southern highlands food systems - tzdpg.or.tz · annex 9 some activities of the soya ni pesa...

TRANSCRIPT

Tanzania:Southern Highlands Food Systems

Soya Bean

Value Chain Analysis

Consultant’s Report (Main)R Trevor Wilson

1 October 2013

Captions for Front Cover Illustrations

(All Photographs by Trevor Wilson)

Clockwise from top left

Soya bean seeds ready for planting: Arusha, 30 August 2013

Preparing land for soya: Farm 8 Nachingwea, 26 December 1961

Well grown healthy soya: Kisolanza south of Iringa, 26 August 2013

Baling soya straw for livestock feed: Farm 4 Nachingwea, 5 May 1961

Maize flour reinforced with soya: Local supermarket, 29 August 2013

Tanzania Southern Highlands Food Systems i

WHAT THEY SAY

Future prospects for the soybean in Tanzania are absolutely bright

Mmbaga 1975

I am very happy that I planted soybeans, even though not many farmers plant it. I am happy because it

has fetched me more income than the normal beans

Marcianna Nyirarukundo, a mother of three children in Kayonza district, Rwanda:

Soy is one of the few plants that provides a complete protein as it contains all eight amino acids

essential for human health

http://www.soyatech.com/soy_facts.htm

In comparison to many of today’s major food sources, soybeans are truly a nutritional superpower.

They contain the highest amount of protein of any grain or legume, and substantial amounts of fat,

carbohydrates, dietary fiber, vitamins, minerals and a virtual drugstore of phytochemicals useful for

the prevention and treatment of many chronic diseases

http://www.soyatech.com/soy_health.htm

Soya meal, the residue after the extraction of the oil, is a very rich protein feeding stuff for livestock

Purseglove 1972

Cocoa, coffee, rice, palm oil and soya bean underpins environmental destruction and biodiversity loss

Donald 2004

ii Soya Bean Value Chain Analysis

List of Contents

WHAT THEY SAY i

ACKNOWLEDGEMENTS vi

CURRENCY EXCHANGE RATE vi

ABBREVIATIONS AND ACRONYMS vii

GLOSSARY OF KISWAHILI WORDS AND PHRASES ix

EXECUTIVE SUMMARY xi

1. INTRODUCTION 1

1.1 Background of the Study and Objectives 1

1.2 Methodology 2

1.3 Brief Overview of the Value Chain 2

1.3.1 Why soya? 2

1.3.2 The value chain 3

2. END-MARKETS 6

2.1 National Market 6

2.2 Export Markets 7

3. THE SOYA BEAN VALUE CHAIN 9

3.1 Overview 9

3.2 The Value Chain Map 9

3.2 Technology Generation 12

3.3 Input Supply and Demand 12

3.4 Production 16

3.4.1. Overview 16

3.4.2. Area planted and unit area yields 16

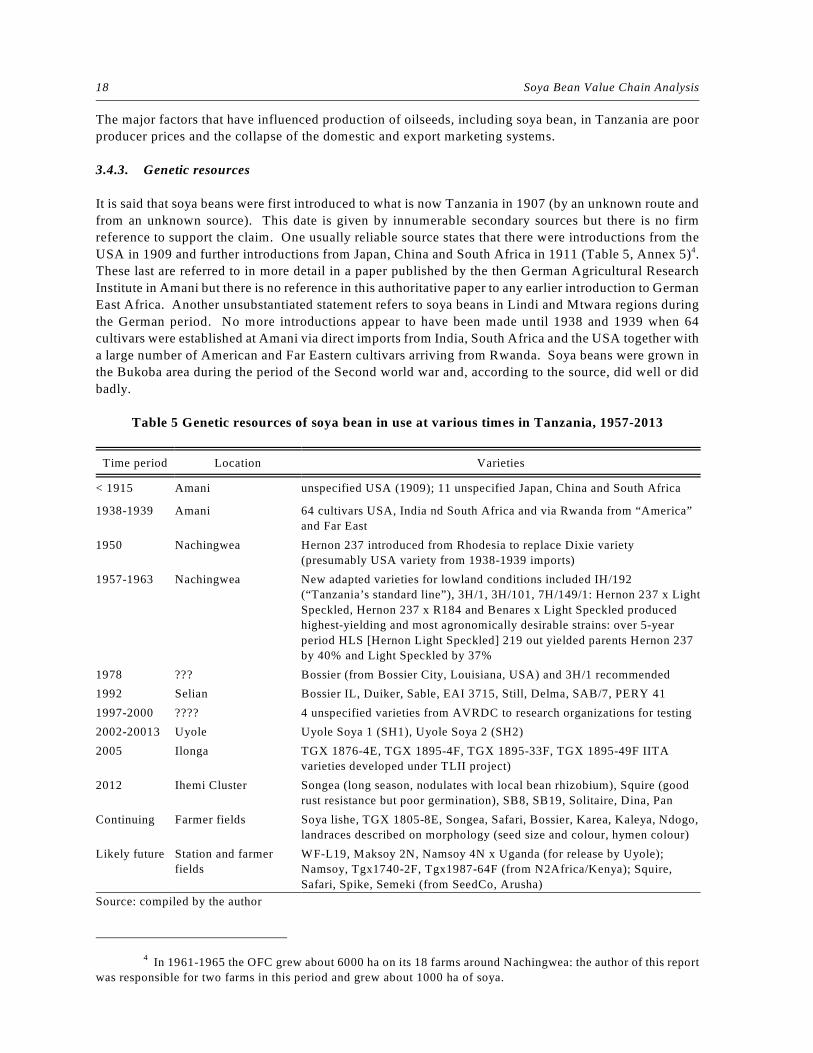

3.4.3. Genetic resources 18

3.4.4. Soya bean output 20

3.4.5. Profits from production 23

3.5 Processing 23

3.5.1 Overview 23

3.5.2 Marketing 25

3.5.3 Home use 25

3.5.4 Fortified foods and other speciality products for human use 26

3.5.5 Animal feed 29

3.5.6 Hindsight 31

3.6 Wholesale and Retail Distribution 31

3.7 Target Group Considerations 31

Tanzania Southern Highlands Food Systems iii

4. SYSTEMIC CONSTRAINTS AND UPGRADING OPPORTUNITIES 33

4.1 Related to Business Enabling Environment 33

4.1.1. Doing business 33

4.1.2. Legislation and regulations 33

4.1.3 Land rights and land markets 35

4.1.4 Government policy for the soya bean and general crop production 35

4.1.5 Food safety and quality 38

4.1.6 Public infrastructure 39

4.2 Related to Vertical and Horizontal Linkages and Value Chain Governance 40

4.2.1 Integration 40

4.2.2 Governance 41

4.3 Related to Support Services 41

4.3.1 Overview 41

4.3.2 The Cereals and Other Produce Board 41

4.3.3 Value chain finance 42

4.3.4 Insurance 43

4.3.5 Research services 43

4.3.6 Extension services 44

4.3.7 Seed supply 45

4.3.8 Market information 45

4.3.9 Transport 46

4.3.10 International and Non-Governmental Organizations 48

5. VISION AND STRATEGY FOR IMPROVED COMPETITIVENESS AND GROWTH 49

5.1 Vision 49

5.2 Strategic Issues Synthesis 49

5.2.1 Existing policies, strategies and programmes 49

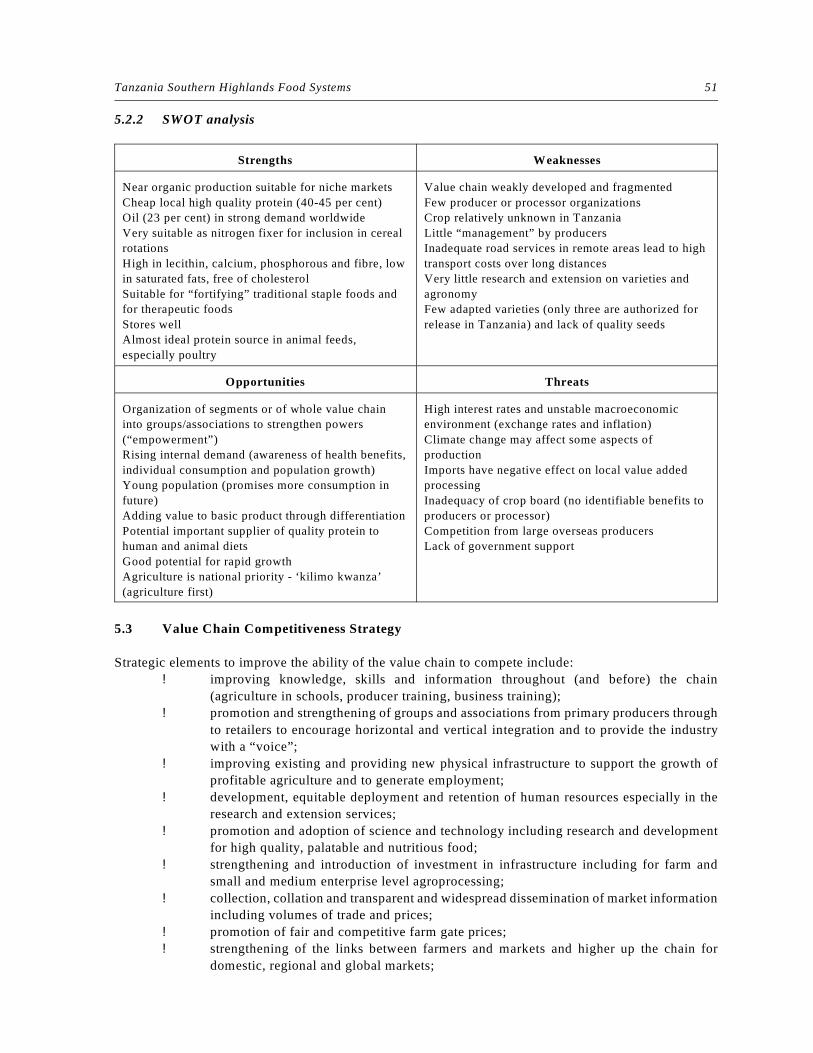

5.2.2 SWOT analysis 51

5.3 Value Chain Competitiveness Strategy 51

5.4 Proposed Strategy Components 52

5.4.1 Sustainable use of land, water and other natural resources 52

5.4.2 Public and private sector investment and financing 53

5.4.3 Improved efficiency in production, marketing and processing 54

5.4.4 Support services (research, extension, training and dissemination of information)

54

5.4.5 Capacity building and empowerment all along the chain 54

5.4.6 Chain governance, regulatory and institutional arrangements 55

5.4.7 Cross-cutting and cross-sectoral issues 55

ANNEX 1 TERMS OF REFERENCE

ANNEX 2 WORK PROGRAMME

ANNEX 3 STAKEHOLDERS MET

ANNEX 4 DOCUMENTS CONSULTED

ANNEX 5 TIMELINES – THE RISE AND FALL OF A MINOR PROTEIN/OILSEED CROP,

1907-2013

iv Soya Bean Value Chain Analysis

ANNEX 6 PRODUCTS CONTAINING SOYA BEANS IMPORTED INTO TANZANIA

ANNEX 7 PARTIAL LIST OF SOYA BEAN PROCESSORS AND PRODUCTS IN TANZANIA

ANNEX 8 POULTRY FEED MANUFACTURING ENTERPRISES IN TANZANIA

ANNEX 9 SOME ACTIVITIES OF THE SOYA NI PESA PROJECT IN THE ROMAN

CATHOLIC DIOCESE OF NJOMBE

ANNEX 10 INTERNATIONAL FUNDING OBTAINED BY TANFEEDS OF MOROGORO

Tanzania Southern Highlands Food Systems v

List of Tables

Table 1 Development conditions and projected demand for soya beans in Tanzania 6

Table 2 Simple listing of supply and service participants in the Soya Bean Value Chain 11

