socialist people’s libyan arab jamahiriya a public ... · socialist people’s libyan arab...

TRANSCRIPT

Report No. : 45019-LY

Socialist People’s Libyan Arab Jamahiriya A Public Expenditure Review

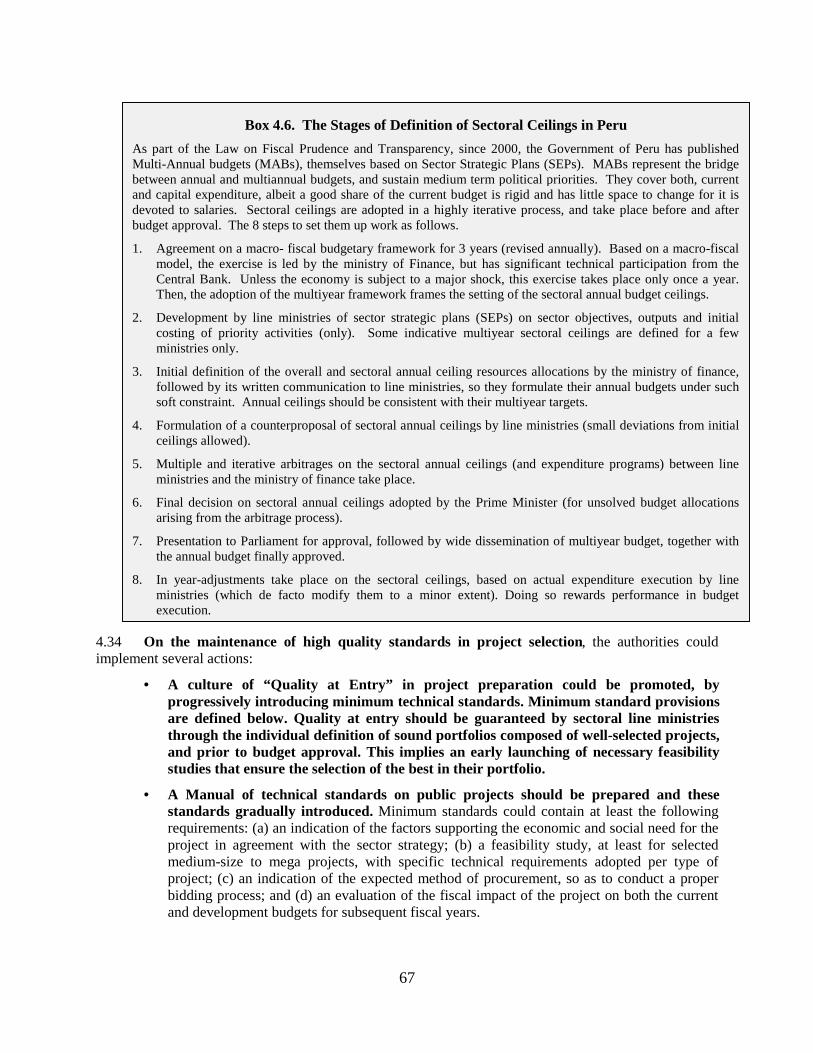

(In Three Volumes) Volume II: Main Report September 30, 2009 Social and Economic Development Group Middle East and North Africa Region

Document of the World Bank

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

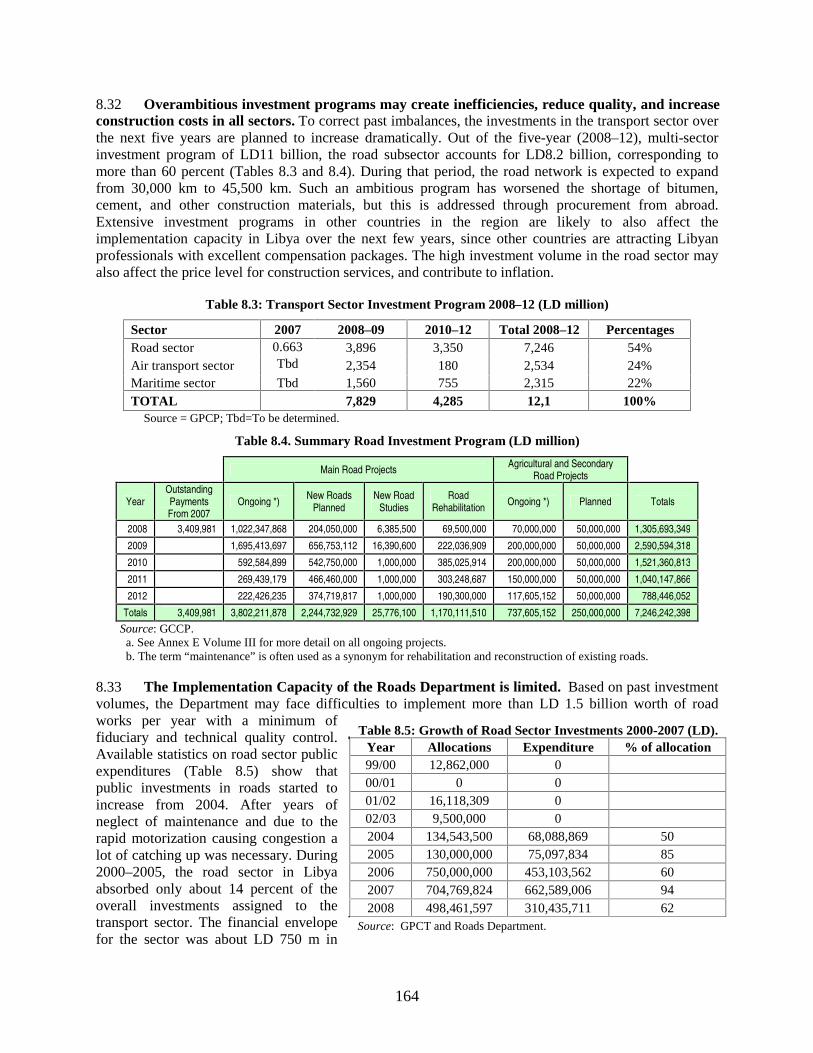

utho

rized

CURRENCY EQUIVALENTS(As of September 30, 2009)

Local Currency Unit = Libyan Dinar Exchange Rate (1.27 LD per USD)

FISCAL YEAR 2009July 1-June 30

WEIGHT AND MEASURES

Metric System

ACRONYMS AND ABBREVIATIONS

ABC Activity based costing AMR Automatic Meter Reading BCM Billion cubic meters BPC Basic Public Congresses Bpd Barrels per day CAPEX Capital expenditures CBL Central Bank of Libya CCGT Combined Cycle Gas Turbine CERA Cambridge Energy Research Associates CFL Compact fluorescent lamp CMM Collection management and metering CPI Consumer price index DBO Design-build-operate DPAT Territorial divisions in charge of

planned investments DSM Demand-side management ECA Energy conservation agreements EPA Effective project approval FAO UN Food and Agriculture

Organization GBHCP General Body for Health Care Planning GCHU General Corporation for Housing

and Utilities GCP General Counsel for Planning GDP Gross domestic product GEA General Environment Authority GECOL General Electricity Company of Libya GER Gross enrollment rate / gross

enrollment ratio GFS Government Financial Statistics GMMR Great Man Made River GMMRA Great Man Made River Authority GNI Gross national income GoL Government of Libya GPCA General People Committee of

Agriculture GPC General People’s Committee GPCEWG General People Committee for

Electricity, Water, and Gas GPCGE General Peoples’ Committee for General

Education GPCF General People’s Committee for Finance

GPCHE General People’s Committee for Health and Environment

GPCHE General Peoples’ Committee for Higher Education

GPCMP General People’s Council for Manpower GPCP General Peoples’ Committee for Planning GPCPF General Peoples’ Committee for

Planning and Finance GPCT General People’s Committee for

Transport (Ministry of Transport) GSC General service company GWA General Water Authority GWh Gigawatt Hour HALE Healthy life expectancy HC Hydrocarbon HDI Human development index HFO Heavy Fuel Oil HIB Housing and Infrastructure Board HUC Housing and Utility Corporation HIV Human immunodeficiency virus HUGC Housing and Utilities General Corporation IBT Increasing block tariff IEA International Association for the

Evaluation of Educational Achievement IMF International Monetary Fund IMR Infant mortality rate IPP Independent power projects IT Information technology Km Kilometer Km2 Square kilometer KV Kilovolt kWh Kilowatt-hour l/c/d Liters consumed daily LD Libyan dinar LFO Light Fuel Oil L/km Liters per kilometer LRAIC Long run average incremental cost LRMC Long-run marginal cost M2 Square meters Mbpd Million barrels per day MCM Million cubic meters MENA Middle East and North Africa

MIC Middle-income country MLD Millions of Libyan Dinars MMBTU Million British Thermal Units MTEF Medium-term expenditure framework MW Megawatts MWEG Ministry of Electricity, Water and Gas NCP National Counsel for Planning NCEP National Centre for Education Planning NDPs National Development Plans NHGDP Non-hydrocarbon gross domestic

product NHPB Non-hydrocarbon primary fiscal balance NOC National Oil Company NPC National Planning Council NPV Net present value NWC National Water Company NWWC National Water and Wastewater

Company OECD Organization for Economic Co-

operation and Development O&M Operations and maintenance OPEX Operational expenditures ORF Oil Reserve Fund Pb Per barrel PBC Performance based contracting PCSC Programme Complémentaire de

Soutien à la Croissance PER Public expenditure review PHC Primary health care PIMS Public investment management system PIP Public investment plan PISA Program for International

Management in Higher Education PMO General Peoples Committee or

Prime Minister’s Office PPA Power purchase agreements PPA Preliminary project approval

