the assn.group™ plan member benefit program

TRANSCRIPT

The ASSN.Group™ Plan Member Benefit Program

Executive Overview

Association Planning Professional Services, LLC 224 Phillip Morris Drive, Suite 402

Salisbury, MD 21804 800-520-6685

www.assngroup.com

The ASSN.Group™ Plan Executive Overview 224 Phillip Morris Drive – Suite 402 – Salisbury, MD 21804 – 800-520-6685

www.assngroup.com

2

An Association Sponsored Member Benefit Program that

Creates Wealth and Minimizes Taxation

The ASSN. Group™ Plan (“the Plan”) is an association member benefit that allows association members to create personal wealth with pre-tax business dollars. The Plan uses an IRC Section 79 group term life insurance program that allows for the deduction by the business of the contributions that fund the insurance. The tax treatment of group life insurance plans is well established in the Internal Revenue Code, tax regulations, and tax cases. The Plan is offered exclusively by sponsoring trade associations. This allows for the Plan to provide some unique benefits to participating businesses. The business can be highly selective when determining the employees who will participate, it allows high funding levels if desired, and it creates an asset with substantial underlying value that can be outside of the reach of business and personal creditors. Benefits include:

Death benefits for business and personal planning The business can be very selective when determining the employees that will participate -

requires participation by as few as two employees Contributions qualify as a deductible business expense Favorable corporate and personal tax treatment Protection from business and personal creditors The ability to supplement employees’ retirement income with tax-free cash flow A unique business tool for use with key employees

An example of how the Plan creates wealth and provides favorable corporate, individual, and estate tax treatment: Mr. John Doe is a partner in Doe, Buck & Herd, P.A. He is 45 years old. He is married with three children. He maximizes his qualified retirement Plan contributions each year. He wants to provide additional benefits to himself and perhaps key employees, use additional pre-tax business income to fund retirement needs, and have payments qualify as a deductible business expense. He wants to create an asset that steadily accumulates value. He wants the asset to be in a creditor proof position. In addition, he needs to provide substantial death benefits to his survivors. Finally, he wants to provide the corporate benefits to only a few select employees but not allow the employees to have total control of the benefits created. The business can commit $100,000 per year to the program on John’s behalf.

The ASSN.Group™ Plan Executive Overview 224 Phillip Morris Drive – Suite 402 – Salisbury, MD 21804 – 800-520-6685

www.assngroup.com

3

The benefits to Mr. John Doe are …

John’s business deducts its contribution of $100,000 per year on John’s behalf.

Approximately 10% of the total contribution will be considered taxable income to John, personally. His out of pocket outlay is limited to his personal taxes on the amount of the personal income.

John’s wife and children are made more financially secure at John’s death.

Assuming retirement at age 67, John then has an asset with a current cash value of $2.1

million and a death benefit of $6.4 million.

John can receive tax-free distributions of $165,900 for 20 years via policy loans. This totals $3,318,000 tax-free. There still remains a death benefit of $3.1 million that is income tax free when paid to John’s beneficiary.

Q. Who benefits from this Plan? The Plan is appealing to business owners, professionals, and executives looking to satisfy a life insurance need and a need for additional income deferral. The Plan allows the insurance need to be addressed by using pre- tax business funds to make premium payments. The Plan provides greater tax efficiency. Perhaps the practice has already taken maximum advantage of a traditional qualified retirement Plan, or perhaps the business does not have a retirement Plan due to the size, census, or other factors related to their business. The Plan is also an ideal alternative to traditional approaches such as deferred compensation, split dollar, and Supplemental Executive Retirement Plans. Q. Can the member be selective in choosing participants in the Plan? Yes. The employer chooses the employees that will participate regardless of the employees’ income, position, or length of service with the business. A minimum of any two employees must participate. Q. How does this Plan help create personal wealth through the business? First, death benefits are provided income tax-free immediately that can satisfy business or personal needs. Contributions to the Plan are deductible to the business thus giving the business less taxable income. Cash values in the insurance accumulate with interest on a tax-deferred basis. Additionally, the asset is outside the reach of personal and corporate creditors. Q. Is the business limited in the amount of pre-tax funds it allocates to this benefit? There are no restrictions as to contribution levels except for what is prudent in relation to business cash flow, and what is considered reasonable compensation for the employee. The premiums are annually determined by independent actuaries. Contribution levels are not impacted by retirement plan contributions, or vice versa. Q. Are the funds I withdraw from a certificate after I leave the Plan tax-free? Yes, if taken in the form of a loan. The Plan uses life insurance with the death benefit as collateral to the extent of the borrowing or advances. Any remainder will be distributed to your beneficiary.

The ASSN.Group™ Plan Executive Overview 224 Phillip Morris Drive – Suite 402 – Salisbury, MD 21804 – 800-520-6685

www.assngroup.com

4

Q. Why is this Plan only available through my association? The Plan is offered only as a member benefit program that is only available through a trade association. Because of existing tax laws and regulations pertaining to associations, specifically group benefit plans, a business may choose to participate in the Plan only if it is a member of a “sponsoring” association. Contributions to the Plan are not deductible if association membership discontinues, i.e. the employer withdraws from the association membership. Q. What tax principals apply to this benefit Plan? The Plan is structured as an IRC Section 79 group life program that is based on long-standing tax, legal, accounting, and actuarial positions and precedents. The Plan has secured independent actuarial valuations and has been reviewed by numerous accounting and legal professionals who view the Plan as a sound, unique planning tool. The IRS recently issued a favorable Technical Advice Memorandum in a case that used an insurance funding structure very similar to the Plan. Q. Am I protected in the event of an unfavorable IRS ruling? While the Plan is prudently structured in its unique design, and has been reviewed by the IRS in an audit of an employer contributor for tax year 2003, the Plan Administrator will be provide technical assistance, at no charge, during any IRS challenge. Finally, it is important to note that the Plan investments are exclusively life insurance policies issued by Jefferson Pilot and other large, financially-sound, national insurance carriers. These are substantive and stable investments regardless of the tax deductions provided by the Plan. Q. Sum up for me, why I should become involved? If the business owner and/or key employees have a need for life insurance with a secure and substantial death benefit beginning in the first year, the Plan provides a tax efficient way to provide the necessary insurance and benefits. If employees are looking for additional benefits and the company is looking for additional deductions, the Plan is a viable option. If another source of benefits is desired, the Plan can provide additional benefits. If creation of an asset that can be protected from business and personal creditors is important, the Plan provides a solution. The ASSN.Group™ Plan employs an actuarial approach to the acquisition and funding of life insurance. Actual results will vary for each employee depending on many factors including, but not limited to age, health considerations, contribution levels, and the timing of any withdrawals. Businesses and employees should not rely solely on the tax considerations and positions used by the Plan, but should consult with their independent tax, accounting, and financial advisors regarding participation in the Plan and the effects of the Plan.