Table 3 Participants and functions in the Soya Bean Value Chain 11

Table 4 Banks operating and providing loans in the Southern Highlands 16

Table 5 Genetic resources of soya bean in use at various times in Tanzania, 1957-2013 18

Table 6 Recent soya bean production and potential area and output increase in Tanzania regions 21

Table 7 Targets for area planted, output, proportion processed and exported and seed production

of soya beans, 2010-2020 22

Table 8 Theoretical gross margin analyses for smalholder soya production in the

Southern Highlands 23

Table 9 Theoretical gross margin analyses for participants in the soya bean value chain 30

Table 10 Projected targets with full implementation of TSDS, 2010-2020 37

Table 11 Components and activities of the Tanzania Soybean Development Strategy (TSDS) 49

Table 12 Existing policies, strategies and programmes of relevance to the soya bean value chain 50

List of Figures

Figure 1 A well grown crop of soya at Makuta Farm south of Iringa 3

Figure 2 Value and amount of exports of soya beans from Tanzania, 1961-2011 8

Figure 3 The Soya Bean Value Chain in Tanzania 10

Figure 4 Agro-vet retail outlet in Tunduma selling a range of seeds, fertilizers and

crop health products 14

Figure 5 Area planted to soya bean in Tanzania, 1961-2011 17

Figure 6 Comparison of world annual average soya bean yields with those in Tanzania 17

Figure 7 Soya bean genetic resources in Tanzania: lines under test at Uyole

Agricultural Research Institute) 20

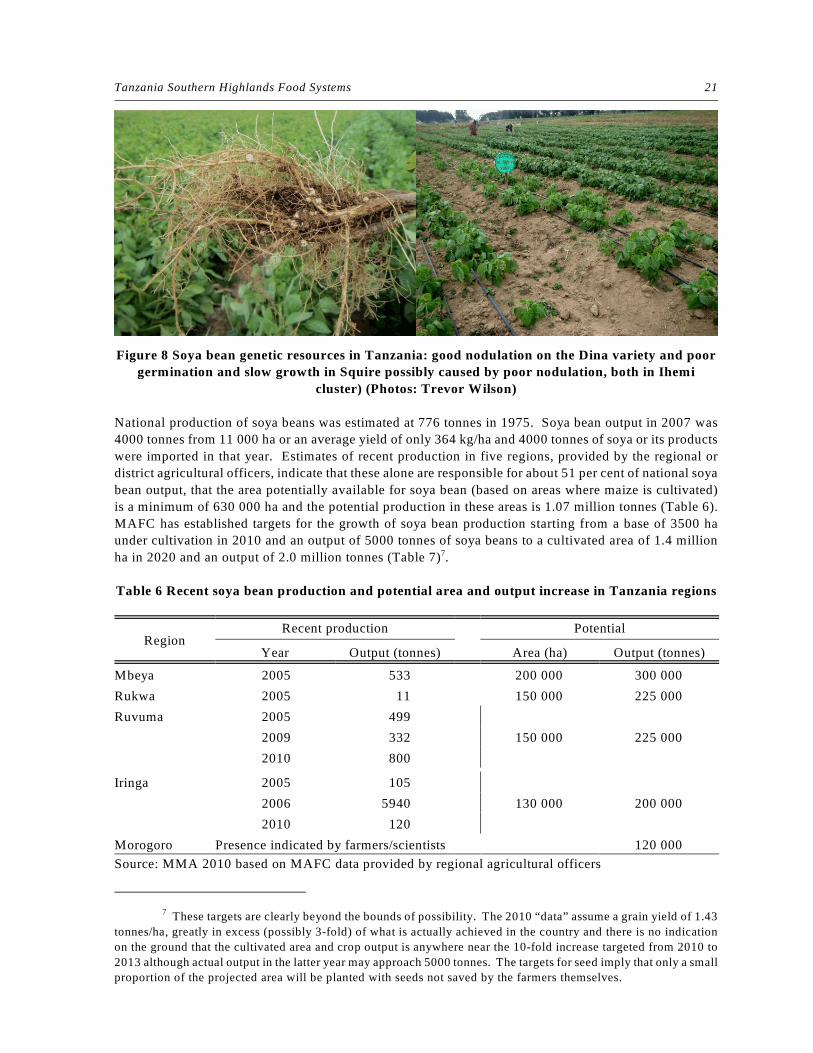

Figure 8 Soya bean genetic resources in Tanzania: good nodulation on the Dina variety

and poor germination and slow growth in Squire possibly caused by poor nodulation,

both in Ihemi cluster) 21

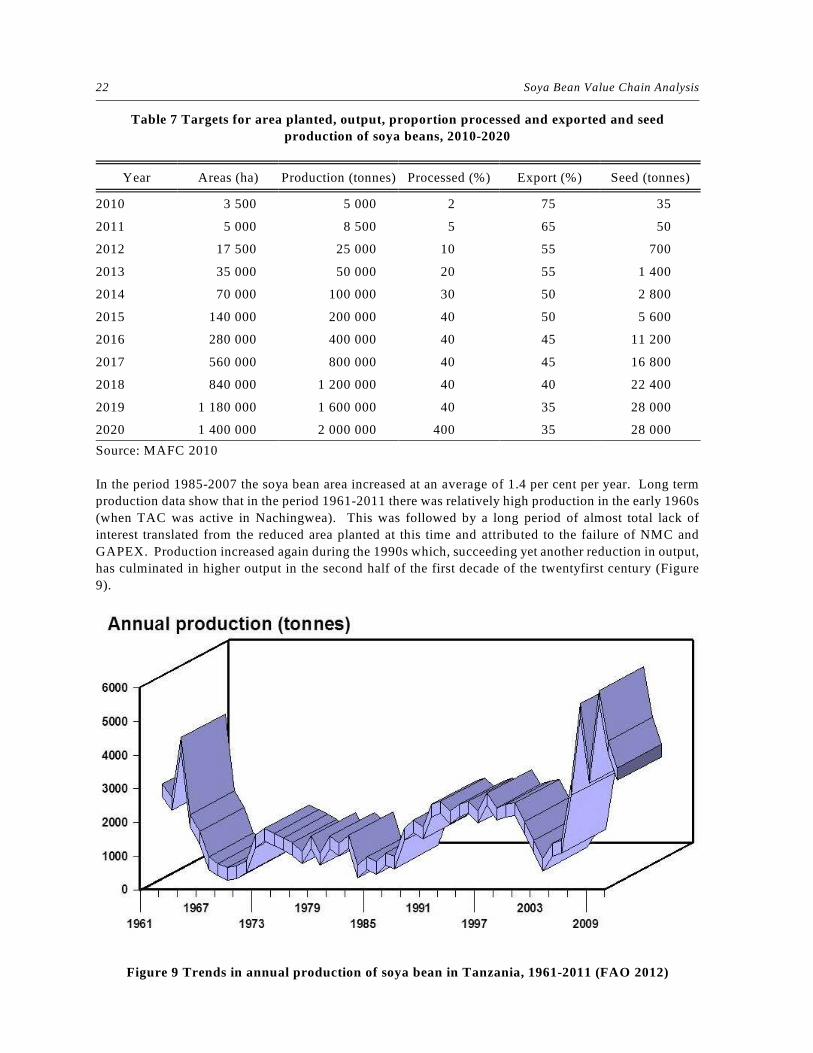

Figure 9 Trends in annual production of soya bean in Tanzania, 1961-2011 22

Figure 10 Representative examples of pathways followed from point of production to final use

for soya bean and its products 24

Figure 11 Steps involved in home processing of raw soya beans to soya milk

as described by a smallholder lady farmer 26

Figure 12 A range of soya products produced in Dar es Salaam in the retail outlet

of the processor 27

Figure 13 An electric powered expeller of the type that can be used for soya bean processing 28

Figure 14 Soya oil and expeller cake processed in Morogoro from local whole soya beans 30

Figure 15 Doing business in Tanzania 33

Figure 16 The food safety policy of Power Foods Ltd, Dar es Salaam 38

Figure 17 Traffic anarchy at a weighbridge on the Dar es Salaam-Morogoro trunk road 39

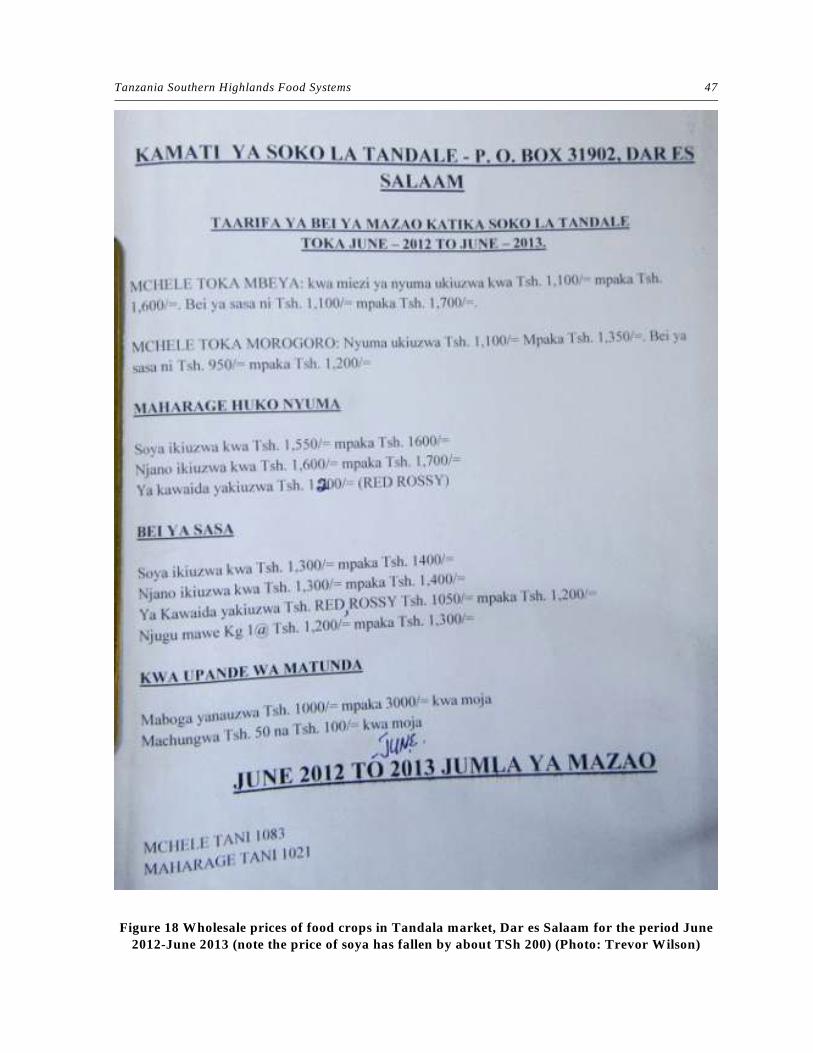

Figure 18 Wholesale prices of food crops in Tandala market, Dar es Salaam for the period

