socioeconomic assessment of wyoming - sheridan media · socioeconomic assessment of wyoming ......

TRANSCRIPT

Socioeconomic Assessment of Wyoming

Prepared by: Economically Needed Diversity Options for Wyoming (ENDOW) Executive Council

Submitted to:Honorable Matt Mead, Governor of Wyoming

Joint Minerals, Business, and Economic Development Interim Committee

August 30, 2017

ENDOW Socioeconomic Report | A Letter from the ENDOW Executive Council P a g e | i

August 30, 2017 Dear Governor Mead and Members of the Joint Minerals, Business and Economic Development Interim Committee, Senate Enrolled Act No. 64 (2017 General Session) requires the Economically Needed Diversity Options for Wyoming (ENDOW) Executive Council (Council) to submit an exhaustive assessment of socioeconomic data. This report provides baseline information for preliminary recommendations to be provided later this year and for Wyoming’s 20-year economic diversification strategy. This report is a sector-by-sector analysis of Wyoming’s industries. These analyses, originally prepared for the Council, have been evaluated and enhanced by business representatives and include national trends, peer state comparisons, workforce data, barriers, enablers and opportunities. Honing into key sectors and specific industries, with the input of the private sector, will help us better understand how to position our workforce, infrastructure, marketing and innovation efforts. We are steadfastly optimistic. We have heard inspiring stories of Wyoming natives who left to pursue education or careers, only to return home later for fulfilling jobs or to establish and expand businesses while enjoying Wyoming’s lifestyle. In addition to pharmaceutical production and groundbreaking biomedical research, Council members have visited large manufacturing facilities as well as small batch, niche manufacturers adding value to our resource base. We have seen the value when high school robotics programs connect with computer machining and firms manufacturing high-tech instruments. The intersection of technology, creativity, engineering and education at makers’ spaces is inspiring. Whether it is virtual reality, unmanned aircraft, high-tech fabrics, or the production of industrial equipment for a global economy — there is existing sector diversity and foundational successes upon which Wyoming can build a viable and diverse economic future. Our work to date has identified areas where more can be done as part of a successful 20-year economic diversification strategy. They include:

• We need to do more to promote and celebrate our successes. There are many uniquely Wyoming stories to tell — ones that will attract other innovative and forward-thinking individuals and inspire Wyoming’s future generations. We need to trumpet these success stories far and wide.

• Wyoming has great accolades in terms of the number of business startups. Wyoming’s past economic development planning, however, has not focused enough on innovation and entrepreneurship. We are near the bottom in terms of attracting venture capital and need to turn that around. Accessing federal research and development funding and transferring technologies from the University to commercialization activity need improvement. The Council is looking at how to attract, grow and inspire entrepreneurs and provide them the space, capital, support, expertise and mentorship they need to solve the world’s problems.

• The Council needs to better understand the role each sector plays in Wyoming’s economy. This includes non-profit organizations, which generate a significant amount of economic and community activity.

• Wonderful Wyoming towns invite visitors offering scenic byways and good amenities. These communities need more development to foster long-term growth. We must focus on people and take to heart what a Sheridan business leader told us, “Our job is not about recruiting businesses, it is about recruiting people.” Housing, community amenities and jobs for spouses are critical to attracting and retaining talent. For a world-class base of workers and entrepreneurs, we must have vibrant and

ENDOW Socioeconomic Report | A Letter from the ENDOW Executive Council P a g e | ii

healthy communities. Key areas include access to health care, housing, attractive downtowns, air service and high-speed internet connectivity. The Council has created subgroups focused on barriers to advancement.

• Workforce is the single greatest inhibitor – and opportunity – for growth and stability. We must accept that encouraging reasonable population growth is necessary and can be achieved in a way that does not compromise our customs, culture or quality of life. The University of Wyoming and Wyoming’s seven community colleges are tremendous assets. They will be integral to providing our workforce better access to cutting-edge training opportunities to respond to a changing economy. Employers tell us we can do more to educate our youth about life skills such as teamwork, leadership and financial literacy. The Council is evaluating workforce solutions using apprenticeship, internship and mentorship as well as specific certification and licensing programs.

• Wyoming currently ranks among the top ten states in annual K-12 per-pupil spending (currently

about $17,000 per student), increasing 62 percent from 2005 to 2015. More than 92% of

Wyomingites 25 and older have earned at least a high school diploma. On a percentage basis, we

graduate fewer students with bachelor’s degrees and Wyoming’s service-producing industries

contribute less to our economy than our peer states or the nation. Educational readiness (pre-

kindergarten through post-secondary) and educational achievement need improvement.

• The Aeronautics Division of the Wyoming Department of Transportation has assembled a workgroup, which includes representation by Council members, to address commercial air service. Commercial air service is a significant limiting factor in expanding and diversifying Wyoming’s economy. Without it, we will be unable to effectively recruit or retain entrepreneurs and businesses that need quick access to markets and customers. An ENDOW Advisory Board member refers to it as “the billion-dollar problem” affecting all rural America. There appears to be no nationwide fix and states will be competing for a limited number of opportunities to solve this problem. Wyoming must be more aggressive in finding solutions to air service.

• Wyoming has invested in the Unified Network. This is a 100-gigabit, redundant, statewide network. Additionally, Wyoming ranks first in the nation in classroom broadband connectivity. We can do more. Internet accessibility has emerged as a barrier to economic advancement and diversification and has been highlighted in community testimonials and the attached socioeconomic report. It is a complex topic and the Council is in the process of evaluating many issues, including: access, speeds, regulatory barriers, and innovative solutions.

• The Wyoming Business Council, Department of Workforce Services, local economic developers, the University of Wyoming and our community colleges have achieved positive results. We can better align the multitude of well-intentioned economic development efforts across and within agencies to produce greater impact and focus. We are learning about agencies’ operations, funding, and how we can coordinate efforts to reduce duplication and integrate programs.

To achieve our goals, Wyoming must be prepared to address current economic circumstances – low growth, lack of diversification, and troubling population trends (e.g., outmigration and aging), while preparing for future challenges presented by a changing global economy and technological advancements. Further, our approach must be different than in the past. Joe Schaffer, Ed.D, President of Laramie County Community College states it well, “Doing the same things over and over with the same results has not served Wyoming well.” The Council is aware and sensitive to past efforts to revitalize Wyoming’s economy. The Council is keen to create benchmarks by which we can measure our outcomes.

ENDOW Socioeconomic Report | A Letter from the ENDOW Executive Council P a g e | iii

By focusing on outcomes, we believe we will be able to develop a strategy that fosters a diversified and sustainable state economy. If we have the political and cultural will to think differently and make the proper investments, we can increase Wyoming’s prosperity and economic diversification.

Sincerely,

Greg Hill, Chair Bill Schilling, Vice Chair

ENDOW Socioeconomic Report | ENDOW Executive Council Members P a g e | iv

ENDOW Executive Council Members

• Greg Hill of Wilson – President and Chief Operating Officer of Hess Corporation, Governor’s Designee and Co-Chair of ENDOW

• Bill Schilling of Casper – Executive Director of Leadership Wyoming. Vice-Chair of ENDOW • Jesus Rios of Sheridan – CEO of Ptolemy Data Systems • Rosie Berger of Big Horn – Former Legislator • Karen Hostetler of Buffalo – Founder and President of Mountain Meadow Wool • Mark Christensen of Gillette – President of The MC Family of Companies and Campbell County

Commissioner • Jerad Stack of Casper - Entrepreneur and Founding Member of Breakthrough 307 • Wally Wolski of Yoder - Goshen County Economic Development Corporation and Goshen County

Commissioner • Matt Kaufman of Cheyenne – Co-founder and Chairman of the Board of the Array School of

Technology and Design and Co-founder of Wyoming Entrepreneurs • Ray Fleming Dinneen of Cheyenne – Founder and Executive Director of CLIMB Wyoming • Mary Ellbogen Garland of Laramie – President and Chair of the John P. Ellbogen Foundation • John Temte of Laramie – Founder and Managing General Partner of Temte Capital • Steven Moldt of Riverton – President of Inberg-Miller Engineers • Cy Lee of Fort Washakie – Executive Director of the Wind River Development Fund • Ike Eastman of Powell – President of Eastmans’ Publishing • Bob Viola of Jackson – Founder and Director of Engineering for Square One Systems Design • Barbara Hoeft of Jackson – Managing Partner of Willow Street Group • Barbara Sessions of Afton – Vice President and CFO for Silver Star Communications • Cindy Johnson of Green River – President of the Para-Transit Division of Syncromatics • Bret Pizzato of Rock Springs – Plant Manager for J.R. Simplot • Steve Russell of Evanston – Former CEO of Carbon Fiber Technology • Senator Eli Bebout of Riverton – President of the Wyoming Senate • Representative Steve Harshman or Casper – Speaker of the Wyoming House of Representatives • Senator Michael Von Flatern of Gillette – Vice President of the Senate and Chairman of the

Senate Minerals, Business and Economic Development Committee • Representative Mike Greear of Worland – Chairman of the House Minerals, Business and

Economic Development Committee

Acknowledgements

Great appreciation is given to the staff members of the Wyoming Business Council, Governor’s Policy

Office, Economic Analysis Division, Wyoming Department of Workforce Services, University of Wyoming,

and Wyoming Community College Commission whose leadership, dedication and extensive

contributions have made this report possible.

