tax accounting method considerations in m&a … · carol specializes in tax accounting for...

TRANSCRIPT

Tax accounting method considerations in M&A transactionsCarol Conjura

John Geracimos

TEI Houston Chapter Tax School

May 10, 2018

2© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Notices

The following information is not intended to be “written advice concerning one or more

Federal tax matters” subject to the requirements of section 10.37(a)(2) of Treasury

Department Circular 230.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

3© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Background

Prior to joining KPMG, Carol was Assistant to the Associate Chief Counsel (Domestic), with the Internal

Revenue Service where she had a principal technical and policy role in the development of IRS

regulations and other guidance on accounting method issues, including the definition of a method of

accounting, procedures for changing methods, inventories, the uniform capitalization rules, long-term

contracts, and the economic performance rules

Professional and industry experience

Carol is a Partner in KPMG’s Washington National Tax Office, in the Income Tax and Accounting Group,

and represents clients on tax planning and compliance matters involving accounting methods and

periods. She also represents clients before the IRS on examination and appeals to resolve accounting

method controversies. Carol specializes in tax accounting for revenue and expenses, capitalization of

costs, inventories, long-term contracts, the uniform capitalization rules, and section 199, drawing on her

prior experience as an attorney for the National Office of the Internal Revenue Service, where she had

principal drafting and review responsibility for regulations implementing the uniform capitalization rules,

accounting for long-term contracts, and economic performance. She has led and participated in industry

and subject matter coalitions on behalf of client groups before Treasury and the Internal Revenue

Service on such matters as environmental remediation costs, cost capitalization for intangible and

tangible property, and tax accounting for land developers and contractors.

Other activities

Immediate Past Chair, and Vice Chair of the AICPA Tax Section’s Tax Accounting Committee.

Former Chair of the Tax Accounting Committee of the American Bar Association from 2008 through

2010, and as Vice Chair of the Committee from 2005 through 2008, and continues to be actively

involved as a member.

She is a frequent author of articles on tax accounting issues for the Journal of Taxation, Tax Advisor,

Journal of Bank Taxation, Journal of Real Estate Taxation, and other professional journals.

She is a frequent speaker on tax accounting issues for various professional organizations, including the

American Bar Association, Bank Tax Institute, Edison Electric Institute, Tax Executives Institute, Federal

Bar Association, NYU Institute on Taxation and numerous other groups.

Carol is also an Editor of the Tax Accounting Department of the Journal of Taxation.

KPMG LLP

1801 K Street, NW

Suite 12000

Washington, DC 20008

Tel 202-533-3040

Fax 202-315-2680

Cell 703-795-0012

Function and specialization

— Timing of revenue and expenses

— Inventories

— Cost capitalization

— Long-term contracts

— Section 199

Education, licenses and

certifications

— BS, Accounting, University of

Virginia

— JD, American University

— American University Law Review

Associations

— AICPA Tax Section

— American Bar Association

— Virginia State Bar

Carol ConjuraPartner

4© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Background

Before joining Washington National Tax in 1997, John served the Internal Revenue Service as an

Assistant Branch Chief in the Office of Chief Counsel (Corporate). As Assistant Branch Chief, he was

responsible for reviewing private ruling letters, technical advice memoranda, and other releases,

involving complex acquisitive reorganizations, tax-free divisive transactions, and other subchapter C

issues.

Professional and industry experience

John is a tax managing director in KPMG LLP’s Washington National Tax Corporate practice where he

concentrates in subchapter C and general corporate tax issues. He consults on corporate tax

transactions, including mergers and acquisitions, corporate divisions, distributions, bankruptcy and

insolvency workouts, liquidations, redemptions, contributions to capital, and the treatment of transaction

costs.

Other activities

John teaches internal and external continuing professional education courses. He is also a frequent

speaker and panelist on subchapter C topics for external groups, including the American Bar

Association, Practicing Law Institute, Executive Enterprises, DC Bar Association, Tax Executives

Institute, Council for International Tax Education, Alliance for Tax Legal & Accounting Seminars, and

Federal Bar Association.

KPMG LLP

1801 K Street, NW

Washington, DC 20006

Tel 202-533-4112

Fax 202-315-3127

Cell 703-365-7300

Function and specialization

Mergers, acquisitions, spin-offs,

divestitures, liquidating and

nonliquidating corporate distributions,

and corporate reorganizations.

