statewide economic impact report

DESCRIPTION

NAIOP Colorado is proud to announce the publication of its inaugural study on the impact of commercial real estate on Colorado\'s economy. A joint study by the University of Colorado and the University of Denver finds that the commercial real estate sector accounts for more than 10 percent of Colorado\'s economy. Commercial real estate generated $23.4 billion in 2006 economic impact, with almost 70 percent coming from existing properties.TRANSCRIPT

Submitted by

University of Colorado Real Estate Center Thomas G. Thibodeau Ph.D. -Academic DirectorBrian Lewandowski - MBA, Leeds School of Business

University of Denver, Franklin L. Burns School of Real Estate & Construction ManagementGlenn R. Mueller Ph.D. - ProfessorAndrew G. Mueller, MSRECM candidate,Burns School of RECM

McGraw Hill Construction Research & Analytics

Real Capital Analytics, Inc.

Colorado’s Commercial Real Estate IndustryStatewide Economic Impact Report

Research sponsored by:

National Association ofIndustrial and Office Properties

The Forum for Commercial Real Estate

Colorado Chapter

Submitted by

University of Colorado Real Estate Center Thomas G. Thibodeau Ph.D. -Academic DirectorBrian Lewandowski - MBA, Leeds School of Business

University of Denver, Franklin L. Burns School of Real Estate & Construction ManagementGlenn R. Mueller Ph.D. - ProfessorAndrew G. Mueller, MSRECM candidate,Burns School of RECM

McGraw Hill Construction Research & Analytics

Real Capital Analytics, Inc.

NAIOP Colorado Chapter1720 S. Bellaire Street, Suite 110

Denver, CO 80222-4303Ph: (303) 782-0155Fax: (303) 820-3844

www.naiop-colorado.org

Research sponsored by

Colorado’s Commercial Real Estate IndustryStatewide Economic Impact Report

The National Association of Industrial and Office Properties is thenation’s leading trade association for developers, owners, investors andother professionals in industrial, office, retail and mixed-use commercialreal estate. Founded in 1967, NAIOP comprises 15,000+ members in 54chapters throughout North America. NAIOP provides networking oppor-tunities, educational programs, research on trends and innovations andstrong legislative representation.

The Colorado Chapter includes over 700 members. Our monthly breakfast meetings are open to non-members.

If you are involved with commercial real estate in Colorado (includingoffice, industrial, retail, mixed use, etc.) as a developer, owner or investoror affiliated service provider, then you should be involved with us!

©2008 National Association of Industrial and Office Properties ColoradoChapter. All Rights Reserved.

Is is important to remember that the data collection measures includedin this report should be regarded as guidelines rather than as absolutestandards. The information readily available may differ according to thegeographic area in question, and results may vary accordingly. Local andregional economic performance is a key factor. Further study and evalua-tion are recommended before any investment decisions are made.

This project is intended to provide information and insight to industrypractitioners and does not constitute advice or recommendations.NAIOP Colorado disclaims any liability for action taken as a result of thisproject and its findings.

About NAIOP

Preface

Foreward

i

List of Tables / List of Figures ................................................................iiList of Appendices..................................................................................iiiExecutive Summary ................................................................................1Introduction ............................................................................................5

Commercial and Multifamily Property in Colorado: 1967-2006 ........7Methodology ........................................................................................10Economic Impacts of Existing Commercial Property ..........................11

Total Area ..........................................................................................11Summary of Impacts for Existing Commercial Properties ................12

Existing Office Properties ..............................................................13Existing Industrial Properties..........................................................14Existing Retail Properties ..............................................................15Existing Hotel Properties................................................................16

Economic Impacts of Tenant Improvements ........................................17Summary of Tenant Improvements Impacts ......................................17

Office Property Tenant Improvements ..........................................18Industrial Property Tenant Improvements ......................................18Retail Property Tenant Improvements............................................19Hotel Property Tenant Improvements ............................................19Multifamily Property Tenant Improvements ..................................20

Economic Impacts of New Construction ..............................................21Summary of Impacts for New Construction ......................................21

Office Property New Construction ................................................22Industrial Property New Construction............................................22Retail Property New Construction..................................................23Hotel Property New Construction..................................................23Multifamily Property New Construction ........................................24

Economic Impacts of Commercial Property Transactions ....................25Economic Impacts of Commercial Property Refinancing ....................26Fiscal Impacts ........................................................................................27

Commercial Property Taxes ..............................................................27Commercial Property Sales Taxes......................................................28

Conclusion ............................................................................................28

Table of Contents

ii

Table 1: Economic Impacts of Commercial Real Estate and Multifamily Construction on Colorado’s Economy....................................................................................2

Table 2: Colorado Real Estate Regions ..................................................................................................................6Table 3: Existing Property, Square Feet (000), by Region, 2006 ..........................................................................12Table 4: Economic Impacts of Existing Commercial Property, by Region, 2006 ................................................13Table 5: Economic Impacts of Existing Office Real Estate, by Region, 2006 ......................................................14Table 6: Economic Impacts of Existing Industrial Real Estate, by Region, 2006..................................................15Table 7: Economic Impacts of Existing Retail Real Estate, by Region, 2006 ......................................................16Table 8: Economic Impacts of Existing Hotel Real Estate, by Region, 2006........................................................17Table 9: Economic Impacts of Tenant Improvements, by Region, 2006 ..............................................................18Table 10: Economic Impacts of Office Tenant Improvements, by Region, 2006 ..................................................18Table 11: Economic Impacts of Industrial Tenant Improvements, by Region, 2006 ..............................................19Table 12: Economic Impacts of Retail Tenant Improvements, by Region, 2006 ....................................................19Table 13: Economic Impacts of Hotel Tenant Improvements, by Region, 2006 ....................................................20Table 14: Economic Impacts of Multifamily Tenant Improvements, by Region, 2006 ..........................................20Table 15: Economic Impacts of New Construction, by Region, 2006 ....................................................................21Table 16: Economic Impacts of Office Construction, by Region, 2006..................................................................22Table 17: Economic Impacts of Industrial Construction, by Region, 2006 ............................................................22Table 18: Economic Impacts of Retail Construction, by Region, 2006 ..................................................................23Table 19: Economic Impacts of Hotel Construction, by Region, 2006 ..................................................................23Table 20: Economic Impacts of Multifamily Construction, by Region, 2006..........................................................24Table 21: Total Commercial Property Transaction Volume, in 000s, by Region, 2006 ..........................................25Table 22: Total Commercial Property Transaction Fees, in 000s, by Region, 2006 ..............................................25Table 23: Total Commercial Property Refinancing Volume, in 000s, by Region, 2006 ..........................................26Table 24: Total Commercial Property Refinancing Fees, in 000s, by Region, 2006 ..............................................26Table 25: Colorado Assessed Property Value and Estimated Taxes, 000s, by Region, 2006 ................................27Table 26: Summary Impacts of Commercial Real Estate and

Multifamily Construction on Colorado’s Economy, 2006........................................................................29Table 27: Per Square Foot Office Property Operating Expenses ..........................................................................32Table 28: Per Square Foot Retail Property Operating Expenses ..........................................................................33Table 29: Industrial Property Operating Expenses, 2006 Estimates ......................................................................33Table 30: Denver-Boulder-Greeley CPI ..................................................................................................................34Table 31: Construction and Tenant Improvements Soft Costs Estimates ..............................................................35

Figure 1: Impacts of Commercial Real Estate and Multifamily Construction on Colorado Regions, 2006 ............3

Figure 2: Direct Spending Per Employee, 2006 ......................................................................................................3

Figure 3: Per Capita Impacts of Commercial Real Estate and Multifamily

Construction on Colorado Regions, 2006 ................................................................................................4

Figure 4: Map of Colorado Real Estate Regions......................................................................................................6

Figure 5: Colorado Commercial and Multifamily Construction, 1967-2006 ............................................................7

Figure 6: Colorado Commercial and Multifamily Property Stock, 1970-2006 ........................................................7

Figure 7: Colorado Commercial and Multifamily Construction Value Versus GDP, 1967-2006 ..............................8

Figure 8: Colorado Commercial and Multifamily Construction as a Percent of GDP, 1967-2006 ..........................9

Figure 9: Colorado Property Tenant Improvements, 1967-2006 ............................................................................9

List of Tables

List of Figures

iii

Appendix A: Economic Impacts, by County, 2006 ..................................................................................................30

Appendix B: Notes to Methodology........................................................................................................................31

Appendix C: RIMS II Colorado Regions ..................................................................................................................36

Appendix D: Supply of Existing Commercial and Multifamily Property

(000s sf), by Property Type, by County, 2006 ....................................................................................37

