stock compensation, deferred compensation and state income

TRANSCRIPT

WHO TO CONTACT DURING THE LIVE PROGRAM

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x1 (or 404-881-1141 x1)

For Assistance During the Live Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 ext. 1 (or 404-881-1141 ext. 1).

Strafford accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code.

• To earn full credit, you must remain connected for the entire program.

Stock Compensation, Deferred Compensation and State

Income Taxes

WEDNESDAY, DECEMBER 11, 2019, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality FOR LIVE PROGRAM ONLY

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

December 11, 2019

Stock Compensation, Deferred Compensation and State Income Taxes

Joseph S. Pancamo, CPA, Region Leader, Global

Employer Services

BDO US

Marlene Zobayan, Partner

Rutlen Associates

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

Stock Compensation, Deferred Compensation and State Income TaxesCOMPLIANCE WITH CORPORATE AND EMPLOYER

FILINGS

Joe Pancamo – BDO USA, LLP

Marlene Zobayan – Rutlen Associates LLC

DisclaimerThis presentation contains general information only and the respective speakers and represented firms are not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. The respective speakers and firms shall not be responsible for any loss sustained by any person who relies on this presentation.

This presentation focuses only on the payroll tax aspects related to employees, other compliance areas including other areas of tax, securities law, labor law, data privacy etc. are not addressed.

6

Agenda1. Background On Stock Compensation And Its Taxation

2. How The Use Of Stock Compensation Can Trigger Nexus

3. Administrative Challenges And Practical Solutions

4. Questions And Answers

7

Background On StockCompensation And Its TaxationS T O C K O P T I O N S

R E S T R I C T E D S T O C K A W A R D S

R E S T R I C T E D S T O C K U N I T S

E M P L O Y E E S T O C K P U R C H A S E P L A N

8

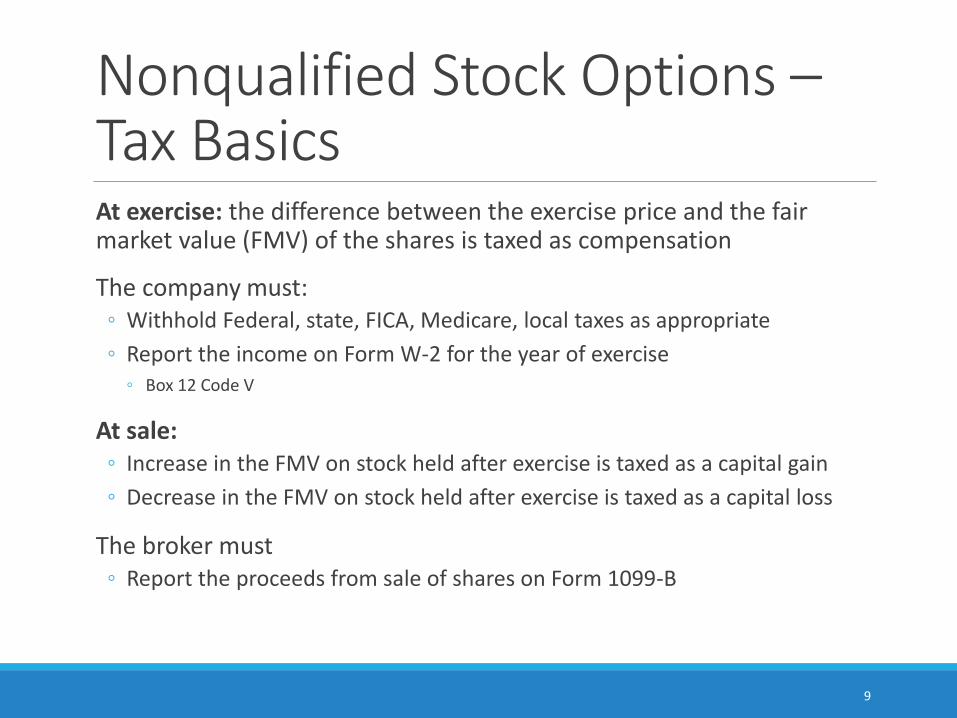

Nonqualified Stock Options –Tax BasicsAt exercise: the difference between the exercise price and the fair market value (FMV) of the shares is taxed as compensation

The company must:◦ Withhold Federal, state, FICA, Medicare, local taxes as appropriate

◦ Report the income on Form W-2 for the year of exercise◦ Box 12 Code V

At sale: ◦ Increase in the FMV on stock held after exercise is taxed as a capital gain

