strategies for driving mobile broadband adoption. portio research ltd

DESCRIPTION

Increase non-voice service adoption, raise ARPU, increase consumer adoption of mobile data services.TRANSCRIPT

© 2010, Portio Research. All Rights Reserved 1

Strategies for Driving Mobile Data and Broadband Adoption

2 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

Portio Research Limited. Published June 2010 by Portio Research Limited © Copyright 2010. www.portioresearch.com

If you have any questions about the legal licence conditions under which this document has been distributed, please contact Portio Research on

Disclaimer and Legal Notices

Disclaimer Every care has been taken i n t he preparation of this study to ensure that the i nformation contained herein is accurate, factual and correct to the best of our knowledge, at time of publishing. All opinions, suppositions, estimates and recommendations included in this document are solely the opinions of the authors unless otherwise stated. Portio Research Limited accepts no liability for any loss or damage or unforeseen consequential loss or damage arising from the use of the information contained within this document. The opinions, suppositions, estimates and recommendations within this document cannot be guaranteed, and r eaders use this information at their own r isk. The i nformation published i n this document i s su bject to change w ithout notice at any t ime, and Portio Research L imited accepts no liability or obligation to inform the reader of such changes. Portio Research Limited do not promote or endorse any specific companies or products, the views and opinions we express in this document ar e wholly our own assessments, and i ndependent f rom any external i nterest or influence. Many terms and phrases and t rade names used i n this document are proprietary and P ortio R esearch Li mited recognises and ackn owledges that all trademarks are copyright, b elonging to their r espective o wners. Where p ossible, t his d ocument acco rds such terms and phrases and trade names to their respective owners. All Rights Reserved. No part of this document can be copied, shared, redistributed, transmitted, displayed in the public domain, stored or displayed on any internal or external company or private network or electronic retrieval system, nor reprinted, republished or reconstituted in any way without the express written permission of the publisher. Forwarding of this electronic document without the correct legal licence is theft. It’s unethical, immoral and against the law.

[email protected] If you did not buy this document and a co lleague or associate has sent it to you, do not assume you are l egally entitled to read i t, i t is your responsibility to ensure you have the correct l egal l icence t o read this document.

© 2010, Portio Research. All Rights Reserved 3

Strategies for Driving Mobile Data and Broadband Adoption

Contents Introduction ......................................................................................................................... 9 Worldwide Mobile Market ................................................................................................. 12 Worldwide Data Services Market ...................................................................................... 16

Strategies for Driving Data ARPU ................................................................................................. 16 Strategies for Creating End-User Demand for Mobile Data Services .............................................. 19 Data Services .............................................................................................................................. 20

Worldwide Mobile Messaging ........................................................................................... 22 Worldwide Mobile Messaging ....................................................................................................... 22 Dominance of SMS ...................................................................................................................... 23

Mobile Messaging – Strategy Case Studies ..................................................................... 26 Case Studies ............................................................................................................................... 26

Telkomsel Indonesia .................................................................................................................. 26 China Mobile ............................................................................................................................. 31 SoftBank Japan ......................................................................................................................... 36

Conclusion ................................................................................................................................... 42 Mobile Broadband – Introduction and Basics ................................................................. 45

Evolution of Mobile Broadband – GSM .......................................................................................... 46 UMTS (Universal Mobile Telecommunications System)............................................................... 46 HSPA (High Speed Packet Access) ........................................................................................... 46 HSPA+ (High-Speed Packet Access Plus/ Evolved HSPA) ......................................................... 46 LTE (Long Term Evolution) ........................................................................................................ 47 LTE Advanced (Long Term Evolution Advanced) ........................................................................ 47 EDGE (Enhanced Data Rates for GSM Evolution) ...................................................................... 48 EDGE Evolution or EDGE II ....................................................................................................... 48

Evolution of Mobile Broadband – CDMA ....................................................................................... 50 CDMA2000 1X EV-DO (Evolution-Data Only) Revision 0 ............................................................ 50 CDMA2000 1X EV-DO (Evolution-Data Only) Revision A ............................................................ 50 CDMA2000 1X EV-DO (Evolution-Data Only) Revision B ............................................................ 50

Evolution of Mobile Broadband – WiMAX ...................................................................................... 52 WiMAX (Worldwide Interoperability for Microwave Access) ......................................................... 52

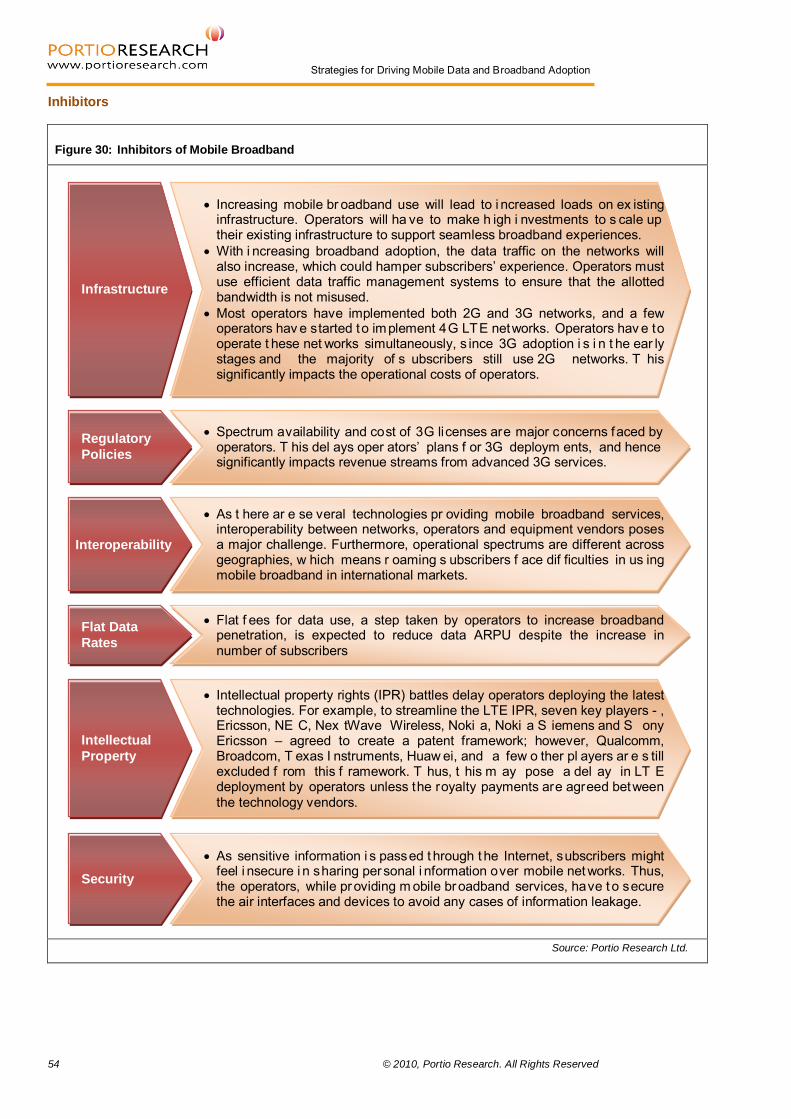

Drivers and Inhibitors – Mobile Broadband .................................................................................... 53 Drivers ...................................................................................................................................... 53 Inhibitors ................................................................................................................................... 54

Mobile Broadband – Hardware ..................................................................................................... 55 USB Modems ............................................................................................................................ 55 Internal Modems ........................................................................................................................ 55 PC Cards .................................................................................................................................. 56

Regional Versions – Mobile Networks ........................................................................................... 57 Mobile Broadband – State of the Markets ........................................................................ 59

Market Size .................................................................................................................................. 59 Mobile Broadband User Base..................................................................................................... 59 Mobile Broadband Revenue ....................................................................................................... 63

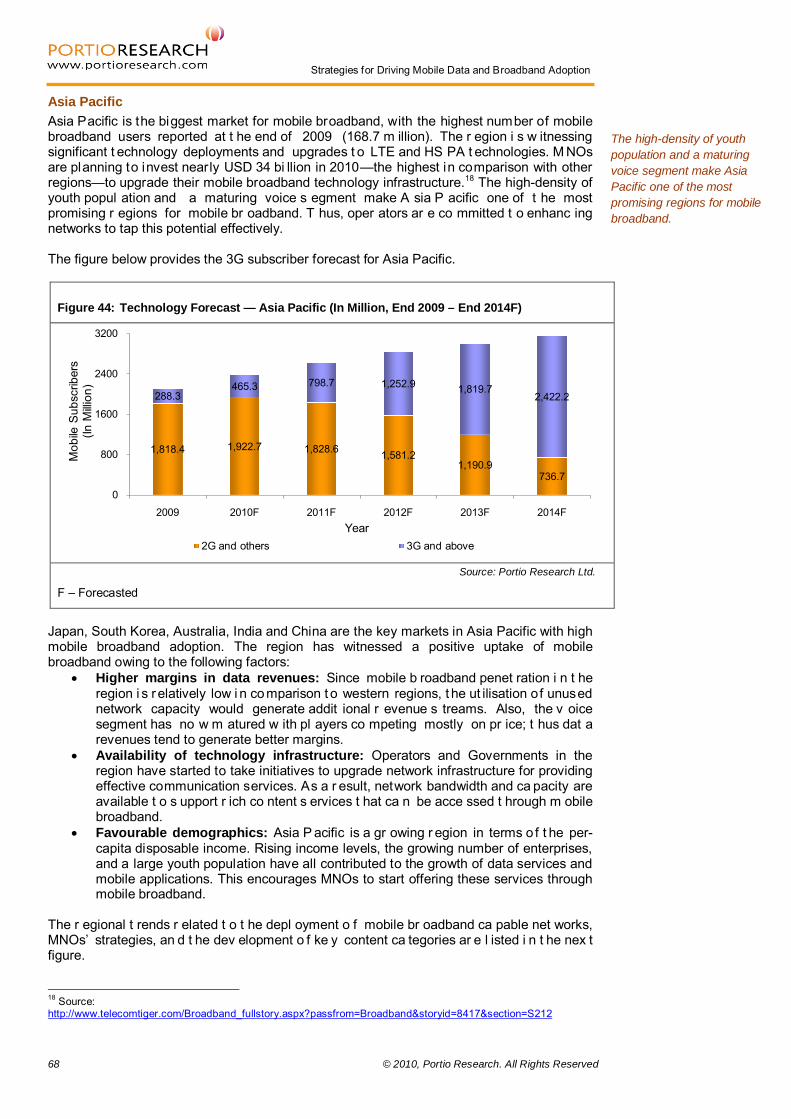

Regional Trends ........................................................................................................................... 66 Europe ...................................................................................................................................... 66 Asia Pacific ............................................................................................................................... 68 North America ........................................................................................................................... 70 Latin America ............................................................................................................................ 72 Africa and Middle East ............................................................................................................... 74

Mobile Broadband – Strategy Case Studies .................................................................... 77 Case Studies ............................................................................................................................... 77

Vodafone UK ............................................................................................................................. 77 NTT DOCOMO Japan................................................................................................................ 82 Verizon Wireless US .................................................................................................................. 90 Orange UK ................................................................................................................................ 94

Key Parameters for the Uptake of Mobile Broadband .................................................................... 97 Mobile Applications – Introduction and Market Size ....................................................... 99

