thailand – stabilität und wachstum - german technology symposium & exhibition (gts05),...

TRANSCRIPT

Thailand – Stabilität und Wachstum- German Technology Symposium & Exhibition (GTS05), Bangkok -

Wirtschaftstag Thailand, Berlin

23 September 2005

Dr. Paul Strunk, Hauptgeschäftsführer

German-Thai Chamber of [email protected]

Kingdom of Thailand514,000 square km, pop. 63.5 million

GDP per capita (PPP):US$ 7,100 (ca. 26% of Germany) [source: UNDP, 2004]

GDP total (PPP):US$ 478 billion [source:CIA, 2004]

Large and modern. Very fast economic growth

Top market and investment location

Source: NESDB

Thai GDP 1996 - 2005 in percentage change

5.9

-10.5

4.4 4.62.1

5.46.9 6.1

5.0

-1.5

-15

-10

-5

0

5

10

15

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Source: EIU, September 04

GDP growth by world region 2002 - 2005 in percentage change

0

1

2

3

4

5

6

7

Japan Euro area United States Developing Asia

2002

2003

2004

2005

External debt reduced from 94 per cent of GDP to 33 per cent of GDP (Q1 05). Reserves equal total debt and cover four times short term debt

Thai external debt vs. reserves in billion US$

109105

96

80

68

5952 49

27 3035 33 33

39

51

43

50 50

0

20

40

60

80

100

120

1997 1998 1999 2000 2001 2002 2003 2004 2005(Q1)

External debt

Reserves

Thai government budgetary balance fiscal years 1997- 2004 in billion Baht (note: fiscal year is Q4 - Q3 of calendar year)

-400000

0

400000

800000

1200000

1997 1998 1999 2000 2001 2002 2003 2004

Revenues

Expenditures

Balance

Thai Consumer Price Index (CPI) in percentage change

4.8

7.78.1

0.3

1.6 1.6

0.7

1.9

3.6

2.7

0

2

4

6

8

10

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

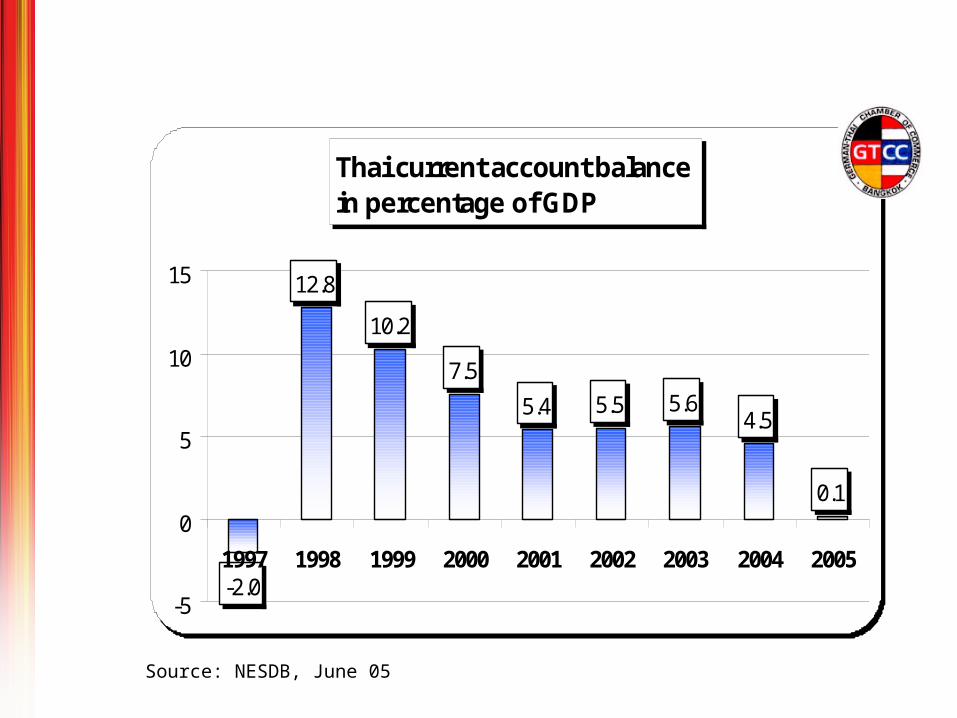

Source: NESDB, June 05

Thai private consumption (percentage change)

3.9

5.3

6.4

4.6

5.6

0

2

4

6

8

2001 2002 2003 2004 2005

Source: NESDB, June 05

Thai private investment (percentage change)

4.9

13.4

17.515.3

10.6

0

10

20

30

2001 2002 2003 2004 2005

Source: NESDB

Thai imports vs. exports in percentage change

31

5

1720

-7

6

19

-3

23

27

16

23

-10

0

10

20

30

40

2000 2001 2002 2003 2004 2005

Thai imports

Thai exports

Source: NESDB, June 05

Thai current account balance in percentage of GDP

12.8

10.2

7.5

5.4 5.5 5.64.5

0.1

-2.0-5

0

5

10

15

1997 1998 1999 2000 2001 2002 2003 2004 2005

BOI approvals double in value in 2003 and rise by another 49 per cent in 2004

BOI approval of foreign projects (in number of projects and value in billion Baht)

