solvency and financial condition report (sfcr)...hdi global specialty se | solvency and financial...

TRANSCRIPT

1 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

Solvency and Financial

Condition Report

(SFCR)

2018

HDI Global Specialty SE

2 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

Contents

Contents ..................................................................................................................................... 2

Summary .................................................................................................................................... 6

A. Business activities and performance ................................................................................. 10

A.1 Business activity ........................................................................................................... 10

A.1.1 Business model ................................................................................................... 10

A.1.2 Profit situation and key transactions ..................................................................... 10

A.1.3 Headquarters, supervisor and auditor .................................................................. 12

A.1.4 Group structure .................................................................................................... 12

A.2 Underwriting performance ............................................................................................. 13

A.3 Investment income ........................................................................................................ 15

A.4 Performance of other activities ...................................................................................... 16

A.4.1 Other income and expenses ................................................................................ 16

A.5 Other information .......................................................................................................... 16

B. System of governance ....................................................................................................... 17

B.1 General information on the system of governance ........................................................ 17

B.1.1 Governance structure .......................................................................................... 17

B.1.2 Remuneration policy ............................................................................................ 20

B.1.3 Key transactions with associated companies and related parties ......................... 21

B.2 Requirements for professional qualification and personal reliability ............................... 21

B.2.1 Description of requirements ................................................................................. 21

B.2.2 Evaluation process............................................................................................... 22

B.3 Risk Management System, including Own Risk and Solvency Assessment (ORSA) ..... 23

B.3.1 Risk management system, including risk management function ........................... 23

B.3.2 Own Risk and Solvency Assessment (ORSA) ...................................................... 26

B.4 Internal Control System ................................................................................................. 28

B.4.1 Components of the Internal Control System ......................................................... 28

B.4.2 Compliance function ............................................................................................ 28

B.5 Alignment of Group Auditing ......................................................................................... 30

B.6 Actuarial function .......................................................................................................... 31

B.7 Outsourcing .................................................................................................................. 32

B.8 Other information .......................................................................................................... 33

B.8.1 Evaluation the appropriateness of the system of governance .............................. 33

3 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

B.8.2 Other information ................................................................................................. 33

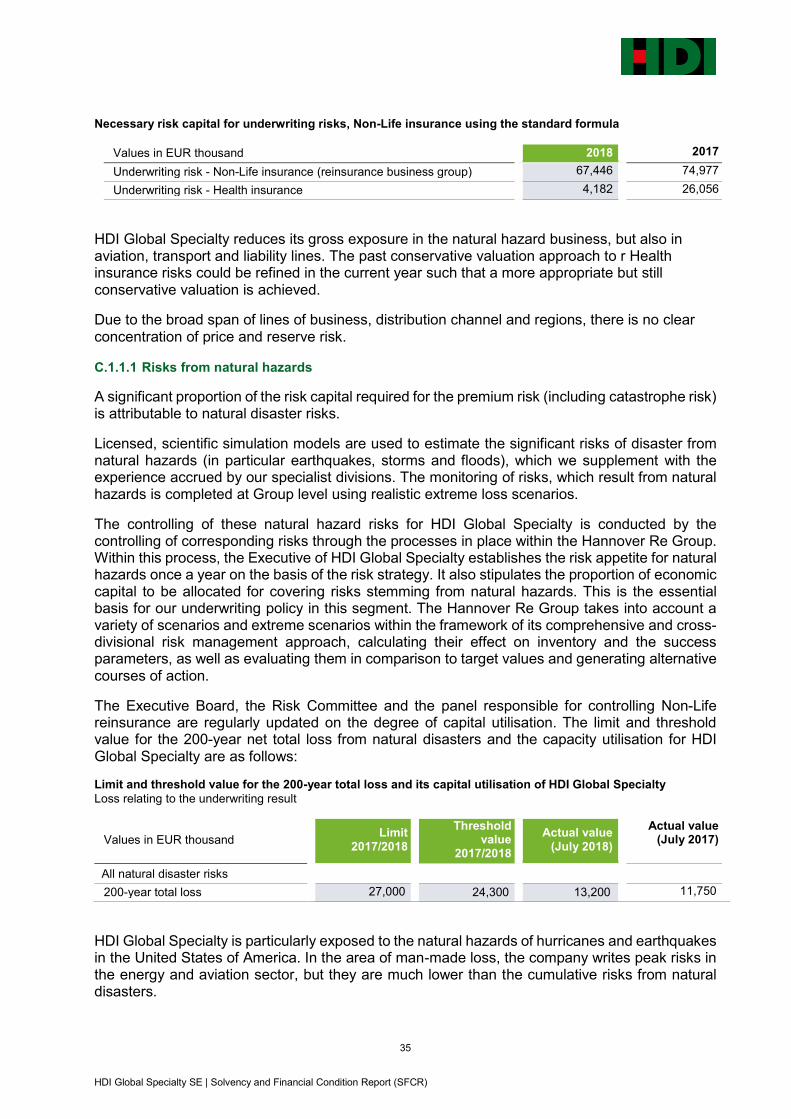

C. Risk profile ..................................................................................................................... 34

C.1 Underwriting risk ........................................................................................................... 34

C.1.1 Underwriting risk - Non-Life insurance and reinsurance ....................................... 34

C.1.2 Reserve risks ....................................................................................................... 36

C.1.3 Risk reduction techniques in Non-Life .................................................................. 36

C.2 Market risk .................................................................................................................... 37

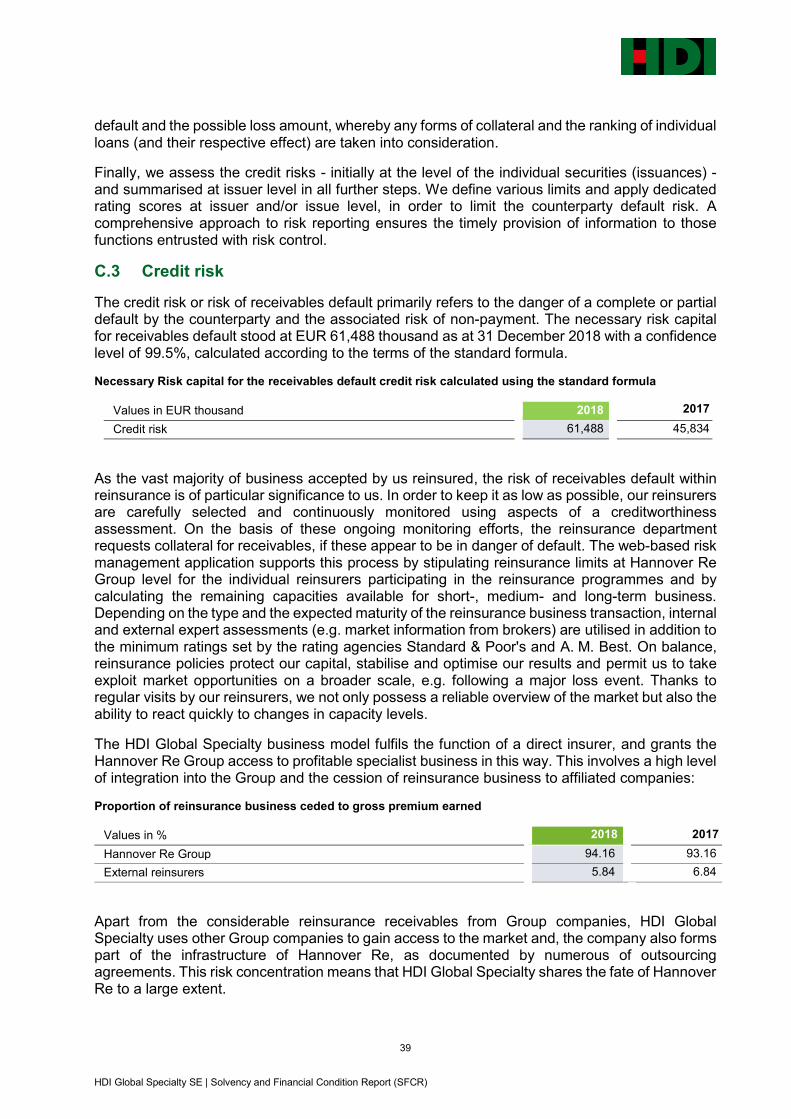

C.3 Credit risk ...................................................................................................................... 39

C.4 Liquidity risk .................................................................................................................. 40

C.5 Operational risk ............................................................................................................. 40

C.6 Other material risks ....................................................................................................... 42

C.6.1 Emerging risks ..................................................................................................... 42

C.6.2 Strategic risks ...................................................................................................... 42

C.6.3 Reputational risks ................................................................................................ 43

C.7 Other information .......................................................................................................... 43

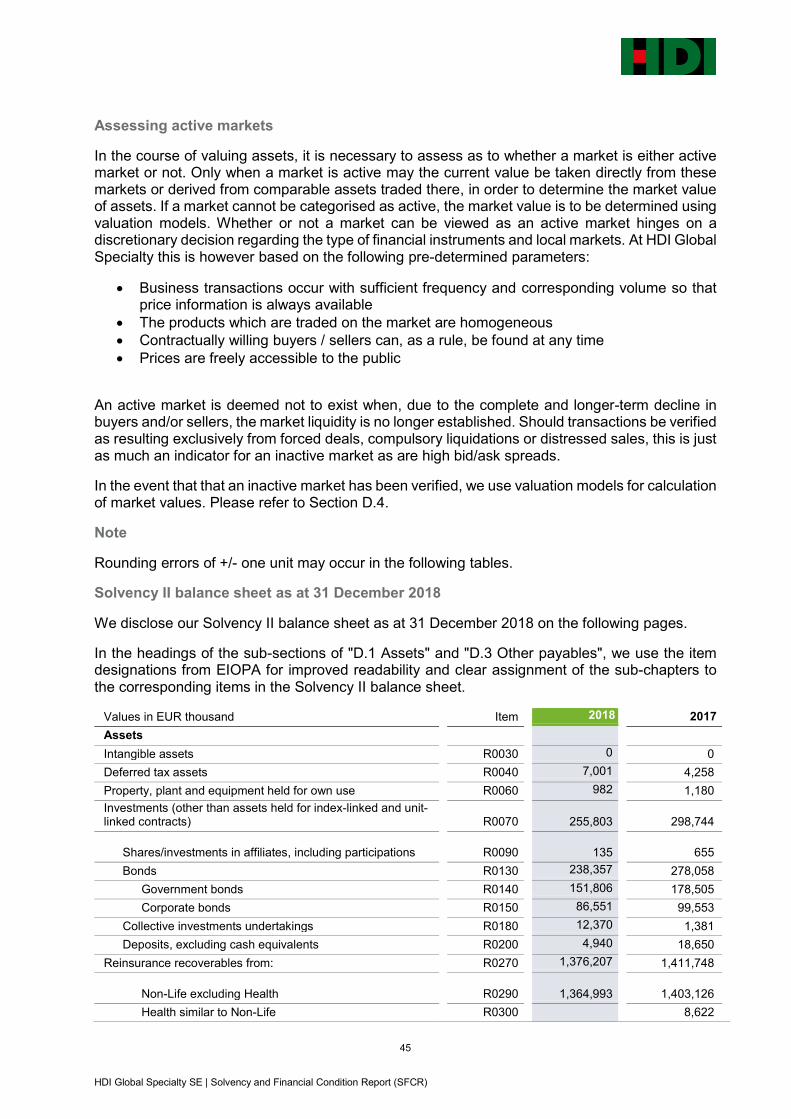

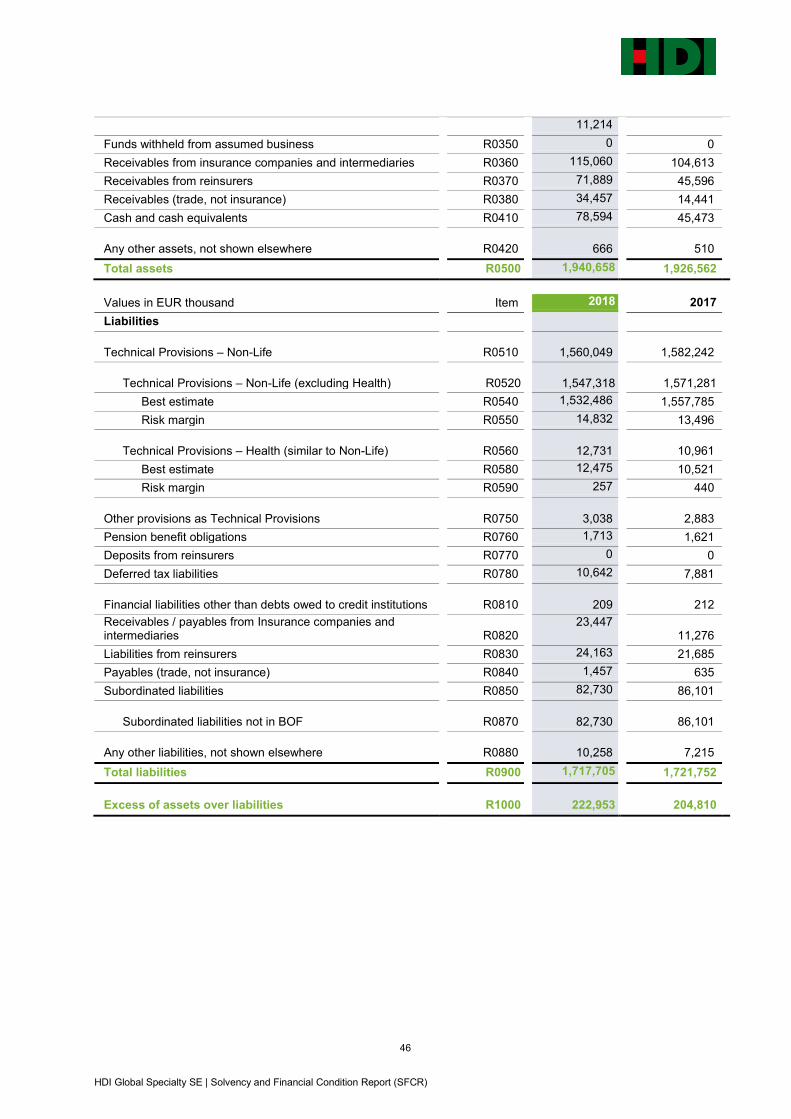

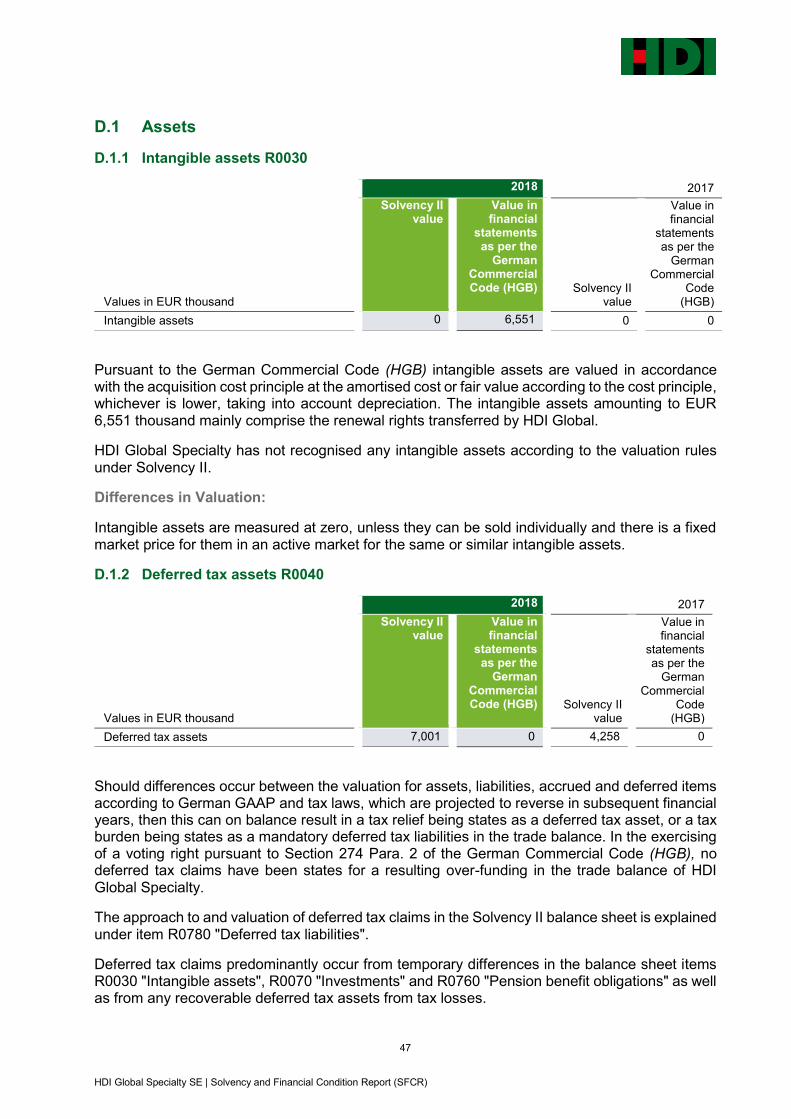

D. Valuation for solvency purposes .................................................................................... 44

D.1 Assets ........................................................................................................................... 47

D.1.1 Intangible assets R0030 ...................................................................................... 47

D.1.2 Deferred tax assets R0040 .................................................................................. 47

D.1.3 Property, plant and equipment held for own usage R0060 ................................... 48

D.1.4 Property (other than for own usage) R0080 ......................................................... 48

D.1.5 Shares/investments in affiliates including participations R0090 ............................ 48

D.1.6 Shares R0100 ...................................................................................................... 49

