tax credit ftc splitting...

TRANSCRIPT

Presenting a live 110‐minute teleconference with interactive Q&A

New Foreign Tax Credit and FTC Splitting Regulationsand FTC Splitting RegulationsMastering Section 909 and 901 Rules to Maximize Efficiencies in Complex FTC Planning

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, MAY 3, 2012

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Peter Daub, Partner, Baker & McKenzie, Washington, D.C., , , g ,

John D. Bates, Atty, Ivins Phillips & Barker, Washington, D.C.

For this program, attendees must listen to the audio over the telephone.

Please refer to the instructions emailed to the registrant for the dial-in information.Attendees can still view the presentation slides online. If you have any questions, pleasecontact Customer Service at1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

Attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online but there is no online audio for this program.

Attendees must stay on the line for at least 100 minutes in order to qualify for a full 2 credits of CPE. Attendance is monitored as required by NASBA.

Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.at 1 800 926 7926 ext. 10.

Tips for Optimal Quality

S d Q litSound Quality

For this program, you must listen via the telephone by dialing 1-866-873-1442and entering your PIN when prompted. There will be no sound over the web connection.co ect o .

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

N F i T C dit d FTC New Foreign Tax Credit and FTC Splitting Regulations Seminar

May 3, 2012

John Bates, Ivins Phillips & [email protected]

Peter Daub, Baker & [email protected]

Today’s Program

Background Issues[Peter Daub]

Slide 7 – Slide 14

Final Sect. 901 Regulations[John Bates]

Slide 15 – Slide 30

Temporary Sect. 909 Regulations: Splitter Arrangements[Peter Daub]

Slide 31 – Slide 57

Temporary Sect. 909 Regulations: Other Rules[John Bates]

Slide 58 – Slide 66

BACKGROUND ISSUESPeter Daub, Baker & McKenzie

BACKGROUND ISSUES

B k dBackground• Congress became concerned about certain structures taxpayers Congress became concerned about certain structures taxpayers

used to claim foreign tax credits.

― Structures involved separation or “splitting” of foreign taxes from E&P based on “technical taxpayer rule” in Sect taxes from E&P based on technical taxpayer rule in Sect. 901 regulations

― Taxpayers claimed credits or deductions for foreign taxes prior to including, in income for U.S. tax purposes, the associated foreign income to which such taxes relate.

― Taxes would offset U.S. tax on unrelated foreign income.g

• Concerns led the Service to enact proposed Sect. 901 regulations in 2006.

I 2010 C t d i d t d S t 909

8

• In 2010, Congress stepped in and enacted Sect. 909.

Background:gGuardian Industries

• Guardian Industries

― Under Luxembourg domestic law, the parent company of a Luxembourg combined group was solely responsible for the u e bou g co b ed g oup was solely espo s ble o t e tax on the group’s combined income, regardless of which entity earned the income.

Accordingly the U S owner of the parent company a ― Accordingly, the U.S. owner of the parent company, a disregarded entity for U.S. tax purposes, was entitled to a credit under Sect. 901 for the full amount of the tax paid

th bi d i th h th i ( on the combined income, even though the income (as computed under U.S. principles) earned by the subsidiaries was not subject to current U.S. tax.

9

Background:g2006 Proposed Regulations

• In response to the taxpayer victory in Guardian Industries the In response to the taxpayer victory in Guardian Industries, the Service issued proposed Reg. §1.901-2(f)(1), which modified the definition of “taxpayer,” for purposes of determining who may claim foreign tax credits (FTCs) in situations in which more than one person could potentially have a right to claim FTCs due to differences between U.S. and foreign law.

• The proposed regulations created a new principle under which, when h ld b d d l bl fmore than one person could be considered eligible for FTCs, any

person taking foreign income into account would be considered eligible for the FTC, in proportion to the amount of income taken into account into account.

• The proposed regulations were aimed specifically at FTC planning using:

Foreign consolidated groups

10

― Foreign consolidated groups ― Hybrid or reverse hybrid entities

Background:g2006 Proposed Regulations (Cont.)

• Problems raised by 2006 proposed regulations:Problems raised by 2006 proposed regulations:― Proposed regulations would rely on foreign law for purposes of

allocating the foreign tax base, rather than look to foreign law only for evidentiary purpose of identifying the facts and incidence only for evidentiary purpose of identifying the facts and incidence of tax.

― U.S. taxpayers would have to make determinations of whether foreign ownership was consistent with U.S. rules applicable to g p ppentities (e.g., hybrids) and the substance-over-form doctrine (e.g., repurchase obligations).

― Would not curtail all possible splitting transactions

11

Background:gSect. 909 Generally

• Congress enacted Sect. 909 as part of P.L. 111-226 on Aug. 10, 2010.

• In a “foreign tax credit splitting event,” Sect. 909 requires U.S. taxpayers to suspend taking into account any foreign income taxes, for purposes of computing earnings and profits (E&P) and FTCs until the tax year in which related income is taken into account by the payor of taxand FTCs, until the tax year in which related income is taken into account by the payor of tax.

• An FTC splitting event occurs if the related income is taken into account by a covered person.

― “Related income” is the income (or E&P) to which the tax relates.

― A “Section 902 corporation” is any foreign corporation with respect to which one or more U.S. corporations meets the ownership requirements of sections 902(a) and (b).

― A “covered person” with respect to the payor of the tax is:

A i i hi h di l i di l 10% l » An entity in which payor directly or indirectly owns 10% vote or value

» A person holding a direct or indirect 10% vote or value interest in payor

» Any person related to the payor under sections 267(b) or 707(b)

12

• Sect. 909 applies to foreign taxes paid or accrued in tax years beginning after Dec. 31, 2010 (and pre-2011 foreign taxes that would be taken into account after that date).

Background:gSect. 909 Comparison With Technical Taxpayer Rules

• Sect. 909

― A timing rule that suspends foreign taxes and foreign tax credits from being taken into account until the related income is taken into account

T h i l t l• Technical taxpayer rules

― An allocation of foreign taxes to the person that earns the income, which prevents an allowance of foreign tax credits to other entities

• Comparative example• Comparative example

― Consider a foreign reverse hybrid entity (i.e., a corporation for U.S. federal tax purposes that is disregarded as an entity separate from its owners for foreign tax purposes)

― Technical taxpayer rules would treat the reverse hybrid entity as if it paid the full amount of foreign tax allocated to the income it generated.

― Sect. 909 suspends the tax until the related income is taken into account

13

by the entity or its owners.

Background:

• Applied only to taxes paid or accrued by a Sect. 902 corporation (i.e., not a U S person)

gNotice 2010‐92 Generally

U.S. person)• Provided an exclusive list of arrangements that would be treated as giving

rise to FTC splitting events, for purposes of applying Sect. 909 to pre-2011 taxes: – Reverse hybrids – Reverse hybrids – Foreign combined reporting regimes (tax consolidations) – Certain group relief/loss surrender arrangements involving disregarded

debt H b id i t t – Hybrid instruments

• Provided guidance on determining, tracking and recognizing pre-2011 split taxes and related income, including guidance on: – Retaining the character of split taxes and related income – E&P ordering rules on the distribution of related income

• Retroactive application, but cuts off pre-2011 split foreign income taxes paid or accrued by a Sect. 902 corporation in taxable years beginning before January 1, 1997

14

• Notice 2010-92 stated that the Service preferred to handle splitter arrangements through Sect. 909 rather than the technical taxpayer rules.

FINAL SECT 901 REGULATIONSJohn Bates, Ivins Phillips & Barker

FINAL SECT. 901 REGULATIONS

Technical Taxpayer Rules

• Foreign tax is considered paid by the person who has legal liability under foreign law f h (§1 901 2(f)(1))

p y

for the tax (§1.901-2(f)(1)).– Treasury and IRS are still considering whether and to what extent to revise or

clarify this general rule in certain circumstances, such as for withholding tax imposed on an amount of income that is considered received by different personsimposed on an amount of income that is considered received by different persons, for U.S. and foreign tax purposes (e.g., certain “repo” transactions).

• The final technical taxpayer regulations address the application of the legal liability rule to foreign consolidated groups and other combined income regimes (§1.901-2(f)(3)(i)).

• Tax is considered computed on a combined basis if two or more persons that would otherwise be subject to foreign tax on their separate taxable incomes add their items of i i d d ti d l t t i l lid t d t bl iincome, gain, deduction and loss to compute a single consolidated taxable income amount, for foreign tax purposes (§1.901-2(f)(3)(ii)).

