standard chart of accounts - australian taxation...

TRANSCRIPT

Standard Chart of Accounts For Software Developers Stakeholder Relationship and Management Group

Presented by

Matthew Hay

Assistant Commissioner, Strategic Program

Service Delivery

Australian Taxation Office

22 May 2014

Standard Chart of Accounts 2

Overview Contemporary and tailored service

How SCoA can reduce effort

Key concepts in developing SCoA

The building blocks of SCoA

Leveraging financial reporting

Achieving tax outcomes

XBRL dimensions

Customise your implementation

Where are we up to?

The end state: what are we aiming for?

Standard Chart of Accounts 3

Contemporary and tailored service In future, business taxpayers will experience more contemporary services that will be

streamlined and tailored based on our knowledge of their tax and super affairs.

We will make greater use of business taxpayers’ natural systems to make reporting a by-

product of their day-to-day activities.

We will offer a standardised record keeping and reporting environment that will support

greater transparency of tax and super affairs.

We will reward this transparency with less effort required to comply (“light” or “no touch”

experience) and greater certainty about the status of tax and super affairs.

Standard Chart of Accounts 4

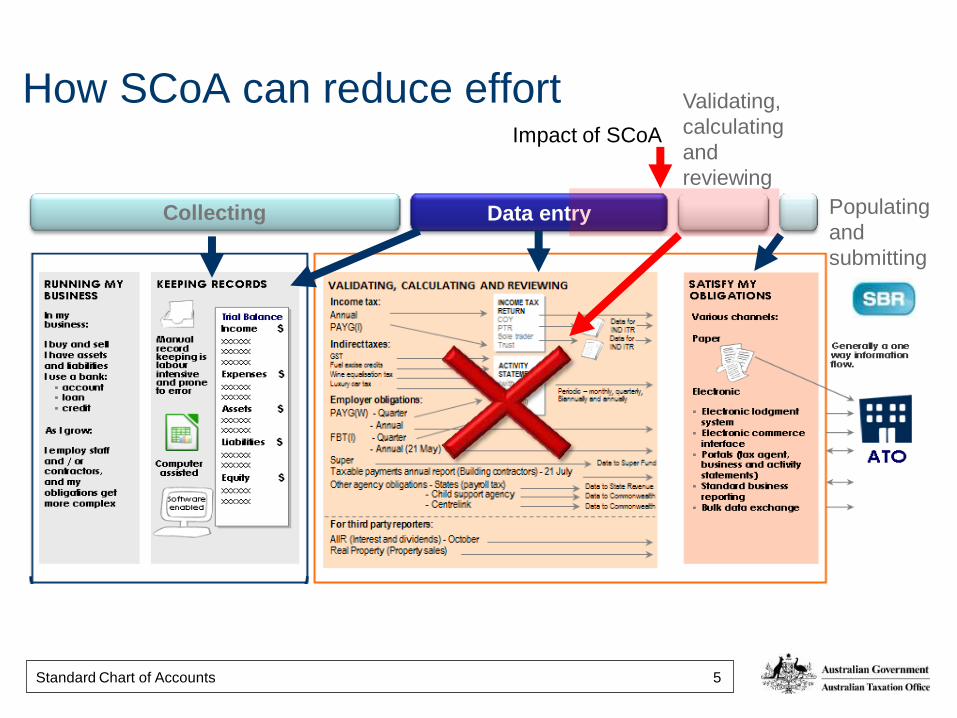

How SCoA can reduce effort

Populating

and

submitting

Validating,

calculating

and

reviewing

Collecting (49%) Data entry (32%) 12% 5%

Data entry (34%)

SCoA

Businesses often undertake a number of steps in financial

reporting to government. These include collecting

data/information, data entry, making calculations,

checking/validating data and populating and submitting reports.

Data is based on 2013 survey of a sample of small businesses, in response to the question: Businesses often undertake a number of steps in financial

reporting for government. These include collecting data/information, data entry, making calculations, checking/validating data and filling in and submitting

the report. Please rank these steps from the most to the least time-consuming/burdensome.

.