ENDOW Socioeconomic Report |Table of Contents P a g e | v

Contents A Letter from the Economically Needed Diversification Options for Wyoming Executive Council ............ i

ENDOW Executive Council Members .......................................................................................................... iv

Socioeconomic Assessment of Wyoming ..................................................................................................... 1

Introduction ................................................................................................................................................... 1

Summary of Socioeconomic Data .................................................................................................................. 2

Demographic Trends in Wyoming ............................................................................................................. 2

Fiscal Sustainability .................................................................................................................................... 3

Industrial Sectors ....................................................................................................................................... 4

Synthesis of Sector Data ........................................................................................................................ 4

Gross Domestic Product and Employment ........................................................................................ 4

Enablers and Barriers ......................................................................................................................... 5

Assets ................................................................................................................................................. 6

Individual Sector Summaries ................................................................................................................. 7

Agriculture, Forestry, Fishing and Hunting (NAICS 11) ...................................................................... 7

Mining, Quarrying and Oil and Gas Extraction (NAICS 21) ................................................................ 8

Utilities (NAICS 22) ............................................................................................................................. 8

Construction (NAICS 23) .................................................................................................................... 9

Manufacturing (NAICS 31-33) .......................................................................................................... 10

Wholesale Trade (NAICS 42) ............................................................................................................ 11

Retail Trade (NAICS 44-45) .............................................................................................................. 12

Transportation and Warehousing (NAICS 48-49) ............................................................................ 13

Information (NAICS 51) .................................................................................................................... 13

Finance, Insurance and Real Estate (NAICS 52-53) .......................................................................... 14

Professional and Business Services (NAICS 54-56) .......................................................................... 15

Education and Health Care Services (NAICS 62) .............................................................................. 15

Leisure and Hospitality NAICS (71-72) ............................................................................................. 16

Other Services (NAICS 81) ................................................................................................................ 17

Public Administration (NAICS 92) .................................................................................................... 17

Assessment of Demographic Trends in Wyoming ....................................................................................... 19

Introduction ......................................................................................................................................... 19

Migration Trends ................................................................................................................................. 19

Race and Ethnicity ............................................................................................................................... 20

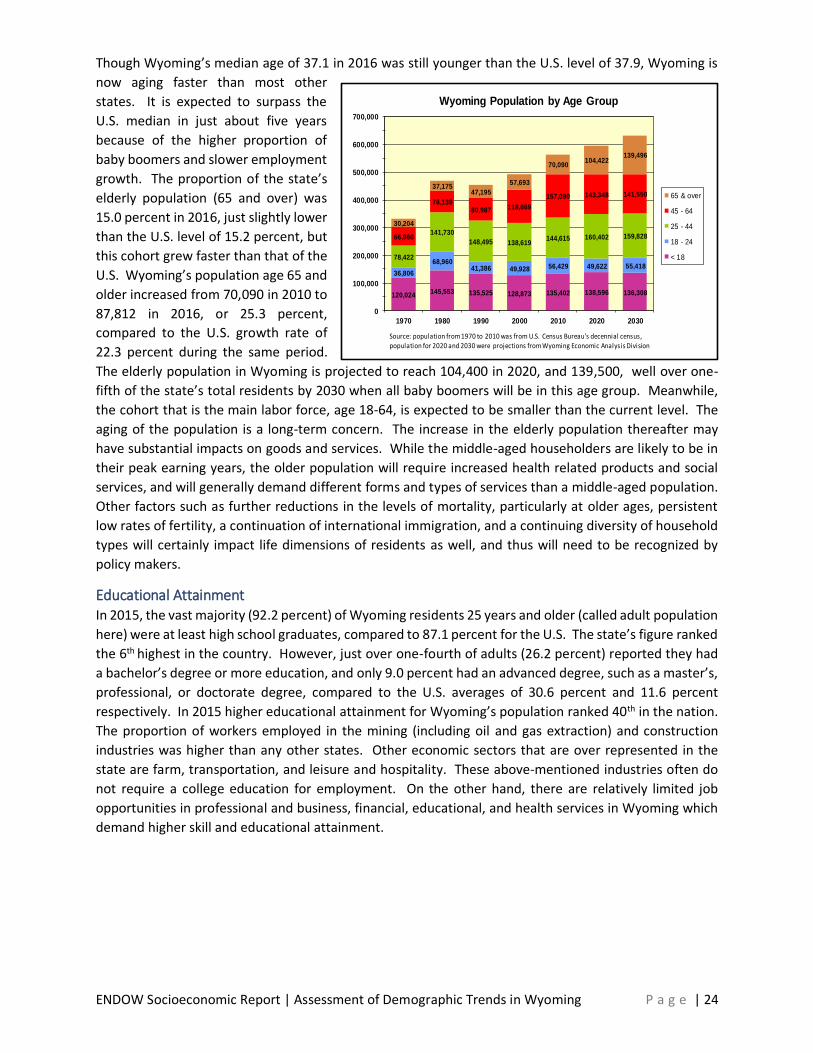

Aging Population .................................................................................................................................. 21

ENDOW Socioeconomic Report |Table of Contents P a g e | vi

Educational Attainment ....................................................................................................................... 24

Other Facts on Wyoming’s Population ................................................................................................ 25

Summary .............................................................................................................................................. 25

Examination of State and Local Fiscal Sustainability ................................................................................... 27

Appendix...................................................................................................................................................... 31

Appendix 1: Assessment of Economy by Industrial Sectors ........................................................................ 31

Agriculture, Forestry, Fishing, Hunting (11)............................................................................................. 34

Mining, Quarrying, Oil and Gas (21) ........................................................................................................ 54

Utilities (22).............................................................................................................................................. 78

Construction (23) ................................................................................................................................... 109

Manufacturing (31-33) ........................................................................................................................... 129

Wholesale Trade ( NAICS 42) ................................................................................................................. 155

Retail Trade (44-45) ............................................................................................................................... 173

Transportation and Warehousing (48-49) ............................................................................................. 188

Information (51)..................................................................................................................................... 213

Finance, Insurance, Real Estate – 52-53 ................................................................................................ 240

Professional and Business Services (54-56) ........................................................................................... 257

Education and Health Services (61-62) .................................................................................................. 284

Leisure and Hospitality (71-72) .............................................................................................................. 315

Other Services (81) ................................................................................................................................ 347

Public Administration (91) ..................................................................................................................... 349

Appendix 2: Wyoming County Profiles, 2016 ............................................................................................ 351

Socioeconomic Assessment of

Wyoming

ENDOW Socioeconomic Report | Introduction P a g e | 1

SOCIOECONOMIC ASSESSMENT OF

WYOMING

Introduction The socioeconomic assessment is the keystone foundational report of the Economically Needed Diversity

Options for Wyoming (ENDOW) Executive Council to foster discussion, understanding, evaluation and

development of a comprehensive economic diversification policy and strategy outlined in Wyoming

Statutes, (W.S.), 9-12-1401 through 9-12-1404.

This report is submitted to fulfill the statutory requirement identified in W.S. 9-12-1402 (a)(ii):

This report is presented in a high-level overview summary, followed by detailed assessments

of Wyoming’s demographic trends, fiscal sustainability and industry sectors. The review of industry

sectors (Page 4 and Appendix 1), utilizing the North America Industrial Code Schedule, (NAICS), will call

out state and national trends of new and emerging sectors and subsectors, descriptions of how

Wyoming compares to surrounding states, Alaska and the US, a description of businesses contained in

each sector, workforce characteristics, strengths and deficiencies, export market activity, asset

maps describing industry characteristics geographically, enablers, incentives and challenges to the

industry and industry expert input and comments.

Looking ahead, the ENDOW Executive Council will submit by December 31, 2017 their preliminary

findings and recommendations in the development of a comprehensive economic diversification

strategy to the Governor and Legislature per details outlined in W.S. 9-12-1402 (a)(iii) and their final

recommendations report will be submitted to the Governor for his approval by August 1, 2018 as

outlined in W.S. 9-12-1402(a)(iv).

“By August 30, 2017, prepare and submit to the Governor and Legislature through the

joint minerals, business and economic development interim committee, an exhaustive

assessment of socioeconomic data, which shall include an examination of state and local

fiscal sustainability, existing, new and emerging economic sectors and subsectors of the

economy, identification of potential business development and innovation zones, an

inventory of existing workforce strengths and deficiencies, economic trends and key

enablers for economic growth in the state and that translates to viable business

development.”

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 2

Summary of Socioeconomic Data This section presents high-level summaries of demographic trends, fiscal sustainability, and industrial

sector assessments. Please see following sections and Appendix 1 for more detailed analyses.

Demographic Trends in Wyoming 1. Nationwide, as low fertility rates continue to persist and baby boomers age, the growth of both

population and labor force is expected to be slow for the next 14 years. The average year-over-

year growth rate for the state is expected to be about 0.5 percent during the period, comparing

to 1.1 percent experienced so far since 2010.

2. Both the U.S. and Wyoming are experiencing considerable growth in older populations.

Wyoming’s total population declined about 1,000, or 0.2 percent between July 2015 and July

2016, but the population 65 and over grew 3.8 percent or 3,140 during the same period, and is

now nearly 88,000. The average annual growth rate for this older population is projected to be

3.3 percent from 2016 to 2030. The total number of residents 65 and over will reach 139,500 by

2030 when all baby boomers will be in this cohort, accounting for 22.0 percent of total population

in Wyoming. The rapid growth of elderly population will present challenges to policy makers and

programs such as Social Security, Medicare and Medicaid. It will also affect families, businesses,

and health care providers.

3. Both the nation and Wyoming’s population continue to grow in diversity. Wyoming’s total

minority population reached 93,256 in July 2016. Minority is defined as any group other than

single-race, Non-Hispanic White. The growth of minorities since 2010 was 14,090 persons, or 17.8

percent growth increase, compared with 3.9 percent increase for the state’s 2016 total

population. Nearly two-thirds of the state’s population growth from 2010 to 2016 was attributed

to the minority population. Future population increases for the U.S. will be from racial and ethnic

groups rather than the Non-Hispanic White.

4. Traditionally a rapid drop in a state’s unemployment rate is attributed to economic expansion

including strong employment growth. However, that is not the case in Wyoming since 2016. In

fact, the unemployment rate in the state has been steadily dropping since May 2016, and the

3.9% in June 2017 was the lowest value since November of 2009, pre-Great Recession.

However, the employment for June 2017 was still about 1% below employments levels one year

ago. Wyoming’s labor force continues to drop, and is estimated to be thousands less compared

to last year. Possible explanations for these phenomena are: 1) some baby boomers (age 53 to

71 in 2017) left the labor force by retiring in the state or out of the state, and 2) younger people

continue to move to other states because of the robust nationwide labor market, particularly in

Wyoming’s neighboring states. Additionally, Texas, Arizona, Oregon, and Washington are all

experiencing strong job growth. For example, Wyoming’s number one competitor (in terms of

labor force), Colorado, had the lowest unemployment rate (2.3%) while Utah had the fastest

employment growth (3.0%) in the country for June 2017. If the U.S. economic expansion

(already one of the longest in history) continues, Wyoming’s labor market will remain tight.