Education, licenses and

certifications

— J.D., The University of Pittsburgh,

1986

— B.A., Gettysburg College, 1983

John GeracimosTax Managing Director, Corporate

5© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Agenda

Common accounting method planning issues in M&A

Common issues and recent guidance with respect to M&A transaction costs

Costs of abandoned transactions

IRS’s Section 355 cost compliance campaign

Uniquest and Section modified section 118

Common accounting method planning issues in M&A

7© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

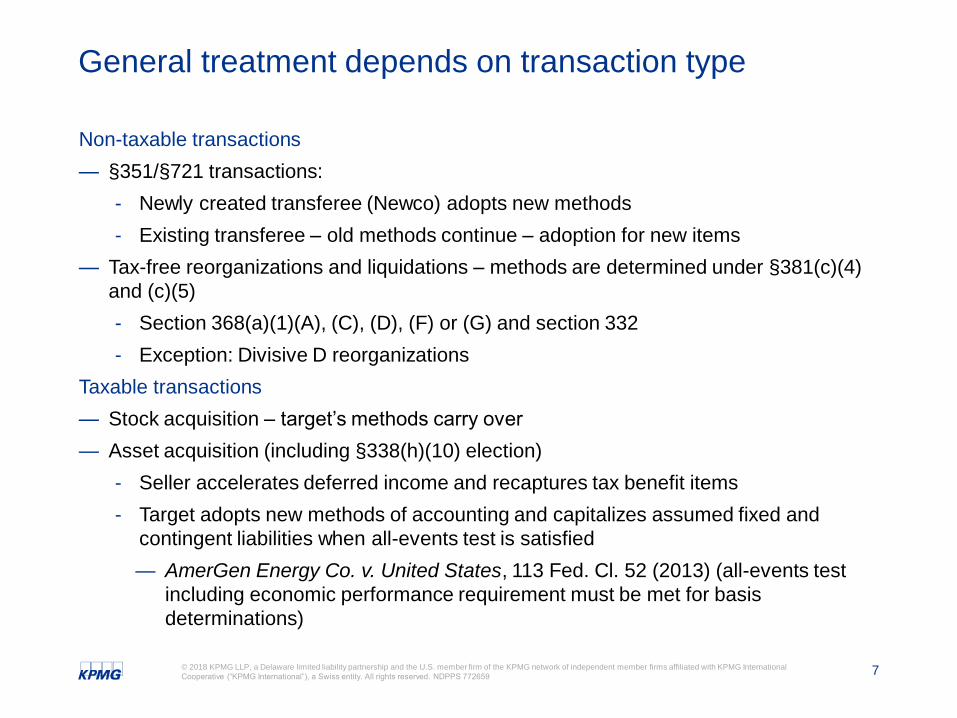

General treatment depends on transaction type

Non-taxable transactions

— §351/§721 transactions:

- Newly created transferee (Newco) adopts new methods

- Existing transferee – old methods continue – adoption for new items

— Tax-free reorganizations and liquidations – methods are determined under §381(c)(4)

and (c)(5)

- Section 368(a)(1)(A), (C), (D), (F) or (G) and section 332

- Exception: Divisive D reorganizations

Taxable transactions

— Stock acquisition – target’s methods carry over

— Asset acquisition (including §338(h)(10) election)

- Seller accelerates deferred income and recaptures tax benefit items

- Target adopts new methods of accounting and capitalizes assumed fixed and

contingent liabilities when all-events test is satisfied

— AmerGen Energy Co. v. United States, 113 Fed. Cl. 52 (2013) (all-events test

including economic performance requirement must be met for basis

determinations)

8© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Section 351/721

Tax accounting history is cut off

— No ability to obtain audit protection for pre-transfer periods

— Generally, section 481(a) does not apply to pre-transfer periods

Exceptions where carryover (step-in-shoes) treatment applies (including method, audit

protection, and section 481(a))

— Depreciation methods for tangible property (section 168(i)(7))

— Amortization under section 197

— Long-term contracts under section 460 percentage of completion method

— LIFO inventory layers for existing transferee

— Contingent liabilities (Rev. Rul. 95-74)

— Advance payment deferral method in same consolidated group

Consolidated group anti-abuse rule (Reg. §1.1502-17)

— Transferee may not adopt new method if the principal purpose is to avoid consent or

use method not acceptable to IRS

Special considerations

9© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Section 351/721 (continued)

Treatment of assumed liabilities is uncertain

— If both the transferor and transferee are in existence after the transaction, an issue

arises as to who may claim the deduction in certain cases

Example:

— Calendar year taxpayer (Transferor) contributes a business division to a subsidiary in a

section 351 transfer August 1, 2017

— Accrued vacation at August 1, 2017 is paid to employees by March 15, 2018

— Is the transferor or transferee entitled to the deduction?

- Rev. Rul. 95-74 (supra implies step in the shoes)

- Cf. PLR 9716001 (accrued vacation benefits paid more than 2 ½ months after the

end of the year of the transfer are deductible by the transferee)

