the brandfinance® football 50

DESCRIPTION

As Bayern takes the top spot and the Bundesliga challenges its European rivals, read on to discover the key trends shaping football's biggest brands in 2013.TRANSCRIPT

BRANDFINANCE FOOTBALL 50

THE ANNUAL REPORT ON THE WORLD’S MOST VALUABLE FOOTBALL BRANDS | MAY 2013

Fussball’s Coming Home Bayern Becomes Football’s Most Valuable Brand

®

2 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

The BrandFinance® Football 50 is published by Brand Finance plc and is the only study to analyse and rank the top 50 most valuable football clubs by brand value.

Brand Finance plc3rd Floor, Finland House, 56 Haymarket, LondonSW1Y 4RN United KingdomTel: +44 (0) 207 389 9400Fax: +44 (0) 207 389 [email protected]

3 Our Verdict

4 The BrandFinance® Football 50 results

6 Winners & Losers

7 The Top 10: Profiles

14 Top 10 Historical Overview

15 Fussball’s Coming Home: The Bundesliga vs The Premier League

16 Branding: What the Clubs Say

20 Glaze of Glory? Manchester United and The Glazers

21 Warrior Enters the Fight: Kit Supplier Competition Intensifies

22 Treasure Chests: The Growing Value of Shirt Sponsorship

24 Methodology: Brand Value

25 Methodology: Brand Strength

26 Our Services

28 About Brand Finance

29 Contacts

30 Appendix (Full results in GBP, USD & EUR)

Contents

BRANDFINANCE® FOOTBALL 50

BRANDFINANCE FOOTBALL 50

THE ANNUAL REPORT ON THE WORLD’S MOST VALUABLE FOOTBALL BRANDS | MAY 2013

Fussball’s Coming Home Bayern Becomes Football’s Most Valuable Brand

®

MAY 2013 | BRANDFINANCE® FOOTBALL 50 | 3

Our Verdict

Welcome to the BrandFinance® Football 50 2013 report highlighting the world’s most valuable football brands.

• This year’s edition of the BrandFinance® Football 50 sees a new champion, FC Bayern München take the number one spot after a tremendous domestic and European season. On pitch success coupled with some of the strongest financials in sport sees its brand grow to $860m.

• Manchester United FC drops to second place, the departure of Sir Alex Ferguson leaving uncertainty over whether the Red Devils can continue their success without him. Its value falls marginally to $837m, but is still only one of two football brands deserving of an AAA+ brand rating, the strongest rating available.

• Spanish and Italian clubs again see their brand value growth hampered by economic conditions. Despite this, Real Madrid CF is up 4% to $621m. FC Barcelona on the other hand has lost $8m in brand value and is now worth $572m.

• Juventus FC ($180m) and SSC Napoli ($101m) both continued their return to form at the expense of FC Internazionale Milano, which takes another dip after a poor season to $151m, while rivals AC Milan see a less dramatic fall in value to $263m.

• Milan’s teams are struggling with ageing stadia, falling attendances and crowd trouble. Serie A was the only league in Europe to see an average attendance fall for 2012/13 and is desperately in need of a rebrand if it wishes to reignite its global appeal to the levels experienced during the 90s.

• Elsewhere, Turkish and Brazilian brands made great strides thanks to their booming economies and passionate domestic fanbases. Galatasaray AŞ is our highest ranking Turkish team valued at $116m, while SC Corinthians Paulista ($103m) takes the honour of highest ranking non-European club.

• Average brand value growth across the top 50 is a healthy 7%, outpacing the growth rates of most national economies. This shows that top level sport is largely recession proof with almost all clubs reporting solid revenue increases.

• Attendances have remained solid, with many top teams filling their stadiums week-in week-out coupled with healthy season ticket waiting lists. Clubs are not resting on their laurels with all working hard to improve the match-day experience via new technology and upgrades.

• Manchester City FC enjoyed a 10% jump in brand value to $332m despite a disappointing season. A failure to build on last year’s success, despite the highest wage bill in Europe, has seen Italian manager Roberto Mancini shown the door. On

a more positive note however, the club’s pioneering plan to export the brand into the US market (partnering with the New York Yankees to form a new MLS franchise) opens up a whole host of new commercial and fan experiences.

• Beyond Europe, the top 50 contains 5 Brazilian clubs led by Corinthians in 19th place. Whilst revenues in the Brazilian game remain well below European equivalents, the combination of the FIFA World Cup 2014 and 2016 Summer Olympic Games being held in Brazil is driving an influx of investment into the sporting sector which despite recent protests should provide an opportunity for the country to shine on a global platform.

• This year we saw a continued rise in the average price paid by sponsors to be associated with the top 50 clubs. Manchester United’s $559m, seven year agreement with Chevrolet set a new record. Qatar Airlines made its first major mark in sport sponsorship; its offer of $38m per year was enough to tempt Barcelona to let it become the club’s first corporate sponsor in 113 years. Meanwhile rival Gulf airline Emirates continued its longstanding affiliation with the game; it now sponsors four of the top 25 teams. This year’s table sees a more diverse portfolio of sectors taking represented on the shirts of the top 50 as more companies recognise the branding benefits the beautiful game can bring.

• 10 different brands now supply kits to the top 50 clubs in what is now a hotly contested and increasingly technical marketplace. Adidas lead the pack with 18 supplier contracts while Nike follows with 14. Both however are feeling the pressure of new market entrants Warrior and Under Armour.

• These US brands have fuelled an upward trend in kit suppliers’ annual payments. With more brands entering the market, competition is forcing suppliers to pay a premium. The awareness that top tier football provides, combined with the return on investment available from replica sales, mean they are willing to make the investment. Arsenal, Manchester City and Lazio have all recently left long-term supplier relationships to secure more lucrative shirt deals. Both sponsors and suppliers must look carefully before taking the plunge however, ensuring they have carefully calculated the likely uplift in their own brand value from association with the World’s most valuable football club brands.

• Outside the top 50 we have seen some other interesting branding trends with the most extreme being Cardiff City; the ‘bluebirds’ have turned red and adopted the Welsh dragon in order to expand the club’s appeal in Asia.

