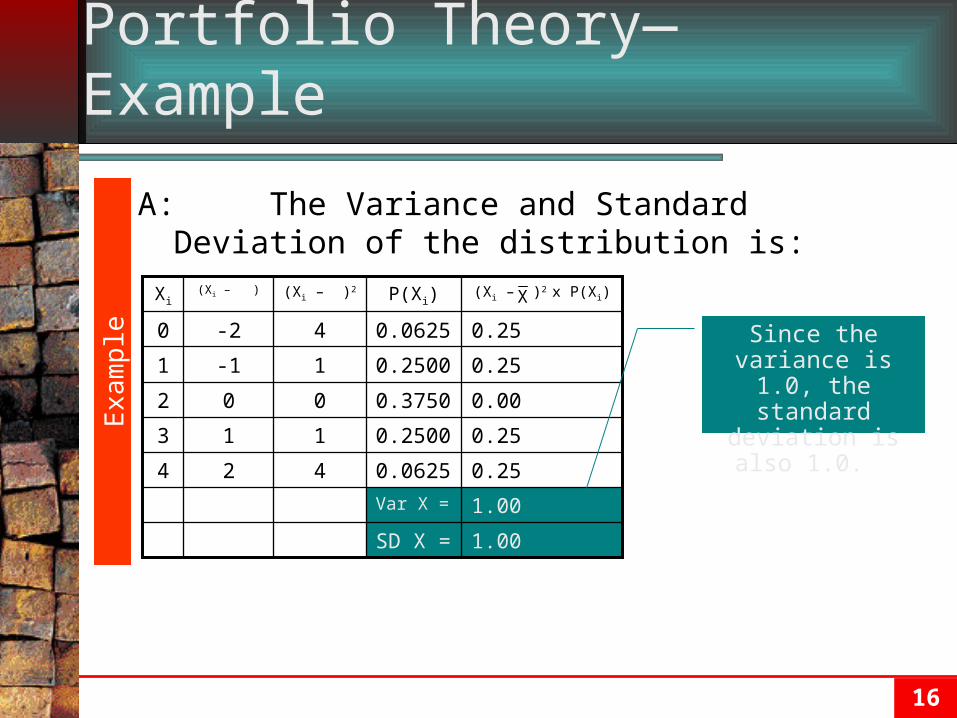

0.250.0625424

0.250.2500113

0.000.3750002

0.250.25001-11

0.250.06254-20

(Xi – )2 x P(Xi)P(Xi)(Xi – )2(Xi – )Xi X

Since the variance is 1.0, the

standard deviation is also 1.0. E

xam

ple

A: The Variance and Standard Deviation of the distribution is:

17

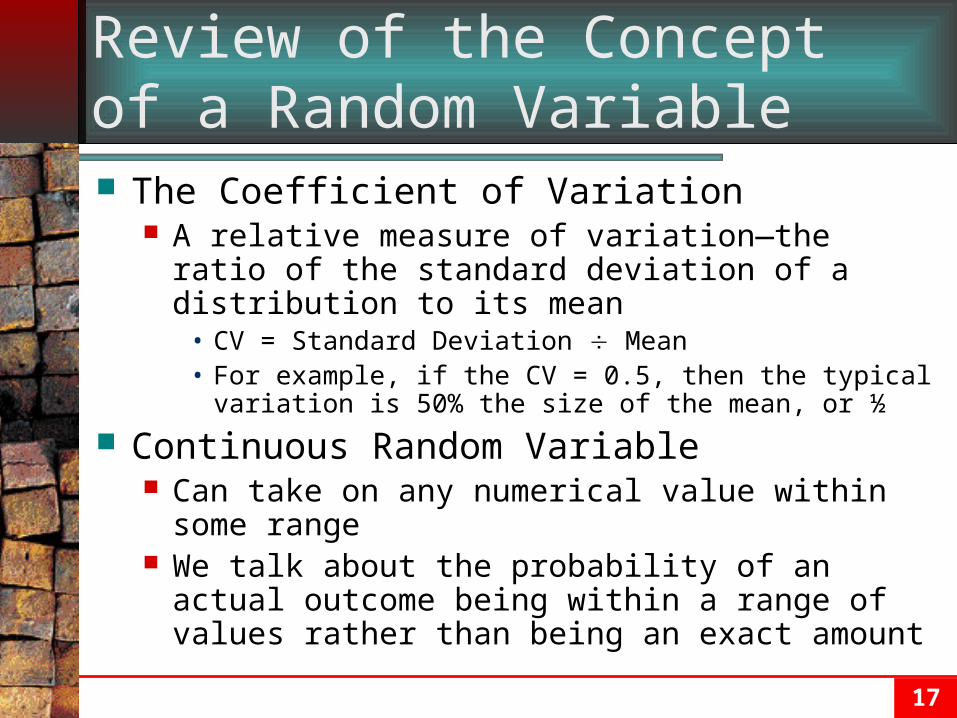

Review of the Concept of a Random Variable The Coefficient of Variation

A relative measure of variation—the ratio of the standard deviation of a distribution to its mean

• CV = Standard Deviation Mean• For example, if the CV = 0.5, then the typical variation is

50% the size of the mean, or ½

Continuous Random Variable Can take on any numerical value within some range We talk about the probability of an actual outcome

being within a range of values rather than being an exact amount

18

The Return on a Stock Investment as a Random Variable In financial theory, the return on a stock investment is

considered a random variable Return is influenced by the future price of the stock and the

expected dividends• There is an element of uncertainty in both of these variables

Return is a continuous random variable with a low value of -100% but no limit to the high value

