the art of economic forecasting and the us economic

TRANSCRIPT

June 21, 2011

333 South Grand Avenue Los Angeles, CA 90071

The Art of Economic Forecasting & the Mid-Year US Economic Outlook

Jeffrey C. ClevelandSenior Economist

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

Can We Model the Economy?The Economy

“Human behavior is simply too complex and nuanced to be fully represented mathematically, at least with the maths known to modern man. Maths can help us to gain insight into economic processes, but it is not the only way to gain such insight, nor even the most productive.” -- DeLisle Worrell, Governor of the Central Bank of Barbados

2

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

33

The US Economy is Like A Giant Jigsaw Puzzle

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

44

Growth/Unemployment Remain the Bigger Risk, Despite Inflation Dominating the Headlines

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

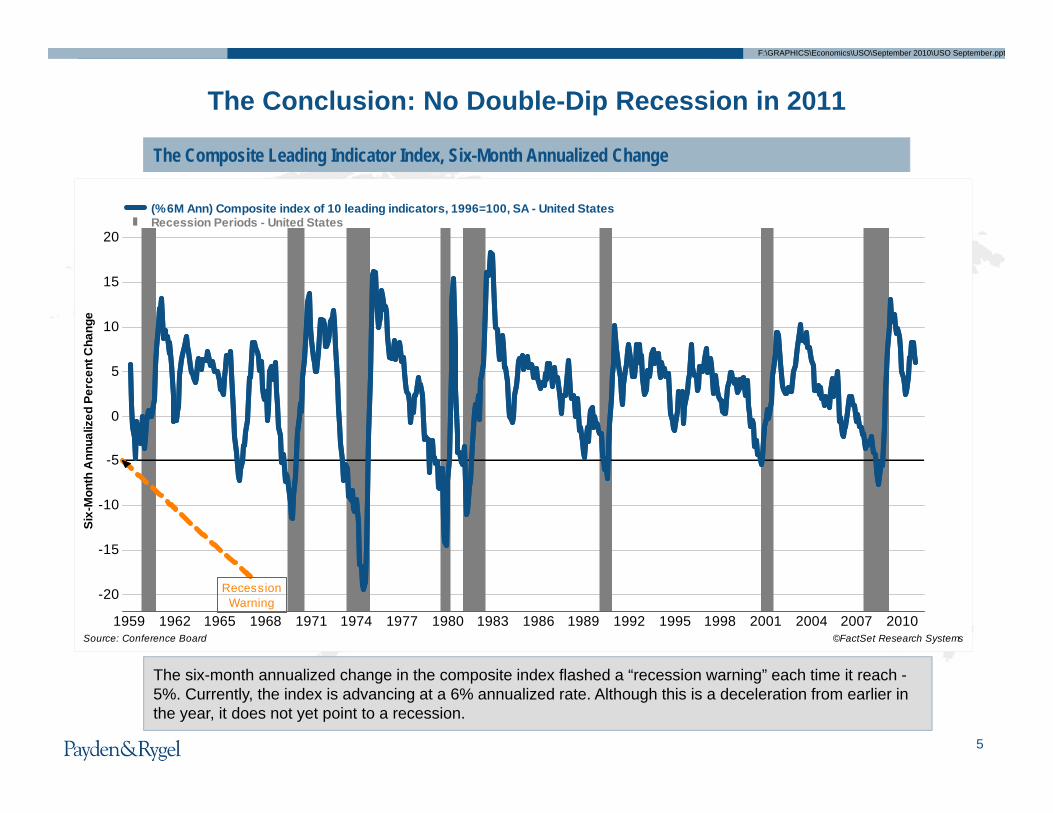

The Composite Leading Indicator Index, Six-Month Annualized Change

The Conclusion: No Double-Dip Recession in 2011

The six-month annualized change in the composite index flashed a “recession warning” each time it reach -5%. Currently, the index is advancing at a 6% annualized rate. Although this is a deceleration from earlier in the year, it does not yet point to a recession.

1959 1962 1965 1968 1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

-20

-15

-10

-5

0

5

10

15

20

Six-

Mon

th A

nnua

lized

Per

cent

Cha

nge

Recession Warning

©FactSet Research SystemsSource: Conference Board

(% 6M Ann) Composite index of 10 leading indicators, 1996=100, SA - United States Recession Periods - United States

5

The Art of Economic ForecastingThe Art of Economic Forecasting

II

The Problem: The Plight of the Fortune Tellers

Types of Forecasting

Our Outlook: The Narrative

The Outlook in Numbers: GDP, Employment, Inflation, Interest Rates

III

IV

I

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

The Problem: The Plight of the Fortune TellersI

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

8

The Problem: How do we make decisions about the future in a world of uncertainty?

The Cardsharps, Cavaggio (1594)

Where is the economy headed?

What is the path of interest rates?

What are the inflation/deflation

risks?

What’s going on in the labor market?

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

Physical science

Rain

Snow

Wind

Laboratory Experiments

Meteorology Economics

Social science

Human Beings

Human Choice

Data Availability

History, But Few Labs

“Most fundamentally, and perhaps most challenging for researchers, the crisis should motivate economists to think further about their modeling of human behavior.” – Ben Bernanke commenting on economics in the

wake of the financial crisis

The Economist or the Meteorologist: Which is More Accurate?