4 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

BrandFinance® Football 50

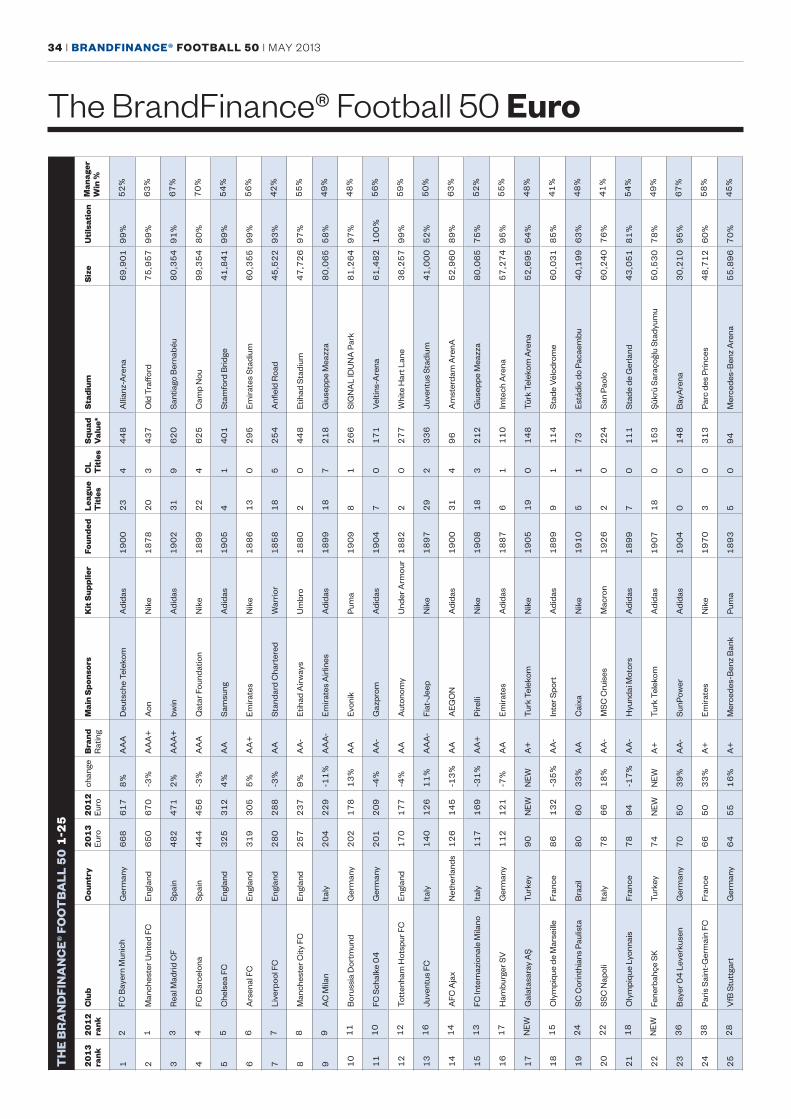

TOP 50 FOOTBALL BRANDS 1-25

Rank 2013 Club Country

Brand Value

2013 (USD M) 2012 (USD M) change (%) Brand Rating

1 FC Bayern Munich

Germany 860 786 9% AAA

2 Manchester United FC

England 837 853 -2% AAA+

3 Real Madrid CF

Spain 621 600 4% AAA+

4 FC Barcelona

Spain 572 580 -1% AAA

5 Chelsea FC

England 418 398 5% AA

6 Arsenal FC

England 410 388 6% AA+

7 Liverpool FC

England 361 367 -2% AA

8 Manchester City FC

England 332 302 10% AA-

9 AC Milan

Italy 263 292 -10% AAA-

10 Borussia Dortmund

Germany 260 227 15% AA

11 FC Schalke 04 Germany 259 266 -3% AA-

12 Tottenham Hotspur FC

England 219 225 -3% AA

13 Juventus FC

Italy 180 160 12% AAA-

14 AFC Ajax

Netherlands 162 184 -12% AA

15 FC Internazionale Milano

Italy 151 215 -30% AA+

16 Hamburger SV

Germany 144 153 -6% AA

17 NEW Galatasaray AŞ

Turkey 116 NEW NEW A+

18 Olympique de Marseille

France 111 168 -34% AA-

19 SC Corinthians Paulista

Brazil 103 77 34% AA

20 SSC Napoli

Italy 101 85 20% AA-

21 Olympique Lyonnais

France 101 120 -16% AA-

22 NEW Fenerbahçe SK

Turkey 95 NEW NEW A+

23 Bayer 04 Leverkusen

Germany 90 64 41% AA-

24 Paris Saint-Germain FC

France 85 64 34% A+

25 VfB Stuttgart

Germany 83 71 18% A+

MAY 2013 | BRANDFINANCE® FOOTBALL 50 | 5

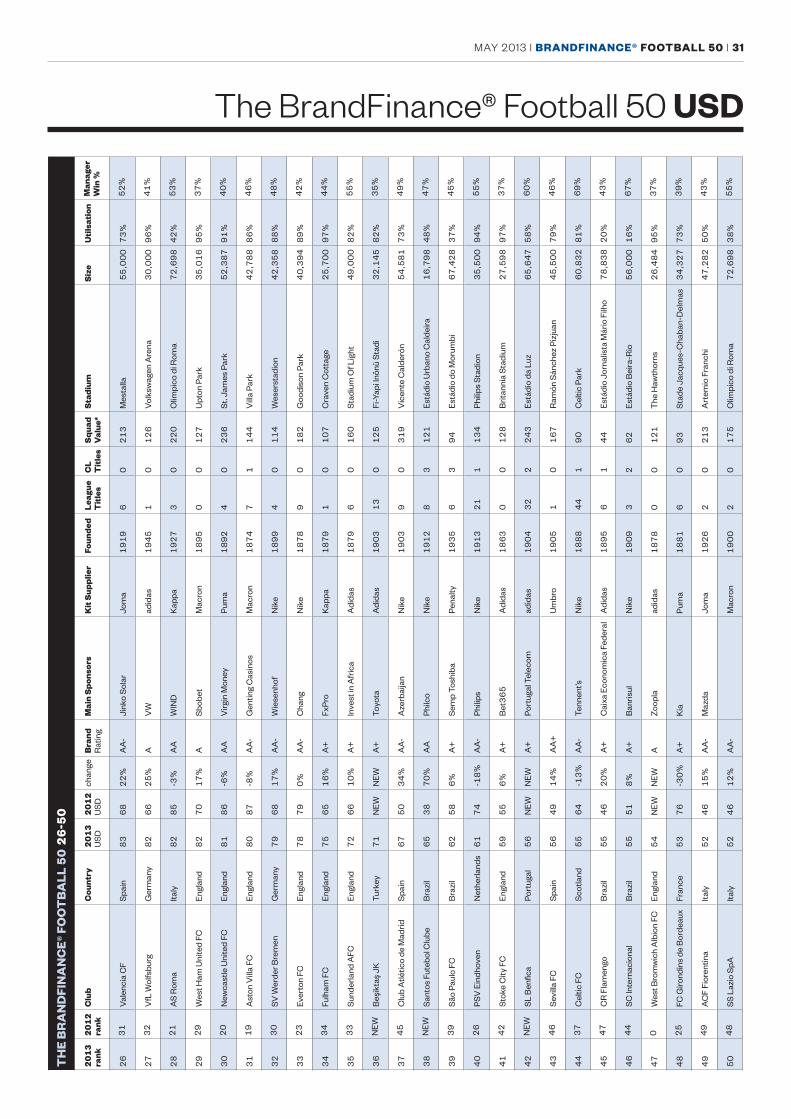

