south asia trade and investment integration: india… · south asia trade and investment...

TRANSCRIPT

ICRIER Country Watch 1

ICRIER

SOUTH ASIA TRADE AND INVESTMENT INTEGRATION: INDIA’S ROLE

RAJIV KUMAR

Presentation at ADB Seminar, ManilaFebruary 20, 2009

ICRIER Country Watch 2

ICRIER

STRUCTURE OF PRESENTATION

• Case for Trade and Investment

• Trends in Trade and Investment Integration

• Regional Integration Initiatives

• Recommendations

ICRIER Country Watch 3

ICRIER

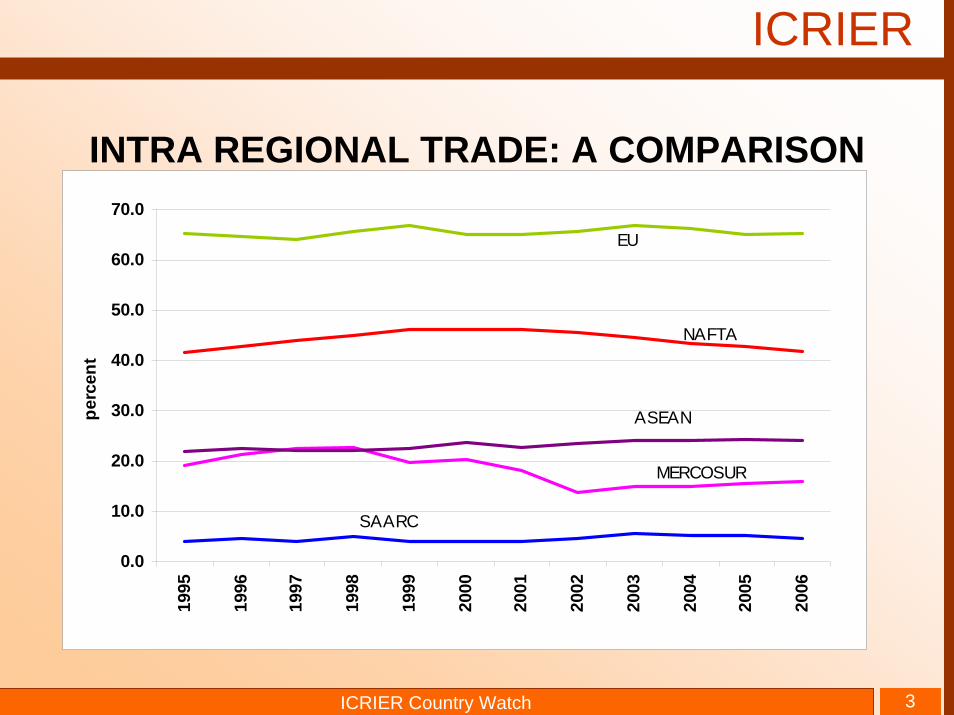

INTRA REGIONAL TRADE: A COMPARISON

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.019

95

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

perc

ent

EU

NAFTA

ASEAN

MERCOSUR

SAARC

ICRIER Country Watch 4

ICRIER

Intra Regional Trade- TrendsIntra Regional Exports Intra Regional Imports

Share in Share in

RegionOwn Total Exports to

World RegionOwn Total Imports to

World

1990-99 2000-07 1990-99 2000-07 1990-99 2000-07 1990-99 2000-07

Afghanistan 1.4 1.4 18.0 44.9 3.5 10.8 12.6 36.6

Bangladesh 4.6 2.3 2.8 1.8 36.4 27.7 12.6 14.9

India 66.5 65.8 4.3 5.3 10.7 13.8 0.6 0.9

Maldives 0.7 0.3 20.9 15.3 2.4 2.0 17.2 20.3

Nepal 3.3 7.7 15.9 58.8 10.0 15.5 20.9 52.0

Pakistan 18.0 16.1 3.9 7.9 10.7 8.1 2.0 2.8

Sri Lanka 5.5 6.4 2.8 6.9 26.3 22.0 10.9 18.3

Country

ICRIER Country Watch 5

ICRIER

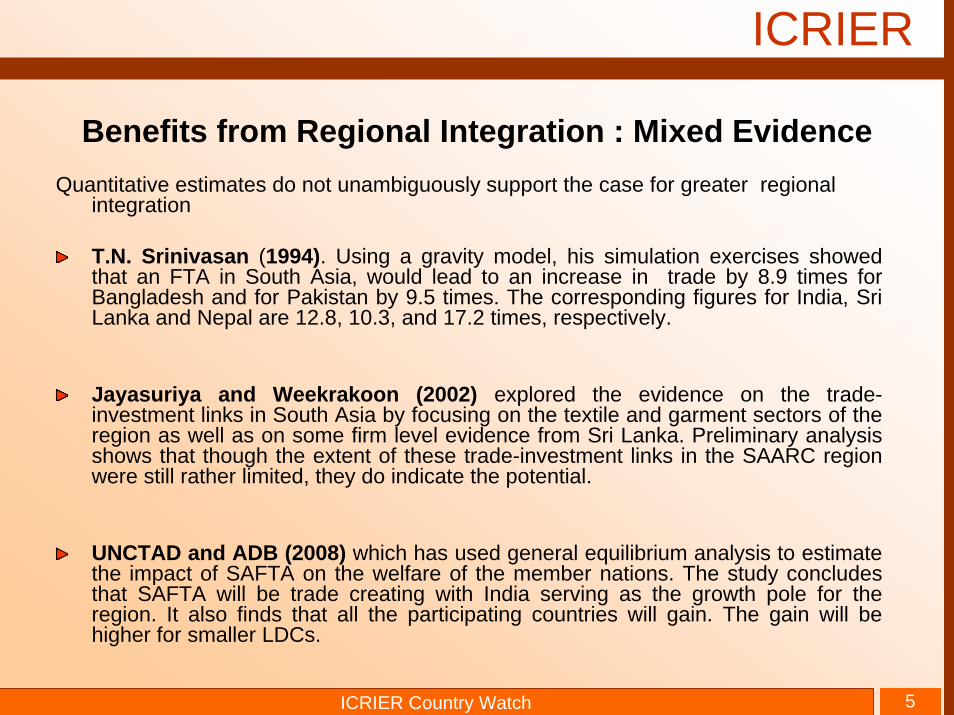

Benefits from Regional Integration : Mixed EvidenceQuantitative estimates do not unambiguously support the case for greater regional

integration

T.N. Srinivasan (1994). Using a gravity model, his simulation exercises showed that an FTA in South Asia, would lead to an increase in trade by 8.9 times for Bangladesh and for Pakistan by 9.5 times. The corresponding figures for India, Sri Lanka and Nepal are 12.8, 10.3, and 17.2 times, respectively.

