société générale beyond europe conference

TRANSCRIPT

1

Forward Looking StatementForward Looking Statement

This presentation includes forward-looking statements or statements about events or circumstances

which have not occurred. We have based these forward-looking statements largely on our current

expectations and projections about future events and financial trends affecting our business and our

future financial performance. These forward-looking statements are subject to risks, uncertainties and

assumptions, including, among other things: general economic, political and business conditions,

both in Brazil and in our market. The words “believes,” “may,” “will,” “estimates,” “continues,”

“anticipates,” “intends,” “expects” and similar words are intended to identify forward-looking

statements. We undertake no obligations to update publicly or revise any forward-looking statements

because of new information, future events or other factors. In light of these risks and uncertainties,

the forward-looking events and circumstances discussed in this presentation might not occur. Our

actual results could differ substantially from those anticipated in our forward-looking statements.

3

100th Phenom 100 jet delivered.

Business Highlights Business Highlights

Legacy 450 and 500 program development on track. In April, first metal

cut for the first Legacy 500 prototype.

Confirmed the sale of 20 EMBRAER 190 jets for Austral.

First deliveries of two EMBRAER 170 jets to Gulf Air, the national carrier from the Kingdom of Bahrain.

Sale and delivery of a Legacy 600 to the Government of Panama.

First four Super Tucano delivered to Ecuador Air Force.

Landmark development contract for KC390 aircraft. Development program at the final phase of preliminary studies.

Phenom 300 certification on schedule, meeting or surpassing all of its performance goals.

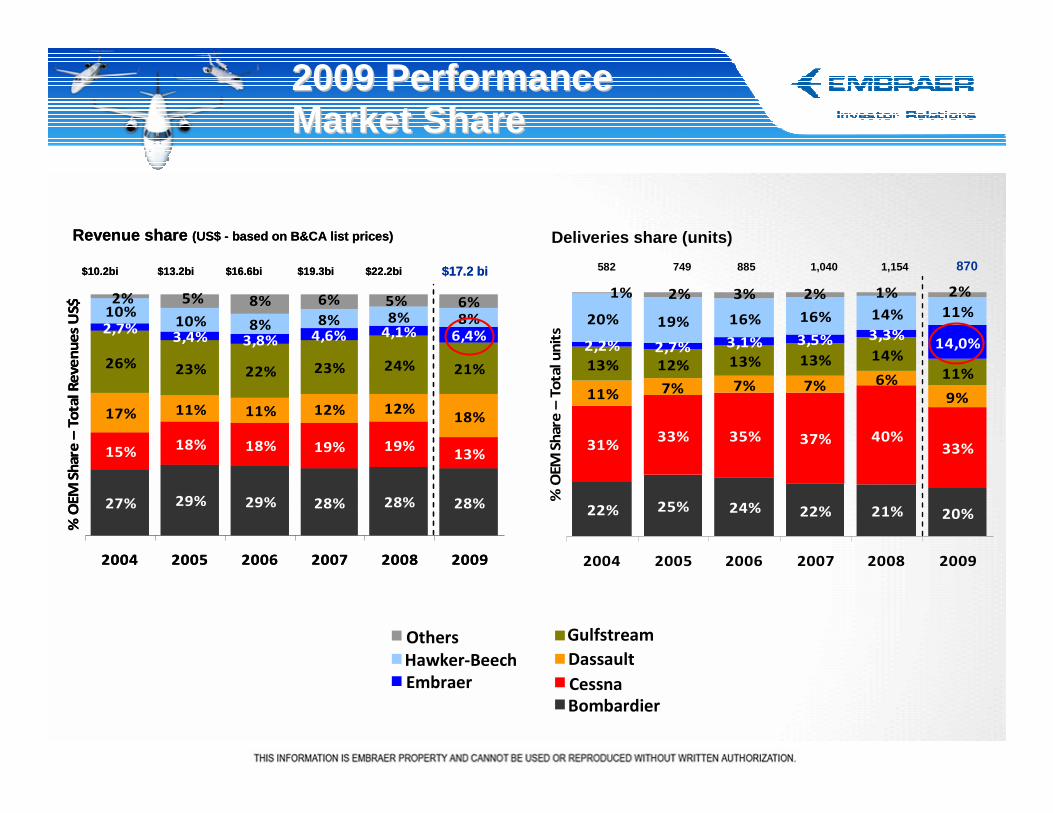

Embraer’s market share in the bizjet market increased from 3% to 14% (deliveries) and 4% to 6.5% (revenues).