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 3

Fiscal Sustainability At the May 11, 2017 meeting, the ENDOW Executive Council adopted as a working definition for

fiscal sustainability the following: “a government’s ability and willingness to generate inflows of

resources necessary to honor current service commitments and to meet financial obligations as they

come due, without transferring financial obligations to future periods that do not result in

commensurate benefits.”

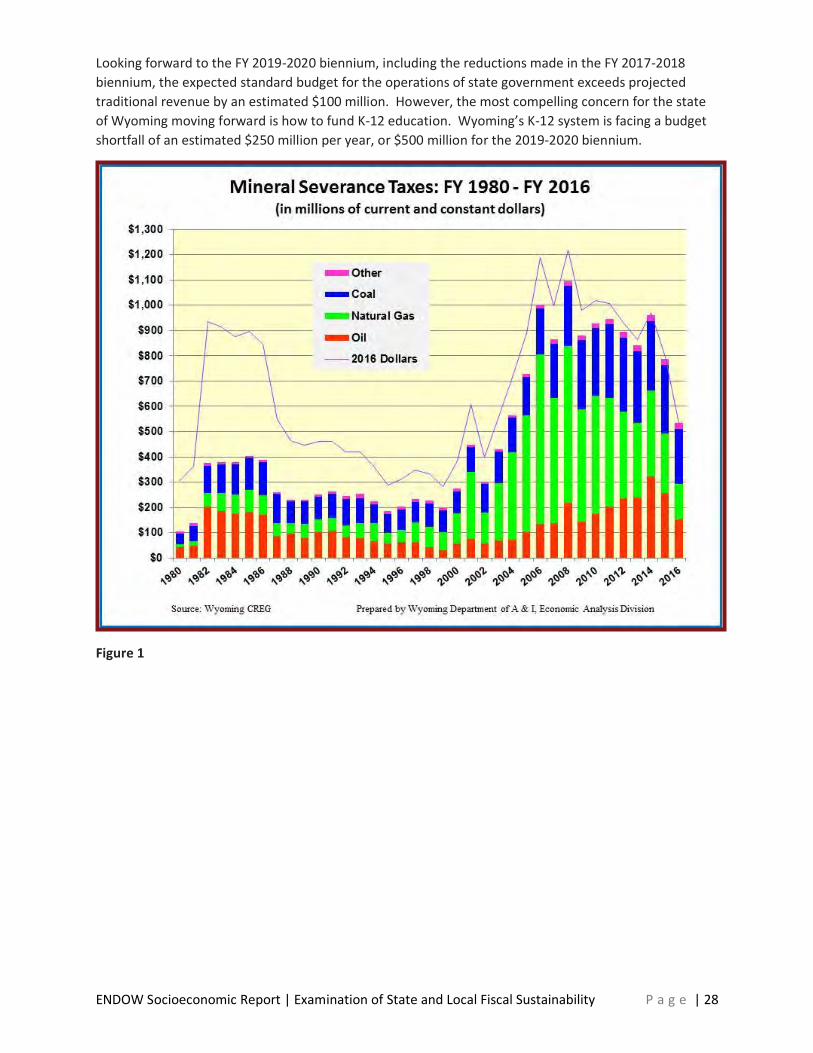

Historically, 70 percent of revenue collected by the state of Wyoming comes from the energy

mineral industry and therefore the condition of state coffers depends directly on the market value

of energy commodities that are traded on a national and international basis

Looking forward to the FY 2019-2020 biennium, including the reductions made in the FY 2017-2018

biennium, the expected standard budget for the operations of state government exceeds projected

traditional revenue by an estimated $100 million. However, the most compelling concern for the

state of Wyoming moving forward is how to fund K-12 education. Wyoming’s K-12 system is facing

a budget shortfall of an estimated $250 million per year, or $500 million for the 2019-2020

biennium.

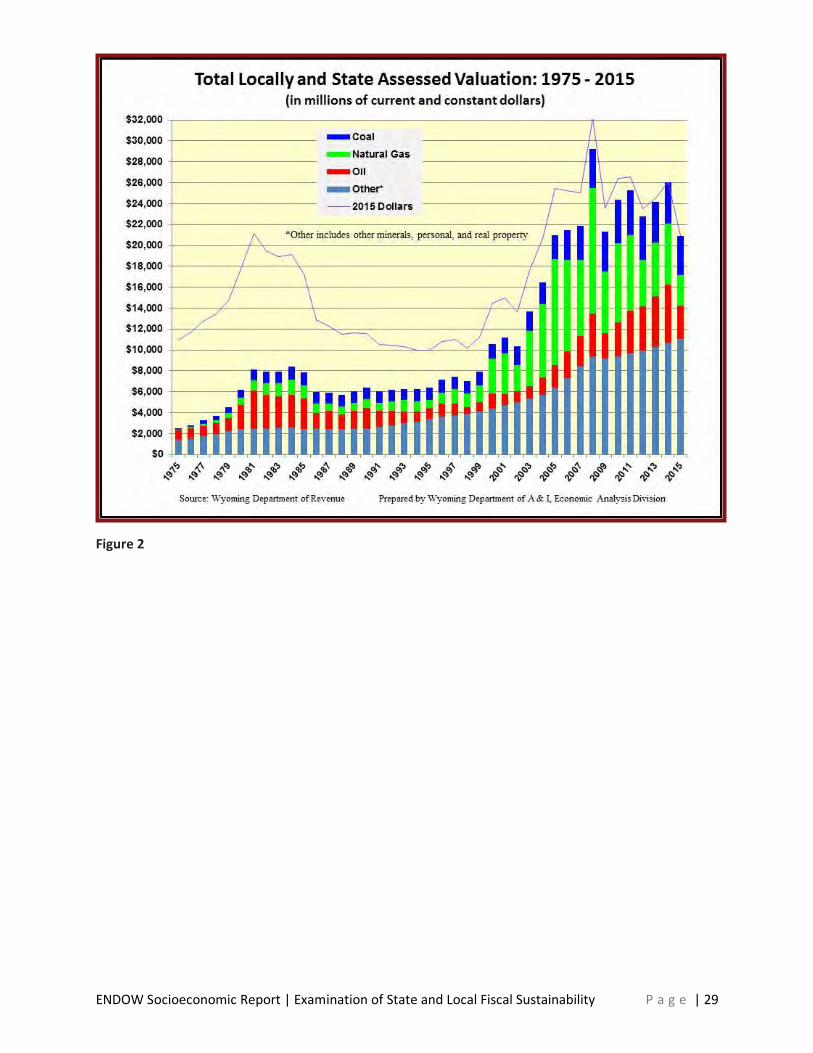

County, municipal and other local government entities were not assessed for fiscal sustainability due

time and staff limitations, but it is presumed local governments are experiencing fiscal crisis in the

same manner. Local governments’ tax base dependence on energy commodity revenues deeply

and directly affect assessed valuation for local levies and state shared revenue.

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 4

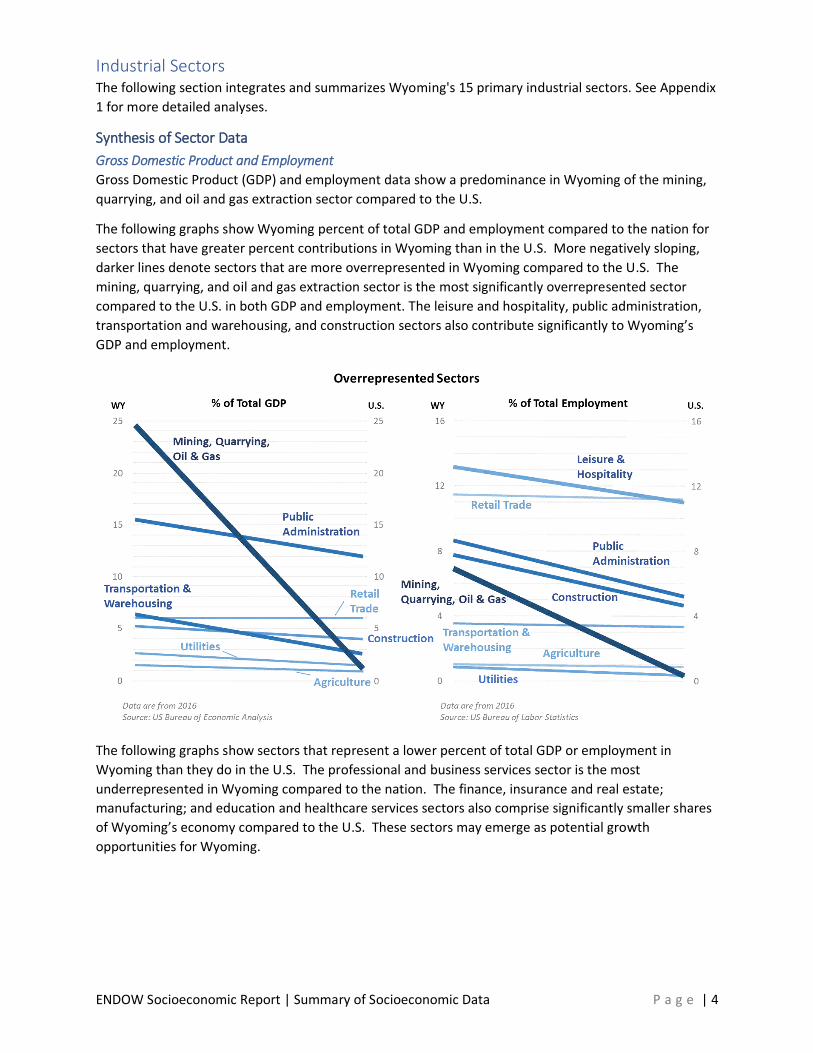

Industrial Sectors The following section integrates and summarizes Wyoming's 15 primary industrial sectors. See Appendix

1 for more detailed analyses.

Synthesis of Sector Data

Gross Domestic Product and Employment

Gross Domestic Product (GDP) and employment data show a predominance in Wyoming of the mining,

quarrying, and oil and gas extraction sector compared to the U.S.

