spirig market introduction strategy phase 1-final version

TRANSCRIPT

MARKET INTRODUCTION USA-STRATEGY PHASE 1

©Distributormax • Tom Ka

March 2011

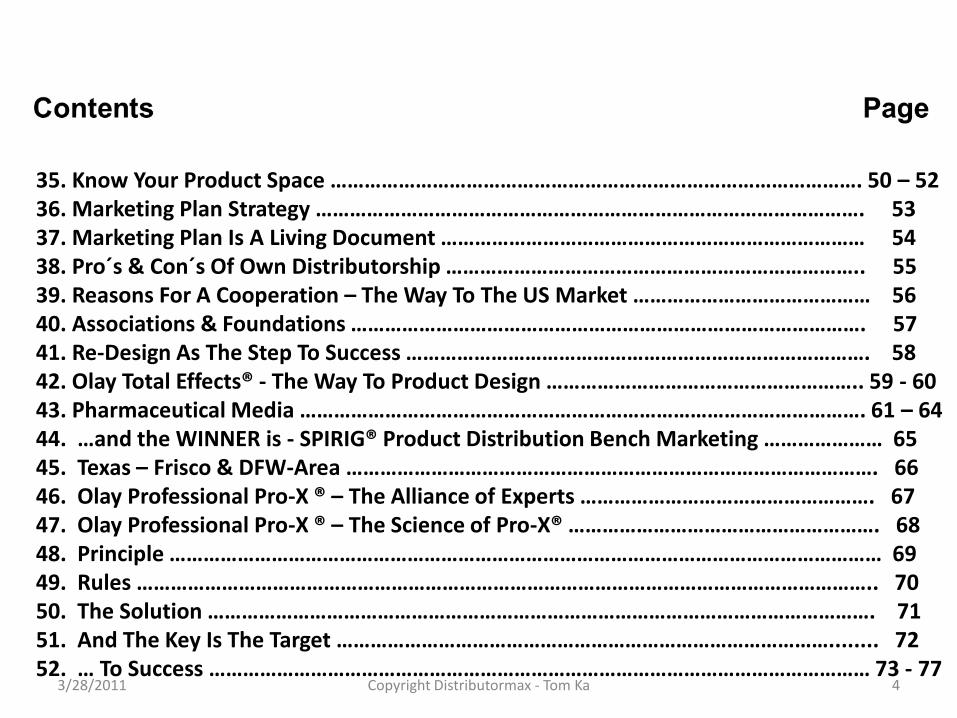

1. Our Targets – Successful Solutions …………………………………………………………………….. 5 2. Direct Distribution ……………………………………………………………………………………………….. 6 3. Employee Portals …………………………………………………………………………………………………. 7 4. Related Products ………………………………………………………………………………………………….. 8 5. Cosmedceuticals – Success Factors Of Proactive Solution® ……………………………….... 9 6. Proactive Solution® Infomercial ………………………………………………………………………….. 10 7. Three Distribution Models ………………………………………………………………………………….. 11 – 12 8. Prescription Drug Channels …………………………………………………………………………………. 13 9. Healthcare Financing ………………………………………………………………………………………..... 14 10. The Buyers: Pharmaceutical Wholesalers …………………………………………………………… 15 11. The Buyers: Retail Pharmacies ……………………………………………………………………………. 16 12. The Buyers: Hospitals …………………………………………………………………………………………. 17 13. The Buyers: Group Purchasing Organisations …………………………………………………….. 18 14. The Buyers: HMO´s ……………………………………………………………………………………………… 19 15. The Buyers: Patients …………………………………………………………………………………............ 20 16. The Buyers: Physicians ………………………………………………………………………………………… 21 17. Direct Distribution: The Role Of GX´s Data Pool ………………………………………………….. 22 18. Network Process Communication - Rollstream® …………………………………………………. 23

3/28/2011 Copyright Distributormax • Tom Ka 2

3/28/2011 Copyright Distributormax - Tom Ka 3

18. Direct-To-Consumer- & Market Leader Web Design ………………………………………….. 24 19. Aveeno® Sun Blockers & Sampling ……………………………………………………………………. 25 – 28 20. Couponing Valassis Com. Inc. & News America Corp. ……………………………………..... 29 – 30 21. Direct-To-Consumer – Using The Web ………………………………………………………………. 31 – 32 22. Direct-To-Consumer – Expenditures …………………………………………………………………. 33 23. Strategies To Get To Know People With Whom You Might Do a Deal ………………. 34 – 35 24. Marketing Plan Strategy ………………………………………………………………………………....... 36 – 37 25. Identifying Potential Partners – People You Already Know ………………………………. 38 26. People You Know That Can Open Doors …………………………………………………………… 39 27. Marketing Plan Strategy …………………………………………………………………………………... 40 28. Publications As Marketing Strategies ………………………………………………………………… 41 – 42 29. Knowledge- & Opinion Buildup ………………………………………………………………………… 43 – 44 30. Marketing Plan Strategy …………………………………………………………………………………… 45 31. The Role Of The Scientist In Finding Leads ………………………………………………………... 46 32. Marketing Plan Strategy …………………………………………………………………………………… 47 – 48 33. Know Your Space ……………………………………………………………………………………………… 49

3/28/2011 Copyright Distributormax - Tom Ka 4

35. Know Your Product Space …………………………………………………………………………………. 50 – 52 36. Marketing Plan Strategy ……………………………………………………………………………………. 53 37. Marketing Plan Is A Living Document ………………………………………………………………… 54 38. Pro´s & Con´s Of Own Distributorship ……………………………………………………………….. 55 39. Reasons For A Cooperation – The Way To The US Market …………………………………… 56 40. Associations & Foundations ………………………………………………………………………………. 57 41. Re-Design As The Step To Success ………………………………………………………………………. 58 42. Olay Total Effects® - The Way To Product Design ……………………………………………….. 59 - 60 43. Pharmaceutical Media ………………………………………………………………………………………. 61 – 64 44. …and the WINNER is - SPIRIG® Product Distribution Bench Marketing ………………… 65 45. Texas – Frisco & DFW-Area …………………………………………………………………………………. 66 46. Olay Professional Pro-X ® – The Alliance of Experts ……………………………………………. 67 47. Olay Professional Pro-X ® – The Science of Pro-X® ………………………………………………. 68 48. Principle ……………………………………………………………………………………………………………… 69 49. Rules ………………………………………………………………………………………………………………….. 70 50. The Solution ………………………………………………………………………………………………………. 71 51. And The Key Is The Target ……………………………………………………………………………........ 72 52. … To Success ……………………………………………………………………………………………………… 73 - 77

OUR TARGETS – SUCCESSFUL SOLUTIONS

3/28/2011 Copyright Distributormax - Tom Ka February 2011 5

High credibility

Guaranteed success

Excellent reputation

Strongest network

Fast market penetration

Multi-ethnic acceptance

Professional appearance

Hi-quality packaging

USP: branding & naming

All-channel referencing

High annual turnover

Efficient ROI

Fast growth

Conclusive concepts

Out-of-the-box-tech

100% authenticity Eagerness to win Multi-channelled

DISTRIBUTORS MEDLINE: www.medline.com

H.D. SMITH: www.hdsmith.com AHP GROUP: www.ahpgroup.com

CARDINAL HEALTH: www.cardinal.com OWENS & MINOR: www.owensminor.com

HENRY SCHEIN: www.henryschein.com HOSPICE PROVIDER GROUP: www.hospiceprovider.com