◦ Decrease in the FMV on stock held after exercise is taxed as a capital loss

The broker must◦ Report the proceeds from sale of shares on Form 1099-B

9

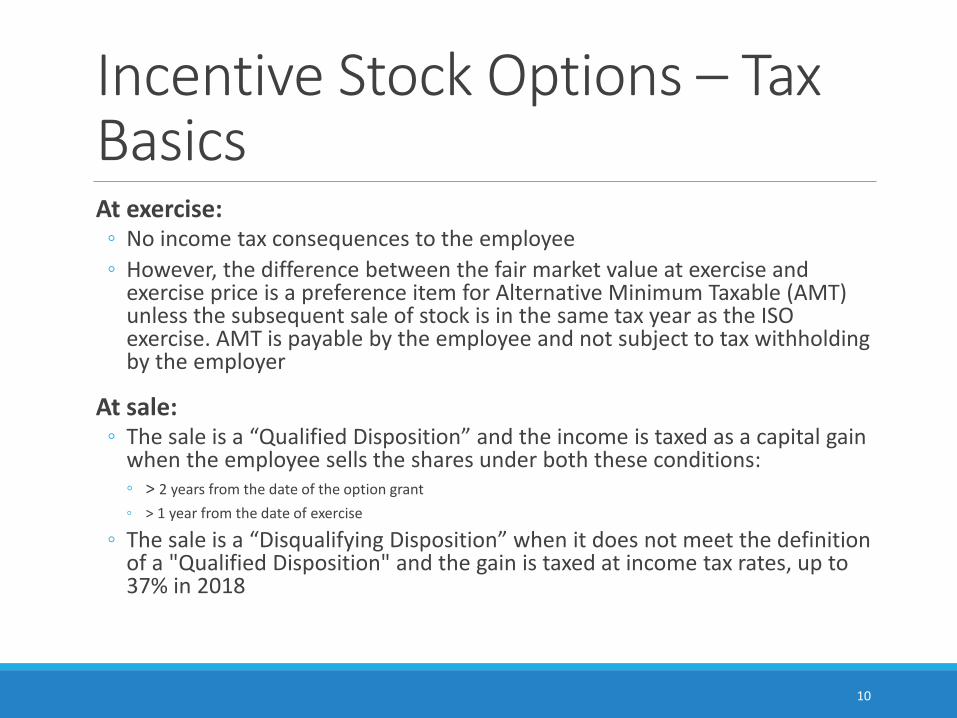

Incentive Stock Options – Tax BasicsAt exercise:

◦ No income tax consequences to the employee

◦ However, the difference between the fair market value at exercise and exercise price is a preference item for Alternative Minimum Taxable (AMT) unless the subsequent sale of stock is in the same tax year as the ISO exercise. AMT is payable by the employee and not subject to tax withholding by the employer

At sale: ◦ The sale is a “Qualified Disposition” and the income is taxed as a capital gain

when the employee sells the shares under both these conditions:◦ > 2 years from the date of the option grant

◦ > 1 year from the date of exercise

◦ The sale is a “Disqualifying Disposition” when it does not meet the definition of a "Qualified Disposition" and the gain is taxed at income tax rates, up to 37% in 2018

