tender - janata · web viewthe bidder is expected to provide training for any other third...

TRANSCRIPT

TenderFor

Supply, Customization, Installation, and Commissioning

of Centralized Real Time On-Line Banking System, Related

Training and Technical Support for Janata Bank Limited on Turn

Key Basis as an On Going Process

(Single-Stage Bidding)

Contract Package N0. G-9.1(JB)

PART-B

Janata Bank LimitedInformation Technology Division

Head Office (22nd Floor)Janata Bhaban

110, Motijheel C/A, DhakaTelephone: +88(0)-2-9553339,

1

Email: [email protected]: www.janatabank-bd.com

PART-B

SECTION VI. TECHNICAL REQUIREMENTS (INCLUDING IMPLEMENTATION SCHEDULE)

2

Table of Contents: Technical Requirements

Background................................................................9Business Function and Performance Requirements.....16Schedule of Requirement...........................................37Technology Requirements..........................................38Functional and Technical Requirements......................44Design, Implementation Methodology and Deliverables…………….............193

System Management, Administration and Security Requirements…………194

Implementation Schedule....................................…..198Required Format of Technical Bids............................201Attachments...........................................................................208

3

Notes on the preparation of the Technical Requirements

The Technical Requirements should include all the technical details that Bidders need, in

combination with the Implementation Schedule and the supporting System Inventory Tables, to

prepare realistic, responsive, and competitive bids.

The Technical Requirements should, as much as possible, be based on and expressed in

terms of the Purchaser’s business, rather than technological needs. This leaves it up to the market

to determine what specific Information Technologies can best satisfy these business needs.

Nevertheless, in the case of a relatively straight-forward Information System, where the business

needs have been clearly linked to technological requirements, it would be acceptable to prepare

Technical Requirements that describe technologies known to satisfy those business needs. Even in

these cases, however, the requirements must be vendor neutral and specified to elicit the widest

range of possible technical responses.

References to brand names, catalog numbers, or other details that limit the source of any

item or component to a specific manufacturer should be avoided. Where such references are

unavoidable, the words “or substantially equivalent” should be added to permit Bidders to bid

equivalent or superior technologies. Only in the most exceptional circumstances may Bidders be

required to offer brand-name items and the equivalency clause be omitted. Bank’s consideration

for exception requires that:

(a) A brand-name component appears to have no equivalent or superior alternative,

because of its unique ability to reliably interoperate with a relatively large base of

existing technologies, to conform with the Purchaser’s adopted technological

standards, and to offer overwhelming savings in terms of avoided costs for

retraining, data conversion, macro / business template redevelopment, etc.;

(b) The Bank has agreed in advance, during project preparation, that such brand-name

restrictions are warranted; and

(c) Such brand-name components are the absolute fewest possible and each

component has been explicitly identified in the Bid Data Sheet for ITB

Clause 16.3.

Similarly, where national standards or codes of practice are specified, the Purchaser should

include a statement that other national or international standards “that are substantially equivalent”

will also be acceptable.

To help ensure comparable bids and ease Contract execution, the Purchaser’s requirements

must be stated as clearly as possible, with minimum room for differing interpretations. Thus,

wherever possible, technical specifications should include definitive characteristics and

quantifiable measures. If technical characteristics in a specific range, or above or below specific

4

thresholds, are required, then these should be clearly specified. For example, the expandability of

a server should be stated as “no less than four processors.” Technical specifications that state only

“four processors” creates unnecessary uncertainty for Bidders regarding whether or not, for

example, a server that could be expanded up to six processor boards would be technically

responsive.

Quantitative technical specifications must, however, be employed with care. They can

dictate technical architectures and, thus, be unnecessarily restrictive. For example, a quantitative

requirement for the minimum width of the data path in a processor may be unnecessarily

restrictive. Instead, a specification of a required level of standard performance benchmark test

may be more appropriate, allowing different technical approaches to achieving the Purchaser’s

functional and performance objectives. In general, the Purchaser should try to use widely accepted

direct measures of performance and functionality whenever possible and carefully review

specifications for those that might dictate technical architectures.

It is important that the Requirements clearly identify which are mandatory features (for

which a bid’s nonconformance might require rejection for non-responsiveness) and which are

preferable features that can be included or excluded from a bid at the Bidder’s option. To enhance

the clarity of the specifications, Purchasers are advised to use the word “MUST” (in bold capitals)

in sentences describing mandatory requirements. The Technical Responsiveness Checklist is also

a useful device to ensure that mandatory and preferred features are clearly indicated.

This section of the SBD contains a sample outline that will help Purchasers organize and

present in a comprehensive way both the business purpose and technical characteristics of the

System to be supplied and installed. The major sections are:

(A) Background (description of the project, history, and structure of the agency,

purpose of the System, etc.)

(B) Business Function and Performance Requirements

(C) Technical Specifications

(D) Testing Requirements

(E) Implementation Schedule

(F) Required Format for Technical Bid

(G) Technical Responsiveness Checklist

(H) Attachments (e.g., drawings of site premises, descriptions of existing technologies,

sample data, and reports, etc.)

Preparation of the Implementation Schedule in Chapter E warrants further explanation and

guidance.

5

Notes on preparation of the Implementation Schedule

The Implementation Schedule presents in summary form:

(a) The key Information Technologies, Materials, and other Goods and Services that

comprise the System to be supplied and/or performed by the successful Bidder

(including a breakdown showing all Subsystems);

(b) The quantities of such Information Technologies, Materials, and other Goods and

Services;

(c) The site(s) where the System will be installed and the services performed; and

(d) When Installation, and Operational Acceptance should take place for all

Subsystems and/or major components of the System, and the overall System itself,

as well as any other major Contract milestones. Note that the delivery date is not

presented in the Implementation Schedule but left for bidders to provide.

Delivery, under Incoterms 2000 for CIP, refers to the shipment date when the

Supplier delivers the goods to the first carrier at the port of embarkation, not to the

arrival of the goods at the destination site. Delivery (shipment) date therefore

varies according to the country of origin of the goods and the Supplier's chosen

method of transport.

The target completion dates given in the Implementation Schedule must be realistic, and

the Schedule itself must contain enough clear information to enable Bidders to quickly prepare

responsive bids with realistic and competitive prices. These prices are to submit in the format of

the Price Schedules included in the Sample Forms Section of these SBD. Thus, the breakdown

provided in the Implementation Schedule should closely mirror that given in the Price Schedules.

If inconsistencies are introduced in these two key forms, confusion and delays will likely occur

during the evaluation.

The Implementation Schedule also fulfills a variety of other important functions:

(a) The performance milestones in the Schedule are used to construct the payment

schedule given in the Special Conditions of Contract;

(b) The Schedule is a key tool that the Purchaser utilizes to monitor and supervise

day-to-day performance by the Supplier;

(c) The application of the liquidated damages provision in the General Conditions of

Contract is linked directly to the dates given in the Schedule; and

(d) The quantities for each item shown in the Schedule are used as the starting point

for any quantity variations the Purchaser may wish to request at the time of

Contract award pursuant to ITB Clause 33.1.

6

The sample tables provided in this section of the SBD are designed to help the Purchaser

organize and present the necessary information. They comprise:

(a) An Implementation Schedule Table;

(b) System Inventory Tables (Supply and Installation cost items and Recurrent cost

items);

(c) A Site Table(s); and

(d) A Table of Holidays and other Non-Working Days.

The Purchaser should modify these tables, as required, to suit the particulars of the System

(and Subsystems) to be supplied and installed. The sample text provided for various sections of

the tables is illustrative only and should be modified or deleted as appropriate.

The Implementation Schedule Table should provide:

(a) Brief identifying descriptions for the major Subsystems and/or major components

of the System and the site(s) where they will be installed;

(b) The Purchaser’s required completion time, specified in weeks from date of

Contract Effectiveness, for Installation and Achieving Operational Acceptance, for

each Subsystem and major component, as well as for Operational Acceptance of

the entire System itself (if required); and

(c) A clear indication of which completion date(s) would be used for assessment of

Liquidated Damages.

In specifying the Schedule, it is essential that the target completion dates be realistic and

achievable in light of the capacity of both the average Supplier and the Purchaser to carry out their

respective contract obligations. In addition, the Purchaser must take care to ensure that the dates

specified in the Schedule are consistent with any specified elsewhere in the Bidding Documents,

especially in the SCC (e.g., in relation to the Time for Achieving Operational Acceptance and/or

times specified for the submission and acceptance of the Agreed and Finalized Project Plan).

The System Inventory Tables give a more detailed description of each of the Information

Technologies, Materials, and other Goods and Services needed for the System (broken down by

Subsystem, if applicable), the required quantities of each, and the location of each on a specific

site (e.g., building, floor, room, department, etc.). Each entry in the System Inventory Tables

should be cross-referenced to the relevant section of the Technical Requirements where that

component is described in detail. There are two sample formats given for the System Inventory

Tables: one for the Supply and Installation cost items and the second for recurrent cost items

needed (if any). The second version of the table permits the Purchaser to obtain price information

about items that are needed during the Warranty and Post-Warranty Service Periods and beyond.

7

The Site Table(s) provides information regarding the physical location of the site(s) where the System is to be supplied, installed, and operated. The site(s) may consist of a number of branch offices in remote regions, different departments or offices in the same city, or a combination of these. The Purchaser must specify this information in sufficient detail so that Bidders can accurately estimate costs related to:

(a) Delivery and insurance;

(b) Installation, including cabling and inter-building communications, etc.;

(c) Any subcontracts needed to perform post-warranty operational support services, such as emergency repair, maintenance, and other support services; and

(d) Any other related Service obligations the successful Bidder will have to perform under the Contract, including related travel and subsistence costs.