4

Financial HighlightsFinancial Highlights

Jet deliveries: 41 aircrafts - 21 commercial jets, 19 executive jets and 1 aircraft for defense.

Net revenues of US$ 990 million. Defense and aviation services positively impacting gross margin.

EBIT of US$ 57 million and EBIT margin of 5.8%, in line with the 6% guidance.

Backlog at US$ 16.0 billion or 3.2 years of annual revenues.

EBITDA margin of 8.1%, above the 7.5% projection for the year.

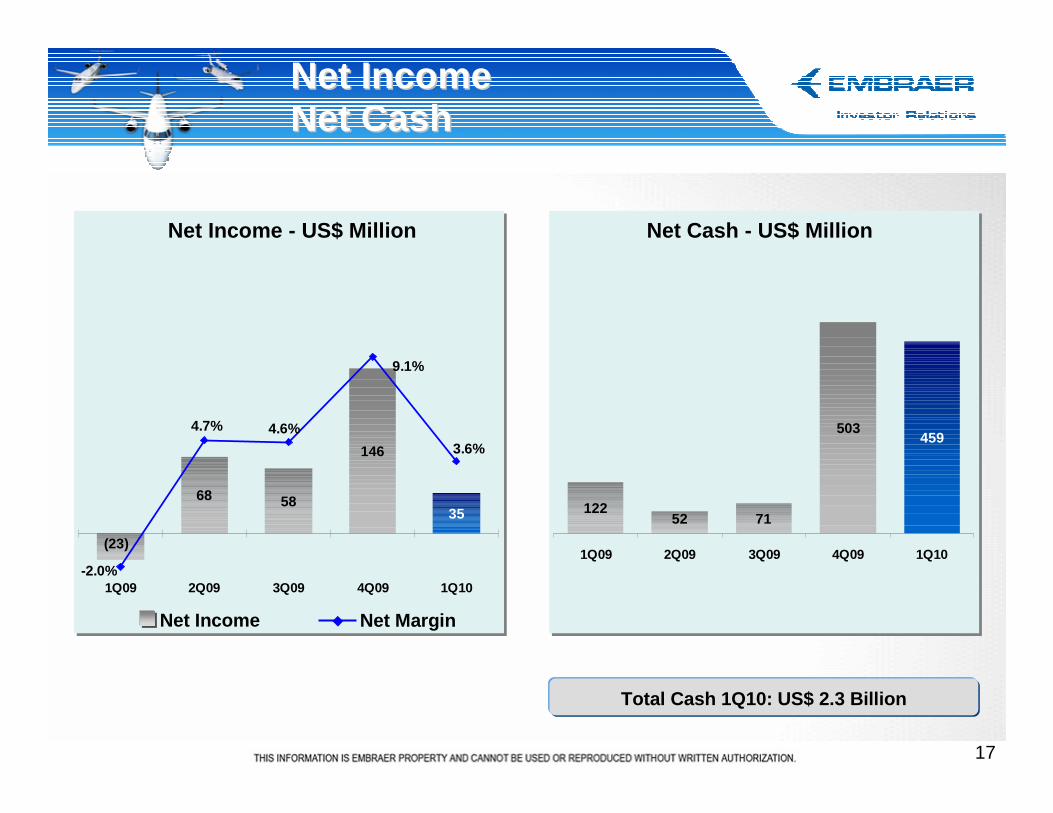

Solid net cash of US$ 459 million.

Net income of US$ 35 million and EPS - ADS of US$ 0,1952.

All operational targets achieved in 2009.

20% reduction of SG&A in 2009.

