the big picture_follow the money

DESCRIPTION

The first course assignment, Group of follow the moneyTRANSCRIPT

Follow the Money GroupJingyuan Hu

Kari HavnevikGu!rún Lilja Jónsdóttir

Francisco Rodríguez Saa

2/1/12 8:18 AMStreamgraph

Page 1 of 1file:///Users/amy/Dropbox/jj/commodity/stream.html

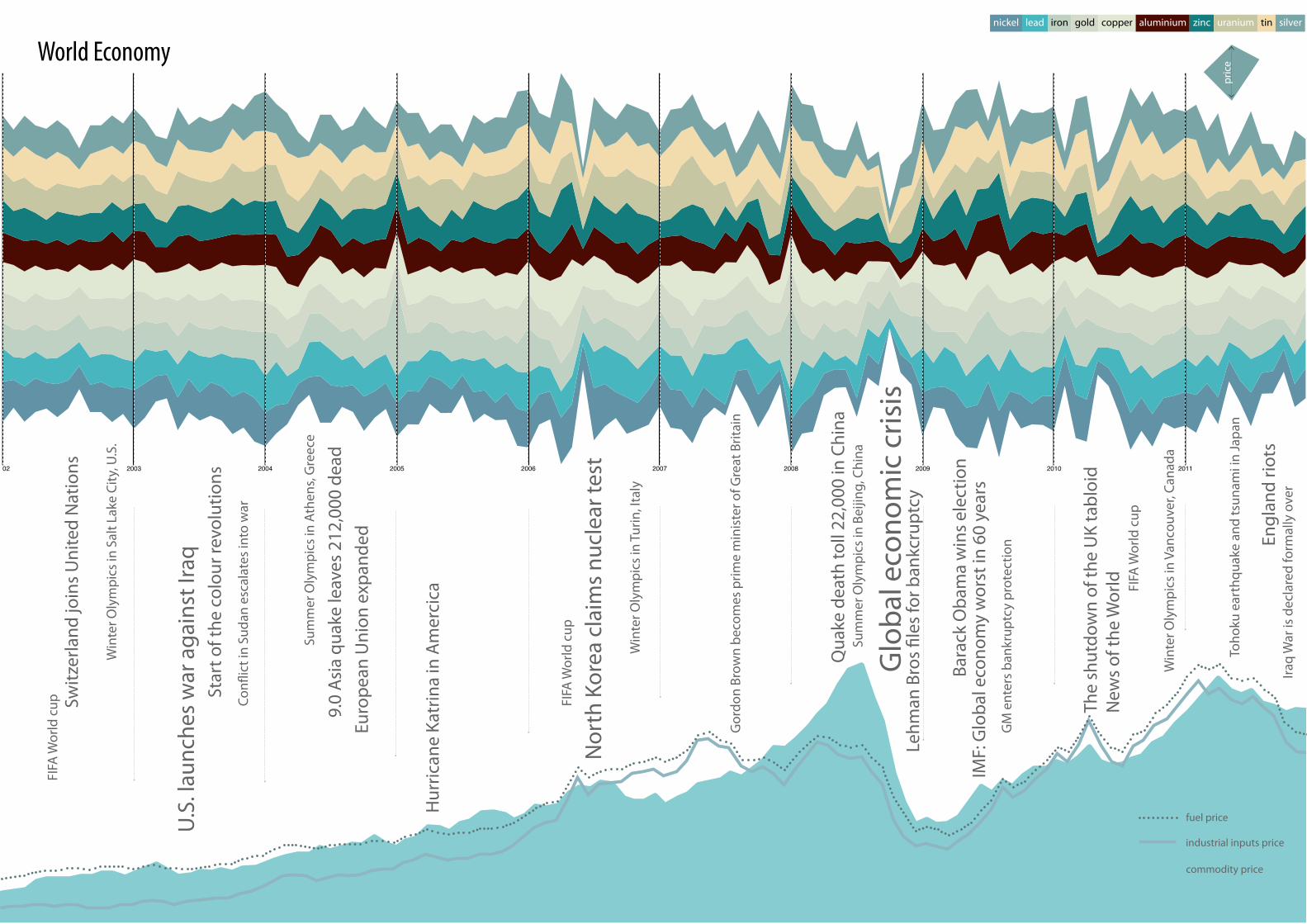

nickel lead iron gold copper aluminium zinc uranium tin silver

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

World Economy

Glo

bal e

cono

mic

cris

is

U.S.

laun

ches

war

aga

inst

Iraq

Nor

th K

orea

cla

ims n

ucle

ar te

st

Hur

rican

e Ka

trin

a in

Am

erci

ca

9.0

Asia

qua

ke le

aves

212

,000

dea

d

Switz

erla

nd jo

ins U

nite

d N

atio

ns

Win

ter O

lym

pics

in S

alt L

ake

City

, U.S

.

FIFA

Wor

ld c

up

Sum

mer

Oly

mpi

cs in

Ath

ens,

Gre

ece

Win

ter O

lym

pics

in Tu

rin, I

taly

Gor

don

Brow

n be

com

es p

rime

min

ister

of G

reat

Brit

ain

Sum

mer

Oly

mpi

cs in

Bei

jing,

Chi

na

Win

ter O

lym

pics

in V

anco

uver

, Can

ada

Star

t of t

he c

olou

r rev

olut

ions

Con!

ict i

n Su

dan

esca

late

s int

o w

ar

Euro

pean

Uni

on e

xpan

ded

Lehm

an B

ros "

les f

or b

ankc

rupt

cy

Qua

ke d

eath

toll

22,0

00 in

Chi

na

Bara

ck O

bam

a w

ins e

lect

ion

GM

ent

ers b

ankr

uptc

y pr

otec

tion

IMF:

Glo

bal e

cono

my

wor

st in

60

year

s

The

shut

dow

n of

the

UK

tabl

oid

New

s of t

he W

orld

Iraq

War

is d

ecla

red

form

ally

ove

rEn

glan

d rio

ts

Toho

ku e

arth

quak

e an

d ts

unam

i in

Japa

n

FIFA

Wor

ld c

up

FIFA

Wor

ld c

up

nickel lead iron gold copper aluminium zinc uranium tin silver

2002 2003 2004 2005 2006 2007

commodity price

industrial inputs price

fuel price

pric

e

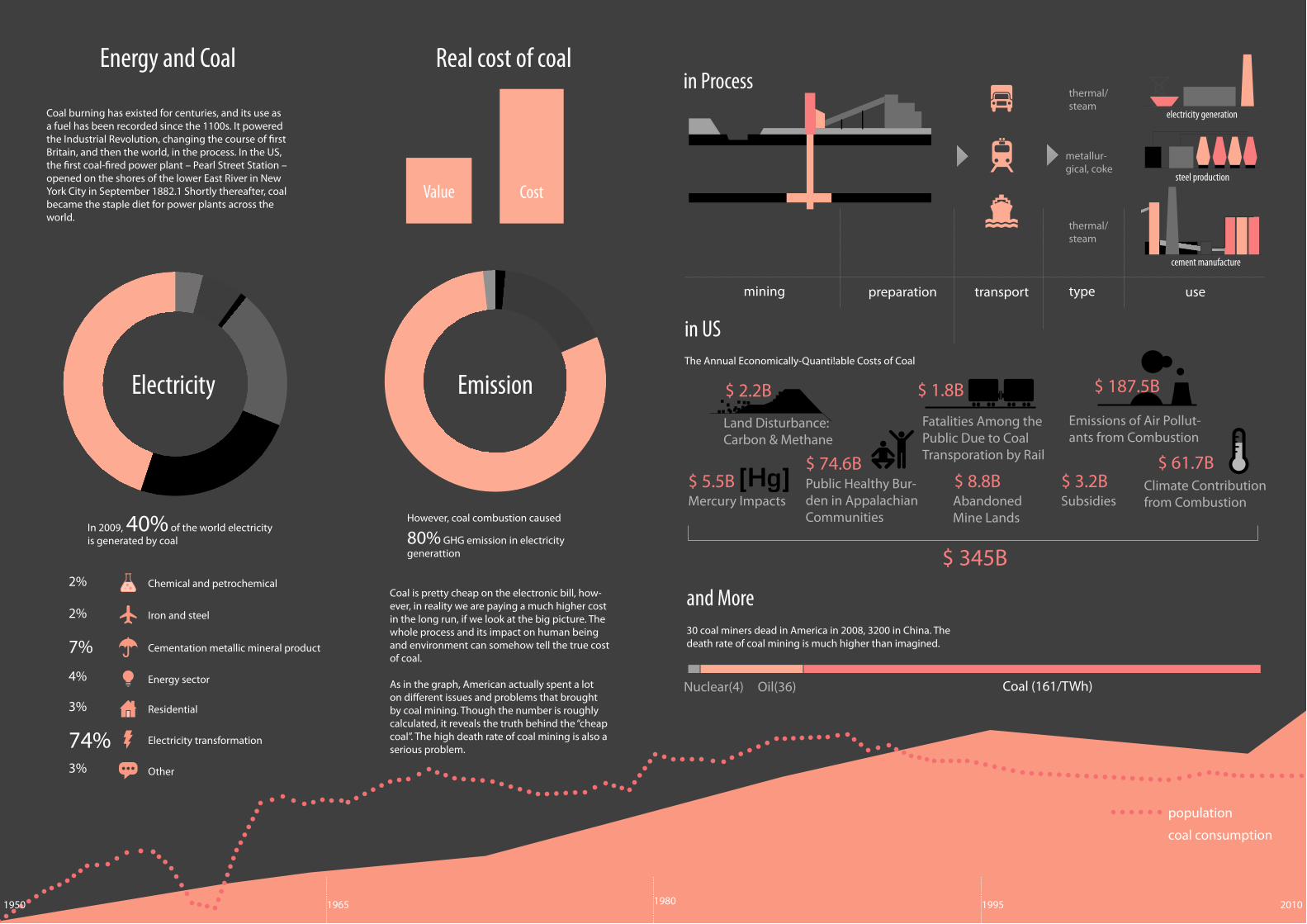

Chemical and petrochemical

Iron and steel

Cementation metallic mineral product

Energy sector

Residential

Electricity transformation

Other

2%

2%

7%4%

3%

74%3%

Energy and Coal Real cost of coal

Electricity Emission

Coal burning has existed for centuries, and its use as a fuel has been recorded since the 1100s. It powered the Industrial Revolution, changing the course of !rst Britain, and then the world, in the process. In the US, the !rst coal-!red power plant – Pearl Street Station – opened on the shores of the lower East River in New York City in September 1882.1 Shortly thereafter, coal became the staple diet for power plants across the world.