PPPs Public-private partnerships PSP Private sector participation RBA Roads and Bridge Authority RR Required revenue RUC Road user charges SDR Special Drawing Rights SEC Secondary Education Certificate Shaabiats Municipalities SMEs Small and medium enterprises SRMCs Short-run marginal costs TCF Trillion cubic feet TDS Total dissolved solids TIMSS Trends in International Mathematics

and Science Study TOU Time-of-Use (tariff) TVET Technical and vocational education

and training U5MR Under-5 mortality rate UfW Unaccounted for water UN United Nations UNAIDS United Nations Joint Programme on

HIV/AIDS UNDP United Nations Development Programme UNESCO United Nations Educational,

Scientific and Cultural Organization UNICEF United Nations Children’s Fund Vpd Vehicles per day WDI World Development Indicators WEG Water, electricity, and gas WHO World Health Organization WHOSIS World Health Organization

Statistical Information System WSS Water supply and sanitation WSSP Water Study and Strategy Proposal–2025 WTO World Trade Organization WWW Water and waste water

Vice President: Shamshad Akhtar Country Director: Mats Karlsson Sector Director: Ritva S. Reinikka Sector Manager: Farrukh Iqbal Lead Economist and Task Team Leader: José R. López-Cálix

SOCIALIST PEOPLE’S LIBYAN ARAB JAMAHIRIYA PUBLIC EXPENDITURE REVIEW

Table of Contents

CHAPTER 1. INTRODUCTION ................................................................................................... 1 I. The Recent Economic Cycles of Libya...................................................................................1 II. The Country’s Social Achievements ......................................................................................4 III. Why a Public Expenditure Review?.......................................................................................4 IV. The Unique Institutional Features Surrounding the Accountability of Public Investment

Management in Libya..............................................................................................................5 V. The Scope and Content of the Public Expenditure Review .................................................8 VI. The Recent Performance of Public Investment.....................................................................9

CHAPTER 2. OVERALL FISCAL DEVELOPMENTS AND SUSTAINABILITY............................... 18 I. Macroeconomic Background................................................................................................18 II. Fiscal Trends From 1990 Through 2007..............................................................................20 III. Fiscal Sustainability Analysis ...............................................................................................21 IV. Dealing with Methodological Limitations............................................................................28 V. Policy Recommendations ......................................................................................................29

CHAPTER 3: THE CONTRIBUTION OF CIVIL SERVICE REFORM TO FISCAL SUSTAINABILITY31 I. Introduction............................................................................................................................31 II. The Size the Libyan Public Administration and its Macroeconomic Implications ........32 III. Compensation Policies and their Implications for the Wage Bill......................................35 IV. The Civil Service Reform (2006-present) ............................................................................36 V. Pay Reform.............................................................................................................................41 VI. Handling of the Retrenched Employees...............................................................................44 VII. Policy Recommendations ......................................................................................................46

CHAPTER 4: MODERNIZING THE PUBLIC INVESTMENT MANAGEMENT SYSTEM IN LIBYA 49 I. Public Investment Trends .....................................................................................................49 II. The Link between Public Investment and Growth.............................................................53 III. Assessing the Budget Cycle of Public Investment...............................................................54 IV. Policy Recommendations ......................................................................................................63 V. The Challenge of Budget Unification...................................................................................70

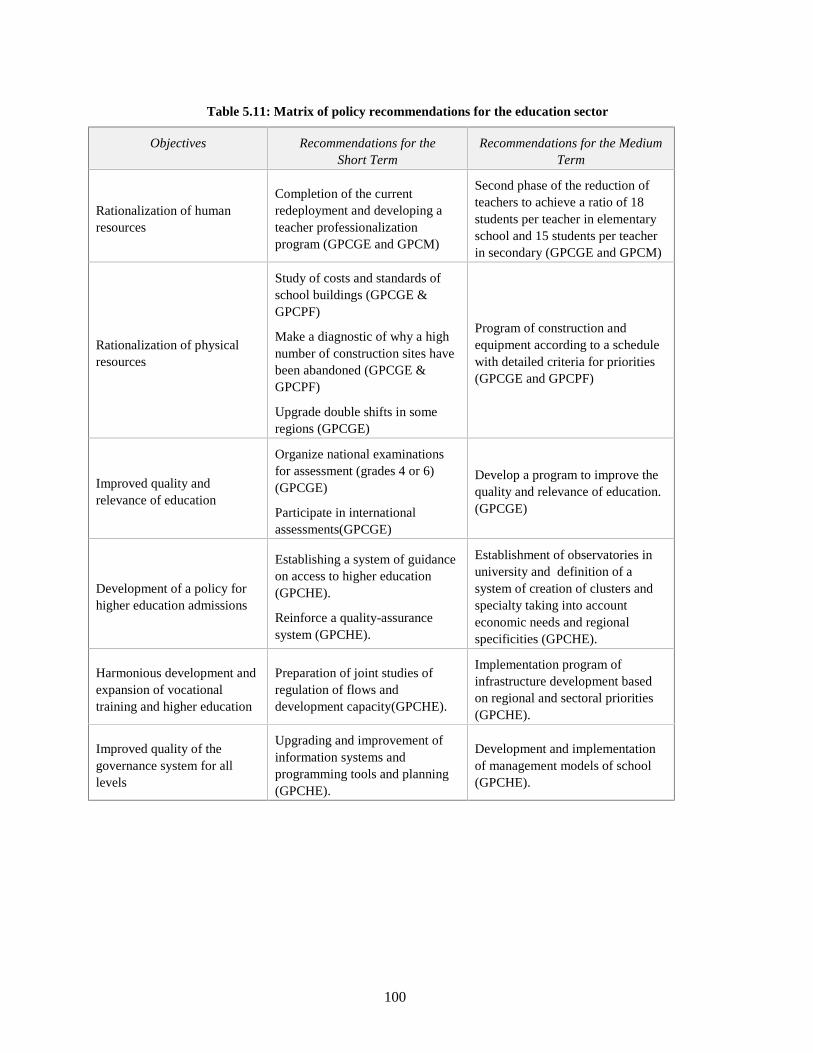

CHAPTER 5: BALANCING EFFICIENCY AND QUALITY OF EDUCATION IN LIBYA ................. 74 I. Introduction............................................................................................................................74 II. The Performance of the Education Sector ..........................................................................75 III. The Institutional Framework and its Accountability .........................................................80 IV. Overall Public Expenditure Patterns...................................................................................81 V. Searching for Quality: The Efficiency of the Education Sector ........................................87 VI. Policy Recommendations ......................................................................................................95

CHAPTER 6: IMPROVING HEALTH SERVICES FOR ALL IN LIBYA....................................... 102 I. Introduction..........................................................................................................................102 II. The Performance of the Health Sector ..............................................................................103 III. The Institutional Framework and its Accountability .......................................................106

IV. Overall Public Expenditure Patterns.................................................................................111 V. Searching for Quality: The Efficiency of the Health Sector ............................................117 VI. Policy Recommendations ....................................................................................................118

CHAPTER 7. INCREASING THE EFFICIENCY OF THE POWER SECTOR IN LIBYA ................. 123 I. Introduction..........................................................................................................................123 II. The Performance of the Power Sector ...............................................................................127 III. The Institutional Framework and Its Accountability.......................................................131 IV. Overall Public Expenditure Patterns.................................................................................136 VI. Searching for Quality: The Efficiency of the Power Sector.............................................142 VII. Policy Recommendations ....................................................................................................146

CHAPTER 8. REBALANCING ROAD MAINTENANCE AND NETWORK DEVELOPMENT........ 155 I. Introduction..........................................................................................................................155 II. The Performance of the Road Sector.................................................................................156 III. The Institutional Framework and Its Accountability.......................................................158 IV. Overall Public Expenditure Patterns.................................................................................163 V. Searching for Quality: The Efficiency of the Roads Sector .............................................168 VI. Policy Recommendations ....................................................................................................170

CHAPTER 9: MAKING WATER USE EFFICIENT AND SUSTAINABLE ................................... 173 I. Introduction..........................................................................................................................173 II. The Performance of the Water Sector ...............................................................................173 III. The Institutional Framework and its Accountability .......................................................180 IV. Overall Public Expenditure Patterns.................................................................................182 V. Searching for Quality: The Efficiency of the Water Sector.............................................187 VI. Policy Recommendations ....................................................................................................191

CHAPTER 10. SETTING PRIORITIES IN THE 2008–12 PUBLIC INVESTMENT PLAN: THE SHIFT

OF PUBLIC INVESTMENT TOWARD PRODUCTIVE ACTIVITIES........................ 195 I. Introduction..........................................................................................................................195 II. The Status of the Pipeline of Public Projects at the End of 2007 ....................................197 III. The Move toward Productive Activities: Key Features of the 2008–12 PIP ..................198 IV. Main Factors Strengthening the Technical Efficiency of Public Investments ...............203 V. Guidelines for the Intrasectoral Selection of Public Projects ..........................................206 VI. Guidelines for Intersectoral Prioritization of Public Projects .........................................217

REFERENCES......................................................................................................................... 223

1

Chapter 1. Introduction

I. The Recent Economic Cycles of Libya 1.1 In a historic context, the present macroeconomic stance of the Socialist People’s Libyan Arab Jamahiriya is solid and remarkable. The recent economic cycles have mainly been determined by fluctuations in oil prices and, somehow, by political events.1 Since 1990, three major periods can be distinguished: 1990–98, 1999–2005, and 2005 onward (Figure 1.1). • During the 1990–98 stagflation period, low and steady oil prices averaged below US$20/barrel and

had a significant impact on the economy. The country suffered the initial impact of the embargo and faced two severe recessions, one in 1990 and another in 1995, when the rate of economic growth reached -20.2 percent and -12.5 percent (-18.6 percent for non-hydrocarbon GDP), respectively. Inflation was high—in the double digits—and was clearly affected by persistent fiscal imbalances, especially during 1992–94. Inflation only decreased by the end of this period, once fiscal balances turned into a surplus. After 1995, both the fiscal balance and capital expenditure trends were closely correlated with the price of oil, which is typical for an oil-dependent economy.