10

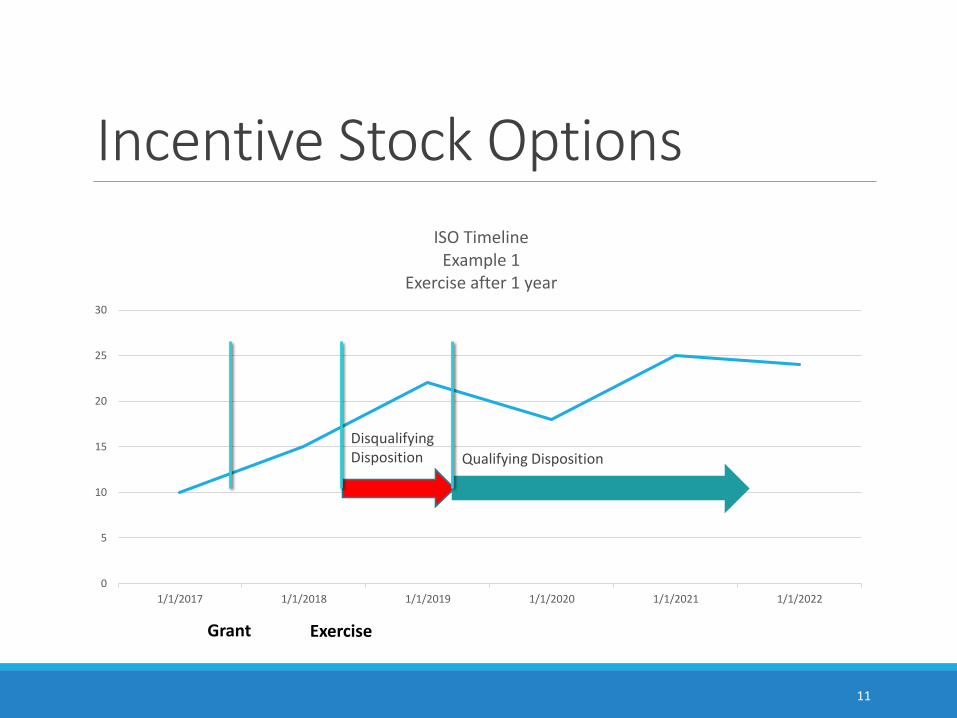

0

5

10

15

20

25

30

1/1/2017 1/1/2018 1/1/2019 1/1/2020 1/1/2021 1/1/2022

ISO TimelineExample 1

Exercise after 1 year

DisqualifyingDisposition

Incentive Stock Options11

Qualifying Disposition

Grant Exercise

11

12

Qualifying Disposition

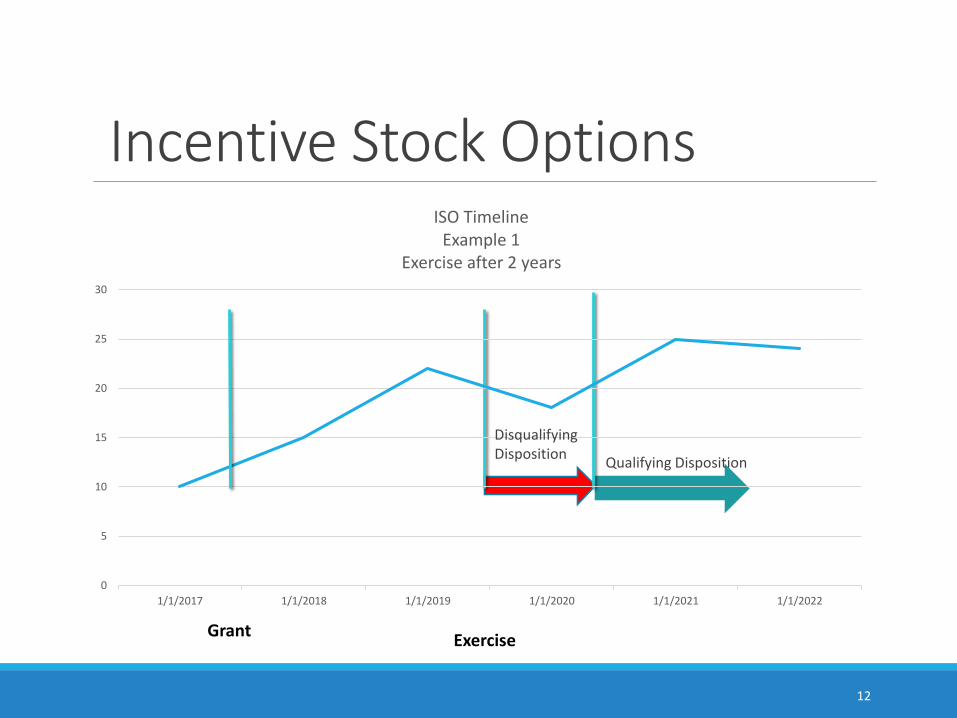

0

5

10

15

20

25

30

1/1/2017 1/1/2018 1/1/2019 1/1/2020 1/1/2021 1/1/2022

ISO TimelineExample 1

Exercise after 2 years

GrantExercise

DisqualifyingDisposition

Incentive Stock Options

12

Incentive Stock OptionsRemember:

Company must report exercise on form 3921

Company must report on W-2 for disqualifying disposition only

Ohio requires withholding on disqualifying dispositions

Pennsylvania does not recognize the qualifying nature of ISOs and ESPP

13

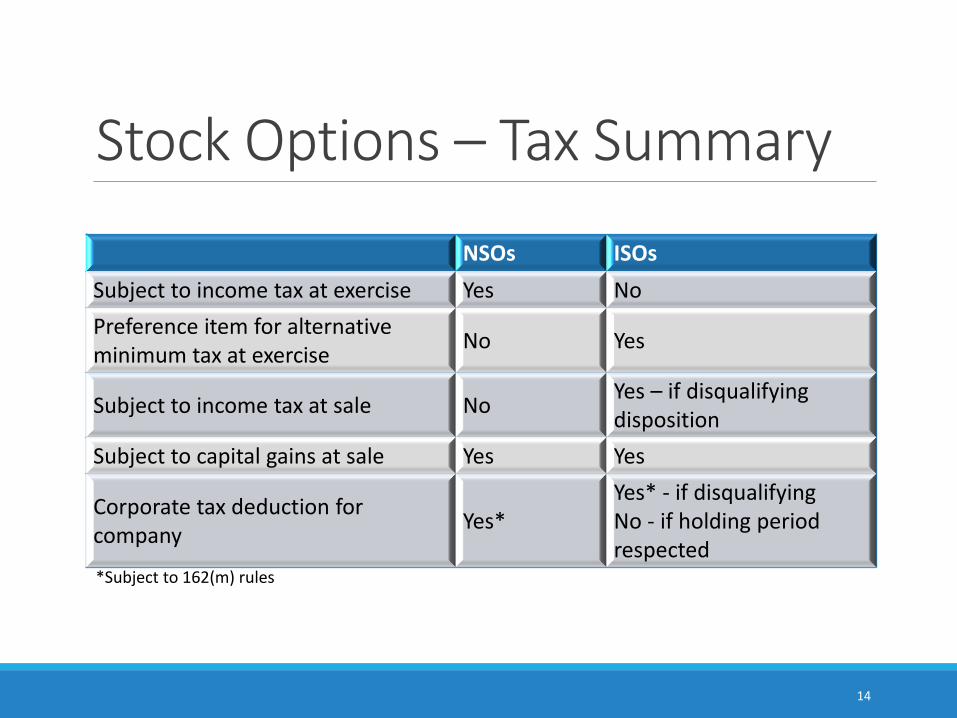

Stock Options – Tax Summary

NSOs ISOs

Subject to income tax at exercise Yes No

Preference item for alternativeminimum tax at exercise

No Yes

Subject to income tax at sale No Yes – if disqualifying disposition

Subject to capital gains at sale Yes Yes

Corporate tax deduction for company

Yes*Yes* - if disqualifyingNo - if holding period respected

14

*Subject to 162(m) rules

Restricted Stock Awards (RSAs) – Tax BasicsAt grant: if the employee makes a s83b election, the fair market value (FMV) of the shares is taxed as compensation

