t he mot and v enture b usiness prof. takao ito, doctor of economics, ph.d. of engineering, graduate...

TRANSCRIPT

THE MOT AND VENTURE BUSINESS

Prof. Takao Ito, Doctor of Economics, PH.D. of Engineering, Graduate School of Engineering, Hiroshima University

Thursday, October 16, 2014

TOPIC 8 PORTFOLIO MANAGEMENT

TOPIC 8 CAPM BASICS The ROI A performance measure used to

evaluate the efficiency of an investment or to compare the efficiency of a number of different investments.

The P/E Ratio of a stock (price-to-earnings ratio, "P/E", "PER", "earnings multiple," or simply "multiple")

It is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share.

Basic formula of the ratio of a stock return

0

01

P

DPPR

P0……Initial priceP1……trading priceD…….Dividend yield

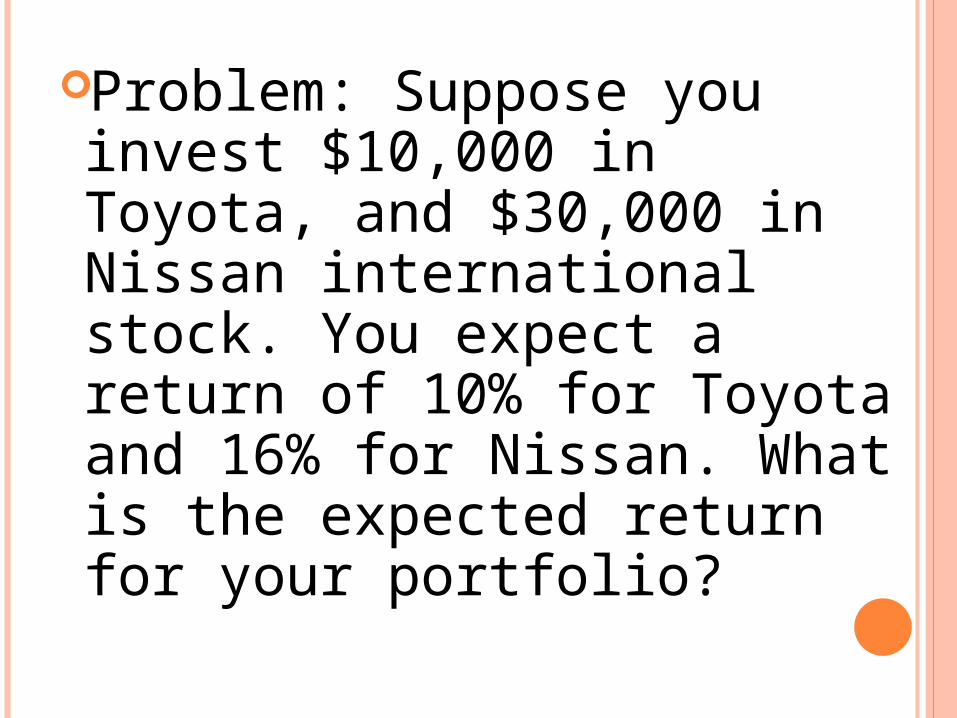

Problem: Suppose you invest $10,000 in Toyota, and $30,000 in Nissan international stock. You expect a return of 10% for Toyota and 16% for Nissan. What is the expected return for your portfolio?

Solution: You have $40,000 invested in total, so your portfolio weight are 10,000/40,000=25% in Toyota and 30,000/40,000=75% in Nissan. Therefore, the expected return on your portfolio is