AMERISOURCE BERGEN: www.amerisourcebergen.com

MC KESSON: www.mckesson.com/en_us/McKesson.cm

DERMATOLOGICAL HOSPITALS www.acnetreatmentjournal.com/Dermatology-Clinic-

Directory/index.htm

ASSOCIATIONS CANADIAN DERMATOLOGY ASSOCIATIONS (CDA•ACD)

SKIN CANCER FOUNDATION www.AAD.org (AMERICAN ACADEMY OF DERMATOLOGISTS•+16.000 members) www.apma.org (AMERICAN PODIATRIC

MEDICAL ASSOCIATION)

Colleagues Journal Articles Private & Public

Insurers Direct to Consumers

Advertising (DTCA)

MEDIA Live Video Detailing

Online events Electronic Sampling

Physician Customer Service Portal www.physiciansinteractive.com

www.mdlinx.com & www.sciencedaily.com www.pharmpro.com

KOL-KEY OPINION LEADERS for

SOCIAL NETWORKS

SPIRIG USA – PHASE 1 DIRECT DISTRIBUTION

DATABASES of PHYSICIAN´s & DERMATOLOGISTS:

www.omnimedicalsearch.com/databases.html www.superpages.com

3/28/2011 Copyright Distributormax - Tom Ka 6

Independent Sales- & Dist. Rep´s segmented in: NE, NW, SMID, SE & SW.

Acquisition with www.careerbuilder.com www.rxinsider.com

www.pharmrep.findpharma.com www.careersinpharmaceutical.com

www.medzilla.com www.pharmaceuticaljobs-usa.com

www.pharmaopportunities.com www.careers.findpharma.com

www.cafepharma.com www.jobsaledirectory.com

www.mypharmaceuticaljob.com www.theladders.com www.pharmrep.com www.monster.com www.hotjobs.com www.webmd.com

3/28/2011 Copyright Distributormax - Tom Ka 7

EMPLOYEES PORTALS

RELATED PRODUCTS

www.amerigel.com www.mustelusa.com www.healthenterprises.com

www.cutivatelotion.com www.magnilife.com

3/28/2011 Copyright Distributormax - Tom Ka 8

COSMEDCEUTICALS – SUCCESS FACTORS OF PROACTIVE SOLUTION®

3/28/2011 Copyright Distributormax - Tom Ka

9

PROACTIVE SOLUTION® INFOMERCIAL

3/28/2011 Copyright Distributormax - Tom Ka 10

THREE DISTRIBUTION MODELS

• 1. Wholesaler Model: This cost-effective distribution alternative for the majority of pharmaceutical products allows wholesalers to provide logistical efficiencies across manufacturers and focus on demand fulfillment and provide a high level of service to end customers.

• 2. Limited Distribution Model: By limiting wholesaler relationships, manufacturers hope to improve inventory management, reduce costs, and mitigate concerns about product and supply chain integrity.

• 3. Direct Distribution Model: Direct distribution by manufacturers has emerged as a viable distribution model, particularly for high-priced biologics with a limited provider base and direct-bulk shipments to customers with their own central distribution warehouse.

3/28/2011

Copyright Distributormax - Tom Ka 11

ASSESS CURRENT STATE

A C T I V I T I E S

D E L I V E R A B L E S

IDENTIFY CHANNEL VALUE

IMPROVE EXISTING AGREEMENTS

• Identify current state • Evaluate existing agreements • Develop wholesale profiles

• Current state channel partner analysis • Economic analysis of existing agreements • Detailed wholesaler profiles

• Define scenarios for future wholesaler business needs • Develop model to quantify value exchange with whole- saler today and in the future • Create forward-looking whole- saler strategy, deployment plan • Create reusable tools/frame- works to revise strategy over time

• Exchange of Value Model • Scenario planning session structure and output • Strategic framework proces- ses and tools • Roadmap for deployment of long-term strategy • Execution Capability Analysis

• Develop a contract strategy for whole- salers • Consider a “limited distribution network” • Understand how current contracts align with ultimate customer needs • Explore potential contracting options to determine how to achieve a win-win rela- tionship with wholesalers • Consider alternatives to existing channel relationships • “Limited distribution” network assess- ment • FFS contracting recommendations • Negotiation strategy • “Next best alternative” analysis

3/28/2011 12

PRESCRIPTION DRUG CHANNELS

“Brand” Manufacturers “Generic” Manufacturers

Repackagers/Marketers

Wholesalers Chain Warehouses Group Purchase

Depots

Hospitals Independent Pharmacies

Chain Drug Stores

Mail Order Pharmacy Services

HMOs

Dispensing Physicians

Nursing Homes

Government

Patient 3/28/2011 13

HEALTHCARE FINANCING

3/28/2011

Copyright Distributormax - Tom Ka 14

Medical Centers (private profit & public non-profit)*

• John Hopkins Hospital www.hopkinsmedicine.org • Mayo Clinic www.mayoclinic.com • Massachusetts General Hospital

www.mgh.harvard.edu • Texas Medical Center

www.universitygeneralhospital.com • Cleveland Clinic

http://my.clevelandclinic.org/default.aspx • New York Presbyterian Hospital http://nyp.org • University of Pennsylvenia Health System

www.pennmedicine.org • University of California - San Francisco Medical Center

www.ucsfhealth.org • University of California – Ronald Reagan Medical

Center www.uclahealth.org/body_med.cfm?id=346

*See also: http://health.usnews.com/health-news/best-hospitals/articles/2010/07/14/best-hospitals-2010-11-the-honor-roll.html

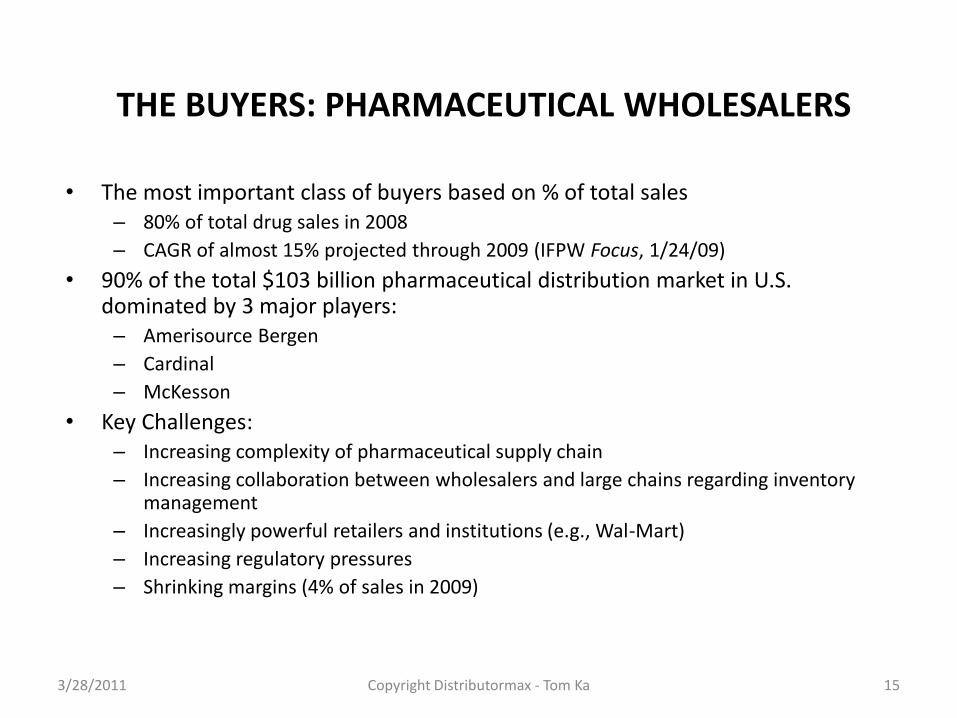

THE BUYERS: PHARMACEUTICAL WHOLESALERS

• The most important class of buyers based on % of total sales – 80% of total drug sales in 2008