Jayasuriya and Weekrakoon (2002) explored the evidence on the trade-investment links in South Asia by focusing on the textile and garment sectors of the region as well as on some firm level evidence from Sri Lanka. Preliminary analysis shows that though the extent of these trade-investment links in the SAARC region were still rather limited, they do indicate the potential.

UNCTAD and ADB (2008) which has used general equilibrium analysis to estimate the impact of SAFTA on the welfare of the member nations. The study concludes that SAFTA will be trade creating with India serving as the growth pole for the region. It also finds that all the participating countries will gain. The gain will be higher for smaller LDCs.

ICRIER Country Watch 6

ICRIER

…contd.

Panagarya (2003), found that trade diversion will probably swamp the beneficial trade creation effects.

Kumar and Saini (2007) look at the Pareto optimality of SAFTA as well as the welfare optimality of alternative sets of coordinated trade policies that go beyond SAFTA using the standard static GTAP model. Their analysis shows that the welfare basis for establishing SAFTA or for deeper trade policy coordination in South Asia was not very strong. Nor was it obvious that cooperation among the South Asia would be forthcoming given the rather meagre anticipated welfare impacts.

ADB-UNCTAD study (2008) has shown that lowering of tariffs following SAFTA will attract FDI from outside the region into South Asia. SAFTA may not only increase intra regional trade but may also attract more vertically integrated FDI into the region.