• The final regulations apply to taxable years beginning after Feb. 14, 2012.– Thus Sect 909 generally does not apply with respect to foreign taxes paid or

16

– Thus, Sect. 909 generally does not apply, with respect to foreign taxes paid or accrued on combined income during tax years beginning after Feb. 14, 2012.

Technical Taxpayer Rules:iTaxes Imposed On Combined Income

• Circumstances in which tax is considered imposed on combined income (§1.901-2(f)(3)(ii))– Foreign consolidated groups, regardless whether foreign law imposes joint

and several liability on the group members– Foreign regimes in which subsidiaries are treated as branches of the parent– Spouses who file jointlyp j y

• It does not matter which person is obligated to remit the tax or actually remits the tax.

• Foreign tax is not considered imposed on the combined income of two orForeign tax is not considered imposed on the combined income of two or more persons merely because one or more of the persons is fiscally transparent under foreign law (§1.901-2(f)(3)(ii)).

17

Technical Taxpayer Rules:i i

• The final technical taxpayer rules differ in several ways from the 2006

Differences From 2006 Proposed Technical Taxpayer Rules

proposed technical taxpayer rules.– The final regulations do not address tax imposed on the income of an

entity that is fiscally transparent for foreign tax purposes, but is treated as a corporation for U.S. tax purposes (i.e., a reverse hybrid entity).

• Reverse hybrid entity structures are covered under the Sect. 909 regulations.

– The final regulations provide somewhat different rules for entities that are fiscally transparent for U.S. tax purposes (i.e., partnerships and disregarded entities).

– The 2006 proposed regulations held off on addressing the effect of hybrid instruments and disregarded payments between related parties, and the final regulations do not address hybrid instruments.

18

• Certain hybrid instrument arrangements are covered under the Sect. 909 regulations.

Technical Taxpayer Rules:i

• Circumstances in which tax is not considered imposed on combined income (§1.901-2(f)(3)(ii)(A) (F))

Taxes Imposed On Combined Income

2(f)(3)(ii)(A)-(F))– Foreign law permits one person to surrender a loss to another person under a group relief or

loss-sharing regime.– Foreign law requires a shareholder of a corporation to include in income amounts g q p

attributable to taxes imposed on the corporation with respect to distributed earnings pursuant to an integrated corporate tax system, and allows the shareholder a credit for the taxes.

– Foreign law requires a shareholder to include income attributable to an interest in a corporation under an anti-deferral regime (i e similar to Subpart F)corporation under an anti-deferral regime (i.e., similar to Subpart F).

– Foreign law reallocates income from one person to a related person under transfer pricing rules.

– Foreign law requires a person to take into account its distributive share of taxable income f i h i fi f f i ( hi )of an entity that is fiscally transparent for foreign tax purposes (e.g., a partnership).• This includes where the entity is treated as a corporation for U.S. tax purposes (i.e., a

reverse hybrid).• A reverse hybrid, however, does not include an entity that is treated as a branch or as

19

y , , yfiscally transparent solely for purposes of calculating the combined income of a foreign consolidated group.

Technical Taxpayer Rules:i i i i

• If foreign tax is imposed on the combined income of two or more persons, foreign law is considered to impose legal liability on each person for the amount of tax

Determining A Person’s Portion Of Combined Income

p g y pattributable to the person’s portion of the foreign tax base (§1.901-2(f)(3)(i)).

• Combined income subject to tax exemption or preferential tax rates is computed separately, and the tax on that combined income base is allocated separately (§1.901-2(f)(3)(i))2(f)(3)(i)).

• Determining a person’s portion of combined income (§1.901-2(f)(3)(iii)(A))– If a return, schedule or other document is filed or maintained for foreign tax

purposes and it shows the person’s income then the person’s portion of combinedpurposes, and it shows the person s income, then the person s portion of combined income is determined by reference to that document.

– If no such document is filed or maintained, then the person’s income is determined from the books of accounts maintained for purposes of computing the person’s p p p g ptaxable income for foreign tax purposes.

• A person’s portion of the combined income is adjusted to give effect to inter-company payments that are deductible under foreign law (interest, rents, royalties, etc.), even if h li i d d f i lid i i (§ 1 901 2(f)(3)( ))

20

the payments are eliminated under a foreign consolidation regime (§ 1.901-2(f)(3)(B)).– Payments that are not deductible under foreign law (e.g., inter-company dividends,

deemed distributions) are not taken into account, however (§1.901-2(f)(3)(B)).

Technical Taxpayer Rules:Example – Inter-Company Payments

• In year 1, C pays 50u of interest to B.• The separate income of B and C reported

th i C t X h d l f 1 dA

(U.S.) on their Country X schedules for year 1 do not reflect the 50u intercompany interest payment.

• The combined income reported for country

( )

The combined income reported for country X purposes is 300u, and Country X imposes 90u of taxes (300u x 30%).

• 45u of the Country X taxes are considered

B(Country X)

50u

E&P 100uInt 50u

150u

paid by each of B and C (but for the interest payment; the Country X taxes would be considered paid 60u by C and 30u by B).

C

50u

Interest

C(Country X)

E&P 200uInt (50u)

150u

21

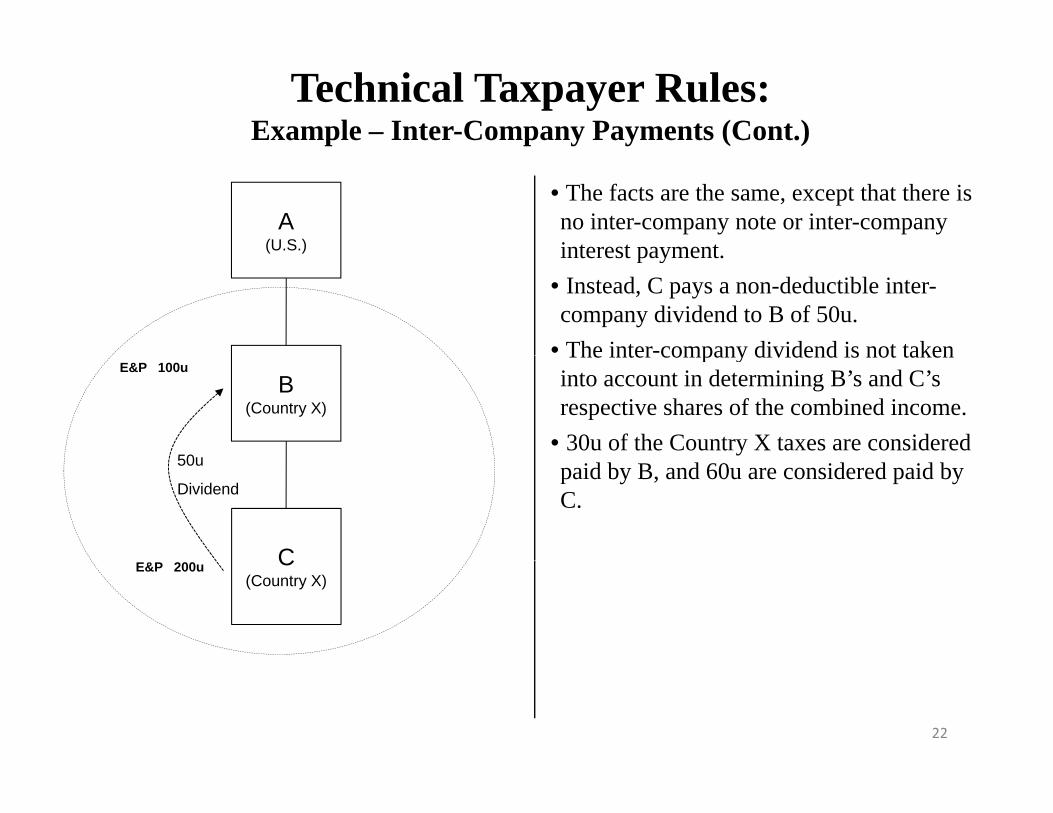

Technical Taxpayer Rules:Example – Inter-Company Payments (Cont.)

• The facts are the same, except that there is no inter-company note or inter-company interest payment

A(U.S.) interest payment.

• Instead, C pays a non-deductible inter-company dividend to B of 50u.

