(special session of imid 01) - 임기조 교수님 홈페이지 입니다. consumed in screen update...

TRANSCRIPT

FPD Roadmap & Market

(Special Session of IMID’01)

Contributors

J.K.Kim (Samsung Electronic)

P. Semenza (SRI)

M.R. Pinnel, J.N. Norman(USDC)

B.H. Lee, K.M. Kim(Samsung SDI)

Y.O. Kim(LG. Philips)

W.K. Lee(Samsung Advanced Institute of Technology)

Coordinator & Summary

Jae Soo Yoo, Professor

ChungAng University (http://display.cau.ac.kr)

전자부품연구원 디스플레이 기술 세미나자료 : www.eic.re.kr

Electronic Information DisplaysElectronic Information DisplaysElectronic Information Displays

CRTCRT FPDFPD ProjectionProjection

Emissive DisplayEmissive Display Non Emissive DisplayNon Emissive Display CRTCRT Light ValveLight Valve

PDPPDP VFDVFD FEDFED ELDELD LEDLED

LCDLCD ECDECD

TNTN STNSTN TFTTFT MIMMIM FLCDFLCD

Electronic Information DisplaysElectronic Information DisplaysElectronic Information Displays

CRTCRT FPDFPD ProjectionProjection

Emissive DisplayEmissive Display Non Emissive DisplayNon Emissive Display CRTCRT Light ValveLight Valve

PDPPDP VFDVFD FEDFED ELDELD LEDLED

LCDLCD ECDECD

TNTN STNSTN TFTTFT MIMMIM FLCDFLCD

The Big Picture

$65

$107

$375

$407

$402

$1,258

$8,486

$5,757

$41,841

$41,275$29,857

$16,801

$111

$128

$514

$626

$29

$781

$5,456

$2

$0 $5,000 $10,000 $15,000 $20,000 $25,000 $30,000 $35,000 $40,000 $45,000

FED

EL

MEMS

LED

VFD

OLED

PDP

LCD (Passive)

LCD (Active)

CRT

2000 2006

Why do a Roadmap?• Generate competitor dialogue to validate perceptions

• Define common issues, gaps, limits

• Evaluate market expectations and demand schedule

• Set technology advancement schedule

• Set performance targets

• Identify and prioritize tradeoffs

• Establish critical mass to enlist supply chain companies

• Distinguish evolutionary development needs from revolutionary advancements

• Compare/contrast with competing technology options

• Identify beneficial standardization topics

Expectations of a Roadmap:What it is and what it is not!

• Roadmap predictions usually are not precise, but they can be reasonably accurate

• A common understanding of trends and targets generates confidence in assessment of competitive position and strategic plan

• Roadmaps don’t have answers, but they make certain the right questions are being asked and the right challenges are being posed

• Roadmaps address WHAT needs to be done and WHEN it needs to be done, not HOW it is accomplished

• Roadmap activities help, not harm, competitive positioning

Roadmap Goal: Predict the evolution of the dominant FPDtechnologies and identify the opportunitiesfor alternative technologies to provide improved performance

Dominant FPD LCD on glass substratesTechnologies: PDP

Projectors with LCD and DMD light valves

Time Scale: 2001 -> 2005 ->2010

Qualification: Data included is for best commercial products,not for laboratory prototypes

Two Routes to Profitability

Reduce Costs

Reduce Costs

Reduce Costs

Reduce Costs

Reduce Costs

Reduce Costs

Improve Performance

Information Content

Response Time

Picture Quality

Power Efficiency… … … . .… … … . .

Information Content

Main metric: Number of pixels

Important factors:Pixel density - pixels per inch or- pixel size (mm)Screen size- diagonal length in inches

Benefits to customer:

•more efficient office work•word processing•spreadsheets•multiple windows

•clearer pictures•digital photography•medical images•geographic information systems•design•electronic commerce

•less eyestrain

Information Content - Status

Current Best: 200 ppi

22” a-Si LCD panel for work-stations9.2M pixels (3840x2400)

6.4” LCD panels for handheld PC0.8M pixels (1028x768)

4” LCD panels for PDA and e-phone0.3M pixels (640x480)

PDP and Projection technologies are well behind in information content,despite the larger screen size.

Projection systems can be tiled seamlessly to overcome this shortcoming.