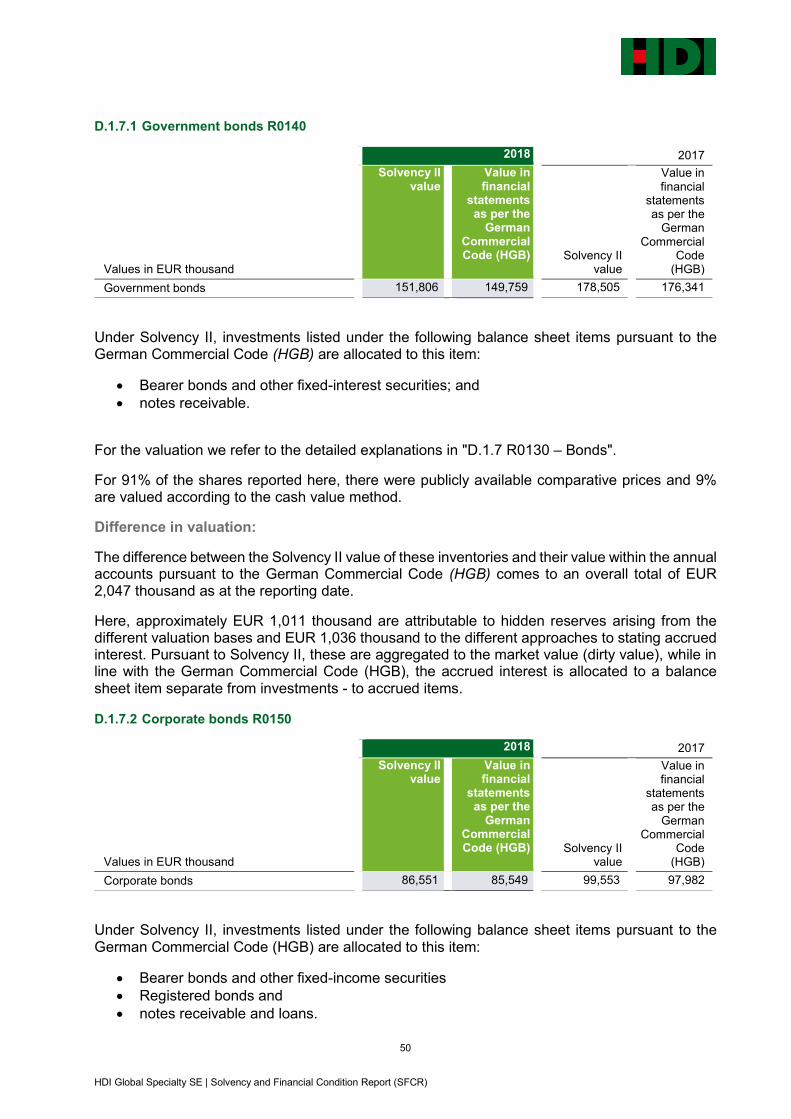

D.1.7 Bonds R0130 ....................................................................................................... 49

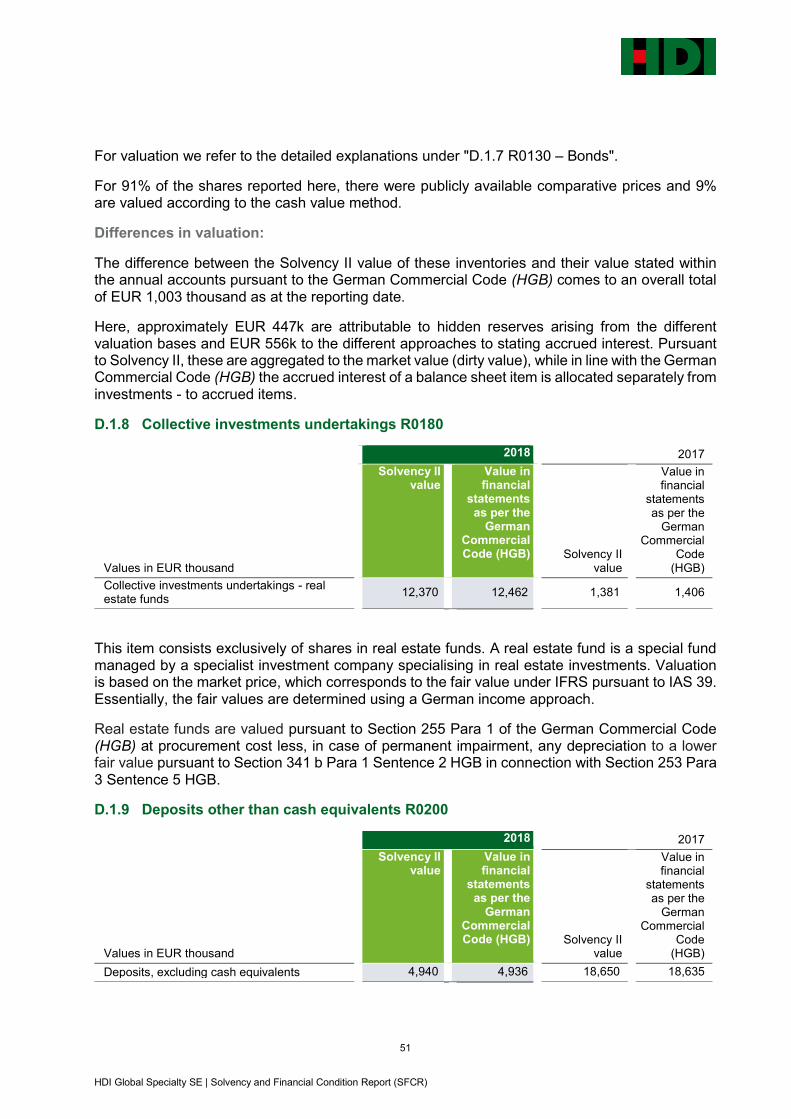

D.1.8 Collective investments undertakings R0180 ......................................................... 51

D.1.9 Deposits other than cash equivalents R0200 ....................................................... 51

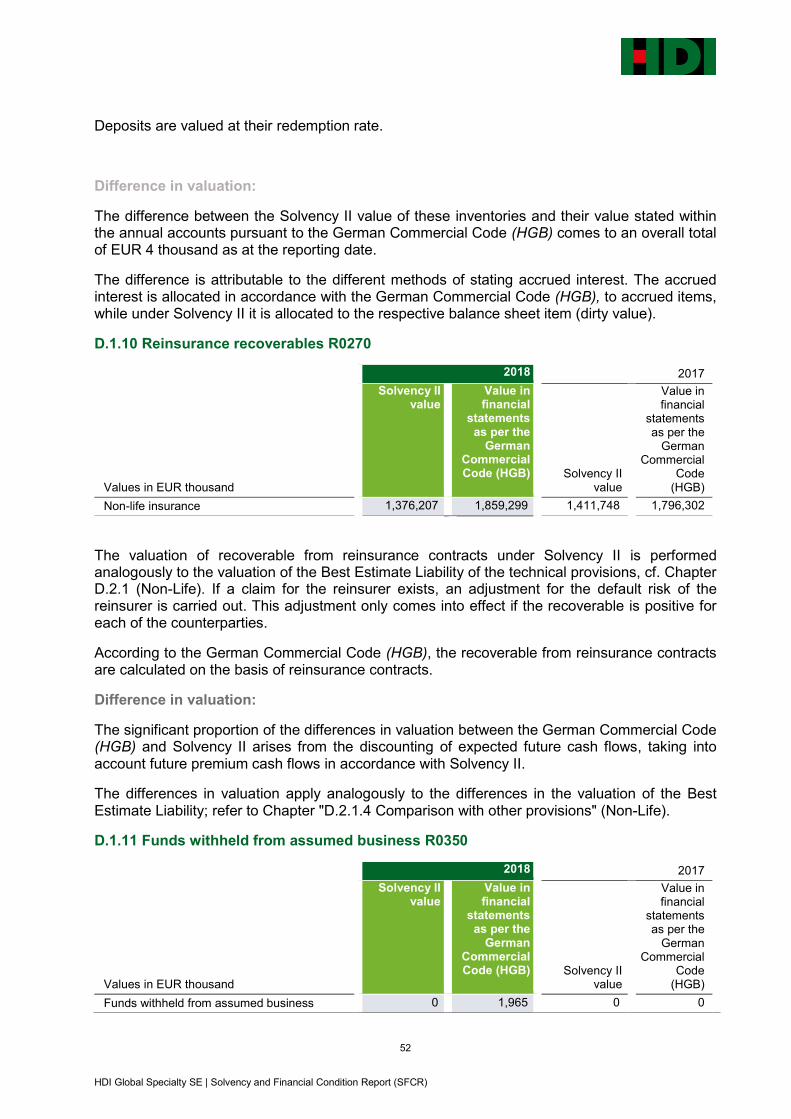

D.1.10 Reinsurance recoverables R0270 ........................................................................ 52

D.1.11 Funds withheld from assumed business R0350 ................................................... 52

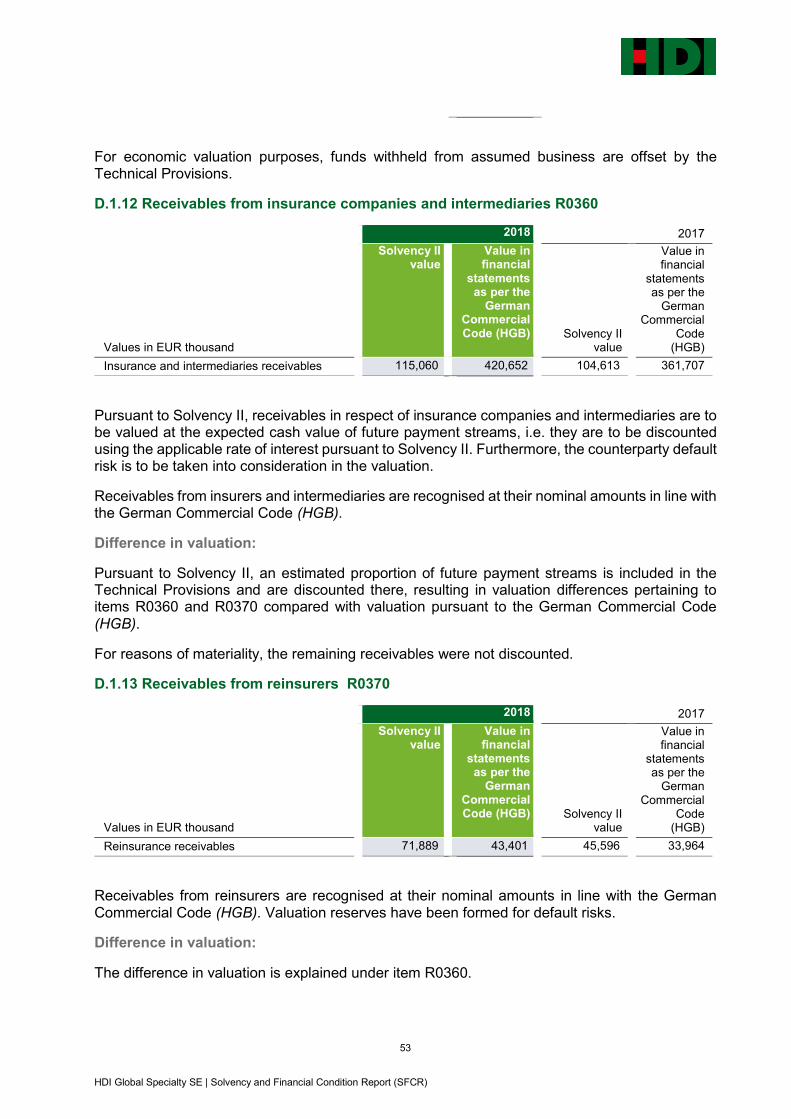

D.1.12 Receivables from insurance companies and intermediaries R0360 ..................... 53

D.1.13 Receivables from reinsurers R0370 .................................................................... 53

D.1.14 Receivables (trade, not insurance) R0380 ........................................................... 54

D.1.15 Cash and cash equivalents R0410 ....................................................................... 54

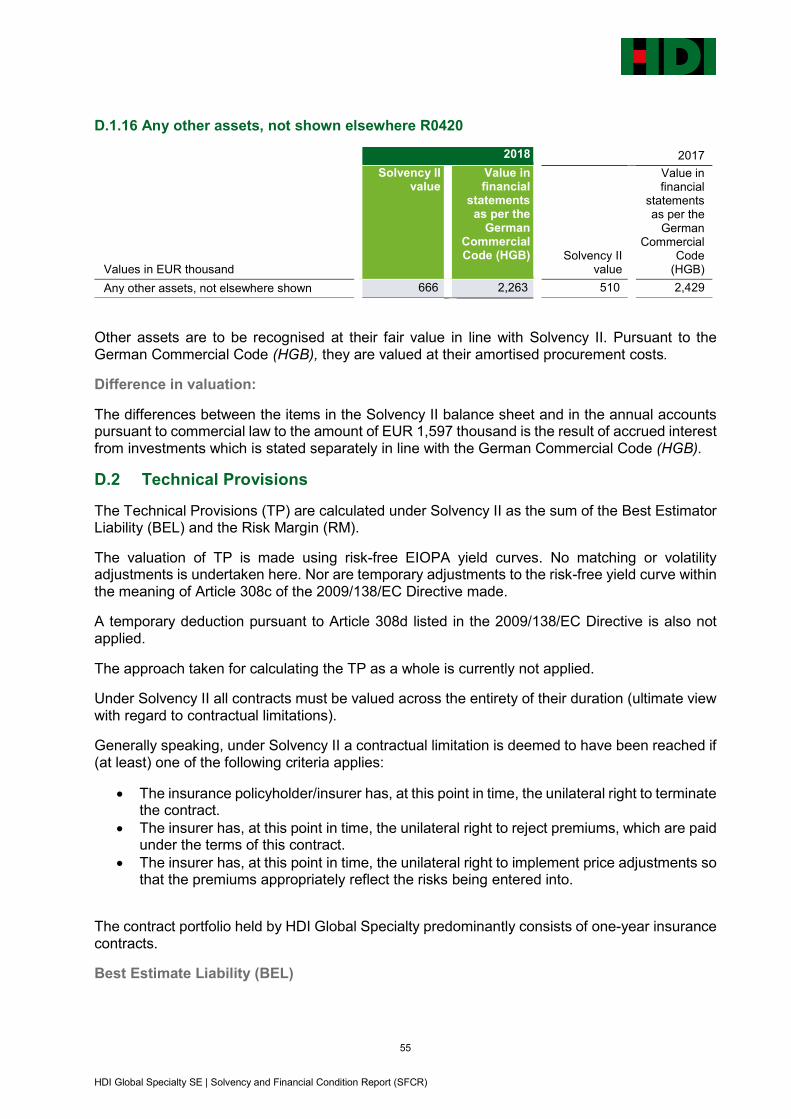

D.1.16 Any other assets, not shown elsewhere R0420 .................................................... 55

D.2 Technical Provisions ..................................................................................................... 55

4 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

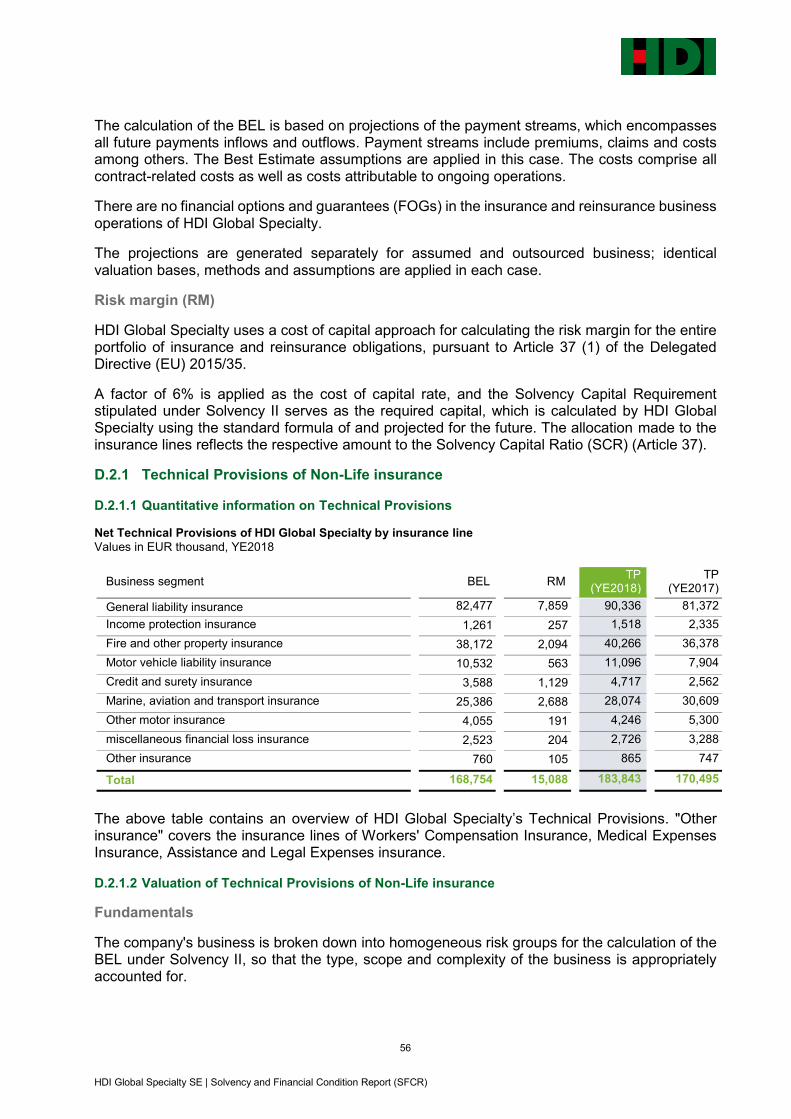

D.2.1 Technical Provisions of Non-Life insurance.......................................................... 56

D.3 Other liabilities .............................................................................................................. 60

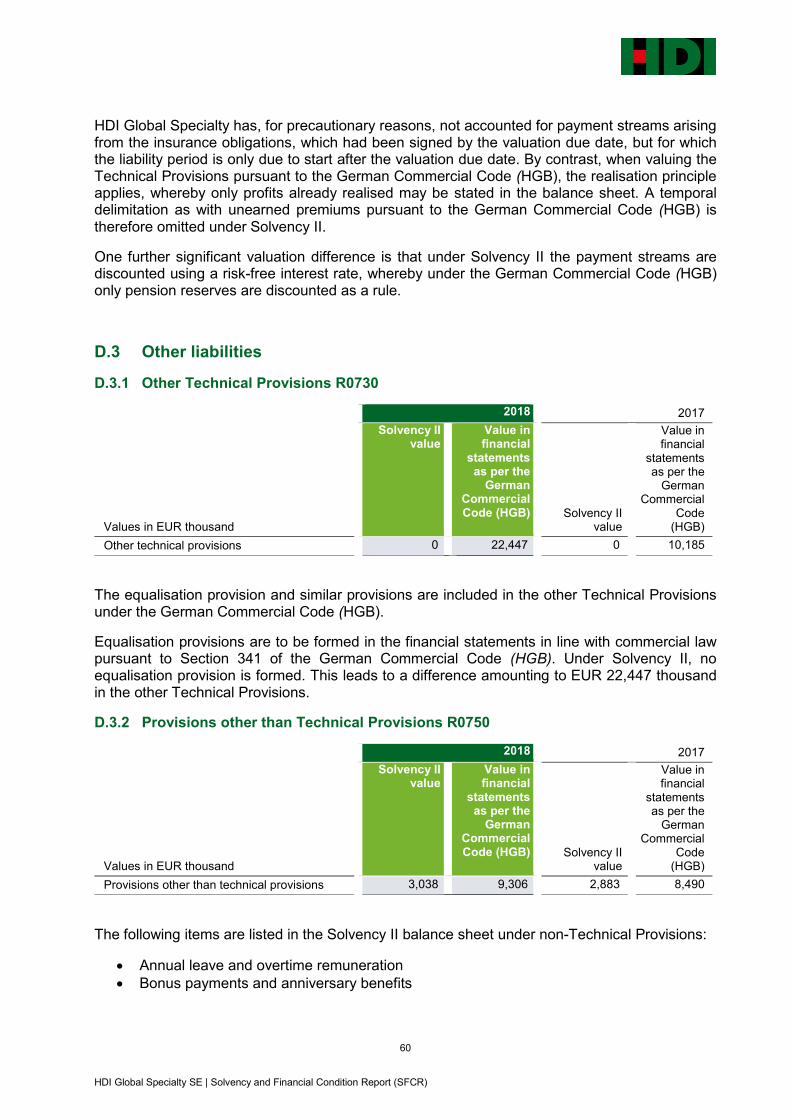

D.3.1 Other Technical Provisions R0730 ....................................................................... 60