— Other examples

- Accrued rebates

- Real estate taxes

Special considerations

10© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

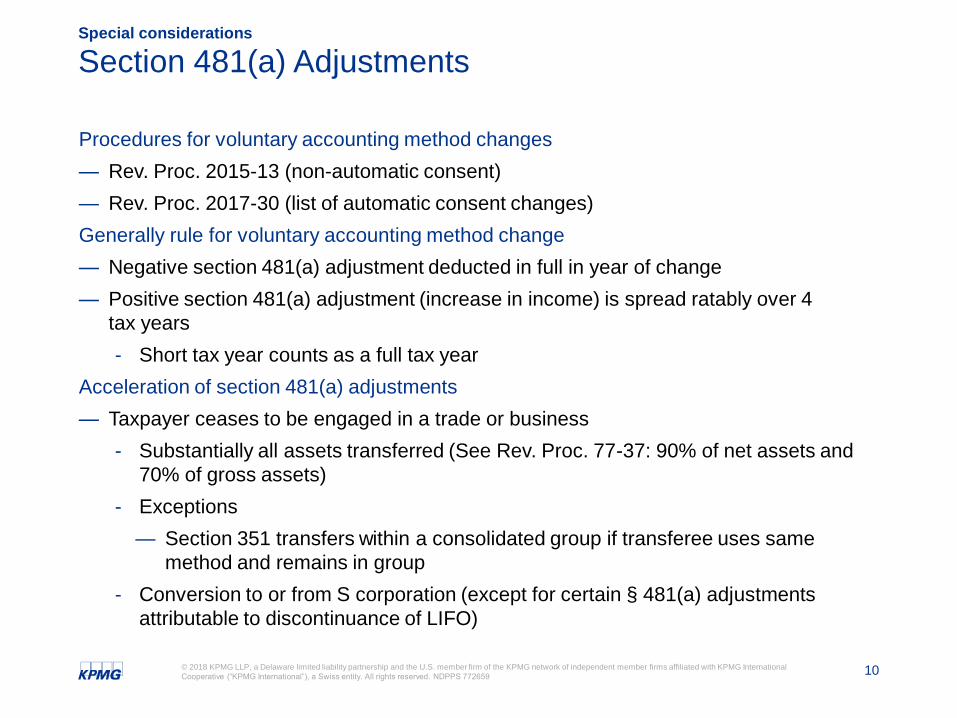

Section 481(a) Adjustments

Procedures for voluntary accounting method changes

— Rev. Proc. 2015-13 (non-automatic consent)

— Rev. Proc. 2017-30 (list of automatic consent changes)

Generally rule for voluntary accounting method change

— Negative section 481(a) adjustment deducted in full in year of change

— Positive section 481(a) adjustment (increase in income) is spread ratably over 4

tax years

- Short tax year counts as a full tax year

Acceleration of section 481(a) adjustments

— Taxpayer ceases to be engaged in a trade or business

- Substantially all assets transferred (See Rev. Proc. 77-37: 90% of net assets and

70% of gross assets)

- Exceptions

— Section 351 transfers within a consolidated group if transferee uses same

method and remains in group

- Conversion to or from S corporation (except for certain § 481(a) adjustments

attributable to discontinuance of LIFO)

Special considerations

11© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

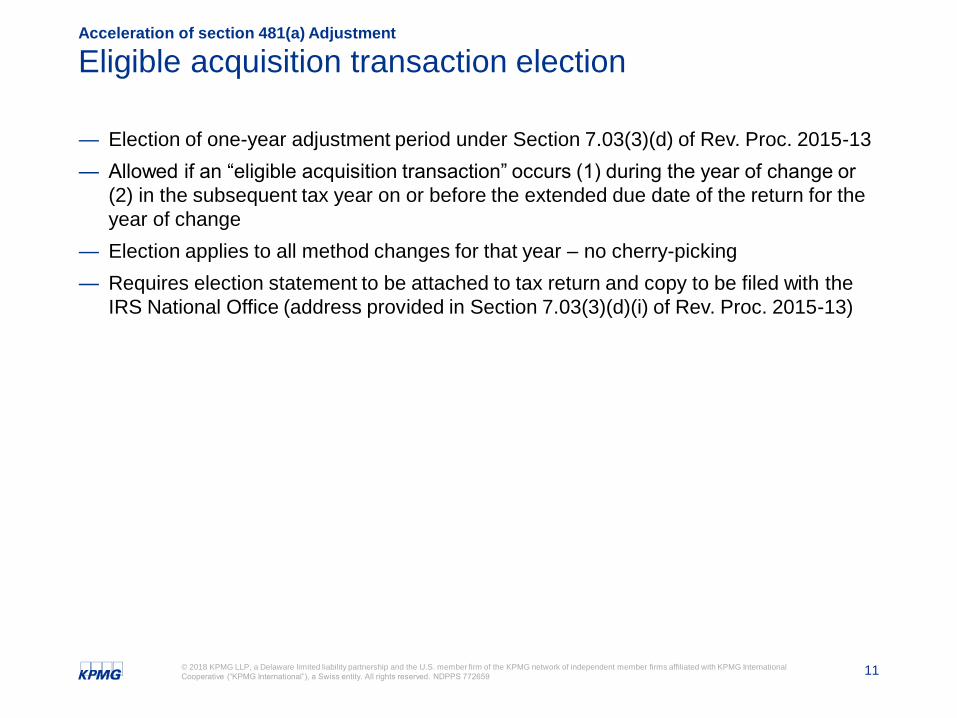

Eligible acquisition transaction election

— Election of one-year adjustment period under Section 7.03(3)(d) of Rev. Proc. 2015-13

— Allowed if an “eligible acquisition transaction” occurs (1) during the year of change or

(2) in the subsequent tax year on or before the extended due date of the return for the

year of change

— Election applies to all method changes for that year – no cherry-picking

— Requires election statement to be attached to tax return and copy to be filed with the

IRS National Office (address provided in Section 7.03(3)(d)(i) of Rev. Proc. 2015-13)

Acceleration of section 481(a) Adjustment

12© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Eligible acquisition transaction

An eligible acquisition transaction includes:

— For a CFC or corporation (other than an S corporation):

- Acquisition of a stock ownership interest in the taxpayer by another party that either

results in the acquisition of control of the taxpayer or causes the taxpayer’s tax year

to end; or

- An acquisition of assets in a transaction to which section 381(a) applies

— For all other taxpayers:

- An acquisition of an ownership interest in the taxpayer by another party that does

not cause the taxpayer to cease to exist for federal income tax purposes

— E.g., the sale or exchange of a partnership interest

Acceleration of section 481(a) Adjustment

13© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Special procedures for section 381 reorganizations

General carryover of pre-existing accounting methods

— Except if the parties have a conflict in methods for the same item, and

— Are integrated businesses after the transaction

Regulations provide procedures, terms and conditions for changing accounting methods

when a change is needed by reason of the regulations

— Reg. §1.381(c)(4)-1 (general methods)

— Reg. §1.381(c)(5)-1 (inventory methods)

— Reg. §1.381(c)(6)-1 (depreciation methods)

These procedures are in lieu of Rev. Proc. 2015-13 and Rev. Proc. 2017-30 and

apply when

— A change in method is necessitated by the reorganization

— The principal method is a permissible method and a change is made to the

principal method

14© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

When are businesses considered integrated?