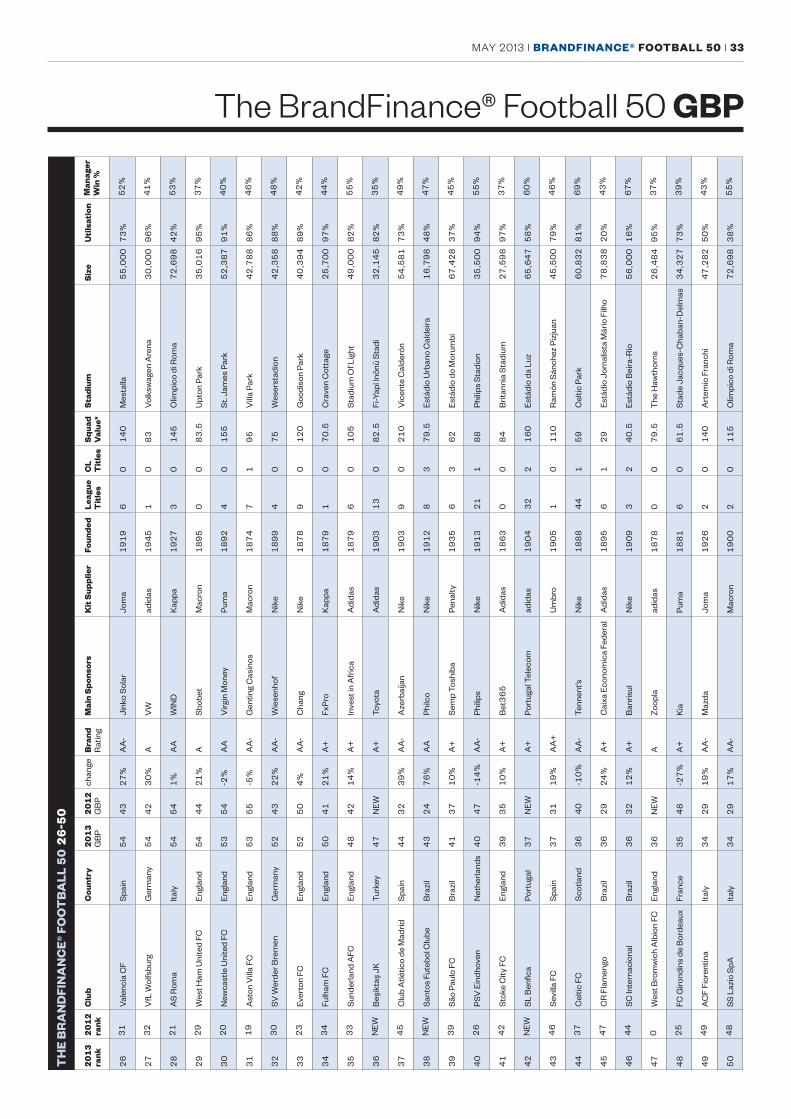

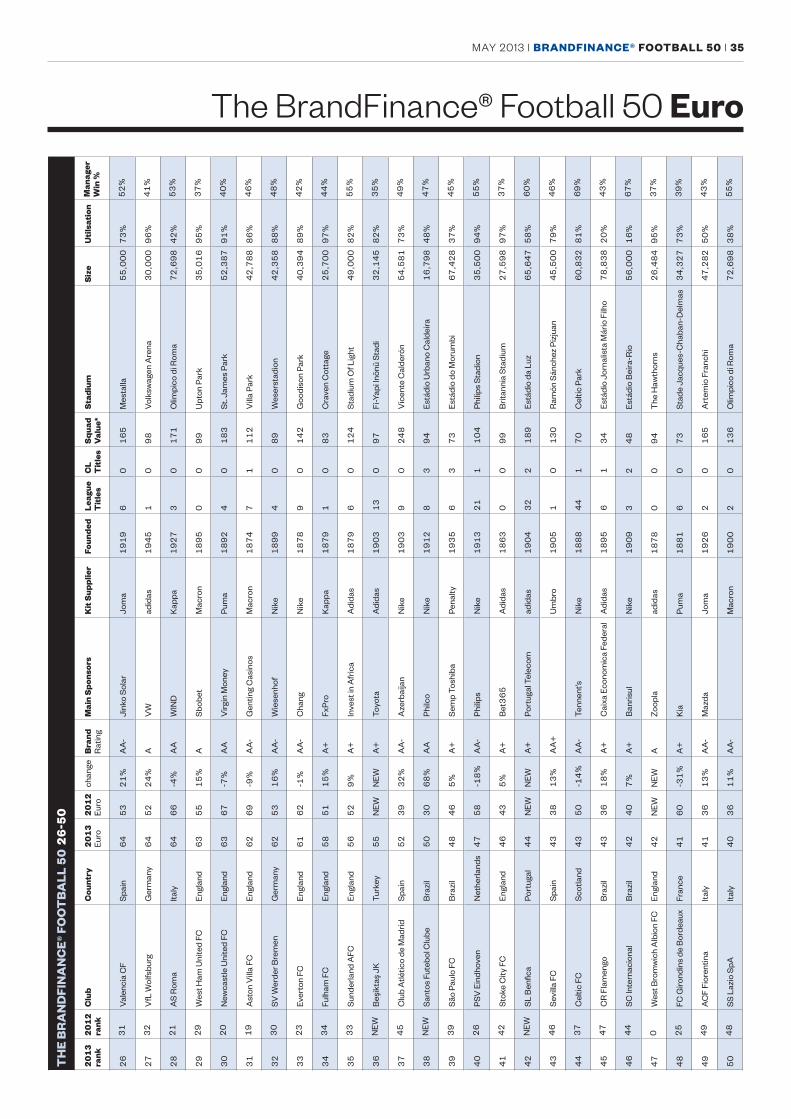

TOP 50 FOOTBALL BRANDS 26-50

Rank 2013 Club Country

Brand Value

2013 (USD M) 2012 (USD M) change (%) Brand Rating

26 Valencia CF

Spain 83 68 22% AA-

27 VfL Wolfsburg

Germany 82 66 25% A

28 AS Roma

Italy 82 85 -3% AA

29 West Ham United FC

England 82 70 17% A

30 Newcastle United FC

England 81 86 -6% AA

31 Aston Villa FC

England 80 87 -8% AA-

32 SV Werder Bremen

Germany 79 68 17% AA-

33 Everton FC

England 78 79 0% AA-

34 Fulham FC

England 75 65 16% A+

35 Sunderland AFC

England 72 66 10% A+

36 NEW Beşiktaş JK

Turkey 71 NEW NEW A+

37 Club Atlético de Madrid

Spain 67 50 34% AA-

38 NEW Santos Futebol Clube

Brazil 65 38 70% AA

39 São Paulo FC

Brazil 62 58 6% A+

40 PSV Eindhoven

Netherlands 61 74 -18% AA-

41 Stoke City FC

England 59 55 6% A+

42 NEW SL Benfica

Portugal 56 NEW NEW A+

43 Sevilla FC

Spain 56 49 14% AA+

44 Celtic FC

Scotland 55 64 -13% AA-

45 CR Flamengo

Brazil 55 46 20% A+

46 SC Internacional

Brazil 55 51 8% A+

47 West Bromwich Albion FC

England 54 NEW NEW A

48 FC Girondins de Bordeaux

France 53 76 -30% A+

49 ACF Fiorentina

Italy 52 46 15% AA-

50 SS Lazio SpA

Italy 52 46 12% AA-

BrandFinance® Football 50

6 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

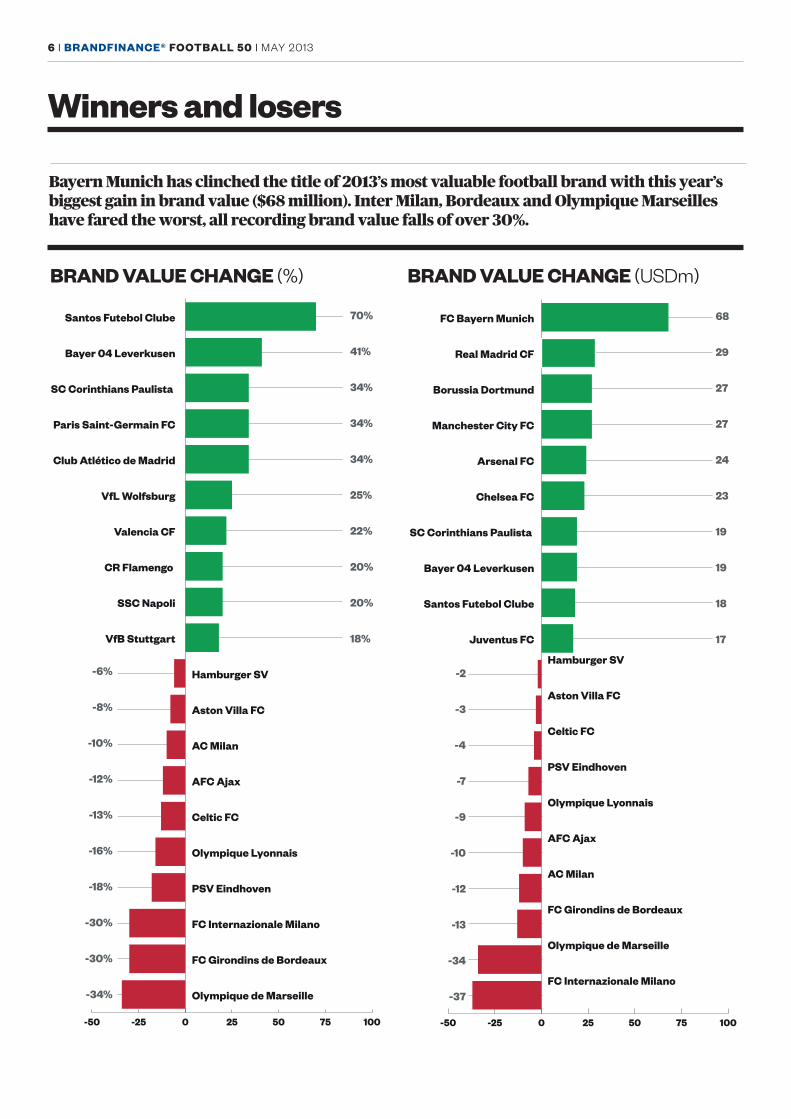

Winners and losers