Appendix E: Economic Impacts of Existing Commercial Property, by County, 2006..............................................38

Appendix F: BOMA Office Expense Definitions ......................................................................................................39

Appendix G: Economic Impacts of Existing Office Real Estate, by County, 2006 ..................................................40

Appendix H: Economic Impacts of Existing Industrial Real Estate, by County, 2006..............................................41

Appendix I: Urban Land Institute Retail Expense Definitions ................................................................................42

Appendix J: Economic Impacts of Existing Retail Real Estate, by County, 2006 ..................................................43

Appendix K: Economic Impacts of Existing Hotel Real Estate, by County, 2006....................................................44

Appendix L: Economic Impacts of Tenant Improvements, by County, 2006 ..........................................................45

Appendix M: Economic Impacts of Office Tenant Improvements, by County, 2006................................................46

Appendix N: Economic Impacts of Industrial Tenant Improvements, by County 2006 ..........................................47

Appendix O: Economic Impacts of Retail Tenant Improvements, by County, 2006 ................................................48

Appendix P: Economic Impacts of Hotel Tenant Improvements, by County, 2006 ................................................49

Appendix Q: Economic Impacts of Multifamily Tenant Improvements, by County, 2006........................................50

Appendix R: Economic Impacts of New Construction, by County, 2006 ................................................................51

Appendix S: Economic Impacts of Office Construction, by County, 2006..............................................................52

Appendix T: Economic Impacts of Industrial Construction, by County, 2006 ........................................................53

Appendix U: Economic Impacts of Retail Construction, by County, 2006 ..............................................................54

Appendix V: Economic Impacts of Hotel Construction, by County, 2006 ..............................................................55

Appendix W: Economic Impacts of Multifamily Construction, by County, 2006......................................................56

Appendix X: Colorado Assessed Property Value and Estimated Taxes, by County, 2006 ......................................57

Appendix Y: Assessed Valuation, Revenue, and Average Levies by County, 2006 ................................................59

List of Appendices

1

The commercial real estate industry impacts the Colorado economy ina variety of ways. The industry purchases construction and buildingmaintenance materials from Colorado suppliers and provides jobs forColorado residents. Existing income-producing properties providepermanent jobs maintaining, managing, and leasing property. Newconstruction and tenant improvements employ construction workers,architects, and engineers. Income-producing property transactions andrefinancing provide employment in the brokerage, financing, and legalprofessions. Finally, revenues generated by property and sales taxesare important sources of financing public services.

Activities in the commercial and multifamily property sectors have twomeasurable impacts on Colorado’s economy. First, income-producingproperty spending has direct impacts on the State’s output, earnings,and employment. Second, each dollar spent in the Colorado realestate industry has an indirect, or multiplier, effect on the Coloradoeconomy. The indirect influence of real estate spending occurs whenmoney spent on real property is used to purchase other goods andservices in the State. For example, real estate employees spend wagesearned in their jobs on housing, food, clothes, entertainment and othergoods and services in Colorado. These expenditures create moreemployment and increase output in other industries.

This report estimates the direct and indirect impacts that income-producing property has on the Colorado economy. Economic impactsare reported separately for existing properties, for tenantimprovements, new construction, transactions, refinancing, and for thefiscal impacts of property and sales taxes. Economic impacts arereported for the entire State of Colorado, for eight regions in Coloradoand for each county.

Direct income-producing property spending was estimated at $12.3 billion in 2006, or 5.4% of Colorado’s economy. The total (direct andindirect) economic impact that income-producing properties had onthe State’s output totaled $24.3 billion in 2006, or 10.5% of Colorado’seconomy. In 2006, there were 137,832 direct employees servicingColorado’s income-producing property sector, earning an annualaverage income of $32,832. Total 2006 employment (direct plusindirect) in the State attributable to income-producing property was254,976, with employees earning an average annual wage of $32,177(Table 1). Most of the economic impact ($16.1B of the $24.3B) wasgenerated by existing income-producing properties. Office and hotelproperties account for nearly 76% of this contribution. New income-producing construction contributed $3.3B in direct spending and $6.9Bin total output (direct plus indirect economic impacts). See Appendix Afor county specific impacts of existing, tenant improvements, andconstruction.

Executive Summary

2

Existing2

Office 3,377,771 7,026,103 1,386,691 2,509,433 38,973 74,756

Industrial 301,387 623,368 132,039 230,295 3,293 6,449

Retail 1,574,128 3,256,520 705,653 1,219,051 18,627 35,106

Hotel 2,881,556 5,158,947 984,274 1,663,087 45,793 67,255

Total Existing 8,134,842 16,064,938 3,208,657 5,621,866 106,686 183,566

Tenant Improvements

Office 96,426 212,582 35,339 72,056 840 1,995

Industrial 14,693 33,231 5,367 11,261 128 312

Retail 94,036 211,932 34,496 71,906 820 1,987

Hotel 112,504 248,651 40,974 84,157 974 2,321

Multifamily 27,195 60,587 10,016 20,616 238 571

Total TI 344,854 766,983 126,192 259,996 3,000 7,186

New Construction

Office 465,385 1,008,333 170,534 341,997 4,054 9,478

Industrial 517,969 1,091,131 190,880 371,999 4,560 10,386

Retail 536,406 1,179,158 196,923 400,545 4,681 11,080

Hotel 313,518 574,134 109,816 189,096 2,608 5,249

Multifamily 1,431,905 3,016,571 522,341 1,018,760 12,242 28,031

Total Construction 3,265,183 6,869,327 1,190,494 2,322,397 28,145 64,224

Other3

Construction Period

Interest/Fees 137,294 137,294 - - - -

Transactions 411,408 411,408 - - - -

Refinancing 47,093 47,093 - - - -

Total Other 595,795 595,795 - - - -

Total All 12,340,674 24,297,043 4,525,343 8,204,259 137,832 254,976

1Employment refers to the number of workers, both full time and part time. 2Existing does not include multifamily.3Other does not include multifamily, nor the impact on employment, earnings, multiplier effect, or impact on individual counties due to the uncertainty of the source of, and redeployment of funds.

Sources: McGraw-Hill Construction Research & Analytics, 2007; BOMA International, Experience Exchange Report 2007; Urban Land Institute, Dollars & Cents ofShopping Centers / The SCORE 2006; PKF Hospitality Research; NAIOP Industrial Income and Expense Report 2001-2002; Real Capital Analytics; NorthMarq Capital; University of Colorado-Boulder; University of Denver

Table 1: Economic Impacts of Commercial Real Estate and Multifamily Construction on Colorado’s Economy

Direct Spending

(000)Total Output

(000)Direct Earnings

(000)Total Earnings

(000)Direct

Employment1

Total Employment

The impact of income-producing property was highly variable by region, with the greatest impactslocated in the Denver Metro, North Front Range, and Mountain Resort regions, tallying 79.3% of thetotal impact collectively (Figure 1).

3

Figure 1: Impacts of Commercial Real Estate and Multifamily Construction on Colorado Regions, 2006

* Regions exclude the refinancing and transaction impacts because these impacts were measured at the state level, but not the county or regional level.

Average direct spending per income-producing real estate employee was $85,212, with a regional standard deviationof $8,613 (10.1%) (Figure 2). The Denver Metro region accounted for nearly 53.2% of direct spending, and thereforegreatly impacted the average.

Figure 2: Direct Spending Per Employee, 2006

4

The per capita impacts of income-producing property on Colorado regions were highly variable in 2006, with thegreatest impact at $16.35 per person occurring in the Mountain Resort region (Figure 3). Naturally, areas with higherlevels of income-producing property activity and comparably smaller populations will have larger per capita impacts, asis true in the Mountain Resort and Pueblo regions. The average per capita impact for the eight regions was $4.34.

Figure 3: Per Capita Impacts of Commercial Real Estate and Multifamily Construction on Colorado Regions, 2006

County Population Source: U.S. Census Bureau, www.census.gov, as of September 26, 2007.

5

I. Introduction

At the request of the Colorado Chapter of the National Association ofIndustrial and Office Properties (NAIOP), the University of Colorado-Boulder and the University of Denver collaboratively analyzed the economic impacts of income-producing property on Colorado’seconomy in 2006.

Income-producing property is undoubtedly a major contributor to theColorado economy in terms of output, employment, and wages. Thisreport defines commercial property as office, industrial, retail, and hotel.Income-producing property is commercial and new multifamilyconstruction. It estimates the economic and fiscal impacts of the income-producing property industry on output, earnings, and employment.

