teknia manufacturing group, s.l.u. 1 - teknia manufacturing group, s.l.u. (incorporated in spain in...

TRANSCRIPT

- 1 -

TEKNIA MANUFACTURING GROUP, S.L.U.

(Incorporated in Spain in accordance with the Spanish Capital Companies Act)

EUR 40,000,000 Senior Unsecured Notes Programme 2018

Teknia Elorrio, S.L.U., Teknia Pedrola, S.L.U., Teknia Barcelona, S.L.U., Teknia

Bilbao XXI, S.L.U., Teknia Montmelo, S.L.U., Teknia Martos, S.L.U., Teknia

Azuqueca, S.L.U., Teknia Manresa, S.L.U., Teknia Epila, S.L.U., Teknia R&D,

S.L., Teknia Brasil Ltda., Teknia Rzeszów S.A., Teknia Kálisz, S.p. z o.o., Teknia

Uherský Brod, a.s., and Teknia Nashville, LLC as Subsidiary Guarantors of the

Programme

INFORMATION MEMORANDUM (DOCUMENTO BASE INFORMATIVO DE

INCORPORACIÓN) ON THE ADMISSION (INCORPORACIÓN) OF MEDIUM-

AND LONG-TERM SECURITIES ON THE ALTERNATIVE FIXED-INCOME

MARKET (“MARF”)

Teknia Manufacturing Group, S.L.U. (indistinctively, “Teknia”, “Teknia Group”, the

“Issuer” or the “Company”) a private company with limited liability (Sociedad Limitada)

organised under the laws of Spain, registered in the Vizcaya Mercantile Registry (Basque

Country, Spain) in volume 3702, folio 22, sheet BI-23069, with tax identification number

B-48.984.090 and LEI code 9598001382GF2BG2PP33 will request the admission of the

Notes (incorporación de valores) to be issued under this Programme on the Alternative

Fixed-Income Market (“MARF”) under the provisions of this Information Memorandum

(Documento Base Informativo de Incorporación).

Admission (incorporación) to MARF will be requested for the Notes issued under the

Programme. MARF is a multilateral trading system and is not a regulated market in

accordance with the provisions of Directive 2004/39/EC of 21 April 2004 on markets in

financial instruments amending Council Directives 85/611/EEC and 93/6/EEC and

Directive 2000/12/EC of the European Parliament and of the Council and repealing

Council Directive 93/22/EEC (“Directive 2004/39/EC”). There is no guarantee that the

price of the Notes in MARF will be maintained. There is no assurance that the Notes will

be widely distributed and actively traded on the market because at this time there is no

active trading market. Nor is it possible to ensure the development or liquidity of the

trading markets for the Notes.

The Notes will be represented by book entries in Iberclear, according to the provisions of

title VIII of the Information Memorandum.

An investment in the Notes involves certain risks.

Read section III of the Information Memorandum on Risk Factors.

This Information Memorandum (Documento Base Informativo de Incorporación) is

not a prospectus (folleto informativo) and has not been registered with the National

Securities Market Commission (CNMV). The offering of the securities does not

constitute a public offering in accordance with the provisions of Article 35 of Royal

Decree 4/2015 of 23 October, approving the revised text of the Securities Market Act

and therefore there is no obligation to approve, register, and publish a prospectus

- 2 -

with the CNMV. The issue of Notes under this Programme is intended exclusively

for professional clients and qualified investors in accordance with the provisions of

Article 205 of Royal Decree 4/2015 and Article 39 of Royal Decree 1310/2005 of 4

November, which partially develops Law 24/1988, of 28 July, on the Securities

Market, with regard to the admission of securities to trading on official secondary

markets, public offerings or subscription, and the prospectus required for this

purpose (“Royal Decree 1310/2005”).

No action has been taken in any jurisdiction to permit a public offering of the Notes

or the possession or distribution of the Information Memorandum or any other

offering material in any country or jurisdiction where such action is required for

said purpose.

This Information Memorandum includes the information required by MARF

Circular 1/2015. The Governing Body of MARF has not made any verification or

checks with respect this Information Memorandum, nor of the rest of the

documentation and information contributed by the Issuer in compliance with said

Circular 1/2015.

ARRANGERS AND PLACEMENT ENTITIES

BANCO DE SABADELL, S.A. and BANKINTER, S.A.

LEGAL ADVISOR OF THE ISSUER

CUATRECASAS GONÇALVES PEREIRA

REGISTERED ADVISOR

PKF ATTEST SERVICIOS EMPRESARIALES, S.L.

The date of this Information Memorandum is 15 of February 2018.