The following graphs show Wyoming percent of total GDP and employment compared to the nation for

sectors that have greater percent contributions in Wyoming than in the U.S. More negatively sloping,

darker lines denote sectors that are more overrepresented in Wyoming compared to the U.S. The

mining, quarrying, and oil and gas extraction sector is the most significantly overrepresented sector

compared to the U.S. in both GDP and employment. The leisure and hospitality, public administration,

transportation and warehousing, and construction sectors also contribute significantly to Wyoming’s

GDP and employment.

The following graphs show sectors that represent a lower percent of total GDP or employment in

Wyoming than they do in the U.S. The professional and business services sector is the most

underrepresented in Wyoming compared to the nation. The finance, insurance and real estate;

manufacturing; and education and healthcare services sectors also comprise significantly smaller shares

of Wyoming’s economy compared to the U.S. These sectors may emerge as potential growth

opportunities for Wyoming.

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 5

Enablers and Barriers

The Executive Council has inventoried a primary list of economic enablers and barriers of businesses and

the diversification of Wyoming’s economy:

✓ Enablers for successful businesses include: low taxes, livability of communities, interstate

highway system, low level of regulatory ‘red tape’, internet connectivity, regional

collaborations, natural resources, community colleges system, many business organizations.

✓ Barriers to business success include: limited workforce in numbers and skills, limited

commercial air transportation, lack of high speed internet in rural areas, proximity to markets,

access to capital, limited health care services, and affordable health insurance.

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 6

Assets

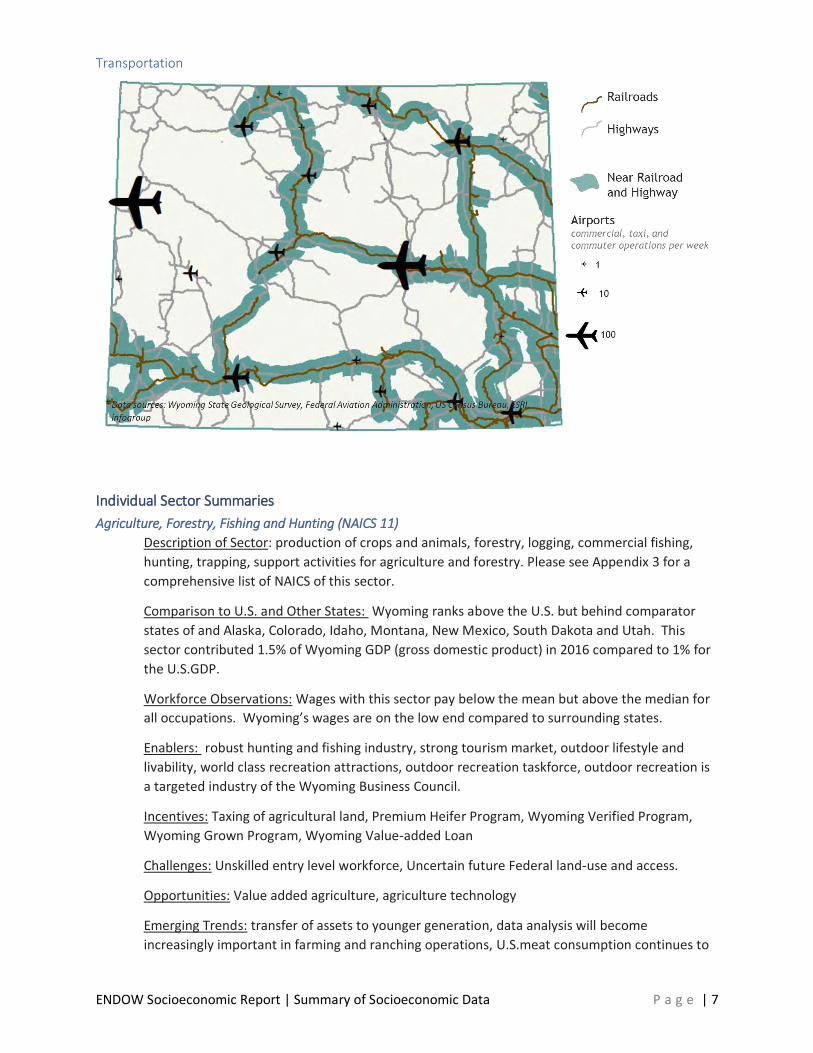

The following maps depict assets that are limiting geographic factors for more than one analyzed sector.

Workforce

The map below depicts population within 60 miles. This is used as a proxy for workforce in several

sectors, in accordance with site selector rules of thumb. According to these rules of thumb, employees

are willing to drive a maximum of ~60 miles to work, and one new employee can be drawn from every

~300 people in a population.

Broadband

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 7

Transportation

Individual Sector Summaries

Agriculture, Forestry, Fishing and Hunting (NAICS 11)

Description of Sector: production of crops and animals, forestry, logging, commercial fishing,

hunting, trapping, support activities for agriculture and forestry. Please see Appendix 3 for a

comprehensive list of NAICS of this sector.

Comparison to U.S. and Other States: Wyoming ranks above the U.S. but behind comparator

states of and Alaska, Colorado, Idaho, Montana, New Mexico, South Dakota and Utah. This

sector contributed 1.5% of Wyoming GDP (gross domestic product) in 2016 compared to 1% for

the U.S.GDP.

Workforce Observations: Wages with this sector pay below the mean but above the median for

all occupations. Wyoming’s wages are on the low end compared to surrounding states.

Enablers: robust hunting and fishing industry, strong tourism market, outdoor lifestyle and

livability, world class recreation attractions, outdoor recreation taskforce, outdoor recreation is

a targeted industry of the Wyoming Business Council.

Incentives: Taxing of agricultural land, Premium Heifer Program, Wyoming Verified Program,

Wyoming Grown Program, Wyoming Value-added Loan

Challenges: Unskilled entry level workforce, Uncertain future Federal land-use and access.

Opportunities: Value added agriculture, agriculture technology

Emerging Trends: transfer of assets to younger generation, data analysis will become

increasingly important in farming and ranching operations, U.S.meat consumption continues to

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 8

drop, Chinese meat consumption continues to rise, Genetically Modified Organism (GMO) foods

and livestock treatment are public concern issues, lumber industry will continue to be largely

controlled by housing demand and trade with Canada, biomass conversion to energy is a viable

form of alternative energy which uses the waste of logging operations.

Mining, Quarrying and Oil and Gas Extraction (NAICS 21)

Description of Sector: companies that extract oil, gas, coal, metals, gravel, other minerals and

support activities for mining and oil and gas extraction. Please see Appendix 3 for a

comprehensive list of NAICS of this sector.

Comparison to U.S. and Other States: This sector represents 30.1% of Wyoming’s GDP

compared to 1.5% for U.S.GDP.

Workforce Observations: Wages with this sector pay above the mean and median for all

occupations. Wyoming’s wages are near the average of comparator states.

Enablers: comparative advantage of natural resources, existing infrastructure built over

decades, Wyoming Infrastructure Authority, Wyomingites and public officials favor natural

resource development.

Incentives: Business Committed Grants (BCG), Large Loan Fund, Challenge Loan

Challenges: Proximity to markets, volatility of natural resource commodity prices, boom-bust

culture, boom-bust tax revenues, cost to produce renewables will become on par with fossil

fuels, advanced carbon technologies early in life cycle, speed of industrial siting process,

inefficient permitting.

Opportunities: Growing and leveraging Wyoming’s robust natural resource base to drive growth

in research and development, tech companies, manufacturing, and other underrepresented

sectors, CO2 capture and use for enhanced oil recovery, and exploration of advances in

technology.

Emerging Trends: Safety is a perennial priority for well-regarded companies in this sector, and

safety metrics are important in evaluating shareholder value. Innovations in horizontal drilling

have bolstered U.S. oil and gas production in the last decade, and have drawn some producers’

focus. to onshore plays, including those in Wyoming. In recent years, low coal, oil, gas, and

renewable prices have led to greater competition in the electricity generation market,

decreased production of traditional resources, reduced shareholder value, and significant

reductions in employed workforce. These effects can be seen in Wyoming and globally. The

downturn has also driven innovation to reduce costs and increase efficiency, and focused U.S.

producers’ attention on plays that can break even at low prices (such as the Permian Basin in

west Texas).

Utilities (NAICS 22)

Description of Sector: Electric power generation/transmission/distribution, natural gas

distribution, water supply and sewage treatment. Please see Appendix 3 for a comprehensive

list of NAICS of this sector.

Comparison to U.S. and Other States: Wyoming exceeds the national average for this sector’s

contribution by .9%. and contributed 2.6% to Wyoming’s GDP in 2016 compared to 1.7% for the

US. Above average contribution amounts to $309 million added to Wyoming’s GDP

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 9

Workforce Observations: Wages within this sector pay above the annual mean and median for

all occupations. Compared to surrounding states; North Dakota, Utah and Colorado have aa

higher annual average wage for this sector.

Enablers: Low regulation, low tax climate

Incentives: Wyoming Infrastructure Authority

Challenges: Large barriers to entry, lack of transmission capacity.

Opportunities: Increasing efficiency of existing plants, natural gas energy generation, CO2

Capture and use from gas power plants, wind energy, nuclear energy, solar energy.

Emerging Trends: Electricity generation by coal and petroleum power plants is decreasing,

nuclear has held steady and renewables and natural gas have increased. As changing technology

and regulatory uncertainty continues to plague energy generation markets, infrastructure is

aging and needs to be updated or replaced. Energy companies are very risk averse and can be

reluctant to make large capital investments as they make decisions on long term factors, with

the life of an asset lasting 50 or more years. Renewable energy sources are becoming more

viable because of decreased cost, increased efficiency and increased ability to store energy for

future use.

Construction (NAICS 23)

Description of Sector: Residential building construction, building equipment contractors,

specialty trade contractors, affordable housing, ag infrastructure upgrades, construction

machinery. Please see Appendix 3 for a comprehensive list of NAICS of this sector.