The mean of the distribution of returns is the stock's expected return

The variance and standard deviation show how likely it is that an actual return will be some distance from the expected value Actual return in a distribution with a large variance is likely to be

different from the mean

19

Figure 8.4: Probability Distributions With Large and Small Variances

20

Risk Redefined as Variability

In financial theory risk is defined as variability in return

A risky stock has a high probability of earning a return that significantly differs from the mean of the distribution While a low-risk stock is more like to earn a return

similar to the expected return

In practical terms risk is the probability that return will be less than expected

21

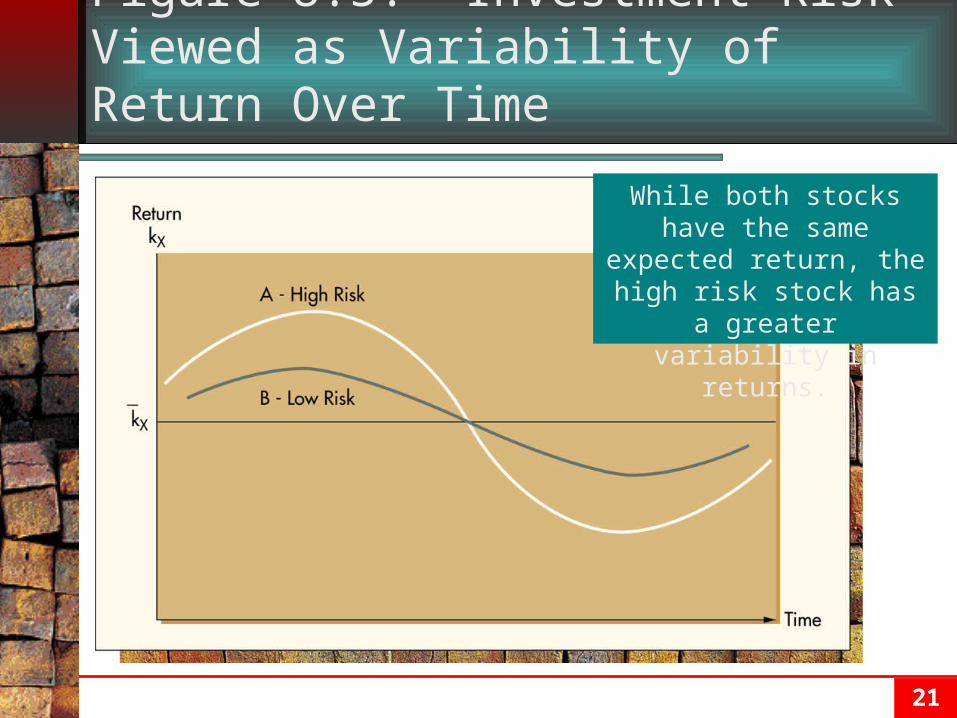

Figure 8.5: Investment Risk Viewed as Variability of Return Over Time

While both stocks have the same expected return, the

high risk stock has a greater variability in

returns.

22

Risk Aversion

Risk aversion means investors prefer lower risk when expected returns are equal

When expected returns are not equal the choice of investment depends on the investor's tolerance for risk

23

Figure 8.6: Risk Aversion

24

Portfolio Theory—Example

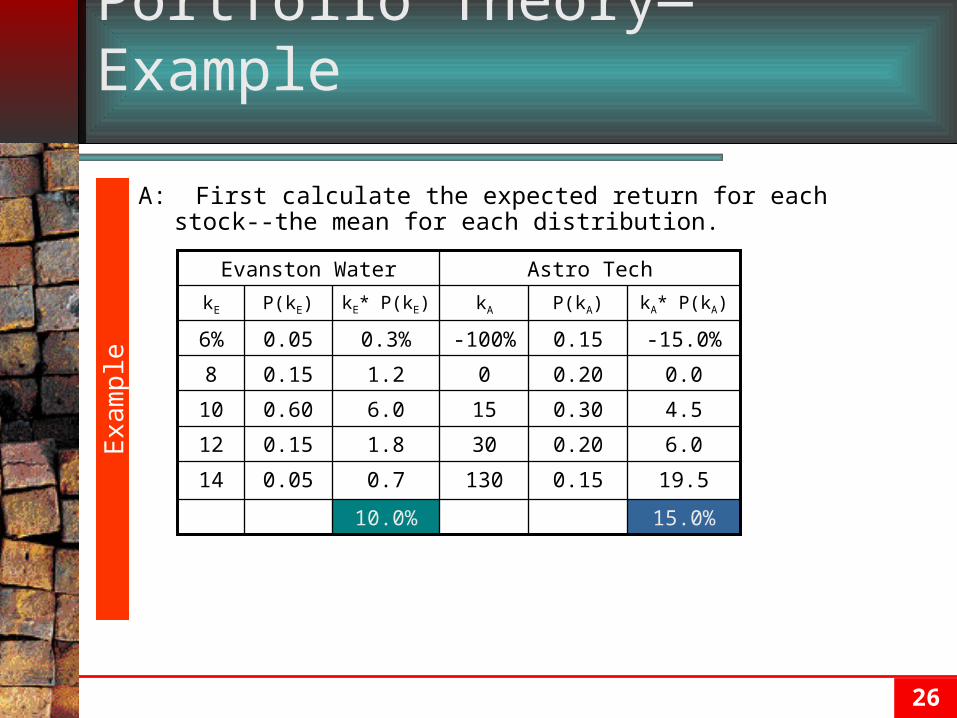

Q: Harold MacGregor is considering buying stocks for the first time and is looking for a single company in which he'll make a major investment. He's narrowed his search to two firms, Evanston Water Inc. (a public utility) and Astro Tech Corp. (a new high-tech company).