Advisors LLC, P.O. Box 143, Kensington, MD 20895-0143 240-604-6945 · Fax: 301-656-1821

ASSNGroup Professional Advisors 2007 Frequently Asked Questions

1. Is the Program considered a “listed transaction” under Treas. Regs. § § 1.6011-4(b)(2) and 301.6111-2(b)(2), a “tax shelter” under IRC §§ 6111(c) and 6111(d) and Treas. Reg. § 301.6111-1T, Q&A 4, a “potentially abusive tax shelter” under IRC § 6112(b) and Treas. Reg. § 301.6112-1(b), or a “reportable transaction” under Treas. Reg. § 1.6011-4(b)?

NO, Based on a review of the above-referenced IRC and Treasury Regulation provisions (the “Tax Shelter Provisions”), the Program does not fall within the definition of a “listed transaction,” a “tax shelter,” "a potentially abusive tax shelter,” or a “reportable transaction” as defined therein. Furthermore, the Program is not considered to be “substantially similar to” a “listed transaction,” a “tax shelter,” a “potentially abusive tax shelter,” or a “reportable transaction” as defined in the applicable sections of the IRC and Treasury Regulations. (See Tax Memo p.29-31)

2. Does (a) the design of the Program would meet the standards of “group-term life

insurance” under IRC § 79, and (b) if so, are participants solely taxed at the Table I rate on the economic benefit of the death benefit provided by the Program?

(a) YES, the Program complies with the § 79 rules, and the Participants are taxed only on the Table I costs for the Program. IRC § 79 and accompanying regulations set forth four criteria life insurance plans must meet in order to be considered “group-term life insurance:”

(1) The plan must provide a general death benefit excludable from gross income under IRC § 101(a).

(2) The plan must be provided to a group of employees as compensation for personal services performed.

(3) The insurance must be provided under a policy carried directly or indirectly by the employer.

(4) The amount of insurance provided each employee must be computed under a formula that precludes individual selection of such amounts. The formula must be based on factors such as age, years of service, compensation or position.

Treas. Reg.§1.79-1(a). The Program complies with all four criteria

Beyond these four requirements, IRC § 79 also requires that life insurance be provided to at least 10 employees at some point during the calendar year. Id. at §1.79-1(c)(1). However, two exceptions exist to the ten employee rule. The Program will be considered group-term life

Advisors LLC, P.O. Box 143, Kensington, MD 20895-0143 240-604-6945 · Fax: 301-656-1821

insurance even though it covers fewer than 10 employees, if either of the following two exceptions are met. Id. at §§1.79-1(c)(2) and (3).

3

The 10-employee rule does not apply, under Treas. Reg. § 1.79-1(c)(2), if:

(1) the life insurance is provided to all full-time employees of the employer;

(2) the amount of insurance provided is computed as either a uniform percentage of compensation or on the basis of coverage brackets established by the insurer. No bracket may exceed 2.5 times the next lower bracket and the lowest bracket must be at least 10% of the highest bracket; and

(3) evidence of insurability is required but is limited to a questionnaire completed by the employee.

Additionally where the Program is integrated with an existing Group coverage TAM 2000274 permits the use of an executive carve out approach. This permits to compliance also with the discrimination rules of Sec. 79(d) where the cumulative death benefit of the HCE’s do not exceed the cumulative death benefit of the rank and file. See Tax Memo p.8-11

If evidence of insurability does not affect an employee’s eligibility, under Treas. Reg. § 1.79-1(c)(3), the 10-employee rule will still not exclude qualification as group-term life insurance if:

(1) it is provided under a common plan to the employees of two or more unrelated employers; and

(2) insurance is restricted to, but mandatory for, all employees of an employer who belong to or are represented by a particular organization that carries on substantial activities other than obtaining insurance

With regard to the first of the four basic requirements, IRC § 101(a) excludes from gross income the amounts payable under a life insurance contract “by reason of the death of the insured,” and under IRC § 101(g), amounts received by a living but terminally or chronically ill insured are deemed paid by reason of the death.

With regard to the second requirement the Program provides a death benefit to employees as compensation for personal services – as opposed, for example, to payments for earnings on stock or payments for property, or other impermissible purposes. Treas. Reg. §§ 1.162-7(b)(1).

With regard to the third requirement, a policy meets this requirement if the employer pays any part of the cost (directly or through another person). The policy may be a master policy or a group of individual policies. The term “policy” includes all obligations of an insurer that are offered or are available to a group of employees because of the employment relationship, even if they are in separate documents. Treas. Reg. § 1.79-0. The Insurer provides master policy and certificates to the members.

With regard to the fourth requirement the Program provides benefits in dollar amounts as specified in the Employer Administrative Agreement. The Program “precludes individual selection of the benefit amount” and is based on factors such as age, years of service, compensation or position, this part of the test should be satisfied.

4

With regard to the ten employee rule under the regulations the Program may or may not cover at least ten employees of an employer. If it does not cover at least ten employees, it is important to consider whether the Program fits the “common plan” exception under Treas. Reg. § 1.79-1(c)(1) and single plan rules of ERISA (see below). A common plan – which is defined as a common plan to two or more unrelated employers – may be exempt from the ten-employee requirement, provided the other conditions are met (i.e., mandatory availability to members, no differentiation on insurability). Though there is no specific guidance from the Service on “common plans,” there is nothing in the Program as not describing a common plan providing benefits to two or more unrelated employers. The Program complies, Additionally, TAM 200002074 confirmed the ability to use a Group Carve out Plan and the taxation to the employees to be effective under Sec. 79 and Table I. The Program also complies with the eligibility and benefits discrimination rules under IRC §§ 79(d)(3) and (4)

(b) YES, Table I is the uniform premium table prescribed by the Treasury to calculate premium cost allocated to employees. IRC § 79(c); Treas. Reg. § 1.79-3(d)(2). If an employee's death benefit under group-term life insurance coverage exceeds $50,000, the premium cost of the excess is gross income to the employee. Treas. Reg. § 1.79-3(d)(3). The Table sets forth the cost of $1,000 of group-term life insurance provided for one month, computed on the basis of 5-year age brackets.

On January 14, 2005, the IRS released Technical Advise Memorandum 200502040, TAM 144621-03, which confirms and supports the Program. The Service determined that a structure identical to the Program that provided the Group Term Life component was not taxable to the employee. Under the Facts, the employee applied for and made after tax payments for the Supplemental Funding. This is how the Program is designed. Under the TAM, a contract is split into two pieces and each piece qualifies as life insurance. This arrangement qualified even when the insurance carrier filed the Group Universal policy with the State Regulatory Agency as a “single integrated permanent insurance policy” [p.3, lines 7-9]. In further support on September 21,2006 the IRS issued LTR200652043 which supports the co-ownership approach. On January 4,2007 Steve Leimberg’s Estate Planning Newsletter#1072 reported the approach as one life Policy Split into Two not a Taxable Sale or Exchange. Also see IRS Letter Ruling 200704017 supporting a partnership providing a self funded group plan to employees and the contributions are deductible by the partnership are deductible under 162(l) and not included in partners income . The Program provides insurance benefits in dollar amounts designated by an Employer Administrative Agreement. Where the Program qualifies as “group-term life insurance,” as stated above, and the death benefit provided under the policy exceeds $50,000, the members should be taxed at the Table I rate. The Program complies – see Treas. Reg. § 1.61-2(d)(2)(ii)(A) Cost of Life Insurance.