Coal is pretty cheap on the electronic bill, how-ever, in reality we are paying a much higher cost in the long run, if we look at the big picture. The whole process and its impact on human being and environment can somehow tell the true cost of coal.

As in the graph, American actually spent a lot on di"erent issues and problems that brought by coal mining. Though the number is roughly calculated, it reveals the truth behind the “cheap coal”. The high death rate of coal mining is also a serious problem.

In 2009, 40% of the world electricity is generated by coal

However, coal combustion caused

80% GHG emission in electricity generattion

30 coal miners dead in America in 2008, 3200 in China. The death rate of coal mining is much higher than imagined.

Value Cost

thermal/steam

mining preparation transport type use

electricity generation

steel production

cement manufacture

metallur-gical, coke

thermal/steam

in US

in Process

and More

$ 345B

Land Disturbance: Carbon & Methane

$ 2.2B $ 1.8B

$ 74.6B$ 8.8B $ 3.2B$ 5.5B

$ 61.7BPublic Healthy Bur-den in Appalachian Communities

Fatalities Among the Public Due to Coal Transporation by Rail

Emissions of Air Pollut-ants from Combustion

Mercury Impacts

Nuclear(4) Oil(36) Coal (161/TWh)

Climate Contribution from CombustionSubsidiesAbandoned

Mine Lands

[Hg]

$ 187.5BThe Annual Economically-Quanti!able Costs of Coal

coal consumption

population

2010199519801950 1965

2010

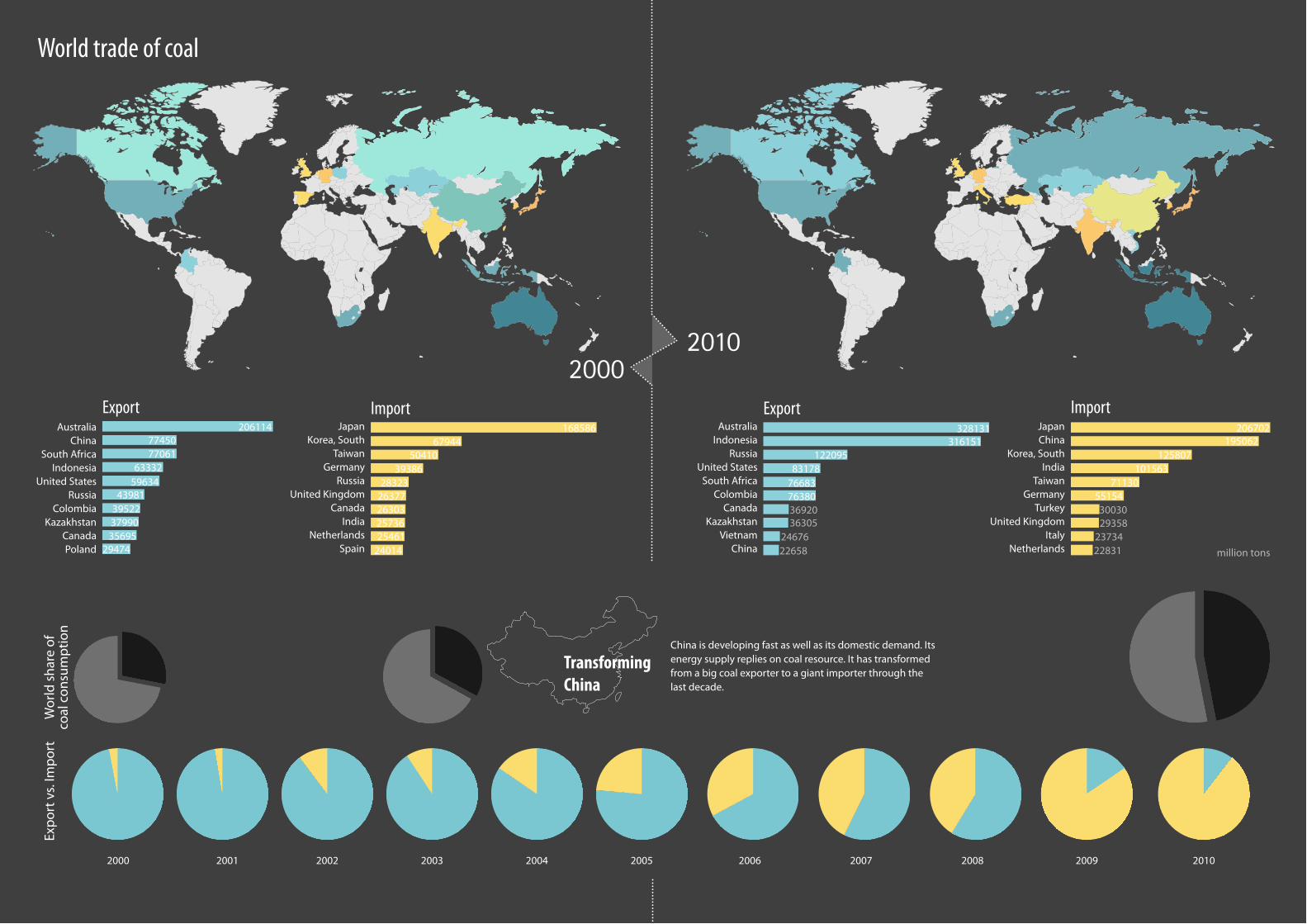

ImportExportAustralia

IndonesiaRussia

United StatesSouth Africa

ColombiaCanada

KazakhstanVietnam

China

JapanChina

Korea, SouthIndia

TaiwanGermany

TurkeyUnited Kingdom

ItalyNetherlands

2000Export

Expo

rt v

s. Im

port

Wor

ld sh

are

of

coal

con

sum

ptio

n

Transforming China

AustraliaChina

South AfricaIndonesia

United StatesRussia

ColombiaKazakhstan

CanadaPoland

ImportJapan

Korea, SouthTaiwan

GermanyRussia

United KingdomCanada

IndiaNetherlands

Spain

China is developing fast as well as its domestic demand. Its energy supply replies on coal resource. It has transformed from a big coal exporter to a giant importer through the last decade.

2000 2003 20062001 2004 2007 20092002 2005 2008 2010

206114 168586 328131316151

12209583178

76683763803692036305

2467622658

7745077061

6333259634

43981395223799035695

29474

6794450410

3938628323

26377263032573625461

24014

206702195062

125807101563

71130551543003029358

2373422831 million tons

World trade of coal

Resource1. http://www.skepticalscience.com/true-cost-of-coal-power.html

2. http://www.coalcrusher.org/coal/coal-application.html

3. http://www.markenglehartevans.com/2011/05/state-grid-vs-beijing-a-familiar-game-of-chicken/

4. http://seekingalpha.com/article/238639-the-coal-situation-in-asia

5. http://www.worldcoal.org/

6. http://www.c2es.org/technology/overview/electricity

7. http://nextbigfuture.com/2011/03/deaths-per-twh-by-energy-source.html

8. http://www.sourcewatch.org/index.php?title=Coal_mining_disasters

9. http://www.mapreport.com/subtopics/i.html

10. http://en.wikipedia.org/wiki/21st_century#Economics_.26_Industry

11. Ming Coal, Mounting Costs: The life cycle consequences of coal (http://chge.med.har-vard.edu/programs/ccf/documents/MiningCoalMountingCosts.pdf )

12. The True Cost of Coal (http://www.greenpeace.org/international/Global/international/planet-2/report/2008/11/cost-of-coal.pdf )

13. BP Statistical Review of World Energy 2011 (http://www.bp.com/assets/bp_internet/globalbp/globalbp_uk_english/reports_and_publications/statistical_energy_re-view_2011/STAGING/local_assets/pdf/statistical_review_of_world_energy_full_re-port_2011.pdf)