Public utilities are low-risk stocks because they are regulated monopolies

High tech firms are high-risk because new technical ideas can succeed tremendously, fail completely or end up in-between

Harold has studied the history and prospects of both firms and their industries, and with the help of his broker has made a discrete estimate of the probability distribution of returns for each stock as follows:

Exa

mpl

e

25

Portfolio Theory—Example

Evaluate Harold's options in terms of statistical concepts of risk and return.

Exa

mpl

e

0.151300.0514

0.20300.1512

0.30150.6010

0.2000.158

0.15-100%0.056%

P(kA)kAP(kE)kE

Astro

Tech

Evanston Water

26

Portfolio Theory—Example

A: First calculate the expected return for each stock--the mean for each distribution.

Exa

mpl

e

15.0%10.0%

130

30

15

0

-100%

kA

0.7

1.8

6.0

1.2

0.3%

kE* P(kE)

19.50.150.0514

6.00.200.1512

4.50.300.6010

0.00.200.158

-15.0%0.150.056%

kA* P(kA)P(kA)P(kE)kE

Astro TechEvanston Water

27

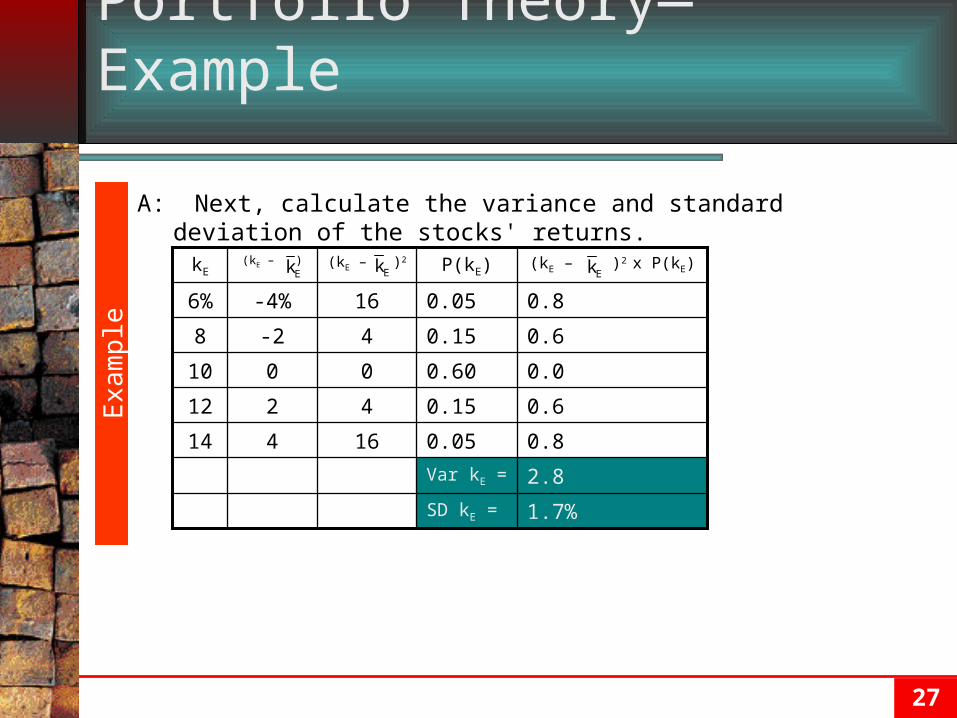

Portfolio Theory—ExampleE

xam

ple

1.7%SD kE =

2.8Var kE =

0.80.0516414

0.60.154212

0.00.600010

0.60.154-28

0.80.0516-4%6%

(kE – )2 x P(kE)P(kE)(kE – )2(kE – )kE Ek Ek Ek

A: Next, calculate the variance and standard deviation of the stocks' returns.

28

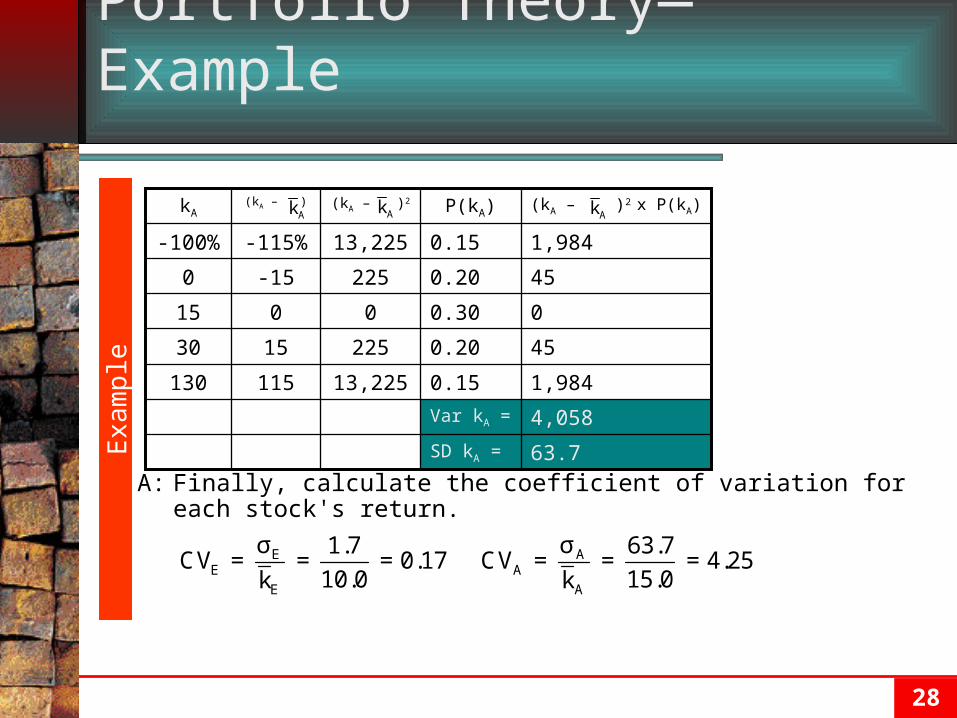

Portfolio Theory—ExampleE

xam

ple

63.7SD kA =

4,058Var kA =

1,9840.1513,225115130

450.202251530

00.300015

450.20225-150

1,9840.1513,225-115%-100%

(kA – )2 x P(kA)P(kA)(kA – )2(kA – )kA Ak Ak Ak

E AE A

E A

σ σ1.7 63.7CV = = = 0.17 CV = = = 4.25

10.0 15.0k k

A: Finally, calculate the coefficient of variation for each stock's return.