• During the 1999–2005 decentralization period, the economy recovered and started to accelerate. This was boosted by the end of the embargo in 2003, and by the initial stage of the oil windfall: oil prices hit US$25/barrel in 2003. The year of the end of the embargo, economic growth reached double digits, mostly reflecting a catch-up effect. Inflation rates were negative, on average, which is consistent with successive fiscal surpluses (except for 2001) in close correlation with oil price fluctuations. The unification of the Libyan dinar (between February 1999 and January 2002) also contributed to the deflation process (especially through the ensuing reduction in exchange rate spreads). In parallel, a short-lived period of political decentralization took place, which led to an increased investment by the Shaabiats: capital expenditure ratios to GDP reached successive double digits since 2002, with a parenthesis in 2003, thus becoming markedly procyclical and, indirectly, a key determinant of growth.

• During the 2006–08 recentralization period, the economy was clearly favored by the deepening of the oil windfall. Strong economic performance accompanied the process of political recentralization. High and successive GDP growth rates reached 6 to 7 percent. Non-hydrocarbon GDP rates (for simplicity referred as “non-oil” GDP rates) also increased, but remained below the rates obtained by overall GDP. Significant fiscal surpluses (above 25 percent of GDP) were obtained despite an always expansive public investment reaching average rates above 16 percent of GDP. A booming investment, however, may have had a price: high inflation. Indeed, despite inflation rates were mainly determined by import prices, an accelerated pace in the implementation of the PIP and its associated rising prices in non-tradables (mostly services) should have also put some degree of pressure on inflation, which reached double digits by early-2008.2

1 It can be argued that the relationship between political events and GDP could be spurious (i.e. superficially like, but genuinely unlike)., but to prove it in econometric

terms would be challenging as, contrary to oil prices, it is very hard to find a single quantitative proxy for political events. In any case, the significant potencial role of the political

cycle and its impact on public expenditure (and growth) patterns are well supported by the economic literature (see Alesina, Roubini and Cohen, 1997). 2 A macroeconomic model developed by the Authorities indicates that high public investment had no perceived effect (especially through services) on prices, at least

until 2007 (see Merza 2008).

2

3

Figure 1.1. Libya: Oil Price, Growth, Public Investment, and the Fiscal Balance

-20

-10

0

10

20

30

40

Pe

rce

nt

/ P

erc

en

t o

f G

DP

0

20

40

60

80

100

120

US

$/b

arr

el, L

ibya

Oil P

rice

GDPGrowth, LHS -20.2 14.5 -3.6 -3.5 2.9 -12.7 3.1 -2.4 0.0 0.4 3.7 5.8 -0.4 12.9 6.0 9.9 5.9 6.8 7.1

Non-oil GDPGrowth 21.7 -6.1 -7.4 4.2 -18.6 0.5 -4.2 -1.2 -1.0 4.5 3.3 -6.8 20.0 5.5 7.2 4.3 3.9 3.8

Inflation, End of Period 10.8 11.7 9.5 7.5 10.7 8.3 0.9 3.3 3.8 1.7 -6.6 -10.3 -7.3 -1.3 -3.5 3.0 7.2 8.1 8.0

Fiscal Balance 1.3 8.4 -0.1 -6.0 -2.8 3.9 11.7 -2.2 -2.4 5.9 13.5 -0.7 10.0 9.5 13.9 30.9 35.5 26.2 35.0

Capital Expenditure 6.6 5.3 6.4 8.8 7.3 6.3 8.0 7.8 5.6 5.8 9.2 8.8 12.0 8.3 16.2 18.2 16.2 21.0 18.0

LibyaOil Price, RHS 22.0 18.5 18.2 16.1 15.3 16.5 19.5 18.4 12.5 17.2 27.0 23.3 24.4 28.2 36.9 51.9 62.5 69.1 108.9

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 p/ 08e/

Embargo Ends

Decentralization Period

Oil Price Hike

Oil PriceSlumps

Deep Recessions

Source: IMF and Bank Staff’s Estimates. LHS =Left Hand Side; RHS = Right Hand Side

4

II. The Country’s Social Achievements 1.2 Libya is an upper-middle-income country with remarkable social achievements. In 2006, it had a population of about 6 million and a gross national income (GNI) per capita of US$7,370. It is a highly urbanized country: 85 percent of the population lives in cities. The hydrocarbon sector represented 97 percent of exports of goods and non-factor services (76 percent of GDP) and 93 percent of government revenues. Hydrocarbons also represent the bulk of nominal gross domestic product (GDP) (72 percent), followed by services (19 percent), and agriculture (3 percent). 1.3 Social indicators are similar to or better than the average in the Middle East and North Africa (MENA) Region. According to the 2007 United Nations Development Programme’s (UNDP’s) Human Development Index, Libya is ranked 59th among the 162 countries. Libya spends considerable public resources on its education sector (7 percent of GDP), but less on the health sector (2 percent of GDP). It has achieved universal enrollment in primary education and an adult literacy rate of 91 percent. Secondary school enrollment has increased from 21 percent in the 1970s to 105 percent in recent years, and tertiary enrollment has recorded a similar pattern. Life expectancy at birth is 73 years (70 years for males and 75 for females), on a par with most middle-income countries. The total fertility rate is 5.2 children per woman of reproductive age, and one-third of the population is below age 15. Infant and under-5 mortality rates are lower than in most MNA countries, at 18 and 19 per 1,000 live births, respectively. Access to improved sanitation is 96 percent in both rural and urban areas. There is almost universal access to primary health facilities at the local level. There are 1.25 physicians and 4.8 nurses per 1,000, population although most likely there are geographic distribution issues. III. Why a Public Expenditure Review? 1.4 Past outcomes show that Libyan Authorities have worked on their macroeconomic and social fundamentals, so as to have a solid base to sustain its steady progress toward building a market-based economy and reintegrating into the world economy. Making optimal use of a sizable public expenditure, and especially public investment, is an essential component of achieving this strategy. Indeed, the country critically needs quality public spending to sustain rapid growth in basic and social infrastructure, while preserving social gains. Much, however, remains to be done in terms of sustainable accelerated growth. Libya’s growth (and fiscal accounts) continues to be highly dependent on hydrocarbon revenue, and the country remains vulnerable to oil price shocks. Since 2004, an oil boom has continued unabated, generating an expansionary fiscal stance and an extraordinary accumulation of net foreign assets, together with large liquidity in deposits in the (public) banking system. Libya has experienced accelerated growth in the 2000s, with an average annual growth rate close to 6.5 percent. 1.5 To preserve high growth and consolidate important social gains, Libya has embarked on a massive multiyear Public Investment Plan (PIP) for 2008–12, with an initial estimated allocation of LD270 billion (Libyan dinar) (about US$225 billion) for the period, then revised down to LD150 billion by end-2008. This leads to an annual average of planned expenses of LD45 billion per year. Compared to LD19 billion executed in development (capital) outlays during 2006, the projected yearly average is about three times the 2006 amount, and illustrates the major challenge faced by the Government, given its weak, but rapidly improving project implementation capacity. Authorities want the PIP to address the most pressing needs in terms of improvement of the provision of public services, and to deal with a backlog of infrastructure rehabilitation, plus major modernization and expansion needs. 1.6 While increased public investment can be accommodated in the Government’s strong budgetary position, it creates multiple challenges. These concern (a) the medium-term sustainability of fiscal trends, (b) the existence and soundness of sectoral strategies, (c) the proper mix (and trends) of development (capital) compared to current outlays, and (d) the quality of public investment, promoted by

5

the use of standards on project management—design, execution, monitoring and evaluation. An adequate response to those challenges is needed to ensure that the PIP 2008-12 investments are supporting faster growth and development, instead of greater opportunities for waste and corruption. 1.7 The PIP 2008-12 also raises important issues concerning the accountability of institutions in the unique context of Libya. The performance of the public investment system is continuously affected by the changing and perceived overlapping of responsibilities among different governmental agencies, the low level of coordination inside the government, the limited capacity of civil servants to control and execute public spending, and the adverse environment to stimulate private participation in the financing and execution of public investment. The rest of this chapter introduces key details about the unique institutional features of the Libyan state, the stylized facts about the most recent execution of the development budget in 2007, and the scope and content of the public expenditure review (PER). These details will familiarize the reader with the main topics of this report. IV. The Unique Institutional Features Surrounding the Accountability of Public Investment Management in Libya 1.8 To realistically assess the accountability of Libyan public investment management, it is necessary to understand its unique institutional characteristics. Libya does not follow international standards on public expenditure management (see IMF 2006) and, as this report shows, the same conclusion applies to public investment, despite very important progress achieved since 2006. Hence, the major challenge that this report addresses is how to gradually introduce those budgeting standards in Libya, given its unique institutional environment. The task requires taking into consideration key features of its political economy. There are at least six institutional factors that frame the accountability of public investment management.

1.9 First, Libya’s institutional policymaking reflects the principle that citizens should participate in government, from the grass roots to the highest levels. After the 1969 revolution, the country embarked on a number of attempts to develop a unique concept of local governance. Several stages have followed. Initially, after the revolution, the country was divided into 10 governorates, which were subdivided into provinces and departments. Then, governorates were abolished in 1975 and replaced by 26 municipalities, branches, and localities, and 340 popular conferences. This was not long-lived. In 1977, the “declaration of people’s power” established local authorities as the basis for the political system. The authority was delegated to the General and Local People’s Conferences, and General and Local People’s Committees in the localities. Consequently, the 26 municipalities were abolished in 1998 and replaced by 31 Shaabiats administrative regions (the singular is Shaabia) and 415 popular conferences. The number of Shaabiats was subsequently reduced to 22. In an important precedent for current events, transition toward full decentralization led to the demise of most ministries, including Communication and Transport, Energy, Agriculture, Health and Social Security, Housing and Utilities, and Education). Barely five ministries with national responsibilities survived, including External Relations and Cooperation, Justice and General Security, Finance and Trade, Tourism, and a lately introduced social sectors “directorate.”