%5.1416.0%7510.0%25

][][)(

NNTTP RExRExRE

In the case of Stock A

Events Probability Ratio of Return

BetterNormalWorse

0.250.5

0.25

20%12%

4%

Expectation value of stock A

l

kkiki PRRE

1

)(

Expectation value of stock AExpectation value of stock A

l

kkiiki PRERR

1

2))(()(

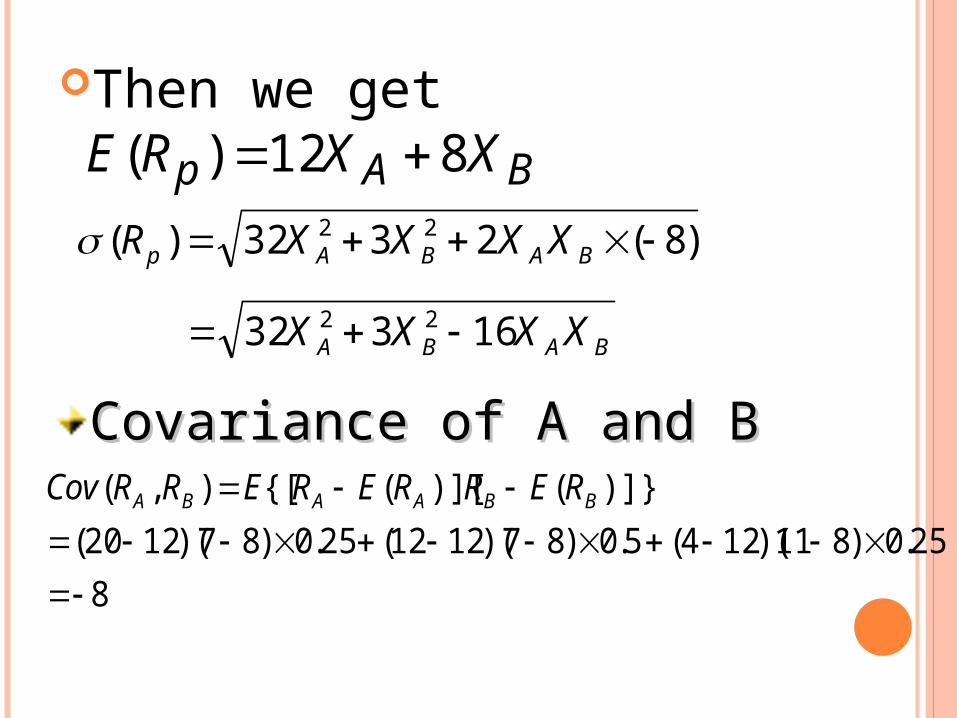

Then we get

%12425.0125.02025.0)( ARE

%32

)124(25.0)1212(5.0)1220(25.0)( 222

AR

Assume that stock B

Event Probability Ratio of Return

BetterNormalWorse

0.250.5

0.25

7%7%

11%

%81125.075.0725.0)( BRE

%3

)811(25.0)87(5.0)87(25.0)( 222

BR

In the case of two stocks: Stock A and stock B, the expectation value and risk

;1 BA XX

);()()( BBAAi REXREXRE

),(2)()(

)(

2222BABABBAA

i

RRCovXXRXRX

R

Then we getBAp XXRE 812)(

BABA

BABAp

XXXX

XXXXR

16332

)8(2332)(

22

22

Covariance of A and BCovariance of A and B

8

25.0)811)(124(5.0)87)(1212(25.0)87)(1220(

)]}()][({[),(

BBAABA RERRERERRCov

Correlation ratio of A and B

816.0332

8

)()(

),(

BA

BAAB RR

RRCov

Risk of stocks A and BRisk of stocks A and B

32251

)1(16)1(332

16332)(

2

22

22

AA

AAAA

BABAp

XX

XXXX

XXXXR

Best answer (differentiate)

%5.78;215.0102/22 BA XX

0)(

A

p

dX

Rd

032251

22102

2

1)(

2

AA

A

A

p

XX

X

dX

Rd

Then we getThen we get

M

E(Rp)

RF

σ(Rp)

G

H

)()1()()1()()( SFSFP REXRXREXRXERE

)()1(

)0)(()()1(

)()()1(2)()1()()(

22

2222

S

FS

SFFSSFP

RX

RRX

RRXXRXRXR

Then we getThen we get

)()(

)()( p

M

FMFP R

R

RRERRE

RFM……capital market line

STOCK J AND STOCK MARKET

)()1()()( MjjjP REXREXRE

),()1(2)()1()()( 2222MjjjMjjjP RRCovXXRXRXR

M

E(Rp)

RF

σ(Rp)

G

H

),()(

)()(

2 MjM

FMFj RRCov

R

RRERRE

)(

),(2

M

Mj

R

RRCov

])([)( FMjFj RRERRE

Let

We can easy to get

RF

COV(Rj,RM)

E(R j )

),()(

)()(

2 MkM

FMFk RRCov

R

RRERRE

])([)( FMkFj RRERRE

RF

β k

E(R k )

