strategic case study f3 handouts - march...

TRANSCRIPT

Professional Examinations

Strategic Level

March 2015

Case Study

FAMILIARISATION AND PRACTICE

WORKBOOK - F3 HANDOUTS

CIMA M ARCH 2015 – ST RA TEGIC CASE STUDY

i i KA PL AN PUBLISH ING

Published by: Kaplan Publishing UK

Unit 2 The Business Centre, Molly Millars Lane, Wokingham, Berkshire RG41 2QZ

Copyright © 2015 Kaplan Financial Limited. All rights reserved.

No part of this publication may be reproduced, stored in a retrieval system or transmitted in any

form or by any means electronic, mechanical, photocopying, recording or otherwise without the

prior written permission of the publisher.

Notice

The text in this material and any others made available by any Kaplan Group company does not

amount to advice on a particular matter and should not be taken as such. No reliance should be

placed on the content as the basis for any investment or other decision or in connection with any

advice given to third parties. Please consult your appropriate professional adviser as necessary.

Kaplan Publishing Limited and all other Kaplan group companies expressly disclaim all liability to

any person in respect of any losses or other claims, whether direct, indirect, incidental,

consequential or otherwise arising in relation to the use of such materials.

KAPL AN PU BLISHING i i i

Chapter 6

FINANCIAL STRATEGY (F3)

FAMILIARISATION

1 FINANCING

EXERCISE 1

Analyse Look’s long term financing arrangements.

2 BUSINESS VALUATIONS

Look wishes to acquire a mobile phone technology company called MobilTronics (MT). The

company develops new technology for the mobile phone industry which it patents and then sells

to various mobile phone manufacturers.

EXERCISE 2

Amanda Wilson, the Director of Finance, wishes to start compiling some valuations of MT but is

unsure of how to do this. She has asked you to prepare some briefing notes for her which

includes the following:

A brief description of the various methods of valuation

Their strengths and weaknesses

An indication of their suitability towards valuing MT

3 FINANCIAL ANALYSIS

EXERCISE 3

Analyse the profitability of Look Group year on year. Use any ratios you consider suitable.

4 INTEGRATED REPORTING

Traditional financial reporting has long been seen as insufficient to allow users to fully understand

the organisation. There has been increasing pressure therefore for entities to provide more

CIMA M ARCH 2015 – ST RA TEGIC CASE STUDY

iv KA PL AN PUBLISH ING

information in their annual reports beyond the financial statements since non-financial

information can also be important to users’ decisions.

For example, the Global Reporting Initiative (GRI) has produced guidelines that propose additional

disclosures in addition to the standard disclosures required in the financial statements. In

particular, the GRI guidelines suggest that entities should disclose economic, environmental and

social performance indicators.

Alternatively, the International Integrated Reporting Council (IIRC) has produced a revolutionary

framework known as the Integrated Reporting Framework (<IR> framework).

EXERCISE 4

Prepare a board paper explaining the main objectives of integrated reporting as well as the

fundamental concepts that underpin it.

Also, comment on the relevance of integrated reporting and its benefits to the Look Group.

KAPL AN PU BLISHING v

Chapter 10

FINANCIAL STRATEGY(F3)

PRACTICE TASKS

EXERCISE 1

TRIGGER

You are called into a meeting with Amanda Wilson and Amanda tells you the following:

“Thank you for your paper regarding the financing of the company.

Following its discussion at the last board meeting, the Board have decided that we need to

restructure our finances to increase the gearing level and take advantage of tax benefit more.

The plan is likely to involve a share buyback of around $10,000 million which is to be financed by

new debt. There are no firm plans as yet but two suggestions have been made:

Option 1: An issue of 10 year bonds.

Our investment bank has advised us that typical required bond yield would be about 8.5% for

bonds of this risk with interest paid annually. The bonds would be redeemed at par. Some

covenants would be required and security would be needed by use of a floating charge.

Option 2: A 10 year bank loan.

Whilst the amount required is large, our bank has identified a number of partners who may be

willing to enter into a syndicate arrangement for the loan. The interest rate would typically be 8%

nominal but interest payments would need to be made on a quarterly basis rather than annually

(not sure how this affects cost if at all?). Covenants are likely to be quite extensive and security

would be a mixture of fixed and floating charge (not sure of the difference and how it affects our

choice?)”

TASK

CIMA M ARCH 2015 – ST RA TEGIC CASE STUDY

vi KA PL AN PUBLISH ING

From: Amanda Wilson

To: You

Date: Today

Subject: Financing options

Hi there

Thanks for the meeting earlier.