◦ Must be made within 30 days of grant

◦ Irrevocable election even if the employee later forfeits the shares

At vest/release: if no s 83b election is made, the fair market value (FMV) of the shares is taxed as compensation income

At sale: ◦ Increase in the FMV on stock held after taxing point is taxed as a capital gain

◦ Decrease in the FMV on stock held after taxing point is taxed as a capital loss

15

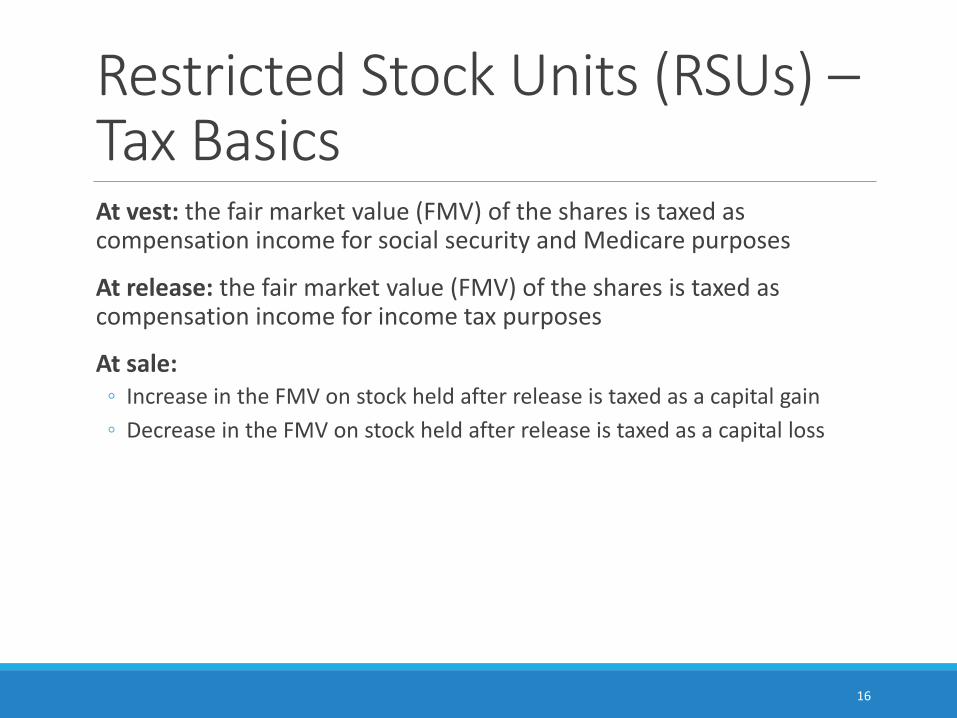

Restricted Stock Units (RSUs) –Tax BasicsAt vest: the fair market value (FMV) of the shares is taxed as compensation income for social security and Medicare purposes

At release: the fair market value (FMV) of the shares is taxed as compensation income for income tax purposes

At sale: ◦ Increase in the FMV on stock held after release is taxed as a capital gain

◦ Decrease in the FMV on stock held after release is taxed as a capital loss

16

ESPP – Tax BasicsAt purchase:

◦ No income tax consequences to the employee

◦ ESPP is not an Alternative Minimum Taxable (AMT) preference item

At sale: ◦ The sale is a “Qualified Disposition” where the income is taxed partly as

income and partly as a capital gain. The sale will be a Qualified Disposition if the employee sells the shares and meets these two conditions:◦ > 2 years from the offering date

◦ > 1 year from the date of purchase

◦ The amount subject to income tax is the amount of the discount as calculated at the time of offering (or the actual discount if less)

◦ If an employee does NOT hold the stock for the required periods, the disposition is referred to as a “Disqualifying Disposition” and the discount is taxed at income tax rates, up to 37% in 2017

18

0

5

10

15

20

25

30

1/1/2017 1/1/2018 1/1/2019 1/1/2020 1/1/2021 1/1/2022

Employee Stock Purchase PlanThe employee’s purchase price is the lower of

a) 85% of the stock price on the offering date

b) 85% of the stock price on the purchase date

19

Example:• Fair market value on first day of offering

period: $15• Fair market value on purchase date: $20• Purchase price: $12.75 (85% of $15)