14. http://www.indexmundi.com/

15. http://en.wikipedia.org/wiki/Coal

16. http://www.visualizing.org/

17. http://www.iea.org/index.asp

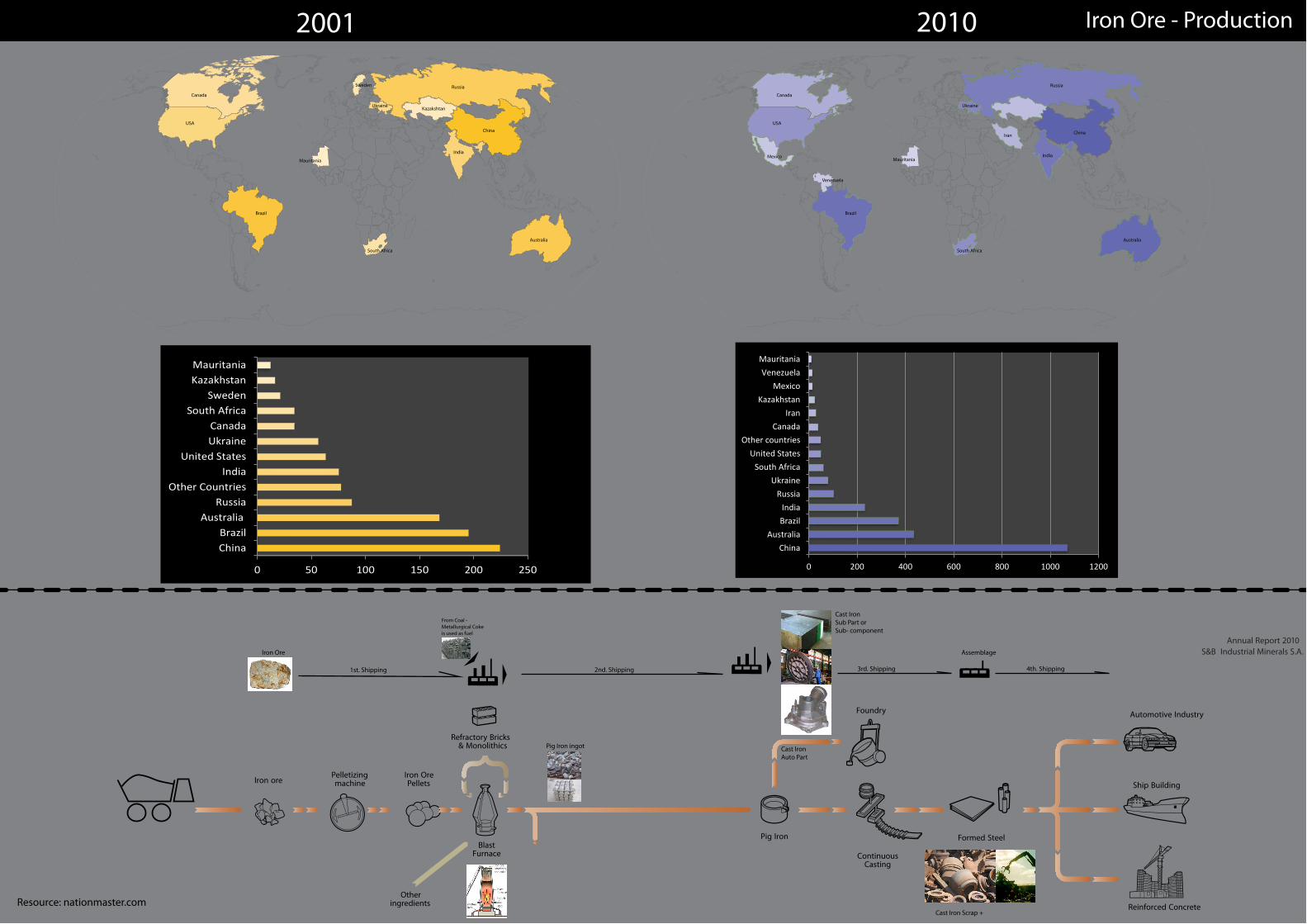

Iron Ore

Cast IronSub Part orSub- component

Assemblage

Cast IronAuto Part

Cast Iron Scrap +

1st. Shipping 2nd. Shipping 3rd. Shipping 4th. Shipping

From Coal - Metallurgical Coke is used as fuel

Pig Iron ingot

S&B Industrial Minerals S.A.Annual Report 2010

Pelletizingmachine

Iron OrePellets

BlastFurnace

Refractory Bricks& Monolithics

Otheringredients

Iron ore Ship Building

Automotive IndustryFoundry

Formed SteelPig Iron

ContinuousCasting

Reinforced Concrete

Iron Ore - Production2001 2010

South Africa

Mauritania

Brazil

Australia

0 50 100 150 200 250

China

Brazil

Australia

Russia

Other Countries

India

United States

Ukraine

Canada

South Africa

Sweden

Kazakhstan

Mauritania

Kazakshtan

Russia

China

India

USA

Canada

Ukraine

Sweden

Australia

South Africa

Mexico Mauritania

Venezuela

Brazil

India

0 200 400 600 800 1000 1200

China

Australia

Brazil

India

Russia

Ukraine

South Africa

United States

Other countries

Canada

Iran

Kazakhstan

Mexico

Venezuela

Mauritania

China

Russia

USA

Canada

Ukraine

Iran

Resource: nationmaster.com

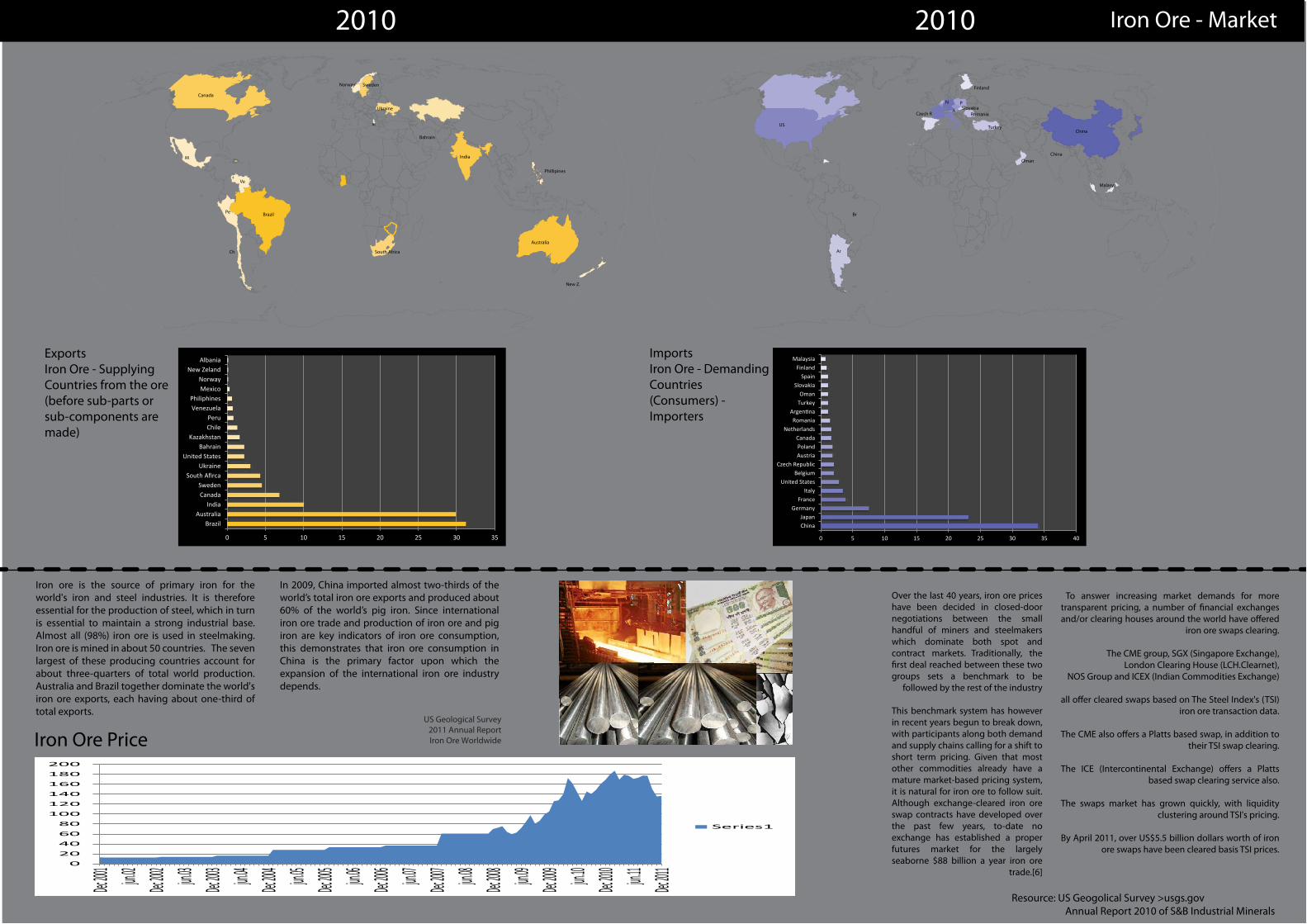

Iron Ore Price

0

20

40

60

80

100

120

140

160

180

200

Dec 2

001 jun.02

Dec 2

002 jun.03

Dec 2

003 jun.04

Dec 2

004 jun.05

Dec 2

005 jun.06

Dec 2

006 jun.07

Dec 2

007 jun.08

Dec 2

008 jun.09

Dec 2

009 jun.10

Dec 2

010 jun.11

Dec 2

011

Series1

Over the last 40 years, iron ore prices have been decided in closed-door negotiations between the small handful of miners and steelmakers which dominate both spot and contract markets. Traditionally, the !rst deal reached between these two groups sets a benchmark to be

followed by the rest of the industry

This benchmark system has however in recent years begun to break down, with participants along both demand and supply chains calling for a shift to short term pricing. Given that most other commodities already have a mature market-based pricing system, it is natural for iron ore to follow suit. Although exchange-cleared iron ore swap contracts have developed over the past few years, to-date no exchange has established a proper futures market for the largely seaborne $88 billion a year iron ore

trade.[6]

To answer increasing market demands for more transparent pricing, a number of !nancial exchanges and/or clearing houses around the world have o"ered

iron ore swaps clearing.

