techno economical aspects of the halal industry and its

TRANSCRIPT

1

Techno Economical Aspects of the Halal Industry and its Services

Dr. Irfan Sungkar M.EcSenior Economist & Halal Industry Consultant

Director, PT. Green Research Indonesia

The First Gulf Conference on Halal Industry and its Services

24-26 January 2011Salmiyah, State of Kuwait-Holiday Inn Hotel, Al

2

الجوانب التقنية ا�قتصادية

لصناعة الح�ل وخدماته

سونغرعرفان . د

اندونيسيا أول اقتصادي لصناعة الحل، مستشار

مؤتمر الخليج ا�ول لصناعة الحل وخدماته2011يناير 24-26

دولة الكويت–السالمية –فندق ھوليدي إن

3

1. SITUATION OVERVIEW

4

• There exists many examples of market failurescommitted abroad by international marketers.

• Mistakes relating to international marketselection occur through inadequate orinappropriate evaluation of market potentials;

• The outcomes are almost always moreexpensive than the costs associated withsystematic evaluation that would haveprevented their occurrence;

• Understanding the nature of the industry,characteristics, consumers behavior and maingrowth factors are critical success factors

MARKET ASSESMENT OF HALAL INDUSTRY:

WHY IT IS IMPERATIVE

5

• Halal Industry is unique in the sense it is an industry where Islamicvalues, ideals and beliefs are implemented and adhered within thewhole chain of the production process of such respective Halalindustry.

• Given that certain aspects of the Halal procedure cannot be fullyverified ex-post through random sampling and testing, very closeand continuous supervision is necessary, especially for Halal servicesector.

• The more stringent (note: This is an arbitrary sentence!) the Halalstandard (e.g. no stunning, no mechanical slaughter), the higher willbe the supervision/transaction costs and the more likely is thetendency towards internalizing the process in a vertically integratedchain. Also, the greater there is the advantage of scale economiesthat allow the spreading of the said transaction/supervision costover a larger output volume. Brazil is able to internalized this cost(WHY?).

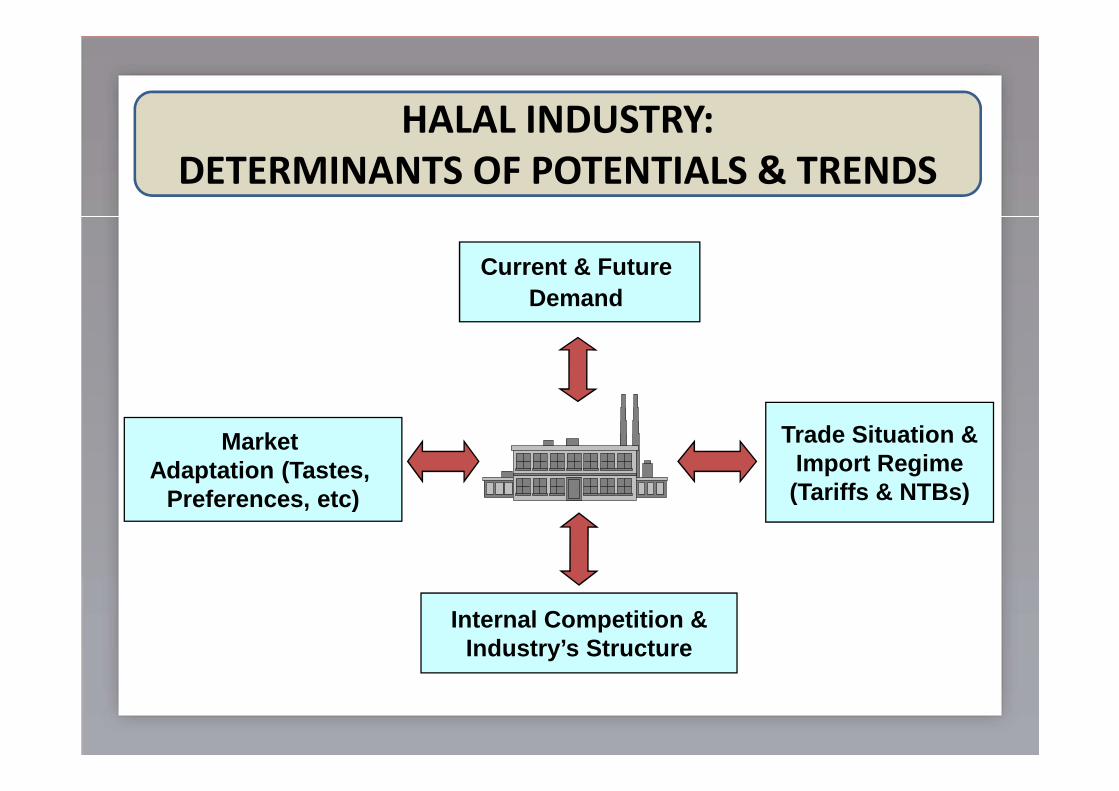

HALAL INDUSTRY:

A PROCESS AND PRODUCT ORIENTED

6

HALAL INDUSTRY:

DETERMINANTS OF POTENTIALS & TRENDS

Trade Situation &Import Regime(Tariffs & NTBs)

Market Adaptation (Tastes,

Preferences, etc)

Current & Future Demand

Internal Competition &Industry’s Structure

4% 1%

Cheapest proteins

Price is the key factor –Low brand awareness

Higher purchasing powerRefrigerator

High Value Added & Convenience Food Products

Primary Products Semi-Processed Products

Value added Products

Modern Retail Outlets

BUSINESS STRATEGY DEPENDS ON THE STAGE OF

INDUSTRIAL DEVELOPMENT (Ex: Poultry sector)

8

2. OIC, MIDDLE-EAST & GCC COUNTRIES

9

REGIONAL BOUNDARIES – M.E.N.A

10

COMPARATIVE SIZE OF THE ECONOMIES

11

OIC COUNTRIES: ECONOMY & MARKET SIZE

12

COMPARATIVE OIC ECONOMIC INDICES

13

REGIONAL COMPARATIVE

Country

• China

• India

• Brazil

• Russia

• Middle-East

Population

(Million)

• 1,330

• 1190

• 195

• 145

• 360

Economic

Growth (%)

• 8.0-9.0%

• 7.0-7.5%

• 4.5-5.5%

• 5.0-6.0%

• 6.0-7.0%

GDP

(Billion US$)

• 4,410

• 1,220

• 1,580

• 1,690

• 2,300

14

DEMOGRAPHIC: SIGNIFICANT FOREIGN WORKERS

0

10

20

30

40

50

60

70

80

90

Avg GCC Saudi

Arabia

Oman Bahrain Kuwait Qatar UAE

Locals Foreigners

15

GCC DEMOGRAPHIC: YOUNG POPULATION

16

3. THE HALAL INDUSTRY

17

EST. SIZE OF HALAL FOOD MARKET (MILL US$, 2010)

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

EGYPT SAUDI ARABIA UAE YEMEN KUWAIT JORDAN OMAN QATAR BAHRAIN

18

SIGNIFICANT IMPORTS OF HALAL PRODUCTS

(EX: HALAL MEAT IMPORTS TO GCC COUNTRIES, 2009)