Comparison to U.S. and Other States: Wyoming is significantly ahead of the U.S. average and on

par with many surrounding states in this industry. Activities in this sector contributed 5.1% to

Wyoming’s GDP in 2016 compared to 4.0% for the US. Wyoming is .8 percentage points ahead

of South Dakota and about a half a percentage point or less behind surrounding states Colorado,

Idaho and Montana. Utah leads the northern Rocky Mountain region at 6.0%. In 2016, Wyoming

ranked 8th nationally for construction as a percentage of gross state product

Workforce Observations: Wyoming wages within this sector pay better than the mean and

median for all occupations. In Wyoming, however, wages are less than the U.S. average, but pay

more than surrounding states Colorado, Idaho, Montana, New Mexico and South Dakota.

Enablers: No corporate and personal income taxes, low sales tax, community college training

programs

Incentives: Business Committee Grants, Community Enhancement Grants, Community

Readiness Grants, Challenge Loan, Workforce Training Grants

Challenges: Lack of skilled workforce (in-state subs, etc.), availability of workforce, significant

out-of-state competition, lack of reliable job base in sufficient numbers for building more homes

for first-time home buyers, lack of appraisers in some of the smaller rural areas, and there is a

problem with replacing them, increased government regulation, as mid-size companies find it

challenging to manage the costs of compliance.

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 10

Opportunities: Encourage politicians to eliminate overlapping government regulations, outdated

regulations, and discourage the implementation of new regulations. Increase high school

recruiting efforts at national level, and provide funding to bring back industrial arts program

Emerging Trends: Collaborative approaches for projects. Labor shortages. Offsite/modular

construction. Sustainable construction. Rising construction costs. Increased legal action and

prosecution for safety violations and incidents amid a building boom. Technology – use of

augmented reality and virtual reality.

Manufacturing (NAICS 31-33)

Description of Sector: The manufacturing sector comprises companies who make products from

materials, substances, and components. These companies include food manufacturing,

beverage and tobacco manufacturing, textile mills, wood product manufacturing, petroleum and

coal products manufacturing, and many others. Please see Appendix 3 for a comprehensive list

of NAICS of this sector.

Comparison to U.S. and Other States: As a percentage of GPD, Wyoming’s manufacturing

industry ranks 43rd in the nation. Manufacturing activities contributed 5.5% to Wyoming’s GDP

in 2016 compared to 11.7% for the US. If Wyoming can close that gap the 6% difference would

add $2 billion to the state’s GDP.

Workforce Observations: Wyoming’s manufacturing workforce is much smaller than that of

comparator states and has seen a decline between 2005 and 2016. The largest portion of

Wyoming’s workforce, 47.2%, is employed in businesses related to petroleum and coal products

manufacturing, chemical manufacturing, plastics and rubber products manufacturing, and

nonmetallic mineral product manufacturing. Nationwide, only 16.5% of manufacturing jobs fall

within these business categories. Wages within this sector pay less than the national average

but more than most surrounding states, including: Idaho, Montana, New Mexico, North Dakota,

South Dakota, and Utah

Enablers: No corporate income tax, no inventory tax, low electric and utility costs, low property

and sale taxes, lower than average workers compensation and unemployment insurance taxes,

less red tape and better government transparency, Manufacturing Works, Market Research

Center, Small Business Innovation Research Center BIR Phase 0 (SBIR), Wyoming Technology

Transfer Center.

Incentives: Sales tax exemption on equipment used in manufacturing, sales tax exemption on

electricity used in manufacturing processes, BRC – build/lease/purchase option, large loan fund,

challenge/bridge loan fund, workforce training funds.

Challenges: Lack of skilled workforce, availability of workforce, workforce housing, proximity to

markets, permitting process, lack of critical mass of employment sector.

Opportunities: Opportunities in this sector include value-added agriculture, value-added

minerals, and manufacturing machines and components. Workforce training funds, sales tax

exemptions on equipment and electricity used in manufacturing process, build/lease/purchase

option, large loan fund, challenge/bridge loan fund are important enablers to this sector in

Wyoming.

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 11

Emerging Trends: U.S. manufacturing production has increased while U.S. manufacturing jobs

have declined steadily for the past 30-40 years, owing to automation, trade, or other influences.

Despite the long-term trend in employment, manufacturing jobs have been increasing slightly

since 2010, and some are optimistic about the future of U.S. manufacturing, citing innovation,

and an emergence of consumers globally.

Wholesale Trade (NAICS 42)

Description of Sector: This sector comprises establishments engaged in wholesaling

merchandise, generally without transformation, and rendering services incidental to the sale of

merchandise. The merchandise described in this sector includes the outputs of agriculture,

mining, manufacturing, and certain information industries, such as publishing. Agriculture

implements; coffee wholesaling; commercial compost; fabrics; farm product raw material

merchant wholesalers; food and beverage equipment and supplies; food hub; food products;

grocers; machinery, equipment and supplies merchant wholesalers; meat products. Please see

Appendix 3 for a comprehensive list of NAICS of this sector.

Comparison to U.S. and Other States: Wyoming lags the U.S. average and surrounding states in

this industry. Activities in this sector contributed 4.3% to Wyoming’s GDP in 2016 compared to

6.1% for the US. Surrounding states Colorado, Idaho, Montana, South Dakota and Utah ranged

from 5.1% to 7.5%. In 2016, Wyoming ranked 44th nationally for wholesale trade; it would rank

21st nationally if we grow our GDP to 6.1%.

Workforce Observations: Wyoming wages within this sector pay better than the mean and

median for all occupations. In Wyoming, however, wages are less than the U.S. average, but pay

more than some surrounding states including Idaho, Montana, New Mexico and South Dakota.

Enablers: Low sales tax, Market Research Center, Small Business Development Centers, lower

than average workers compensation and unemployment insurance, less red tape and barriers to

entry (licensing, permitting, etc.)

Incentives: Challenge/Bridge Loan Program, Tradeshow Incentive Grants

Challenges: lack of market due to low population, extremely small rural trade areas, significant

leakage to out-of-state centers, Walmart effect (big-box retail squeezing out other retail),

Amazon effect (online sales eroding traditional retail), significant competition (tradition and web

presence), unskilled entry level workforce.

Opportunities: No response from industry

Emerging Trends: ·Rise in implementation and use of connected robotics allows companies to

gain efficiency and cut costs on the customer’s factory floor, in the warehouse, and elsewhere.

Wholesale distribution companies historically spent less time and effort in developing brand

awareness to let customers know why they should choose their company; that is changing in

favor of increased brand awareness efforts. Blockchain technology is allowing companies to

make and verify transactions on networks in near real time without a central point of control. E-

commerce is morphing into digital commerce, which is not only a transaction, but a way of

doing business. This includes branding, image, customer service and transactions. The amount

of data produced today is increasing exponentially, allowing companies to analyze it and garner

new insights about customers and themselves. Distributors have a twofold opportunity to

capitalize on the internet of things. This includes sensors within the business, such as

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 12

warehousing, transportation and equipment monitoring to improve operations. To reduce

warehouse space, goods can be produced inside a mobile hub near the end customer, speeding

delivery and always being in stock. While still in the early stages, drones and driverless vehicles

will allow companies to address driver shortages, increase safety, lower shipping costs, and

more. Drone technology has potential in many trades, but those focused on construction and

similar markets can use drones to provide aerial imagery, coupled with data analytics and 3D

modeling algorithms, can provide accurate measurements and material requirements.

Retail Trade (NAICS 44-45)

Description of Sector: Motor Vehicles, Furniture, Electronics, Building Materials, Food and

Beverage, Health and Personal Care, Clothing, Gasoline, General Merchandise. Please see

Appendix 3 for a comprehensive list of NAICS of this sector.

Comparison to U.S. and Other States: Wyoming retail (5.8 percent of state GDP) trails U.S. by

just .3 percent. Closing the gap could add $103M in revenue. Wyoming trails all neighbors

(aside from Colorado, at 5.6 percent) slightly. Outliers Utah, S. Dakota and Idaho rely much more

heavily on retail for revenue. Wyoming is ahead of the U.S. in many sectors of the Retail

Industry, however finds itself notably behind in Food and Beverage (8 percent vs. 14 percent)

Health and Personal Care (5.4 percent vs 10.5 percent) and Clothing (8.8 percent vs. 12.2

percent)

Workforce Observations: Wyoming lags the U.S. in annual wages in many retail sectors,

significantly in electronics and appliances (31.7K vs 45.4K), in the industry, Wyoming finds itself

in the middle of the pack amongst its neighbors, with Colorado as an outlier on the high end of

annual wages.

Enablers: Low sales tax, Market Research Center, Small Business Development Center, lower

than average workers compensation and unemployment insurance, less red tape and barriers to

entry (licensing, permitting, etc.), strong tourism market brings new money into economy.

Incentives: Main Street Program, Main Street Loan Program, Challenge/Bridge Loan Program

Challenges: lack of market due to low population, extremely small rural trade areas, significant

leakage to out-of-state centers, Walmart effect (big-box retail squeezing out other retail),

Amazon effect (online sales eroding traditional retail), retail industry has very low margins to

begin (1%-2%), lack of consolidated information for entrepreneurs, significant competition

(tradition and web presence), unskilled entry level workforce.

Opportunities: Retail support technology, augmented reality – try before you buy clothes,

games and more, AI – chat bots, virtual agents offer customer service and support interactions o

Robotic process automation for repetitive, rules-based, high-volume tasks, food and beverage,

health and personal care and clothing sectors of retail Industry.

Emerging Trends: ·Growth will primarily come from emerging global markets. Diminishing

importance of stand-alone brick and mortar stores represents both barrier and opportunity to

small retailers, Subscription-based services – groceries, prescriptions, etc. Customers now seek

personalized brand interactions and engagements – think geotagged coupons, social media-

tailored ads, etc.

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 13

Transportation and Warehousing (NAICS 48-49)

Description of Sector: 1,200 firms averaging 9-12 years depending and employing 9,500 people

primarily in truck transportation (39 percent) but also warehousing and storage (29 percent).

See Appendix 3 for a complete list of NAICS in this sector.