June 2012-June 2013 47

vi Soya Bean Value Chain Analysis

List of Boxes

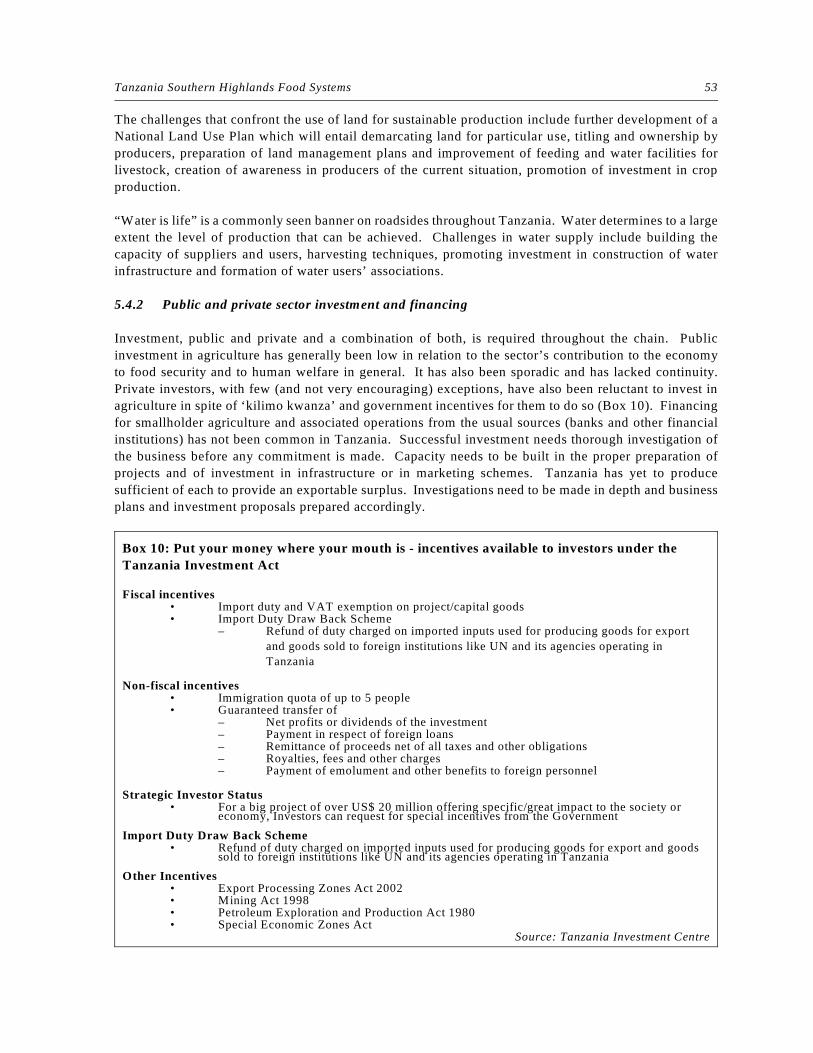

Box 1: The Southern Agricultural Growth Corridor of Tanzania (SAGCOT) 4

Box 2: Let them eat cake – supplements and concentrate feed manufacture 15

Box 3: Small is beautiful – an Arusha home-based initiative supplying foods fortified with soya 28

Box 4: Is bigger better? – a Dar es Salaam medium scale enterprise producing soya foods 29

Box 5: Sound and fury – over regulation and under enforcement of crop trade activities 34

Box 6: ‘KILIMO KWANZA’ – The Principal Points and the Ten Pillars 36

Box 7: Objectives of the Tanzania Soybean Development Strategy 37

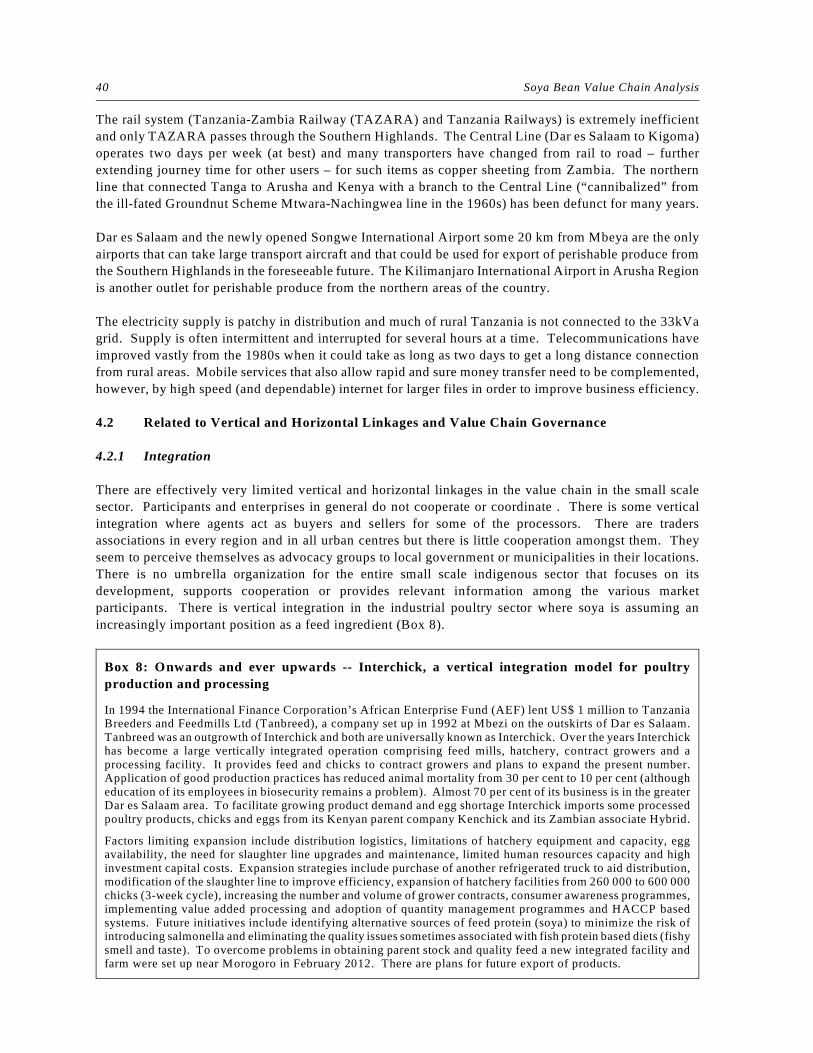

Box 8: Onwards and ever upwards -- Interchick, a vertical integration model for poultry production

and processing 40

Box 9: Uyole Agricultural Research and Training Institute 44

Box 10: Put your money where your mouth is - incentives available to investor

under the Tanzania Investment Act 53

§ § § § § § § § § § § § § § §

ACKNOWLEDGEMENTS

Thanks are due first to all those participants in the soya bean value chain who agreed to meet and have

discussions with the Consultant (having for the most part met and had discussions with innumerable

predecessors) and sharing their views as well as their hopes and fears with him: many of these are listed

in Annex 3 which provides a listing of the people met during the course of the study.

Many documents have been written on soya beans and their value chain. This report has drawn deeply

on these earlier documents and in particular for its strategic interventions on the Tanzania Soybean

Development Strategy.

The Consultant responsible for writing this report thanks Michael Winklmaier, Chief Technical Adviser

of the Southern Highlands Food Systems Programme and his office staff for all the help provided over the

course of the study. He also thanks Diana Templeman, FAOR Tanzania for her support before and during

the study, Joan Kimirei, National Consultant for assistance during an extended trip up-country and Peter

Jimbuku driver extraordinary and general factotum.

§ § § § § § § § § § § § § § §

CURRENCY EXCHANGE RATE

US$ 1.00 = Tanzania Shillings (TSh) 1600 approximately in September 2013

Tanzania Southern Highlands Food Systems vii

ABBREVIATIONS AND ACRONYMS

AfricaRice Africa Rice Center (formerly the West Africa Rice Development Association (WARDA))

AGG Agricultural Green Growth

AKIRIGO Kilombero High Quality Rice Growers Organization

ALM Agricultural Sector Lead Ministries

ARI Agricultural Research Institute

ASA Agricultural Seeds Agency

ASARECA Association for Strengthening Agricultural Research in Eastern and Central Africa

ASDP Agriculture Sector Development Programme

ASDS Agricultural Sector Development Strategy

AVRDC World Vegetable Research Centre (acronym from previous title of Asian Vegetable

Research and Development Centre)

BRELA Business Registrations Licensing Agency

CAADP Comprehensive African Agriculture Development Programme

CAMARTEC Centre for Agricultural Mechanization and Rural Technology

CGIAR Consultative Group for International Agricultural Research

CIAT Centro Internacional de Agricultura Tropical (International Centre for Tropical

Agriculture)

CPD Continuing Professional Development

CRDB Cooperative Rural Development Bank

CRS Catholic Relief Services (also sometimes known as Caritas)

DAADP Comprehensive African Agriculture Development Programme

DRC Democratic Republic of Congo

DRT Department of Research and Training

EAC East African Community

EAGC Eastern Africa Grains Council

EAIRO East African Industrial Research Organization

EBT Exim Bank (Tanzania)

FAO Food and Agriculture Organization

FBO Faith Based Organization

FDI Foreign Direct Investment

FEWS NET Famine Early Warning Systems Network

GAPEX General Agricultural Products Export Company (GAPEX)

GDP Gross Domestic Product

GM Genetically modified, Genetic modification

IITA International Institute of Tropical Agriculture

IRDP Institute of Rural Development Planning (IRDP)

IRRI International Rice Research Institute

KATRIN Kilombero Agricultural Research and Training Institute

MATI Ministry of Agriculture Training Institutes

MFI Microfinance Institutions

MITM Ministry of Industries, Trade and Marketing

MKUKUTA National Strategy for Growth and Reduction of Poverty II (NSGRP II: MKUKUTA is the

Swahili acronym)

MLFD Ministry of Livestock and Fisheries Development

MUCCOBS Moshi University College of Cooperative and Business Studies

MWI Ministry of Water and Irrigation

NADO Njombe Agricultural Development Organization

NALPIG National Agriculture and Livestock Extension Policy and Implementation Guidelines

NARS National Agricultural Research System

viii Soya Bean Value Chain Analysis

NBC National Bank of Commerce

NBS National Bureau of Statistics

NGO Non-Governmental Organization

NMB National Microfinance Bank

NMC National Milling Corporation

NPS National Panel Survey

NSCU National Soybean Coordinating Unit

NSRGP National Strategy for Growth and the Reduction of Poverty

OCHA United Nations Office for the Coordination of Humanitarian Affairs

OFC Overseas Food Corporation (the “Groundnut Scheme”)

ORP Oilseeds Research Programme

OUT Open University of Tanzania

PASS Private Agricultural Sector Support Programme

PHS Plant Health Service

PMO-RALG Prime Minister’s Office-Regional Administration and Local Government (PMO-RALG)

