swfs: inward vs. outward investment...

TRANSCRIPT

SWFs: Inward vs. Outward Investment Mandates Conditions for Success

Eliot Kalter President of EM Strategies

Co-Head, SovereigNET: Fletcher Network for Sovereign Wealth and Global Capital [email protected]

October 7, 2014

Presentation Overview

2

•Sovereign Wealth Funds as Global Investors Growing relevance among global investor SWFs are heterogeneous with wide range of purposes/mandates

•Sovereign Wealth Funds Purpose and Asset Allocation SWF mandates greatly influence asset allocation strategies Most SWFs are able to take advantage of the liquidity premium stemming from long liability structures

•SWF Direct Investments by Region and Sector Outward investments concentrated on real estate in developed economies Inward investment less than 30% of total direct investment; highly concentrated; greater focus on infrastructure investment

•Outward vs. Inward Investment Benefits of outward compared with benefits of inward investment Dangers of inward investment and policies needed to enable long-term success

Scale of SWF Among Global Institutional Investors Source of SWF Funding

SWF as Global Investors

35%

28%

27%

5% 3% 2%

AUM of Global Investors Proportion of Total ($120 trillion)

Pension funds

Insurance funds

Mutual funds

Sovereign wealthfunds

Private equity

Evolution of SWF

1. SWFs proportionately small on global scale 2. Predominantly established since 1980,

overwhelmingly emerging economies to sterilize large capital inflows

3. Rapid growth with over 60% of SWF established since 2000

4. Growing importance in global economy with long-term investment horizon allowing significant anti-cyclical investments

SWF Specification by Purpose

M ajor Purposes of SWF

Country Fund Purpose Kazakhstan Kaz Natl Fund Stabilization Algeria Rev Reg Fund Stabilization Iran Oil Stab Fund Stabilization Singapore Temasek Savings US-NM NM St Inv Council Savings Brazil Sov Fund Savings UAE ADIA Savings Kuwait KIA Savings Qatar QIA Savings UAE ICD Savings Libya LIA Savings UAE IPIC Savings US AK Per Fund Savings Brunei Brunei Inv Agency Savings US Texas Per School Savings Canada AB Heritage Fund Savings Oman Gen Res Fund Savings China SAFE Reserve Investment China CIC Reserve Investment China HKMA Reserve Investment Singapore GIC Reserve Investment Korea KIC Reserve Investment Saudi Arabia SAMA Reserve Investment China NSSF Pension Reserve Australia AFF Pension Reserve Ireland NPRF Pension Reserve New Zealand NZ Super Fund Pension Reserve Russia NWF Pension Reserve Norway GPG-G Stab/Savings/Pension Azerbaijan State Oil Fund Stab/Savings East Timor Tiimor-Leste Stab/Savings

Chile Soc & Eco Stab Fund Stab/Pension Malaysia Khazanah Sov Dev Bahrain Mumtalakat Sov Dev UAE Mubadala Sov Dev France Strg Inv Fund National Strategic

SWF Size and Scale as an Investor Class

1. SWFs have over $6T in asset under management 2. Asset concentration is high with the top 10 funds

holding 79% of total SWF AUM and the top 20 funds 93%

3. Among the top 10 funds 7 are from China, Singapore, Saudi Arabia and the UAE

4. 18 funds have assets in excess of $50B 5. All SWFs (except stabilization) have long-term

investment horizons

1. Stabilization - fiscal stabilization through the investment of excess budgetary reserves

2. Savings – wealth preservation, expansion, and inter-generational transfer

3. Reserve Investment – excess reserve management, beyond that required for stabilization or for direct monetary policy support

