strategic factors impacting the california crude oil … · strategic factors impacting the...

TRANSCRIPT

1

California Independent Petroleum Association28th Annual Meeting

1June 12, 2004

P..Strategic Factors Impacting The California Crude Oil Market

California Independent Petroleum Association

28th Annual Meeting

June 12, 2004Hyatt Regency Huntington Beach

Mike SarnaEric WeiLong Beach Office

California Independent Petroleum Association28th Annual Meeting

2June 12, 2004

P..About Purvin & Gertz, Inc.

• Privately-Owned, Independent International Energy Consulting Firm

• Founded in 1947• Over 100 staff members worldwide• All consultants have chemical engineering

degrees• Representative offices in

– Houston, Texas (Headquarters)– Long Beach, California (Since 1982)– Calgary, Canada– Singapore– London, England– Moscow, Russia– Buenos Aires, Argentina

• Website at www.purvingertz.com

• Main Services:– Crude oil and natural gas market analysis– Refinery analysis (technical & economic)– Refined product market analysis– Terminal/Pipeline infrastructure analysis– Due diligence/ Independent engineer– Strategic planning/ M&A assistance– Asset valuation– Litigation support– Training & Seminars

– Studies are conducted on single or multi-client basis

– Routine Publications– Petroleum & natural gas price forecast– Global supply/demand projections

2

California Independent Petroleum Association28th Annual Meeting

3June 12, 2004

P..Presentation Overview

• California Crude Oil Market– California Refinery Demand– ANS Supplies– California Supplies– Foreign Supplies

• Factors Impacting California Crude Oil Price– California Benchmark Crude Oil Price– Import Costs– Global Supply-Demand Balance– International Crude Price– California Crude Oil Quality Differentials

• Closing Remarks

California Independent Petroleum Association28th Annual Meeting

4June 12, 2004

P..California Crude Oil Marketing Regions

• Refineries in San Francisco and Los Angeles are dependent on ANS and imported crude oil deliveries by tanker.

• Refineries in Central California process SJV and OCS crude.

• Closure of Shell Bakersfield refinery pending.

NEVADA

CALIFORNIA

ARIZONALos AngelesRefining Capacity

970 MBPD

Los AngelesRefining Capacity

970 MBPD

Ventura

Gaviota

Central AreaRefining Capacity

185 MBPD

Central AreaRefining Capacity

185 MBPD

San FranciscoRefining Capacity

620 MBPD

San FranciscoRefining Capacity

620 MBPD

3

California Independent Petroleum Association28th Annual Meeting

5June 12, 2004

P..California Crude Oil Supply Shift

• Decline in ANS supplies has led to increased dependence on foreign crude oils.

• Refiners must create strategies for foreign crude oil supplies. • Growing role of imported crudes creates basis for projecting the

value of California crudes.

1997 CRUDE OIL DEMAND1,617 Thousand Barrels Per Day

CA52%ANS

37%

Foreign11%

2003 CRUDE OIL DEMAND1,791 Thousand Barrels Per Day

CA43%

ANS23%

Foreign34%

Source: EIA, CEC, Purvin & Gertz Analysis

California Independent Petroleum Association28th Annual Meeting

6June 12, 2004

P..California Fuel Consumption Growth

California population growth will continue to drive demand growth for gasoline, jet and diesel fuels.

California refinery crude runs are likely to creep further, but more refined product imports are also expected.

California refiners will import more crude oil to meet growing demand.

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

FU

EL

CO

NS

UM

PT

ION

-M

BP

D

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

AN

NU

AL

GR

OW

TH -%

TOTAL VEHICLE FUEL CONSUMPTION

(MBPD)

VEHICLE CONSUMPTION

Annual Growth %

Source: CalTrans

4

California Independent Petroleum Association28th Annual Meeting

7June 12, 2004

P..Historical West Coast Refinery Crude Runs

Crude runs increased 4% in 2003: – MTBE Phase-out – Economic recovery

Washington refineries account for roughly 23% (~540 MBPD) of crude demand.