Information Content – Conflicts

•Efficiency•small pixels lead to smaller aperture ratios

•Video display••large pixel numbers require high data rates (16 large pixel numbers require high data rates (16 GbGb/s for 9Mpixels)/s for 9Mpixels)

•Limits of human vision•200-250 ppi for laptops and desktops•300 ppi for handheld displays •150 ppi for conference/classroom/public use

•Software – OS and applications•must compensate for smaller icons, fonts etc

Information Content – Future Goals

Work-stations 20M pixels 40M pixels30” screen at 200 ppi 40” screen at 200 ppi

Handhelds 3M pixels 3M pixels8” screen at 300 ppi 8” screen at 300 ppi

Wall Displays 50M pixels 250M pixels8’ x 4’ screen at 100 ppi 20’ x 6’ screen at 150 ppi

2005 2010

Information Content – Paths to Progress

LCD

Projection

Alternatives

2005 2010

poly-Si TFTsbetter conductors – Ag,Cu?seamless tilingselective refreshnew drive schemes

LCOS light valves

Continuous grain TFTs

Scanned laser projectors

Flexible substratesRoll-to-roll processingAM-OLED

Response Time - Status

LCD 15-20 ms Liquid Crystal responsevarying with level of adjustment required

PDP Phosphor response – 15 msDischarge response – few msTime-modulated gray scale – 8-12 sub-frames

Projection ferroelectric LCDs are fast DMD is even faster

Response Time – Future Goals

2005 2010

LCD 8 - 10 ms 4 – 5 ms

PDP 10 bit gray scale 12 bit

Projection 4 - 5 ms 2 - 3 ms

Response Time – Paths to Progress

LCD

PDP

Projection

Alternatives

2005 2010

Smaller cell gapsReduced viscosityFerroelectric, OCB, ECB modes?New drive schemes

Continuous grain TFTs

?

FEDOLED

?

? ?

OCB = Optically Compensated BendECB = Electrically controlled birefringent

Power Efficiency

Metrics:Lumens created per WattWatts consumed in screen update

Factors:Efficiency of light creationEfficiency of light transmission

(e. g. aperture ratio)Efficiency of electronics

Ambiguities:Measure peak or average luminance?Standard measure of switching power

Benefits to Customer:

•Battery life•portable PCs•phones/PDAs

•Power cost•office displays•home entertainment•air conditioning

•Environmental impact•fewer power stations•less CO2 emission

Power Efficiency - Status

Transmissive LCD 1-2 lm/W

Reflective LCD < < 1 mW/cm2 for static images< 1 mW/cm2 for video

PDP 1.5 lm/W

Projection 14 lm/W

Power Efficiency – Future Goals

Trans. LCD 5 lm/W 10 lm/W

Refl. LCD - static 1 µW/cm2 0.5 µW/cm2

- video 10 µW/cm2 5 µW/cm2

PDP 3 lm/W 5 lm/W

Projection 20 lm/W 25 lm/W

2005 2010

Power Efficiency – Paths to Progress

LCD

PDP

Projection

Alternative

2005 2010

Integrate CF with arrayPoly-Si TFTsEmbedded memory or bistable modesMulti-format drivers

Improved geometriesNew addressing schemes

Better sources Improved light collection

OLED

Frame sequential color(O)LED backlight

Better materials

Electrophoresis

Application Cell Phone Video phone Internet access

HDTV/ Publicity

Color Mono Color Color Color Drive mode Passive Passive Active Active

Diagonal size 1.5" 3" 6" 60" Pixel number 128x64 320x240 640x480 1280x720

Pixel size (µm) 300 63x190 63x190 350x1050 Number of Colors 1-16 262K 262K 16.8M

Brightness (candela/m2) 100 300 300 500 Lifetime (hours) 10,000 10,000 20,000 30,000

Dark room Contrast 100 200 200 400 Contrast ratio at 100,000 lux 5 10 10 5

Viewing Angles (degrees) 160 160 160 160 Response Time (µsec) 10 10 10 10

Voltage 6 9 6 9 Power (mW) 200 500 600 30,000

Thickness (mm) 2 2 5 10 Weight (gms) 10 20 50 5,000

Year (on glass) 2001 2002 2003 - Year (on plastic) 2003 2004 2005 2006

Reference Display Parameters

OverviewLiquid Crystal Displays (J.K.Kim, Y.O.Kim)Plasma Display Panels (B.H.Lee)Organic Light-Emitting Diode Displays (K.M.Kim)Microdisplays, FED, … (W.K.Lee)Conclusion

Outline

Historical and projected growth in the FPD market

Source: DisplaySearch

InformationNetwork

Service

* CD-ROM

* DVD

* Game

* E-Paper

* Web

* On-Line DB

* Internet

* Cable

* Wireless

* Satellite

* E-Banking* On-Line Shopping

* E-Trade

User PlatformHomeM/M

NPC

PDA

Mobile Phone

E-Book

MobileM/M

D-TVPCSTBWeb PADDVC/DSC

Electronic commercial transactions over the network

Ⅰ. Market Outlook Answer for “?”