Guidance under section 446(d) is considered relevant

— Taxpayers may use different methods of accounting is trades or businesses are

“separate and distinct”

— Facts and circumstances test

- Separate books and records

- Separate employees

- Separate functions (except if same function but geographically separate may still

be separate)

- CCA 201430013: Disregarded entities (SMLLC’s) can be a separate trade or

business due to legal separation even without other factors

15© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Determination of the principal method

For each integrated trade or business, the acquiring corporation’s method, unless:

— Both gross receipts (for representative period) and adjusted basis of assets of acquired

component business are larger than acquiring’s

— If more than one principal method, acquiring corporation may choose which one will be

the principal method

— Inventories

- Aggregate fair market value of type of goods held by each component trade

or business

- Simplifying convention: Acquiring corporation may elect to aggregate fair market

value of all goods held by each component trade or business

16© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Procedures, terms, and conditions

Change to principal method

— Automatic under the final regulations (no Form 3115)

— Exam scope limitations do not apply

— No audit protection

— Change reflected on acquiring corporation’s tax return, whether the acquiring or

acquired corporation makes the change

— §481(a) adjustment or cutoff method, as applicable determined as of beginning of day

after date of distribution

- No spread for negative §481(a) adjustment

- 4-year spread for positive §481(a) adjustment

17© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Not all changes covered by the regulations

Changes must be made under the voluntary change procedures (i.e., Rev. Proc. 2015-13

or Rev. Proc. 2017-30)

— Principal method is not a permissible method

— Parties do not want to use principal method

— Parties want to opt-out of the regulation procedure

Advantages to opt-out

— Audit protection

— Section 481(a) adjustment determined at beginning of the year

Modified due date for Form 3115 is the later of:

— Ordinary due date, or

— Earlier of:

- 180 days after transaction or

- Date acquiring corporation files tax return

18© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Effect of short tax years on accounting methods

Certain accounting method provisions are applied with respect to the end of a tax year:

— Recurring item exception (Treas. Reg. §1.461-5)

— 12-month rule for prepaid expenses (Treas. Reg. §1.263(a)-4(f)))

— 2.5 month rule for deferred compensation (§404)

Other accounting methods are impacted by tax years

— Deferral method for advance payments under Rev. Proc. 2004-34

Short tax years must be taken into account in applying these rules – may cause income to

be accelerated or expenses to be deferred

19© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Treatment of deferred revenue

Accounting methods in general

— Book defers until earned

— Permissible tax methods (Rev. Proc. 2004-34)

- Current inclusion method or 1-year deferral method

Taxable asset acquisitions (treatment unsettled)

— Income approach: deferred revenue & obligations acquired as of transaction date may

give rise to taxable income to buyer (James M. Pierce Corp.)

— Capitalization approach: obligations acquired do not give rise to taxable income

20© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Treatment of deferred revenue (continued)

Stock acquisitions (taxable or non-taxable)

— CCA 2016190009

- In Year 1, Taxpayer using the deferral Method had 100% of its stock acquired by

unrelated taxpayer

- Acquirer wrote down the associated deferred revenue liability to fair value on the

date of acquisition

- Issue – whether taxpayer could use the deferral method for payments received in

Year 1 when the full amount of payments received would not be recognized in

revenues in its AFS in a future year

- IRS concluded deferral method was still available; however, taxpayer required to

recognize the full amount of the payment received no later than Year 2

Common issues and recent guidance with respect to transaction costs

22© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Investment banker fees

— Rev. Proc. 2011-29 provides a safe harbor for the documentation requirement

— Applies to “success-based fees” for services performed in the process of investigating

or otherwise pursuing a “covered transaction.”

- Taxable acquisitions of assets constituting a trade or business

- Taxable acquisitions of an ownership interest in a business entity if the parties are

related immediately afterward

- Reorganizations described in sections 381(a)(1)(A), (B), or (C), or acquisitive “D”

reorganizations

— If elected, the safe harbor permits the taxpayer to deduct 70% of the success-based

fee and capitalize the remaining 30%

- Taxpayer must attach an election statement to the original tax return for the year in

which the fee is paid

- The election is not an accounting method and does not affect the treatment of other

success-based fees

- What if you forget to attach the statement?

23© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Application of safe harbor to deemed asset transactions

CCA 201624021

— Target shareholders sold stock of Target S Corp to Acquiring Corp on

December 31, 2012

— Parties jointly elected to treat the transaction as a deemed asset acquisition under

Section 338(h)(10)

— Target incurred success-based fees and made the safe harbor election to deduct 70%

of the fees on its return for the 2012 tax year

— IRS concluded the safe harbor did not apply – the deemed asset sale did not meet the

definition of a “covered transaction”

— Covered transactions for taxable asset acquisitions include only acquisitions of assets

by the taxpayer

24© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Proper allocation of debt issuance costs

Many covered transactions involve debt financing

Debt financing is treated as a separate transaction under Reg. sec. 1.263(a)-5

— Debt issuance costs are amortizable using the constant yield method per

Reg. sec. 1.446-5

Application of 70-30 fee safe harbor has been uncertain

1. Apply safe harbor to entire fee and allocate debt issuance with respect to 30%

2. Allocate to debt financing first and apply safe harbor to remainder

— IRS position is the approach in 2.

25© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Proper treatment of non-facilitative costs

Acquirer’s non-facilitative costs

— May be deductible under section 162(a) if investigating the expansion of a business

- Except if Reg. sec. 1.263(a)-4 would require capitalization as an acquired or

created intangible

— Legislative history to section 195 treats acquisition of a subsidiary as an acquisition of

assets for this purpose

- Applies to business investigatory costs for expansion but not start up costs

— See Specialty Restaurants, Bennett Paper

- Thus, if acquirer is acquiring a different line of business, section 195 would apply to

the non-facilitative costs

— Such costs are amortizable over 15 years

Target’s non-facilitative costs

— Deductible under section 162(a)

- Section 195 would not apply to a target’s non-facilitative costs

- Still have to be tested under Reg. sec. 1.263(a)-4

26© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Allocation of target transaction costs to pre-acquisition or post-acquisition period

GLAM 2012-010: The “next-day” rule

— Reg. sec. 1.1502-76(b)(1)(ii)(B) provides that:

- If, on the day of S’s change in status as a member, a transaction occurs that is

properly allocable to the portion of S’s day after the event resulting in the change,

S… must treat the transaction for all Federal income tax purposes as occurring at

the beginning of the following day.

- A determination as to whether a transaction is properly allocable to the portion of

S’s day after the event resulting in S’s change in status will be respected if it is

reasonable and consistently applied by all affected persons

— IRS ruled that next day rule does not apply to non-qualified stock options and

investment banking fees that are triggered by the acquisition because they relate to

pre-acquisitions services

Prop. Treas. Reg. Sec. 1.1502-76(b) modifying the “next-day” rule

— An extraordinary item that results from a transaction that occurs on the day of S’s

change in status as a member, but after the event resulting in the change, must be

reported on the tax return for the period beginning the day after S’s change in status.

— The Prop. next-day rule does not apply to any extraordinary item that becomes

includible or deductible simultaneously with the event that causes the change in

S’s status.

27© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Regulatory approval

Reg. sec. 1.263(a)-5(e) treats regulatory approval costs as inherently facilitative

CCA 201713010

— IRS concluded that costs incurred in activities to satisfy a regulatory agency’s

conditions for a merger are not per se facilitated transaction costs

Taxpayer, a holding company of several regulated utilities planned a merger with another

regulated utility

Regulatory board approval was conditioned on

— Providing rate credit to customers

— Contributing to a customer investment fund

— Paying amounts to state for future development

— Commitment to contribute annual amount to charities and community

IRS rejected examining agent’s arguments for capitalization

— The “but for” test is not dispositive

— Facilitative costs including regulatory approval costs are costs directly associated with

pursuing the transaction and would not be otherwise deductible operating costs if

incurred outside the context of a merger

Facilitative costs

28© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Support payments to shareholders

PLR 201736002

— IRS ruled that investment adviser’s support payment to target shareholders to induce

them to approve a merger with acquirer was a deductible business expense under

section 162(a)

Taxpayer, an investment adviser to acquirer, provided ongoing management

services under an investment management agreement

— Fees were variable and depended part on asset size of acquirer

After acquirer entered into a merger agreement to acquire target in a taxable

acquisition of stock

Taxpayer made a support payment to target shareholders and did not acquire any

ownership interest in target

IRS ruled that the payments were not capitalizable under either

— Reg. sec. 1.263(a)-5 (no capital transaction), or

— Reg. sec. 1.263(a)-4 (did not provide taxpayer a “right” to provide and/or be

compensated for services)

— Fees were characterized as business development expenses to help induce

higher fees

Costs of abandoned transactions

30© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

General rule

Taxpayer may deduct costs of abandoned transaction under section 165. See, e.g., Sibley,

Lindsay & Curr Co. v. Commissioner, 15 T.C. 106 (1950), acq. 1951-1 C.B. 3.

Factual question – when is transaction abandoned? Often difficult in IPO context – is the

transaction abandoned or shelved until market improves?

Note that section 165 does not require taxpayer to be engaged in business as is the case

with section 162.

More complex issues if taxpayer abandons transaction and consummates another

transaction.

31© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Reg. 1.263(a)-5(c)(8)

Costs to facilitate Transaction A will facilitate Transaction B “only if” the transactions are

mutually exclusive (Reg. 1.263(a)-5(c)(8)).

— This language does not say that A must be capitalized into B if the transactions are

mutually exclusive. Rather, it says that: if A and B are not mutually exclusive, A will not

be capitalized into B and, if A and B are mutually exclusive, A may be capitalized into B

depending on facts and circumstances.

— Preamble to final regulations supports and clarifies this interpretation: Costs to facilitate

Transaction A will facilitate Transaction B “only if” the transactions are mutually

exclusive and the taxpayer abandoned A in order to do B.

— Case law – was process abandoned? Were transactions considered as alternatives to

achieve a similar objective?

— If first transaction a Covered Transaction, TP may deduct pre-BLD non-IF costs for that

transaction. See Reg. 1.263(a)-5(l), Example (11)(iii).

32© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

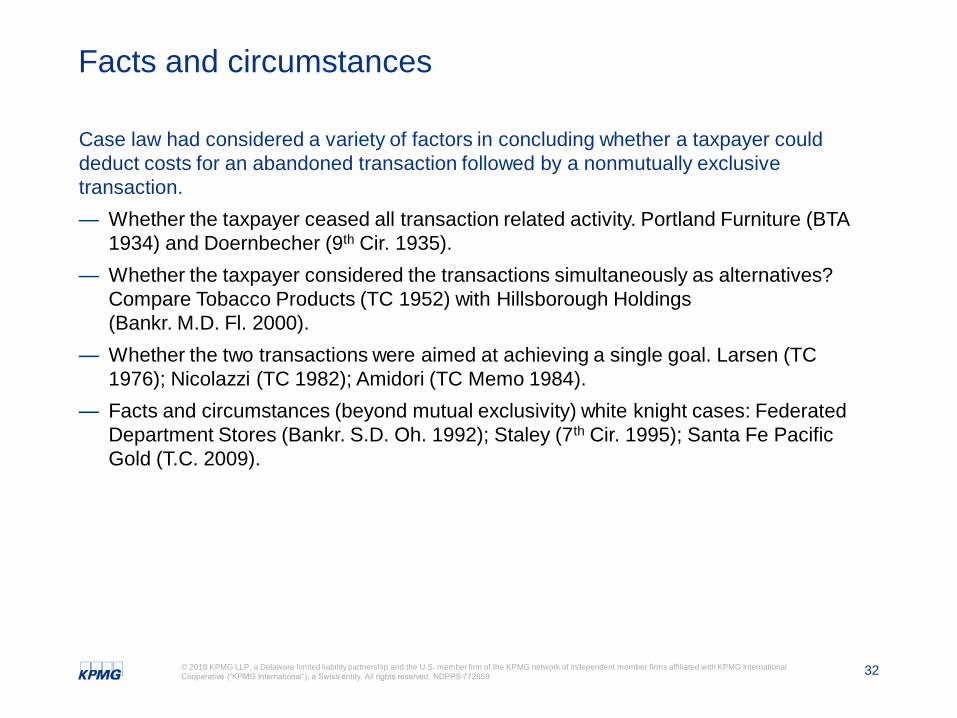

Facts and circumstances

Case law had considered a variety of factors in concluding whether a taxpayer could

deduct costs for an abandoned transaction followed by a nonmutually exclusive

transaction.

— Whether the taxpayer ceased all transaction related activity. Portland Furniture (BTA

1934) and Doernbecher (9th Cir. 1935).

— Whether the taxpayer considered the transactions simultaneously as alternatives?

Compare Tobacco Products (TC 1952) with Hillsborough Holdings

(Bankr. M.D. Fl. 2000).

— Whether the two transactions were aimed at achieving a single goal. Larsen (TC

1976); Nicolazzi (TC 1982); Amidori (TC Memo 1984).

— Facts and circumstances (beyond mutual exclusivity) white knight cases: Federated

Department Stores (Bankr. S.D. Oh. 1992); Staley (7th Cir. 1995); Santa Fe Pacific

Gold (T.C. 2009).

33© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Mutually exclusive?

Practical exclusivity or structural exclusivity?

Practical exclusivity – Taxpayer could have undertaken both transactions as a structural

matter but could not have done so as a practical matter. For example, Acquiring could not

afford to acquire Target 1 and Target 2, although it could have structurally acquired both.

See Reg. 1.263(a)-5(l), Example (4) (TP considers the acquisition of three potential

targets, “any or all of which [the taxpayer]… might consummate and has the financial

ability to consummate.”)

Structural exclusivity – Taxpayer could not have undertaken both transactions as a

structural matter. For example, a Target TP only can be acquired by a single acquiring

entity. See Reg. 1.263(a)-5(l), Example (3) (discussion portion of the example (as opposed

to the fact portion) concludes that the IPO and the borrowing and the acquisitions and the

borrowing “are not mutually exclusive transactions” so that the costs of investigating the

abandoned IPO and the abandoned acquisition transactions cannot be viewed as

facilitating the consummated borrowing transaction).

1.263(a)-5(c)(8)

34© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Effect of section 1234A

Cases historically did not address character of deduction. Several cases (e.g., Santa Fe

Pacific Gold) concluded that the taxpayer could deduct amounts under both section 162

and 195 and did not distinguish between the two theories based on character.

Section 1234A – Gain or loss attributable to the cancellation, lapse, expiration, or other

termination of –

(1) A right or obligation (other than a securities futures contract, as defined in section

1234B) with respect to property which is (or on acquisition would be) a capital asset in

the hands of the taxpayer, or

(2) A section 1256 contract (as defined in section 1256) not described in paragraph (1)

which is a capital asset in the hands of the taxpayer, shall be treated as gain or loss

from the sale of a capital asset.

Effect on receipt and payment of termination fees and capitalized facilitative costs of

abandoned transaction.

Character

35© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Effect of section 1234A (continued)

TAM 200438038 (June 2, 2004) – TP had agreement with T to acquire T’s stock subject to

termination fee; T broke off with TP and paid TP termination fee. TAM concluded ordinary

income. No mention of 1234A.

PLR 200823012 (Mar. 10, 2008) – Same facts and same conclusion as TAM, stating that

1234A did not apply. Perhaps because TP did not have an agreement to acquire a capital

asset from T.

Pilgrims Pride (5th Cir. 2015) (1234A only applies to derivative rights, not to payment for

capital asset itself).

Character

36© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Effect of section 1234A (continued)

CCA 201642035 (Feb. 9, 2016) – Same facts as PLR, but concludes that, notwithstanding

that contract between TP and T rather than TP and selling shareholders, because

“contract between the acquiring corporation and the target corporation is a customary part

of the process by which the stock of a publicly held corporation is acquired”, gain or loss

with respect to agreement with respect to T stock was subject to 1234A and must be

capital.

