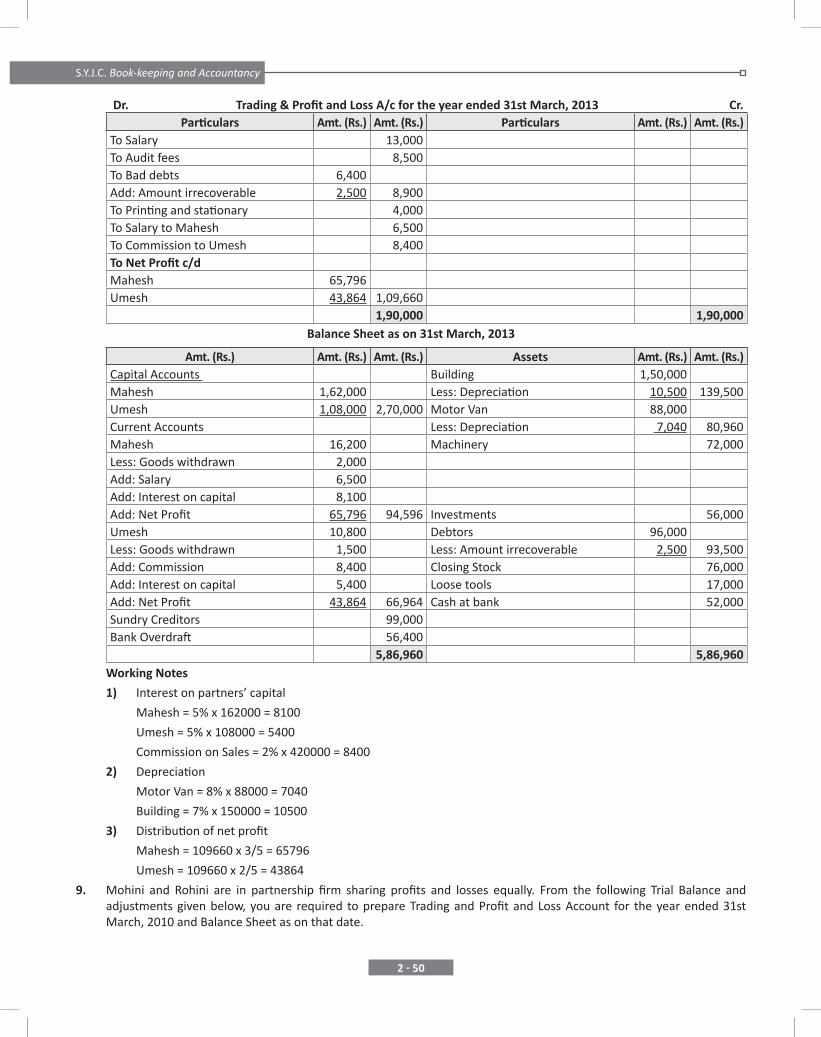

sr. no. particulars page no. chapters/syjc/bk chapter 2.pdf · s.y.j.c. book-keeping and...

TRANSCRIPT

2 - 11

CHAPTER 2: PARTNERSHIP FINAL ACCOUNTS

Sr. No. Particulars Page No.

1. Theory 2 - 12

2. Section I :

From the Textbook - Solved Problems 2 - 27

3. Section II :

From the Textbook - Practical Problems 2 - 35

4. Section III :

Solved Additional Problems 2 - 54

5. Section IV :

Homework Problems 2 - 65

6. Section V :

Revision Problems 2 - 70

7. Section VI :

Objective type questions 2 - 75

2 - 12

S.Y.J.C. Book-keeping and Accountancy

Partnership Final Accounts

Partnership final accounts are prepared in a similar way as sole proprietorship accounts. They include Trading A/c, Profit & Loss A/c and the Balance Sheet.

Final accounts are prepared for the following purpose:-

i. To find out the gross profit or loss for the period

ii. To find out the net profit or loss for the period

iii. To know the financial position of the business as on a particular date

iv. To prepare various statements to plan for the future

v. To know how much are the debtors and creditors of the firm

vi. To know the sources of funds (liabilities) and the application of funds (assets)

vii. To calculate various ratios for analysis

viii. To provide audited financial statements and other documents to the bank for obtaining loans

ix. To value goodwill of the firm in cases of admission, retirement or death of a partner and on dissolution of the firm

x. To find the tax payable and make advance tax payments.

Preparation of Final Accounts

Final accounts of a partnership firm are similar to that of a sole trader. Only difference is that the profit is distributed among the partners whereas in a sole proprietorship it is added to the proprietor’s capital. First a trial balance is to be prepared from all the debit and credit balances of all the ledger accounts. From this, trading and profit & loss accounts are generated. Finally, a balance sheet is prepared to reflect the position as at period end. A trading account shows the gross profit or loss whereas a profit & loss account reflects the net position.

I. Manufacturing Account

It is prepared only for manufacturing concerns. It shows the cost of production.

II. Trading Account

Trading account is prepared in a trading concern and is a part of the profit & loss account. It records all transactions related to goods and direct expenses. If the credit side is greater than the debit side, the gross profit thus arrived at is transferred to the credit side of profit & loss account. On the other hand, if the debit side is greater than the gross loss is transferred to the debit side of the profit & loss account.

a. Debit side of Trading Account

• Opening stock

• Purchases after deducting amounts for goods destroyed by fire, goods withdrawn by partners, goods distributed as free samples, etc.

• Direct expenses meaning those expenses directly related to production or purchases of goods such as wages, freight inwards, factory rent, octroi, import duty, customs duty, manufacturing expenses such as electricity of factory, etc.

b. Credit side of Trading Account

• Sales of goods

• Closing stock

• Goods destroyed by fire, goods withdrawn by partners, goods distributed as free samples, etc. may alternately be shown here instead of as a deduction from purchases.

2 - 13

Partnership Final Account

Journal entries for Trading Account

1. Transferring items on the debit side such as opening stock, purchases, etc.

Since all these accounts show a debit balance in the trial balance and are all direct expenses, we need to debit the Trading A/c.

Trading A/c Dr. xxx

To Opening Stock A/c xxx

To Purchases A/c xxx

To Direct expenses A/c xxx

To Sales returns A/c xxx

(Being transfer of opening stock, purchases, direct expenses and sales returns to trading A/c)

2. Transferring items on the credit side such as sales, purchase returns and closing stock.

Since all the above items are credit balances in the trial balance, we need to transfer them to the credit side of the Trading A/c. Hence, we credit the Trading A/c and debit all these accounts thereby closing these accounts and transferring the balances to the Trading A/c.

Sales A/c Dr. xxx

Purchase Returns A/c Dr. xxx

Closing Stock A/c Dr. xxx

To Trading A/c xxx

(Being transfer of sales, purchase returns and closing stock to the Trading A/c)

3. Transfer of Gross Profit

Trading A/c Dr. xxx

To Profit & Loss A/c xxx

(Being transfer of gross profit to the profit & loss A/c)

4. Transfer of Gross Loss

Profit & Loss A/c Dr. xxx

To Trading A/c xxx

(Being transfer of gross loss to the profit & loss A/c)

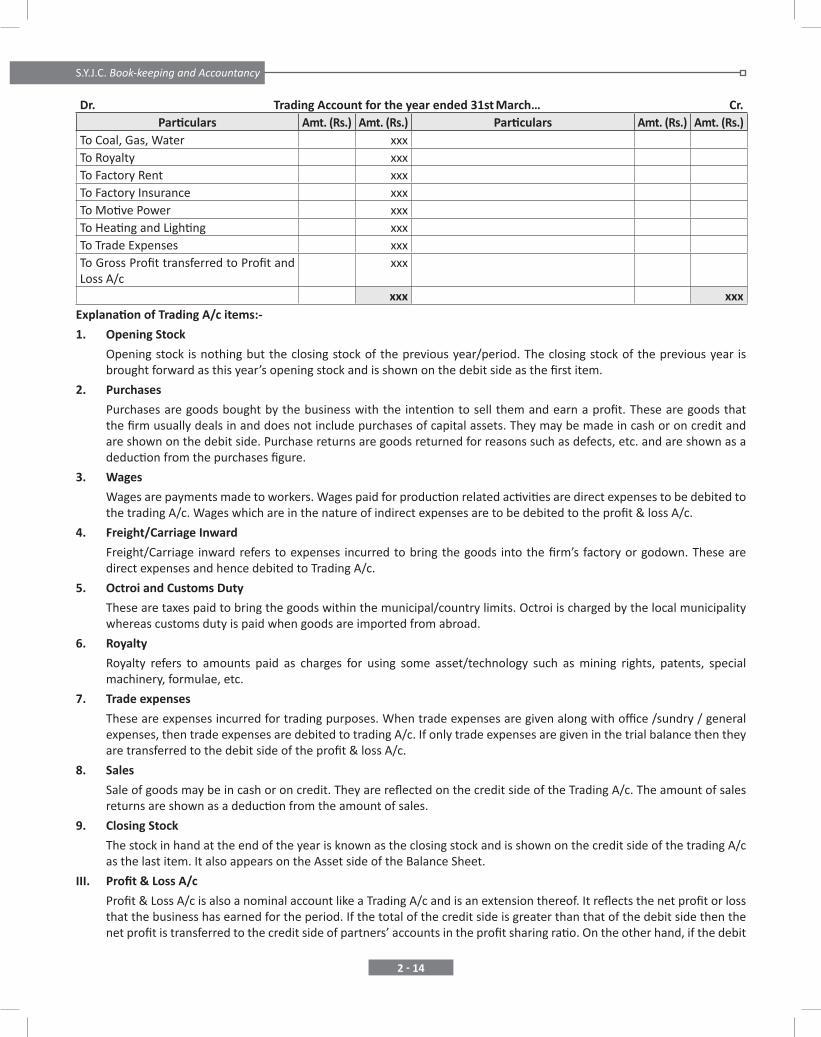

Format of Trading Account is shown as below:

Name of the firm

Dr. Trading Account for the year ended 31st March… Cr.Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)

To Opening Stock xxx By Sales xxxTo Purchase xxx Less: Sales Return (Return Inward) xxx xxxLess: Purchase Return (Return Outward) xxx xxx By Goods Destroyed by fire/theft xxxTo Wages xxx By Goods withdrawn for personal use

(i.e. Drawing)xxx

To Wages and salaries xxx By Goods distributed as free sample xxxTo Freight xxx By Closing Stock xxxTo Carriage inward xxx By Gross Loss transferred to Profit and

Loss A/cxxx

To Octroi xxxTo Import Duty xxxTo Customs Duty xxxTo Works Manager Salary xxxTo Power, Fuel and Oil xxx

2 - 14

S.Y.J.C. Book-keeping and Accountancy

Dr. Trading Account for the year ended 31st March… Cr.Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)

To Coal, Gas, Water xxxTo Royalty xxxTo Factory Rent xxxTo Factory Insurance xxxTo Motive Power xxxTo Heating and Lighting xxxTo Trade Expenses xxxTo Gross Profit transferred to Profit and Loss A/c

xxx

xxx xxxExplanation of Trading A/c items:-

1. Opening Stock

Opening stock is nothing but the closing stock of the previous year/period. The closing stock of the previous year is brought forward as this year’s opening stock and is shown on the debit side as the first item.

2. Purchases

Purchases are goods bought by the business with the intention to sell them and earn a profit. These are goods that the firm usually deals in and does not include purchases of capital assets. They may be made in cash or on credit and are shown on the debit side. Purchase returns are goods returned for reasons such as defects, etc. and are shown as a deduction from the purchases figure.

3. Wages

Wages are payments made to workers. Wages paid for production related activities are direct expenses to be debited to the trading A/c. Wages which are in the nature of indirect expenses are to be debited to the profit & loss A/c.

4. Freight/Carriage Inward

Freight/Carriage inward refers to expenses incurred to bring the goods into the firm’s factory or godown. These are direct expenses and hence debited to Trading A/c.

5. Octroi and Customs Duty

These are taxes paid to bring the goods within the municipal/country limits. Octroi is charged by the local municipality whereas customs duty is paid when goods are imported from abroad.