•Low Cost

•Monitor Market in earnest

•New Application Market- LCD TV- Web Pad- Car Navigation- …

4 / 9

Ⅱ. TFT-LCD Trends Application trends

Analog Analog / Digital Digital

1990 2000

• CRT leads the Market• TFT-LCD

• CRT vs. TFT-LCD• TFT-LCD leads the Market• PDP, OLED

•Calculator

•STN-LCD Display

•TFT-LCD NBPCSize / Performance Performance / Cost

•TFT-LCD MonitorSize Performance

Cost is a basic issue

•LCD TV Cost / Performance

•Small Mobile Performance

5 / 9

Word processorsWatches

CalculatorsPachinkoNegative growth

Portable LCTVs

Notebook PCsHome appliance

Camcorders/monitorsData projectors

FA, MEPortable game equipment

Car clocks/metersPortable phones100-199%

Automotive monitors

Electronics notebooksCamcorder/finders

Portable DVD playersDesktop monitors

Stand-alone TVsDigital Still Cameras200-299%

PDAsPublic display monitors300-499%

Industrial MonitorsProjection TVs500% or higher

Product NameGrowth Rate

Projected growth rate over the period of 1999-2005

Source: Fuji Chimera

Ⅱ. TFT-LCD Trends Product Performance trends

NTPCNTPC

MonitorMonitor

(13.3(13.3””XGA)XGA)

20052005

Weight

Thickness

Power Con.

20012001

390(g)

5.5mm

4.6W/150nit

320(g)

3.5mm

2.xW/200nit

160。

UXGA

200nit(IPS)

170 。

QUXGA

300nit

• IMT-2000• PDA• Web Pad

MobileMobileApplicationApplication(3.8(3.8””QVGA)QVGA)

W.V.A

Resolution

Brightness

Power Con.

Response Time

Weight

Core Technology

40mW

30ms

60g

Touch, Reflective

<30mW

<10ms

<40g

Circuit Integration

19981998

535(g)

6.5mm

4.0W/100nit

90。

/ 120。

XGA

200nit(film)

-

-

-

-

TVTV

Response Time

Brightness

Panel size(max)

<20ms

400nit

29”

<10ms

>500nit

40”class

-

-

-

8 / 9

TechnologySize

inchesMaximumResolution

Brightnesscd/㎡

Colorbits

ContrastRatio

PowerW

TFT LCD 24-42" 1080 lines >300 8 300-500:1 40-150

Plasma <40" 720 lines >300 8 150-200:1 300

Plasma >40" 1080 lines >400 8 250-350:1 400

HTPS .9-1.3" 1080 lines >1000 8 100:1 50-100

* HTPS: High Temp. P-Si for ProjectorSource: Display Search ‘99. 5, LCD added

The Winner Display;

•Which can render natural color ?•Which can provide reasonable price ?