4 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

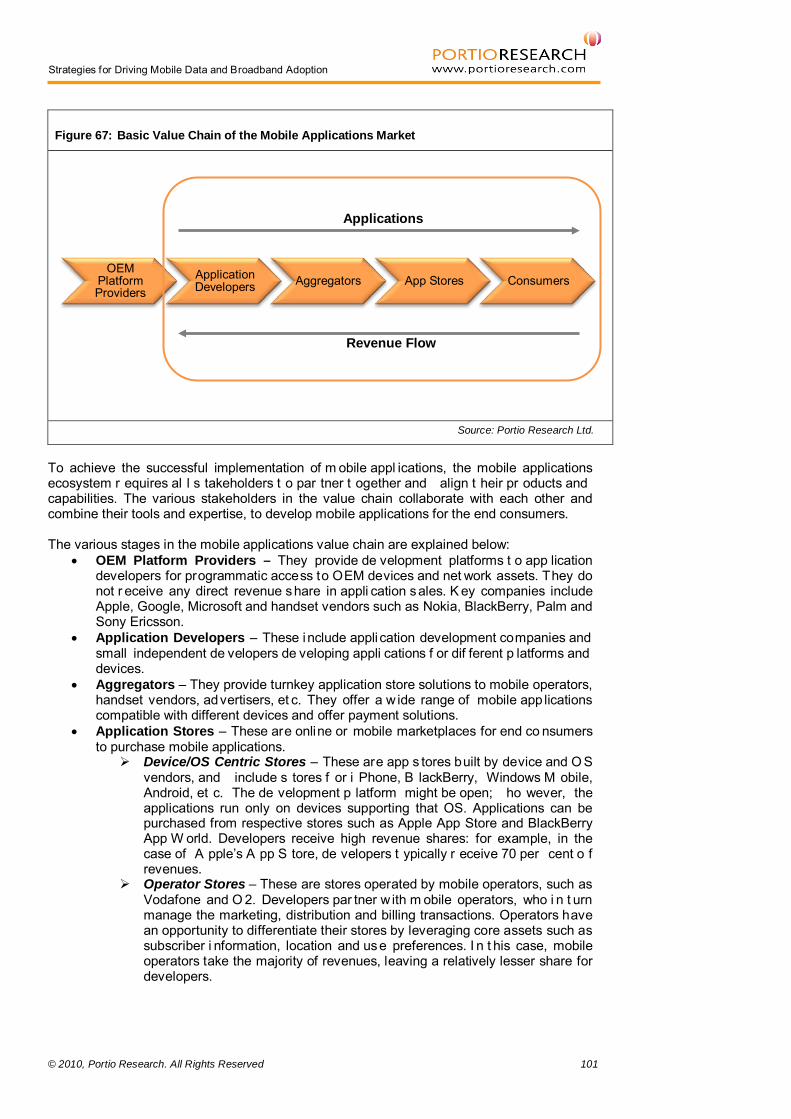

Overview ..................................................................................................................................... 99 Value Chain and Ecosystem ....................................................................................................... 100

Mobile Application Stores ......................................................................................................... 102 Business Model and Revenue Sharing ........................................................................................ 103

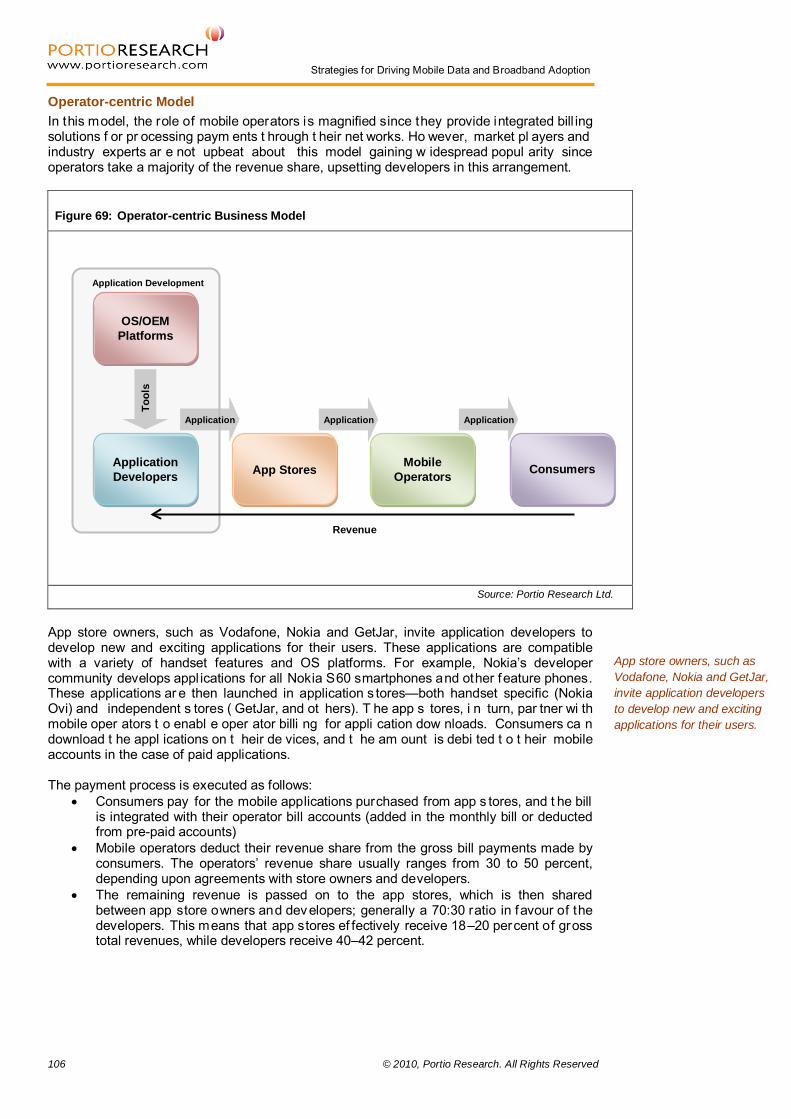

App-centric Model .................................................................................................................... 104 Operator-centric Model ............................................................................................................ 106

Market Size ................................................................................................................................ 108 Mobile Applications User Base ................................................................................................. 108 Mobile Applications Revenue ................................................................................................... 111

Mobile Applications – Strategy Case Studies ................................................................ 115 Apple App Store ......................................................................................................................... 115

Business Model ....................................................................................................................... 116 Key Developments .................................................................................................................. 116

Vodafone 360 ............................................................................................................................ 117 Business Model ....................................................................................................................... 119 Key Developments .................................................................................................................. 119

GetJar ....................................................................................................................................... 120 Business Model ....................................................................................................................... 120 Key Partnerships ..................................................................................................................... 121 Downloads .............................................................................................................................. 121

Conclusion ................................................................................................................................. 123 App Stores .............................................................................................................................. 123

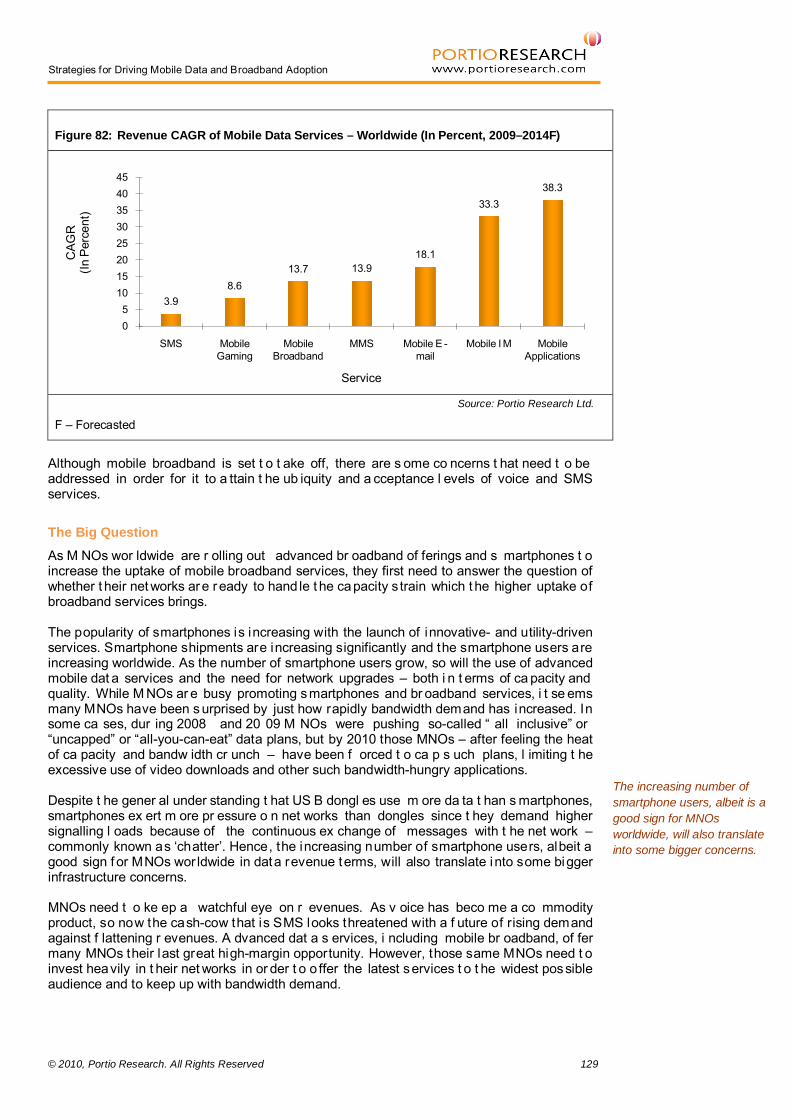

Conclusion ...................................................................................................................... 127 Current Scenario ........................................................................................................................ 127 The Big Question ....................................................................................................................... 129

Investment in Mobile Broadband Networks ............................................................................... 130 Growing Demand for Data Services ......................................................................................... 130 Coping with High Data Use ...................................................................................................... 132 AT&T – A Lesson To Be Learnt ................................................................................................ 132

Possible Answers and the Way Forward ..................................................................................... 134 Augmenting Networks .............................................................................................................. 134 Getting the Pricing Models Right .............................................................................................. 135 Future Outlook......................................................................................................................... 137

Appendices ..................................................................................................................... 139 Glossary .................................................................................................................................. 140 Portio Research Classifications ................................................................................................ 153 Companies Mentioned in this Report ........................................................................................ 154 About the Authors .................................................................................................................... 157

Also available from Portio Research Limited................................................................................ 158

© 2010, Portio Research. All Rights Reserved 5

Strategies for Driving Mobile Data and Broadband Adoption

List of Figures Figure 1: Comparison on the basis of Mobile Broadband Parameters – Regional .......................... 10Figure 2: Mobile Subscribers – Worldwide (In Million, 2009 – 2014F) ........................................... 12Figure 3: Worldwide Subscriber Base – Regional Contribution (In Percent, 2009) ......................... 13Figure 4: Worldwide Subscriber Base – Regional Contribution (In Percent, 2014F) ....................... 13Figure 5: Mobile Subscriber Base Growth by Region (In Percent, 2009 – 2014F) .......................... 14Figure 6: Factors Behind a Successful Data Service .................................................................... 17Figure 7: Data Services Covered in Our Reports ‘Strategies for Creating End-User Demand for

Mobile Data Services’, ‘Strategies for Driving Data ARPU’ and ‘Strategies for Driving Mobile Data and Broadband Adoption’ .......................................................................... 20