– CAGR of almost 15% projected through 2009 (IFPW Focus, 1/24/09)

• 90% of the total $103 billion pharmaceutical distribution market in U.S. dominated by 3 major players: – Amerisource Bergen

– Cardinal

– McKesson

• Key Challenges: – Increasing complexity of pharmaceutical supply chain

– Increasing collaboration between wholesalers and large chains regarding inventory management

– Increasingly powerful retailers and institutions (e.g., Wal-Mart)

– Increasing regulatory pressures

– Shrinking margins (4% of sales in 2009)

3/28/2011 Copyright Distributormax - Tom Ka 15

THE BUYERS: RETAIL PHARMACIES

• More than 50,000 drug stores in the U.S. – Independents (40% of market and sliding)

– Large chains (e.g., Walgreen’s, Rite-Aid, CVS)

• Key Trends: – Continued growth of large chains at the expense of independents

– Growing power of large chains due to use of IT: • Item data capture (more information about the direct consumer than the

manufacturers)

• Direct Profitability Analysis (DFP) – influences shelf-space allocation

• Forward investment buying - JIT delivery of drugs; buying on deal rather than on demand

• Key Challenges: – Growth of the discount “mega-markets” such as Wal-Mart, Costco

– Slowdown in new drug introductions

– Changing consumer preferences for places to buy drugs

3/28/2011 Copyright Distributormax - Tom Ka 16

THE BUYERS: HOSPITALS

• Largest dispensers of drugs (Differentiated by number of beds)

– Teaching hospitals average > 300 beds; so marketing emphasis is directed towards them mostly by

• Key Trends: – Size of the market in $ is growing substantially

– Selection of drugs moving away from physician to others (e.g., hospital pharmacists) – “hospital formulary”

– Growth in power of Pharmacy & Therapeutics (P&T) committees in teaching hospitals

• Key Challenges: – Availability of physicians to marketing & sales staff is limited

– “Free market” forces don’t completely apply in hospital settings

– Focus on cost containment as cost of drugs skyrockets

– Complex purchasing systems; emergence of group purchasing organizations

3/28/2011 Copyright Distributormax - Tom Ka 17

THE BUYERS: GROUP PURCHASING ORGANIZATIONS (GPO´s)

www.premierinc.com

www.novationco.com

www.amerinet-gpo.com

www.vha.com

www.uhc.edu www.provistaco.com

3/28/2011 Copyright Distributormax - Tom Ka 18

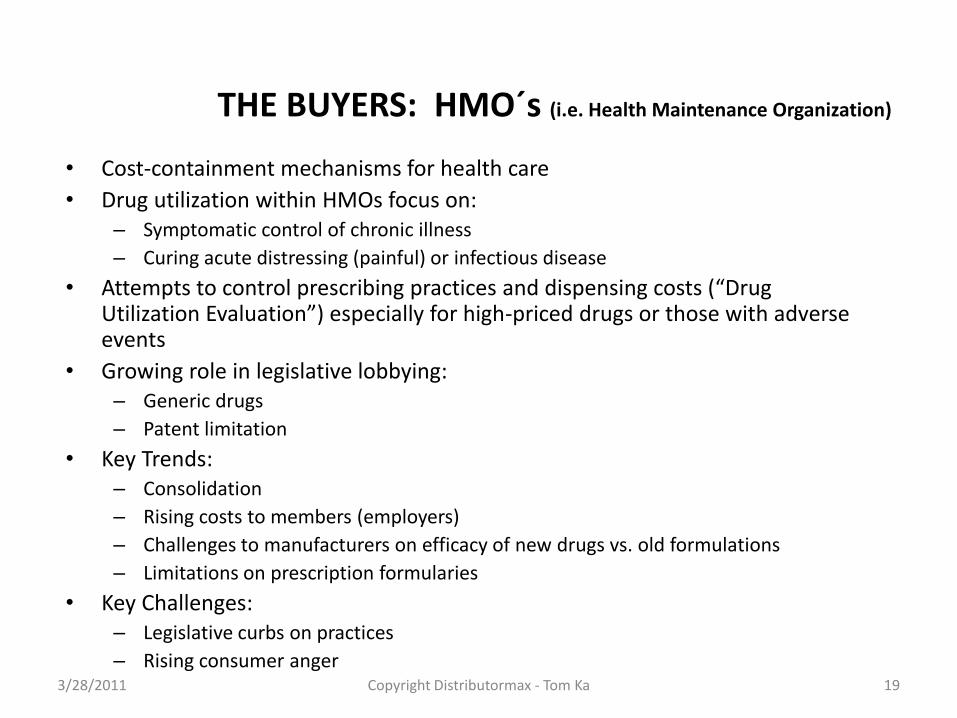

THE BUYERS: HMO´s (i.e. Health Maintenance Organization)

• Cost-containment mechanisms for health care

• Drug utilization within HMOs focus on: – Symptomatic control of chronic illness

– Curing acute distressing (painful) or infectious disease

• Attempts to control prescribing practices and dispensing costs (“Drug Utilization Evaluation”) especially for high-priced drugs or those with adverse events

• Growing role in legislative lobbying: – Generic drugs

– Patent limitation

• Key Trends: – Consolidation

– Rising costs to members (employers)

– Challenges to manufacturers on efficacy of new drugs vs. old formulations

– Limitations on prescription formularies

• Key Challenges: – Legislative curbs on practices

– Rising consumer anger

3/28/2011 Copyright Distributormax - Tom Ka 19

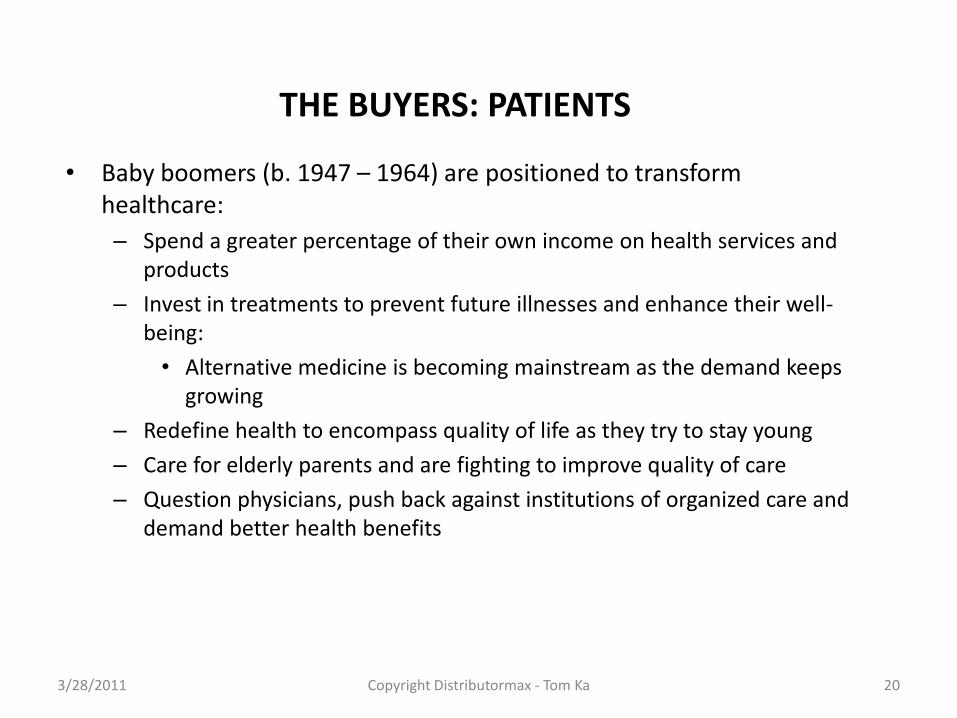

THE BUYERS: PATIENTS

• Baby boomers (b. 1947 – 1964) are positioned to transform healthcare:

– Spend a greater percentage of their own income on health services and products

– Invest in treatments to prevent future illnesses and enhance their well-being:

• Alternative medicine is becoming mainstream as the demand keeps growing

– Redefine health to encompass quality of life as they try to stay young

– Care for elderly parents and are fighting to improve quality of care

– Question physicians, push back against institutions of organized care and demand better health benefits

3/28/2011 Copyright Distributormax - Tom Ka 20

THE BUYERS - PHYSICIANS

• The doctor-patient relationship is changing: – Patients want to see the full range of options with all the relevant evidence so they

can participate in decisions regarding treatment

– Patients are seeking supplemental sources of information in addition to their doctors

– Patients are using the Internet to gather information about their disease conditions and the efficacy and side effects of drugs

– More and more patients want to use doctor-provided web sites or to e-mail their doctors

• But…. – The physician is still seen as the primary marketing target for new drugs, with over

90% of the spending on sales and marketing directed to physicians

3/28/2011 Copyright Distributormax - Tom Ka 21

DIRECT DISTRIBUTION – THE ROLE OF GXS´DATA POOL

certified by GS1's Global Data Synchronization Network

3/28/2011 22

NETWORK PROCESS COMMUNICATION – ROLLSTREAM®

3/28/2011 23

DIRECT-TO-CONSUMER- & MARKET LEADER WEB DESIGN

www.nexium.net www.olay.com/skin-care-products/total-effects?TID=7b5c6d91-da4b-416c-b9fd-054fd7ef5395

www.aveeno.com www.aveeno.com

3/28/2011 Copyright Distributormax - Tom Ka 24

AVEENO® SUN BLOCKERS

3/28/2011 Copyright Distributormax - Tom Ka 25

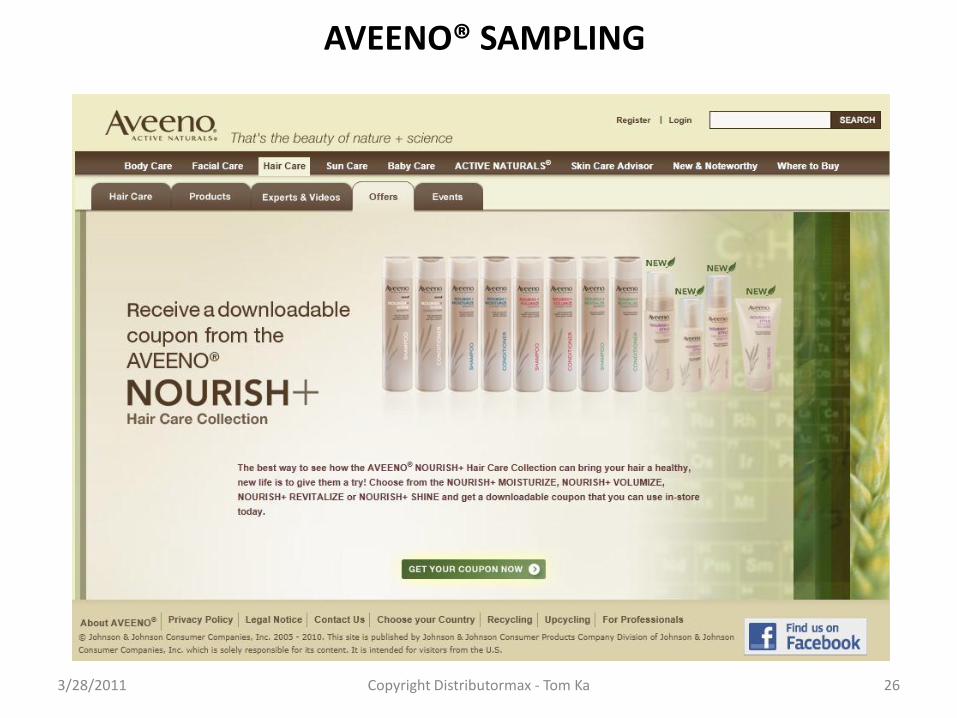

AVEENO® SAMPLING

3/28/2011 Copyright Distributormax - Tom Ka 26

AVEENO® SAMPLING #2

3/28/2011 Copyright Distributormax - Tom Ka 27

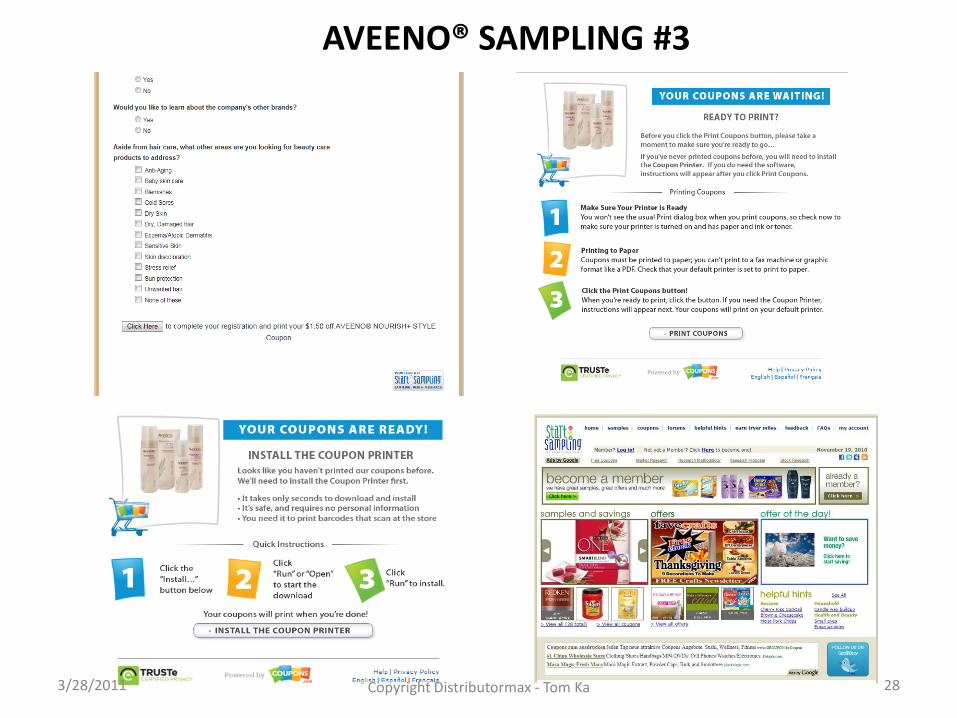

AVEENO® SAMPLING #3

3/28/2011 Copyright Distributormax - Tom Ka 28

COUPONING-VALASSIS COMM. INC. (www.redplum.com)