HDTV Display Competitors

•400 - 500 cd/m2 for day light viewing

•300:1 Minimum Contrast

•Color reproduction > 70% of NTSC

•Color temperature > 9000 ̊ K

For Bright and High Contrast D-TV

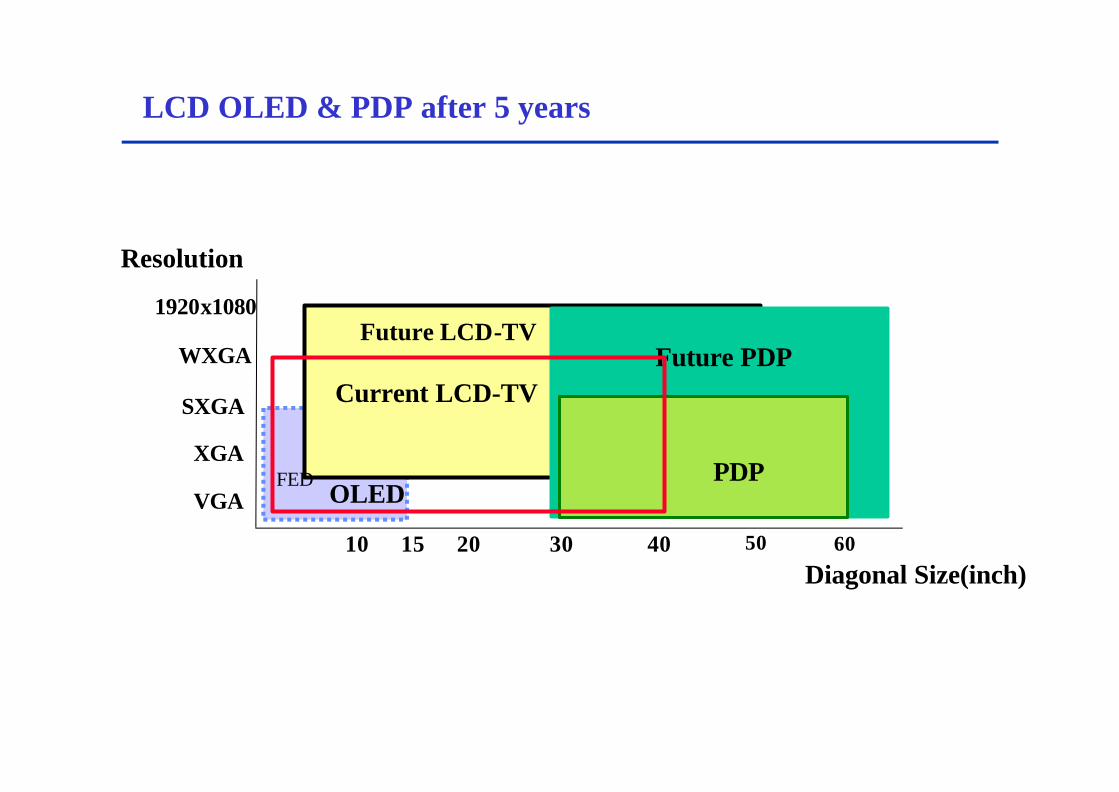

1920x1080

10 2015

Resolution

Diagonal Size(inch)

VGA

XGA

SXGA

WXGA

Current LCD-TV

FEDOLED

Future LCD-TV

LCD OLED & PDP after 5 years

Future PDP

30 40 50

PDP

60

-1% -1%

5%8% 8% 10% 11%

9%

8% 4%2%

-3%

-

5,000

10,000

15,000

20,000

25,000

Q1 '00 Q2 Q3 Q4 Q1 '01 Q2 Q3 Q4 Q1 '02 Q2 Q3 Q4

-30%

-25%

-20%

-15%

-10%-5%

0%

5%

10%

15%

Demand Supply Ratio

ü Continuous Glut till 2002 (over 10%) if every LCD maker invests as planed

ü Samsung’ forecast : Balance coming in Q3 ’02 by Capacity ramp-up delayMore investment will delay Balance over Q4 ’02

ü Uncertainty - Monitor demands increase (‘01 : 12M → 14~15M) - Demand of Small & Medium size (PDA,HHP,Game,AV etc)- TFT LCD line conversion to Small Size- Low Yield for High Resolution / Slim & Light Model

Demand & Supply

Lamp Reflector

LampPCB(Source)

Top Chassis

LCD Panel

Plastic Mold Frame

PCB(Gate)

Gate TCP(Flat Type)

Source TCP(Bent Type)

BEFDiffuserLGPReflector Sheet

Assembly structure of a TFT-LCD Module

- Larger Glass Size- Glass area utilization- Improve Cost of Ownership

Shorten TAT (Turn Around Time)Shorten Transportation distance

- Process SimplificationTFT Process reduction (7 5 4 mask step)Automation : LC & Module line

- Reduce number of parts

- Material reductionSpin coating slit coatingRecycling

Productivity

Cost saving

Panel Cost down approach

Mother Glass Size v. productivity

131.45

3.6

11.4510

Gen1

Gen 3Gen 3.5

Gen 4

Gen 2

Gen 5

5.65.0

Gen 1 Gen 2 Gen 3 Gen 3.5 Gen 4 (Gen 5)

300x400 370x470 550x650 600x720 730x920 1000X1200680x880 1100x1250

main product 10.4 12.1 14.1 14.1 /17 15 /17(x4) (x6) (x6) (x9)/(x6) (x15)/(x12)

Display Size & Pixel density for large screen

Screen Size

40”

24”

15”17”

Pixel Contents1M 2M

1280x768

1920x1200

1280x1024

1024x768

1280x76830”

4M

XGA .8 M pixelsSXGA 1.5 MUXGA 1.9 MD-TV 1M/2MWUXGA 2.3M

(1) High Volume Production- Cost burden divide by number of panels per glass

(2) High Yield mfg. Skills for large size

(3) Reduced process for cost down

(4) Materials cost saving

(5) New Process & Materials development

Challenge to $10/inch !(1)+(2)+(3)+(4)+(5)

Cost Effective Manufacturing

Roadmap ; an optimum set of products that Match the market requirements at the time market desire them

Suppliers ; develop the equipment and materials

Manufactures ; install and optimize the process

Correct Capacity to address the desired markets

Performance/Cost

The ideal goal of roadmap

Win / WinWin / Win

Thank You!