9

Types of ForecastsII

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

11

Types of Forecasts

Forecast Type Example“Theory-free” forecasts Leading indicators

Mathematical “models” of the economy The Fed model

Market-based models The Yield Curve

“The Mental Model” The Art: Combines narrative + economic indicators + market-

based indicators

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

12

The US Index of Leading Indicators Suggests Growth Will Improve

2006 2007 2008 2009 2010 2011

-5.0

0.0

5.0

10.0

Qua

rter

-ove

r-Q

uart

er A

nnua

lized

Per

cent

Cha

nge

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0 Quarter-over-Q

uarter Annualized Percent C

hange

Sources: The Conference Board and The Commerce Department

Composite index of 10 leading indicators (Left)Real Gross Domestic Product (Right)

Composite of 10 Leading Economic Indicators and Real Gross Domestic Product (GDP)

The Conference Board’s Leading Economic Index (LEI) leads turning points in the economy by an average of 7 months. The index correctly predicted a rebound in real GDP growth over the past 2 years. At the present time, it is pointing to continued expansion in the second half of 2011.

Recession Periods – United States

Last Updated: Q2 2011

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

1313

Short-Term Focus: Leading Economic Indicators Score CardLead Time(months) Reliability

Growth Momentum (3-Month Change)

Pointing to Recession?

Financial Indicators

Yield Curve 12 to 24 High Moderating XM2 12 to 24 Low Rising XStock Prices 3 to 6 Medium Moderating XReal Indicators

Building Permits 6 to 9 High Stable XISM Manufacturing Index 3 to 6 High Moderating XConsumer Expectations 3 to 6 Low Moderating XNew Orders for Nondefense Durable Goods 1 to 3 High Moderating XUnemployment Insurance Claims 1 to 3 Medium Moderating XNew Orders for Consumer Goods 1 to 3 Medium Moderating X Average Weekly Hours (Manufacturing) 1 to 3 High Stable X

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

Real GDP and Yield Spread between 2-Year and 10-Year US Treasuries

The yield curve tends to lead the economy by between 1 to 2 years, and is defined as the difference between 2-and 10-year US Treasury yields. To illustrate, if investors think the coming two years will be much better for the economy than the next six years, the yield spread will be small or even negative. Currently, however, the curve is pointing towards a continued expansion.

The Yield Curve Is Indicating Positive Growth

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010-1%

-0.5%

0%

0.5%

1%

1.5%

2%

2.5%

3%

3.5%

Yiel

d Sp

read

in B

asis

Poi

nts

-6%

-4%

-2%

0%

2%

4%

6%

Year-to-Year Percent Change

Sources: Federal Reserve and the Commerce Department

US Treasury Yield Curve (10Yr - 2Yr) (Left)US Gross Domestic Product (Right)

Recession Periods - United States

14

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

Money Supply (M2) and National Product Account

After falling sharply during the recession, the money supply (M2) began to expand again in mid-2010. M2 tends to lead the economy by between one to two years, so the recent expansion is a positive sign for future growth.

The Money Supply Has Begun to Expand

2001 2002 2003 2004 2005 2006 2007 2008 2009 20100%

2%

4%

6%

8%

10%

12%

Year

-to-

Year

Per

cent

Cha

nge

in M

2

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

Year-to-Year Percent Change in N

PA

©FactSet Research SystemsSource: The Federal Reserve

Money Supply M2 (Left)National Product Account GDP (Right)

Recession Periods - United States

15

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

Stock Market Growth is Slower But Still Above Year-Ago LevelsUS Stock Prices

Despite a recent slowing, the S&P 500 is over 13% higher than it was one year ago. Stock prices generally lead the economy by between three to six months.

2009 2010-60%

-40%

-20%

0%

20%

40%

60%

80%

Year

-to-

Year

Per

cent

Cha

nge

©FactSet Research SystemsSource: Standard & Poor's

S&P 500 Stock Price Index Recession Period - United States

Equity prices are still rising, just less quickly

16

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

After Plummeting Post-Tax Credit, Home Sales Show Some Life

Existing Home Sales and Economic Growth

The federal homebuyer tax credit produced a large spike in sales of existing homes in 2009-2010. Following the expiration of the credit, homes sales experienced the largest month-to-month percentage drop in history. However, after the initial adjustment, sales appear to be growing again, perhaps aided by record low mortgage rates and investors looking for deals on foreclosed homes.

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Year

-to-

Year

Cha

nge

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

Year-to-Year Change

©FactSet Research SystemsSources: National Association of Realtors and Commerce Department

US Existing-Home Sales (Left)US Real Gross Domestic Product, Lagged 1 Yr (Right)

Recession Periods - United States

17

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

ISM Purchasing Managers Index and Non-Residential Business Investment

The Institute of Supply Management’s Index of manufacturing activity rose dramatically following the recession and continues to rise as demand returns and companies replenish their low inventories. Recently, the index reached a 25-year high. The steep pull back is a concern, but the measures is above 50, indicating expansion, not contraction. Business investment is likely to continue to grow in coming months.

Manufacturing and Business Investment Continue to Drive Growth

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010-20

-15

-10

-5

0

5

10

Year

to Y

ear P

erce

nt C

hang

e

35

40

45

50

55

60

Index

Sources: Institute for Supply Management and the Commerce Department

ISM Manufacturing Index (Right)Business Investment (Left)Recession Periods - United States

18

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

Confidence and Consumer Spending Battered by Gas Prices

2005 2006 2008 2009 2011

30

40

50

60

70

80

90

100

110

Inde

x

-2%

-1%

0%

1%

2%

3%

4%

Year-over-Year Percent Change

Sources: The Conference Board and The Commerce Department

The Conference Board Consumer Confidence Expectations (Left)Real Consumer Spending (Right)

Consumer Expectations Six Month Hence and Real Consumer Spending

After faltering in the summer of 2010, consumer confidence and consumer spending have rebounded into year end. Rising gas prices stifled consumer spending and sentiment in early 2011. Over the past decade, expectations have had an 89% correlation with consumer spending.