PPP Public-Private Partnership

R&D Research and Development

RATIN Regional Agricultural Trade Intelligence Network

RUDI Rural and Urban Development Initiatives

RUTF Ready to Use Therapeutic Food

SACCOS Savings and Credit Cooperative Society

SADC Southerna Africa Dvelopment Community

SAGCOT Southern Agricultural Growth Corridor of Tanzania

SIDO Small Industries Development Organization

SME Small and Medium Enterprises

SPS Sanitary and Phytosanitary

SUA Sokoine University of Agriculture

SUIT Special Units for Implementation

TAC Tanganyika Agricultural Corporation

TAFMA Tanzania Animal Feed Manufacturing Association

TASTA Tanzania Seed Traders Association

TBS Tanzania Bureau of Standards

TDV Tanzania Development Vision 2025

TFDA Tanzania Food and Drugs Authority

TIB Tanzania Investment Bank

TIN Tax Identification Number

TIRDO Tanzania Industrial Research Development Organization

TOSCI Tanzania Official Seed Certification Institute

TPB Tanzania Postal Bank

TPRI Tropical Pesticides Research Institute

TRA Tanzania Revenue Authority

TSDS Tanzania Soybean Development Strategy

USAID United States Agency for International Development

UDSM University of Dar es Salaam

UNICEF United Nations Children’s Fund

USDA United States Department of Agriculture

WARDA West Africa Rice Development Association

WEF World Economic Forum

WFP World Food Programme

ZARDEF Zonal Agricultural Research and Development Fund

ZSC Zonal Steering Committee

Tanzania Southern Highlands Food Systems ix

GLOSSARY OF KISWAHILI WORDS AND PHRASES

(most of these in the text are placed between single quotation marks)

dagaa sun dried small fish, mostly from Lake Victoria (a much valued human food that

is also used as a major protein source in animal feeds: sometimes quaintly

translated as “sardine” to distinguish it from commercial fishmeal)

kilimo kwanza agriculture first

lishe literally “feed”: in this context, cereal flours fortified with soya

soya ni pesa soya is money

tuborishe chacula let’s improve food, let’s make food better

ugali thick maize porridge

uji thin maize gruel

x Soya Bean Value Chain Analysis

Tanzania Southern Highlands Food Systems xi

EXECUTIVE SUMMARY

The soya bean value chain extends from the primary producer to the consumer whether this latter be a

human being making use of soya and its products to improve his or her diet or an animal whose diet is

being improved by its owner. Producers are overwhelmingly in the traditional systems who grow a small

area of soya mainly as a diversification crop and use the product for their own consumption or for sale to

contribute to household income. There is little large scale production although there is increasing interest

by this class of farmer who not only sees the crop as a means of diversification but also as a contributor

(through nitrogen fixation) to improved soil fertility and better structure. Large farmers are also aware

of the current and future industrial demand for a high quality protein to be incorporated in to animal feeds.

The limited area of production is exacerbated by fluctuating but generally low yields that are due in the

smallholder sector to poor crop management and little use of fertilizer and on both small and large scale

farms by the limited availability of quality seed and the absence of adapted varieties (only two varieties

are officially certified for use in Tanzania). The Southern Highlands – particularly the area around Songea

and Njombe for smallholder production and the “Ihemi Cluster” south of Iringa for large scale production

– are the foci of most soya cultivation. There is increasing demand for soya for use as a fortifier in human

foods and there is an active cadre of small to medium scale entrepreneurial processors (mostly women)

servicing this requirement. Similarly there is a growing demand for soya as an ingredient in animal

(especially poultry) feeds. Much of the demand for animal feed is met by imports of meal or cake from

India and from neighbouring Zambia, Malawi and Uganda. Current national production is estimated

(more likely guessed) at 5000 tonnes per year from about 5000 ha of land. The official Tanzania Soybean

Development Strategy projects (unrealistically) production of 2.0 million tonnes of soya from 1.4 million

ha with 40 per cent being used for processing and 35 per cent for export by 2020. The potential for greatly

increased production and for export is, nonetheless, enormous. Tanzania has natural resources suitable

for soya bean production and the country is well placed geographically to supply external demand. It has

so far failed to capitalize on its natural comparative advantage and there have been virtually no exports

of beans or meal.

The value chain includes a large assemblage of participants at several levels. These include smallholder

and large scale primary producers, brokers (who put producers in contact with potential purchasers, agents

(who buy and sell often to order for processors), dealers (who buy and sell often without handling any

product), small and medium scale processors (and their staff and labourers) who use soya as an additive

to staple foods, animal feed manufacturers, importers, wholesalers, institutional customers (World Food

Programme, Save the Children, retailers (supermarkets and small shops) and consumers. To these may

be added suppliers of inputs, research and extension workers and policy makers. There are as few as two

links between the producer and the plate but there may be up to ten transactions before the final product

gets to the consumer. Most participants seem to operate on low margins although the biggest profits

appear to be between the processor and the wholesaler and the wholesaler and retailer. Sales of product

are almost all by individual bargaining in one-on-one situations but local prices – which fluctuate

considerably within and between years – are known to both sellers and buyers and deals are usually

concluded quickly and amiably. Very little use is made of new technology at smallholder producer level

but large scale producers are generally well mechanized throughout the production cycle and make use

of appropriate fertilizers. Technology in the small producer enterprises is also basic including mostly

manual operations for packaging, sealing containers and labelling. Many of the smaller processors have

not yet adopted bar coding as a means to differentiate their products and assure traceability.

A recent analysis of global food security placed Tanzania in 99th place among 105 countries with four of

the six countries below it being contiguous (Burundi, Democratic Republic of Congo) or near (Ethiopia,

Chad) neighbours. According to the World Bank Tanzania ranks 127 out of 183 countries in doing

business with the regional average being 137. Concurrently the World Economic Forum finds Tanzania

xii Soya Bean Value Chain Analysis

to be one of 37 factor-driven economies and ranks it 120 (down from 113 the previous year) out of 142

and cites the major reasons for this lowly position, in order of priority, as access to finance, corruption,

tax rates, inadequate infrastructure, inflation and inefficient government bureaucracy. This does not bode

well for encouraging external nor internal investment in new or the expansion of existing businesses.

Tanzania is widely regarded as a country with a heavy regulatory burden that is only lightly implemented.

Participants in agricultural value chains are subject to an onerous regime of form-filling and permissions.

Multiple – and often conflicting – legal instruments under the jurisdiction of multiple ministries and other

official bodies impinge upon the agricultural, trading and marketing sectors. In general, however, value

chain participants are ignorant of the laws or choose wilfully to ignore them, being virtually safe from

sanction as they know the responsible authorities are in no position (financially and materially) to enforce

them. The Tanzania Soybean Development Strategy (such a strategy or policy has been developed for

each crop and livestock species in the agricultural sector) is designed to stimulate soya bean production.

In addition to aspiring to a production of 2.0 million tonnes in 2020 it is the aim of the to increase soya

bean consumption from 0.5 kg per person per year to 15.0 kg per year, increase local soya bean processing

into various products, ensure a significant increase in the contribution of soya bean to poverty reduction,

malnutrition, employment and national GDP and increase Tanzania’s competitiveness as a soya bean

producer and exporter in Africa and worldwide. The strategy emphasizes the importance of competitive

markets including commercialization, value added products and sustainable development and is said to

be amongst many of Tanzania’s initiatives to invite and open doors for private sector investments.

Weak horizontal and vertical linkages affect the whole chain. Participants and enterprises do not

cooperate or coordinate (indeed the latter seems to be a totally alien concept). The capacity to influence

domestic policy as well as more mundane aspects such as collective access to inputs and other service is

thus limited. In summary both horizontal and vertical integration remain marginal. The soya bean value

chain can be considered to be a “market-type governance” with many producers and many traders and

local retailers. Relationships among stakeholders in the value chain are mainly determined by the price

at which the product is sold. Coordination is required for the whole chain encompassing all participants

to generate communication and trust. The Southern Highlands Soya Bean Value Chain is largely driven

by market forces with respect to prices and their up- and down-stream effects on supply and operations

throughout the chain. The major issues include lack of governance, poor supervision of lower-end

associations, many small participants and small transactions, lack of market coordination, unclear and

conflicting roles and mandates in district councils, weak industry associations and inadequate or non-

enforcement of operating procedures.

Research on soya beans has been very limited. Extension services are poor with not very well trained and

poorly equipped staff. The ratio of service providers to service receivers is low. The transfer of extension

services from the centre to local authorities in the name of devolution has had an even further negative

effect on the provision of services.

Among the strengths of soya beans are near organic production suitable for niche markets, cheap local

high quality protein (40-45 per cent), oil (23 per cent) in strong demand worldwide, very suitable as

nitrogen fixer for inclusion in cereal rotations, as human food high in lecithin, calcium, phosphorous and

fibre, low in saturated fats, free of cholesterol, suitable for “fortifying” traditional staple foods, stores well

and is an almost ideal protein source in animal feeds, especially poultry.

Counteracting the strengths are weakness which that the value chain is weakly developed and fragmented,

there are few producer or processor organizations, the crop is relatively unknown in Tanzania, there is

little “management” by producers, there are inadequate road services in remote areas that lead to high

transport costs over long distances, very little research and extension on varieties and agronomy and there

are very few adapted varieties (only three are authorized for release in Tanzania) and a lack of quality

seeds.

Tanzania Southern Highlands Food Systems xiii

Opportunities exist in the organization of segments or of whole value chain into groups/associations to

strengthen powers (“empowerment”), there is rising internal demand for human food (awareness of health

benefits, individual consumption and population growth), Tanzania’s yung population (promises more

consumption in future), value can be added to basic product through differentiation, the crop is a

potentially important supplier of quality protein to human and animal diets, there is good potential for

rapid growth and agriculture is a national priority (‘kilimo kwanza’ = agriculture first).

Threats to development are high interest rates and unstable macroeconomic environment (exchange rates

and inflation), climate change may affect some aspects of production, imports have a negative effect on

local value added processing, there is competition from large overseas producers and there is little real

government support.

The problems of the industry are widely known as are the solutions. The quandary is to apply the latter

to the former. If this can be done the Vision could be:

By 2025, a more efficient and sustainable soya bean chain supplying raw materials for

fortification of human food and high quality protein for incorporation into animal feeds. It also

creates additional employment and contributes to increased incomes, reduced poverty, improved

food security and a better quality of life for all Tanzanians.

Strategic elements to improve the competitive status of the soya bean value chain include:

! improving knowledge, skills and information throughout (and before) the chain

(agriculture in schools, producer training, business training);

! promotion and strengthening of groups and associations throughout the chain to

encourage vertical and horizontal integration and to provide the industry with a “voice”;

! improving existing and providing new physical infrastructure to support the growth of

profitable agriculture and generate employment;

! development, equitable deployment and retention of human resources especially in the

livestock extension and animal health delivery services;

! promotion and adoption of science and technology including research and development

for high quality and nutritious food;

! strengthening and introduction of investment in infrastructure including for farm level

agroprocessing and physical market infrastructure;

! collection, collation and transparent and widespread dissemination of market information

including volumes of trade and prices;

! promotion of fair and competitive farm gate prices;

! strengthening of the links between farmers and markets and higher up the chain for

domestic, regional and global markets;

! promoting private sector investment and encouragement of public-private partnerships

(although great faith is placed on privatization and private sector investment it is not a

panacea)

! increasing the amount, broadening the range and improving the quality of processed soya

(fortified) products;

! ensuring that Tanzania’s soya products are produced (and can be verified as having been

produced) to international standards of food safety;

! facilitating access to finance and credit including links to capital and short term markets

and introducing insurance for crops;

! mitigating and adapting to the effects of climate change (research programmes to improve

existing and develop new technologies);

xiv Soya Bean Value Chain Analysis

! promotion of measures to cushion producers from the effects of drought and

strengthening of the Famine Early Warning System (FEWS);

! ensuring that land tenure arrangements for both traditional producers and those wishing

to invest in large scale production are favourable to long term investment; and

! implementing the National Strategy on Agriculture and HIV/AIDS to support increased

white meat production.