• The inter-company dividend is not taken

( )

The inter company dividend is not taken into account in determining B’s and C’s respective shares of the combined income.

• 30u of the Country X taxes are considered

B(Country X)

50u

E&P 100u

paid by B, and 60u are considered paid by C.

C

50u

Dividend

C(Country X)

E&P 200u

22

Technical Taxpayer Rules:

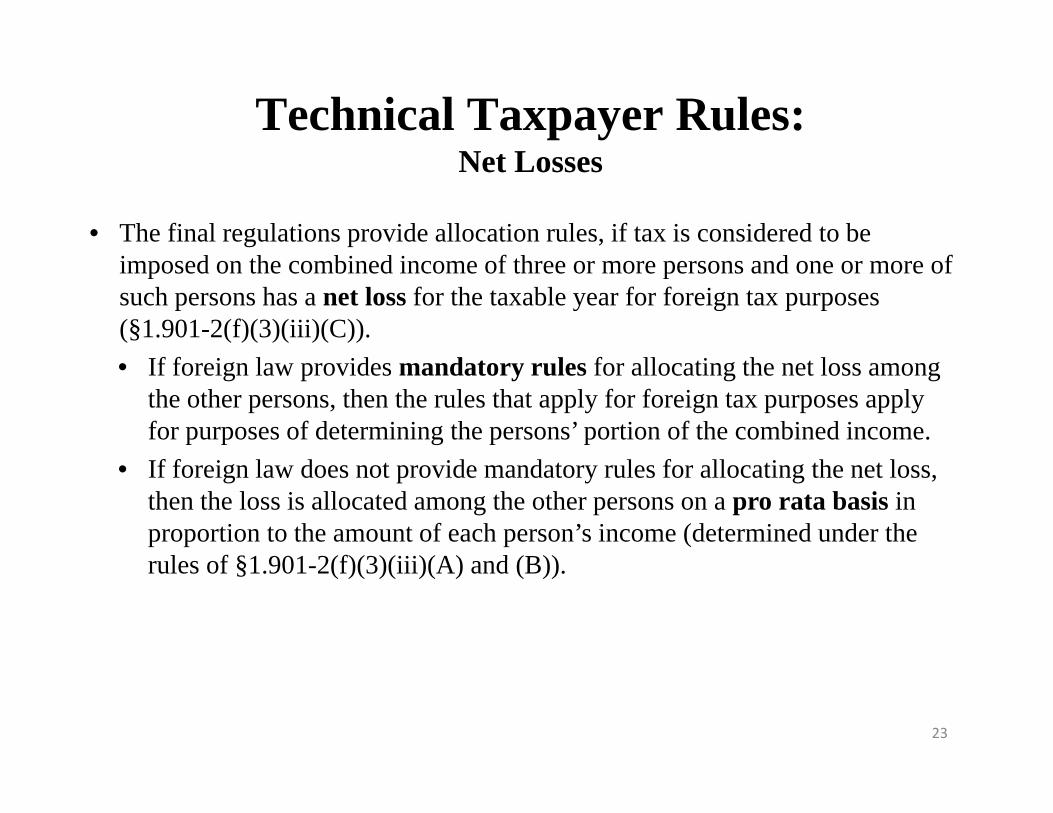

• The final regulations provide allocation rules, if tax is considered to be

Net Losses

imposed on the combined income of three or more persons and one or more of such persons has a net loss for the taxable year for foreign tax purposes (§1.901-2(f)(3)(iii)(C)).• If foreign law provides mandatory rules for allocating the net loss among

the other persons, then the rules that apply for foreign tax purposes apply for purposes of determining the persons’ portion of the combined income.

• If foreign law does not provide mandatory rules for allocating the net loss, then the loss is allocated among the other persons on a pro rata basis in proportion to the amount of each person’s income (determined under the

l f §1 901 2(f)(3)(iii)(A) d (B))rules of §1.901-2(f)(3)(iii)(A) and (B)).

23

Technical Taxpayer RulesExample – Net Losses

• In Year 1, B has income of 100u, C has income of 200u, and D has a net loss of (60u)

A(U.S.)

(60u).• Country X imposes tax of 72u (240u x 30%) on the group.

• Country X does not provide mandatoryE&P 100u Country X does not provide mandatory rules for allocating D’s loss, so it is allocated among B and C proportionally according to their respective income.

B(Country X)

E&P 100u

• (20u) of loss is allocated to B ((60u) x (100u/300u)), and (40u) is allocated to C.

• Thus, B’s portion of the combined income i 80 (100 20 ) d C’ ti i 160

C Dis 80u (100u – 20u), and C’s portion is 160u (200u – 40u).

• B is considered to have paid 24u of Country X tax (72u * (80u/240u)), and C is

(Country X) (Country X)

E&P (60u)E&P 200u

2424

X tax (72u (80u/240u)), and C is considered to have paid 48u of Country X tax.

Technical Taxpayer Rules:P t hi A d Di d d E titiPartnerships And Disregarded Entities

• If foreign law imposes tax at the entity level on income of a partnership (i.e., a hybrid partnership) then the partnership is considered to be legally liable forhybrid partnership), then the partnership is considered to be legally liable, for purposes of the technical taxpayer rules (§1.901-2(f)(4)(i)).

• If foreign law imposes tax at the entity level on income of a disregarded entity (i.e., a hybrid disregarded entity), then the person treated as owning the assets of the disregarded entity, for U.S. tax purposes, is considered legally liable (§1.901-disregarded entity, for U.S. tax purposes, is considered legally liable (§1.9012(f)(4)(ii)).

• The final regulations provide rules for allocating foreign taxes if a partnership’s U.S. taxable year ends, or if there is a change in ownership in a partnership or disregarded entity, and the foreign taxable year of entity does not end (§1.901-2(f)(4)).y g y y (§ ( )( ))– The allocations of foreign taxes incurred for the foreign taxable year in which the

event occurs are made under the principles of §1.1502-76(b).– The allocations are based on the respective portions of the taxable income of the

hybrid entity, as determined under foreign law for the foreign taxable year that are y y, g g yattributable to the period ending on the relevant date and the period ending after such date.

– This is consistent with §1.338-9(d), which governs the apportionment of foreign taxes paid by a target corporation acquired in a transaction treated as an asset

i i i f U S b f hi h h f i bl f h

25

acquisition for U.S. tax purposes, but for which the foreign taxable year of the target does not close.

Technical Taxpayer Rules:P t hi A d Di d d E titi (C t )Partnerships And Disregarded Entities (Cont.)

• Transactions to which these allocation rules can applyA con ersion of a partnership to a disregarded entit in hich case the foreign– A conversion of a partnership to a disregarded entity, in which case the foreign tax is allocated between the partnership and the owner of the disregarded entity

– A termination of a partnership under Sect. 708(b)(1)(A) (actual termination from the cessation of business activities) or Sect. 708(b)(1)(B) (technical termination from a sale of more than 50% of the partnership interests within a 12 month-from a sale of more than 50% of the partnership interests within a 12 month-period)

• In the case of a termination under Sect. 708(b)(1)(B), the foreign tax is allocated between the “old” partnership and the “new” partnership.

– A transfer of a partnership interest or other variance in the ownership of the– A transfer of a partnership interest or other variance in the ownership of the partnership during the year, likely including a change in ownership resulting from a Sect. 721 contribution or Sect. 731 distribution

– A transfer of the interests in a disregarded entityA conversion of a disregarded entity to a partnership– A conversion of a disregarded entity to a partnership

• If multiple events occur during the year, then these rules are applied to each event successively.

• Foreign tax allocated to a terminating partnership is treated as paid or accrued by the partnership on the last day of its final U S taxable year

26

partnership on the last day of its final U.S. taxable year.

Technical Taxpayer Rules:Example – Technical Termination Of Partnership

• On Sept. 30 of Year 1, A sells its 50% interest in D to C, resulting in a termination of the partnership under Sect. 708(b)(1)(B), for U.S. tax purposes.

• As a result of the termination, “old” D’s taxable year closes on Sept. 30 of Year 1 for U.S. tax purposes, and “new” D has a short U.S. taxable year, beginning on Oct. BA

A sells interest in Don September 30

C y , g g1 and ending on Dec. 31 of Year 1.

• The sale of A’s interest does not close D’s taxable year, for country M tax purposes. D h 400 f t bl i f it f i t bl

B(U.S.)

50%

A(U.S.)