19

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

2005 2006 2007 2008 2009 2010-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Year

to Y

ear P

erce

nt C

hang

e

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Year to Year Percent Change

©FactSet Research SystemsSources: Census Department and the Commerce Department

Business Investment (Left)Capital Expenditure Excluding Aircraft and Defense (Right)Recession Periods - United States

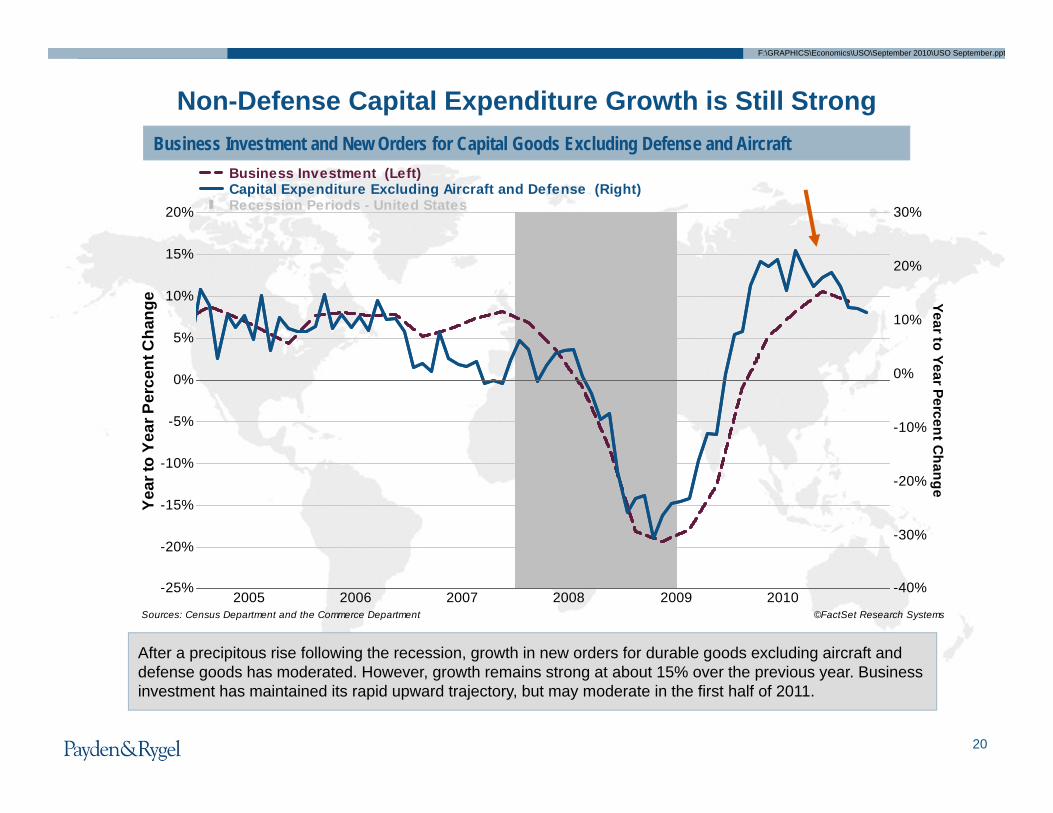

Business Investment and New Orders for Capital Goods Excluding Defense and Aircraft

After a precipitous rise following the recession, growth in new orders for durable goods excluding aircraft and defense goods has moderated. However, growth remains strong at about 15% over the previous year. Business investment has maintained its rapid upward trajectory, but may moderate in the first half of 2011.