D.3.2 Provisions other than Technical Provisions R0750............................................... 60

D.3.3 Pension benefit obligations R0760 ....................................................................... 61

D.3.4 Funds withheld on ceded business R0770 ........................................................... 62

D.3.5 Deferred tax liabilities R0780 ............................................................................... 62

D.3.6 Financial liabilities other than liabilities to credit institutions R0810 ...................... 63

D.3.7 Liabilities from insurance companies & intermediaries R0820 .............................. 64

D.3.8 Liabilities from reinsurers R0830 .......................................................................... 64

D.3.9 Payables (trade, not insurance) R0840 ................................................................ 65

D.3.10 Subordinated liabilities not in basic own funds (BOF) R0870 ............................... 65

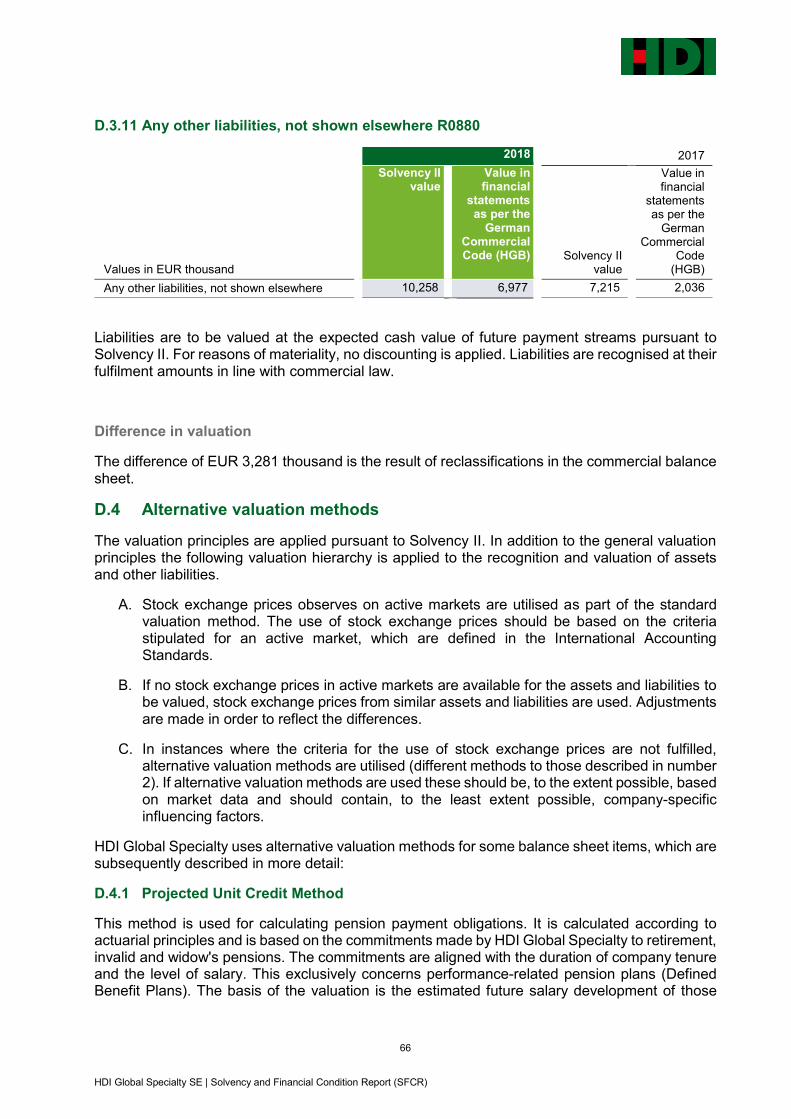

D.3.11 Any other liabilities, not shown elsewhere R0880 ................................................ 66

D.4 Alternative valuation methods ....................................................................................... 66

D.4.1 Projected Unit Credit Method ............................................................................... 66

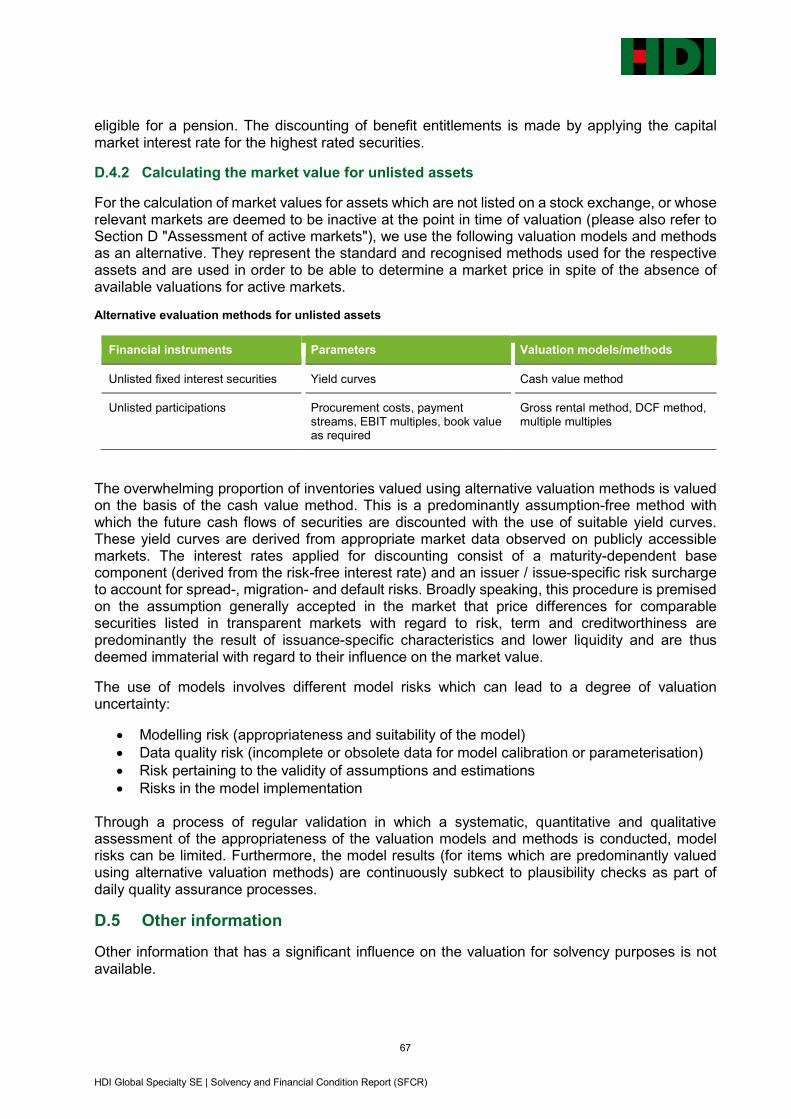

D.4.2 Calculating the market value for unlisted assets .................................................. 67

D.5 Other information .......................................................................................................... 67

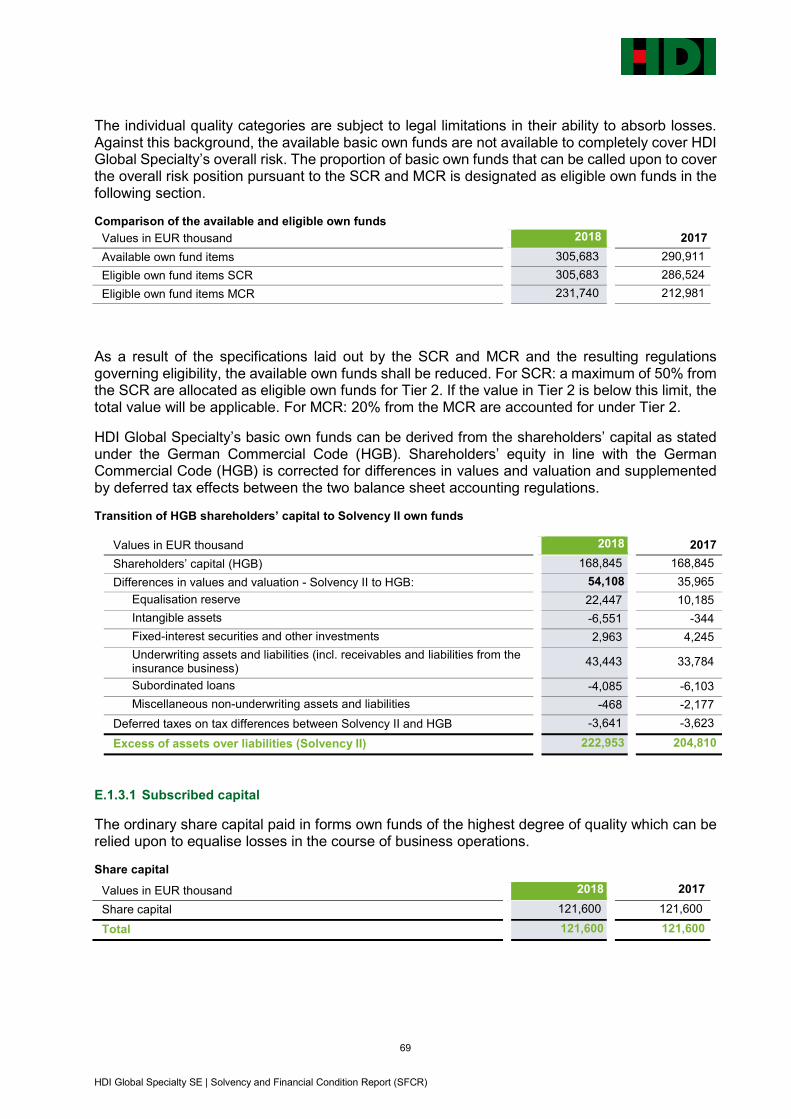

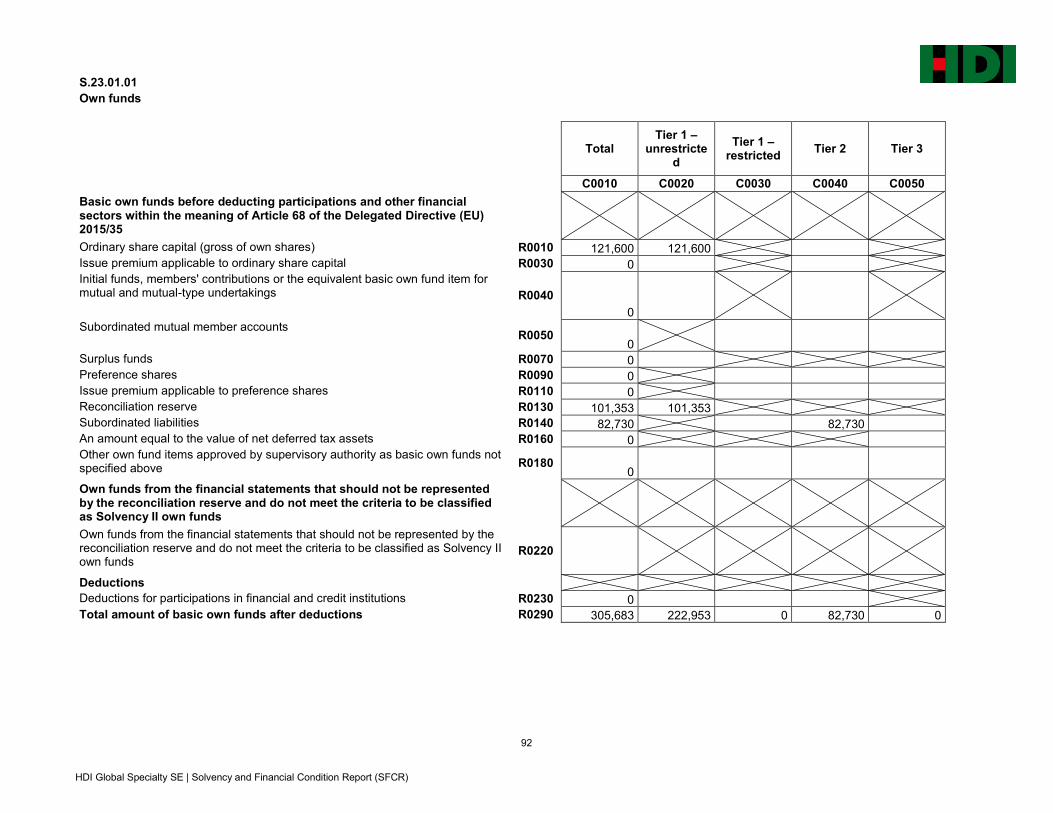

E. Capital management ......................................................................................................... 68

E.1 Own funds ..................................................................................................................... 68

E.1.1 Management of own funds ................................................................................... 68

E.1.2 Tiering .................................................................................................................. 68

E.1.3 Basic own funds ................................................................................................... 68

E.2 Solvency Capital Requirement and Minimum Capital Requirement ............................... 71

E.2.1 Solvency Capital Requirement (SCR) .................................................................. 71

E.3 Use of the duration-based equity risk sub-module when calculating the Solvency Capital

Requirement ......................................................................................................................... 72

E.4 Differences between the standard formula and any internal models used ..................... 72

E.5 Non-compliance with the Minimum Capital Requirement and the Solvency Capital

Requirement ......................................................................................................................... 72

E.6 Other information .......................................................................................................... 73

Glossary of abbreviations and terms ........................................................................................ 74

Notification sheets to be published ........................................................................................... 76

5 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

This document is an English language translation of the German document prepared by a

professional translation service in accordance with international translation standard. However,

in case of discrepancies, the German language document is the sole authoritative and

universally valid version.

