strategic audit: adobe systems inc

TRANSCRIPT

Kiana NakagawaMay 2015

Adobe Systems, Inc. Strategic Audit

Table of Contents:

Overview..............................................1Corporate Governance........................5Board of Directors.............................8Top Management...............................10External Analysis...............................12External Forces..................................13Industry Analysis..............................18Further Notes.....................................23Internal Analysis...............................25Resources............................................27Functions............................................28Alternatives........................................33Autodesk & Beyond..........................45Implimentation..................................46Evaluation & Control........................48Annotated Bibliography....................51

1

Overview John Warnock and Charles Geschke started

Adobe in 1982. Their universal page description caused a

technological paradigm shift, cutting creatives’ dependence

on commercial printing companies. In this manner, Adobe

broke into the creative software market and derived its first

success by exploiting first-mover advantage and the positive feedback loop1. Then, in 1999,

Adobe established itself as the leader in visual media software when it overtook competitor,

Quark, in a format war2. This was accomplished because of Adobe’s strategic move to offer

its format reader–Acrobat Reader– for free which catalyzed the network effect. Since then,

Adobe has been adopted as an industry standard, creating a virtual monopoly over visual,

creative software. Adobe increased the utility and perceived value of its products by bundling

related products: Bridge, Illustrator, InDesign, Photoshop, ImageReady, Version Cue, and

Stock Photos. This essentially locked in customers by increasing customer switching costs;

customers would need to relearn six software programs to do work efficiently if they switched;

even now, there are individual program substitutes, but nothing with across-the-board

compatibility like Adobe.

In 2013, Adobe shifted to “the cloud” and stopped producing shrink-wrapped

software. This transformed its business model and pricing structure. As the current leader,

implementing this disruptive technology has upset Adobe’s customers. Over 26,000 users

signed a petition to eliminate the mandate of the subscription model (Change). Though this

may be a short-term response, a survey conducted by CNET showed that 93% of Adobe users

are looking for alternatives to Adobe’s software. 1 A positive feedback loop happens when network effects start to take hold; wherein the network of com-plementary products is a primary determinant of the demand for an industry’s product (Jones Hill 233).2 Format wars are the battles to control the source of differentiation and thus the value that such differen-tiation can create (Jones Hill 230).

Warnock (Left) & Geschke (Right)

2

The switch created a more predictable income model for Adobe. This move also added

further protection for Adobe. There is not a way to calculate the exact amount of losses, but

Adobe has lost profits from the piracy and illegal ripping of its software. Moving to the cloud

has cut off many of the channels for its programs to be stolen and illegally downloaded.

Plus, “it is better for the company to develop disruptive technology [that] cannibalize[s] its

established sales base than to have the sales base taken away by new entrants” (Jones Hill 255).

Adobe’s mission is to change the world through digital experiences through the company’s addressed market segments

while: achieving and maintaining an above-average return on investment

for shareholders measured in terms of return on equity, earnings per share,

revenue growth, and operating profit; maintaining or achieving the number

one or two position in addressed market segments in terms of market

share, customer satisfaction, revenue generation, product margin, product

functionality, and technological leadership; treating all employees with

respect and rewarding both group and individual performance that exceeds

commitments and expectations; being a good corporate citizen in the local

and national locations where the company produces, sells, and services its

products.

Revolutionize how the world engages with ideas and information.

3

Current Position Adobe had $4.1 billion in sales for 2014 with an operating

income of $4.9 million. Profit margins shrank from 7.2% in 2013 to

6.5% in 2014, which is an even more significant decrease in profits

compared to 2010 – before Adobe switched to the cloud-based

business model – when profit margins were 20.4%.

Adobe’s current strategies have stemmed from its mission

and vision. Adobe is a focused differentiator using an international

strategy13 to push its current growth objectives. CEO Shantanu

Narayen explains Adobe’s current mindset as follows: “Traditionally,

your company gave you a product and your job was to market it –

how to position the brand, messaging and allocating media spend,

for example. The new questions to ask are: Are we thinking broadly

enough about what our product is? How can I bring together the

power of digital marketing to dramatically improve the product

experience?”

Adobe has three business segments:

1. Creative Cloud (18 solutions) – graphic design, video editing,

and web development applications

2. Marketing Cloud (6 solutions) – web analytics solutions: social,

advertising, media optimization, targeting, web experience

management, content management

3. Publishing (9 solutions) – created for authors, instructional designers, and eLearning

3 A global strategy that can be implemented when there are low cost-pressures coupled with low pressures to localize

Adobe Systems, Inc.NASDAQ: ADBE

Flash Facts

Trading:$77.02 / share

P/E:126.3

Market Cap:$38.4 billion

Q1 Earnings:$1.11 billion (surpassed target range, $1.05 - $1.10 billion)

Subscriptions:28% increase from Q1 2014

Figures as of May 8, 2015

4

The doubt surrounding whether or not the switch to the cloud was successful seems to have

been put to rest after Adobe

released its 10-K for 2014.

Revenues generated by

subscriptions surpassed

revenues generated by

products.

The future looks promising

for Adobe.

Revenue 2013 2014

Products 2,470,098 1,627,803

$ (000s) Change (872,745) (842,295)

% Change (26.11%) (34.10%)

Subscriptions 1,137,856 2,076,584

$ (000s) Change 464,650 938,728

% Change 69.02% 82.50%

Adobe’s Marketing Cloud has taken off, but its Publishing Cloud has yet to redeem itself after

a recent re-design. Methods to buffer and balance Adobe’s offering-portfolio are mentioned in

the alternatives suggested later in the paper.

63%

33%

4%

REVENUE STREAMS 2014

65%

30%

5%

REVENUE STREAMS 2013

DigitalMedia

DigitalMarketing

Print &Publishing

5

Corporate Governance

6

Adobe, driven by CEO, Shantanu Narayen, has been increasing profits and long-

term profitability by participating in the consolidation trend (via acquisitions) of its

industry; developing new markets through diversification of its business efforts (by getting

into marketing and customer relationship management (CRM) software solutions); and

by securing market share in the creative-solutions software market and taking market

share in the software for CRM market. “Pursuing strategies that maximize the long-term

profitability and profit growth of the company is… generally consistent with satisfying the

claims of various stakeholder groups” (Jones Hill 382).

7

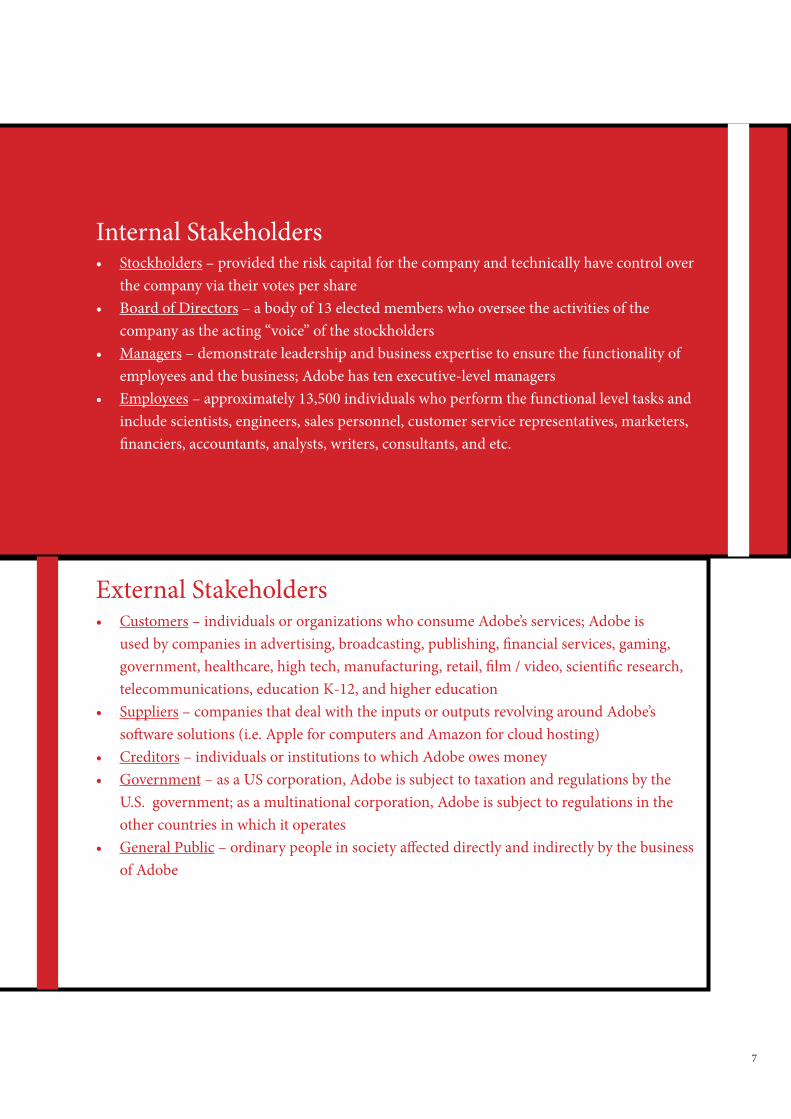

• Stockholders – provided the risk capital for the company and technically have control over the company via their votes per share

• Board of Directors – a body of 13 elected members who oversee the activities of the company as the acting “voice” of the stockholders

• Managers – demonstrate leadership and business expertise to ensure the functionality of employees and the business; Adobe has ten executive-level managers

• Employees – approximately 13,500 individuals who perform the functional level tasks and include scientists, engineers, sales personnel, customer service representatives, marketers, financiers, accountants, analysts, writers, consultants, and etc.