Non-Defense Capital Expenditure Growth is Still Strong

20

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

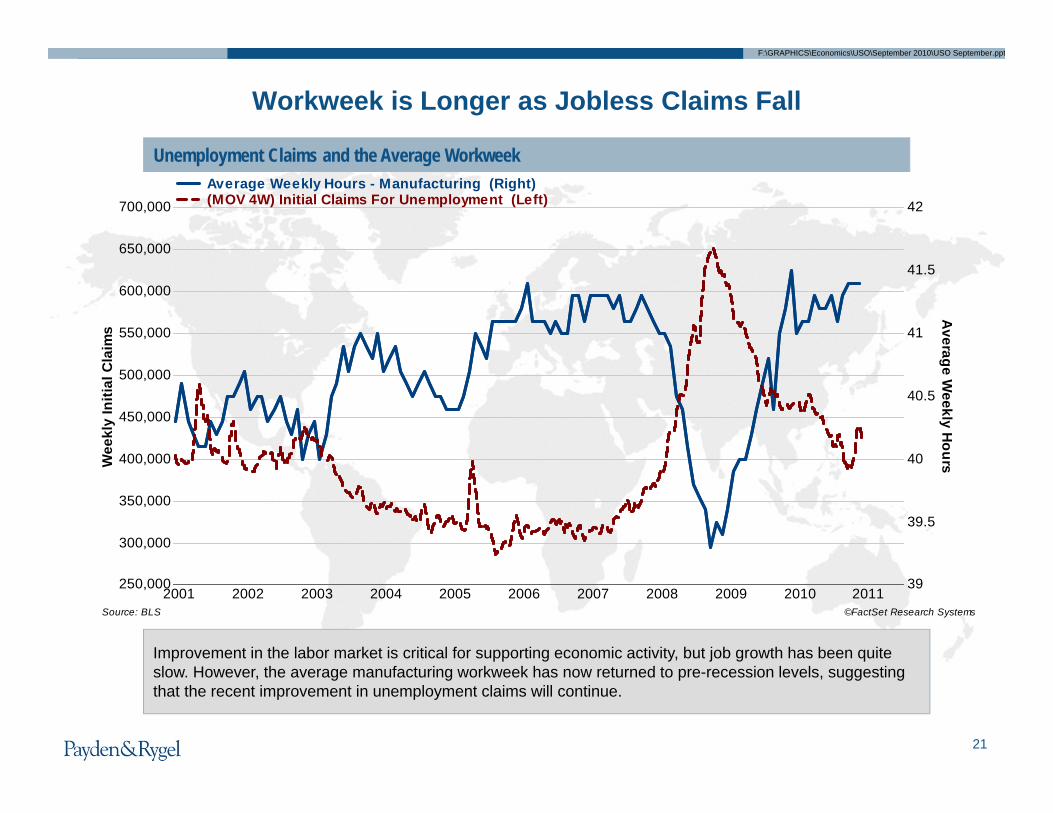

Unemployment Claims and the Average Workweek

Workweek is Longer as Jobless Claims Fall

Improvement in the labor market is critical for supporting economic activity, but job growth has been quite slow. However, the average manufacturing workweek has now returned to pre-recession levels, suggesting that the recent improvement in unemployment claims will continue.

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

700,000

Wee

kly

Initi

al C

laim

s

39

39.5

40

40.5

41

41.5

42

Average W

eekly Hours

©FactSet Research SystemsSource: BLS

Average Weekly Hours - Manufacturing (Right)(MOV 4W) Initial Claims For Unemployment (Left)

21

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

The Composite Leading Indicator Index, Six-Month Annualized Change

The Conclusion: No Double-Dip Recession in 2011

The six-month annualized change in the composite index flashed a “recession warning” each time it reached -5%. Currently, the index is advancing at a 6% annualized rate. Although this is a deceleration from earlier in the year, it does not yet point to a recession.

1959 1962 1965 1968 1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

-20

-15

-10

-5

0

5

10

15

20

Six-

Mon

th A

nnua

lized

Per

cent

Cha

nge

Recession Warning

©FactSet Research SystemsSource: Conference Board

(% 6M Ann) Composite index of 10 leading indicators, 1996=100, SA - United States Recession Periods - United States

22

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

1946 1949 1952 1955 1958 1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009

-4

-2

0

2

4

6

Yiel

d Sp

read

: 10-

year

Tre

asur

y yi

elds

min

us 3

-mon

th b

ill y

ield

s

©FactSet Research SystemsSource: FactSet

US Benchmark Bond - 10 Year - Yield - US Benchmark Bond - 3 Month - Yield Recession Periods - United States

The Yield Curve Model

The yield curve is the single most reliable predictor of recessions. Over the past 60 years, each time the yield curve “inverted,” or 3-month yields were higher than 10-year yields, the business cycle peaked about 18-24 months later and a recession followed. There was one false signal during the mid-1960s. Currently, the curve is very steep, indicating that the expansion is likely to continue.

False alarm

23

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

Mathematical Models of the EconomyThe Economy

“Human behavior is simply too complex and nuanced to be fully represented mathematically, at least with the maths known to modern man. Maths can help us to gain insight into economic processes, but it is not the only way to gain such insight, nor even the most productive.” -- DeLisle Worrell, Governor of the Central Bank of Barbados

24

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

Our Outlook: The Economic NarrativeIII

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

2626

The US Economy is Like A Giant Jigsaw Puzzle

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

1951 1954 1957 1960 1963 1966 1969 1972 1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 20081

1.5

2

2.5

3

3.5

4

Mul

tiple

of N

omin

al G

DP

Source: Federal Reserve

Credit market Debt Outstanding to Nominal GDP

2727

Boom and Bust Cycle Still in the Unwinding Phase

After building too many homes and employing too many workers in housing-related industries, the 2007 bust forced a reallocation of resources (both labor and capital) across the economy.

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

Trill

ions

of U

S $

Sources: Federal Reserve Flow of Funds and Federal Reserve Bank of New York Report #458, July 2010Shadow Banking consists of: total outstanding open market paper, total repo liabi

Shadow Banking Liabilities Commercial Banking Liabilities

28

The Real Financial System: George Bailey Is Dead

George Bailey’s system dominated here

“Shadow Banking” – Vital to Credit Process, Now in Retreat

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

This Time Really IS Different: Nonfarm Employment From the Start of Each Recession

29

Nonfarm Employment Levels, Percent Change Since Peak By Recession

Current recovery levels of employment are 5% below pre-recession peak

Recession Start Year

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

This Time Really IS Different: Real GDP Since the Start of Each Recession

30

Real GDP Level, Percent Change Since Peak by Recession

Economic output is back above the pre-recession peak, but still a following a shallow path relative to previous recoveries