50% 50%

C(U.S.)

• D has 400u of taxable income for its foreign taxable year ending Dec. 31, Year 1, with respect to which country M imposes 120u of income tax.

• The 120u of Country M tax must be allocated to the DI 400 period from Jan. 1-Sept. 30 and the period from Oct. 1-

Dec. 31, based on the principles of §1.1502-76(b).(Country M) Income 400u

Tax 120u (400u * 30%)

27

Technical Taxpayer Rules:C Wh O P P T Of A thConsequences When One Person Pays Taxes Of Another

• The final regulations indicate that U.S. tax principles apply to determine the tax consequences if one person remits a tax that is the legal liability oftax consequences, if one person remits a tax that is the legal liability of another person.– For example, a payment of tax for which a corporation has legal liability

by a shareholder will ordinarily result in a deemed capital contribution d d d t f t b th tiand deemed payment of tax by the corporation.

– Under a similar rationale, a payment of tax for which a shareholder has legal liability by a corporation will typically result in a deemed distribution and a deemed payment of tax.p y

• It should be possible to avoid such consequences, if a shareholder pays a corporation’s tax and a corporation reimburses the shareholder for paying its tax liability pursuant to a lending or agency arrangement.

28

Technical Taxpayer Rules:T iti ITransition Issues

• The preamble to the final regulations states that it is clear under current law that the person who paid or accrued foreign income taxes in a pre effectivethat the person who paid or accrued foreign income taxes in a pre-effective date year is the person who is eligible under Sect. 904(c) to carry forward such taxes to a post-effective date year; notwithstanding that such person may not be considered the taxpayer under the final regulations, had the taxes been paid or accrued in the post effective date carryover yearpaid or accrued in the post-effective date carryover year.

• Similarly, the preamble states that the person who paid or accrued foreign income taxes in a post-effective date year is the person who is eligible under Sect. 904(c) to carry back such taxes to the last pre-effective date year.

• The final regulations permit taxpayers to apply the combined income rules of §1.901-2(f)(3) of the final regulations to taxable years beginning after Dec. 31, 2010, and on or before Feb. 14, 2012.– This provision permits taxpayers to avoid uncertainty regarding theThis provision permits taxpayers to avoid uncertainty regarding the

application of Sect. 909 to foreign taxes paid or accrued by foreign consolidated groups in pre-effective date taxable years beginning in 2011 and 2012.

29

Technical Taxpayer Rules:T iti I (C t )Transition Issues (Cont.)

• The preamble to the final regulations expressed concern regarding potential whipsaws when multiple persons claim a foreign tax credit for a singlewhipsaws, when multiple persons claim a foreign tax credit for a single payment of foreign income tax where different persons are considered to pay the tax under the final regulations and under prior law.

• To prevent treating more than one person as paying a single amount of tax, §1.901-2(f)(4) (governing foreign taxes for which partnerships and disregarded entities are legally liable) will not apply to any amount of tax paid or accrued in a post-effective date year of any person, if such tax would p p y y p ,be treated as paid or accrued by a different person in a pre-effective date year under the prior regulations.

30

TEMPORARY SECT. 909 Peter Daub, Baker & McKenzie

9 9REGULATIONS: SPLITTER ARRANGEMENTSARRANGEMENTS

Temporary Sect. 909 Regulations: Splitter Arrangements

– Sect 909 extends to include S corporations and taxes paid or accrued by

ArrangementsScope

Sect. 909 extends to include S corporations and taxes paid or accrued by persons other than Sect. 902 corporations.

– Sect. 909 applies at the partner level, and similar rules apply for S corporations and trusts.p

– Splitter arises if the related income “was, is or will be” taken into account for U.S. tax purposes by a covered person.

– Similar to Notice 2010-92, the temporary regulations provide an exclusive list Similar to Notice 2010 92, the temporary regulations provide an exclusive list of arrangements that give rise to splitters:

• Reverse hybrid splitter arrangements

• Loss-sharing splitter arrangements• Loss sharing splitter arrangements

• Hybrid instrument splitter arrangements

• Certain partnership tracker arrangements

32

– No “new” splitters were introduced, although the scope of the rules has been expanded.

Effective Dates

• Foreign taxes paid or accrued by Sect 902 corporation in taxable • Foreign taxes paid or accrued by Sect. 902 corporation in taxable years beginning on or before Dec. 31, 2010

― See Notice 2010-92, incorporated in Treas. Reg. §1.909-6T.

• Foreign taxes paid or accrued in taxable years beginning on Jan. 1, 2011 and before Jan. 1, 2012

― Splitters described in Notice 2010-92 apply (regardless of whether p pp y ( gforeign taxes are paid by Sect. 902 corporation).

― Partnership inter-branch payment splitters in Treas. Reg. §1.909-2T(b)(4) apply.2T(b)(4) apply.

― Rules for split taxes in Treas. Reg. §1.909-3T(b) apply.

― Until further notice, related income “pro rata” method (but not

33

the “related income first” method) and split taxes rules in Notice 2010-92 apply.

Effective Dates (Cont.)

• Foreign taxes paid or accrued in taxable years beginning on Jan. 1, 2012 and before Feb. 14, 2012

― In general, the 2012 temporary regulations (including the exclusive splitters in Treas. Reg. §1.909-2T(b)) apply.

― However, the foreign consolidated group splitter in Notice 2010-92 applies, such that an arrangement is a splitter unless the foreign tax is apportioned under the principles of Treas. Reg. §1.901-2(f)(3), revised as of April 1 2011 (taxpayers can also choose to apply the final version of of April 1, 2011 (taxpayers can also choose to apply the final version of Treas. Reg. §1.901-2(f)(3)).

• Foreign taxes paid or accrued in taxable years on or after Feb. 14, 2012

Th 2012 l i (i l di h l i li i T ― The 2012 temporary regulations (including the exclusive splitters in Treas. Reg. §1.909-2T(b)) apply.

― The 2012 technical taxpayer final regulations apply; failure to properly apply these rules to a foreign consolidated group results in a splitter

34

apply these rules to a foreign consolidated group results in a splitter.

Temporary Sect. 909 Regulations – Splitter Arrangements

• Substantially identical to Notice 2010-92; Reverse Hybrid Structures(Sec 4 02 of Notice 2010–92)

Arrangements Reverse Hybrid Splitter Arrangements—Treas. Reg. §1.909‐2T(b)(1)

Substantially identical to Notice 2010 92; extended to cover taxes paid or accrued by persons other than Sect. 902 corporations

• The split taxes are the foreign taxes paid or accrued on income of the reverse hybrid

USP USP

(Sec. 4.02 of Notice 2010 92)

accrued on income of the reverse hybrid.

• The “related income” is the U.S. E&P of the reverse hybrid attributable to the activities of the reverse hybrid that gave rise to the

h h h h l f

orFHCFHC

income with respect to which the split foreign taxes were paid or accrued.

• Splitter exists even if the reverse hybrid has a loss or deficit in E&P, for U.S. tax purposes

LPLocal: Partnership

US: Corporation DE 1

(e.g., due to timing difference). DE 1 LP

35

Temporary Sect. 909 Regulations – Splitter Arrangements Arrangements

Foreign Consolidated Groups—Treas. Reg. §1.909‐5T(b), 6T(b)(2)

• Notice 2010-92 pre-2011 splitter category

• For taxable years beginning after Dec. 31, 2010 and on or For taxable years beginning after Dec. 31, 2010 and on or before Feb. 14, 2012, taxpayers may choose between:1. Allocation under the final Sect. 901 technical taxpayer

regulations, or 2 A li ti f th N ti 2010 92 litt l2. Application of the Notice 2010-92 splitter rules.

• For taxable years beginning after Feb. 14, 2012: Taxes are allocated under the final Sect. 901 technical taxpayer regulations, allocated under the final Sect. 901 technical taxpayer regulations, so splitter no longer occurs.

36

Temporary Sect. 909 Regulations – Splitter Arrangements Arrangements

Foreign Consolidated Groups—Treas. Reg. § 1.909‐5T(b), 6T(b)(2)

• Foreign consolidated group: Exists when a foreign country imposes tax on the combined income of two or more entities, whether through consolidation or attribution of income

US Parentthrough consolidation or attribution of income

• Splitter arrangement: Exists to the extent that the payor of taxes did not allocate the foreign consolidated tax liability among the members

Sect. 902Corp’n

(Country A)consolidated tax liability among the members of the consolidated group based on each member’s share of the consolidated taxable income― Sect. 909 applies even if the payor of taxes

Sect. 902Corp’n

(Country A)

Sect. 902Corp’n

(Country A)pp p yhas a deficit in E&P for a particular year.