3. Is the Program a “split dollar arrangement” as that term is defined in Treas. Reg. § 1.61-22(b)?

NO, the Program is not a Split Dollar arrangement. Treas. Reg. § 1.61-22(b) defines “split dollar arrangement” for purposes of tax treatment under the IRC as any arrangement between a life insurance contract “owner” and a “non-owner” under which:

5

(1) either party to the arrangement pays, directly or indirectly, all or any portion of the premiums on the life insurance contract, including a payment by means of a loan to the other party that is secured by the life insurance contract; and

(2) at least one of the parties to the arrangement paying premiums is entitled to recover, either conditionally or unconditionally, all or any portion of those premiums, and the recovery is to be made from, or is secured by, the proceeds of the life insurance contract (emphasis added)

The Program does not permit recovery of premium so the Split Dollar regulations do not

apply. Additionally, the regulations do not apply. That is because Treas. Reg. § 1.61-22 excludes from the definition of split dollar arrangement any arrangement that is part of an IRC § 79 group-term life insurance plan. The only relevant limitation is that an IRC § 79 plan would not be excluded from the definition of split-dollar arrangement if it provided “permanent” benefits. No permanent benefit is provided by the Program .Treas. Reg. §1.79-0. Treas. Reg. § 1.61-22(b)(1)(iii). A “permanent benefit” is an economic value provided under a life insurance policy which extends beyond one policy year. The actuary’s certifications indicate the funding of the Program does not provide a benefit extending beyond one year. Additionally if the Service were to deem a “conversion” occurred, the Regulations specifically excludes: a right to convert (or continue) life insurance after group coverage terminates; any other feature that provides no economic benefit to the employee; or a feature under which term life insurance is provided at a level premium for a period of five years or less. Treas. Reg. § 1.79-0 (emphasis added). Coverage under the Program ends effective as of the next anniversary date of the policy. The day after the termination of coverage, the assignment of rights in the policy is released. Upon release and continued payment of the full premium by the owner of the policy directly to the insurance company, coverage may continue. If this were to be considered a conversion it would not be a permanent benefit, and therefore the Program qualified under IRC § 79 plan, the Program should not be considered a “split-dollar arrangement.” 4. Whether the Program creates the possibility of a Prohibited Transaction under IRC

§ 4975(e)?

NO, the Program is not a Prohibited Transaction. IRC § 4975 imposes a tax on prohibited transactions between “plans” and disqualified persons. For this purpose, the IRC defines “plan” as 403(a) plans or 401(a) trusts which are exempt from tax under 501(a), individual retirement accounts, Archer medical savings accounts, health savings accounts, and a trust, plan, account or annuity which has been determined to be one of the preceding by the Secretary of the Treasury. The Program provides only a death benefit to covered individuals. The Program is not a 403(a) plan, a 401(a) trust or one of the types of savings accounts described in IRC § 4975(e). The Program is not a Prohibited Transaction. 5. Is the Program required to comply under IRC § 419A as a welfare benefit fund?

NO, the Program is not required to comply with IRC §§ 419 or 419A. IRC §§ 419 and 419A place limitations on the deductibility of amounts contributed by employers to a “welfare benefit fund” (including, in some cases, reserve requirements).

6

A “welfare benefit fund” is any fund which is part of a plan or arrangement of an employer through which welfare benefits are provided to employees or their beneficiaries. Treas. Reg. § 1.419-IT, Q&A 3. An employee benefit is a “welfare benefit” unless deductions for employer contributions for the benefit are governed by IRC § 83(h) (transfers of restricted property), IRC § 404 (qualified pension, profit sharing, and stock bonus plans and other deferred compensation arrangements), or IRC § 404A (foreign deferred compensation plans). IRC § 419(e)(2).

IRC § 419(e)(3)(A) – (C). The first five possibilities do not seem relevant to the Program, but we should consider whether the Program could be an “account held for an employer by any person.” The regulations spell out the test and the Program passes the test. Under Treas. Reg. § 1.419-1T Q&A3, any of the accounts described below, as only the accounts described below, are accounts held for an employer under IRC § 419(e)(3)(C):

(1) a retired lives reserve or premium stabilization reserve maintained by an insurance company for a particular employer;

(2) payments from an employer to an insurance company under an “administrative

services only” arrangement with respect to a separate account the insurance company maintains for the employer for the purpose of providing benefits; and

(3) an insurance or premium arrangement between an employer and an insurance

company if the employer has any right to refund, credit, or additional benefits based on the benefit, claims, administrative expense or investment experience attributable to such employer.

The Program would not be considered a welfare benefit fund under IRC § 419A and would, therefore, not be subject to the deduction limitation. Additionally, based upon the actuaries certificates, the accounts would comply with the Safe Harbor of IRC § 419A(c)(2)(1) and the Program would satisfy the funding requirements of IRC § 419A if the Program were instead to be considered a welfare benefit fund for purposes of IRC § 419 and 419A. 6. Does the Program constitute a “pension plan” as described in Rev. Rul. 81-162?

NO, Revenue Ruling 81-162 was issued to clarify whether a plan providing benefits through the purchase of ordinary life insurance contracts, which may be converted to annuity payments upon retirement, constitutes a pension plan. The tax regulations provide that a pension plan is a plan established and maintained primarily to provide for payments to employees over a period of years, usually for life. A pension plan may also provide for the payment of incidental death benefits through insurance or otherwise. IRC § 401(a); Treas. Reg. § 1.401-1(b)(1)(i).

Revenue Ruling 81-162 clarified whether a plan created for the purchase of ordinary life insurance contracts and not primarily for the payment of benefits to employees over a period of years with only an “incidental” life insurance benefit was a pension plan. The life insurance benefits were the primary purpose of the plan, not merely an “incidental benefit” under IRC § 401(a). The fact that the insurance contracts could later be converted to a life annuity did not make the plan a pension plan.

7

The Program was developed for the primary purpose of providing death benefits through life insurance. As long as it does not provide life insurance benefits that are merely “incidental” to a retirement benefit over a period of years, it is not considered a pension plan.

7. Is the Program a “nonqualified deferred compensation plan” as described in IRCode Sec. 409A?

NO, the Program is not deferred compensation. New IR Code Sec. 409A defines a nonqualified deferred compensation plan as any plan that provides for the deferral of compensation other than a qualified employer plan or any bona fide vacation leave, sick leave, compensatory time, disability pay, or death benefit plan. The IRS provided the definition of “death benefit plan” on December 21, 2004 with the issuance of Notice 2005-1. The Program complies with the definition as set forth in Treas. Reg. 1.31.3121(v)(2)-1(b)(4)(iv)(C).