Bayern Munich has clinched the title of 2013’s most valuable football brand with this year’s biggest gain in brand value ($68 million). Inter Milan, Bordeaux and Olympique Marseilles have fared the worst, all recording brand value falls of over 30%.

-50 -25 0 25 50 75 100

Olympique de Marseille

FC Girondins de Bordeaux

FC Internazionale Milano

PSV Eindhoven

Olympique Lyonnais

Celtic FC

AFC Ajax

AC Milan

Aston Villa FC

Hamburger SV

VfB Stuttgart

SSC Napoli

CR Flamengo

Valencia CF

VfL Wolfsburg

Club Atlético de Madrid

Paris Saint-Germain FC

SC Corinthians Paulista

Bayer 04 Leverkusen

Santos Futebol Clube

Change in brand value ()

70%

41%

34%

34%

34%

25%

22%

20%

20%

18%

-6%

-8%

-10%

-12%

-13%

-16%

-18%

-30%

-30%

-34%

BRAND VALUE CHANGE (USDm)BRAND VALUE CHANGE (%)

-50 -25 0 25 50 75 100

FC Internazionale Milano

Olympique de Marseille

FC Girondins de Bordeaux

AC Milan

AFC Ajax

Olympique Lyonnais

PSV Eindhoven

Celtic FC

Aston Villa FC

Hamburger SV

Juventus FC

Santos Futebol Clube

Bayer 04 Leverkusen

SC Corinthians Paulista

Chelsea FC

Arsenal FC

Manchester City FC

Borussia Dortmund

Real Madrid CF

FC Bayern Munich

Change in brand value ()

68

29

27

27

24

23

19

19

18

17

-2

-3

-4

-7

-9

-10

-12

-13

-34

-37

MAY 2013 | BRANDFINANCE® FOOTBALL 50 | 7

The Top 10: Profiles

Worthy winnersOver the next 6 pages are mini-profiles of the world’s 10 most valuable football brands, starting with this year’s winner FC Bayern München.