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

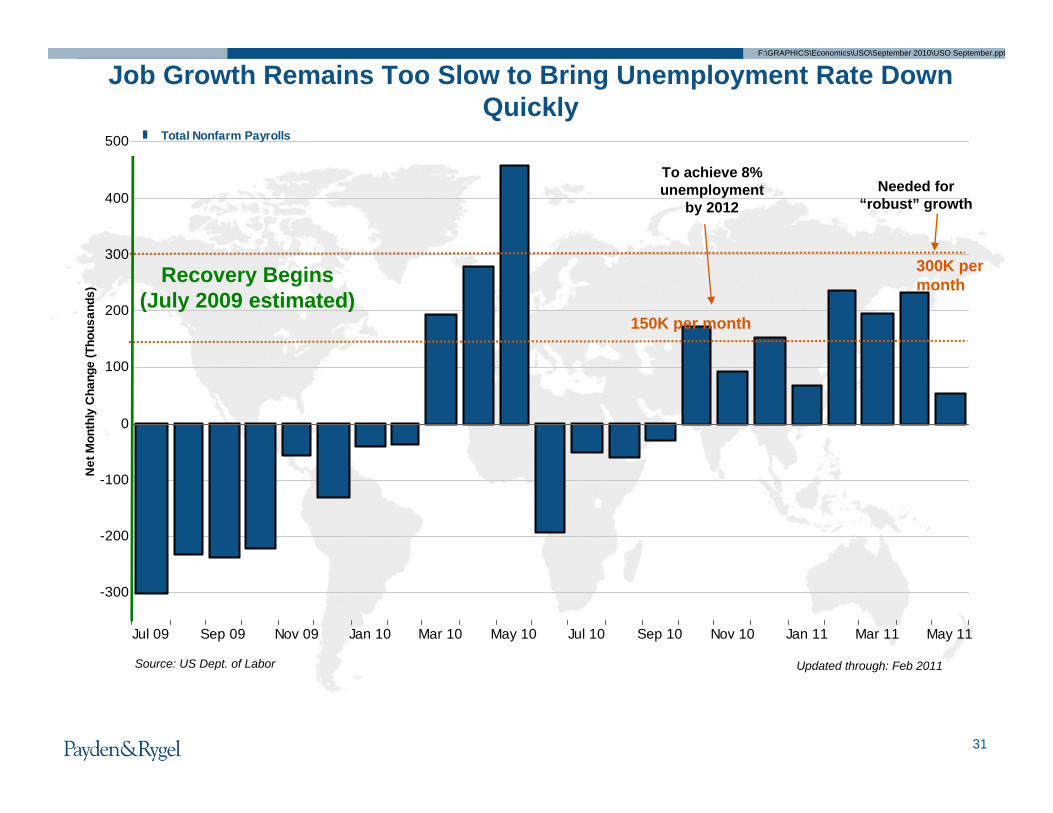

Jul 09 Sep 09 Nov 09 Jan 10 Mar 10 May 10 Jul 10 Sep 10 Nov 10 Jan 11 Mar 11 May 11

-300

-200

-100

0

100

200

300

400

500

Net

Mon

thly

Cha

nge

(Tho

usan

ds)

Total Nonfarm Payrolls

31

Job Growth Remains Too Slow to Bring Unemployment Rate Down Quickly

300K per month

150K per month

Recovery Begins (July 2009 estimated)

Needed for “robust” growth

To achieve 8% unemployment

by 2012

Updated through: Feb 2011Source: US Dept. of Labor

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

32

Too Few Have Jobs

Updated through: Apr 2011Source: US Dept. of Labor1948 1951 1954 1957 1960 1963 1966 1969 1972 1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008

54

56

58

60

62

64

66

Perc

ent o

f Wor

king

Age

Pop

ulat

ion

Empl

oyed

Cyclical: The current ratio at 58.4% in May when compared

to the long-term trend at approximately 61.8%

suggests there are 6 million people able to work but

unemployed.

Structural: The long-term trend line reflects

structural shifts in the US economy (e.g., rise of

female labor force participation and the baby

boomer retirement)

©FactSet Research SystemsSource: BLS

Employment-to-Population Ratio (% of Working Age, Civilian, Non-instititional Population Employed)Recession Periods - United StatesTrendline: 10 Year Moving Average