The CME group, SGX (Singapore Exchange), London Clearing House (LCH.Clearnet),

NOS Group and ICEX (Indian Commodities Exchange)

all o"er cleared swaps based on The Steel Index's (TSI) iron ore transaction data.

The CME also o"ers a Platts based swap, in addition to their TSI swap clearing.

The ICE (Intercontinental Exchange) o"ers a Platts based swap clearing service also.

The swaps market has grown quickly, with liquidity clustering around TSI's pricing.

By April 2011, over US$5.5 billion dollars worth of iron ore swaps have been cleared basis TSI prices.

Iron ore is the source of primary iron for the world's iron and steel industries. It is therefore essential for the production of steel, which in turn is essential to maintain a strong industrial base. Almost all (98%) iron ore is used in steelmaking. Iron ore is mined in about 50 countries. The seven largest of these producing countries account for about three-quarters of total world production. Australia and Brazil together dominate the world's iron ore exports, each having about one-third of total exports.

In 2009, China imported almost two-thirds of the world’s total iron ore exports and produced about 60% of the world’s pig iron. Since international iron ore trade and production of iron ore and pig iron are key indicators of iron ore consumption, this demonstrates that iron ore consumption in China is the primary factor upon which the expansion of the international iron ore industry depends.

US Geological Survey2011 Annual ReportIron Ore Worldwide

Iron Ore - Market2010 2010

ExportsIron Ore - Supplying Countries from the ore (before sub-parts or sub-components are made)

ImportsIron Ore - Demanding Countries (Consumers) - Importers

South Africa

M

Ch

Pe

Ve

Brazil

New Z.

Ar

Br

0 5 10 15 20 25 30 35

Brazil

Australia

India

Canada

Sweden

South AĮrca

Ukraine

United States

Bahrain

Kazakhstan

Chile

Peru

Venezuela

Philiphines

Mexico

Norway

New Zeland

Albania

0 5 10 15 20 25 30 35 40

China

Japan

Germany

France

Italy

United States

Belgium

Czech Republic

Austria

Poland

Canada

Netherlands

Romania

ArgenƟna

Turkey

Oman

Slovakia

Spain

Finland

Malaysia

Ukraine

Phillipines

Malasya

Finland

Slovakia

Turkey

Oman

China

China

Romania

N PA

Czech R

Al

Bahrain

Australia

India

Canada

SwedenNorway

US

Resource: US Geogolical Survey >usgs.gov Annual Report 2010 of S&B Industrial Minerals

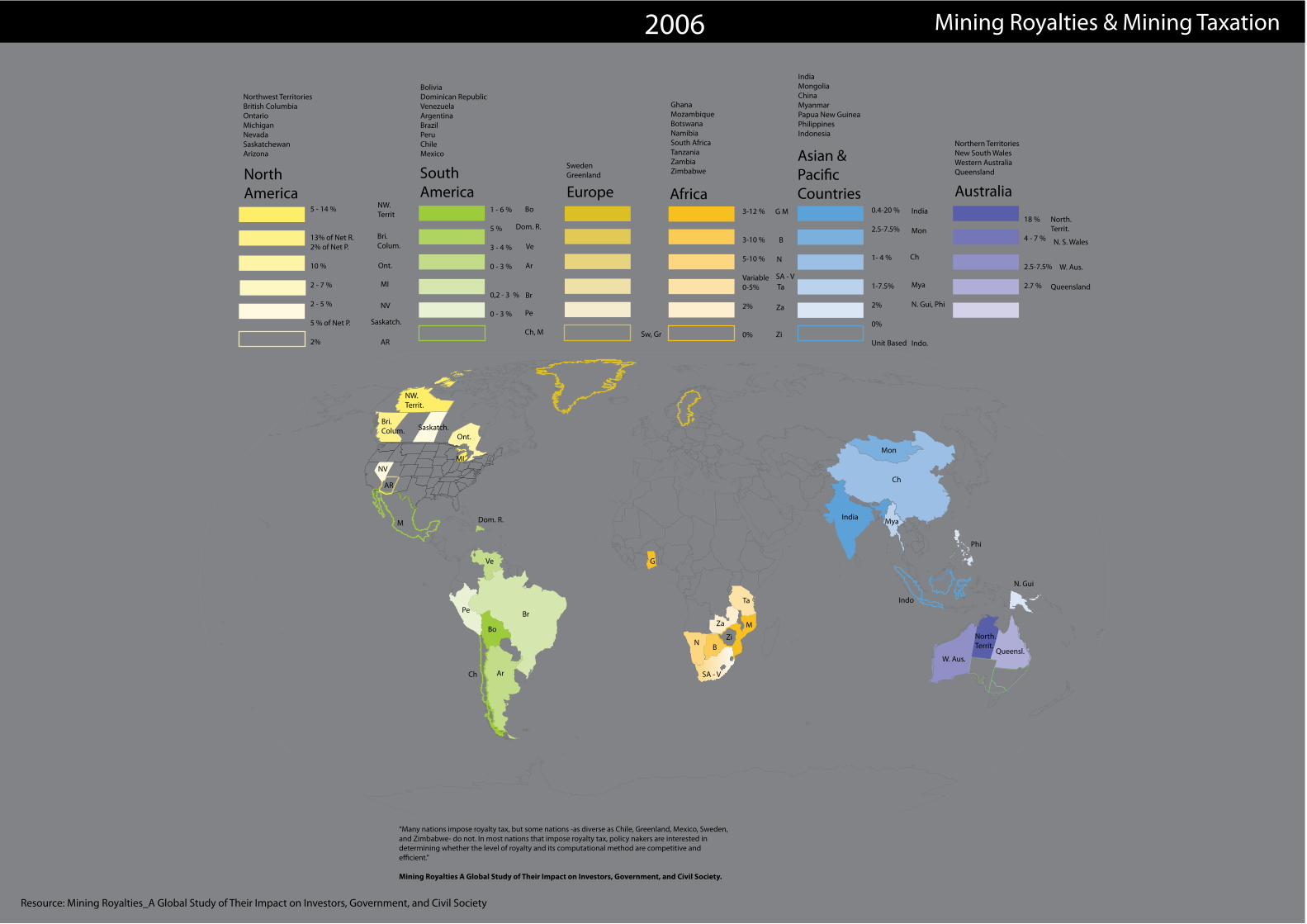

“Many nations impose royalty tax, but some nations -as diverse as Chile, Greenland, Mexico, Sweden, and Zimbabwe- do not. In most nations that impose royalty tax, policy nakers are interested in determining whether the level of royalty and its computational method are competitive and e!cient.”

Mining Royalties A Global Study of Their Impact on Investors, Government, and Civil Society.

Mining Royalties & Mining Taxation2006

Europe

Sw, Gr

SwedenGreenland

1 - 6 %

5 %

3 - 4 %

0 - 3 %

0,2 - 3 %

0 - 3 %

South America

Ch, M

Ar

Pe

Ve

Br

Dom. R.

Bo

BoliviaDominican RepublicVenezuelaArgentinaBrazilPeruChileMexico

3-12 %

3-10 %

5-10 %

Variable0-5%

2%

0%

GhanaMozambiqueBotswanaNamibiaSouth AfricaTanzaniaZambiaZimbabwe

Africa

SA - V

B

N

Ta

Zi

Za

G M 0.4-20 %

2.5-7.5%

1- 4 %

1-7.5%

2%

0%

Unit Based

IndiaMongoliaChinaMyanmarPapua New GuineaPhilippinesIndonesia

Asian & Paci"c Countries

Ch

Indo.

Mon

Mya

N. Gui, Phi

India

Northern TerritoriesNew South WalesWestern AustraliaQueensland

18 %

4 - 7 %

2.5-7.5%

2.7 %

Australia

N. S. Wales

North. Territ.

Queensland

W. Aus.

M Dom. R.

Ont.

NW. Territ.

Bri. Colum. Saskatch.

B

SA - V

N

Ta

Zi

Za

G

Ch Ar

Pe

Ve

Br

Bo MNorth.Territ.

Queensl.W. Aus.

Indo

Phi

N. Gui

Mon

MyaIndia

ChAR

MINV

Northwest TerritoriesBritish ColumbiaOntarioMichiganNevadaSaskatchewanArizona

North America

5 - 14 %

13% of Net R.2% of Net P.

10 %

2 - 7 %

2 - 5 %

5 % of Net P.

2% AR

Saskatch.

Bri. Colum.

NW. Territ

MI

NV

Ont.