29

Portfolio Theory—Example

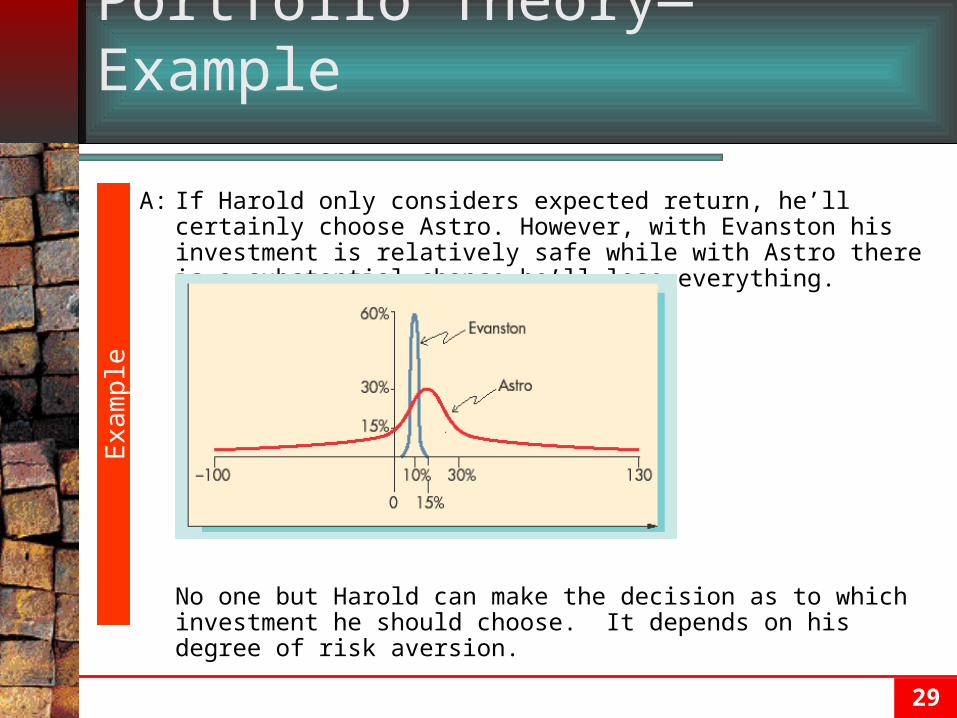

A: If Harold only considers expected return, he’ll certainly choose Astro. However, with Evanston his investment is relatively safe while with Astro there is a substantial chance he’ll lose everything.

No one but Harold can make the decision as to which investment he should choose. It depends on his degree of risk aversion.

Exa

mpl

e

30

Decomposing Risk—Systematic (Market) and Unsystematic (Business-Specific) Risk

Fundamental truth of the investment world The returns on securities tend to move up and down

together• Not exactly together or proportionately

Events and Conditions Causing Movement in Returns Some things influence all stocks (market risk)

• Political news, inflation, interest rates, war, etc. Some things influence only particular firms (business-

specific risk)• Earnings reports, unexpected death of key executive, etc.

Some things affect all companies within an industry• A labor dispute, shortage of a raw material

31

Decomposing Risk—Systematic (Market) and Unsystematic (Business-Specific) Risk

Comparison of IBM, Boeing and the S&P500

020406080

100120140

10/1

0/20

00

11/1

0/20

00

12/1

0/20

00

1/10

/200

1

2/10

/200

1

3/10

/200

1

4/10

/200

1

5/10

/200

1

6/10

/200

1

7/10

/200

1

8/10

/200

1

9/10

/200

1

10/1

0/20

01

Date

Sto

ck

Pri

ce

02004006008001000120014001600

IBM Boeing S&P500

Ind

ex V

alu

e

Market reopens after World Trade

Center collapses.

32

Decomposing Risk—Systematic (Market) and Unsystematic (Business-Specific) Risk

Movement in Return as Risk The total movement in a stock's return is the total risk

inherent in the stock

Separating Movement/Risk into Two Parts A stock's risk can be separated into systematic or

market risk and unsystematic or business-specific risk

33

Portfolios

A portfolio is an investor's total stock holding Risk and Return for a Portfolio

Each stock in a portfolio has its own expected return and its own risk

Portfolios have their own risks and returns• The return on a portfolio is a weighted average of the returns

of the individual stocks in the portfolio• The risk is the variance or standard deviation of the

probability distribution of the portfolio's return• Not the same as the weighted average of the standard

deviations or variances of the individual stocks within the portfolio

34

Portfolios

The Goal of the Investor/Portfolio Owner Goal of investors: to capture the high

average returns of equities while avoiding as much risk as possible

• Generally done by constructing diversified portfolios to minimize portfolio risk for a given return

Investors are concerned with how stocks impact portfolio performance, not with the stocks' stand-alone characteristics

35

Diversification—How Portfolio Risk Is Affected When Stocks Are Added

Diversification means adding different (diverse) stocks to a portfolio Can reduce (but not eliminate) risk in a portfolio

Business-Specific Risk and Diversification Business-specific risk is a series of essentially

random events that push the returns of individual stocks up or down

• Their effects simply cancel when added together over a substantial number of stocks