6 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

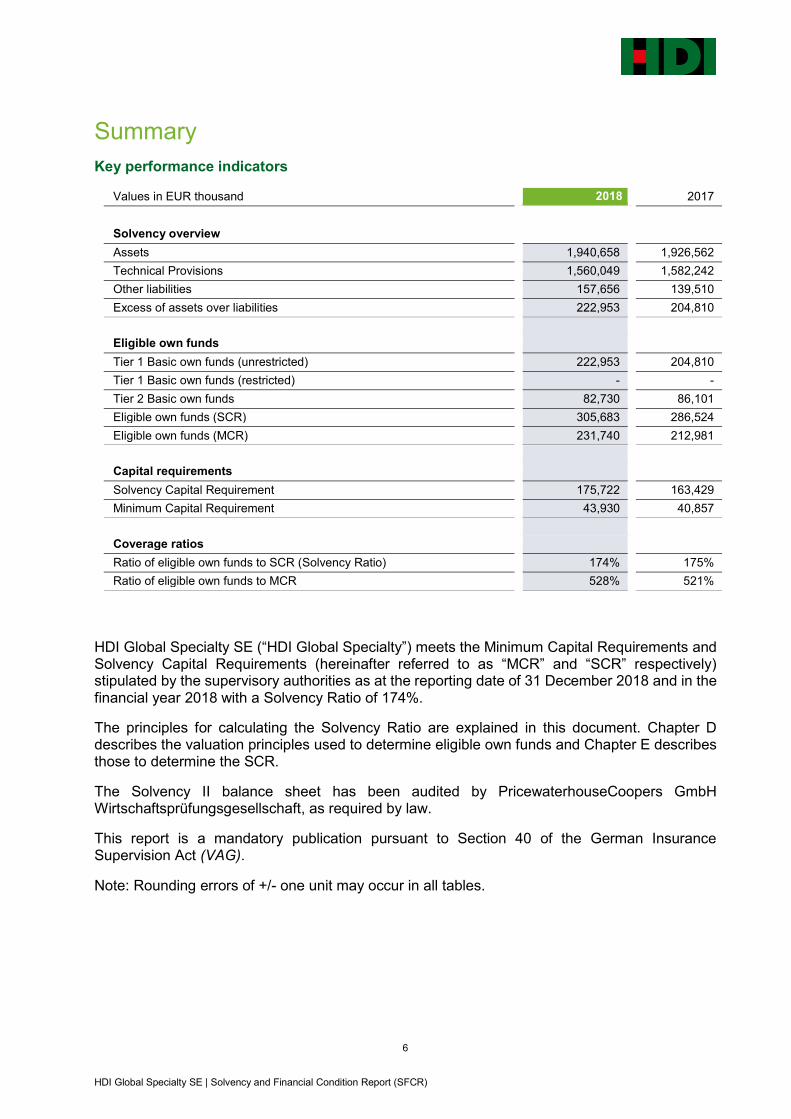

Summary

Key performance indicators

Values in EUR thousand 2018 2017

Solvency overview

Assets 1,940,658 1,926,562

Technical Provisions 1,560,049 1,582,242

Other liabilities 157,656 139,510

Excess of assets over liabilities 222,953 204,810

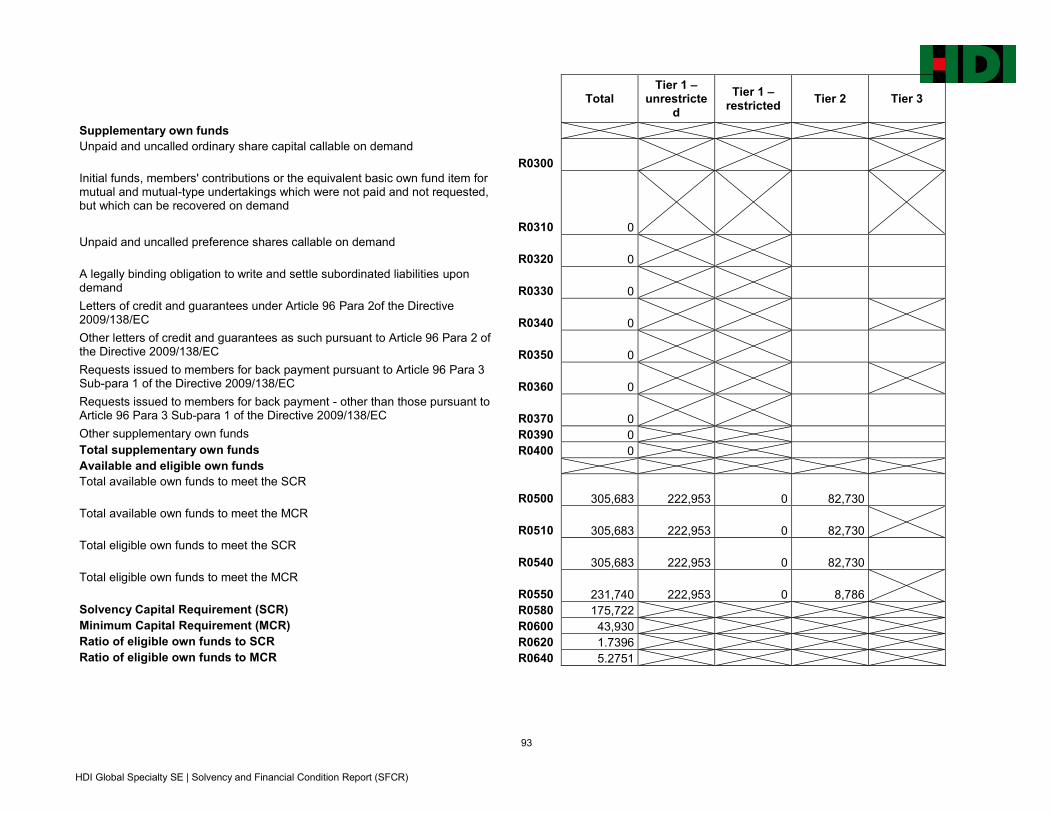

Eligible own funds

Tier 1 Basic own funds (unrestricted) 222,953 204,810

Tier 1 Basic own funds (restricted) - -

Tier 2 Basic own funds 82,730 86,101

Eligible own funds (SCR) 305,683 286,524

Eligible own funds (MCR) 231,740 212,981

Capital requirements

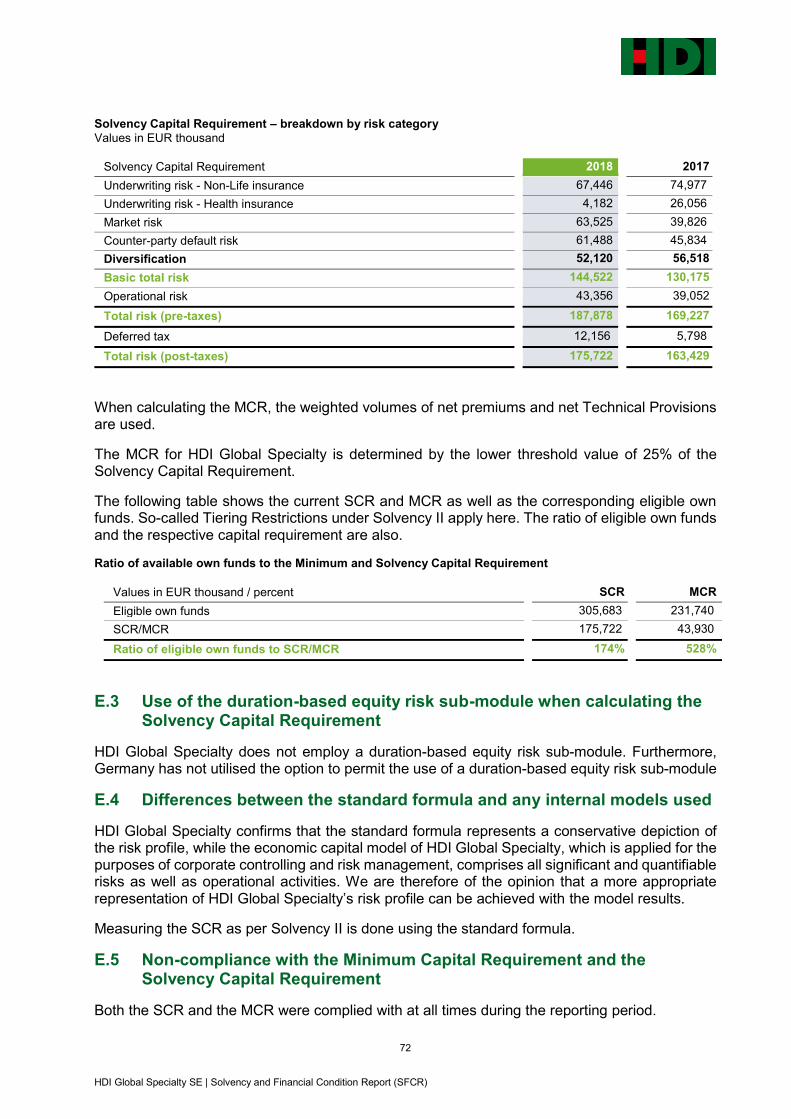

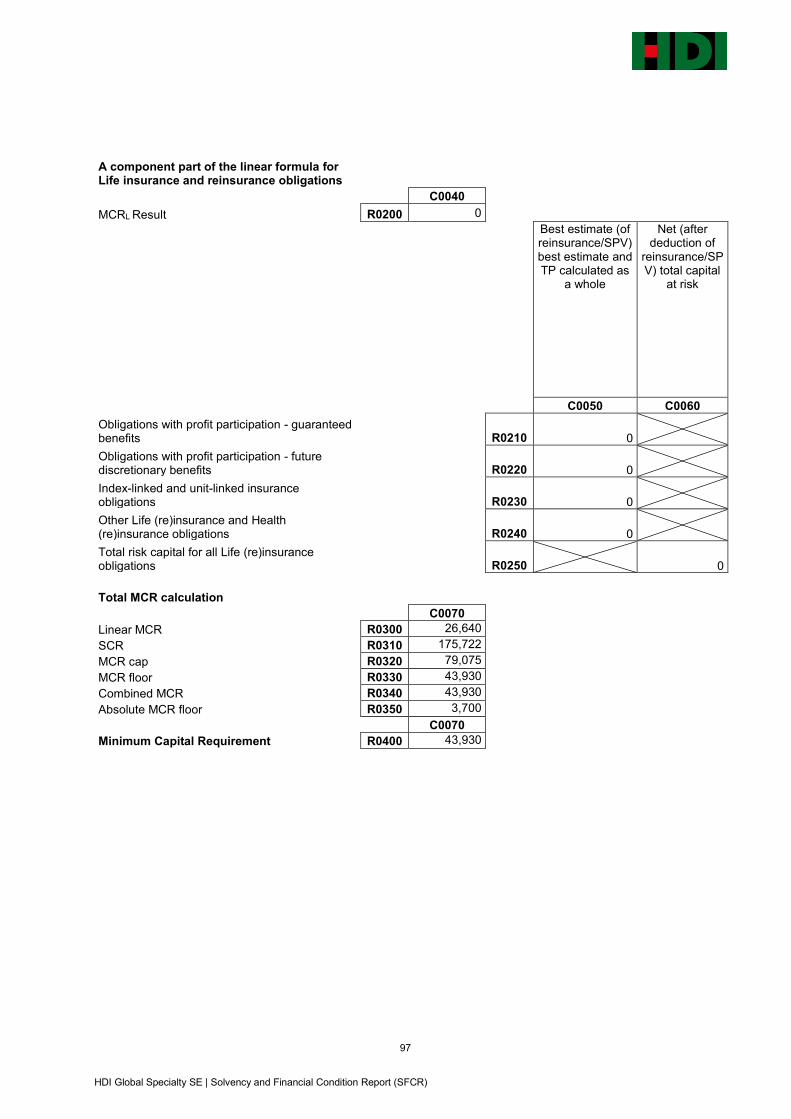

Solvency Capital Requirement 175,722 163,429

Minimum Capital Requirement 43,930 40,857

Coverage ratios

Ratio of eligible own funds to SCR (Solvency Ratio) 174% 175%

Ratio of eligible own funds to MCR 528% 521%

HDI Global Specialty SE (“HDI Global Specialty”) meets the Minimum Capital Requirements and Solvency Capital Requirements (hereinafter referred to as “MCR” and “SCR” respectively) stipulated by the supervisory authorities as at the reporting date of 31 December 2018 and in the financial year 2018 with a Solvency Ratio of 174%.

The principles for calculating the Solvency Ratio are explained in this document. Chapter D describes the valuation principles used to determine eligible own funds and Chapter E describes those to determine the SCR.

The Solvency II balance sheet has been audited by PricewaterhouseCoopers GmbH Wirtschaftsprüfungsgesellschaft, as required by law.

This report is a mandatory publication pursuant to Section 40 of the German Insurance Supervision Act (VAG).

Note: Rounding errors of +/- one unit may occur in all tables.

7 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

A. Business activity and performance

HDI Global Specialty conducts property and casualty insurance business. Its global presence and activities across all lines of Non-Life insurance allows the company to achieve an effective risk diversification. HDI Global Specialty writes single risk business, while also working together with underwriting agencies. We write business from Hannover, where the head office of the company is situated, as well as from our branches in London (UK), Stockholm (Sweden), Sydney (Australia) and Toronto (Canada). Our branch in Milan (Italy) is currently not writing any new business. HDI Global Specialty was able to increase its premium volume during the reporting period. The 2018 financial year was satisfactory for HDI Global Specialty, taking into account the major loss events occurred. Despite an overall higher burden of claims, a positive underwriting result (according to the German Commercial Code (HGB)) of EUR 7,558 thousand could be achieved. We are satisfied with the performance of our investments during the reporting period. Ordinary investment income developed as expected. The financial year ended with a loss of EUR 20,500 thousand (previous year: loss of EUR 9,200k) each before profit transfer or loss absorption and before allocation to the statutory reserve.

Details on the business and performance can be found in Section A.

Apart from the listed developments, there were no significant changes in business performance.

B. System of governance

HDI Global Specialty operates an effective system of governance which enables the company to achieve the goals for its business and risk strategy. Written guidelines are available for all significant business transactions. The key functions pursuant to Section 26 and Sections 29- 31 of the German Insurance Supervision Act (VAG) have been set up, entrusted with the tasks described, equipped with necessary powers and staffed with appropriate resources.

Both the Internal Control System and the Risk Management System are consistent with the complexity of the business. The remuneration system is based on the goal of sustainable performance.

Apart from monitoring the internal risk management and control system, the system of governance also comprises the ORSA process (process of the company's Own Risk and Solvency Assessment). The Executive Board confirmed the ORSA process was carried out in the reporting period and approved the ORSA report. At present, the Executive Board of HDI Global Specialty does not see any risks that might either endanger the continued existence of the company in the short or medium term or, in the long term that may significantly impair its net assets, financial position and results of operations.

The business model employed by HDI Global Specialty includes collaboration with underwriting agencies and third party administrators and envisages comprehensive outsourcing activities. Furthermore, activities are outsourced to Hannover Re in order to achieve a high level of integration into the Hannover Re Group. Amended guidelines were approved and corresponding processes implemented. Three key outsourcing activities were undertaken.

The Executive Board and the key function holders have commissioned the Risk Committee with conducting an assessment of the system of governance. The Risk Committee and the key function holders has reached the conclusion that the system of governance at HDI Global Specialty is, in terms of its type, scope and complexity, appropriate for the inherent risks of its business activities.

8 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

A major change in the system of governance occurred as a result of the Executive Board expansion to four members and the associated revision of the schedule of responsibilities.

The individual elements of the system of governance system at HDI Global Specialty are explained in Section B.

C. Risk profile

In the context of its business operations, HDI Global Specialty enters into a broad variety of risks. These risks are deliberately accepted, steered and monitored. They specifically concern underwriting risks pertaining to Property and Casualty insurance, as well as capital market risks, liquidity risks and counter-party default risks. Operational, strategic and reputational risks also arise in the course of business operations. We describe the cause of these risks and how we deal with them in Section C. We also explain how we handle potential future risks (emerging risks).