This information will also help Bidders identify which site(s) may warrant a site visit during the period they are preparing their bids. If the System presents complex installation problems, a de-tailed site layout drawing should be included in the Bidding Documents.

8

A. Background

9

1. The Purchaser and it’s mission

1.1. Janata Bank Limited, a banking company incorporated under company act 1994 with all the liabilities and assets of Janata Bank {which was duly established as per Bangladesh Bank’s (Nationalization) Order, 1972 (the Presidential Order No. 26 of 1972)} having its Head Office at 110, Motijheel Commercial Area, Dhaka Bangladesh is the second largest commercial bank having 844 branches serving all over Bangladesh.

1.2. The mission of the bank is to actively participate in the socio- economic development of the nation by operating a commercially sound banking organization, providing credit to viable borrowers, efficiently delivered and competitively priced, simultaneously protecting depositors’ funds and providing a satisfactory return on equity to the owners.

2. Objectives of the Purchaser (Janata Bank Limited)

2.1. Currently 136 (excluding 4 overseas branches) out of total 844 branches at home are partially computerized in an off-line mode, using 5 different application systems developed locally by multiple vendors and organizations. 4 overseas branches and CE’s office in UAE currently computerized under Centralized as well as Distributed On-Line banking System.

2.2. With the advancements in information and communication technology, the customers, particularly the high net-worth individuals and blue chip corporate, are becoming technology aware day by day. They increasingly expect for better service, better value for time, effective fund management tools. This necessitates that bank look towards innovative solutions for retaining the existing and attracting fresh high net-worth individuals and blue chip corporate. To retain customers and to allure new customers, banks now need to provide efficient services over diverse delivery channels such as ATM under shared network, Internet Banking, Mobile/WAP Banking, EFT, POS etc. 24x7x52-hour service, the Bank intends to purchase REAL TIME ON-LINE BANKING SYSTEM.

2.3. To computerize all branches of the bank would require a huge amount of money. On the other hand, most of the branches are not performing according to their potentiality. Therefore, it is advised in the Terms of Reference (TOR) under the EGBM Project for designing a minimum IT Platform (MITP) for Janata Bank Limited, which would ensure the value addition both in technology and performance. Following that IT platform design, the bank authority may decide to automate banking activities fully in the future. Accordingly a Minimum IT Platform for Janata Bank Limited was designed. The project authority also advised the Bank to prepare a phase-wise automation plan for the Bank. This IT Investment Plan has been prepared on the basis of that directive and inline with the Minimum IT Platform design.

2.4. This Tender has been developed to bring uniformity and to keep pace with the technological advancement in the banking sector by introducing a world-class industry standard State-Of -The-Art On-Line Banking System in Janata Bank Limited in phases.

2.5. Project Scope:The Bank adopted a plan to introduce Real Time On-Line Banking System in the selected 235 (Corporate, AD, and ‘Grade-1’ category) branches in phases. In the 1 st Phase Head Office Divisions, CDC, DRS, Local Office and 11 corporate branches are selected. In the

10

2nd phase Stage-1 remaining 123 branches (123 off-line computerized in Bangladesh) and in 2nd phase Stage-2, 100 non-computerized branches will be selected.

Table-1: The details of the delivery phases are as under:

Phase Stage No. Of Branch

Name & Area Estimated Time

(month)1st Phase

Pilot Project

12 HO Division, CDC & DRSLocal Office, DhakaJanata Bhaban Corp. Branch, DhakaKawran Bazaar Corp. Branch, DhakaNagar Bhaban Corp. Branch, DhakaBB Road Corp. Branch, NarayangonjSK. Mujib Road Corp. Branch, Ctg.Lal Dighi East Corp. Branch, Ctg.Khulna Corp. BranchBarisal Corp. BranchSylhet Corp. BranchRajshahi Corp. BranchRangpur Corp. Branch

14

2nd Phase 1st Stage 123 Remaining Off-Line Computerized Corporate, AD, Grade-1 Branches.

10

2nd Stage 100 Remaining Grade-1 Branches 12Total 235 36

1) At the Phase-1 of automation, HO Divisions, CDC, DRS, Local Office and 11 other corporate branches will be automated, covering all the 5 different Banking Software currently running in Janata Bank Limited. Data Migration Tools for all the different software will be developed. HO Divisions and branches will be connected to Data Center at Head Office. Phase-I will be treated as the PILOT implementation. Training of the Bank Personnel will also be done simultaneously. Multiple delivery channels like ATM, Internet Banking, Mobile/WAP Banking, EFT, etc. will be completed at this stage. Vendor personnel will carry out the customization and implementation in this phase.

2) At the Phase-2 Stage-1, 123 Corporate, AD & Grade-1 branches currently running under Off-Line Banking Application Software will be brought under On-Line Banking System. The vendor and bank personnel will carry out the customization & implementation jointly.

3) At the Phase-2, Stage-II, automation of 100 non-computerized Grade-1 branches will be automated with On-Line Banking System and will be connected with CDC & DRS. Customization & Implementation will be done by Bank personnel under the supervision of the vendor.

4) The bank will use any/all communication facility like VSAT, Radio Link, Leased line, Fiber Optic cable etc. depending on the availability of the communication facility at all locations.

5) Supplier will submit detail implementation Plan & Methodology to implement the above plan as well as breakup of ownership cost of all items.

11

2.6. Tender Scope:

1st phase:-

This tender is for the implementation of the 1st phase of the above mentioned project. The bidder will bid for the Real Time On-Line Banking Application Software for the 1st Phase (for CDC, DRS, Head Office Divisions, Local Office and 11 Corporate branches of Janata Bank Limited), Identify and advise requirements (detailed specifications and configuration) for the RDBMS, System Software, Utility Software, Hardware for CDC & DRS, Hardware and Software for Networking/Communication (LAN/WAN requirement), Hardware, Equipments & Accessories regarding Site Preparation for CDC, DRS, Hardware & Software for Branches/Offices in details for the 1st phase. This tender is a single package, single lot. The bidders must bids for all the components as per Requirement Schedule/List of this tender. Evaluation will be done on the basis of the full package.

The Bidder must bid for the followings:

a) Banking Application System (Core System):- Centralized Real Time On-Line Banking Application Software for CDC, DRS, Head Office Divisions, Local Office and 11 Corporate Grade-1 Branches.

b) Operation Systems:- Operating System for the Servers at CDC, DRS and also for the Workstations at Head Office Divisions, Local Office and 11 Corporate Grade-1 Branches.

c) RDBMS: - RDBMS for CDC and DRS and other areas.

d) Utility Software: Report Writing Software, Encryption /Description Software, Antivirus, Anti Spam, Anti Spy-ware and Anti Ad-ware Software. NMS etc.

e) Security Software: Security Software required for the safety of the On-Line BAS. Also for WAN/LAN Security etc.

f) Customization/Development, Installation and Implementation: Customization/Development, Installation and Implementation of the On-Line BAS. Installation and Implementation of all other software.

g) Training: All types of Training relating to On-Line BAS, All other Software, to run the proposed system adequately. Also for project management.

The Bidders must identify and Suggest the Volume, Quantity and Specification of the followings in their bids:-

a) Hardware for CDC: - Sarvers, External Data Storage, Tape Library etc.

b) Hardware for DRS: - Sarvers, External Data Storage, Tape Library etc.

c) Machine and Equipments for CDC: AC, Generators, On-Line UPS, LAN Cabling, Power Cabling, Security Access System, Fire Protection System.

d) Machine and Equipments for DRS: AC, Generators, On-Line UPS, LAN Cabling, Power Cabling, Security Access System, Fire Protection System.

e) Printers: Printers for all areas (Heavy Duty System Printers for CDC & DRS, Printers for HO Divisions and all branches).f) Switch, Router, and Firewall for CDC & DRS

12

g) Switch, Router, and Firewall for branchesh) Bandwidth Requirements: Required Bandwidth for CDC, DRS and Branches.i) Communication Media (Leased): The bank will use any/all communication facility like VSAT, Radio Link, Leased line, Fiber Optic Cable etc. depending on the availability of the communication facility at all locations.

Supplier will submit detail implementation Plan & Methodology to implement the above plan as well as breakup of ownership cost of all items.

13

3. Acronyms used in these Technical Requirements

Term Explanation

Bps Bits Per Second

Cps Characters Per Second

DBMS Data Base Management System

DOS Disk Operating System

Dpi Dots Per Inch

EDW Enterprise Data Warehouse

Ethernet IEEE 802.3 Standard LAN Protocol

GB Gigabyte

Hz Hertz (Cycles Per Second)

IEEE Institute Of Electrical And Electronics Engineers

ISO International Standards Organization

JB Janata Bank Limited

KB Kilobyte

KVA Kilo Volt Ampere

LAN Local Area Network

Lpi Lines Per Inch

Lpm Lines Per Minute

Mb Megabyte

MTBF Mean Time Between Failures

NCB Nationalized Commercial Banks (Government Owned)

NIC Network Interface Card

NOS Network Operating System

ODBC Open Data Base Connectivity

OLE Object Linking And Embedding

OS Operating System

PCL Printer Command Language

PPM Pages Per Minute

RAID Redundant Array Of Inexpensive Disks

RAM Random Access Memory

RDBMS Relational Data Base Management System

RISC Reduced Instruction Set Computing

14

Term Explanation

SCSI Small Computer System Interface

SNMP Simple Network Management Protocol

SQL Structured Query Language

TCP/IP Transport Control Protocol / Internet Protocol

V Volt

WAN Wide Area Network

15

B. Business Functions and Performance Requirements

16

1. Business Performance Requirements of the System

To ensure the value addition both in technology and performance, Janata Bank Limited management has decided to automate banking activities fully in future. Under EGBM Project, the bank has designed a Minimum IT Platform (MITP) and has prepared a phase-wise automation plan for the bank. The bank decided to purchase a world-class industry standard State-Of -The-Art On-Line Banking System for the Bank in phases to bring uniformity and to keep pace with the technological advancement in the banking sector.

a. Functional Performance Requirements of the System

With the advancements in information and communication technology, the customers, particularly the high net-worth individuals and blue chip corporate, are becoming technology aware day by day. They increasingly expect for better service, better value for time, effective fund management tools. This necessitates that bank look towards innovative solutions for retaining the existing and attracting fresh high net-worth individuals and blue chip corporate. To retain customers and to allure new customers, bank now intends to purchase REAL TIME ON-LINE BANKING APPLICATIONM SYSTEM.