• Is essentially random and can be diversified away• For this to work, the stocks within the portfolio must be from

fundamentally different industries

36

Diversification—How Portfolio Risk Is Affected When Stocks Are Added Systematic (Market) Risk and Diversification

If the returns of all stocks move up and down more or less together, it's not possible to reduce risk completely

• Systematic risk can be reduced but never entirely eliminated

The Portfolio If we have a portfolio that is as diversified as the market, its

return will move in tandem with the market The Impact on Portfolio Risk of Adding New Stocks

If we add a stock to the portfolio which has returns perfectly positively correlated with the portfolio, it will generally add risk to the diversified portfolio

If we add a stock that is perfectly negatively correlated with the portfolio, it will decrease the risk of the portfolio

37

Diversification—How Portfolio Risk Is Affected When Stocks Are Added The Risk of the New Additions By Themselves and in

Portfolios Stocks with equal stand-alone risk can have opposite risk

impacts on a portfolio because of the timing of the variation in their returns

A stock's risk in a portfolio sense is its market risk Choosing Stocks to Diversify for Market Risk

How do we diversify to reduce market risk in a portfolio• Theoretically it's simple: just add stocks that move counter

cyclically with the market• Unfortunately it's difficult to find stocks that move in that direction• However numerous stocks exist that have returns that are less than

positively correlated with the market• Adding these stocks to the portfolio will generally reduce risk

somewhat, but will not eliminate it

38

Diversification—How Portfolio Risk Is Affected When Stocks Are Added

The Importance of Market Risk Modern portfolio theory is based on the

assumption that investors focus on portfolios rather than on individual stocks

• How stocks affect portfolios depends only on market risk

For the small investor with a limited portfolio, these concepts do not apply

39

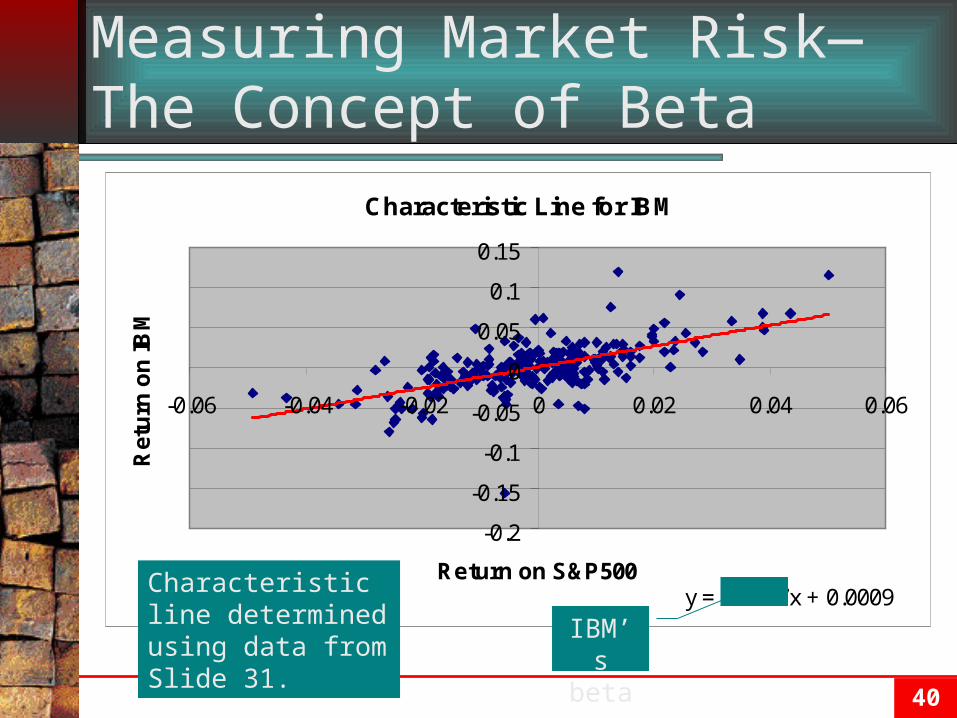

Measuring Market Risk—The Concept of Beta Market risk is a crucial concept in investing, so we need

a way to measure it for individual stocks A stock's beta measures its market risk

It measures the variation of a stock's return which accompanies the market's variation in return

Developing Beta Beta is developed by determining the historical relationship

between a stock's return and the return on a market index, such as the S&P500

• The stock's characteristic line reflects the average relationship between its return and the market

• Beta is the slope of the characteristic line

Projecting Returns with Beta Knowing a stock's beta enables us to estimate changes in its

return given changes in the market's return

40

Measuring Market Risk—The Concept of Beta

Characteristic Line for IBM

y = 1.3037x + 0.0009

-0.2

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

-0.06 -0.04 -0.02 0 0.02 0.04 0.06

Return on S&P500

Ret

urn

on

IBM

Characteristic line determined using data from Slide 31.