Economic impacts are reported for the entire State of Colorado andseparately by region based on economic and geographic similaritiesidentified in the 2006 publication “Economic Contributions of RealEstate Activity and Value in Colorado” produced by the BusinessResearch Division of the Leeds School of Business at the University ofColorado-Boulder (Table 2 and Figure 4). The appendices provideindividual county impacts. Impacts for Broomfield County are notreported separately due to the inauguration of county status in 2001.Since Broomfield County was created from land located in Adams,Boulder, Jefferson, and Weld counties, the impacts that income-producing property had in Broomfield County are included in thesefour counties.

The income-producing property industry contributes to the Coloradoeconomy by purchasing goods and services from Colorado suppliersand by providing jobs throughout the lifecycle of a property. From the time an income-producing property is conceived by a developer,lawyers, architects, engineers, and a host of other real estateprofessionals become involved in the planning of the building, thesurrounding land, and the public and private infrastructure required tosupport the development. During the construction phase, an even largergroup of professionals are called to action, from builders to constructionmanagers orchestrating numerous construction trades, includingcarpenters, steel workers, plumbers, electricians, landscape architects,heavy equipment operators, concrete specialists, and many more.Finally, once construction is complete, the property employs another setof individuals to keep the building operating, including leasing agents,financiers, maintenance workers, and property managers.

6

Figure 4: Map of Colorado Real Estate Regions

Source: Business Research Division, Leeds School of Business.

The total economic impact of income-producing property spending on the Colorado economy is estimated in twoparts. First, spending has a direct contribution to output, earnings, and employment. Employment refers to the number of employees, both full time and part time. Spending also has an indirect, or multiplier, effect on the economybecause the dollars spent (or earned) in income-producing property are used to purchase other goods and services inthe state. This multiplier effect is measured using the U.S. Department of Commerce, Bureau of Economic Analysis’s(BEAs) Regional Input-Output Modeling System (RIMS) II multipliers. These multipliers estimate the influence ofspending in one or more industries on output, earnings, and employment in other industries. The multipliers areproduced by BEA using data on the local area personal income and the national input-output accounts.

This report captures a snapshot of the lifecycle of income-producing property for the State of Colorado in 2006.

Table 2: Colorado Real Estate Regions

Region Counties

North Front Range Boulder, Weld, and Larimer CountiesGrand Junction Mesa CountyDenver Metro Denver, Arapahoe, Adams, Broomfield, Douglas, and Jefferson CountiesEastern Plains Baca, Bent, Cheyenne, Crowley, Elbert, Huerfano, Kiowa, Kit Carson, Las Animas, Lincoln, Logan, Morgan,

Otero, Phillips, Prowers, Sedgwick, Washington, and Yuma CountiesMountain Resort Eagle, Pitkin, Routt, San Miguel, Summit, Garfield, and Grand CountiesPueblo Pueblo CountyColorado Springs El Paso and Teller CountiesMountain Rural Alamosa, Archuleta, Chaffee, Clear Creek, Conejos, Costilla, Custer, Delta, Dolores, Fremont, Gilpin,

Gunnison, Hinsdale, Jackson, La Plata, Lake, Mineral, Moffat, Montezuma, Montrose, Ouray, Park, RioBlanco, Rio Grande, Saguache, and San Juan Counties

Source: Business Research Division, Leeds School of Business

7

A. Commercial and Multifamily Property in Colorado: 1967-2006The commercial and multifamily construction industries have added more than one billion square feet of office,industrial, retail, hotel and multifamily space in Colorado since 1967. Construction has traversed through three majorcycles over 30 years, and it is currently in its fourth. The first cycle started in the 1960s and peaked in 1973. The nextcycle bottomed out in 1975 and peaked in 1984, fueled by office construction. The third cycle bottomed in 1991, withthe slowest construction expansion in the 30-year period, which was followed by 10 years of increasing constructionactivity. Colorado is currently in another cycle that bottomed in 2003 and is now moving toward another peak (Figure 5).

Figure 5: Colorado Commercial and Multifamily Construction, 1967-2006

Sources: McGraw-Hill Construction Research & Analytics, Bureau of Economic Analysis

The total stock of income-producing property increased at a 2.84% compound annual growth rate from 1970 to 2006.The total stock naturally tracks the construction of new income-producing property as it is the product of existing, new,and decommissioned properties. In 2006, income-producing property, including office, industrial, retail, hotel, and multifamily, totaled nearly 1.35 billion square feet in Colorado, compared to 491.3 million in 1970 (Figure 6).

Figure 6: Colorado Commercial and Multifamily Property Stock, 1970-2006

Source: McGraw-Hill Construction Research & Analytics

8

The rate of income-producing property construction and the growth rate of the Colorado economy are closely linked,with a correlation of 0.79 from 1967 to 2006 (Figure 7). Over time, the major drivers of Colorado’s economy have alsochanged, with manufacturing representing 16.5% of Colorado’s GDP in 1967, compared to 6.5% in 2006. Conversely,Professional Business Services is now a major underpinning of the Colorado economy, representing 13.7% of 2006State GDP.

Figure 7: Colorado Commercial and Multifamily Construction Value Versus GDP, 1967-2006

Sources: McGraw-Hill Construction Research & Analytics, Bureau of Economic Analysis

Real estate is one of the three basic “factors of production” (land, labor, and capital) required for virtually all economicactivities. When new jobs are created in the state, greater demand is placed on places to eat, work, shop, play, and sleep.

From 1967 to 2006, commercial and multifamily property construction has gone through four extended growth periods(including the current cycle). Peak construction as a percent of GDP occurred in 1972, comprising 4.9% of GDP (Figure8). Conversely, at 0.37%, 1991 brought the lowest contribution of GDP from construction. Income-producing propertyconstruction’s 30-year average contribution to Colorado’s GDP is 2.0%, signaling that the 1.4% of State GDP in 2006was an underperforming year overall.

Figure 8: Colorado Commercial and Multifamily Construction as a Percent of GDP, 1967-2006

Source: Bureau of Economic Analysis, University of Colorado-Boulder, University of Denver.

In addition to income-producing property construction, expenditures on tenant improvements are a major contributorto local and state economies. From 1996 to 2006, tenant improvements have averaged $262 million annually inColorado (Figure 9).

Figure 9: Colorado Tenant Improvements, 1967-2006

Source: McGraw-Hill Construction Research & Analytics.

9

10

With the continued growth in population and employment, thedemand for income-producing property is expected to continue toremain strong, with the natural cycles inherent to the industry.

II. Methodology

The base methodology for this report was obtained from the NAIOPpublication “How to Calculate the Economic Contribution of Office,Industrial and Retail Real Estate to the Local Community” by StephenS. Fuller, Ph.D., George Mason University (2007). This study builds onthe NAIOP methodology by including commercial tenantimprovements, commercial transaction costs and commercial financingcosts. For greater detail regarding the methodology, see Appendix B.

Data from McGraw-Hill Construction Research & Analytics on the totalsquare feet of existing commercial real estate for each property typewere employed, along with data on specific property-type operatingexpenses to estimate aggregate spending and employment foroperations, maintenance, management, and utilities. McGraw-HillConstruction Research & Analytics data on square feet of newconstruction, by property type, along with data on per square footconstruction costs obtained from R. S. Means, were used to estimatethe value of new construction. Data on tenant improvements were alsoprovided by McGraw-Hill Construction Research & Analytics.

RIMS II multipliers, obtained from the BEA through the StateDemography Office, provided the basis for estimating directemployment and earnings based on direct spending, as well as theindirect output, employment, and earnings.

BEA publishes RIMS II multipliers by industry sector and by economicregion in Colorado (Appendix C). This study employs the multipliersthat include the impact of local government. Multipliers are reportedfor output, earnings, and employment. For instance, if the utilitiesindustry output multiplier is 2.1365 for the State of Colorado, then theimpact of $1 million in utilities spending on Colorado’s economy is$2.1365 million ($1 million direct spending and $1.1365 millionindirect). Direct earnings can be estimated using the BEA directearnings per dollar of sales to final demand multiplier, which in thisscenario is 0.1808. Therefore, the $1 million in utilities spendinggenerates $180,800 in direct earnings. Similarly, employment can beestimated using the direct employment per million dollars of sales tofinal demand multiplier. The employment multiplier in this example is2.2577. That means there are 2.2577 jobs generated for every $1million in utility expenditures. It should be noted that the estimatedmultiplier impacts on specific counties are estimates and are moreaccurate in non-metropolitan areas. The difficulty estimatingmetropolitan county multiplier effects is because metropolitan areas

11

have greater economic overlap since goods and labor are oftenprovided from neighboring counties; and commuting employees spenda higher proportion of their earnings near their home. The multipliereffects in this report assume that the economic activities from income-producing property in a county are proportional to the area of income-producing property in that region.