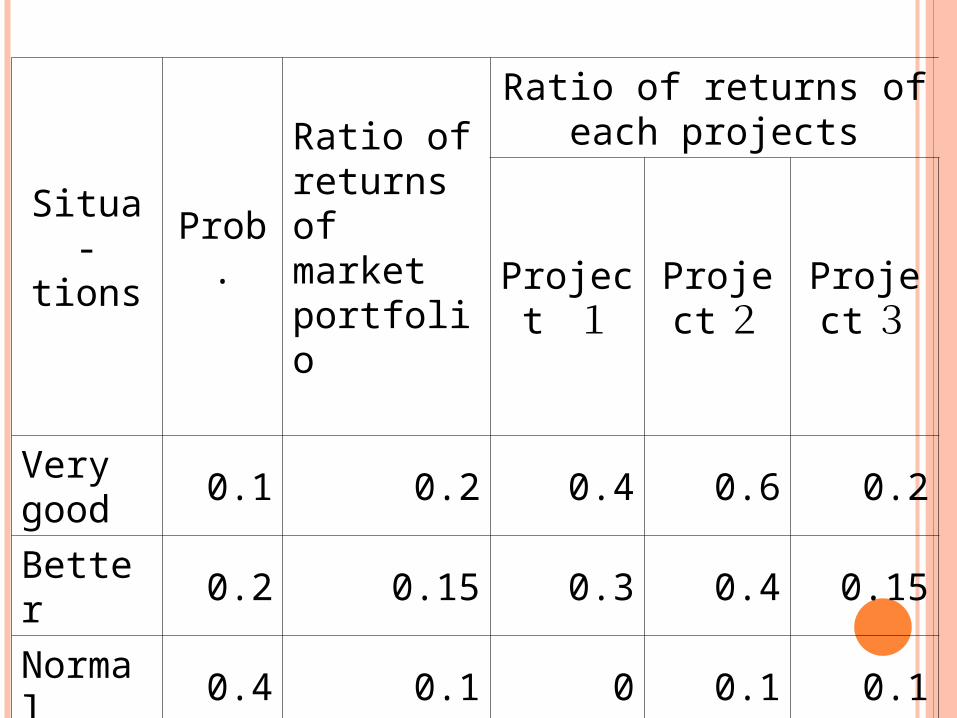

Situa-tions

Prob.

Ratio of returns of market portfolio

Ratio of returns of each projects

Project 1

Project 2

Project3

Very good

0.1 0.2 0.4 0.6 0.2

Better 0.2 0.15 0.3 0.4 0.15

Normal

0.4 0.1 0 0.1 0.1

Worse 0.2 0 -0.1 -0.1 0

Worst 0.1 -0.1 -0.2 -0.4 -0.05

E(RM)=0.1×0.2 + 0.2×0.15 + 0.4×0.1 + 0.2×0 + 0.1× ( -0.1 ) = 0.08

σ 2( RM )= 0.1×(0.2-0.08) 2+ 0.2×(0.15-0.08) 2 + 0.4×(0.1-0.08) 2+ 0.2×(0-0.08) 2 + 0.1×(-0.1-0.08) 2 =0.0071

① ② ③ ④ ⑤ ⑥

Situations Prob.:PRate of

returns:RK

P*R k

[R k- E(Rk) ] [RM - E(R

M) ] ②×⑤

Project 1

1 0.1 0.4 0.04 0.0408 0.00408

2 0.2 0.3 0.06 0.0168 0.00336

3 0.4 0 0 -0.0012 -0.00048

4 0.2 -0.1 -0.02 0.0128 0.00256

5 0.1 -0.2 -0.02 0.0468 0.00468

E(R1)= 0.06 COV(R1,RM)= 0.0142

Project 2

1 0.1 0.6 0.06 0.0648 0.00648

2 0.2 0.4 0.08 0.0238 0.00476

3 0.4 0.1 0.04 0.0008 0.00032

4 0.2 -0.1 -0.02 0.0128 0.00256

5 0.1 -0.4 -0.04 0.0828 0.00828

E(R2)= 0.12 COV(R2,RM)= 0.0224

Project 3

1 0.1 0.2 0.02 0.0168 0.00168

2 0.2 0.15 0.03 0.0063 0.00126

3 0.4 0.1 0.04 0.0008 0.00032

4 0.2 0 0 0.0048 0.00096

5 0.1 -0.05 -0.005 0.0198 0.00198

E(R3)= 0.085 COV(R3,RM)= 0.0062

20071.0

0142.0

)(

),(2

11

M

M

R

RRCov

15.30071.0

0224.0

)(

),(2

22

M

M

R

RRCov

87.00071.0

0062.0

)(

),(2

33

M

M

R

RRCov

03.005.008.0])([ FM RRE

11.0

)05.008.0(205.0])([)( 11

FMF RRERRE

1445.0

)05.008.0(15.305.0])([)( 22

FMF RRERRE

0761.0

)05.008.0(87.005.0])([)( 33

FMF RRERRE

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

1 2 3 4

THANK YOU FOR YOUR ATTENTION!