- 3 -

CONTENTS

I. IMPORTANT INFORMATION 8

II. SUMMARY 11

1. Overview of the Business of the Issuer 11

2. History 12

3. Relevant aspects of recent activity 13

4. Organizational Structure 13

5. Strategy 15

6. Financial information 16

III. RISK FACTORS 23

1. Risks related to the Issuer’s Industry and Business 24

2. Financial risk factors 37

3. Risks relating to the Notes issued under the Programme 40

IV. DECLARATION OF LIABILITY 44

1. Person responsible for the information contained in the Information

Memorandum 44

2. Statement of the person responsible for the content of the Information

Memorandum 44

V. FUNCTIONS OF THE REGISTERED ADVISOR OF MARF 44

VI. INDEPENDENT AUDITORS 46

1. Name and address of the auditors of the Issuer for the period covered by

the historical financial information (together with their membership in a

professional body) 46

2. If auditors have resigned, been removed from their duties or have not

been re-appointed during the period covered by the historical financial

information, indicate the details, if material 47

VII. INFORMATION ON THE ISSUER 47

- 4 -

1. Full name of the Issuer including its address and identification data 47

2. Description of the Issuer 48

2.1. Milestones of the Issuer 48

2.2. Main Shareholders 49

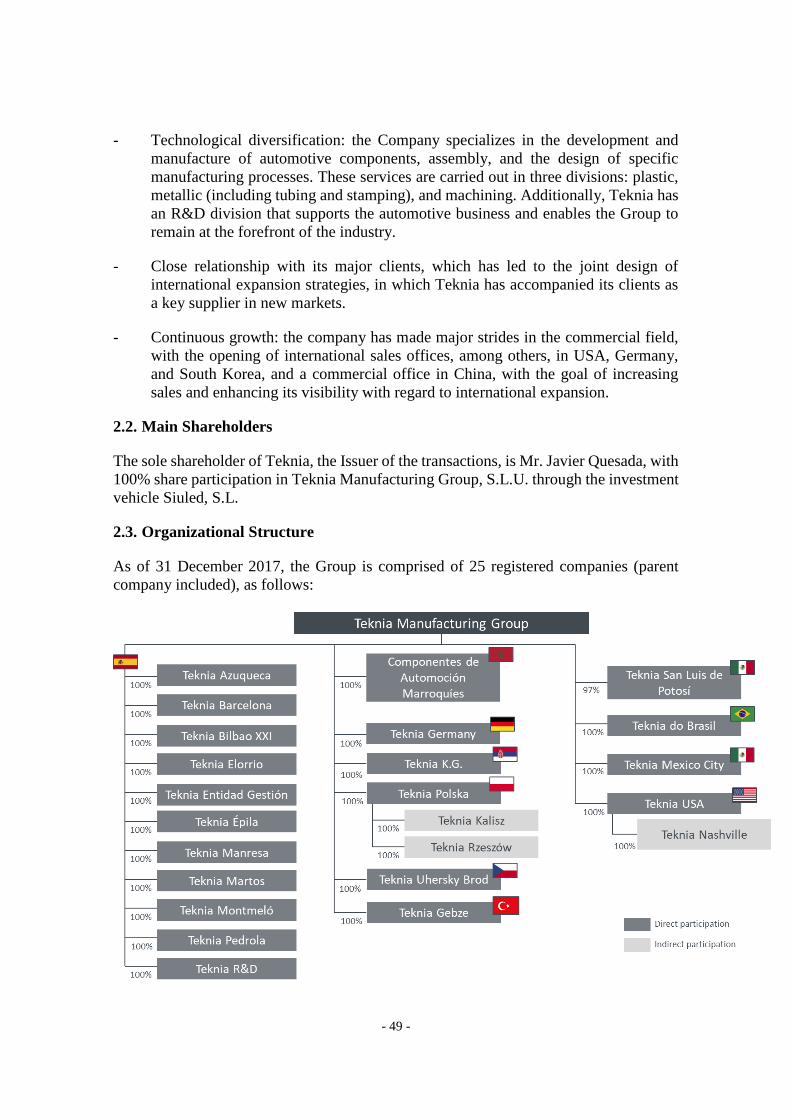

2.3. Organizational Structure 49

2.4. Corporate purpose 53

2.5. Administrative and management bodies 54

2.5.1. Board of Directors 54

2.5.2. Senior Management 54

2.6. Industry and Activity 60

2.6.1. Industry introduction 60

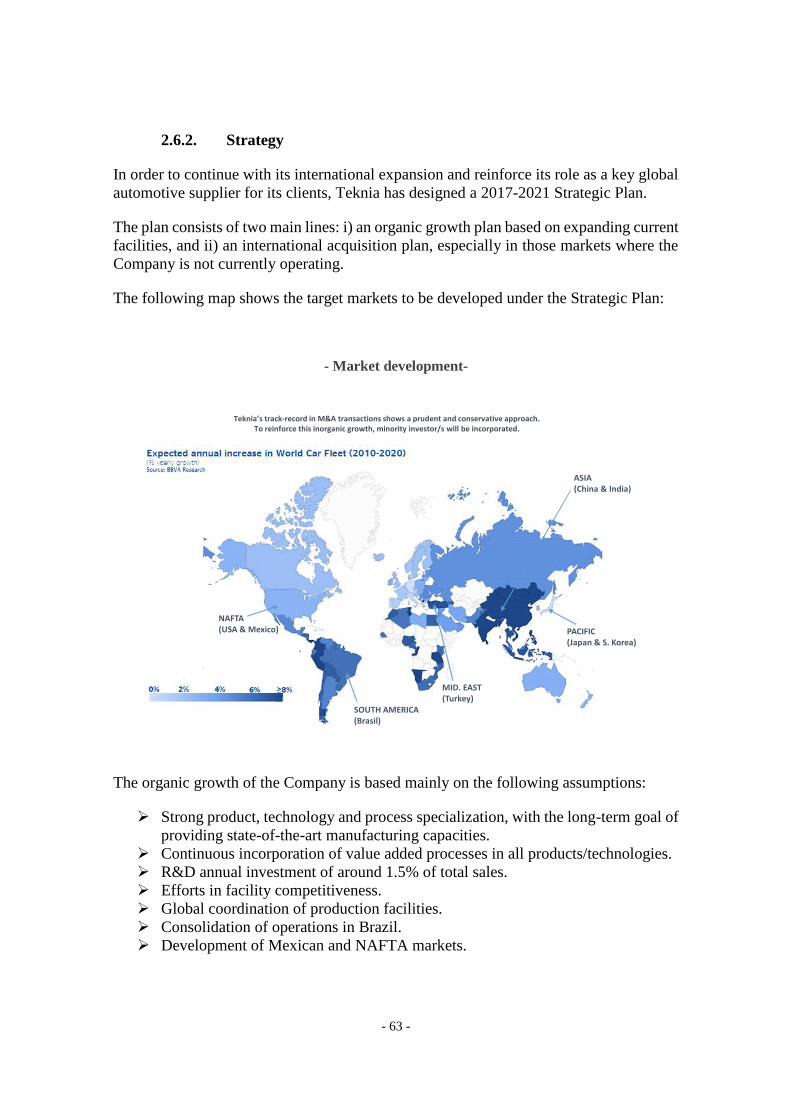

2.6.2. Strategy 63

2.6.3. Trends in the industry 64

2.6.4. Business Units 65

2.6.5. International expansion 65

2.6.6. Sectors of activity 66

2.7. Declaration on the absence of significant changes in the prospects of the

Issuer 69

2.8. Information on significant changes in the prospects of the Issuer 69

3. Reasons for the Issue and use of proceeds 69

4. Financial information 69

4.1. Audited historical financial information 69

4.2. Financial Statements of the Issuer 70

4.3. Financial ratios as of 31 December 2016 and 2015 76

4.4. Audit of historical annual financial information 77

- 5 -

4.4.1. Statement that historical financial information has been audited. If audit

reports on the historical financial information have been refused by the

auditors or if they contain qualifications or disclaimers, such

qualifications or disclaimers must be reproduced in full, explaining the

reasons. 77

4.4.2. Indication of other information in the Information Memorandum which

has been audited by the auditors 77

4.4.3. Where financial data in the Information Memorandum is not extracted

from the audited Financial Statements of the Issuer, you must declare the

source of the data and state that the data is unaudited 77

4.5. Age of the most recent financial information 77

4.6. Judicial, administrative and arbitration proceedings 77

5. Significant changes in the financial or trading position of the Issuer 77

VIII. DESCRIPTION OF THE NOTES 78

1. Total amount of the securities issued/admitted to trading 78

2. Date of issue of the Notes 78

3. Form and Denomination 78

4. Status of the Notes and Guarantee 79

5. Price of the Notes 79

6. ISIN Code 80

7. Register, Title and Transfers 80

8. Guarantees and Security 81

8.1. Subsidiary Guarantors 82

8.2. Nature of the Guarantees 84

8.3. Accession of additional Subsidiary Guarantors or Share Pledge over

Subsidiaries 84

8.4. Release of Subsidiary Guarantors 85

8.5. Limitations 86

- 6 -

9. Covenants 86

9.1. Negative Pledge 86

9.2. Change of Control 88

9.3. Related-party Transactions 89

9.4. Limitation on Indebtedness 90

9.5. Limitation on sale of assets and mandatory tender offer for the Notes 91

9.6. Limitation on Dividends 93

9.7. Limitation on Investments 94

9.8. Limitation on Structural Modifications 95

9.9. Transactions with Subsidiaries 95

9.10. Information and Reports 96

10. Interest 97

11. Redemption and Purchase 98

(i) the Issuer has or will become obliged to pay additional amounts as

provided or referred to in Condition 15 (Taxation) as a result of any

change in, or amendment to, the laws or regulations of the Kingdom of

Spain or any political subdivision or any authority thereof or therein

having power to tax, or any change in the application or official

interpretation of such laws or regulations (including a holding by a court

of competent jurisdiction), which change or amendment becomes

effective on or after the Issue Date; and 98

(ii) such obligation cannot be avoided by the Issuer taking reasonable

measures available to it; 99

12. Payments 100

13. Placement of each issue under the Programme 101

14. Further issues 101

15. Taxation 101

16. Events of Default 103

- 7 -

17. Prescription 105

18. Paying Agent 105

19. Syndicate of Noteholders, Modification and Waiver 105

20. Notices 117

21. Governing Law and Jurisdiction 117

IX. ADMISSION OF THE SECURITIES 118

1. Request for admission of the securities to the Alternative Fixed

Income Market. Deadline for admission to trading 118

2. Cost of all legal, financial, and audit services and other costs to the

Issuer regarding the registration of the Programme 119

X. THIRD PARTY INFORMATION, STATEMENT BY EXPERTS

AND DECLARATIONS OF INTEREST 119

XI. REFERENCES 119

- 8 -

I. IMPORTANT INFORMATION

Neither the Issuer nor the Bookrunners have authorized anyone to provide information to

potential investors other than the information contained in this Information Memorandum

and other publicly available information. Potential investors should not base their

investment decision on information other than that contained in this Information

Memorandum and alternative sources of public information.

The Bookrunners assume no liability for the content of the Information Memorandum.

The Bookrunners have signed a contract with the Issuer, but neither the Bookrunners nor

any other entity has made any commitment to underwrite the issue, without prejudice to

the ability of the Bookrunners to acquire part of the Notes on their own behalf.

This Information Memorandum is not a prospectus (folleto informativo) and has not been

registered with the National Securities Market Commission (CNMV). The offering of the

securities does not constitute a public offering in accordance with the provisions of Article

35 of Royal Decree 4/2015 of 23 October, approving the revised text of the Securities

Market Act (“SML”), and therefore there is no obligation to approve, register, and publish

a prospectus with CNMV.

Admission (incorporación) to MARF will be requested for the Notes issued under the

Programme. MARF is a multilateral trading system and is not a regulated market in

accordance with the provisions of Directive 2004/39/EC. This Information Memorandum

includes the information required by MARF Circular 1/2015. The Governing Body of

MARF has not made any verification or checks with respect this Information

Memorandum, nor of the rest of the documentation and information contributed by the

Issuer in compliance with said Circular 1/2015.There is no guarantee that the price of the

Notes in MARF will be maintained.

The Notes will be represented by book entries in Iberclear, according to the provisions of

section VIII of the Information Memorandum.

- 9 -

SELLING RESTRICTIONS

No action has been taken in any jurisdiction to permit a public offering of the Notes or

the possession or distribution of the Information Memorandum or any other offering

material in any country or jurisdiction where such action is required for said purpose.

In particular:

European Union

The Notes are only directed to qualified investors according to the provisions in Article

2.1.e) of Directive 2003/71/EC. Therefore, this Information Memorandum has not been

registered with any competent authority of any Member State.

Spain

This Information Memorandum has not been registered with the National Securities

Market Commission in Spain (“Comisión Nacional del Mercado de Valores” or

“CNMV”). The issue of the Notes will not constitute a public offering in accordance with

the provisions of Article 35 of Royal Decree 4/2015 of 23 October, approving the revised

text of the Securities Market Act. The issue of Notes shall be intended exclusively for

professional clients and qualified investors in accordance with the provisions of Article

205 of Royal Decree 4/2015 of 23 October, approving the revised text of the Securities

Market Act and Article 39 of Royal Decree 1310/2005 of 4 November, which partially

develops Law 24/1988, of 28 July, on the Securities Market, with regard to the admission

of securities to trading on official secondary markets, public offerings or subscription,

and the prospectus required for this purpose (“Royal Decree 1310/2005”).

Portugal

This Information Memorandum has not been registered with the Portuguese Securities

Market Commission (Comissão do Mercado de Valores Mobiliários) and no action has

been undertaken that would be considered a public offer of the Notes in Portugal.

According to the above, the Notes to be issued under this Programme may not be offered,

sold, or distributed in Portugal except in accordance with the provisions of Articles 109,

110 and 111 of the Portuguese Securities Code (Código dos Valores Mobiliários).

Andorra

No action has been undertaken that may require the registration of this Information

Memorandum with any authority of the Principality of Andorra.

Switzerland

This document does not constitute an offer to sell or a solicitation to buy the Notes in

Switzerland. The Notes issued under the Programme shall not be subject to public

offering or advertised, directly or indirectly, in Switzerland and will not be listed on SIX,

- 10 -

the Swiss Exchange, or any other Swiss market. Neither this document nor the issue or

marketing materials of the Notes constitute a prospectus within the meaning of articles

652a or 1156 of the Swiss Code of Obligations, nor a listing prospectus according to the

Admission rules of the SIX Swiss Exchange or any other Swiss market.