517

761

575

483563

734

136213 210

100

213

317

0

400

800

1999 2000 2001 2002 2003 2004

Applicationsapproved

Value in billion baht

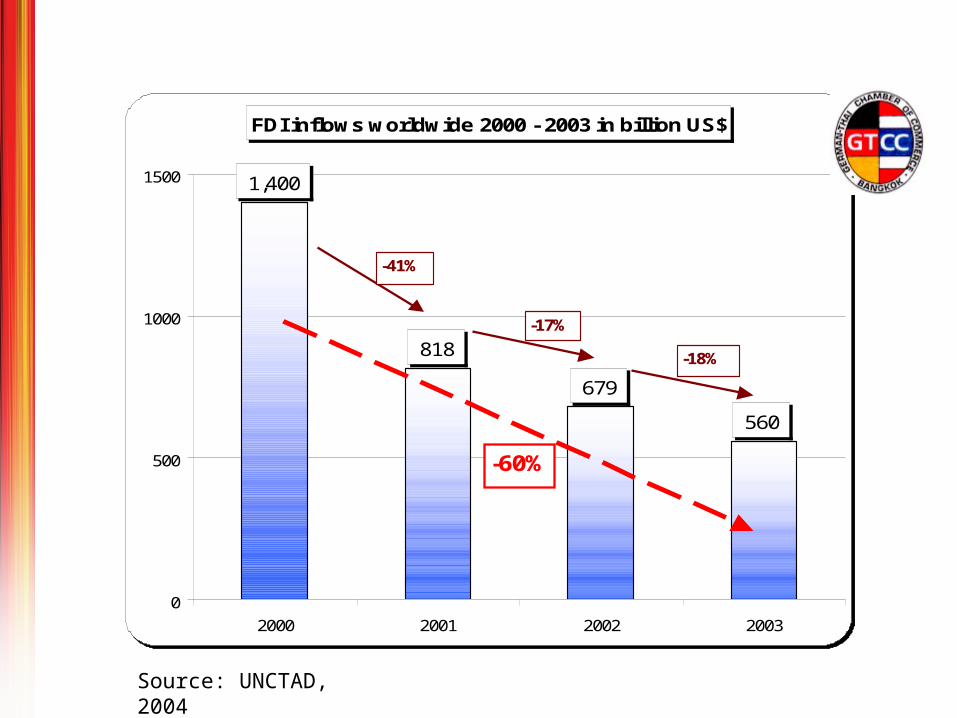

FDI inflows worldwide 2000 - 2003 in billion US$

1,400

818

679

560

0

500

1000

1500

2000 2001 2002 2003

-41%

-18%

-17%

-60%

Source: UNCTAD, 2004

BOI approval of foreign projects (in number of projects and value in billion Baht)

387428

152191

0

300

600

2004 (Jan - Jul) 2005 (Jan - Jul)

Applicationsapproved

Value in billion baht

BOI approvals rise by 26 per cent in value in Jan – Jul 2005 vs. Jan – Jul 2004

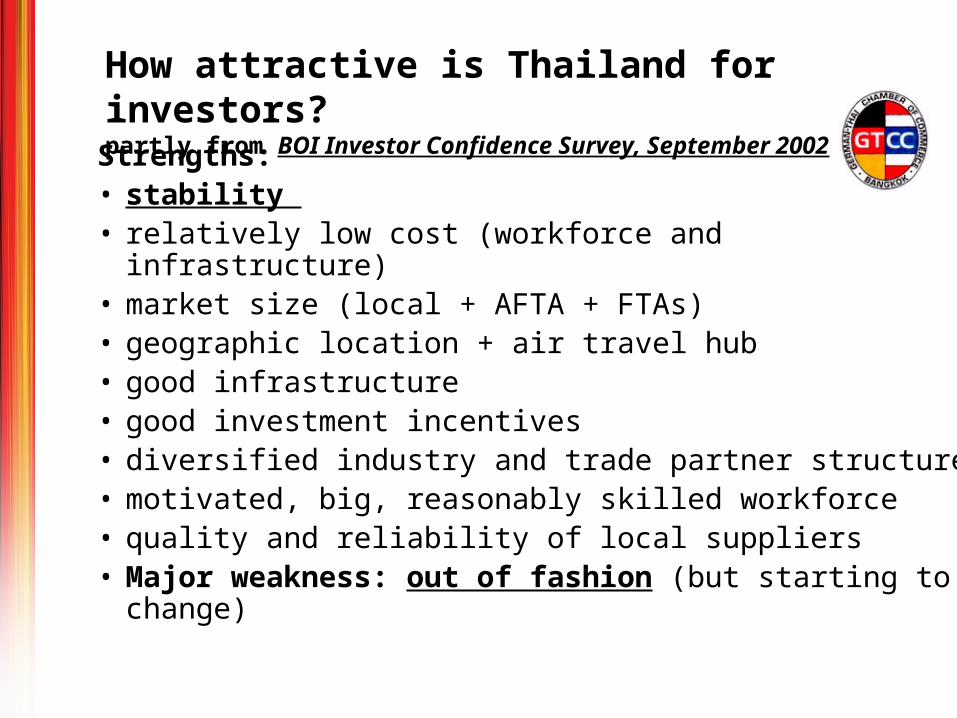

How attractive is Thailand for investors?