2.1. Real Time On-Line Banking Application System (BAS):-

The bidder must submit the details of the core banking application as per its own style and form to describe how best its product/service would fulfill the bank’s functional and non-functional requirements.

The On-Line BAS should be capable enough to scale both horizontally and vertically in order to grow with the increase number of customer as well as with the addition of new delivery channels. It should be highly parameterized so that all the rules can easily be applied for different banking products and services and also posses the flexibility of modifying the screen and report content without modifying the source code having in-built security features in multiple levels.

However, the bidder must provide its additional response to the bank’s requirements in terms of General & Technical Requirements with required status information on detailed functional and non-functional requirements

Systems Specifications Requirement Study:

The successful bidder will conduct a detailed systems requirements study and provide a Functional Requirements Specification Manual (“FRSM”) relating to the functionalities as required to support the various products and services offered currently by the Bank or to be offered by the Bank in the near future in terms of its business strategy. In doing so the bidder is expected to take into account the minimum requirements laid down in General & Technical Requirements. Also it should include all the areas where the Bidder is sug-gesting a work-around. If the work-around involves re-alignment or re-engineering of a business process, the re-aligned/ re-engineered process should be included in the FRSM.

17

The FRSM should include the standard operating procedure proposed for the re-aligned/ re-engineered process. The Bidder is expected to assist the Bank in aligning/ engineering the business requirements with the application so as to enable centraliza-tion of desired business process, eliminate redundant and duplicate processes, increase operational efficiency and improve customer service. Bidder is expected to prepare de-tailed documentation, presentation, workflows for the business processes affected due to implementation of On-Line BAS, delivery channels and other applications imple-mented by the Bidder.

The Bidder is also expected to suggest suitable Business Continuity procedures appli-cable to its solution in case the solution is unavailable. These procedures should ensure that the customers of the Bank are not denied banking services due to the solution be-ing unavailable to the Bank’s users.

The FRSM should include capabilities to automatically detect, inform and reverse transactions that may be incomplete due to hardware failures.

The Bidder shall provide the FRSM to the Bank for review and comment and any comments or suggestions of Bank will be incorporated therein.

The Bidder will suggest the number and volume of the Functional and Technical Group for the bank and their responsibilities.

The Bank will identify the functional heads for each process, who will be responsible for the review, comments and sign – off of the FRSM.

The FRSM will deem to be completed when signed – off from the Bank. The bidder is also expected to carry out and document a detailed current assessment

study for all business activities, product and service offered by the bank to gain under-standing of the bank’s existing business and operations. The bidder is expected to help the bank to parameterize the product and provide valuable inputs at the time of system parameterization based on the current state assessment study undertaken by the bidder.

The Bidder will suggest the number and volume of the Functional and Technical Group for the bank and their responsibilities

Gap Identification and Resolution

The Bidder will be responsible for gap identification and resolution so as to:

a. Provide all functionalities as mentioned in the FRSM.b. The Bidder will provide the Bank with the gap identification report along with the nec-

essary solutions to overcome the gaps and the time frames.c. The Bidder will ensure that all gaps identified at the time of system testing will be im-

mediately resolved.d. The Bidder will ensure that gaps pointed out by the audit and inspection team, statu-

tory and regulatory bodies, or any other third party agency engaged by the Bank will be immediately resolved.

e. The Bidder shall resolve gaps by proposing a suitable work around or customizing the proposed solution by way of modifications / enhancements, as necessary, to the pro-posed software solution.

f. The Bidder shall provide all statutory, regulatory and ad-hoc MIS (Management Infor-mation System) reports as required by the Bank in the desired format during the initial phase of customization process.

18

g. The Bidder shall provide for all subsequent changes to reports as suggested by the statutory and regulatory bodies from time to time immediately to the Bank at no addi-tional cost to the Bank.

h. The Bidder shall provide for a flexible report writer utility and train the Bank person-nel in using the same.

i. The Bidder will give adequate time to the Bank for reviewing the gap report.j. The Bidder will incorporate all the suggestions made by the Bank to the gap report.k. The Bidder will ensure that they have the necessary infrastructure and people in place

to resolve all the gaps within the time lines agreed, for the implementation and roll out.l. The cost of all customizations as mentioned above is required to be included in the

Price Bid and the Bank will not make any additional costs for such effort till all the branches are live. While costing the customization effort required, the Bidder should exclude the effort required from the Bank’s side.

Data Migration

a. The Bidder will be responsible for successful data migration from the legacy systems to the new environment for all the branches. It is the bidder’s responsibility to liaise with the legacy system for the purpose of data mapping and extraction in what ever format the On-Line BAS bidder wants the data. The bank will not bear any additional cost for data migration, nor will be responsible for the same. The bidder has to develop Data Migration tools for the existing Off-Line Banking Application Software (Plat-forms of the legacy systems are stated at the Section-I, Attachment-1 ) for smooth Data Migration, which shall be use for entire project/any future data migration.

b. Entire data pertaining to live accounts (from the time of account opening or from the time the data is available) for accounts like term deposits, recurring deposits, loans and advances, etc. should be migrated to the proposed solution for all the branches being converted to CBS. The history data should at least fulfill the objectives of printing backdated customer statements (for all products, accounts, and schemes supported by the legacy application), general ledger, profit & loss statements, trial balance, account master information, standing instructions and transaction history (including GL, P&L heads and other office accounts) and should also support printing MIS reports as de-sired by the Bank for the legacy data migrated.

c. Migration of all outstanding entries from the legacy systems to the new CBS applica-tion for the identified general ledger and profit and loss heads for future reconciliation.

d. The Bidder will be responsible for formulating the “Data Migration Strategy” and process documents which will have to be reviewed and signed – off by the Bank prior to commencement of the data migration exercise. The On-Line BAS bidder would need to factor all effort to liaise, interact, develop tools, correspond etc. with the legacy vendor to obtain the data as desired by the CBS solution.

e. The Bidder will prepare the “Data Migration Strategy” and process documents within shortest possible time.

f. The Bidder will give the Bank adequate time to review and sign – off the Data Migra-tion Strategy and process documents.

g. All comments and suggestions of the Bank must be incorporated in the data migration strategy and process documents before obtaining sign – off.

h. The Bidder may associate the Bank’s personnel proficient in the legacy systems for as-sistance during the data migration exercise.

19

i. For this purpose adequate training would need to be imparted by the Bidder to the Bank’s personnel for the same.

j. In the event of any gaps in the field mapping reports the same would be discussed with the Bank and the agreed solution would be documented by the Bidder and signed off from the Bank at no additional cost to the bank. The Bidder would give the Bank ade-quate time for the review of the agreed solution.

k. The Bidder shall ensure that workarounds or default values moved to the production database as a result of gaps in the field mapping are duly taken care of after successful migration to CBS and the Bank officials informed of the same in writing.

l. It will be the responsibility of the Bidder to ensure complete data cleaning and valida-tion for all data migrated from the legacy systems to the new application.

m. The Bidder will be responsible to massage the data as per the software / upload format required by the solution. It will be the responsibility of the Bidder to convey to the Bank, at least 60 days in advance from the date of migration, all the mandatory fields required for the functioning of the proposed applications that are not available in the legacy systems and that needs to be obtained by the Bank.

n. In the event the Bank is unable to obtain all the mandatory fields as conveyed by the Bidder, the Bidder shall suggest the most suitable workaround to the Bank. The Bidder shall document the suggested workaround and sign-off will be obtained from the Bank for the suggested workaround.

o. The Bidder will be responsible for development of data entry programs / applications with appropriate validations/checks that may be required for the purpose of data mi-gration in order to capture data available with / obtained by the Bank in non – elec-tronic format. These programs / applications should be made available to the Bank at least 30 days in advance from the date of migration. The bidder will be responsible to install the data capture tool at the branches where required and train the branch users on data entry.

p. The Bidder will conduct training for the Branch personnel or any other third party data entry agencies during the time of data entry.

q. The Bidder will be responsible for uploading the data entered by the Bank through the manual data entry screens, programs / applications.

r. The Bidder shall ensure that sufficient training is imparted to the data migration team of the Bank with regards to but not limited to On-Line BAS data structure, field map-ping requirements, field validations, default values and gaps in field mapping reports.

s. The Bidder shall develop the data conversion programs to convert banks data to On-Line BAS upload format. The Bidder shall perform mock data migration tests to vali-date the conversion programs.

t. The Bidder will be responsible for assisting the Bank in conducting the acceptance testing and in verifying the completeness and accuracy of the data migrated from the legacy applications to the proposed systems.

u. The Bank or its consultants may, at its will, verify the test results provided by the Bid-der.

v. The Bank reserves the right “to audit” / “appoint an external auditor to audit” the process of data migration and / or the completeness and accuracy of the data migrated during the entire exercise of data migrations.

w. Any gaps / discrepancy observed will be reported in writing to the Bidder, who will act upon it and resolve the same immediately or within 5 working days from the day of re-porting the same.

x. The Bidder will be responsible for obtaining the data from the branches for the pur-pose of migration.

20

y. The Bidder will be responsible to develop control reports for verification of the data both before and after migration.