6. Royalty

Royalty refers to amounts paid as charges for using some asset/technology such as mining rights, patents, special machinery, formulae, etc.

7. Trade expenses

These are expenses incurred for trading purposes. When trade expenses are given along with office /sundry / general expenses, then trade expenses are debited to trading A/c. If only trade expenses are given in the trial balance then they are transferred to the debit side of the profit & loss A/c.

8. Sales

Sale of goods may be in cash or on credit. They are reflected on the credit side of the Trading A/c. The amount of sales returns are shown as a deduction from the amount of sales.

9. Closing Stock

The stock in hand at the end of the year is known as the closing stock and is shown on the credit side of the trading A/c as the last item. It also appears on the Asset side of the Balance Sheet.

III. Profit & Loss A/c

Profit & Loss A/c is also a nominal account like a Trading A/c and is an extension thereof. It reflects the net profit or loss that the business has earned for the period. If the total of the credit side is greater than that of the debit side then the net profit is transferred to the credit side of partners’ accounts in the profit sharing ratio. On the other hand, if the debit

2 - 15

Partnership Final Account

side total is greater than the credit side total, then the net loss is transferred to the debit side of partners’ accounts in the profit sharing ratio. When fixed capital method is followed, the net profit/loss is transferred to the current accounts of partners and when fluctuating capital method is followed then the net profit/loss is transferred to the capital accounts of the partners.

a. Debit side of Profit & Loss A/c

• Brought forward gross loss from Trading A/c

• All indirect expenses of the current period, which are due whether paid or payable

b. Credit side of Profit & Loss A/c

• Brought forward gross profit from Trading A/c

• All indirect incomes of the current period whether received or receivable

Journal entries for Profit & Loss Account

1. Transfer of indirect expenses to profit & loss A/c

Since all these accounts show a debit balance in the trial balance we need to debit the Profit & Loss A/c while closing these accounts and transferring the individual balances of every indirect expense account.

Profit & Loss A/c Dr. xxx

To Indirect expenses A/c xxx

(Being transfer of all indirect expenses to profit & loss A/c)

2. Transfer of revenue/income to profit & loss A/c

Since revenue/income accounts have a credit balance, we need to transfer these onto the credit side of the profit & loss A/c as we close invidually close them.

Income A/c Dr. xxx

To Profit & Loss A/c xxx

(Being transfer of all incomes and revenue to profit & loss A/c)

3. Transfer of Net Profit

Profit & Loss A/c Dr. xxx

To Partners Capital/Current A/c xxx

(Being transfer of net profit to the partner’s capital/current accounts)

4. Transfer of Net Loss

Partners Capital/Current A/c Dr. xxx

To Profit & Loss A/c xxx

(Being transfer of net loss to the partner’s capital/current accounts)

Format of Profit & Loss Ac/ from the book.

Name of the firm

Dr. Profit and Loss Account for the year ended 31st March….. Cr.Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)

To Gross loss b/d (Transferred from Trading A/c)

xxx By Gross Profit b/d (Transferred from Trading A/c)

xxx

To Salaries xxx By Interest received xxxTo Salaries and Wages xxx By Discount Received xxxTo Unproductive Wages xxx By Commission received xxxTo Office expenses xxx By Dividend received xxxTo Sundry expenses xxx By Rent received xxxTo Printing Stationary xxx By other Receipt xxxTo Postage and Telegram xxx By Profit on sale of Asset xxxTo Telephone charges xxx By Interest on Investments xxx

2 - 16

S.Y.J.C. Book-keeping and Accountancy

Dr. Profit and Loss Account for the year ended 31st March….. Cr.Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)

To Legal charges xxx By Old R.D.D xxxTo Electricity charges xxx Less: New Bad debts xxxTo Audit Fees xxx Less: Old Bad Debts xxxTo Bank charges xxx Less: New R.D.D. xxx xxxTo Interest paid xxx By Interest on Drawings xxxTo Warehouse rent xxx By Net Loss transferred to partner’s

capital/current accountsXY

xxxxxx xxx

To Rent, Rates and Taxes to Insurance xxxTo Trade expenses xxxTo Travelling expenses xxxTo Discount allowed xxxTo Advertisement xxxTo Export duty xxxTo Carriage outward xxxTo Packing charges xxxTo Conveyance xxxTo Bad debts xxxAdd: New Bad Debts xxxAdd: New R.D.D. xxx

xxxLess: Old R.D.D. xxx xxxTo Provident Fund contribution xxxTo Repairs and renewals xxxTo Interest on Capital xxxTo Salary to partners xxxTo Commission to partners xxxTo Interest on partners loan xxxTo Net Profit transferred to Partner’s Capital/current accountsXY

xxxxxx xxx

xxx xxxExplanation of Profit & Loss A/c items:-

1. Salaries and wages

Salaries and wages are amounts paid to staff. Salaries are paid to office staff whereas wages are paid to factory staff. If Salaries & Wages appears in the trial balance, treat it as an indirect expense and debit it to Profit & Loss A/c. If Wages & Salaries appears in the trial balance, treat it as a direct expense and debit it to the Trading A/c.

2. Insurance

Insurance premium paid or payable is an indirect expense and is incurred to provide for anticipated losses of goods, assets, factory, etc. It is debited to Profit & Loss A/c.

3. Bad debts

Bad debts are amounts owed by debtors but which can now not be recovered. Since, they are an expense, they are debited to the Profit & Loss A/c.

2 - 17

Partnership Final Account

4. Reserve for Doubtful Debts

Provision made for doubtful debts is called reserve for doubtful debts. If it is shown in the trial balance, then it is shown on the credit side of Profit & Loss A/c. If it appears in the adjustments, then it is debited to Profit & Loss A/c and also shown as a deduction from Debtors in the balance sheet.

5. Discount allowed

Since it is an expense, it is debited to the Profit & Loss A/c.

6. Discount received

Since it is an income, it is credited to the Profit & Loss A/c.

7. Commission paid

Commission is paid to salesmen to increase sales and develop the business. Since it is an expense, it is debited to the Profit & Loss A/c.

8. Commission received

Sometimes, the firm may receive commission for the sales it makes on behalf of its principal. In such cases, the income is credited to the Profit & Loss A/c.

9. Dividend received

A firm may receive dividends on the investments it has made and the income is credited to the Profit & Loss A/c.

10. Depreciation

Depreciation is the provisions made for the wear and tear of assets and the passage of time. It is debited to the Profit & Loss A/c.

11. Rent paid

The firm may pay rent for the space it occupies such as a rented factory, or rented office building. It is debited to the Profit & Loss A/c.

12. Rent received

Sometimes, the firm may let out its premises to others for consideration. The same being income, is credited to the Profit & Loss A/c.

IV. Balance Sheet

Unlike the three earlier accounts, a balance sheet is not an account. It is a statement which shows the financial position of the firm as on a particular date. It comprises of sources of funds or the liabilities, which also includes the credit balances of partners’ capital/current accounts. The other half of the statement is made up of application of funds or in other words, the assets, which may sometimes include the debit balances of partners’ capital/current accounts. The Partnership Act, 1932 does not specify any particular format unlike the Companies Act, 2013. Nevertheless, we should try to follow one particular rule – arrange the items based on their liquidity. Either start with the most liquid i.e. Cash or begin with the most illiquid i.e. Fixed assets.

Here we have arranged the items starting with the most illiquid.

Balance Sheet of M/s…

As on 31st March ....

Liabilities Amount Rs. Amount Rs. Assets Amount Rs. Amount Rs.Partner’s Capital A/c

X

Y

xxx

xxx xxx

Goodwill xxx

Partner’s Current A/c

X

Y

xxx

xxx xxx Patents xxxReserve Funds xxx Copyrights xxxBank Loan xxx Trademarks xxxPartner’s Loan xxx Land & Building xxxOther loans xxx Freehold Property xxx

2 - 18

S.Y.J.C. Book-keeping and Accountancy

Liabilities Amount Rs. Amount Rs. Assets Amount Rs. Amount Rs.Sundry Creditors xxx Leasehold Property xxxBills Payable xxx Plant & Machinery xxxBank Overdraft xxx Furniture & Fixtures xxxOutstanding expenses xxx Vehicles xxxIncome received in advance xxx Investments xxx

Interest accrued on investments xxxLoans and advances xxxSundry Debtors xxxBills receivable xxxClosing Stock xxxLoose Tools xxxStationary xxxPrepaid Expenses xxxIncome receivable xxxBank xxxCash at hand xxxPartner’s Current A/c (debit balance) xxx

xxx xxxContingent Liability xxx

Explanation of Balance Sheet items:-

1. Fixed Assets

Fixed assets are assets used for production purposes or for running the business. They are not bought for resale.

a. Tangible Assets

These are assets which have a physical existence and can be seen.

E.g.: Machinery, buildings, Vehicles, etc.

b. Intangible Assets

These are assets which cannot be seen with our eyes and have no physical presence.

E.g.: Goodwill, Copyrights, Patents, etc.

2. Current Assets

These are assets which are held for a short period of time and change form. Cash is converted into goods purchased. Stock of goods is converted to debtors when credit sales are made. Debtors are converted to cash again when they pay off. They are short-lived and hence are not fixed.

E.g.: Cash, Bank, Debtors, Stock, etc.

3. Fictitious Assets

These are not real assets. These are intangible but have no resale value.

E.g.: Preliminary expenses, Accumulated losses, Discount on issue of securities, etc.

4. Liabilities

a. Fixed liabilities

These are long term liabilities and are usually available during the life of the business.

E.g.: Capital, Long-term loans, etc.

b. Current liabilities

These are short term liabilities and are usually on the books for less than a year.

E.g.: Bills payable, sundry creditors, bank overdraft, etc.

c. Contingent liabilities

These are not part of the balance sheet. These are not current liabilities but may become liabilities on the happening or not happening of a future uncertain event. They are shown as a note to the balance sheet.

2 - 19

Partnership Final Account

Final Accounts Adjustments

We prepare final accounts based on information provided by the trial balance. But sometimes, there is additional information that is given along with the trial balance for which no entries have been passed. We need to consider the effects of such adjustments when we are preparing our final accounts based on the double entry system. Every adjustment outside of a trial balance has at least 2 effects. If all the effects necessary for an adjustment are not given, then the final accounts will not tally. Also, some adjustments are hidden or are silent such as Wages (10 months) or 12% Bank Loan. In such cases it is important that effects for these are also given when preparing the final accounts.

1) Closing Stock

Closing stock pertains to the stock of goods on hand at the end of the year. As per Accounting Standard-2, closing stock is valued at cost or market price, whichever is less. If closing stock is given in the trial balance, there is only one effect – Asset side of Balance sheet. If closing stock is given as an adjustment then there are two effects

a. Balance sheet – Asset side

b. Trading Account – Credit side

The Journal entry for the same is as follows –

Closing Stock A/c Dr. xxx

To Trading A/c xxx

Since closing stock is an asset, it is reflected on the asset side of the balance sheet. Also, since closing stock are goods unsold, the cost needs to be carried forward to the next period so that the profit of the current year is not disturbed. Hence, we need to credit the Trading A/c. This closing stock becomes the opening stock of the next year.

2) Outstanding expenses

These are expenses of the current year but which have not been paid. Since these pertain to the current year a provision needs to be made in the accounts of the current year.

a. Trading/Profit & Loss A/c – Debit Side (If an expense of the same name exists in the trial balance, then this outstanding portion needs to be added to that expense in the trading/profit & loss account.)

b. Balance Sheet – Liability side

The Journal entry for the same is as follows –

Particular Expense A/c Dr. xxx

To Outstanding expense a/c xxx

Any expense payable becomes a liability. Hence, we need to show it on the liability side of the balance sheet. Also, since the expense is of the current year, we need to debit the trading/profit & loss account to arrive at the correct profit or loss.