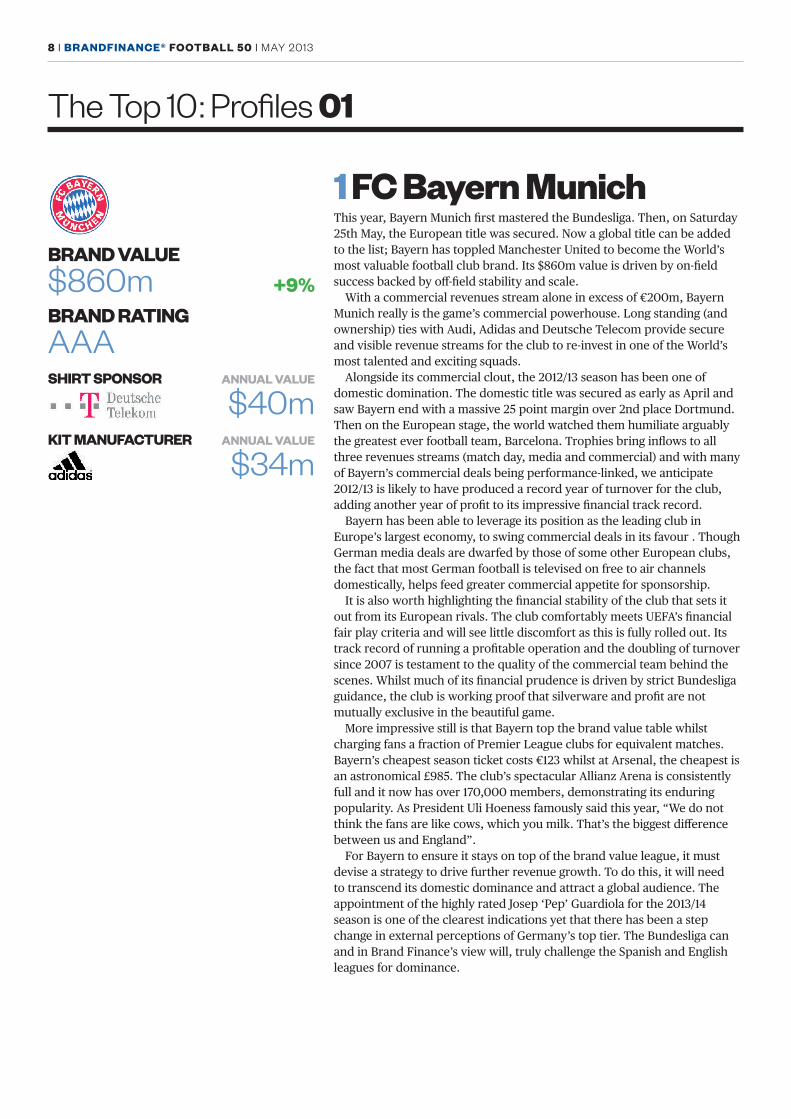

01 FC Bayern Munich Germany2013 USD 860 2012 USD 786 Change 9% Brand rating AAA 2012 rank: 2

02 Manchester United FC England2013 USD 837 2012 USD 853 Change -2% Brand rating AAA+ 2012 rank: 1

03 Real Madrid CF Spain2013 USD 621 2012 USD 600 Change 4% Brand rating AAA+ 2012 rank: 3

04 FC Barcelona Spain2013 USD 572 2012 USD 580 Change -1% Brand rating AAA 2012 rank: 4

05 Chelsea FC England2013 USD 418 2012 USD 398 Change 5% Brand rating AA 2012 rank: 5

06 Arsenal FC England2013 USD 410 2012 USD 388 Change 6% Brand rating AA+ 2012 rank: 6

07 Liverpool FC England2013 USD 361 2012 USD 367 Change -2% Brand rating AA 2012 rank: 7

08 Manchester City FC England2013 USD 332 2012 USD 302 Change 10% Brand rating AA- 2012 rank: 8

09 AC Milan Italy2013 USD 263 2012 USD 292 Change -10% Brand rating AAA- 2012 rank: 9

10 Borussia Dortmund Germany2013 USD 260 2012 USD 227 Change 15% Brand rating AA 2012 rank: 11

BRAND VALUE CHANGE (USDm)

8 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

The Top 10: Profiles 01

1 FC Bayern MunichThis year, Bayern Munich first mastered the Bundesliga. Then, on Saturday 25th May, the European title was secured. Now a global title can be added to the list; Bayern has toppled Manchester United to become the World’s most valuable football club brand. Its $860m value is driven by on-field success backed by off-field stability and scale.

With a commercial revenues stream alone in excess of €200m, Bayern Munich really is the game’s commercial powerhouse. Long standing (and ownership) ties with Audi, Adidas and Deutsche Telecom provide secure and visible revenue streams for the club to re-invest in one of the World’s most talented and exciting squads.

Alongside its commercial clout, the 2012/13 season has been one of domestic domination. The domestic title was secured as early as April and saw Bayern end with a massive 25 point margin over 2nd place Dortmund. Then on the European stage, the world watched them humiliate arguably the greatest ever football team, Barcelona. Trophies bring inflows to all three revenues streams (match day, media and commercial) and with many of Bayern’s commercial deals being performance-linked, we anticipate 2012/13 is likely to have produced a record year of turnover for the club, adding another year of profit to its impressive financial track record.

Bayern has been able to leverage its position as the leading club in Europe’s largest economy, to swing commercial deals in its favour . Though German media deals are dwarfed by those of some other European clubs, the fact that most German football is televised on free to air channels domestically, helps feed greater commercial appetite for sponsorship.

It is also worth highlighting the financial stability of the club that sets it out from its European rivals. The club comfortably meets UEFA’s financial fair play criteria and will see little discomfort as this is fully rolled out. Its track record of running a profitable operation and the doubling of turnover since 2007 is testament to the quality of the commercial team behind the scenes. Whilst much of its financial prudence is driven by strict Bundesliga guidance, the club is working proof that silverware and profit are not mutually exclusive in the beautiful game.

More impressive still is that Bayern top the brand value table whilst charging fans a fraction of Premier League clubs for equivalent matches. Bayern’s cheapest season ticket costs €123 whilst at Arsenal, the cheapest is an astronomical £985. The club’s spectacular Allianz Arena is consistently full and it now has over 170,000 members, demonstrating its enduring popularity. As President Uli Hoeness famously said this year, “We do not think the fans are like cows, which you milk. That’s the biggest difference between us and England”.

For Bayern to ensure it stays on top of the brand value league, it must devise a strategy to drive further revenue growth. To do this, it will need to transcend its domestic dominance and attract a global audience. The appointment of the highly rated Josep ‘Pep’ Guardiola for the 2013/14 season is one of the clearest indications yet that there has been a step change in external perceptions of Germany’s top tier. The Bundesliga can and in Brand Finance’s view will, truly challenge the Spanish and English leagues for dominance.

BRAND VALUE$860m +9%BRAND RATINGAAA SHIRT SPONSOR ANNUAL VALUE

$40mKIT MANUFACTURER ANNUAL VALUE

$34m

MAY 2013 | BRANDFINANCE® FOOTBALL 50 | 9

The Top 10: Profiles 02

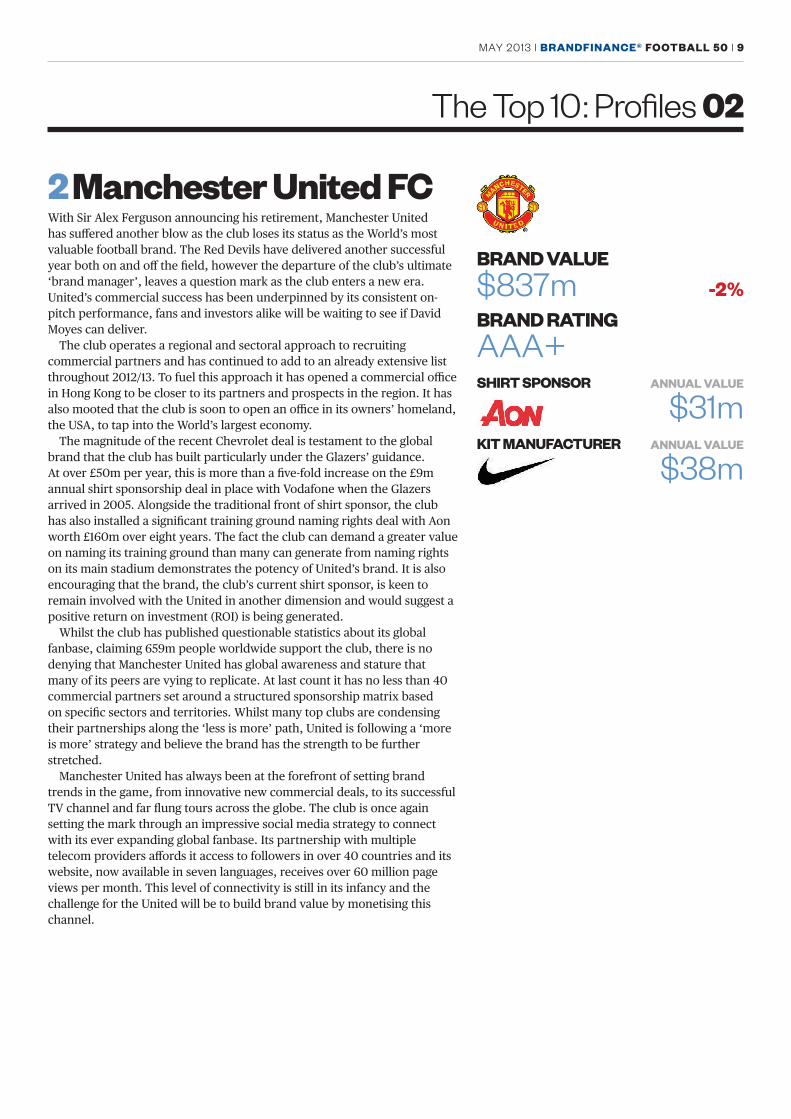

2 Manchester United FCWith Sir Alex Ferguson announcing his retirement, Manchester United has suffered another blow as the club loses its status as the World’s most valuable football brand. The Red Devils have delivered another successful year both on and off the field, however the departure of the club’s ultimate ‘brand manager’, leaves a question mark as the club enters a new era. United’s commercial success has been underpinned by its consistent on-pitch performance, fans and investors alike will be waiting to see if David Moyes can deliver.