OverviewLiquid Crystal Displays (J.K.Kim, Y.O.Kim)Plasma Display Panels (B.H.Lee)Organic Light-Emitting Diode Displays (K.M.Kim)Microdisplays, FED, … (W.K.Lee)Conclusion

Outline

Plasma Display Panel Market Overview

•The worldwide color PDP system market will

exceed $2.7 billion in 2001 and $16.4 billion in

2006

•Nearly 314,000 PDPs will be shipped in 2001,

growing to 6.2 million in 2007

•PDP sales will switch from a business-dominated

market in 2001 to a television-dominated market

in 2007

•The majority of PDP production will be in Japan

throughout much of the forecast period; however,

companies in Korea, Taiwan, and elsewhere are

expected to have an impact by 2007

Applications for PDP (1)Applications for PDP (1)

Public InformationPublic InformationⅡⅡ(Trades Show & Shopping (Trades Show & Shopping Mall)Mall)

A Clear image & pleasing DesignA Clear image & pleasing Design

Clear text,ideal suitable for Clear text,ideal suitable for large quantity of Datalarge quantity of Data

Stationary InformationStationary Information(Airport,Station & Bus (Airport,Station & Bus terminal)terminal)

A High class & noble A High class & noble ambianceambiance

Public Public InformationInformationⅠⅠ(Lobby & Hotel (Lobby & Hotel Lounge)Lounge)

Applications for PDP (2)Applications for PDP (2)

Space saving & Wide viewing angle for Biz. Space saving & Wide viewing angle for Biz. presentationpresentation

Conference Conference RoomRoom

A clearer & softer text imageA clearer & softer text image

Financial MarketFinancial Market

Wide screen with high Wide screen with high quality picture quality picture

Home TheaterHome Theater

Worldwide PDP System Shipment Value

Source: Stanford Resources/iSuppli, Plasma Display Panels 2001

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

1999 2000 2001 2002 2003 2004 2005 2006 2007

Mill

ions

Consumer Conference Room Desktop MonitorsFinancial Exchange Industrial/Medical Public InformationRetail/Signage

PDP System Price Comparison by Screen Size

Source: Stanford Resources/iSuppli, Plasma Display Panels 2001

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

1999 2000 2001 2002 2003 2004 2005 2006 2007

Ave

rag

e S

ellin

g P

rice

<=29.x 30.x-34.x 35.x-39.x 40.x-44.x 45.x-54.x >=55.x

Technology Road MapTechnology Road Map

Property 1998 2001 2004

Screen Size

(inch)

PDP TVs

Presentation PDPs

Pixel resolutionPDP TVs

Presentation PDPs

Brightness

(cd /m 2)

PDP TVs

Presentation PDPs

Contrast

(in dark room)

PDP TVs

Presentation PDPs

Power (W )PDP TVs

Presentation PDPs

Lifetime (hour)PDP TVs

Presentation PDPs

Panel thickness

(m m )

PDP TVs

Presentation PDPs

Panel weight

(kg)

PDP TVs

Presentation PDPs

200

600 500

100 60

40 30

50" 60"

852×480 1366×768

1366×768 1920×1 0 8 0

350 400

250 300

500:1 700:1 1,000:1

500:1 700:1

350 300 350

20,000 30,000

50 40

50"42"