I need you to put together a briefing document which provides a fully justified

recommendation to the Board on which financing option to choose and how it should be

progressed.

Some of the terminology may confuse the rest of the Board so make sure you explain the

technical terms to them.

Thank you

Respond to Amanda’s email by preparing a briefing paper (Time allocation 45 minutes)

EXERCISE TWO

Note: This task requires some detailed calculations which are unlikely to be required in the case

study exam. We have included this task to give you a full working example of HOW to value a

business – crucial if you are going to need to comment on other peoples’ calculations – a more

likely scenario. If the key valuations were provided as reference material in the exam the time

allowed for this task would be reduced to 45 minutes.

COMBINED TRIGGER AND TASK

You receive the following email from Amanda Wilson.

To: Senior Manager

From: Amanda Wilson

Subject: Project Sheldon

Date: Today

Hi

I’m currently with the Board at a remote location to discuss the feasibility of a potential major

acquisition of another company in our industry. This is EXTREMELY confidential at present, hence

why we have met at my home to discuss it. I can not tell you the name of the company at present

so the acquisition is simply called project Sheldon.

KAPL AN PU BLISHING vi i

As part of our discussions, the question of how much we are prepared to offer for Sheldon has

come up and I need you to prepare some information for me. I need you to do the following:

Determine a minimum and maximum value for Sheldon using the information I’ve attached

to this email. Attachment 1 is some financial information on Sheldon, attachment 2

is some basic working assumptions.

Determine an initial offer.

Impact on our share price following acquisition.

Your thoughts and recommendation regarding the offer - don’t worry about the strategic

implications, just the financial ones, particularly from our shareholders point of view.

You will see from attachment 2 that if this does proceed it is likely to be a share for share

exchange as we do not want to have to raise external finance for this.

Again, let me emphasise the confidential nature of this so do not discuss this with anyone else.

I need the requested information emailing to me by 11:00 am this morning - sorry for the rush.

Regards

Amanda Wilson

Attachment 1

** CONFIDENTIAL **

Project Sheldon - Financial information

Statement of profit or loss

Year ended

30 September

2014

$ million

Revenue 31,025

Costs of revenues (11,248)

Overheads (8,542)

Operating Profit 11,235

Finance charges (158)

Taxation (2,215)