Figure 8: SMS and MMS Traffic – Worldwide (In Billion, 2009) ..................................................... 22Figure 9: Mobile E-mail and Mobile IM Users – Worldwide (In Million, 2009) ................................. 22Figure 10: Revenue of Mobile Messaging Services (In USD Billion, 2009) ...................................... 23Figure 11: Comparison of Mobile Messaging Services ................................................................... 24Figure 12: SMS Traffic – Telkomsel and Excelcomindo (In Billion, 2007 – 2009) ............................. 26Figure 13: SMS Traffic – Telkomsel (In Billion, Q1 2009 – Q4 2009) ............................................... 27Figure 14: SMS Revenue – Telkomsel (In USD Million, Q1 2009 – Q3 2009) .................................. 27Figure 15: SMS Tariffs and Promotional Plans – Telkomsel ........................................................... 28Figure 16: MMS Users – China Mobile (In Million, End 2007 – End 2009) ....................................... 31Figure 17: MMS Traffic per Active User per Year – China Mobile (2007 – 2009) ............................. 32Figure 18: MMS Revenue – China Mobile (In USD Million, 2007 – 2009) ........................................ 32Figure 19: M-News Paying Subscribers – China Mobile (In Million, End 2006 – End 2009) .............. 34Figure 20: Number of S! Information Channel Applications – SoftBank (January 2010 – April 2010) 36Figure 21: 3G Subscribers as a Percentage of Total Subscriber Base – Japan (In Percent, Q2 2009 –

Q4 2009) ..................................................................................................................... 37Figure 22: Mobile Internet Subscribers – SoftBank (In Million, Q2 2009 – Q4 2009) ....................... 38Figure 23: Data ARPU – SoftBank (In USD, Q2 2009 – Q4 2009) .................................................. 38Figure 24: Revenue CAGR of Mobile Messaging Services (In Percent, 2009 – 2014F) ................... 42Figure 25: UMTS Evolution – Data Transfer Rates ......................................................................... 47Figure 26: LTE Evolution – Data Transfer Rates ............................................................................ 48Figure 27: EDGE Evolution – Data Transfer Rates ......................................................................... 49Figure 28: CDMA2000 Evolution – Data Transfer Rates ................................................................. 51Figure 29: Drivers of Mobile Broadband ......................................................................................... 53Figure 30: Inhibitors of Mobile Broadband ..................................................................................... 54Figure 31: USB Modems/ Dongles ................................................................................................ 55Figure 32: PC and Express Cards ................................................................................................. 57Figure 33: Mobile Broadband User Base – Worldwide (In Million, 2009 – 2014F) ............................ 59Figure 34: Worldwide Mobile Broadband Users – Regional Contribution (In Percent, 2009) ............. 60Figure 35: Worldwide Mobile Broadband Users – Regional Contribution (In Percent, 2014F) ......... 61Figure 36: Mobile Broadband User Base Growth by Region (In Percent, 2009 – 2014F) ................. 61Figure 37: Mobile Broadband Users as a Percentage of Total Mobile Subscribers – Regional (In

Percent, 2009 & 2014F) ............................................................................................... 62Figure 38: Mobile Broadband Revenue – Worldwide (In USD Billion, 2009 – 2014F) ....................... 63Figure 39: Worldwide Mobile Broadband Revenue – Regional Contribution (In Percent, 2009) ........ 64Figure 40: Worldwide Mobile Broadband Revenue – Regional Contribution (In Percent, 2014F) .... 64Figure 41: Mobile Broadband Revenue Growth by Region (In Percent, 2009 – 2014F) .................... 65Figure 42: Technology Forecast — Europe (In Million, End 2009 – End 2014F) .............................. 66Figure 43: Regional Trends — Europe .......................................................................................... 67Figure 44: Technology Forecast — Asia Pacific (In Million, End 2009 – End 2014F) ....................... 68Figure 45: Regional Trends — Asia Pacific .................................................................................... 69Figure 46: Technology Forecast — North America (In Million, End 2009 – End 2014F) ................... 70Figure 47: Regional Trends — North America ................................................................................ 71Figure 48: Technology Forecast — Latin America (In Million, End 2009 – End 2014F) .................... 72Figure 49: Regional Trends — Latin America ................................................................................. 73Figure 50: Technology Forecast —Africa and Middle East (In Million, End 2009 – End 2014F) ........ 74Figure 51: Regional Trends — Africa and Middle East ................................................................... 75

6 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

Figure 52: 3G Subscribers as a Percentage of Total Subscriber Base – The UK (In Percent, December 2009) .......................................................................................................... 78

Figure 53: Increase in 3G Subscribers Percentage – The UK (In Percentage Points, Q1 2009 – Q4 2009) .......................................................................................................................... 78

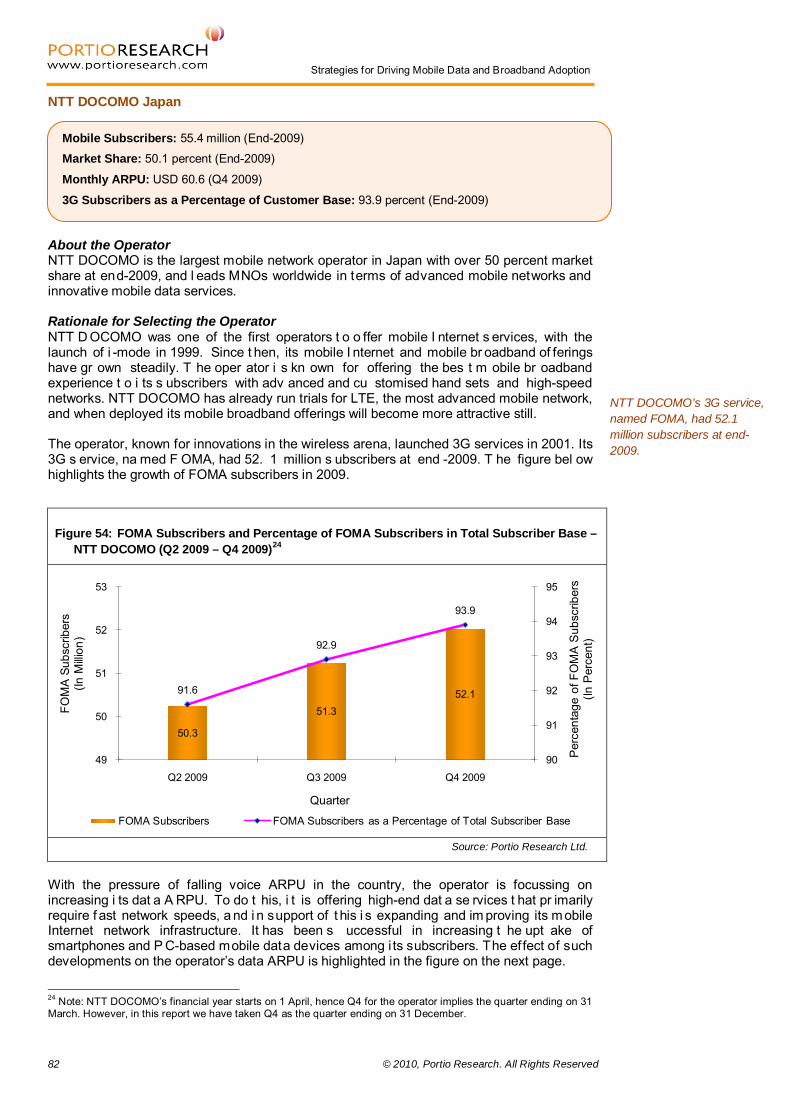

Figure 54: FOMA Subscribers and Percentage of FOMA Subscribers in Total Subscriber Base – NTT DOCOMO (Q2 2009 – Q4 2009) .................................................................................. 82

Figure 55: Packet ARPU – NTT DOCOMO (In USD, Q2 2009 – Q4 2009) ...................................... 83Figure 56: i-mode ARPU – NTT DOCOMO (In USD, Q2 2009 – Q4 2009) ...................................... 84Figure 57: Subscribers – Bee TV (In Million, Q2 2009 – Q4 2009) .................................................. 85Figure 58: Subscribers – i-concier (In Million, Q2 2009 – Q4 2009) ................................................. 85Figure 59: Number of Content Sites – NTT DOCOMO (Q2 2009 – Q4 2009) .................................. 86Figure 60: Subscribers – Pake-hodai (In Million, Q2 2009 – Q4 2009) ............................................ 86Figure 61: PC Data Communication Devices Sold – NTT DOCOMO (In Million, Q2 2009 – Q4 2009)

..

............................................................................................................................... 87Figure 62: PC Data Communications Flat Rate and Use Based Data Plan Subscriptions – NTT

DOCOMO (In Million, Q2 2009 – Q4 2009) ................................................................... 87Figure 63: Data ARPU – The US (In USD, Q1 2009 – Q4 2009) ..................................................... 90Figure 64: Monthly Data Plans for Mobile Subscribers – Verizon Wireless (March 2010) ................. 92Figure 65: MNOs’ Absolute and Percentage Growth in 3G Subscriber Base – The UK (2009) ......... 94Figure 66: 3G Dongle Subscribers and Percentage of 3G Dongle Subscribers in Total 3G Subscriber

Base – Orange UK (Q2 2009 – Q4 2009) ..................................................................... 95Figure 67: Basic Value Chain of the Mobile Applications Market ................................................... 101Figure 68: App-centric Business Model ....................................................................................... 104Figure 69: Operator-centric Business Model ................................................................................ 106Figure 70: Revenue Sharing in the Case of an Operator-centric Business Model .......................... 107Figure 71: Mobile Applications User Base – Worldwide (In Million, 2009 – 2014F) ........................ 108Figure 72: Worldwide Mobile Applications Users – Regional Contribution (In Percent, 2009) ......... 109Figure 73: Worldwide Mobile Applications Users – Regional Contribution (In Percent, 2014F) ..... 110Figure 74: Mobile Applications User Base Growth by Region (In Percent, 2009 – 2014F) .............. 110Figure 75: Mobile Applications Revenue – Worldwide (In USD Billion, 2009 – 2014F) ................... 111Figure 76: Worldwide Mobile Applications Revenue – Regional Contribution (In Percent, 2009) .... 112Figure 77: Worldwide Mobile Applications Revenue – Regional Contribution (In Percent, 2014F) 112Figure 78: Mobile Applications Revenue Growth by Region (In Percent, 2009 – 2014F) ................ 113Figure 79: Apple’s App Store – Total Application Downloads ........................................................ 115Figure 80: Break-out of Available Applications by Category – Apple App Store (In Percent, April 2010)

............................................................................................................................. 116Figure 81: Mobile Broadband User Base as a Percentage of Total Mobile Subscribers – Worldwide

(In Percent, 2009 – 2014F) ........................................................................................ 128Figure 82: Revenue CAGR of Mobile Data Services – Worldwide (In Percent, 2009–2014F) ......... 129Figure 83: Mobile Broadband CAPEX and Revenues by Region (In USD Billion, 2010F) ............... 130Figure 84: Average Monthly Data Use for USB Dongles, Feature Phones and Smartphones –

Worldwide (In GB, 2009) ............................................................................................ 131Figure 85: Average Worldwide Selling Price of Nokia Handsets and Apple’s iPhone (In USD, 2007 –

2009) ........................................................................................................................ 135Figure 86: Average Cost per MB of Mobile Data Services – North America (In USD, 2007 – 2009) 136

© 2010, Portio Research. All Rights Reserved 7

Strategies for Driving Mobile Data and Broadband Adoption

List of Tables Table 1: Mobile Subscribers – Regional (In Million, 2009 – 2014F) .............................................. 12Table 2: Success Factors – Telkomsel Indonesia ....................................................................... 30Table 3: Success Factors – China Mobile ................................................................................... 35Table 4: Success Factors – SoftBank Japan ............................................................................... 41Table 5: Factors Affecting the Uptake of Mobile Messaging Services .......................................... 43Table 6: Number of Network Providers with High Speed Network Deployments – Regional (March