CCA also applied to TP’s capitalized facilitative costs for the abandoned transaction (to the

extent that it exceeded received termination fee): “Because this loss was attributable to

the termination of Acquirer’s right with respect to Target’s stock – property that would have

been a capital asset in Acquirer’s hands – the loss is treated as a loss from the sale of a

capital asset under section 1234A.”

Q – same result for capitalized abandoned costs at T level? Is INDOPCO intangible a

capital asset.

FFA 20163701F (May 3, 2016) – TP T in failed inversion transaction had to pay

termination fee. Because the amount related to a contractual right concerning a capital

asset, T had to treat payment as a capital loss.

Character

37© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

PLR 201518012

Addressed whether a payment to terminate a management agreement was required to be

capitalized

The managers were hired as turn around experts, and services included ongoing

monitoring and business advisory services

Fee paid out of proceeds of subsequent IPO, but fee not contingent on a successful IPO

However, it was necessary to terminate the agreement to undergo the IPO

IRS held the termination payment was not capitalized as a cost that facilitated the IPO

Termination payment in IPO

IRS section 355cost compliancecampaign

39© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

LB&I section 355 compliance campaign

March 13, 2018 – IRS LB&I announced Large Business and International Compliance

Campaigns for Section 355 costs:

Costs to facilitate a tax-free corporate distribution under IRC Section 355, such as a spin-

off, split-off or split-up, must be capitalized and are not currently deductible. Some

taxpayers may execute a corporate distribution and improperly deduct the costs that

facilitated the transaction in the year the distribution was completed. The goal of this

campaign is to ensure taxpayer compliance with the requirement to capitalize, not deduct,

the facilitative costs when the distribution is completed. The treatment stream for this

campaign is issue-based examinations.

40© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

LB&I compliance campaign

What is section 355?

General Acquisition Cost Rules

Application of Acquisition Cost Rules to Section 355 Transactions

What could be the focus of the compliance campaign?

41© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Section 355

Spin-off (Dividend equivalent)

Pro-rata

distribution

of C stock

to S/Hs

C

S/Hs

D

S/Hs

D C

Before distribution After distribution

42© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Section 355 requirements

I. Section 355(a) Statutory Requirements

— Control Immediately Before

— Distribution of Stock and Securities Constituting Control

— Not a Device for Distribution of E&P

— Distributing & Controlled Engaged in an Active Trade or Business

— Not a cash-rich split-off

— Neither D nor C is a REIT (new rule)

II. Section 355(a) Nonstatutory Requirements

— Business Purpose

— Continuity of Shareholder Interest

— Continuity of Business Enterprise

III. Special Corporate-Level Requirements

— Section 355(d)

— Section 355(e)

43© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

What costs are we talking about?

Examples:

— Legal Fees

— Investment Bank Fees

— Lender Fees

— Sponsor Fees

— Due Diligence Costs

— Tax planning and Structuring Costs

— Transfer Costs

— SEC Filing Preparation

— Accounting Fees – Carve out Financials

— Stand-Up Consultant Costs

44© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

General rule

Generally – TP must capitalize amounts paid to “facilitate” capital transactions:

— Acquisition of assets constituting a trade or business (whether TP is the acquirer or the

target)

— Acquisition of interests in a business entity if TP and entity are related within the

meaning of 267(b) or 707(b) (more than 50 percent)

— Acquisition of an ownership interest in the TP other than a redemption

— Restructuring, recapitalization, or reorganization of capital structure (including

368 reorganizations and 355 distributions)

— Transfer under section 351 or 721;

— Formation or organization of disregarded entity

— Acquisition of capital, including stock issuance

— Borrowing

Exceptions – Integration Costs and Covered Transaction Costs

Transaction costs

45© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

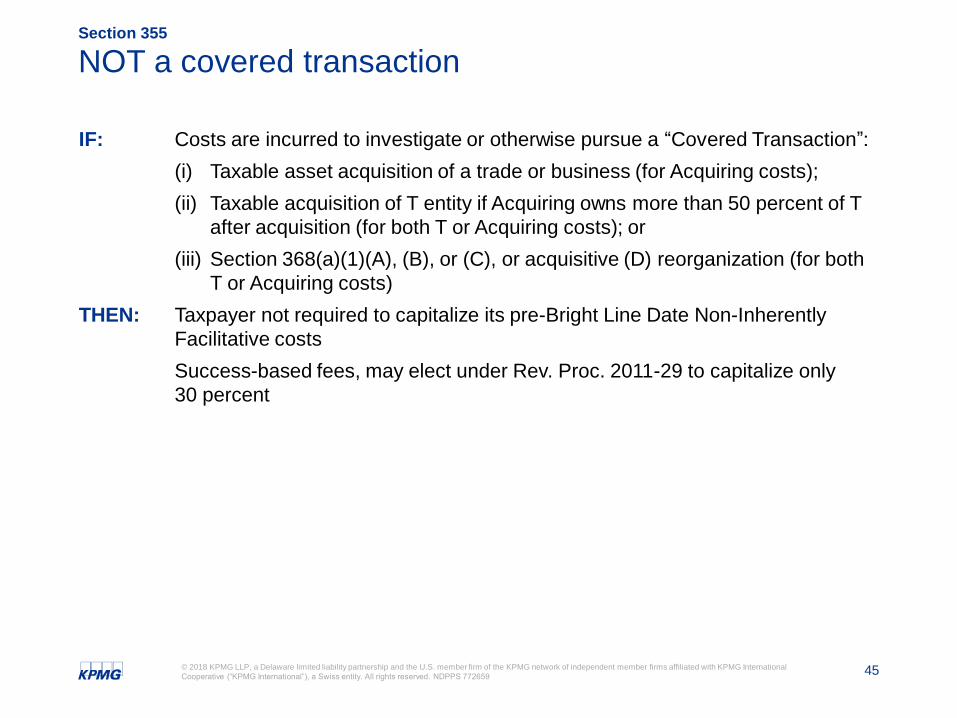

NOT a covered transaction

IF: Costs are incurred to investigate or otherwise pursue a “Covered Transaction”:

(i) Taxable asset acquisition of a trade or business (for Acquiring costs);

(ii) Taxable acquisition of T entity if Acquiring owns more than 50 percent of T

after acquisition (for both T or Acquiring costs); or

(iii) Section 368(a)(1)(A), (B), or (C), or acquisitive (D) reorganization (for both

T or Acquiring costs)

THEN: Taxpayer not required to capitalize its pre-Bright Line Date Non-Inherently

Facilitative costs

Success-based fees, may elect under Rev. Proc. 2011-29 to capitalize only

30 percent

Section 355

46© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Dis-integration costs

Regulations define facilitative costs – costs paid in the process of investigating or

otherwise pursuing; fact that costs would not have been incurred but-for the transaction, a

factor, but not determinative.

Preamble to proposed regulations:

The terms reorganization and restructuring are not intended to refer to mere changes

in an entity's business processes, commonly referred to as “re-engineering.” Thus, a

taxpayer's change from a batch inventory processing system to a “just-in-time”

inventory processing system, regardless of whether the taxpayer refers to such change

as a business “restructuring,” is not within the scope of the rule, as demonstrated by

example in the proposed regulations.

See also Reg. § 1.263(a)-4(l), Example (5).

Significant non-facilitative but-for costs: operational and dis-integration costs

What could we deduct?

Uniquest v U.S., purchase price adjustments, and amended section 118

48© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Uniquest Delaware LLC v. U.S., (W.D. N.Y., Mar. 27, 2018)

2006 – Uniquest purchased building with

expectation to receive NY State Brownfield Tax

Credits

Started asbestos remediation

Aug. 2007 – Determined it would not qualify for

credits

Nov. – Dec. 2007 -- Contacted Empire State

Corporation about grants and negotiated in

June 2008 – requested more grant funding

January 2009 – new grant proposal

2009 – Grants disbursed

Uniquest

LLC

49© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Uniquest (W.D. N.Y., Mar. 27, 2018)

Uniquest did not include amount as taxable income

Parties filed motions for summary judgement

Uniquest arguments:

— Common-law inducement doctrine

— Common-law exclusion for capital contributions to partnership

— Section 118 exclusion for income passed through to corporate partners

Government arguments

— Glenshaw Glass overrules common-law inducement doctrine

— No common-law exclusion for capital contributions to partnership

— Taxpayer failed property to plead 118 exclusion for corporate partners

50© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Uniquest: Purchase price adjustment

Taxpayer argued that receipt of grant should be viewed as adjustment in the purchase

price of its improvements in the building

Long history of purchase-price adjustment doctrine:

Brown (B.T.A. 1928); Freedom Newspapers (T.C. Memo 1977)

RR 73-559, RR 76-96, RR 88-95, RR 2007-27

Service conceded point in General Motors (T.C. 1999) where it furthered their

consolidated return argument

Government brief: “… Plaintiffs attempt to invent a new doctrine, a so-called inducement

doctrine… ”

— Argued that Glenshaw Glass overruled authorities

— Also, argued grant was not inducement as TP started work on building before it

sought grants

51© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Uniquest: Conclusion on PP adjustment

The cases Plaintiffs cite in support of their contention that a common law inducement

doctrine applies in this case to exempt the ESD grants from Uniquest’s income are either

factually distinguishable or grounded in an outdated definition of income. As the

Government seems to concede, if not for Glenshaw Glass, the holding in Brown might

compel the result that Plaintiffs seek. However, the case law that has followed the

Supreme Court’s decision in Glenshaw Glass, as well as the text of the IRC,

overwhelmingly indicate that gross income includes “all realized gains and forms of

enrichment… Except those specifically exempted,” Collins, 3 F.3d at 630 (internal

quotation marks omitted), and that no common law inducement doctrine survives.

52© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Uniquest: Purchase price adjustment

District Court’s conclusion arguably over-broad regarding Glenshaw Glass

TP did not have unfettered accession to wealth; had to invest funds in

designated project

Broad reading also would overrule Service’s revenue rulings

Are we now taxing receipt by auto-purchasers of manufacturer incentives? See

RR 76-96

Arguably, doctrine still should apply under more favorable facts

53© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 772659

Relevance to 118 amendment

JC&JA amended section 118

— NSCtC does not include

— Contribution by any governmental entity or civic group (other than a contribution by a

shareholder as such)

Applies to:

— Contributions after date of enactment

— Except for contributions by a governmental entity pursuant to a master development

plan that has been approved prior to the effective date by a governmental entity

ISSUE: whether corporations can apply purchase price adjustment theory to receipt

of grants in lieu of section 118

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved. NDPPS 772659

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular

individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such

information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on

such information without appropriate professional advice after a thorough examination of the particular situation.

kpmg.com/socialmedia