The Program was developed for the primary purpose of providing death benefits through life insurance. The new rules targets certain nonqualified deferred compensation plans and specifically excludes death benefit plans from further compliance requirements.

8. Does IRC § 264(a) prevents the deduction of premiums paid by a participating employer in the Program?

NO, IRC § 264 does not limit the deduction under the Program. IRC § 264(a) prevents employers from becoming beneficiaries of insurance policies on their employees’ lives. Employers may not deduct premiums as business expenses where the employer may be directly or indirectly treated as a beneficiary under the policy. An employer is treated as beneficiary of the policy if it can borrow on the policy, surrender the policy for its cash value, or use the cash value of the policy as collateral for a loan. In addition, the employer will be treated as a beneficiary if it is a named beneficiary under the policy or if a creditor of the employer is a beneficiary under the policy. Treas. Reg.§ 1.264-1(b). Thus, an employer may not deduct premiums if it retains the right to receive either a return on the cash value of the policy or a return of its premium payments. Rev. Rul. 70-148. Similarly, a corporation may not deduct premiums paid under an employee's insurance contract that requires assignment of the policies to the employer and grants the employer the exclusive right to surrender the policies and receive cash surrender values. Treas. Reg.§ 1.264-1(b).

The Program does not allow the participating employers to benefit directly or indirectly as beneficiaries of policies that are funded by the Program. Neither the employer nor any of its creditors may be a named beneficiary, or may access or borrow against the value of the policy. Where the Program operates exclusively through a third-party (i.e., Advisors), the deduction to participating employers should not be compromised.

9. Are employer contributions to the Program, currently deductible by the employer, subject only to limitations on reasonable compensation?

YES, the contributions are currently deductible. IRC § 162(a) (1) allows a deduction for ordinary and necessary business expenses including “a reasonable allowance for salaries or other compensation for personal services actually rendered.” Specifically, amounts paid for sickness, accident, welfare, medical and similar benefits are deductible under Section 162(a)(1). Treas Reg.§1.162-10(a). (No deduction would be allowed, however, if under any circumstances, the

8

amounts may be used to provide benefits under certain deferred compensation plans. Id.) The test is whether the amounts are reasonable and are, in fact, payment for services. Treas.Reg. §1.162-7(a).

Where the actuarially determined contributions are equal to the cost of the current death benefit protection provided under the Program, there are no factors that should question whether compensation would be reasonable. Where these benefits would be provided to employees of participating employers as compensation for services – rather than, for example, as stock dividends or payment for property.

10. Does the Program meet the requirements of a “group insurance arrangement” within the meaning of Labor Reg. § 2520.104-21?

YES, the Program qualifies as a group insurance arrangement. Labor Reg. § 2520.104-21 exempts certain welfare benefit plans from reporting and disclosure requirements under ERISA. Specifically, the administrator of group insurance arrangements which cover fewer than 100 participants at the beginning of the plan year and which meet certain requirements do not have to file a terminal report regarding the plan. Labor Reg. § 2520.104-21(a). The group insurance arrangement must:

1. provide benefits to two or more unaffiliated employers, but not in connection with a multi-employer plan;

2. fully insure one or more welfare plans of each participating employer through insurance contracts purchased solely by the employer or partly by the employer and partly by the employee, with all benefit payments made by the insurance company (under certain conditions); and

9 Revised 1/27/05

3. use a trust (or other entity such as a trade association) as the holder of the insurance contracts and uses a trust for payment of the premiums to the insurance company.

Labor Reg. § 2520.104-21(a).

The first requirement is satisfied by providing benefits to two ore more unaffiliated employers. The Program should be considered a multi-employer plan. (See #2, above) A multi-employer plan is a plan maintained under one or more collective bargaining agreements between one or more employee organizations and more than one employer, to which more than one employer is required to contribute. IRC § 414(f)(1); ERISA § 3(37). The Program is not created pursuant to a collective bargaining agreement. The Program is not an “employee organization” as that term is defined by ERISA. An “employee organization” is an organization in which employees participate that exists to deal with employers concerning employee benefit plans or other matters incidental to the employment relationship. ERISA§3(4). The Program exists for the sole purpose of providing death benefits to the employees of participating employers. The Program is not an organization in which employees participate to deal with employers.

The Program satisfies the second requirement by insuring a group insurance benefit for each participating employer through insurance contracts purchased solely by the employer. All benefit payments will be made directly by the insurance company to the employees. The Program appears to meet the third requirement of the regulation. Out of prudence the Administrator is complying with the ERISA rules of Reporting and Disclosure. Pursuant to Notice 90-24 and 2002-24, an IRS Form 5500 is not required to be filed. A Summary Plan Description is provided to the Employer but is not required to be filed with DOL.

11. Is the Program considered a Multiple Employer Welfare Arrangement (“MEWA”) under ERISA?

NO, the Program has no MEWA compliance issues. Under ERISA § 3(40)(A), a MEWA is an employee welfare benefit plan or other arrangement established or maintained to offer or provide any benefit of the type provided by ERISA welfare benefit plans – which includes death benefits under ERISA § 3(1) – to employees or beneficiaries of two or more employers, including one or more self-employed individuals. The definition specifically excludes arrangements established or maintained pursuant to a collective bargaining agreement or by rural electric cooperatives or rural cooperating telephone associations. Also, for purposes of determining whether an arrangement covers multiple employers, or only one, a group of trades or businesses will be deemed to be a single employer if they are under “common control” as defined in IRC § 414(c) and Treas. Reg. § 1.44(1). The Program will qualify as a Single Plan. ( DOL Advisory Opinion 83-22A and 2003-17A, EBIA’s ERISA Compliance Manual Sec. XIX.D.)

12. Is the Program in compliance with The COLI Best Practices and the 2006 Tax Law changes?

YES. Because of the use of the co-ownership arrangement the provisions of the COLI Best Practices are followed. The participant having the right to name a beneficiary during employment is a safe harbor for compliance purposes. This approach can also be wrapped around an existing COLI program to provide compliance on a tax deductible basis.

10 Revised 1/27/05

13. Is the Plan in compliance with the guidelines of New Tax Circular 230?

YES. On December 20, 2004, Treasury and the IRS issued Circular 230 regulations (T.D.9165) addressing opinion standards for tax professionals who provide advice on federal tax issues or submissions to the IRS. The Plan is not a “tax shelter “ or a potentially abusive tax shelter as defined in IRC 6011, 6111 or 6112. It is not a listed transaction and the Plan’s principal purpose or significant purpose is not the avoidance or evasion of any tax, the Plan is not subject to any confidentiality agreement or subject to any contractual protection. The Plan does not fall into any one of the five (5) prohibited areas (see Q&A#1), See Tax Memo p29-32.