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

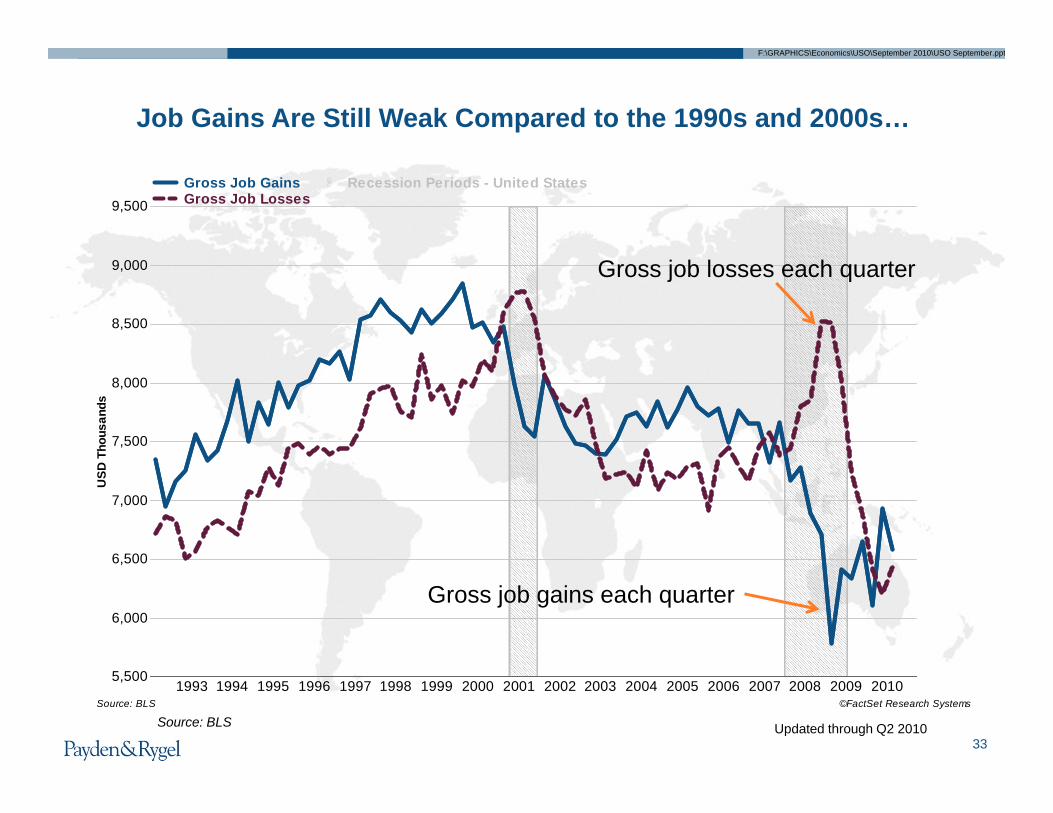

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 20105,500

6,000

6,500

7,000

7,500

8,000

8,500

9,000

9,500

USD

Tho

usan

ds

©FactSet Research SystemsSource: BLS

Gross Job GainsGross Job Losses

Recession Periods - United States

33

Job Gains Are Still Weak Compared to the 1990s and 2000s…

Gross job losses each quarter

Gross job gains each quarter

Updated through Q2 2010Source: BLS

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

Small Business Plans to Hire/Fire and Job Openings

34

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 20112,000

2,500

3,000

3,500

4,000

4,500

5,000

Job

Ope

ning

s, T

hous

ands

-10

-5

0

5

10

15

20

% Plans to H

ire/Fire(+/-) Over the N

ext Three Months

Sources: National Federation of Independent Businesses, Bureau of Labor Statistics

Plans to Hire/Fire Over the Next Three Months (Right)Job Openings, Total Nonfarm (Left)Recession Periods - United States

Small businesses employ 91 million workers and account for most of the hiring in the last 12 months…

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

35

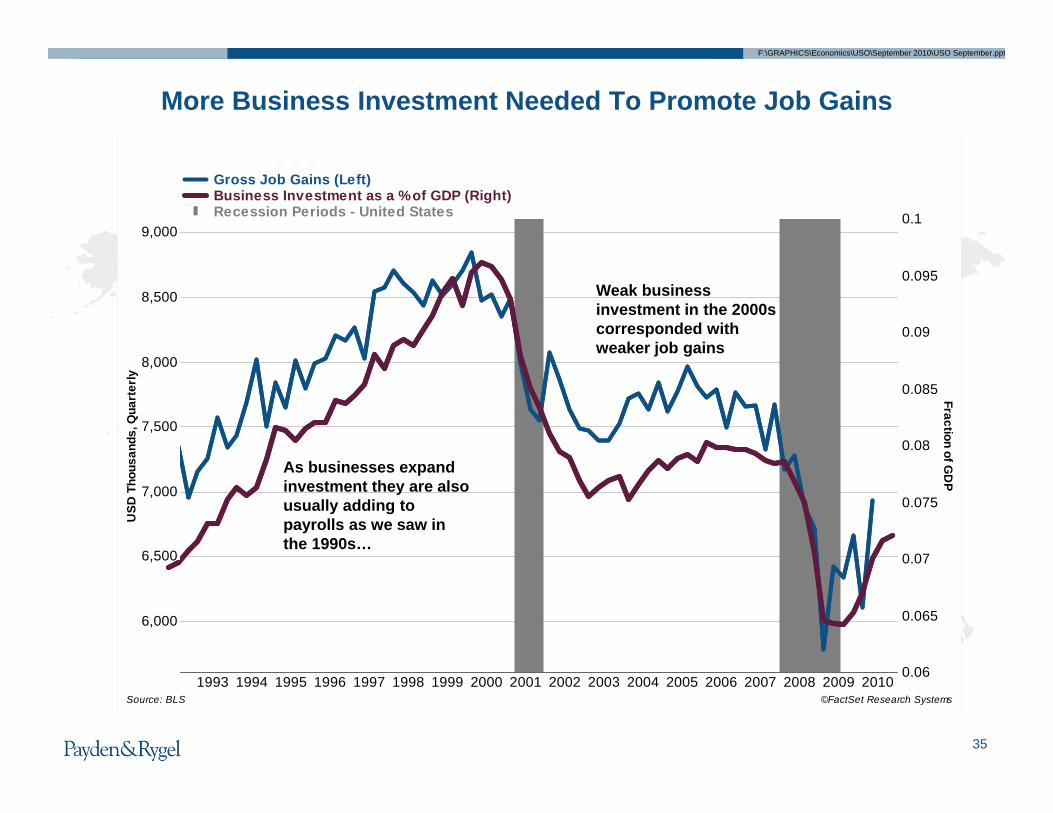

More Business Investment Needed To Promote Job Gains

Updated through: 10-29-20101993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

6,000

6,500

7,000

7,500

8,000

8,500

9,000

USD

Tho

usan

ds, Q

uart

erly

0.06

0.065

0.07

0.075

0.08

0.085

0.09

0.095

0.1

Fraction of GD

P

©FactSet Research SystemsSource: BLS

Gross Job Gains (Left)Business Investment as a % of GDP (Right)Recession Periods - United States

As businesses expand investment they are also usually adding to payrolls as we saw in the 1990s…

Weak business investment in the 2000s corresponded with weaker job gains

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

36

What’s the Fed To Do? Another Way To Think of Monetary PolicyThe Fed wants some positive rate of inflation (approximately 2%) and higher inflation expectations…

….but not too much inflation!