3) Prepaid expenses

Conversely, there are certain expenses which are paid in advance but actually pertain to the next year.

a. Balance Sheet – Assets side

b. Trading/Profit & Loss A/c – Debit side (deduct from the particular expense head)

The Journal entry for the same is as follows –

Prepaid expense A/c Dr. xxx

To Particular Expense A/c xxx

Since these are in the nature of assets, we show them on the asset side of the balance sheet. Also, since the expense is not of this year, we reduce the same from the particular expense in the trading/profit & loss account.

4) Income received in advance

Similar to prepaid expenses, there is income received in advance. This is income that pertains to the next year but has been already received this year.

a. Profit & Loss A/c – Credit side (deduct from the particular income)

b. Balance Sheet – Liability side

The Journal entry for the same is as follows –

Particular Income A/c Dr. xxx

To Income received in advance A/c xxx

2 - 20

S.Y.J.C. Book-keeping and Accountancy

Using the earlier logic of prepaid expenses, since this income is received in advance, it does not belong to the current year and hence needs to be deducted from the particular income. Also, since it’s an amount received in advance, it becomes a liability for the firm.

5) Income receivable

Income receivable refers to the income due but not yet received. It is an income of the current year.

a. Profit & Loss A/c – Credit side (add to the particular income)

b. Balance sheet – Asset side

The Journal entry for the same is as follows –

Income receivable A/c Dr. xxx

To Particular Income A/c xxx

Any outstanding income yet to be received is an asset of the firm. Hence it appears on the asset side of the balance sheet. Also, since it is an income of the current year, it is added to the particular income on the credit side of the profit and loss account.

6) Bad debts

A bad debt is the amount that debtors owe the firm but is now irrecoverable. It is in the nature of a loss and if it is shown in the trial balance then they appear on the debit side of the Profit & Loss A/c.

a. Profit & Loss A/c – Debit side (add to the already given bad debts)

b. Balance sheet – Asset side (deduct from sundry debtors)

The Journal entry for the same is as follows –

Bad debts A/c Dr. xxx

To Sundry Debtors A/c xxx

Bad debts are debts which are irrecoverable and hence need to be written off. To write them off, we deduct them from the sundry debtors. Also, since bad debts are in nature a loss, they get debited to the profit and loss account.

7) Reserve for Doubtful Debts/ Provision for Doubtful Debts/ RDD

Firms make provisions for expected losses based on their prior experience. Provision for bad debts or doubtful debts is made to cover for possible losses from debtors going bad. If RDD already exists in the trial balance, then the same is credited to the profit & loss account since this is the old RDD and needs to be reversed. The effects for RDD appearing as an adjustment are as follows -

a. Profit & Loss A/c – Debit side (add to old bad debts)

b. Balance Sheet – Asset Side (Deduct from Sundry Debtors)

The Journal entry for the same is as follows –

Reserve for Doubtful Debts A/c Dr. xxx

To Sundry Debtors A/c xxx

The Reserve for Doubtful Debts is created out of the current year’s profits and hence the same needs to be debited to the profit & loss account. Also, since they effectively reduce the amount of debtors that the firm expects to realize, we show them as a deduction from sundry debtors in the balance sheet.

Dr. Profit & Loss Account for the year ended ..... Cr.Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)

To Bad Debts

Add: New Bad Debts

Add: New RDD

Less: Old RDD

xxx

xxx

xxx

xxx

By Old RDD

Less: Old Bad Debts

Less: New Bad Debts

Less: New RDD

xxx

xxx

xxx

xxx xxxxxx

xxx

xxx xxxNote: If Old RDD is more than the total of the old bad debts, new bad debts and the new RDD, then it is shown on the credit

side of the profit & loss account so as to avoid a negative figure on the debit side of the profit and loss account.

2 - 21

Partnership Final Account

8) Reserve for Discount on Debtors

Firms allow discounts to their customers and for this purpose create a reserve fund to finance the future discounts to debtors.

a. Balance Sheet – Asset side (deduct from sundry debtors)

b. Profit & Loss A/c – Debit side (add to discount allowed if already given in trial balance, else debit profit and loss account separately)

The Journal entry for the same is as follows –

Reserve for Discount on Debtors A/c Dr. xxx

To Sundry Debtors A/c xxx

The logic is similar to creation of RDD. Since, the reserve is created for a possible expense; we need to debit the profit and loss account. Also, since it effectively reduces the amount of debtors, we deduct it from the sundry debtors amount in the balance sheet.

9) Reserve for Discount on Creditors

Firms also create reserves for discounts they expect from creditors.

a. Balance sheet – Liability side (deduct from sundry creditors)

b. Profit & Loss A/c – Credit side (add to discount received if already exists in trial balance, else credit separately)

The Journal entry for the same is as follows –

Sundry Creditors A/c Dr. xxx

To Reserve for Discount on Creditors A/c xxx

Since this is an income for the firm, we need to credit the profit and loss account. Simultaneously, it also reduces the amount payable to the creditors and hence is deducted from sundry creditors.

10) Depreciation

Depreciation is charged on assets to account for the decrease in value due to wear and tear, passage of time, etc.

a. Profit & Loss A/c – Debit side

b. Balance Sheet – Asset side (deduct from particular fixed assets on which depreciation is charged)

The Journal entry for the same is as follows –

Depreciation A/c Dr. xxx

To Fixed Asset A/c xxx

Profit & Loss A/c Dr. xxx

To Depreciation A/c xxx

Depreciation being an expense we debit the profit and loss account. We also deduct the same from the asset as it signifies a reduction in its value. To give effect to this, we pass two separate entries. The first one reduces the value of the asset whereas the second one debits the profit and loss account.

11) Interest

I. Interest on Partner’s Capital

a. Profit & Loss A/c – Debit side

b. Partner’s Capital/Current A/c – Credit side

The Journal entry for the same is as follows –

Interest on Capital A/c Dr. xxx

To Partner’s Capital /Current A/c xxx

Profit & Loss A/c Dr. xxx

To Interest on Capital A/c xxx

Interest on capital is an expense of the firm and hence needs to be debited to the profit and loss account. On the other hand, it increases the amount owed by the firm to the partners and hence needs to be credited to the partners’ capital/current account.

2 - 22

S.Y.J.C. Book-keeping and Accountancy

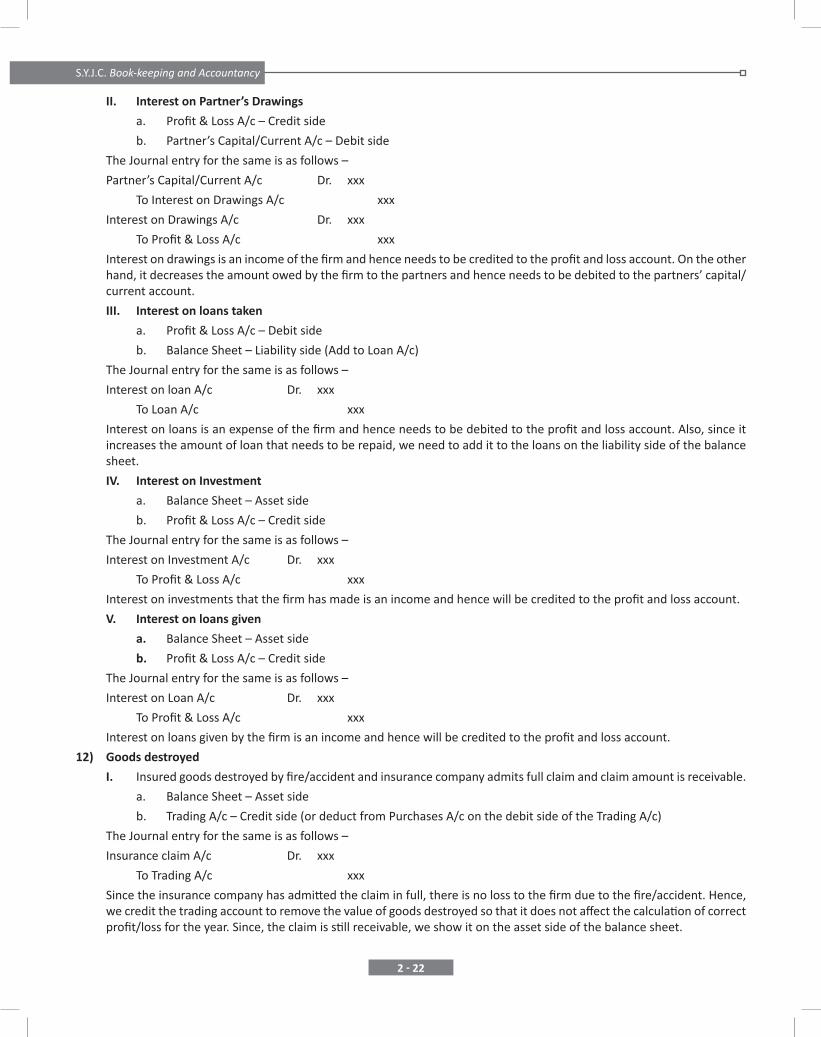

II. Interest on Partner’s Drawings

a. Profit & Loss A/c – Credit side

b. Partner’s Capital/Current A/c – Debit side

The Journal entry for the same is as follows –

Partner’s Capital/Current A/c Dr. xxx

To Interest on Drawings A/c xxx

Interest on Drawings A/c Dr. xxx

To Profit & Loss A/c xxx

Interest on drawings is an income of the firm and hence needs to be credited to the profit and loss account. On the other hand, it decreases the amount owed by the firm to the partners and hence needs to be debited to the partners’ capital/current account.

III. Interest on loans taken

a. Profit & Loss A/c – Debit side

b. Balance Sheet – Liability side (Add to Loan A/c)

The Journal entry for the same is as follows –

Interest on loan A/c Dr. xxx

To Loan A/c xxx

Interest on loans is an expense of the firm and hence needs to be debited to the profit and loss account. Also, since it increases the amount of loan that needs to be repaid, we need to add it to the loans on the liability side of the balance sheet.

IV. Interest on Investment

a. Balance Sheet – Asset side

b. Profit & Loss A/c – Credit side

The Journal entry for the same is as follows –

Interest on Investment A/c Dr. xxx

To Profit & Loss A/c xxx

Interest on investments that the firm has made is an income and hence will be credited to the profit and loss account.

V. Interest on loans given

a. Balance Sheet – Asset side

b. Profit & Loss A/c – Credit side

The Journal entry for the same is as follows –

Interest on Loan A/c Dr. xxx

To Profit & Loss A/c xxx

Interest on loans given by the firm is an income and hence will be credited to the profit and loss account.

12) Goods destroyed

I. Insured goods destroyed by fire/accident and insurance company admits full claim and claim amount is receivable.

a. Balance Sheet – Asset side

b. Trading A/c – Credit side (or deduct from Purchases A/c on the debit side of the Trading A/c)

The Journal entry for the same is as follows –

Insurance claim A/c Dr. xxx

To Trading A/c xxx

Since the insurance company has admitted the claim in full, there is no loss to the firm due to the fire/accident. Hence, we credit the trading account to remove the value of goods destroyed so that it does not affect the calculation of correct profit/loss for the year. Since, the claim is still receivable, we show it on the asset side of the balance sheet.

2 - 23

Partnership Final Account

II. Insured goods destroyed by fire / accident and insurance company admits partial claim.

a. Trading A/c – Credit side – Total value of goods destroyed

b. Profit & Loss A/c – Debit side – Actual loss amount

c. Balance Sheet – Asset side – Claim amount

The Journal entry for the same is as follows –

Insurance claim A/c Dr. xxx

Goods lost by fire/accident A/c Dr. xxx

To Trading A/c or Purchases A/c xxx

Profit & Loss A/c Dr. xxx

To Goods lost by fire/accident A/c xxx

In this case, since only a partial claim has been accepted by the insurance company, the firm suffers a loss to the extent of the claim not admitted. The gross value of goods is credited to the trading account or purchases account to remove the value of goods from the current year’s calculations. The amount of claim is a receivable and hence is shown as an asset in the balance sheet. The part of the claim that has not been admitted is a loss and hence needs to be debited to the profit and loss account.