The club operates a regional and sectoral approach to recruiting commercial partners and has continued to add to an already extensive list throughout 2012/13. To fuel this approach it has opened a commercial office in Hong Kong to be closer to its partners and prospects in the region. It has also mooted that the club is soon to open an office in its owners’ homeland, the USA, to tap into the World’s largest economy.

The magnitude of the recent Chevrolet deal is testament to the global brand that the club has built particularly under the Glazers’ guidance. At over £50m per year, this is more than a five-fold increase on the £9m annual shirt sponsorship deal in place with Vodafone when the Glazers arrived in 2005. Alongside the traditional front of shirt sponsor, the club has also installed a significant training ground naming rights deal with Aon worth £160m over eight years. The fact the club can demand a greater value on naming its training ground than many can generate from naming rights on its main stadium demonstrates the potency of United’s brand. It is also encouraging that the brand, the club’s current shirt sponsor, is keen to remain involved with the United in another dimension and would suggest a positive return on investment (ROI) is being generated.

Whilst the club has published questionable statistics about its global fanbase, claiming 659m people worldwide support the club, there is no denying that Manchester United has global awareness and stature that many of its peers are vying to replicate. At last count it has no less than 40 commercial partners set around a structured sponsorship matrix based on specific sectors and territories. Whilst many top clubs are condensing their partnerships along the ‘less is more’ path, United is following a ‘more is more’ strategy and believe the brand has the strength to be further stretched.

Manchester United has always been at the forefront of setting brand trends in the game, from innovative new commercial deals, to its successful TV channel and far flung tours across the globe. The club is once again setting the mark through an impressive social media strategy to connect with its ever expanding global fanbase. Its partnership with multiple telecom providers affords it access to followers in over 40 countries and its website, now available in seven languages, receives over 60 million page views per month. This level of connectivity is still in its infancy and the challenge for the United will be to build brand value by monetising this channel.

BRAND VALUE$837m -2%BRAND RATINGAAA+ SHIRT SPONSOR ANNUAL VALUE

$31mKIT MANUFACTURER ANNUAL VALUE

$38m

10 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

The Top 10: Profiles 03, 04

3 Real Madrid CFThe departure of the ‘Special One’, Jose Mourinho, caps the end of a disappointing season for Real Madrid, leaving it stuck in third place in the BrandFinance® Football 50. Whilst the 2011/12 season saw Real generate the largest revenues in the game (€513m), the club’s brand value has been constrained by Spain’s economic woes. The distribution of media rights in La Liga continues to be negotiated individually, although this is set to move to a collective basis shortly, which will squeeze Real Madrid’s media income. The club has expressed an interest in increasing the match-day and commercial revenue streams to help continue its growth.

Redevelopment plans are currently being tendered to transform the Bernabeu, with club President Florentino Perez stating, “I want a stadium that doesn’t look like a stadium and is profitable”. The drive will be to not only provide an improved match-day experience but create sources of revenue that can be generated every day of the week.

Away from the field, the club operates an expanding and very successful merchandising operation, selling over 1.5 million replica shirts last season alone. For the 4th consecutive summer the team will complete a tour of the US, nurturing a strong following in both North and South America. Mourinho tested the Real Madrid ‘blue book’ during his reign and has since departed to once again take up the reins at Chelsea. Real meanwhile, can ill afford another under-par season and the appointment of a successful new manger will be crucial to maintaining the club’s top three standing. The prospect of reclaiming the title of World’s most valuable football brand, last held in 2010, seems a distant prospect for now.

BRAND VALUE$621m +4%BRAND RATINGAAA+ SHIRT SPONSOR ANNUAL VALUE

$30mKIT MANUFACTURER ANNUAL VALUE

$39m

4 FC BarcelonaFC Barcelona’s brand value remained stagnant this year as following the end of Pep Guardiola’s trophy-filled golden era. The Catalans will be hoping the signing of the hugely marketable Brazilian superstar Neymar will follow in the footsteps of Maradona, Cruyff and Messi, who have made the club a multinational institution. It is a tantalising prospect for any football fan to see two of the World’s most exciting talents, Messi and Neymar, playing together in the same team.

Although Barca won La Liga this season, that victory was overshadowed by a failure to reach the Champions League or Copa Del Rey final. The club missed out on the rewards of additional trophies and so the players and coaching staff forfeited bonuses of €12m. Under the financial stewardship of Javier Faus and Sandro Rosell, FC Barcelona have been able to embark on a successful strategy of cutting costs and securing long term partners such as Audi, Coca Cola and Movistar in addition to kit and shirt sponsorship from Nike and the Qatar Foundation. Impressively they have managed this without compromising their football on the pitch. All these elements combined resulted in FC Barcelona producing an historic €48m profit.

The Nou Camp, Europe’s largest football stadium, has a capacity of 98,787, with average attendance figures ranging between 79,000 and 84,000. However, despite revenue growth 4.5% this year to almost €494m, Barcelona continues to lag behind Real Madrid and is the only one of the ‘Big Four’ in the BrandFinance® Football 50 never to have been named as football’s most valuable brand.

BRAND VALUE$572m -1%BRAND RATINGAAA SHIRT SPONSOR ANUAL VALUE

$38mKIT MANUFACTURER ANNUAL VALUE

$46m

MAY 2013 | BRANDFINANCE® FOOTBALL 50 | 11

The Top 10: Profiles 05, 06

5 Chelsea FCChelsea has enjoyed a 5% jump in brand value following Champions League and, more recently, Europa League success, which boosted all three revenue streams. High staff turnover has continued however, with the manager count during the Abramovich reign now in double digits. This continued managerial merry-go-round along with its limited stadium capacity is weighing on the Chelsea’s ability to challenge the BrandFinance® Football 50’s ‘Big Four’.

Whilst the club has lacked consistency on the pitch, it has enjoyed great stability with its long standing commercial partners Adidas and Samsung. Alongside these global brands it has added Delta, Gazprom, Audi and more recently Singha Beer, demonstrating the increasingly global appeal of the Chelsea brand. The club also has in place an innovative branding partnership with F1 team Sauber, focusing on ways to enhance sporting and business performance. This includes the exchange of knowledge in sport science, launching joint commercial initiatives, merchandising, events, marketing and linked sponsorship opportunities. We expect to see more collaborations of this manner throughout football as different sports recognise the synergies and commonalities that exist.

BRAND VALUE$418m +5%BRAND RATINGAA SHIRT SPONSOR ANNUAL VALUE

$21mKIT MANUFACTURER ANNUAL VALUE

$15m

6 Arsenal FCWhilst Arsenal endured another trophy-less year, off the pitch its fortunes have been more impressive. The club has been criticised in recent years for its poor commercial revenues relative to its peers. However, earlier this month it announced a record breaking kit deal with Puma. Reported to be worth £30m a year, the deal was enough to see the Gunners end a 20 year alliance with Nike. In addition, significantly increased extension of shirt sponsorship and naming rights has been agreed with Emirates Airlines through to 2019. The club now needs to feed its increased revenues into on pitch talent to end its eight year trophy drought.