January 2005○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

The AssnR Group News

Technical Advise Memorandum (TAM) 200502040,January 14, 2005 Supports the Program!

Program to avoid the possibility of constructive receipt ofthe inside buildup of the contract.7. Employees in the Group Universal program were issueda certificate from the Insurance Carrier describing benefitsand stating the benefits were subject to the terms andconditions of the Group Policy.[p.3 l.4-5]8. According to the Insurance Carrier the policy includingthe Supplemental Fund was filed with the state insuranceregulators as a single life insurance product. The cashvalue features of the insurance contract was referred toas the Fund [p.3 l.7-11].

THE LAW - Group Universal Program

9. The legislative history of section 79 of the Code statesthat the cost of group-term life insurance protection abovethe exclusion level is to be taxed to an employee “if it isprovided under a plan arranged for by the employer wherethe protection the employee receives (over and above thatprovided by his own contributions) is provided directly bythe employer, or indirectly by the employer’s chargingmore than the cost of the insurance to other employees(such as those in younger age brackets) and less to thosein the older age brackets, such as the specific employeein question” S.Rep. No. 830, 88th Cong., 2d Sess. 1(1964), 1964-1 (Part 2) C.B. 502, 550 [p.6 l 21-28].10. Section 83 of the Code provides rules governing thetaxation of property transferred in connection with theperformance of services. Generally upon the transfer ofsubstantially vested property to a service provider, theservice provider must recognize income under section83(a) in amount equal to the excess of the fair marketvalue of the property over the amount the service providerpaid for the property. Section 1.83-3(e) defines propertyin the case of a transfer of life insurance contract or othercontract providing life insurance protection as only thecash surrender value of the contract. Section 83(e) (5) ofthe Code provides that section 83 does not apply to group-term life insurance to which section 79 applies [p.2 l.29 -p.3 l.2].11. The IRS determined the Group Universal life insurancecan be tested as a separate policy for determining whether

Technical Advise Memorandum 200502040 (the TAM)issued on January 14,2005 confirms the structure of theASSN GroupR (The Program). The ability to separate agroup certificate into two separate contracts for taxpurposes and have both contracts qualify as life insuranceunder Sec. 7702(a) assures the benefit structure andcompliance standards. This is the result even when theInsurance Carrier has filed the contract with the State’sInsurance Regulatory Agency as “a single integratedpermanent insurance policy” [p.3 l. 7-9].

The TAM fact pattern has many similarities and the pointsof law that are relied upon by the IRS supports the non-taxation of the transaction for the Program.

FACTS:

1. The Employer (Taxpayer) offered to employees a groupterm life program [p.2 l.2].2. Each employee paid a portion of the cost [p.2 l.7-9].3. The eligible employees apply to the Administrator (notthe insurance carrier) to be covered by a group term lifeprogram [p.2 l.14]. The Taxpayer directs payment to theAdministrator.4. The premium charged for the group universal lifeinsurance were based on $1,000’s of coverage and wasage related. Rates charged to the employees for thecoverage could be changed annually to reflect theexperience of the group [p.2 l.26-30].5. An employee enrolled in the group universal programalso would have Taxpayer contribute payments to thegroup universal life fund (Supplemental Fund) [p.2 l.33].6. Amounts contributed to the Supplemental Fund werededucted by the Taxpayer and were deemed after taxcontributions by the employee. Amounts contributed tothe Supplemental Fund earned income. Those amountswere available for loans to the employees. At death anybalance of the Supplemental Fund was payable to theemployee’s named beneficiary [p.2 l.34-39].The Program takes a more cautious and prudent approachand does not permit an employee to access the cash inthe Supplemental Fund while they are a part of the

Assn.TM Group News

Advisors, LLCP.O. Box 143

Kensington, MD 20895-0143Phone: (240) 604-6945 . Fax: (301) 656-1821

the insurance qualifies as group-term life insurance forSection 79 [p.7 l.36-38].12. The IRS determined the regulations and statue do notrequire the employee to include amounts in income forpermanent benefits where the Taxpayer is not financingportions of the permanent benefits [p.8 l. 25-32].13. The Supplemental Fund is treated as a separate policy[p. 8 Is 14-17, 33-34].14. The amounts charged to permanent benefits providedunder the policy does not reduce the amounts includiblein income under the other policy [p. 8, fn. 2].15. Section 83 does not apply because there was notransfer of appreciated property. Under Section 83(e), whereSection 79 applies, then Section 83 does not apply.Accordingly, even if Section 83 were applicable, therewould be no income recognition under Section 83 [p. 91.14-11].16. The Group Universal Life Program being offered doesnot create any additional employee income under Section61 [p. 9 1.11-13].

Based on the facts in the TAM, which follow our Program,and the interpretation of the Law, the IRS concluded theGroup Universal Life Insurance Program does not createtaxable distributions to the covered employees [p. 1 1.5-7].

ASSN.Group Plan 5 page Explanation 224 Phillip Morris Drive—Suite 402—Salisbury, MD 21804 1

The Standard Treatment of a Sec. 79 Group Life Insurance Plan

Employer

Insurance

Carrier

Employee 1099 income addition for the cost of insurance death benefits above $50,000

Deductible Contribution

• The employer funds group life insurance for the em-ployees.

• The employer deducts the full amount.

• The insurance carrier provides group life coverage.

• The employee realizes income only if the insurance death benefit exceeds $50,000.

ASSN.Group Plan 5 page Explanation 224 Phillip Morris Drive—Suite 402—Salisbury, MD 21804 2