Interfaces

a. The Bidder will be responsible for identifying the detailed interface requirements for integrating the proposed packages to the systems, as mentioned in Annexure-1, there-after and for all other functionalities as mentioned in the tender proposal.

b. The Bidder will present to the Bank the interface requirements for review.c. The Bidder will give the Bank adequate time to review the interface requirements.d. Any suggestions from the Bank will have to be included by the Bidder.e. The Bidder will be responsible for developing, testing and maintaining the interfaces.

In case of any subsequent change, modification or alteration to the Banks existing ap-plication software packages, the Bank will obtain the API for such existing application and provide the same to the Bidder for interface.

f. The Bidder must ensure that all interfaces are automated with minimal manual inter-vention. All 3rd party applications proposed by the bidder to meet the functional re-quirements of the bank should provide an on-line interface with the On-Line BAS.

g. The Bidder will ensure and incorporate all necessary security and control features within the application, operating system, data base, network etc. so as to maintain in-tegrity and confidentiality of data at all times.

h. The Bidder will be responsible for setting up the test environment for interface testing and Assist the Bank in preparing the test cases for the testing Ensure that the test cases meet all the testing requirements of the Bank. Resolve all errors, bugs, enhancements / modifications required during and after

testing but not before go live (within a maximum of 7 working days) Fix bugs and errors in one day after ‘go-live’ and obtain sign – off from the bank

immediately after such fixing. If any workaround solution is suggested, that should be provided ON THE SAME DAY, in respect of errors and bugs affecting the functioning of the Bank.

Testing

a. The Bank proposes to conduct “User Acceptance Test” (“UAT”) testing for the pur-pose of ensuring that all the functionality requested for by the Bank is available and is functioning accurately. The UAT would be carried out for the On-Line BAS, including the entire proposed module, all the delivery channels and all the 3rd party software proposed.

b. The Bidder will convey to the Bank that all the customizations that are required to “Go Live”, as agreed upon and signed off by the Bank are completed and the solution is ready for testing.

c. The Bidder will set up a test server, to accommodate a minimum of 25 concurrent users, which shall support simultaneous data migration testing and install the applica-tions including the customizations, parameterize it as per Bank’s requirement and up-load live data of a sample branch in the test server. The Bank expects the test environ-ment to be available to the Bank at all times, for the purpose of testing. The Bidder is expected to provide for the requisite test and development infrastructure including hardware, software, operating system and database for all applications including any 3rd party solutions being offered by the Bidder. The Bank expects the Bidder to set up

21

the required solutions (including the client desktops) and provide connectivity to test server at CDC/DRS at the desired testing center of the Bank for the purpose of testing. The Bank shall not pay any additional amounts to the Bidder for the purpose of creat-ing the test environment.

d. The Bidder will install client version of the solution on the PCs provided by the Bank.e. The Bidder will assist the Bank in preparing test cases including test data.f. The Bidder will assist the Bank in conducting all the tests and analyzing / comparing

the results. Bidder shall provide 5 full time resources conversant in all business areas, for trouble-shooting during the entire UAT process.

g. Any deviations / discrepancies / errors observed during the testing phase will be for-mally reported to the Bidder and the Bidder will have to resolve them in one day and sign – off from the same will be obtained from the Bank. However, workaround solu-tion should be provided ON THE SAME DAY, in respect of errors and bugs affecting the functioning of the Bank.

h. The Bidder will be responsible for maintaining appropriate program change control and version control for all the modifications /enhancements carried out during the im-plementation / testing phases.

i. The Bidder will be responsible for providing and updating system & user documenta-tion as per the modifications.

Pilot Implementation

a. The pilot implementation will consist of implementing the proposed On-Line BAS (all modules) including the delivery channels and 3rd party applications in the identified branches/offices and associated extension counters.

b. The Bidder will be responsible for setting up all the servers at the CDC and DRS. In-stallation & Configuration of the OS, RDBMS, Utility Software, Security Software and Management Software in all the places/Sites.

c. The bidder will be responsible for setting up all the networking and communication hardware and software and testing of the same.

d. The Bidder will be responsible for installing the applications with all the customiza-tions duly tested.

e. The Bidder will set all the parameters in the applications as accepted in the test envi-ronment. The Bidder shall be responsible for accuracy of the parameters set according to business needs of the Bank.

f. The Bidder will be responsible for migration of the legacy branch data to the new sys-tem..

g. The Bidder will be responsible for ensuring that all the client software is installed at the branch computers.

h. The Bidder will be responsible for imparting the required training to the branch per-sonnel prior to implementation.

i. The Bidder is required to be present at each of the branches/offices under migration for at least the first two-weeks after the branch has been migrated to the proposed solution for handholding, troubleshooting and hands-on training. Adequate Bidder personnel are required to be present on – site, conversant in all business areas of that branch.

j. The Bidder will assist the Bank in testing the reports generated using the proposed ap-plication with those generated by the old system during the parallel run. The Bidder personnel will investigate any differences observed in the report generated using legacy system as compared to the report generated from the On-Line BAS and initiate corrective action.

22

k. The Bidder will assist the Bank in deciding when to discontinue the parallel run.l. The Bidder will be responsible for implementing the delivery channels and ensure that

the customers of the branch being converted to the On-Line BAS are able to utilize the delivery channels.

m. Branch pilot implementation phase will be deemed complete once the Bidder has ob-tained a sign-off for implementation at all the pilot branches/offices from the Bank. The branch/offices will need to live run successfully for a period of at least 15 working days before signing – off on pilot implementation.

n. In the event of any deviations / discrepancies / errors observed at the pilot branches, the sign off will only be given by the Bank once the deviations / discrepancies / errors reported by the branch have been successfully rectified by the Bidder.

o. The Bidder shall depute relevant personnel to attend and resolve the branch problems immediately.

Introduction of New Products

Electronic Bill Presentment & Payment:

a. The On-Line BAS should have the capability to directly interface with the utility com-panies registered with the Bank and upload the data received from these companies on a periodic basis for bill details and payments to be made;

b. Facility to provide for bill presentment and payment through various delivery channels being offered by the Bank as well as through the Branches on the On-Line BAS.

c. All transactions to be effected in the On-Line BAS on an on- line real time basis for bill payments made by customers either through the branches / any other delivery channels offered by the Bank.

Flexibility

Flexibility in design should allow fast and inexpensive system changes to support new regulations and changes in products and services, as well as changes in reporting requirements.

Should have the ability to expand the system, changes in reporting as & when require.

Collection / Payment services:

On-Line BAS should have the capability to directly interface with such new applications and delivery channels, as may be used by the Bank from time to time. It should also support various collection services on behalf of the government authorities or utility companies. Such services may include

Income Tax, Sales Tax, Corporation Tax, Excise and Customs Duty Service tax Electricity, Telephone BB bonds Ministry & Government Accounts

Audit Tools

23

The Bidder is expected to provide various audit tools for auditing all the components proposed by the Bidder as part of the solution. These should include tools for auditing:

Operating Systems Database Systems Auditing the Network Application Systems

The Bidder is expected to develop application audit tools (for example identifying income leakages, non compliance to policies and procedures, etc.), as requested by the Bank’s internal auditors/departments from time to time, within the contract period.

Consolidation from Non-Online BAS Branches, Offices, Overseas Branches and Subsidiaries of the Bank

The Bidder is expected to build the required interfaces to the legacy branch systems. At an interval specified by the Bank (daily, weekly, etc.) the specified branches would upload data to the CBS. This data should be used for consolidating the Division/Area/Zonal/Zone/Region/ Branch/Bank wise General Ledger and also for generating various MIS Reports. The bidder also has to build the same interface for Subsidiaries (such as Janata Exchange Company, Srl, Italy) and Overseas Branches (Janata Bank Limited, UAE) under Multi-Bank, Multi-Book and Multi-Location System.

Central Bank Reporting

The Bidder must developed/furnished/make available all the Bangladesh Bank (Central Bank) reporting facilities as per requirements of the central bank.

BASEII-II Compliance

The Bidder must make the supplied Centralized Real Time On-Line Banking System as BASELL-II Compliance system either by the System itself or by third party solution.

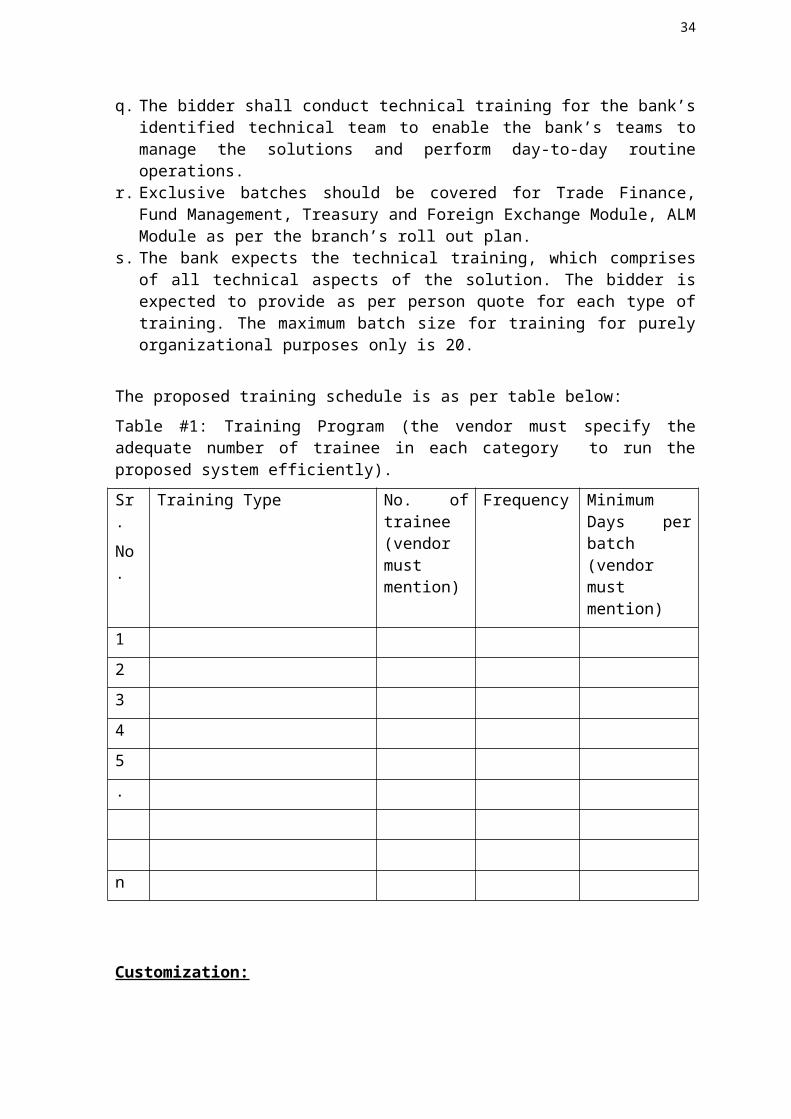

Training:

a. The Bidder will be responsible for training the Bank’s employees in the areas of im-plementation, operations, management, error handling, system administration etc. The Training should at least cover the following Areas:i. Functionality available in the solutionii. Customization developmentiii. Parameterizationiv. Data Migration (data mapping, field validations, default values, gaps in data

migration, manual data entry programs)v. Impact Analysisvi. Auditing techniquesvii. Advanced User Trainingviii. Advanced trouble shooting techniquesix. Deployment of various products / packages provided as part of the solution in-

cluding the delivery Channels

24

x. Techniques of generating various MIS reports from the solution providedxi. Development and deployment of new products using the proposed solutionxii. Using of all the auditing tools being providedxiii. Developing new Audit Reports / Tools using the proposed solution.xiv. Advanced training on the operating systems, database systems and network sys-

tems to be used by the proposed solution.xv. Training for Report Writer facility to create new reports and modify existing re-

portsxvi. System & Application Administration at branches

b. The Bank will be responsible for identifying the appropriate personnel for all the train-ing requirements.

c. The Bidder is expected to conduct an Executive Awareness Program for the senior level management team of the Bank for 3 days.

d. The Bidder is expected to train the Bank personnel as a par table stated below. The vendor should mention the adequate number of trainee and duration of the training.

e. The Bidder should also suggest the bank for additional training requirement deem nec-essary to complete the project and submit the complete training schedule.

f. The Bidder will also be responsible to train all users in the pilot branches and branches. The user training will be held at the Bank’s respective branches or at the training centers as required by the Bank.

g. The Bidder can use the Bank’s IT infrastructure available at the IT Division/Training Institute/Centers for the purpose of providing training to users. The Bank expects the Bidder to set up the required solutions (including the client desktops) at the training centre of the Bank for the purpose of training. The Bank shall not pay any additional amounts to the Bidder for the purpose of creating the training environment at the Bank’s training centers. Except for end user training, the bank will not provide any premises to the bidder to conduct trainings.

h. The Bidder will be responsible to install the required applications / systems, training server at CDC and also ensure connectivity to the training server, for the purpose of training at the training centers. There will be no cost payable by the Bank for the appli-cation, database and operating system software installation at such training sites. How-ever, if the Bidder wants to quote separately for these components then it can be in-cluded as part of the Commercial Bid. The training hardware at the data centre should be capable to support a minimum of 100 concurrent users. The Bank expects the train-ing environment to be available to the Bank at all times, for the purpose of training.

i. The Bidder will impart training to all the pilot branch end users on the On-Line BAS prior to the Branch going live. The Bidder must ensure that proficient personnel con-duct the training at the respective training centers identified for the same. The Bidder should ensure that the end user training is scheduled and completed at least a week prior to the branch going live.

j. The Bidder will be responsible for providing the users with the requisite training mate-rial in both hard and soft copies at least for the core team / implementation training, technical training, end user training and train the trainers. The onus of preparing the training material will be on the Bidder.

k. The Bidder will be responsible for preparing, circulating and collecting training feed-back forms from the participants.

l. The feedback forms will be prepared by the bidder, reviewed and given to the Bank. The changes, if any, suggested by the Bank or its consultants, should be incorporated and implemented by the Bidder.

25

m. The Bidder will provide a detailed training schedule to the Bank for review and sign – off prior to commencement of the training.

n. The Bidder will be responsible for providing on going training at defined intervals to the identified Bank personnel.

o. The Bidder at no point should entrust the responsibility of training the users to the Bank’s employees, however the Bidder can request for any assistance from the Bank’s employees to impart training to other users.

p. The bidder is expected to provide training for any other third party products quoted to meet the scope of the tender proposal to the core teams as selected by the bank.

q. The bidder shall conduct technical training for the bank’s identified technical team to enable the bank’s teams to manage the solutions and perform day-to-day routine oper-ations.

r. Exclusive batches should be covered for Trade Finance, Fund Management, Treasury and Foreign Exchange Module, ALM Module as per the branch’s roll out plan.

s. The bank expects the technical training, which comprises of all technical aspects of the solution. The bidder is expected to provide as per person quote for each type of train-ing. The maximum batch size for training for purely organizational purposes only is 20.

The proposed training schedule is as per table below:

Table #1: Training Program (the vendor must specify the adequate number of trainee in each category to run the proposed system efficiently).

Sr.

No.

Training Type No. of trainee (vendor must mention)

Frequency Minimum Days per batch (vendor must mention)

1

2

3

4

5

.

n

Customization:

The bidder is required to customize all the application software provided by him to suit and fulfill Bank’s requirement as per the requirements in full. Proper documentation of the customization must be provided to bank by vendor.

26

User documentation

On-Line BAS package should include the executable application program files, comprehensive user manual, training material and any other documents needed for running the package.

User documentation should have help on all the modules of the package and should be organized in such a manner that the following details are available to the user:

Table of contents or overview Introduction and background to the module Services and facilities available Step-by-step guide for the work flow Option/screen –wise details of functionality modes like Add, Modify, and View etc. Screen-wise field definitions, data types, data length and field description Description of symbols used and notations, if any Important manual check points, warning on critical inputs or processes for the success

of the operation Linkage points with other modules, if any Help should be available at two levels -- Global Help, through the Help option in the

menu bar or on-line context sensitive help invoked by pressing a function key on the keyboard at any time.

2.2. Related Information Technology Issues and Initiatives

2.2.1. Hardware and System Software

The bidder should provide a diagrammatic overview of the proposed hardware (Computer, LAN and WAN), Operating System, RDBMS (including, Development tools, report writ-ing tools and encryption software for internet banking) Utility and communication soft-ware depicting total hardware architecture for On-Line BAS across the bank’s target sites for On-Line BAS, i.e., the CDC, DRS, offices and branches. Apart from this, the bidder must furnish proposed hardware and system software Configuration and Specification based on the Bench Mark Study successfully done by the developer of the On-Line BAS. Bidder must attach the full Bench Mark Study Report. The Bidders must identify and sug-gest the Volume, Quantity and Specification for all the Hardware, Peripherals, Accessories and Equipments require for the proposed System. The bidder will suggest and offer the best possible solution considering the cost and benefit. Bidder must undertake that the configuration recommended would deliver the performance requirements necessitated by Janata Bank Limited. If selected, the Bidder will have the obligation under the Contract to deliver the performance promised.

The Bidder should indicate the Configuration and Specification comprise of open standard platforms technologies and operating environment. However, if the proposed solution makes use of proprietary components, they must be clearly identified and details regarding their availability, support, upgrades, maintenance, and other related issues must be given.

27

As per the assessment and suggestion of successful bidder, Hardware & Peripheral System, Network & Communication System, Appliances, Machine and Equipments will be procured.

To that end, Bidder must categorically specify the exact hardware and system software required to operate the proposed On-Line BAS successfully based on the Bench Mark Study done by the On-Line BAS Developer. Required details include:

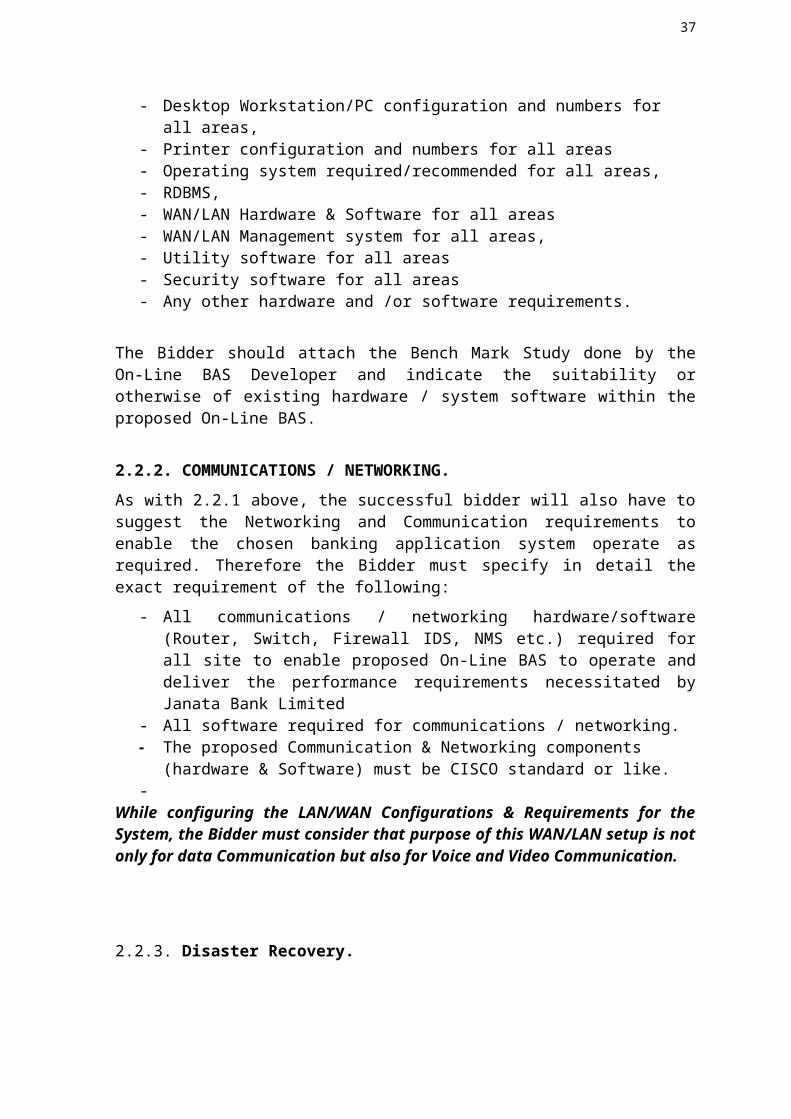

- Server configuration, both at the CDC, DRS, - Quantity of Servers- Desktop Workstation/PC configuration and numbers for all areas,- Printer configuration and numbers for all areas- Operating system required/recommended for all areas,- RDBMS,- WAN/LAN Hardware & Software for all areas- WAN/LAN Management system for all areas,- Utility software for all areas- Security software for all areas- Any other hardware and /or software requirements.

The Bidder should attach the Bench Mark Study done by the On-Line BAS Developer and indicate the suitability or otherwise of existing hardware / system software within the proposed On-Line BAS.

2.2.2. COMMUNICATIONS / NETWORKING.

As with 2.2.1 above, the successful bidder will also have to suggest the Networking and Communication requirements to enable the chosen banking application system operate as required. Therefore the Bidder must specify in detail the exact requirement of the following:

- All communications / networking hardware/software (Router, Switch, Firewall IDS, NMS etc.) required for all site to enable proposed On-Line BAS to operate and deliver the performance requirements necessitated by Janata Bank Limited

- All software required for communications / networking.- The proposed Communication & Networking components (hardware & Software)

must be CISCO standard or like.-

While configuring the LAN/WAN Configurations & Requirements for the System, the Bidder must consider that purpose of this WAN/LAN setup is not only for data Communication but also for Voice and Video Communication.

2.2.3. Disaster Recovery.

Bidder must indicate total proposals in regard to disaster recovery, including all software, hardware, and communications and networking requirements.

28

The Bank plans to have a fully operational hot or warm disaster recovery site located in a suitable distant place. The Bidder must indicate the appropriateness or otherwise of each option. Bank wanted to have the DRS at the premise of Netaigonj Corporate Branch, Narayangonj.

General featuresThe proposal for hardware should:

Cover the server sizing of processors, storage, memory, backup devices, ports, printers, scanners.

Take into account peak time operations, scalability requirements and response time to all online users through the nodes installed at different branches/offices geo-graphically spread all over the country. Necessary ‘hardware sizing information’ is provided below within this section

Be capable of handling 24x7-hour service to the clients and to support delivery channels including any-branch banking, Internet banking, Tele banking, ATMs, Call center etc.

Comprise of open standard platforms technologies and operating environment. However, if the proposed solution makes use of proprietary components, they must be clearly identified and details regarding their availability, support, upgrades and maintenance and other related issues must be given.

Contain an undertaking that the configuration recommended would deliver the per-formance requirements necessitated by Janata Bank Limited. If selected, the Bid-der will have the obligation under the Contract to deliver the performance promised.

Consider that the bank may reuse the existing hardware at the branches to the ex-tent possible.

Have components within the server that are hot swappable and should incur no downtime due to component failure.

Have servers with dual power supplies. The power input to the power supplies will be from separate UPS. In case of failure of one power supply, the second power supply should be able to take the full load without causing any interruption in ser-vices.

Have network interface cards (NIC) of adequate capacity. The bidder may be required to verify the benchmarking results on the recom-

mended hardware ported with required system/application software to meet the re-sponse time and other efficiency parameters.

The Bidder needs to state application architecture as well as system software re-quirements at various levels viz. CDC, DRS & Branches. The audit trait functions, security system software details must comprise requirements and versions of Oper-ating Systems, Compilers, and audit trail functions, security, RDBMS, middleware and front ends at various levels. The detailed components of the various system software, versions, and number of users along with the details whether the run time or development version required, must be clearly defined.

The licensing policies (which includes upgrades) for each of the product recom-mended and offered must be spelt out clearly in the quotations.

Estimated SAN (Storage Area Network) storage capacity at the CDC and DRS each. If the individual solutions suggested by the bidder necessitate additional ca-

29

pacity, then the bidder would need to provide accordingly to meet the tender pro-posal and SLA requirements.

2.2.4. Site Preparation and Supply of all Components

Central Data Centre (CDC) and Disaster Recover Site (DRS)

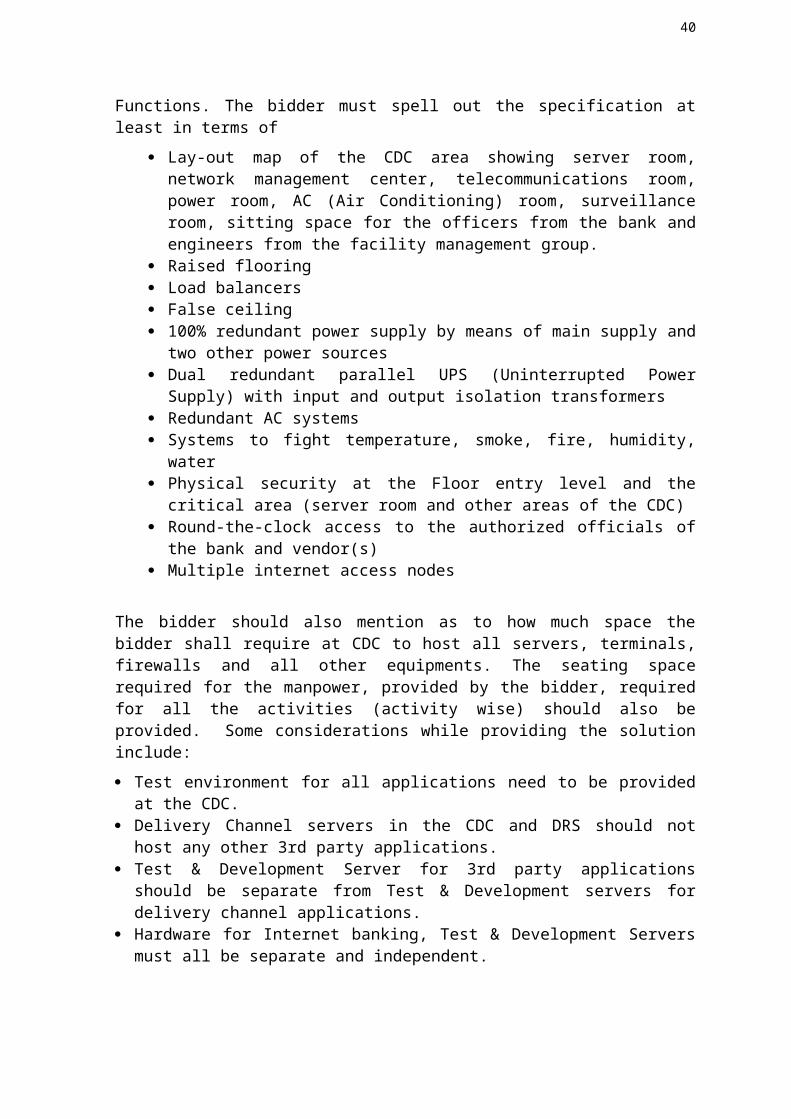

The Bank will provide space for a Central Data Centre (CDC) at 48, Motijheel, Dhaka as per the recommendation of the bidder. The central host will undertake centralized back-office processing, end-of-the-day and start-of-day operations, back-ups and other key functions. The Data Centre will also have control over Network Management Functions. The bidder must spell out the specification at least in terms of

Lay-out map of the CDC area showing server room, network management center, telecommunications room, power room, AC (Air Conditioning) room, surveil-lance room, sitting space for the officers from the bank and engineers from the fa-cility management group.

Raised flooring Load balancers False ceiling 100% redundant power supply by means of main supply and two other power

sources Dual redundant parallel UPS (Uninterrupted Power Supply) with input and output

isolation transformers Redundant AC systems Systems to fight temperature, smoke, fire, humidity, water Physical security at the Floor entry level and the critical area (server room and

other areas of the CDC) Round-the-clock access to the authorized officials of the bank and vendor(s) Multiple internet access nodes

The bidder should also mention as to how much space the bidder shall require at CDC to host all servers, terminals, firewalls and all other equipments. The seating space required for the manpower, provided by the bidder, required for all the activities (activity wise) should also be provided. Some considerations while providing the solution include:

Test environment for all applications need to be provided at the CDC. Delivery Channel servers in the CDC and DRS should not host any other 3rd party ap-

plications. Test & Development Server for 3rd party applications should be separate from Test &

Development servers for delivery channel applications. Hardware for Internet banking, Test & Development Servers must all be separate and

independent. Space for complete hardware and software with required redundancy for security viz.

Firewall, IDS etc. must be provided. UPS of appropriate capacity All the similar specifications applicable to the CDC but not mentioned here should also be provided for CDC.

All the similar specifications applicable to the DRS should also be provided for DRS.

30

The location of the CDC will be at the Head Office. Information about the actual location of CDC and DRS will be supplied to the potential bidders at the Pre-Bid meeting.