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

2007 2007 2007 2008 2008 2008 2008 2009 2009 2009 2009 2010 2010 2010 2010 20110

0.5

1

1.5

2

2.5

Trill

ions

of U

SD

Source: Federal Reserve

U.S. Treasuries Mortgage-backed Securities

Term Auction Credit Federal Agency Debt

37

Policy Response: The Fed’s Balance Sheet, Quantitative Easing 1 & 2

QE1: Federal Agency

Source: Federal Reserve

“If action is taken by the Fed, a clear option is to grow the size of the balance sheet since the policy interest rate, for all practical purposes, cannot go any lower” – Dennis P. Lockhart, President, Federal Reserve Bank of Atlanta, 9/28/2010

Updated through: 3-1-2011

QE1: Mortgage-Backed Securities – shrinking

over time

QE2 + reinvestment of maturing mortgage debt

US Treasuries

Liquidity Facilities & Other

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

2006 2007 2008 2009 20100

0.5

1

1.5

2

2.5

3

Trill

ions

of U

S D

olla

rs

©FactSet Research SystemsSource: Federal Reserve

Reverse Repurchase AgreementsDeposits, Depository InstitutionsCurrency in Circulation (Left)

3838

The Other Side of the Fed Balance Sheet: New “Bank Reserves” Created To Pay for Treasury Purchase Program (QE2)

“Bank Reserves”

Physical Currency(Cash in your wallet)

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

39

The Limits of QE: Banks Accumulate Excess Reserves, Not New Loans

01/2006 01/2007 01/2008 01/2009 01/20100

500

1,000

1,500

2,000

2,500

USD

Bill

ions

Excess Reserves

Commercial Banks, Cash Assets

Federal Reserve Assets

Source: Federal Reserve

Commercial Banks, Cash AssetsFederal Reserve AssetsExcess Reserves

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

11/2010 12/2010 01/2011 02/2011 03/2011 04/2011 05/2011 06/2011

1,000

1,200

1,400

1,600

1,800

2,000

USD

Bill

ions

6,680

6,700

6,720

6,740

6,760

6,780

6,800

USD

Billions

Commercial Banks, Loans & Leases (Right)

Excess Reserves (Left)

Commercial Banks, Cash Assets (Left)

Source: Federal Reserve

Commercial Banks, Cash Assets (Left)Excess Reserves (Left)Commercial Banks, Loans & Leases (Right)

40

The Limits of QE: Banks Accumulate Excess Reserves, Not New Loans

The banks are hoarding money…

…and not making new loans.

In textbooks, reserves work through the “money multiplier” to increase aggregate lending and demand.

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

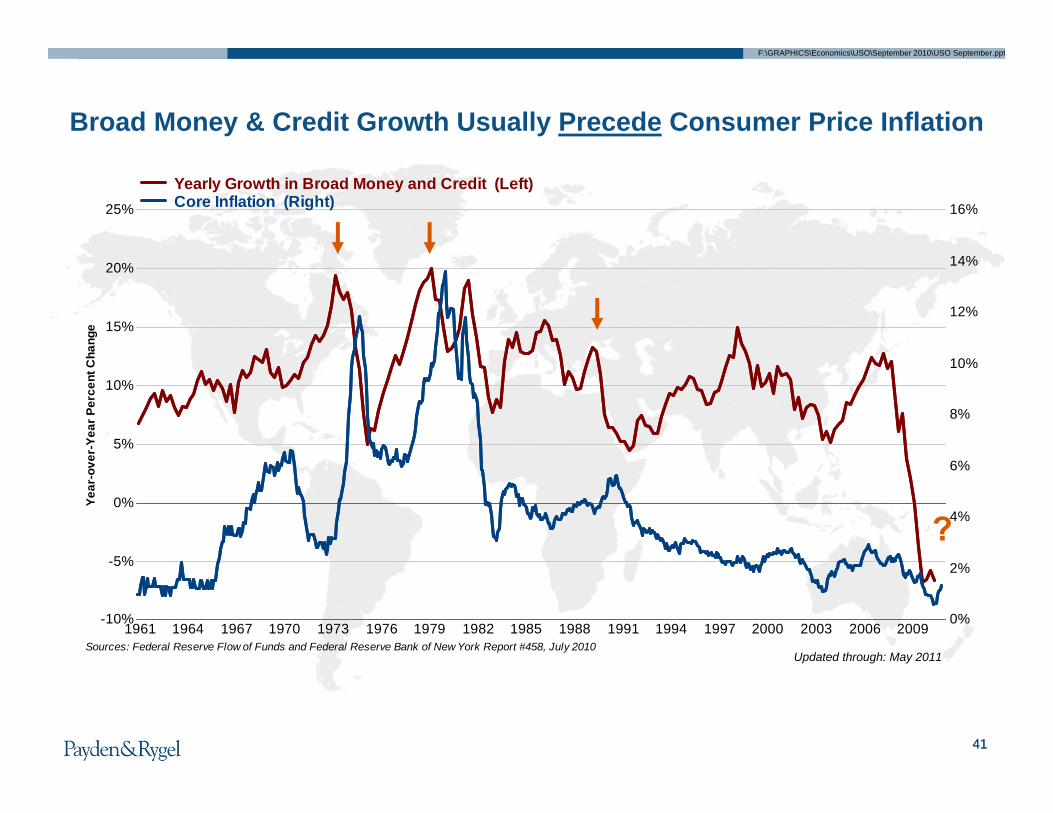

1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009-10%

-5%

0%

5%

10%

15%

20%

25%

Year

-ove

r-Ye

ar P

erce

nt C

hang

e

0%

2%

4%

6%

8%

10%

12%

14%

16%

Sources: Federal Reserve Flow of Funds and Federal Reserve Bank of New York Report #458, July 2010

Yearly Growth in Broad Money and Credit (Left)Core Inflation (Right)

4141

Broad Money & Credit Growth Usually Precede Consumer Price Inflation

?

