starting as a private limited company in nl

TRANSCRIPT

Starting asa Private Limited

Company

byJürgen van de Sande

30 March 2016

Let’s introduce myself

Jürgen van de Sande AA

accountant partner

starting companies and growers SMEsannual reports, fiscal declarationsfinance, structure/organization, acquisitionhuman resources, dwo and accountancy departments

OUR VISION

An entrepreneur’s life is full of important events. Like starting your company, growing or downsizing, cooperating or ending

your business. Each and every choice you make will affect the future of your company.

De Wert is your partner of choice. We have been supporting entrepreneurs since 1959 with accountancy, tax and HR advice, payroll and administrative services. Therefore, no matter what

phase your company is in: rest assured with De Wert.

Introduction De Wert

The first step is the hardest …

Little ones grow

Sometimes it hurts to let go

Program

• General Legal forms in NL Private Company (B.V.) as legal person Establishment requirements Share transfer restrictions Governance Liability Annual report, publication and minutes

• Taxation Corporate Income Tax Wage Tax Income Tax

B.V.

Which legal forms do we know in NL?

stichting

V.O.F. coöperatie N.V.

and more...eenmans-zaak B.V.

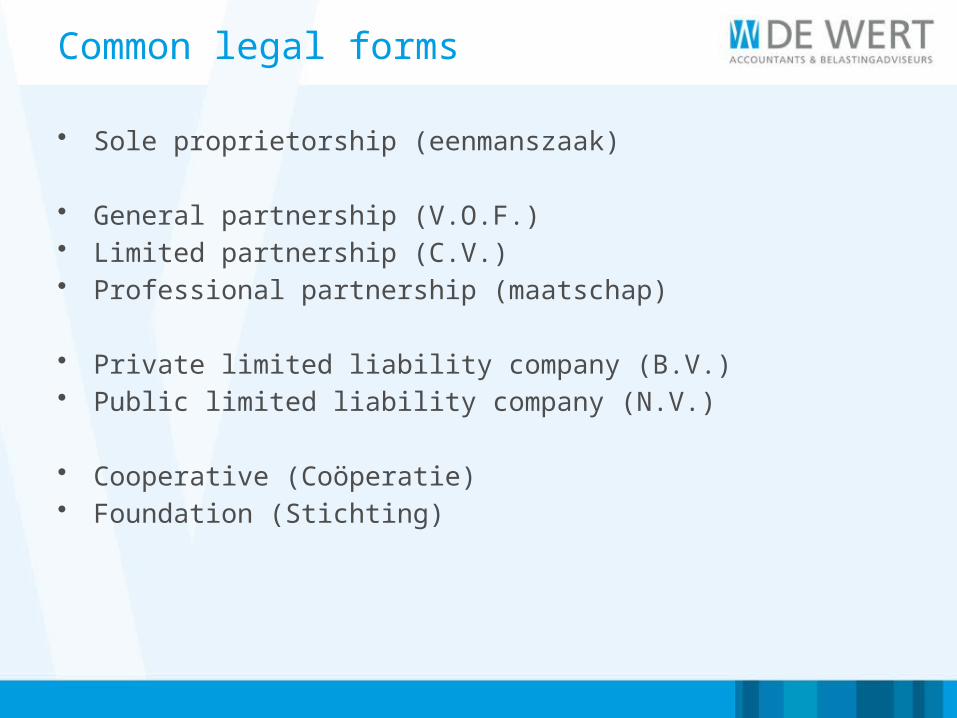

Common legal forms

• Sole proprietorship (eenmanszaak)

• General partnership (V.O.F.)• Limited partnership (C.V.)• Professional partnership (maatschap)

• Private limited liability company (B.V.)• Public limited liability company (N.V.)

• Cooperative (Coöperatie)• Foundation (Stichting)

Choice legal forms

• Income tax• Corporate income tax

• Fully liable• Limited liability

Tax regime versus Liability

Private Company as legal person

• A ‘person’ having rights and obligations

• Incorporation towards third parties

• By one or more persons (shareholders)

Establishment requirements

Requirements:• a notarial deed of incorporation• Dutch language• articles of association• minimum issued share capital € 0,01• appointing executive board• registering at Chamber of Commerce

Options: priority shares preferent shares

Share transfer restrictions

• Shares in a B.V. are always on name

• Share transfer restrictions in articles of association

• Deed of transfer executed before a civil-law notary

Governance

• Board of directors• General Meeting of shareholders• Supervisory board in addition

Board of directors: Responsible for managing the B.V. Appointed and removed by the shareholders Solely or only jointly authorized to represent the company Prior approval for certain acts

Liability

No liability for natural person (director and/or shareholder)

Directors’ liability:• In the formation phase• Up till registration in the Trade Register• Severally liable by mismanagement• Discharge from liability

Directors’ and shareholders’ liability:• Distribution test

Equity test Continue to pay its debts payable (of at least 12 months)