United States

This document must not be distributed, directly or indirectly, in (or sent to) the United

States of America (according to definitions of the “Securities Act” of 1933 of the United

States of America – “U.S. Securities Act”). This document is not an offer to sell securities

or a solicitation to buy any securities in any jurisdiction in which such offer or sale is

considered contrary to law. The Notes issued under the Programme will not be registered

in the United States for the purposes of the U.S. Securities Act and may not be offered or

sold in the United States without registration or an exemption application for registration

under the U.S. Securities Act. There will not be a public offering of the notes in the United

States or in any other jurisdiction.

- 11 -

II. SUMMARY

1. Overview of the Business of the Issuer

Teknia Manufacturing Group, S.L.U. was incorporated as a private company with limited

liability under the laws of Spain on 30 July 1998. This Spanish, family-owned company

is engaged in the manufacture of automotive parts, and currently has 20 production plants,

4 commercial offices, and 5 Research & Development (“R&D”) centres.

The Company designs, develops, manufactures and supplies its activities in the

automotive business in three product categories: plastic, metallic (tubing and stamping)

and machining, and sells its products to Tier1 suppliers (c. 80% of sales) and Original

Equipment Manufacturer - “OEMs”- (c.20% of sales).

Teknia Group began its international expansion in 1999 with the acquisition of Tecnotubo

in Brazil. The following graph shows the Teknia Group’s current locations:

In addition, to i) enhancing its product range, ii) providing its clients with the latest

products, and iii) relying on cutting-edge technology, Teknia engages in intense R&D,

which allows the Company to be a leading manufacturer within the industry and a partner

to its clients.

- 12 -

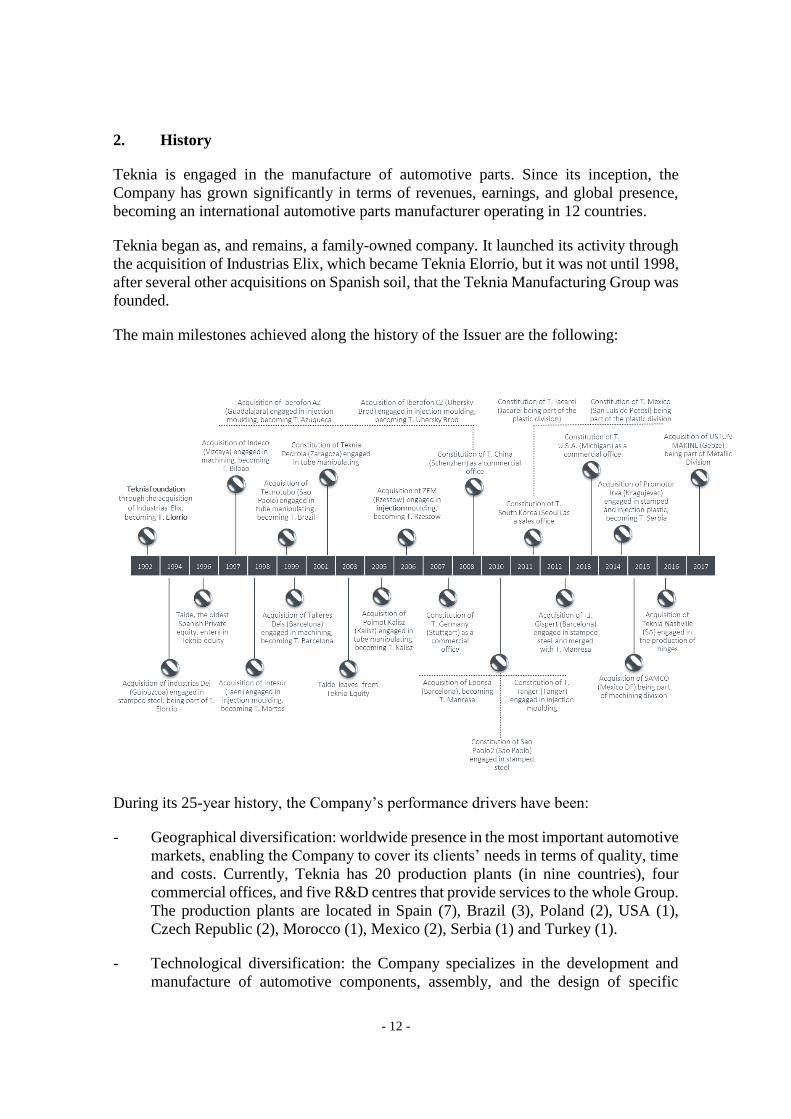

2. History

Teknia is engaged in the manufacture of automotive parts. Since its inception, the

Company has grown significantly in terms of revenues, earnings, and global presence,

becoming an international automotive parts manufacturer operating in 12 countries.

Teknia began as, and remains, a family-owned company. It launched its activity through

the acquisition of Industrias Elix, which became Teknia Elorrio, but it was not until 1998,

after several other acquisitions on Spanish soil, that the Teknia Manufacturing Group was

founded.

The main milestones achieved along the history of the Issuer are the following:

During its 25-year history, the Company’s performance drivers have been:

- Geographical diversification: worldwide presence in the most important automotive

markets, enabling the Company to cover its clients’ needs in terms of quality, time

and costs. Currently, Teknia has 20 production plants (in nine countries), four

commercial offices, and five R&D centres that provide services to the whole Group.

The production plants are located in Spain (7), Brazil (3), Poland (2), USA (1),

Czech Republic (2), Morocco (1), Mexico (2), Serbia (1) and Turkey (1).

- Technological diversification: the Company specializes in the development and

manufacture of automotive components, assembly, and the design of specific

- 13 -

manufacturing processes. These services are carried out in three divisions: plastic,

metallic (including tubing and stamping), and machining. Additionally, Teknia has

an R&D division that supports the automotive business and enables the Group to

remain at the forefront of the industry.

- Close relationship with its major clients, which has led to the joint design of

international expansion strategies, in which Teknia has accompanied its clients as

a key supplier in new markets.

- Continuous growth: the company has made major strides in the commercial field,

with the opening of international sales offices, among others, in USA, Germany,

and South Korea, and a commercial office in China, with the goal of increasing

sales and enhancing its visibility with regard to international expansion.

3. Relevant aspects of recent activity

The Group consists in two main business lines: automotive and R&D. The R&D division

supports the automotive business and enables the Group to remain at the forefront of the

industry.

The Plastic division is the largest in terms of sales (approximately 45% of total aggregated

sales in 2016), followed by the Metallic division (approximately 39% of total sales), and

the Machining division (approximately 16% of total sales).

4. Organizational Structure

As of 31 December 2017, the Group is comprised of 25 registered companies (parent

company included), as follows:

(1) Source: Individual Audited Annual Accounts (Aggregated Data)

- 14 -

Siuled, S.L. is the investment vehicle through which Mr. Javier Quesada owns 100% of

Teknia Manufacturing Group.

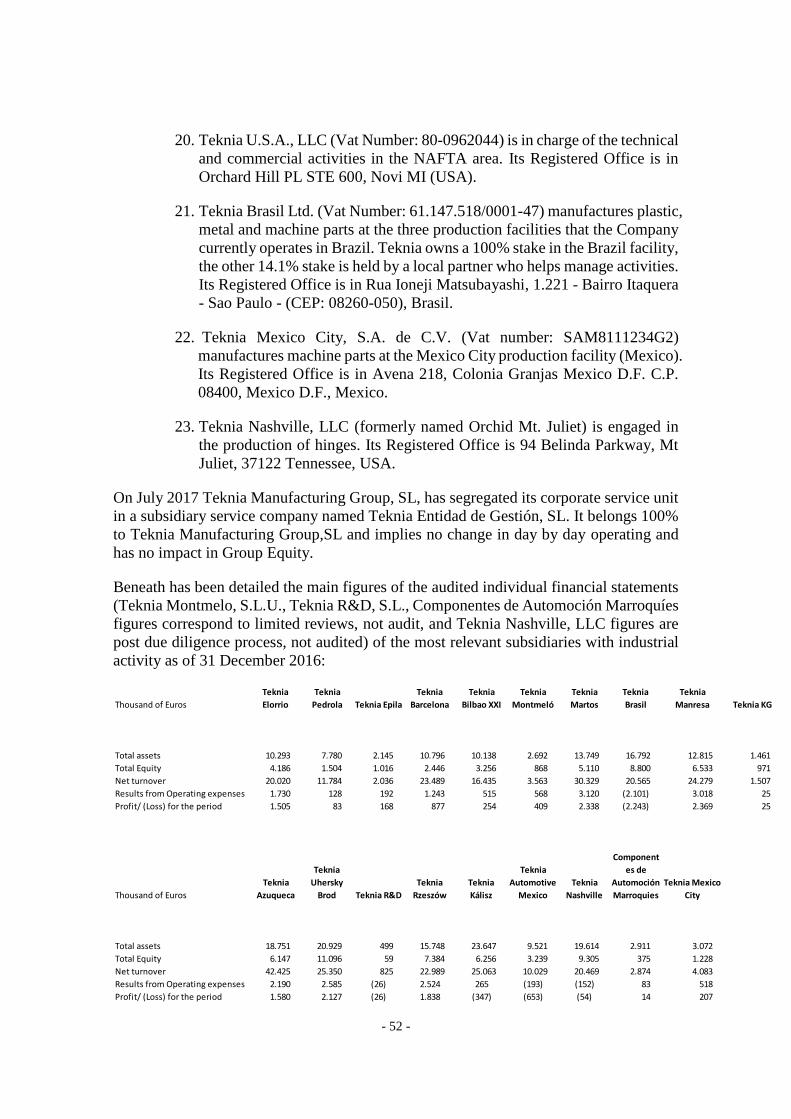

Beneath has been detailed the main figures of the audited individual financial statements