III. Uninsured goods lost by fire/accident

a. Trading A/c – Credit side (or deduct from Purchases A/c on the debit side of the Trading A/c)

b. Profit & Loss A/c – Debit side

The Journal entry for the same is as follows –

Profit & Loss A/c Dr. xxx

To Trading A/c or Purchases A/c xxx

This is a total loss to the firm and hence the value of goods is removed from the trading account or is reduced from the value of purchases so as to arrive at a correct gross profit/loss. The profit and loss account is then debited to record the loss sustained.

13) Goods lost due to theft

a. Trading A/c – Credit side (or deduct from Purchases A/c on the debit side of the Trading A/c)

b. Profit & Loss A/c – Debit side

The Journal entry for the same is as follows –

Profit & Loss A/c Dr. xxx

To Trading A/c or Purchases A/c xxx

Goods stolen or lost due to theft are a loss to the firm. The same logic applies as in loss of uninsured goods. The value of goods is removed from the trading account or is reduced from the value of purchases so as to arrive at a correct gross profit/loss. The profit and loss account is then debited to record the loss sustained.

14) Goods distributed as free samples

a. Trading A/c – Credit side (or deduct from Purchases A/c on the debit side of the Trading A/c)

b. Profit & Loss A/c – Debit side

The Journal entry for the same is as follows –

Advertisement A/c Dr. xxx

To Trading A/c or Purchases A/c xxx

Profit & Loss A/c Dr. xxx

To Advertisement A/c xxx

Goods distributed as free samples are in the nature of advertisement expenses for the firm. The value of goods is removed from the trading account or is reduced from the value of purchases as the goods are taken out from the firm. The profit and loss account is then debited to record the expenditure on advertisement.

2 - 24

S.Y.J.C. Book-keeping and Accountancy

15) Goods withdrawn by a Partner

a. Trading A/c – Credit side (or deduct from Purchases A/c on the debit side of the Trading A/c)

b. Partners’ Capital/Current A/c – Debit side

The Journal entry for the same is as follows –

Drawings A/c Dr. xxx

To Trading A/c or Purchases A/c xxx

Partner’s Capital / Current A/c Dr. xxx

To Drawings A/c xxx

Goods withdrawn go out from the firm and hence need to be credited to the trading/purchase account. Also, since goods withdrawn are essentially in the nature of drawings, they are debited to the partners’ capital/current accounts.

16) Unrecorded purchases

Unrecorded purchases are goods purchased but not recorded in the books of accounts although they are included in the stock.

a. Trading A/c – Debit side (add to purchases)

b. Balance Sheet – Liability side (add to creditors)

The Journal entry for the same is as follows –

Purchases A/c Dr. xxx

To Creditors A/c xxx

Since we have not recorded the purchase before, but the same has already been included in the closing stock, we need to pass an entry to record the purchases. We debit the purchase account and credit the creditors.

17) Unrecorded Sales

Sales made to customers on credit but not recorded in the sales book are known as unrecorded sales.

a. Trading A/c – Credit side (add to sales)

b. Balance Sheet – Asset side (add to debtors)

The Journal entry for the same is as follows –

Debtors A/c Dr. xxx

To Sales A/c xxx

Since we have not recorded the sale we need to pass an entry to record the sale. We credit the sales account and debit the debtors.

18) Capital expenditure wrongly recorded as revenue expenditure and vice versa

Sometimes, capital expenses such as expenses incurred on installation of an asset are wrongly included as revenue expenditure. They are expended in the profit and loss account instead of getting capitalized.

a. Balance Sheet – Asset side (add to the particular asset)

b. Trading/Profit & Loss A/c – Debit side (deduct from the particular expense)

The Journal entry for the same is as follows –

Asset A/c Dr. xxx

To Expense A/c xxx

Alternatively, revenue expenditure gets recorded as capital expenditure and this wrongly increases profit.

a. Balance Sheet – Asset side (reduce from the particular asset)

b. Trading/Profit & Loss A/c – Debit side (add to the particular expense)

The Journal entry for the same is as follows –

Expense A/c Dr. xxx

To Asset A/c xxx

2 - 25

Partnership Final Account

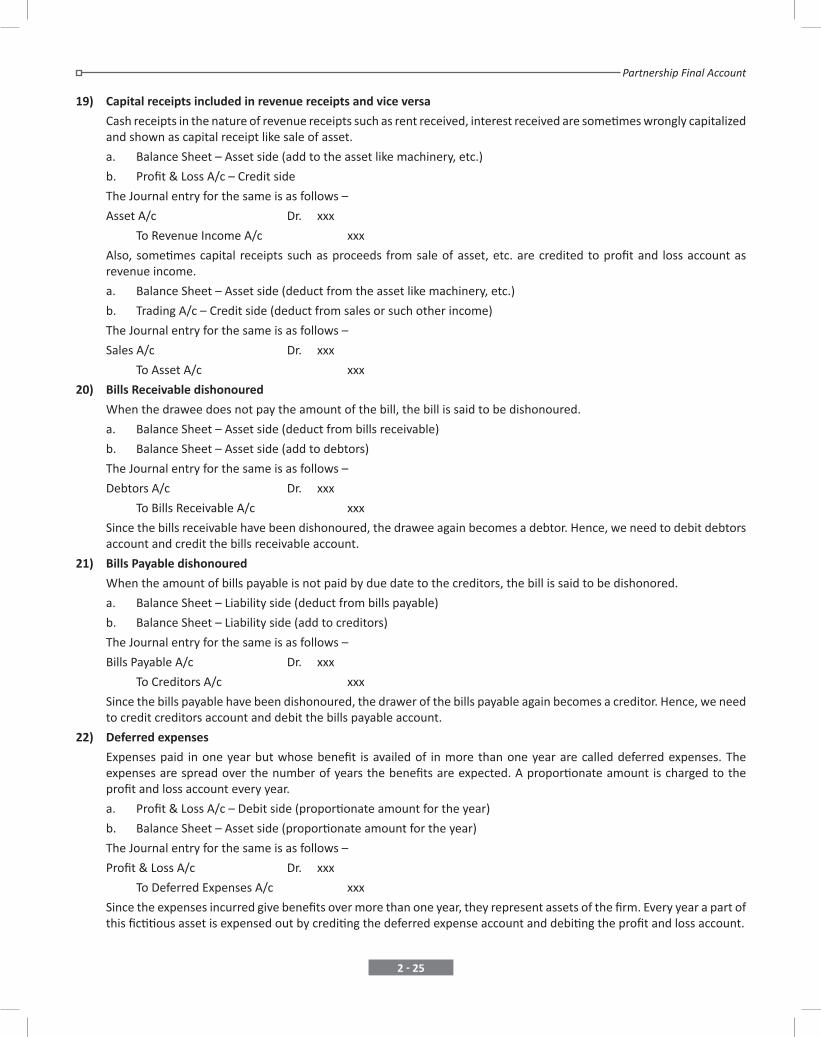

19) Capital receipts included in revenue receipts and vice versa

Cash receipts in the nature of revenue receipts such as rent received, interest received are sometimes wrongly capitalized and shown as capital receipt like sale of asset.

a. Balance Sheet – Asset side (add to the asset like machinery, etc.)

b. Profit & Loss A/c – Credit side

The Journal entry for the same is as follows –

Asset A/c Dr. xxx

To Revenue Income A/c xxx

Also, sometimes capital receipts such as proceeds from sale of asset, etc. are credited to profit and loss account as revenue income.

a. Balance Sheet – Asset side (deduct from the asset like machinery, etc.)

b. Trading A/c – Credit side (deduct from sales or such other income)

The Journal entry for the same is as follows –

Sales A/c Dr. xxx

To Asset A/c xxx

20) Bills Receivable dishonoured

When the drawee does not pay the amount of the bill, the bill is said to be dishonoured.

a. Balance Sheet – Asset side (deduct from bills receivable)

b. Balance Sheet – Asset side (add to debtors)

The Journal entry for the same is as follows –

Debtors A/c Dr. xxx

To Bills Receivable A/c xxx

Since the bills receivable have been dishonoured, the drawee again becomes a debtor. Hence, we need to debit debtors account and credit the bills receivable account.

21) Bills Payable dishonoured

When the amount of bills payable is not paid by due date to the creditors, the bill is said to be dishonored.

a. Balance Sheet – Liability side (deduct from bills payable)

b. Balance Sheet – Liability side (add to creditors)

The Journal entry for the same is as follows –

Bills Payable A/c Dr. xxx

To Creditors A/c xxx

Since the bills payable have been dishonoured, the drawer of the bills payable again becomes a creditor. Hence, we need to credit creditors account and debit the bills payable account.

22) Deferred expenses

Expenses paid in one year but whose benefit is availed of in more than one year are called deferred expenses. The expenses are spread over the number of years the benefits are expected. A proportionate amount is charged to the profit and loss account every year.

a. Profit & Loss A/c – Debit side (proportionate amount for the year)

b. Balance Sheet – Asset side (proportionate amount for the year)

The Journal entry for the same is as follows –

Profit & Loss A/c Dr. xxx

To Deferred Expenses A/c xxx

Since the expenses incurred give benefits over more than one year, they represent assets of the firm. Every year a part of this fictitious asset is expensed out by crediting the deferred expense account and debiting the profit and loss account.

2 - 26

S.Y.J.C. Book-keeping and Accountancy

23) Commission to partner as a percentage of sales/profit

Partners sometimes are allowed a percentage of the sales they make or the profit they achieve as commission.

a. Profit & Loss A/c – Debit side

b. Partners’ Capital/Current A/c – Credit side

The Journal entry for the same is as follows –

Profit & Loss A/c Dr. xxx

To Partners’ Capital/Current A/c xxx

Commission paid is an expense for the firm. After calculating the commission by applying the percentage given to the sales/profit figure, we need to the debit the profit and loss account. Also, since the commission payable to the partner increases the amount due to partners, we need to credit the partners’ capital/current account.

Summary of Adjustments:

Adjustments 1st Effect 2nd Effect1. Closing Stock Balance Sheet Asset Side Trading A/c Credit side2. Outstanding Expenses Add to that particular expenses on the

debit side of Trading/Profit and Loss A/c

Balance Sheet Liability Side

3. Prepaid Expenses Balance Sheet Asset side Deduct from that particular expenses on the debit side of Trading/profit and loss A/c

4. Income received in advance (Pre-received Income)

Deduct from that particular income on the credit side of Profit and Loss A/c

Balance Sheet Liability Side

5. Income receivable (Outstanding Income)

Balance Sheet Asset Side Add on that particular Income on the credit side pf profit and loss A/c

6. Bad Debts (Additional or New Bad debts)

Show to the Debit side of profit and loss A/c (Add to old Bad Debts)

Deduct from Sundry debtors in Balance Sheet Asset Side

7. Provision for Doubtful Debts (Reserve for Doubtful Debts, New R.D.D.)

Show to the debit side of profit and loss A/c (Add to old bad debts)

Deduct from Sundry Debtors in Balance Sheet Asset Side

8. a. Reserve For Discount on Debtors

Show to the debit Side of Profit and loss A/c (Add to discount received)

Deduct from Sundry Debtors Balance Sheet Asset Side

b. Reserve for Discount on Creditors

Deduct from sundry creditors in Balance Sheet Liability Side

Show to the credit side of profit and loss A/c (Add to discount received)

9. Depreciation Show on the debit side of the profit and loss A/c

Deduct from that particular asset in Balance Sheet Asset side

10. a. Interest on Capital Show to the debit side of profit and loss A/c

Partner’s capital/ current A/c/ credit side or add to capitals

b. Interest on Drawing Show to the debit side of partner’s capital/current A/c or Less from capital

Show to the credit side of profit and loss A/c

c. Interest on loan taken Show to the debit side of profit and loss A/c

Add to loan taken in the Balance Sheet liability side

11. Interest on Investment and loan given Balance sheet asset side Show to the credit side of profit and loss A/c

12. a. Insured Goods destroyed by Fire/accident

i. Balance sheet asset side (claim amount)

ii. Profit and loss A/c (loss amount)