IBM’s beta

41

Measuring Market Risk—The Concept of Beta

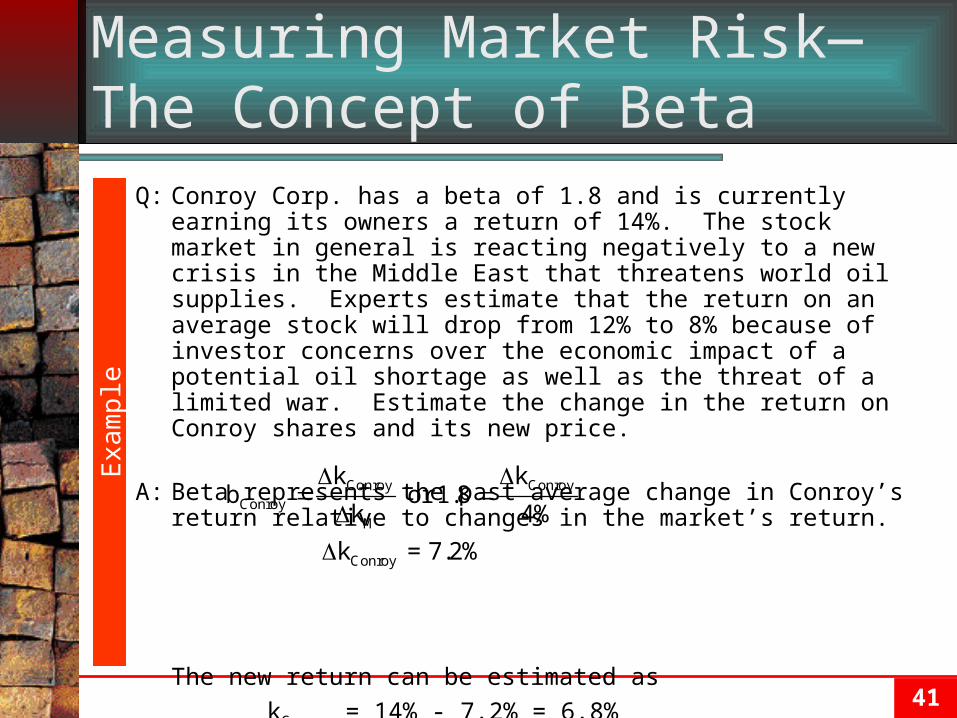

Q: Conroy Corp. has a beta of 1.8 and is currently earning its owners a return of 14%. The stock market in general is reacting negatively to a new crisis in the Middle East that threatens world oil supplies. Experts estimate that the return on an average stock will drop from 12% to 8% because of investor concerns over the economic impact of a potential oil shortage as well as the threat of a limited war. Estimate the change in the return on Conroy shares and its new price.

A: Beta represents the past average change in Conroy’s return relative to changes in the market’s return.

The new return can be estimated as

kConroy = 14% - 7.2% = 6.8%

Exa

mpl

e

Conroy ConroyConroy

M

Conroy

k kb or 1.8

k 4%

k = 7.2%

42

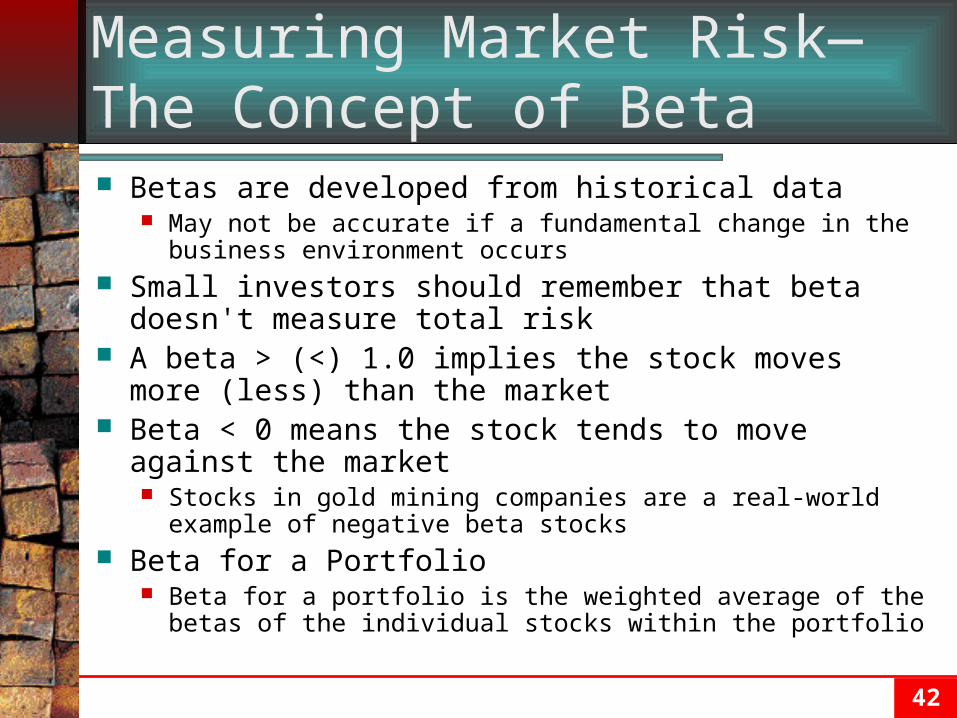

Measuring Market Risk—The Concept of Beta Betas are developed from historical data

May not be accurate if a fundamental change in the business environment occurs

Small investors should remember that beta doesn't measure total risk

A beta > (<) 1.0 implies the stock moves more (less) than the market

Beta < 0 means the stock tends to move against the market Stocks in gold mining companies are a real-world example of

negative beta stocks Beta for a Portfolio

Beta for a portfolio is the weighted average of the betas of the individual stocks within the portfolio