First day of offering period Purchase date

Discount

$12.75

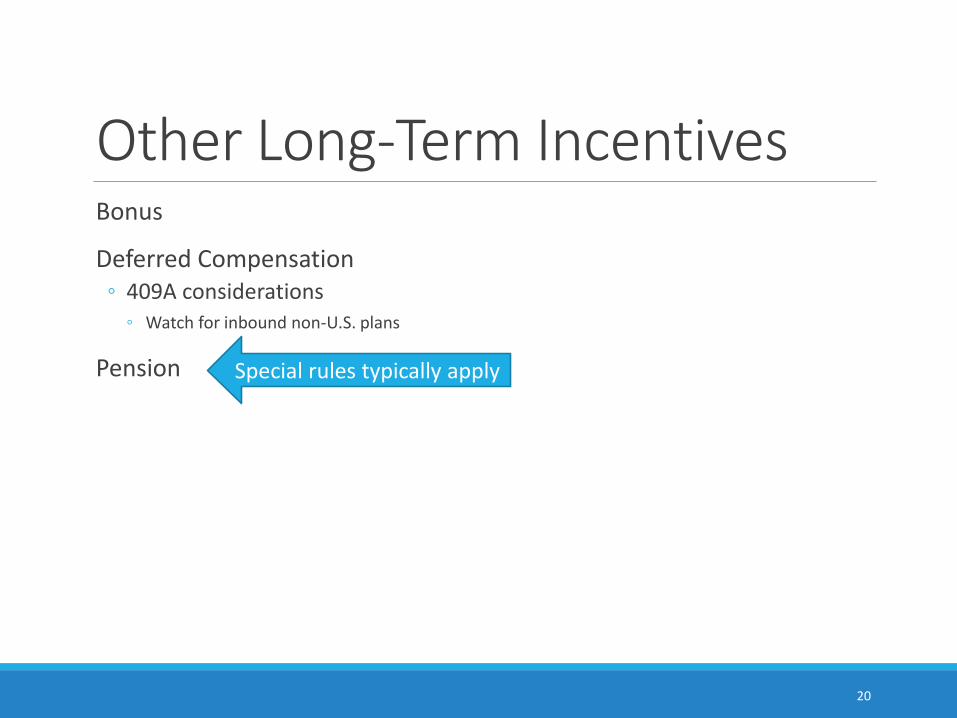

Other Long-Term Incentives Bonus

Deferred Compensation◦ 409A considerations

◦ Watch for inbound non-U.S. plans

Pension Special rules typically apply

20

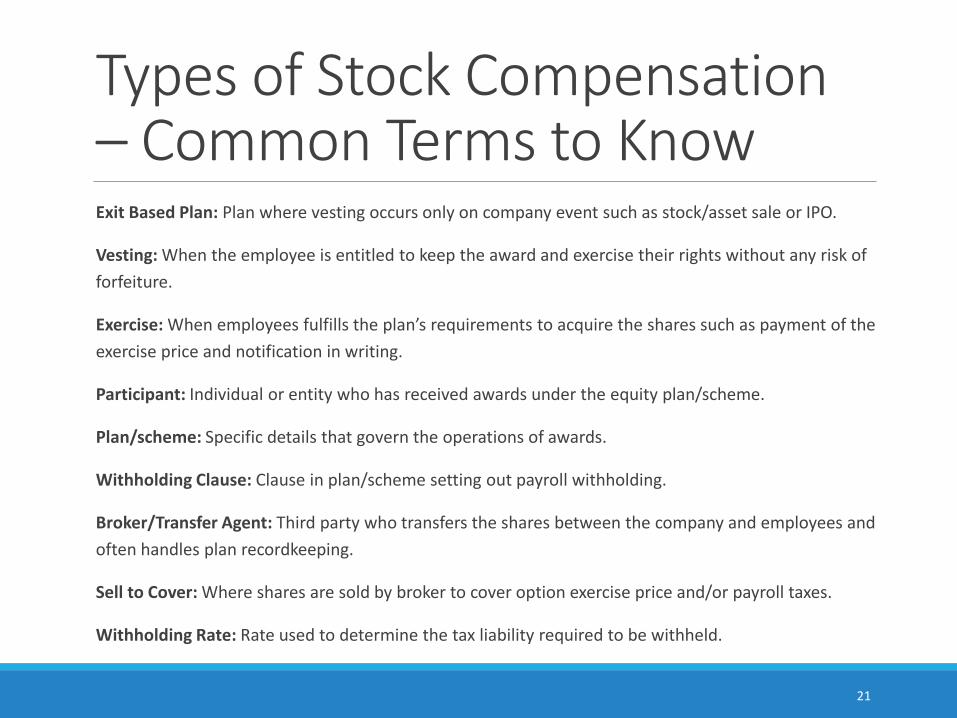

Types of Stock Compensation – Common Terms to KnowExit Based Plan: Plan where vesting occurs only on company event such as stock/asset sale or IPO.

Vesting: When the employee is entitled to keep the award and exercise their rights without any risk of

forfeiture.

Exercise: When employees fulfills the plan’s requirements to acquire the shares such as payment of the

exercise price and notification in writing.

Participant: Individual or entity who has received awards under the equity plan/scheme.

Plan/scheme: Specific details that govern the operations of awards.

Withholding Clause: Clause in plan/scheme setting out payroll withholding.

Broker/Transfer Agent: Third party who transfers the shares between the company and employees and

often handles plan recordkeeping.

Sell to Cover: Where shares are sold by broker to cover option exercise price and/or payroll taxes.

Withholding Rate: Rate used to determine the tax liability required to be withheld.

21

Types of Stock Compensation – International IssuesTaxation outside the U.S. varies widely

◦ Do employer homework before making any promises to make grants!

Examples of common issues◦ Stock options (sometimes) and RSAs (often) can be taxable at grant

◦ Tax withholding may be required

◦ Some countries assess the employer for the taxes if there is a failure to withhold

◦ Employer social taxes can be high and uncapped

◦ ISOs and ESPP do not receive preferential tax treatment outside the U.S.