Trading A/c – credit side (gross amount)

b. Uninsured Goods destroyed by Fire/ accident

Profit and loss A/c debit side Show to the credit side of Trading A/c

Goods Stolen Profit and Loss A/c debit side Show to the credit side of Trading A/c 13. Goods distributed as free samples Profit and loss A/c debit side (Add in

advertisements)Show to the credit side of trading A/c

2 - 27

Partnership Final Account

Adjustments 1st Effect 2nd Effect14. Goods withdrawn by Partners for

personal usePartners capital/ current A/c debit side Show to the credit side of trading A/c

or Deduct from purchase A/c15. a. Unrecorded Purchases Add to purchase on the debit side of

Trading A/c Add to creditors on the Liability Side of Balance Sheet

b. Unrecorded Sales Add to debtors on the asset side of the Balance Sheet

Add to Sales on the credit side of Trading A/c

16. a. Capital Expenditure included in revenue expenditure

Add to that particular asset in Balance Sheet Asset side

Deduct from that particular revenue expenses on the debit side of Trading or profit and loss A/c

b. Revenue expenditure included in capital expenditure

Add to that particular revenue expenditure

Deducted from that particular Asset in Balance Sheet

17. Bills Receivable Dishonoured Add the amt of bill dishonored to sundry debtors in the Balance Sheet asset side

Deduct the Amount of bill dishonored from Bills Receivable

18. Bills Payable Dishonoured Deduct the amt of bill dishonored from Bills payable

Add the Amount of bill dishonored to sundry creditors in the Balance Sheet liability side

19. Deferred expenses of Advertisement paid for 5 years

Advertisement related to current year debited to profit and loss A/c

Remaining Amount of advertisement is shown on asset side of the Balance Sheet as Prepaid Advertisement

20. Revenue receipts included in capital receipts e.g. sales of goods included in sale of furniture

Add to furniture on the asset side of the Balance Sheet

Add to Sales on the credit side of Trading A/c

21. Commission to partners as percentage of gross profit/sales

Show to the debit side of profit and loss A/c Show to the credit side of Partner’s capital /currents A/c or add to partner’s capital A/c

Section I : From the Textbook - Solved Problems:-

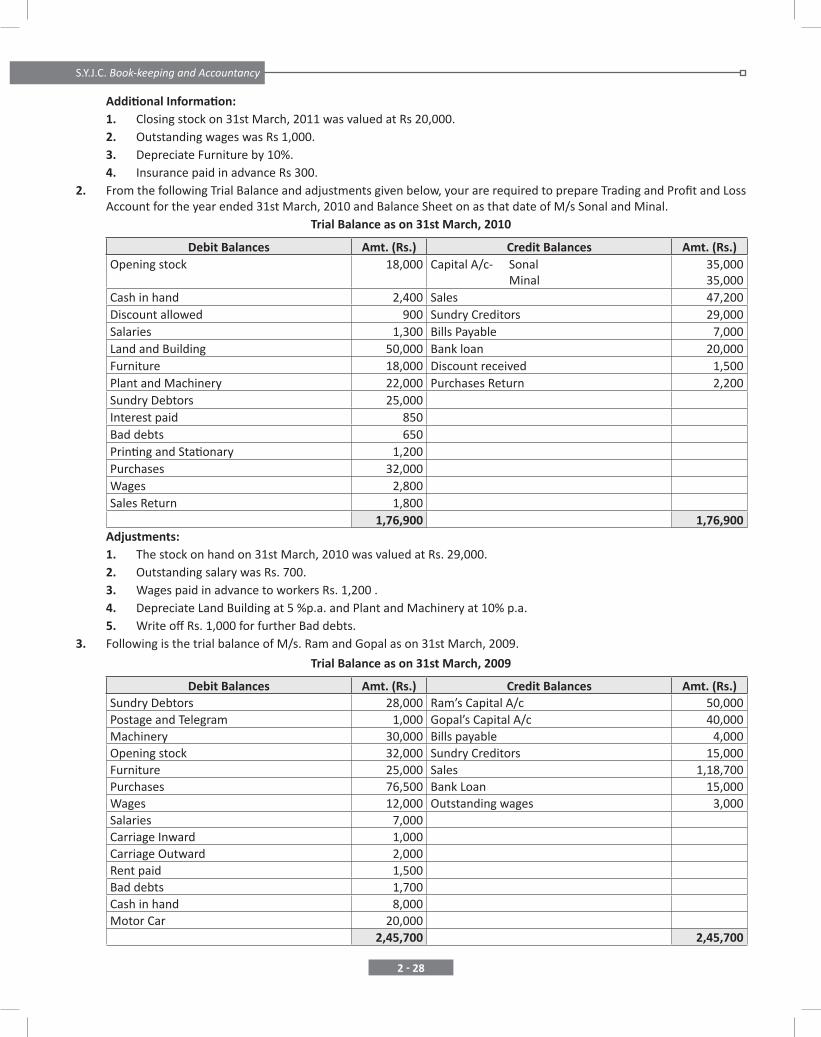

1. From the following Trial Balance of M/s. Ganesh and Kartik, you are required to prepare Trading and Profit & Loss Account for the year ended 31st March, 2011 and Balance sheet as on that date after taking into account the additional information.

Trial Balance as on 31st March, 2011

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Opening stock 18,000 Capital A/c - Ganesh 50,000Purchases 24,000 Kartik 30,000Wages 2,400 Sundry Creditors 10,000Carriage Inward 1,200 Bills Payable 7,800Cash in hand 3,800 Rent received 2,200Insurance 1,200 Sales 52,500Postage and Telegram 700Sundry Debtors 21,000Land and Building 40,000Furniture 28,000Travelling expenses 1,300Discount allowed 900Bad debts 2,000Bills Receivable 8,000

1,52,500 1,52,500

2 - 28

S.Y.J.C. Book-keeping and Accountancy

Additional Information: 1. Closing stock on 31st March, 2011 was valued at Rs 20,000. 2. Outstanding wages was Rs 1,000. 3. Depreciate Furniture by 10%. 4. Insurance paid in advance Rs 300.2. From the following Trial Balance and adjustments given below, your are required to prepare Trading and Profit and Loss

Account for the year ended 31st March, 2010 and Balance Sheet on as that date of M/s Sonal and Minal.Trial Balance as on 31st March, 2010

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Opening stock 18,000 Capital A/c- Sonal

Minal35,00035,000

Cash in hand 2,400 Sales 47,200Discount allowed 900 Sundry Creditors 29,000Salaries 1,300 Bills Payable 7,000Land and Building 50,000 Bank loan 20,000Furniture 18,000 Discount received 1,500Plant and Machinery 22,000 Purchases Return 2,200Sundry Debtors 25,000Interest paid 850Bad debts 650Printing and Stationary 1,200Purchases 32,000Wages 2,800Sales Return 1,800

1,76,900 1,76,900 Adjustments: 1. The stock on hand on 31st March, 2010 was valued at Rs. 29,000. 2. Outstanding salary was Rs. 700. 3. Wages paid in advance to workers Rs. 1,200 . 4. Depreciate Land Building at 5 %p.a. and Plant and Machinery at 10% p.a. 5. Write off Rs. 1,000 for further Bad debts.3. Following is the trial balance of M/s. Ram and Gopal as on 31st March, 2009.

Trial Balance as on 31st March, 2009

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Sundry Debtors 28,000 Ram’s Capital A/c 50,000Postage and Telegram 1,000 Gopal’s Capital A/c 40,000Machinery 30,000 Bills payable 4,000Opening stock 32,000 Sundry Creditors 15,000Furniture 25,000 Sales 1,18,700Purchases 76,500 Bank Loan 15,000Wages 12,000 Outstanding wages 3,000Salaries 7,000Carriage Inward 1,000Carriage Outward 2,000Rent paid 1,500Bad debts 1,700Cash in hand 8,000Motor Car 20,000

2,45,700 2,45,700

2 - 29

Partnership Final Account

Profit sharing ratio of Ram and Gopal is 3:2. Prepare Trading and Profit and Loss Account for the year ended 31st March, 2009 and Balance Sheet as on that date after taking into consideration the following adjustments.

1. The closing stock is valued at cost price Rs. 45,000 while its market price is Rs. 50,000. 2. Outstanding expenses were salaries Rs. 800, Rent Rs. 500. 3. Provide Depreciation on Machinery at 15% and Furniture at 10% p.a. 4. Goods costing Rs. 3,000 distributed as free sample. 5. Interest on Bank loan is payable Rs. 1,500.

4. Raja and Rani are partners of ‘Maharaja Traders’. They decided to share profits and losses in the ratio of 3:2. From the following Trial Balance and additional information, you are required to prepare Trading and Profit Loss Account for the year ended 31st March, 2013 and Balance Sheet as on that date.

Trial Balance as on 31st March, 2013

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Purchases 90,500 Sales 1,20,300Sundry Debtors 34,000 Creditors 45,500Bills Receivable 35,000 Bills Payable 32,000Opening stock 34,600 Capital A/c - Raja

Rani

1,50,000

1,00,000Land and Building 1,20,000 Raja’s loan A/c 11,000Work’s Manager Salary 4,700 Commission received 2,500Motive Power 5,500Plant and Machinery 80,000Audit fees 3,400Salaries and Wages 14,500Trade expenses 2,100General expenses 1,800Wages and Salaries 20,700Loose tools 10,000Prepaid rent 4,500

4,61,300 4,61,300 Additional Information:

a. Stock on hand on 31st March, 2013 was cost Rs. 42,000 and its market price was Rs. 45,000. b. Audit fees paid in advance of Rs. 1,500. c. Motive power includes Rs. 3,000 paid for deposit of power meter. d. Goods worth Rs. 2,500 taken by Raja for his personal use are not entered in the books of account. e. Bills payable dishonoured of Rs. 2,500. f. Depreciate plant and machinery at 5% p.a. and loose tools at 10% p.a. g. Commission includes, pre-received amount of Rs. 1,000.

5. From the following Trial Balance of M/s Sharma and Varma, you are required to prepare a Trading and Profit and Loss Account for the year ended 31st March, 2013 and Balance Sheet as on that date after taking into consideration the additional information given below. Partners share profits and losses in their capital ratio.

Trial Balance as on 31st March, 2013

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Stock on 1st April, 2012 28,000 Capital A/c - Sharma

Varma 90,00060,000

Purchases 1,75,000 Sundry Creditors 30,000Salaries 17,500 Rent received 3,500Unproductive wages 1,800 Bank overdraft 24,500Carriage 1,200 Sales 2,26,750

2 - 30

S.Y.J.C. Book-keeping and Accountancy

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Royalties 2,500Freight 1,400Printing and Stationary 2,100Sundry debtors 40,000Furniture 20,000Leasehold property 95,000Investment 35,000Travelling expenses 1,750Advertisement (for 3 years) 4,275Bad debts 1,425Discount allowed 800Cash in hand 7,000

4,34,750 4,34,750 Additional Information: 1. Stock on hand on 31st March, 2013 was at cost Rs. 38,000. 2. Provide R.D.D at 5% on Sundry Debtors and Reserve for discount on debtors at 3%. 3. Goods worth Rs. 5,000 destroyed by fire and Insurance company admitted a claim of Rs. 4,300. 4. Rent of Rs. 800 is still receivable from the tenant. 5. Depreciate Furniture at 12% p.a.6. Rane and Chavan are partners sharing profits and losses in the ratio of 7:6. From the following Trial Balance and additional

information prepare Trading and Profit and Loss Account for the year ended 31st March, 2012 and Balance Sheet as on that date.

