spanning the globe - socal afp scafp.pdfspanning the globe bank of america merrill lynch november...

TRANSCRIPT

Spanning the Globe

Bank of America Merrill Lynch

November 16, 2012

Southern California AFP

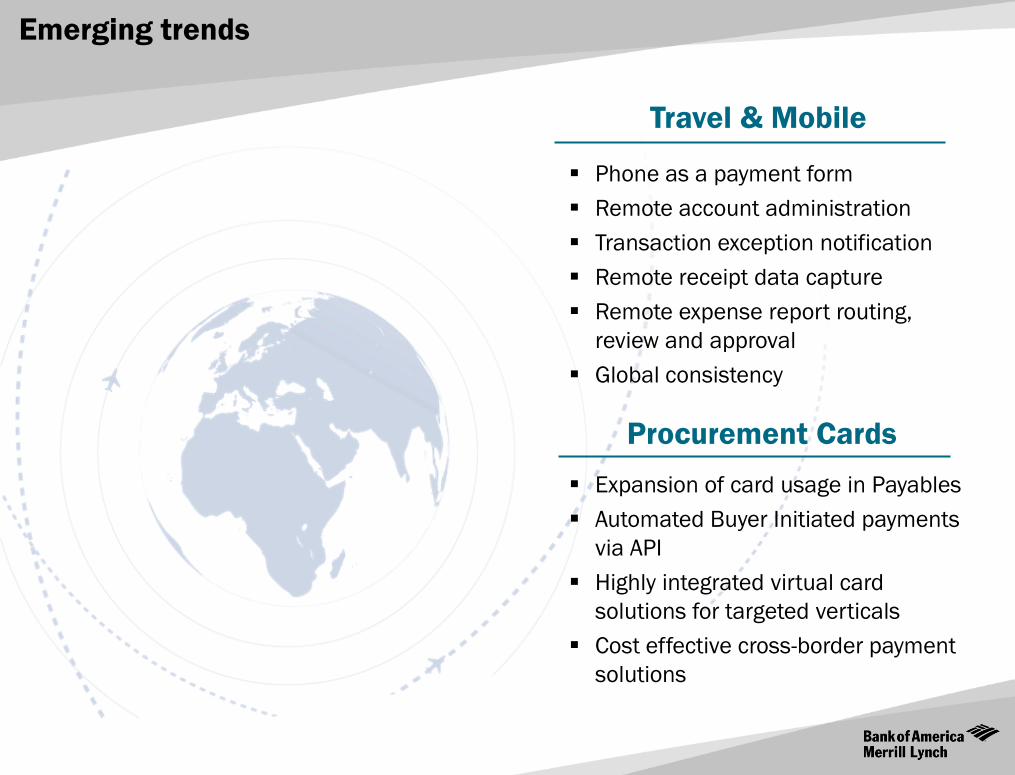

Emerging trends

Card growth

Corporate Travel models Vary

Procurement & Payables Cards Evolve

Inconsistent Approach

What’s in a Global Card program?

Key Elements of Any Global Card Program

Global Card Program Benefits

Four Factors for Achieving Success

Program optimization

Choose the right approach

Understand regional differences

Identify dedicated resources

Key Takeaways

2

agenda

Emerging trends

Phone as a payment form

Remote account administration

Transaction exception notification

Remote receipt data capture

Remote expense report routing,

review and approval

Global consistency

Travel & Mobile

Expansion of card usage in Payables

Automated Buyer Initiated payments

via API

Highly integrated virtual card

solutions for targeted verticals

Cost effective cross-border payment

solutions

Procurement Cards

Projected Commercial Card Purchase Volume Growth 2010-2015

Card Growth

Sources: Glenbrook Commercial Card Sizing August 2011, EIU Forecasts October 2011.

(1) MasterCard Commercial Growth Projections.

Projected Commercial Card

Purchase Volume 2010 $1.1T

41%59%

US ROW

Projected Commercial Card

Purchase Volume 2015: $2.2T

43%57%

US ROW

14.1

4.6

7.8 8.2 8.9 8.9 10.0

11.2 13.2 13.8 14.0 14.4 15.0 15.0 15.2

34.7

37.4

6.6

1.6 3.0 3.9 5.2 5.1 7.3

7.9 11.4

5.3 6.3

12.4

5.1

15.9 24.1

0.7

1.0

(1)

(1)

(1)

(1)

(1)

7.5 6.2 5.2 5.0 3.7 4.9 5.3 8.7 8.1

10.1

18.8

13.3

3.9 3.9 2.4 2.6

14.0

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Glo

ba

l

UK

So

uth

Afr

ica

Au

str

alia

Ge

rma

ny

Sp

ain

Can

ad

a

Fra

nce

U.S

.