◦ Employees who move overseas will likely have a trailing tax liability and will owe taxes to the U.S. even if the exercise occurs after they are established elsewhere, even if they are not U.S. citizens

◦ Securities, labor laws and foreign exchange laws should be reviewed

22

State Taxation of Stock Compensation

Most states follow U.S. federal taxation of stock compensationo Timing of taxation

o Amount subject to taxation

Exceptions:o Pennsylvania does not provide tax favorable treatment for• Incentive Stock Options (ISOs)

• S423 Employee Stock Purchase Plans

o Ohio requires withholding for disqualifying dispositions of shares from ISOs and ESPPs

o State level tax favorable treatment for stock options that meet certain conditions• Hawaii

• Rhode Island

23

State Taxation of Stock CompensationFederal:

◦ 22% on supplemental income paid in the year up to $1,000,000

◦ 37% on supplemental income paid in the year over $1,000,000

State:◦ California – 10.23% (bonuses and stock compensation), 6.6% other supplemental

income

◦ New York – 9.62%

◦ Some states do not have supplemental withholding rate. Employers should withhold at W4 (or state equivalent) withholding rate

State payroll taxes◦ For example, CA SDI, Oregon Transit Tax, etc. usually apply

Local taxes:◦ Varies

24

Local and Municipal TaxesDo not forget local taxes such as:

◦ State disability and similar payroll taxes

◦ California, New Jersey, Pennsylvania

◦ Local city and municipality taxes

◦ New York City

◦ Pennsylvania townships and school districts

25

In 2019, the Tax Foundation

estimated that there are approx.

4,964 local income taxes in

the U.S.

Deposit RulesIn general the Federal tax deposit rules for stock compensation follows the company’s regular deposit schedule; BUT if the cumulative Federal tax deposit for all employees exceeds $100,000, the amounts withheld must be deposited with the IRS by the next business day

Federal tax deposit generally includes:

Some states have similar rules; e.g.◦ California: Next day deposit required if subject to the Federal next day

deposit plus $500 in California PIT

26

• Federal income tax withheld• Social security withheld• Medicare tax withheld

• Employer’s portion of social security • Employer’s portion of Medicare

Deposit Timing For Stock CompensationTax event date requiring Federal deposit:

◦ Incentive stock options: none

◦ Non-qualifying stock options: settlement (if no later than the third business day after exercise)◦ 2003 IRS Field Directive*

◦ For this purpose business day = day stock exchange is open

◦ RSAs: vest date unless s83b election made

◦ RSUs: release date

◦ Employee stock purchase plan: none

*Assertion of the Penalty for Failure to Deposit Employment Taxes Field Directive March 14, 2003

27

How The Use Of Stock Compensation Can Trigger Nexus

28

Employee WithholdingExplanation of How Employer Nexus is Triggered

- Employment Mobility

- Permanent Establishment

- General Activity and Time

29

Employee WithholdingExamples

Activity in Location◦ Management

◦ Sales

◦ Operations

Time in Location

30

Employee WithholdingTelecommuting Issues and Challengeso Formal policies increase awareness

o Nexus triggered (impact on other taxes)

o Potential double-taxation

o Key point: Before implementing a telecommuting policy, understand the tax profile and its impact on employees and the company.

o Evaluate an employee’s “work state” location.

31

Implications and Issues Related to Corporate Income Apportionment

Payroll Factors: General Rules◦ Uniform Division of Income for Tax Purposes (“UDITPA”) § 13

◦ The payroll factor is a fraction, the numerator of which is the total amount paid in a state and the denominator is the total amount paid everywhere during the tax period.

◦ Compensation includes wages, salaries, and other compensation (i.e. equity awards, bonuses) paid for services to the taxpayer.

◦ Payroll “paid” should be determined by the normal accounting methods of the business so that if the taxpayer “accrues” such matters the payroll should be treated as “paid” for purpose of UDITPA § 13.

33

Implications and Issues Related to Corporate Income Apportionment

Alternative Methods or Discretionary Adjustments

◦ Uniform Division of Income for Tax Purposes (“UDITPA”) § 18◦ If the apportionment provisions of the Act do not fairly represent the extent of the Taxpayer’s business

activities within the state, the taxpayer may petition for or the [tax administrator] may require, in respect to all or any part of taxpayer’s business activity, if reasonable:

◦ Separate Accounting

◦ The exclusion of any one or more of the factors

◦ The inclusion of one or more additional factors which will fairly represent the taxpayer’s business activity in the state, or

◦ The employment of any other method to effectuate allocation and apportionment of the taxpayer’s income

34

Corporate Income, Franchise, and Sales Tax Exposures“Doing Business” vs. “Transacting Business”

◦ “Doing Business” – J.C Snavely & Sons, Inc. v. Wheeler◦ A corporation is essentially doing business in any state where it “transacts some substantial part

of its ordinary business”

◦ Four criteria to consider:

◦ Whether the corporation pays state taxes

◦ Whether it maintains property, employees, inventory, bank accounts, etc. in the state

◦ Whether it makes contracts in the state

◦ Whether its management functions in the state are pervasive

35

Corporate Income, Franchise, and Sales Tax Exposures“Doing Business” vs. “Transacting Business”

◦ “Transacting Business” - Cal. Corp. Code § 191◦ Entering into repeated and successive transactions of its business in this state, other than

interstate or foreign commerce.