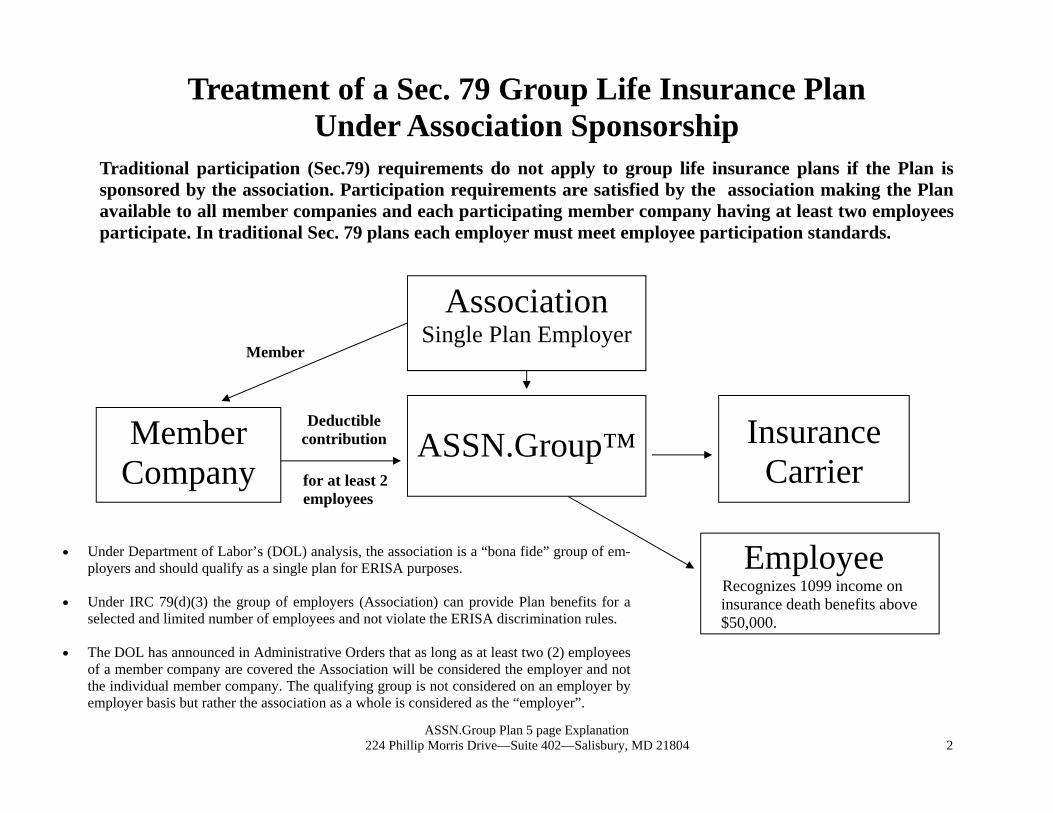

Treatment of a Sec. 79 Group Life Insurance Plan Under Association Sponsorship

Traditional participation (Sec.79) requirements do not apply to group life insurance plans if the Plan is sponsored by the association. Participation requirements are satisfied by the association making the Plan available to all member companies and each participating member company having at least two employees participate. In traditional Sec. 79 plans each employer must meet employee participation standards.

Employee Recognizes 1099 income on insurance death benefits above $50,000.

Insurance Carrier

Member

Deductible contribution Member

Company

Association Single Plan Employer

ASSN.Group™

• Under Department of Labor’s (DOL) analysis, the association is a “bona fide” group of em-ployers and should qualify as a single plan for ERISA purposes.

• Under IRC 79(d)(3) the group of employers (Association) can provide Plan benefits for a

selected and limited number of employees and not violate the ERISA discrimination rules. • The DOL has announced in Administrative Orders that as long as at least two (2) employees

of a member company are covered the Association will be considered the employer and not the individual member company. The qualifying group is not considered on an employer by employer basis but rather the association as a whole is considered as the “employer”.

for at least 2 employees

ASSN.Group Plan 5 page Explanation 224 Phillip Morris Drive—Suite 402—Salisbury, MD 21804 3

The amount of the deduction is determined by annual actuarial calcula-tions that provide a stable funding approach over the working life of the employee.

Deductible Premium Payment Minimal Annual Variance

Age 67 $43.51/1,000

Age 35 $1/1,000

ASSN.Group™

Employee Income Addition

$1/1,000 Over $50,000

Employer

Deduction

• Age 35 premium rates are very low (i.e. $1 for each $1,000 of life in-surance coverage).

• Premiums will increase steadily until age 67 (i.e. $43.51 per $1,000 of coverage).

• Employer contributes using a stable funding amount (i.e. $20/1,000) This approach was reviewed and accepted in the Wells Fargo case.

ASSN.Group Plan 5 page Explanation 224 Phillip Morris Drive—Suite 402—Salisbury, MD 21804 4

It is anticipated that 85-90% of the aggregate premium will be deductible by the employer without attribution to employee. The remaining amount is at-tributed to the employee as income.

Association

Employer

Employee Co-Owner

ASSN.Group™ Co-Owner

Group Universal Life

Certificate

Income Addition for Employee

1099 for amount over $50k in insurance

death benefits

• Approximately 10% of total premium will be considered as

income to employee.

• The insurance used is a Sec. 79 Group Life plan.

• The insured and ASSN.Group™ have a co-ownership agreement.

• ASSN.Group™ has an interest solely in death benefits.

Member

100% Payment

90% Deduction

Table I Cost

10% in Income

ASSN.Group Plan 5 page Explanation 224 Phillip Morris Drive—Suite 402—Salisbury, MD 21804 5

At termination of employment, termination of participa-tion by employer in the Plan, or termination of the Plan... • Co-ownership agreement lapses and employee is the sole

owner. • Surrender of the certificate will result in a taxable event and

income taxation to the employee according to then existing tax rules.

• If employee keeps the certificate “in force”, there is no sur-

render and no current income tax ramifications to the em-ployee.

The ASSN.Group™ Plan

Presented by Association Professional Planning Services, LLC

September 2007

ASSN.Group Plan - 224 Phillip Morris Drive - Suite 402 -Salisbury, MD 21804 - 800-520-6685 - www.assngroup.com 2

Create WealthMinimize Taxation

The ASSN.Group™ Plan is an association member benefit program that creates personal wealth for a select group of employees using pre-tax business dollars.

The ASSN.Group™ Plan is an IRC Section 79 life insurance program offered exclusively in conjunction with sponsoring associations.

ASSN.Group Plan - 224 Phillip Morris Drive - Suite 402 -Salisbury, MD 21804 - 800-520-6685 - www.assngroup.com 3

Exclusive Member Benefit Program

Only members of a sponsoring, tax-exempt trade association qualify for participation in the ASSN.Group™ Plan.

Benefits to the association include:RecruitmentRetentionNon-dues revenue

ASSN.Group Plan - 224 Phillip Morris Drive - Suite 402 -Salisbury, MD 21804 - 800-520-6685 - www.assngroup.com 4

Strategic Business Issues

Successful business owners face some or all of these issues:

Asset Protection Key Person Recruitment and RetentionSuccession Planning/Business ContinuityTax Planning

ASSN.Group Plan - 224 Phillip Morris Drive - Suite 402 -Salisbury, MD 21804 - 800-520-6685 - www.assngroup.com 5

A Unique Corporate Benefit Plan

Highly selective, as few as two employees

Contributions are deductible by the business

Assets grow on a tax deferred basis and are secure from creditors

Death benefits to satisfy a variety of business and personal objectives

ASSN.Group Plan - 224 Phillip Morris Drive - Suite 402 -Salisbury, MD 21804 - 800-520-6685 - www.assngroup.com 6