The economic impacts of income-producing property transactions andrefinancing were estimated on a direct basis only. The indirect, or multiplier, effect is omitted because of the difficulty in knowing howmuch of the interest and fee income is spent in Colorado. Fiscalimpacts are based on State of Colorado reported estimates of assessedincome-producing property values and estimated property mill levies ineach county.

III. Economic Impacts of Existing Commercial Property

Existing commercial property undoubtedly has a profound impact onthe Colorado economy in terms of output, earnings, and employmentderived from operating expenditures. These operating expendituresinclude a variety of services, such as management, cleaning, repairs,maintenance, leasing, expenditures on utilities, and so on, that keepthe property functioning.

To assess these impacts, data has been gathered from numerous publicand private sources. Necessary data included existing income-producing property area in square feet by type and by county,operating expenditures per square foot, and industry economicmultipliers. The economic impact of tenant improvements andconstruction of new properties are examined in a later section.

A. Total AreaIn 2006, the three major metropolitan areas in Colorado (DenverMetro, North Front Range, and Colorado Springs) contained 83.5% ofthe existing commercial and multifamily stock in Colorado, with nearly1.13 billion square feet of income-producing property. The DenverMetro region alone represented 57.2% of the existing stock of income-producing property. Table 3 provides total income-producing propertyspace, by property type, for each of the eight regions in the State.Individual county estimates are provided in Appendix D.

12

B. Summary of Impacts for Existing Commercial PropertiesDirect spending in the existing inventory of all commercial properties totaled $8.1 billion in 2006, for a total (direct andindirect) effect of $16.1 billion on Colorado’s economy, or 7.0% of State GDP (Table 4)1. For existing real estate, directspending generally includes operating costs associated with the administration, cleaning, maintenance, utilities, andtaxes on the properties. The existing income-producing property sector employed 106,686 direct employees earningan average wage of $30,076. The 183,566 direct and indirect employees earned an average wage of $30,626. SeeAppendix E for county impact.

1 The analysis of existing property does not include multifamily.

13

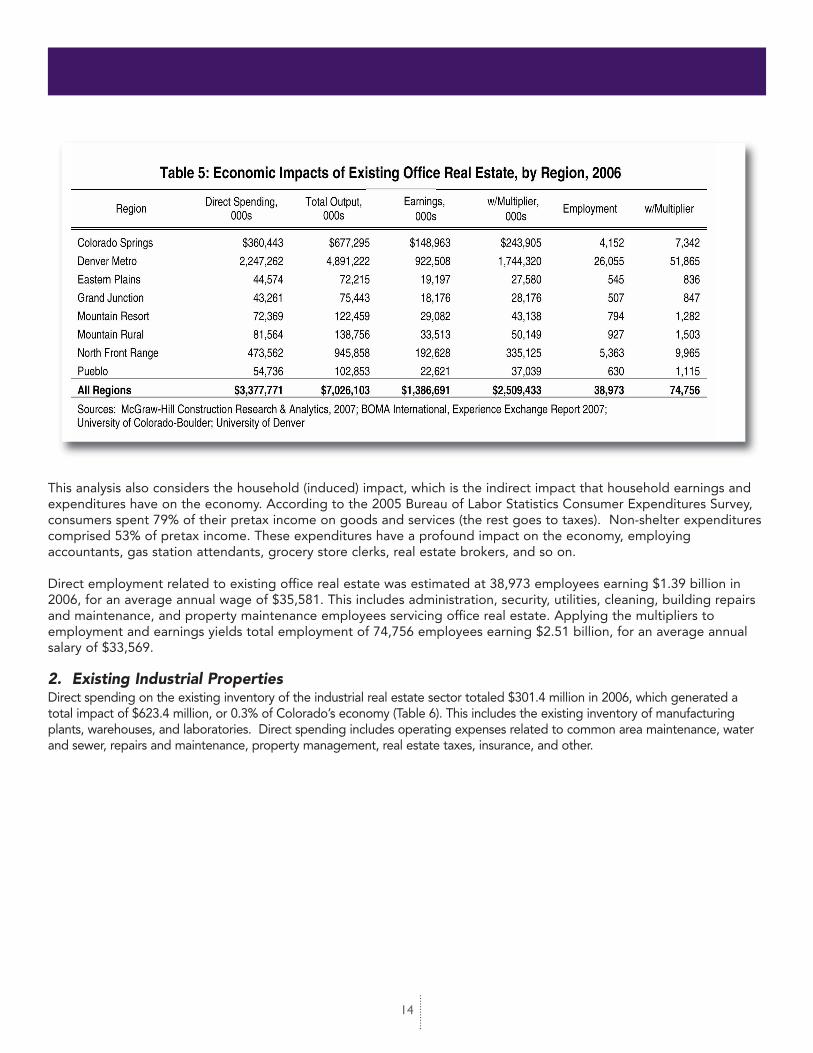

1. Existing Office PropertiesDirect spending in the existing inventory of office properties totaled $3.38 billion in 2006, which generated a $7.03billion total impact on Colorado’s economy, more than 3.0% of Colorado’s total output (Table 5). Direct spendingincludes operating expenses related to administration, security, utilities, cleaning, building repairs and maintenance, andproperty maintenance (see Appendix F for the Building Owners and Managers Association definitions). This sectordirectly employed 38,973 workers at an average wage of $35,581. The impacts varied widely by region, with the DenverMetropolitan region accounting for two-thirds of the existing office impact. Appendix G provides county level impacts.

Each dollar spent providing goods and services for existing office properties has a multiplier effect on the economydue to inter-industry relationships. For example, office properties occasionally need parking lots resurfaced, whichaffect the resurfacing company directly, but also impacts revenues for companies that sell resurfacing supplies andequipment. Hence, a dollar spent by a firm on commercial property has a ripple effect throughout the economy. Sincesome of the supplies and equipment are purchased from out of state, the multiplier effect is smaller than the nationalmultiplier. The same holds true for counties within Colorado – goods and services are imported from other counties,which reduces the impact on the primary county. This regional multiplier disparity has been accounted for by the BEARIMS II multipliers.

14

This analysis also considers the household (induced) impact, which is the indirect impact that household earnings andexpenditures have on the economy. According to the 2005 Bureau of Labor Statistics Consumer Expenditures Survey,consumers spent 79% of their pretax income on goods and services (the rest goes to taxes). Non-shelter expenditurescomprised 53% of pretax income. These expenditures have a profound impact on the economy, employingaccountants, gas station attendants, grocery store clerks, real estate brokers, and so on.

Direct employment related to existing office real estate was estimated at 38,973 employees earning $1.39 billion in2006, for an average annual wage of $35,581. This includes administration, security, utilities, cleaning, building repairsand maintenance, and property maintenance employees servicing office real estate. Applying the multipliers toemployment and earnings yields total employment of 74,756 employees earning $2.51 billion, for an average annualsalary of $33,569.

2. Existing Industrial PropertiesDirect spending on the existing inventory of the industrial real estate sector totaled $301.4 million in 2006, which generated atotal impact of $623.4 million, or 0.3% of Colorado’s economy (Table 6). This includes the existing inventory of manufacturingplants, warehouses, and laboratories. Direct spending includes operating expenses related to common area maintenance, waterand sewer, repairs and maintenance, property management, real estate taxes, insurance, and other.

15

Direct employment related to industrial real estate was estimated at 3,293 employees earning $132.0 million in 2006,for an average annual wage of $40,092 (see Appendix H for county impacts). Applying the multipliers to employmentand earnings yields total employment of 6,449 employees earning $230.3 million, for an average annual salary of$35,708.

3. Existing Retail PropertiesDirect spending in the retail real estate sector totaled $1.57 billion in 2006, which generated a $3.26 billion impact onColorado’s economy, or roughly 1.4% of Colorado’s total output (Table 7). Direct spending includes operating expensesrelated to building maintenance, external property maintenance (i.e., parking lot), utilities, advertising and promotion,insurance, and general and administrative expenses, and so on (See Appendix I for Urban Land Institute definitions).

16

Direct employment related to retail real estate was estimated at 18,627 employees earning $705.7 million in 2006, for an average wage of $37,884 (see Appendix J for county impacts). This includes building maintenance, externalproperty maintenance (i.e., parking lot), utilities, advertising and promotion, insurance, and general and administrativeexpenses. Applying the household multipliers to employment and earnings yields total employment of 35,106 employees earning $1.2 billion, for an average salary of $34,725.