Strategic areas that need to be addressed include:

! sustainable use of land, water and natural feed resources;

! public, private and public/private sector investments and financing;

! improvement of the productivity and efficiency of production (including provision of

improved genetic material (varieties)), marketing and processing (and especially for small

scale processing of fortified human foods);

! rendering more effective the support services including research, extension, training and

dissemination of information;

! general capacity building (including linking large farmers to outgrower schemes) and

empowerment all along the chain;

! chain governance, regulatory and institutional arrangements; and

! cross-cutting and cross-sectoral issues.

Tanzania Southern Highlands Food Systems 1

White Meat (pigs and poultry) and Soya Bean subsectors have subsequently been added: throughout this1

report we have preferred to use “soya bean” rather than “soybean” other than in direct quotes or citations.

1. INTRODUCTION

1.1 Background of the Study and Objectives

The Southern Highlands Food Systems (SHFS) Development Programme comprises two projects – URT

132 “Food Systems Development in Tanzania” and URT 133 “Advisory Services Capacity Development

in Support of Food Security in the United Republic of Tanzania”. These were combined in 2010 with the

object of improved implementation. Both projects are closely aligned with the Government of Tanzania’s

Agricultural Sector Development Strategy (ASDS) that is designed to put in place a policy environment

more favourable to private investment in agriculture and provide sector-specific policies having a bearing

on agricultural productivity and profitability.

The overall project outcome for URT 132 is defined as “Public and private organisations and food chain

actors have improved capacity to coordinate, plan and support food chain and business development in

the rice, maize, edible oil and red meat sub-sectors of the Southern Highlands” . In order to achieve this1

outcome, the project has five major outputs:

! Output 1: Sub-sector specific strategies and priorities identified;

! Output 2: Public-private sector coordination and capacity strengthened;

! Output 3: Best practises for new market mechanisms promoted;

! Output 4: Food-chain innovation capacity strengthened; and

! Output 5: Strategies to improve capacity utilization of agro-processing facilities identified

The envisaged outcome for URT 133 is “Enhanced capacity of advisory service providers and farmers in

farm management and marketing to enable them to respond better to market opportunities”. This project

is also expected to contribute to Government restructuring efforts by focussing on market oriented

extension. The interventions are expected to enhance farm profitability and competitiveness and the

income derived from farming operations through four outputs:

! Output 1: Awareness of policy makers and programme managers to market oriented

agricultural extension and knowledge of “good practices” heightened and realized;

! Output 2: Capacity of advisory service providers in farm management and marketing at

central, district and ward levels developed;

! Output 3: Capacity of smallholder farmers and farmer groups developed; and

! Output 4: Linkages between producer groups, private agricultural service providers and

financial institutions and market outlets established.

Value chain analysis thus cuts across both projects and their outputs.

The major objectives of the study were to:

! identify strengths and bottlenecks in production, processing, marketing and the

institutional environment of the Tanzania soya bean industry and establish links amongst

performance drivers along the value chain with efficiency/competitiveness issues;

! present and take part in a validation workshop with public and private sector stakeholders

on the results of the assessment;

! propose strategic interventions to government and private sector stakeholders regarding

the improvement of organization and performance of the soya bean chain with a view to

increasing efficiency and competitiveness; and

! prepare a publishable report on the “Tanzanian Soya Bean Value Chain Analysis”.

2 Soya Bean Value Chain Analysis

Neonotonia wightii (Am.) Lackey (formerly Glycine javanica L.), known as ‘fundofundo’ in parts of2

Tanzania, is a native herbaceous perennial with a strong taproot and trailing, climbing and twining stems: it is a

constituent of high animal feed value in many pastures in drier areas.

1.2 Methodology

The soya bean value chain analysis was undertaken in the period 9 August to 15 November 2013,

including a field mission in Tanzania from 13 August to 24 September 2013 in support of the Food and

Agriculture Organization (FAO) Programme “Tanzania Southern Highlands Food Systems”. The Mission

was conducted according to Terms of Reference furnished by FAO (Annex 1). During a comprehensive

work programme (Annex 2) meetings and discussions were held with stakeholders across the whole

spectrum of the sector (Annex 3) and many documents were consulted (Annex 4).

In brief the methodology of the study comprised:

! a thorough review of the literature and study of secondary data covering, inter alia, trends

in production, consumption and trade, yields, prices, concentration of production,

capacity utilization and description of the linkages within the soya bean value chain;

! limited collection of primary data through a series of field visits and detailed discussions

with stakeholders in both the public and private sectors;

! identification of key constraints limiting sector competitiveness and development; and

! identification and elaboration of policy options.

The range and breadth of the literature sources in Annex 4 show the wealth of data on the soya bean food

chain. Much of it, however, predates the mid 1980s and much of it is qualitative. There is such disparity

among quantitative data sources that its reliability and indeed its usefulness is open to doubt: data

presented in this report should thus be considered indicative rather than definitive.

1.3 Brief Overview of the Value Chain

1.3.1 Why soya?

The soya bean Glycine max (L.) Merr is a legume native to East Asia . It is classed as an oilseed and not2

as a pulse by FAO. Soya exhibits variable growth from heights of less than 0.2 to 2.0 m (Figure 1). Pods,

stems and leaves are covered with fine hairs. The leaves fall before the seeds mature. Seeds are very

variable in size and colour.

Among the multiple reasons for increasing the area of soya are: it provides a cheap source of locally

grown protein (40-50 per cent) and quality oil (~ 23 per cent) with high commercial value; soya is an

important human nutritional supplement especially for certain “at risk” groups as it is free of cholesterol,

high in calcium, phosphorous and fibre, low in saturated fats and contains isoflavones (anti-cancer

compounds; the current and expanding role of soya as an ingredient in commercial livestock feed; an

increasing number of small and large scale farmers growing or wanting to grow soya; rapidly increasing

long term national and global demand; nitrogen-fixing properties and effects on soil fertility and structure;

an excellent break crop in predominantly cereal rotations; fewer pests and diseases than other legumes

(although is a potential and increasing problem; grain resists ingress of water and stores well at low

moisture contents; suitable soils and climate in many parts of the country and especially in the Southern

Highlands; and international support for research for improved soya varieties and agronomy.

This combination of factors endows soya with the capacity for rapid and widespread expansion of

production.

Tanzania Southern Highlands Food Systems 3

Figure 1 A well grown crop of soya at Makuta Farm south of Iringa (Photo: Trevor Wilson)

1.3.2 The value chain

Soya bean is, and always has been, a minor crop in Tanzania. It contributes, nonetheless, to national and

household food supply, provides income, adds diversity to arable production systems and (as it is a

legume) fixes nitrogen that improves soil fertility and condition. Much of Tanzania is suitable for

cultivation of the soya bean and it is indeed grown in most areas. Favoured areas, however, are the

Southern Highlands (Iringa, Mbeya, Rukwa and Ruvuma Regions), Morogoro Region, the southern Lindi

and Mtwara Regions and the northern Arusha, Kilimanjaro and Manyara Regions. Most soya is grown

by smallholder farmers under rainfed conditions in small plots using local or “nondescript” varieties that

are produced from home saved seed and using traditional husbandry methods. Some larger mechanized

farms in the Ihemi Cluster of the Southern Agricultural Growth Corridor of Tanzania (SAGCOT) (Box

1) already grow, or have well advanced plans to grow, soya bean: these are or will be partially integrated

operations with some degree of processing and organized marketing. Soya bean contributes little to

Agricultural Gross Domestic Product (GDP) at present but has great potential to bestow much more.

Annual production of grain soya in the early twentyfirst century has been in the range of 3000-5000 tonnes

from a cultivated area of 5000-6000 ha.

Production of soya bean is effectively entirely for the domestic market but the supply is considerably less

than the demand. There are formal imports, mainly from India and neighbouring countries to overcome

the deficit and there are also some “informal” imports from Tanzania’s contiguous states.

4 Soya Bean Value Chain Analysis

Box 1: The Southern Agricultural Growth Corridor of Tanzania (SAGCOT)

“SAGCOT is about doing things differently to get things done and to make a real difference.

This is about business as unusual.”

SAGCOT is an agricultural public-private partnership that is designed to develop the Corridor’s agricultural

productivity and profitability. SAGCOT was initiated at the World Economic Forum (WEF) Africa summit of

2010 with the support of founding partners including farmers, agribusinesses and companies from across the

private sector together with the Government of Tanzania. The SAGCOT Investment Blueprint was launched

nationally by Prime Minister Pinda in Dar es Salaam and internationally by H.E. President Kikwete at the WEF

in Davos in 2011.

SAGCOT’s mandate is to mobilize private sector investment. SAGCOT’s general objective is to foster

inclusive, commercially successful agribusinesses that will benefit the region’s small scale farmers. In so doing,

it will improve food security, reduce rural poverty and ensure environmental sustainability. The specific

objectives are to:

! provide opportunities for smallholder producers to engage in profitable agriculture including

fostering strong links between smallholders and commercial agribusinesses, through

outgrower schemes;

! strengthen smallholder producer associations; and

! increase the area under irrigation.

The risk sharing model of a Public-Private Partnership (PPP) approach has been demonstrated to be successful

in achieving these goals and SAGCOT marks the first PPP of such a scale in Tanzania’s agricultural history.

The corridor concept developed by SAGCOT aims to link the central infrastructure ”spine” of road and rail

(running from the port of Dar es Salaam through Morogoro, Iringa and Mbeya to the Democratic Republic of

Congo (DRC) Malawi and Zambia) to targeted areas of high agricultural potential (the Clusters). In this way

a focussed, efficient critical mass of commercial farming (small scale, emerging or large scale) and agribusiness

can be developed.

The Investment Blueprint showcases investment opportunities in the Corridor and lays out a framework of

institutions and activities required to reap the development potential of the region. In addition to the Blueprint

the SAGCOT Greenprint focuses on Agricultural Green Growth (AGG) and identifies five priorities to create

an enabling environment for increasing green investment opportunities (conservation agriculture or precision

agriculture are such opportunities) via:

! agricultural extension;

! support for local organizations;

! systematic land and water use planning;

! producing guidelines for investment in land and agriculture; and

! a pro-AGG investment generation programme.

The SAGCOT Centre Ltd was opened for business in October 2011. The first cluster to be developed was

Kilombero where a Rice Partnership is being developed with the support of both the private sector and the

international community (especially USAID’s Feed the Future programme). The Kilombero Rice Partnership

brings together small and large scale rice farmers, including Kilombero Plantations Ltd and AKIRIGO (a small

scale farmers’ apex organisation), local, national and international agribusiness and research, extension and

demonstration operations. A Sugar Partnership is also under development in the Kilombero Cluster. The

SAGCOT Centre is now considering the Ihemi Cluster based loosely around Mafinga some 70 km south of

Iringa on the main north-south highway. The two crops selected for early development of their value chains are

soya beans followed by (Irish) potatoes. Expansion of soya bean cultivation provides one of the major

opportunities for cultivation in the Southern Agricultural Growth Corridor offering potential for import

substitution as well as for earning foreign exchange through export to regional and wider markets.