ICRIER Country Watch 7

ICRIER

MOTIVATIONS FOR REGIONAL INTEGRATION

PURE ECONOMIC EFFICIENCY GAINS

NON-TRADITIONAL GAINS

STRATEGIC GAINS

DEVELOPMENT AND ENVIRONMENT EFFICIENCY GAINS

ICRIER Country Watch 8

ICRIER

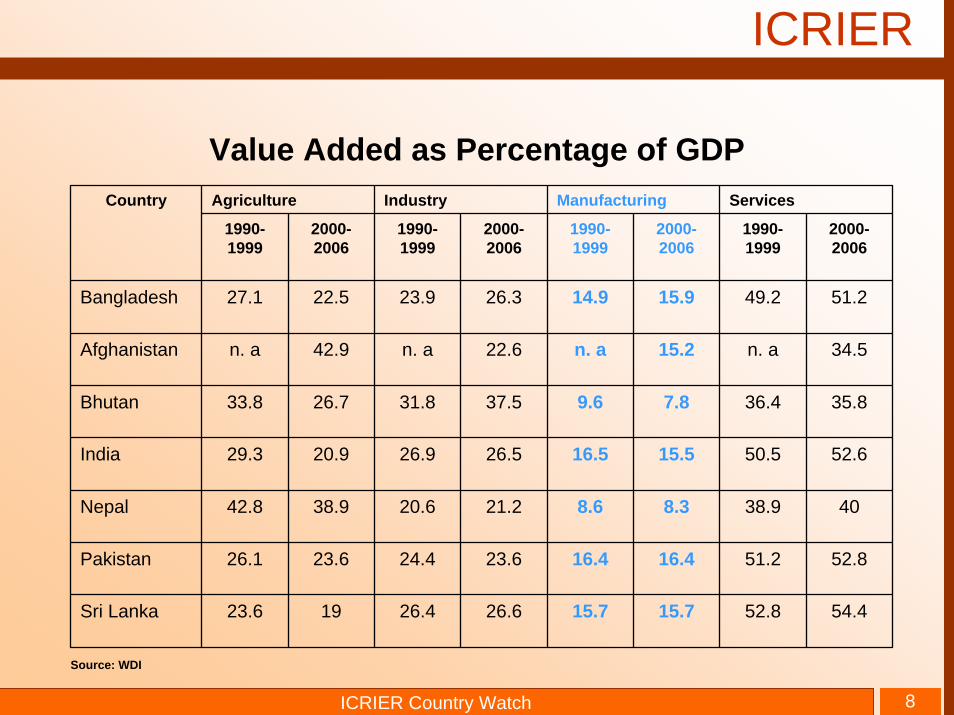

Agriculture Industry Manufacturing Services

1990-1999

2000-2006

1990-1999

2000-2006

1990-1999

2000-2006

1990-1999

2000-2006

Bangladesh 27.1 22.5 23.9 26.3 14.9 15.9 49.2 51.2

Afghanistan n. a 42.9 n. a 22.6 n. a 15.2 n. a 34.5

Bhutan 33.8 26.7 31.8 37.5 9.6 7.8 36.4 35.8

India 29.3 20.9 26.9 26.5 16.5 15.5 50.5 52.6

Nepal 42.8 38.9 20.6 21.2 8.6 8.3 38.9 40

Pakistan 26.1 23.6 24.4 23.6 16.4 16.4 51.2 52.8

Sri Lanka 23.6 19 26.4 26.6 15.7 15.7 52.8 54.4

Country

Value Added as Percentage of GDP

Source: WDI

ICRIER Country Watch 9

ICRIER

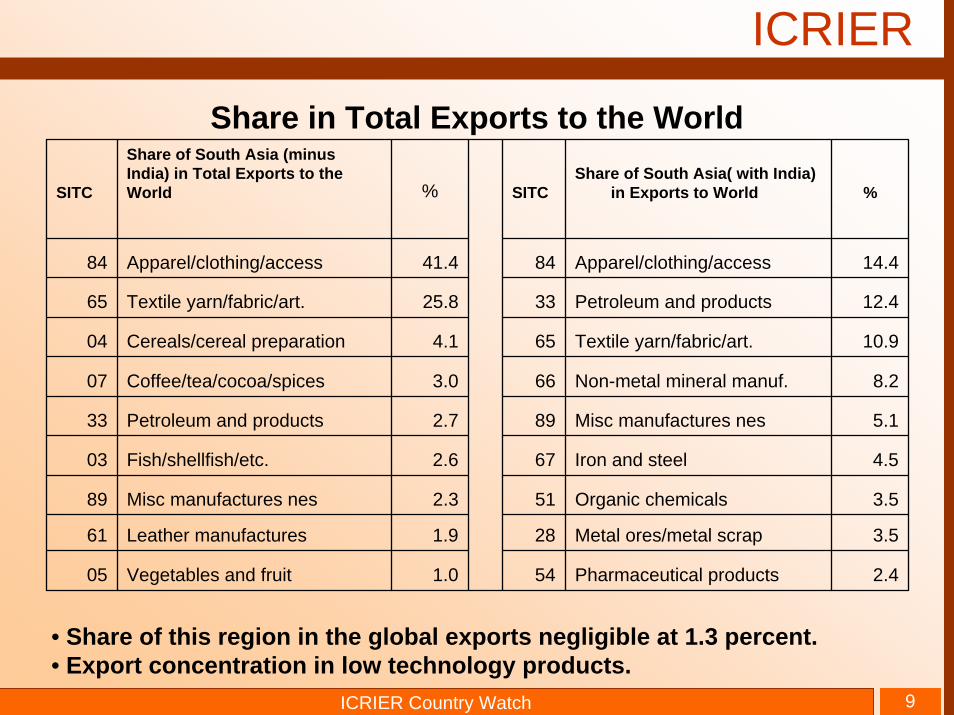

Share in Total Exports to the World

SITC

Share of South Asia (minusIndia) in Total Exports to theWorld % SITC

Share of South Asia( with India) in Exports to World %

84 Apparel/clothing/access 41.4 84 Apparel/clothing/access 14.4

65 Textile yarn/fabric/art. 25.8 33 Petroleum and products 12.4

04 Cereals/cereal preparation 4.1 65 Textile yarn/fabric/art. 10.9

07 Coffee/tea/cocoa/spices 3.0 66 Non-metal mineral manuf. 8.2

33 Petroleum and products 2.7 89 Misc manufactures nes 5.1

03 Fish/shellfish/etc. 2.6 67 Iron and steel 4.5

89 Misc manufactures nes 2.3 51 Organic chemicals 3.5

61 Leather manufactures 1.9 28 Metal ores/metal scrap 3.5

05 Vegetables and fruit 1.0 54 Pharmaceutical products 2.4

• Share of this region in the global exports negligible at 1.3 percent.• Export concentration in low technology products.

ICRIER Country Watch 10

ICRIER

IMPLICATIONS OF LOW MANUFACTURING SHARES

Manufacturing sector in the region suffers from under funding of technology, inappropriate scales and, poor infrastructure.

Growth not sufficiently employment intensive or inclusive.