2.2.5. Other sites

The Bank will provide space for all other sites. The bidder is expected to prepare layout map for each of the sites, if needed, or representative site and develops the sites comprising

Space for WAN equipments Data cabling False ceiling 100% redundant power supply by means of main supply and two other power

sources UPS (Uninterrupted Power Supply) with input and output isolation transformers AC systems Renovated counters and/ or sitting space for specified employees of the office/

branch Systems to fight temperature, smoke, fire, humidity, water Physical security at the Floor entry level Round-the-clock access to the authorized officials of the bank and vendor(s) Internet access nodes for selected sites

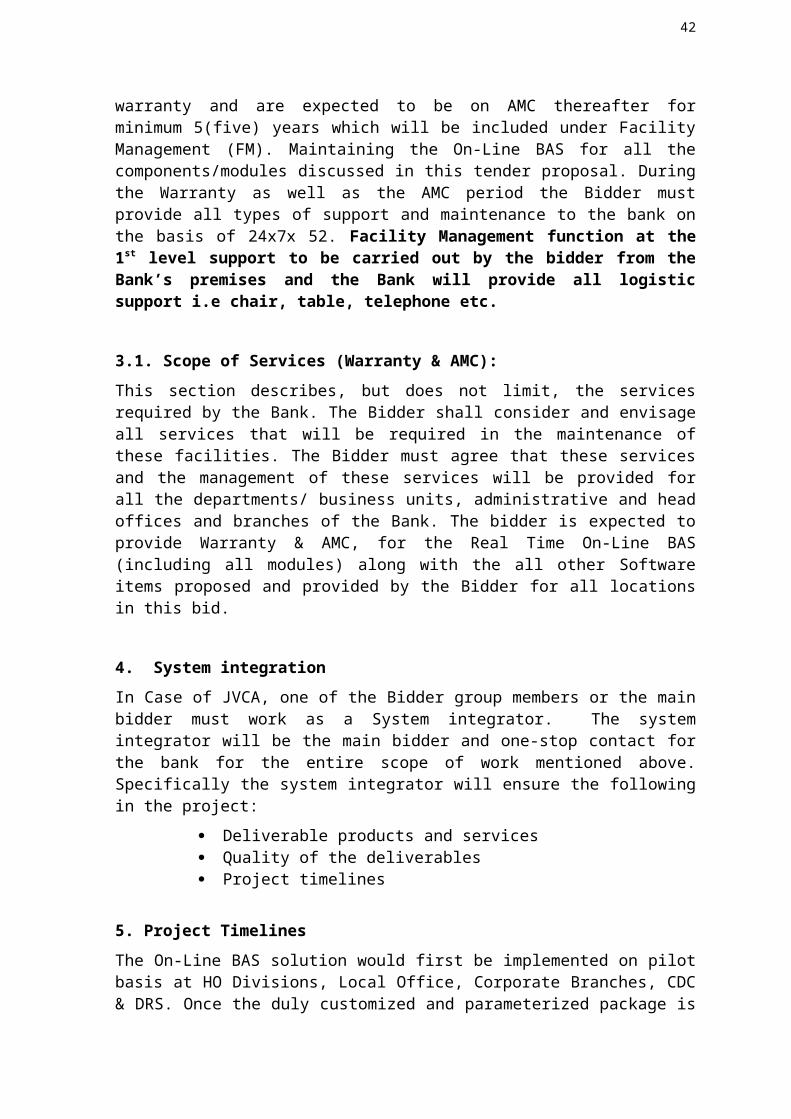

3. Warranty and Annual Maintenance Contract (AMC)

While bidding for providing facilities management services to the Bank the bidder needs to consider that all the solutions provided by the bidder by way of this tender proposal should come with 1 (one) year onsite free service warranty and are expected to be on AMC thereafter for minimum 5(five) years which will be included under Facility Management (FM). Maintaining the On-Line BAS for all the components/modules discussed in this tender proposal. During the Warranty as well as the AMC period the Bidder must provide all types of support and maintenance to the bank on the basis of 24x7x 52. Facility Management function at the 1st level support to be carried out by the bidder from the Bank’s premises and the Bank will provide all logistic support i.e chair, table, telephone etc.

3.1. Scope of Services (Warranty & AMC):

This section describes, but does not limit, the services required by the Bank. The Bidder shall consider and envisage all services that will be required in the maintenance of these facilities. The Bidder must agree that these services and the management of these services will be provided for all the departments/ business units, administrative and head offices and branches of the Bank. The bidder is expected to provide Warranty & AMC, for the Real Time On-Line BAS (including all modules) along with the all other Software items proposed and provided by the Bidder for all locations in this bid.

4. System integration

In Case of JVCA, one of the Bidder group members or the main bidder must work as a System integrator. The system integrator will be the main bidder and one-stop contact for

31

the bank for the entire scope of work mentioned above. Specifically the system integrator will ensure the following in the project:

Deliverable products and services Quality of the deliverables Project timelines

5. Project Timelines

The On-Line BAS solution would first be implemented on pilot basis at HO Divisions, Local Office, Corporate Branches, CDC & DRS. Once the duly customized and parameterized package is implemented in the pilot branches/offices in 14 months. The solution shall then be implemented at another 123 identified branches / offices as per the Bank’s priorities in the 1st stage of 2nd phase another 100 branches will be introduce to the same solution in the 2nd stage of the 2nd phase. The phase-1 of the project (under this tender) will reasonably be completed within 14 months. Maximum time allocated to successfully complete the whole project (all the phases) is 36 months. The bidder must submit the implementation schedule of 1 st phase reasonably completed within 14 th

month from the date of signing of the contract.

The Bank envisages implementing On-Line BAS in Stages as under:

Pilot Stage Implementation (Phase-1)

Pilot stage implementation in HO Divisions, CDC, DRS, Local Office and 11 Corpo-rate Branch within 14 months from the date of issue of the Work Order. All interfaces as required by the bank should be developed and successfully implemented by the end of the pilot implementation phase.

For the pilot implementation stage to be completed, all the testing including “Computer Room Pilot” and “User Acceptance Testing” should be completed. It will be the Bid-der’s responsibility to create the testing environment for the bank’s employees to do the testing and the Bidder will be required to assist the Bank in the entire testing phase. The testing environment should at all times support 15 concurrent users. The Bidder needs to provide separate test environment for On-Line BAS (Including all Modules), Deliv-ery Channels and other Software being a part of the solution to be provided by the Bid-der. The bank will not provide any desktops for the bidder personnel.

The CDC should be operational within 6 months from the date the Purchase Order is is-sued.

The Bank expects the Bidder to provide all the services related to On-Line BAS from the day the first pilot branch is successfully implemented.

The help desk should be fully functional from the day the first pilot branch is success-fully implemented.

The DRS site should be made available for implementing within 2 months from the date of the CDC going live and functional and be completed with within 2month.

Pilot (Phase-1) Implementation will be completed within 14 months.

Phase-2

Stage-1 Implementation:

Stage–2 implementation of 123 Branches currently running under Off-line Banking System within 10 month after completion of Pilot stage Implementation.

32

Stage-2 Implementation:

Stage-2 implementation of 100 non-computerized Grade-1 branches within 12 month after completion of Stage-2.

The Bank expects every new branch / office being migrated to the centralized-banking solution or being networked to be able to utilize the services of the helpdesk and the customer call center.

The Bank expects that all the customers of every new branch being migrated to the core-banking solution should be able to utilize all the delivery channels and any new branch opened by the Bank is also expected to directly operate on the proposed Real Time On-Line BAS and all delivery channels.

C. Technical Specifications

33

1. General Technical Requirements

1.1. Computing Hardware Support:The manufacturing vendor(s) should be in existence for at least 10 (Ten) years and offering the same brand for an equivalent period of time. The offered brand should be amongst the top 10 (Ten), according to the assessment of a reputed global market analyst, such as ‘Gartner’. The local partner/agent of the vendor must have at least 5 (Five) years proven experience in providing maintenance services.

And, the local partner/agent's relationship with the Principal/Manufacturer shall be at least 2 (Two) years.

1.2. Language Support: All information technologies must provide support for the Bengali and/or English language. Specially, all display technologies and software must support the complete ISO character sets and Unicode 2.1 or higher character set and performs sorting accordingly. Standard English language character sets for UK and USA should be supported by the technology in order to make the underlying system compatible with the international community. All keyboards of personal computers MUST support English and Bangla Character Set

1.3. Dates: All information technologies must properly display, calculate, and transmit date data, including, but not restricted to 21st Century date data. Preferred date formats are:

DD/MM/YYYY,

DD-MM-YYYY, and

DD Month, YYYY

Where DD, MM and YYYY represent two-digit date value, two-digit month value and four-digit year value respectively as prescribed by Gregorian calendar and Bangla Academy for Bengali calendar.

1.4. Electrical Power: All active (powered) equipment must operate on 220V±20V, 50Hz±2Hz. All active equipment must include power plugs of standard in Bangladesh.

1.5. Environmental: Unless otherwise specified, all equipment must operate in environments of 10–40 degree centigrade, 20–80 percent relative humidity, and 0–40 grams per cubic meter of dust.

1.6. Safety: Unless otherwise specified, all equipment must operate at noise levels no greater than 55 decibels. All electronic equipment that emits electromagnetic energy must be certified as meeting US FCC class A & B or EN 55022 and EN 50082–1 or equivalent emission standards. It has been observed that power fluctuation and blackout are common in the contemporary (2007) power supply system. Hence proper use of power cable, fuse & cut–out, surge suppresser, uninterruptible power supply, voltage

34

regulator, power conditioner, and earthed line should be introduced for all electrical and electronic equipment. All electrical and electronic equipment may produce carbide, CFC or other hazardous’ gases during their operation. Therefore proper air circulation and exhaustion facility should be introduced at the surroundings of all electrical and electronic equipment.