2010) .......................................................................................................................... 45Table 7: Examples of Partnerships between Mobile Operators and Laptop Manufacturers ........... 56Table 8: Regional Versions – Mobile Networks ........................................................................... 57Table 9: Mobile Broadband User Base – Regional (In Million, 2009 – 2014F) .............................. 60Table 10: Mobile Broadband User Base as a Percentage of Total Mobile Subscribers – Regional (In

Percent, 2009 – 2014F) ............................................................................................... 62Table 11: Mobile Broadband Revenue – Regional (In USD Billion, 2009 – 2014F) ......................... 63Table 12: Success Factors – Vodafone UK .................................................................................. 81Table 13: Success Factors – NTT DOCOMO Japan ..................................................................... 89Table 14: MNOs’ Key Performance Indicators – The US (2009) .................................................... 90Table 15: Success Factors – Verizon Wireless US ....................................................................... 93Table 16: Success Factors – Orange UK ...................................................................................... 96Table 17: Strategies to Push Mobile Broadband Uptake ................................................................ 97Table 18: Major Application Stores ............................................................................................. 103Table 19: Mobile Applications User Base – Regional (In Million, 2009 – 2014F) ........................... 109Table 20: Mobile Applications Revenue – Regional (In USD Million, 2009 – 2014F) ..................... 111Table 21: Top 20 Applications on GetJar and Total Downloads, as of November 2009 ................ 122Table 22: Key Success Factors for Application Stores ................................................................ 125Table 23: Mobile Applications and Data Transfer Rate Requirements .......................................... 131Table 24: Strategies to Cope with the Increasing Demand Data Services place on Networks ....... 134Table 25: Prices of iPhone Models offered by AT&T ................................................................... 136

8 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

Chapter 1 Introduction

© 2010, Portio Research. All Rights Reserved 9

Strategies for Driving Mobile Data and Broadband Adoption

Introduction Mobile handsets have become an intrinsic part of users’ lives worldwide. For many, it is the only way to co mmunicate w ith f amily and f riends, and n ot o nly are these users today completely dependent on t heir mobile handsets f or communication, they also rely on them for several other purposes that are equally important in their daily lives. Mobile handsets are now used for purposes previously associated with only PCs. Users are, for example, accessing the Internet on t heir handsets, buying t ickets for events and t ravel, and finding routes to their favourite destinations through maps. With the changing requirements of mobile subscribers, operators worldwide need to innovate and take proactive initiatives in order to retain subscriber interest in their services. Mobile broadband is one s uch dynamic area where a num ber of changes are taking place; millions of mobile applications are being developed worldwide and low-cost smartphones are being introduced by mobile network operators (MNOs). MNOs worldwide have taken several initiatives to cater to the increasing uptake of mobile broadband services, including the deployment of advanced and high-speed mobile networks. Mobile broadband services are al ready popular in advanced mobile markets and operators in em erging markets ar e al so m aking e fforts t o pen etrate t hese services. O perators ar e offering a variety of attractive price plans, ranging from ‘pay as you go’ to ‘flat-rate unlimited use’ plans, to provide freedom of choice to their subscribers to select a dat a plan that best suits their requirements. Apart from pricing, operators are trying to attract more users to their mobile broadband services with a range of high quality hardware offerings, including laptops and dongles manufactured by leading manufacturers worldwide. In order to deliver these advanced offerings, operators are upgrading their mobile networks, including their core networks. Currently, more than 300 MNOs worldwide have deployed CDMA 2000 net works, which includes both CDMA2000 1X and 1xEV-DO.1 The number of operators worldwide with hi gh s peed packe t acce ss (HSPA) depl oyments i s also abo ve 300.2

• Network

Some of the major MNOs in advanced markets, such as the US and Japan, have already run trials on LTE or 4G networks; and many MNOs worldwide have expressed plans to depl oy LTE net works i n t heir r espective markets by end-2013. W ith such infrastructure deployments scheduled, the future for mobile broadband services looks promising. MNOs w orldwide hav e t o constantly make e fforts t o en sure t hat t heir mobile br oadband packages ar e b etter i n e very sense. T he four most im portant parameters that M NOs worldwide should focus on in order to make their mobile broadband offerings more attractive are listed below:

• Pricing • Content • Devices

The figure on the next page compares the performance of regions worldwide on the basis of these parameters.

1 Source: CDMA Development Group (CDG) 2 Source: 3G Americas

Mobile broadband services are already popular in advanced mobile markets and operators in emerging markets are also making efforts to penetrate these services.

10 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

North America leads other regions worldwide in terms of advanced mobile network deployments and i nnovative content offerings. Verizon and A T&T are all s et t o launch 4G networks in 2011, f or which t rials are currently running. When it comes to mobile content, Apple’s App Store is the clear leader among application stores. Europe al so scores hi gh on t his net work parameter, at tributable primarily to the advanced Western European markets – as many countries in Eastern Europe are still developing their networks. In t erms of devices and pr icing of se rvices, A sia P acific i s the leading regional market. In some co untries, such a s Chi na an d I ndia, MNOs are f looding the market w ith low-cost smartphones capable of per forming any function and r unning any application. Whereas in markets such as Japan and South Korea, MNOs are offering some of the most adv anced handsets t hat al low subscribers to get t he b est user experience f rom mobile appl ications. MNOs in Asia Pacific are known to offer mobile services at prices well below the worldwide average, as they recognise that pricing is probably the most important factor influencing the decision of the r egion’s m obile subscribers. For t his reason, MNOs i n Asia P acific are especially careful when pricing their offerings.

3 Note: The value of each axis ranges between 0 and 5, with 0 denoting the worst performer and 5 denoting the best performer for the respective parameter. For instance, a score of 5 for pricing does not imply that the region has the highest prices, but rather it is offering services at low prices keeping the subscribers’ price sensitivity in perspective.

Figure 1: Comparison on the basis of Mobile Broadband Parameters – Regional3

Source: Portio Research Ltd.

MNOs in Asia Pacific are known to offer mobile services at prices well below the worldwide average, as they recognise that pricing is probably the most important factor influencing the decision of the region’s mobile subscribers.

0

1

2

3

4

5Network

Pricing

Content

Devices

North America Europe Asia Pacific Latin America Africa and Middle East

© 2010, Portio Research. All Rights Reserved 11

Strategies for Driving Mobile Data and Broadband Adoption

Chapter 2 Worldwide Mobile Market

12 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

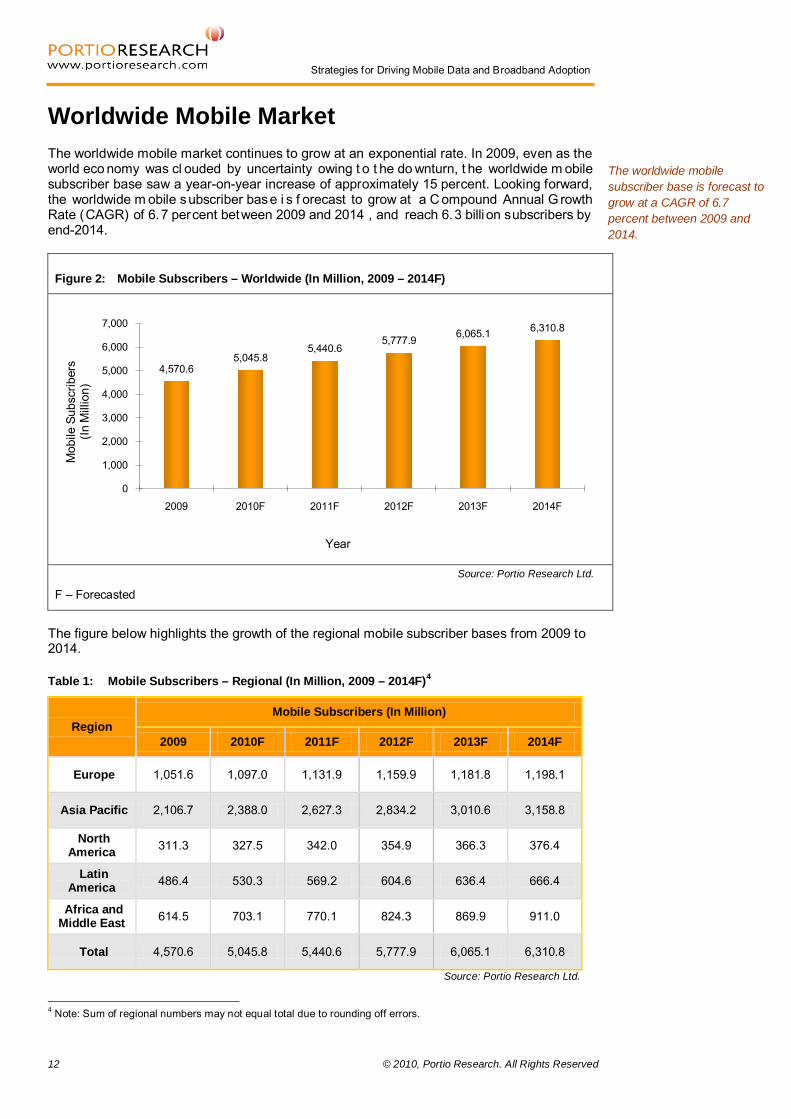

Worldwide Mobile Market The worldwide mobile market continues to grow at an exponential rate. In 2009, even as the world eco nomy was cl ouded by uncertainty owing t o t he do wnturn, t he worldwide m obile subscriber base saw a year-on-year increase of approximately 15 percent. Looking forward, the worldwide m obile subscriber base i s f orecast to grow at a C ompound Annual G rowth Rate (CAGR) of 6.7 percent between 2009 and 2014 , and reach 6.3 billi on subscribers by end-2014.

Figure 2: Mobile Subscribers – Worldwide (In Million, 2009 – 2014F)

Source: Portio Research Ltd.

F – Forecasted

The figure below highlights the growth of the regional mobile subscriber bases from 2009 to 2014.

Table 1: Mobile Subscribers – Regional (In Million, 2009 – 2014F)4

Region Mobile Subscribers (In Million)

2009 2010F 2011F 2012F 2013F 2014F

Europe 1,051.6 1,097.0 1,131.9 1,159.9 1,181.8 1,198.1

Asia Pacific 2,106.7 2,388.0 2,627.3 2,834.2 3,010.6 3,158.8

North America 311.3 327.5 342.0 354.9 366.3 376.4

Latin America 486.4 530.3 569.2 604.6 636.4 666.4

Africa and Middle East 614.5 703.1 770.1 824.3 869.9 911.0

Total 4,570.6 5,045.8 5,440.6 5,777.9 6,065.1 6,310.8

Source: Portio Research Ltd.

4 Note: Sum of regional numbers may not equal total due to rounding off errors.

4,570.65,045.8

5,440.65,777.9 6,065.1 6,310.8

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2009 2010F 2011F 2012F 2013F 2014F

Mob

ile S

ubsc

riber

s(In

Mill

ion)

Year

The worldwide mobile subscriber base is forecast to grow at a CAGR of 6.7 percent between 2009 and 2014.