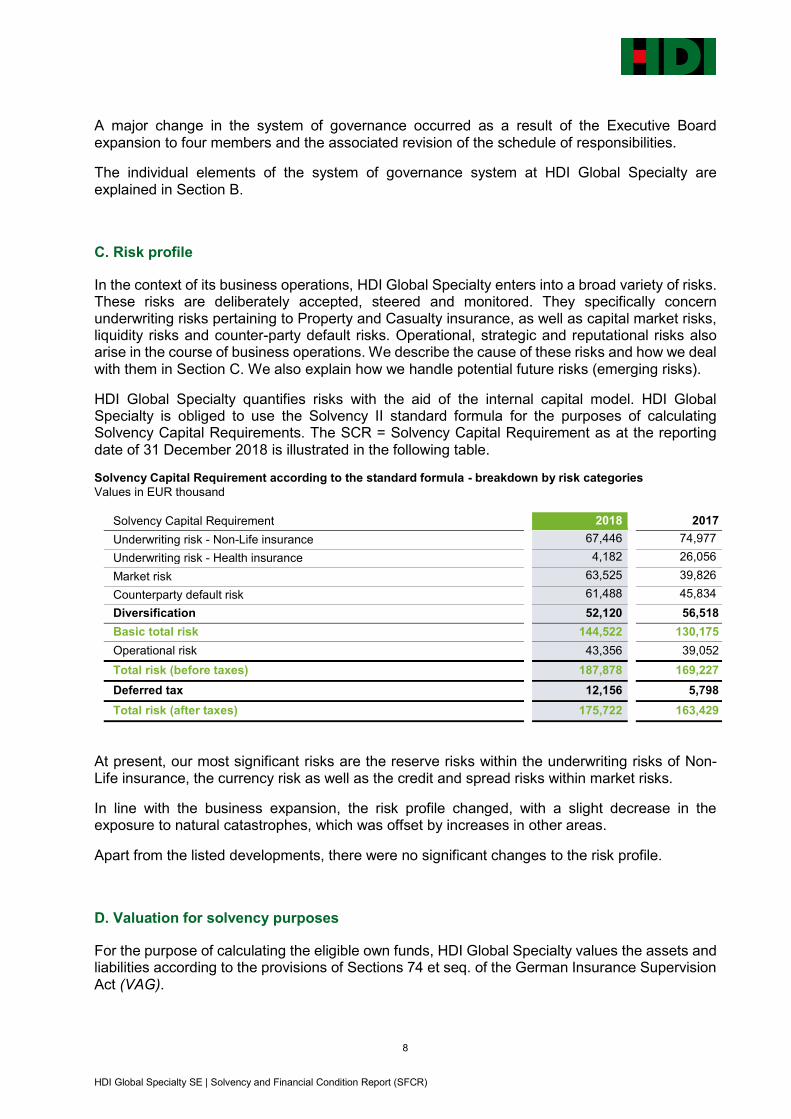

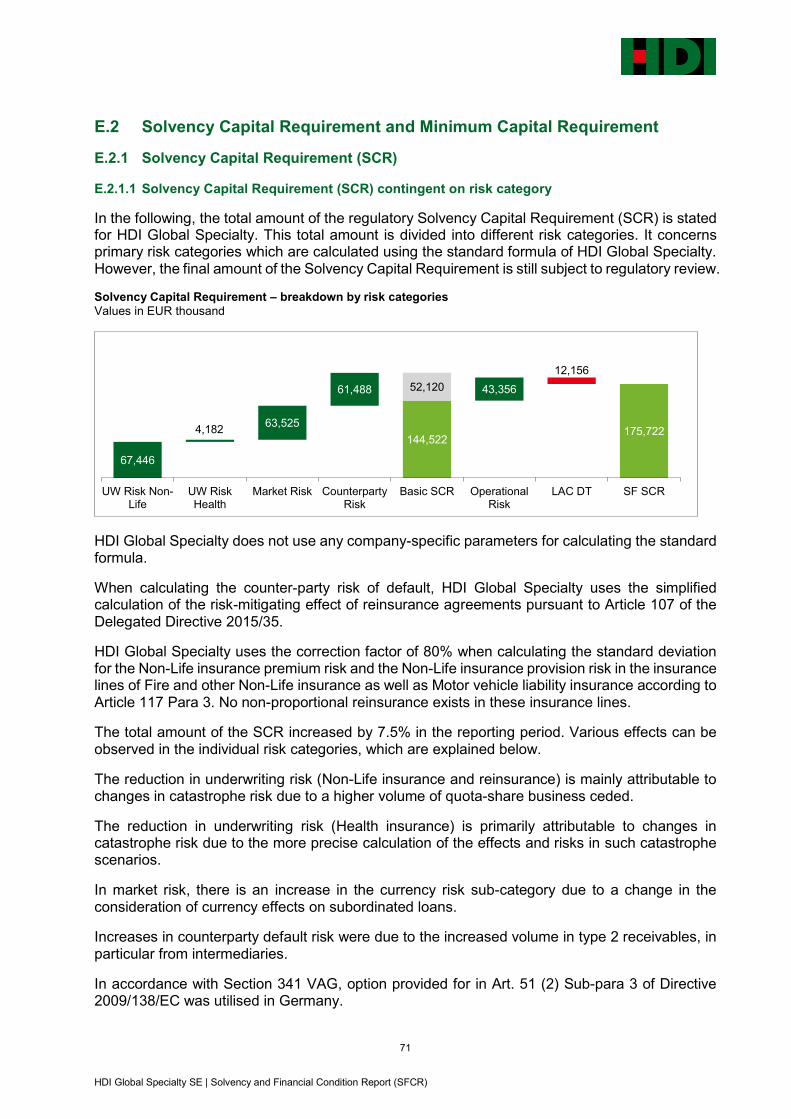

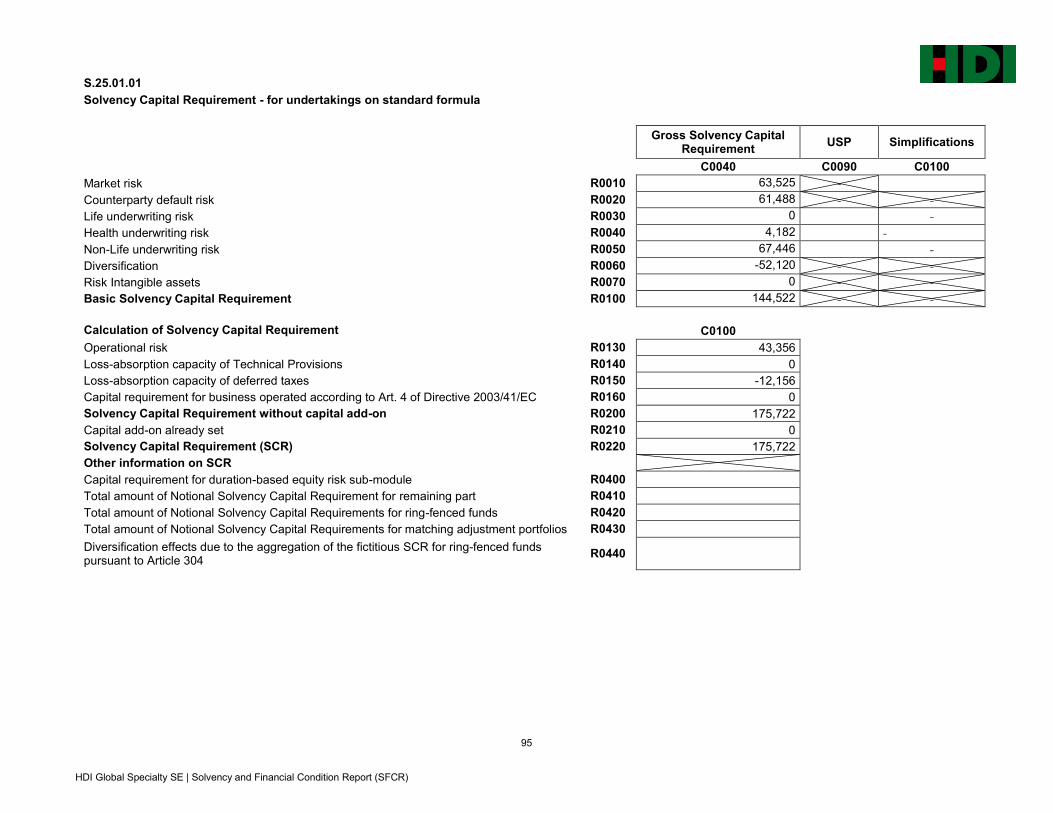

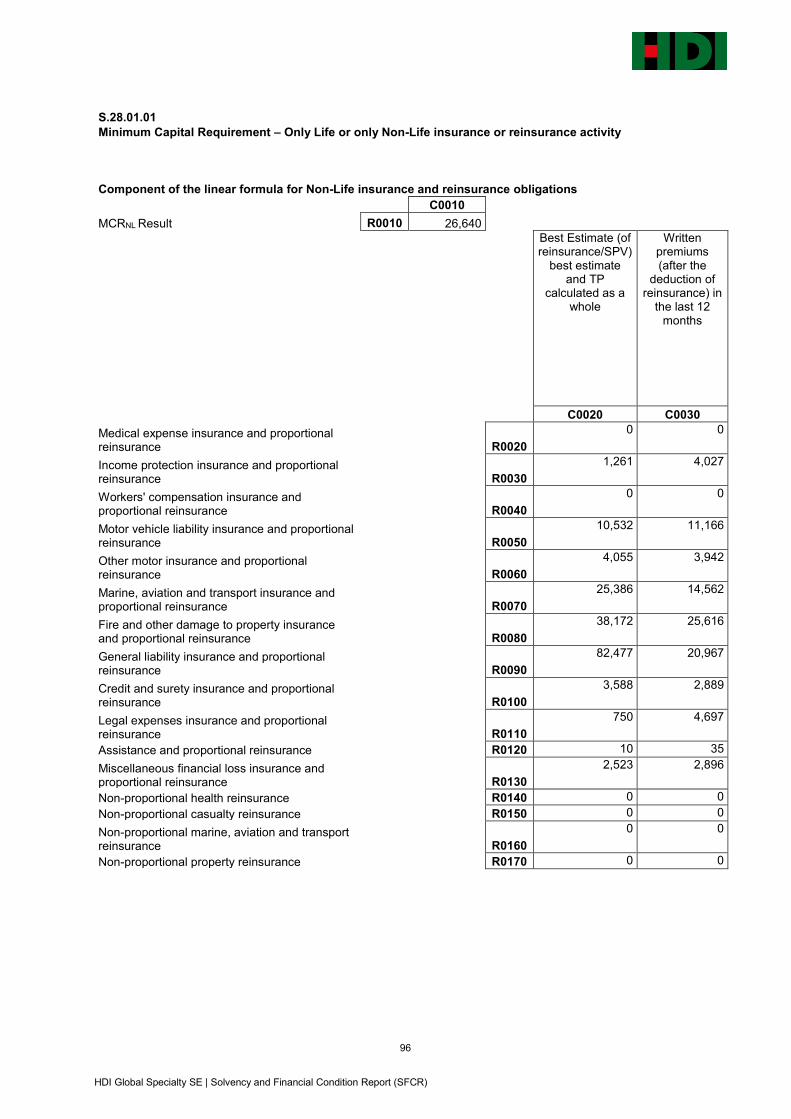

HDI Global Specialty quantifies risks with the aid of the internal capital model. HDI Global Specialty is obliged to use the Solvency II standard formula for the purposes of calculating Solvency Capital Requirements. The SCR = Solvency Capital Requirement as at the reporting date of 31 December 2018 is illustrated in the following table.

Solvency Capital Requirement according to the standard formula - breakdown by risk categories

Values in EUR thousand

Solvency Capital Requirement 2018 2017

Underwriting risk - Non-Life insurance 67,446 74,977

Underwriting risk - Health insurance 4,182 26,056

Market risk 63,525 39,826

Counterparty default risk 61,488 45,834

Diversification 52,120 56,518

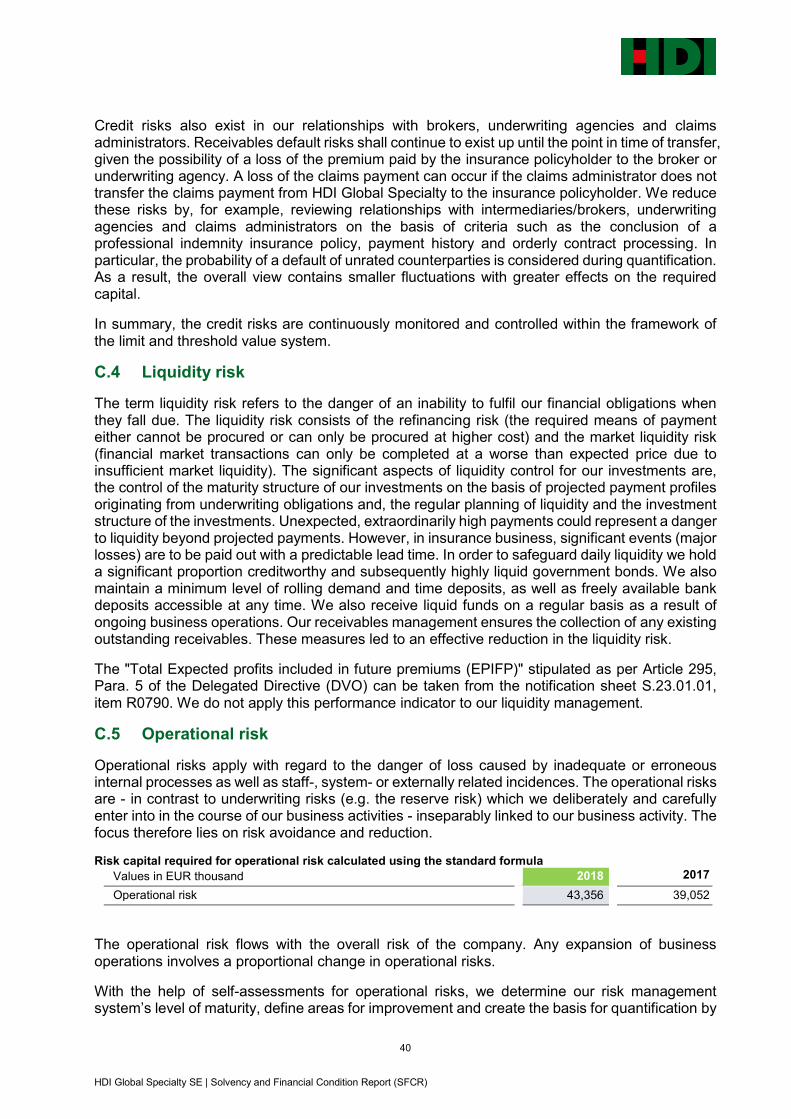

Basic total risk 144,522 130,175

Operational risk 43,356 39,052

Total risk (before taxes) 187,878 169,227

Deferred tax 12,156 5,798

Total risk (after taxes) 175,722 163,429

At present, our most significant risks are the reserve risks within the underwriting risks of Non-Life insurance, the currency risk as well as the credit and spread risks within market risks.

In line with the business expansion, the risk profile changed, with a slight decrease in the exposure to natural catastrophes, which was offset by increases in other areas.

Apart from the listed developments, there were no significant changes to the risk profile.

D. Valuation for solvency purposes

For the purpose of calculating the eligible own funds, HDI Global Specialty values the assets and liabilities according to the provisions of Sections 74 et seq. of the German Insurance Supervision Act (VAG).

9 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

The valuation for solvency purposes is set as a principle at the fair value (market value). Insofar as IFRS values appropriately reflect the fair value, they shall be applied.

Technical Provisions pursuant to Solvency II definitions differentiate significantly from the definition of provisions pursuant to the German Commercial Code (HGB) both in terms of structure and in relation to the calculations; cf. Section D.2.

HDI Global Specialty does not currently use any adjustments to the interest yield curves prescribed by the EIOPA and no transitional measures pursuant to Sections 80, 82, 351 and 352 VAG.

There were no significant changes in the reporting period.

E. Capital management

HDI Global Specialty endeavours at all times to maintain a Solvency Ratio of at least 120%, and thus exceed the requirement of 100% stipulated by the supervisory authorities. In addition, a threshold value of 140% has been defined. If the Solvency Ratio falls below this threshold value, HDI Global Specialty will adopt capital measures aimed at either strengthening the company’s equity or reducing the risk capital, or both.

The Solvency Ratio is continuously monitored. Any changes are taken into account as part of planning and potential changes in the Solvency Ratio, which can be caused by larger transactions, are examined ahead of time. During the financial year 2018, there was no breach of the threshold value of 140%. Further information on the calculation of the Solvency Ratio can be found in Section E.

The own funds consist of basic own funds, which comprise the excess of assets over liabilities and subordinated loans. No ancillary own funds are utilised.

HDI Global Specialty’s own funds grew according to schedule over the course of the reporting period as a result of the excesses generated. An overwhelming share of the total eligible own funds falls within the highest quality level (tier 1). The remaining shareholder’s equity is held by HDI Global Specialty in the subordinated loans, which are classified as tier 2.

The total Solvency Capital Requirement calculated according to the standard formula increased by 7.5% during the reporting period. Various changes can be observed in the individual risk categories, which are explained in Chapter E.

HDI Global Specialty uses the standard formula for calculating the Solvency Capital Requirement. The internal model is applied in a broad range of company management and decision-making processes. The future development of the SCR and MCR is forecast at regular intervals as part of the planning process.

Apart from the listed developments, there were no significant changes in capital management.

10 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

A. Business activities and performance

A.1 Business activity

A.1.1 Business model

HDI Global Specialty (formerly Inter Hannover) achieved a gross premium volume of approximately EUR 946,760 thousand in the calendar year 2019, a result that is significantly above the previous year's level of EUR 831,263 thousand. We operate within the market segment of Non-Life insurance.

We write Single risk business while also working together with underwriting agencies (underwriting agents). In addition to our headquarters in Hannover, we also write business in our branches in London (UK), Stockholm (Sweden), Sydney (Australia) and Toronto (Canada). Our branch in Milan (Italy) is currently not writing any new business. The focus of our strategy is on short-term business. Moreover, we also offer specialist coverage in niche areas. We strive to achieve the overarching Group objective: "long-term success in a competitive business". The entirety of our business activities is focused on being the best possible option for our business partners when choosing the primary insurance partner. For this reason our focus is on the customer and their needs.

We achieve competitive advantages for the benefit of our customers and shareholders, by keeping our administrative costs for our insurance business lower than those of our competitors. We aim to be a high yield top-performing company, while also being able to offer our customers direct insurance protection at affordable conditions.

We balance risks effectively through the broad diversification of our portfolio. In doing so, we ensure that the different risks do not fully correlate on an intra-country basis.

We are tasked with steering HDI Global Specialty within the scope of a clearly defined risk appetite in order to exploit business opportunities while securing our long-term risk bearing capacity.

We also operate in selected market segments and niche reinsurance business in addition to our core business of direct insurance..

In the Non-Life insurance segment, we see ourselves as a reliable, flexible and innovative partner. Effective cycle management and outstanding risk management are key elements of our competitive positioning, in addition to the objective of cost leadership.

A.1.2 Profit situation and key transactions

We are satisfied with the course of business in 2018 in spite of the continuing intensely competitive market conditions and an unusually high number of major losses occurring. . Although rates continued to decrease in the majority of markets during the financial year, HDI Global Specialty was able to realise profitable insurance business opportunities. On balance, we have continued our risk adequate and selective underwriting policy, and have consistently distanced ourselves from business operations that did not meet our demands. Fortunately, we were able to increase the premium income compared with the previous year’s level.

The gross premium volume in the financial year amounted to EUR 946,760 thousand, and is thus clearly above the level in the previous year (EUR 831,263 thousand). The overwhelming share - at EUR 850,500 thousand (previous year: EUR 763,000 thousand) - is attributable to the direct insurance business. Our business operations were also supplemented to a limited extent by assumed reinsurance business. The gross premiums written for assumed reinsurance business amounted to EUR 96,200 thousand (previous year: EUR 68,300 thousand).

11 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

The branches continued to make a significant contribution to the gross premium income with a total of 79.1% (previous year: 82.2%) or EUR 748,400 thousand (previous year: EUR 683,300 thousand), which underscores the international positioning of HDI Global Specialty.

During the financial year 2019, we registered premiums of EUR 373,300 thousand (previous year: EUR 368,100 thousand) through the branch in London. We took advantage of new business opportunities and further expanded our business with existing customers. On the other hand, we consistently distanced ourselves from business operations that did not meet our demands. As expected, the overall premium volume remained almost constant. The Stockholm branch registered gross premiums of EUR 230,900 thousand in the financial year 2018 (previous year: EUR 198,500 thousand) and, hence, was able to maintain its market position in spite of intense competition. We were also able to expand our business activities at the Hannover location and registered EUR 198,300 thousand (previous year: EUR 148,000 thousand). Our company location in Sydney experienced a very positive development where we were able to significantly increase the gross premium written from EUR 62,300 thousand to EUR 81,400 thousand, thanks to some new business relationships. After a short consolidation phase in Canada, we were able to increase the gross premiums written at our branch in Toronto to EUR 62,900 thousand (previous year: EUR 54,400 thousand).

We ceded a significant share of our business to Hannover Re Group in line with our strategy. We also utilised external reinsurance to a limited extent, in order to establish optimal control our risks. With gross premiums earnings at EUR 895,600 thousand (previous year: EUR 798,400 thousand), the earned premiums for our own account stand at EUR 78,900 thousand (previous year: EUR 65,400 thousand).

As there were a lower number of major loss events, the (gross) financial loss ratio improved compared with the previous year and we were able to achieve a ratio of 65.6% (previous year: 69.6.%). Gross expenses for insurance claims therefore stand at EUR 587,600 thousand (previous year: EUR 555,800 thousand).

Gross expenses for insurance operations stands at EUR 275,300 thousand (previous year: EUR 233,700 thousand) or 30.7% (previous year: 29.3%).

The combined loss-expense ratio (gross) stands at 96.4% (previous year: 98.9%).

The equalisation provision and similar provisions were allocated in accordance with the statutory regulations to the amount of EUR 12,300 thousand (previous year: EUR 3,600 thousand). We have filled the historical observation period – which serves as the basis for the calculation of the equalisation provision - with the loss ratios from the tables published by the German Federal Financial Supervisory Authority (BaFin) for the insurance industry, insofar as was necessary and in line with statutory regulations. Subsequently, the balance sheet value of the equalisation provision and similar provisions stood at EUR 22,500 thousand (previous year: EUR 10,200 thousand). On balance, we achieved an underwriting result for our own account of EUR -4,500 thousand in the past financial year (previous year: EUR 6,600 thousand).

Current income from investments in the reporting year amounted to EUR 4,479 thousand (previous year: EUR 8,716 thousand) and was attributable, with a value of EUR 41 thousand (previous year: EUR 4,001 thousand), to income from participations and, with a value og EUR 4,438 thousand (previous year: EUR 4,715 thousand) to current interest received from bearer bonds and other fixed-interest securities.

The result from the disposal of investments amounted to EUR -431 thousand (previous year: EUR -1,388 thousand) and comprised the profits from the disposal of investments amounting to EUR 340 thousand (previous year: EUR 543 thousand) and losses from the disposal of investments amounting to EUR 771 thousand (previous year: EUR 1,931 thousand). The result

12 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

from the disposal is exclusively attributable to disposals of bearer bonds and other fixed-interest securities. Depreciation on investments amounted to EUR 1,204 thousand (previous year: EUR 1,583 thousand) and are predominantly attributable to bearer bonds and other fixed-interest securities, which were recognised according to the strict lowest value principle. The write-ups on investments, for which write-downs were made in the previous year, stand at EUR 337 thousand (previous year: EUR 110 thousand).

Investment management during the financial year generated expenses amounting to EUR 586 thousand (previous year: EUR 604 thousand).

In total, the net investment income amounted to EUR 2,595 thousand (previous year: EUR 5,252 thousand).

Other income comprised the other earnings amounting to EUR 11,223 thousand (previous year: EUR 8,588 thousand) and other expenses of EUR 27,247 thousand (previous year: EUR 28,366 thousand), which on balance generated a loss amounting to EUR 16,024 thousand (previous year: loss of EUR 19,748 thousand) for other income.

The financial year was completed with a net loss of EUR 20,500 thousand (previous year: loss of EUR 9,200 thousand) before the respective transfer of profit or loss and before allocation to the statutory reserve. The loss is fully covered by the current controlling and profit transfer agreement. The profit transfer stood at EUR 0 as in the previous year.

A.1.3 Headquarters, supervisor and auditor

HDI Global Specialty is a European Company, i.e. Societas Europaea (SE), with its headquarters located in Roderbruchstrasse 26, 30655 Hannover, Germany, and has been entered in the Commercial Register of the District Court of Hannover under the number HRB 211924. During the reporting year, 100% of HDI Global Specialty’s shares were held by Hannover Rück SE, Hannover ("Hannover Re"), having its registered office at Karl-Wiechert-Allee 50, 30625 Hannover, Germany. Talanx AG, Hannover, is the majority owner of Hannover Re with a shareholding of 50.2%, which in turn belongs to HDI Haftpflichtverband der Deutschen Industrie V.a.G. (HDI), Hannover with a 79% share.

HDI Global Specialty is regulated by the German Federal Financial Supervisory Authority (BaFin), located in Graurheindorfer Strasse 108, 53117 Bonn, Germany, as the responsible supervisory authority.

The appointed auditor for HDI Global Specialty within the meaning of Section 318 of the German Commercial Code (HGB) is PricewaterhouseCoopers GmbH Wirtschaftsprüfungsgesellschaft, located Fuhrberger Strasse 5, 30625 Hannover.

A.1.4 Group structure

This report refers to HDI Global Specialty as an individual company. Since HDI Global Specialty also operates as a subsidiary in a group, we provide information in this section about the group.