0

500

1000

1500

2000

2500

1996 1997 1998 1999 2000 2001 2002 2003

CA WA

Thousands Of Barrels Per Day

Source: EIA, CEC

California Independent Petroleum Association28th Annual Meeting

8June 12, 2004

P..Historical California Crude Runs By Source

855

611

188

849

591

285

829

409

401

842

357

488

805

331

537

793

385

549

759

417

615

0

200

400

600

800

1000

1200

1400

1600

1800

1997 1998 1999 2000 2001 2002 2003

CA Crude ANS Crude Imported Crude

Thousands of Barrels Per Day

Source: CA DOGGR, CEC, EIA, Purvin & Gertz Analysis

5

California Independent Petroleum Association28th Annual Meeting

9June 12, 2004

P..ANS Disposition

ANS deliveries have favored Washington over California– Lower transportation costs

• Better utilization of Jones Act tankers

– Limited infrastructure for larger foreign crude tankers

Some west coast refiners control a significant share of ANS marketing– ConocoPhillips– ExxonMobil– BP

California Independent Petroleum Association28th Annual Meeting

10June 12, 2004

P..Historical ANS Production

ANS declines have slowed due to recent recovery enhancements & development of new fields.

ANS deliveries to California have declined.

Washington refineries have continued to rely on ANS.

-

500

1,000

1,500

2,000

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Total Cook Inlet ProductionAlaskan North Slope

WA Refinery Crude Demand

(Thousand Barrels per Day)

Washington Refinery Crude Demand

Source: EIA, AK Dept. Of Oil & Gas

6

California Independent Petroleum Association28th Annual Meeting

11June 12, 2004

P..California Oil Production Declines

• Total California production declined at an annual rate of 1.9%.• LA Basin crudes declined at a faster 4% annually.

Thousands Of Barrels Per Day

700

750

800

850

900

950

1000

1050

1100

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

California Independent Petroleum Association28th Annual Meeting

12June 12, 2004

P..Foreign Crude Sources

Foreign supplies– Arab Gulf– S. America– Mexico– Canada– Asia

International crude oil price linkages

– Mexico– S. America– Arab Gulf

FROM ARAB GULF

FROMEUROPE, AFRICA

& ARAB GULF

ARGENTINA & AUSTRAILIA

7

California Independent Petroleum Association28th Annual Meeting

13June 12, 2004

P..2003 California Foreign Crude Oil Imports

The Arab Gulf crudes make up 58% of foreign imports, while Latin American crudes accounted for 31%.

Thousands Of Barrels Per Day

0

50

100

150

200

250

SAUDI A

RABIA

ECUA

DOR IRA

Q

MEXICO

ANGOLA

ARGEN

TINA

AUST

RALIA

CANA

DA

UNITE

D ARA

B EMIRA

TES

INDONE

SIA OMANPE

RU

KUWAIT

YEMEN

COLO

MBIABR

UNEI

VENEZ

UELA

NIGERIA

BRAZ

IL

EQUA

TORIA

L GUIN

EA VIETN

AM

California Independent Petroleum Association28th Annual Meeting

14June 12, 2004

P..Benchmark Crude Pricing Basis: Import Parity

ANS – Middle East Import Parity Differential, $/BBL

ANS can be used as a benchmark crude for evaluating U.S. West Coast crude oil prices.

ANS prices have gradually risen to levels consistent with delivered imports from Middle East (Western Hemisphere Import Parity Pricing).

(1.40)

(1.20)

(1.00)

(0.80)

(0.60)

(0.40)

(0.20)

-

0.20

0.40

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Est. Middle East Import Cost (VLCC w/ Lightering)