• Customers – individuals or organizations who consume Adobe’s services; Adobe is used by companies in advertising, broadcasting, publishing, financial services, gaming, government, healthcare, high tech, manufacturing, retail, film / video, scientific research, telecommunications, education K-12, and higher education

• Suppliers – companies that deal with the inputs or outputs revolving around Adobe’s software solutions (i.e. Apple for computers and Amazon for cloud hosting)

• Creditors – individuals or institutions to which Adobe owes money• Government – as a US corporation, Adobe is subject to taxation and regulations by the

U.S. government; as a multinational corporation, Adobe is subject to regulations in the other countries in which it operates

• General Public – ordinary people in society affected directly and indirectly by the business of Adobe

External Stakeholders

Internal Stakeholders

8

As an American corporation, Adobe’s bylaws revolve around its

obligations to stockholders, who determine and communicate to C-level

management through the Board of Directors. Adobe has thirteen board

members: three of whom have ties to Adobe, while the remainder have

business external to Adobe. Adobe’s board members bring a diverse array of

input to the company which allows Adobe to keep on top of – and even get

ahead of – external trends.

The board acts a fiduciary for stockholders and aligns interests between

stockholders and managers via appropriate incentives, which are spelled out

in the bylaws. These guidelines promote “transparency and the highest ethical

business practices [including honest and ethical conduct; full, fair, accurate,

timely, and understandable disclosure; and compliance with governmental

laws, rules and regulations], enabling a relationship of trust among Adobe’s

board, management team and stockholders” (Adobe).

Adobe is currently paying the price of investing in future profit growth;

its profitability has slowed due to the change in business plan (led by CEO

Narayen) and the initial investments required for continued development.

This may render some of its stakeholders unhappy or at least wary because

of a shrinking profit margin, but this is seen as a short-term issue that has

not deterred investors and has arguably pleased stockholders because of the

perceived long-term benefits. According to Adobe’s P/E ratio, investors are

willing to pay 126.30 times what each share is earning, meaning stockholders

could capitalize on their stocks for handsome amounts.

Board of Directors

Dr. Charles M. Geschke Chairman, Co-founder, Adobe Systems, Inc.

Dr. John E. WarnockChairman, Co-founder, Adobe Systems, Inc.

Shantanu Narayen President & CEO, Adobe Systems, Inc.

Amy BanseSr. VP, Comcast Coproration

James E. DaleyRetired, Executive VP, Electronic Data Systems Corporation

Dr. Robert Sedgewick Professor of computer science, Princeton University

9

As a U.S. corporation, Adobe files quarterly and annual reports

with the SEC which are prepared according to GAAP and are audited by an

independent and accredited accounting firm, as per U.S. regulation. This

satisfies governmental and creditor claims and assures many of the other

external stakeholders, like suppliers and the general public that Adobe’s

business is legitimate.

Adobe’s executive management team strives to run its business in a

manner that maximizes long-term stockholder interest with the guidance of

Adobe’s Board of Directors.

Robert BurgessFormer Chairman, Macromedia, Inc.

Michael R. CannonRetired, President, Dell Corporation

Laura DesmondGlobal CEO, Starcom Media Vest Group

Dan Rosenweig President & CEO, Chegg.com

Edward W. BarnholtRetired Chairman, President, & CEO, Agilent Technologies

Frank Calderoni Executive Advisor, Cisco

Kelly BarlowPartner, ValueAct Capital

10

Adobe’s executives work to maximize long-term stockholder interests by creating

superior solutions that satisfy old and new customers. This increases profits and allows for

Adobe to offer competitive salaries and compensation to the programmers and personnel who

create and market superior products. This continues cycling onto itself to create the sought-

after, long-term stockholder and stakeholder benefits.

CEO Narayen guided Adobe through dozens of acquisitions, the introduction of a new

business unit (Marketing Cloud), the transition to the cloud, and consequently, a new revenue

model. Changes like these can result in loss of leadership due to shareholder activism – and

there was a brief petition going around to have Narayen removed – but through Narayen’s

management, which called for complete transparency of the shifts and clear communication

about the change in control measurements (focusing on usage over profits), shareholder

worries subsided, and the company’s worth reached an all-time high in April 2015, with a

market cap of $39.55 billion.

Through thoughtful direction and execution of growth strategies– which maintained

transparency–and holding accountability for meeting milestones, the executives have been

able to create value for all of Adobe’s stakeholders.

Top Management

11

Adobe Leaders-Joined Adobe 1998 -Formerly COO where he led $3.4 billion acquisition of Macromedia 2005-Serves on boards of Pfizer, Inc. and Haas School of Business, University of California at Berkeley. -2009, led $1.8 billion acquisition of Omniture, Inc.

Shantany Narayen President & Chief Executive Officer

Michael DillonSenior VP, General Counsel & Corporate Secretary

Ann LewnesSenior VP & Chief Marketing Officer

Donna MorrisSenior VP, People & Places

Matt ThompsonExecutive VP, Worldwide Field Operations

“Great legal teams thrive on change.”-Joined Adobe 2012-14 years at Sun Microsystems (prior to acquisition by Oracle) and served as general counsel and corporate secretary from 2004 – 2010

“Great marketing is equal parts data and creativity.”-Joined Adobe 2006 from Intel-Member of the American Advertising Federation’s Hall of Achievement

“Our people make Adobe exceptional.”-Joined Adobe in 2002 through Accelio acquisition -Promoted in 2007-Named a Top 10 Breakaway HR Leader in 2013 by Evanta-Formerly a board member of Second Harvest Food Bank

“Customers inspire us.”-Joined Adobe 2007-Member of board of directors at Appirio and at Special Olympics Northern California

Mark GarrettExecutive Vice President & Chief Financial Officer

“Business model innovation keeps us resilient.” -Joined Adobe 2007-Served as SVP and CFO of EMC’s Software Group-Sits on board of directors of Informatica Corp. and Model N, Inc.

Bryan LamkinSenior VP, Technology & Corporate Development

“We’re inventing the future through art and science”-Rejoined Adobe 2013 after previously serving 1992 – 2006 -Established Adobe’s Creative Suite and Photoshop businesses

Gerri Marin-FlickingerSenior VP & Chief Information Officer

“IT innovation drives the business.”-Joined Adobe 2007 as CIO and Senior VP-Former CIO at VeriSign, Network Associates, McAfee-Member of Wall Street Journal CIO Natwork and Sierra Ventures CIO Advisory Board

Brad RencherSenior VP and GM, Digital Marketing

“Digital moments are built in milliseconds.”-Joined adobe 2009 via Omniture acquisition -Promoted to SVP and GM in 2010

David WadhwaniSenior VP & GM, Digital Media

“Create with impact.”-Joined Adobe 2005 through Macromedia acquisition -Member of the Fine Arts Museums’ Board of Trustees

12

External Analysis

13

Opportunities

There are over 80 million members of the Millennial generation in the U.S. alone (U.S.

Chamber of Commerce Foundation). These digital natives are subject to increasing pressures

for digital literacy. “According to one estimate, as of 2009, advertising-supported Internet

services directly or indirectly employed three million Americans, 1.2 million of whom hold

jobs that did not exist two decades ago” (Department of Commerce). In order to differentiate

in the job market, knowledge of software manipulation, database use, and analytics will be

necessary (Ritz).