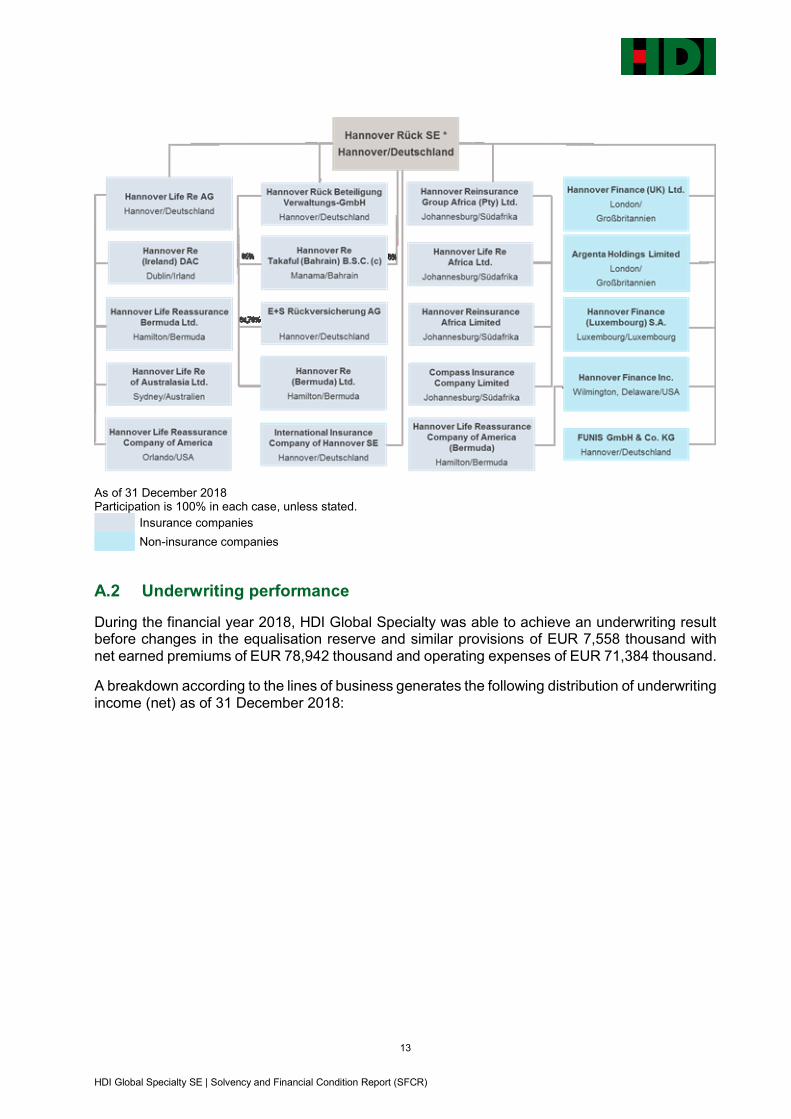

Hannover Re and its subsidiaries (together the "Hannover Re Group") operate all lines of Non-Life and Life reinsurance worldwide.

The infrastructure of Hannover Re consists of more than 130 subsidiaries and investment companies, branches and representative offices worldwide with approximately 2,500 employees. The Group's operations in Germany are conducted by the subsidiary E+S Rückversicherung AG. HDI Global Specialty conducts primary insurance business in selected markets.

Subsidiaries of Hannover Re (selection as of 31 December 2018)

13 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

As of 31 December 2018 Participation is 100% in each case, unless stated.

Insurance companies

Non-insurance companies

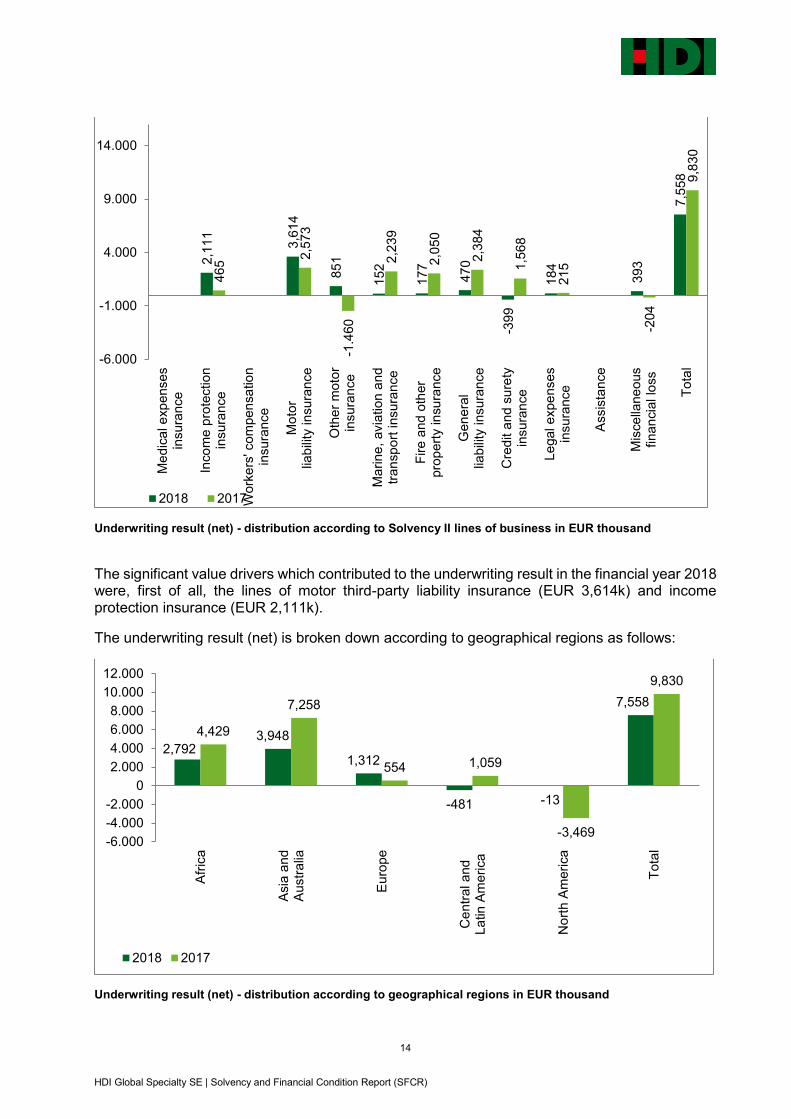

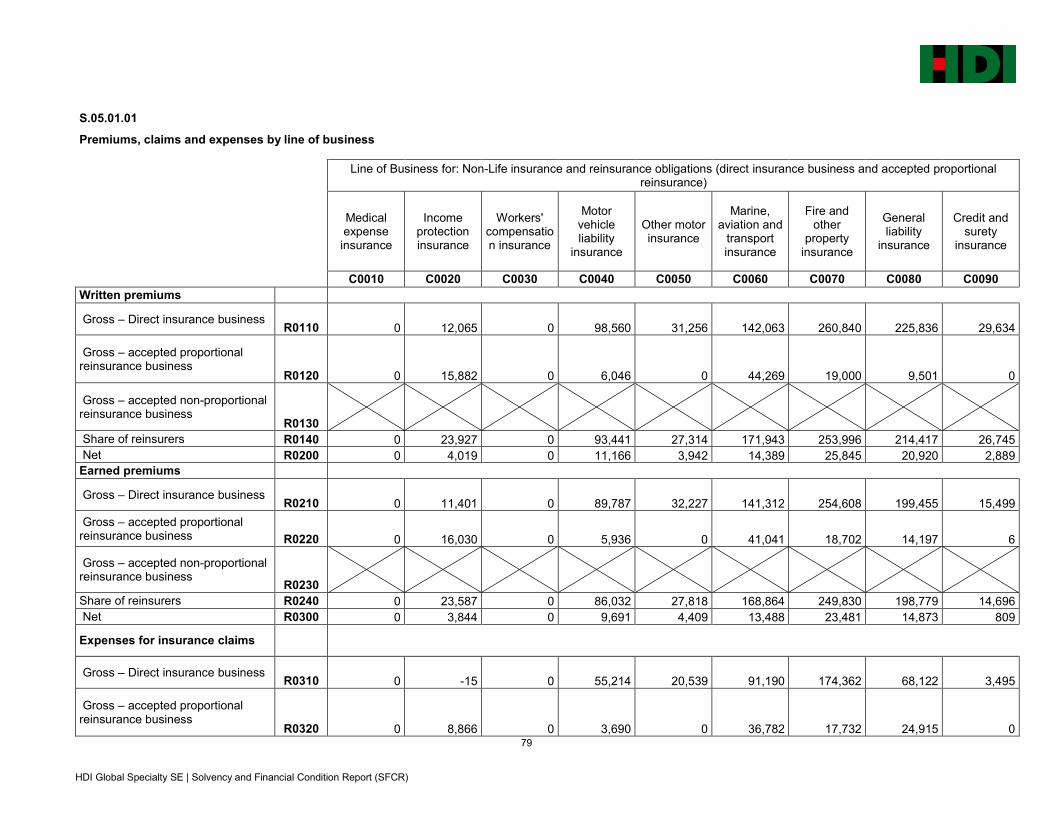

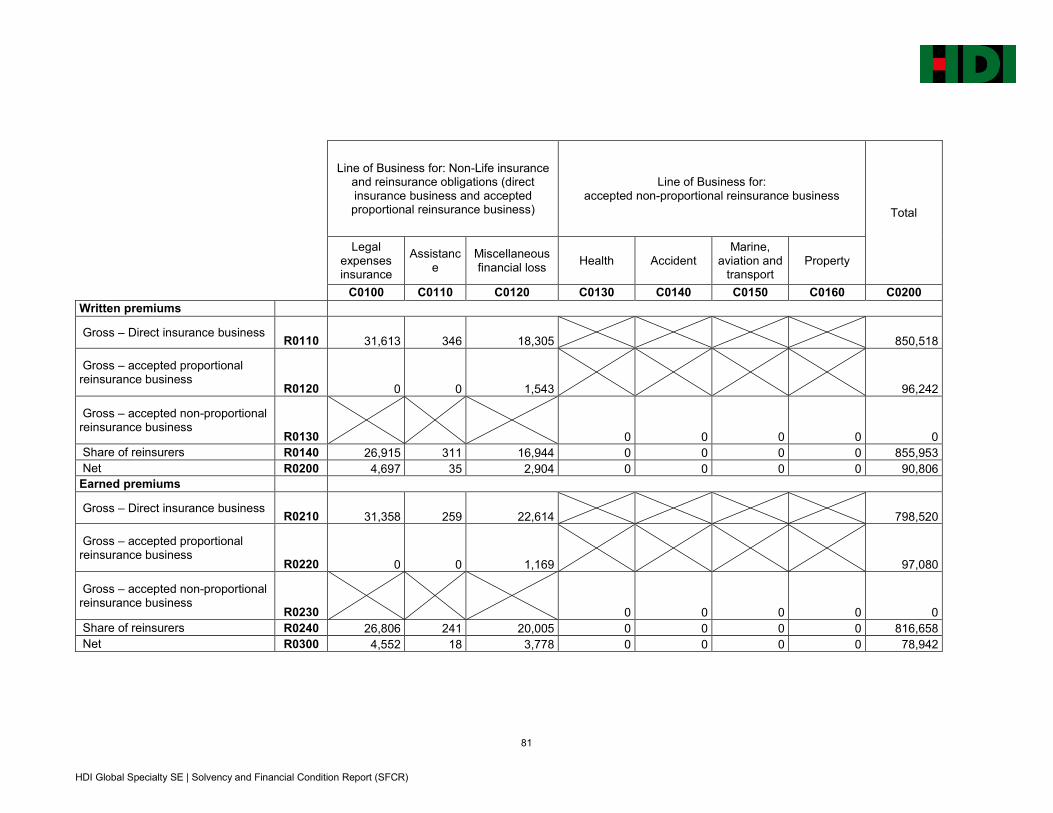

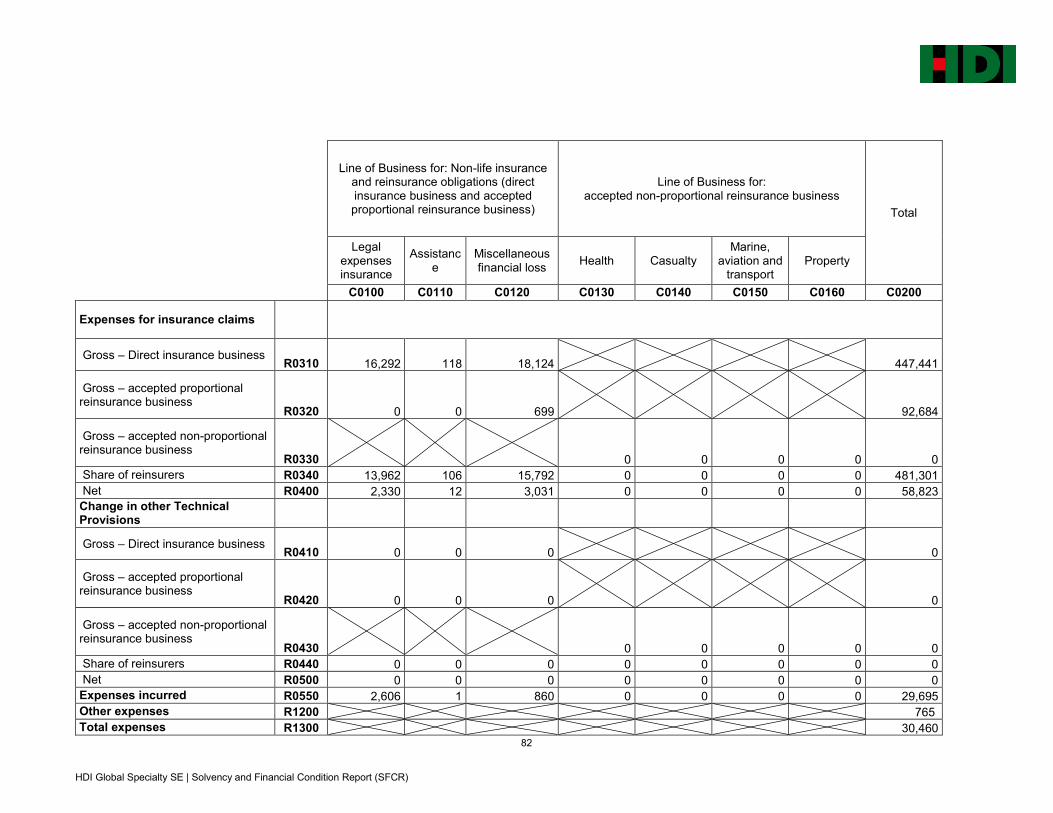

A.2 Underwriting performance

During the financial year 2018, HDI Global Specialty was able to achieve an underwriting result before changes in the equalisation reserve and similar provisions of EUR 7,558 thousand with net earned premiums of EUR 78,942 thousand and operating expenses of EUR 71,384 thousand.

A breakdown according to the lines of business generates the following distribution of underwriting income (net) as of 31 December 2018:

14 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

Underwriting result (net) - distribution according to Solvency II lines of business in EUR thousand

The significant value drivers which contributed to the underwriting result in the financial year 2018 were, first of all, the lines of motor third-party liability insurance (EUR 3,614k) and income protection insurance (EUR 2,111k).

The underwriting result (net) is broken down according to geographical regions as follows:

Underwriting result (net) - distribution according to geographical regions in EUR thousand

2,1

11

3,6

14

851

152

177

470

-399

184

393

7,5

58

465

2,5

73

-1.4

60

2,2

39

2,0

50

2,3

84

1,5

68

215

-204

9,8

30

-6.000

-1.000

4.000

9.000

14.000M

edic

al e

xp

enses

insura

nce

Inco

me p

rote

ction

insura

nce

Work

ers

' com

pen

sa

tio

nin

sura

nce

Mo

tor

liab

ility

insura

nce

Oth

er

moto

rin

sura

nce

Ma

rine

, avia

tion a

nd

tran

sp

ort

insura

nce

Fire

and

oth

er

pro

pert

y in

su

rance

Gen

era

llia

bili

ty insura

nce

Cre

dit a

nd s

ure

tyin

sura

nce

Le

gal expe

nses

insura

nce

Assis

tance

Mis

ce

llane

ous

finan

cia

l lo

ss

Tota

l

2018 2017

2,7923,948

1,312

-481 -13

7,558

4,429

7,258

554 1,059

-3,469

9,830

-6.000

-4.000

-2.000

0

2.000

4.000

6.000

8.000

10.000

12.000

Afr

ica

Asia

and

Austr

alia

Euro

pe

Ce

ntr

al and

La

tin

Am

erica

No

rth

Am

eri

ca

Tota

l

2018 2017

15 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

Measured against the overall underwriting result during the financial year 2018, the regions of Asia and Australia (EUR 3,948k) and Africa (EUR 2,792k) made the most significant value contributions for HDI Global Specialty. Central and Latin America (EUR -481k) have, by contrast, delivered a negative result.

A.3 Investment income

As an insurance company, we naturally focus primarily on our value retention when managing our capital investments and attach great importance to the stability of the resulting returns. For this reason, we align our investment portfolio with the principles of a balanced risk/return ratio and a broad level of diversification. With a low-risk mix overall, our capital investments reflect both the currency composition and maturity structure of our liabilities. Our portfolio predominantly comprises fixed-interest securities and does not contain instruments subject to securitisation. Credit, spread and currency risks subsequently represent a significant contribution to market risk.

The development of investments in the reporting period aligned with our expectations. Although, in light of continued low interest rates and the global economic development being characterised by diverse uncertainties and risks, the year under review was once again a challenging one, we were spared from any defaults in our fixed-income portfolio. Ordinary investment income developed in line with our expectations.

Income from the disposal of investments is predominantly attributable to our normal business activities.