(Teknia Montmelo, S.L.U.,Teknia R&D, S.L., Componentes de Automoción Marroquíes

figures correspond to limited reviews, audited) of the most relevant subsidiaries with

industrial activity as of 31 December 2016:

Thousand of Euros

Teknia

Elorrio

Teknia

Pedrola Teknia Epila

Teknia

Barcelona

Teknia

Bilbao XXI

Teknia

Montmeló

Teknia

Martos

Teknia

Brasil

Teknia

Manresa Teknia KG

Total assets 10.293 7.780 2.145 10.796 10.138 2.692 13.749 16.792 12.815 1.461

Total Equity 4.186 1.504 1.016 2.446 3.256 868 5.110 8.800 6.533 971

Net turnover 20.020 11.784 2.036 23.489 16.435 3.563 30.329 20.565 24.279 1.507

Results from Operating expenses 1.730 128 192 1.243 515 568 3.120 (2.101) 3.018 25

Profit/ (Loss) for the period 1.505 83 168 877 254 409 2.338 (2.243) 2.369 25

Thousand of Euros

Teknia

Azuqueca

Teknia

Uhersky

Brod Teknia R&D

Teknia

Rzeszów

Teknia

Kálisz

Teknia

Automotive

Mexico

Teknia

Nashville

Component

es de

Automoción

Marroquies

Teknia Mexico

City

Total assets 18.751 20.929 499 15.748 23.647 9.521 19.614 2.911 3.072

Total Equity 6.147 11.096 59 7.384 6.256 3.239 9.305 375 1.228

Net turnover 42.425 25.350 825 22.989 25.063 10.029 20.469 2.874 4.083

Results from Operating expenses 2.190 2.585 (26) 2.524 265 (193) (152) 83 518

Profit/ (Loss) for the period 1.580 2.127 (26) 1.838 (347) (653) (54) 14 207

- 15 -

5. Strategy

The Company’s performance drivers have been:

- Geographical diversification: worldwide presence in the most important automotive

markets, enabling the Company to cover its clients’ needs in terms of quality, time

and costs. Currently, Teknia has 20 production plants (in nine countries), four

commercial offices, and five R&D centres that provide services to the whole Group.

The production plants are located in Spain (7), Brazil (3), Poland (2), USA (1),

Czech Republic (2), Morocco (1), Mexico (2), Serbia (1) and Turkey (1).

- Technological diversification: the Company specializes in the development and

manufacture of automotive components, assembly, and the design of specific

manufacturing processes. These services are carried out in three divisions: plastic,

metallic (including tubing and stamping), and machining. Additionally, Teknia has

an R&D division that supports the automotive business and enables the Group to

remain at the forefront of the industry.

- Close relationship with its major clients, which has led to the joint design of

international expansion strategies, in which Teknia has accompanied its clients as

a key supplier in new markets.

- Continuous growth: the company has made major strides in the commercial field,

with the opening of international sales offices, among others, in USA, Germany,

and South Korea, and a commercial office in China, with the goal of increasing

sales and enhancing its visibility with regard to international expansion. Moreover,

it has acquired over 20 companies during its existence, which, along with the

company’s growth, has enabled it to achieve its current size.

- 16 -

6. Financial information

The financial information presented in this Information Memorandum includes the

consolidated financial statements of Teknia Group for the years ended 31 December, 2015

and 31 December, 2016, which have been extracted from the audited consolidated annual

accounts of the Group for the years ended 31 December 2016 and 31 December 2015,

included in “Annex 1” and “Annex 2” of this Information Memorandum.

In addition, the individual audited annual accounts of the Subsidiary Guarantors for the

year ended 31 December 2016 have also been included as “Annex 3” to this Information

Memorandum.

The consolidated financial statements as of 31 December 2016 and 2015, have been

prepared from the accounting records of the Group and are presented in accordance with

the commercial legislation and the established rules in the General Accounting Plan

approved by Royal Decree 1514/2007 and the amendments made thereto by Royal Decree

1159/2010.

Certain data contained in this Information Memorandum, including financial information,

have been subject to rounding adjustments. Accordingly, in certain instances, the sum of

the numbers in a column or a row of the tables may not conform exactly to the total figure

given for that column or row, or the sum of certain numbers presented as a percentage

may not conform to the total percentage given.

- 17 -

Audited Consolidated Income Statement for the financial years ended on 31

December 2016 and 2015 (in thousands of Euros)

- 18 -

CO NSO LIDATED INCO ME STATEMENT

2016 2015 Var 16-15

A) CO NTINUING O PERATIO NS

1. Revenue 297.662 246.279 20,9%

a) Sales 294.979 245.031 20,4%

b) Services rendered 2.683 1.248 115,0%

2. Changes in inventories of finished goods and work in progress 2.389 1.048 128,0%

3. Work carried out by the company for own assets 1.100 572 92,3%

4. Supplies (166.666) (138.749) 20,1%

a) Merchandise used (8.847) (5.389) 64,2%

b) Raw materials and other consumables used (130.560) (109.850) 18,9%

c) Subcontracted work (27.217) (23.286) 16,9%

d) Impairment of merchandise, raw materials and other supplies (42) (224) -81,3%

5. O ther operating income 1.340 1.141 17,4%

a) Non-trading and other operating income 1.264 980 29,0%

b) Operating grants taken to income 76 161 -52,8%

6. Personnel expenses (65.646) (52.949) 24,0%

a) Salaries and wages (51.047) (40.877) 24,9%

b) Employee benefits expense (14.476) (12.024) 20,4%

c) Provisions (123) (48) 156,3%

7. O ther operating expenses (42.643) (36.925) 15,5%

a) Losses, impairment and charges in trade provisions (47) (326) -85,6%

b) Other operating expenses (42.596) (36.599) 16,4%

8. Amortisation and depreciation (9.787) (7.705) 27,0%

9. Non-financial and other capital grants 5 5 -

11. Impairment and gain/(losses) on disposal of fixed assets (19) 1.965 -101,0%

a) Impairments and losses - (317) -100,0%

b) Results due to divestment and others (19) 2.282 -100,8%

14. O ther results 135 141 -4,3%

A.1) RESULTS FRO M O PERATING ACTIVITIES

(1+2+3+4+5+6+7+8+9+10+11+12+13+14) 17.870 14.823 20,6%

15. Finance income 250 320 -21,9%

a) Dividends 3 3 -

b) Marketable securities and other financial instruments 10 99 -89,9%

c) Allocation of grants, donations and bequests of a financial nature 237 218 8,7%

16. Finance expenses (2.550) (1.688) 51,1%

18. Exchange gains/(losses) (1.079) (1.989) -45,8%

19. Impairment and profit/loss on divestment of financial instruments - (228) -100,0%

a) Impairments and losses - (228) -100,0%

A.2) NET FINANCE INCO ME/(EXPENSE) (14+15+16+17+18+19) (3.379) (3.585) -5,7%

A.3) PRO FIT/(LO SS) BEFO RE INCO ME TAX (A.1 + A.2 ) 14.491 11.238 28,9%

24. Income tax (3.521) (1.629) 116,1%

A.4) PRO FIT/(LO SS) FRO M CO NTINUING O PERATIO NS (A.3 +22) 10.970 9.609 14,2%

B) DISCO NTINUED O PERATIO NS - - -

A.5) CO NSO LIDATED PRO FIT/(LO SS) FO R THE PERIO D (A.4) 10.970 9.609 14,2%

Balance attributed to the parent company 10.987 9.659 13,7%

Balance attributed to external shareholders (17) (50) -66,0%

Thousand of Euros

- 19 -

Audited Consolidated Balance Sheet for the financial years ended on 31 December

2016 and 2015 (in thousands of Euros)