partly from BOI Investor Confidence Survey, September 2002

Strengths:• stability • relatively low cost (workforce and infrastructure)• market size (local + AFTA + FTAs)• geographic location + air travel hub• good infrastructure• good investment incentives• diversified industry and trade partner structure• motivated, big, reasonably skilled workforce• quality and reliability of local suppliers• Major weakness: out of fashion (but starting to

change)

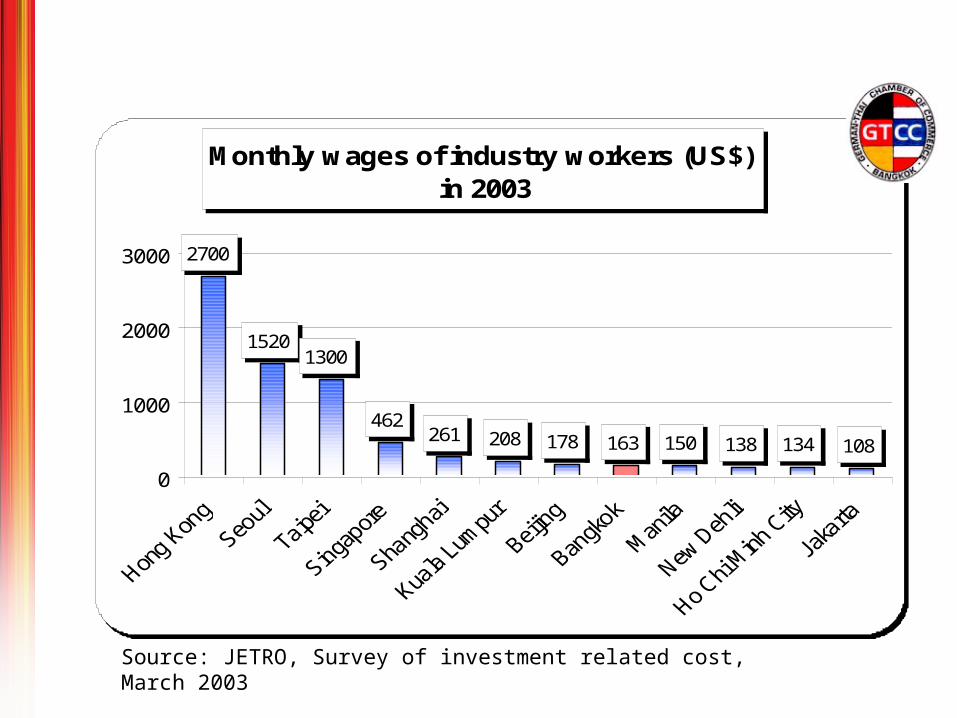

Monthly wages of industry workers (US$) in 2003

2700

15201300

462261 208 178 163 150 138 134 108

0

1000

2000

3000

Source: JETRO, Survey of investment related cost, March 2003

Office rent monthly per square meter (US$) in 2003

46 45

39 38 37

2422 21 20

17

108

0

10

20

30

40

50

Source: JETRO, Survey of investment related cost, March 2003

Housing rent for expatriates (US$ per month) in 2003

4,650

4,000

3,461

2,836 2,800

2,073 2,0001,729 1,723

1,4961,311

763

0

1000

2000

3000

4000

5000

Source: JETRO, Survey of investment related cost, March 2003

Electricity rate for business use (US$) per month in 2003 (at contracted power: 2,000 kW, amount of use: 500,000 kWh)

77,660

52,240 50,000 48,300 45,220

35,000 34,100 31,540 30,200 28,240 26,700 25,440

0

30000

60000

90000

Source: JETRO, Survey of investment related cost, March 2003

UNCTAD:Top FDI destinations 2004 - 2007 (Global Investment Prospects Assessment [GIPA] among 87 FDI experts, Aug 04)

7755

43

21

0

10

Political & Economic Risk Consultancy (PERC) 2002 report

Quality of life for expatriate families (lower number represents a better mark)

2.26

3.76 3.84 3.98 4.04 4.09 4.144.84

5.42 5.686.59

3.45

0

2

4

6

8

10

“Thailand’s people are some of the most hospitable in the world, and it is hard not to feel comfortable in the land of smiles”

Key industries and sectors for investment from a GTCC view:

• automotive components• chemicals + plastics• diverse manufacturing (German

investment,e.g., in packaging, optical lenses, shower cabins, butterfly valves, household appliances, compressed air pumps, construction machines, electronics)

• agro-industries• education, R+D, certification, calibration

diversified industry structure allows for diversified investment