1.10 Second, since 2006, there has been an ongoing recentralization of the state. Libya is now in a process of political (and fiscal) recentralization. This process reverts the aborted experience of delegation of expenditure responsibility (decentralization) to the Shaabiats carried on during 1999–2005. This is a major institutional change. During decentralization, most of the functional and operational development budget decisions were transferred from a streamlined Central Government to the Shaabiats. There are few written assessments of the decentralization period, but broad and deep consensus prevails among officials

6

that decentralization severely damaged the economy and, more important, weakened the country’s governance.3 During 1999–2005, fiscal management failures were multiple: (a) the number of public servants more than doubled from half a million to over a million, and growth took place especially at the local level, leading to numerous “ghost”(absent from duty) workers; (b) the number of projects exploded at the local level, leading development (capital) expenditure to increase from 5.8 percent of GDP to 18.2 percent of GDP; (c) data collection on budget execution by the Shaabiats was completely abandoned, leading to a complete lack of monitoring, transparency, and accountability mechanisms, and a severe deterioration of key national accounts; and (d) in part as a popular response to perceived budgetary disarray, tax revenue dramatically shrank from 15.1 percent of GDP to 2.6 percent of GDP. According to officials, a weakened Central Government coupled with unaccountable decentralized institutions led perceived corruption to spread. A high authority interviewed was perhaps not exaggerating when he affirmed that “badly implemented decentralization was demolishing the country.” 1.11 Third, put it in perspective, institutional reorganization has become an endless and erratic process. The current period of recentralization is part of a sequence of continuous reorganization of the state that has characterized Libya over more than three decades. Ensuing changes have left a fragile and fragmented institutional environment, leading to blurring roles and unstable governance. This phenomenon has particularly hit all ministries associated to the sectors assessed under this Public Expenditure Review. All of them disappeared during the early years of decentralization, only to be recently re-created: Planning in 2003; Higher Education in 2004; General Education, Agriculture, Water, Gas and Transportation in 2006; and Electricity (power) in 2007.4 As a result, there is confusion of institutional roles at the central level, the policy development functions of central institutions are not clear, and some institutional bodies have legislative (through ad hoc decrees) and executive powers (Smith 2006). Consequently, since 2006, despite efforts to redefine the role of ministries in more detail, many institutional overlaps prevail at the central level. A well-known example is the multiple number of institutions in charge of water policy, but this case is far from being unique. 1.12 Fourth, until very recently, the public investment system has worked with a myopic approach relying on poor information. Continuous institutional reorganization, with its ensuing gap in the collection of reliable data, has made it very difficult for Libyan policymakers to make well-informed strategic decisions. Until 2008, on budgetary issues, officials from the Ministries of Planning, Finance, and other sectors had prepared their development budgets in a context of severe information and analytical gaps, featuring a generalized shortage of reliable hard data and time series, scarce institutional memory, and inexperienced and only recently hired staff. Until then, the predominant focus was on day-to-day decisions in a “myopic approach” to policymaking. Most recent quick progress in strengthening the institutional framework, in improving the reliability and timeliness of information and in enforcing budget norms have led all ministries and public entities to approach the less steep side of the learning curve, followed by gradually major improvements in budget execution (see below). Planning and finance officials have become familiar with their counterparts in sectoral ministries, who are gotten used to new budgeting procedures, thus contributing to raise staff productivity. 1.13 Fifth, the current public expenditure institutional framework is also unsatisfactory in a number of procedural aspects. A detailed analysis of the public investment management system is presented in chapter 3. Just to mention a few ones worth mentioning: (a) dual budgeting and its ensuing lack of a clear relationship with the budget process for current expenditure; (b) partial, but promising medium-term expenditure programming; (c) the absence of a performance-based approach to budgeting;

3 The UNDP (2002) and Smith (2006) are the only mid-course existing reports, but they do not provide an assessment. 4 The functions of some ministries were preserved under another institution or under the protection of a higher authority, i.e. the planning function was preserved under the

Planning Council.

7

(d) multiple weaknesses in the procedures for reporting on the budget; (e) and limited budget preparation and execution skills at the sectoral and Shaabia levels of government. 1.14 Sixth, the nascent respect for public investment procedures is working to remedy the previously generalized lack of transparency and accountability. As an example, until very recently there was a generalized lack of feasibility studies in public projects. This was inherited from the 1999-2005 decentralization period. With few exceptions, no single project (of which there are more than 23,000) implemented by Shaabiats during such period, or by the Central Government, was supported by a feasibility study. Indeed, the practice of having projects approved with barely the submission of a simple “sheet of paper” describing generalities of the project, was widespread. Only since late 2006, has the re-created Ministry of Planning introduced highly valuable initial forms with which to prepare project requests. Similarly, the use of modern information technology (IT) in an integrated financial management system was introduced in 2007. Basic reporting on project execution was reestablished in 2007, but compliance is partial and considerable room for improvement exists. In a context of multiple bank accounts (up to 4,000 according to IMF 2006) and predominantly paper-based transactions, reporting on expenditure execution can only be inaccurate and delivered with delays. Thus, the ensuing gaps of transparency and accountability in budget execution remain important. In addition, the reestablishment of the General Peoples’ Committee for Planning (GPCP) as central player in public investment has left the role of local planning councils unclear (Smith 2006). 1.15 On another example of such unpredictable institutional changes, on March 2, 2008, Colonel Muammar Gaddafi announced another sweeping major government reform. Gaddafi charged that the Cabinet has failed to manage the hydrocarbon windfall well and that major public works projects have been falling seriously behind schedule. Consequently, he indicated that all ministers will be phased out at the end of 2008, as part of a major reform of the state; in the meantime, however, the announcement was accompanied by an important Cabinet reshuffle.5 Full details of the government reform have not been completed yet, as in March 2009, a Congress of the Libyan General People’s Committees postponed the reform to a later date. But according to initial media leaks, only five ministries—Defense, Security, External Affairs, Finance, and Planning—would have continued after the transition period. Other “surviving ministries” would have been downgraded under the global direction of a prime minister, who would be held accountable to local congresses and national commissions. Five commissions are currently at work—(a) budget (finance and planning), (b) governance (new institutional organization of the government), (c) wealth distribution (in charge of the oil fund management and increased cash transfer programs), (d) economic laws (design of a new private sector environment, including increased privatization), and (e) legal environment (judicial reform and other laws). In the March 2009 Congress, however, an important change took place: the ministries of Finance and Planning were merged, a recommendation of this report that is examined in full detail below (see Chapter 4). 1.16 In parallel, Gaddafi also announced a Wealth Redistribution Program. This initiative would disburse cash transfers to half a million households. Whereas the initially announced amount was LD25 billion to LD30 billion (US$20 billion to US$25 billion), enabling every Libyan family to receive, on average, a significant sum (initially US$4,000 per month per family), the overall sum was subsequently decreased. However, the 2008 budget approved only LD4.6 billion (US$3.6 billion). Last March 2009, clear key details of the program were also suspended until further notice and contingent on the eventual fiscal space that eventually higher future oil prices than current ones might open.

5 Baghdadi Mahmudi was newly appointed prime minister. He was a deputy prime minister in the previous Cabinet. Mohammed Ali al-Huwaiz, the former finance minister and

the new deputy prime minister, adds further reformist credentials to the new cabinet. Ahmed Munaisi Abdel-Hamid, the former governor of the Central Bank of Libya, replaced al-

Huwaiz as the new finance minister. The economy and trade portfolio was taken over by Tayeb Safi Tayeb. The reshuffling also transformed the energy ministry into a new

Ministry for Industry, Electricity, and Mineral Resources. The planning minister was also replaced.

8

1.17 In the meantime, the economic diversification reform program continues, though with renewed priorities. For instance, the prime minister has emphasized banking sector reform, including opening of the sector to private and foreign banks, and access to the World Trade Organization (WTO). The Government has also reaffirmed its intention to continue its efforts to make Libya more attractive to foreign direct investment. Gaddafi has also highlighted the government’s intention to focus on the needs of low-income populations, while improving long overdue infrastructure gaps. All these processes, however, are still likely to move at a gradual pace, given a cumbersome bureaucracy and rather “rocky” decision making accompanying the ongoing state restructuring. 1.18 In any case, the PIP 2008–12 offers Libya a golden opportunity to support sustained expansion of economic growth, boost employment, and foster social development, while managing its abundant oil resources well. Sound financial management of its public investment is essential. It requires the gradual introduction of standards in public investment management. These standards would be highly valuable tools to the success of the 2008–12 PIP.