Light weight

Large Size

High Brightness

Thin thickness

High Contrast

High Definition

Low Power

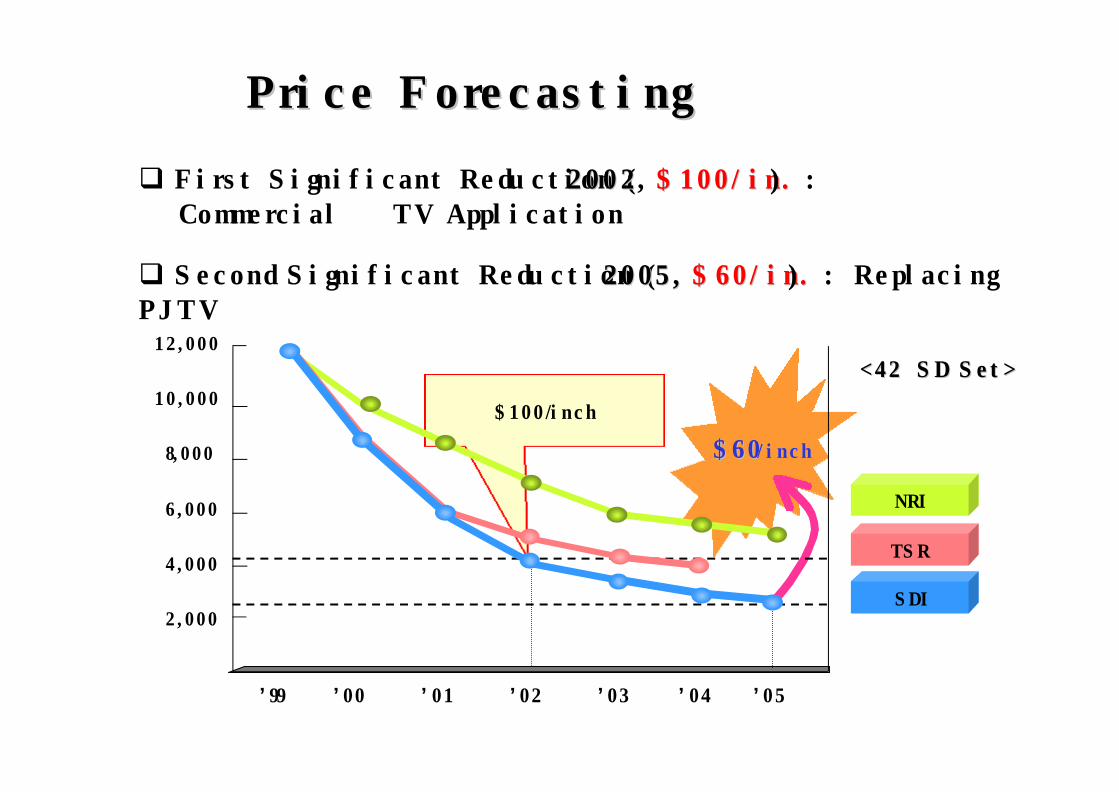

$100/inch

$60$60//inchinch

12,000

10,000

8,000

6,000

4,000

2,000

q First Significant Reduction (20022002, $100/in.$100/in.) :Commercial → TV Application

Price ForecastingPrice Forecasting

q Second Significant Reduction (2005, 2005, $60/in.$60/in.) : Replacing PJTV

<<4242″″SD Set>SD Set>

’99 ’00 ’01 ’02 ’03 ’04 ’05

NRI

TSR

SDI

Summary of Plasma Display Panels

• Plasma display panels making an impact in the business market; entry to lucrative consumer TV market delayed by high end-user prices

• Costs of PDPs will drop surely and steadily

• For HDTV applications, the most important criteria for PDPs are resolution (pixels per inch), size, luminance, power consumption, and cost.

• Manufacturers will need to highlight the flexibility and uniqueness of the PDP to generate acceptance of HDTV

OverviewLiquid Crystal Displays (J.K.Kim, Y.O.Kim)Plasma Display Panels (B.H.Lee)Organic Light-Emitting Diode Displays (K.M.Kim)Microdisplays, FED, … (W.K.Lee)Conclusion

Outline

Duty Number of Driving : Scan Line <120

2 4 6 8 10 Panel Size(Inch)

104

105

106

Mobile Phone

NavigationCar Multi.

Game, PDA

Duty drive:Scan Line number<120

120×160

QVGA

HVGA

QVGA

256×64

Passive Matrix(Small Molecule)

PDA(IMT2K)DSC, DVDCar Audio

Active Matrix(Small Molecule &

Polymer)

SVGA

HVGA

MonitorNote - PC

OLED Market Entry

OLED Advantages

• Excellent “Look” (Emissive Technology)

- Superior viewing angle and contrast ratio

• Low Power(Low operating voltage)

- Generate and modulate light when and where it is needed

• Manufacturing- Many options(evaporation, inkjet, roll-to-roll and so on..)

- Low panel cost(Simple panel construction, no gas, less vacuum)

■ Over 80 company projects

■ Over 50 government and university lab efforts

■ Over 20 OLED fabs under construction or in planning

PMAM PLED

‘97

NEC

5.7” QVGA

LG

8” VGA

Mono (Multi)

Color

Samsung SDI

5.7” QVGA

Pioneer

256*64

‘98 ‘99 ‘00 ‘01

Pioneer

5.2” QVGA

Sanyo

2.1” QVGA

LG

3.8” QVGA

Philips

2”Polymer

Seiko-Epson

2.5” Polymer

TDK

256*64

TDK Mono, QVGA

Idemitsu

5”

Sanyo-Kodak

5.5” QVGA

Samsung

128*64

Ritek

2.5”

Sony

13.1” SVGA

Samsung SDI

8.4” SVGA

Toshiba

1.8” Polymer

Application for OLED■ Car stereo (aftermarket) is ideal first product(Pioneer,TDK)

- Limited operating time

- Adds value to competitive product

- Low volume

■ Cell phone is a key OLED market (Pioneer and others)

- Huge market opportunity

- Reliability issue

- Slow growth predicted until price is aligned with LCD,

- power budget is established and reliability is proven

- Less competition at the outdoor sunlight, compared to

R-LCD

■ OLED pursues all applications !