Jet DeliveriesJet Deliveries

2010 projected deliveries • 90 commercial jets• 17 Legacy / Lineage• 120 Phenom

5

3441

35 36

615

22

55

1724

1Q09 2Q09 3Q09 4Q09 1Q10

PhenomCommercial Jets, Legacy and Lineage

6

Firm Order BacklogFirm Order Backlog

US$ Billion

4.16.4

11.4 10.79.0

10.6 10.1 10.4

14.8

18.816.6 16.0

20.9

2.2 2.3

3.94.2 4.2

3.12.6 2.8 2.8 3.0

3.83.3 3.2

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 1Q10

Firm Order Backlog Backlog/Revenue (Years)

7

Revenue by SegmentRevenue by Segment

Commercial aviation Executive aviation OthersAviation servicesDefense

75%67% 66%

44%53%

6%7% 6%

16%

19%

6% 14% 16%26%

12%

11% 10% 10% 11% 14%

3% 2%2% 2%2%

1Q09 2Q09 3Q09 4Q09 1Q10

Global BusinessGlobal Business

� Operations in Brazil, USA, Europe and Asia

� Dual listed in Brazil’s Bovespa (1989) and NYSE (20 00)

Melbourne*

Fort Lauderdale

Nashville

USA

Taubaté

Botucatu

Gavião Peixoto

São José dos Campos

Brazil

Évora*

Alverca

Portugal

Le Bourget

Villepinte

France

Harbin

Beijing

China

Singapore

Singapore

Countries of Operation Factories Offices Service Centers Contracted/ Planned Authorized Network* Under construction

� One of Brazil’s largest exporters of manufactured g oods

� Diversified customer-base across five continents

Product PortfolioProduct Portfolio

capacity: 70 to 80 seatsrange: 2,100 nm (3,900 Km)

capacity: 78 to 88 seatsrange: 2,000 nm (3,700 Km)

capacity: 98 to 114 seatsrange: 2,400 nm (4,500 Km)

capacity: 108 to 122 seatsrange: 2,200 nm (4,100 Km)

capacity: 37 seatsrange: 1,750 nm (3,250 Km)

capacity: 50 seatsrange: 1,550 nm (2,900 Km)

capacity: 50 seatsrange: 2,000 nm (3,700 Km)

capacity: 44 seatsrange: 1,650 nm (3,050 Km)

Worldwide DistributionWorldwide Distribution

Diversified Customers Across 5 Continents

Asia Pacific /China

14%

Middle East /Africa

21%

Europe / CIS

33%

LatinAmerica

17%

NorthAmerica

15%

Firm Orders

Asia Pacific / China

14%

Middle East / Africa

9%

Europe / CIS

21%

NorthAmerica

44%

Latin America12%

Embraer Bombardier

Sukhoi Boeing Airbus

Antonov

Comac

Mitsubishi

Commercial Jets Market Share Evolution Worldwide

0%

15%

30%

45%

60%

75%

1995 1997 1999 2001 2003 2005 2007

Considering Accumulated Firm Orders:

30-120 Seats Jets

47%42%

3%2%2%2%1%1%

Product PortfolioProduct Portfolio

Large

Aircraft Model

Phenom 100

Phenom 300

Legacy 450

Legacy 500

Legacy 600

Lineage 1000

Seats / Range

4 / 1,160 nm

6 / 1,800 nm

4 to 8 / 2,200 to 2,300 nm

4 to 8 / 2,800 to 3,200 nm

10 to 14 / 3,250 nm

13 to 19 / 4,400 to 4,500 nm

Entry

Light

Mid-light

Mid-size

Ultra-large

Super Mid-Size

Certified: 2008

Certified: 2009

Expected Certification: 2013

Certified: 2000

Certified: 2008

Expected Certification: 2012

Ultra-Long Range

Competitors

• Cessna - MustangCJ1+

• Cessna - CJ3• Hawker - H400XP

• Bombardier -Lear 60XR

• Cessna - XLS+

• Cessna - Sovereign• Hawker - H900XP

• Bombardier -Challenger 300/605

• Dassault – Falcon2000EX/LX

• Airbus - A318 Elite

Legacy 650 10 to 14 / 3,900 nmExpected Certification: 2010

• Bombardier –Global XRS

• Gulfstream – G550

2009 Performance 2009 Performance Market ShareMarket Share

22% 25% 24% 22% 21% 20%

31%33% 35% 37% 40%

33%

11% 7% 7% 7% 6%

9%

13% 12% 13% 13% 14%

11%

2,2% 2,7% 3,1% 3,5% 3,3%14,0%

20% 19% 16% 16% 14% 11%

2%2%3%2%1% 1%

2004 2005 2006 2007 2008 2009%

OEM

Sh

are

– T

ota

l u

nit

s

Deliveries share (units)