© 2010, Portio Research. All Rights Reserved 13

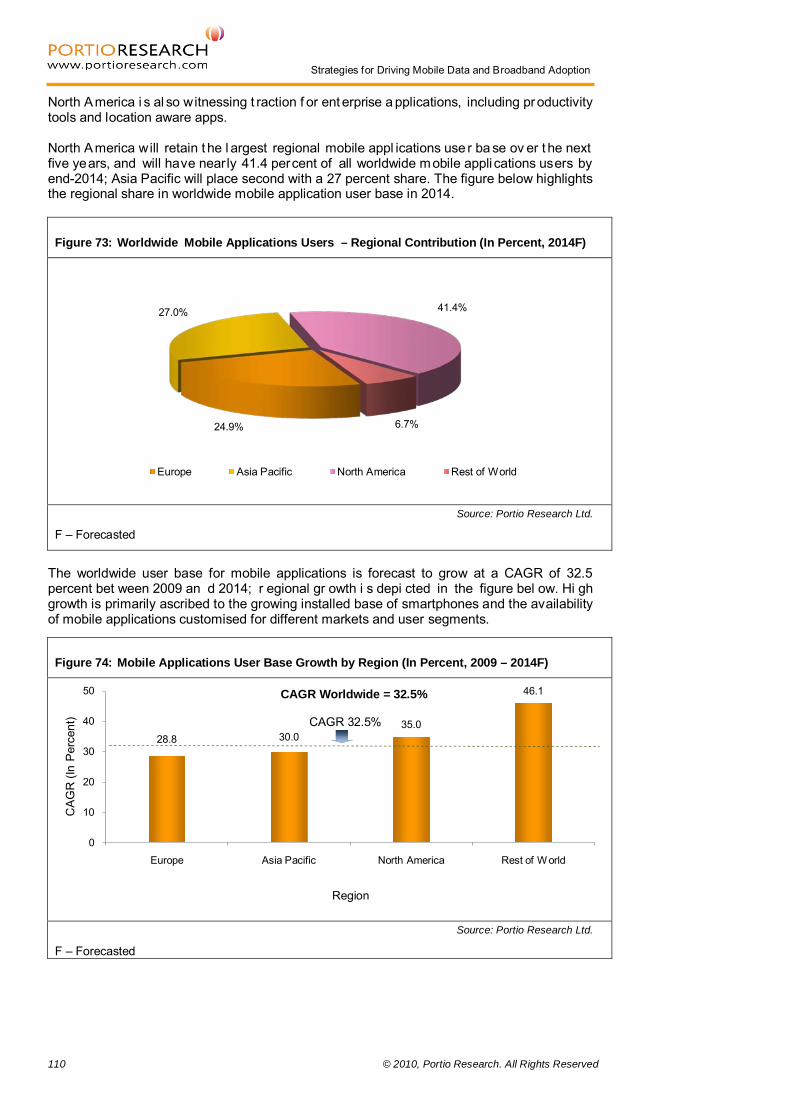

Strategies for Driving Mobile Data and Broadband Adoption Asia Pacific possesses the largest mobile subscriber base worldwide. In 2009, this regional subscriber base constituted 46.1 percent of the worldwide mobile subscriber base; Europe placed second with a 23 percent contribution. The figure below shows the regional share in the worldwide mobile subscriber base in 2009.

Asia Pacific will continue to dominate the worldwide mobile industry in terms of subscriber base in the coming years, and will strengthen its position further with over 50 percent of the worldwide mobile subscriber base residing in the region by end-2014. Europe is expected to lose some of its share, with its contribution dropping to 19 percent by end-2014. The figure below highlights the regional share in the worldwide mobile subscriber base in 2014.

5, 6 Note: The percentages do not add up to 100 percent because of rounding off errors.

Figure 3: Worldwide Subscriber Base – Regional Contribution (In Percent, 2009)5

Source: Portio Research Ltd.

Figure 4: Worldwide Subscriber Base – Regional Contribution (In Percent, 2014F)6

Source: Portio Research Ltd.

F – Forecasted

23.0%

46.1%6.8%

10.6%

13.4%

Europe Asia Pacific North America Latin America Africa and Middle East

19.0%

50.1% 6.0%

10.6%

14.4%

Europe Asia Pacific North America Latin America Africa and Middle East

14 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

The worldwide mobile subscriber base is forecast to grow at a CAGR of 6.7 percent between 2009 and 2014. During this period, Asia Pacific will lead regions worldwide in terms of subscriber growth with a CAGR of 8.4 percent, albeit with Africa and Middle East in close pursuit, while Europe is ant icipated t o witness t he l owest growth rate with a CA GR of 2. 6 percent.

Figure 5: Mobile Subscriber Base Growth by Region (In Percent, 2009 – 2014F)

Source: Portio Research Ltd.

F – Forecasted

8.4

2.6

3.9

6.5

8.2

0

3

6

9

Asia Pacific Europe North America Latin America Africa and Middle East

CA

GR

(In

Per

cent

)

Region

CAGR Worldwide = 6.7 % CAGR 6.7%

© 2010, Portio Research. All Rights Reserved 15

Strategies for Driving Mobile Data and Broadband Adoption

Chapter 3 Worldwide Data Services Market

16 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

Worldwide Data Services Market

‘Strategies for Dr iving Mobile Dat a and B roadband Adoption’ i s t he l atest edi tion in Portio Research’s series of reports covering the worldwide mobile data services market. It follows earlier analysis in Portio’s ‘Strategies for Driving Data ARPU’ (published in 2008) and ‘S trategies f or Cr eating E nd-User Dem and f or M obile Dat a S ervices’ (published in 2006), which both covered the popular data services of their time, and the strategies adopted by MNOs worldwide. The section below briefly discusses the evolution of mobile data services and the ef fective strategies adopted by MNOs to popularise their data offerings. Strategies for Driving Data ARPU

The ‘Strategies f or Dr iving Dat a A RPU’ report anal ysed m obile oper ators’ shift i n focus towards data services, mainly due t o decl ining revenues from voice services. This r eport focussed on summarising successful data strategies adopted by mobile network operators, and covered the following types of services:

• Messaging services SMS Mobile e-mail Mobile IM

• Non-messaging mobile services Mobile music Mobile games Mobile TV and video Mobile user generated content Mobile commerce Mobile portals

Furthermore, t he r eport i ncluded i nformation on i nnovative dat a s ervices adopt ed by emerging nations such as India, Egypt, China, South Africa and Kenya. This report summarised various f actors t hat enabl e MNOs to l aunch and dr ive successful data services. Let us look at the highlights of these factors.

© 2010, Portio Research. All Rights Reserved 17

Strategies for Driving Mobile Data and Broadband Adoption

Figure 6: Factors Behind a Successful Data Service

Source: Portio Research Ltd. Expand Perceived Value The r eport hi ghlighted t he im portance of implementing a s ervice t hat adds v alue t o subscribers, rather t han being just an addi tion/upgrade t o t he exi sting ar ray of s ervices. Furthermore, it is equally important to price the service while keeping in mind the target audience. The service price is a combination o f t he following factors – understanding t he target audi ence and t heir pr eferences, t he value t hat t he new service w ill deliv er t o the audience, and a cost that falls within the spending power of the target audience. Striking the right balance between these factors can make a new data service successful. A good ex ample o f de livering value t o s ubscribers i s V odafone E gypt’s M inicall s ervice. Minicall is an audi o m essaging service t hat all ows subscribers t o r ecord sh ort voice messages and send them as SMS to any network. Minimise ‘Clicks to Access’ For mass adoption of a data service, the operator should ensure that the usability of such a service is simple and t he service is easy to acce ss. A subscriber may lose interest if they have to go through several links/buttons to access the service. Though it is understandable that not all services can be provided at the single click of a button, the operator should ensure that the portal that hosts the data service is accessible and easy to use. 3 I talia launched new han dsets al ong with the l aunch of its mobile T V s ervices. T hese handsets came with a TV button that gave subscribers easy access to mobile TV. Choose the Right Data Service An operator should not only understand the subscriber’s need for a data service, it should also under stand t he r esources required to im plement s uch a s ervice. Each dat a s ervice requires a different degree of resources; an operator should keep a watchful eye over the feasibility of i ntroducing a s ervice, eas e of upgr ading it, and t he ca pital and manpower required.

Factors Behind a

Successful Data

Service

Expand Perceived

Value

Minimize 'Clicks to Access'

Choosing the Right

Data Service

Launch Timing

Business Model

Continuing Updgrades

An operator should not only understand the subscriber’s need for a data service, it should also understand the resources required to implement such a service.

18 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

Launch Timing Correctly planning the right time to launch a data service plays a very important part in helping subscribers to easily relate to the service. Among the notable success stories highlighting the importance of effective launch timing is NTT DOCOMO’s l aunch of m obile e-mail services in Ja pan, since Ja panese subscribers were more inclined to write lengthy messages, as opposed to the general t rend of sending SMS. Similarly, 3 Italia launched its mobile TV services during the 2006 football World Cup (which Italy went on to win). These two services garnered success with increased user base for the services, and subsequently increased data ARPU. Creating the Right Business Model For a data service to be a commercial success, an appropriate business model must be identified. Even if a data service achieves high adoption rates, the operator may not gain the maximum benefit if the business model is not right. As data services involve other players in the value chain, it is important for the operator to have control over this value chain to garner success from the services. NTT DOCOMO’s DCMX (Mobile Credit Card) service was lauded for its successful business model. N TT DO COMO acq uired a s take i n Sumitomo Mitsui Car ds, a co mpany with experience i n del ivering cr edit ca rd s ervices. T his par tnership was cr ucial for cr eating a successful business model for the DCMX data service. Be Ready with Upgrades The success of a dat a service is quickly outlived by new innovative services; its lifecycle is short due to the high number of innovations in the mobile industry. Hence, operators should offer regular upgrades to the portfolio of services provided. The pr ogression f rom monophonic r ingtones t o pol yphonic ringtones t o ca ller r ing back tones, and f inally, to full t rack music downloads demonstrates the importance of upgrades within existing services.

Correctly planning the right time to launch a data service plays a very important part in helping subscribers to easily relate to the service.

The success of a data service is quickly outlived by new innovative services; its lifecycle is short due to the high number of innovations in the mobile industry.

© 2010, Portio Research. All Rights Reserved 19

Strategies for Driving Mobile Data and Broadband Adoption Strategies for Creating End-User Demand for Mobile Data Services

Our ‘S trategies for Cr eating E nd-User Dem and f or M obile Dat a S ervices’ r eport was released in 2006. As voice services were getting commoditised in the developed nations and operators were forced to adopt new data services, this report analysed the strategies adopted by operators for different mobile services. This report acted as a ‘best practice’ case hi story that co uld be f ollowed by mobile ope rators. S ome o f t he im portant recommendations made by the report are as follows: Choice and Flexibility A dat a s ervice w ill be s uccessful if it offers several options. T hese opt ions can be with respect t o t he a vailability of t he co ntent and t he hands ets, and al so h ow t he co ntent i s stored in the handset after its purchase. Segmentation Segmenting the data service according to the target audience is a key factor in the success of the service. A data service, even if it is good, may not achieve success if it is not targeted at the right audience. Low-Cost Services and Transparent Pricing A data service should be priced according to the affordability of the target audience. Additionally, a service should be cross-subsidised; for example, to drive the use of SMS, the operator can increase voice tariffs and simultaneously reduce SMS prices. High-Value Proposition A subscriber will use a data service only if they can realise the value in using such a service. The value offered by the service should be per ceived as greater than the cost of using the service. Focus on Brand Subscribers feel more confident in using the services of a known brand. Hence, branding is a key aspect that drives the uptake of a s ervice. Operators should create partnerships with leading brands to provide data services. Innovation Innovative s ervices al ways ca tch subscribers’ attention. A n i nnovative s ervice s hould be supplemented with devices that can support it. Simplicity and Ease of Use Operators and handset vendors should pay attention to the user-interface of a data service. A great data service that is not easy to use may not garner success. SMS is an apt example in this case, as the service is easy to use. Handsets Handset vendors should work in coordination with mobile operators to launch handsets that are capable of supporting i nnovative services l aunched by operators. Handsets should be simple to use and offer several choices in terms of features and prices to match subscribers’ expectations.