4. Existing Hotel PropertiesDirect spending in the hotel real estate sector totaled $2.88 billion in 2006, which generated a $5.16 billion impact onColorado’s economy, or roughly 2.2% of Colorado’s total output (Table 8). Direct spending operating expenditures persquare foot were obtained from PKF Hospitality Research. This sector employed an estimated 45,793 workers at anaverage wage of $21,494 (see Appendix K for impact by county). This includes managerial operations and buildingmaintenance workers, as well as hotel room cleaners. Applying the household multipliers to employment and earningsyields total employment of 67,255 employees earning $1.7 billion, for an average salary of $24,728.

17

IV. Economic Impacts of Tenant Improvements

The economic impacts of tenant improvements were calculated separately. However, since tenant improvements areessentially construction, the RIMS II construction multipliers were employed to calculate the multiplier effects of directspending on output, earnings, and employment resulting from industry expenditures on tenant improvements.

Necessary data included income-producing property alterations by value, by type, and by county; industry soft costs(i.e., architectural, engineering, construction management, and site improvement); hard costs (construction materialsand construction worker wages); and industry multipliers. Property alteration figures were obtained from McGraw-HillConstruction Research & Analytics; industry soft costs were estimated as a percentage of total project costs obtainedby RS Means CostWorks for Building Construction; and RIMS II construction industry multipliers were obtained fromthe State Demography Office, compiled by the Bureau of Economic Analysis.

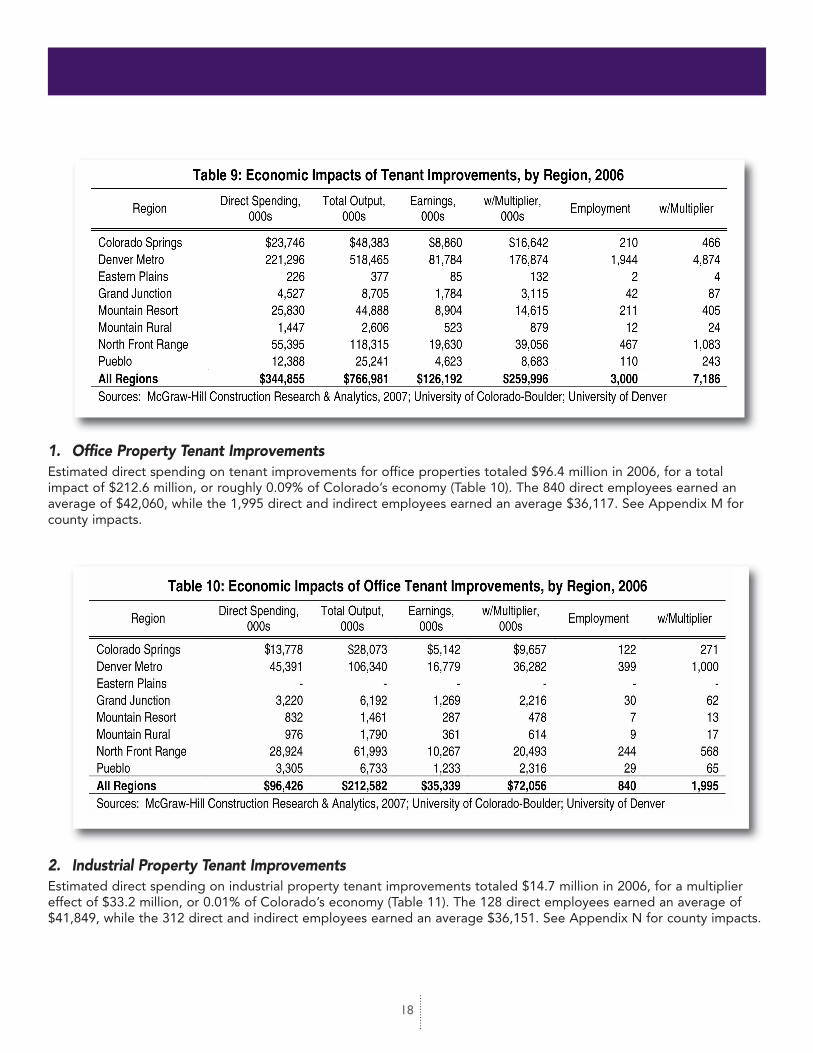

A. Summary of Tenant Improvements ImpactsDirect spending on tenant improvements totaled $344.9 million in 2006, for a total (direct and indirect) effect of $767.0million on Colorado’s economy, or 0.33% of State GDP (Table 9). Income-producing property tenant improvementsemployed 3,000 direct employees earning an average wage of $42,062. The 7,186 direct and indirect employees earned an average wage of $36,181. See Appendix L for county impacts.

18

2. Industrial Property Tenant ImprovementsEstimated direct spending on industrial property tenant improvements totaled $14.7 million in 2006, for a multipliereffect of $33.2 million, or 0.01% of Colorado’s economy (Table 11). The 128 direct employees earned an average of$41,849, while the 312 direct and indirect employees earned an average $36,151. See Appendix N for county impacts.

1. Office Property Tenant ImprovementsEstimated direct spending on tenant improvements for office properties totaled $96.4 million in 2006, for a totalimpact of $212.6 million, or roughly 0.09% of Colorado’s economy (Table 10). The 840 direct employees earned anaverage of $42,060, while the 1,995 direct and indirect employees earned an average $36,117. See Appendix M forcounty impacts.

19

4. Hotel Property Tenant ImprovementsEstimated direct spending on hotel property tenant improvements totaled $112.5 million in 2006, for a multiplier effectof $248.7 million, or 0.11% of Colorado’s economy (Table 13). The 974 direct employees earned an average of $42,086,while the 2,321 direct and indirect employees earned an average $36,252. See Appendix P for county impacts.

3. Retail Property Tenant ImprovementsEstimated direct spending on retail property tenant improvements totaled $94.0 million in 2006, for a multiplier effect of$211.9 million, or roughly 0.09% of Colorado’s economy (Table 12). The 820 direct employees earned an average of$42,065, while the 1,987 direct and indirect employees earned an average $36,186. See Appendix O for county impacts.

20

5. Multifamily Property Tenant ImprovementsEstimated direct spending on tenant improvements for multifamily properties totaled an estimated $27.2 million in2006, for a multiplier effect of $60.6 million, or 0.03% of Colorado’s economy (Table 14). The 238 direct employeesearned an average of $42,073, while the 571 direct and indirect employees earned an average $36,112. See AppendixQ for county impacts.

Table 15: Economic Impacts of New Construction, by Region, 2006

21

V. Economic Impacts of New Construction

Necessary data for calculating the impacts of income-producing property construction include the amount of newincome-producing space, by property type, and by county; site development costs; industry soft costs (i.e.,architectural, engineering, and construction management); hard costs (construction materials and construction workerwages); and industry construction multipliers. Financing development costs (construction loan fees and constructionloan interest) are accounted for in the Transactions and Refinancing sections. Data on new construction were obtainedfrom McGraw-Hill Construction Research & Analytics; industry soft costs were estimated as a percentage of totalproject costs obtained by RS Means CostWorks for Building Construction; and RIMS II construction industry multiplierswere obtained from the State Demography Office, compiled by the Bureau of Economic Analysis.

A. Summary of Impacts for New Construction

Direct spending on income-producing property construction totaled $3.3 billion in 2006, with an output multipliereffect of $6.9 billion, or roughly 3.0% of Colorado’s output (Table 15). Direct employment in new commercial andmultifamily construction totaled 28,145 employees earning $1.2 million, for an average wage of $42,298. Theemployment multiplier effect of new construction totaled 64,224 direct and indirect employees earning an estimated$2.3 billion, for an average wage of $36,161 in 2006. See Appendix R for county impacts. Separately, the impacts ofconstruction loan interest and fees attributable to new construction were estimated at $117.0 million.

Region Direct Spending,

000s Total Output,

000s Earnings,

000s w/Multiplier,

000s Employment w/Multiplier

Colorado Springs $300,118 $611,511 $111,952 $210,309 2,660 5,892

Denver Metro 1,368,077 3,197,129 512,550 1,097,491 12,014 30,099

Eastern Plains 8,034 13,429 3,018 4,718 72 131

Grand Junction 56,719 109,104 22,315 39,015 532 1,090

Mountain Resort 444,195 772,354 153,133 251,526 3,636 6,972

Mountain Rural 270,627 474,764 94,434 155,989 2,242 4,330

North Front Range 506,165 1,056,574 177,518 345,656 4,230 9,598

Pueblo 311,248 634,462 115,574 217,693 2,759 6,110

All Regions $3,265,183 $6,869,328 $1,190,494 $2,322,398 28,145 64,224 Sources: McGraw-Hill Construction Research & Analytics, 2007; University of Colorado-Boulder; University of Denver

Table 16: Economic Impacts of Office Construction, by Region, 2006

22

2. Industrial Property New ConstructionDirect spending on industrial property construction totaled an estimated $518.0 million in 2006, for a total effect of$1.09 billion, or 0.47% of Colorado’s economy (Table 17). The 4,560 direct employees earned an average of $41,861,while the 10,386 direct and indirect employees earned an average $35,817. See Appendix T for county impacts.