1,040885749 1,154582 870

27% 29% 29% 28% 28% 28%

15%18% 18% 19% 19%

13%

17% 11% 11% 12% 12%18%

26% 23% 22% 23% 24% 21%

2,7%3,4% 3,8% 4,6% 4,1% 6,4%

10%10% 8% 8% 8%

6%8%

6%8% 5%5%2%

2004 2005 2006 2007 2008 2009

% O

EM

Sh

are

– T

ota

l R

eve

nu

es

US$

$13.2bi$10.2bi $17.2 bi$16.6bi $19.3bi $22.2bi

Revenue share (US$ - based on B&CA list prices)

27% 29% 29% 28% 28% 28%

15%18% 18% 19% 19%

13%

17% 11% 11% 12% 12%18%

26% 23% 22% 23% 24% 21%

2,7%3,4% 3,8% 4,6% 4,1% 6,4%

10%10% 8% 8% 8%

6%8%

6%8% 5%5%2%

2004 2005 2006 2007 2008 2009

% O

EM

Sh

are

– T

ota

l R

eve

nu

es

US$

$13.2bi$10.2bi $17.2 bi$16.6bi $19.3bi $22.2bi

Revenue share (US$ - based on B&CA list prices)

Others

Hawker-Beech

Embraer

Gulfstream

Dassault

Cessna

Bombardier

TRANSPORTTRANSPORTTRANSPORTTRANSPORT

Product PortfolioProduct Portfolio

FFFF----5 BR5 BR5 BR5 BR

Aircraft ModernizationAircraft ModernizationAircraft ModernizationAircraft Modernization

• Currently in “Preliminary Design Phase”

• Market Forecast 2025: 700 aircraft / US$ 50+ bi

EMBRAER KCEMBRAER KC --390390

• New tactical military transport aircraft

• Payload: 19 ton / Range: 1,450 nm (2,685 km)

• Contract signed with Brazilian Air Force in April 2 009

15

Net Revenue Net Revenue SG&A ExpensesSG&A Expenses

Net Revenue/Gross Margin - US$ Million

Net Revenues Gross Margin

SG&A Expenses - US$ Million

Selling Expenses G&A Expenses

1,1541,457

1,2461,610

990

18.2% 23.1% 18.8%20.8% 21.7%

1Q09 2Q09 3Q09 4Q09 1Q10

2010 Guidance: Net revenues - US$ 5.0 billion

121

66 74 7392

3747 52

55

35

86

1Q09 2Q09 3Q09 4Q09 1Q10

103

121 125

147

16

Income from OperationsIncome from OperationsEBITDAEBITDA

Income from Operations - US$ Million

Income from Operat. Operating Margin

EBITDA - US$ Million

EBITDA EBITDA Margin

2010 Guidance:EBIT - US$ 300 millionEBIT margin - 6.0%

27

175

68 66 57

5.8%

4.1%5.5%

12.0%

2.4%

1Q09 2Q09 3Q09 4Q09 1Q10

2010 Projection:EBITDA - US$ 375 million EBITDA margin - 7,5%

47

196

90 89 80

13.5%

7.2%5.6%

8.1%

4.1%

1Q09 2Q09 3Q09 4Q09 1Q10

17

Net IncomeNet IncomeNet CashNet Cash

Net Cash - US$ Million

12252 71

503459

1Q09 2Q09 3Q09 4Q09 1Q10

Net Income - US$ Million

Net Income Net Margin

35

146

5868

(23)

3.6%

9.1%

4.6%4.7%

-2.0%1Q09 2Q09 3Q09 4Q09 1Q10

Total Cash 1Q10: US$ 2.3 Billion

18