Tanzania Southern Highlands Food Systems 5

Soya is extremely important in human nutrition and is especially useful as a supplement for children and

the sick. It is also a major protein component of commercial livestock feed particularly for monogastrics.

For most applications some form of processing is required before it can be used. In Tanzania, however,

soya is not a traditional food and the transformation technology is not known. Smallholder adoption of

soy bean as a crop would be facilitated by integration of consumption into local diets but dissemination

of processing and cooking methods would be required to achieve this.

Actual or potential soya markets in Tanzania include household consumption, small and medium scale

food processors, small and medium-to-large scale animal feed processors and – in the future – exports.

Local production is dominated by small farmers who cannot benefit from economies of scale and often

make “emergency” sales for immediate needs. Small traders buy at the production point and move the

product to processors and consumers in a generally ill-defined chain. Small traders dealing in small

amounts that are subject to physical and biological degradation do little to improve the end product.

The present situation with regard to animal feed production is that processors continue to use local low

cost fishmeal (‘dagaa’) as the main protein ingredient. The associated human health risks (due to

Salmonella contamination) and the taint (“fishy taste”) imparted to poultry meat are widely accepted.

‘Dagaa’ is a lower quality protein than soya bean meal, a fact that is encouraging some feed manufacturers

to turn to international soya markets where standardized quality beans and meal are available. Import

substitution should be a further driver to increased domestic soya bean production.

The sector is extremely undeveloped with few or no horizontal or vertical linkages in the chain. Low or

sporadic demand for soya and its products and tenuous market linkages do not encourage farmers to invest

in soya production. Some beans are sold in local markets to a few consumers for use to fortify local foods

but demand for home consumption is extremely limited. Some small and medium scale soya foods and

animal compound processors already make use of domestic production. Often, however, purchases are

very small (from small scale producers) or sporadic (from medium scale producers) which inhibits their

potential function as production drivers. Processor problems are exacerbated by others that include

product quality, inappropriate buildings, qualified labour, old machinery, excessive utility costs (coupled

to unreliability of supply) and operating capital that have a negative impact on efficiency and profitability.

Direct Government research since Independence on soya bean has been limited but this continues at Uyole

in the Southern Highlands. Some new varieties have been released and others are being developed and

tested. Sokoine University of Agriculture (SUA) has also undertaken limited research on the crop. In

common with the research community as a whole, attempts to improve soya production and processing

have suffered from limited funding and outmoded equipment for many years and research and

development (R&D) have suffered as a result. Extension services for soya are particularly weak and

devolution of these from the central Ministry and its branches to local authorities (who are even more

constrained for funds than the ministry and its specialized institutions) has been a brake on expanded soya

production. Some seeds and fertilizer and crop health inputs are available at many small private outlets

throughout the highlands and indeed over most of the country but these are not specific to the soya bean..

Broad opportunities exist for enhancing the soya bean value chain from the producer to the consumer.

There is increasing interest in the crop not only from the Government of Tanzania itself but also from

international development agencies and Non-Governmental Organizations (NGO) as well as the private

sector. Models need to be developed that can be applied and multiplicated throughout the Southern

Highlands. Promoting and building the technical and financial capacity of civil society organizations

(making use of existing producer, trader and processor organizations (such as Njombe Agricultural

Development Organization (NADO), Rural and Urban Development Initiatives (RUDI) and the single-

crop Kilombero High Quality Rice Growers Organization AKIRIGO)) and assisting in the creation of new

ones as models for soya bean production, marketing, processing and use could yield huge dividends.

6 Soya Bean Value Chain Analysis

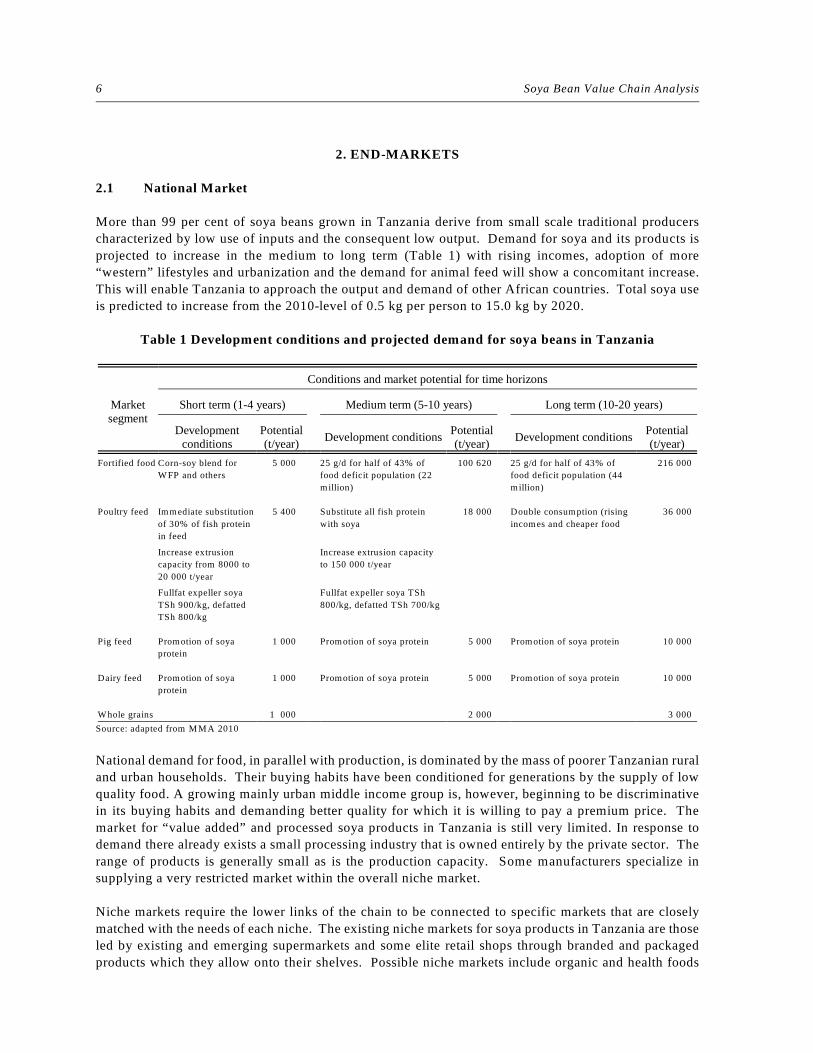

2. END-MARKETS

2.1 National Market

More than 99 per cent of soya beans grown in Tanzania derive from small scale traditional producers

characterized by low use of inputs and the consequent low output. Demand for soya and its products is

projected to increase in the medium to long term (Table 1) with rising incomes, adoption of more

“western” lifestyles and urbanization and the demand for animal feed will show a concomitant increase.

This will enable Tanzania to approach the output and demand of other African countries. Total soya use

is predicted to increase from the 2010-level of 0.5 kg per person to 15.0 kg by 2020.

Table 1 Development conditions and projected demand for soya beans in Tanzania

Marketsegment

Conditions and market potential for time horizons

Short term (1-4 years) Medium term (5-10 years) Long term (10-20 years)

Developmentconditions

Potential(t/year)

Development conditionsPotential(t/year)

Development conditionsPotential(t/year)

Fortified food Corn-soy blend for

WFP and others

5 000 25 g/d for half of 43% of

food deficit population (22

million)

100 620 25 g/d for half of 43% of

food deficit population (44

million)

216 000

Poultry feed Immediate substitution

of 30% of fish protein

in feed

5 400 Substitute all fish protein

with soya

18 000 Double consumption (rising

incomes and cheaper food

36 000

Increase extrusion

capacity from 8000 to

20 000 t/year

Increase extrusion capacity

to 150 000 t/year

Fullfat expeller soya

TSh 900/kg, defatted

TSh 800/kg

Fullfat expeller soya TSh

800/kg, defatted TSh 700/kg

Pig feed Promotion of soya

protein

1 000 Promotion of soya protein 5 000 Promotion of soya protein 10 000

Dairy feed Promotion of soya

protein

1 000 Promotion of soya protein 5 000 Promotion of soya protein 10 000

Whole grains 1 000 2 000 3 000

Source: adapted from M M A 2010

National demand for food, in parallel with production, is dominated by the mass of poorer Tanzanian rural

and urban households. Their buying habits have been conditioned for generations by the supply of low

quality food. A growing mainly urban middle income group is, however, beginning to be discriminative

in its buying habits and demanding better quality for which it is willing to pay a premium price. The

market for “value added” and processed soya products in Tanzania is still very limited. In response to

demand there already exists a small processing industry that is owned entirely by the private sector. The

range of products is generally small as is the production capacity. Some manufacturers specialize in

supplying a very restricted market within the overall niche market.

Niche markets require the lower links of the chain to be connected to specific markets that are closely

matched with the needs of each niche. The existing niche markets for soya products in Tanzania are those

led by existing and emerging supermarkets and some elite retail shops through branded and packaged

products which they allow onto their shelves. Possible niche markets include organic and health foods

Tanzania Southern Highlands Food Systems 7

and geographically differentiated ones with the last being distinguished by an institution, a company or

even a village. An entry point for geographic brand differentiation would be to develop, secure and

activate intellectual property rights for distinctive varieties of food products. The set of value enhancing

activities that is preliminary to entering this niche entails the prior creation and sharing of intangible assets

in the form of geographical indicators. A geographical indicator in this context is similar to a trademark

and can act as a certification that the product possesses specific qualities or enjoys a certain reputation

arising from its geographical origin. It the food source can be appropriately protected as intellectual

property it can provide farm groups with a sustainable competitive advantage

There is increasing demand for protein for inclusion in animal feeds with current demand being estimated

at 150 000 tonnes per annum. Currently there is considerable use of ‘dagaa’ but this is of variable quality

and the amount of sand in the product causes wear to machinery. Prices of ‘dagaa’ have also increased

which makes soya meal a safer alternative at a possibly lower cost. The dried fish are also likely to be

contaminated by salmonella bacteria salmonella that can cause food poisoning in people. Thus soya meal

is a preferred source of protein (and has several other nutritional advantages that are discussed later in this

report). As the local production is insufficient to supply this demand segment feed manufacturer import

by sea from India and by road from Zambia Meat consumption in Tanzania.

Increased globalization and the influence of information technology mean that more and more local

consumers have access to knowledge on health and safety issues related to food products. It is thus

important that livestock feed industries are aware of and respond to this trend. They should then produce

feeds with the desired raw materials to ensure that the final products possess acceptable standards that can

guarantee demand. If the Tanzania livestock industry is to improve its access to markets and achieve

international recognition the use of acceptable feed ingredients is one of several critical attributes that will

ensure consumer confidence.