With the downturn demographic dividend becomes doubtful

Marked dualism all across South Asia: SMEs generally neglected

Greater regional cooperation will benefits the manufacturing sector through -Trade expansion and economies of scale.- South Asian Supply Chain Networks.- Setting region wide regulatory norms and standards

ICRIER Country Watch 11

ICRIER

Trends in Intra Regional Trade ( contd.)

Most of the trade of the countries in the region is extra regional.

In recent times, the South Asian market has become important especially for the smaller countries like Afghanistan and Nepal.

Though dominating the region’s trade, India sources less than one percent of its imports from the region.

Unilateral liberalisation by India has effectively eroded the advantage the SAARC members can have in the Indian market.

There have been changes in the direction of the region’s trade. India-Sri Lanka bilateral trade has increased significantly . There has also been an increase in India’s trade with Pakistan.

ICRIER Country Watch 12

ICRIER

Regional Shares in Global FDI Inflow

EU USA China ASEAN S. Asia EU USA China ASEAN S. Asia

US $ million Share in World FDI (%)

1996 124811 84455 41726 30490 3359 31.78 21.5 10.62 7.76 0.86

1997 142400 103398 45257 34307 5371 29.11 21.13 9.25 7.01 1.1

1998 281000 174434 45463 22276 3889 39.62 24.59 6.41 3.14 0.55

1999 502636 283376 40319 28766 3234 45.74 25.79 3.67 2.62 0.29

2000 695277 314007 40715 23540 4658 49.26 22.25 2.88 1.67 0.33

2001 381558 159461 46878 20729 6415 45.83 19.15 5.63 2.49 0.77

2002 307345 74457 52743 18024 6984 49.41 11.97 8.48 2.9 1.12

2003 256707 53146 53505 24491 5469 45.51 9.42 9.49 4.34 0.97

2004 204245 135826 60630 35245 7601 27.52 18.3 8.17 4.75 1.02

2005 486409 101025 72406 41071 9866 51.43 10.68 7.66 4.34 1.04

2006 530976 175394 69468 51483 22274 40.66 13.43 5.32 3.94 1.71

Year

FDI Inflow into South Asia has increased by 8 times over 1995 and 2006, it is less than 2 percent of world FDI