3/28/2011 Copyright Distributormax - Tom Ka

29

COUPONING-NEWS AMERICA CORP. (www.smartsource.com)

3/28/2011 Copyright Distributormax - Tom Ka 30

DIRECT-TO-CONSUMER-USING THE WEB

• Pharmaceutical executives expect that DTC spending will not slow down, but shift from “promotion” to “drug adherence” over the next 12-18 months

• Keeping people on drugs to treat chronic conditions (e.g., hyperlipidemia) will be the new focus of DTC advertising

• The Web and other related technologies are being explored to improve drug adherence

• Nearly one-third of those who contacted their doctors after seeing a DTC ad first went to the web to find out more

3/28/2011 Copyright Distributormax - Tom Ka 31

• Issues: – Regulatory:

• FDA Center for Drug Evaluation & Research (CDER) – OTC and ethical drug approval

• FDA Division of Drug Marketing, Advertising and Communications (DMAC) – approves labeling, advertising and marketing materials

• Little formal guidance for online marketing or advertising

– Coordination: • Offline and online campaigns rarely coordinated

– Metrics for evaluating the effectiveness of online campaigns not well understood

– Consumers: • Mistrust of online health websites

• Concerns about misuse of personal data

• Reluctance to enroll in wellness programs or disease management programs

• But…they want a doctor-approved resource for information and..

• Better access to their own doctors!

DIRECT-TO-CONSUMER-USING THE WEB

3/28/2011 Copyright Distributormax - Tom Ka 32

Vytorin (Merck/SP)

$155 Million (2005)

Nexium

(AstraZeneca)

$224 Million (2005)

Source: Donohue JM. NEJM. 2007;357:673-81; *WSJ Oct 7, 2005;

**WSJ Apr 16, 2004

Lunesta (Sepracor)

$214 Million (2005)

Coke Classic

$146 Million

(2004)* Bud Light

$136 Million

(2003)**

DIRECT-TO-CONSUMER-EXPENDITURES

3/28/2011 33

• BDMs (Business Development Managers)need to

– Network within their industry

– Attend conferences, exhibitions, functions

• Inadequate to do it once

• Needs to be a constant never ending networking strategy:

– to go to events,

– to see, and to be seen,

– to get to know the people in the industry

• The longer that strategy is implemented, the more successful it will be

• The success of the strategy is limited only by

– Financial resources to travel

– The degree of intimacy established in networking

STRATEGIES TO GET TO KNOW PEOPLE WITH WHOM YOU MIGHT DO A DEAL

3/28/2011 Copyright Distributormax - Tom Ka 34

• Scientists also play a critical role in this networking

– Scientists should regularly go to the conferences in their field

– Conferences are attended by business development staff of biotech and pharmaceutical companies

• Staff of biotech and pharmaceutical companies attend conferences to see what new science is emerging

– Opportunities for scientists to establish rapport and relationships with business development staff from staff of pharmaceutical companies

• Again, must be constant strategy, inadequate to do it once

STRATEGIES TO GET TO KNOW PEOPLE WITH WHOM YOU MIGHT DO A DEAL

3/28/2011 Copyright Distributormax - Tom Ka 35

• This strategy is not devious, nor need it be selfishly pursued

• If its totally selfishly motivated, with a “hard sell” networking is unlikely to work,

• excellent friendships and personal relationships

• BDMs

– actively attend conferences and exhibitions,

– those that are identified as providing opportunities to build networks that are identified as potentially valuable

– Do not expect overnight results

– Results may take a few years to pay off

• Scientists

– Actively attend those conferences where relationships can be nurtured and rapport built

MARKETING PLAN STRATEGY

3/28/2011 Copyright Distributormax - Tom Ka 36

• Make this a strategy in a marketing plan

• Do not make it something that is casually applied, with unpredictable hit or miss results

• Systematic:

– Identify conferences and exhibitions

– Identify who should go to obtain maximum advantage

– Consistency go each year to renew, and reinforce relationships

– Ensure adequate financial resources to implement this expensive commitment

MARKETING PLAN STRATEGY

3/28/2011 Copyright Distributormax - Tom Ka 37

• When something is ready for a deal, ask “Who do we know that may be interested in this”

• More likely to do a deal with someone that you already know, rather than someone that you don’t know yet

• What existing relationships might suggest that someone you already know may be interested

– What companies have existing deals been with ?

– What people met at conferences and exhibitions may be interested

– Former PhD students in industry

– Former colleagues in industry

– Who in your network that you already know may be interested

IDENTIFYING POTENTIAL PARTNERS – PEOPLE YOU

ALREADY KNOW

3/28/2011 Copyright Distributormax - Tom Ka 38

• Asks these questions in a wider framework

• Not just who do you know that may be interested in a deal

• More important:

– Who do you know that can open the door and introduce you to someone that may be interested in doing a deal

– That represents an even wider network of potential parties with whom the opportunity for a deal may arise

• Even more important

– Ask the person you know if they know someone else who can open the door for you

– That represents an even wider network

PEOPLE YOU KNOW THAT CAN OPEN DOORS

3/28/2011 Copyright Distributormax - Tom Ka 39

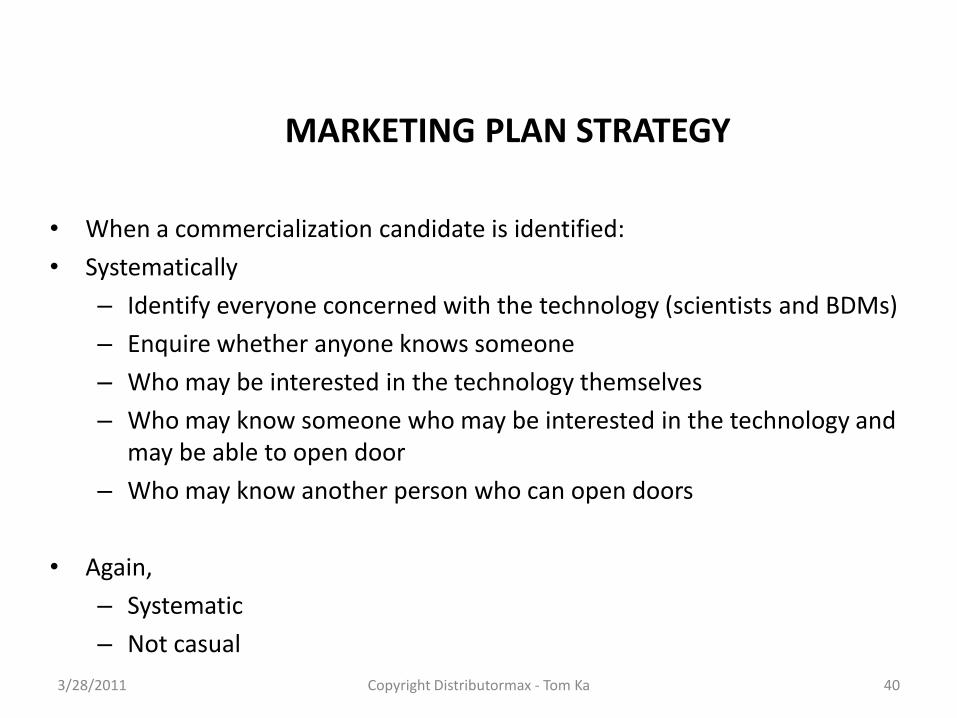

• When a commercialization candidate is identified:

• Systematically

– Identify everyone concerned with the technology (scientists and BDMs)

– Enquire whether anyone knows someone

– Who may be interested in the technology themselves

– Who may know someone who may be interested in the technology and may be able to open door

– Who may know another person who can open doors

• Again,

– Systematic

– Not casual

MARKETING PLAN STRATEGY

3/28/2011 Copyright Distributormax - Tom Ka 40

• Publications and commercialization sometimes perceived as being on a collision course

– Publication means disseminating, and disseminating adversely affects novelty

– Commercialisation perceived as needing secrecy, and that is not consistent with the publication objective.