Resource: Mining Royalties_A Global Study of Their Impact on Investors, Government, and Civil Society

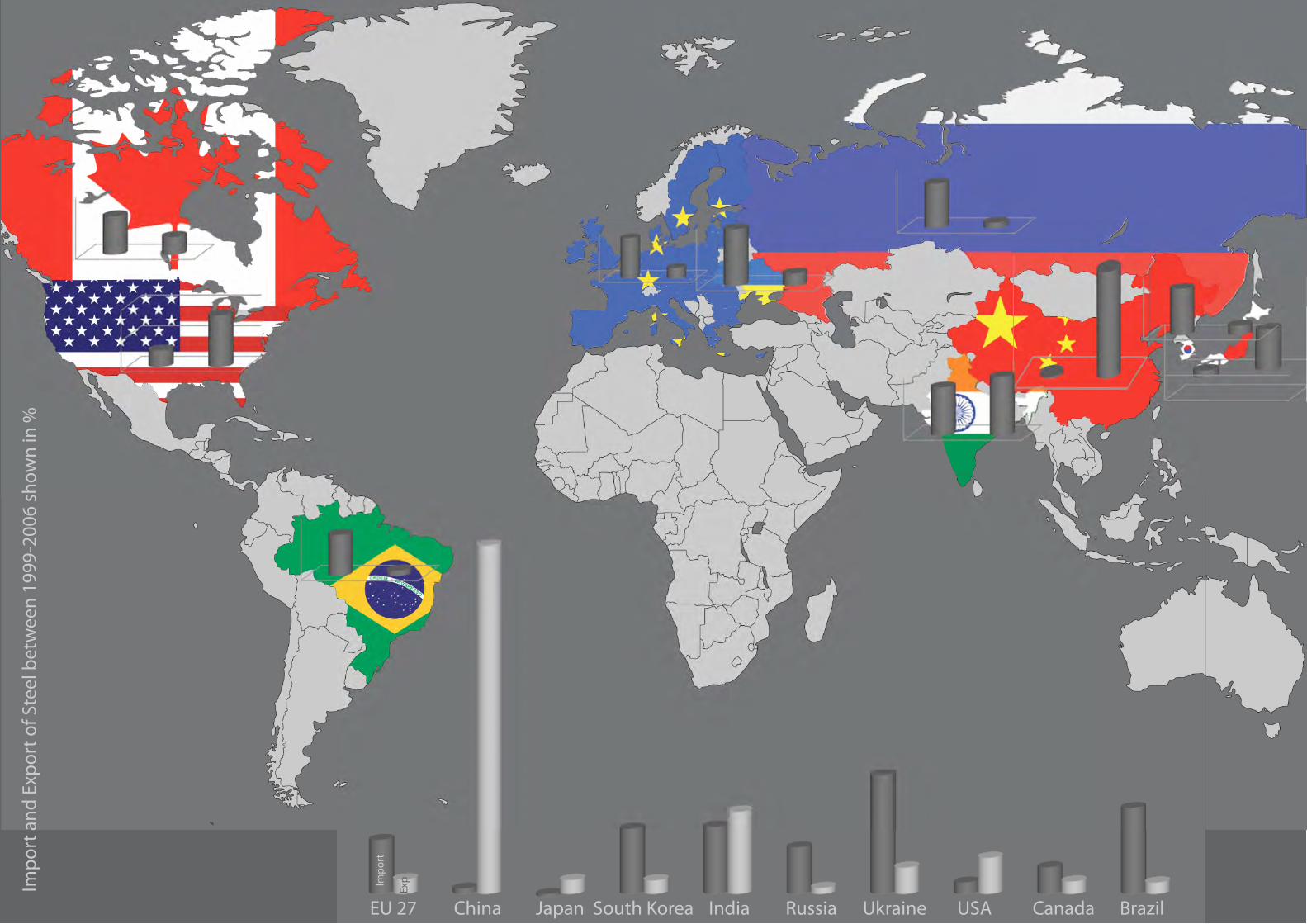

EU 27 China Japan South Korea India Russia Ukraine USA Canada Brazil

Impo

rt a

nd E

xpor

t of S

teel

bet

wee

n 19

99-2

006

show

n in

%

Impo

rt

Exp

Ϭ�

ϭϬϬ�

ϮϬϬ�

ϯϬϬ�

ϰϬϬ�

ϱϬϬ�

ϲϬϬ�

ϭϵϵϴ� ϮϬϬϮ� ϮϬϬϲ� ϮϬϬϴ�Ϭ�

ϭϬϬ�

ϮϬϬ�

ϯϬϬ�

ϰϬϬ�

ϱϬϬ�

ϲϬϬ�

ϭϵϵϴ� ϮϬϬϮ� ϮϬϬϲ

Ϭ�

ϭϬϬ�

ϮϬϬ�

ϯϬϬ�

ϰϬϬ�

ϱϬϬ�

ϲϬϬ�

ϭϵϵϴ� ϮϬϬϮ� ϮϬϬϲ� ϮϬϬϴ

Ϭ�

ϭϬϬ�

ϮϬϬ�

ϯϬϬ�

ϰϬϬ�

ϱϬϬ�

ϲϬϬ�

ϭϵϵϴ� ϮϬϬϮ� ϮϬϬϲ� ϮϬϬϴ�

��

��

��

��

��

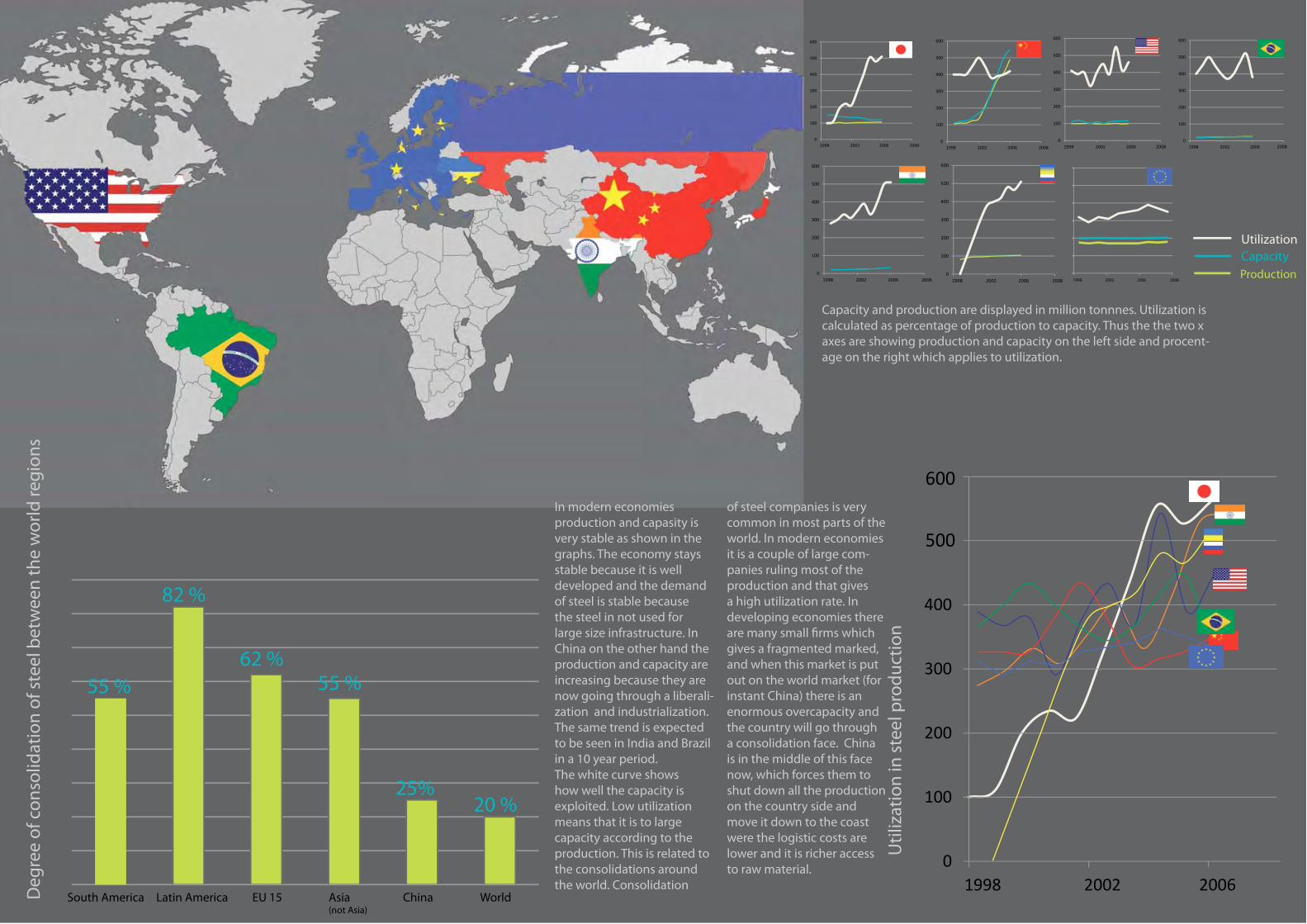

55 %

82 %

62 %55 %

25%20 %

WorldChinaAsia(not Asia)

EU 15Latin AmericaSouth America

UtilizationCapacityProduction

Deg

ree

of c

onso

lidat

ion

of st

eel b

etw

een

the

wor

ld re

gion

s

Util

izat

ion

in st

eel p

rodu

ctio

n

Ϭ�

ϭϬϬ�

ϮϬϬ�

ϯϬϬ�

ϰϬϬ�

ϱϬϬ�

ϲϬϬ�

ϭϵϵϴ� ϮϬϬϮ� ϮϬϬϲ� ϮϬϬϴ�

Ϭ�

ϭϬϬ�

ϮϬϬ�

ϯϬϬ�

ϰϬϬ�

ϱϬϬ�

ϲϬϬ�

ϭϵϵϴ� ϮϬϬϮ� ϮϬϬϲ�

�

�

�

�

� � � � � �1998 2002 2006 2008

20082008

Ϭ�

ϭϬϬ�

ϮϬϬ�

ϯϬϬ�

ϰϬϬ�

ϱϬϬ�

ϲϬϬ�

ϭϵϵϴ� ϮϬϬϮ� ϮϬϬϲ�

Capacity and production are displayed in million tonnnes. Utilization is calculated as percentage of production to capacity. Thus the the two x axes are showing production and capacity on the left side and procent-age on the right which applies to utilization.