Trial Balance as on 31st March, 2012

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Opening stock 44,000 Reserve for doubtful debts 2,100Bills Receivable 28,000 Sundry creditors 55,400Wages and Salaries 12,000 Sales 2,00,000Sundry Debtors 52,000 General Reserve 28,000Purchases 1,30,000 Outstanding salaries 2,700Building 80,000 Capital A/c- Rane 80,000

Discount 1,400 Chavan 60,000General expenses 3,800Audit fees 4,000Bad debts 3,500Cash at Bank 11,500Travelling expenses 4,200Motor Car 45,000Trade expenses 4,300Ret for 9 months 4,500

4,28,200 4,28,200 Adjustments: a. Closing stock is valued at Rs. 42,000. b. Bills Receivables included dishonor bill of Rs. 4,000 c. Goods worth Rs. 2,100 were taken by Rane for his personal use was not entered in the books of account. d. Goods worth 4,000 were sold on 27th March, 2012, but no entry was made in the books of account. e. Write off 2,000 for bad debts and maintain R.D.D at 5% on Sundry debtors. f. Travelling expenses includes, personal travelling expenses of Mr. Chavan of Rs. 800. g. Depreciate Building at 7% p.a.

2 - 31

Partnership Final Account

7. M/s. Vijay Raj Traders is a Partnership firm in which Vijay and Raj are partner sharing profits and losses in the ratio of 8:7. From the following Trial Balance prepare Trading and Profit Loss Account for the year ended 31st March, 2013 and Balance sheet as on that date.

Trial Balance as on 31st March, 2013

Debit Balances Amt. (Rs.) Credit Balance Amt. (Rs.)Current A/c-Raj 1,500 Capital A/c - Vijay 72,000Purchases 1,42,000 Raj 63,000Sundry Debtors 80,000 Current A/c - Vijay 2,490Bills Receivables 12,000 Sales 2,13,000Commission 3,000 Sundry Creditors 47,500Opening stock 27,000 Bills Payable 19,500Cash in hand 3,500 Commission 2,50010% Government bonds (Purchased on 1.1.2013) 20,000Rent and Taxes 2,390Building 70,000Furniture 15,000Salaries 21,000Wages 8,000Insurance 3,600Motor Car 10,000Bad debts 1,000

4,19,990 4,19,990 Adjustments: 1) Stock on hand on 31st March, 2013 was valued at Rs. 35,000. 2) Vijay is allowed a salary of Rs. 3,500 and Raj is entitled to get commission at 2% on sales. 3) Interest on partners capital@ 5% is to be provided. 4) Depreciate Furniture at 15% and Building at 10% p.a. 5) Rs. 2,000 due from customer is not recoverable. 6) Insurance is paid for the year ended on 30th June, 2013. 7) Prepaid commission is Rs. 1,000 and pre-received commission is Rs. 700.

8. Tambe and Pitale are partners sharing profits and lossess equally. From the following Trial Balance and adjustments, prepare Trading and Profit and Loss Account for the year ended 31st March, 2012 and Balance Sheet as on that date.

Trial Balance as on 31st March, 2012

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Land and Building 75,000 Capital A/c - Tambe 70,000Machinery (Addition on 1st July, 2011 Rs. 10,000)

55,000 Pitale 50,000

Opening stock 23,000 Sales 85,000Wages 5,750 Sundry Creditors 44,250Cash at Bank 3,500 10% Bank loan

(Taken on 1st October 2011) 20,000Sundry Debtors 32,800 Sundry Income 1,500Purchases 63,000 Pre-received rent 2,500Carriage 1,250 Provident fund 30,000Rent, Rates and Taxes 2,400Furniture and fixture 26,600Salaries 3,500Office expenses 2,450Drawing A/c - Tambe Pitale

5,0004,000

3,03,250 3,03,250

2 - 32

S.Y.J.C. Book-keeping and Accountancy

Adjustments:

1) Closing stock is valued at Rs. 20,000.

2) Goods worth Rs. 2,000 were purchased on 31st March, 2013 and included in closing stock but not recorded in the books of account.

3) Goods worth Rs. 2,500 were sold, but not recorded in the books of account.

4) Outstanding office expenses were Rs. 1,700.

5) Depreciate Machinery at 10% p.a.

6) Write off Rs. 1,500 for Bad debts.

9. Sachin and Nilesh are partners sharing profits and losses equally. From the following Trial Balance and adjustments. You are required to prepare a Trading and Profit and Loss Account for the year ended 31st March, 2010 and Balance sheet as on that date.

Trial Balance as on 31st March, 2010

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)

Drawings: Sachin

Nilesh

5,000

4,000

Capital A/c - Sachin

Nilesh

70,000

60,000

Sundry Debtors 45,000 Current A/c - Sachin

Nilesh

4,750

3,800

Cash at Bank 22,800 Sundry Creditors 52,500

Land and Building 75,000 Bank overdraft 17,250

Opening stock 38,200 Sales 2,07,650

Import duty 6,400

Audit fees 3,750

Wages 4,150

Brokerage 2,400

Motor Van 40,000

Machinery 32,000

12% Debentures 25,000

Factory Rent 2,250

Salaries 7,500

Purchases 1,02,500

4,15,950 4,15,950

Adjustments:

1) Stock on hand on 31st March, 2010 was valued at Rs. 41,000.

2) Outstanding expenses were: salary Rs. 1,500, audit fees Rs. 1,250.

3) Interest on partner’s capital at 5% p.a. is allowed while interest on drawings is charged at 4% p.a.

4) Depreciate Machinery at 12.5% and Motor Van 8% p.a.

5) Sachin is entitled to get salary at Rs. 400 per month and Nilesh is to get 4% commission on Gross profit.

6) Sales includes, sale of machinery of Rs. 2,000 which is sold on 1st April, 2009.

7) Debentures purchased on 1st October, 2009.

2 - 33

Partnership Final Account

10. Ramdeo and Mahadeo are partners sharing profits and losses in the ratio of 2:1. From the following Trial Balance and adjustments, prepare Trading and Profit and Loss Account for the year ended 31st March, 2011 and Balance Sheet as on 31st March, 2011.

Trial Balance as on 31st March, 2011

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Opening Stock 20,250 Sales 1,47,500Furniture and fixtures 15,000 Sundry Creditors 33,500Cash in hand 1,802 Dividend received 4,000Bad debts 1,250 Provident fund 17,500Salaries and wages 9,750 Interest on P.F. Investment 1,250Purchases 87,500 Capital A/c - Ramdeo 80,000Sundry Debtors 41,500 Mahadeo 40,000General expenses 1,900Land and Building 75,000Carriage inward 1,748Goodwill 30,000Provident fund contribution 1,250Advertisement (for 3 years)w.e.f. 1st October, 2010 4,800Provident fund investment 19,000Shares in B Ltd. 13,000

3,23,750 3,23,750 Adjustments: 1) Stock on hand on 31st March, 2011 was valued at Rs. 25,000. 2) Rs. 2,000 paid during the year as Building repairs wrongly debited to Building account. 3) Depreciate Land and Building at 10% p.a. 4) Maintain R.D.D. at 5% on Sundry Debtors. 5) Reserve for discount on Debtors and Creditors are to be made at 3% and 4% respectively. 6) Uninsured goods worth Rs. 2,000 were destroyed by fire.

11. From the following Trial Balance of M/s. Pravin and Ramesh, you are required to prepare Trading and Profit and Loss Account for the year ended 31st March, 2013 and Balance Sheet as on that date.

Trial Balance as on 31st March, 2013

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Plant and Machinery 1,40,000 Capital A/c - Pravin

Ramesh2,00,0001,50,000

Goodwill 40,000 Sales 3,30,000Furniture 80,000 Sundry Creditors 1,05,000Coal, Gas and Water 4,300 12% Bank loan (Taken on 1st October, 2012) 40,000Land and Building 1,20,000Purchases 2,32,000Postage and Telegrams 2,200Export duty 15,500Wages and Salaries 31,000Rent and Taxes 7,200Cash in hand 18,000Freight 6,200Prepaid rent 3,600Sundry Debtors 76,000

2 - 34

S.Y.J.C. Book-keeping and Accountancy

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Insurance 4,200Opening stock 39,000Discount 5,800

8,25,000 8,25,000 Adjustments:

1) Closing stock in hand was valued at Rs. 61,000.

2) Goods distributed as free samples were Rs. 3,000.

3) Postal stamps in hand on 31st March, 2013 were Rs. 700.

4) Provides 5% interest on capitals.

5) Prepaid insurance Rs. 900.

6) Provide Reserve for doubtful debts at 5% on Sundry Debtors.

7) Wages paid for installation of machinery were included in Wages A/c Rs 5,000. Depreciate Machinery at 5%

12. Mr. Ajit and Mr. Sujit are partners of the firm sharing profits and losses in the ratio of 3:2. Their Trial Balance as on 31st March, 2012 was given below. Prepare Trading and Profit and Loss Account for the year ended 31st March, 2012 and Balance Sheet as on that date.

Trial Balance as on 31st March, 2012

Particulars Debit Amt. (Rs.) Credit Amt. (Rs.)Capital A/c - Ajit

Sujit

50,000

40,000Purchases and Sales 62,750 1,22,000Sundry Debtors and Creditors 24,000 47,000Interest 2,900 2,000Opening stock 21,500 -Wages 8,500 -Land and Building 75,000 -Loose tools 15,000 -Power, Fuel and Oil 2,750 -Export duty 1,200 -Salaries 10,800 -Electricity charges 1,400 -Investments 24,000 -Reserve fund - 8,000Ajit’s loan A/c - 10,000Bank overdraft - 11,000Patents 32,000 -Administration expenses 4,300 -Cash in hand 2,000 -Heating and lighting 1,900 -

2,90,000 2,90,000 Adjustments:

1) Stock on hand on 31.3.2012 was valued at Rs. 17,000. 2) 1/8th of the patents are to be written off. 3) Goods of Rs. 7,000 destroyed by fire and insurance company admitted a claim of Rs. 6,100. 4) Rs. 1,000 received on account is commission wrongly included in Ajay’s loan account. 5) Provide 8% Depreciation on Land and building and 5% on Loose Tools. 6) Outstanding expenses were: Salaries Rs. 1,200 Electricity charges Rs. 1,800. 7) Our customer, Mr. Rakesh failed to pay his due of Rs. 1,000.

2 - 35

Partnership Final Account

13. Dhanesh and Ganesh are partners sharing profits and losses in their capital ratio. From the following Trial Balance and adjustments given below, you are required to prepare Trading and Profit and Loss Account for the year ended 31st March, 2011 and Balance Sheet as on that date.

Trial Balance as on 31st March, 2011

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Stock on 1st April, 2010 88,000 Sales 6,40,000Purchases 3,40,000 Sundry Creditors 80,000Return inward 20,000 Bills Payable 72,000Carriage 8,000 Capital A/cs - Dhanesh 1,92,000Motive power 12,000 Ganesh 1,28,000Wages 1,12,000Sundry Debtors 1,44,000Salaries 76,000Insurance 4,800Postage 7,200Commission 10,000Plant and Machinery 1,20,000Furniture 32,000Advertisement 16,000Office Rent (Paid for 10 months) 20,000Buildings 48,000Cash in hand 6,000Bill Receivable 48,000

11,12,000 11,12,000 Adjustments:

1) Closing stock was valued at market price of at Rs. 1,76,000 which is 10% above the cost. 2) Depreciate Plant and Machinery and Building at 20% and 10% respectively. 3) Goods withdrawn by Dhanesh of Rs. 20,000 during the year were not recorded in the books of accounts. 4) Bad debts were Rs. 4,000 and provide for R.D.D. at 5% on Sundry Debtors. 5) Goods worth Rs. 12,000 were purchased and included in closing stock, but not recorded in the books of accounts. 6) Dishonoured Bill Payable of 8,000 was wrongly included in Bills Receivable, however balances of Debtors and

Creditors were taken correctly.

Section II : From the Textbook - Practical Problems :-

1. From the following Trial Balance of M/s. Ajay and Vijay, you are required to prepared Trading and Profit and Loss Account for the year ended 31st March, 2009 and Balance Sheet as on that date.