ICRIER Country Watch 13

ICRIER

Country-wise FDI Inflows in South Asia

Year Afghanistan Bangladesh Bhutan India Maldives Nepal Pakistan Sri Lanka

1996 1 232 1 2525 9 19 439 133

1997 -1 575 -1 3619 11 23 711 433

1998 0 576 - 2633 12 12 506 150

1999 6 309 1 2168 12 4 532 201

2000 0 579 0 3585 13 0 309 173

2001 1 355 0 5472 12 21 383 172

2002 1 328 2 5627 12 -6 823 197

2003 2 350 3 4323 14 15 534 229

2004 1 460 3 5771 15 0 1118 233

2005 4 692 9 6676 9 2 2201 272

2006 2 625 6 16881 14 -7 4273 480

Cumulative 15 5082 25 59280 133 83 11829 2672

• Very low FDI in general. • India again predominates.

ICRIER Country Watch 14

ICRIER

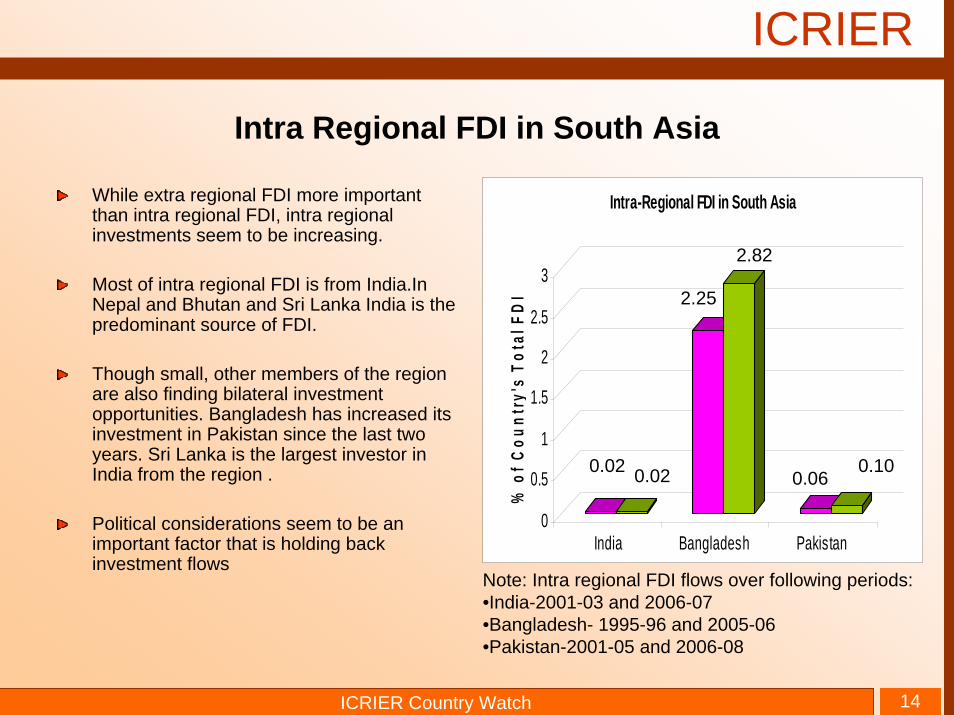

Intra Regional FDI in South Asia

While extra regional FDI more important than intra regional FDI, intra regional investments seem to be increasing.

Most of intra regional FDI is from India.In Nepal and Bhutan and Sri Lanka India is the predominant source of FDI.

Though small, other members of the region are also finding bilateral investment opportunities. Bangladesh has increased its investment in Pakistan since the last two years. Sri Lanka is the largest investor in India from the region .