37

Temporary Sect. 909 Regulations – Splitter Arrangements Arrangements

Foreign Consolidated Groups—Treas. Reg. § 1.909‐5T(b), 6T(b)(2)

• Pre-2011 split taxes: Taxes paid or accrued by one member of the foreign consolidated group that are imposed on a covered person’s share of the consolidated taxable income

US Parentshare of the consolidated taxable income included in the foreign tax base

• Related income: The E&P of such other member attributable to the activities of that other member that gave rise to income

Sect. 902Corp’n

(Country A)

Liability for foreign tax on consolidated group income

Incomeg

included in the foreign tax base, with respect to which the pre-2011 split taxes were paid or accrued

Sect. 902Corp’n

(Country A)

Sect. 902Corp’n

(Country A)

group income

Income Income

38

Technical Taxpayer Rules:p yGeneral Rule

• Tax is considered paid by the person who has legal liability under foreign law for the tax.

• Treasury and the Service are still considering whether and easu y a d t e Se v ce a e st ll co s de g w et e a d to what extent to revise or clarify the general rule.

• For example, whether there should be a special rule for determining who has legal liability in the case of a determining who has legal liability in the case of a withholding tax imposed on an amount of income that is considered received by different persons for U.S. and f i t ( i th f t i “ ” foreign tax purposes (e.g., in the case of certain “repo” transactions)

39

Technical Taxpayer Rules:Taxes Imposed On Combined Income

• Prop Reg Sect 1 901-2(f)(2) addressed application of legal liability rule to

pApplication Of Legal Liability Rule

Prop. Reg. Sect. 1.901 2(f)(2) addressed application of legal liability rule to foreign consolidated groups and other combined income regimes:

• When the regime imposes joint and several liability in the U.S. sense

• When the regime treats subs as branches of the parent corp (or otherwise g p p (attributes income of subs to the parent), OR

• When some of the group members have limited obligations, or even no obligation, to pay the consolidated tax.

• Prop. Reg. Sect. 1.901-2(f)(2)(i) provided that the foreign tax must be apportioned among the persons whose income is included in the combined base pro rata, based on each person’s portion of the combined income as computed under foreign law. computed under foreign law.

• Treas. Reg. Sect. 1.901-2(f)(3)(i) adopts Prop. Reg. Sect. 1.901-2(f)(2)(i) with minor modifications.

• Thus, a foreign tax credit splitting event will not occur with respect to

40

foreign taxes paid or accrued on combined income during tax years beginning after Feb. 14, 2012.

Technical Taxpayer Rules:Taxes Imposed on Combined Income

• However with respect to foreign income taxes paid or accrued on

pApplication of Legal Liability Rule (Cont.)

• However, with respect to foreign income taxes paid or accrued on combined income during taxable years beginning after Dec. 31, 2010 and on or before Feb. 14, 2012, temporary regulations under Sect. 909 provide that an FTC splitting event occurs to the extent that a 9 9 p C p gtaxpayer does not allocate the foreign consolidated tax liability among the members of the foreign consolidated group based on each member’s share of the consolidated taxable income included in the foreign tax base, under the principles of Prop. Reg. Sect. 1.901-2(f)(3) prior to its amendment by the final regulations.

• Note that under the final regulation, combined income subject to tax exemption or preferential tax rates is computed separately, and the tax on that combined income base is allocated separately. Treas. Reg. Sect. 1.901-2(f)(3)(i)

41

Technical Taxpayer Rules:Taxes Imposed On Combined Income

U d th fi l l ti t i id d t d

p“Tax Computed On A Combined Basis”

• Under the final regulations, tax is considered computed on a combined basis if two or more persons that would otherwise be subject to foreign tax on their separate taxable incomes add their items of income, gain, deduction and loss to compute a single consolidated taxable income amount, for foreign tax purposes.

• Foreign tax is not considered to be imposed on the combined income of two or more persons if because one or more of such income of two or more persons if, because one or more of such persons is a fiscally transparent entity under foreign law, only one of such persons is subject to tax under foreign law (even if two or more of such persons are corporations for U S federal

42

two or more of such persons are corporations for U.S. federal income tax purposes).

Technical Taxpayer Rules:Taxes Imposed On Combined Income

• Therefore, foreign tax is not considered imposed on combined income solely because foreign la :

p“Tax Computed On A Combined Basis” (Cont.)

law:A. Permits one person to surrender a loss to another person pursuant to a group relief or

other loss-sharing regimeB. Requires a shareholder of a corporation to include in income amounts attributable to

taxes imposed on the corporation with respect to distributed earnings pursuant to an taxes imposed on the corporation with respect to distributed earnings, pursuant to an integrated tax system that allows the shareholder a credit for such taxes

C. Requires a shareholder to include, pursuant to an anti-deferral regime, income attributable to the shareholder’s interest in the corporation

D Reallocates income from one person to a related person under foreign transfer pricingD. Reallocates income from one person to a related person under foreign transfer pricingprovisions

E. Requires a person to take into account a distributive share of taxable income of an entity that is a partnership or other fiscally transparent entity for foreign tax purposes, ORO

F. Requires a person to take all or part of the income of an entity that is a corporation for U.S. tax purposes into account, because foreign law treats the entity as a branch or fiscally transparent entity (a reverse hybrid).― A reverse hybrid does not include an entity that is treated under foreign law as a

43

y y gbranch or fiscally transparent entity solely for purposes of calculating combined income of a foreign consolidated group.

Temporary Sect. 909 Regulations –Splitter Arrangements Splitter Arrangements

Partnership Allocation Splitter—Treas. Reg. §1.909‐2T(b)(4)

• Not a Notice 2010-92 pre-2011 splitter category; old Sect. 704(b) regulations apply

T bl b i i ft D 31 2010 d • Taxable years beginning after Dec. 31, 2010 and on or before Feb. 14, 2012: Old Sect. 704(b) regulations apply, but also subject to treatment as splitter arrangement under temporary Sect. 909 regulationstemporary Sect. 909 regulations

• Taxable years beginning after Dec. 31, 2011: Temporary Sect. 704(b) regulations apply, except for taxes derived from ( ) g pp y, ppartnerships whose agreements were entered into before Feb. 14, 2012. ― Taxes derived from pre-Feb. 14, 2012 partnerships are

bj t t S t 909 l ti litt l

44

subject to Sect. 909 regulation splitter rules.

Temporary Sect. 909 Regulations –Splitter Arrangements Splitter Arrangements

Partnership Allocation Splitter—Treas. Reg. § 1.909‐2T(b)(4)

• Notice 2010-92 observed that allocations that meet the requirements of the Sect. 704(b) regulations relating to partnership items can result in allocations of a partnership’s creditable foreign tax expenditures (CFTEs) and related creditable foreign tax expenditures (CFTEs) and related income to different partners.

• Although the notice did not treat these allocations as foreign Although the notice did not treat these allocations as foreign tax credit splitting events, both the temporary Sect. 704(b) regulations issued as part of the same package as the Sect. 901 regulations and the Sect. 909 regulations themselves, in their different ways and for different periods prospectively different ways and for different periods, prospectively eliminate the benefits of such allocations.

45

FTC Splitting Events – Sect. 704(b)CFTEs – Old And New Examples

A BOld Example

75k M 25K M

24(i) And (ii) A B

A B

AB

75k – M25k – N100k

7,500 – X12,500 – Y

25K – M25k – N50k

2,500 – X12,500 – Y

incomeincome

taxAB

DE1 DE2 N

20,000 15,000

ETR = 20% ETR = 30%100k 50k

DE1(M)

DE2N

M –40%

N –20%

75,000

New Example

75k – M25k – N100k

25k – M25k – N50k

incomeincome

Country X

100k – income

<75k>

25k TI

Country Y

50k – income

75k

125k TI

7,500 – X11,250 – Y5,000 – Y

23,750

2,500 – X3,750 – Y5,000 – Y

11,250

tax

4646

25k TI

10k Tax

125k TI

25 k TaxETR = 23.75% ETR = 22.50%

FTC Splitting Events –p gSect. 704(b), Cont.