ASSETS

2016 2015 Var 16-15

A) NO N-CURRENT ASSETS 98.442 73.629 33,7%

I. Intangible fixed assets

1. Consolidated goodwill 6.661 2.495 167,0%

2. Research - -

3. Other intangible assets 2.910 2.833 2,7%

9.571 5.328 79,6%

II. Tangible fixed assets

1. Land and buildings 24.945 21.664 15,1%

2. Technical installations and other fixed material assets 47.933 31.517 52,1%

3. Fixed assets under construction and advances 1.276 3.284 -61,1%

74.154 56.465 31,3%

V. Long-term financial investments 2.542 501 407,4%

VI. Deferred tax assets 12.036 11.203 7,4%

VIII. Non-current trade receivables 139 132 5,3%

B) CURRENT ASSETS 115.014 90.597 27,0%

I. Non-current assets held for sale 220 -

II. Inventories 41.555 33.641 23,5%

III. Trade and other receivables

1 Trade receivables for sales and services 53.925 44.299 21,7%

2. Trade receivables from group companies and associates - 16 -100,0%

3. Current tax assets 663 1.109 -40,2%

4. Other receivables 3.247 2.225 45,9%

57.835 47.649 21,4%

IV. Current investments group companies and associates

1 Loans to related parties - 18 -100,0%

2. Other financial assets of group companies and associates - 3.345 -100,0%

- 3.363 -100,0%

V. Current investments 46 1 4500,0%

VI. Current accruals 1.082 1.082 0,0%

VII. Cash and other cash equivalents 14.276 4.861 193,7%

TO TAL ASSETS (A+B) 213.456 164.226 30,0%

Thousands of euros

- 20 -

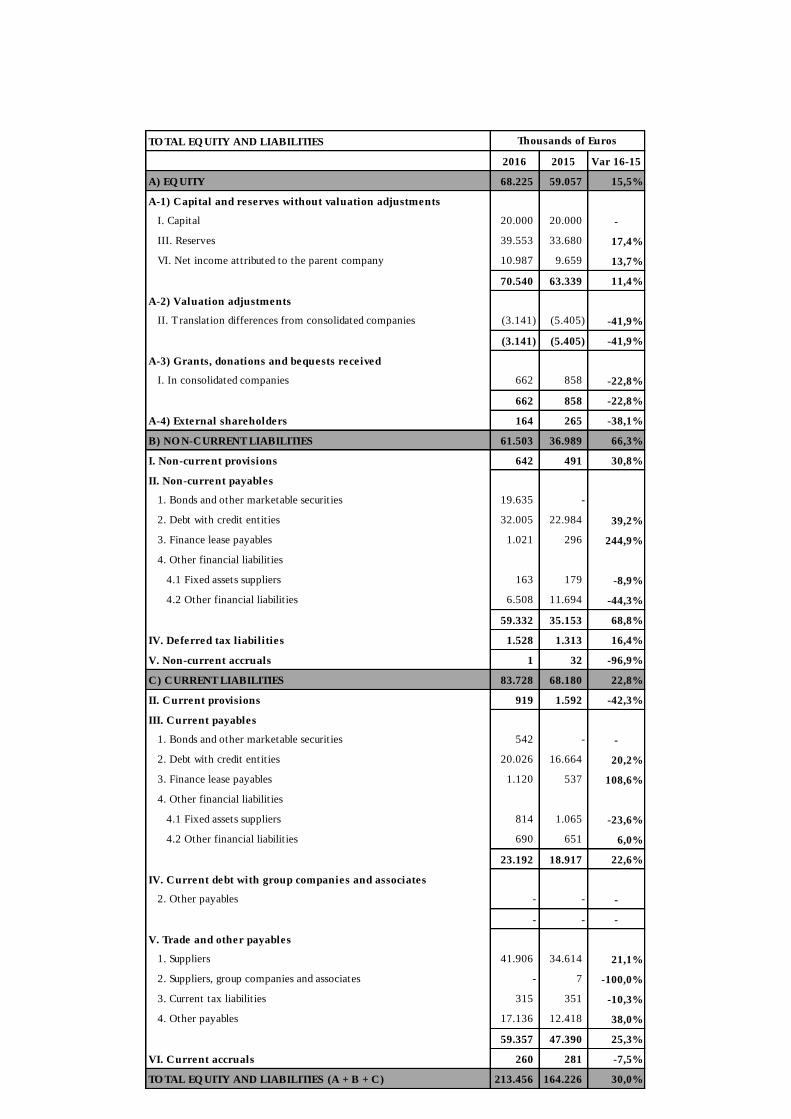

TO TAL EQ UITY AND LIABILITIES

2016 2015 Var 16-15

A) EQ UITY 68.225 59.057 15,5%

A-1) Capital and reserves without valuation adjustments

I. Capital 20.000 20.000 -

III. Reserves 39.553 33.680 17,4%

VI. Net income attributed to the parent company 10.987 9.659 13,7%

70.540 63.339 11,4%

A-2) Valuation adjustments

II. Translation differences from consolidated companies (3.141) (5.405) -41,9%

(3.141) (5.405) -41,9%

A-3) Grants, donations and bequests received

I. In consolidated companies 662 858 -22,8%

662 858 -22,8%

A-4) External shareholders 164 265 -38,1%

B) NO N-CURRENT LIABILITIES 61.503 36.989 66,3%

I. Non-current provisions 642 491 30,8%

II. Non-current payables

1. Bonds and other marketable securities 19.635 -

2. Debt with credit entities 32.005 22.984 39,2%

3. Finance lease payables 1.021 296 244,9%

4. Other financial liabilit ies

4.1 Fixed assets suppliers 163 179 -8,9%

4.2 Other financial liabilit ies 6.508 11.694 -44,3%

59.332 35.153 68,8%

IV. Deferred tax liabilities 1.528 1.313 16,4%

V. Non-current accruals 1 32 -96,9%

C) CURRENT LIABILITIES 83.728 68.180 22,8%

II. Current provisions 919 1.592 -42,3%

III. Current payables

1. Bonds and other marketable securities 542 - -

2. Debt with credit entities 20.026 16.664 20,2%

3. Finance lease payables 1.120 537 108,6%

4. Other financial liabilit ies

4.1 Fixed assets suppliers 814 1.065 -23,6%

4.2 Other financial liabilit ies 690 651 6,0%

23.192 18.917 22,6%

IV. Current debt with group companies and associates

2. Other payables - - -

- - -

V. Trade and other payables

1. Suppliers 41.906 34.614 21,1%

2. Suppliers, group companies and associates - 7 -100,0%

3. Current tax liabilit ies 315 351 -10,3%

4. Other payables 17.136 12.418 38,0%

59.357 47.390 25,3%

VI. Current accruals 260 281 -7,5%

TO TAL EQ UITY AND LIABILITIES (A + B + C) 213.456 164.226 30,0%

Thousands of Euros

- 21 -

Audited Consolidated Cash Flow Statements of the financial years ended on 31

December 2016 and 2015 (in thousands of Euros)

- 22 -

CO NSO LIDATED CASH FLO W STATEMENT

2016 2015 Var 16-15

A) CASH FLO WS FRO M O PERATING ACTIVITIES

1. Profit/(loss) for the period before tax 14.491 11.238 28,9%

2. Adjustments for 13.082 7.610 71,9%

a) Amortisation and depreciation (+) 9.787 7.705 27,0%

b) Valuation allowances for impairment losses (+/-) 973 233 317,6%

c) Changes in provisions (+/-) 270 430 -37,2%

d) Grants recognised in the income statement (-) (242) (5) 4740,0%

e) Proceeds from disposals of fixed assets (+/-) 19 (2.282) -100,8%

g) Finance income (-) (250) (320) -21,9%

h) Finance expenses (+) 2.550 1.688 51,1%

k) Other income and expenses (-/+) (25) 161 -115,5%

3. Changes in operating assets and liabilities (8.782) (3.940) 122,9%

a) Inventories (+/-) (6.624) (1.493) 343,7%

b) Trade and other receivables (+/-) (6.899) (3.345) 106,2%

c) Other current assets (+/-) (45) (266) -83,1%

d) Trade and other payables (+/-) 5.567 1.638 239,9%

c) Other current liabilit ies (+ /-) (770) (413) 86,4%

f) Other non-current assets and liabilit ies (+/-) (11) (61) -82,0%

4. O ther cash flows from operating activities (4.050) (4.346) -6,8%

a) Interest paid (-) (1.964) (1.319) 48,9%

c) Interest received (+) 250 102 145,1%

d) Income tax received (paid) (2.336) (3.129) -25,3%

5. Cash flows from/used in operating activities (+/-1+/-2+/-3+/-4) 14.741 10.562 39,6%

B) CASH FLO W'S FRO M INVESTING ACTIVITIES

6. Payments for investments (-) (21.409) (19.921) 7,5%

a) Group companies, net cash flows in consolidated companies (422) (3.473) -87,8%

d) Intangible assets (618) (876) -29,5%

e) Property, plant and equipment (19.551) (15.572) 25,6%

g) Other financial assets (818) -

7. Proceeds from sale of investment (+) 2.490 8.670 -71,3%

e) Property, plant and equipment 2.425 8.670 -72,0%

g) Other financial assets 65 -

8. Cash flows front/used in investing activities (6+7) (18.919) (11.251) 68,2%

C) CASH FLO WS FRO M FINANCING ACTIVITIES

9. Proceeds from and payments for equity instruments (215) 82 -362,2%

a) Issue of equity instruments (+) - 74 -100,0%

e) Acquisition of equity instrument from external shareholders (-) (215) -

g) Grants, donations and bequests received (+) - 8 -100,0%

10. Proceeds from and payments for financial liability instruments 17.438 (626) -2885,6%

a) Issue

1. Bonds and other marketable securities (+) 19.600 -

2. Debt with credit entities (+) 13.675 19.392 -29,5%

5. Other debts (+) 1.142 528 116,3%

b) Redemption and repayment of

2. Debts with financial institutions (-) (10.751) (18.616) -42,2%

5. Other payables (-) (6.228) (1.930) 222,7%

11. Dividends and interest on other equity instruments paid (3.630) (3.525) 3,0%

a) Dividends (-) (3.630) (3.525) 3,0%

12. Cash flows from/used in financing activities (+/-9+/-10-11) 13.593 (4.069) -434,1%

D) EFFECT O F EXCHANGE RATE FLUCTUATIO NS - -

E) NET INCREASE/DECREASE IN CASH AND CASH EQ UIVALENTS (+/-5+/-8+/-12+/-D) 9.415 (4.758) -297,9%

Cash and cash equivalents at the beginning of the period 4.861 9.619 -49,5%

Cash and cash equivalents at the end of the period 14.276 4.861 193,7%

Thousands of Euros

- 23 -

Financial ratios as of 31 December 2016 and 2015:

III. RISK FACTORS

The following are the risks to which Teknia Group is exposed, including those arising

from the business areas in which it operates, as well as those specifically related to

its business. The materialization of any of these risks could have a negative effect on

its business, financial position, and the results of Teknia Group operations, and

subsequently the nominal and/or interest that investors receive for the Notes.

Prospective investors should carefully consider the risks described below in

conjunction with other information contained in this document. In addition, these

risks are not the only ones to which the Issuer could be exposed; it may be the case

that risks which are currently unknown or not considered relevant at this time could

materialize in the future.