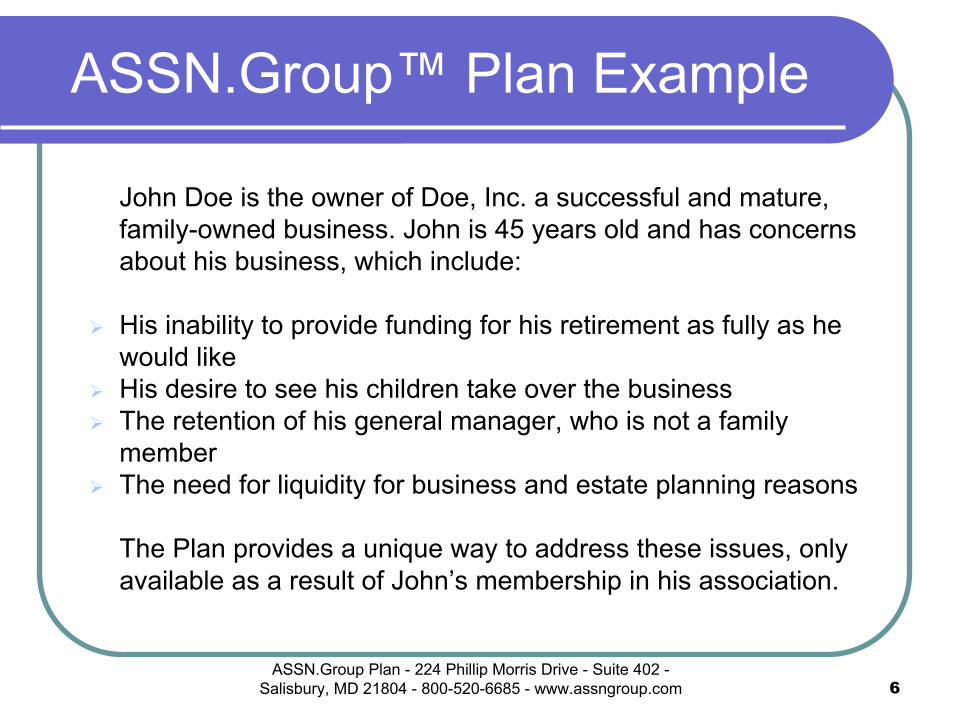

ASSN.Group™ Plan Example

John Doe is the owner of Doe, Inc. a successful and mature, family-owned business. John is 45 years old and has concerns about his business, which include:

His inability to provide funding for his retirement as fully as he would likeHis desire to see his children take over the businessThe retention of his general manager, who is not a family memberThe need for liquidity for business and estate planning reasons

The Plan provides a unique way to address these issues, only available as a result of John’s membership in his association.

ASSN.Group Plan - 224 Phillip Morris Drive - Suite 402 -Salisbury, MD 21804 - 800-520-6685 - www.assngroup.com 7

How Does The Plan Affect John & His Business?

Each year, John’s company, Doe, Inc. deducts its payment for the selected participants

Approximately 10% of the total payment will be considered taxable income to the participants

John may make a payment for his general manager, yet control theemployee’s access with an employment contract

The death benefits needed for his business and family can now befunded through the Plan with funds deducted by the business

Assets may be secure from business and personal creditors

ASSN.Group Plan - 224 Phillip Morris Drive - Suite 402 -Salisbury, MD 21804 - 800-520-6685 - www.assngroup.com 8

Program Support & Infrastructure

How are the Association, its Board, and its Membership protected under the ASSN.Group™ Plan?

ASSN.Group Plan - 224 Phillip Morris Drive - Suite 402 -Salisbury, MD 21804 - 800-520-6685 - www.assngroup.com 9

Program Support & Infrastructure

Association sponsors – not endorses Hold harmless provisionsAdvisor interaction requiredNon-exclusive sales producersSales trainingHigh cash value policyExperienced professionals

ASSN.Group Plan - 224 Phillip Morris Drive - Suite 402 -Salisbury, MD 21804 - 800-520-6685 - www.assngroup.com 10

Professional Team

Association Professional Planning Services, LLC (APPS)(Plan Adminstration & Distribution)

Walter Moore, MBA - PresidentMichael Payne, J.D., LLM – Exec Vice Pres & Corp CounselStephen Smith, CSA – Senior Vice PresidentKathy Kiernan, MBA – Vice President

Advisors, LLC – (Plan Technical Matters)Lawrence Bell, J.D., LLM

Bakos Enterprises and Insurance Strategies Consultants(Independent Actuaries)

ASSN.Group Plan - 224 Phillip Morris Drive - Suite 402 -Salisbury, MD 21804 - 800-520-6685 - www.assngroup.com 11

Disclaimer

If this advice is or is intended to be used or referred to in promoting, marketing or recommending this Plan, the regulations under IRC Circular 230 require that we advise you of the following:

1. This writing is not intended or written to be used, and it cannot be used, for the purpose of avoiding tax penalties that may be imposed on a taxpayer;

2. The advice is written to support the promotion or marketing of the transaction(s) or matter(s) addressed by the written advice; and

3. The taxpayer should seek advice based on the taxpayer's particular circumstances from an independent tax advisor.

May 2004

Assn.TM Group News

Buy-Sell Arrangement as a Business Planning Toolwith the Assn.TM Group Plan

With the level of wealth attained by some business ownerstoday, it is often extremely difficult to help meet the variousfinancial goals they may have in one business successionplan. In addition to estate and gift tax laws and limits placedon a succession plan by income, the financial representativehas to grapple with connecting the business succession planto the owner’s retirement plan, as well as the owner’s overallestate plan. This is no easy task, especially when you considerthe competing interests between each plan category. From aretirement plan standpoint, it makes sense to have anexecutive own their policy so that they can access the cashinside the policy. However, viewing this from an estate planand income tax standpoint (executive may be income taxedon premium payments), the plan quickly loses its luster.

The two basic buy-sell agreements, the cross purchase andthe entity purchase agreement, come up short in many ways.Assuming cash value life insurance is used to fund a crosspurchase agreement, typically the policy is owned by theother business owners, either directly (cross purchase) or inan escrow account (trusteed cross purchase). This willnormally avoid estate inclusion of the policy in the insured’sestate with proper planning, but the insured does not haveaccess to the policy cash value. If the shareholders “swap”policies at retirement, the difference between what shareholder“A” paid into shareholder “B’s” policy (the premium basis)and what the cash value is in “A’s” policy, would have to berecognized by “A” as ordinary income (and vice versa). Thereis no easy way to deal with this issue.

Assuming life insurance is used as the funding mechanism,an ideal buy-sell plan would:1) Provide sufficient funds to the buyer of the business

interest upon the death, withdrawal or retirement of thebusiness owner to enable the buyer to purchase theinterest

2) Require the same number of policies as there are owners

3) Provide a step-up in basis for the surviving owners4) Allow the insured tax- free access to the cash value at

retirement5) Avoid Alternative Minimum Tax6) Avoid Transfer for Value

As stated above, the two basic types of buy-sell agreements,come up short. The standard cross-purchase arrangementrequires that multiple policies be purchased, [n(n-1) wheren=number of shareholders]. You can avoid this with atrusteed or escrow buy-sell arrangement, but you still havepotential transfer for value issues and the parties will haveto swap policies at retirement to have access to the cashvalue. An entity buy-sell arrangement has potential problemsunder 3, 4 and 5 above. With The ASSN.TM Group Plan, wemay meet some or all of the client’s goals listed above.