Bahrain

3,0% Kuwait

12.4%

Oman

5,8%

Qatar

6,3%

Saudi Arabia

49,5%

United Arab

Emirates

23,0%

Total Halal Meat Imports: US$ 2.48 billion

19

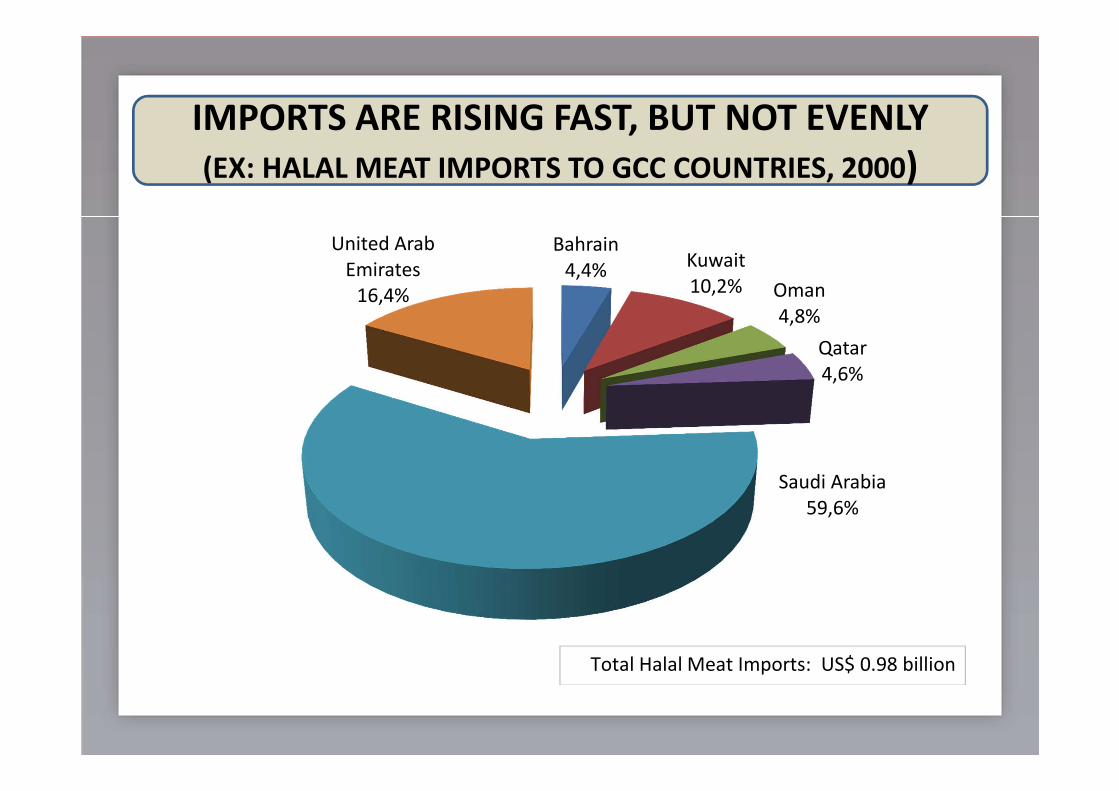

IMPORTS ARE RISING FAST, BUT NOT EVENLY

(EX: HALAL MEAT IMPORTS TO GCC COUNTRIES, 2000)

Bahrain

4,4%Kuwait

10,2% Oman

4,8%

Qatar

4,6%

Saudi Arabia

59,6%

United Arab

Emirates

16,4%

Total Halal Meat Imports: US$ 0.98 billion

20

WITH LARGE PRICE VARIATIONS (EX: FROZEN CHICKEN)

9.13

7.64 7.80 7.52 7.40

6.235.68 5.43 5.36

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

CoopIslami

Al Salwa Al Watania(S. Arabia)

Khazan(Kuwait)

Sadia (Brazil )

Struer(Denmark)

Al Wadi(France)

Doux(France)

Seara(Brazil)

Local Brand

Foreign Brand

21

GCC IS NOT A SINGLE MARKET: DIFFERENT FAVORITE

PRODUCTS IN EACH COUNTRY (EX: KUWAIT)

68.9 67.8

56.750 47.8 44.4 42.2

32.2 3022.2

16.7 13.3 11.1 10 8.9 6.7 3.3

01020304050607080

Nug

gets

Sau

sage

s

Sha

war

ma

Sou

ps

Min

ced

Mea

t

Sto

ck /

Bro

th

Bur

ger

Sam

osa

Sal

ami /

Kaa

lbaa

s

Mea

t bal

ls

Spr

ing

Rol

ls

Mea

t Fla

vour

Kab

ab

Oth

ers

Kof

ta

Gra

vies

Esse

nce

and

Gra

nule

s

%

22

GCC IS NOT A SINGLE MARKET: DIFFERENT FAVORITE

PRODUCTS IN EACH COUNTRY (EX: UAE)

55.80

49.50 49.00

38.10 36.40 33.9028.80

18.90 17.50 16.40 15.40 12.80 11.60 11.608.40 7.80

2.1

0.00

10.00

20.00

30.00

40.00

50.00

60.00N

ugge

ts

Bur

ger

San

dwic

h/S

haw

arm

a

Sau

sage

s

Sou

ps

Tikk

a

Sto

ck/B

roth

Mea

t Fla

vour

Sam

osa

Min

ced

Mea

t

Gra

vies

Kab

ab

Spr

ing

Rol

ls

Mea

t bal

ls

Esse

nce

and

Gra

nule

s

Kof

ta/S

hish

Kof

ta

Oth

ers

%

23

TYPICAL RETAIL DISTRIBUTION CHANNEL IN GCC

FOREIGN SUPPLIERS

CONSUMER (RETAIL) MARKET

Importers

Wholesalers and Semi-wholesalers

Hypermarket, Big/Large

Supermarkets

Smaller Supermarket,

Grocery Shops, Etc.“Baqalas”

Other Outlets

Cooperative Shops

40% 15-20%20-25% 5% 25%

24

PRICE DIFFERENTIALS: LOCAL – IMPORTS - FOREIGN(EX: CHICKEN NUGGET PRICE/KG IN THE UAE & MALAYSIA)

Local Brand Foreign Brand Malaysia Brand

25

ANALYSIS OF PRICE & PRODUCTS COMPETITIVENESS(EX: EX- JEBEL ALI PRICE OF MALAYSIAN CHICKEN NUGGET)

26

MAJOR FOOD COMPANIES IN GCC COUNTRIES

� Americana Group – Head Quarter in Kuwait

� Processing Plants in Kuwait, Jeddah and Cairo –

Among the Largest in GCC & Middle East;

◦ Available in all GCC Countries.