• But that is too simple a view

• Scientists and BDMs are now much more sophisticated

• BDMs know that publications and peer recognition are an important driver for innovation and inventiveness, and personal satisfaction of scientists

• Scientists know that publication can potentially destroy the transformation of the outcomes of their research into useful and beneficial products for the community

PUBLICATIONS AS A MARKETING STRATEGY

3/28/2011 Copyright Distributormax - Tom Ka 41

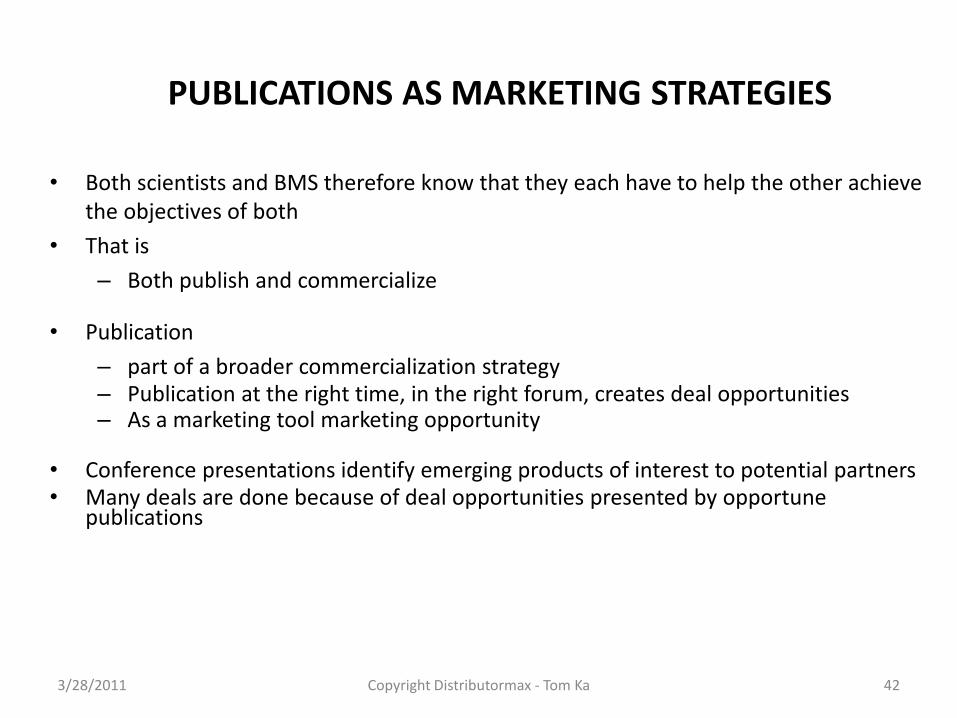

• Both scientists and BMS therefore know that they each have to help the other achieve the objectives of both

• That is

– Both publish and commercialize

• Publication

– part of a broader commercialization strategy – Publication at the right time, in the right forum, creates deal opportunities – As a marketing tool marketing opportunity

• Conference presentations identify emerging products of interest to potential partners • Many deals are done because of deal opportunities presented by opportune

publications

PUBLICATIONS AS MARKETING STRATEGIES

3/28/2011 Copyright Distributormax - Tom Ka 42

KNOWLEDGE- & OPINION BUILDUP

http://factsandcomparisons.com www.pdrbookstore.com/Default.asp?mlc=G3008PH01

http://corporate.everydayhealth.com/index.aspx http://pdrhealth.com/home/home.aspx 3/28/2011 Copyright Distributormax - Tom Ka 43

www.webmd.com www.phrma.org/about_phrma

www.mdlinx.com www.sciencedaily.com

• Specialists newsletters published regularly on industry news informing the industry about new science, new deals, etc.

KNOWLEDGE- & OPINION BUILDUP #2

3/28/2011 Copyright Distributormax - Tom Ka 44

• Give consideration to the optimal

– Manner of publication

– Place of publication

• What is the best audience for the publication

– Is one publication option better than another

• Marketing Plan might consider systematic

– Identification of publications

– Identification of optimal means of dissemination

– Processes to accelerate or delay publication for maximum advantage

– Achieving publications as a marketing tool and opportunity

MARKETING PLAN STRATEGY

3/28/2011 Copyright Distributormax - Tom Ka 45

• Why do scientists produce the greatest number of leads ?

– They have good industry contacts and large personal networks

– Long history of association with industry

– Sponsored research relationships with industry

– Consulting engagements by industry

– Networks amongst their former students

– Companies want to deal with scientists that are leaders in their field, particularly scientists where that leadership is demonstrated through publications

• Need to engage scientists not just once, but continually

– When Developer Disclosure Form signed

– When product search is done

– When product application is filed

THE ROLE OF THE SCIENTIST IN FINDING LEADS

3/28/2011 Copyright Distributormax - Tom Ka 46

• Encourage scientists:

– to form, expand and maintain their networks and contacts

– to maintain a high profile

– to undertaking private consulting

– to attend conferences

– to publish

– to get the business cards of people that they meet

• Enquire of scientists systematically about potential licensees that they can identify

– Not just once

– Repeatedly

MARKETING PLAN STRATEGY

3/28/2011 Copyright Distributormax - Tom Ka 47

• Seek out relationships with industry that can sponsor applied research

– Identify who they are

– Identify their needs

– Implement the strategy by forging networks and relationships with them

• Not likely to be an overnight response

– Expertise, capability, resources, and willingness to undertake applied research takes time to filter out to potential partners

• Perseverance pays off

MARKETING PLAN STRATEGY

3/28/2011 Copyright Distributormax - Tom Ka 48

• Product Watch

• Patent Watch

• Literature Watch

• Newsletter Watch

• Press Release Watch

• All of these are means by which you can keep up with what is happening relevant to your science

– Knowing what is going on in your product space will help identify

– Potential licensees who may be interested in your products

– Potential strategic alliance partners

– Potential infringers

KNOW YOUR SPACE

3/28/2011 Copyright Distributormax - Tom Ka 49

• Newsletter Watch and Press Release Watch

• News services

– Daily email with links to press releases issued in last 24 hours containing your key words Google words)

• All are means to keeping informed about what is going on

• Identify

– Potential licensees

– Potential strategic alliance partners

– Potential infringers

KNOW YOUR PRODUCT SPACE

3/28/2011 Copyright Distributormax - Tom Ka 50

www.thelancet.com www.eblue.org

http://wokinfo.com/media/pdf/09jcrnewtitles.pdf www.wiley.com

KNOW YOUR PRODUCT SPACE #2

3/28/2011 Copyright Distributormax - Tom Ka 51

• Industry Watch

• Be aware of new products and inventions that enter the market place in your space