36

Corporate Income, Franchise, and Sales Tax ExposuresEmployee Withholding Creates a Paper Trail

◦ Track employees’ location(s) to ensure accurate employer withholding reporting/withholding obligations

◦ Issues under payroll review or audit

37

Corporate Income, Franchise, and Sales Tax ExposuresSpecific Examples

- Neighboring States◦ New York / New Jersey

◦ Kansas / Missouri

◦ Locality Tax Requirements

38

State Legislation of NoteWayfair: June 21, 2018

- States rights to charge tax on virtual purchases.

Quill Corp. v. North Dakota

- Physical Presence

Voluntary Basis

- Individual Tax Returns

Amazon in 2017

- Agreement to collect

39

Sourcing of Income Earned vs. recognized

◦ Earned over time

◦ Recognized at a specific point in time

Extent of taxation and withholding is dependent on residency status◦ In general, states tax:

◦ Residents on worldwide income

◦ State tax credits may be available

◦ Non-residents on sourced income

40

40

U.S. Income Tax Sourcing RulesSince January 1, 2006 Federal sourcing is based on U.S. workdays from grant to vest

Some treaties state otherwise:◦ U.S.: Canada

◦ U.S.: Japan

◦ U.S.: U.K.

Specific grants may require different sourcing◦ E.g., an award granted for a project undertaken in a particular location

State sourcing may differ◦ E.g., Arizona, California

41

Sourcing PrinciplesThe general rule is that income is sourced where it is earned or over the “earnings period”

Each state may have a different view of the earnings period particularly for stock compensation

42

Earned Paid

Base salary Daily Bi-weekly or semi-monthly or monthly

Bonus Over bonus performance period or related to the achievement of a goal

Quarterly or annually or achievement of target

Commission Related to a sale After sale close

Pension Daily Post retirement

Stock options From grant to vest/exercise Upon exercise

Restricted Stock Units

From grant to vest/release Upon release

Each double tax treaty is different

U.S. has double tax treaties with almost 70 countries

BUT generally an individual is tax exempt if :◦ The employee is present in the host country for 183 days or less,

◦ In the taxable year concerned or rolling 12 month period

◦ The employee compensation is paid by or on behalf of an employer which is not a resident of the host country, and

◦ The compensation is not borne by a Permanent Establishment (PE) or fixed base which the employer has in the host country

◦ Economic employer

43

Totalization AgreementsSimilar to double tax treaties but focus is social security

U.S. has totalization agreements with 27 countries

Generally, individual can be covered in “Home Country” for up to 5 years

◦ Requires a document from the social security authorities known as Certificate of Coverage

If “local” employee in new country, income can be subject to social tax in new country only

May mean that income tax and social tax are sourced differently for the same income

44

State Sourcing Of Stock CompensationInconsistency in allocation methods; e.g.

◦ Workdays from grant to vest◦ Georgia

◦ New York

◦ Workdays from grant to exercise◦ Arizona

◦ California

◦ Exceptions◦ Illinois - Five-year special rule

◦ North Carolina - location of grant

◦ Ohio - Degree of appreciation method

Most states do not have designated allocation methodology◦ Default to Federal allocation rules?

45

There are 41 states in the U.S.

that charge an income tax

plus District of Columbia

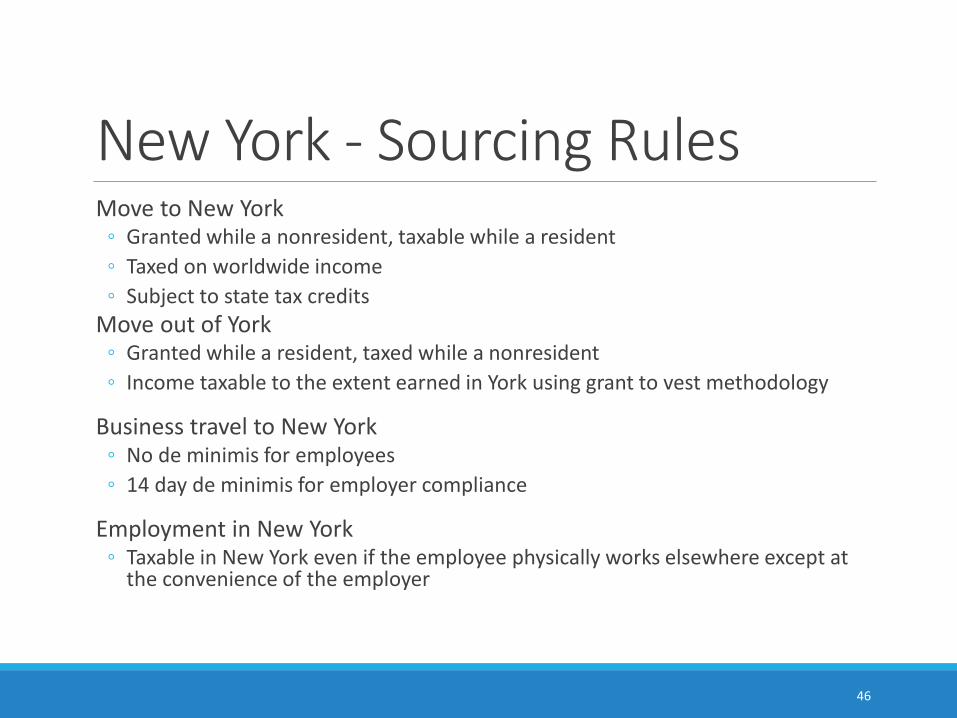

New York - Sourcing RulesMove to New York

◦ Granted while a nonresident, taxable while a resident

◦ Taxed on worldwide income

◦ Subject to state tax credits

Move out of York◦ Granted while a resident, taxed while a nonresident

◦ Income taxable to the extent earned in York using grant to vest methodology

Business travel to New York◦ No de minimis for employees

◦ 14 day de minimis for employer compliance

Employment in New York◦ Taxable in New York even if the employee physically works elsewhere except at