Comparison to U.S. and Other States: Transportation occupies more than twice the share of

Wyoming’s GDP as it does on a national level (6.2% v. 2.8%), and 150% to 300% more than

regional neighbors. The percentage of total employment, however is more in line with regional

neighbors and nearly identical to the U.S. share.

Workforce Observations: Wages in this sector generally lag national averages, but the difference

is particularly stark in air ($36K vs $84K) and pipeline ($94K vs $122K) transportation.

Enablers: Interstate 80, Interstate 90, Interstate 25, Wyoming highway quality and performance

consistently leads nation, less government red tape and more government transparency, gas tax

competitive with surrounding states, pervious success with Sierra Trading Post, Lowes’s, and

Walmart distribution centers, wages on par with entry level manufacturing jobs.

Incentives: BRC – Infrastructure Grants, WYDOT – minimum revenue guarantee grants,

workforce training grants.

Challenges: ongoing infrastructure maintenance costs, trucking and shipping costs higher in

rural areas, lack of rail served sites in some areas of Wyoming, lack of long term comprehensive

air service solution, lack of proximity to markets, generally favors Casper and Cheyenne, natural

resource jobs compete for workers, CapEx can be a barrier to entry. Consolidation has yielded

fewer and larger airlines, which often leaves rural airports behind. Low-cost and Ultra Low-Cost

carriers continue to nibble away at market share from the established carriers, shrinking the

difference between the three models. On the ground, Uber is expected to reach $42 billion in

revenue by 2025 through both geographical expansion and other markets that involve moving

something from A to B. Amazon has trained consumers to expect goods in hours, not days.

Automation.

Opportunities: Logistics as a service – companies able to provide software and analytics at

various points along the supply chain can improve customer service and maximize efficiency for

distributors. The consumer trend toward transparent order status means the industry is

investing in new tech and partnerships. As consumers purchase products through ever more

varied channels, new technology will be required to meet fulfillment and shipping challenges

Emerging Trends: Automation, Uber disruption, airline consolidation

Information (NAICS 51)

Description of Sector: The Information sector comprises companies that produce and distribute

information and cultural products, provide the means to distribute these products or other data

or communications, and process data. They include publishing industries, motion picture and

sound recording industries, broadcasting, telecommunications, and data processing, hosting,

and related services. See Appendix 3 for a complete list of NAICS in this sector.

Comparison to U.S. and Other States: This sector contributes less to Wyoming’s economy than

it does to comparator states’ and the US, representing 30.1% of Wyoming’s GDP, and 1.5% of

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 14

U.S. GDP. Wyoming can grow the economy by $1.3 billion over the next 20 years, by increasing

the 1.8% Wyoming GDP contribution to the 5.6% GDP contribution of the US.

Workforce Observations: Wages within this sector Wyoming wages in this sector are about half

of the wages in the sector for the US.

Enablers: No income taxes, Wyoming’s outdoor lifestyle and livability, reputation for data

centers (Microsoft, EchoStar, Ptolemy, Green House), low electricity rates, cool climate reduces

cooling costs, Breakthrough 307, Wyoming Technology Business Center.

Incentives: BRC- Managed Cost Data Center Grants, tradeshow incentive grants, challenge loan,

SBIC, workforce training grants

Challenges: lack of amenities to attract millennial talent, lack of skilled workforce, availability of

workforce, cost of housing in some areas of the state (Jackson, Laramie), broadband may be a

challenge in some parts of Wyoming, lack of long-term comprehensive air service solution,

proximity to markets, transmission capacity.

Opportunities: Opportunities for growth in this sector include data centers and

telecommunications. Data centers have been identified as an important opportunity and are a

large focus in this report. Assets from industries within this sector are enablers for other

sectors, and are also represented there. Expanding the footprint of this industry in Wyoming,

especially broadband, will enable growth in other sectors.

Emerging Trends: The prevalence of technology and digitization is driving innovation in the

publishing industry. The telecommunications industry is expected to grow, consolidate through

mergers and acquisitions, and continue to innovate. While data center square footage is

predicted to rise, the number of data centers is also expected to peak in 2017.

Finance, Insurance and Real Estate (NAICS 52-53)

Description of Sector: Leasing; monetary authorities – central bank; credit intermediation;

securities, commodity contracts, investments; insurance carriers and related activities; funds,

trusts and other financial vehicles; real estate; rental and leasing services and lessors of

nonfinancial intangible assets. See Appendix 3 for a complete list of NAICS in this sector.

Comparison to U.S. and Other States: Wyoming general ranks behind the U.S. and other

surrounding states in this industry. Financial activities contributed 13.9% to Wyoming’s GDP in

2016 compared to 19.8% for the US. If Wyoming can close that gap the 6% difference would add

$2 billion to the State’s GDP.

Workforce Observations: Wages within this sector general pay above the mean and median for

all occupations. In Wyoming, however, wages are on the lower end as compared to surrounding

states.

Enablers: No corporate or personal income tax, law are favorable for trust industry.

Incentives: Challenge Loan Program, USDA, SBA loan programs

Challenges: Significant barriers to entry (legal, regulatory, etc.) for startups, real estate

development costs are higher in rural areas, heavily focused in two areas of the state (Jackson

and Cheyenne).

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 15

Opportunities: Industry consolidation, family trusts

Emerging Trends: · Deregulation will allow financial institutions to invest more in customers and

less on risk mitigation, asset management, technology will change the fundamentals of the

traditional jobs in this industry, most ventures will require larger partners.

Professional and Business Services (NAICS 54-56)

Description of Sector: The Professional and Business Services Sector (sometimes called the

knowledge sector) comprises companies that perform professional, technical, scientific,

administrative, and managerial services for other businesses or entities. These often require a

high degree of expertise and training. Companies in this sector perform services such as

engineering, research and development, accounting, architecture, legal services, design,

computer systems design, advertising, management of companies or enterprises, and

administrative and support services. See Appendix 1 for a comprehensive list of NAICS codes in

this sector. See Appendix 3 for a complete list of NAICS in this sector.

Comparison to U.S. and Other States: There is tremendous opportunity for growth in this

sector, as it contributes significantly less to Wyoming’s economy than it does to other states and

the US. It makes up 4.5% of Wyoming’s GDP. Over the next 20 years, Wyoming can grow its

economy by $2.7 billion by increasing the Professional and Business Services 4.5% contribution

to the Wyoming GDP to the U.S. contribution of 12.8%.

Workforce Observations: Wages within this sector pay above the mean and median for all

occupations. However, Wyoming wages in this sector are low compared to most comparator

states.

Enablers: No income taxes, Wyoming’s outdoor lifestyle and livability, Breakthrough 307,

Wyoming Technology Business Center

Incentives: Main Street Technical Assistance Grants, BRC – Business Committed Grants, BRC-

Community Enhancement Grants, Challenge Loan, Workforce Training Grants.

Challenges: lack of amenities to attract millennial talent, lack of skilled workforce, availability of

workforce, cost of housing in some areas of the state (Jackson, Laramie), broadband may be a

challenge in some parts of Wyoming, lack of long-term comprehensive air service solution.

Opportunities: Opportunities in this sector include growing Professional and Business services

that are traditionally performed out of state, and leveraging Wyoming’s robust natural resource

base (e.g. minerals, oil and gas, agriculture) to drive growth in research and development, tech

companies, and other professional and business services entities.

Emerging Trends: Automation, continued innovation in models (e.g. “Uberization”), and

increased funding for research and development are some emerging trends within this sector.

Education and Health Care Services (NAICS 62)

Description of Sector: The Education and Health Services sector comprises companies and

entities that provide healthcare, social assistance, instruction, or training. This includes

physicians’ offices, hospitals, dentists, home health services, residential care facilities, public and

private schools, universities and colleges, day cares, and other entities. See Appendix 3 for a

comprehensive list of NAICS in this sector.

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 16

Comparison to US and other states: This sector contributes less to Wyoming’s economy than it

does to comparator states’ and the US. Wyoming can grow their economy by $1.37 billion over

the next 20 years, by increasing the 4.5% Wyoming GDP contribution to the 8.5% U.S. GDP

contribution.

Workforce Observations: Wyoming wages in this sector are near the average of comparator

states

Enablers: No corporate and personal income taxes, Wyoming’s outdoor lifestyle and livability,

Community College training programs.

Incentives: BRC – Business Committed Grants, Community Enhancement Grants, Community

Readiness Grants, Challenge Loan, Workforce Training Grants.

Challenges: challenged funding environment for UW and Wyoming schools due to recent drop in

commodity production, lack of fast, cost-competitive broadband, and challenged recruitment

and retention of workforce, especially physicians. This recruitment and retention is enabled by

livability and amenities.

Opportunities: Opportunities in this sector include healthcare, especially telehealth.

Emerging Trends: For-profit higher education institutes are focused on areas where there are

skills gaps, including middle skills jobs. Healthcare is innovating in many areas, including

business and financial models, care delivery, and predictive analytics.

Leisure and Hospitality NAICS (71-72)

Description of Sector: Restaurants, tourism, coffee shops, bed and breakfasts, hunting/fishing,

accommodation/food services, arts/entertainment/recreation, bakeries, outfitting, outdoor

recreation, candy shops, visual arts, performing arts, music, gaming, roasteries, wineries,

distilleries, craft brewing and agro-tourism.

Comparison to U.S. and Other States: Wyoming is on par with the U.S. average for this

industry. This is comparable with many surrounding states, but lags Colorado, New Mexico and

Utah. Activities from this sector contributed 3.7% to Wyoming’s GDP in 2016 compared to 3.9%

for the US. If Wyoming were at the U.S. average, it would add $69 million to the state’s GDP.

Workforce Observations: Wages within this sector pay below the mean and median for all

occupations. In Wyoming, however, wages are less than the U.S. average, but pay more than

some surrounding states including Idaho, Montana, New Mexico, North Dakota, South Dakota

and Utah.

Enablers: Low sales tax, Wyoming Arts Council, Wyoming Humanities Council, Strong tourism

market, outdoor lifestyle and livability, recreation attractions, Wyoming Women’s Business

Center, Wyoming Restaurant and Lodging Association.

Incentives: BRC – Community Enhancement Grants, Challenge Loan, Wyoming Women’s

Business Center -Microloan Program, Wyoming Arts Council grants, Wyoming Humanities

Council Grants, Main Street Program, Main Street Technical Assistance grants.