Trial Balance as on 31st March, 2009

Particulars Debit Amt. (Rs.) Credit Amt. (Rs.)Capital A/c’s - Ajay Vijay

60,00035,000

Purchases and Sales 46,700 85,000Sundry Debtors and Creditors 28,000 25,000Bills Receivable and payable 5,000 6,000Commission 4,600 1,800Opening stock 18,000Wages 9,900Investment 13,500Postage and Telegrams 3,600Insurance 1,200

2 - 36

S.Y.J.C. Book-keeping and Accountancy

Particulars Debit Amt. (Rs.) Credit Amt. (Rs.)Plant and Machinery 40,700Furniture 18,000Cash in hand 2,500Carriage 3,200Bad debts 400Prepaid Rent 7,000Salaries 10,500

2,12,800 2,12,800 Adjustments:

1) The closing stock is valued at Rs. 31,000.

2) Outstanding expenses were wages Rs. 1,400, salaries Rs. 800.

3) Depreciate Plant and Machinery by 10%.

4) Insurance at Rs. 500 is paid in advance.

5) Provide for further bad debts of Rs. 1,500.

6) Commission due but not received Rs. 1,200.

Solution 1:

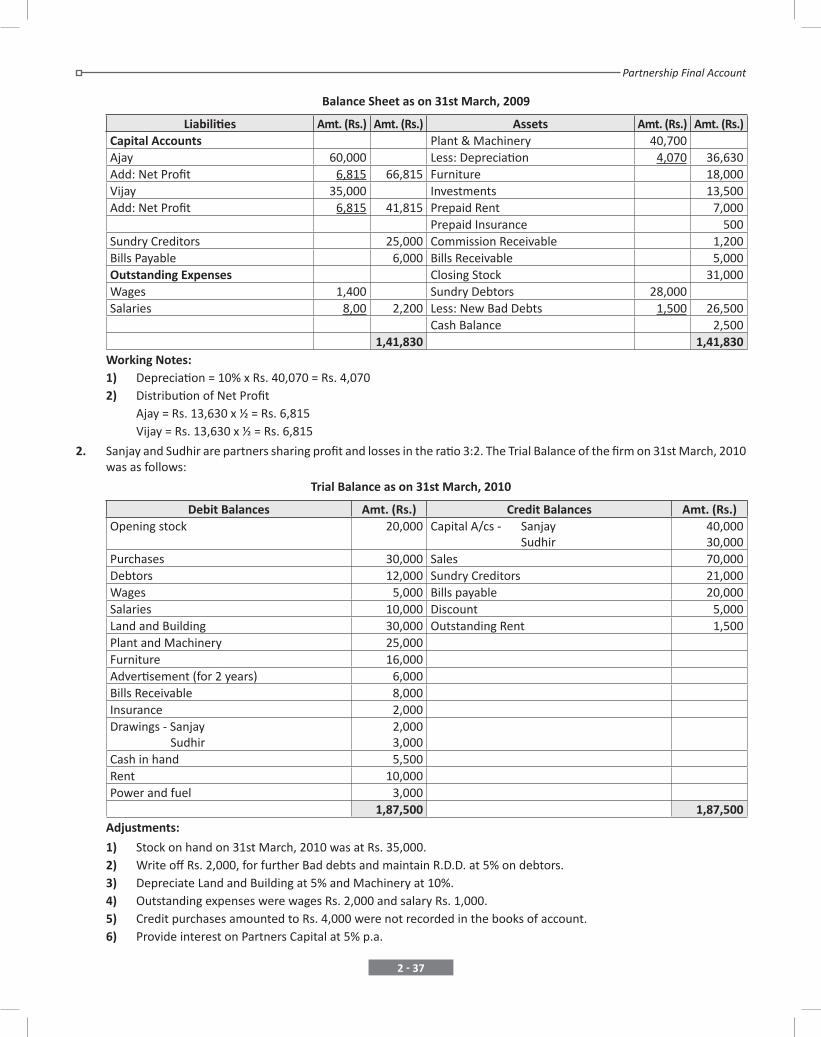

In the books of M/s Ajay and Vijay

Dr. Trading & Profit and Loss A/c for the year ended 31st March, 2009 Cr.

Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)

To Opening Stock 18,000 By Sales 85,000 To Purchases 46,700 To Wages 9,900 Add : O/s wages 1,400 11,300 To Carriage 3,200 By Closing Stock 31,000 To Gross Profit c/d 36,800

1,16,000 1,16,000 To Salaries 10,500 By Gross Profit b/d 36,800 Add : O/s salaries 800 11,300 By Commission 1,800 To Commission 4,600 Add: Commission due but not received 1,200 3,000 To Postage & Telegram 3,600 To Insurance 1,200 Less: Advance 500 700 To Bad debts 400 Add: New Bad debts 1,500 1,900 To Depreciation Plant & Machinery 4,070 To Net Profit c/d Ajay 6,815 Vijay 6,815 13,630

39,800 39,800

2 - 37

Partnership Final Account

Balance Sheet as on 31st March, 2009

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)Capital Accounts Plant & Machinery 40,700Ajay 60,000 Less: Depreciation 4,070 36,630Add: Net Profit 6,815 66,815 Furniture 18,000Vijay 35,000 Investments 13,500Add: Net Profit 6,815 41,815 Prepaid Rent 7,000 Prepaid Insurance 500Sundry Creditors 25,000 Commission Receivable 1,200Bills Payable 6,000 Bills Receivable 5,000Outstanding Expenses Closing Stock 31,000Wages 1,400 Sundry Debtors 28,000Salaries 8,00 2,200 Less: New Bad Debts 1,500 26,500

Cash Balance 2,500 1,41,830 1,41,830

Working Notes: 1) Depreciation = 10% x Rs. 40,070 = Rs. 4,070 2) Distribution of Net Profit Ajay = Rs. 13,630 x ½ = Rs. 6,815 Vijay = Rs. 13,630 x ½ = Rs. 6,815

2. Sanjay and Sudhir are partners sharing profit and losses in the ratio 3:2. The Trial Balance of the firm on 31st March, 2010 was as follows:

Trial Balance as on 31st March, 2010

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Opening stock 20,000 Capital A/cs - Sanjay

Sudhir40,00030,000

Purchases 30,000 Sales 70,000Debtors 12,000 Sundry Creditors 21,000Wages 5,000 Bills payable 20,000Salaries 10,000 Discount 5,000Land and Building 30,000 Outstanding Rent 1,500Plant and Machinery 25,000Furniture 16,000Advertisement (for 2 years) 6,000Bills Receivable 8,000Insurance 2,000Drawings - Sanjay Sudhir

2,0003,000

Cash in hand 5,500Rent 10,000Power and fuel 3,000

1,87,500 1,87,500 Adjustments:

1) Stock on hand on 31st March, 2010 was at Rs. 35,000. 2) Write off Rs. 2,000, for further Bad debts and maintain R.D.D. at 5% on debtors. 3) Depreciate Land and Building at 5% and Machinery at 10%. 4) Outstanding expenses were wages Rs. 2,000 and salary Rs. 1,000. 5) Credit purchases amounted to Rs. 4,000 were not recorded in the books of account. 6) Provide interest on Partners Capital at 5% p.a.

2 - 38

S.Y.J.C. Book-keeping and Accountancy

From the above Trial Balance and adjustments prepare Trading and Profit and Loss Account for the year ended 31st March, 2012 and Balance Sheet as on that date.

Solution 2: Dr. Trading & Profit and Loss A/c for the year ended 31st March, 2012 Cr.

Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)To Opening Stock 20,000 By Sales 70,000 To Purchases 30,000 Add: Unrecorded purchases 4,000 34,000 To Wages 5,000 Add: Outstanding wages 2,000 7,000 To Power & Fuel 3,000 By Closing Stock 35,000 To Gross Profit c/d 41,000 1,05,000 1,05,000 To Commission By Gross Profit b/d 41,000 To Salaries 10,000 By Discount 5,000 Add: Outstanding salaries 1,000 11,000 To Advertisement 3,000 To Insurance 2,000 To Rent 10,000 To Bad debts 2,000 To New RDD 500 To Interest on Capital Sanjay 2,000 Sudhir 1,500 3,500 To Depreciation Plant & Machinery 2,500 Land & Building 1,500 4,000 To Net Profit c/d Sanjay 6,000 Sudhir 4,000 12,000 46,000 46,000

Balance sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)Capital Accounts Land & Building 30,000 Sanjay 40,000 Less: 5% Depreciation 1,500 28,500 Less: Drawings 2,000 Add: Interest on Capital 2,000 Plant & Machinery 25,000 Add: Net Profit 6,000 46,000 Less: 10% Depreciation 2,500 22,500 Sudhir 30,000 Furniture 16,000 Less: Drawings 3,000 Add: Interest on Capital 1,500 Add: Net Profit 4,000 32,500 Closing Stock 35,000 Sundry Creditors 21,000 Sundry Debtors 12,000 Add: Unrecorded purchases 4,000 25,000 Less: New bad debts 2,000 Less: New RDD 500 9,500 Bills Payable 20,000 Bills Receivable 8,000 Outstanding wages 2,000 Prepaid Advertisement 6,000 Outstanding salaries 1,000 Less: Expensed for 1 year 3,000 3,000 Outstanding rent 1,500 Cash in hand 5,500 128,000 128,000

2 - 39

Partnership Final Account

3. Rohan and Roshan are partners in ‘Shan Traders’ sharing profits and losses in the ratio of 2:1. From the following Trial Balance and adjustments prepare Trading and Profit and Loss Account for the year ended 31st March, 2011 and Balance Sheet as on that date.

Trial Balance as on 31st March, 2011

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Opening stock 32,000 Sales 1,93,500Purchases 64,000 Sundry Creditors 15,000Plant and Machinery 30,000 Unpaid wages 1,500Furniture 18,500 Return outward 2,500

Carriage 1,500

Capital A/c - Rohan

Roshan

90,000

50,000Wages and Salaries 35,000Bills Receivable 5,000Sundry Debtors 32,000Conveyance 4,000Rent, Rates and Taxes 2,000Return Inward 3,500Cash in hand 14,750Land and Building 83,500Bad debts 1,750Patents 25,000

3,52,500 3,52,500 Adjustments:

1) Closing stock: Cost price Rs. 25,000 and market price Rs. 30,000.

2) An amount of Rs. 3,500 spent for repairs to Building is debited to Building account.

3) Depreciate Plant and Machinery and Building at 5% p.a.

4) Goods of Rs. 750 taken by Roshan for this personal use.

5) Included in wages advances given to workers Rs. 3,000.

6) Provide Rs. 1,500 for bad and doubtful debts on Debtors.

Solution 3:

In the books of M/s Rohan and Roshan

Dr. Trading & Profit and Loss A/c for the year ended 31st March, 2011 Cr.

Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)

To Opening Stock 32,000 By Sales 1,93,500 To Purchases 64,000 Less : Return inward 3,500 1,90,000 Less: Return outward 2,500 61,500 By Goods taken by Roshan for

personal use 750

To Carriage 1,500 To Wages & Salaries 35,000 Less: Advance 3,000 32,000 By Closing Stock 25,000 To Gross Profit c/d 88,750 2,15,750 2,15,750To Depreciation By Gross Profit b/d 88,750 Plant & Machinery 1,500 Land & Building 4,000 5,500 To Rent, Rates and taxes 2,000

2 - 40

S.Y.J.C. Book-keeping and Accountancy

Dr. Trading & Profit and Loss A/c for the year ended 31st March, 2011 Cr.

Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)

To Repairs 3,500 To New RDD 1,500 To Conveyance 4,000 To Bad debts 1,750 To Net Profit c/d Rohan 47,000 Roshan 23,500 70,500 88,750 88,750

Balance Sheet as on 31st March, 2011

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)Capital Accounts Land & Building 83,500

Rohan 90,000 Less: Repairs wrongly debited 3,500 Less: Drawings - Less: Depreciation 4,000 76,000 Add: Net Profit 47,000 1,37,000

Plant & Machinery 30,000 Roshan 50,000 Less: Depreciation 1,500 28,500 Less: Goods taken for personal use 750 Patents 25,000 Add: Net Profit 23,500 72,750 Furniture 18,500

Sundry Debtors 32,000 Less: New RDD 1,500 30,500 Closing Stock 25,000

Sundry Creditors 15,000 Bills Receivable 5,000 Unpaid wages 1,500 Advance to workers 3,000

Cash in hand 14,750 2,26,250 2,26,250

Working Notes:

1) Repairs wrongly debited to building

Since revenue expenditure has been wrongly capitalised we need to reverse the entry. Hence,

Repairs A/c Dr. 3,500

To Land & Building A/c 3,500

Repairs need to be debited to the profit and loss account.