0

10

20

30

40

50

60

70

80

90

100

AMLCD AMOLED

(%)

Labor & Other

Module Material (Driver IC,Controller, Backlight)

Cell Material (Color filter,Poliarizer)

Array Material

Equipment Depreciation

Building Depreciation

• Driving Curcuit Integrated( No need Drive IC … )▶ Self Luminescence : No need Color Filter, Polarizer, Backlight

Cost Competitiveness

< 2.x” TFTLCD : AMOLED >

Street Price Forecast (2.x”size)

üü AMOLED Should maintain cost merit compared to TFT LCDAMOLED Should maintain cost merit compared to TFT LCD

0

10

20

30

40

50

60

2001 2002 2003 2004 2005

Year

US$

STN LCD

TFT LCD

AMEL

AMEL (SDI Forcast)

Continued ChallengesContinued Challenges

• Lifetime- Differential aging of colors

- Temperature/Moisture sensitivity

• Driving schemes- TFTs/pixel (Pixel uniformity, additional cost, large area)

• Manufacturing- Yield- Manufacturing processes- Improved equipment

3,000h,

>10,000h

Green

>10,000h<2.000hPolymer

>10,000h6,000~10,000hS/M

RedBlue

Technology Road Map

Cellular/PDA PC TV

Ultra Lo-power Hi-Picture Quality

Product

Small~ Mid Mid~ Large LargeSizeDisplay

Glass/Metal Coating →Encap.

Normal Top Emission →Structure

2~3K 10K 20~30KLife(Hr)

1 2 4EfficiencyOLED

3RD Gen.2nd Gen.(Display Circuit Integ)

CurrentP-Si Generation

’01 ‘03 ’05Year

Competing Technologies

• OLED does not (yet) enable new applications

• VFD, LED

– OLED can take market share in segmented displays when price is lower

• PMLCD

– All current OLEDs compete with PMLCD

– Command premium price for better visual quality

– This cannot last; OLED price must drop

• AMLCD

– AMOLED cannot seriously compete until beyond 2007

– LCD manufacturers will phase in AMOLED slowly

– Current investment in LTPS; must get this value first

• Remember: Competition is a moving target!

Patent Issues

• Small molecule

– Kodak original patent-holder

– First patent expires 2003, but Kodak has many later patents

– Formidable patent strength in Japan (more than 8,800 OLED patents filed by Japanese companies since 1997)

• E.g., Sharp, Matsushita, NEC, Fujitsu, Toshiba, SEL

– Inevitable lawsuits

• Polymer

– CDT original patent-holder

– Most polymer companies American or European

– Expect ramp-up from Japan in near future

Thoughts for the Future

• Next key step: Establishment of manufacturing infrastructure

• Creating big expectations too early can backfire– “OLEDs will take over the cell phone market”– “OLEDs will replace LCDs as the desktop

monitor”– OLED e-paper– No need for this “hype”: OLED is easy to sell

because it looks good!

• Low price will create large market early• No fundamental barriers to OLED’s success!

OverviewLiquid Crystal Displays (J.K.Kim, Y.O.Kim)Plasma Display Panels (B.H.Lee)Organic Light-Emitting Diode Displays (K.M.Kim)Microdisplays, FED, … (W.K.Lee)Conclusion

Outline

FED

CRT

Operating Mechanism

u cathodoluminescence same as CRT

(electrons hit phosphors make light)

1µm Cathode electrode

(Cr)

Gate electrode

(Cr)

Insulator (SiO2)

Microtip(Mo)

PackagingSpacerPhosphor

Advantages of FED

• Flat, Thin, and low power CRT

• Provides CRT-like images

– Natural-color images from all viewing angles

– True video speed

– High Brightness

– High Contrast Ratio

• Instant-on over a wide temperature range

Accomplishment

Product

R&D4” Mono

(LETI,’91)

2.4” Color(FED,

Candescnet, ’96)

10.4”VGA(Pixtech, ’96)