• Reimburse the deficit

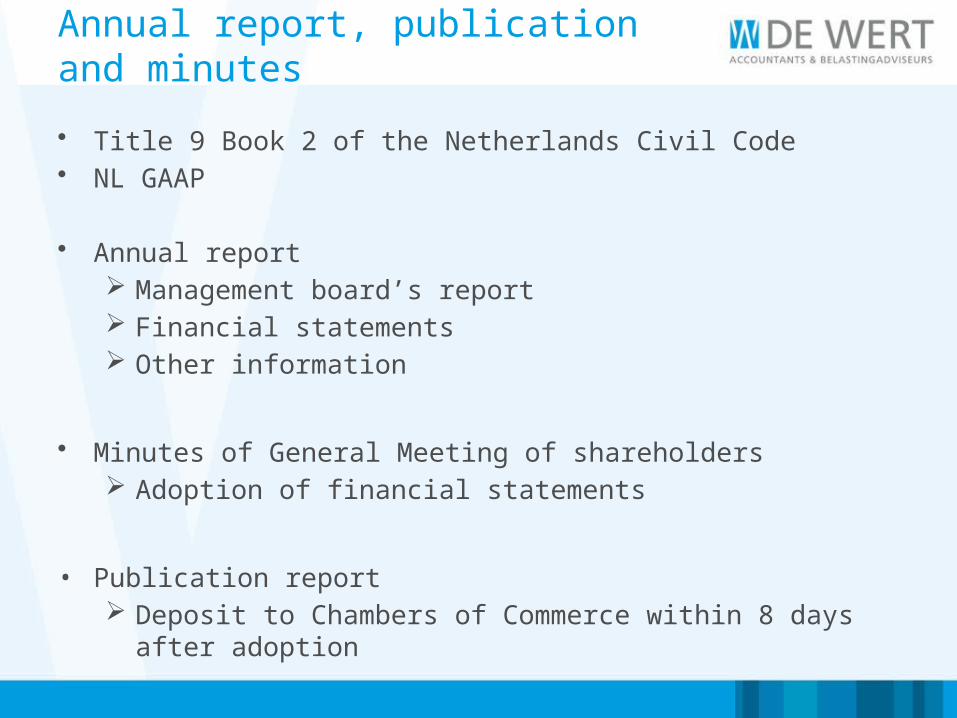

Annual report, publication and minutes

• Title 9 Book 2 of the Netherlands Civil Code• NL GAAP

• Annual report Management board’s report Financial statements Other information

• Minutes of General Meeting of shareholders Adoption of financial statements

• Publication report Deposit to Chambers of Commerce within 8 days after adoption

Taxation

• Corporate income tax • Wage tax• Income tax

Based on Tax Legislation 2016

Corporate income tax (CIT)

Objects

1) Subject to CIT2) Tax base and rates3) Dividend (tax)4) Participation exemption5) Innovation box6) Fiscal unity

Corporate income tax (CIT) #1

Subject to CIT

• CIT is charged to legal entities of which the capital is partially or fully divided into shares

• Examples of such legal entities are the Dutch N.V. and B.V.

Corporate income tax (CIT) #2

Tax base and rates

• CIT is charged on the taxable profits earned by the company in any given year less the deductible losses.

• Deductible losses 1 previous year 9 subsequent years

• The following are the applicable corporate income tax rates for 2016:Profit from Profit up to and including Rate€ 0 € 200k 20%> € 200k 25%

Corporate income tax (CIT) #3

Dividend (tax)

• Pay out profits to the shareholders

• Tax rate is 15%

• Advance tax payment on CIT and income tax

Corporate income tax (CIT) #4

Participation exemption

• To prevent double taxation

• Profit distribution between group companies is exempted from tax

• At least 5% of the nominal paid-in capital of a company is required

Corporate income tax (CIT) #4

Participation exemption

• Example

• Subsidiary B.V. pays out € 50k dividend to Parent B.V.: without participation exemption this benefit would be taxable for Parent B.V.

100%

Parent B.V.

Subsidiary B.V.

dividend € 50k

Corporate income tax (CIT) #5

Innovation box

• For innovative activities Patent Research and development project (WBSO)

• CIT rate for innovative activities 5% Option to declare 25% of the total profit limited to € 25k for 3

years

• Losses on innovative activities can be deducted at the normal CIT rate

Corporate income tax (CIT) #6

Fiscal unity

• Companies effectively established in NL• Same tax regime• Same financial year

≥ 95%

Parent B.V.

Subsidiary B.V.

Wage tax

Salary director/shareholder

• Usual wage settlement (article 12a Wage Tax) A minimum wage of € 44k applies for employees with a

substantial interest in the employer Not applicable when the usual wage is less than € 5k per year

• Others have a higher wage? 75% of that higher usual wage, but at least € 44k The salary of the highest-paid employee

• No profits to pay € 44k salary as a startup? Request for a decision “reducing usual wage”

Wage tax

Salary director/shareholder

• Social security?

Depends on the relation of authority director and/or spouse ≥ 50% votes director and/or 3rd degree ≥ 2/3 shares director cannot be dismissed against his will

Without a relation of authority the director/shareholder cannot rely on the social security insurances

• Advance tax payment on income tax

Income tax

Boxes

Box I: Taxable income from work and home

Box II: Taxable income from substantial interest

Box III: Taxable income from savings and investments (no further explanation)

Income tax: Box I

Taxable income from work and home

• Income from current employment Employment with the B.V. Salary director/shareholder

• Income from providing of assets towards the B.V. Building: rental income Loan: interest income Exemption 12%

• Tax rate is progressive to a maximum of 52%

Income tax: Box II

Taxable income from substantial interest

• Minimum of 5% of the issued capital of shares

• Regular benefits and/or sales benefits Dividend Sale of shares

• Tax rate is 25%

Starting asa Private Limited

Company

So … why?

• Splitting liabilities and risks• Flexibility in operations• Facilitate attracting and distributing funding• Sale of spare parts• Acquire new subsidiaries• Increase opportunities of continuity

Questions?