The number of start-ups took a dip in 2012, but have been rebounding ever since, with

over 300 million startups every year (Webb). Many of these companies will be going online

and entrepreneurs will be looking for ways to create content and track performance.

Historic preservation is going digital. “With creativity, there are ways to marry

preservation with 21st century comfort and convenience” (Bedard). There are over 35,000

museums in the U.S.; that is more than all the McDonald’s and Starbucks combined

(Ingraham). The masses are becoming more aware of the damage that is caused to historic

sites because of tourism, and sites are trying to find ways to combat the issue without being

subject to negative economic repercussions (Eadington 8).

Spending on software in big emerging markets (Brazil, Russia, India, China: BRIC) is

increasing by as much as 10% each year, as compared to the 2% growth in the U.S., Europe,

and Japan (BSA Software Alliance). Production of software in the BRIC nations is also

increasing, but as these systems are small and primitive, acquisitions and or partnerships with

native publishers could lead to a strong foothold into a country.

Visual effects in media are relying more and more on 3D software, and 3D printing

External Forces

14

looks like it may be the next “big thing”. “The 3D printing market just aggregated an estimated

revenue of 3.3 billion US-dollars worldwide in 2014. That´s over a third more than in the

previous year 2013” (Klarmann). Also, formatting and technical standards in this industry

have yet to be set.

Mobile technology is improving and becoming more accessible, with global revenue

from apps expected to rise by around 62% to $25 billion (Wolonick). This has three

implications: creators need means to produce these applications; advertisements are taking on

a new platform; mobile technology is changing the way users interact with media (i.e. multi-

touch gestures, 3-D designs are more comprehensible, work leaves the desktop). Software

applications are condensing to run on the new, smaller, mobile processors because high-

memory products cannot run efficiently.

This uptake of mobile technology has other consumer consequences that companies

need to be prepared to undertake. With 1.6 billion users worldwide, user expectations for

app performance are increasing. This increases the stakes amongst competition when 30%

of respondents to Kleiner Perkins’s survey said that they would spend more money with an

organization that had a good mobile app (Brauer). Along with increased incentive to produce

superior applications, there is a smaller window of opportunity for companies to prove their

worthiness. With the average person looking at his or her smartphone over 150 times a day,

there are too many things competing for the attention of consumers (Keyes). Attention spans

have shrunk from 12 seconds in 2000 to a mere 8 seconds in 2013 (Keyes). This trend has

been snowballing for decades. In 1976, “[Steve] Jobs knew that consumers did not want to

buy a computer they would have to learn how to use over the course of many months” (Mars).

Apple products are so simple to use today that even babies are able to manipulate them with

precision. Computer scientist, Doug Englebart, noted back in the 1960s (much to his dismay)

that consumer markets prioritized user-friendly devices over learnable devices even if the

15

latter, learnable devices could do more effectively complete a task once mastered (Mars).

Adobe currently offers software in the “learnable” category. There is yet to be a standard

to capture customers on this platform and become the standard for the mobile devices of

creatives, marketers, and publishers.

New advertising methods are needed to effectively exploit mobile platforms and

to evaluate a campaign’s performance. According to Edelman Berland, more than 80% of

marketing professionals are receiving informal digital training and only 29% of respondents

have faith in the measurement approach used to monitor and quantify the effectiveness of

marketing efforts (Konrad). Marketers are gravitating toward software that can consolidate

digital platforms and help customize messages depending on said platforms. These types of

software systems are categorized as Software as a Service (SaaS), and its demand is growing.

According to a study done by Siemer & Associates, 83% of companies either have adopted

or expect to adopt SaaS technologies in the immediate future (Roe). Furthermore, customer

relationship management (CRM) SaaS solutions are the most requested applications across

enterprises worldwide; the global CRM market grew 12.5% between 2011 and 2012, resulting

in an $18 billion industry (Roe).

Whether or not to move to the cloud is a business decision that consumers have

been adopting by default. At first there was a lot of resistance, but now cloud computing is

becoming more accepted and enables SaaS systems to bundle, increasing value and usability.

Cloud computing also enables this type of work to become even more mobile. Projects,

statistics, and tools are no longer anchored to hardware; this circles around again to how

mobile technology is improving and gaining popularity.

The software industry is aging, and there have been trends of consolidation: trends

in which Adobe has been actively participating. Adobe has engaged in more than 12 major

acquisitions in the past five years (Adobe 2014). There are many promising companies that

16

could be bought or taken over.

Threats

Exchange rate fluctuations can have major repercussions for companies that operate

on the global scale. Adobe experienced a loss of $8.2 million in 2014 due to foreign currency

fluctuations and hedges (Adobe 2014). That is a fraction of a percent of Adobe’s total revenue,

but the company should continue to hedge against such losses.

Cyber-criminals and cyber-espionage are advancing and the stakes are growing as

more information is going online. Malicious cyber activity contributes to:

• The loss of intellectual property and business confidential information

• The loss of sensitive business information, including possible stock market manipulation

• Opportunity costs, including service and employment disruptions, and reduced trust for

online activities

• The additional cost of securing networks, insurance, and recovery from cyber attacks

• Reputational damage to the hacked company (McAfee Research Team)

This type of activity leads to $400 billion in annual losses globally (McAfee Research

Team). The actual losses due to piracy and pilferage (inventory shrinkage) are difficult to

estimate, as many companies do not know the extent of their losses.

Competitors and ownerless, open-source contributors are building alternative creative

software solutions. Open-source14 solutions sprout up everywhere and can have significant

impacts on revenues. There are numerous free solutions out there for single Adobe products

with more being introduced and updated every year. These alternatives have the potential

to gain widespread acceptance, jeopardizing the monopolistic hold Adobe has had on the

creative-solution software market. This makes users scruitinize the value they derive from

Adobe’s services and poses a major threat to Adobe’s position.

4 Open-source refers to a source code (what is essentially software) that is freely available and can be distributed and modified by anyone.

17

Adobe’s business depends on its patents and other intellectual property. Intellectual

property rights differ from country to country. This affects Adobe’s capacity to protect its

products/ services and causes problems with third-party affiliates. This can inhibit growth and

day-to-day business in general. The infringement of copyrighted material results in damaging

losses and can usually only be resolved by going through costly legal channels. One of the

more publicized events for Adobe is its pending lawsuit against Forever 21. Adobe and other

creative-solution software companies filed a lawsuit against the California-based retailer in

January 2015 (Niccolai). Forever 21 denies the allegations and is asking for a trial jury on the

matter (Niccolai).

As mentioned before, there have been trends of consolidation. This is a threat to

small companies as it increases the viability of being acquired, possibly through a hostile

takeover. Adobe is not a small company, but considering how big other players are, even it

must acknowledge this risk. As an example, Apple has more than $155 billion in cash and

could easily buy Adobe (Apple). This acquisition would allow for Apple to fix Flash and have

a superior script running on its products; secure its hold on creatives and creative agencies by

rewriting Adobe to only be compatible with Apple products (locking out computers running

on Linux or Windows); and Apple could drive down Adobe’s prices and secure its monopoly

by making it impossible for competitors to enter this market.

18

Industry Analysis The global software and services industry is growing at a rate of 5.8%, reaching

a value of $3.0 trillion in 2014 (Market Line 7). It is highly fragmented; the four largest

companies (IBM, Google, Microsoft, and HP), which make up less than 10% of the market,

operate alongside many smaller companies (Market Line 11). The industry is going through

a period of commoditization15, made evident by trends of mergers and acquisitions (M&A)

and of universal transcriptions (standardized formats / codes) which can make it difficult to

create something “completely new”. This makes it even more challenging for companies to

differentiate when users prefer homogenous end-products because of the network effect and

the guaranteed “compatibility it creates between products and their compliments” (Jones Hill

231).

Software companies maintain a lot of the value with regards to Porter’s Five Forces

Analysis. Software companies license their products / services and variable costs are low.

The first copy of a digital good / service is high, but “[t]he variable costs of software licenses

are close to zero” and, as another property of digital goods, software can be copied easily

without compromising quality

(Bauxmann 19).

Participants in the

software industry realize that they

are partaking in a winner/first-

creator-takes-all market.