Profit after tax 8,862

CIMA M ARCH 2015 – ST RA TEGIC CASE STUDY

vii i KA PL AN PUBLISH ING

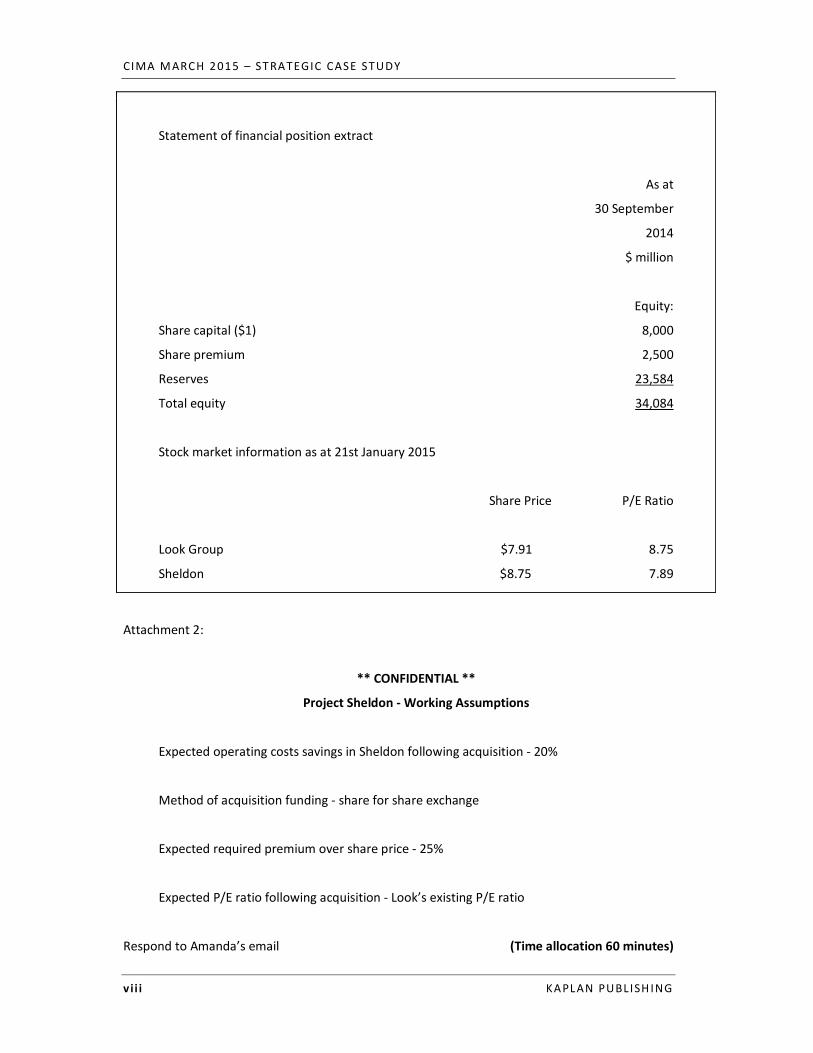

Statement of financial position extract

As at

30 September

2014

$ million

Equity:

Share capital ($1) 8,000

Share premium 2,500

Reserves 23,584

Total equity 34,084

Stock market information as at 21st January 2015

Share Price P/E Ratio

Look Group $7.91 8.75

Sheldon $8.75 7.89

Attachment 2:

** CONFIDENTIAL **

Project Sheldon - Working Assumptions

Expected operating costs savings in Sheldon following acquisition - 20%

Method of acquisition funding - share for share exchange

Expected required premium over share price - 25%

Expected P/E ratio following acquisition - Look’s existing P/E ratio

Respond to Amanda’s email (Time allocation 60 minutes)

KAPL AN PU BLISHING ix

EXERCISE THREE

COMBINED TRIGGER AND TASK

You receive the following email:

From: [email protected]

Subject: Leasing decision

Date: Today

Hi

Look Group is having to undertake a major equipment replacement exercise, total cost is

$2,000 million. The two options are either leasing or buying the equipment ourselves.

The lease will be a 5 year finance lease with annual payments of around $501 million at an

interest rate of 8%. We will be able to claim tax relief on the accounting depreciation if

we lease. Tax as you know is 20% paid one year in arrears.

If purchased, the finance is likely to be 5 year bank loan(s) also at an average rate of 8%

and tax writing down allowance will be available on a straight line basis.

In your absence last week I got one of the accountants in your department to put a lease

versus buy appraisal together which I have attached. It does not look right to me. I need

you to do the following:

Firstly, have a quick look at the attached appraisal and see if you can see what’s wrong

with it. I’ve checked all the arithmetic in the spreadsheet and that’s fine so it must be

something more fundamental - the two results can not possibly be that far apart! I can

not understand why 6.4 % has been used as a discount rate and why the loan cashflows

have not been shown in the buying appraisal so please could you explain this to me? Do

not worry about doing the corrections, I can do that myself but I need the detail of the

errors.

I’m also a bit rusty on these things so how do we choose between the two options given

the results are negative?

Secondly, could you explain the differences, if any, in the accounting treatment between

the two options. Again, just an explanation, don’t worry about doing any calculations on

this.

Finally, any other factors you think we should be considering in the decision.

Thanks

CIMA M ARCH 2015 – ST RA TEGIC CASE STUDY

x KA PL AN PUBLISH ING

ATTACHMENT

Leasing Evaluation Year> 0 1 2 3 4 5 6

$'000 $'000 $'000 $'000 $'000 $'000 $'000

Lease payment (500,913) (500,913) (500,913) (500,913) (500,913)

Interest (160,000) (107,127) (58,484) (13,732) 27,440

Tax relief on interest 20%

(32,000) (21,425) (11,697) (2,746) 5,488

Tax relief on depreciation 20% 80,000 80,000 80,000 80,000 80,000

Net cashflow (660,913) (560,040) (500,822) (446,342) (396,220) 85,488

Discount factors 6.40%

1.0000

0.9398

0.8833

0.8302

0.7802

0.7333

0.6892

Present Value (621,159) (494,693) (415,775) (348,258) (290,555) 58,919

Total Leasing PV = (2,111,521)

Buying Evaluation Year> 0 1 2 3 4 5 6

$'000 $'000 $'000 $'000 $'000 $'000 $'000

Asset purchase (2,000,000)

Depreciation

(400,000) (400,000) (400,000) (400,000) (400,000)

Tax relief on depreciation 80,000 80,000 80,000 80,000 80,000

Net cashflow (2,000,000) (400,000) (320,000) (320,000) (320,000) (320,000) 80,000

Discount factors 6.40%

1.0000

0.9398

0.8833

0.8302

0.7802

0.7333

0.6892

Present Value (2,000,000) (375,940) (282,662) (265,659) (249,680) (234,661) 55,137

Total Leasing PV = (3,353,465)

Respond to the email (Time allocation 45 minutes)