Challenges: Stable and consistent access to big game hunting licenses, lack of available and

sustainable air service, lack of available workforce, uncertain future of land use and access at

federal level.

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 17

Opportunities: Tourism; art; new potential wolf and grizzly hunting markets; take advantage of

Wyoming resources including lots of animals, open spaces and quality outfitting industry; ensure

a system of stable licensing.

Emerging Trends: Incoming young workforce in need of opportunities, Gaming industry

attempts to broaden and enter new markets, expanding on E-Casinos, sports gaming and

underutilized opportunities, Many aspects of the outdoor recreation industry are growing

because of changing technology and an increased desire for personalized experience, Because of

regular exposure to brands such as amazon and Starbucks, consumers have expectations of

instant, responsive, mobile and seamless travel experiences, Health, safety, social impact,

experience and transparency have become new drivers of the food service industry.

Other Services (NAICS 81)

Description of Sector: The Other Services sector comprises establishments engaged in providing

services not specifically provided for elsewhere in the classification system. Establishments in

this sector are primarily engaged in activities, such as equipment and machinery repairing,

promoting or administering religious activities, grantmaking, advocacy, and providing dry

cleaning and laundry services, personal care services, death care services, pet care services,

photofinishing services, temporary parking services, and dating services.

Private households that engage in employing workers on or about the premises in activities primarily concerned with the operation of the household are included in this sector.

Comparison to U.S. and Other States: Wyoming is on par with the U.S. average for this industry. This is comparable with many surrounding states and the US. Activities from this sector contributed 1.5% to Wyoming’s GDP in 2016 compared to 2.1% for the US.

Workforce Observations: In Wyoming wages are less than the U.S. average, but pay more than

some surrounding states including Idaho, Montana, New Mexico, North Dakota, South Dakota

and Utah. In 2016, it is estimated that 7,288 worked in this sector earning an average annual

wage of $34,505.

Emerging Trends: Of the 2,952 registered charitable nonprofits in Wyoming, 2,336 (79%) are

comprised of small, community-based organizations, for example: adult and youth sports

organizations, community theatres, small museums, 4-H clubs and library foundations. All have

budgets under $100,000 and most of them rely heavily on volunteers. Many start-up nonprofits

fall into this category as well. Note: 1,878 of the public charities are non-reporting and therefore

have been included in this 79% due to their annual receipts being less than $50,000.

The remaining 616 charitable nonprofits address more complex community needs. There are

465 nonprofits (16%) with budgets between $100,000 and $999,000. Examples of organizations

in this budget range include food pantries, animal rescues, rural-based senior centers, and child

advocacy organizations. There are 151 nonprofits (5%) with budgets over $1 million. Examples in

this group include hospitals, mental health centers, youth and recreation centers, child

development centers and community foundations.

Public Administration (NAICS 92)

Description of Sector: The Public Administration sector consists of establishments of federal,

state, and local government agencies that administer, oversee, and manage public programs

ENDOW Socioeconomic Report | Summary of Socioeconomic Data P a g e | 18

and have executive, legislative, or judicial authority over other institutions within a given area.

These agencies also set policy, create laws, adjudicate civil and criminal legal cases, provide for

public safety and for national defense. In general, government establishments in the Public

Administration sector oversee governmental programs and activities that are not performed by

private establishments. In addition to state, county, local governments, the K-12 public school

systems/districts, community colleges, university are in this category along with federal agencies

and military entities.

Comparison to U.S. and Other States: Wyoming’s sparse and rural population and multiple

counties, cities, towns and school districts coupled with state executive, justice and legislative

systems, federal agencies, and military bases and camps, provides a high sector share to the

state’s GDP make-up. Only Alaska and New Mexico of the comparator states exceed Wyoming’s

GDP percentage. Activities from this sector contributed 15.6% to Wyoming’s GDP in 2016

compared to 12% for the US.

Workforce Observations: In Wyoming, wages are less than the U.S. average, but pay more than

some surrounding states including Idaho, Montana, New Mexico, North Dakota, South Dakota

and Utah.

Emerging Trends: Declining local and state revenues have consequently reduced employment

and service levels throughout the state.

ENDOW Socioeconomic Report | Assessment of Demographic Trends in Wyoming P a g e | 19

Assessment of Demographic Trends in Wyoming Introduction Population change is a function of three

processes: births, deaths, and migration

either, into (in-migration) or out of a

population (out-migration), collectively

referred to as the demographic process.

It is of vital importance to study the

sources of population change because

the determinants of the processes of

natural increase (combined effects of

births and deaths) and migration are

quite different. Both births and deaths

are physiological and biological

processes. Migration, however, is a

behavior involving people moving from

one area to another often because of

employment, income, and other socioeconomic changes.

Although births and deaths influence a state’s population by increasing or decreasing its size, their effects

on other non-demographic and socioeconomic factors are considerably more long-term. Migration, on

the other hand, has an immediate impact on an area because it is likely to involve young adults in their

family formation ages. Migration results in a near simultaneous change in demand for goods and services.

Migration Trends Wyoming’s migration (either inflow or outflow) history has been predominately driven by employment

opportunities in the state and economic

conditions in the rest of the country.

Wyoming’s total population experienced a

dramatic increase of nearly 180,000 (or

54%) from 1970 to 1983 as oil production

was booming. This rapid growth was

immediately followed by a decline of

57,700 people (or 11%) during the last

seven years in 1980s, as oil prices dropped

by 70 percent in constant dollars. The first

few years of the 1990s brought steady

growth as the national economy,

particularly California, contracted,

however, strong national expansion in the

rest of the 1990s played a major role for the

negative net migration flow, more people left than moved into Wyoming. By the end of the decade

Wyoming experienced 8.9 percent growth compared to the U.S. average of 13.2 percent. The booming

natural gas exploration during the first decade of the new century drew many younger workers into the

state, particularly between 2006 and 2009. Total population in Wyoming grew 14.1 percent from 2000 to

2010, faster than the U.S. average of 9.7 percent. However, since 2013 the state has experienced three

-30,000

-25,000

-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

325,000

350,000

375,000

400,000

425,000

450,000

475,000

500,000

525,000

550,000

575,000

600,000

Ne

t Mig

ratio

nPo

pu

lati

on

* Net Migration = In-migration - Outmigration

Wyoming Population and Net Migration: 1970 to 2016

Net Migration* Population Natural Incease (R)

Source: U.S. Census Bureau Prepared by WyomingEconomic Analysis Division

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

Source: Wyoming Department of Health

Number of Births and Deaths in Wyoming: 1970 to 2016

Births Deaths

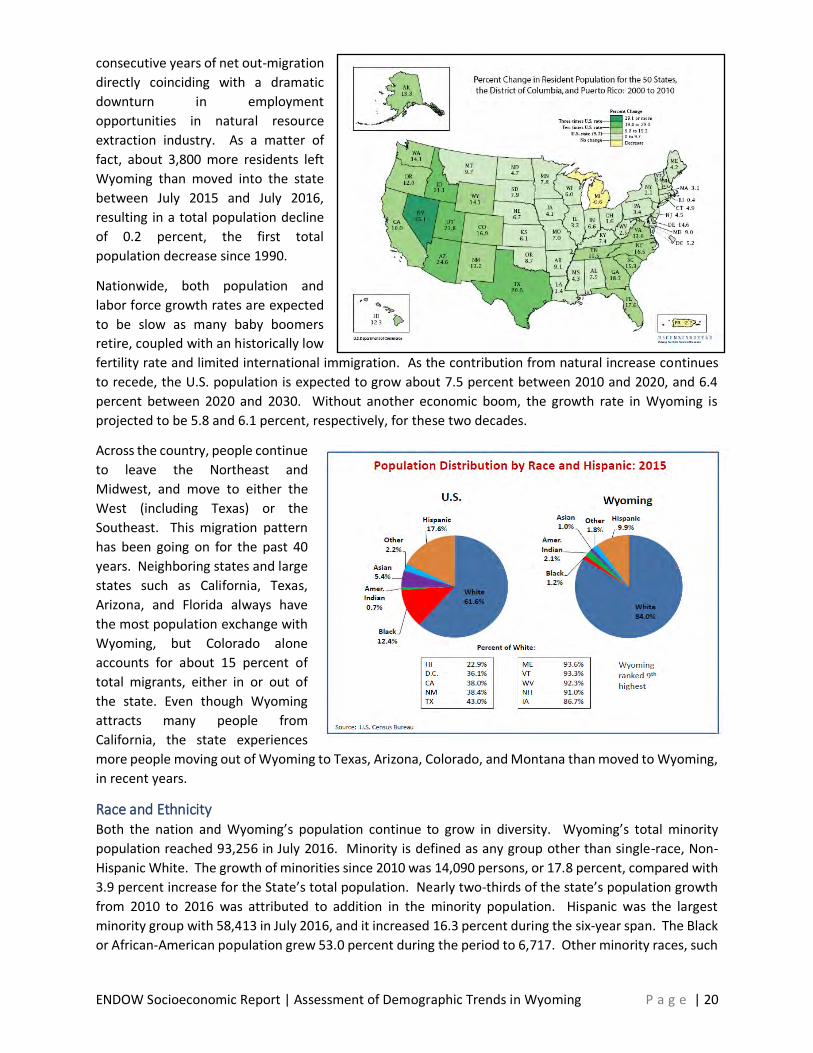

ENDOW Socioeconomic Report | Assessment of Demographic Trends in Wyoming P a g e | 20

consecutive years of net out-migration

directly coinciding with a dramatic

downturn in employment

opportunities in natural resource

extraction industry. As a matter of

fact, about 3,800 more residents left

Wyoming than moved into the state

between July 2015 and July 2016,

resulting in a total population decline

of 0.2 percent, the first total

population decrease since 1990.

Nationwide, both population and

labor force growth rates are expected

to be slow as many baby boomers

retire, coupled with an historically low

fertility rate and limited international immigration. As the contribution from natural increase continues

to recede, the U.S. population is expected to grow about 7.5 percent between 2010 and 2020, and 6.4

percent between 2020 and 2030. Without another economic boom, the growth rate in Wyoming is

projected to be 5.8 and 6.1 percent, respectively, for these two decades.