A subscriber will use a data service only if they can realise the value in using such a service. The value offered by the service should be perceived as greater than the cost of using the service.

20 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

Data Services

Figure 7: Data Services Covered in Our Reports ‘Strategies for Creating End-User Demand for Mobile Data Services’, ‘Strategies for Driving Data ARPU’ and ‘Strategies for Driving Mobile Data and Broadband Adoption’

Source: Portio Research Ltd.

Messaging Services

• SMS • MMS • E-Mail • IM

As indicated i n ou r e arlier r eports (‘Strategies for C reating End-User D emand f or M obile D ata Services’ and ‘ Strategies for D riving D ata A RPU’), S MS co ntinues to be t he m aster of al l messaging services. Revenue generated by SMS services currently equates to much more than the consolidated revenues of the other messaging services and this trend is expected to continue.

Emerging Broadband

Services

• Social Networking • Audio and Video Downloads/ Streaming • Online Gaming

The evolution of mobile communication from simple voice and SMS to advanced data services and beyond has now led to the introduction of mobile broadband services. These services have started to achieve great popularity and penetration across most markets. Social networking has achieved immense worldwide popularity. Social networks allow subscribers to co nnect w ith f riends and al so upl oad p ictures/videos. As m obile br oadband a llows access to social networks through mobiles, it was an immediate success. The key drivers for mobile social networking are ease of using the service, ability to access the service anytime and anywhere, and the availability of mobile applications to send and receive messages or upload pictures/ videos. In the near future, social networking is expected to be a major driver for mobile broadband. Audio downloads became popular when mobile handsets with audio playback capabilities were introduced i n t he market; t he sa me l ogic applied t o video dow nloads. F urthermore, w ith the increasing popularity of streaming websites, mobile audio/video streams are also on the rise. Another popular mobile broadband service is online gaming, which has achieved popularity due to the availability of high-end handsets. Online gaming is more popular among the youth generation, supported by the availability of free and ad-funded games.

Other Services

• Services with limited popularity Mobile TV Video Calling

• Popular services from the past Ringtones

Mobile TV has yet not achieved the universal popularity it was expected to attain. Countries such as France and Italy, that have a particularly high inclination towards sports, have adopted Mobile TV quickly and have contributed to the success of such services in these nations. However, similar success has not been replicated in developing nations, mainly due to the high cost of services. Video calling services have also seen limited adoption, mainly due to the high cost of the services, but also because video calling requires 3G enabled handsets, which limits service use to high-end smartphones only. Ringtones slowly drowned under the evolution of mobile handsets and full track downloads. When a handset is capable of playing MP3 songs and the same can be used as a ringtone, the use of ringtones markedly declines.

© 2010, Portio Research. All Rights Reserved 21

Strategies for Driving Mobile Data and Broadband Adoption

Chapter 4 Worldwide Mobile Messaging

22 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

Worldwide Mobile Messaging Worldwide Mobile Messaging

Mobile messaging services are the most widely used mobile data services worldwide, and operators worldwide have been u sing these services to shore up revenues in recent years as v oice margins have declined. SMS is the most popular mobile messaging service, and accounts for the largest contribution to MNOs’ data revenues. MMS has typically performed well in advanced markets, but has struggled in emerging markets. Mobile e-mail and mobile instant m essaging (IM) are f aring well i n developed mobile m arkets, and they are seeing uptake in developing countries as well. The figure below compares the worldwide SMS and MMS traffic for 2009.

Figure 8: SMS and MMS Traffic – Worldwide (In Billion, 2009)

Source: Portio Research Ltd.

The figure below compares the number of mobile e-mail and mobile IM users worldwide for 2009.

Figure 9: Mobile E-mail and Mobile IM Users – Worldwide (In Million, 2009)

Source: Portio Research Ltd.

5,449.3

119.40

1,000

2,000

3,000

4,000

5,000

6,000

SMS MMS

Traf

fic(In

Bill

ion)

Service

330.5

191.1

0

50

100

150

200

250

300

350

Mobile E -mail Mobile I M

Use

rs(In

Mill

ion)

Service

Mobile e-mail and mobile instant messaging (IM) are faring well in developed mobile markets, and they are seeing uptake in developing countries as well.

© 2010, Portio Research. All Rights Reserved 23

Strategies for Driving Mobile Data and Broadband Adoption Dominance of SMS

The m obile m essaging segment comprises four services—SMS, MMS, mobile e -mail and mobile I M. S MS r ules t he mobile messaging world beca use of its ubi quity in all mobile markets worldwide and its use by nearly every mobile s ubscriber w orldwide. The f igure below compares revenue generated by each mobile messaging service in 2009.

Figure 10: Revenue of Mobile Messaging Services (In USD Billion, 2009)

Source: Portio Research Ltd.

The figure c learly highlights t he dominance o f SMS; i t a lone gener ated over double the collective revenues for the other three services in 2009. The primary factors behind the popularity of SMS are:

• Simplicity • Ease of use • Low cost • Compatibility with all handsets

MMS, mobile e-mail and mobile IM services cannot be availed on simple handsets, and instead demand a certain set of handset capabilities. In addition, subscribers are required to possess greater technical kn ow-how t o use these services w hereas using S MS i s more straight forward. The figure be low co mpares t he f our mobile messaging s ervices on t he bas is of t he aforementioned parameters.

102.3

26.717.3

4.3

0

20

40

60

80

100

120

SMS MMS Mobile E -Mail Mobile I M

Rev

enue

(In U

SD B

illio

n)

Service

MMS, mobile e-mail and mobile IM services cannot be availed on simple handsets, and instead demand a certain set of handset capabilities.

24 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

Figure 11: Comparison of Mobile Messaging Services

Source: Portio Research Ltd.

SMSMMS

Mobile E-mailMobile IM

Simplicity Ease of Use Cost Handset Compatibility

© 2010, Portio Research. All Rights Reserved 25

Strategies for Driving Mobile Data and Broadband Adoption

Chapter 5 Mobile Messaging – Strategy Case Studies

26 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

Mobile Messaging – Strategy Case Studies Case Studies

Telkomsel Indonesia About the Operator Telkomsel is t he l argest m obile net work operator i n I ndonesia with cl ose t o 50 per cent market share at end-2009. Rationale for Selecting the Operator The operator has launched several i nnovative services in the market that have spurred i ts data revenue, and in 2009 the MNO’s non-voice revenue was 29 percent of its total operating revenue. SMS has l ed t he growth of da ta services i n Indonesia, with T elkomsel subscribers ge nerating t he hi ghest SMS t raffic in t he country. T he figure bel ow compares the annual SMS traffic for the two leading MNOs in Indonesia.

Figure 12: SMS Traffic – Telkomsel and Excelcomindo (In Billion, 2007 – 2009)7

Source: Portio Research Ltd.

All oper ators i n Indonesia are t rying t o dif ferentiate their SMS o fferings w ith ch eap and attractive pr ice pl ans, and T elkomsel i s no ex ception. Ho wever, T elkomsel i s not onl y focussing on service pricing, but is also making efforts to increase the quality and appeal of its SMS o fferings; this i s done by ensuring regular SMS pl atform upgrades and launching innovative s ervices s uch a s SMS Me , Web 2 SMS, SMS G IFT, SM S Pro , SM S2.0 a nd Facebook SMS. Furthermore, with t he i ncreasing use of SMS, i t i s al so m aking efforts t o maintain network quality. Additionally, the MNO is promoting SMS by offering services that use SMS as the access platform.

7 Note: For Telkomsel, only chargeable SMS are shown in the Figure.

49.5

78.0

100.4

12.6 17.8

63.6

0

20

40

60

80

100

120

2007 2008 2009

SMS

Traf

fic

(In B

illio

n)

Year

Telkomsel Excelcomindo

With the increasing use of SMS, Telkomsel is also making efforts to maintain network quality.

Mobile Subscribers: 81.6 million (End-2009)

Market Share: 49.0 percent (End-2009)

Monthly ARPU: USD 4.8 (2009)

SMS Traffic: 26.9 billion (Q4 2009)

© 2010, Portio Research. All Rights Reserved 27

Strategies for Driving Mobile Data and Broadband Adoption The figure below highlights the quarterly growth in Telkomsel’s SMS traffic.

Figure 13: SMS Traffic – Telkomsel (In Billion, Q1 2009 – Q4 2009)8

Source: Portio Research Ltd.

In 2009, SMS r evenue constituted 74 per cent of Telkomsel’s d ata revenue. T he average price of an S MS has reduced ov er t he years, but the surge i n SMS t raffic has of fset t his decline, and this has enabled the operator to increase SMS revenue with each succeeding quarter of 2009. The figure below depicts the growth in Telkomsel’s SMS revenue in 2009.

Figure 14: SMS Revenue – Telkomsel (In USD Million, Q1 2009 – Q3 2009)

Source: Portio Research Ltd.

In 2009, T elkomsel’s S MS r evenue w itnessed a 23 per cent year-on-year growth. S MS revenue generated in Q4 2009 grew by 37 percent in comparison with Q1 2009 revenue.

8 Note: These are only chargeable SMS.

22.9

23.9

26.7 26.9

20

22

24

26

28

Q1 2009 Q2 2009 Q3 2009 Q4 2009

SMS

Traf

fic(In

Bill

ion)

Quarter

206.1

236.6

279.9 282.5

200

220

240

260

280

300

Q1 2009 Q2 2009 Q3 2009 Q4 2009

SMS

Rev

enue

(In U

SD M

illio

n)

Quarter

28 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

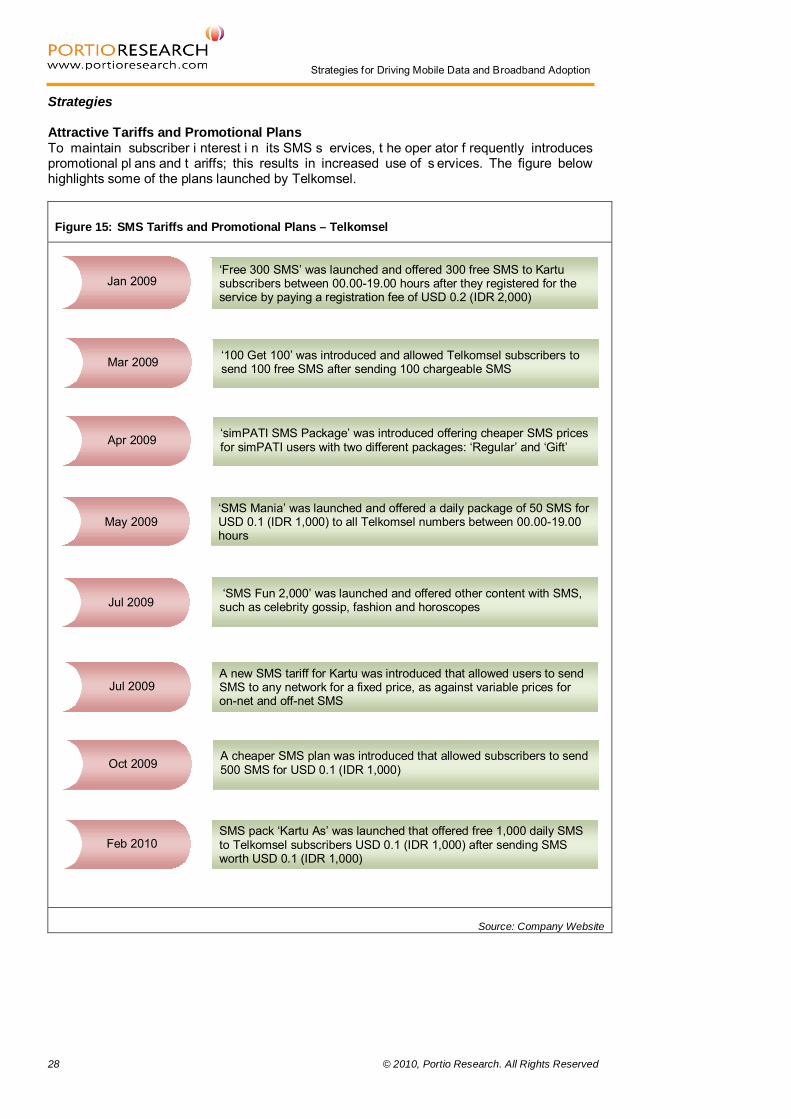

Strategies Attractive Tariffs and Promotional Plans To maintain subscriber i nterest i n its SMS s ervices, t he oper ator f requently introduces promotional pl ans and t ariffs; this results in increased use of s ervices. The figure below highlights some of the plans launched by Telkomsel.