CFTEs Old and new examples 24(i) and (ii)CFTEs – Old and new examples 24(i) and (ii)

• Country X imposes a 40% tax on Business M income. and Country Y imposes a 20% tax on Business N income.Under the AB partnership agreement partnership items from • Under the AB partnership agreement, partnership items from Business M are allocated 75% to A and 25% to B.

• Partnership items from business N are allocated 50/50.I ld b t t l th ll ti i l d B i • In old, but not new, example these allocations include Business M and Business N CFTEs, respectively.

• Under § .704-1(b)(4)(vii)(c)(2), net income attributable to M and N are separate CFTE categories because the partnership and N are separate CFTE categories, because the partnership agreement provides for different allocations of the net income attributable to businesses M and N.

4747

FTC Splitting Events –gSect. 704(b), Cont.

CFTEs – Old and new examples 24(i) and (ii), Cont.CFTEs Old and new examples 24(i) and (ii), Cont.

• Under §1.704-1(b)(4)(viii)(c)(3), the $100,000 of net income attributable to Business M is in the Business M CFTE category, and the $50,000 of net income attributable to Business N is in the Business N CFTE category.

• Under §1.704-1(b)(4)(viii)(d)(1), the $10,000 of Country X tax is allocated to the M CFTE category, and $10,000 of Y tax is allocated to the N CFTE category because the income in those respective to the N CFTE category, because the income in those respective categories is included in the respective bases upon which foreign tax is imposed.

4848

FTC Splitting Events –gSect. 704(b), Cont.

CFTEs Old and new examples 24(i) and (ii) ContCFTEs – Old and new examples 24(i) and (ii), Cont.

• Under old §1.704-1(b)(4)(viii)(d)(3), the additional $15,000 of Country Y tax is allocated to the N CFTE category, because that category includes the items attributable to the relevant that category includes the items attributable to the relevant activities of the recipient branch. Because the partnership agreement allocates this tax in the same proportion (50/50) as the allocation of the income in the business N CFTE category, it is respected as in accordance with the partners’ interests in it is respected as in accordance with the partners interests in the partnership.

• With the elimination of § .704-1(b)(4)(viii)(d)(3), the additional $15,000 must be allocated under §1.704-$ , §1(b)(4)(viii)(d)(1) to the M CFTE category, because the related $75,000 of income that Country Y taxes is in the business M CFTE category. Accordingly, the tax must be allocated in the same proportion (75/25) as the allocation of the income in the

4949

same proportion (75/25) as the allocation of the income in the Business M category.

FTC Splitting Events – 704(b)CFTEs – Example 24(iii)CFTEs – Example 24(iii)

37.50 – M18.75 – M

income

Facts37.50 – M6.25 – M

A B25k – N81.25 - Total

7.5k – X12.5k – Y20k Total

income

tax

• Assume the same facts as Example 24 (i) and (ii), except that under the partnership agreement, the $75k inter‐branch payment is reflected by allocating $75k of M income 50/50 among the partners.

25k – N68.75 - Total

2.5k – X12.5k – Y15k Total

income

tax

AB

20k – Total

ETR 24.6%

partners.• Under §1.704‐1(b)(4)(viii)(c)(2)(iii), the $75k payment is treated as a divisible part of the Business M activity and, therefore, a separate activity.

15k – Total

ETR 21.8%

DE1 DE2

Country X

100k – income

<75k>

Country Y

50k – income

75k

100k 50k• Under §1.704‐1(b)(4)(viii)(c)(2)(i), the disregarded payment activity and the Business N activity are treated as a single CFTE category, because both are shared equally.

• Under §1 704‐1(b)(4)(viii)(d)(1) the $10k countryDE1(M)

DE2N

75,000

25k TI

10k Tax

125k TI

10k Tax

Under §1.704 1(b)(4)(viii)(d)(1), the $10k country X tax is allocated to the M CFTE category, and all $25k of Country Y tax is allocated to the N CFTE category.

• The Country X tax is allocated 75/25 to A and B, th i bj t t C t X t

5050

the same as income subject to Country X tax.• The Country Y tax is allocated 50/50 to A and B, the same as income subject to Country Y tax.

Temporary Sect. 909 Regulations –Splitter Arrangements Splitter Arrangements

U.S. Equity Hybrid Instrument Splitter Arrangements—Treas. Reg. §1.909‐2T(b)(3)(i)

• Substantially identical to Notice 2010-92; Hybrid Instrument Structures(Sec 4 05 of Notice 2010–92)

USP

Substantially identical to Notice 2010 92; extended to cover taxes paid or accrued by persons other than Sect. 902 corporations

• Split taxes are the additional foreign taxes paid or accrued by the owner of hybrid

(Sec. 4.05 of Notice 2010 92)

Interest income for foreign Holdco

(h ld )

paid or accrued by the owner of hybrid instrument, because it is subject to foreign tax on income from the instrument.

• “Related income” includes payments or accruals giving rise to split taxes that are

Deduction for

gpurposes (holder)

OUS: Equity

accruals giving rise to split taxes that are deductible by the issuer, for foreign tax purposes.

• Includes a U.S. equity instrument with respect to which the issuer is entitled to a foreign tax Deduction for

foreign tax purposes

Opco (issuer)

q yForeign: Debt

Operating income remains in Opco for U.S. tax purposes

to which the issuer is entitled to a foreign tax deduction for amounts paid or accrued with respect to the instrument, regardless of whether it is debt for foreign tax purposes(e g notional interest deduction)

51

tax purposes (e.g., notional interest deduction)

Temporary Sect. 909 Regulations – Splitter Arrangements Arrangements

U.S. Debt Hybrid Instrument Splitter Arrangements—Treas. Reg. §1.909‐2T(b)(3)(ii)

• Substantially identical to Notice 2010-92; Hybrid Instrument Structures(Sec 4 05 of Notice 2010–92) Substantially identical to Notice 2010 92;

extended to cover taxes paid or accrued by persons other than Sect. 902 corporations

• Split taxes are the foreign taxes paid or accrued by the issuer on the income that

USP

(Sec. 4.05 of Notice 2010 92)

accrued by the issuer on the income that would have been offset by the interest paid or accrued on the instrument, had the interest been deductible for foreign tax purposes.

“R l d ” h f

Dividend income for foreign tax purposes; interest income and E&P increase for

Holdco (holder)

• “Related income” is the gross amount of interest income recognized by the instrument owner for U.S. tax purposes.

• Includes any instrument that is treated as Dividend distribution for foreign tax purposes; interest

E&P increase for U.S. tax purposes

(holder)

Opcoequity for foreign tax purposes but as debt for U.S. federal income tax purposes

purposes; interest expense and E&P deduction for U.S. tax purposes

Opco (issuer) US: Debt

Foreign: Equity

52

Temporary Sect. 909 Regulations – Splitter A t

• A “U.S. combined income group” includes:U.S. combined group

Arrangements Loss‐Sharing Splitter Arrangements—“U.S. Combined Income Group”

A U.S. combined income group includes:

― A single individual or corporation (U.S. or foreign)

― All entities beneath the individual or US Sub

USP*Assume USP and US Sub are consolidated

corporation that combine items of income, deduction, gain or loss, for U.S tax purposes, with such individual or corporation

UK HoldcoU.S. combined group

― A U.S. consolidated group is deemed to be a single corporation; individuals filing a joint return are treated as a single individual.

UK DE1 UK CFC

• U.S. combined group income consists of aggregate taxable income of members with positive taxable income, as computed under foreign law.

UK DE2

U.S. combined group

UK Hybrid

U.S. combined group

53

foreign law.

Temporary Sect. 909 Regulations – Splitter A t

• Notice 2010-92 applied only to shared Loss Surrender Structures(Sec 4 04 of Notice 2010 92)

Arrangements Loss‐Sharing Splitter Arrangements—Treas. Reg. §1.909‐2T(b)(2)

pp ylosses attributable to disregarded debt; the temporary regulations are much broader.

• A “loss-sharing splitter arrangement” is extended to include an arrangement

USP

(Sec. 4.04 of Notice 2010–92)

extended to include an arrangement arising under a foreign group relief or other loss-sharing regime, to the extent a shared loss of a “U.S. combined income group” could have been used to offset income of that group (a “usable

UK Holdco

offset income of that group (a usable shared loss”) but is used instead to offset income of another U.S. combined income group.