◦ This is a good case study to show how Kuwaiti

company and products can attain success in

highly competitive foodservice market in the

region.

◦ Principal suppliers to foodservice outlets in

Middle-East

27

MAJOR FOOD COMPANIES IN GCC COUNTRIES

� Al-Islami – Dubai Cooperative Society

(UAE)

◦ Available in All GCC countries. Has one of the

highest market share in UAE;

� Al Kabeer – Cascade Marine Foods Llc

(UAE)

◦ Not available in all GCC countries. One of the

highest market share in UAE and Saudi Arabia

� IFFCO Group – Major consumer goods in GCC;

28

MAJOR FOOD COMPANIES IN GCC COUNTRIES (ii)

(The list is NOT extensive: for purpose example only)

� Universal Islamic Meat (UAE)

◦ Mostly available only in UAE. Presence in Saudi Arabia and Kuwait is

limited.

� GCC Food Company (UAE)

◦ Based in Dubai with large range of products. Took over Canned beef

products from Americana in 2003

� Al Watania Poultry (Saudi Arabia)

◦ Available widely in Saudi Arabia. The largest dessert-based poultry

farms in the world (near Riyadh)

� Radwa Food Production and Sunbullah Co. (Saudi Arabia)

◦ Radwa introduced ‘Satay’ (Ex. of business flexibility)

◦ Both has higher market share in Saudi Arabia

� Khazan Meat Factory (Kuwait)◦ Has the second highest market share in Kuwait.

29

HOW TO BE COMPETITIVE WHEN PRODUCTION

FACTORS ARE EXPENSIVE or RARE?

� Fact: Local raw materials are limited and expensive. Thus, Has liberal import regime◦ Major Kuwaiti & GCC company imports almost all the main raw materials

and ingredients from the most competitive sources in the world;

� Fact: Labor shortage. Thus, Labor intensive production facility is not encouraged◦ Whenever possible, capital intensive production facilities are being used.

There is a free movement of labor forces in the designated large area production facilities;

◦ The result: GCC country has a free market. So, company has to be competitive or ceased operation

◦ Business flexibility & innovative: Targeted segment & niche products (Good example: Americana Group)

30

DOWNSIDE: HALAL COMPLIANCE IN QUESTION

� How many Kuwaiti company, or any GCC-based companycan ensure all their raw materials and ingredients boughtfrom many sources/countries are Halal?

◦ Need to buy raw materials/ingredients from Halal certified sources (Is there any Halal assurance system?)

◦ Do you need Halal certificate for imported pastries to produce sambosa? (L-cysteine could be used)

◦ Do you need Halal MSGs as a taste enhancer? (The case of Ajinomoto in Indonesia during 2000’s: Consumers’ revolt knowing porcine-based enzyme was used as catalyst agent in the production process)