Across the country, people continue

to leave the Northeast and

Midwest, and move to either the

West (including Texas) or the

Southeast. This migration pattern

has been going on for the past 40

years. Neighboring states and large

states such as California, Texas,

Arizona, and Florida always have

the most population exchange with

Wyoming, but Colorado alone

accounts for about 15 percent of

total migrants, either in or out of

the state. Even though Wyoming

attracts many people from

California, the state experiences

more people moving out of Wyoming to Texas, Arizona, Colorado, and Montana than moved to Wyoming,

in recent years.

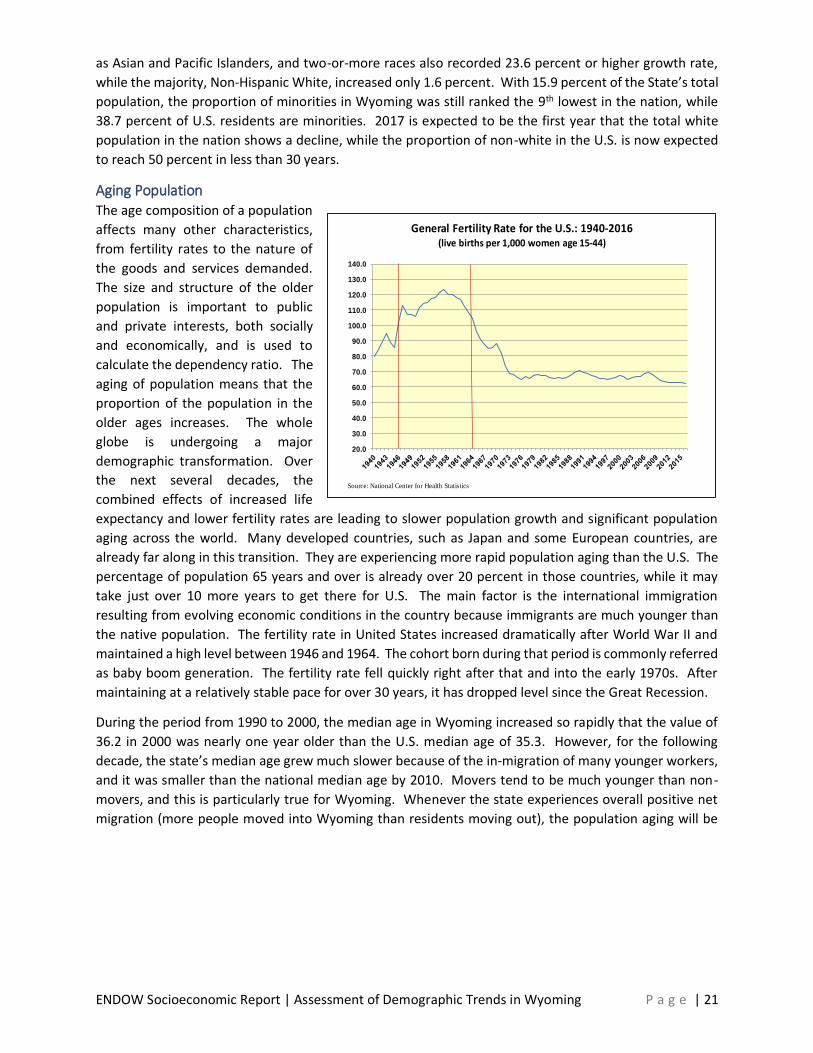

Race and Ethnicity Both the nation and Wyoming’s population continue to grow in diversity. Wyoming’s total minority

population reached 93,256 in July 2016. Minority is defined as any group other than single-race, Non-

Hispanic White. The growth of minorities since 2010 was 14,090 persons, or 17.8 percent, compared with

3.9 percent increase for the State’s total population. Nearly two-thirds of the state’s population growth

from 2010 to 2016 was attributed to addition in the minority population. Hispanic was the largest

minority group with 58,413 in July 2016, and it increased 16.3 percent during the six-year span. The Black

or African-American population grew 53.0 percent during the period to 6,717. Other minority races, such

ENDOW Socioeconomic Report | Assessment of Demographic Trends in Wyoming P a g e | 21

as Asian and Pacific Islanders, and two-or-more races also recorded 23.6 percent or higher growth rate,

while the majority, Non-Hispanic White, increased only 1.6 percent. With 15.9 percent of the State’s total

population, the proportion of minorities in Wyoming was still ranked the 9th lowest in the nation, while

38.7 percent of U.S. residents are minorities. 2017 is expected to be the first year that the total white

population in the nation shows a decline, while the proportion of non-white in the U.S. is now expected

to reach 50 percent in less than 30 years.

Aging Population The age composition of a population

affects many other characteristics,

from fertility rates to the nature of

the goods and services demanded.

The size and structure of the older

population is important to public

and private interests, both socially

and economically, and is used to

calculate the dependency ratio. The

aging of population means that the

proportion of the population in the

older ages increases. The whole

globe is undergoing a major

demographic transformation. Over

the next several decades, the

combined effects of increased life

expectancy and lower fertility rates are leading to slower population growth and significant population

aging across the world. Many developed countries, such as Japan and some European countries, are

already far along in this transition. They are experiencing more rapid population aging than the U.S. The

percentage of population 65 years and over is already over 20 percent in those countries, while it may

take just over 10 more years to get there for U.S. The main factor is the international immigration

resulting from evolving economic conditions in the country because immigrants are much younger than

the native population. The fertility rate in United States increased dramatically after World War II and

maintained a high level between 1946 and 1964. The cohort born during that period is commonly referred

as baby boom generation. The fertility rate fell quickly right after that and into the early 1970s. After

maintaining at a relatively stable pace for over 30 years, it has dropped level since the Great Recession.

During the period from 1990 to 2000, the median age in Wyoming increased so rapidly that the value of

36.2 in 2000 was nearly one year older than the U.S. median age of 35.3. However, for the following

decade, the state’s median age grew much slower because of the in-migration of many younger workers,

and it was smaller than the national median age by 2010. Movers tend to be much younger than non-

movers, and this is particularly true for Wyoming. Whenever the state experiences overall positive net

migration (more people moved into Wyoming than residents moving out), the population aging will be

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

120.0

130.0

140.0

Source: National Center for Health Statistics

General Fertility Rate for the U.S.: 1940-2016(live births per 1,000 women age 15-44)

ENDOW Socioeconomic Report | Assessment of Demographic Trends in Wyoming P a g e | 22

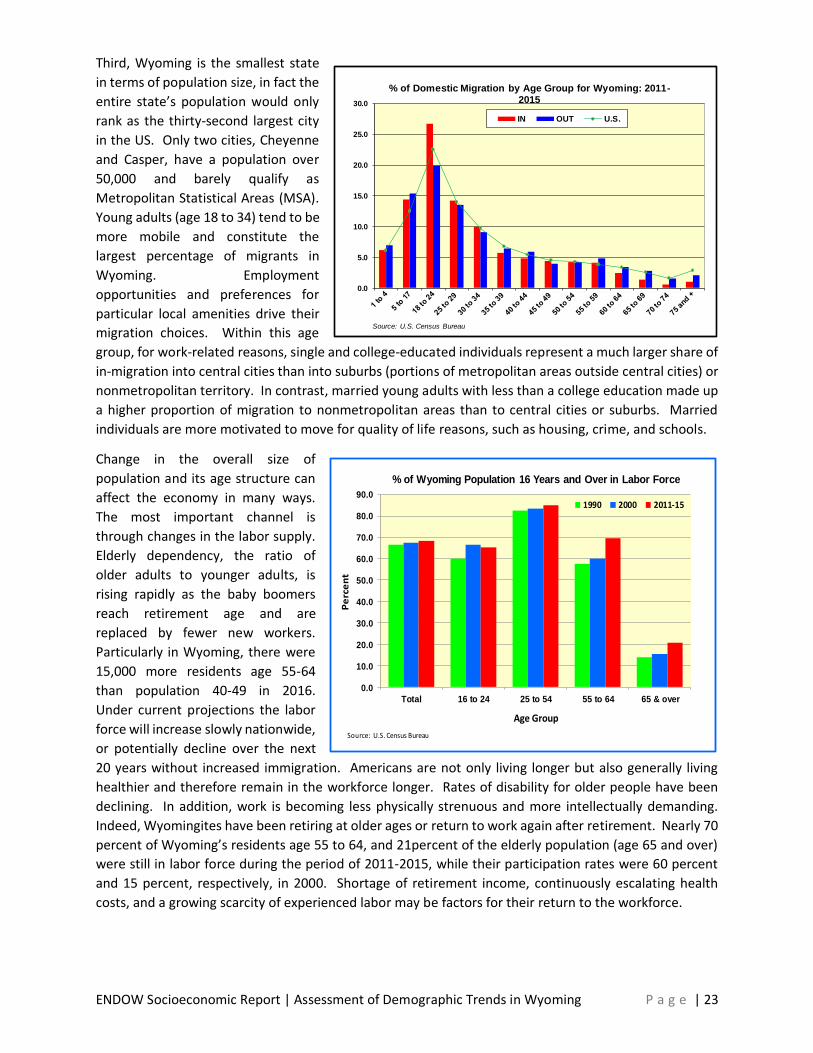

slower. Otherwise, the aging process is

always faster, such as during the period

from July 2015 to July 2016 when

Wyoming’s median age increased 0.3

years, one of the fastest in the country.

Wyoming’s pace in population aging is

expected to continue to accelerate for

the next 20 years.

There are a few factors contributing to

the state’s rapid aging. First, Wyoming

has one of the highest proportions of

early baby boomer population in the

nation. During oil boom time in the late

1970s and early 1980s, tens of

thousands of young workers

migrated into the state. Though

some moved out when the bust

happened in mid 1980s, many of

them remained. This group of baby

boomers were between 52 and 70

years old in 2016. On the other hand,

the percentage of population age 36

to 51 (so called generation X) in

Wyoming is very low because a

significant number of them left the

state in late 1980s and 1990s when

they were young adults. Therefore,

much of this aging is due to the baby