5 The process by which the eco-nomic value of software distinguishes in terms of attributes (uniqueness) and end up becoming simple commodities in the eyes of consumers.

19

Buyer Power: Moderate (buyers are not price sensitive but large buyers exist for these

differentiated products)

• Products are differentiated. There are dozens of companies that able to make billions of

dollars in the industry—without competing on price—because each company is able

to capitalize on specific market segments without interfering with another’s business

(Gartner Research).

• Customers are not highly

price-sensitive (e.g.

Microsoft suite’s online

price is $219.99).

• There is low risk of backward integration: creating software takes a considerable amount of

initial funding and expertise.

• Software is not highly substitutable (the alternative to many software solutions would be to

do things manually, which would be less efficient in terms of time and errors, and be lower

in quality).

• There exists large buyers (multinational companies or government entities) may wield

significant power; if a large client drops a software, revenues could take a huge hit.

However, the cost to service a large corporation (over a small buyer) differs only in service

costs (Bauxmann 19). As indicated previously, the variable costs to reproduce software are

minimal.

• Both large and small firms may serve many small businesses or individuals who have less

bargaining power.

• If there are new / smaller companies, buyers may still go with the name-brand company, as

it reflects a reliable reputation.

• Switching costs are high for four reasons: (1) software is a complex product and

Company Software-type2013 Revenue

(Billions of $)

MicrosoftApplication software: functional-level

systems65.7

OracleEnterprise software: database

management systems29.6

IBMDevelopment software: consumer

software and hosting29.1

20

in switching, one would need to learn how to use the new software, which is time-

consuming; (2) the existing network has compatibilities that may be disrupted and would

need to be fixed, raising the costs involved; (3) there are disruption risks in transferring

data (a necessary step in switching) in which important information may either be lost or

corrupted; and (4) penalty fees may arise from terminating a license contract prematurely.

Supplier Power: Moderate (need experts that cost a lot, but there are numerous suppliers for

other components needed to run software production)

• Hardware suppliers are dependent on the industry. Though there are a limited number of

suppliers – which would usually indicate high supplier power – this is mitigated by the

fact that software is a complementary product to hardware; therefore, the “health” of the

hardware industry is, if not dependent, at least influenced by the software industry. “The

greater the supply of high-quality software applications running on these machines, the

greater the value of personal computers to customers, the greater the demand for PCs [or

Macs], and the greater the profitability of the personal computer industry” (Jones, Hill 60).

• Suppliers of expertise have a lot of power. Software engineers in the US average $75,000

and $90,000 salaries (U.S. News). The average American makes only $35,000 a year

(Durden).

• Suppliers of cloud hosts are increasing (McCue).

• Tangible inputs vary in availability and cost, depending on how specialized the software

engineering is. As a general statement, a computer could be all one needs to develop

software. However, costs for “providing services associated with the software, such as

consulting maintenance, and support” are not negligible and are often overlooked as a key

factor to the success of the software (Buxmann 19).

• Forward integration is not only inhibited by the financial burden of an initial investment

and variable support costs, but by the lack of qualified persons who can supply the

21

expertise (Rothwell).

New Entrants: Moderate (more people are capable of creating software without formal

education, but economies and benefits of scale give existing firms a head over new entrants)

• Technology enables entrepreneurs to easily create web-based and open-source models.

• Larger software companies have economies of scale (Gartner Research).

• Smaller software companies are highly specialized with customized services (Gartner

Research).

• Large companies experience benefits of scale: name recognition / reliability inhibit new

entrant (Porter 3).

• Need to create strong distribution relationships, which may not be particularly easy if a

firm does not have a big name

• Hyper-competition: if a firm cannot adapt / keep up, it will die (a start-up may miss

the new trend developing a solution to something from last week); rapid and dynamic

competition creates seemingly unsustainable advantage.

• Regulation varies drastically in this industry and depends on the nature / sensitivity of the

product / service

• Entry is achievable but M&A’s pose a threat to small companies’ survival

• Switching costs are high, as mentioned before.

• In 2012, seed investment deals in U.S. tech more than tripled to 1,700 from 2009, but there

was an estimated failure rate of 90% (Carroll).

Threat of Substitutes: Low (Software takes the place of doing things manually, but physical

items are now integrating capabilities that minimize the need for software).

• Increased value-added offerings / components that come with complementary products

act as substitutes and could be shrinking the size of a potential market (i.e. some cameras

have immediate image editing capabilities in its operating system and therefore eliminates

22

– or at least lessens – the need for application software).

• Other substitutes for software include doing things “by hand” or using manual input /

computational methods. This is quickly going out of fashion as pressures for efficiency and

usability increase.

Degree of Rivalry: Moderate (differentiation and industry growth results in lack of price

competition)

• Globally, this industry is expected to grow 27.2% over the next four years, reaching a value

of $3.748 trillion (MarketLine 1).

• Industry profit margins were 14.5% in 2014

• This industry group is fragmented, with large incumbents operating alongside smaller

companies, although diverse product portfolios and strong growth help alleviate rivalry

(MarketLine 13).

• There are high initial costs, but low variable costs, as mentioned before.

• Switching costs are high, as mentioned before.

• Diversification of existing companies is growing (via innovation and aforementioned

M&A) – eases pressure (Market Line 13).

• There are no real signs of price-based competition.

• Exaggerated posturing through personalities and egos (i.e. Steve Jobs’s public put-down of

Flash) (Jobs).

Competition is specialized, fragmented, and intense. At this point, Adobe still has

brand-loyal customers, but it should be wary of the fast industry growth rate. In 1999, Adobe

overtook Quark, which had 80% market share at the time, because Adobe innovated more

quickly and stayed on top of trends. If it does not want to lose its crown, Adobe’s managers

need to strengthen its inimitable value proposition to secure competitive advantage and

maintain its hold on the value it has spent over 25 years creating.

23

There exists a “software ecosystem” that contains a set of businesses that interact with

a shared market for software and services and acts as a single unit, underpinned by a common

platform. As an (over-simplified) example, consider the following:

Each level of this ecosystem has different external forces acting upon it: different

consumers, suppliers, substitutes, and new and existing competitors. There are also the

exchanges of information, resources, and artifacts going backward—up the value chain—from

the consumer. In regards to this perspective, understanding where Adobe lies in the value

chain has enabled it to find other opportunities on which to capitalize while creating more

barriers to entry by increasing the value and interconnectivity of its applications, driving up

switching costs for consumers.

Adobe’s production segment is the heart of value-creation for its customers. It uses

innovation to create high-quality software solutions for creatives, marketers, and publishers.

At its position in the larger value chain, Adobe is responsible for content creation (R&D),

content editing (production), and content bundling (marketing). It then transfers the final

services to the network, Amazon: Adobe’s cloud host which acts as the “distributor” in this

value chain. The software then is accessed by the “markets” which are businesses, marketers,

and individuals. There is another section along the value chain that does not interact with the

software but does receive the end results. These end persons or entities consume the products

of the software: websites, advertisements, movies, photos, etc.

Software-type

Platform Personal Computer / Tablet

Operating System MS Windows

Application MS Office

End-User Program MS Excel

Further Notes

24

By stepping back and looking at the larger value chain, Adobe found that it could

provide a solution and add value further forward in the chain: the link between the markets

and end consumers. In 2014, Adobe launched Adobe Marketing Cloud. One section of

Adobe’s actual consumers – marketers – needed more efficient ways to deliver, monitor, and

track the effectiveness of their campaigns across media platforms. As early as 2009, Adobe

began acquiring companies that had analytics software (Adobe). It then encoded these

software solutions to create a set of cohesive and compatible programs that could be bundled

and distributed.

Adobe’s production segment, or content-editing segment, is the center of gravity

around which Adobe’s success and other efforts revolve. It has capitalized on growth

opportunities by applying these competencies to other areas and business models.

Raw Materials Content Network Markets End

Consumer

- computers- facilities- labor

*see section below: Adobe

- hosts- distributors

-businesses- other service

providers

- end consumer or

media content

Content Acquisition/

Creation

Content Editing

Content Bundling

- program writing / buying

- formatting- compatability

- encoding

- Creative Suite- Marketing Suite

- Publishing

Value Chain for Software:

Component Examples:

Adobe’s Role in the Value Chain:

25

Internal Analysis

26

Adobe has been a leader for many years with over 43% of the global creative software

market share (Trefis Team). With increasing competition and major external influences,

Adobe has only recently undertaken major restructuring to reverse its weaknesses and amplify

its strengths.