1.7. Notes to Bidder: The manufacturing vendor(s) should be in existence for at least 5 (five) years and offering the same brand for an equivalent period of time. The offered brand should be amongst the top 10 (10), according to the assessment of a reputed global market analyst, such as ‘IBS Magazine’, ‘Gartner’. The local agent of the Bidder must have proven experience in providing warranty & post warranty support services of Banking Application Software related at least five (05) years. The local partner/agent's relationship with the Principal/Manufacturer shall be at least one (2) year.

S/N Description Requirements

1. Manufacturing vendor in existence

At least 5 (five) years

2. Offered brand Amongst the top 10 (Ten) according to the assessment of a reputed global market analyst, such as ‘IBS Magazine’, ‘Gartner’, etc.

3. Local partner/agent Proven experience in providing warranty & post warranty support services of Banking Application Software related at least five (05) years.

4. Local partner/agent's relationship with the Principal/Manufacturer

At least 2 (two) year.

All items must be supplied locally by local vendors/distributors/service providers/business associates for ensuring local support and maintenance services. Licensing for all software (where applicable) must be registered through Regional Headquarters, under which Bangladesh falls, of the global software vendors for ensuring convenient upgradeability and renewal (as and when necessary).

35

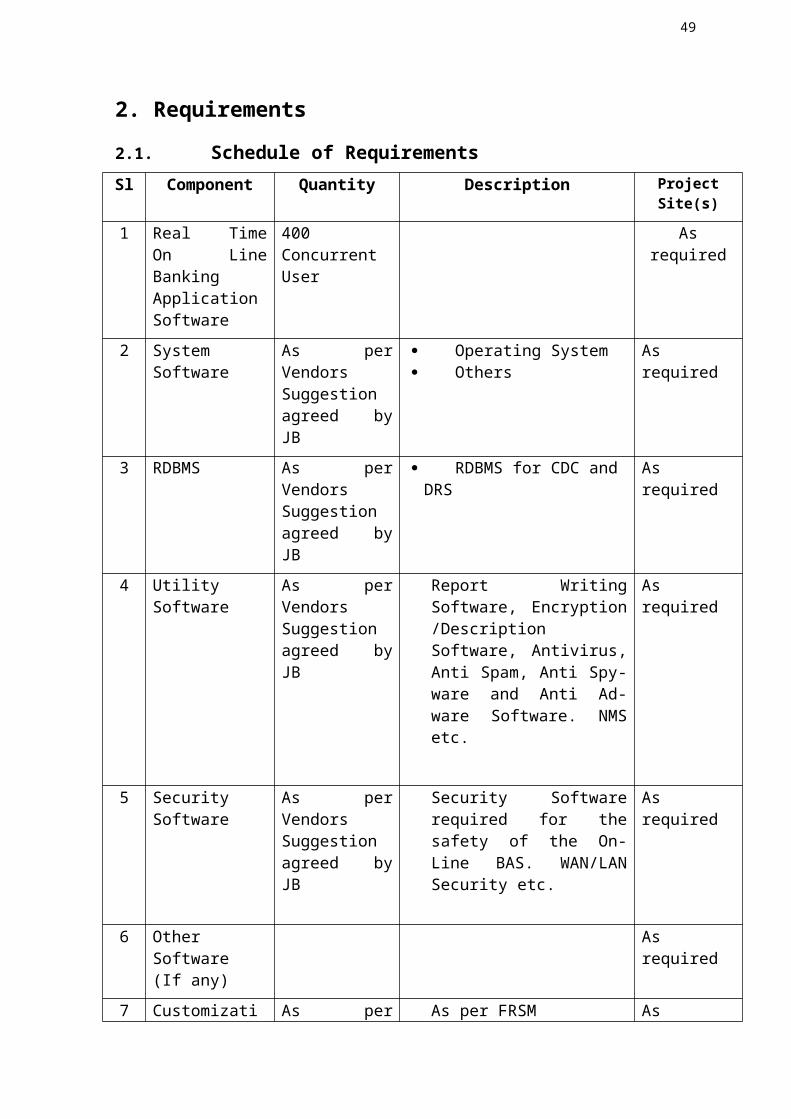

2. Requirements

2.1. Schedule of Requirements

Sl Component Quantity Description Project Site(s)

1 Real Time On Line Banking Application Software

400 Concurrent User

As required

2 System Software As per Vendors Suggestion agreed by JB

Operating System Others

As required

3 RDBMS As per Vendors Suggestion agreed by JB

RDBMS for CDC and DRS

As required

4 Utility Software As per Vendors Suggestion agreed by JB

Report Writing Software, Encryption /Description Software, Antivirus, Anti Spam, Anti Spy-ware and Anti Ad-ware Software. NMS etc.

As required

5 Security Software

As per Vendors Suggestion agreed by JB

Security Software required for the safety of the On-Line BAS. WAN/LAN Security etc.

As required

6 Other Software (If any)

As required

7 Customization/Development and Implementation

As per Vendors Suggestion agreed by JB

As per FRSM As required

8 Training As per Vendors Suggestion agreed by JB

As per Section VI, B. Busi-ness Function & Performance requirements’ Clause 2.1 (Training)

As required

9 Recurrent Services

As required As required

10 Turnkey Services As required

The bidder must submit the bid for all the components with detailed specification as per defined Technical, Financial, Legal & General requirements. In case of incomplete or in-sufficient data, the bid may face undesirable result.

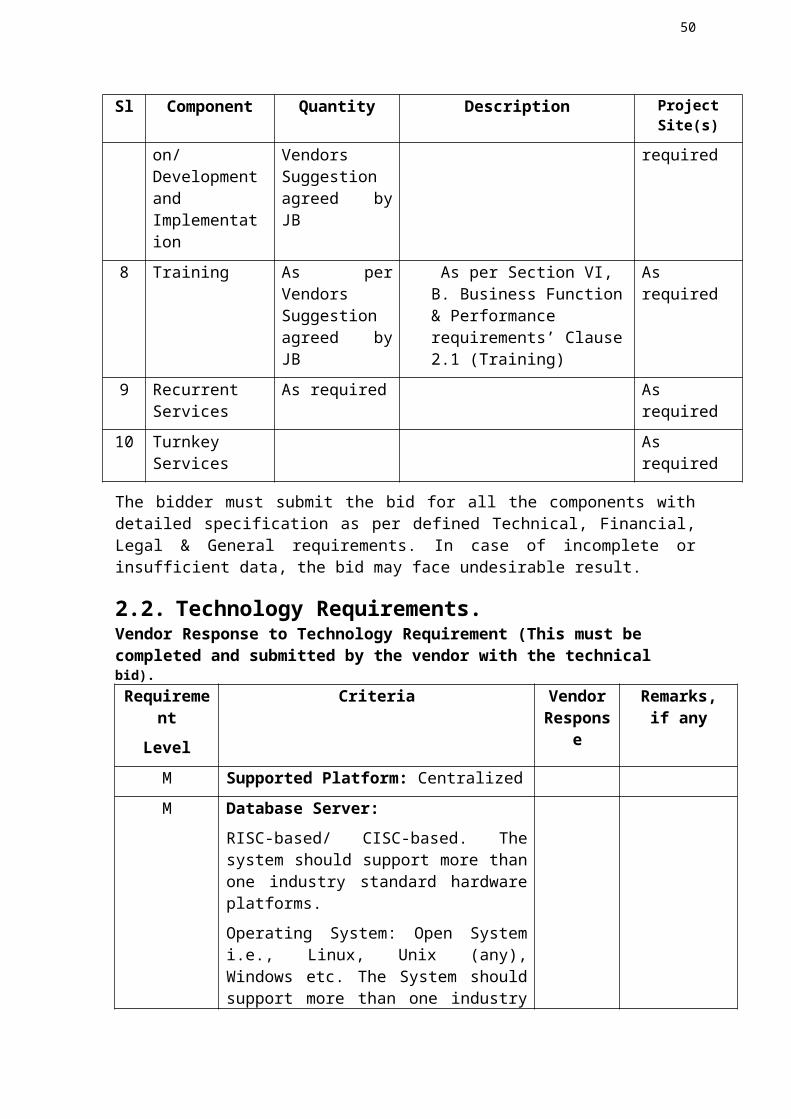

2.2. Technology Requirements.

36

Vendor Response to Technology Requirement (This must be completed and submit-ted by the vendor with the technical bid).Requirement

Level

Criteria Vendor Response

Remarks, if any

M Supported Platform: Centralized

M Database Server:

RISC-based/ CISC-based. The system should support more than one industry standard hardware platforms.

Operating System: Open System i.e., Linux, Unix (any), Windows etc. The System should support more than one industry standard operating system.

Database: Open Industry standard – Relational Database - The system should support more than one industry standard RDBMS.

M Application Server: CISC-based: Mention Units, No. Of Processors, Memory etc.

M Product Architecture:

Based on open systems and use industry standard platforms and technologies.

Core application based on an n-tier architecture

Browser based thin client as per industry standard.

Support for TCP/IP

Support Symmetric multi-processing

Support Multi Company, Multi Book and Multi Currency, Multi-Location, Multy-Country

Capability to be deployed over a high latency network. Specify latency tolerance.

Support for distributed computing

Ability to interface with 3rd party software like card management system, transaction switching system, IVR and other delivery channel management system using ISO 8583 messaging.

Ability to monitor server process and automatically bring up the replacement.

Support for 24x7x52 operations for all delivery channel like ATM/POS/Internet

37

banking/IVR.

Remote monitoring and administration of application servers.

The System must have Multi-Server Processing/Processing Load Balancing Capability

Parallel processing as a way to minimize re-sponse time for a transaction.

M Product Security:

Support for industry standard protocols such as https, SSL, RC4

Ability to plug in third party algorithms for security.