4. Pension Reserve – national pension reserve management

5. Development – strategic asset management, including privatization

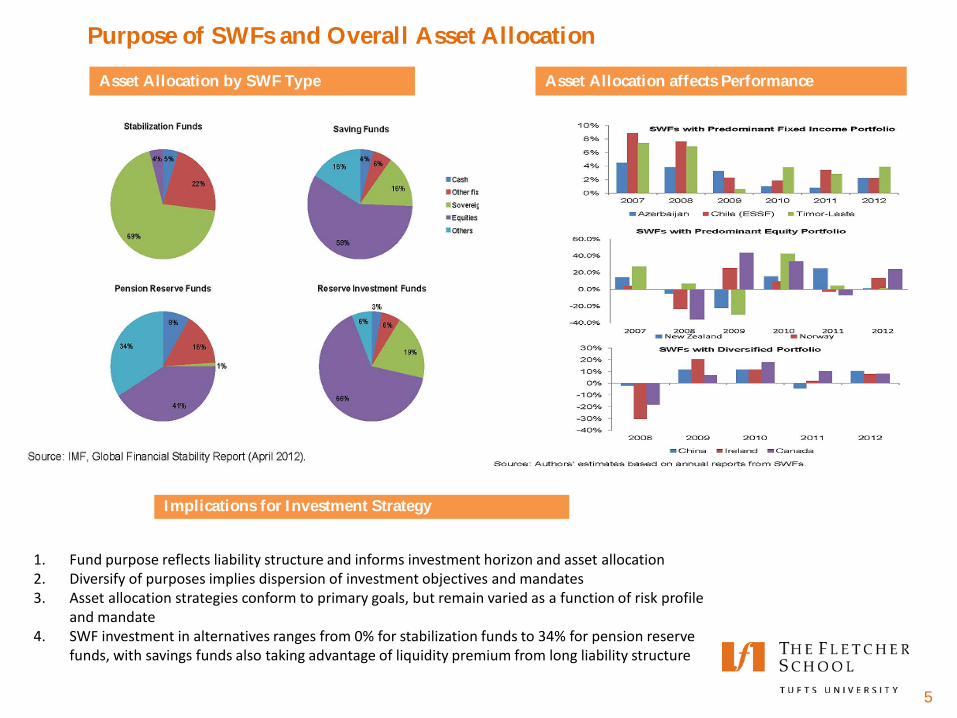

Purpose of SWFs and Overall Asset Allocation

5

Asset Allocation by SWF Type Asset Allocation affects Performance

1. Fund purpose reflects liability structure and informs investment horizon and asset allocation 2. Diversify of purposes implies dispersion of investment objectives and mandates 3. Asset allocation strategies conform to primary goals, but remain varied as a function of risk profile

and mandate 4. SWF investment in alternatives ranges from 0% for stabilization funds to 34% for pension reserve

funds, with savings funds also taking advantage of liquidity premium from long liability structure

Implications for Investment Strategy

SWF Direct Investments by Region and Sector in 2013

6

The Vast M ajority of Direct Investment is to Developed M arkets with a Focus on Real Estate Investment to Developing Countries is Concentrated in Infrastructure and Commodities

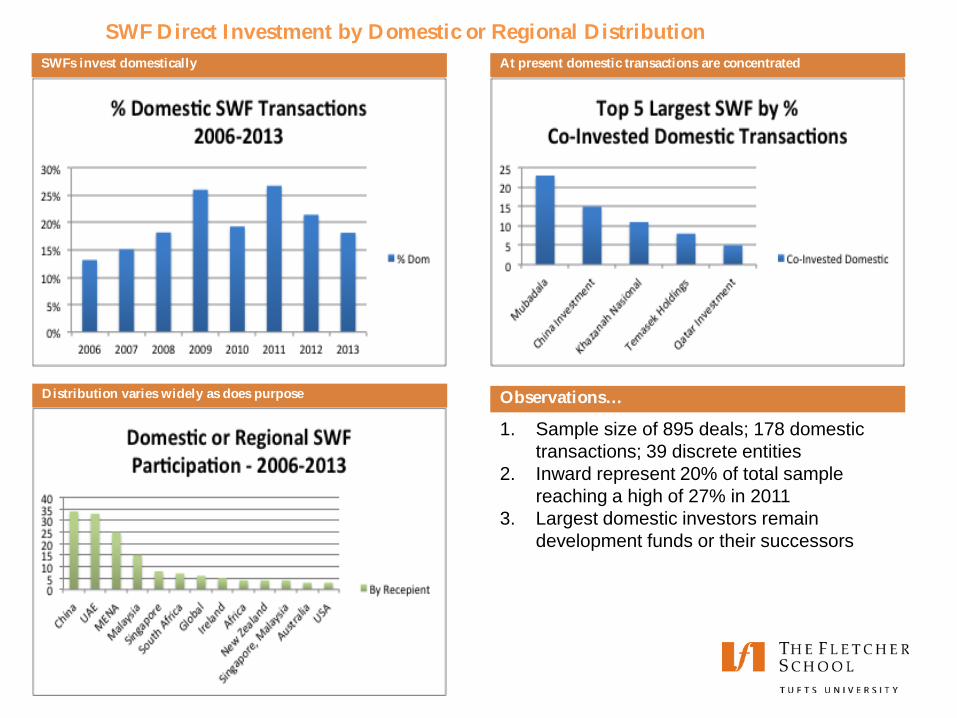

SWFs invest domestically At present domestic transactions are concentrated

Observations… Distribution varies widely as does purpose

1. Sample size of 895 deals; 178 domestic transactions; 39 discrete entities

2. Inward represent 20% of total sample reaching a high of 27% in 2011

3. Largest domestic investors remain development funds or their successors

SWF Direct Investment by Domestic or Regional Distribution

Benefits of SWF Outbound Investment

8

• SWF mandates: Stabilization, inter-generational wealth preservation, pension and reserve investment management