2.2 Export Markets

The soya bean and its meal derivative are among the most important agricultural traded products in the

world. During the 52-year period 1961 to 2012 world production of soya beans rose about 10-fold from

26.9 million tonnes per year to 253.1 million tonnes per year on a harvested area that increased less than

5-fold from 23.8 million ha to 106.6 million ha (FAO 2012). In 2010 the amount of soya bean exports

around the world was 83.4 million tonnes valued at US$ 39.7 billion tonnes (US$ 425/tonne) and soya

beans occupied second place in world trade in terms of value. In addition to whole beans, 64.5 million

tonnes of soya cake were exported valued at US$ 22.7 billion (US$ 353/tonne) with this product

occupying eighth place in value in world trade (FAO 2012). The United States of America, Brazil,

Argentina and China were by far the largest producers of the crop in 2012. The first three of these

countries were also the largest exporters. China was by far the largest importer of soya and its products

followed by Japan, The Netherlands, Germany and Mexico. Current global demand for soya beans is

driven by the need for protein meals for the dairy and meat industries, World prices are mainly influenced

by those pertaining in Argentina and Brazil and at the Port of Rotterdam. The world price increased by

48 per cent in 2007/2008 due to a stagnant supply and a globally heavy demand and is expected in the

medium term to continue because of shrinking carryover stocks. Expansion of the area cultivated to soya

in South America and improvements in yield can be expected to stabilize prices up to a projected 2017-

2020.

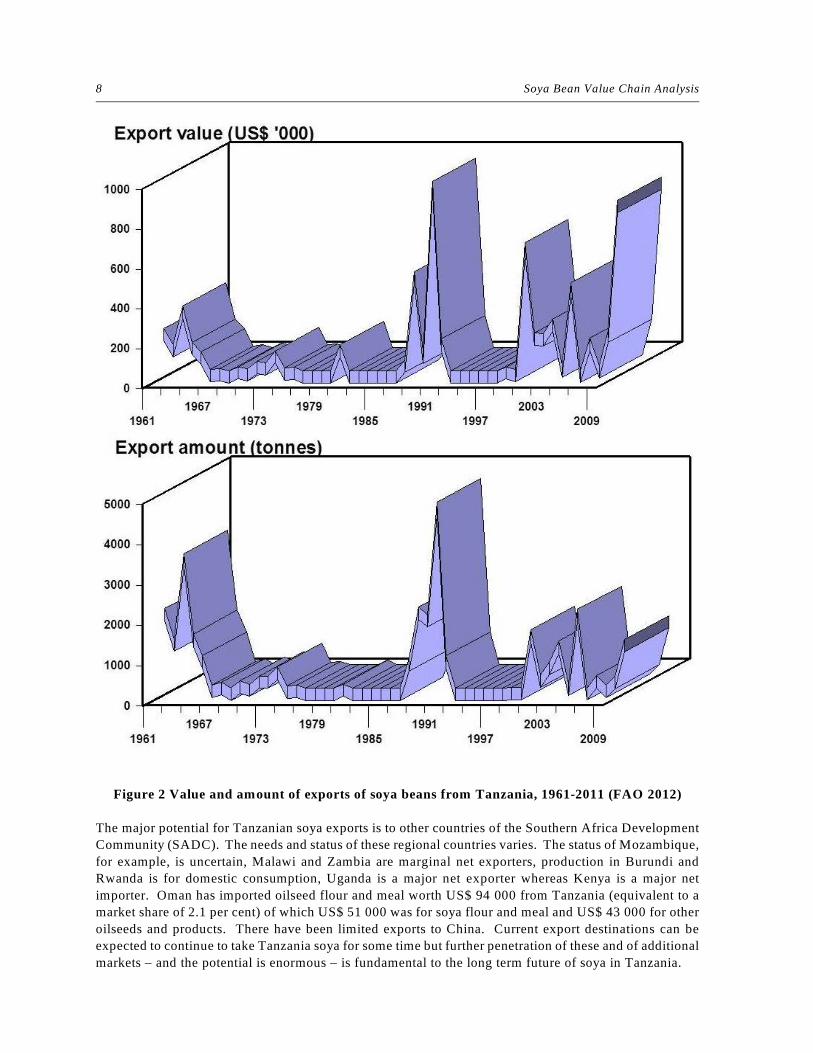

There are no official data for exports of soya from Tanzania. The county has, however, long exported

soya beans either for comparative breeding trials in other countries or as an item of commerce (Figure 1).

In the 1960s much of the Tanzania crop, and much of this from the farms of the Overseas Food

Corporation (OFC, the “Groundnut Scheme”), was exported to the Far East. A few years later the

Japanese attempted to negotiate a concession to grow soya for export to their own country.

8 Soya Bean Value Chain Analysis

Figure 2 Value and amount of exports of soya beans from Tanzania, 1961-2011 (FAO 2012)

The major potential for Tanzanian soya exports is to other countries of the Southern Africa Development

Community (SADC). The needs and status of these regional countries varies. The status of Mozambique,

for example, is uncertain, Malawi and Zambia are marginal net exporters, production in Burundi and

Rwanda is for domestic consumption, Uganda is a major net exporter whereas Kenya is a major net

importer. Oman has imported oilseed flour and meal worth US$ 94 000 from Tanzania (equivalent to a

market share of 2.1 per cent) of which US$ 51 000 was for soya flour and meal and US$ 43 000 for other

oilseeds and products. There have been limited exports to China. Current export destinations can be

expected to continue to take Tanzania soya for some time but further penetration of these and of additional

markets – and the potential is enormous – is fundamental to the long term future of soya in Tanzania.

Tanzania Southern Highlands Food Systems 9

3. THE SOYA BEAN VALUE CHAIN

3.1 Overview

The value chain describes the range of activities required to move a commodity through the various stages

that bring if from the first point of production to the last point of consumption. This usually involves (an

often complex) combination of physical change, inputs from various producer services, transfer of

ownership and delivery. Commodity value chains are increasingly recognized as providing a solid

framework for the analysis of the public and private sector participants within them as well as the overall

performance of particular markets.

The soya bean value chain from supply and use of inputs, via production and processing to marketing and

retailing and on to the consumer is confounded by many technical and institutional impediments. The

chain is fragmented, unorganized, disorganized, uncontrolled (in spite, in some links, of being over-

regulated) and uncoordinated. There is an unknown but, in terms of total smallholder families, few

households involved in primary production. A very few large farms grow soy beans on a regular basis

but more of this type of production is expected. Brokers or traders operate across most links of the chain.

Some processing is done at household level and there is a (growing) number of small and large scale

commercial processors who produce both human food and animal feed with soya as an ingredient. Human

food containing soya or soy bean meal is sold in some supermarkets and smaller retail outlets. Soya in

animal feeds is used by the manufacturer or sold retail to individual livestock farmers mainly in the poultry

layer or broiler segment. The horizontal and vertical linkages of the value chain are generally weak and

uncompetitive and in need of support to strengthen them.

The soya bean value chain includes whole beans and soya bean meal. Both items are produced mainly

for the domestic market (but see Figure 2 for long term exports). Imports are almost all soya bean meal

for the livestock feed industry and small amounts of oil for cooking. Processed products are derived after

some form of treatment to extract protein (the primary case in Tanzania) or oil. Soya bean meal is the

material remaining after solvent extraction or mechanical expelling of oil from the bean and has a protein

content of about 50 per cent. The meal is “toasted” (a misnomer because the heat treatment is with moist

steam) and then ground in a hammer mill before being incorporated into animal feed. Participants in the

chain include primary producers, traders, processors, wholesalers and retailers and consumers. Most

participants are rather specialized and their functions relate to one or a very few links in the value chain.

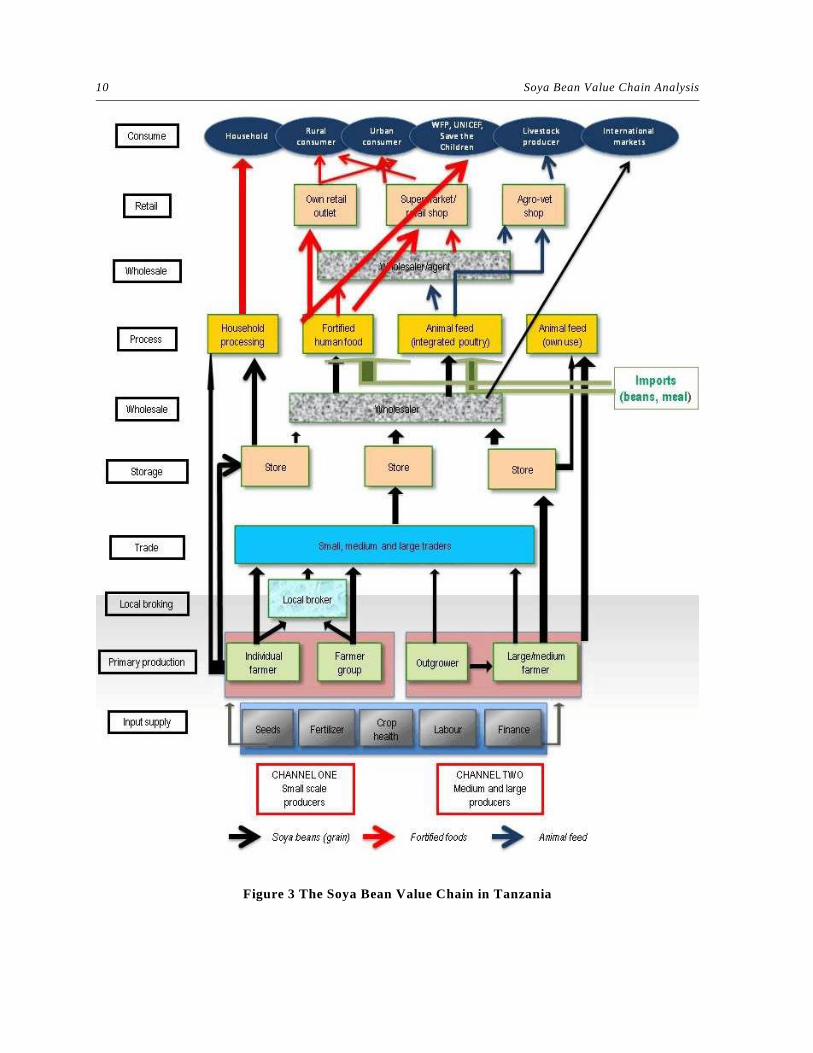

3.2 The Value Chain Map

The value chain map (Figure 3) shows that the whole is suspended from the end user. If the link to the

rest of the chain were to be broken the whole would be susceptible to collapse. This situation is more or

less true for all other links in the chain. Each link takes the product from its immediate predecessor and

“processes” it to an output that is used by the next link. Nominally, the value of product increases at each

stage until it reaches the consumer.

It is possible to provide a succinct list of most of the participants in the chain (Table 2) but pivotal roles

are played by the middle links through which all products must pass. Many participants in the chain

(Table 3) occupy more than one role. Further up the chain some processors are also wholesalers and

retailers and operate in both the domestic and export markets. Primary producers may sell beans directly

through a market, to a trader or to a processor or may use a combination of all three outlets. A trader can

sell to another trader, directly to a wholesaler or retailer or to a processor or, again, may broaden his option

by using a combination of these channels. Processors, especially the smaller enterprises, may buy beans

directly from farmers or from traders and sell the products to wholesalers or retailers.

10 Soya Bean Value Chain Analysis

Figure 3 The Soya Bean Value Chain in Tanzania

Tanzania Southern Highlands Food Systems 11

Table 2 Simple listing of supply and service participants in the Soya Bean Value Chain

Core actors Service suppliers

Producers (smallholder farmers, farmer groups, large

scale farmers with possible outgrowers)

Traders and agents

Processors

Wholesalers

Retailers (shops, supermarkets)

Importers (soya meal from India and Zambia)

Research

Training and Education Institutions

Extension service

Inputs (seed, fertilizer, plant health products)

Transport

Financial services

Associations (producer, trader, processor)

Cereal and Mixed Crops Board

Table 3 Participants and functions in the Soya Bean Value Chain

Participant Functions

Producers Most soya beans are grown by traditional smallholders, mostly located in the Southern

Highlands with another group around Babati in Manyara Region, who use little technology.