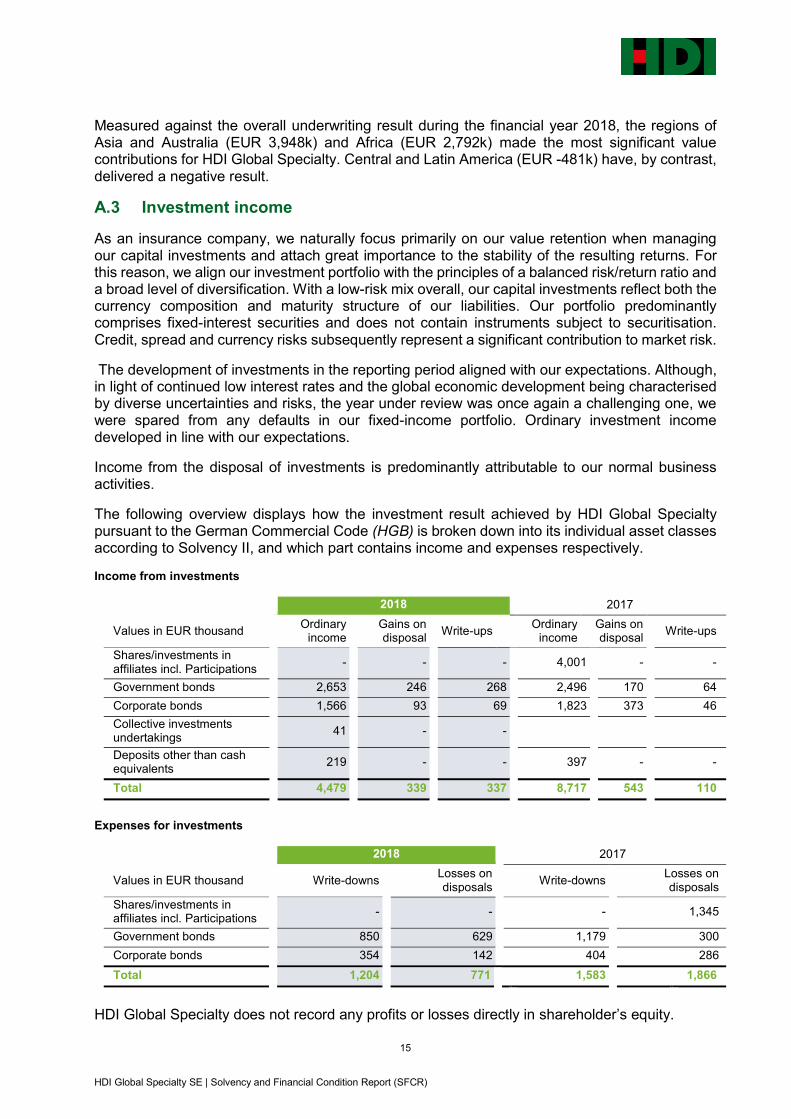

The following overview displays how the investment result achieved by HDI Global Specialty pursuant to the German Commercial Code (HGB) is broken down into its individual asset classes according to Solvency II, and which part contains income and expenses respectively.

Income from investments

2018 2017

Values in EUR thousand Ordinary

income Gains on disposal

Write-ups Ordinary

income Gains on disposal

Write-ups

Shares/investments in affiliates incl. Participations

- - - 4,001 - -

Government bonds 2,653 246 268 2,496 170 64

Corporate bonds 1,566 93 69 1,823 373 46

Collective investments undertakings

41 - -

Deposits other than cash equivalents

219 - - 397 - -

Total 4,479 339 337 8,717 543 110

Expenses for investments

2018 2017

Values in EUR thousand Write-downs Losses on disposals

Write-downs Losses on disposals

Shares/investments in affiliates incl. Participations

- - - 1,345

Government bonds 850 629 1,179 300

Corporate bonds 354 142 404 286

Total 1,204 771 1,583 1,866

HDI Global Specialty does not record any profits or losses directly in shareholder’s equity.

16 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

A.4 Performance of other activities

A.4.1 Other income and expenses

Other income and expenses are presented in the following tables. Information is stated in line with the German Commercial Code (HGB).

Other result

Values in EUR thousand 2018 2017

Other income 2,607 8,588

Other expenses 14,779 28,336

Other result -12,172 -19,748

Other expenses predominantly include staff and material expenses, which cannot be allocated to the functional divisions as well as expenses affecting the company as a whole such as, for example, remuneration for the annual financial statement audit.

A.5 Other information

Other information with a significant influence on the business activities and performance of HDI Global Specialty is not available.

17 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

B. System of governance

B.1 General information on the system of governance

B.1.1 Governance structure

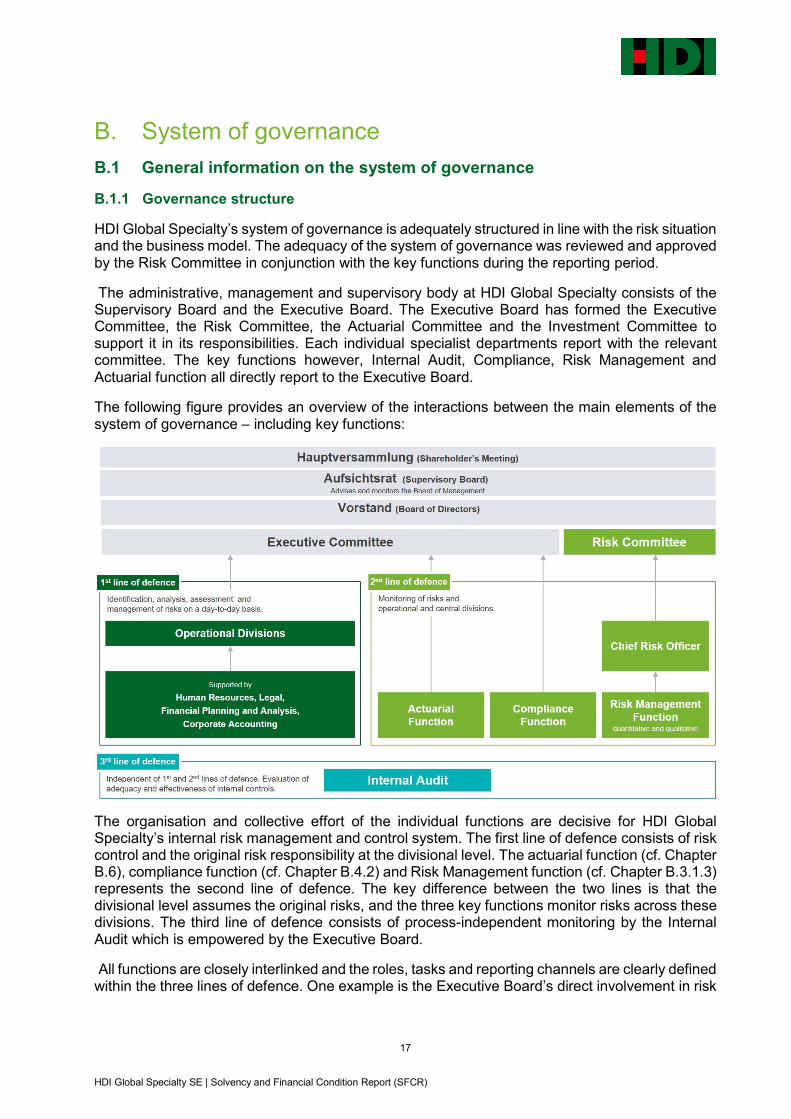

HDI Global Specialty’s system of governance is adequately structured in line with the risk situation and the business model. The adequacy of the system of governance was reviewed and approved by the Risk Committee in conjunction with the key functions during the reporting period.

The administrative, management and supervisory body at HDI Global Specialty consists of the Supervisory Board and the Executive Board. The Executive Board has formed the Executive Committee, the Risk Committee, the Actuarial Committee and the Investment Committee to support it in its responsibilities. Each individual specialist departments report with the relevant committee. The key functions however, Internal Audit, Compliance, Risk Management and Actuarial function all directly report to the Executive Board.

The following figure provides an overview of the interactions between the main elements of the system of governance – including key functions:

The organisation and collective effort of the individual functions are decisive for HDI Global Specialty’s internal risk management and control system. The first line of defence consists of risk control and the original risk responsibility at the divisional level. The actuarial function (cf. Chapter B.6), compliance function (cf. Chapter B.4.2) and Risk Management function (cf. Chapter B.3.1.3) represents the second line of defence. The key difference between the two lines is that the divisional level assumes the original risks, and the three key functions monitor risks across these divisions. The third line of defence consists of process-independent monitoring by the Internal Audit which is empowered by the Executive Board.

All functions are closely interlinked and the roles, tasks and reporting channels are clearly defined within the three lines of defence. One example is the Executive Board’s direct involvement in risk

18 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

management with all members, whilst also being represented in the Risk Committee with the Chief Risk Officer being a member of the Executive Board.

Supervisory Board

The Supervisory Board of HDI Global Specialty consists of three members who also actively involved in the management bodies of other Group companies. In the last reporting period, the Supervisory Board held three Supervisory Board meetings.

The primary task of the Supervisory Board is to monitor the management of the company and supervise its management activities of the Executive Board at HDI Global Specialty. Such monitoring includes reviewing the accounting process, the effectiveness of the Internal Control System, the risk management as well as the internal audit system. The Supervisory Board also monitors of the audit of the annual financial statements. Along with the reviewing the annual financial statements, the Supervisory Board also reviews the management report and the proposal for the declaration of dividends, where relevant, but also reserves the right to appoint the auditor and submit the audit application.

In addition, the Supervisory Board enjoys the right to reserve approval for measures and business activities conducted by the Executive Board such as, changes to the strategic principles, the adoption of annual results planning or the conclusion or termination of company agreements as well as significant cooperation agreements.

Executive Board

The Executive Board of HDI Global Specialty was comprised of three members until 31 July 2018. On 01 August 2018, Richard Taylor was appointed to as an additional member of the Executive Board as the Chief Marketing Officer. Normally, twelve ordinary Board meetings are held in each calendar year, which can be supplemented by extraordinary meetings as required.

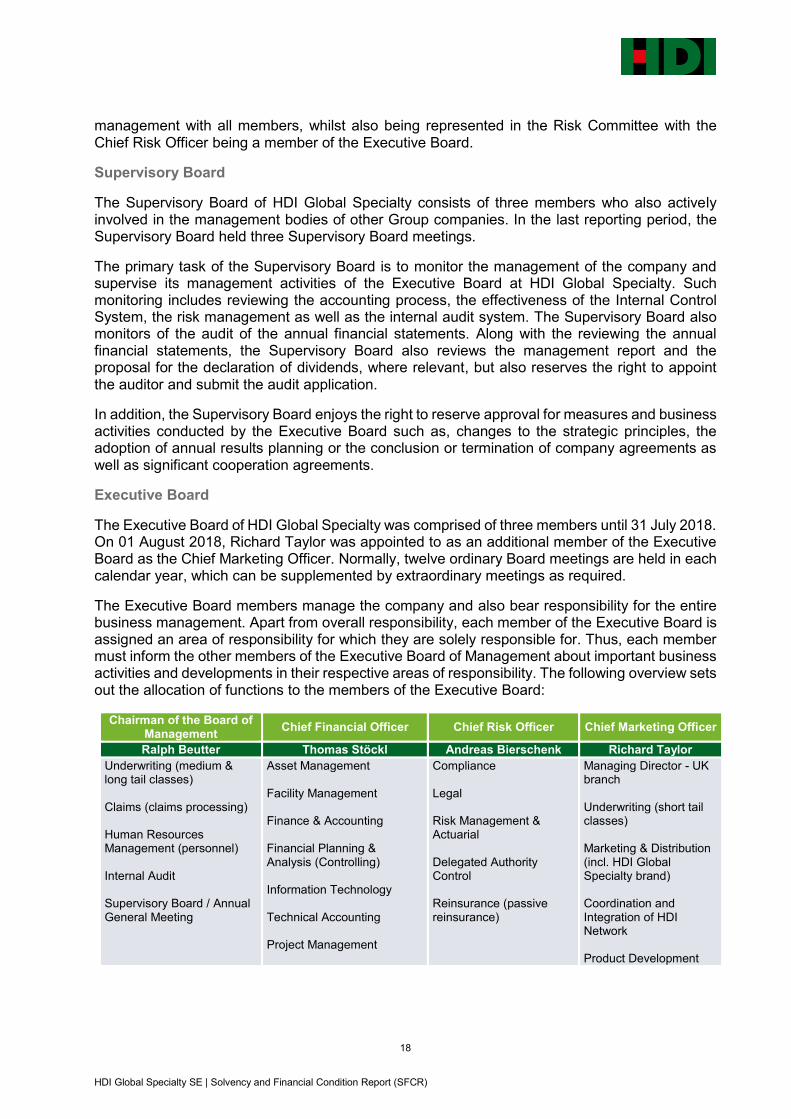

The Executive Board members manage the company and also bear responsibility for the entire business management. Apart from overall responsibility, each member of the Executive Board is assigned an area of responsibility for which they are solely responsible for. Thus, each member must inform the other members of the Executive Board of Management about important business activities and developments in their respective areas of responsibility. The following overview sets out the allocation of functions to the members of the Executive Board:

Chairman of the Board of Management

Chief Financial Officer Chief Risk Officer Chief Marketing Officer

Ralph Beutter Thomas Stöckl Andreas Bierschenk Richard Taylor

Underwriting (medium & long tail classes) Claims (claims processing) Human Resources Management (personnel) Internal Audit Supervisory Board / Annual General Meeting

Asset Management Facility Management Finance & Accounting Financial Planning & Analysis (Controlling) Information Technology Technical Accounting Project Management

Compliance Legal Risk Management & Actuarial Delegated Authority Control Reinsurance (passive reinsurance)

Managing Director - UK branch Underwriting (short tail classes) Marketing & Distribution (incl. HDI Global Specialty brand) Coordination and Integration of HDI Network Product Development

19 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

The main tasks of the Executive Board include reporting to the Supervisory Board. The Supervisory Board is informed by the Executive Board in writing about the business development and the risk situation of the company. Moreover, the Executive Board of Management is responsible for deciding on certain business activities. These decision-making responsibilities derive from statutory law, the Articles of Association or the Procedure Rules of HDI Global Specialty and include, for example, the preparation and submission of the annual financial statements, the approval of resolutions raised in the Annual General Meeting as well as the establishment of a monitoring system to identify developments as soon as possible that could jeopardise the existence of the company.

Committees of the Executive Board

HDI Global Specialty’s business policy is based on the principle of "delegation of responsibility"; to delegate the decision-making capabilities of the Executive Board to the lowest functional level possible. To achieve this, the Executive Board established the Risk Committee, the Executive Committee, the Actuarial Committee and the Investment Committee.

The Risk Committee advises the Executive Board on implementing risk-reducing measures in keeping with the business strategy and the business plan of HDI Global Specialty. In addition, the Risk Committee supports the Executive Board in ensuring the effective implementation of the risk management system and in performing the annual evaluation of the business organisation. The Risk Committee also checks how risk-based considerations are dealt with in internal rules and guidelines.

The main task of the Executive Committee is to support the Executive Board in the day-to-day management of operational activities. This Committee also ensures that effective and clear reporting lines are established and adhered to within the business organisation. To achieve these goals throughout HDI Global Specialty, the heads of the two largest branches in London and Stockholm join the four Executive Board Members to make up the members of the Executive Committee.

The Actuarial Committee is tasked with assisting the Executive Board to determine appropriate reserves and in reviewing the calculation of reserves. Further, this committee supports the Executive Board of Management in determining reserves for major losses and in reviewing the pricing strategy.

The Investment Committee is responsible for implementating the current investment guideline and assisting the Executive Board of Management with making investment decisions. Another task is monitoring the securities portfolio and reporting on its performance.

Key functions

HDI Global Specialty has four key functions. These are the Compliance function, the Risk Management function, the Actuarial function and the Internal Audit function, the key functions have been provided with adequate resources, in order to fulfil their tasks.

The key functions directly report to the Executive Board, which also requests regular and ad-hoc reports from these functions on their activities and internal assessments. Written guidelines ensure the proper allocation of tasks to the key functions and help establish the necessary authorisations for the fulfilment of the requirements placed upon them. The operational independence of the key functions is safeguarded by the system of governance to incorporate the ”Three Lines of Defence” model.

The relevant main tasks and responsibilities are further detailed in Chapters B.3.1.3, B.4.2, B.5 and B.6.

20 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

Changes within the reporting period

In the last reporting period, Richard Taylor was appointed to the Board of Management with effect as of 01 August 2018 and, as a result, the number Executive Board members increased from three to four.

B.1.2 Remuneration policy

The remuneration strategy of HDI Global Specialty as a subsidiary of Hannover Re is geared to the goal of sustainable performance of the company and of the Group. The remuneration structure and the remuneration regulations of HDI Global Specialty are integrated in the remuneration organisation of the Hannover Re Group.

B.1.2.1 Remuneration of the Board of Management

The level and structure of the of the Executive Board remuneration at HDI Global Specialty is dictated by the size and activity of the company, its economic and financial situation, its success and future prospects, as well as the customary practice regarding remuneration taking into account a comparative environment (horizontal) and the remuneration structure, which otherwise applies to the company and the Group (vertical). Remuneration is also dictated by the tasks of the respective Executive Board member, his or her personal performance and the performance of the Full Executive Board.

In alignment with these objectives, the remuneration system exhibits two components: Fixed salary / benefits in kind as well as variable remuneration. Both positive and negative developments are accounted for when designing the variable remuneration scheme. On balance, remuneration is set in a way that it works in sync with achieving sustainable company growth, as well as being competitive and in line with the market practice. The remuneration model envisages a percentage split between fixed remuneration and variable remuneration in the event that targets are met.

The performance-related remuneration (variable remuneration) is contingent on certain predefined results and the attainment of certain targets. The objective specifications differ depending on the function of the affected Executive Board member. Variable remuneration comprises a short-term variable component, an annual cash bonus and a long-term share-based remuneration, the so-called Share Award Programme. The level of variable remuneration is determined during the Supervisory Board meeting.

B.1.2.2 Remuneration of the Supervisory Board

The members of the Supervisory Board are reimbursed for any costs incurred relating to the fulfilment of their term.

B.1.2.3 Staff and manager remuneration

The remuneration system in the management level below the Executive Board also includes variable remuneration in addition to a fixed annual salary. This comprises a short-term variable remuneration component, the annual cash bonus and a long-term share-based remuneration, the so-called Share Award Programme.

For members of staff at the levels of Chief Manager, Senior Manager and Manager, with the Group Performance Bonus (GPB) the opportunity is also granted to participate in a variable remuneration system. The GPB is a remuneration model linked to the success of the Hannover Re Group, which was introduced in 2004 and, since an amendment to the calculation basis in 2006, has remained unchanged.

21 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

For members of staff at the HDI Global Specialty branch in London working below the management levels 2 and 3, the remuneration system includes a short-term variable remuneration component in addition to the fixed annual salary. The bonus payment contingent on the branch’s result and the employee’s individual target attainment. The bonus payment is between 20% and 60% of basic salary depending on the position held by the employee.

Members of staff at the HDI Global Specialty branch in Stockholm working below the management levels 2 and 3 receive a fixed annual salary and have the opportunity to participate in a variable remuneration system under the "Profit Sharing Scheme". The bonus payment is up to 40% dependent on the economic result delivered by the Scandinavian branch overall, and up to 60% on the result of the company division in which the member of staff is employed.

B.1.3 Key transactions with associated companies and related parties

In this reporting year, the terms and conditions were amended for the grant of a subordinated loan by Hannover Re. Regulatory aspects were taken into account for the alteration.

B.2 Requirements for professional qualification and personal reliability

On 16 October 2015, the framework guideline of Hannover Re pertaining to the fulfilment of the Fit & Proper requirements in the Hannover Re Group was decreed by the Executive Board. With a resolution of 29 November 2016, the Executive Board of HDI Global Specialty (at the time known as Inter Hannover) adopted the specifications of this framework guideline.