1. Office Property New ConstructionDirect spending on office property construction totaled $465.4 million in 2006, for a total effect of $1.01 billion, or0.44% of Colorado’s economy (Table 16). The 4,054 direct employees earned an average of $42,068, while the 9,478direct and indirect employees earned an average $36,084. See Appendix S for county impacts.

Region Direct Spending,

000s Total Output,

000s Earnings,

000s w/Multiplier,

000s Employment w/Multiplier

Colorado Springs $91,291 $186,003 $34,070 $63,985 809 1,792

Denver Metro 237,507 556,420 87,797 189,843 2,087 5,231

Eastern Plains 240 401 90 141 2 4

Grand Junction 17,885 34,389 7,046 12,308 168 344

Mountain Resort 16,919 29,520 5,836 9,628 139 266

Mountain Rural 17,101 30,378 5,995 10,017 142 278

North Front Range 67,385 136,467 23,333 44,118 556 1,228

Pueblo 17,058 34,755 6,366 11,956 151 335

All Regions $465,385 $1,008,333 $170,534 $341,997 4,054 9,478

Sources: McGraw-Hill Construction Research & Analytics, 2007; University of Colorado-Boulder; University of Denver

Table 17: Economic Impacts of Industrial Construction, by Region, 2006

Region Direct Spending,

000s Total Output,

000s Earnings,

000s w/Multiplier,

000s Employment w/Multiplier

Colorado Springs $26,640 $54,306 $9,889 $18,630 236 523

Denver Metro 127,348 298,623 46,835 101,652 1,119 2,806

Eastern Plains 750 1,255 281 440 7 12

Grand Junction 17,236 33,185 6,759 11,843 162 332

Mountain Resort 6,448 11,199 2,210 3,633 53 101

Mountain Rural 1,618 2,832 575 945 14 26

North Front Range 46,013 94,657 15,971 30,713 382 855

Pueblo 291,916 595,075 108,359 204,143 2,587 5,731

All Regions $517,969 $1,091,131 $190,880 $371,999 4,560 10,386

Sources: McGraw-Hill Construction Research & Analytics, 2007; University of Colorado-Boulder; University of Denver

23

3. Retail Property New ConstructionDirect spending on retail property construction totaled an estimated $536.4 million in 2006, for a multiplier effect of$1.18 billion, or 0.51% of Colorado’s output (Table 18). The 4,681 direct employees earned an average of $42,070,while the 11,080 direct and indirect employees earned an average $36,150. See Appendix U for county impacts.

4. Hotel Property New ConstructionDirect spending on hotel property construction totaled $313.5 million in 2006, for a multiplier effect of $574.1 million,or 0.25% of Colorado’s economy (Table 19). The 2,608 direct employees earned an average of $42,100, while the 5,249direct and indirect employees earned an average $36,024. See Appendix V for county impacts.

Table 20: Economic Impacts of Multifamily Construction, by Region, 2006

24

5. Multifamily Property New ConstructionDirect spending on multifamily construction totaled $1.4 billion in 2006, for a multiplier effect of $3.0 billion, or 1.3% ofColorado’s economy (Table 20). The 12,242 direct employees earned an average of $42,667, while the 28,031 directand indirect employees earned an average $36,344. See Appendix W for county impacts.

Region Direct Spending,

000s Total Output,

000s Earnings,

000s w/Multiplier,

000s Employment w/Multiplier

Colorado Springs $88,705 $180,734 $33,105 $62,173 786 1,742

Denver Metro 663,282 1,545,691 252,256 534,276 5,822 14,577

Eastern Plains - - - - - -

Grand Junction 4,866 9,356 1,917 3,348 46 94

Mountain Resort 341,461 593,816 117,729 193,406 2,795 5,361

Mountain Rural 43,500 76,195 15,170 25,022 360 695

North Front Range 290,091 610,781 102,164 200,535 2,433 5,564

Pueblo - - - - - -

All Regions $1,431,905 $3,016,571 $522,341 $1,018,760 12,242 28,031 Sources: McGraw-Hill Construction Research & Analytics, 2007; University of Colorado-Boulder; University of Denver

25

VI. Economic Impacts of Commercial Property Transactions

The buying and selling of commercial property in 2006 resulted in a total sales volume of $7.48 billion in the State ofColorado and an estimated $411.4 million in transaction fees (Tables 21 and 22). According to NorthMarq Capital, atypical commercial property transaction generates 5.5% of the total transaction amount in fees that are paid toprofessionals and businesses engaged in the transaction. This percentage represents the total of brokeragecommissions, loan origination fees, title insurance fees, engineering costs, closing costs, and other typical fees incurredwhen the title of a commercial property changes hands. The impact of transaction fees on direct employment andearnings, including their multipliers, have not been calculated due to the ambiguous sources and uses of funds. Forinstance, loan origination fees paid to a bank are not bank expenditures nor purely profit; rather, these funds arereinvested in and out of the state. See Appendix B for notes on methodology.

26

VII. Economic Impacts of Commercial Property Refinancing

Refinancing commercial property in 2006 created a total new loan volume of $3.14 billion in the State of Colorado, andan estimated $47.1 million in fees (Tables 23 and 24). According to NorthMarq Capital, a typical commercial propertyloan refinancing generates an average 1.5% of the total loan amount in fees paid to commercial banks, loan officers,appraisers, inspectors, engineers, and other professionals involved with refinancing. The indirect impacts of refinancingfees and mortgage interest on economic activity have not been calculated due to the ambiguous sources and uses offunds. For instance, mortgage interest paid to a bank are not bank expenditures nor purely profit; rather, these fundsare deposited nationally and reinvested in and out of the state. See Appendix B for details on methodology.

27

VIII. Fiscal Impacts

Commercial property impacts federal, state, and local governments in terms of property taxes, sales taxes, anddevelopment fees. Development fees were excluded from the fiscal analysis due to the extremely varying feestructures throughout Colorado counties and cities; however, fees were included in the output analysis since they wereaggregated in the per square foot soft construction costs. Most fees are designed to directly offset a public cost, suchas adding water meters, inspecting properties, or providing other services. Property taxes have a direct local impactbased on the geographical locale of the property, whereas sales taxes depend on where purchases are made. Bothhave significant impacts on government revenues, contributing a combined estimated $1.26 billion to local, county,and state government.

A. Commercial Property TaxesCommercial property taxes, excluding multifamily properties, totaled $1.18 billion in 2006, including county, city,school, and special districts. In 2006, office property taxes were estimated at $353.5 million; industrial property taxes,including manufacturing, totaled $430.7 million; retail property taxes were estimated at $326.2 million; and hotelproperty taxes were estimated at $67.0 million (Table 25).

Colorado property taxes are calculated based on assessed values and mill levies (county, city, special district, andschool). Property values are multiplied by the assessment ratio (29% for non-residential property), then multiplied bythe property tax mill rate.

Assessed property values for 2006 and estimated mill levies are published on the Department of Local Affairs, Divisionof Property Taxation website as of September 7, 2007(http://www.dola.colorado.gov/dpt/publications/2006_annual_report_index.htm). See Appendix X and Appendix Y forcounty detail.

28

B. Commercial Property Sales Taxes

Sales tax revenues obtained from direct spending on constructionmaterials in the State of Colorado were estimated at $75.2 million in2006. The total impact of sales tax revenues (direct and indirectimpacts) were estimated at $160.7 million in 2006. This assumes that60% of new construction are material purchases, 20% of additions toproperties are material purchases, and 40% of tenant alterations arematerial purchases.

Material purchases have a direct impact on municipalities and countiesbased on the location of the purchases (which may be a differentcounty). Therefore, if an office building is constructed in Greeley,Colorado, a portion of the materials are probably purchased inCommerce City. Hence, Greeley does not receive the full benefit ofthe construction expenditure. For simplicity in estimating sales taxesfrom construction material purchases, an assumption was made that100% of the materials are purchased in the county where constructiontakes place. This surely overstates the impacts for some counties andunderstates the impacts for other counties, but only the aggregatefiscal impact is reported here.