Figure 15: SMS Tariffs and Promotional Plans – Telkomsel

Source: Company Website

‘SMS Mania’ was launched and offered a daily package of 50 SMS for USD 0.1 (IDR 1,000) to all Telkomsel numbers between 00.00-19.00 hours

May 2009

Jul 2009

‘SMS Fun 2,000’ was launched and offered other content with SMS, such as celebrity gossip, fashion and horoscopes

Jul 2009

A new SMS tariff for Kartu was introduced that allowed users to send SMS to any network for a fixed price, as against variable prices for on-net and off-net SMS

Apr 2009

‘simPATI SMS Package’ was introduced offering cheaper SMS prices for simPATI users with two different packages: ‘Regular’ and ‘Gift’

Jan 2009

‘Free 300 SMS’ was launched and offered 300 free SMS to Kartu subscribers between 00.00-19.00 hours after they registered for the service by paying a registration fee of USD 0.2 (IDR 2,000)

Mar 2009

‘100 Get 100’ was introduced and allowed Telkomsel subscribers to send 100 free SMS after sending 100 chargeable SMS

Oct 2009 A cheaper SMS plan was introduced that allowed subscribers to send

500 SMS for USD 0.1 (IDR 1,000)

Feb 2010

SMS pack ‘Kartu As’ was launched that offered free 1,000 daily SMS to Telkomsel subscribers USD 0.1 (IDR 1,000) after sending SMS worth USD 0.1 (IDR 1,000)

© 2010, Portio Research. All Rights Reserved 29

Strategies for Driving Mobile Data and Broadband Adoption Regular Upgrades of SMS Services and SMS Platform Telkomsel has transformed i ts SMS offerings f rom being a simple text-based service to an advanced service with features such as divert, auto reply, black list and white list. Some of their innovative SMS services are listed below:

• SMS Me • Web 2 SMS • SMS GIFT • SMS Pro • SMS2.0 • Facebook SMS

These efforts are aimed at making Telkomsel’s SMS services more personalised and attractive. The operator is not only upgrading its SMS services regularly, but is also of fering services through t he m ost adv anced m essaging platforms. For example, i n Ju ne 2009, Telkomsel upgraded its SMS platform with Acision’s Text Suite, to enable users to enjoy additional features su ch a s bl ocking uns olicited S MS (or S MS s pam), aut omatic replies, message forwarding and automatic copy messages. Improving Network Quality and Capacity With i ncreasing s ubscriber numbers and d ata t raffic, m obile net works worldwide require frequent upgrades. Without such upgrades, networks will succumb to the increasing strain, affecting the quality of services. Keeping this in mind, Telkomsel has invested hugely in network expansion. In Q1 2009, it increased its base transceiver station (BTS) number by 28 percent and overall network capacity by 39 percent. In 2008, the operator added 6,014 new BTS that allowed it to carry 30 percent higher SMS traffic on the day of Lebaran (a religious festival), compared with its capacity in 2007.9

9 Source: Company Reports

Using SMS as a Platform for Other Services Telkomsel has introduced several services that use SMS as the access platform. With the increasing upt ake o f t hese s ervices, SMS us e i s gai ning new hei ghts i n t he co untry. Telkomsel is offering mobile banking services through three platforms—SMS, single banking and IVR (Interactive Voice Response)—with SMS being the most popular platform used by subscribers. In 2008, Telkomsel started its mobile advertisement services. This allows content providers to push and adv ertise their products through SMS, along with other content such as news and information.

Telkomsel is not only upgrading its SMS services regularly, but is also offering services through the most advanced messaging platforms.

30 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

The t able below highlights t he f actors which enabl ed the operator to generate high SMS traffic.

Table 2: Success Factors – Telkomsel Indonesia

Factor Strategy

Attractive Tariffs and Promotional Plans

Telkomsel regularly introduces attractive SMS plans that offer cheap or free SMS. Different plans target subscribers with different use needs.

Regular Service and Platform Upgrades

Telkomsel has introduced several innovative SMS-based services, such as SMS Facebook. SMS Facebook is gaining rapid popularity among users and is driving SMS use further. Apart from interesting services, Telkomsel has increased the appeal of its SMS offerings with the introduction of features such as divert, auto reply, black list, white list, etc.

Improving Network Quality and Capacity

Telkomsel is focusing on network quality in order to continue delivering high quality services to its subscribers despite increased SMS traffic. It is also investing to strengthen network capacity.

SMS as a Platform for Other Services

Telkomsel is providing additional services that use SMS as an access platform, and these services are witnessing increasing demand in the local market.

Source: Portio Research Ltd.

© 2010, Portio Research. All Rights Reserved 31

Strategies for Driving Mobile Data and Broadband Adoption China Mobile About the Operator China Mobile is the largest MNO worldwide in terms of subscriber base, with 522.3 million subscribers at end-2009; the subscriber base grew nearly 14.2 percent during 2009. Rationale for Selecting the Operator Messaging services, such as SMS, MMS, mobile e-mail and mobile IM, have been the key focus of operators to generate data revenues. China Mobile’s continuous efforts to promote messaging se rvices, es pecially MMS, r equire a s pecial mention. M MS has per formed exceptionally well in t he Chinese m arket, compared with i ts per formance in other markets where it has been a distant second to SMS. While many other markets are struggling to increase MMS uptake, China Mobile’s MMS user base has shown a double-digit growth rate during 2007–2009. During 2007–2009, the number o f China M obile’s MMS users increased at a CA GR of near ly 27.5 per cent, with year-on-year growth of MMS users standing at 15.1 percent in 2009.

Figure 16: MMS Users – China Mobile (In Million, End 2007 – End 2009)

Source: Portio Research Ltd.

90.8

128.2

147.5

0

20

40

60

80

100

120

140

160

2007 2008 2009

MM

S U

sers

(In M

illio

n)

Year

While many other markets are struggling to increase MMS uptake, China Mobile’s MMS user base has shown a double-digit growth rate during 2007–2009.

Mobile Subscribers: 522.3 million (End-2009)

Market Share: 72.4 percent (End-2009)

Monthly ARPU: USD 11.0 (Q4 2009)

MMS Users: 147.5 million (End-2009)

32 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

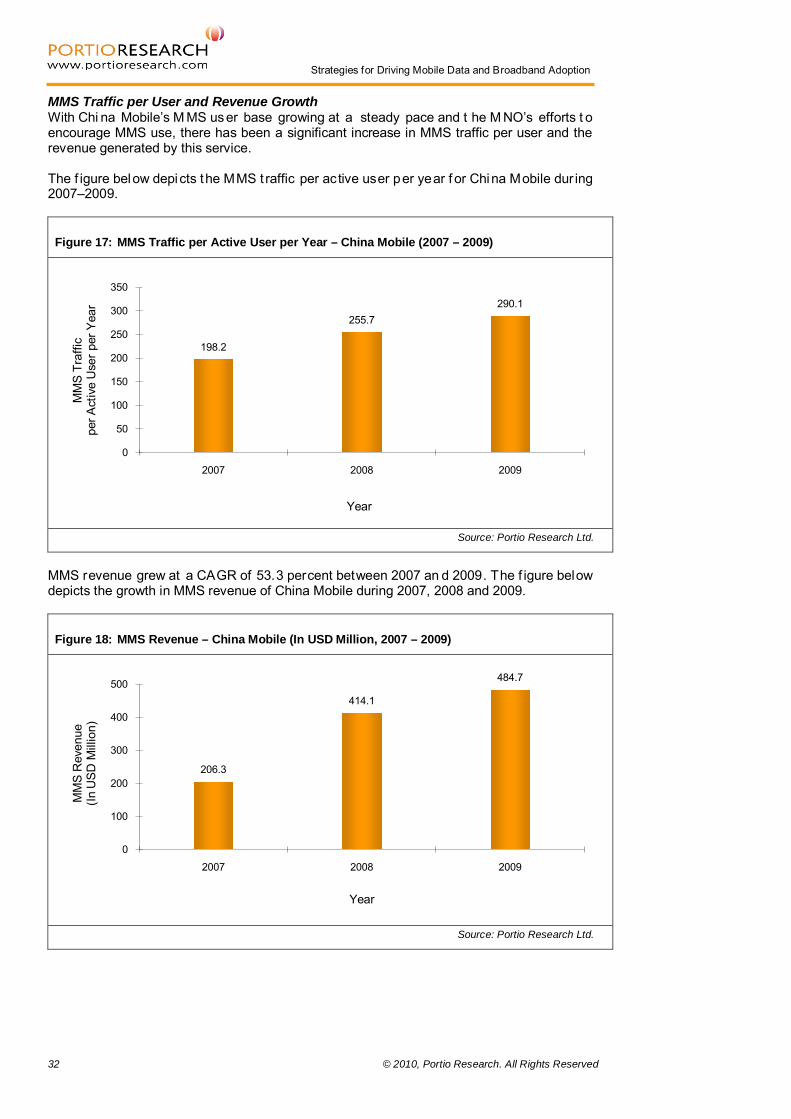

MMS Traffic per User and Revenue Growth With Chi na Mobile’s M MS user base growing at a steady pace and t he M NO’s efforts t o encourage MMS use, there has been a significant increase in MMS traffic per user and the revenue generated by this service. The f igure below depicts the MMS t raffic per active user per year f or China Mobile dur ing 2007–2009.

Figure 17: MMS Traffic per Active User per Year – China Mobile (2007 – 2009)

Source: Portio Research Ltd.

MMS revenue grew at a CAGR of 53.3 percent between 2007 an d 2009. The f igure below depicts the growth in MMS revenue of China Mobile during 2007, 2008 and 2009.

Figure 18: MMS Revenue – China Mobile (In USD Million, 2007 – 2009)

Source: Portio Research Ltd.