Over 5,000 global companies use Adobe’s products and services; nine out of the top

ten retailers and banks and eight out of the top ten media outlets and auto manufacturers use

Adobe’s products and services (Company Profile: Adobe Systems Incorporated). This shows

that Adobe’s services can be scaled to meet the needs of an individual, freelance graphic

designer or a multinational corporation.

Adobe’s center of gravity lies in its R&D, marketing, and human resources departments

and revolves around producing high-quality, innovative solutions. These distinct competencies

contribute to Adobe’s competitive advantage, but each segment also has aspects that could be

optimized to increase customer responsiveness and efficiency.

The following is a discussion of what Adobe has at its disposal to achieve its vision,

growth objectives, and sustainable competitive advantage.

Quality & Innovation

Human Resources

R&DMarketing

27

Resources Adobe received over 1,000 patents in the past five years (Patexia). The following graph

shows how many patents Adobe (in red) has compared to other tech companies. For its size,

Adobe has a monumental amount of patents in its arsenal.

Adobe’s facilities gained recognition as “Greenest Office in America”, setting the bar

for corporate environmental initiatives (Knox). With 70% of its workspaces LEED certified,

Adobe “assures that [its 13,500]employees breathe clean air, drink safe water, work under

natural light, and enjoy the benefits of innovative and creative workspace design” (Adobe).

This contributes to Adobe’s efficiency, stabilizing long-term costs.

Source: https://www.patexia.com/

Patents held by Adobe in comparison with other digital service providers

28

FunctionsMarketing

Adobe is ranked 77th on Interbrand’s “Best Global Brands” (Interbrand). It also has

a massive global network for delivery and customer support (Adobe 2014). Adobe recently

increased its services by adding Adobe Marketing Cloud. This is Adobe’s attempt to address

customer responsiveness by positioning itself as “a single source for a full spectrum of

marketing efforts – from the creation of materials to distribution, management, and even

measurement across platforms” (Interbrand). Adobe also switched from physical products to

a cloud subscription. This change allows for Adobe’s engineers to churn out updates at more

frequent intervals (instead of waiting the usual 12-18 month product cycle) (Narayen).

This switch is also reflective of an entire business model change. Adobe’s products

have become services with a wide array of support options, including access to a library of

how-to videos, customer service via online chats and phone, and other platforms to educate

consumers and marketers about the cloud (Adobe). This increases efficiency for users and

therefore utility, but Adobe lacks strong communication conveying these benefits. A survey

conducted on Adobe users by CNET showed that 93% are looking for alternatives to Adobe’s

software.

By nature, Adobe has a unique cost structure which, combined with a virtual

monopoly, has allowed for it to price its items in the past at a high point. When Adobe

switched to the cloud, it enabled the company to unravel its previous decision to bundle

software to further capitalize on the changing consumer demands.

Adobe has strong strategic alliances. For example, Adobe partnered with Publicis

Group (one of the “Big Four” multinational advertising / PR companies: owns Leo Burnette

and Saatchi & Saatchi) to create the first end-to-end marketing management platform that

29

automates and connects all components of a client’s marketing efforts (Adobe). This improves

efficiency for both Adobe and Adobe’s customers, while also securing a large group of

customers.

Research and Development

“Our researchers look years into the future, giving them the opportunity to explore

innovations well in advance of clearly identified customer needs” (Adobe).

As displayed before, Adobe either acquired or created more than 400 patents in 2014

alone. Adobe’s branch of R&D, called Adobe Research, had ten papers accepted to SIGGRAPH

2014, an annual conference on computer graphics (Adobe). Adobe collaborates with over 50

universities, and over half of its collaborators are published in peer-reviewed conferences and

journals (Adobe). In an environment where growth no longer happens through innovation

but acquisition, Adobe has the resources and capabilities to foster its growth through

innovation.

Adobe’s spending on R&D has consistently made up 27% of operating expenses

over the past three years. Adobe recently launched its “rejuvenated” Publishing Cloud with

the hopes it can balance its portfolio. Q2 reports should show indicators of whether or not

Adobe’s endeavor was successful.

Human Resources

Adobe fosters innovation through its company culture, implementing many programs

to encourage employees to innovate. Adobe recently received press for its Kickbox – literally

a red box in which there are materials to help an employee turn a big idea into a product

(Fortune). Things like this, paired with professional development opportunities, competitive

salaries, and incentives are how Adobe attracts top-tier employees (Adobe). Adobe currently

sits 83rd on Fortune 500’s “Best Companies to Work For” and has been on this list for 14

years. That is not to say that Adobe is not also susceptible to poachers. For example, Chief

30

Technology Officer, Kevin Lynch, left Adobe to spearhead the iWatch project with competitor

Apple (Adobe). There is a constant battle to capture and retain the best scientists, engineers,

and managers, but Adobe has strong programs and incentives in place to stave off the

competition fairly well.

Finance

Adobe’s financial position is a bit confusing to navigate and is riddled with strengths

and weaknesses for the company. Its strong points are its large amounts of cash ($1.1 billion,

2014) and its growing, predictable-income via subscription (up 140% from 2013, beating Wall

Street expectations). Adobe also funds its operations well and had a debt ratio of 37.2% in

2014, on par with the industry average.

Its major financial weaknesses are seen in lower-than-industry-average profit margins

(6.5% in 2014) and ROE (4.0% in 2014). R&D and marketing and sales make up 27% and

53% of operating expenses respectively in 2014 and have been increasing as profit margins

are decreasing. It makes one wonder whether these figures represent optimal efficiency and

returns.

PROFIT MARGIN DEBT RATIO ROE

2010 2011 2012 2013 2014 Industry Average

31

Production

Adobe has superior product / service offerings. It recently has kept pace and, in some

instances, outranked major software players Oracle, IBM, and HP even though Adobe is

dwarfed by their size (market caps in billions: Oracle - $188.9, IBM - $167.5, HP $59). Adobe

is listed as a top vendor for global service quality management and customer experience

management (TechNavio). Only a year after the launch of its Marketing Cloud, Forrester

Research placed Adobe as the leader in Web Content Management, beating out Oracle, IBM

and HP (Schadler). Adobe also sits at the top of Gartner’s Magic Quadrant, outpacing the

“visionary” of this segment, Salesforce.com, with

regards to its strategy and ability to implement it as

a digital marketing hub (Frank). This reflects strong

barriers to imitation regarding intangible assets

and capabilities, adding to Adobe’s competitive

advantage.

The cost of the first copy of a digital good /

service is high, but “[t]he variable costs of software

licenses are close to zero” and, as another property of

digital goods, software can be copied easily without

compromising quality (Bauxmann 19). This is a

generalized strength for the digital goods industry,

mentioned before, and it would be great to see

Adobe capitalizing on this further.

Adobe is dependent on third-party sellers

and it has one host for its cloud computing (Adobe). This value-chain decision leaves Adobe

susceptible to the risks experienced by third-parties.

Source: Forrester Report

Source: Gartner Report

32

Adobe managers have been sentimental and myopic, especially with regards to Flash.

Flash, which became irrelevant on the mobile market back in 2010, is being phased out as a

rich-text platform on the internet (Firefox and Youtube have already transferred away from

Flash in favor of HTML5), and the application is riddled with imperfections that hackers

exploit heavily (Jobs). Yet Adobe pushed Flash for years afterwards, wasting resources and

time. The publicity regarding Flash (via Steve Jobs’s letter) and the lack of response from

Adobe regarding this situation and its security compromise left stakeholders furious. Clearly,

Adobe’s marketing / public relations was not very customer responsive in this instance.

Moreover, it has taken Adobe more than two months to patch the points of hacker-entry in

Flash. After that Adobe needed to release emergency updates three times in two weeks to

patch more zero-day hacks (Adobe). This is not to say that Flash is completely irrelevant. It

is still the top choice for game designers, animators, and those who create other interactive

media.

Customer Service

Adobe’s capacity to respond to customers poses a major weakness, which Adobe

has been trying to correct by the aforementioned changes in business model and service

expansion. According to beta-site, Tech Radar, of the top ten most hated programs of all time,

Adobe has two programs on the list: Flash Player and Adobe Reader (Marshall). Also, Adobe’s

recent business-model shift left many in an uproar; a petition was signed by 26,000 users to

eliminate the mandate of the subscription model (Elst). This probably greatly contributed to

the motivation behind the 93% of users looking for alternatives. To avoid losing customers,

Adobe will need to incorporate methods to convey value into its growth strategy.