In modern economies production and capasity is very stable as shown in the graphs. The economy stays stable because it is well developed and the demand of steel is stable because the steel in not used for large size infrastructure. In China on the other hand the production and capacity are increasing because they are now going through a liberali-zation and industrialization. The same trend is expected to be seen in India and Brazil in a 10 year period. The white curve shows how well the capacity is exploited. Low utilization means that it is to large capacity according to the production. This is related to the consolidations around the world. Consolidation

of steel companies is very common in most parts of the world. In modern economies it is a couple of large com-panies ruling most of the production and that gives a high utilization rate. In developing economies there are many small ! rms which gives a fragmented marked, and when this market is put out on the world market (for instant China) there is an enormous overcapacity and the country will go through a consolidation face. China is in the middle of this face now, which forces them to shut down all the production on the country side and move it down to the coast were the logistic costs are lower and it is richer access to raw material.

Ϯϱ ϯϱ

Top

Wor

ld E

xpor

ters

, mill

ion

of R

olle

d St

eel,

tonn

s

The change in the steel production in the New member States of EU from 1989-2000

The

larg

est E

U st

eel p

rodu

ctio

n co

ntrie

s 200

7

2007

2007

20092008

ϭϱ

23,3 %

15,4%

9,2%

9,1%

6,9 %

5,1 %

5,1%3,6 %3,5 % 3,4 %

Poland Chech Republic Romania

1989

2000

-30,5 % -59,7% -66,7%

Germany

South Korea

Ukraine

Russia

Japan

20092008

2007

20092008

2007

20092008

2007

20092008

Production in New EU member statesParticularly the large steel producing regions in the New Member States, Poland, the Czech Republic and Romania have experienced massive restructuring and reorganization since the collapse of the planned economies. From 1989 to 2000 total steel production decreased by between 30-66 % in these major steel producing countries. Outdated capacities were dismantled and former volume output has increasingly been shifted towards quality-output. From 2002-2007, total steel production in the new EU Member States has stabilized.

The largest EU steel producing countries are Germany, Italy, France, Spain, the UK, Belgium, Poland, Austria, Nederland and the Czech Republic. These relative positions have been steady for years. All together, the output level among New Member States are modest compare to the largest producing steel companies the EU 15 and only two New Member States are in the top 10.

The reason for the great decline of the new member states in EU was because of old and poor technology which was still the fact after the Sovjet time. When these counties left the Sovjet regime they went through a transition in economy. They went from planned economy to market based economy, which resulted in overcapasity. In that period of time they produced poor steel with low quality which is not the case today. Now the focus is based on high quality steel.

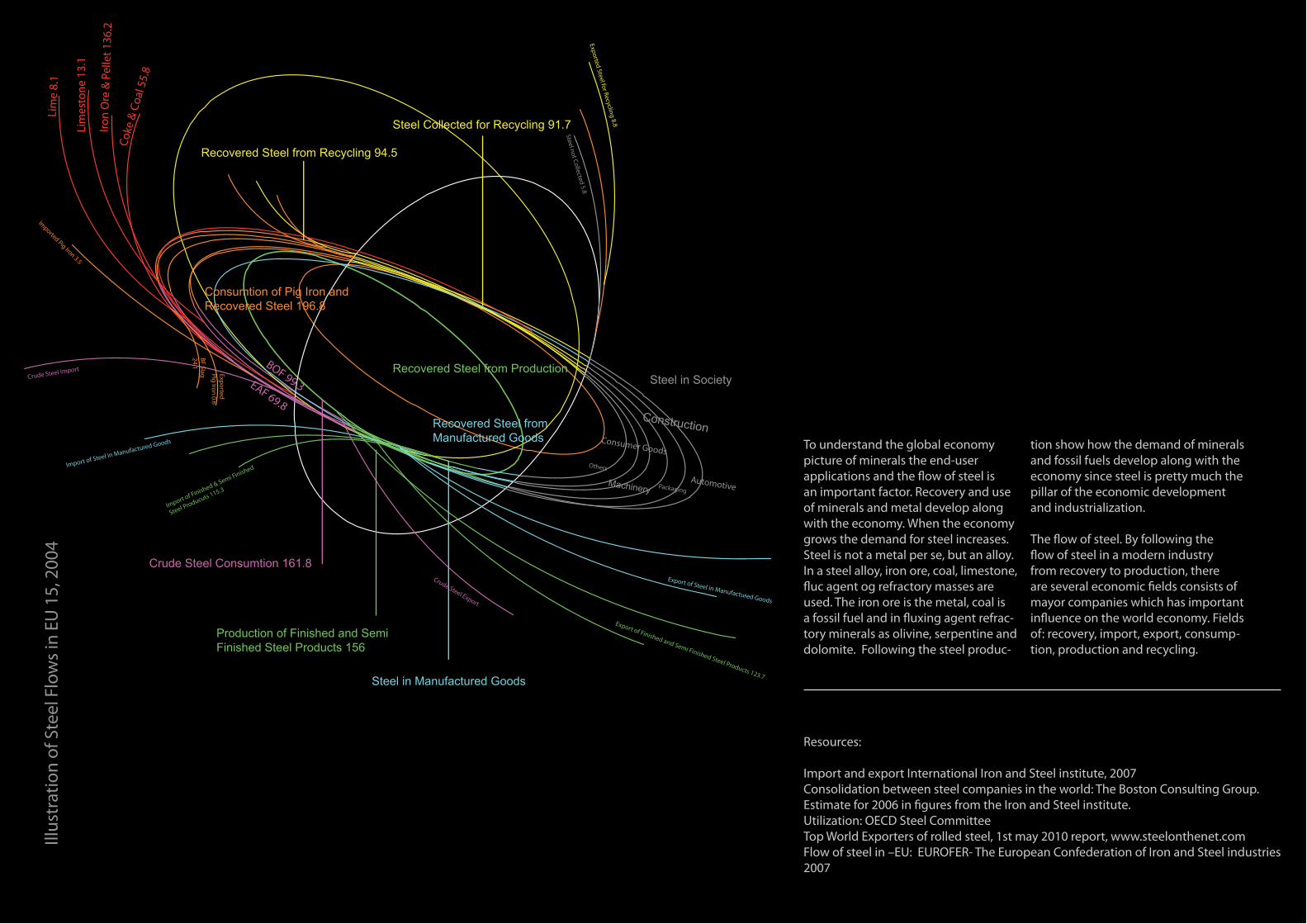

Machinery

Construction

Production of Finished and Semi Finished Steel Products 156

Crude Steel Consumtion 161.8

Steel Collected for Recycling 91.7

Recovered Steel from Recycling 94.5

Steel in Manufactured Goods

Consumtion of Pig Iron and Recovered Steel 196.8

Recovered Steel from Production

Recovered Steel from Manufactured Goods

Steel in Society

Coke

& C

oal 5

5.8

Lim

e 8.

1

Lim

esto

ne 1

3.1

Iron

Ore

& P

elle

t 136

.2

Imported Pig Iron 3.5

Exported Pig Iron 0.6

BF Slag 24.1

Crude Steel ImportBOF 99.3EAF 69.8

Import of Finished & Semi Finished

Steel Producuts 115.3

Import of Steel in Manufactured Goods

Crude Steel Export

Export of Finished and Semi Finished Steel Products 123.7

Export of Steel in Manufactured Goods

Packaging

Others

Automotive

Consumer Goods

Steel not Collected 5.8Exported Steel for Recycling 8.8

Illus

trat

ion

of S

teel

Flo

ws i

n EU

15,

200

4

To understand the global economy picture of minerals the end-user applications and the ! ow of steel is an important factor. Recovery and use of minerals and metal develop along with the economy. When the economy grows the demand for steel increases. Steel is not a metal per se, but an alloy. In a steel alloy, iron ore, coal, limestone, ! uc agent og refractory masses are used. The iron ore is the metal, coal is a fossil fuel and in ! uxing agent refrac-tory minerals as olivine, serpentine and dolomite. Following the steel produc-

tion show how the demand of minerals and fossil fuels develop along with the economy since steel is pretty much the pillar of the economic development and industrialization.

The ! ow of steel. By following the ! ow of steel in a modern industry from recovery to production, there are several economic " elds consists of mayor companies which has important in! uence on the world economy. Fields of: recovery, import, export, consump-tion, production and recycling.