Goal #1: Provide Sufficient Funds to the Buyerand Limit Number of PoliciesLet’s use as an example a corporation with five shareholders.Using a standard cross-purchase arrangement, the groupwould need 20 policies to fund the buy-sell. Some insuranceagents may not see the problem with this, but trust me, clientswill not be thrilled to have to buy 20 policies. With the GroupBenefit plan, all we need is five policies. Each shareholderwould name the other four shareholders as a partialbeneficiary of the Group benefit. This would give eachshareholder access to enough cash to buy their portion of adeceased shareholder’s stock. If the shareholders also own apartnership, another option would be for the shareholdersto name the partnership as beneficiary. Under the terms ofthe partnership agreement, the partnership would distributethe life insurance death benefit to the surviving partnerswho would then use the proceeds to purchase stock fromthe deceased shareholder’s estate. This should also avoidany transfer for value issue as discussed below.

Assn.TM Group News

Since each shareholder will own their certificate, additionalcash flow may be necessary to fund a buy-out at retirementor other withdrawal during life. An installment sale may makesense. Because the cash value in the policy is owned by theinsured, the buy-sell agreement could have one valuationformula used for lifetime buy-outs and another for buy-outsat death. Caution would need to be exercised when using thistechnique, especially when a family-owned business is involved.The buy-sell agreement may not peg the value of the businessfor federal estate tax purposes.

Goal #2: Provide Increase-in-Basis toSurviving OwnersUnlike an entity buy-sell arrangement, the Group BenefitPlan should result in an increase in the surviving owner’sbasis. This is the result because under the ASSN.TM GroupPlan the surviving owners will receive cash to buy the businessinterest directly from the decedent’s estate. If a new ownerbecomes part of the buy-sell agreement, the other ownersjust simply change beneficiary designations on the plandocuments to include the new owner. If a partnership werenamed as beneficiary, this would not be necessary.

Goal #3: Tax free access to the Cash Value inRetirementUnder the Group Benefit Plan, the insured can own his orher own policy, and be able to access the cash value tax-freeafter they are no longer participants in the plan. Althougheach participant is taxed on the economic benefit of theGroup death benefit, there is never a distribution of thecertificate to the insured. The insured owns the certificatefrom the start and once participation in the plan is terminated,can access the policy cash value tax-free. An ILIT/ILP canalso own the policy. (See Estate Planning Memorandum.)

Goal #4: Avoid Alternative Minimum TaxThe Group Benefit Plan avoids Alternative Minimum Tax(AMT) issues with regard to the Group death benefit becausethe C - Corporation (employer) is never the beneficiary ofthis amount (S - Corporations avoid AMT). It may be thebeneficiary of the remaining death benefit, but never theGroup death benefit. Theoretically, the remaining deathbenefit could be considered a preferenceitem for purposes of alternative minimum tax. However: (1)the remaining death benefit is typically significantly smaller

than the Group death benefit, and (2) AMT is not a hugeproblem. It is a prepayment of tax, that a corporation maytake a deduction for in subsequent years.

Goal #5: Avoid Transfer for ValueUnlike a traditional cross-purchase agreement established forthree or more shareholders in a corporation, the GroupBenefit Plan avoids all transfer for value issues without theneed to set up a partnership. With the ASSN.TM Group Plan,there is no transfer of the life insurance policy or an interesttherein for valuable consideration. Using the example above,each shareholder (or ILIT/ILP) will own their own certificateand name the other shareholders. The act of naming a personas beneficiary of a policy does not rise to the level oftransferring an interest in a policy for purposes of the transferfor value rule under IRC Section 101 (a)(2).

Section 101 deals with the transfer of ownership rights. Abeneficiary of a policy does not have any contractual rightsin the life insurance policy. Note, however, that if the clientbelieves that the potential for a transfer for value problemunder Section 101 is high, then suggest that the client havetheir attorney draft a partnership agreement between the clientand the other shareholders.

If the insured owns the certificate, the entire death benefitmay be included in his or her estate under Section 2042 ofthe Code. However, if the insured is obligated under thebuy-sell agreement to name the co-shareholder(s) asbeneficiary, an amount equal to the death benefit may beconsidered indebtedness of the insured to the co-shareholder(s) and deductible for estate tax purposes underSection 2053. This issue should be carefully reviewed by theclient’s tax attorney or CPA. Alternatively, a partnershipestablished by the shareholders could be named owner andbeneficiary under the policy, as well as irrevocable beneficiaryunder the Group Benefit Plan.

Utilizing the Group Benefit Plan in the Estate Planning Case

ASSN.™ Group News

The ASSN.™ Group Plan is a powerful financial tool when used for estate planning purposes. This method can provide the Participant with a death benefit that may avoid both income and estate taxes. How can you accomplish this? The first step in the process is for the Plan Participant to establish an Irrevocable Life Insurance Trust (ILIT) or Insurance Limited Partnership (ILP)–typically with defective grantor trust provisions–that will be the owner of the life insurance certificate insuring the Plan Participant. The Participant is underwritten for a life insurance policy that will provide the death benefit amount as designed under §79 rules of the Group Benefit Plan. The Trustee of the ILIT/LIP signs the life application as the owner of the certificate. The ILIT/ILP completes and signs a co-ownership agreement. The beneficiary of the death benefit in the Group Benefit Plan is stipulated as the ILIT/ILP. The Employer pays the Group Term Benefit cost–the tax-deductible annually actuarially determined amount. The remaining premium is also paid by the Employer generally as a §162 Plan (Bonus Plan Option). The gift that is considered made to the trust (ILIT/ILP) would be the total of the economic benefit of the death benefit provided by the Group Benefit Plan and the total remaining premium paid if utilizing the Bonus Plan option. At termination of the Group Benefit Plan, the ILIT/ILP would retain all rights to the life insurance policy on the Plan Participant. If a Corporate-Owned policy is used, the gift made to the ILIT/ILP would be the economic benefit on the Group Benefit Plan death benefit only. At Plan termination, the ILIT/ILP would lose the death benefit provided by the Group Benefit Plan Certificate since the Plan is no longer owned by the ILIT/ILP. This is a short-term estate planning solution and is generally not recommended. Working with advisors many use a Spousal ILIT for increased flexibility in estate planning cases and rollout.

Steps to utilize the Group Benefit Plan in the estate

planning case

STEP 1 Set up ILIT/ILP

Step 2 Co-ownership Agreement.

Administrative Agreement, and

Application

Step 3 Certificate issued on Plan

Participant

Step 4 Employer pays Group

Term Benefit; remaining premium paid as Bonus

to Participant

Step 5 Death Benefit has Gift Tax ramifications (see

chart)

Step 6 At termination, ILIT/ILP

retains all rights to certificate unless corporate-owned

Gift Taxes Due on Group Benefit Plan

If a Bonus Option If Corporate-Owned

The economic benefit of the death benefit provided by the Group Benefit Plan

The economic benefit of the death benefit in the Group Benefit Plan only.