So far Adobe has sustained long-term competitive advantage. It started to lose its edge

due to lack of customer responsiveness and current lack of substantial, visible benefits from its

innovations.

33

Alternatives

34

The following are alternative strategies for growth. They are grouped based on area

of focus between new and existing markets, as well as new and existing product offerings.

Each of these recommendations plays on Adobe’s distinct competencies and resources while

capitalizing on external factors and moving Adobe toward its mission.

Adobe should pursue a growth strategy because, as mentioned in the Industry

Analysis, Adobe will competing in a state of hyper-competition.

Market Penetration (Focus: existing markets with existing products)

Alternatives in this section can be implemented on top of other growth strategies. It is

important to secure as much of the market as possible as a high-tech company. Becoming the

standard is how a company ensures long-term competitive advantage, but even after becoming

ubiquitous, a company needs to stay prevalent in consumers’ minds; if not, it risks fading into

the noise.

General Increase in Marketing

Adobe needs to focus on educating its existing users

in regard to the increased utility/ benefits they derive from

having Adobe on the cloud. This will work to secure the

wavering consumer loyalty and ensure customer satisfaction.

The “new users” (users that started using Adobe after its switch to the cloud) do not need

to be reassured, but this marketing effort can only strengthen Adobe’s position with these

subscribers. Another way that Adobe can increase the satisfaction of consumers is to increase

the efforts and highlight the returns being generated from recently acquired Behance (the

leading online platform for the showcasing and discovering of creative work). This is a

Alternative Growth Strategies

“Today it’s important to be present, be relevant,

and add value.” – Nick Besbeas, Head of Marketing, LinkedIn,

35

talent-access point. It brings together businesses and creatives. This type of platform could

strengthen program-loyalty on two fronts: that of users and that of businesses.

To further address businesses, Adobe should also be focusing on educating CMOs

about the superior benefits revolving around the Adobe Marketing Cloud as compared to

those of competitors like salesforce.com. Other promotional activities include sponsoring

marketing tradeshows, conferences, and summits: the types of conferences that corporate-

level, marketing decision-makers attend. This would allow Adobe to target large numbers of

marketing officials, while giving them the space to show how its services are superior to the

competition’s.

Increase Educational Tools to Capture and Secure Existing-Market Shares

Adobe already has more than 40% of the global market share in creative software, but

analysts believe this percentage will prove volatile (Trefis Team). With 93% of Adobe users

looking for alternatives to its software solutions, the security of Adobe’s reign seems unstable

at best (Shankland). If a competing solution were to be released tomorrow, it would be a

serious scramble for Adobe. Young marketers entering the workforce today, along with the

future generations of marketers / creatives, have shorter attention spans (down to 8 seconds in

2013 from 12 seconds in 2000), increasing the preference for usable-solutions over learnable-

solutions (Keyes). Expanding Adobe’s existing library of tutorials (by language and for other

programs) would create a stronger sense of utility in a consumer’s mind, as well as offer

another point for Adobe to drive traffic to its other resources like Behance. It would also allow

Adobe to more punctually convey the more rapid turnover of new benefits: from a 12 to an 18

month product cycles to immediate innovation on any compelling offer (Narayen).

Adobe already has the resources and capabilities to fund, produce, and evaluate this

endeavor. Plus, with regards to the Creative Cloud, much of the content Adobe would need

already exists. It would not even need to create these tools, but simply construct a small series

36

of algorithms to identify which videos on Youtube have the highest hits and rankings on

tutorial-style videos. Adobe could then negotiate with the creator either rights to the video or

hire him or her to reproduce their content as Adobe sees fit.

As for Adobe Marketing Cloud, no educational resources exist yet. Establishing some

would largely benefit customers, as well as Adobe’s top line and usage/subscription rates.

The 57% of marketers who do not have faith in their campaign measurement approaches are

looking for ways to gain confidence in quantifying and categorizing this “big data,” which is

what Adobe Marketing Cloud does (Ramos). The learning resources would enable marketers

to make that leap from “aspiring editor16” to “content master27”.

This platform would also serve as another feedback loop for Adobe’s own marketing

(What are consumers stuck on? Is the SaaS’s usability keeping up with its powerful

capabilities?), and reinforce the sense of community customers perceive around the Adobe

brand. Adobe would be helping its customers do their job. This would create massive amounts

of perceived value, which would offer Adobe more pricing flexibility and maybe even boost

profit margins.

Product Development (Focus: existing markets with new products)

Focus in this area would work to increase Adobe’s offerings and secure more of its

existing market share.

Adobe Smart screen / work environment

Adobe recently started producing physical products that complement its software. The

digital pen and ruler increase user-value, enabling a creative individual to get more out of the

Adobe’s products with their existing tablet or touch-screen enabled device.

Adobe could continue creating value in this manner by introducing the new “optimal work

environment” for those who use Adobe’s software. This new optimal work environment

6 “Misguided marketers who lack strategy, but think they understand Content Marketing” (Ramos).7 “Marketers who incorporate consumer feedback into an evolving strategy and have the technology to successfully measure the impact of their endeavors on overall revenue” (Ramos).

37

consists of whiteboard-sized smart-screens that allow for interaction and immediate response

across multiple devices through the cloud.

These screens would redefine the workplace and allow for marketers, engineers, and

scientists to interact with their creations as their customers would interact with the products.

Adobe could create a strategic alliance with SHARP. SHARP is the ideal company for this

situation as it would not compromise the existing relationships Adobe has with Apple or

Microsoft (as it would if Adobe tried to go with Samsung). SHARP is also one of the few

companies that focuses on projector-less interactive technology as opposed to projector-

centric boards.

Other Software Solutions: Presenter Applications and Project Management Software

Many of the creatives who use Adobe software use it to complete larger initiatives.

For example, a marketer may use Photoshop to create an advertisement that is part of a larger

campaign or initiative. Adobe created the Marketing Cloud to address the project-needs of

marketers. Adobe could introduce other software that helps manage projects for other market

segments. This would allow Adobe to further capitalize on its acquisitions (i.e. Omniture) by

continuing to apply and exploit its online optimization and analytics segments.

Presentations are used across industries; from a marketer preparing a forecast, to a

manager making a pitch to the board, to an executive unveiling a new strategy. Adobe could

create a presentation program that combines the color pallet capabilities from InDesign,

minor animations from Flash, and the basis for appealing infographics and supportive charts

from Media Optimizer.

These software offerings would expand Adobe’s service portfolio. The fact that it

would be cloud-based – differentiating it from existing software applications – would increase

usability for consumers and allow them to work real-time across devices from anywhere.

38

Video Hosting

This alternative expands upon a few of Adobe’s existing software offerings: Flash and

Premier. Film, animation, and game creators could publish what they produce using Adobe

software on an Adobe platform. Adobe could diversify its revenue sources even further by

allowing for advertisements on this venture.

Adobe holds a spot on Bytelevel Research’s Web Globalization Report Card, which

shows that Adobe has the ability to construct and maintain successful web presences (The

2015 Web Globalization Report Card).

Acquire Autodesk

Rumors have leaked that Adobe is looking to buy The Foundry because of its 3D

software. Bidding for The Foundry starts at £200 million (Armstrong). The Foundry has very

little to offer in the realm of 3D printing, and Adobe would be wasting resources on playing

catch-up to Autodesk.

Autodesk is the leader in 3D software technology and will soon be the leader in 3D

printing technology. It caters to engineers, architects, and other digital hobbyists: similar

segments that Adobe tries to reach. Autodesk also has a 180+ million user-base worldwide

and a product portfolio containing over 100 elements in 17 languages. Autodesk Education

Community has over 150 million members and over 1,900 training centers (Autodesk). Adobe

could apply these resources to address its own weaknesses and mitigate the threats of digital

illiteracy.

The reason Autodesk is not yet the leader in 3D printing is because it has yet to create

the software that can efficiently link up 3D application software to the actual printers (Dove).

This dilemma may sound familiar because it is the exact problem to which Dr. Warnock and

Dr. Geschke devised a solution that started Adobe’s journey to success. They invented desktop

printing, and Adobe has the capabilities and resources to repeat history and revolutionize

39

personal 3D printing. This would very much boost Adobe’s current profits and ensure long-

term sustainable competitive advantage when its becomes the accepted standard.