The Emirates Stadium continues to sell out and be one of the highest yielding stadia in the world; once again the stadium will host a number of events during the summer football break that will bring in ancillary revenues and act as a touch-point for the brand to new consumers. Arsenal is unique in that match-day revenues continue to be its largest income stream.

Speculation is still rife about a potential takeover approach for the club, either from one of its current wealthy shareholders or an external consortium. With its listed shares at an all-time high, valuing the club at just over £1bn, it would take a brave investor to see where they could eke out a return.

BRAND VALUE$410m +6%BRAND RATINGAA+ SHIRT SPONSOR ANNUAL VALUE

$8mKIT MANUFACTURER ANNUAL VALUE

$20m

12 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

The Top 10: Profiles 07, 08

7 Liverpool FCDespite a very slight brand value fall after another disappointing year on the field, Liverpool is backed by an increasingly solid commercial team and experienced US owners. With a brand new shirt supplier, the 2012-13 season saw the first evidence of the club’s impressive deal with new market entrant Warrior. This deal saw Liverpool move away from a 22 year relationship with Adidas and take a gamble on Warrior’s first foray into the ultra competitive football apparel market and away from its lacrosse and hockey roots. However, whilst the deal alone represents a 100% increase in value, it also opens the club up to greater branded merchandise opportunities previously contracted out in the Adidas deal.

Liverpool’s tremendous heritage has not gone unnoticed by kit supplier Warrior. Drawing inspiration from Liverpool’s 1964/65 kit they have reintroduced the iconic yellow Liver Bird emblem last seen on the shirt in 1985 during the club’s golden era. Football clubs tend to move slowly when it comes to visual identity changes and it speaks positively of Liverpool and Warrior’s relationship that they recognise the opportunity and have the conviction to make such a change.

Despite the shrewd business and marketing minds now steering the club, Liverpool must return to the European stage to drive all three revenues streams, and equally push on with the development of Anfield to tap into the great match-day yields available from such a rich heritage and loyal fans.

8 Manchester City FCWinning no major trophies, losing in the final of the FA cup to underdogs Wigan and a disappointing Champions League outing led to the sacking of Roberto Mancini. The fact it happened on the anniversary last year’s of Premier League title confirmation, shows the strong desire of the Abu Dhabi based owners to turn things around. With one of the largest wage bills in Europe, the club needs on pitch success to drive all three revenue streams and make Man City a sustainable business operation; this will soon become compulsory as Financial Fair Play kicks in.

Whilst match-day and media revenues are largely dictated by on-field activities, City has been frantically trying to catch up with its neighbours to boost commercial income, recently opening a commercial office in the centre of London, akin to their red rivals. Long term, lucrative deals are currently in place with Etihad for naming rights and shirt sponsorship, as well as a new kit supplier partnership with Nike worth £12m per year being rolled out for the 2013/14 season. Outside these traditional sponsorship avenues, the club has made the pioneering move of acquiring the rights to

Major League Soccer’s 20th expansion franchise. Whilst the deal has only just been announced and full details of ‘NYCFC’ (to be launched in cooperation with the New York Yankees in 2015) are yet to emerge, it shows the commitment of the owners of Manchester City to take the brand global and become ‘noisy neighbours’ both on and off the pitch.

BRAND VALUE$361m -2%BRAND RATINGAA SHIRT SPONSOR ANNUAL VALUE

$31mKIT MANUFACTURER ANNUAL VALUE

$38m

BRAND VALUE$332m +10%BRAND RATINGAA- SHIRT SPONSOR ANNUAL VALUE

$31mKIT MANUFACTURER ANNUAL VALUE

$40m

MAY 2013 | BRANDFINANCE® FOOTBALL 50 | 13

The Top 10: Profiles 09, 10

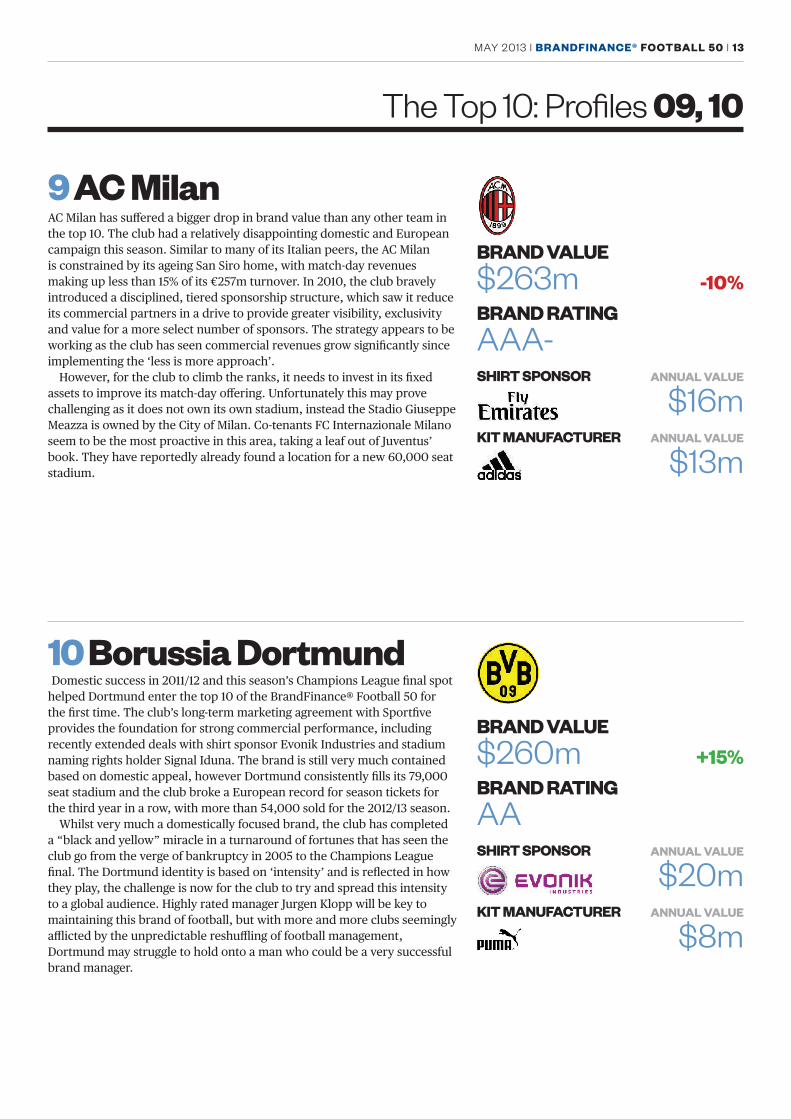

9 AC MilanAC Milan has suffered a bigger drop in brand value than any other team in the top 10. The club had a relatively disappointing domestic and European campaign this season. Similar to many of its Italian peers, the AC Milan is constrained by its ageing San Siro home, with match-day revenues making up less than 15% of its €257m turnover. In 2010, the club bravely introduced a disciplined, tiered sponsorship structure, which saw it reduce its commercial partners in a drive to provide greater visibility, exclusivity and value for a more select number of sponsors. The strategy appears to be working as the club has seen commercial revenues grow significantly since implementing the ‘less is more approach’.