Resources:

Import and export International Iron and Steel institute, 2007Consolidation between steel companies in the world: The Boston Consulting Group. Estimate for 2006 in " gures from the Iron and Steel institute. Utilization: OECD Steel CommitteeTop World Exporters of rolled steel, 1st may 2010 report, www.steelonthenet.comFlow of steel in –EU: EUROFER- The European Confederation of Iron and Steel industries 2007

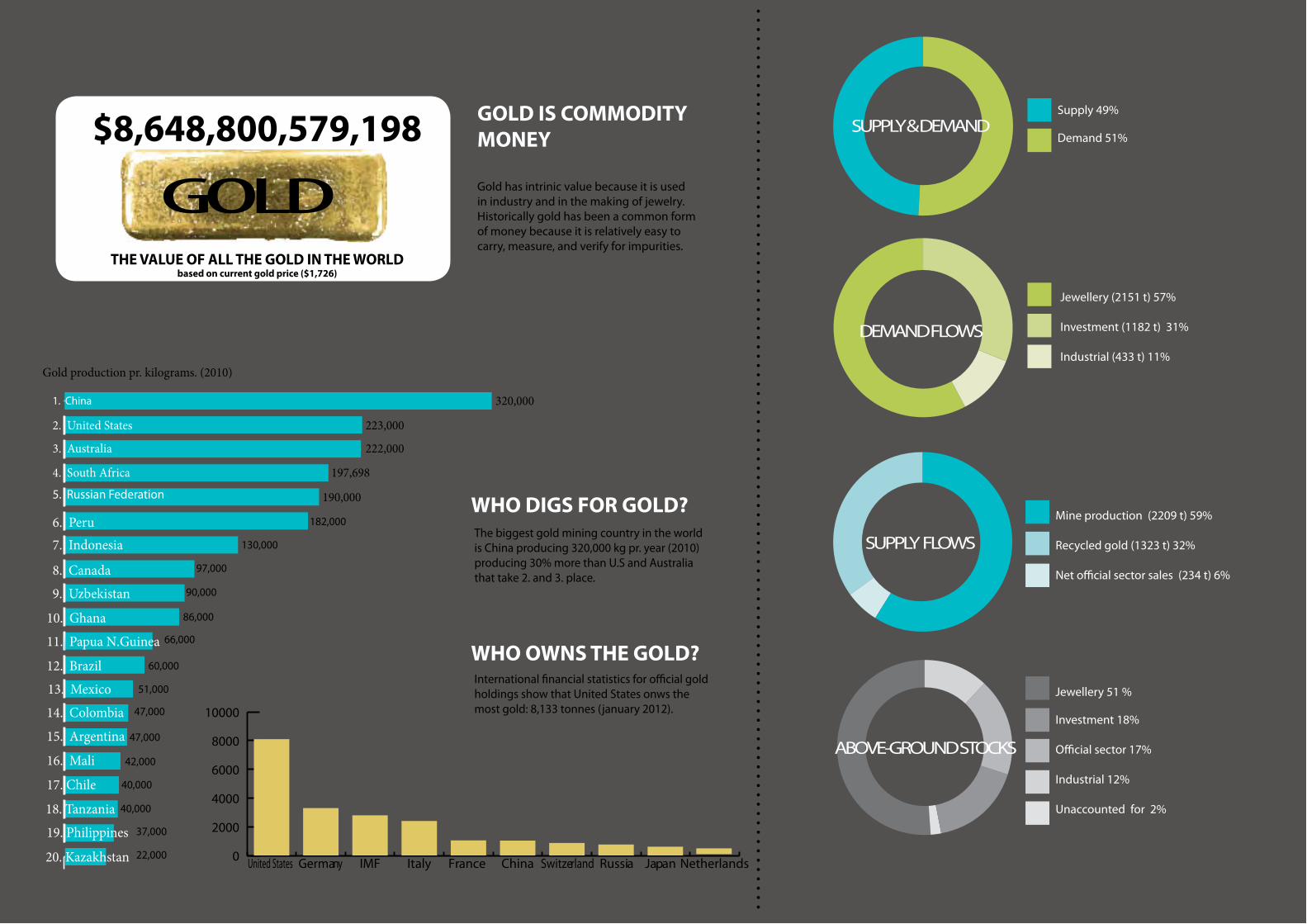

SUPPLY AND DEMAND

Gold demand in the third quarter of 2011 reached 1,053.9 tonnes, an increase of 6% compared to the same period last year. This equates to US$57.7bn, an all-time high in value terms. Demand growth was driven by investment de-mand, which rose by 33% year-on-year to 468.1 tonnes, generating a record quarterly value of US$25.6bn.

Investment demand in Europe reached a record quarterly value of !4.6bn, equating to 118.1 tonnes - a year-on-year increase of 135%. The increase in overall investment demand was all the more impressive given the sharp gold price correction in September, which encouraged a wave of pro"t taking among bar and coin investors. Virtually all markets saw strong double-digit growth in demand for gold bars and coins. Chinese jewellery demand was 13% higher year-on-year at 131.0 tonnes, equivalent to RMB46.0bn. The bulk of this increase was seen in smaller cities as retail chains expanded their networks to meet increasing demand fuelled by rising income levels. China’s growing appetite for gold as a means of investment saw demand for gold bars and coins expand by 24% from year earlier levels to 60.2 tonnes. Jewellery demand in India was sluggish during the seasonally slow months of July and August, compounded by high in#ation and greater volatility in the local gold price. Buying has since recovered slightly with the onset of the fes-tive and wedding season. Overall, Indian jewellery demand in Q3 saw a 26% decline in tonnage, when compared to the same quarter in 2010, to 125.3 tonnes, however yearly demand to the end of September is very close to the record levels seen in 2010.

1. China

3. Australia

2. United States

4. South Africa5. Russian Federation

6. Peru7. Indonesia

8. Canada9. Uzbekistan

10. Ghana11. Papua N.Guinea12. Brazil13. Mexico14. Colombia15. Argentina16. Mali17. Chile18. Tanzania19. Philippines

223,000

222,000

197,698

190,000

182,000

20. Kazakhstan

130,000

97,000

90,000

86,000

66,000

60,000

51,000

47,000

47,000

42,000

40,000

40,000

37,000

22,000

The biggest gold mining country in the world is China producing 320,000 kg pr. year (2010)producing 30% more than U.S and Australia that take 2. and 3. place.

$8,648,800,579,198

THE VALUE OF ALL THE GOLD IN THE WORLD based on current gold price ($1,726)

GOLD

SUPPLY & DEMANDSupply 49%

Demand 51%

DEMAND FLOWS

Jewellery (2151 t) 57%

Investment (1182 t) 31%

Industrial (433 t) 11%

SUPPLY FLOWS

ABOVE-GROUND STOCKS

Mine production (2209 t) 59%

Recycled gold (1323 t) 32%

Net o$cial sector sales (234 t) 6%

Jewellery 51 %

Investment 18%

O$cial sector 17%

Industrial 12%

Unaccounted for 2%

0

2000

4000

6000

8000

10000

NetherlandsJapan RussiaSwitzerlandChinaFrance ItalyIMFGermanyUnited States

International "nancial statistics for o$cial gold holdings show that United States onws the most gold: 8,133 tonnes (january 2012).

GOLD IS COMMODITY MONEY

Gold has intrinic value because it is used in industry and in the making of jewelry. Historically gold has been a common form of money because it is relatively easy to carry, measure, and verify for impurities.

WHO OWNS THE GOLD?

320,000

Gold production pr. kilograms. (2010)

WHO DIGS FOR GOLD?

W

0

100

200

300

400

500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

(Total cash cost US$/oz)