Neth

erla

nds

Me

xic

o

Ko

rea

Ja

pa

n

UA

E

Bra

zil

Ind

ia

Chin

a

Nominal GDP Growth Secular Growth

Corporate Travel Models Vary

Corporate Travel Products

Individual Walking Card

Lodged Card & Walking Card

Lodged Card & Prepaid Card

Procurement & Payables Card Evolving

B2B Opportunities

BIP, Single Use, Supplier Cards

P-Card & Payables Cards

Initial P-Card Deployment

Inconsistence Approach

Multiple programs in

place with multiple

banks

Acceptance rate of card

brand can vary

Cards don’t support

cardholders — they don’t

work when needed

Different functionality by

country; makes

implementation,

management and

training more difficult

Collating paper expense

reports for approval gives

no visibility of data

Disparate card programs

provide limited or no data

electronically or create

paper processes

Reporting solutions

should be web based and

available 24/7/365,

multi-currency, multi-

language and should

support multiple countries

Lack of integration with

EMS & ERP systems

Company level support

needs to be available

within office hours for

program administrators

Cardholder support not

multi-lingual

Lack of local knowledge

and expertise around

highly complex country

laws and regulations

Card provider that is not

part of an integrated

treasury model

Lack of skilled client

advisory services and

single point of contact for

card solutions

CARD USAGE DATA VISIBILITY SERVICING

What’s in a Global Card Program?

Process efficiency and savings,

supporting paper to electronic migration

Reduced risk and improved cash flow

visibility

Seamless reporting, data integration

and consolidation

Consolidated view across currencies

and countries

Reduced foreign exchange expense

Settlement and payment in local

currencies with the convenience of a

single point of contact

Global and knowledgeable relationship

management

Multi-language cardholder and

company-level support and service in

local time

Key Elements of a Global Card program

COVERAGE

DEDICATED

SUPPORT

LOCAL

FOCUS

REPORTING &

INTEGRATION

Global Card Program Benefits

Strategically optimize payments

Take advantage of growing acceptance

Use robust platforms for flexibility and control

Having cards as a convenient tool for enabling start-up

expenditures

A single view into purchasing/T&E spend enterprise-wide

Help to avoid FX fees by transacting in local currencies

Help to enhance paper-to-electronic payments strategy

Ability to implement consistent controls, common purchasing tools

and uniform policies around the globe

Four Factors for Achieving Success

Identify

Dedicated

Resources

Program

Optimization

Understand

Regional

Differences

Choose the

Right

Approach

Program Otimization

Questions to ask:

What’s the best currency to use in a

country?

What’s the best way to structure a program

to ensure compliance with local laws and

regulations and to optimize the program

within cultural norms?

How can I leverage my global banking

provider to:

o Build out my program in local currencies

o Support due diligence on local banks

o Ensure consistent service levels

o Consolidate data globally

Program

Optimization

Choose the Right Approach

Leverage your banking provider to:

Assist you with issuing an RFP

Provide their intellectual capital to optimize

your program

Implement a global program that integrates

best practices by country and region

o Direct issuance

o Direct issuance combined with local

partnerships or consortiums

Provide completed due diligence on partner

banks and legal and regulatory

requirements

Facilitate data consolidation globally

Provide a central implementation manager

and account manager with global program

ownership

Choose the

Right

Approach

Understand Regional Differences

Regional and country differences in card programs drive the need to:

Utilize different product capabilities

Understand local card and cultural nuances

Understand different legal and regulatory environments

Understand

Regional

Differences

Identify Dedicated Resources

Identify

Dedicated

Resources

Implementation

Global, regional resources to build,

implement program

Builds reporting platform and hierarchies

to support reporting, data integration

Provides training to Program

Administrators

Servicing

Cardholder

Company-level

Account Management

Overall growth strategies and program

optimization

Best practice-sharing across clients and

industries

Acts as a point of escalation for issues

Key Takeaways

Obtain global consensus for Global Card program and approach to adoption

Manage your global expectations strategically

Determine your

requirements and

match needs with

solutions in market

Ensure you receive rich data that can be consolidated globally; reporting should be seamless

Know all the tools to integrate management of both travel and procurement expenses