Standard Chart of Accounts 5

Data entry

Collecting Data entry

How SCoA can reduce effort

Populating

and

submitting

Validating,

calculating

and

reviewing

Impact of SCoA

Standard Chart of Accounts 6

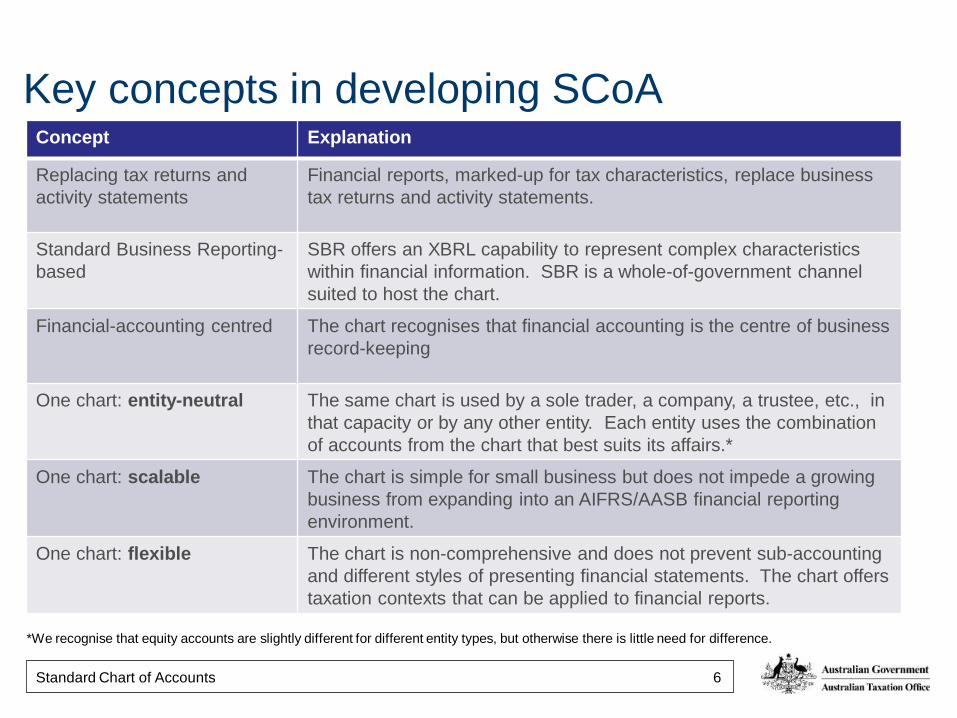

Key concepts in developing SCoA Concept Explanation

Replacing tax returns and

activity statements

Financial reports, marked-up for tax characteristics, replace business

tax returns and activity statements.

Standard Business Reporting-

based

SBR offers an XBRL capability to represent complex characteristics

within financial information. SBR is a whole-of-government channel

suited to host the chart.

Financial-accounting centred The chart recognises that financial accounting is the centre of business

record-keeping

One chart: entity-neutral

The same chart is used by a sole trader, a company, a trustee, etc., in

that capacity or by any other entity. Each entity uses the combination

of accounts from the chart that best suits its affairs.*

One chart: scalable

The chart is simple for small business but does not impede a growing

business from expanding into an AIFRS/AASB financial reporting

environment.

One chart: flexible

The chart is non-comprehensive and does not prevent sub-accounting

and different styles of presenting financial statements. The chart offers

taxation contexts that can be applied to financial reports.

*We recognise that equity accounts are slightly different for different entity types, but otherwise there is little need for difference.

Standard Chart of Accounts 7

The building blocks of SCoA

Example reports

Business guidance

Financial

account

report

elements

Bisected by fixed and optional

taxation characteristics

Validation rules

Concise accounting policies for small

business

element definitions for small business

financial reports

worked examples on ato.gov.au

Sales $400,000

ABC Pty Ltd

[…]

XBRL taxonomy

Closing Assets = Closing Liabilities + Opening

Equity + Equity Increases(Decreases) + Income –

Expenses

Assessable Income – Deductions = Taxable

Income or Net Income

Standard Chart of Accounts 8

Leveraging financial reporting

AASB Conceptual framework

Balance sheet (stmt of fin

position)

P&L (stmt of fin

performance)

SoCiE (stmt of

changes in equity)

Standard chart of accounts Uses conceptual framework to offer

concise, uniform accounting policies for small proprietary companies (and other

non-reporting entities)

ATO XBRL tags

Offers dimensions to ‘tag’ financial accounting information for various

revenue obligations

Line items Assessable

income

Deduction

Revenue $5,000,000 $4,700,000

Cost of sales $3,900,000 $3,700,000

Gross profit $1,100,000

Other expenses $400,000 $50,000

Normalised profit $700,000

Abnormal expenses $40,000 $20,000

Net profit before tax $660,000

Cash flow (stmt of

cash flows)

Small business: A small business chart would be grounded in fundamental accounting

concepts, but with simple accounting policies for both cash and accruals taxpayers.