Updated through: May 2011

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

The Outlook in NumbersIV

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

43

2011 Baseline US Economic Forecast*

Actual Forecast

2009 2010 2011Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Real GDP(quarter-to-quarter annualized percent change)

1.6 5.0 3.7 1.7 2.6 3.1 2.0 2.5 3.0 3.3

Unemployment Rate(percent)

9.6 10.0 9.7 9.7 9.6 9.6 8.9 8.8 8.6 8.5

Headline CPI Inflation(year-over-year percent change)

-1.6 1.5 2.4 1.8 1.2 1.2 2.2 3.5 3.3 2.8

Core CPI Inflation(year-over-year percent change)

1.5 1.7 1.3 1.0 0.9 0.6 1.1 1.2 1.4 1.6

Federal Funds Rate(percent)

<0.25

<0.25

<0.25

<0.25

<0.25 <0.25 <0.25 <0.25 <0.25 <0.25

10-Year Treasury(percent)

3.30 3.54 3.71 3.49 2.80 3.37 3.47 3-4% 3-4% 3-4%

*Data represent quarterly averages

“I can calculate the motions of heavenly bodies, but not the madness of people.” – Sir Isaac Newton

Inflation still below Fed’s target

Unemployment will remain high

Fed keeps “foot on pedal”

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

100

200

300

400

500

600

700

1‐2% 2‐3% 3‐4% 4‐5% 5‐6% 6‐7% 7‐8% 8‐9% 9‐10% 10% or Higher

Cumulative %

Freq

uency (M

onths)

Interest Rate Buckets

Frequency (Left) Cumulative % (Right)

Source: Robert Shiller

44

Updated through Nov. 2010

Interest rates have been below 5% over 70% of the time since 1871!

High Interest Rates are the Anomaly, Not Low OnesNominal Long-Term Monthly Yields since 1871

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

4545

U.S. Interest Rate Scorecard

Factor Comment Explanatory Power Impact on Rates AssessmentFundamental Factors – Help to establish long-term fair value

GDP Growth Below long-term trend of 3% High

Economic and structural fundamentals point to

continued low yields. The most significant change in

last six months is the “bottoming” in the core

rate of inflation.

Inflation Rising from historic lows High

Foreign Central Banks Foreign central banks hold nearly 50% of marketable Treasury debt Medium

Federal Reserve policy Monetary policy stance (short-term rates) High

Bank Lending and Private Debt Issuance

Banks are buying Treasuries instead of making new loans

Medium

Technical Factors – Influence near-term volatilityMarket Sentiment Concern for higher rates High

Technical factors are mixed and do not suggest

immediate upward pressure on interest

rates.

Investor Safe-Haven Demand for Treasuries

High global demand for a safe-haven investment

Medium

Treasury Auctions

Federal Reserve Purchases (QE2)

Record funding requirements

$600 billion program over 8 mos. plus mortgage reinvestment

Medium

Medium

Conclusion: Yields on benchmark 10-year US Treasuries should fluctuate between 3% and 4% in 2011. As for the federal funds rate, we do not anticipate rate hikes in 2011. This implies a steep yield curve throughout the year.

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

46

The Risks to the Forecast“I can calculate the motions of heavenly bodies, but not the madness of people.” – Sir Isaac Newton

Oil Prices Shock

Fiscal/Regulatory Uncertainty

Global Growth Slowdown

QE3?

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

Biographies

Jeffrey C. ClevelandSenior Economist

2006 – Joined Payden & Rygel

Jeffrey Cleveland is a Senior Economist at Payden & Rygel. He isresponsible for developing views on the US and global economy. Hisresearch areas include macroeconomics, central banks and themoney markets, money supply, credit cycles, housing, state and localgovernments and regional economics.

Prior to joining Payden & Rygel, Cleveland was a senior associate atDavid Taussig & Associates in Newport Beach, California, where hemanaged the firm’s fiscal and economic impact studies andconsulting services. Cleveland worked with local agencies, includingcities, counties, and agencies to analyze the impact of economicdevelopment projects on municipal finance. He also assisted infinding municipal finance solutions to budget and service needs.

Cleveland is a member of the National Association for BusinessEconomics (NABE). He is also an avid open-water swimmer. Heswam across the English Channel in September 2008, across theCatalina Channel in 2009 and around Manhattan in 2010. This isconsidered the triple crown of open-water swimming, with only 35people having done this in history.

Jeffrey Cleveland earned a MA in International Political Economy withan emphasis in international money and finance from ClaremontGraduate University. He received a BA in Economics/Global PoliticalEconomy from Whittier College through the Whittier ScholarsProgram.

F:\GRAPHICS\Economics\USO\September 2010\USO September.ppt

Question & Answer Session

Thank you for joining us.To learn more about Payden & Rygel, visit payden.com.

Thank you for joining us.To learn more about Payden & Rygel, visit payden.com.

Jeffrey C. ClevelandSenior Economist