43

Using Beta—The Capital Asset Pricing Model (CAPM) The CAPM helps us determine how stock prices

are set in the market Developed in 1950s and 1960s by Harry Markowitz

and William Sharpe

The CAPM's Approach People won't invest unless a stock's expected return

is at least equal to their required return The CAPM attempts to explain how investors'

required returns are determined

44

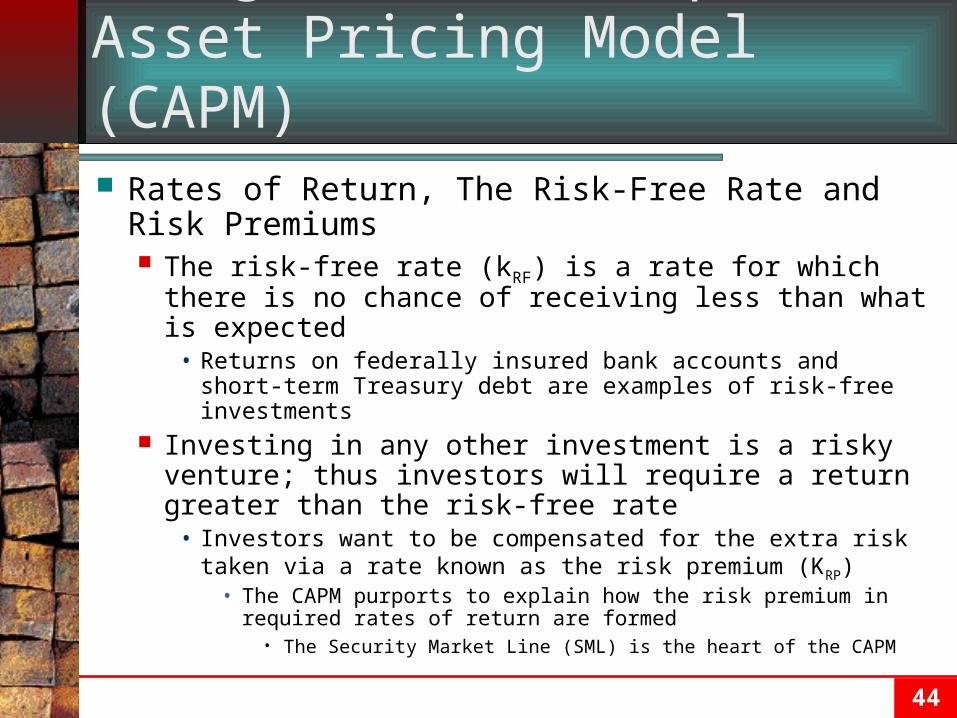

Using Beta—The Capital Asset Pricing Model (CAPM) Rates of Return, The Risk-Free Rate and Risk

Premiums The risk-free rate (kRF) is a rate for which there is no

chance of receiving less than what is expected• Returns on federally insured bank accounts and short-term

Treasury debt are examples of risk-free investments Investing in any other investment is a risky venture;

thus investors will require a return greater than the risk-free rate

• Investors want to be compensated for the extra risk taken via a rate known as the risk premium (KRP)

• The CAPM purports to explain how the risk premium in required rates of return are formed

• The Security Market Line (SML) is the heart of the CAPM

45

The Security Market Line (SML) The SML proposes that required rates of return

are determined by:

The Market Risk Premium• Is a reflection of the investment community's level of risk aversion• It is the risk premium for an investment in the market as a whole

The Risk Premium for Stock X• The beta for Stock X times the risk premium of the market• Says that the risk premium for a stock is determined only by the

stock's relationship with the market as measured by beta

X RF M RF X

Market Risk Premium

Stock X's Risk Premium

k k k k b

46

The Security Market Line (SML) The SML as a Portrayal of the Securities Market

The standard equation of a straight line is• y = mx + b

• Where: y is the vertical axis variable; x is the horizontal axis variable; m is the slope of the line and b is the y intercept

The SML can be viewed as a straight line:

X RF M RF X

y = b + xm

k k k k b

• The slope of the SML plotted in risk-return space reflects the general level of risk aversion

• The vertical intercept of the SML represents investment in short-term government securities

47

The Security Market Line (SML) The SML as a Line of Market Equilibrium

If, for every stock, its expected return equals its required return, the SML represents equilibrium

Suppose that a stock's expected return now becomes less than its required return

• Investors would no longer desire that stock and owners of the stock would sell while potential buyers would no longer be interested

• The stock price would drop because supply would exceed demand

• Since the stock price is dropping, its expected return is increasing, driving it back toward equilibrium

• The SML represents a condition of stable equilibrium

48

The Security Market Line (SML) Valuation Using Risk-Return Concepts

The SML allows us to calculate the minimum required rate of return for a stock

This return can then be used in the Gordon model to determine an intrinsic value for a stock

The Impact of Management Decisions on Stock Prices Since managers can influence a stock's beta and