Adobe would have all of this at its disposal if it were to acquire Autodesk.

Adobe would also be eliminating a massive source of competition in the markets of

architecture, engineering, construction, manufacturing, media, and entertainment. Autodesk

just completed an “acquisition spree” that increased the software solutions for film, animation,

and games in its portfolio mix, encroaching upon Adobe’s territory and threatening its hold

on market share (“Autodesk Continues Acquisition Spree”).

Another opportunity that Autodesk is tapping into – and that, subsequently, Adobe

would have access to if it acquired Autodesk – is reaching a much younger demographic.

Autodesk just partnered with toy manufacturer, Mattel, to launch a 3D platform in which kids

can design and print their own toys (Sawers). Autodesk is securing the loyalty of the future

inventors, engineers, architects, and designers. This could be a massive threat to Adobe’s future

profitability, but merging with Autodesk would turn this threat into a strong, sustainable

competitive advantage point.

Overall, Autodesk is in strong financial health. Autodesk’s 2015 revenues jumped after

a brief decline in 2014, with margins similar to Adobe at 3.26% (Autodesk). It has a market

cap of $13.7 billion and returns on equity of 3.65% (Autodesk). Even though it just went

through its acquisition spree, Autodesk remains stable, with a debt ratio of 33.67% (Autodesk).

Also, Autodesk just completed the same shift to the cloud (and through the same host as

Adobe – Amazon Web Services – which significantly lowers any transitional problems Adobe

might have encountered), and has seen a 28% ($1.16 billion) increase in its deferred revenue

(Autodesk).

Market Development (Focus: new markets and existing products)

Adobe could continue to push its products to other industries (sports and science) or

40

demographics (children) to name a few. Some of these potential markets could handle Adobe’s

products as is, but others would need simplified versions of its current offerings.

Target: Small Businesses and “Average Bloggers”

There are more than 300 million startups annually (Webb). Adobe could expand

its market outside of corporation accounts and specialized designers, expanding to a more

massive collection of businesses and individuals. This would require Adobe to create solutions

that are tailored more to the “common person”.

Adobe could create “lite” versions of its software (creative, marketing, and publishing).

This would decrease the complexity of its products, add another price-point to Adobe’s mix,

and increase the potential number of consumers.

Bonus: This particular alternative has even more long-term potential if Adobe sets

its “lite” version software to be most compatible with content management king, Wordpress.

Wordpress is the most popular blog host, with over 74 million dependent sites and more than

26,000 additions a day in the U.S. (Colao).

Adobe currently offers creation, publishing, and analytics solutions, but does not host

or manage content the way Wordpress does (and does well).

Diversification (Focus: new markets and new products)

Shifting away from the existing offerings and market for Adobe, there seems to be a

plethora of options. Adobe could open an advertising academy; get into film production; start

writing operating system software. Each of these options would require Adobe to either push

innovation from within or gain it through alliances or acquisitions (similar to how it acquired

Omniture and used its resources to start Adobe Marketing Cloud).

Internet-of-things38

8 The network of physical objects or “things” embedded with electronics, software, sensors and connec-tivity to enable it to achieve greater value and service by exchanging data with the manufacturer, operator and/or other connected devices. Each thing is uniquely identifiable through its embedded computing system but is able to interoperate within the existing Internet infrastructure.

41

Adobe could strike up partnerships for projects revolving around internet-of-things.

Adobe would implement its software into the “interface” of the partner’s facility. This would

redefine user experiences wherever it were implemented. For example, imagine being able to

“try on” outfits without the tediousness of looking for matching items, or putting clothes on

and off. Just stand in front of a full body “mirror” that has an overlay of real-time animation-

generating software; drag and drop outfits on you; easily locate or have delivered desired

items; pay before your items are finished being packaged. These experiences can be applied to

homes, restaurants, fitness, and more.

Some options like this already exist (i.e. Warby Parker and its at-home fittings or Chili’s with

its on-table, touch-screen ordering and check-outs), but a preferred standard or model has not

yet arisen.

Granted, this segment is full of “next bests,” and therefore a major rush to be the

“first” is on. Companies with deeper pockets (Google and Apple) are vying for similar

diversification moves. Adobe may be punching above its weight if it tried to pursue some of

these diversification options.

Museum Exhibit Design and Archiving

Adobe’s existing solutions could be applied to creating interactive exhibits and

archiving artifacts. In addition, having items archived could enable the creation of virtual

tours. Virtual tours in themselves have three implications; they lengthen the life of sites /

artifacts by decreasing the wear of direct tourism, decrease art crime because of a proliferation

in databases and track-ability, and increase the reach of museums’ potential market. Imagine

bringing the Louvre to a history class or walking through the Coliseum – as it is today and as

it was in Ancient Rome, thanks to additional simulation – from one’s living room.

Many existing virtual exhibits are already running on Flash (i.e. Sistine Chapel), but a

standard for archiving and exhibit design has yet to be established. Google attempted an

42

endeavor in 2011 called Google Art Project, but it only has 150 collections focused on art

museums (“Google Art Project”).

At physical sites, Adobe could create a hybrid Photoshop-Flash software solution to

create interactive exhibits. This could increase the appeal of certain exhibits as well as offer

another layer of preservation to sites that would otherwise experience a lot of wear from

visitor interaction. Even if Adobe is a forward-thinking company, its mission is to “change the

world through digital experiences,” and it can do so by integrating with historic preservation.

This alternative has quite an extensive potential market, but a short cap on potential

profitability. There are over 35,000 museums in the U.S. and more than 19,000 in Europe

(Ingraham). Of the museums with financial data, only 40% reported annual income of more

than $10,000 on IRS returns (Ingraham). Adobe could become the standard for this market

(similar to how it became the standard in desktop publishing), and go down in history by

preserving history.

Of these alternatives, the acquisition of Autodesk is my ultimate recommendation.

Autodesk will clearly be a major acquisition, but taking the financial hit now will secure

Adobe’s competitive advantage. It would not be the first time Adobe undertook an acquisition

of this magnitude. In 2005, it acquired Macromedia for one-third of its market cap ($15.1

billion, December 2005) at a price of $3.4 billion (Adobe). If Adobe waits, Autodesk’s stock

will just continue to rise, and if Autodesk develops a dominant design of commercial software

to connect its 3D desktop solutions to 3D printers with another company (i.e. Microsoft),

Adobe will be shut out of that market (NASDAQ). Owning the technical standard is key

locking in a company’s competitive advantage in this industry, especially because it would

be capitalizing on first-mover advantage by patenting the software and creating an initial

monopoly.

43

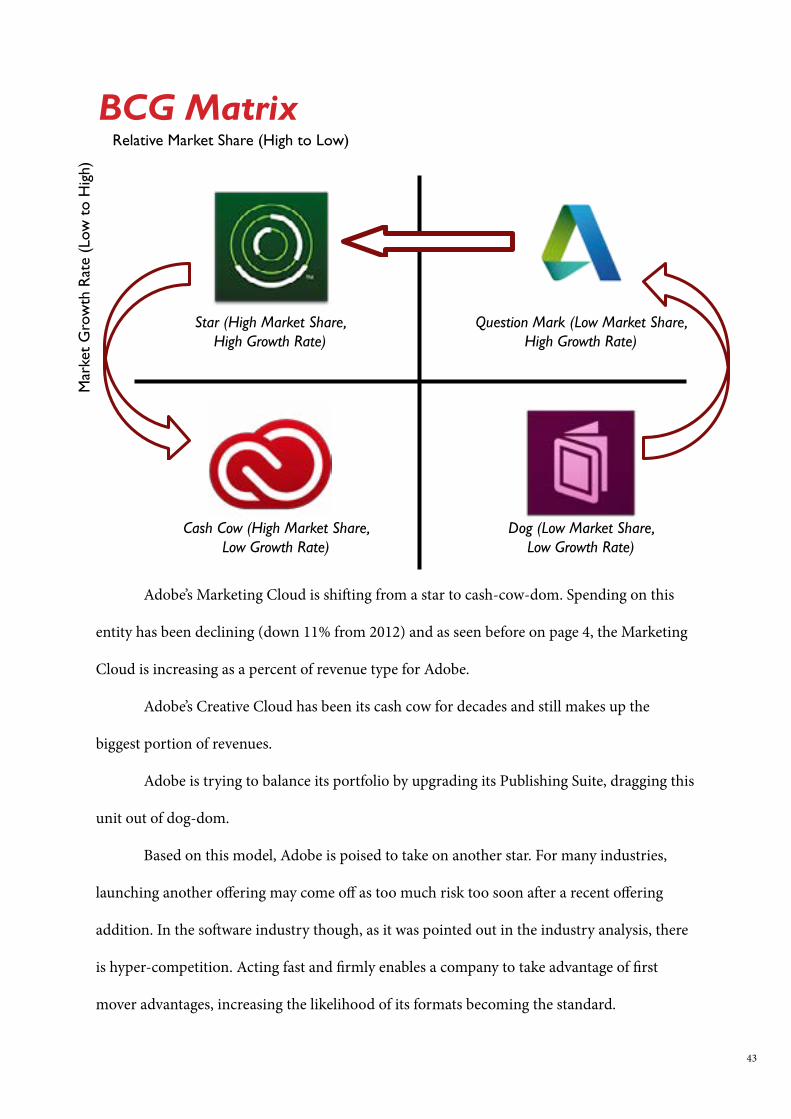

Adobe’s Marketing Cloud is shifting from a star to cash-cow-dom. Spending on this