B.2.1 Description of requirements

The professional qualification (fitness) of individuals with key tasks refers to a professional qualification suitable for the respective position as well as the skills and experience, which are necessary for a robust and cautious management approach, and for the fulfilment of the position. The appropriateness is assessed according to the principle of proportionality and takes into account the company-individual risks as along with the type and scope of the business operations. Individuals, who actually head up the company and for members of the Supervisory Board, have to comply with Specialist "fitness" requirements stemming from established supervisory practices. Collective "fitness" requirements have been established for mutual controlling and monitoring. The requirements placed on the professional qualifications of those holding key functions are closely linked to the special features of the respective governance tasks.

Individuals with key tasks must, as part of their personal reliability (propriety), act responsibly and with integrity, and carry out their activities both dutifully and with necessary level of care. Conflicts of interest must be avoided and the individual must not demonstrate a lack of reliability in the form of criminal actions prior to their nomination/ appointment. There is no requirement for personal reliability to be positively established. It will be assumed, whenever there are no observable facts indicating the contrary. Unreliability is only to be assumed if personal circumstances according to general life experience give reason to believe that this could undermine the thorough and proper exercising of the function.

For HDI Global Specialty, the circle of individuals entrusted with key tasks consists of persons who

actually head up the company (Executive Board of members, Executive Directors), including authorised representatives of an EU/EEA branch,

hold other key tasks (members of the Supervisory Board, owners of one of the key functions including Compliance, Internal Audit, Risk Management, Actuarial , individuals who have significant influence on company decision-making processes).

22 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

With regard to their various roles, these individuals are required to provide evidence of their professional qualifications in different areas as follows:

Educational background

Practical knowledge

Management experience

Language skills

Knowledge in relation to the relevant

Key function task

Collective requirements

Required specialist knowledge

In the event that key tasks are outsourced, general requirements for this are defined within the Outsourcing Guideline. HDI Global Specialty ensures that individuals deployed by the service provider who are responsible for the key task have suitable qualifications and are personally reliable. In accordance with the supervisory regulations, HDI Global Specialty appointed an Outsourcing Officer, who is subject to registration with the regulatory body accordingly as the person responsible for the relevant key function within the company. The overseeing Outsourcing Officer is responsible for the proper fulfilment of the duties associated with the outsourcing of the key task.

B.2.2 Evaluation process

The requirements and reporting processes with respect to the supervisory authority correspond to the current standard processes based on the BaFin information sheets on professional competence and reliability.

Pursuant to the framework guideline for fulfilling the Fit & Proper requirements, at the preliminary stage of recruiting new members of staff who will actually head up the company or hold other key roles, a detailed curriculum vitae will be submitted and a requirements profile set, which detail and describe the necessary qualifications. The attachment to the framework guideline contains a checklist, which is to be used in the assessment of the Fit & Proper requirements of these individuals.

The requirements profile contains evidence of the following minimum requirements:

Description of the position with key tasks:

Performance catalogue (job description)

Authority to make decisions

Level of staff responsibility

Professional qualification (general):

Level of education (commercial or job-specific training)

University degree or professional standards (such as, for example, for auditors or actuaries)

Knowledge and understanding of business strategy

Knowledge of the system of governance

Foreign language skills, minimum of English and other foreign languages where possible

Professional qualification (depending on the particular position):

Industry experience

Knowledge and understanding of the business model

23 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

Ability to interpret accounting and actuarial data

Knowledge and understanding of the regulatory frameworks affecting the company

Expertise in personnel management, staff selection, succession planning

The procedure for assessing the transfer of tasks stipulates that, at the preliminary stage of recruiting new members of staff, detailed curriculum vitae must be submitted and a requirements profile must be set, which contains the verification of predefined minimum requirements. If aspects of the requirements profile are not fulfilled at the point of time of recruiting for a new position, a corresponding justification is to be documented in writing. The continual safeguarding of compliance with the relevant requirements is undertaken every five years in the form of an assessment of the requirements profile, undertaken by the responsible organisational unit.

As part of the event-driven assessment, any significant changes in the underlying parameters trigger an assessment of compliance with the catalogue of requirements. This involves a differentiation of the characteristics deemed necessary in the person and in the position.

The assessment and control processes are summarised in an overview, which contains the assessment cycle of the requirements profile and the responsibility for the assessment and duty to inform held by those who individuals who actually head up the company, and those individuals who have other key tasks.

B.3 Risk Management System, including Own Risk and Solvency Assessment (ORSA)

B.3.1 Risk management system, including risk management function

B.3.1.1 Strategy implementation

During the reporting period, HDI Global Specialty was a primary insurer integrated in the Hannover Re Group, and adhered to the Hannover Re Group strategy. Ten guiding principles were embedded in the Group strategy, aimed at safeguarding the achievement of the vision that spans across all lines of business. The significant strategic starting points of reference for the Group-wide risk management are the following principles of the Group strategy:

We actively manage risks.

We ensure an appropriate capital position.

Our operations are defined by sustainability, integrity and compliance.

Beginning with the Group strategy, HDI Global Specialty specifies its vision in its own company strategy from which, in turn, the risk strategy was derived.

The risk strategy, the risk register, the limit and threshold value system, our risk and capital management guideline and the guidelines for managing the strategic, reputational and operational risks are assessed by at least once a year. This allows us to ensure the topicality of our risk management system.

Our total corporate risk is controlled in such a way that the probability of an absolute default of our economic capital - as well as our equity - is no more than 0.5% per annum. These performance indicators are monitored via our internal capital model and also the standard formula, and the Executive Board is updated quarterly on compliance with these variables by way of regular risk reporting. The level of capital deemed necessary is stipulated by the requirements of the Solvency II standard formula, as well as the statutory regulations and our internal economic capital model.

B.3.1.2 Risk capital

24 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

It is our objective to ensure an appropriate ratio between risks to our own funds in the interests of our shareholders and customers. Our quantitative risk management provides a uniform framework for the valuation and control of all risks affecting the company and our capital position. The standard formula specified by the supervisory authorities and the internal capital model are the instruments deployed as a first step. The internal capital model of HDI Global Specialty is a stochastic company model and covers all branches of HDI Global Specialty. A key parameter in risk and corporate controlling is the level of economic own funds, which is calculated using market-consistent valuation principles, and which is also the basis for the calculation of own funds under Solvency II.

Using the internal capital model, HDI Global Specialty can determine the necessary risk capital as the Value at Risk (VaR) of the economic change in value of one year and at a confidence level of 99.5%. This corresponds with the goal of preventing a breach of the one-year probability of ruin of 0.5%. In accordance with reporting obligations stipulated by the supervising authorities, HDI Global Specialty regularly calculates the capitalisation using the Solvency II standard formula. This results in the corresponding capital requirements for market risks, underwriting risks, receivables default risks and operational risks. The internal target capitalisation should always be in excess of 120% of the requirements set by the supervisory authorities.

B.3.1.3 Organisation of risk management and tasks of the risk management function

The risk management function consists of three primary components: the Risk Committee, the Chief Risk Officer and the risk monitoring function.

Risk Committee

The tasks of the Risk Committee are derived from the rules of procedure regarding the Risk Committee. One of its core tasks is to assist the Executive Board in all matters relating to risk management. The scope of decision-making for the Risk Committee lies within the boundaries of risk appetite set by the Executive Board. Any instances of increase in risk appetite require the approval of the Executive Board. The Risk Committee monitors the risk situation of HDI Global Specialty. Further tasks include assessing the system of governance, providing recommendations for improvement and monitoring the implementation of risk-related measures.

Chief Risk Officer

The Chief Risk Officer heads up the independent risk monitoring function, hold the furole of Chairman of the Risk Committee and is a member of the Executive Board. The tasks of the Chief Risk Officer include safeguarding the operating conditions needed for an effective risk management system. The Chief Risk Officer is also closely involved in the key decision-making processes of HDI Global Specialty, and informs the Risk Committee and the risk monitoring functions regarding relevant activities.

Risk monitoring function

The risk monitoring function coordinates, and bears responsibility for the monitoring (identification, assessment, monitoring and reporting) of all significant risks as well as the regular coordination and execution of the ORSA Process (Own Risk and Solvency Assessment, cf. B.3.2). It also develops and implements methods, standards and processes for assessment and monitoring of risk.

The risk monitoring function fulfils its tasks objectively and independently for HDI Global Specialty.

25 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

B.3.1.4 Key elements of our risk management system

Our risk strategy, the guideline for risk and capital management, the limit and threshold value system and the guidelines for managing strategic, reputational and operational risk for those significant risks affecting HDI Global Specialty describe the key elements of our risk management system. The risk management system is subject to a permanent cycle of planning, activity, control and improvement. In particular, systematic risk identification, analysis, assessment, control and monitoring as well as risk reporting play a key role in the effectiveness of the overall system.

The guideline covering risk and capital management contains, among other things, a description of the tasks, rights and responsibilities, the organisational operating conditions and the risk control process. The regulations are derived from the corporate and risk strategy and also account for the supervisory requirements placed on risk management.

Risk communication and an open risk culture are important concerns in the company’s risk

management.

Risk bearing capacity concept

The calculation of risk bearing capacity includes the determination of the total amount of risk coverage available and the calculation of how much thereof should be used for the purpose of covering all significant risks. This is done in sync with the specifications of the risk strategy and the determination of risk appetite by the Executive Board. Our risk model enables the evaluation of quantifiable individual risks as well as the overall risk position. A limit threshold value system exist for the monitoring of significant risks. This system incorporates - in addition to risk-relevant indicators - the parameters derived and calculated from the risk-bearing capacity. Compliance with the overall risk appetite is continually checked using the results of the standard formula and the internal capital model.

Risk identification

A significant information base for monitoring risks if for regular identification of risk. The documentation of all identified risks is executed in the risk register, which contains all significant risks. Risk identification works, for example, in the form of qualitative assessments, interviews or scenario analyses. External insight and recognised industry expertise from relevant committees or working groups are integrated into the process. Risk identification is the key to keeping our risk management permanently up to date.

26 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

Risk analysis and assessment

In principle, every identified risk, which is deemed significant, is subject to quantitative assessment. Only those types of risk which cannot (or only with great difficulty) be subject to quantitative risk measurement such as, for example, strategic risks, reputational risks or emerging risks. A qualitative assessment is conducted more or less by way of expert assessments. The quantitative assessment of significant risks and the overall risk position is done using the internal capital model of HDI Global Specialty, which is operated by the risk management function. Risk concentration and risk diversification are taken into consideration in the model.

Risk control

The control of all significant risks is the task of the operational units within the scopes of their remit. The identified and analysed risks are either consciously accepted, avoided or reduced. During the division’s decision-making process the risk-to-reward ratio is taken into consideration. Risk control is supported, for example, by the underwriting guidelines specifications, the investment guideline and the defined limit and threshold values.

Risk monitoring

The task of the risk management function is to monitor all identified significant risks. This includes, among other things, the monitoring of the risk strategy implementation and compliance with the defined limit and threshold values and the upholding of risk-relevant methods and processes. An important task of risk monitoring is also to determine whether the risk control measures were executed and whether the measures’ intended effect is sufficient.

Risk communication and risk culture

Risk management is firmly integrated into our operational processes. This is supported by transparent risk communication and an open approach to dealing with risks within the framework of our risk culture. The regular exchange of information between risk-controlling and risk-monitoring units is fundamental for the proper functional ability of risk management.

Risk reporting

Our risk reporting provides systematic and timely information on all significant risks and their potential impact. The risk reporting function consists of regular risk reports regarding, for example the comprehensive risk situation and compliance with the parameters defined in the risk strategy. In addition to regular reporting, an integrated immediate reporting function regarding significant and short-term risks can be implemented as needed.

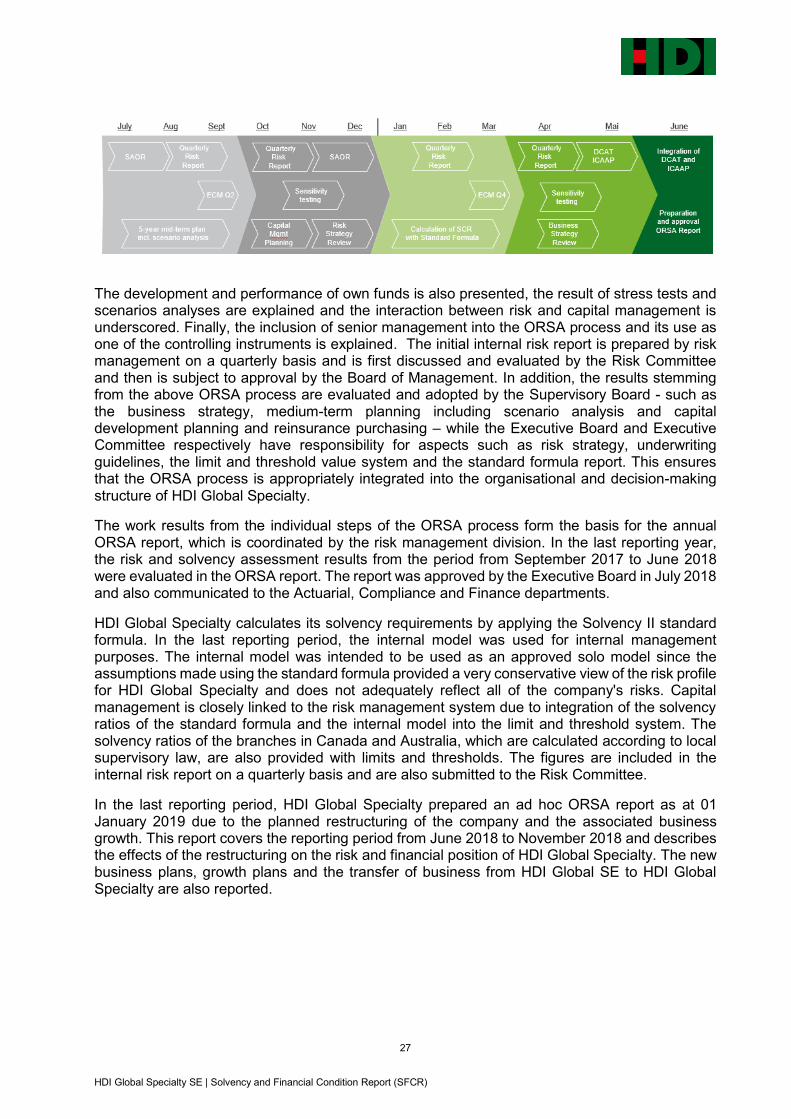

B.3.2 Own Risk and Solvency Assessment (ORSA)

The annual ORSA report primarily consists of an analysis of current and future risks which could threaten the continued existence of HDI Global Specialty. Here, the internal model and the Solvency II standard formula are used, and the results are analysed and displayed. ORSA process comprises the following steps:

27 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

The development and performance of own funds is also presented, the result of stress tests and scenarios analyses are explained and the interaction between risk and capital management is underscored. Finally, the inclusion of senior management into the ORSA process and its use as one of the controlling instruments is explained. The initial internal risk report is prepared by risk management on a quarterly basis and is first discussed and evaluated by the Risk Committee and then is subject to approval by the Board of Management. In addition, the results stemming from the above ORSA process are evaluated and adopted by the Supervisory Board - such as the business strategy, medium-term planning including scenario analysis and capital development planning and reinsurance purchasing – while the Executive Board and Executive Committee respectively have responsibility for aspects such as risk strategy, underwriting guidelines, the limit and threshold value system and the standard formula report. This ensures that the ORSA process is appropriately integrated into the organisational and decision-making structure of HDI Global Specialty.

The work results from the individual steps of the ORSA process form the basis for the annual ORSA report, which is coordinated by the risk management division. In the last reporting year, the risk and solvency assessment results from the period from September 2017 to June 2018 were evaluated in the ORSA report. The report was approved by the Executive Board in July 2018 and also communicated to the Actuarial, Compliance and Finance departments.

HDI Global Specialty calculates its solvency requirements by applying the Solvency II standard formula. In the last reporting period, the internal model was used for internal management purposes. The internal model was intended to be used as an approved solo model since the assumptions made using the standard formula provided a very conservative view of the risk profile for HDI Global Specialty and does not adequately reflect all of the company's risks. Capital management is closely linked to the risk management system due to integration of the solvency ratios of the standard formula and the internal model into the limit and threshold system. The solvency ratios of the branches in Canada and Australia, which are calculated according to local supervisory law, are also provided with limits and thresholds. The figures are included in the internal risk report on a quarterly basis and are also submitted to the Risk Committee.

In the last reporting period, HDI Global Specialty prepared an ad hoc ORSA report as at 01 January 2019 due to the planned restructuring of the company and the associated business growth. This report covers the reporting period from June 2018 to November 2018 and describes the effects of the restructuring on the risk and financial position of HDI Global Specialty. The new business plans, growth plans and the transfer of business from HDI Global SE to HDI Global Specialty are also reported.

28 HDI Global Specialty SE | Solvency and Financial Condition Report (SFCR)

B.4 Internal Control System

B.4.1 Components of the Internal Control System

Business activities are conducted in such a way that they are always in line with statutory regulations. The Internal Control System (ICS) is an important subsystem which serves to safeguard and protect existing assets, prevent and/or unearth errors and irregularities and ensure compliance with laws and regulations. The core elements of the ICS of HDI Global Specialty are documented in a guideline, which establishes a common understanding of the differentiated implementation of the necessary control measures. It is ultimately tasked with ensuring consistent control and monitoring of our corporate strategy’s implementation.

The guideline defines the terms, regulates responsibilities and offers a guide for the description of controls. Furthermore, it is the basis for the implementing internal targets and the fulfilment of external requirements which are placed on HDI Global Specialty. The ICS consists of systematically designed organisational and technical measures and controls in the company. This include, for example:

the principle of dual control (i.e. the “Four-eyes Principle”),

the separation of functions,

the documentation of controls within processes

technical plausibility checks and access permissions in the IT systems.

The functional capability of the ICS is contingent on the involvement of Senior Management, managers and employees at all levels. Financial reporting must fulfil both international and national accounting standards as well as all requirements stipulated by supervisory authorities. Therefore, processes with integrated control measures within the accounting and financial reporting function ensure that the annual financial statements are both complete and correct. With the aid of a structure listing differentiated criteria, control points and materiality thresholds, we are able to identify and minimise the risk of significant error in the annual financial statements at an early stage.

B.4.2 Compliance function

Implementation of the Compliance function

HDI Global Specialty has opted for a decentralised approach towards the implementation of the Compliance function, i.e. the tasks of the Compliance function will not be fulfilled by the Compliance department, but by various departments. Hence, the Compliance function is situated in various divisions and branches.

The Compliance function is free of any influences that could inhibit the objective, fair and independent execution of its tasks. The Compliance function is authorised to view all relevant information at any time and to approach members of staff directly regarding Compliance-relevant questions.