spri. nersa, the national energy regulator south africa

TRANSCRIPT

PRESENTATION TO BASQUE MINISTERIAL ENERGY SEMINAR

24 May 2016 – Presented by Sibusiso Zungu

NERSA MANDATE

WHITE PAPER ON RENEWABLE ENERGY POLICY

RENEWABLE ENERGY POLICY IMPLEMENTATION

RENEWABLE ENERGY FEED- IN TARRIFS (REFITs)

NEW GENERATION CAPACITY REGULATIONS

INTEGRATED RESOURCE PLAN 2010-2030

MINISTERIAL DETERMINATION

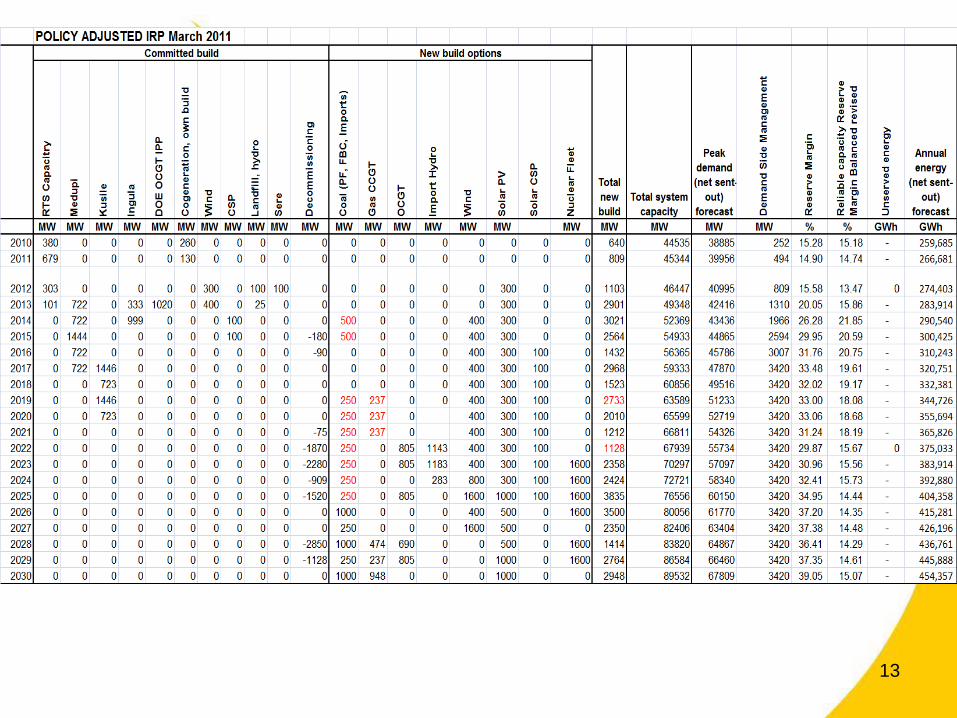

POLICY ADJUSTED IRP 2010-2030

NET NEW CAPACITY (2030)

DoE RENEWABLE ENERGY IPP PROCUREMENT

CURRENT CAPACITY ALLOCATIONS

TARIFF COMPARISONS

OPERATIONAL INSTALLED CAPACITY UNDER RE IPPP

CONCLUDING REMARKS

PRESENTATION OUTLINE

2

NERSA MANDATE (1)

NERSA’s mandate is anchored in:

4 Primary Acts:

National Energy Regulator Act, 2004 (Act No. 40 of 2004)

Electricity Regulation Act, 2006 (Act No. 4 of 2006)

Gas Act, 2001 (Act No. 48 of 2001)

Petroleum Pipelines Act, 2003 (Act No. 60 of 2003)

3 Levies Acts:

Gas Regulator Levies Act, 2002 (Act No. 75 of 2002)

Petroleum Pipelines Levies Act, 2004 (Act No. 28 of 2004)

Section 5B of the Electricity Act, 1987 (Act No. 41 of 1987)

3

4

Electricity Regulation Act No.4 of 2006:

Objectives of this Act include the following:

i. To Achieve the efficient, effective, sustainable and orderly development

and operation of electricity supply infrastructure in South Africa,

ii. To Promote the use of diverse energy sources and energy efficiency,

iii. To Promote competitiveness, customer and end-user choice

iv. To facilitate a fair balance between the interests of customers and end

users, licensees, investors in the electricity supply industry and the public

NERSA MANDATE (2)

5

White Paper on Renewable Energy Policy of the Republic of South Africa

of November 2003:

A target of 10,000 GWh renewable energy contribution to final energy

consumption by 2013, to be produced mainly from biomass, wind, solar

and small-scale hydro.

This policy document is being reviewed to assess progress after the

first 5yrs of policy implementation and also propose medium to long

terms RE targets.

6

NERSA RESPONSE:

Prepared Renewable Energy Feed-In-Tariffs (REFITs)

Held Public hearings and stakeholder workshops on REFITs

Prepared the PPA for Renewable Energy Purchases under REFITs

Assisted in the preparation of the DoE RE IPP commercial agreements

Made allowance in the Eskom’s Multi Year Price Determination (MYPD) in terms

of revenue for IPP purchases

Approved the Grid Code for Wind Generation

Approved the Transmission and Distribution Use of System framework

Granted licences to the DoE RE IPP programme successful Bidders

NERSA introduced a REFIT framework in two phases.