V. The Scope and Content of the Public Expenditure Review 1.19 In a bid to strengthen its technical capacity to manage the public investment program, the Government of Libya has requested the assistance of the World Bank in carrying out a Public Expenditure Review (PER). The present PER—the first ever produced in Libya—is an external review of the country’s fiscal policies and expenditure programs. 1.20 The PER focuses on the assessment of public investment management. Public expenditure management in oil-producing economies consists of three pillars (Figure 1.8). A first pillar deals with the collection and saving of oil revenues. This pillar leads to one stream of a large literature exploring both fiscal sustainability, and the pros and cons of an alternative model of oil stabilization funds. A second pillar deals with the management of oil resources through development(also called capital or investment) expenditures—and their link to current expenditure. This pillar leads to a second stream of a large literature assessing public investment budgeting and standards, and the multiple effects of sizable public investment programs—financed by the oil windfall. The third pillar deals with the management of oil resources to finance social programs—basically through current transfer expenditures. This is the case of programs like the one on Wealth Redistribution recently proposed by Colonel Gaddafi. Hence, per the Authorities’ request, this PER mainly deals with the second pillar, even though a few sections deal indirectly with topics referred to in the other pillars. 1.21 More in detail, the PER underscores the importance of modernizing the public investment system, thus improving the efficiency of public expenditure and obtaining value for money for the Libyan people. It provides a unique opportunity to propose a new framework for planning and efficiently executing public investment projects under the PIP 2008-12. In the context of a sound macroeconomic and budgetary environment, a sustainable and more effective and efficient public expenditure is the sine qua non condition to improved provision of public services to the population and increased private sector participation. The three PER goals are to (i) support the preparation of key components of a medium-term

W R

S E M

D E M

G F

M

O R O R

Figure 1.2. The Three Pillars of Fiscal Management in an Oi l-dependent Economy

9

expenditure framework, drawing lessons from past budgetary management performance in order to avoid implementation problems during 2008–12 and from fiscal sustainability analysis; (ii) deepen the Government’s strategic approach in the adoption of specific sectoral investment decisions; and (iii) introduce high technical standards in public investment management, while improving the effectiveness of investments in the five important sectors selected. In parallel, the PER provides guidance to country officials in conducting preparation and self-evaluation of public expenditures, and in identifying needs for possible technical assistance in selected areas. 1.22 The PER consists of three volumes. Volume I was the synthesis. This Volume II is the main text and is divided into two parts. The first part presents a detailed description of fiscal trends and a fiscal sustainable analysis of public expenditure in the medium term, a review of the civil service reform and a comprehensive diagnostic of the public investment management system. The second part presents comprehensive sectoral analyses. Per the Authorities’ request, the PER adopts a very selective approach, and is focused on five sectors: Education, Health, Power (Electricity), Roads, and Water. All sectoral chapters review the sector’s performance, the institutional framework—including the existence or no of sectoral strategies and their internal consistency—the sector expenditure trends, and, the quality of sectoral public expenditure (investment). Each chapter also provides a matrix of detailed recommendations for line ministries and budget officials. Given severe data shortcomings in terms of quality and availability, the period of analysis mainly refers to the most recent years. Finally, chapter 10 examines in detail the content of the 2008-12 PIP, and the intra- and inter-sectoral criteria trade-offs that should guide project selection in the future. For its part, Volume III includes several annexes on special technical topics, an extensive Statistical Appendix—probably the first of its kind for Libya—and a list of references used in the study—both foreign and Libyan. The Statistical Appendix and Libyan references are evidence of the openness and transparency with which Libyan Authorities have collaborated during the preparation of this report. Having said this, and considering that concrete details of the revised composition and amounts of the multiyear program are now available,6 it is useful to have a first look at the recent performance of the development budget, as it is done in the next section. VI. The Recent Performance of Public Investment

1.23 The size and performance of public investment in Libya have been steadily improving during recent years. Perhaps the best way to familiarize the reader with the main focus of this report—public expenditure with a focus on the development budget—is to examine the most recent stylized facts of the development (capital) budget execution in 2007. Indeed, whereas chapter 2 explores the overall fiscal patterns in detail, this section deals directly with the most salient features of public investment until end-2007. This is made possible by the recent completion and release of an official report on the execution of the 2007 development budget, last November 2008. 1.24 Libya’s recent efforts in devoting sizable resources to fill the infrastructure gap inherited from the embargo have been remarkable and unprecedented.7 The development budget is booming. Supported by the oil windfall, the Central Government invested more than LD41 billion (US$32 billion) over the 2003-07 period (of which

6 Authorities approved an initial 2008-12 PIP in October 2007, and then completed a full and definite draft last November 2008, during the preparation of the 2009 budget, which

is assessed below (see Chapter 10). 7 Unless indicated otherwise, this section is based upon GPCP (2007).

Figure 1.3: Capital Expenditure

(In US$ per inhabitant)

0

500

1.000

1.500

2.000

2.500

1999 2001 2003 2005 2007

Trend line

Source: The General People’s Committee for Planning.

10

4/5th over the last three years). On a per capita basis, capital expenditure increased US$1,859 per Libyan between 2003 and 2007, thus multiplying 6 times during such period. Indeed, capital expenditures rose sharply to US$2,209 in 2007, from US$350 in 2003 (and US$329 in 1999) (Figure 1.3).8 Thus, a massive amount of resources became available for investing in projects (so-called contracts in Libya—see below chapter 4), leading to an expansive fiscal stance. 1.25 However, not all sectors benefitted from increased budget allocations equally. Overall, the big winners of such an increase were housing and urban development, as well as basic infrastructure, which together represented about half of total investment for 2007 (30 percent and 20 percent respectively) (Table 1.1); whereas social spending represented 10 percent. On per capita terms, and during 2003-07, social spending also resulted in an increase of only US$132 per inhabitant, whereas capital expenditure in basic infrastructure and in housing and urban development projects increased US$316 and US$638 per inhabitant respectively.

Table 1.1: Actual Capital Expenditure, 1999 and 2003-2007

1999 2003 2004 2005 2006 2007 (In million of LD, unless otherwise indicated)

Total 794 2,530 3,581 9,597 8,924 16,939 Social spending 1/ 191 633 809 1,017 1,018 1,689 Of which: Education 2/ 121 307 560 838 742 1,229

Health 69 326 249 179 274 454 Basic infrastructure (w/o Housing) 187 … 729 2,965 1,524 3,172 Of which: Power 93 … 541 1,496 1,000 1,874

Communications and Transport 94 98 188 469 524 1,298 Housing and urban development 130 195 340 343 2,733 5,103 Others 3/ 286 1,604 1,702 6,272 3,648 6,975 Population (Million of inhabitants) 5,203 5,629 5,740 5,854 5,970 6,089 Average exchange rate (LD/USD) 0.464 1.284 1.305 1.308 1.314 1.259

(In million of US$) Total 1,712 1,971 2,744 7,335 6,791 13,451 Social expenditure 1/ 2/ 411 493 620 777 773 1,341 Of which: Education 1/ 262 239 429 640 565 975

Health 149 254 191 137 208 361 Basic infrastructure (w/o Housing) 403 … 559 1,501 1,160 2,519 Of which: Power 200 … 415 1,143 761 1,488

Communications and Transport 203 76 144 358 399 1,031 Housing and urban development 281 152 260 262 2,081 4,052 Others 3/ 617 1,249 1,304 4,794 2,777 5,539

(In US$ per inhabitant) Total 329 350 478 1,253 1,138 2,209 Social spending 1/ 2/ 79 88 108 133 130 220 Of which: Education 1/ 50 43 75 109 95 160

Health 29 45 33 23 35 59 Basic infrastructure (w/o Housing) 77 … 97 256 195 413 Of which: Power 38 … 72 195 128 244

Communications and Transport 39 13 25 61 67 169 Housing and urban development 54 27 45 45 348 665 Others 3/ 118 222 227 819 465 910

Source: The General People’s Committee for Planning. 1/ Include general education, higher education, and vocational and technical training. 2/ Include health and environment, and social affairs. 3/ Include agriculture, finance and building of administrative centers, among others.

8 This amount is non negligible: just for reference purposes, the Libyan minimum wage is LD250 (around US$210)

11

Table 1.2: Capital Expenditures (In percent of GDP)

1999 2003 2004 2005 2006 2007 Total 4.8 7.5 8.2 16.1 12.1 21.0

Social spending 1/ 2/ 1.1 1.9 1.9 1.7 1.4 1.9

Of which: Education 1/ 0.7 0.9 1.3 1.4 1.0 1.4

Health 0.4 1.0 0.6 0.3 0.4 0.5 Basic infrastructure (w/o Housing) 1.1 … 1.7 3.3 2.1 3.6 Of which: Power 0.6 … 1.2 2.5 1.4 2.1

Communications and Transport 0.6 0.3 0.4 0.8 0.7 1.5 Housing and urban development 0.8 0.6 0.8 0.6 3.8 5.8 Others 3/ 1.7 4.7 3.9 10.5 5.0 7.9

Source: The General People’s Committees for Finance and Planning. 1/ Includes general education, higher education, and vocational and technical training. 2/ Includes health and environment, and social affairs. 3/ Includes agriculture, finance and building of administrative centers, among others.

• Among social spending, the most salient feature was the rapid upsurge in education

investments per inhabitant to US$160 from US$43. In the health sector, however, such increase was rather modest (US$59 from US$45).

• Investment on basic infrastructuremultiplied more than four times during this period, to US$413 in 2007 from US$97 in 2004. Two-thirds of such increase corresponded to power—an increase three times the per capita level of 2004—and the rest to communications and roads transportation, whose investment multiplied almost seven times during such period.

• Building of new housing facilities led to an impressive upturn of almost 25 times over the past five years, to US$665 from US$27 per inhabitant.

• Measured in real 2003 terms, rising capital outlays followed a volatile pattern. On aggregate (per capita) terms, it fell –32 percent and 10.1 percent in years 2003 and 2006, while it grew by 37.4 percent, 155 percent and 79 percent in 2004, 2005 and 2007, respectively. A similar volatile behavior was followed by all sectors, except for health investments, which plummeted for three successive years and then mildly recovered in the last two years.9

1.26 In short, total public investments rose tripled to 21 percent of GDP in 2007, from 7.5 percent of GDP in 2003 (and more than four times 4.8 percent of GDP in 1999). While the overall increase was significant, investment in social spending remained unchanged at 1.9 percent of GDP. Not only education outlays grew modestly to 1.4 percent of GDP from 0.9 percent of GDP, but health investments halved to 0.5 percent of GDP from 1.0 percent of GDP. Again, the big winners were, in the order, housing and urban development, and basic infrastructure (especially power) (Table 1.2). 1.27 Regarding performance, the execution of the development budget also improved considerably between 2004 and 2007. In 2007, the actual/budgeted ratio rose to 92 percent, well above the 74 percent of 2004 (Table 1.3). This is the highest rate of execution achieved in more than 25 years (GPCM 2007). In doing so, Libya reached a level of public investment execution that is reasonably high by international standards. Indeed, according to the Public Expenditure and Financial Accountability (PEFA) international benchmarks, a level of execution between 5 and 10 percent deserves a “B” grade.10

9 Estimates are available from the author upon request. 10 An important caveat applies here. Actual expenditure in Libyan fiscal accounts correspond to authorized expenditure, i.e. resources available to executing projects, not to committed expenses (in accounting terms).