Replace depleting natural resources with alternative sources of export proceeds Investment diversification of Sovereign reserves with higher risk-adjusted returns

• Investing abroad helps avoid Dutch Disease Capital inflows from resource sector can result in real appreciation of the country’s exchange

rate, reducing the cost of imports and reducing competitiveness of non-resource economy, such as manufacturing and agricultural

Uneven or distorted sectoral development of local economy with loss of employment and sectoral diversification

Capture and manage accumulation of assets to reintegrate them into the domestic economy based on absorptive capacity

• Advance domestic institution building Serving as a bridge between global markets their local markets, transferring international

investment, capital market expertise and governance structure to build domestic capacity

M ost SWFs have M andates that Require Investment Abroad

The Benefits of Inward Investment

9

Sovereign development/investment funds: • Complements direct domestic investments through the state budget allocation process with

investment in strategic sectors of the domestic economy

• Oversee the management of state assets (including privatization) Inward investment has been concentrated in a handful of countries (China, UAE, Malaysia Singapore

and South Africa), mainly through investment vehicle to oversee management of state resources

• Catalyze co-investment by foreign investors who might otherwise be concerned about issues of governance and political risk

• Promote the development of domestic capital markets by enhancing the governance of pre-IPO companies, thereby improving the overall investment climate

• Facilitate knowledge transfer, capacity building, enhanced project governance

External Investment M andates can be in Conflict with Countries’ Development Needs

Dangers of Inward Investment

10

• Domestic investments driven by non-commercial, political agenda Domestic projects can conflict with budgetary investment agenda, bypass the budget process, and

promote a higher likelihood of politicizing the investment process The majority of the SWFs started since 2000 (excluding the developed economies) have Transparency

International scores of less than 5 out of 10 (54% of funds had TI scores of less than 3 and 79% had TI scores less than 5)

Studies show that SWFs with greater involvement of political leaders in fund management have lower long-term investment returns

• Danger of pro-cyclical investment, which can contribute to domestic inflation and asset price

appreciation

• Concentration of domestic investment can undermine fiscal and currency stabilization benefits of SWF structure

Advance, rather than lessen likelihood of Dutch disease Leading to a misallocations of scarce investment capital Investment beyond the absorptive capacity of the economy