2016 2015

PERFORMANCE

EBT / Total Assets 6,8% 6,8%

Turnover / Total Assets 139,4% 150,0%

ROA (OP/Total assets) 8,4% 9,0%

ROE 16,1% 16,3%

Net Result / Turnover 3,7% 3,9%

EBITDA / Turnover 9,3% 9,1%

BALANCE STRUCTURE

Equity / Total Debt 47,0% 56,2%

Total Debt/ Total Equity and Liabilities 68,0% 64,0%

Non Current Liabilities / Current Liabilities 73,5% 54,3%

Cash and similar / Total Debt 9,8% 4,6%

Net Financial Debt / EBITDA (1)

2,47 2,18

Consolidated Profit for the Period / Financial Cost (2)

4,77 6,02

Bank Financial Debt / Total Debt 37,3% 38,5%

SHORT TERM STABILITY

Current Assets / Current LiabiIities 137,4% 132,9%

Current Assets - Inventories / Current Liabilities 87,7% 83,5%

Current Assets / Total Assets 53,9% 55,2%

(1) Net Debt includes all debt (M&A deferred payments included)

(2) Financial cost: Forex cost not included

- 24 -

1. Risks related to the Issuer’s Industry and Business

1. The automotive industry is cyclical, and cyclical downturns in our business

segments negatively impact our business, financial position, results of

operations, and cash flows

The volume of automotive production and the level of new vehicle purchases are

cyclical and fluctuate, sometimes significantly year-on-year. These fluctuations

are caused by several factors, such as general economic conditions, interest rates,

consumer confidence, patterns of consumer spending, fuel costs, and the

automobile replacement cycle. Such fluctuations give rise to changes in demand

for our products and may have a significant adverse impact on our results of

operations. Additionally, TIER 2 customers commit to purchasing minimum

quantities from their suppliers, but since the economic crisis, their budget gaps

have increased. As our business has certain fixed costs that must be met regardless

of product demand, cyclical downturns can further affect the results of our

operations.

The highly cyclical and fluctuating nature of the automotive industry presents a

risk that is beyond our control and that cannot be accurately predicted. Moreover,

a number of factors that we cannot anticipate could, and have had cyclical effects

in the past. Decreases in demand for automobiles generally, or in the demand for

automobiles that use our products specifically, could materially and adversely

affect our business, financial position, the results of operations, and cash flows.

2. Our business is primarily contingent upon the automotive industry, which is

affected by global economic conditions and geopolitical considerations

A significant economic downturn could have a material adverse effect on our

business. Continued concerns about the systemic impact of a potential long-term

wide-spread recession, energy costs (including the recent volatility in oil prices),

the availability and cost of credit, diminished business and consumer confidence,

and increased persistent unemployment in Europe have contributed to a rise in

market volatility and lower expectations for Western and emerging economies.

Recent macroeconomic data points to a potential slowdown in the emerging

markets economies, a fact that would impact the global automotive industry,

lowering its sales forecast and thus, challenging Teknia Manufacturing Group’s

capacity to meet its business plan.

In addition, any increased financial instability may lead to longer-term disruptions

in the credit markets, which could impact our customers’ ability to obtain

financing for their businesses at reasonable prices, and could impact their

customers when seeking financing for automobile purchases. Our TIER 1 and

OEMs customers typically require significant financing for their respective

businesses. Our suppliers, as well as the other players that supply our customers,

may face similar difficulties in obtaining financing for their businesses.

- 25 -

If capital is not available to our customers and suppliers, or if its cost is

prohibitively high, their businesses would be negatively impacted. Any such

negative impact, in turn, could have an adverse material impact on our company,

either through the loss of revenues to any of our customers so affected, or due to

our inability to meet our commitments without excess expense resulting from

disruptions in supply caused by the suppliers so affected. Financial difficulties

experienced by any major customer could have a material adverse impact on us if

such customer i) were unable to pay for the products we provide, ii) materially

reduced its capital expenditure, and resulting demand for, new product lines, or

iii) we otherwise experienced a loss of, or material reduction in, business from

such customer.

Additionally, protectionist pressures have been rising worldwide, as signaled by

policy statements and opinion polls, as well as by recent developments in

multilateral, regional and bilateral trade negotiations.

The risk of a resurgence of protectionism in the aftermath of the financial crisis

should not be neglected. A resurgence of trade protectionism would not only

significantly impair the global recovery process by further hampering trade flows

and global demand but it would also reduce the global growth potential in the long

run.

As a result of such difficulties, we could experience lost revenues, significant

write-offs of accounts receivable, significant impairment charges, or additional

restructurings beyond the steps taken to date.

3. Geopolitical risks could result in the break-up of the European Union (EU)

In the automotive industry, the European market is one of the most important and

mature. On the other hand, this sector is highly dependent on the ability to finance

companies and individuals. These characteristics make it sensitive to a

hypothetical breakdown of the EU because (i) would have to redesign the

allocation of production units in order to ensure supply industry (ii) probably

would be a new financial crisis that could influence negatively in vehicle purchase

decisions and therefore directly impact on sales and production.

If it happens, it could materially and adversely impact our business, financial

condition, results of operations and cash flows.

4. We operate in a very competitive business environment

Despite the industry’s entry barriers, there are a variety of competing actors who

are reduced to local players in the presence of global suppliers. Each has its

competitive advantages, and the goal is to continue to grow, pro-market in the

case of emerging countries, or at the expense of competitors in more mature

markets. This implies that we must maintain very high standards of quality,

engineering, research and development, logistics, costs and financial solvency.

- 26 -

5. Limited international positioning

The segment of second-tier suppliers has the characteristic of operating as a link

between two large sectors: commodities suppliers (as suppliers) and 'Tier 1'

suppliers and OEMs as customers. These segments are also more mature and with

higher level of concentration. In this competitive environment, there are large

multinational companies of large size and influence in the economy which have a

high bargaining power over Tier 2 companies. The company is gradually

increasing its international footprint and getting strategic position in certain

markets and products. Nevertheless, sometimes the company could be in a weak

negotiation position that could negatively impact in results of operations and cash

flows.

6. A significant decline in business with our key customers could adversely affect

our business, financial position, and the results of operations

Although we supply our products to several leading automobile manufacturers, as

is common in our industry we depend on certain large-value customers for a

significant proportion of our revenues. For example, 2016’s total annual sales

-BOSCH 15%, JCI 6%, CONTINENTAL 7%, VALEO 8%, RENAULT-NISSAN

4%, AUTOLIV 4%, TRW/ZF 4%- would represent 48% of the estimated revenue.

The loss of all or a substantial portion of our sales to any of our large-volume

customers could have a material adverse effect on our business, financial position,

or the results of operations, by reducing cash flows and limiting our ability to

spread our fixed costs over a larger revenue base. We may make fewer sales to

these customers for a variety of reasons, including, but not limited to:

• Loss of awarded business;

• Reduced or delayed customer requirements;

• TIER 2s sourcing business traditionally outsourced to us;

• Strikes or other work stoppages affecting our customers’ production;

• Bankruptcy or insolvency of a customer; or

• Reduced demand for our final customers’ products.

7. We are dependent on the ability to obtain and maintain sufficient capital

financing, including working capital lines and credit insurance, which impacts

the liquidity and financial position of all players

Our working capital requirements can vary significantly, depending in part on the

level, variability and timing of our customers’ worldwide vehicle production and

the payment terms with our customers and suppliers.

- 27 -

Moreover, if our suppliers were to suspend normal trade credit terms and require

payment in advance or payment on delivery. If our available cash flows from

operations are not sufficient to fund our ongoing cash needs, we would be required

to look to our cash balances and availability for borrowings under our credit

facilities to satisfy those needs, as well as potential sources of additional capital,

which may not be available on satisfactory terms and in adequate amounts, if at

all.

There can be no assurance that we, our customers, and our suppliers will continue

to have such ability. This may increase the risk that we will be unable to produce

our products or will have to pay higher prices for our inputs. These higher prices

may not be recovered in our sales prices.

Our suppliers often seek to obtain credit insurance based on the strength of the

financial position of our subsidiary with the payment obligation, which may be

less robust than our consolidated financial position.

Access to funding could also be adversely impacted as Central Banks around the

world begin to withdraw liquidity from global markets because of the improving

growth and higher inflation expectations.

If we were to experience liquidity issues, our suppliers may not be able to obtain

credit insurance and, in turn, would likely not be able to offer us the payment

terms we have received historically. Our failure to receive such terms from our

suppliers could have a material adverse effect on our liquidity.

8. Risks related to Research and Development (R&D) project success

Teknia has a R&D division that provides services such as: product development,

prototype manufacturing, and simulations for the automotive business.

In 2016, the Group allocated EUR 1,978 thousand to research and development

projects (according to Spanish tax regulation), with dedicated 11 employees. This

amount is pending to be accredited by a certification entity approved by Entidad

Nacional de Acreeditación (ENAC). Teknia relies on this division to ensure one

of the most updated product ranges in the industry with cutting-edge technology

in its three divisions, and to be a true partner for its clients rather than a mere

provider.

The Strategic Plan includes allocating the expenses incurred by the Company’s

R&D projects.

The allocation of these expenses is constrained by the following aspects:

• The expenses have to be specifically itemized by project and the related costs

clearly identified so that they can be allocated over time.

- 28 -

There must be sound reasons for believing in the technical success and economic-

commercial profitability of the project(s). In the event of non-compliance with

any of these conditions, the Company may not be able to allocate all of the

expenses anticipated in the Strategic Plan.

9. Risk of loss of key personnel

We have a management team with a substantial amount of expertise in the

automotive industry. The departure of key members of management could result

in the loss of valuable know-how and/or less or unsuccessful implementation of

strategies.

10. Risk linked with post-merger integration and synergies of the companies

acquired

We have made strategic acquisitions and divestitures, and may consider or

undertake further acquisitions in the future. We may also consider or undertake

strategic divestitures when they are aligned with our strategy.