12

Table 1.3: Budgeted and Actual Capital Expenditures, Total, 2004-2007

Year

Budgeted Million of LD

Actual Million of LD

Actual to budget ratio

Budgeted % of GDP

Actual % of GDP

Unspent % of GDP

2004 4,839 3,581 74.0 11.1 8.2 -2.9 2005 11,105 9,597 86.4 18.7 16.1 -2.6 2006 11,356 8,924 78.6 15.7 12.3 -3.4 2007 18,507 16,939 91.5 21.0 19.2 -1.8

Sources: The General People’s Committees for Finance and Planning. 1.28 But not all sectors improved their performance in equal terms. At the sectoral level, the best performing sectors were: electricity (power), gas and water sector occupied the first position (120 percent), followed by higher education and housing (above 90 percent). In contrast, health and communication and transport occupied the last positions (below 75 percent). (Table 1.4).

Table 1.4: Budgeted and Actual Capital Expenditures per Sector, 2007 Sector

Budgeted Million of LD

Actual Million of LD

Actual to budget ratio

Budgeted % of GDP

Actual % of GDP

Total selected sectors 10,801 9,959 92.2 12.3 11.3 Education 1,339 1,229 91.8 1.5 1.4

General Education 428 355 82.9 0.5 0.4 Higher Education 685 682 99.5 0.8 0.8 Technical and Vocational Training 226 192 85.2 0.3 0.2

Health and Environmental Care 635 455 71.5 0.7 0.5 Electricity, Gas and Water 1,560 1,874 120.2 1.8 2.1 Communications and Transport 1,736 1,298 74.8 2.0 1.5 Housing and Public Utilities 5,531 5,103 92.3 6.3 5.8

Others 7,705 6,980 90.6 8.7 7.9 Of which: General Security 324 294 90.8 0.4 0.3

Financial Sector 1,495 1,193 79.8 1.7 1.4 Oil Extraction 2,803 2,803 100.0 3.2 3.2 Agriculture, Livestock and Fishing 333 313 94.2 0.4 0.4 GMR Authority 900 900 100.0 1.0 1.0 General Committee for Defense 812 812 100.0 0.9 0.9

Total 18,507 16,939 91.5 21.0 19.2

Source: The General People’s Committee for Planning. 1.29 In the meantime, the quality of the overall composition of the pipeline has also improved.Divided in four categories—(a) finished (or completed), (b) ongoing (or underway), (c) stopped (or dropped) and (d) contracted, but non-started, the situation was as follows (see Table 1.5):

• Ongoing projects neared almost half of the total number of projects contracted for all sectors. At one extreme, Electricity, Gas and Water appeared with a sizable exceptional high amount of projects underway (84 percent of their total number of sectoral projects). At the other extreme, Higher Education had the lowest percentage of ongoing projects (41 percent).

• On finished projects, about one third reported as fully completed (against 31 percent in 2006). At one extreme, again (against 38 percent in 2006—see Table A.2.11 in Volume III), Electricity, Gas and Water appeared with a sizable exceptional low amount of past projects completed in 2007 (2 percent of their total number of sectoral projects); whereas at the other extreme Health and Environment and Higher Education projects completed the highest percentage of their number of sectoral projects, with 56.8 percent and 51.4 percent respectively.

13

• Dropped projectsrepresent about 12 percent of the total number of projects (against 17 percent in 2006). The two sectors with the highest sectoral percentage of the number of projects stopped are Housing, Technical and Vocational Training, and General Education. Together, these three sectors represented 97 percent of the total number of projects dropped.

• Finally, committed, but non-started projectsrepresented about 10 percent of the total number of projects (against 14 percent in 2006). At one extreme, General Education, Electricity, Gas and Water, and Housing showed the highest percentage of projects in such situation. Together these three sectors represented 82 percent of the total number of projects ready to start. At the other extreme, Health and Communication, Transportation and telecommunications showed very small percentages of their number of projects non-started.

Table 1.5: Status of Projects per Sector, 2007 Sector

Finished Underway Stopped Not started

Total

(Number of projects) Education 2,087 2,595 495 736 5,913 General education 1,375 1,926 420 667 4,388 Higher education 481 383 9 62 935 Technical and vocational training 231 286 66 7 590

Health and Environment 412 313 0 0 725 Electricity, Gas and Water 3 115 0 19 137 Communications, Transportation and Telecommunications 230 240 20 3 493 Housing and Public Utilities 1,365 3,433 1,602 646 7,046 Total 5,448 7,951 2,193 1,635 17,227

(% of sectoral total) Education 35.3 43.9 8.4 12.4 100.0 General education 31.3 43.9 9.6 15.2 100.0 Higher education 51.4 41.0 1.0 6.6 100.0 Technical and vocational training 39.2 48.5 11.2 1.2 100.0

Health and Environment 56.8 43.2 0.0 0.0 100.0 Electricity, Gas and Water 2.2 83.9 0.0 13.9 100.0 Communications, Transportation and Telecommunications 46.7 48.7 4.1 0.6 100.0 Housing and Public Utilities 19.4 48.7 22.7 9.2 100.0 Total 31.6 46.2 12.7 9.5 100.0

(% of total) Education 38.3 32.6 22.6 45.0 34.3 General education 25.2 24.2 19.2 40.8 25.5 Higher education 8.8 4.8 0.4 3.8 5.4 Technical and vocational training 4.2 3.6 3.0 0.4 3.4

Health and Environment 7.6 3.9 0.0 0.0 4.2 Electricity, Gas and Water 0.1 1.4 0.0 1.2 0.8 Communications, Transportation and Telecommunications 4.2 3.0 0.9 0.2 2.9 Housing and Public Utilities 25.1 43.2 73.1 39.5 40.9 Total 100.0 100.0 100.0 100.0 100.0

Source: The General People’s Committee for Planning. 1.30 And at the decentralized level of execution, the performance of project execution per Shaabia—measured by the number of finished projects—improved overall with respect to the accumulated values of the 1999-2006 period, but with a great dispersion in 2007 (Figure 1.4). Those Shaabiat with the highest completion ratios—above the national threshold (of 31.6%)—represent about one third of all districts, and most of them implemented a number of projects below the national median (of 718 projects). Such evidence clearly suggests that Shaabiat managing a small number of projects have more probabilities to complete them.

14

Figure 1.4: Distribution of Finished Projects per Shaabia, 2007

1.31 On average, project completion by Shaabiats remained constant at 32 percent between 2007 and the period 1999-2006.Below, there is a more detailed analysis per sector follows, which gives a more sanguine picture, especially for the sectors covered by this study (see Table 1.6). 1.32 And the quality of the decentralized pipeline also improved among sectors. On General Education, the evidence suggests that the quality of the composition of investment projects—measured by the percentage of completion—decreased from 68 percent to 31 percent (Figure 1.5). However, this was partly offset by a rising number of projects underway, which increased from 12 to 44 percent. Not started committed projects also doubled to 15 percent, which suggests that the sector keeps new projects on hold.

Figure 1.5: Change in Project Status in the General Education Sector for Shabiaat

General Education projects (1999-2006)

Finished projects

(67.98%)

Underway projects (12.01%)

Stopped projects

(12.92%)

Not started projects (7.09%)

Source: The General People’s Committee for Planning and Annex A in Volume III.

0

500

1000

1500

2000

2500

0,0 10,0 20,0 30,0 40,0 50,0 60,0

ALR

Others

TRI

SAB

GHA

ALK

JAB

WAH

JAF

BATMER

NALBEN

Liby

a=

31.6

ALW

WAS

ALM

ALZALN

SIR

ALJ

ALG

AJD

DAR

% of total projects

To

taln

um

be

ro

fpro

ject

s

MUS

Source: The General People’s Committee for Planning

Finished31%

Stopped10%

Not started15%

Underway44%

2007

15

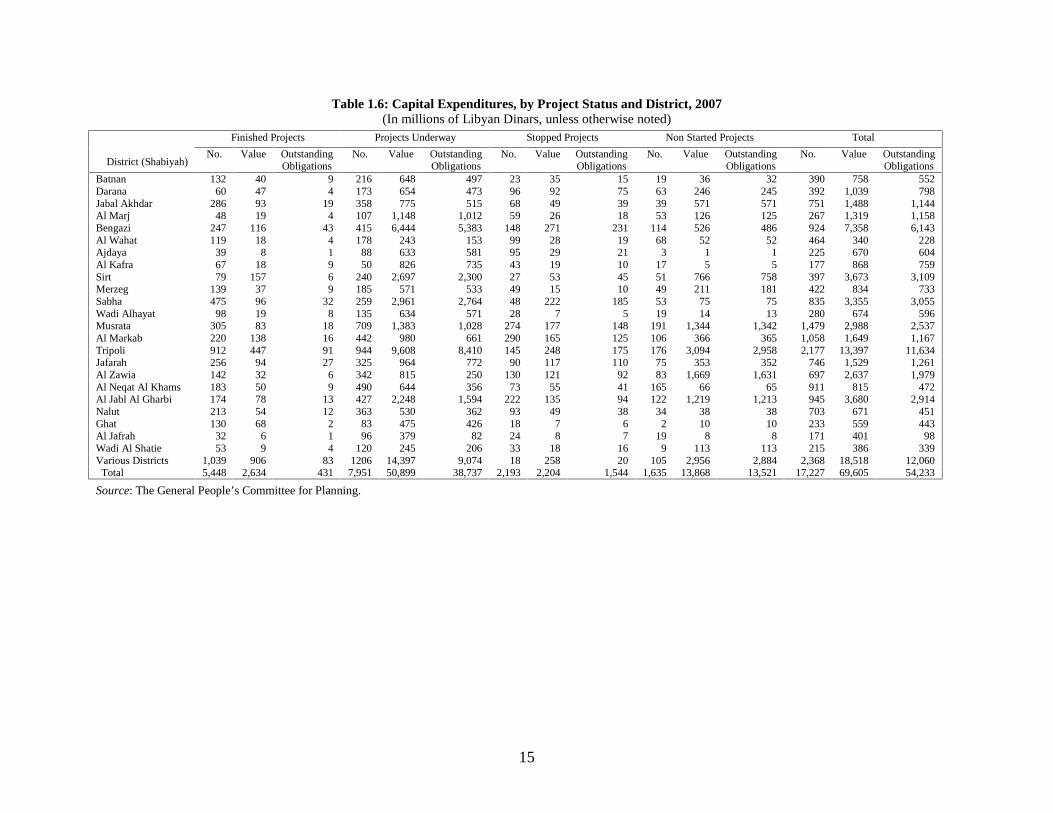

Table 1.6: Capital Expenditures, by Project Status and District, 2007(In millionsof Libyan Dinars, unlessotherwise noted)