Political considerations seem to be an important factor that is holding back investment flows

0.02 0.02

2.25

2.82

0.06 0.100

0.5

1

1.5

2

2.5

3

% o

f Cou

ntry

's T

otal

FD

IIndia Bangladesh Pakistan

Intra-Regional FDI in South Asia

0.02 0.02

2.25

2.82

0.060.10

Note: Intra regional FDI flows over following periods:•India-2001-03 and 2006-07•Bangladesh- 1995-96 and 2005-06•Pakistan-2001-05 and 2006-08

ICRIER Country Watch 15

ICRIER

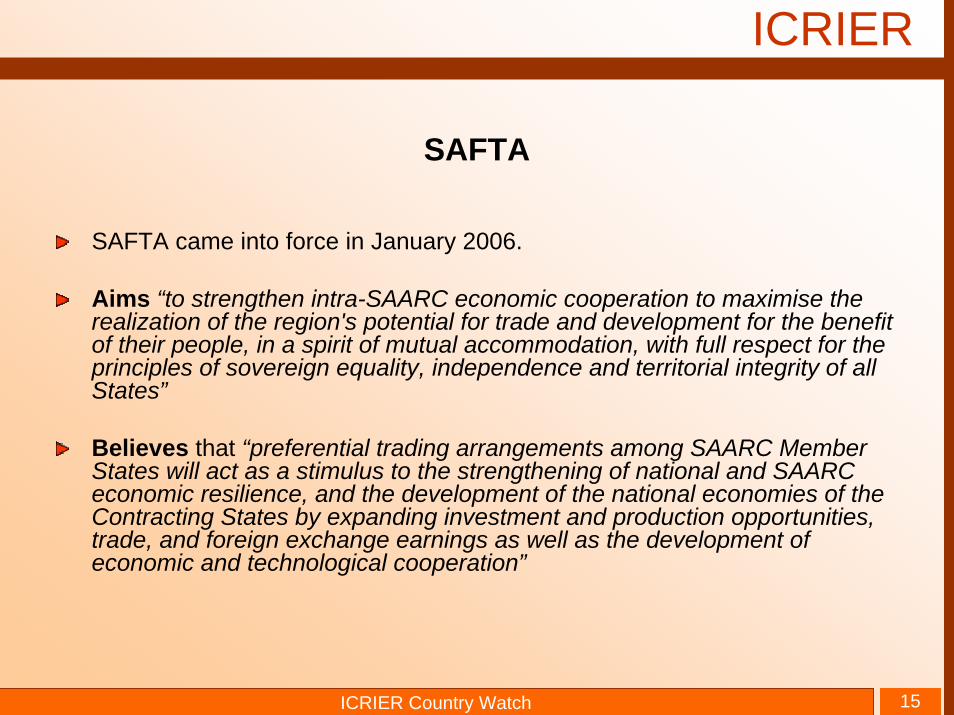

SAFTA

SAFTA came into force in January 2006.

Aims “to strengthen intra-SAARC economic cooperation to maximise the realization of the region's potential for trade and development for the benefit of their people, in a spirit of mutual accommodation, with full respect for the principles of sovereign equality, independence and territorial integrity of all States”

Believes that “preferential trading arrangements among SAARC Member States will act as a stimulus to the strengthening of national and SAARC economic resilience, and the development of the national economies of the Contracting States by expanding investment and production opportunities, trade, and foreign exchange earnings as well as the development of economic and technological cooperation”

ICRIER Country Watch 16

ICRIER

…SAFTA

SAFTA is governed by WTO principals of reciprocity and special and differential treatment of LDCs.Focuses on elimination of tariffs, para-tariffs and non-tariff.Entails adoption of trade facilitation and other measures, and the progressive harmonization of legislations by the member States in the relevant areas.Implementation of SAFTA through,-The highest decision making body and responsible for the administration and implementation of this Agreement : SAFTA Ministerial Council-Supported by Committee of Experts (comprising of Senior Economic Official from each member State). The COE to also act as Dispute Settlement Body.Tariffs phase-out schedule (Phase out by 2016):

Non LDCs for LDCs- Tariff to be reduced to 0-5% by 2009.

Non-LDCs for Non-LDCs : To reduce tariffs to a maximum of 20 per cent (2006-08) and to 0-5 percent in the next five years.

Schedule for LDCs: To reduce tariffs to a maximum of 30 per cent (2006-08) and further to 0-5 percent during 2008-2016. Products that qualify for SAFTA preferences also subject to rules of origin, sensitive lists, balance of payments, and safeguard measures.

ICRIER Country Watch 17

ICRIER

Weaknesses in SAFTAPakistan has ratified SAFTA but has not accorded MFN Status to India and continues to use a positive list.

The time frame (by the year 2016) to reduce the tariffs to zero percent is too long.