entity has been declining (down 11% from 2012) and as seen before on page 4, the Marketing

Cloud is increasing as a percent of revenue type for Adobe.

Adobe’s Creative Cloud has been its cash cow for decades and still makes up the

biggest portion of revenues.

Adobe is trying to balance its portfolio by upgrading its Publishing Suite, dragging this

unit out of dog-dom.

Based on this model, Adobe is poised to take on another star. For many industries,

launching another offering may come off as too much risk too soon after a recent offering

addition. In the software industry though, as it was pointed out in the industry analysis, there

is hyper-competition. Acting fast and firmly enables a company to take advantage of first

mover advantages, increasing the likelihood of its formats becoming the standard.

BCG MatrixRelative Market Share (High to Low)

Mar

ket

Gro

wth

Rat

e (L

ow t

o H

igh)

Star (High Market Share, High Growth Rate)

Question Mark (Low Market Share, High Growth Rate)

Dog (Low Market Share, Low Growth Rate)

Cash Cow (High Market Share, Low Growth Rate)

44

45

Autodesk&Beyond

46

From now until 2017, Adobe should focus on generating as much cash in-flow as

possible through its existing business units by:

• Increasing learning tools (and subsequently perceived-value) around all of its programs

• Pushing sales of its upgraded Publishing Cloud

• Securing sales through momentum and word-of-mouth of the Marketing Cloud

• Increasing incentives for sales personnel to acquire more accounts and subscriptions

Also during this time, Adobe should complete its $2 billion stock buyback program

(Adobe Systems, Inc.).

As shown previously, Adobe is in good financial standing with a healthy debt ratio. It

also has over $1 billion in cash and cash equivalents at its disposal as of November 28, 2014

(Adobe 2014). The cash on hand is clearly not enough for an acquisition that will be over $13

billion, but Adobe could finance this endeavor by borrowing and / or issuing stock. Adobe’s

strong price-to-earnings ratio gives it a lot of leverage in financing this acquisition using

equity.

By late 2016, Adobe should begin negotiations to acquire Autodesk. The alternatives of

merging and forming a strategic alliance are also available, but Autodesk is one third the size

of Adobe and could be bought before it outpaces Adobe.

Once Autodesk has been acquired, there are many things working in Adobe’s favor to

Implementation

2015 2016

Stabilize & Strengthen

Begin Negotiations

47

ensure a smooth transition of data and of company cultures. Autodesk switched to the cloud

in 2014, meaning its financial model is similar to Adobe’s and would not require adjustments

to Adobe’s current model. Autodesk uses the same cloud host as Adobe – Amazon Web

Services – which also eases the transition of Autodesk’s solutions and data without fear of data

corruption or loss. Adobe just has to lift the metaphorical gate between the two cloud farms.

Adobe’s leadership, specifically CEO Narayen, has guided Adobe through dozens of

acquisitions in his time at the company, including Omniture (which enabled Adobe to launch

its Marketing Cloud) and Macromedia (which gave Adobe Flash and Dreamweaver and

consequently the window to enter the market of the online world). There may be many steps

Adobe can take while merging with Autodesk that were similar in these acquisitions. CEO

Narayen could mimic the successful aspects and apply the optimum controls based on the

Macromedia acquisition: ensure company culture integration by having engineer and scientist

liaisons, create a spot on the board for an Autodesk executive, and highlight the similarities in

the missions to unite the two cultures under the common purpose.

2017 2018

Acquire Autodesk

48

Evaluation & Control Firstly, Adobe should watch how the market reacts to this new endeavor by tracking

stock prices. Whether it needs to combat negative reactions or support positive ones,

Adobe will need to continue to be transparent with shareholders just as it was throughout

its transition to the cloud. “I think shareholders are incredibly perceptive if you are clear

about where you are headed. If you provide milestones along the way and if you measure

yourself against the milestones so that people have something to calibrate you against, they

understand.” Narayen “while going through [a] transition you have to have fortitude. One

thing companies need to do is be transparent.”

The other benefit of such open communication enables an employee, manager, or

general function to see where and how it contributes to the company’s success and serves as an

immediate feedback loop, lessening the time it takes to correct a situation or confirm success.

This would continue to drive Adobe’s high level of quality and rapid innovation turnover.

Clear communication, objectives, and incentives will also help Adobe maximize its new mass

of engineers while encouraging its current scientists to continue to challenge themselves.

Financial checkpoints that the market and Adobe will be monitoring are increased

profitability and revenue growth. Combining resources and markets with Autodesk will

undoubtedly have overall increases in subscriptions but looking at subscription increases per

business unit will be a major indicator as to the actual performance of this endeavor.

Hopefully combining competencies across such large companies, while simultaneously

tapping into the fast-growing 3D printing market, will drive down costs and increase profit

margins. This would subsequently increase returns, and Adobe will be able to push its ROE

back up to industry standards.

The last party (and arguably the most important) Adobe should be monitoring is its

49

customers. Adobe can accomplish this by watching the unique hits on the videos in its new

education-video library. This would serve as an indicator to Adobe of the new degree to

which it is conveying value. Also keeping tabs on any forums surrounding the videos would

enable the company to deepen relationships and customer intimacy.

Lastly, Adobe should continue to monitor the progress of its customers: awards

and media surrounding consumer-success. After all, what they do would not be possible

without Adobe’s software. Celebrating them increases existing customer intimacy and is an

opportunity to convey Adobe’s value to the skeptics. This should significantly drive down the

93% of formerly disgruntled users.

“I would never speculate on the limit. Every time you speculate, you’re way too conservative.”

-John Warnock

50

51

Adobe. Adobe: Creative, Marketing, and Document Management Solutions. N.p., n.d. Web.

07 May 2015.

This is the initial window through which the following was explored: corporate social

responsibility, corporate governance, executive profiles, press releases on Adobe’s (re)

actions to external trends, product descriptions, and service offerings.

Adobe Systems, Inc. Form 10-K for the Fiscal Year Ended November 26, 2010. Adobe Systems,

Inc. website. Accessed December 14, 2014.

Use of Adobe’s 10-K forms covered: financials; Adobe’s perceived threats; major

business transactions; performance as divided by financial-model and business unit;

and other insights into Adobe and how it perceives its endeavors.

Adobe Systems, Inc. Form 10-K for the Fiscal Year Ended November 25, 2011. Adobe Systems,

Inc. website. Accessed December 14, 2014.

Use of Adobe’s 10-K forms covered: financials; Adobe’s perceived threats; major

business transactions; performance as divided by financial-model and business unit;

and other insights into Adobe and how it perceives its endeavors.

Adobe Systems, Inc. Form 10-K for the Fiscal Year Ended November 30, 2012. Adobe Systems,

Inc. website. Accessed December 14, 2014.

Use of Adobe’s 10-K forms covered: financials; Adobe’s perceived threats; major

business transactions; performance as divided by financial-model and business unit;

and other insights into Adobe and how it perceives its endeavors.

Adobe Systems, Inc. Form 10-K for the Fiscal Year Ended November 29, 2013. Adobe Systems,

Inc. website. Accessed December 14, 2014.

Use of Adobe’s 10-K forms covered: financials; Adobe’s perceived threats; major

Annotated Bibliography

52