Finished Projects Projects Underway Stopped Projects Non Started Projects Total

District (Shabiyah)No. Value Outstanding

ObligationsNo. Value Outstanding

ObligationsNo. Value Outstanding

ObligationsNo. Value Outstanding

ObligationsNo. Value Outstanding

ObligationsBatnan 132 40 9 216 648 497 23 35 15 19 36 32 390 758 552Darana 60 47 4 173 654 473 96 92 75 63 246 245 392 1,039 798Jabal Akhdar 286 93 19 358 775 515 68 49 39 39 571 571 751 1,488 1,144Al Marj 48 19 4 107 1,148 1,012 59 26 18 53 126 125 267 1,319 1,158Bengazi 247 116 43 415 6,444 5,383 148 271 231 114 526 486 924 7,358 6,143Al Wahat 119 18 4 178 243 153 99 28 19 68 52 52 464 340 228Ajdaya 39 8 1 88 633 581 95 29 21 3 1 1 225 670 604Al Kafra 67 18 9 50 826 735 43 19 10 17 5 5 177 868 759Sirt 79 157 6 240 2,697 2,300 27 53 45 51 766 758 397 3,673 3,109Merzeg 139 37 9 185 571 533 49 15 10 49 211 181 422 834 733Sabha 475 96 32 259 2,961 2,764 48 222 185 53 75 75 835 3,355 3,055Wadi Alhayat 98 19 8 135 634 571 28 7 5 19 14 13 280 674 596Musrata 305 83 18 709 1,383 1,028 274 177 148 191 1,344 1,342 1,479 2,988 2,537Al Markab 220 138 16 442 980 661 290 165 125 106 366 365 1,058 1,649 1,167Tripoli 912 447 91 944 9,608 8,410 145 248 175 176 3,094 2,958 2,177 13,397 11,634Jafarah 256 94 27 325 964 772 90 117 110 75 353 352 746 1,529 1,261Al Zawia 142 32 6 342 815 250 130 121 92 83 1,669 1,631 697 2,637 1,979Al Neqat Al Khams 183 50 9 490 644 356 73 55 41 165 66 65 911 815 472Al Jabl Al Gharbi 174 78 13 427 2,248 1,594 222 135 94 122 1,219 1,213 945 3,680 2,914Nalut 213 54 12 363 530 362 93 49 38 34 38 38 703 671 451Ghat 130 68 2 83 475 426 18 7 6 2 10 10 233 559 443Al Jafrah 32 6 1 96 379 82 24 8 7 19 8 8 171 401 98Wadi Al Shatie 53 9 4 120 245 206 33 18 16 9 113 113 215 386 339Various Districts 1,039 906 83 1206 14,397 9,074 18 258 20 105 2,956 2,884 2,368 18,518 12,060Total 5,448 2,634 431 7,951 50,899 38,737 2,193 2,204 1,544 1,635 13,868 13,521 17,227 69,605 54,233

Source: The General People’s Committee for Planning.

16

1.33 On Higher Education, despite the project completion ratio lowered from 70 to 51 percent, it remained high. In addition, the percentage of ongoing projects almost tripled from 16 to 41 percent. Finally, the percentage of dropped projects is nil, which would reflect a solid preparation (Figure 1.6).

Figure 1.6: Change of Project Status in the Higher Education Sector

Higher Education Projects (1999-2006)

Finished contracts (69.78%)

Underway contracts (15.93%)

Stopped contracts (4.95%)

Not-started contracts (9.34%)

Source: The General People’s Committee for Planning and Annex A in Volume III.

1.34 On Health and the Environment, the pattern is quite similar to Higher Education: a mildly lower percentage of projects completed, combined with the rapid increase of new ongoing projects. The ratio of underway projects increased to 41 percent in 2007, from an average of 17 percent in the period 1999-2006. The viability of health projects submitted also improved considerably as indicated by the share of stopped projects, which reached only 1 percent in 2007 (Figure 1.7).

Figure 1.7: Change of Project Status in the Health and Environment Sector

Health and environment projects (1999-2006)

Not started projects (8.80%)

Stopped projects (9.26%)

Underway projects (17.20%)

Finished projects

(64.74%)

Source: The General People’s Committee for Planning and Annex A in Volume III.

1.35 On Electricity, Gas and Water, the demand for new investment projects was highest among sectors: the share of ongoing projects surged to 84 percent from an average 19 percent during 1999-2006. There is no doubt about the large budget devoted to expanding and improving the power and water infrastructure. In the same vein, the number of dropped projects became nil, which is a positive development (Figure 1.8).

Finished

51%Under

way

41%

Not

started7%

Stopped

1%

2007

Finished51%

Stopped1%

Not started

7%

Underway41% 2007

17

Figure 1.8: Change of Project Status in the Electricity, Gas and Water Sector

Electricity projects (1999-2006)

Not started projects (4.76%)

Stopped projects

(23.81%)

Underway projects (19.05%)

Finished projects

(52.38%)

Source: The General People’s Committee for Planning and Annex A in Volume III.

1.36 On Transport and Communications, project implementation improved considerably between both dates, with parallel increases in the number of completed and ongoing projects, which suggests a rising number of projects growing in recent years. The number of stopped projects has also fell sharply to only 4 percent in 2007 (Figure 1.9).

Figure 1.9: Change of Project Status in the Transport and Communications Sector

Communication and transportation projects (1999-2006)

Not started projects

(13.93%)Stopped projects

(18.36%)

Underway projects (22.30%)

Finished projects

(45.41%)

Source: The General People’s Committee for Planning and Annex A in Volume III.

Underway48%

Not started

1%

Stopped4%

Finished47%

2007

Finished2%

Stopped0%

Not started

14%

Underway84%

2007

Chapter 2. Overall Fiscal Developments and Sustainability This chapter provides a macroeconomic background, identifies the fiscal trends and challenges, and assesses fiscal sustainability for Libya. The chapter is to a large extent based on public expenditure plans that were formulated in early 2009, a time witnessing unparalleled global financial crisis where oil prices have declined sharply from historically high levels. In 2008, record oil prices contributed to maintaining a substantially strong fiscal position. Current oil prices of $60-70 per barrel and an expected increase in oil output would still result in a surplus, albeit declining and possibly turning into a deficit as prices approach $40, in 2009 and over the medium term. Nevertheless, these plans are not consistent with sustaining a stable real per capita expenditure out of hydrocarbon wealth at oil prices below $60 per barrel. It would, therefore, be essential that any plans to increase spending, e.g. disbursements under the Wealth Distribution Program (WDP), be limited and considered within the overall sustainable expenditure envelop as defined in this chapter, in order to maintain macroeconomic stability and intergenerational equity. Deviations from the sustainable expenditure benchmarks could in fact be desirable. However, deviations should be temporary, well-justified by economic reasons, and guided by the objective of maintaining overall macroeconomic stability. In addition to maintaining sustainable levels of public expenditure, emphasis should be placed on ensuring its high quality.

I. Macroeconomic Background 2.1 Libya’s economy is dominated by the hydrocarbon sector. Libya holds the largest oil reserves in Africa, with total proven oil reserves of 43.7 billion barrels at end-2007.11 In addition, Libya has vast natural gas reserves estimated at 52.8 trillion cubic feet (Tcf), and with new discoveries, reserves will probably reach 70 Tcf to 100 Tcf.12 Overall, the sector accounts for more than 70 percent of gross domestic product (GDP), about 97 percent of foreign exchange earnings, and 90 percent of government revenue.

2.2 The economy strengthened since 2001 (Table 2.1). High international oil prices since 2004 and until recently, and a stronger performance in the non-hydrocarbon sector since the lifting of the embargo, have led to robust economic growth with real GDP growing at more than 6 percent on average.

11 National Oil Company estimates. 12 This is equivalent to 9 billion barrels of oil. With 2008 oil production (1.81 million barrels per day and natural gas production of about 1.06 Tcf per year, and assuming no new discoveries, Libya’s oil and natural gas reserves would last for about 65 years and 50 years, respectively.

Table 2.1. Libya: Real GDP Growth (in percent, period averages)

1991-95 1996-2000 2001-05 2006 2007 2008

Real GDP -0.5 1.0 6.8 5.9 6.0 3Non-hydrocarbons 1.6 3.0 8.5 7.9 9.9 8Hydrocarbons -1.2 -0.3 5.8 4.3 2.8 0

Per capita GDP in ’000 dollars 7.0 6.9 5.7 9.5 11.814.5CPI inflation (average) 9.5 2.2 -3.4 1.4 6.2 10.4Oil export price (US$/barrel) 1/ 16.9 18.9 32.9 62.5 69.3 96.7

Source: Libyan authorities; and Fund staff estimates.