4~5”QVGA(Canon, Fujitsu,

Futaba, ’96)

5.3” QVGA(Candescnet, ’00)

13.2” SVGA(Candescnet, ’00)

12.1” VGA(M)(Pixtech, ’99)

5.1”, 5.6”QVGA(Motorola, ’98)

5”Mono(Futaba, ’95)

15”VGA(Pixtech, ’99)

5.2” QVGA(Candescnet, ’01)

13.2” SVGA(Candescnet, ’01)

15” VGACNT-Diode

(Samsung, ’00)

~ ‘95 ‘96 ‘97 ‘98 ‘99 ‘00 ‘01

7” Wide 480x234(C)to Audi for Evaluation

(Pixtech, ’01)

4.5”QVGA(Samsung, ’97)

5.2”QVGA(Samsung, ’98)

4.5”CNT-FED(Samsung, ’99)

10.4” VGA(Samsung, ’00) 7” QVGA

CNT-triode (Samsung, ’01)

- Coexistence of various technologies

- From Microtip type to New Emission type (‘00.05)

- Monitor to TV (‘00.11)

Players

MatsushitaCandescent Motorola Canon Samsung

BSD*Type Mircrotip CNT SED CNT2.6”

MulticolorStatus13.2 SVGA

Color 15” VGA Color30” SED

Color15” VGAMono7” VGA Color

-Manufacturing

Line

2G PP Lineplan 3.5G MP

Line

2G PP LineNo announce

for MP

Announced MPin 2003 R&D Line

42” TV LargeTarget

ApplicationTV

Mid & LargeMonitor & TVMid & Large

42” TVLarge

TVMid & Large

Low Power StructureStrength

Ultra SmallHole

Invisible SpacerJoint with

SONY

Carbon SurfaceEmission

Technology

SED Technology

CarbonEmission

Manufacturing

* BSD:Ballistic Electron Surface Emitting Display

◆◆ CNTCNT--FEDFED

CNT, Graphiteⓔ ⓔⓔ

◆◆ BSD (Ballistic electron SurfaceBSD (Ballistic electron Surface--emitting Display)emitting Display)

Surface Electrode

Lower ElectrodePorous Poly Silicon

Porous Poly Silicon Layer

Oxidation Layer Metal electrode

Poly Si Poly-Si

Solid

Vacuum

Competing Technologies

• Samsung Developed 7” Full Color Test Vehicle

- CNT : good electron emitters

- Screen printing Method

Well established, Low cost & Good scalability

• Matsushita Demonstrate

3” Multicolor @ SID 2000

- Target : 20~40” TV

- Operating Vacuum : 1~10Pa

- Power Consumption : 100W @ 42”

Summary

ü FED has advantages - Thin and low power Consumption- CRT-like images(Natural Color, True Video speed, High Brightness)- Reliability

ü Problems to Solve- not so easy to make Large Screen- doesn’t have exact application

ü New approaches- SED, CNT, BSD type for Large Screen and Cheap Process- Target market changes from Middle size to Large size

ü Who can replace the Conventional CRT?

Microdisplay Market

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

1999 2000 2001 2002 2003 2004 2005 2006

Th

ou

san

ds

of

Do

llars

LCD LCOS MEMS Emis/ScanSource: Stanford Resources/iSuppli, Microdisplays 2002 (preliminary)

Application Categories

• Projection

– Front

• business

• auditorium

• home theater

– Rear

• television

• video cubes

• monitors

•Near-Eye

– Viewfinders

– Handheld

• cell phone

• PDA

– Head-Worn

• headset

• head-mounted

Projection and Near-Eye Percentages

0%

20%

40%

60%

80%

100%

2000units

2000value

2006units

2006value

Projection Near-Eye

75%

72%

74%

71%

Source: Stanford Resources, Inc. Microdisplays 2001

Near Eye Applications

• Camcorders

– Microdisplay viewfinder often in conjunction with backside or flip-out direct-view display.

– Cost, usage, and performance tradeoffs

• Digital cameras

– Potential advantages of microdisplay viewfinder: sunlight readability, high pixel count, large image size, zoom ability

– But, smaller budget for display

• Consumer market

– Short product cycles

– Lower price, higher performance each generation

• LCD and LCOS high volume proven

02-03-29

Microdisplays Summary

•In 2006, near-eye applications will account for 74% of the units, while projection applications will account for 70% of themarket value.

•LCD microdisplays will continue to lead in both shipments and value compared to other technology types

•Manufacturing Issues

– Supply and demand

– Ramp-up to full volume

•Cooperation vs. Competition

– Industry structure