Source: Platts , Purvin & Gertz Analysis

8

California Independent Petroleum Association28th Annual Meeting

15June 12, 2004

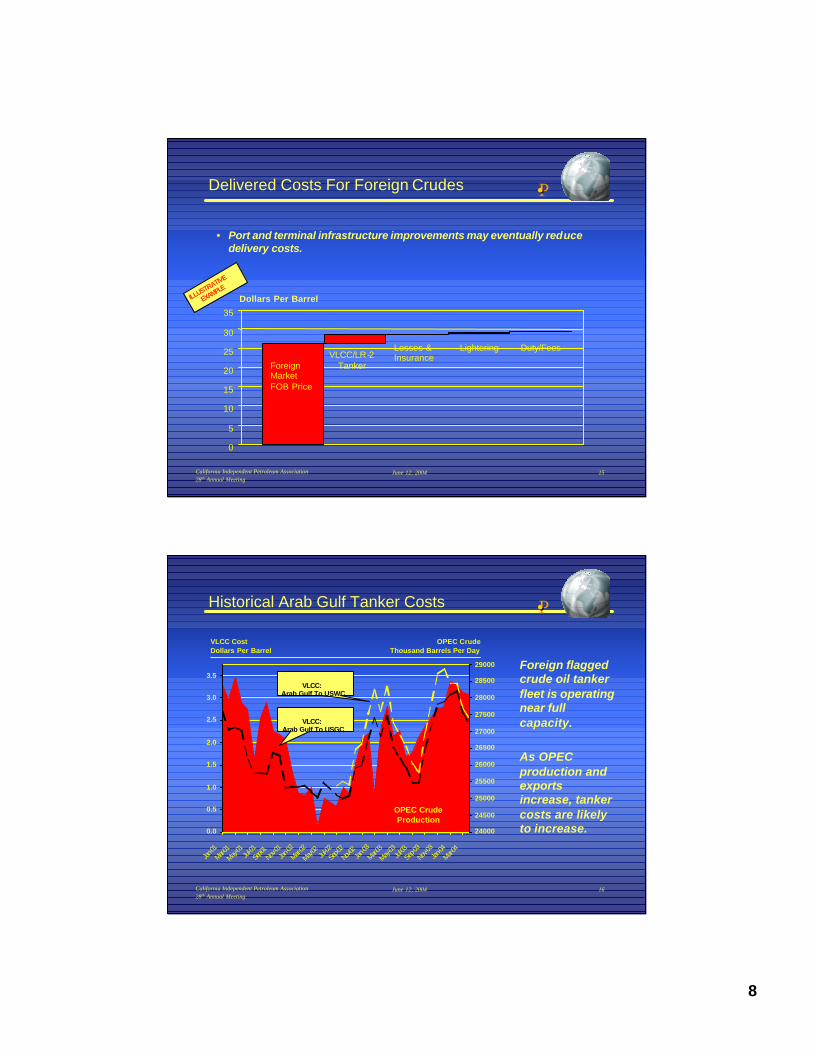

P..Delivered Costs For Foreign Crudes

• Port and terminal infrastructure improvements may eventually reduce delivery costs.

0

5

10

15

20

25

30

35

Foreign MarketFOB Price

VLCC/LR-2Tanker

Losses &Insurance

Lightering Duty/Fees

Dollars Per BarrelILLUSTRATIVE

EXAMPLE

California Independent Petroleum Association28th Annual Meeting

16June 12, 2004

P..VLCC CostDollars Per Barrel

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan-01

Mar-01

May-01

Jul-01

Sep-01

Nov-01

Jan-02

Mar-02

May-02

Jul-02

Sep-0

2No

v-02 Jan-03

Mar-03

May-03

Jul-03

Sep-0

3Nov-

03Jan

-04Mar-0

4

24000

24500

25000

25500

26000

26500

27000

27500

28000

28500

29000

OPEC Crude Production

OPEC CrudeThousand Barrels Per Day

VLCC:Arab Gulf To USGC

VLCC:Arab Gulf To USWC

Historical Arab Gulf Tanker Costs

Foreign flagged crude oil tanker fleet is operating near full capacity.

As OPEC production and exports increase, tanker costs are likely to increase.

9

California Independent Petroleum Association28th Annual Meeting

17June 12, 2004

P..Thousands Of Barrels Per Day

0

2

4

6

8

10

12

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

0

10

20

30

40

50

60

70

80

90

1002004 $/BBL

OPEC SPARE

CAPACITY

Price

Crude Price And OPEC Spare Capacity

Strong demand growth led by Asia and U.S. economic recovery has cut spare OPEC crude oil production capacity.

Despite production increases by OPEC and Former Soviet Union, crude oil inventories remain tight.

Unlike previous oil shocks, the current price environment is accompanied by high OPEC and non-OPEC utilization.

Source: IEA, Platts

OPEC CUTS-LOW UTILIZATION

HIGH OPEC UTILIZATION

Iraq War

California Independent Petroleum Association28th Annual Meeting

18June 12, 2004

P..World Crude Oil Demand Growth

Seasonal global petroleum demand usually peaks in winter months.

Growth in worldwide demand over 2nd Half of 2003 was roughly 4.5 million barrels per day.

Over the last 3 years, roughly 65% of worldwide demand growth was driven by Asian countries.

Oil Demand Growth From 1Q 2001 (Millions Of Barrels Per Day)

-2

-1

0

1

2

3

4

5

1Q 20

01

2Q 20

01

3Q 20

01

4Q 20

01

1Q 20

02

2Q 20

02

3Q 20

02

4Q 20

02

1Q 20

03

2Q 20

03

3Q 20

03

4Q 20

03

1Q 20

04

China

World

Other Asia (Excl. Japan)

Source: IEA

10

California Independent Petroleum Association28th Annual Meeting

19June 12, 2004

P..Crude Oil Valuation Overview

Regional Benchmark Crude Pricing• International Import Parity• International Export Parity• Marginal Production Costs CRUDE OIL

VALUATION

Value Adjustments For Crude Quality• Refinery economic indifference

California Independent Petroleum Association28th Annual Meeting

20June 12, 2004

P..Estimating The Crude Oil Quality Differential

Key Assumptions• Refineries will

expand crude oil consumption until favorable economics disappear (marginal refinery mode).