However, we may not be able to identify suitable acquisition candidates in the

future, or may not be able to close acquisitions on favourable terms. We may lack

sufficient management, financial and other resources to successfully integrate

future acquisitions or to ensure that such future acquisitions will perform as

planned or prove to be beneficial to our operations. We may not be offered suitable

terms, including price, for the divestitures we wish to make. Acquisitions and

divestitures involve numerous other risks, business concerns, undisclosed risks

impacting the target, and potential adverse effects on existing business

relationships with current customers and suppliers. In addition, any acquisitions

or divestitures could affect our financial position, cash flow or create dilution for

our stockholders. In certain transactions, our acquisition analysis includes

assumptions regarding the consolidation of operations and improved operating

cost structures for combined operations. Such synergies or benefits may not be

achieved according to the anticipated schedule or in the anticipated amount, if at

all. Any future acquisitions may result in significant transaction expenses,

unexpected liabilities, and risks associated with entering new markets, in addition

to integration and consolidation risks.

As a result of our acquisitions or divestments, we may assume continuing

obligations, deferred payments, and liabilities. Any past or future acquisitions may

result in exposure to third parties for liabilities, such as liability for faulty work

done by the acquired business, and liability of the acquired business or assets that

may or may not be adequately covered by insurance or by indemnification, if any,

from the former owners of the acquired business or assets. In connection with

divestitures, we may remain exposed to the buyer for tax or environmental

purposes, or other liabilities of the divested business. The occurrence of any of

these liabilities could have a material adverse effect on our business and the results

of operations.

- 29 -

11. We base our strategy on investing substantial resources in markets where we

expect growth and take the time to alter this strategy in case expectations are

not realized

Our future growth is dependent on us making the right investments at the right

time to support product development and manufacturing capacity in areas where

we can support our customer base. We have identified certain markets, including

NAFTA, ASIA, Turkey, Japan and PACIFIC AREA, as key markets where we

are likely to experience substantial growth, and accordingly have made, and

expect to continue making, substantial investments, both directly and through

participation in various partnerships and joint ventures to support anticipated

growth in those regions. If we are unable to expand customer demand in these

regions, we may not only fail to achieve the expected rates of return on our

existing investments, but we may incur losses on such investments and be unable

to redeploy the invested capital in a timely manner to take advantage of other

markets, potentially resulting in lost market share. Our results will also suffer if

these regions do not grow as quickly as we anticipate.

12. Other risks of doing business in foreign countries

International operations are subject to various risks that could have a material

adverse effect on those operations and our business as a whole, including but not

limited to:

o Exposure to local economic and social conditions, including logistical and

communication challenges;

o Exposure to local political conditions;

o Exposure to local public health issues and the resulting impact on economic

and political conditions;

o Exposure to potentially undeveloped legal systems, which make it difficult

to enforce contractual rights; and exposure to potentially adverse changes in

laws and regulatory practices;

o Exposure to local tax requirements and obligations;

o Foreign currency exchange rate fluctuations and currency controls;

o Greater risk of uncontrollable accounts and longer collection cycles;

o The necessity of foreign representatives and/or consultants;

o The risk of government sponsored competition;

o The difficulty of managing and operating an enterprise spread over various

countries;

o Controls on the repatriation of cash, including the imposition or increase of

withholding and other taxes on remittances and other payments by foreign

subsidiaries; and

o Export and import restrictions.

13. Our success depends in part on our ability to leverage our engineering

capabilities, as well as research and development initiatives to pursue new

business opportunities

- 30 -

Typically, the terms and conditions of the agreements with our customers include

a commitment regarding minimum purchase volumes from us. However, such

contracts routinely state that customers have the contractual right to unilaterally

terminate our contracts with them with no notice or limited notice. If such

contracts are terminated by our customers, our ability to obtain compensation from

our customers for such termination is generally limited to the direct out-of-pocket

costs that we incur for materials, works-in-progress, and in certain instances,

underappreciated capital expenditures and tooling. Further, there is no guarantee

that our customers will renew their purchase orders with us. We cannot assure you

that the results of our operations will not be materially and adversely impacted in

the future if we are unable to realize revenues from our awarded business, if our

customers cancel the awarded business or if our customers fail to renew their

contracts with us.

14. Infringement of intellectual property license rights and the failure to protect the

Group’s intellectual property may adversely affect our business

We believe that we either own or may validly use all of the intellectual and

industrial property rights required for our business operations, and that we have

taken all reasonable measures to protect our rights or obtain warranties from the

owners of third party rights. However, we cannot rule out the risk that our

intellectual and industrial property rights may be disputed by a third party on the

grounds of pre-existing rights or for any other reason. Furthermore, for countries

outside of Europe and North America, we cannot be sure of holding or obtaining

intellectual and industrial property rights that offer the same level of protection as

those in Europe and North America.

15. We may not realize all of the sales expected from our entire order backlog

Although not a common occurrence, occasionally some projects in the backlog do

not end in production and sales. This may be due to different reasons: i) projected

drop in vehicle sales, ii) changes in strategic production decisions, iii) faulty

planning and design tools, and iv) other unforeseen circumstances. At the same

time, investment in productive capacity can be made before any changes in the

production schedule, resulting in poorly sized assets.

Moreover, during the industrialization process of an order (usually 6-18 months),

we may realise the infeasibility of the project. In the majority of cases, this is

discussed and resolved with the customer and with the appropriate joint actions.

In others cases, however, we have to decide cease production on the project.

All these circumstances may cause a decline in sales compared with the provisions

and the profitability of the company.

16. Increases in labour costs, potential labour disputes and work stoppages at our

facilities and the facilities of our suppliers or customers could materially

adversely affect our financial performance

- 31 -

We have specific exposure to labour strikes at our companies, mainly in

international operations. For example, in 2014, we had a strike at our plant in

Jacarei, Brazil due to a dispute regarding a 10% wage increase (the Brazilian

Subsidiary is not profitable). If major work disruptions involving our employees

were to occur, our business could be adversely affected by a variety of factors,

including a loss of revenues, increased costs and reduced profitability. We cannot

assure that we will not experience a material labour disruption at one or more of

our facilities in the future. We cannot guarantee that we will be able to successfully

extend or renegotiate our collective bargaining agreements as they expire from

time to time. If we fail to extend or renegotiate any of our collective bargaining

agreements or are only able to renegotiate them on terms that are less favourable

to us, we may need to incur additional costs, which could have a material adverse

effect on our business, financial position, and the results of operations.

Furthermore, many of the manufacturing facilities of our customers and suppliers

are unionized and are also subject to the risk of labour disruptions. A significant

labour disruption could lead to a lengthy shutdown of our customers’ or our

suppliers’ production lines, which could have a material adverse effect on our

operations and profitability.

17. Our business is subject to environmental, health and safety laws and regulations,

and our ongoing operations may expose us to related liabilities

The nature of our operations subjects us to various statutory compliance and

litigation risks under health, safety and employment laws. Although we make

continuous efforts to comply with regulations, we cannot guarantee that there will

be no accidents or incidents suffered by our employees, our contractors, or other

third parties on our sites. If any of these incidents occur, we could be subject to

prosecution and litigation, which may lead to the imposition of fines, penalties,

and other damages, and may harm our reputation. Such events could have a

material adverse effect on our business, financial position, and operational results.

18. Delivery interruptions of raw materials or components, or an increase in prices

could impact our manufacturing process

We depend on regular deliveries from particular suppliers of components and raw

materials. The foregoing means that interruptions or stoppages in such deliveries

could materially and adversely affect our operations until an alternative is found.

In addition, we may not be able to find acceptable alternatives, and any such

alternatives could result in increased costs and potential losses on certain contracts.

Even if acceptable alternatives are found, the process of locating and securing

such alternatives might be disruptive to our business and might lead to the

termination of supply agreements with our customers.

If any of our suppliers fail or refuse to deliver materials to us for an extended

period of time, or if we are unable to negotiate acceptable terms for the supply of

materials with these or alternative suppliers, our business could suffer. We may

- 32 -

not be able to find acceptable alternatives, and any such alternatives could result

in increased costs and potential losses on certain contracts. Even if acceptable

alternatives are found, the process of locating and securing such alternatives might

be disruptive to our business and might lead to the termination of supply

agreements with our customers.

We depend on the ability of our suppliers to provide materials and components

that meet our customers’ technical specifications, quality standards, and delivery

schedules.

19. Our operations depend on our ability to maintain continual, uninterrupted

production at our manufacturing facilities, as well as the continual,

uninterrupted performance of our information technology (“IT”) system

Like any industrial society, the maintenance of production equipment is essential

for the proper functioning of the business. This investment requires dedication

and funding. However, we cannot guarantee that our efforts can prevent any event

that could result in production problems.

On the other hand, the increasingly intense need for better

management/production information systems is a key business element. Moreover,

many customers require us to share information systems (Case EDI) with

commercial, technical, and logistics areas. Teknia is investing in IT systems and

implementing an adequate Enterprise Resource Planning (“ERP”) throughout the

Group to ensure the quality and easy management of the information.

If any of these key elements suffers a loss, it could cause problems in the

production and shipping of parts and therefore affect profitability.

20. Product liability claims and recall costs could harm profitability and damage

our reputation

We face an inherent business risk of exposure to product liability claims in the

event of the failure of our products to perform to specifications, or if our products

are alleged to result in property damage, bodily injury or death. We are generally

required under our customer contracts to indemnify our customers for product

liability claims concerning our products. Accordingly, we may be materially and

adversely impacted by product liability claims.

If any of our products are, or are alleged to be, defective, we may be required to

participate in a recall involving those products. In addition, our customers demand

that we bear the cost of the repair and replacement of defective products, which

are either covered under warranty or are the subject of a recall.