Dangers are Significant and can Outweigh Benefits if not Addressed

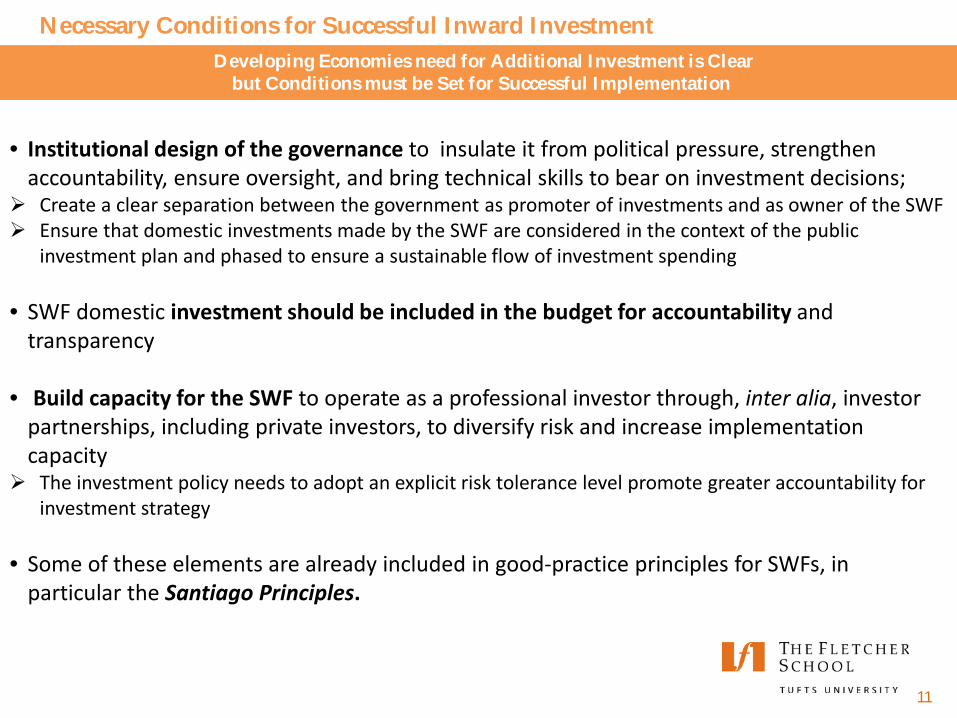

11

• Institutional design of the governance to insulate it from political pressure, strengthen accountability, ensure oversight, and bring technical skills to bear on investment decisions; Create a clear separation between the government as promoter of investments and as owner of the SWF Ensure that domestic investments made by the SWF are considered in the context of the public

investment plan and phased to ensure a sustainable flow of investment spending

• SWF domestic investment should be included in the budget for accountability and transparency

• Build capacity for the SWF to operate as a professional investor through, inter alia, investor partnerships, including private investors, to diversify risk and increase implementation capacity The investment policy needs to adopt an explicit risk tolerance level promote greater accountability for

investment strategy

• Some of these elements are already included in good-practice principles for SWFs, in particular the Santiago Principles.

Necessary Conditions for Successful Inward Investment Developing Economies need for Additional Investment is Clear

but Conditions must be Set for Successful Implementation

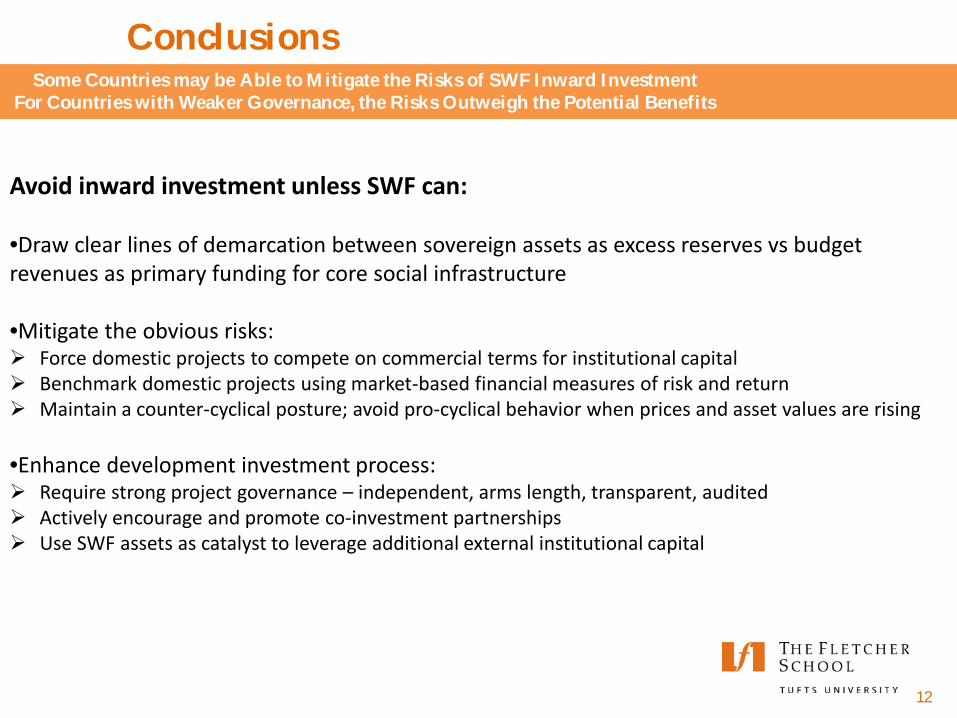

Conclusions

12

Some Countries may be Able to M itigate the Risks of SWF Inward Investment For Countries with Weaker Governance, the Risks Outweigh the Potential Benefits

Avoid inward investment unless SWF can:

•Draw clear lines of demarcation between sovereign assets as excess reserves vs budget revenues as primary funding for core social infrastructure

•Mitigate the obvious risks: Force domestic projects to compete on commercial terms for institutional capital Benchmark domestic projects using market-based financial measures of risk and return Maintain a counter-cyclical posture; avoid pro-cyclical behavior when prices and asset values are rising

•Enhance development investment process: Require strong project governance – independent, arms length, transparent, audited Actively encourage and promote co-investment partnerships Use SWF assets as catalyst to leverage additional external institutional capital