• Split taxes are the foreign taxes on UK DE1 UK CFC

$30 Tax on Interest

p gincome equal to the “usable shared loss” that is offset.

• “Related income” is the income of a U.S. combined income group that is offset by the usable shared loss of

$100 Interest

UK DE2

54

offset by the usable shared loss of another U.S. combined income group.

Temporary Sect. 909 Regulations – Splitter Arrangements

• Under §1.909-2T(b)(2)(ii), the loss-USP

Arrangements Loss‐Sharing Splitter Arrangements—Treas. Reg. §1.909‐2T(b)(2) Ex. 1

§ ( )( )( ),sharing with CFC3 is not taken into account. Instead, under §1.909-2T(b)(2)(iii)(B), DE’s 100u loss reduces CFC2’s E&P.

• A splitter arrangement occurs CFC1 EP – 0u • A splitter arrangement occurs

because the 50u usable shared loss of the CFC2 U.S. combined income group was used instead to offset income of CFC3, which is included in the CFC3 U S combined income CFC2 CFC3

(A)

E&P – 200uE&P 50u the CFC3 U.S. combined income group.

• Under §1.909-2T(b)(2)(iv), the split taxes are the 15u of Country A income taxes paid by CFC2 and under

CFC2(A)

CFC3(A)

<100u>TI – 100u

Tax – 30uE&P – 200u

Tax – 30u170u

E&P – 50uTax – 15u

35u<100u><65u>

p y§1.909-2T(b)(2)(v), the related income is the 50u of CFC3’s income that equals the amount of income of the CFC3 U.S. combined income group that was offset by the usable

DE(A)

Combined group

170u

E&P - <100u>

55

shared loss of the CFC2 U.S. combined income group.

Country A Group30% Tax Rate

Temporary Sect. 909 Regulations – Splitter Arrangements

• Under §1.909-2T(b)(2)(iii)(B), the shared loss of the CFC2 U S bi d i g i th 100 l

USP

Arrangements Loss‐Sharing Splitter Arrangements—Treas. Reg. §1.909‐2T(b)(2) Ex. 2

CFC2 U.S. combined income group is the 100u loss incurred by DE that is used to offset 100u of HP1’s income. Under §1.909-2T(b)(2)(i), the usable shared loss of the CFC2 U.S. combined income group is 100u.

• The shared loss of the CFC2 combined group offsets 100u Country B income of HP1 The shared loss is

CFC1(B)

EP – 0u100u Country B income of HP1. The shared loss is treated as offsetting 50u of the CFC2 U.S. combined group’s income and 50u of the CFC3 U.S. combined income group’s income.

• It is a splitter arrangement, because 50u of the 100u usable shared loss of the CFC2 U S combined group

CFC2 CFC3

(B)

EP – 0uHP1 – 100uHP1 tax <15u>

E&P – 100uHP1 – 100uDE <100u> usable shared loss of the CFC2 U.S. combined group

was used to offset income of the CFC3 U.S. combined group. Under §1.909-2T(b)(2)(iv), the split taxes are the 15u of Country B tax paid by CFC2 on 50u income, which is equal to the amount of the CFC2 U.S. combined income group’s usable shared loss that was

(B) (B)

DE

50% 50%

HP1

HP1 tax - <15u>85u

DE - <100u>HP1 tax - <15u>

CFC2 tax - <30u>55u

E&P 20E&P <100u> combined income group s usable shared loss that was used to offset income of another U.S. combined income group. Under §1.909-2T(b)(2)(v), the related income is the 50u of CFC3’s income that was offset by the usable shared loss of the CFC2 U.S. combined income group.

DE(B)

HP1(B)

E&P – 20ouDE – <100u>Tax – 30u

E&P - <100u>

56

g p

Country B Group - 30% Tax RateCountry B’s loss-sharing regime allows a loss of one entity may offset

the income of one or more of the others

Temporary Sect. 909 Regulations –Splitter Arrangements p gArrangements Not Covered

T ti t th t t FTC litti t• Transactions or arrangements that are not FTC splitting events:― Incorporation of partnership or disregarded entity ― Inclusion in income under foreign anti-deferral regime

Covered asset acquisitions described in Sect 901(m)― Covered asset acquisitions described in Sect. 901(m)

• Preamble indicates Treasury and the Service are considering whether other transactions could constitute FTC splitting p gevents (e.g., distribution subject to foreign withholding tax but that is disregarded for U.S. tax purposes)― Would apply on prospective basis only

57

TEMPORARY SECT. 909 John Bates, Ivins Phillips & Barker

9 9REGULATIONS: OTHER RULES

Sect. 909 Regulations:R l t d IRelated Income

• For a reverse hybrid splitter, a covered person’s aggregate amount of related income must be adjusted annually for the activities of the covered personincome must be adjusted annually for the activities of the covered person giving rise to income included in the foreign tax base, even if the net amount is negative (referred to as a dynamic approach) (§1.909-2T(b)(1)(iii)).– Does not include items of income or expense of a disregarded entity

d b h b id l th i l d d i th f i towned by a reverse hybrid, unless they are included in the foreign tax base

• In comparison, an annual approach rather than dynamic approach applies for other splitter arrangements (other than foreign consolidated groups).p g ( g g p )– As an example, for a loss-sharing splitter arrangement, related income is

an amount of income of the individual or corporate member of the U.S. combined group equal to the amount of income of that U.S. combined group that is offset by the usable shared loss of another U.S. combinedgroup that is offset by the usable shared loss of another U.S. combined group (§1.909-2T(b)(2)(v)).

• Related income is determined without regard to the application of §1.960-1(i)(4) (effect of separate limitation losses on earnings and profits in another separate category) or Sect 952(c)(1) (certain E&P deficits) (§ 1 909

59

separate category) or Sect. 952(c)(1) (certain E&P deficits) (§ 1.909-6T(d)(2)).

Sect. 909 Regulations:R l t d I (C t )Related Income (Cont.)

• Related income-ordering rulesFor pre 2011 splitter arrangements the defa lt r le is that if the E&P of a– For pre-2011 splitter arrangements, the default rule is that if the E&P of a covered person include amounts attributable to both related income and other income, then distributions, deemed distributions and inclusions out of E&P of the covered person are considered made out of related income and other income on a pro rata basis (§1.909-6T(d)(3)).pro rata basis (§1.909 6T(d)(3)).

– However, for pre-2011 splitter arrangements, a taxpayer can elect to apply a related-income-first method, which can provide a benefit of both releasing split taxes and carrying up foreign taxes under Sect. 902 (§1.909-6T(d)(4)).

– For post-2010 taxable years, however, a taxpayer must use a pro rata methodFor post 2010 taxable years, however, a taxpayer must use a pro rata method (the related-income-first method is unavailable) (§1.909-3T(a)).

• Distributions of related income to persons other than the payor retain their character as related income, with respect to split taxes.

• Related income carries over to the successor corporation in a Sect. 381 transaction.Related income carries over to the successor corporation in a Sect. 381 transaction.• The regulations adopt an aggregate approach in the partnership context, in

determining whether related income is taken into account by a covered person.• Distributions of previously taxed income do not release any split taxes.

60

Sect. 909 Regulations:R l t d I (C t )Related Income (Cont.)

• Related income is considered taken into account by a Sect. 902 shareholder if is taken into account by the Sect 902 shareholder itself or by an affiliatedis taken into account by the Sect. 902 shareholder itself, or by an affiliated corporation that is a member of the Sect. 902 shareholder’s U.S. consolidated group.

• Related income is considered taken into account by a Sect. 902 corporation if ith (i) th l t d i i fl t d i th E&P f th S t 902either (i) the related income is reflected in the E&P of the Sect. 902

corporation, by reason of an actual or deemed distribution out of the E&P of the covered person attributable to the related income; or (ii) the Sect. 902 corporation and covered person are combined in a Sect. 381 transaction.– Under the statute, split foreign taxes of a Sect. 902 corporation are

released when either the Sect. 902 corporation, or a Sect. 902 shareholder with respect to the Sect. 902 corporation, takes related income into account.