Standard Chart of Accounts 9

Leveraging financial reporting

AIFRS AASB Conceptual

framework

Balance sheet (stmt of fin

position)

P&L (stmt of fin

performance)

SoCiE (stmt of

changes in equity)

Cash flow (stmt of

cash flows)

Defines accounting policies for non-small proprietary

companies

ATO XBRL tags

Offers dimensions to ‘tag’ financial accounting information for various

revenue obligations

Line items Assessable

income

Deduction

Revenue $50,000,000 $47,000,000

Cost of sales $39,000,000 $37,000,000

Gross profit $11,000,000

Other expenses $4,000,000 $3,500,000

Normalised profit $7,000,000

Abnormal expenses $400,000 $250,000

Net profit before tax $6,600,000

Medium – large business: A chart grounded in the Australian implementation of the International

Financial Reporting Standards is recognised as suitable for medium-large business.

Standard Chart of Accounts 10

Achieving tax outcomes

The use of ‘tax codes’ for GST in many accounting software packages

shows that software already uses financial data in more than one

dimension. These ‘tax codes’ are used to produce reports that would

populate the BAS as a result of journal entries within the software.

XBRL dimensions give us the ability to create a range of tax codes

across different revenue products and to make those ‘codes’ present

in the final report.

If the ATO receives financial reports within a standard-chart format,

then it may be possible to rationalise the number of ‘tax codes’ and

simplify reporting across revenue products.

Standard Chart of Accounts 11

$45,000

$2,000

$12,000

Sales

Purchases

Other inventory

increase (decrease)

Financial Accounting

XBRL dimensions Small business: Financial accounting report elements are the focus of SCoA and its

primary dimension

Standard Chart of Accounts 12

XBRL dimensions Small business

Sales

Purchases

Other inventory

increase (decrease)

Financial Accounting

$2,000

$45,000 $45,000

$12,000

Assessable income

Ordinary Statutory Deduction

Core income tax

Standard Chart of Accounts 13

XBRL dimensions Small business

Sales

Purchases

Other inventory

increase(decrease)

Financial Accounting

Assessable income

Ordinary Statutory Deduction

Core income tax

$45,000

$2,000

$12,000

$20k

$15k

$10k

$5k

$4k

$3k

Taxable supplies/acquisitions

Input taxed supplies/acquisitions

GST free supplies/acquisitions

GST

Standard Chart of Accounts 14

Customise your implementation

The chart is intended to be capable of ‘as is’ implementation for a

variety of businesses.

Developers encouraged to customise implementation of SCoA to

maximise the utility of SCoA to the full range of business taxpayers.

Sub-accounting SCoA line items

Integrate features that populate line items (e.g. fixed assist register to

populate depreciation and gains/losses on the disposal of assets.

Use market specific descriptions for line items within the chart.

Standard Chart of Accounts 15

Where are we up to?

Finalising high level design.

Technically proving SCoA by applying SCoA to existing financial

statements and working papers of small – large businesses.

Preparing to consult and co-design with key stakeholders about:

– How the SCoA concept might be most effectively implemented

– Accounting policies that would apply to small business financial

reports.

Standard Chart of Accounts 16

Digital business, business data kept \in the cloud,

single ledger, single data and messaging standards

The end state: what are we aiming for?

Digital business

ATO

Other third parties

Software developers

Transactions automatically imported, coded and reconciled in near-time. Instant visibility

Over time, more online services wholesaled

Expand SaaS and SCoA-enabled cloud-based solutions

Instant access to business records, tax

treatment applied to transactions on the go

Tax forms no more: One touch payroll and financial statements marked up for tax (SCoA) submitted in place of tax forms directly from software

Businesses

Tax practitioners

Instant access to apply tax

treatment to complex transactions,

assistance “as you go”

Standard Chart of Accounts 17

Questions?

© COMMONWEALTH OF AUSTRALIA 2014

This presentation was current in May 2014.

(02) 9354 3900