A REFIT is a pre-approved tariff for a specific Renewable Energy

generation technology e.g. wind

By nature REFITs include a premium above tariffs for conventional

generation to attract investors and developers

REFIT was only for those selling to the “Buyer” so that the price is diluted

to end user

REFITs did not apply to bilateral agreements.

7

8

Phase I tariffs approved in March 2009:

Technology Tariff (R/kWh)

CSP trough (6hrs storage) 2.10

Wind 1.25

Small Hydro 0.94

Landfill gas 0.90

9

Technology Tariff (R/kWh

CSP trough (no storage) 3.14

CSP tower (6 hrs storage) 2.31

Biomass Solid 1.18

Biogas 0.96

Landfill gas 0.90

Large scale grid-connected PV (≥ 1MW) 3.94

Phase II tariffs approved in October 2009:

New Generation Capacity Regulations were gazetted on 5 August 2009

for procurement of generation capacity and the role of the Government

institutions

Regulations were later reviewed and gazetted on 4 May 2011.

In revised regulations, DoE is responsible for planning and procurement

of new generation capacity. Public Finance Management Act requires

procurement to be done through a competitive bidding process.

Competitive Bidding chosen over REFITs, however, NERSA’s

experience with REFIT was carried across into the process i.e. PPA

term, Eskom as Buyer, RE technologies.

DoE/National Treasury assisted by NERSA were responsible for

developing technology specific PPAs and Procurement Documents.

10

11

In terms of 2011 New Generation Capacity Regulations , The Minister may,

in consultation with the Regulator determine that new generation capacity is

needed to ensure the continued uninterrupted supply of electricity and

determine the types of energy sources from which electricity must be

generated, and the percentages of electricity that must be generated from

such sources.

The Integrated Resource Plan (IRP) 2010-30 was promulgated

in March 2011

IRP is “living plan” which should be revised by the Department

of Energy (DoE) every two years but is only in the process of

being updated this year

DOE initiated first iteration of IRP in January 2010

IRP included scenarios, policy options and technology choices

Publication participation conducted in June 2010

Public consultation and subsequent independent international

consultant input resulted in changes to the IRP modelling as

well as new scenarios to test additional policy options process

led to refinements, and to the approved Policy-Adjusted IRP

12

13

14

MINISTERIAL DETERMINATION

15

16

The procurement document released on 3rd August 2011 provided for

procurement of 3 725MW in five different bidding phases

100MW of the 3 725MW were reserved for small-scale Renewable

Energy programme i.e. capacity range of 1– 5 MW.

A hybrid procurement method (i.e. price competition within a prescribed

ceiling price) was adopted by the DoE.

Phase 1: On 7 December 2011, 28 preferred bidders were selected

from a total of 53 bids. Energy Regulator approved 28 generation

licenses on 26 April 2012

Phase 2: On 21 May 2012, 19 preferred bidders were selected from a

total of 79 bids. Energy Regulator approved 19 generation licenses

in September 2012.

Phase 3: On 04 November 2013, 17 preferred bidders selected from

total of 93 bids. Energy Regulator approved 17 generation licences in

March 2014. 17

18

To ensure integrity of the adjudication process international reviewers

were used and strict process rules applied

Government decided to get maximum leverage out of the process

and imposed social and developmental requirements on the bidders

These requirements included:

Local Content

Broad Based Black Economic Empowerment (BBBEE)

Price

70 %

30 %

Economic Development

Job creation

Socio Economic

Local content

Project cost

Rand/MW

19

Technology

Ministerial

Determination

MW

First Bid

Allocation

MW

Second Bid

Allocation

MW

Third Bid Allocation

MW

Onshore wind 1 850 634 562.5 435

Solar photovoltaic 1 450 631.5 417.1 787

Concentrated solar

power200 150 50 200

Small hydro (≤ 10MW) 75 0 14.3 0

Landfill gas 25 0 0 18

Biomass 12.5 0 0 16

Biogas 12.5 0 0 12

Total 3 625 1 415.5 1 043.9 1 456

Source: Department of Energy

20

Source: Department of Energy

21

Source: Department of Energy 22

2,37

1,56

1,26

0,77

BW1 BW2 BW3 BW4

Portfolio Price Trend R/kWh

Prices stated in April 2015

terms. Energy weighted

average (R/kWh) considering

average technology RFP

submission price (published)

per BW and projected,

annual energy contribution

per technology type.

Operational Installed Capacity under RE IPP Programme

as at 31 December 2015

7 191

639

1045

1522

1709

1860

2021 2021

Q3 FY13/14 Q4 FY13/14 Q1 FY14/15 Q2 FY14/15 Q3 FY14/15 Q4 FY14/15 Q1 FY15/16 Q2 FY15/16 Q3 FY15/16

RENEWABLE GENERATION:MW OPERATIONAL

23

REIPPs have

consistently

contributed new

capacity to the

network since the end

of 2013. At December

2015, 83% of IPPs

scheduled to be

operational have

started commercial

operations. The

average lead time for

these 40 projects to

complete has been 1.7

years.

Over 2021 MW of Renewable Energy is connected to the grid as of December

2015

Renewable Energy development requires sound policy and regulatory

framework

Government institutions and industry stakeholders need to cooperate in order to

implement renewable energy policy successfully

The competitive bidding process resulted in efficient prices

Limiting new capacity has led to a manageable process

It is expected that renewable energy will improve the socio-economic

development of South Africa while contributing to of emission reduction.

24

Thank You

Tel: 012 401 4600

Fax: 012 401 4700

Website: www.nersa.org.za

Physical Address:

Kulawula House

526 Madiba Street

Arcadia,0083

Pretoria

25