future growth rates, management's decisions impact the price of the stock

49

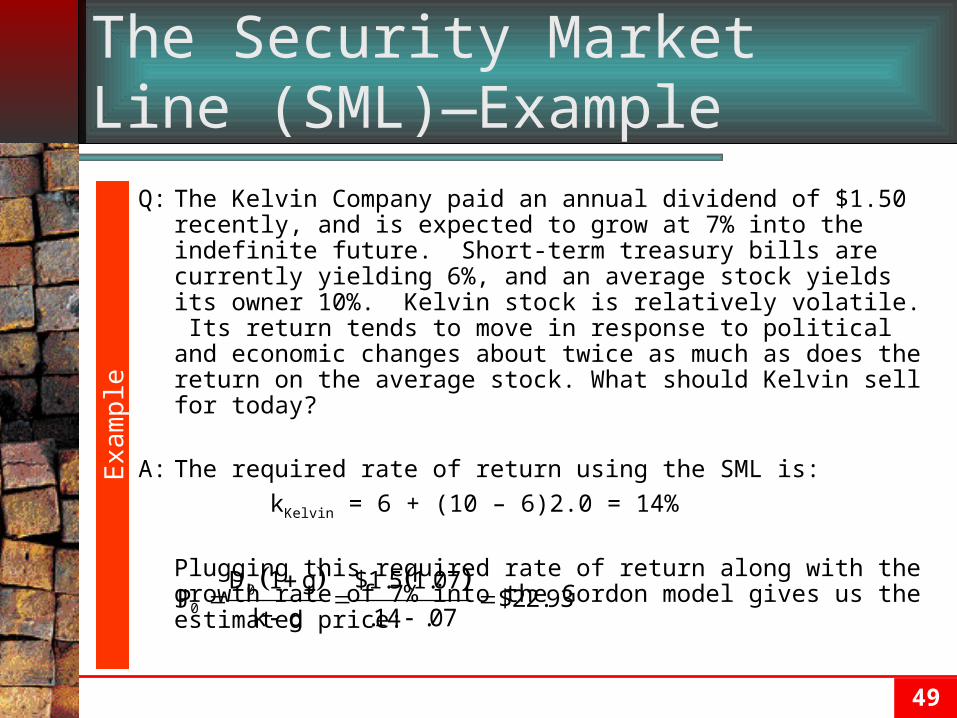

The Security Market Line (SML)—Example

Q: The Kelvin Company paid an annual dividend of $1.50 recently, and is expected to grow at 7% into the indefinite future. Short-term treasury bills are currently yielding 6%, and an average stock yields its owner 10%. Kelvin stock is relatively volatile. Its return tends to move in response to political and economic changes about twice as much as does the return on the average stock. What should Kelvin sell for today?

A: The required rate of return using the SML is:

kKelvin = 6 + (10 – 6)2.0 = 14%

Plugging this required rate of return along with the growth rate of 7% into the Gordon model gives us the estimated price:

Exa

mpl

e

00

D 1 g $1.5 1.07P $22.93

k g .14 .07

50

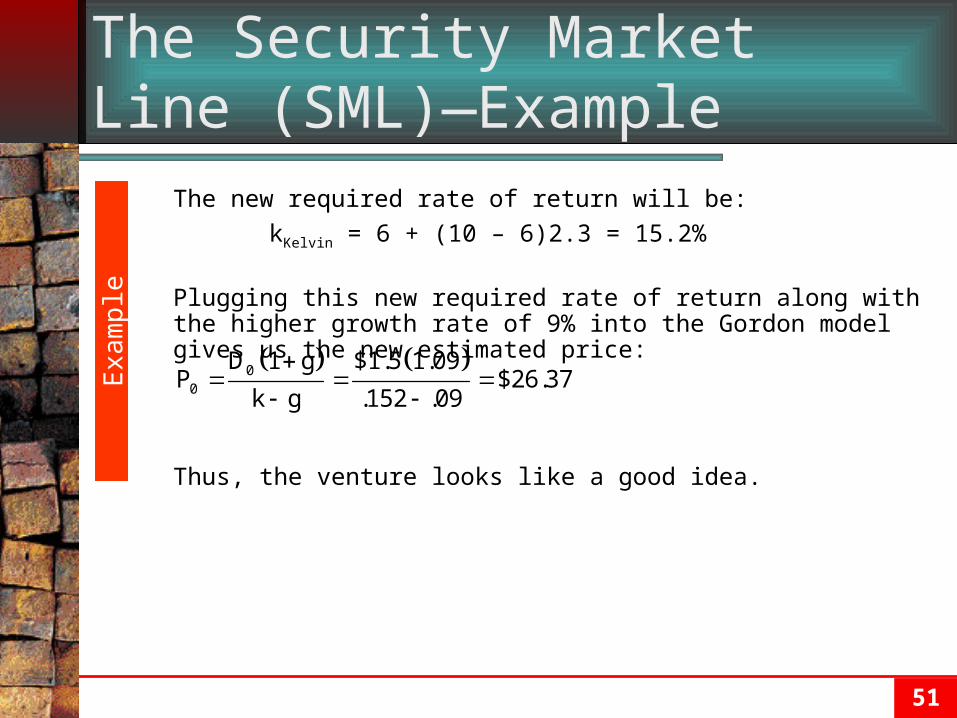

The Security Market Line (SML)—Example

Q: The Kelvin Company has an exciting new opportunity. The firm has identified a new field into which it can expand using technology it already possesses. The venture promises to increase the firm's growth rate to 9% from the current 7%. However, the project is new and unproven, so there's a chance it will fail and cause a considerable loss. As a result, there's some concern that the stock market won't react favorably to the additional risk. Management estimates that undertaking the venture will raise the firm's beta to 2.3 from its current level of 2.0. Should Kelvin undertake the new project if the firm’s current stock price is $22.93?

A: The objective of the firm’s management should be to maximize

shareholder wealth. If growth is expected to increase, this will have a positive impact on stock price; however, if an increase in beta is expected, stockholders will demand a higher rate of return which will cause an offsetting drop in the stock price. The expected price of the stock given both the increase in the growth rate and the increase in the firm’s beta must be calculated.

Exa

mpl

e

51

The Security Market Line (SML)—Example

The new required rate of return will be:

kKelvin = 6 + (10 – 6)2.3 = 15.2%

Plugging this new required rate of return along with the higher growth rate of 9% into the Gordon model gives us the new estimated price:

Thus, the venture looks like a good idea.

Exa

mpl

e

00

D 1 g $1.5 1.09P $26.37

k g .152 .09

52

The Security Market Line

Adjustments to Changing Market Conditions The response to a change in the risk-free rate

• If all else remains the same, a change in the risk-free rate causes a parallel shift in the SML

• The slope of the SML remains the same which means KM must increase by the amount of the change in kRF

The response to a change in risk aversion• Changes in attitudes toward risk are reflected by rotations of

the SML around its vertical intercept

53

The Validity and Acceptance of the CAPM and SML CAPM is an abstraction of reality designed to

help make predictions Its simplicity has lead to its popularity

• It relates risk and return in an easy-to-understand concept

However, CAPM is not universally accepted Continuing debate exists as to its relevance and

usefulness• Fama and French found no historical relationship between

the returns on stocks and their betas