• Identify

– Potential licensees

– Potential research collaborators

– Potential strategic alliance partners

– Potential infringers

KNOW YOUR PRODUCT SPACE #3

3/28/2011 Copyright Distributormax - Tom Ka 52

• Marketing plan should:

– Identify what to watch

• Industry watch

• Patent Watch

• Literature Watch

• Press Release Watch

• Newsletter Watch

– Who will have responsibility for watching

– Process of assessment and review of intelligence gathered

– Process of planning to maximise taking advantage of intelligence learned

MARKETING PLAN STRATEGY

3/28/2011 Copyright Distributormax - Tom Ka 53

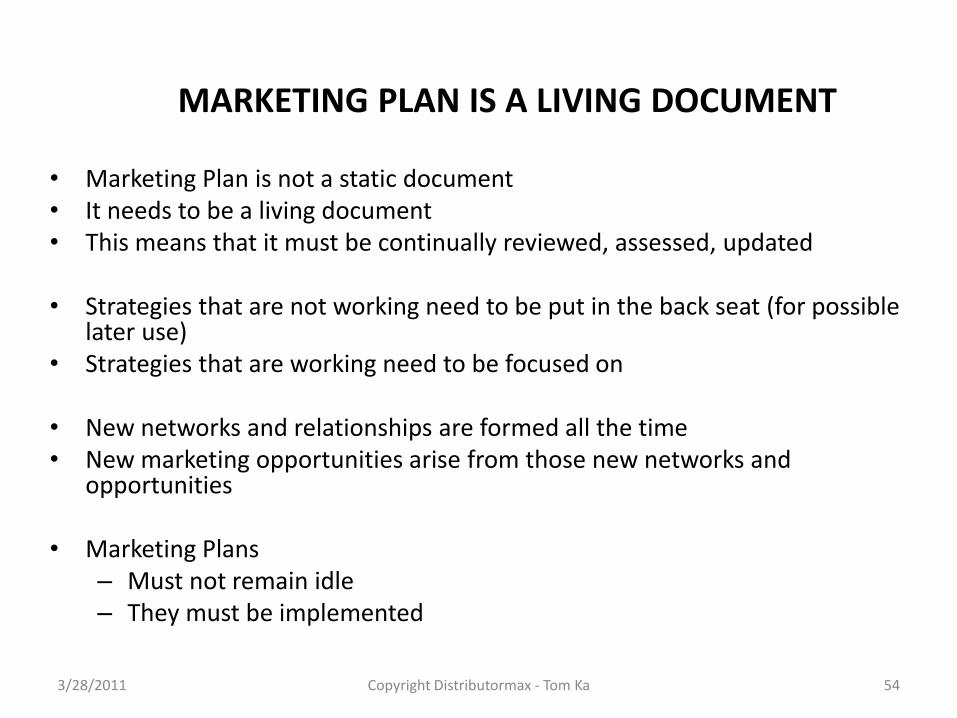

• Marketing Plan is not a static document • It needs to be a living document • This means that it must be continually reviewed, assessed, updated

• Strategies that are not working need to be put in the back seat (for possible

later use) • Strategies that are working need to be focused on

• New networks and relationships are formed all the time • New marketing opportunities arise from those new networks and

opportunities

• Marketing Plans – Must not remain idle – They must be implemented

MARKETING PLAN IS A LIVING DOCUMENT

3/28/2011 Copyright Distributormax - Tom Ka 54

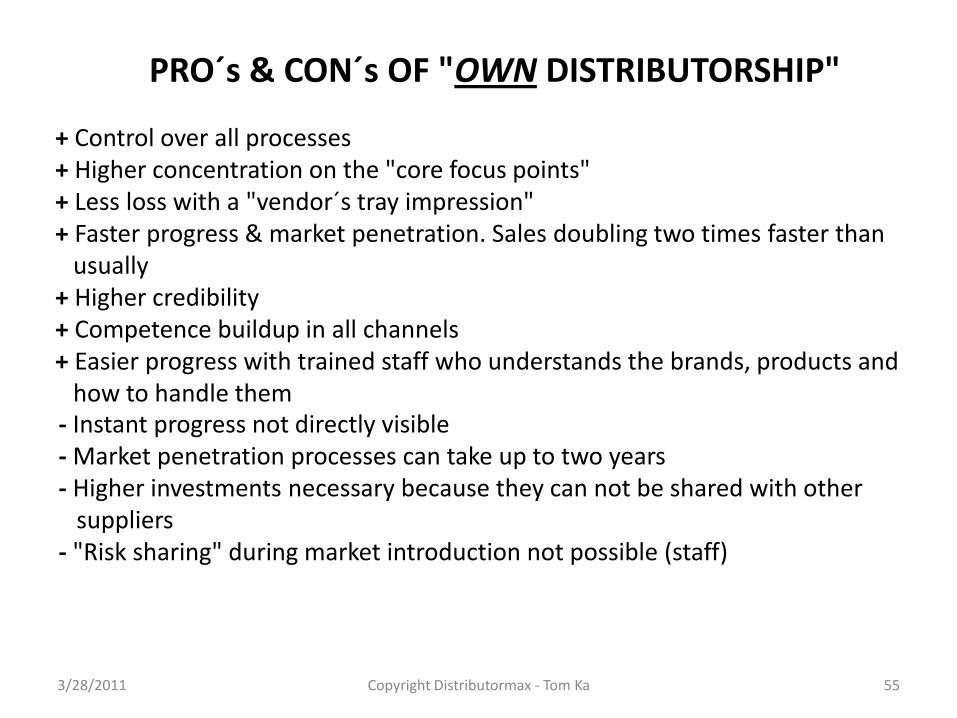

PRO´s & CON´s OF "OWN DISTRIBUTORSHIP"

+ Control over all processes + Higher concentration on the "core focus points" + Less loss with a "vendor´s tray impression" + Faster progress & market penetration. Sales doubling two times faster than usually + Higher credibility + Competence buildup in all channels + Easier progress with trained staff who understands the brands, products and how to handle them - Instant progress not directly visible - Market penetration processes can take up to two years - Higher investments necessary because they can not be shared with other suppliers - "Risk sharing" during market introduction not possible (staff)

3/28/2011 Copyright Distributormax - Tom Ka 55

3/28/2011 Copyright Distributormax - Tom Ka 56

REASONS FOR COOPERATION - THE WAY TO THE US MARKET

Over 13 years of international distribution- and fair experience in the range of cosmeceutical and personal care products in higher price segments. Coordinated marketing for commercial products worldwide including Asia, USA, South America, Australia and Far East. Development, negotiation and purchase with international contacts for market penetration. Specialized in naming, branding and packaging for high-end consumer products.

Cultivated partnerships with industry vendors to increase sales and perform synergetic cooperations. Far more than 5,000 customer data of chains, drugstores and pharmacies that are possible active buyers from SPIRIG AG.