• Crude oil supply costs based on market alternatives or marginal production costs.

Crude Oil Demand Curve(Refinery Breakeven)

Crude Oil Supply Curve(Supplier Indifference)

Market Clearing Price(US$/ Barrel)

Market Crude Oil Demand (Barrels Per Day)

Refiner’sMargin(US$/ BBL)

Supplier’sSurplus(US$/ BBL)

Marginal Refinery Operation

Determines Market Value

Marginal Refinery Operation

Determines Market Value

CLASSIC SUPPLY-DEMAND FRAMEWORK

ILLUSTRATIVE

EXAMPLE

11

California Independent Petroleum Association28th Annual Meeting

21June 12, 2004

P..Determining Crude Oil Quality Differentials

Crude oil quality differentials are based on the crude oil’s relative value in the marginal refinery mode.

The marginal refinery mode in the West Coast is usually FCC Cracking, which produces residual fuel oil.

RelativeMarket Clearing Price

Total Crude Oil Demand (Barrels Per Day)

REFINERY OPERATING MODE ECONOMICS

Coking Mode Variable

Realization

Coking Mode Variable

Realization

FCC Cracking Mode Variable

Realization

FCC Cracking Mode Variable

Realization

HydroskimmingMode Variable

Realization

HydroskimmingMode Variable

Realization

ToppingMode Variable

Realization

ToppingMode Variable

Realization

Crude Oil Price(US$/BBL)

ILLUSTRATIVE

EXAMPLE

California Independent Petroleum Association28th Annual Meeting

22June 12, 2004

P..Main Factors Impacting Crude Quality Differentials

• Refinery cracking yields– Fuel oil yield

• Vacuum residue• Viscosity blending properties

– Gasoline yield

• Refinery processing cost– Sulfur– Nitrogen/ Metals– Gas oil volume

• Refined product prices– Light product – fuel oil differential– Marginal product disposition

• Export parity• Import parity

Refinery Cracking

Mode

Crude Oil

Gasoline,Jet &Diesel

RefineryFuelOil

12

California Independent Petroleum Association28th Annual Meeting

23June 12, 2004

P..Recap

• California refineries are expected to expand as California product demand grows.

• Foreign crude imports will continue to increase as ANS and California supplies decline.

• Light sour crude oil from the Arab Gulf and Latin America will be the main source of foreign crude.

• Quality differentials for crude oils are usually dependent on the economics of the marginal refinery mode.

• Crude oil supplies in California are expected to follow import parity.

• Worldwide petroleum demand growth, particularly in Asia, has created a tight market for crude oil and tanker services.

• VLCC tanker costs from the Arab Gulf to the U.S. can have a significant impact California crude oil prices.

California Independent Petroleum Association28th Annual Meeting

24June 12, 2004

P..Outlook And Comments

• Although significant risk exists, strong Asian demand growth is likely to continue requiring increases in worldwide production.

• Supply concerns related to Middle East tensions have recently moved crude oil prices beyond industry fundamentals.

• Iraq and Former Soviet Union are seen as the main wildcards for increased crude supplies.

• Near-term crude oil prices should ease as non-OPEC production increases in 2004 and 2005.

• Long-run crude oil prices should more closely follow reserve development costs.

• Some California refiners may elect to import product rather than increase crude run due to high cost of expansion and difficulty with latest CARB specifications.

13

California Independent Petroleum Association28th Annual Meeting

25June 12, 2004

P..About This Presentation

This presentation has been prepared for the California Independent Petroleum Association (Client). It provides an overview of the factors expected to influence the market for crude oil in the California region.

Neither the presentation nor any part of the presentation shall be provided to third parties without the written consent of Purvin & Gertz. Any third party in possession of the presentation may not rely upon its conclusions without the written consent of Purvin & Gertz. Possession of the presentation does not carry with it the right of publication.

Some of the information on which this report is based has been provided by others including the Client. Purvin & Gertz has utilized such information without verification unless specifically noted otherwise. Purvin & Gertz accepts no liability for errors or inaccuracies in information provided by others.

Purvin & Gertz conducted this analysis and prepared this report utilizing reasonable care and skill in applying methods of analysis consistent with normal industry practice. Al l results are based on information available at the time of review. Changes in factors upon which the review is based could affect the results. Forecasts are inherently uncertain because of the events or combinations of events that cannot reasonably be foreseen including the actions of government, individuals, third parties and competitors. NO IMPLIED WARRANTY OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE SHALL APPLY.