61

Sect. 909 Regulations:3T(b) Anti Avoidance Rule-3T(b) Anti-Avoidance Rule

• For post-2010 taxable years, a special anti-avoidance rule applies.• Split foreign ta es incl de ta es paid or accr ed ith respect to the amo nt of a• Split foreign taxes include taxes paid or accrued with respect to the amount of a

disregarded payment that is deductible by the payor of the disregarded payment under the laws of a foreign jurisdiction in which the payor of the disregarded payment is subject to tax on related income from a splitter arrangement (§1.909-3T(b)).– The anti-avoidance rule therefore expands the class of taxes that constitute split– The anti-avoidance rule, therefore, expands the class of taxes that constitute split

taxes.– This anti-avoidance rule applies only if there is a splitter arrangement in the first

instance.– It does not cause a tax on a disregarded payment to constitute a split tax absent– It does not cause a tax on a disregarded payment to constitute a split tax, absent

the existence of a splitter arrangement.– Applies only if there is a disregarded payment

• The amount of the deductible disregarded payment to which the rule applies is limited to the amount of related income from the splitter arrangement (§1 909 3T(b))to the amount of related income from the splitter arrangement (§1.909-3T(b)).

• This rule prevents taxpayers from circumventing Sect. 909 by eliminating what would otherwise be split taxes through the use of disregarded payments.

• Applies retroactively to taxable years beginning on or after Jan. 1, 2011.

62

Sect. 909 Regulations:3T(b) A ti A id R l (C t )-3T(b) Anti-Avoidance Rule (Cont.)

• U.S. hybrid equity instrument

$100 interest i f f i

USP2. Disregarded interest payment ($100 foreign deduction for F Holdco $30 foreign

y q ysplitter arrangement on instrument issued by F Opco to F Holdco• F Holdco has $100 of income, which would give rise to $30 ofincome for foreign

tax purposesF Holdco (holder)

1 $100 related

Holdco, $30 foreign tax for F DE)

which would give rise to $30 of split taxes. But, F Holdco makes $100 deductible interest payment to F DE and thus is not subject to

F Opco

1. $100 related income on U.S. equity hybrid instrument

foreign tax on income from U.S. hybrid equity instrument.• Deductible interest payment is disregarded for U S tax purposes

$100 operating income for U.S. tax purposes, ($100) interest deduction for foreign tax

F Opco (issuer)F DE disregarded, for U.S. tax purposes.

• F DE is subject to $30 of tax on deductible interest payment.• $30 of foreign tax is treated as

63

purposes split tax under -3T(b) anti-avoidance rule.

Sect. 909 Regulations:3T(b) A ti A id R l (C t )-3T(b) Anti-Avoidance Rule (Cont.)

• Reverse hybrid splitter arrangementUSP

• Reverse hybrid splitter arrangement • Reverse hybrid earns $100 operating income• DE1 would be subject to $30 foreign

DE2DE1

DE1 makes $100 interest payment to DE2

$20 net income tax and

tax on $100 operating income, but for deductible interest payment to DE2.• Interest payment is disregarded, for U S tax purposes

ReverseHybrid

$100 operating income

$20 net income tax and $10 withholding tax on $100 interest payment

U.S. tax purposes.• DE2 is subject to $20 net income tax and $10 withholding tax on the interest payment.

I h b h• It appears that both taxes are considered split taxes, under -3T(b).

64

Sect. 909 Regulations:3T(b) A ti A id R l (C t )-3T(b) Anti-Avoidance Rule (Cont.)

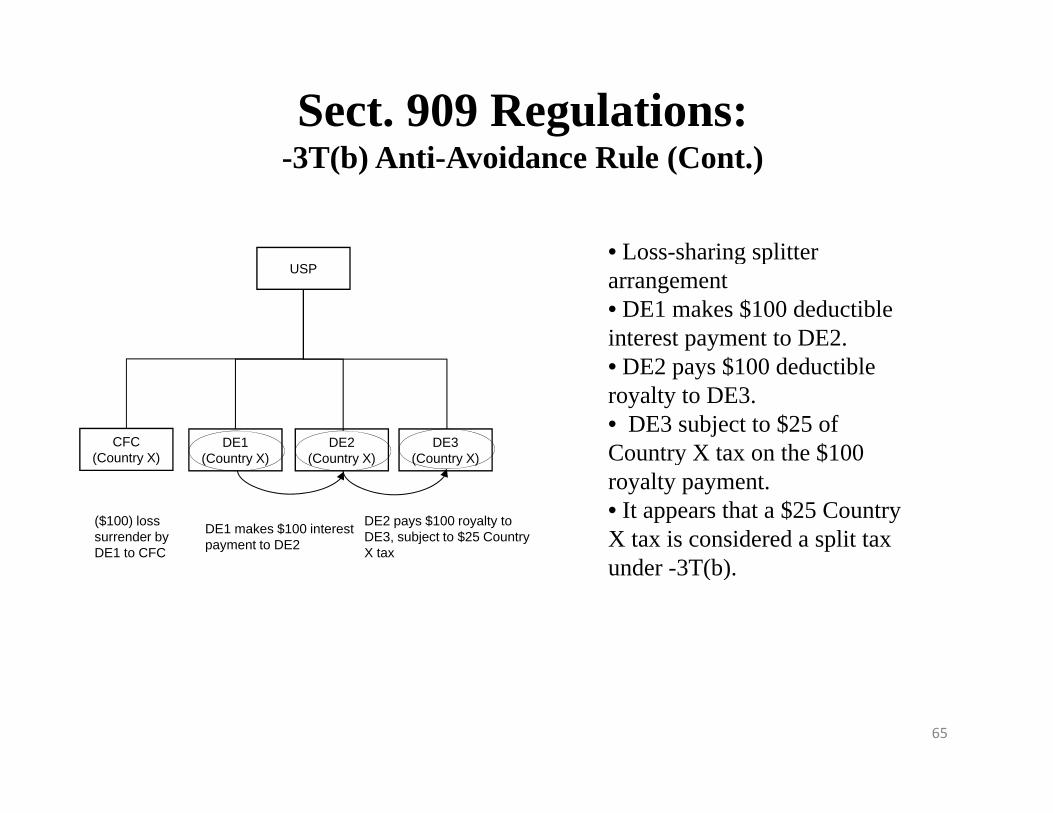

• Loss sharing splitterUSP

• Loss-sharing splitter arrangement • DE1 makes $100 deductible interest payment to DE2.

DE3(Country X)

CFC(Country X)

DE1(Country X)

DE2(Country X)

• DE2 pays $100 deductible royalty to DE3. • DE3 subject to $25 of Country X tax on the $100(Country X)(Country X)

DE1 makes $100 interest payment to DE2

(Country X) (Country X)

DE2 pays $100 royalty to DE3, subject to $25 Country X tax

($100) loss surrender by DE1 to CFC

Country X tax on the $100 royalty payment.• It appears that a $25 Country X tax is considered a split tax

d 3T(b)under -3T(b).

65

Sect. 909 Regulations:Coordination With Other FTC RulesCoordination With Other FTC Rules

• Split taxes are treated as paid or accrued in the year the related income is taken into account for purposes of applying Sect. 164(a) (providing a deduction for foreign taxes), Sect. 904(c) (providing for the carryover foreign taxes in excess of the annual f i t dit li it ti ) d S t 6511(d)(3)(A) ( idi 10 t t t fforeign tax credit limitation), and Sect. 6511(d)(3)(A) (providing a 10-year statute of limitations).– That is, Sect. 909 applies first to determine when the foreign taxes are paid or

accrued.S li d id d i h hi h h l– Split taxes are not treated as paid or accrued in the year to which the tax relates (as under normal Sect. 905(a) principles).

• Interaction with Sect. 905(c) rules for foreign tax redeterminations (e.g., an additional assessment of foreign tax for a prior year).

If d i i f f i l i d di di i– If a redetermination of foreign taxes claimed as a direct credit occurs in a post-2010 taxable year, and the redetermination relates to a pre-2011 taxable year, then Sect. 909 will not apply to any increase in the foreign taxes.

• The additional taxes are taken into account in the relation-back year under the normal application of Sect 905(c)normal application of Sect. 905(c).

– If a redetermination of foreign taxes paid or accrued by a Sect. 902 corporation occurs in a post-2010 taxable year, and the redetermination relates to a pre-2011 taxable year, then additional taxes are treated as pre-2011 taxes.

S t 909 ill l t h t if th lif 2011 lit t I

66

• Sect. 909 will apply to such taxes if they qualify as pre-2011 split taxes. In such case, the taxes become suspended in the year in which they would otherwise be taken into account through a pooling adjustment under the normal application of Sect. 905(c).