31

4. THE CONSUMERS: BEHAVIOR, TRENDS & ISSUES

32

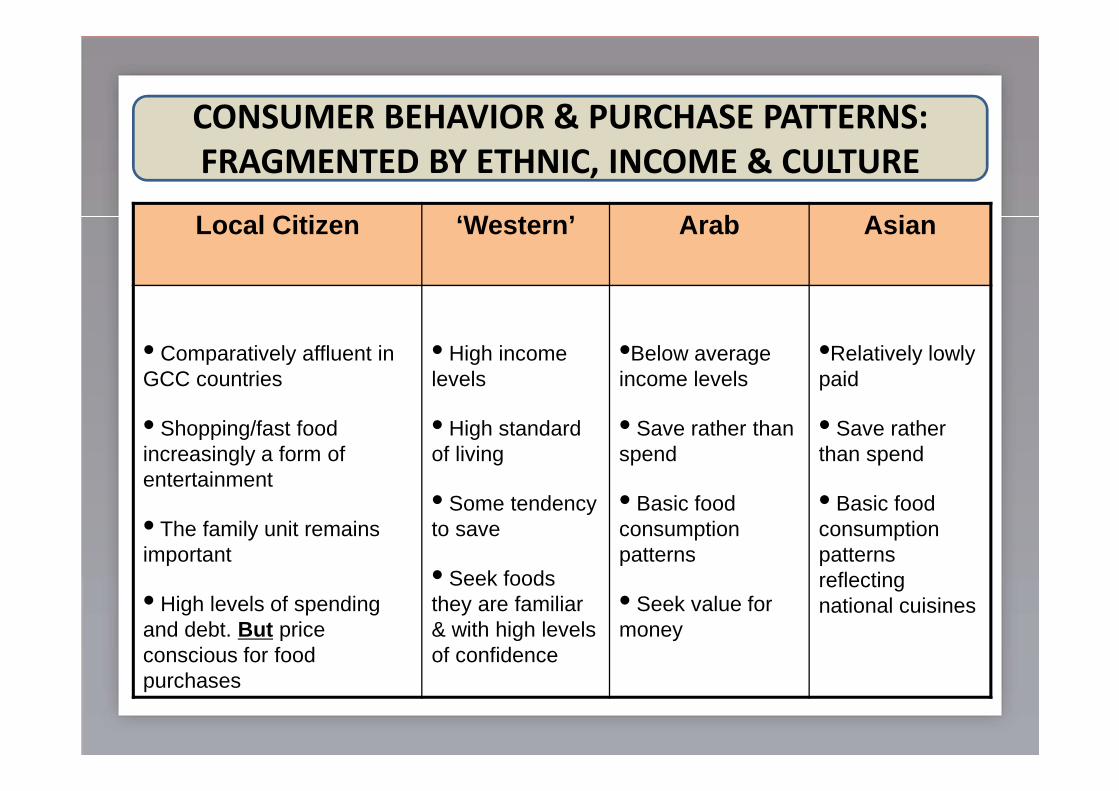

CONSUMER BEHAVIOR & PURCHASE PATTERNS:

FRAGMENTED BY ETHNIC, INCOME & CULTURE

Local Citizen ‘Western’ Arab Asian

• Comparatively affluent in GCC countries

• Shopping/fast food increasingly a form of entertainment

• The family unit remains important

• High levels of spending and debt. But price conscious for food purchases

• High income levels

• High standard of living

• Some tendency to save

• Seek foods they are familiar & with high levels of confidence

•Below average income levels

• Save rather than spend

• Basic food consumption patterns

• Seek value for money

•Relatively lowly paid

• Save rather than spend

• Basic food consumption patterns reflecting national cuisines

33

CONSUMERS MAY HAVE LIMITED KNOWLEDGE(WHETHER ISLAMIC SYMBOLS PERSONIFIES HALAL?)

0%

20%

40%

60%

80%

100%

Malays Chinese Indians Others

40,3%

10,7%

18,2%22,2%

59,7%

89,3%81,8%

77,8%

Yes

No

Meat & meat-

based

Processed food PharmaceuticalsCosmetics &

personal-care

100% 0%

98.0% 68.0% 28.0%32.0%

Source: Consumer Survey in Southeast Asia and GCC Countries, 2008

VARIED AWARENESS LEVEL ON ‘HALAL’(POLARIZATION ON THE CONCEPT OF HALAL)

CONSUMERS ARE ABLE TO MAKE INFORMED

CHOICE ABOUT HALAL CERTIFICATIONS?

TO REGULATE HALAL CERTIFICATION OR LET THE MARKET DECIDE?

MORE COMPLEX AS THE HALAL MARKET GROWSIS IT TRUE THAT SOME ARE RENT SEEKERS?

WHO SHOULD PROVIDE DATA & INFO? WHOM IS THE REPRESENTATIVE OF OIC?

37

• Brand has the power to

differentiate the product and

‘communicate’ values to the

consumers;

• An effective branding and market

positioning strategy gives

additional values for the

products to be able to be sold at

‘premium’ prices;

• It avoid the products from

commoditization.

REACHING THE CONSUMERS: IMPORTANCE OF

BRAND AND MARKET POSITIONING STRATEGY

38

• Consumers/buyers perceives unique added

values which match their needs more closely;

• Consumer’s values, beliefs, lifestyles and taste

perception are related to food consumption

and purchasing behavior. Actual choice of

food products depend on consumer value

orientations;

• Need to aware of attitude/perception bias

and purchasing realities when doing research

FACTORS BEYOND BRANDING: CONSUMERS’

VALUE ORIENTATIONS AND BELIEFS

39

THANK YOU – Q & A

IRFAN SUNGKAR

ECONOMIST & HALAL INDUSTRY CONSULTANT

DIRECTOR - PT. GREEN RESEARCH INDONESIAEMAIL: [email protected]; [email protected]

Mobile (KL): +60.17- 250 8190