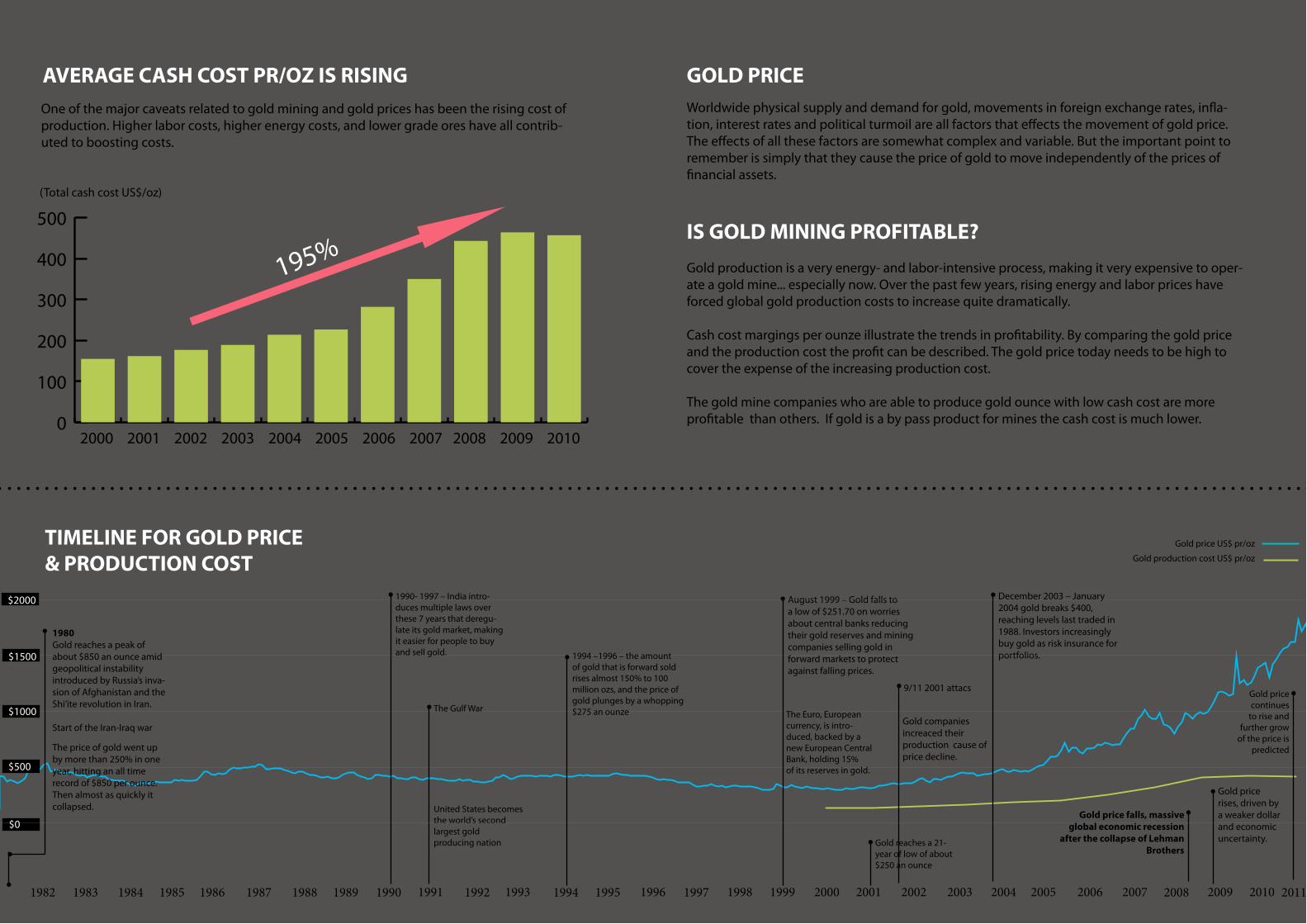

AVERAGE CASH COST PR/OZ IS RISING

Dec 20Dec 2010Dec 2009Dec 2008Dec 2007Dec 2006Dec 2005Dec 2004Dec 2003Dec 2002Des 2001Dec 2000Dec 1999Dec 1998Dec 1997Dec 1996Dec 1995Dec 1994Dec 1993Dec 1992Dec 1991Dec 1990Dec 1989Dec 1988Dec 1987Dec 1986Dec 1985Dec 1984Dec 1983Dec 1982an.82

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

August 1999 – Gold falls to a low of $251.70 on worries about central banks reducing their gold reserves and mining companies selling gold in forward markets to protect against falling prices.

December 2003 – January 2004 gold breaks $400, reaching levels last traded in 1988. Investors increasingly buy gold as risk insurance for portfolios.

Gold price continues

to rise and further grow

of the price is predicted

Worldwide physical supply and demand for gold, movements in foreign exchange rates, in!a-tion, interest rates and political turmoil are all factors that e"ects the movement of gold price. The e"ects of all these factors are somewhat complex and variable. But the important point to remember is simply that they cause the price of gold to move independently of the prices of #nancial assets.

IS GOLD MINING PROFITABLE?Gold production is a very energy- and labor-intensive process, making it very expensive to oper-ate a gold mine... especially now. Over the past few years, rising energy and labor prices have forced global gold production costs to increase quite dramatically.

Cash cost margings per ounze illustrate the trends in pro#tability. By comparing the gold price and the production cost the pro#t can be described. The gold price today needs to be high to cover the expense of the increasing production cost.

The gold mine companies who are able to produce gold ounce with low cash cost are more pro#table than others. If gold is a by pass product for mines the cash cost is much lower.

Gold price US$ pr/oz

Gold production cost US$ pr/oz

TIMELINE FOR GOLD PRICE& PRODUCTION COST

9/11 2001 attacs

One of the major caveats related to gold mining and gold prices has been the rising cost of production. Higher labor costs, higher energy costs, and lower grade ores have all contrib-uted to boosting costs.

GOLD PRICE

195%

The Gulf War

United States becomes the world’s second largest goldproducing nation

The Euro, European currency, is intro-duced, backed by a new European Central Bank, holding 15%of its reserves in gold.

Gold companies increaced their production cause of price decline.

Gold price rises, driven by a weaker dollar and economic uncertainty.

$0Gold price falls, massive

global economic recession after the collapse of Lehman

Brothers

The price of gold went up by more than 250% in one year, hitting an all time record of $850 per ounce. Then almost as quickly it collapsed.

1980Gold reaches a peak of about $850 an ounce amid geopolitical instability introduced by Russia’s inva-sion of Afghanistan and the Shi’ite revolution in Iran.

Start of the Iran-Iraq war

1990- 1997 – India intro-duces multiple laws over these 7 years that deregu-late its gold market, making it easier for people to buy and sell gold. 1994 –1996 – the amount

of gold that is forward sold rises almost 150% to 100 million ozs, and the price of gold plunges by a whopping $275 an ounze

Gold reaches a 21-year of low of about $250 an ounce

$2000

$1500

$500

$1000

W

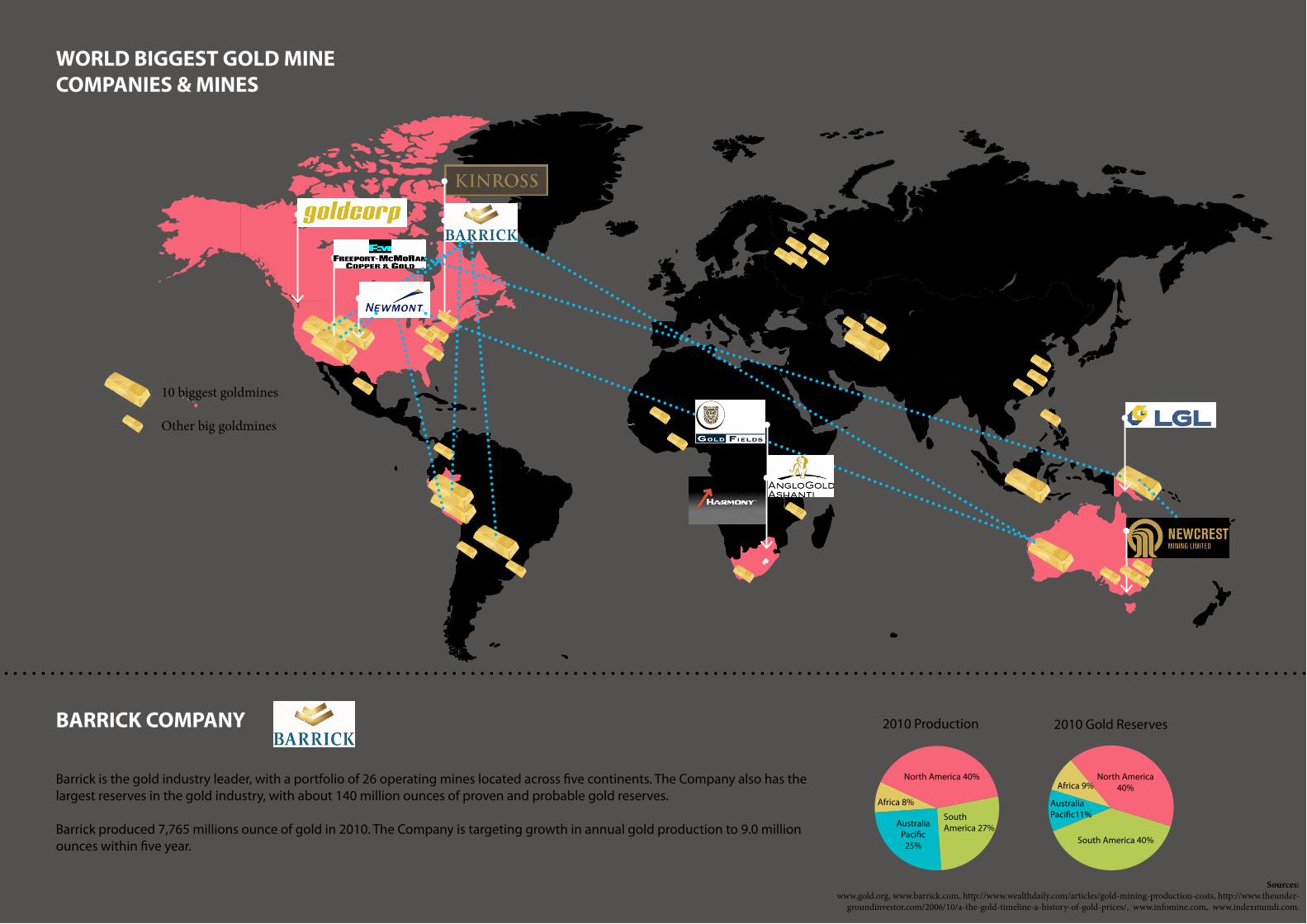

10 biggest goldmines

Other big goldmines

WORLD BIGGEST GOLD MINE COMPANIES & MINES

North America 40% North America 40%

South America 40%

South America 27%Australia

Paci!c25%

AustraliaPaci!c11%

Africa 8%

Africa 9%

2010 Production 2010 Gold ReservesBARRICK COMPANY

Barrick is the gold industry leader, with a portfolio of 26 operating mines located across !ve continents. The Company also has the largest reserves in the gold industry, with about 140 million ounces of proven and probable gold reserves.

Barrick produced 7,765 millions ounce of gold in 2010. The Company is targeting growth in annual gold production to 9.0 million ounces within !ve year.

Sources: www.gold.org, www.barrick.com, http://www.wealthdaily.com/articles/gold-mining-production-costs, http://www.theunder-

groundinvestor.com/2006/10/a-the-gold-timeline-a-history-of-gold-prices/, www.infomine.com, www.indexmundi.com.