the convenience of the employer

46

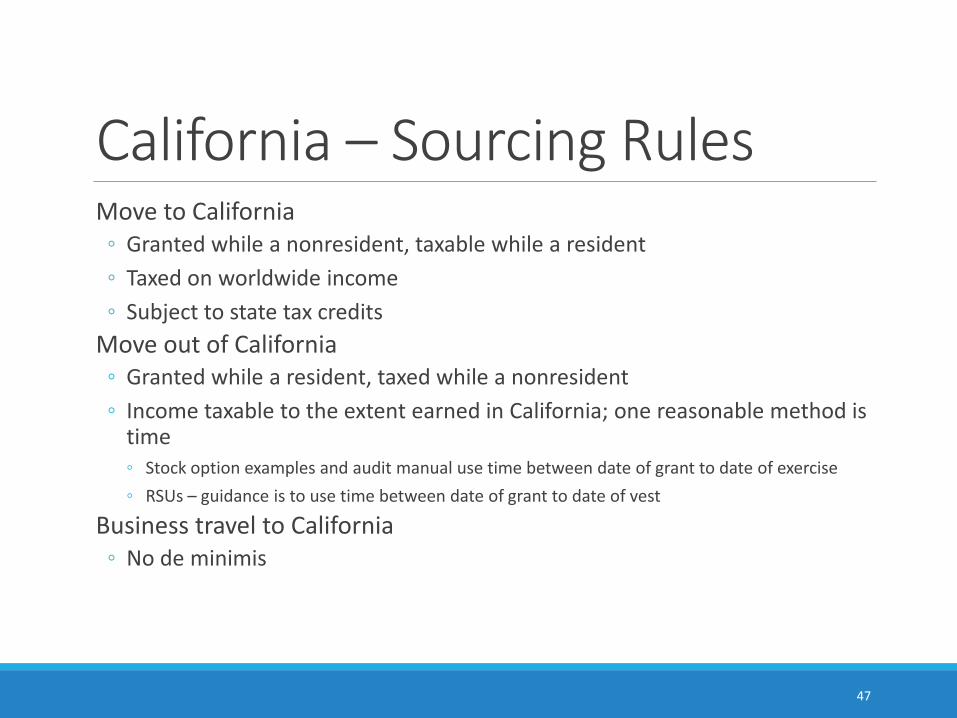

California – Sourcing RulesMove to California

◦ Granted while a nonresident, taxable while a resident

◦ Taxed on worldwide income

◦ Subject to state tax credits

Move out of California◦ Granted while a resident, taxed while a nonresident

◦ Income taxable to the extent earned in California; one reasonable method is time◦ Stock option examples and audit manual use time between date of grant to date of exercise

◦ RSUs – guidance is to use time between date of grant to date of vest

Business travel to California◦ No de minimis

47

Administrative Challenges And Practical Solutions

48

Examples of StatesCalifornia

New York

Illinois

49

Trends in AuditSpecific Examples of States and Audit Practices

Compensation Matching

- Reporting

- Withholding

Sourcing based on employment role

50

Trends in AuditPolicy Issues Companies Need to Examine

◦ What companies and their tax staffs can do if employees have cash flow problems or file returns in multiple states.

◦ Tax Equalization

◦ Tax Protection

51

Background on HR, Stock Plan, and Relevant Payroll SystemsWhat Tools are Available and Systems Limitations

Software Solutions

- HRIS

- Travel

- Equity Withholding

52

Background on HR, Stock Plan, and Relevant Payroll SystemsHow to Make These More Sophisticated

All-inclusive software solution integrations

- Employment Management, Travel, and Tax

53

Background on HR, Stock Plan, and Relevant Payroll SystemsHow Tax Specialists Can Help in this Effort

Diagnostic Reviews

Projections and Automation

Accuracy

Timelines

54

Challenges with Employee MovementCreating Internal Mechanisms to Track Employee Movements

◦ How Tax Specialists Can Help in this Effort

◦ Implementation of Software Solutions

◦ Travel and Threshold Matrix

◦ Tax Planning

55

Challenges with Employee MovementWhat Companies are Doing

◦ The habit of monitoring only executives and the inherent dangers

◦ Situations in which execs move from low-tax to high-tax states

◦ Need for additional controls

◦ Exposure

◦ Paper trail

◦ Employee Satisfaction

◦ Lack of Tax Policies

56

Questions?

Joseph S. Pancamo, CPA

Global Employer Services

BDO USA, LLP

312-233-1840

57

Marlene Zobayan

Rutlen Associates LLC

650-868-9282