The sensitive lists are too large and no binding commitment to reduce or remove the lists.

Members are free to have bilateral agreements that include deeper tariff cuts and cover larger number of sectors including sometimes service sectors.

Technical assistance in SAFTA, designed to assist LDCs in building their negotiating and trading capacities, is in the nature of ‘best endeavour clause’ without any binding commitments.

No timeframe under SAFTA for removing NTBs.

ICRIER Country Watch 18

ICRIER

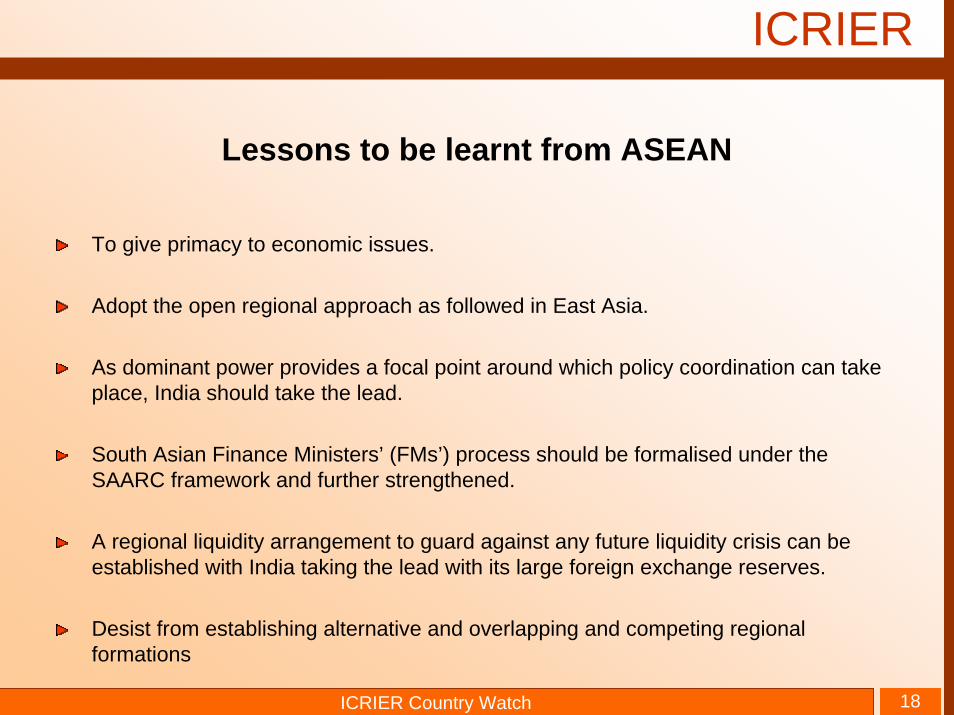

Lessons to be learnt from ASEAN

To give primacy to economic issues.

Adopt the open regional approach as followed in East Asia.

As dominant power provides a focal point around which policy coordination can take place, India should take the lead.

South Asian Finance Ministers’ (FMs’) process should be formalised under the SAARC framework and further strengthened.

A regional liquidity arrangement to guard against any future liquidity crisis can be established with India taking the lead with its large foreign exchange reserves.

Desist from establishing alternative and overlapping and competing regional formations