1/ Libya’s oil export price is approximately three percent below the WEO international petroleum price.

19

2.3 The external current account surplus increased substantially in recent years due to high oil exports. With growing export revenues and falling imports—mainly due to the constraining effect of the sanctions—Libya’s current account surplus increased during the 1990s (Table 2.2). Buoyant oil revenue has led to large surpluses in the external current account, which reached 41 percent of GDP in 2008. The rise in oil receipts more than offset the increase in imports, resulting in a further build up of the net foreign assets of the Central Bank of Libya (CBL) and the Libyan Investment Authority (LIA) to about $136.1 billion in 2008 (the equivalent of about 24 months of imports).

2.4 Libya’s fiscal surplus at about 25 percent of GDP in 2008. Revenue increased to 64 percent of GDP due to higher oil prices. At the same time, overall expenditure increased by 45 percent, reflecting a rapid increase in virtually all expenditure items, albeit at a slower rate than was envisioned in the budget. Current expenditures increased by about 40 percent, largely on account of spending under the WDP, which was limited to LD 3.3 billion (about 3.3 percent of GDP), compared to LD 4.6 billion approved in the budget. Capital expenditures increased by about 47 percent, reflecting spending necessary to upgrade the infrastructure.

2.5 The rapid growth in public expenditures contributed to inflationary pressures, along with higher import costs of food products. The annual consumer price index (CPI) accelerated from 1.4 percent in 2006 to 6.2 percent in 2007 (Table 2.1). Although this was largely driven by higher imported food prices, prices of nontradables also increased (for example, dwellings and transportation).13 This indicated that the rise in domestic demand mostly from increased public expenditures and the rapid growth of credit extended by specialized banks are also playing a role. In 2008, inflation accelerated further, averaging about 10 percent.

13 Libya imports more than 75 percent of its food items.

Table 2.2. Libya: Balance of Payments and Reserves (In billions of dollars, unless otherwise indicated. Period averages)

1991-95 1996-2000 2001-05 2006 2007 2008

Exports, f.o.b. 9.6 12.0 17.4 39.2 47.0 62.0Of which: Hydrocarbons 8.7 11.5 16.9 38.2 45.8 60.7

Imports, f.o.b. 7.2 5.6 7.9 13.1 17.7 21.7Current account balance 1.3 5.4 6.9 25.2 29.1 36.6

(As a percent of GDP) 4.0 14.8 19.1 44.6 40.7 40.7Overall Balance (deficit -) 0.5 1.9 5.3 19.8 20.2 16.8

(As a percent of GDP) 1.6 4.9 14.7 35.1 28.2 18.7

Gross Official reserves1/ 1.2 7.4 22.6 74.8 98.3 136.1

Source: Libyan authorities; and Fund staff estimates. 1/ From 2006 represents total foreign assets (net foreign assets + Libyan Investment Authority

Table 2.3. Libya: Central Government Finances (In percent of GDP, period averages)

1991-95 1996-2000 2001-05 2006 2007 2008

Revenue 29.6 36.8 50.0 62.4 60.8 6Hydrocarbon 16.1 22.6 41.9 57.5 54.5 5Non-hydrocarbon 13.5 14.1 8.0 4.9 6.3

Of which: Tax 7.4 9.7 4.5 2.5 2.9Expenditure and net lending 28.9 31.5 37.6 31.0 35.33

Current 22.1 24.2 24.6 13.4 14.1 1Of which: wages 12.3 13.2 8.8 6.6 10.1 1

Capital 6.8 7.3 13.0 17.6 21.1 2Overall position (deficit -) 0.7 5.3 12.4 31.4 25.5 2Non-hydrocarbon deficit -15.4 -17.3 -29.5 -26.2 -29.0-32.7

20

2.6 Libya continues to face other economic challenges. Despite recent reform efforts, the economy remains highly dependent on oil and dominated by the public sector. There is a need to redouble the efforts to put in place an environment that is conducive to allowing the private sector to take a leading role in diversifying the economy and creating productive job opportunities for the rapidly growing labor force. To this end, there is a large scope for streamlining and modernizing the regulatory environment. It is also important to further advance financial sector reforms, building on the substantial progress achieved in recent years.

II. Fiscal Trends From 1990 Through 2007 2.7 The overall fiscal surplus reached a peak of 31 percent of GDP in 2006 due to the increase in oil prices. It then started to decline as result of the very rapid increase in capital expenditures (Table 2.3). On average, oil revenue continued to increase due to both higher prices and increased oil production. Tax revenue grew by 41 and 40 percent in 2007 and 2008, respectively, due to the ongoing reform of the tax and customs administration. Nonetheless, it declined in relation to GDP due to the sharp increase in hydrocarbon GDP in nominal terms (Figure 2.1). Overall expenditures grew by 37 percent in 2007 compared to 2006, reflecting rapid growth in both current (28 percent) and capital (45 percent) outlays. The same trend continued in 2008 where expenditures increased by 45 percent with current and capital expenditure growing at 42 percent and 47 percent, respectively. The level of public expenditure in recent years was sustainable under the high oil prices prevailing until end-2008. As the next section illustrates they became unsustainable as oil prices declined. Even when these high levels were sustainable, questions were raised about the challenge to maintain the quality of public expenditure in view of its very rapid growth rate. This challenge would be substantial for the administrative capacity of any country, whether it is developing or developed.

2.8 While the overall fiscal surplus remained substantial, the non-hydrocarbon deficit increased. This is due to the rapid growth in overall expenditures and the growing importance of oil revenue to the budget. The share of hydrocarbon revenue in the budget has been increasing over time, especially in the past two years when its share of total revenue increased from an average of 53 percent during 1990–95 to 83 percent during 2001–05, and to 90 percent in 2007 and 2008 (Table 2.4 and Figure 2.2).

2.9 The composition of government spending is shifting towards more capital expenditures. While it remained stable at around 23 percent of total expenditures throughout the 1990s, capital expenditures almost tripled, reaching around 60 percent of total expenditures by 2007 and 2008 (Table 2.4 and Figure 2.2). This largely reflected the priority the authorities placed

Table 2.4. Libya: Hydrocarbon Revenue, Current and Capital Expenditures1/

(In percent of budget, period averages)

1991-95 1996-2000 2001-05 2006 2007 2008

Hydrocarbon revenue 53.1 60.7 82.6 92.2 89.7 89.7Tax revenue 25.5 26.9 10.1 4.0 4.8 4.8Current Expenditure 76.5 76.6 64.7 43.2 40.1 39.2

Of which: wages 42.6 42.0 23.5 21.3 23.7 17.3Capital Expenditure 23.5 23.4 35.3 56.8 59.9 60.8Sources: Libyan Authorities; and Fund staff estimates.1/ Revenue is expressed as a percent of total revenue and expenditure as a percent ot total expenditure

21

on upgrading the infrastructure. In 2009, overall public expenditure is expected to show a small decline despite the projected decline in oil revenue by almost 40 percent. Current expenditure is

envisaged to increase by about 25 percent, mostly on account of transfers related to the Economic and Social Development Fund (ESDF) and a 16 percent projected increase in the wage bill. Capital expenditure is expected to decline by 20 percent, consistent with the authorities’ policy to rationalize public investment. This a positive development in view of the very rapid increase in recent years and the country’s implementation capacity as mentioned above. It is, however, important to focus on improving the quality of expenditure.

III. Fiscal Sustainability Analysis

2.10 The main indicator usually used for assessing the fiscal sustainability in hydrocarbon-producing countries is the non-hydrocarbon primary fiscal balance (NHPB) relative to the non-hydrocarbon GDP (NHGDP).14 During high oil prices, governments may decide to spend the revenue windfall and still end up with an apparently improving fiscal position. This could be the case, when the analysis is inappropriately focused on the overall fiscal position, even when expenditures reach unsustainable levels. The NHPB is therefore a better indicator for assessing the fiscal stance in such cases. For Libya, the NHBP shows a steadily increasing deficit relative to the nonhydrocarbon GDP since 1990. The nonhydrocarbon deficit widened from an average of about 16 percent of GDP in 1990-95 to almost 33 percent in 2008. This constituted a substantial widening of the non-oil deficit (Table 2.3). In addition to the obvious concerns this situations raises about the quality of expenditure and the implications for inflation, concerns regarding long term fiscal sustainability have become pressing in view of the recent decline in oil prices.

14 The NHPB is the overall balance excluding oil and interest-related earnings or payments.

Figure 2.1. Libya: Composition of Budgetary Revenue

(In percent of GDP, period averages)

0

10

20

30

40

50

60

70

1991-95 1996-2000 2001-05 2006 2007 2008

Hydrocarbon revenueNon-hydrocarbonTax revenueRevenue

Source: Libyan authorities; and Fund staff estimates.

Figure 2.2. Libya: Hydrocarbon Revenue, Current and Capital Expenditures (In percent of total, period averages)

0

10

20

30

40

50

60

70

80

90

100

1991-95 1996-2000 2001-05 2006 2007 2008

CurrentCapitalHydrocarbon Revenue

Source: Libyan authorities; and Fund staff estimates.

22

2.11 High oil prices represent both an opportunity and a challenge for Libya, like other oil-producing countries. With the surge in oil revenues, the fiscal position improves and governments can increase their spending to satisfy current economic needs and invest in economic development. However, hydrocarbon resources are nonrenewable. In the long term, policymakers have to consider the exhaustibility of these resources, the uncertainty of their future value, and in turn the implication for intergenerational equity and fiscal sustainability. The exhaustibility of resources also raises the importance of the quality of expenditure, as this expenditure in this case should be considered a transformation of wealth from a mineral form to other forms that need to be of high quality.