Warranty provisions are established based on our best estimate of the amounts

necessary to settle existing or probable claims on product defect issues. Recall

costs are costs incurred when government regulators or our customers decide to

recall a product due to a known or suspected performance issue and we are

- 33 -

required to participate either voluntarily or involuntarily. Currently, under most

customer agreements, we only account for existing or probable warranty claims.

We have no warranty and recall data that allows us to establish accurate estimates

of, or provisions for, future warranty or recall costs relating to new products,

assembly programmes, or technologies being brought into production. In addition,

our insurance covering product recalls is limited in amount and coverage and in

some jurisdictions non-existent. The obligation to repair or replace such products

could have a material adverse effect on our profitability and financial position.

A decrease in the actual and perceived quality of our products could damage our

image and reputation, as well as the image and reputation of one or more of our

brands. Defective products could result in loss of sales, loss of customers and loss

of market acceptance. In turn, any major defect in one of our products could also

have a material adverse effect on our reputation and market perception, which in

turn could have an adverse effect on our sales and the results of our operations.

21. Increased capital expenditure requirements for our ongoing operations will

consume cash from our operations and borrowings

Our ability to undertake such operational and maintenance measures largely

depends on the cash flow from our operations and our access to capital. We intend

to continue to fund our cash needs through cash flows from operations.

However, there may be unforeseen capital expenditure needs for which we may

not have adequate capital. The timing of capital expenditures may also cause

fluctuations in our operational results.

22. Our inability to offset price concessions or additional costs from our customers

could negatively impact our profitability

We face continual pricing pressure, in addition to pressures to absorb costs related

to product design and engineering, as well as other items previously paid for

directly by TIER 1, such as tooling. Typically, in line with our industry practice,

our customers benefit from price reductions during the lifecycle of a contract. We

expect to offset these price concessions by achieving production efficiencies;

however, we cannot guarantee that we will do so. If we fail to achieve production

efficiencies that fully offset price concessions or do not otherwise offset such price

concessions, our profitability and the results of our operations could be adversely

affected.

23. A breach of the covenants of our Notes or financing contracts could adversely

affect our financial position

This Programme contemplates several covenants that the Teknia Group has to

meet at the end of the period. Such covenants are reflected in section 8 of the

Information Memorandum.

- 34 -

Additionally, the Teknia Group has Notes, Commercial Paper and financing

contracts amounting to EUR 82,52 million (excluding market interest

adjustments for interest-free loans) as of 31 December 2016. This financing

requires the Teknia Group to meet during its term, mainly, covenants related to:

i) the indebtedness ratio (net financial debt/Consolidated EBITDA), and ii) the

solvency ratio (equity/financial debt).

Any breach of the covenants of the Notes or syndicated loan terms may require

the Teknia Group to repay the Notes or syndicated loan early, which may

adversely affect our business, its results, or its financial, economic or equity

situation.

24. Shareholding concentration situation

The Company has an ownership structure concentrated on one partner (and

founder) almost since its inception. This situation limits the ability, if necessary,

to obtain funds from shareholders in a hypothetical distress situation. The

Company also faces the usual risks associated with a possible succession process.

Although it is not close in time, it could rush in case of an event or incident. It

could distract the management, the shareholders, and impact negatively in

strategic targets of the company, and therefore, in the growth, results and cash

flows generation.

25. The value of our deferred tax assets could become impaired, which may

materially and adversely affect our operating results

The deferred tax assets included as of December 2016 are related with net

operating loss carry forwards and non-used tax deductions that can be used to

offset taxable income in future periods and reduce the income taxes payable in

those future periods. Our ability to utilize our net operating loss carry forwards

may be limited or delayed. We periodically determine the probability of the

realization of deferred tax assets, using significant judgments and estimates with

respect to, among other things, historical operating results, expectations of future

earnings, and tax planning strategies. If we determine in the future that there is not

sufficient evidence to support the valuation of these assets, due to the factors

described above or other factors, we may be required to adjust the valuation

allowance to reduce our deferred tax assets. Such a reduction could result in

material non-cash expenses in the period during which the valuation allowance is

adjusted and could have a material adverse effect on the results of our operations.

In addition, adverse changes in the underlying profitability and financial outlook

of our operations in several foreign jurisdictions could lead to changes in our

valuation allowances against deferred tax assets and other tax accruals that could

adversely affect our financial results.

Finally, the Company and some of its Spanish subsidiaries and holding companies

form a tax group subject to the special tax consolidation regime for corporate

income tax purposes. If, for whatever reason, the consolidated tax regime were

forfeited or the tax group extinguished, the right to offset the tax loss carry

- 35 -

forwards and use the tax credits of the tax group would be assigned to the

companies that generated them. This could limit the ability of the companies to

effectively make use of these deferred tax assets and that could adversely affect

our financial results.

26. Our profitability may be adversely affected by our inability to utilize tax losses

in certain jurisdictions

We have incurred losses in some countries in which we may not be able to partially

offset against income we have earned therein. In some cases, we may not be able

to utilize these losses at all if we cannot generate profits in those countries or if

we have ceased conducting business in those countries altogether. Our inability to

utilize material tax losses could materially and adversely affect our profitability.

At any given time, we may face other tax exposures arising from changes in tax

laws, tax reassessments or otherwise. To the extent that we cannot implement

measures to offset these exposures, they may have a material adverse effect on

our profitability.

This could limit the ability of the companies to effectively make use of these

deferred tax assets and that could adversely affect our financial results.

27. We are subject to a complex local and international tax environment that often

requires us to make subjective determinations (i.e. Transfer pricing,

international and local laws, regulations and criteria)

We are subject to many different forms of taxation including but not limited to

income tax, value added tax, social security, and other payroll-related taxes. Tax

law and administration is complex and often requires us to make subjective

determinations. The tax authorities may not agree with the determinations that we

make with respect to the application of tax law. Such disagreements could result

in lengthy legal disputes and, ultimately, in the payment of substantial amounts of

tax, interest, and penalties, which could have a material effect on the results of our

operations.

28. At certain times, we may not be adequately insured

We currently have insurance arrangements in place for products and public

liability, property damage, business interruption (including for sudden and

unexpected environmental damage). However, these insurance policies may not

cover losses or damages resulting from the materialization of any of the risks we

are subject to. Furthermore, significant increases in insurance premiums could

reduce our cash flow. It is also possible that, in the future, insurance providers

may no longer wish to insure businesses in our industry against certain

environmental occurrences.

- 36 -

29. Significant changes in laws and governmental regulations could have an

adverse impact in our profitability

The legal, regulatory, and industry standard environment in our principal markets

is complex and dynamic, and future changes to the laws, regulations and market

practices concerning, for example, CO2 emissions and safety tests and protocols,

could have an adverse effect on the products we produce and our profitability.

Additionally, we could be adversely affected by changes in taxation or other laws

and jurisprudence which impose additional costs on automobile manufacturers or

consumers, or more stringent fuel economy and emissions requirements on

manufacturers from which we derive some of our sales.

30. Terrorism, other acts of violence, wars or political changes in geographical

areas where we operate may affect our business and results

Terrorism, other acts of violence, or war may negatively affect our business and

the results of our operations. There can be no assurance that there will not be

terrorist attacks or violent acts that may directly affect us, our customers, or

partners. In addition, political changes in certain geographical areas where we

operate may affect our business and the results of operations. Any of these

occurrences could cause a significant disruption in our business and could

adversely affect our business operations, financial position, and operational results.

31. Natural catastrophe affecting any of our plants

The Company’s plants are exposed to natural disasters. Should a natural disaster

occur, the effect could damage part or all of the machinery and thus cease

production for a certain period of time. In this case, the Company may have to

assume high costs to repair or substitute the affected equipment in order to restore

production. Such events could have a material adverse effect on our business

operations, financial position, and operational results.

32. We may be subject to current or future restrictions on the transfer of funds

Under the current foreign exchange regulations in certain countries in which we

operate, there are restrictions on the transfer of funds to and from such countries,

which may include restrictions on the disposition of funds deposited with banks

and restrictions on transferring funds abroad, and may require official approval to

buy foreign currency. Additionally, we have trapped cash in certain jurisdictions

in which we operate in relation to our joint ventures and local law. These

restrictions could impact the payment of dividends to us by certain of our

subsidiaries. If we were unable to repatriate funds from any such countries, we

would not be able to use the cash flow from our businesses to finance our operating

requirements elsewhere and satisfy our debt obligations, including the Notes.

33. The automotive industry’s reputation is at risk due to recent events involving

the manipulation of vehicle emission software

- 37 -

Given the strict legislation in automotive sector and high level of quality, from

time to time a global loss may occur (for instance, TAKATA Corp. is facing the

most important recall in history). In addition other type of events, as Volkswagen

Group admission to having installed software to manipulate the emission readings

of US Environmental Protection Agency tests, could deteriorate reputation of

those companies and its supply chain. As of now, it is uncertain how much those

events will impact in our business or the car industry in general. One thing is sure;

the world no longer considered the companies in this sector to be reliable, efficient,

and trustworthy.

Our activity depends greatly on the automotive industry. If this industry lowers its

sales forecast and thus its production levels due to reputation problems, Teknia

could see some of their future deliveries compromised and their financial results

affected. The results could result in the failure to achieve the projected business

plan.

34. The Catalan situation may adversely affect our business in Catalonia

In connection with the political situation in Catalonia, although the recent

measures taken by the Spanish Government have helped to mitigate the

uncertainty level in that region, originated by a movement seeking independence,

to the date of registration of this Information Memorandum, there is still some

uncertainty on the outcome of the political and economic outlook in Catalonia,