198.2

255.7290.1

0

50

100

150

200

250

300

350

2007 2008 2009

MM

S Tr

affic

pe

r Act

ive

Use

r per

Yea

r

Year

206.3

414.1

484.7

0

100

200

300

400

500

2007 2008 2009

MM

S R

even

ue(In

USD

Mill

ion)

Year

© 2010, Portio Research. All Rights Reserved 33

Strategies for Driving Mobile Data and Broadband Adoption Strategies Triggering the Uptake of MMS Services • Challenge: The ear ly uptake o f M MS by subscribers i s co nstrained by the fact t hat

creating and edi ting m ultimedia co ntent i s far more complicated t han w riting t ext messages. This hampers growth in P2P MMS traffic.

• China Mobile’s Strategy: China M obile s timulated MMS adopt ion by pushing A 2P

MMS and ot her MMS-based innovative services. A2P MMS-based services—M-News, entertainment and gr eeting M MS a vailable on the Monternet Web portal mobile—provide addi tional impetus to tap the potential of MMS. Dur ing 2007, A2P MMS t raffic accounted for more than 70 per cent of China Mobile’s total MMS traffic; the remaining percentage was P2P MMS traffic.10

The use of A2P MMS in turns increase P2P MMS through the message forward facility. Subscribers simply forward the MMS, without needing to be co ncerned about creating the MMS, as it is generated by the application. Once subscribers are familiar with MMS services, us ers ca n cr eate t heir own M MS co ntent, and t his in t urn i ncreases t he popularity of the service among them.

Innovative Offerings

MMS traffic is still dominated by A2P MMS, with the continued success of the M-News and Monternet services.

• M-News: This i s a m obile newspaper service that allows users t o receive information including breaking news alerts and weather reports through MMS (on their MMS-capable hands ets). Chi na M obile pr ovides the M-News se rvice in co llaboration w ith media organisations, including China Daily (a national English newspaper) and other local news sources. The news alert MMS includes ten pages of headline news, weather information and photos. The alerts are provided twice a day at a monthly charge of RMB 5 (USD 0.7), and the service is exempt from data charges. Salient Features: High cu stomisability allowing t he provision o f co ntent i n a nu mber o f ca tegories

including news al erts and information in areas such as m usic, movies, lif e, sports and finance

Option to forward M-News MMS to other users Opportunity for subscribers to share their opinions with editors and other readers Increased revenue opportunity for MNOs without the need to own any content Easy to subscribe/unsubscribe to the service as subscribers merely need to send a

text message for initiating/discontinuing the subscription Impact: The M-News service was received well by subscribers, and it became a major factor in the growth of MMS traffic in China. It was nominated as a star service for the operator i n the year of its launch (2006), and the MMS t raffic per month in China has increased by more than seven times between 2006 and 2009. The paying subscriber base for the M-News service during 2006–2009 is depicted in the figure below. The number of M-News subscribers increased at a CAGR of nearly 107.5 percent between 2006 and 2009.

10 Source: http://wwwen.zte.com.cn/endata/magazine/ztetechnologies/2007year/no4/articles/200704/t20070423_161773.html

The early uptake of MMS by subscribers is constrained by the fact that creating and editing multimedia content is far more complicated than writing text messages.

34 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

Figure 19: M-News Paying Subscribers – China Mobile (In Million, End 2006 – End 2009)

Source: Portio Research Ltd.

• Monternet: Monternet i s a s et of data of ferings based on the mobile Internet platform

provided by China Mobile. The service allows subscribers to use different content categories on the Monternet Web portal; subscribers can use their handsets (feature phones or smartphones) or ‘Go with E’ cards with their laptops to access the Monternet Web portal for sending and receiving MMS.

Leveraging Events for MMS Promotion • Green Box Environmental Protection Plan—517 Special Event: In May 2007, China

Mobile celebrated the World Telecommunication and Information Society Day, and invited i ts s ubscribers t o participate i n t he G reen O lympics. T he e vent enco uraged subscribers to throw their old phones into green boxes. The initiative attracted many celebrities, and the mobile operator organised an MMS photo shooting event – ‘Good Shape f or t he O lympics’ – to spread t he m essage of it s co mmitment t owards the environment.

• Olympics 2008: China Mobile released an MMS containing the ‘2008 Olympics Mascot’ on the Monternet Web portal, and the company allowed its subscribers to download and send the MMS through their handsets and laptops. The promotion of the Olympics was the first of its kind in China, and was successful in pushing MMS services further into the market.

5.5

23.6

41.5

49.1

0

10

20

30

40

50

2006 2007 2008 2009

M-N

ews

Payi

ng S

ubsc

riber

s(In

Mill

ion)

Year

© 2010, Portio Research. All Rights Reserved 35

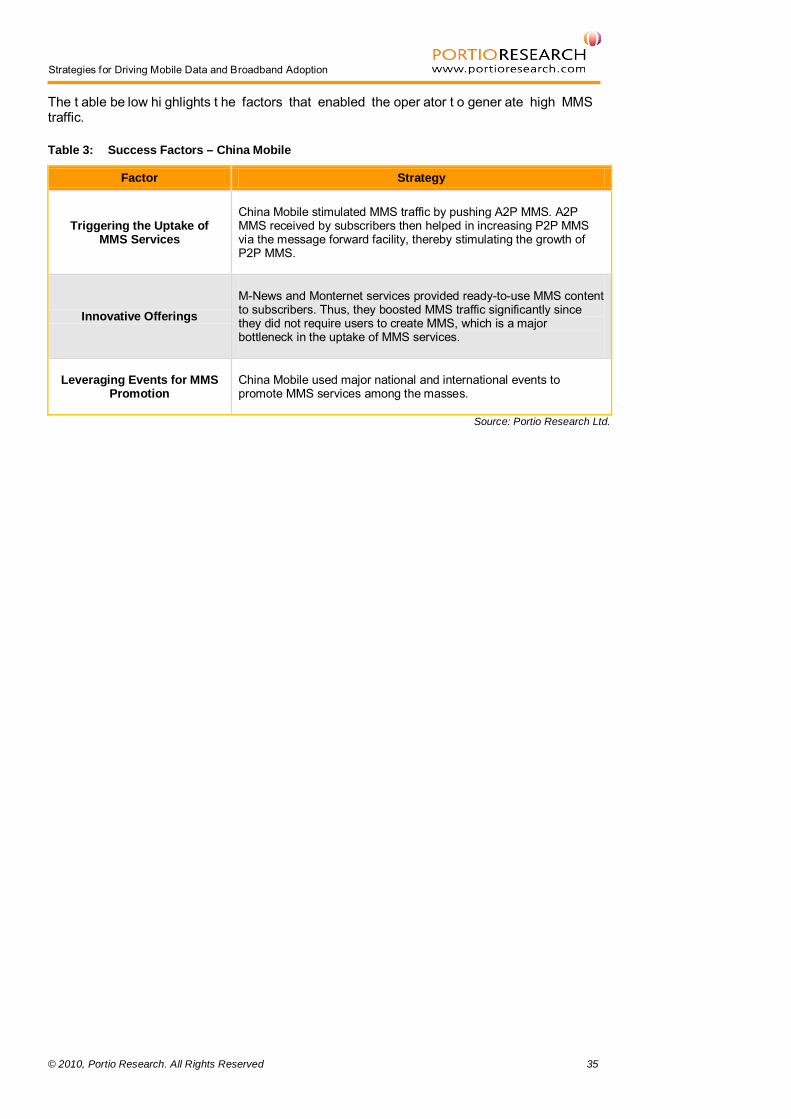

Strategies for Driving Mobile Data and Broadband Adoption The t able be low hi ghlights t he factors that enabled the oper ator t o gener ate high MMS traffic.

Table 3: Success Factors – China Mobile

Factor Strategy

Triggering the Uptake of MMS Services

China Mobile stimulated MMS traffic by pushing A2P MMS. A2P MMS received by subscribers then helped in increasing P2P MMS via the message forward facility, thereby stimulating the growth of P2P MMS.

Innovative Offerings

M-News and Monternet services provided ready-to-use MMS content to subscribers. Thus, they boosted MMS traffic significantly since they did not require users to create MMS, which is a major bottleneck in the uptake of MMS services.

Leveraging Events for MMS Promotion

China Mobile used major national and international events to promote MMS services among the masses.

Source: Portio Research Ltd.

36 © 2010, Portio Research. All Rights Reserved

Strategies for Driving Mobile Data and Broadband Adoption

SoftBank Japan About the Operator SoftBank is the third largest mobile operator in Japan, but the first operator in Japan to migrate its entire subscriber base to a 3G network. Rationale for Selecting SoftBank SoftBank has introduced a pack combining Web access and e-mail access. Considering the high I nternet us e by Japanese su bscribers and by combining e -mail wi th Web ac cess, SoftBank has paved the way for increased e-mail use by its subscribers. Subscribers using this pack can send and r eceive e-mails on the network for free, and to other networks at a minimal cost. The operator has introduced services that increase the presence and familiarity of mobile e-mail among its subscribers. In January 2008, it launched S! Information Channel , a s ervice that deliv ers i nformation t o s ubscribers via e -mail. T he s ervice had near ly 2 million registered users as of April 2009, and continues to grow in popularity and add subscribers and applications at a steady pace. The figure below highlights the increasing number of applications on the S! Information Channel.

SoftBank has introduced services that increase the presence and familiarity of mobile e-mail among its subscribers.

Figure 20: Number of S! Information Channel Applications – SoftBank (January 2010 – April 2010)

Source: Portio Research Ltd.

21,08621,171

21,587 21,618

20,800

20,900

21,000

21,100

21,200

21,300

21,400

21,500

21,600

21,700

Jan-10 Feb-10 Mar-10 Apr-10

Num

ber o

f App

licat

ions

Month

Mobile Subscribers: 21.7 million (End-2009)

Market Share: 19.4 percent (End-2009)

Monthly ARPU: 21.5 USD (Q4 2009)

3G Subscribers as a Percentage of Customer Base: 96.4 percent (End-2009)

© 2010, Portio Research. All Rights Reserved 37

Strategies for Driving Mobile Data and Broadband Adoption With the highest 3G penetration among subscribers, SoftBank has a solid f oundation for increasing i ts dat a ARPU. Moreover, after the decommissioning of its 2G net works by 31 March 2010, S oftBank is t he only network with 100 per cent 3G s ubscription. The figure below highlights the 3G penetration of SoftBank and its competitors in 2009:

Figure 21: 3G Subscribers as a Percentage of Total Subscriber Base – Japan (In Percent, Q2 2009 – Q4 2009)11

Source: Portio Research Ltd.

SoftBank introduced e -mail facilities for i ts s ubscribers t hrough a service ca lled S ! Mail. Though S! Mail was marketed and perceived as an MMS service, it offered traditional push e-mail s ervices to it s s ubscribers. S ! M ail s ubscribers ca n enclose pi ctures, voice c lips, videos, etc., while sending e-mails, and the service permits users to send e-mails only by keying i n the r ecipient’s m obile number. A ny subscriber using the S ! B asic data p lan w ill have access to e-mail, along with 3G and other Internet services including e-mail. SoftBank, after the change in management from Vodafone K.K., launched 3G services for the third time in Japan in 2005. This move garnered more success than the earlier two 3G service launches by Vodafone K .K. ( before acq uisition by SoftBank). Though late i n introducing 3G , mobile I nternet and e -mail s ervices, S oftBank has s een a significant increase in the adoption of its new services. The adoption of mobile e-mail by SoftBank subscribers has been steadily increasing; one of the m ain factors i s t he s ales of i Phones. S oftBank, pr esently the onl y operator t o o ffer iPhones in Ja pan, ex perienced a steady increase in i Phone s ales and dat a services including mobile e-mail. The following ch art depi cts t he i ncrease i n I nternet ado ption by SoftBank subscribers.