2) Depreciation on

Plant and Machinery = Rs. 30,000 x 5% = Rs. 1,500

Land & Building (after deducting wrongly debited repairs)

Rs. (83,500 – 3,500) x 5% = Rs. 4,000

3) Closing stock is valued at cost and market price, whichever is less. In this case, it is at cost.

4) Distribution of Profit & Loss

Rohan – Rs. 70,500 x 2/3 = Rs. 47,000

Roshan – Rs. 70,500 x 1/3 = Rs. 23,500

2 - 41

Partnership Final Account

4. Given below is the Trial Balance of M/s Roma and Mona partnership firm. Prepare Trading and Profit and Loss Account for the year ended 31st March, 2012 and Balance Sheet as on that date.

Trial Balance as on 31st March, 2012

Debit Balances Amt. (Rs.) Credit Balances Amt. (Rs.)Stock on 1st April, 2011 52,000 Provident fund 50,000Sundry Debtors 84,000 Interest on P.F. Investment 2,800Bad debts 3,000 Sundry Creditors 84,000Premises 78,000 Rent Received 9,600Salaries 28,000 Reserve for Doubtful Debts 2,000Motor Vehicle 50,000 Discount received 3,600Purchases 1,76,000 Sales 3,20,000Provident Fund Investment 50,000 Capital A/c - Roma 50,000Provident Fund contribution 5,500 Mona 50,000

Wages 22,000Rent (for 10 months) 16,000Office Expenses 5,000Discount allowed 2,500

5,72,000 5,72,000 Adjustments:

1) Stock on 31st March, 2012 was valued at Rs. 80,000.

2) Goods of Rs 6,000 were sold and dispatched on 27th March, 2012, but no entry was made in the books of accounts.

3) Write off Bad debts of Rs. 4,000 and provide for R.D.D. at 5% on sundry debtors.

4) Provide reserve for discount on debtors at 2% and on creditors at 3%.

5) Outstanding wages Rs. 4,000 and outstanding salaries Rs 3,066.

6) Depreciate Motor Vehicle at 5% p.a.

Solution 4:

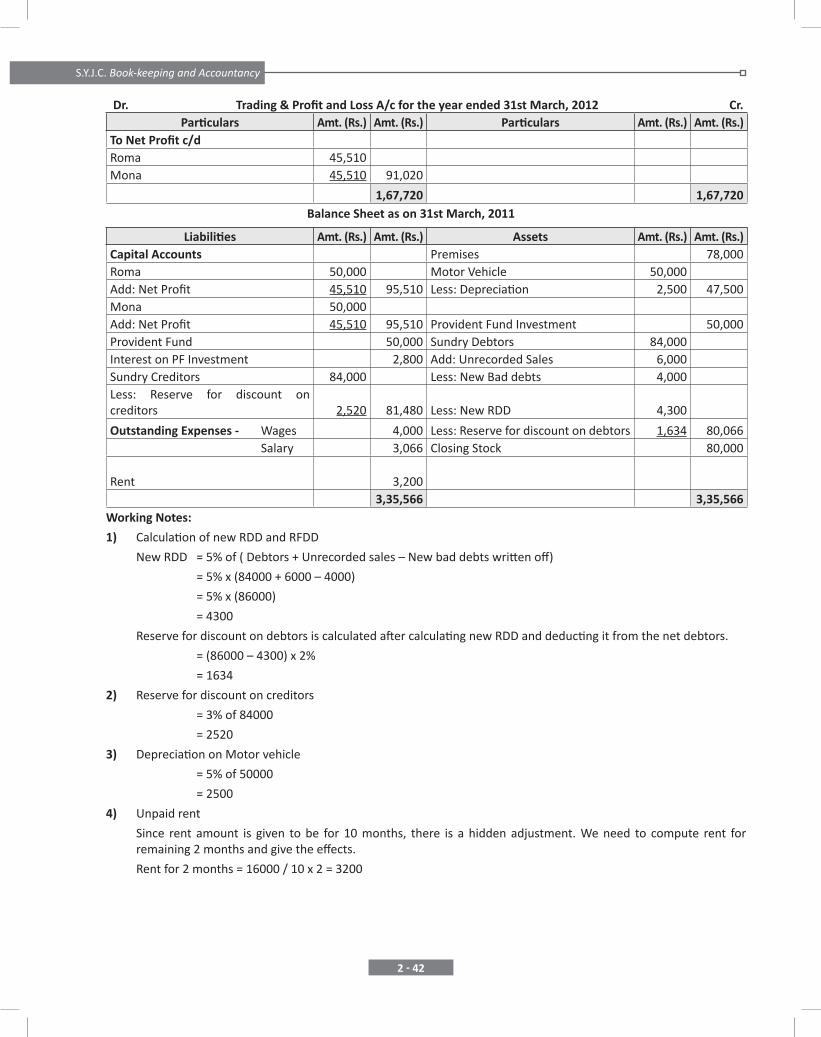

In the books of M/s Roma and Mona

Dr. Trading & Profit and Loss A/c for the year ended 31st March, 2012 Cr.Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)

To Opening Stock 52,000 By Sales 3,20,000 To Purchases 1,76,000 Add: Unrecorded Sales 6,000 326,000 To Wages 22,000 By Closing Stock 80,000Add: Outstanding wages 4,000 26,000 To Gross Profit c/d 1,52,000 4,06,000 4,06,000 To Salary 28,000 By Gross Profit b/d 1,52,000 Add: Outstanding Salary 3,066 31,066 By Rent received 9,600 To Old Bad debts 3,000 By Discount received 3,600 Add: New RDD 4,300 By Reserve for discount on creditors 2,520 Less: Old RDD 2,000 9,300 To Reserve for discount on debtors 1,634 To Depreciation 2,500 To Provident Fund contribution 5,500 To Rent 16,000 Add: Outstanding rent for 2 months 3,200 19,200 To Office expenses 5,000 To discount allowed 2,500

2 - 42

S.Y.J.C. Book-keeping and Accountancy

Dr. Trading & Profit and Loss A/c for the year ended 31st March, 2012 Cr.Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)

To Net Profit c/d Roma 45,510 Mona 45,510 91,020

1,67,720 1,67,720Balance Sheet as on 31st March, 2011

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)Capital Accounts Premises 78,000 Roma 50,000 Motor Vehicle 50,000 Add: Net Profit 45,510 95,510 Less: Depreciation 2,500 47,500 Mona 50,000 Add: Net Profit 45,510 95,510 Provident Fund Investment 50,000 Provident Fund 50,000 Sundry Debtors 84,000 Interest on PF Investment 2,800 Add: Unrecorded Sales 6,000 Sundry Creditors 84,000 Less: New Bad debts 4,000 Less: Reserve for discount on creditors 2,520 81,480 Less: New RDD 4,300

Outstanding Expenses - Wages 4,000 Less: Reserve for discount on debtors 1,634 80,066 Salary 3,066 Closing Stock 80,000 Rent 3,200 3,35,566 3,35,566

Working Notes:

1) Calculation of new RDD and RFDD

New RDD = 5% of ( Debtors + Unrecorded sales – New bad debts written off)

= 5% x (84000 + 6000 – 4000)

= 5% x (86000)

= 4300

Reserve for discount on debtors is calculated after calculating new RDD and deducting it from the net debtors.

= (86000 – 4300) x 2%

= 1634

2) Reserve for discount on creditors

= 3% of 84000

= 2520

3) Depreciation on Motor vehicle

= 5% of 50000

= 2500

4) Unpaid rent

Since rent amount is given to be for 10 months, there is a hidden adjustment. We need to compute rent for remaining 2 months and give the effects.

Rent for 2 months = 16000 / 10 x 2 = 3200

2 - 43

Partnership Final Account

5. From the following Trial Balance of M/s. Kale and Gore, you are required to prepare Trading and Profit and Loss Account for the year ended 31st March, 2013 and Balance Sheet on that date. They share profits and losses in their capital ratio.

Trial Balance as on 31st March, 2013

Debit Balances Amt. (Rs.) Credit Balances Amt (Rs)Opening stock 28,000 Capital A/c- Kale

Gore

80,000

40,000Purchases 1,16,400 Sundry Creditors 54,000Trade Expenses 2,400 Sales 2,12,000Royalties 6,200 Reserve for Doubtful Debts 1,800Wages and Salaries 14,800 Bills payable 36,000Advertisement 8,200Salaries 11,000Plant and Machinery 44,000Freehold Property 36,000Office Rent 4,000Motor Van 63,000Bills Receivable 16,000Sundry Debtors 60,000Cash in hand 10,000Bad debts 1,000General expenses 2,800

4,23,800 4,23,800 Adjustments:

1) Closing stock was valued at cost Rs. 76,000 while its market price was Rs. 80,000.

2) Uninsured goods worth Rs. 10,000 were stolen.

3) Goods worth Rs. 10,000 were sold and delivered on 31st March, 2013, but no entry is passed sales book.

4) Depreciate Plant and Machinery at 10% and Motor van at 15% p.a.

5) Bills Receivable includes a dishonoured bill of Rs. 4,000.

6) Create a reserve for doubtful debts at 5% on Debtors.

Solution 5:

In the books of M/s Kale and Gore

Dr. Trading & Profit and Loss A/c for the year ended 31st March, 2013 Cr.

Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)

To Opening Stock 28,000 By Sales 2,12,000 To Purchases 1,16,400 Add: Unrecorded sales 10,000 2,22,000 To Trade expenses 2,400 By Uninsured goods To Wages and salaries 14,800 Stolen 10,000 To Royalties 6,200 By Closing Stock 76,000 To Gross Profit c/d 1,40,200 3,08,000 3,08,000 To Salaries 11,000 By Gross Profit b/d 1,40,200 To Advertisement 8,200 To Depreciation Plant & Machinery 4,400 Motor Van 9,450 13,850 To Office Rent 4,000

2 - 44

S.Y.J.C. Book-keeping and Accountancy

Dr. Trading & Profit and Loss A/c for the year ended 31st March, 2013 Cr.

Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)

To Bad debts 1,000 Add: New RDD 3,700 Less: Old RDD 1,800 2,900 To General expenses 2,800 To Uninsured goods stolen 10,000 To Net Profit c/d Kale 58,300 Gore 29,150 87,450 1,40,200 1,40,200

Balance Sheet as on 31st March, 2013

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)Capital Accounts Plant & Machinery 44,000 Kale 80,000 Less: Depreciation 4,400 39,600 Add: Net Profit 58,300 1,38,300 Freehold Property 36,000Gore 40,000 Motor Van 63,000 Add: Net Profit 29,150 69,150 Less: Depreciation 9,450 53,550 Sundry Creditors 54,000 Bills Receivable 16,000 Bills Payable 36,000 Less: Dishonoured 4,000 12,000

Sundry Debtors 60,000 Add: Unrecorded Sales 10,000

Add: Bill receivable dishonoured 4,000 Less: New RDD 3,700 70,300 Closing Stock 76,000 Cash in hand 10,000 2,97,450 2,97,450

Working Notes:

1) Depreciation

Plant & Machinery – 10% x 44000 = 4400

Motor Van – 15% x 63000 = 9450

2) Reserve for Doubtful debts

Net Debtors = Debtors + Unrecorded sales + BR dishonoured

= 74000

New RDD = 5% x 74000 = 3700

3) Distribution of Profits

Profit is distributed in the ratio of the outstanding capitals. Since the capitals stand in the ratio of 80000:40000, profit sharing ratio is 2:1.

Kale = 87450 x 2/3 = 58300

Gore = 87450 x 1/3 = 29150.