ICRIER Country Watch 19

ICRIER

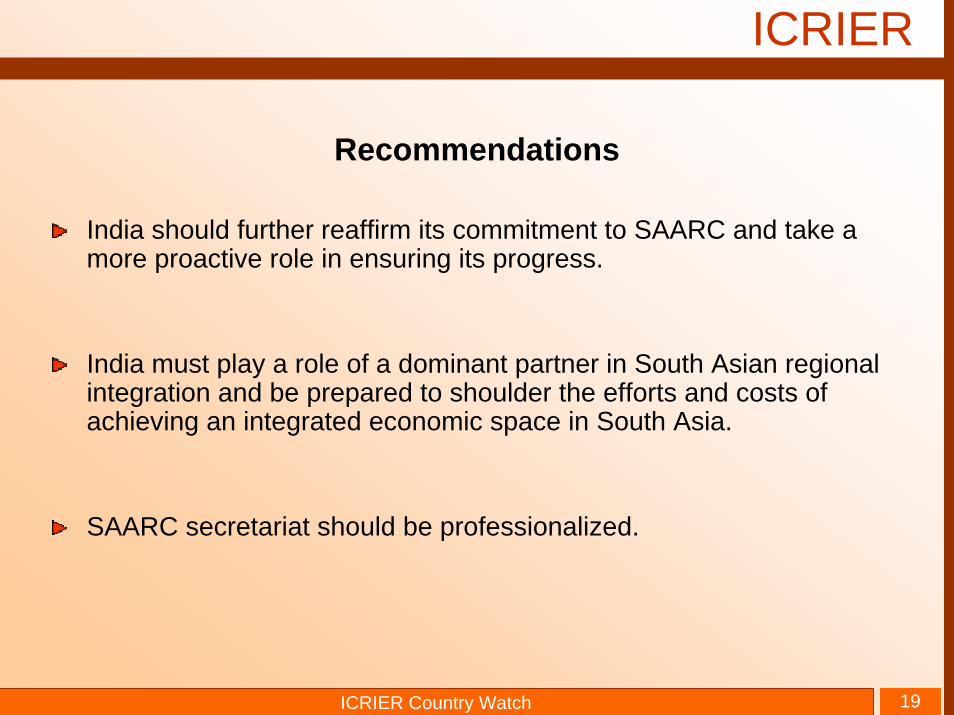

Recommendations

India should further reaffirm its commitment to SAARC and take amore proactive role in ensuring its progress.

India must play a role of a dominant partner in South Asian regional integration and be prepared to shoulder the efforts and costs ofachieving an integrated economic space in South Asia.

SAARC secretariat should be professionalized.

ICRIER Country Watch 20

ICRIER

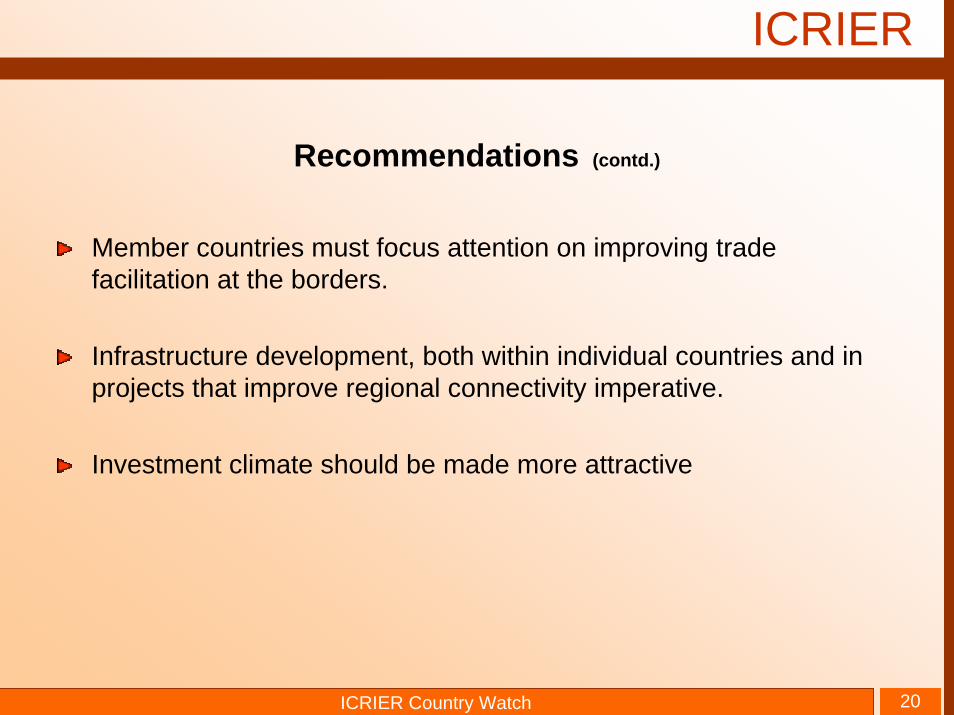

Recommendations (contd.)

Member countries must focus attention on improving trade facilitation at the borders.

Infrastructure development, both within individual countries and in projects that improve regional connectivity imperative.

Investment climate should be made more attractive

ICRIER Country Watch 21

ICRIER

Recommendations (contd.)

Exaggerated perceptions of security threats.

Coordinated action on part of the stake holders who either expect to gain from regional integration necessary.

More resources and powers to be given to border states.

ICRIER Country Watch 22

ICRIER