Some small scale farmers are receiving support from NGOs in technology and group formation.

Large scale grower are concentrated in the so-called Ihemi Cluster of SAGCOT around Mafinga

(some already have “outgrowers” and others have plans to develop an outgrower programme.

There are other large scale producers in Arusha and Kilimanjaro Regions.

Traders Primary buyers or brokers and secondary buyer-agents operate throughout the country wherever soya isgrown. Trading usually takes place at the point of production. A majority of traders have close links withthe processors.

Processors Some large scale and numerous small and medium scale processors operate mainly in Dar es Salaam andArusha with limited presence elsewhere in the country. Processing is for inclusion in human foods asfortifiers. Numerous (as many as 500 with trading licences) small private retailers sell small quantitiesof feed and feed additives and supplements. Main products are Chick Starter (and a more expensiveversion containing a coccidiostat), Layers, Broiler Starter, Broiler Growers and Broiler Finisher: in 2013all is in the form of mash although some firms have or will shortly have pelleting capacity. There is noregular production of pig compound feeds. Many small producers buy ingredients and mix their ownconcentrate feed.

Wholesalers Most processors act as their own wholesalers although there is a limited number of independent specialistdealers.

Retailers Processors often act as their own retailers. Supermarkets are the main retail outlets although soya fortifiedfood product are also occasionally on sale in small urban and rural shops. Retailing of soya beans isusually done by recognized but informal businesses.

Input suppliers Little use is made of modern inputs by smallholders. Seeds are available in very limited quantities throughUyole, the Agricultural Seeds Agency (ASA) and other suppliers. Fertilizer and crop health products areavailable at agro-dealer shops. MAFC and the municipalities provide limited extension services.Financial services are extremely limited and available only to a favoured few.

Research Public sector research on soya is very limited. Uyole Agricultural Research Institute Mbeya has a singleresearcher working on soya. It also has responsibilities in training and extension. Some large farmersundertake their own “research”, mainly in the form of variety observation plots: one farmer iscollaborating with the Centro Internacional de Agricultura Tropical (CIAT, International Centre forTropical Agriculture) in this kind of trial.

Every link in the chain relies on goods and services in order to fulfil its role(s). At the various stages,

goods and services include land, labour, soya beans and meal, input suppliers for fertilizers and plant

health products, transport, energy and finance. Also required are clearly defined and enunciated standards

and a regulatory framework under – and applied by – law. Many of these requirements continue to be

weak or non-existent in Tanzania.

12 Soya Bean Value Chain Analysis

3.2 Technology Generation

Technology in soya bean production includes inputs such as seeds of improved varieties, fertilizer, crop

health products (weed killers and pest control items for insects, fungi, viruses and bacteria), machinery

use for agricultural operations and for processing and proper and hygienic presentation of products at the

retail level. Technology has a key role in improving competitiveness and especially vis-à-vis near

neighbours operating in and competing for the same environment.

Soya bean production in the Southern Highlands is of two types. The one, dominant, is based on

traditional systems that use very little modern technology on individually small areas ranging from a few

hundred square metres to upwards of one hectare in area. The other, subordinate at least for the present,

is a large scale “modern” system with areas of up to 100 ha that uses a range of inputs and operates with

modern machinery.

Several technological interventions suitable for small scale are available but for the most part they are not

used by producers and probably not even communicated to them by technical staff. Some are somewhat

sophisticated or too expensive for use at the present state of development of soya bean cultivation. Low

adoption of available technologies is caused by poor extension services, difficulties in gaining access to

the technologies (cost/location) and the low level of knowledge among most soya bean producers.

The Agricultural Research Institute-Uyole (properly the Southern Highlands’ Zone Agricultural Research

and Development Institute) has the mandate for applied research for the Southern Highlands. It is

committed to undertaking research and facilitating the adoption of appropriate technologies in the region.

Its impact is limited, however, by low staffing levels and limited budgets. Similarly the official extension

services suffer from the same problems.

Adoption of known, improved, but not over ambitious management and technological practices could,

however, bring about spectacular increases in the output and quality of soya beans and their derived

products. Amongst such practices are:

! use of seeds of high yielding varieties (these are rare in Tanzania);

! inoculation of seeds with suitable strains of Rhizobium to encourage strong growth

(suitable strains are, in the main, still to be identified for particular soya varieties and

local environments);

! timely planting, weeding and harvesting;

! use of correct fertilizers for legume crops;

! application of crop health products (arthropods, fungi, viruses and bacteria) when

indicated; and

! storage under suitable conditions of temperature and vermin control. Failure to overcome

the lack of use of available, effective, cheap and simple technology will inevitably result

in even further loss of competitiveness as the peers of Tanzania’s crop producers and

processors in neighbouring countries, especially Kenya, Uganda and Zambia, are making

widespread use of it.

3.3 Input Supply and Demand

The most important inputs for soya bean production are perceived to be:

! seeds;

! fertilizers and crop health products;

! fixed and mobile equipment and tools;

! credit.

Tanzania Southern Highlands Food Systems 13

Limited access to inputs including credit and poor dissemination and uptake of knowledge on management

are recognized constraints to development of the smallholder sector. There is no mention of soya in either

the ASDP Performance Report or the National Panel Survey (NPS) for 2010/2011. According to the NPS

the f arming sector is characterized by extremely limited use of modern inputs. Fertilizer use declined

after the phasing out of subsidies in 1991-1994 but since the return of limited subsidies fertilizer use has

increased again. Only 32.1 per cent of farmers used fertilizer in 2010/2011, much of this being organic

(i.e. farmyard manure) but, on the positive side, the regions with highest fertilizer use were Ruvuma and

Mbeya. It must be noted, however, that the Southern Highlands (Ruvuma, Mbeya and Iringa) are the

major focus for the National Agricultural Input Voucher Scheme whereby 51 per cent of farmers used

chemical fertilizers with 65.3 per cent of these using a voucher to purchase inputs. Even where it is used,

fertilizer application across all crops is in the range 5 kg/ha to 8 kg/ ha whereas annual nutrient depletion

is 61 kg/ha. Tanzania has some of the worst soil nutrient depletion in the region, making the case for more

fertilizer use all the more compelling. Use of insecticides and fungicides decreased from 17 per cent in

2002/2003 to 14 per cent in 2007/2008. The percentage of farmers purchasing seeds dropped from 35 in

2008/2009 to 28 in 2010/2011. Most seed purchases were of local varieties (which has the merit of

maintaining and even enhancing the diversity of the gene pool) with very few farmers buying improved

certified seeds or improved quality declared seeds. Given the status of soya research in the country it is

likely that the use of top quality seeds for this crop is lower than the general average for all crops.

The low level of mechanization among smallholders is both cause and symptom of rural poverty. Given

the generally abundant availability of land, a household’s capacity to maintain and increase its production

through use of a larger land area depends on how much labour it can hire or use labour-saving techniques

such as animal traction, tractors and minimum cultivation as well as the extent to which a market in land

exists and functions properly. A major limitation on farmer productivity (inputs versus yield) is the heavy

reliance on hand hoes – over 95 per cent of households use them as the main cultivating tool -- which

imposes obvious limits on the area that can be cultivated using family labour alone. The use of animal

traction is also limited but, whereas most farmers do not own an ox, some 18 per cent can afford to rent

an ox plough and 18 per cent also hire an ox seed planter. The use of mechanized traction and harvesting

machinery is less than 10 per cent for the former and virtually nil for the latter. Only 14 608 households

(0.3 per cent) use power tillers (“Kubota” in local parlance) and these are mainly for rice.

The majority of farmers are purely subsistence operators. One third of farmers sell part of their crops

(mainly maize and paddy). Postharvest storage is used to gain a better price out of season. Some 67 per

cent of farmers store their product in sacks or open drums whereas 17 per cent store using older traditional

methods. Storing under methods that would decrease postharvest losses such as improved local structures,

purpose-built structures and airtight drums is used by only 6 per cent of farmers.

Access to credit from commercial banks, Savings and Credit Cooperative Societies (SACCOS) or other

formal lenders is still very restricted. In 2010/2011 only 2.2 per cent of farmers said they received credit

for purchase of inputs such as improved seeds, fertilizers or fungicides.

Access to extension services is not quite so limited as access to credit yet it is not widespread. Just over

one quarter of rural producers received advice on production practices. Access seems to be positively

related to wealth. Public extension is supposedly widely available but there is clear inadequate provision.

There are the beginnings of private extension by seed, fertilizer and crop health wholesalers and retailers.

Access to extension services and inputs is better in and near towns where private suppliers with a range

of local and international products are rather common (Figure 4). The few distribution centres in rural

areas, especially in remoter locations, force producers to travel long distances to purchase inputs. Some

inputs are obtainable at rural markets and other informal distribution points but the risks are that the

products are counterfeit or have been diluted and there is little quality control. The imbalance in location

and availability of inputs – both physical and intellectual – is a fundamental problem for the chain.

14 Soya Bean Value Chain Analysis

Figure 4 Agro-vet retail outlet in Tunduma selling a range of seeds, fertilizers and crop health

products (Photo: Trevor Wilson)

Processors of fortified human foods and animal feeds face problems of supply of their basic material – the

whole soya bean. Fortified food processors are mainly small operations who obtain beans from the

Southern Highlands or the Babati area whence the supply is erratic and of inconsistent quality. Transport

costs are also high.

Feed manufacturers, especially the larger ones, have bigger requirements for soya beans. Soya bean meal

is increasingly being used as a protein replacement for fish meal but the local product is not preferred as

better (and more consistent) quality product that is also de-fatted can be obtained more cheaply from India.

The Tanzania Animal Feed Manufacturing Association (TAFMA) represents the animal feed

manufacturers. Several maize and wheat flour millers produce animal feeds and there are several

specialized companies in Dar es Salaam and its environs and many more in the larger towns (Box 2).

Millers who produce feed are, in effect, using a by-product – wheat or maize bran – of their operations

to produce a high value product whereas specialized firms have to obtain their ingredients from a variety

of sources: maize and wheat bran from internal resources, sunflower cake also from the local oil milling

industry (limited amounts of cotton seed cake are also used) and fish meal (made from pounded ‘dagaa’)

mainly from Lake Victoria. Compound feeds are more widely available in the populated areas than in the

remoter parts of the country where most pigs and poultry are found. Many medium scale producers resort

to mixing their own compounds from individual commodities, especially in the rural areas and especially

for pigs.

Tanzania Southern Highlands Food Systems 15

Tanfeeds has been successful in obtaining large amounts of grant and loan funding from two international3

sources: see Annex 10.

Box 2: Let them eat cake – supplements and concentrate feed manufacture

There is strong and growing demand – poultry feed production increased from 490 000 tonnes in 2001/2002 to

574 90 tonnes in 2006/2007 – for concentrate feeds and supplements from the white meat chain and for table egg

production. Poultry feed comprises a range of products including chick starter, chick special starter (with a

coccidiostat included), layers mash, broiler starter, broiler grower and broiler finisher each of different formulation

sold at a different price. Several industrial scale millers produce livestock feed, in part to add value to the maize