Conclusion

The impact of the income-producing property industry on Colorado’seconomy is significant. Adding together the individual property sectorsfor existing property operations, new construction, transactions, andrefinancing, commercial property and new multifamily constructiondirectly contributed $12.3 billion to Colorado’s economy in 2006.Including the indirect impact on output, income-producing propertycontributed an estimated $24.3 billion to Colorado’s GDP, or 10.5% ofthe State economy (Table 26). Income-producing property directemployment totaled 137,832 in Colorado in 2006, or 6.1% of Stateemployment, at an average wage of $32,832. Including the indirectemployment, income-producing property employed 254,976 in 2006,at an average wage of $32,177.

29

1 Existing does not include multifamilies.2 Other does not include the impact on employment, earnings, multiplier effect, or impact on individual counties due to the uncertainty of

the source of, and redeployment of funds.

Sources: McGraw-Hill Construction Research & Analytics, 2007; BOMA International, Experience Exchange Report 2007; Urban LandInstitute, Dollars & Cents of Shopping Centers / The SCORE 2006; PKF Hospitality Research; NAIOP Industrial Income and ExpenseReport 2001-2002; Real Capital Analytics; NorthMarq Capital; University of Colorado-Boulder; University of Denver

Direct Spending (000) Total Output (000) Percent of Colorado’s GDP

Existing1

Office 3,377,771 7,026,103 3.0%Industrial 301,387 623,368 0.3%Retail 1,574,128 3,256,520 1.4%Hotel 2,881,556 5,158,947 2.2%Total Existing 8,134,842 16,064,938 7.0%

Tenant ImprovementsOffice 96,426 212,582 0.1%Industrial 14,693 33,231 0.0%Retail 94,036 211,932 0.1%Hotel 112,504 248,651 0.1%Multifamily 27,195 60,587 0.0%Total TI 344,854 766,983 0.3%

New ConstructionOffice 465,385 1,008,333 0.4%Industrial 517,969 1,091,131 0.5%Retail 536,406 1,179,158 0.5%Hotel 313,518 574,134 0.2%Multifamily 1,431,905 3,016,571 1.3%Total Construction 3,265,183 6,869,327 3.0%

Other2

Construction Period Interest/Fees 137,294 137,294 0.1%Transactions 411,408 411,408 0.2%Refinancing 47,093 47,093 0.0%Total Other 595,795 595,795 0.3%

Total All 12,340,674 24,297,043 10.5%

Table 26: Summary Impacts of Commercial Real Estate and Multifamily Construction on Colorado’s Economy, 2006

30

Ap

pend

ix A

: Eco

nom

ic Im

pact

s, b

y Co

unty

, 200

6 *E

XIS

TIN

G, T

EN

AN

T IM

PR

OV

EM

EN

TS, A

ND

CO

NS

TRU

CTI

ON

Cou

nty

Dire

ct

Spe

ndin

g, 0

00s

Tota

l Out

put,

000s

E

arni

ngs,

00

0s

w/M

ultip

lier,

000s

E

mpl

oym

ent

w/M

ultip

lier

Cou

nty

Dire

ct

Spe

ndin

g,

000s

Tota

l Out

put,

000s

E

arni

ngs,

00

0s

w/M

ultip

lier,

000s

E

mpl

oym

ent

w/M

ultip

lier

Ada

ms

$847

,960

$1

,910

,667

$3

31,4

86

$666

,440

9,12

9

19,

490

La

Pla

ta

$82,

382

$1

35,0

71

$30,

243

$4

5,15

8

1,15

7

1,66

9

Ala

mos

a

2

3,04

2

36,2

30

9

,268

1

3,32

0

315

4

56

La

ke

33

,507

57,8

66

11,

883

19,

103

294

540

Ara

paho

e

1,39

3,23

4

3,0

90,0

47

554,

390

1

,086

,026

1

5,82

7

32,

334

Larim

er

520

,519

9

51,5

38

1

92,7

22

3

16,4

26

5,33

7

9,48

5

Arc

hule

ta

8

,357

14

,067

3,0

47

4,

701

9

6

152

Las

Ani

mas

16,1

21

25

,096

6,29

7

9,04

9

23

0

32

5

Bac

a

1,9

54

3,1

13

870

1,22

6

25

37

Li

ncol

n

8,8

59

14

,440

3,48

9

5,23

1

99

159

Ben

t

2,4

65

3,9

07

1

,029

1,47

4

33

49

Lo

gan

25

,772

40,8

40

10,

467

15,

117

351

509

Bou

lder

79

4,11

8

1,7

55,4

91

313,

782

614

,778

9,29

2

18,

610

Mes

a

1

95,5

15

350

,032

7

9,07

0

127

,418

2,

348

3,

971

Cha

ffee

19,

955

32,7

21

7

,324

1

0,94

1

281

4

05

M

iner

al

2

,026

3,4

04

830

1,

217

24

37

Che

yenn

e

2,8

12

4,5

45

1

,171

1,70

9

33

52

M

offa

t

14,3

51

23

,733

5,30

7

7,97

7

18

2

27

1

Cle

ar C

reek

9,9

04

16,4

30

3

,802

5,64

9

130

1

93

M

onte

zum

a

29,9

80

49

,561

1

1,27

8

16,

837

401

592

Con

ejos

2,1

17

3,3

41

894

1,27

0

28

41

M

ontro

se

44

,456

80,4

47

17,

930

29,

228

51

5

89

4

Cos

tilla

1,2

66

1,9

92

526

74

9

17

25

M

orga

n

16,5

69

28

,886

6,68

3

1

0,13

9

19

4

31

3

Cro

wle

y

7

06

1,1

25

304

43

3

9

14

O

tero

18,1

10

28

,749

7,57

5

1

0,85

7

24

4

35

6

Cus

ter

1

,777

2

,730

6

37

929

2

7

37

Our

ay

2

,832

4,7

21

1,

072

1,

610

35

54

Del

ta

11,

105

19

,354

4,6

68

7,

223

14

1

228

Par

k

9,7

39

16

,795

3,47

5

5,56

3

87

158

Den

ver

2,

018,

989

4

,410

,503

80

7,29

6 1

,553

,129

2

4,45

0

47,

624

Phi

llips

2,9

04

4

,650

1,28

2

1,82

2

3

7

5

6

Dol

ores

1

2,65

3

21,4

93

5

,399

7,88

1

136

2

22

P

itkin

3

40,1

30

569

,276

117

,798

184

,652

4,

045

6,

318

Dou

glas

42

8,83

8

9

64,0

24

168,

492

337

,017

4,64

9

9

,868

Pro

wer

s

14,6

57

22

,877

5,81

6

8,33

7

206

294

Eag

le

550,

747

9

04,1

54

189,

822

2

91,5

36

7,

587

1

1,04

2

Pue

blo

476

,610

9

47,6

24

1

83,0

13

3

29,5

58

4,83

0

9,65

7

El P

aso

847,

023

1,5

86,9

34

342,

970

5

64,4

21

11,

014

1

8,36

7

Rio

Bla

nco

7

,199

11,9

20

2,

665

4,

007

9

0

13

6

Elb

ert

315,

190

641

,237

11

7,74

2

220

,718

2,80

3

6

,187

Rio

Gra

nde

7

,796

12,4

05

3,

268

4,68

7

10

0

15

0

Frem

ont

28,

520

54

,752

1

1,67

9

19,

616

33

9

602

Rou

tt

1

83,1

62

303

,201

6

3,69

6

9

8,39

6

2,

379

3,

559

Gar

field

16

0,32

8

264

,997

5

4,91

0

8

5,30

9

1,97

6

2

,980

Sag

uach

e

1,0

35

1

,648

46

1

64

9

13

20

Gilp

in

213,

870

3

66,1

26

73,

534

1

18,7

31

2,

057

3,5

93

S

an J

uan

1

,348

2,2

27

512

760

1

8

2

7

Gra

nd

184,

233

304

,082

6

3,28

1

9

7,95

2

2,

441

3,6

18

S

an M

igue

l

1

21,5

80

199

,535

4

1,68

7

64,

142

1,

676

2,

438

Gun

niso

n

6

6,61

6

1

12,0

97

23,

519

3

6,78

5

760

1,2

12

S

edgw

ick

2

,835

4,4

70

1,

153

1,

656

4

0

5

7

Hin

sdal

e

1,6

58

2,6

87

580

87

2

2

5

35

Sum

mit

278

,854

4

52,7

95

96,

690

1

46,2

55

4,14

6

5,83

0

Hue

rfano

6,0

55

9,3

83

2

,298

3,31

7

8

8

123

Telle

r

30,2

22

57

,685

1

1,32

5

1

9,73

5

384

659

Jack

son

1

,435

2

,397

5

65

835

1

8

27

Was

hing

ton

2

,154

3,4

50

952

1,35

2

2

7

4

1

Jeffe

rson

1,00

6,53

2

2,2

31,2

63

401,

639

785

,150

1

1,59

5

23,

488

Wel

d

2

69,3

72

491

,505

101

,264

164

,944

2,

738

4,

881

Kio

wa

7

,829

12

,410

3,2

65

4,

675

105

1

53

Y

uma

4

,388

7,0

17

1,

900

2,

712

5

7

8

5

Kit

Car

son

8

,611

13

,484

3,3

55

4,

853

125

1

76

CO

LORA

DO

11,

744,

880

23,

701,

247

4,5

25,3

43

8,2

04,2

61

137

,831

2

54,9

76

Sou

rces

:

McG

raw

-Hill

Con

stru

ctio

n R

esea

rch

& A

naly

tics,

200

7; B

OM

A In

tern

atio

nal,

Exp

erie

nce

Exc

hang

e R

epor

t 200

7; U

rban

Lan

d In

stitu

te, D

olla

rs &

Cen

ts o

f Sho

ppin

g C

ente

rs /

The

SC

OR

E 2

006;

PK

F H

ospi

talit

y R

esea

rch;

NA

IOP

Indu

stria

l Inc

ome

and

Exp

ense

Rep

ort 2

001-

2002

; Uni

vers

ity o

f Col

orad

o-B

ould

er; U

nive

rsity

of D

enve

r. C

ount

y im

pact

s ex

clud

e ec

onom

ic e

ffect

s of

tran

sact

ions

and

refin

anci

ng.

31

EXISTING PROPERTIESTo estimate direct spending (from total operating expenses) byproperty type and by county, total area was multiplied by the persquare foot (PSF) operating expenses. Total square feet of commercialand multifamily property space, by property type, by county, wasobtained from McGraw-Hill Construction Research & Analytics.Operating expenses by property type were obtained from BOMA, ULI,NAIOP, PKF Hospitality Research, and RS Means CostWorks. Whenpossible, expenditures were segmented by services to buildings,management services, and utilities.

Total operating expenses were multiplied by the output multiplier toestimate the total impact of the sector on Colorado’s GDP. The directearnings per dollar of sales to final demand were used to estimate thedirect impact of expenditures in the commercial real estate sector. Thetotal earnings per dollar of sales to final demand multipliers were usedto estimate the total (direct and multiplied) impacts of the sector onincomes. Similarly, the direct employment per million dollars of sales tofinal demand multipliers were used to estimate the impacts of thesector on employment; and total employment per dollar of sales tofinal demand was used to estimate the total (direct and multiplied)employment impact.

Employment is limited to those employed by the commercial realestate sector, specifically omitting those employees working in thecommercial real estate space (i.e., the retail space lessor, not theclothing store clerk).

Note that Broomfield was not included in the McGraw-Hill ConstructionResearch & Analytics data for existing commercial real estate.Broomfield became a county in 2001, comprised of land from Adams,Boulder, Jefferson, and Weld counties. The impact from BroomfieldCounty real estate is included in these four counties.

1. OFFICE DATAPer square foot (PSF) office operating costs were obtained from theExperience Exchange Report 2007 published by BOMA International(Table 27). BOMA reports PSF operating costs categorized by cleaning,repairs/maintenance, utilities, roads/grounds, security and administrative(Appendix F). For the purpose of this study, these categories were thengrouped by services to buildings (cleaning, repairs/maintenance,roads/grounds, and security), management services (administrative), andutilities. Taxes have been included by BOMA in the administrative seg-ment of operating expenses.

Appendix B: Notes to Methodology

32

BOMA segregated the data by three regions: Denver, Suburbs, and Boulder. Denver and Suburbs had similar costestimates ($11.11 PSF and $14.19 PSF, respectively). Boulder estimates were much less ($6.45 PSF), since this analysiswas performed at the county level and not the city level.

2. RETAIL DATAPer square foot retail operating expenses were provided in the Urban Land Institute’s Dollars and Cents of ShoppingCenters (see Table 28). The PSF operating expenses were categorized by maintenance and housekeeping, advertisingand promotion, real estate taxes, insurance, and general and administrative functions (Appendix I). For the purpose ofthis study, these categories were then grouped by services to buildings (cleaning, repairs/maintenance, roads/grounds,and security) and management services (administrative).

33

ULI data was segmented into five categories of shopping centers: Super Regional, Regional, Super Community,Neighborhood, and Convenience. A weighted average was calculated using the total area by type in Colorado, fortotal PSF operating expenditures of $9.84.

3. INDUSTRIAL DATAPer square foot industrial operating expenses were provided in NAIOP’s Industrial Income and Expense Report: 2001-2002 (Table 29). This was the most current expense report detailing operating expenses for the industry; thereforeexpenses were inflated appropriately for 2006 using the Denver-Boulder-Greeley CPI (Table 30). The median operatingexpenses of $1.08 were applied throughout Colorado.

34

4. HOTEL DATAPer square foot hotel operating expenses were obtained from PKF Hospitality Research and were estimated at $46.98per square foot.

5. MULTIPLIERSRegional Input-Output Modeling System (RIMS II) multipliers published by the Bureau of Economic Analysis were usedto estimate the total output, earnings, and employment multiplier effects by industry sector by region in Colorado.

RIMS II multipliers are segmented by industry sector and by economic region in Colorado (Appendix C). This studyemploys the multipliers with the impact of local government included. Multipliers are reported by output, earnings,and employment and impacts can be calculated as a function of output, earnings, and employment, or from outputalone. For instance, if the utilities industry output multiplier is 2.1365 for the State of Colorado, then the impact of $1million in utilities spending on Colorado’s economy is $2.1365 million ($1 million direct spending and $1.1365 indirect).Direct earnings can then be calculated using the direct earnings per dollar of sales to final demand multiplier, which inthis scenario is 0.1808. Therefore, the $1 million in utilities spending equates to $180,800 in direct earnings. Similarly,employment can be calculated using the direct employment per million dollars of sales to final demand multiplier,which in this scenario is 2.2577, or 2.2577 employees for every $1 million in utility expenditures. Conversely, simpleearnings and employment multipliers can be utilized if direct earnings and employment are already known.

TENANT IMPROVEMENTS & CONSTRUCTIONTenant improvements and construction area and value were obtained from McGraw-Hill Construction Research &Analytics. This value does not include soft costs or site development. Soft costs for architectural, engineering, and construction management were obtained from RS Means CostWorks, while site development costs were obtainedanecdotally from the Clayton Lane2 case.

2 The Clayton Lane case was prepared November 8, 2006 by David B. Agnew, Esq., and Thomas G. Thibodeau, Ph.D., as an analysis tool of amajor redevelopment in Cherry Creek, Colorado.

Table 30: Denver-Boulder-Greeley CPI

Year Index Percentage

Change

2001 181.3 - 2002 184.8 1.93% 2003 186.8 1.08% 2004 187.0 0.11% 2005 190.9 2.09% 2006 197.7 3.56%

Source: Bureau of Labor Statistics, http://data.bls.gov/

35

HARD AND SOFT COSTSThe economic value of construction spending to the Colorado economy can be separated into two components, softcosts and hard costs. Soft costs are defined as the initial spending on a construction project that include architects,engineers, development (land entitlement), land planning, legal services, land improvements, landscape architecture,and infrastructure improvements (Table 31). Hard costs are defined as direct outlays during the construction processand include both labor and building materials plus construction equipment costs. The labor spending represents theemployment in the construction sector of skilled workers, including carpenters, steel workers, electricians, plumbers,building engineers, and heavy equipment operators. It also includes indirectly employed workers in such companies asraw materials producers of lumber, concrete, and steel.

BUILDING OPERATIONSBuildings also contribute economically to the State of Colorado’s economy after construction is complete and thespace is occupied. This contribution can be defined as the amount of money spent on an annual basis to operate,maintain, and clean the property; property management services used to bill and maintain relationships with tenants;the utilities that the building consumes; and financing costs that are received by lenders within the State of Colorado.

TRANSACTIONS AND REFINANCINGTwo industries rely heavily on commercial real estate transactions: commercial real estate brokerage, and commercialmortgage brokerage and investment. Commercial real estate brokers make their entire profession from buying andselling real estate for investors and leasing of commercial space to and for tenants. Banks invest a large portion oftheir mortgage pools in commercial properties and draw significant fees from securitizing large portfolios ofcommercial mortgages into commercial mortgage-backed security (CMBS) pools.