ASSOCIATIONS & FOUNDATIONS

www.apma.org American Podiatric Medical Association

www.aad.org American Academy of Dermatology

www.dermatology.ca Canadian Dermatology Association

www.skincancer.org Skin Cancer Foundation 3/28/2011 Copyright Distributormax - Tom Ka 57

RE-DESIGN AS THE STEP TO SUCCESS

Changes from left to right

Old Improved

Static Dynamic

Common declaration

USP

Increased value

Visually increased value

Negative DOWNflow

Positive UPflow

Negative claim

Core visualisation: Scientific appeal

Positive claim

Visually boosted functionality

3/28/2011 Copyright Distributormax - Tom Ka 58

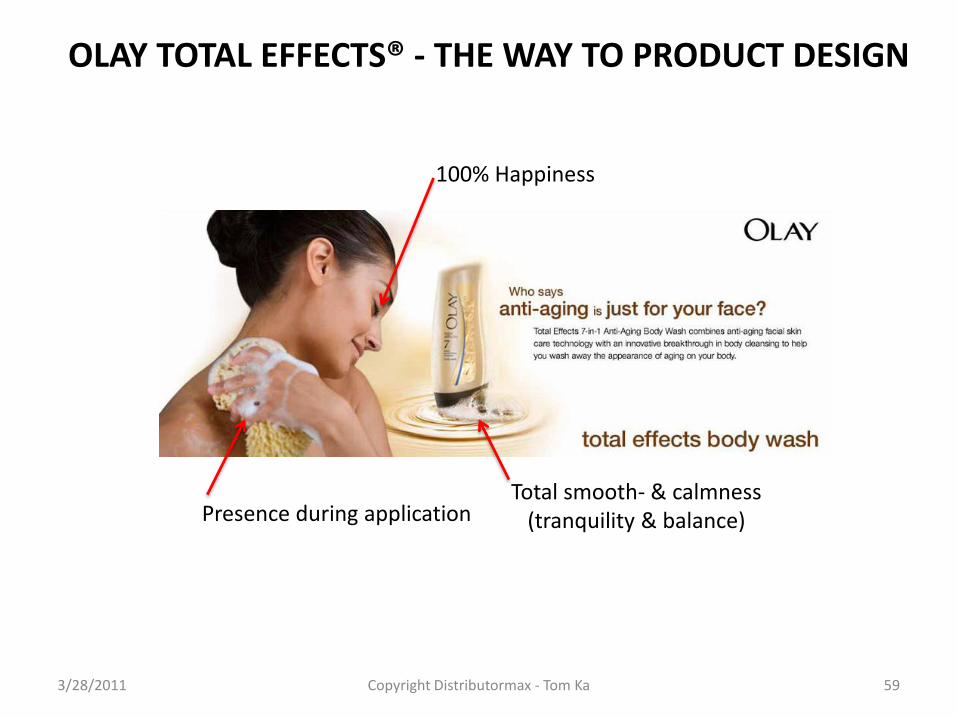

OLAY TOTAL EFFECTS® - THE WAY TO PRODUCT DESIGN

Presence during application Total smooth- & calmness (tranquility & balance)

100% Happiness

3/28/2011 Copyright Distributormax - Tom Ka 59

OLAY TOTAL EFFECTS® - THE WAY TO PRODUCT DESIGN

Benefits

Organic shape Hi-Glam special foil

USP Visualization centered

USP

USP

Higher appeal by structurized bottle surface

3/28/2011 Copyright Distributormax - Tom Ka

60

3/28/2011 Copyright Distributormax - Tom Ka • February 2011 61

PHARMACEUTICAL PRINT MEDIA #1

www.positivehealth.com www.pharmacytimes.com

www.uspharmacist.com www.drugtopics.com

3/28/2011 Copyright Distributormax - Tom Ka • February 2011 62

PHARMACEUTICAL PRINT MEDIA #2

www.pharmacytoday.org www.findpharma.com www.retailclinician.com

3/28/2011 Copyright Distributormax - Tom Ka • February 2011 63

PHARMACEUTICAL PRINT MEDIA #3

www.pharmamanufacturing.com www.pharmaceuticalcommerce.com

www.pharmacyweek.com www.ascp.com

3/28/2011 Copyright Distributormax - Tom Ka • February 2011 64

PHARMACEUTICAL MEDIA #4

www.eyeforpharma.com www.drugstorenews.com

www.thepinksheet.com www.chaindrugreview.com

…and the WINNER is…

SPIRIG® Product Distribution Bench Marketing

• Centrally located in Frisco/TX. • NO state taxes • No turbulent & extreme weather & damage risks • Highest police presence & supervision • Cheap labor • Only few working unions • Close to Mexico • Fast harbor connection • Close to DFW Int. Airport – Centrally located • Excellent infrastructure • Very high public security • Lowest crime rates • 76% White inhabitants (11% Hispanic & 4% Black,

7% other) • Fastest growing city 2000-2009 in USA • One of the highest nationwide per capita incomes • Nationwide most HQ´s in DFW-area • Lowest unemployment rate in the USA • Unique nationwide position • Friendliest people in the nation • Highest infrastructure • Ideally linked to international networks

• All time zones covered by one office: Only 1hour - EST & 2hrs. + PST

• Rated together with McKinney as the #1 USA city with best living conditions (TIME MAGAZINE 2010)

• Many newly built industrial buildings to choose for storage & warehousing

• More than 13 years of personal international marketing experience

• We do business not for profit only • Maximum 4 hrs. flight time within USA • Already existing infrastructure • Prestigeous address • NO suite/PO box numbers • Complete professionalism • German & English native speaking • 24/7 reachability and service • Huge amount of human highly skilled employees • 5 interstates connected in Dallas • Rail- & harbor hubs • DFW #1 in FORTUNE® Top-500 & Top-1000

companies • Environmental & professional stewardship of

branding, naming, distribution & fulfillment

3/28/2011 © • Distributormax • Tom Ka • February 2011

65

3/28/2011 Copyright Distributormax - Tom Ka • February 2011 66

…and the WINNER is… SPIRIG® Product Distribution Bench Marketing

3/28/2011 Copyright Distributormax - Tom Ka • February 2011 67

TEXAS: FRISCO & DFW-AREA

www.dallascounty.org/department/plandev/zoning.html

3/28/2011 Copyright Distributormax - Tom Ka • February 2011 68

OLAY PROFESSIONAL PRO-X® - ALLIANCE OF EXPERTS

3/28/2011 Copyright Distributormax - Tom Ka • February 2011 69

OLAY PROFESSIONAL PRO-X® - SCIENCE OF PRO-X®

PRINCIPLE

3/28/2011 Copyright Distributormax - Tom Ka • February 2011 70

What we think, we become. - Buddha

RULES

3/28/2011 Copyright Distributormax - Tom Ka January

2011 71

SPIRIG PHARMA AG

TOMORROW

Unauthorized start

without highly professional

partner & concept will lead

to direct disqualification &

eternal market loss!

THE SOLUTION

3/28/2011 Copyright Distributormax - Tom Ka January

2011 72

… is the way.

…AND THE KEY IS THE TARGET!

3/28/2011 Copyright Distributormax - Tom Ka January

2011 73

… TO SUCCESS!

3/28/2011 Copyright Distributormax - Tom Ka January

2011 74

PLEASE TURN THE KEY!

3/28/2011 Copyright Distributormax - Tom Ka January

2011 75

IN 2011

3/28/2011 Copyright Distributormax - Tom Ka January

2011 76

…TO HEALTH!

3/28/2011 Copyright Distributormax - Tom Ka January

2011 77

www.istockphoto.com/stock-video-7459537-composite-opening-health.php www.istockphoto.com/stock-video-13236978-unlocking-truth-hd-video.php

u.s.a.