However, for the club to climb the ranks, it needs to invest in its fixed assets to improve its match-day offering. Unfortunately this may prove challenging as it does not own its own stadium, instead the Stadio Giuseppe Meazza is owned by the City of Milan. Co-tenants FC Internazionale Milano seem to be the most proactive in this area, taking a leaf out of Juventus’ book. They have reportedly already found a location for a new 60,000 seat stadium.

10 Borussia DortmundDomestic success in 2011/12 and this season’s Champions League final spot

helped Dortmund enter the top 10 of the BrandFinance® Football 50 for the first time. The club’s long-term marketing agreement with Sportfive provides the foundation for strong commercial performance, including recently extended deals with shirt sponsor Evonik Industries and stadium naming rights holder Signal Iduna. The brand is still very much contained based on domestic appeal, however Dortmund consistently fills its 79,000 seat stadium and the club broke a European record for season tickets for the third year in a row, with more than 54,000 sold for the 2012/13 season.

Whilst very much a domestically focused brand, the club has completed a “black and yellow” miracle in a turnaround of fortunes that has seen the club go from the verge of bankruptcy in 2005 to the Champions League final. The Dortmund identity is based on ‘intensity’ and is reflected in how they play, the challenge is now for the club to try and spread this intensity to a global audience. Highly rated manager Jurgen Klopp will be key to maintaining this brand of football, but with more and more clubs seemingly afflicted by the unpredictable reshuffling of football management, Dortmund may struggle to hold onto a man who could be a very successful brand manager.

BRAND VALUE$263m -10%BRAND RATINGAAA- SHIRT SPONSOR ANNUAL VALUE

$16mKIT MANUFACTURER ANNUAL VALUE

$13m

BRAND VALUE$260m +15%BRAND RATINGAA SHIRT SPONSOR ANNUAL VALUE

$20mKIT MANUFACTURER ANNUAL VALUE

$8m

14 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

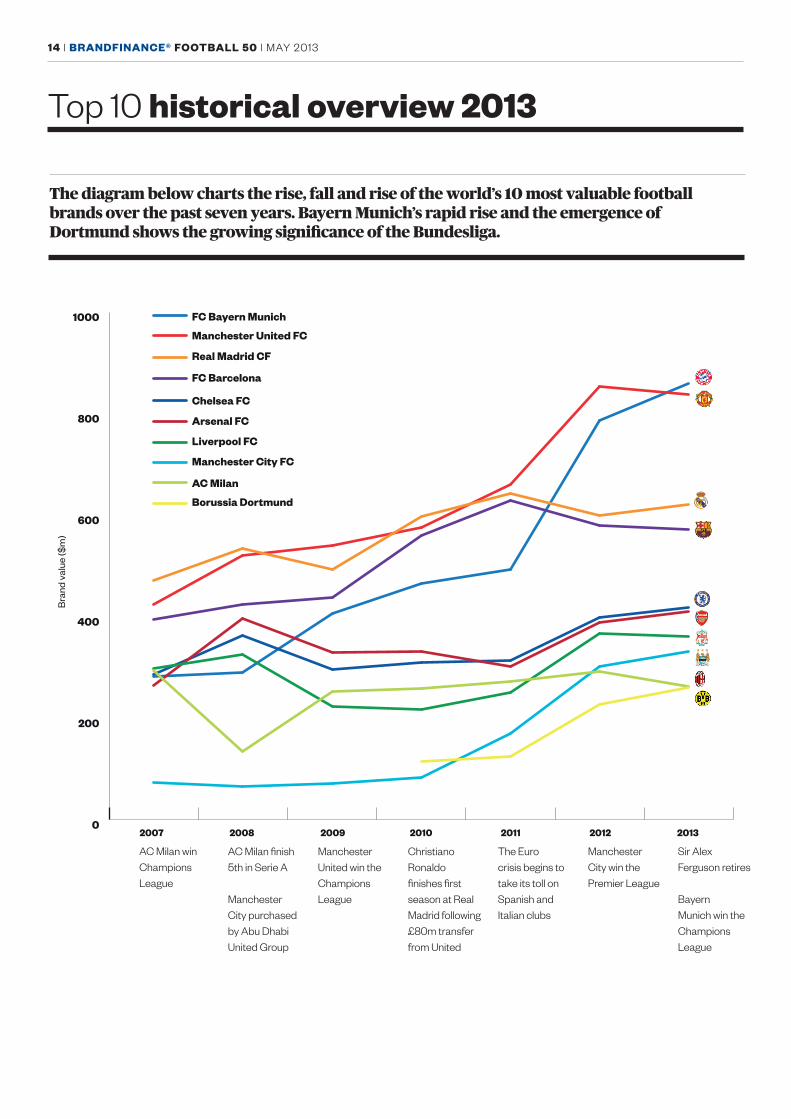

Top 10 historical overview 2013

The diagram below charts the rise, fall and rise of the world’s 10 most valuable football brands over the past seven years. Bayern Munich’s rapid rise and the emergence of Dortmund shows the growing significance of the Bundesliga.

0

200

400

600

800

1000 FC Bayern Munich

Manchester United FC

Real Madrid CF

FC Barcelona

Chelsea FC

Arsenal FC

Liverpool FC

Manchester City FC

AC Milan

Borussia Dortmund

Bra

nd v

alue

($m

)

2007 2008 2009 2010 2011 2012 2013

AC Milan finish 5th in Serie A

Manchester City purchased by Abu Dhabi United Group

Manchester United win the Champions League

Christiano Ronaldo finishes first season at Real Madrid following £80m transfer from United

The Euro crisis begins to take its toll on Spanish and Italian clubs

Manchester City win the Premier League

Sir Alex Ferguson retires

Bayern Munich win the Champions League

AC Milan win Champions League

MAY 2013 | BRANDFINANCE® FOOTBALL 50 | 15

Fussball’s Coming Home: The Bundesliga vs The Premier LeagueWith UEFA’s Financial Fair Play soon to curb the advantages given to clubs currently treated as billionaires’ playthings, profit generation is only set to become more important. Commercial success allows clubs to sustain on-pitch performance through the acquisition of better players, more experienced staff and capital expenditure on training facilities. In turn, victories on the field reinforce financial success by attracting richer sponsors, driving sales of merchendise and boosting demand for tickets. A club that is successful both as a business and as a sporting endeavour is a force to be reckoned with and the Bundesliga may have found the formula to achieve that perfect balance.

14 of the Bundlesliga’s 18 clubs were in the black in 2012, with an overall profit for the Bundesliga of €55m, based on total revenues of €2.1bn. Over the same period the English Premier League (EPL) made a staggering €245m loss despite generating €2.8bn of revenue. The Bundesliga has fostered its profitability through strict cost control; only 38% of total income goes to players and coaches whereas in the EPL the figure is far greater at 64%.

Ticket prices in the Bundesliga are low, with the cheapest average ticket costing approximately €12. The low ticket prices are a matter of policy for German football and purposefully kept low, unlike in the EPL where free market supply and demand means prices are on average three time higher. These low ticket prices, coupled with large, modern stadia have allowed the German top division to attract the biggest crowds over a sustained period of any league in the world. Average attendances of 45,000 at Bundesliga games far outnumber the 34,000 attending EPL matches.

However, despite the record attendances, the low prices are limiting match-day revenues, forcing German

Bundesliga English Premier League

Year formed 1963 1992

Number of Clubs 18 20

Revenue Data

Total League Revenue, Financial Year 2011 (USD m) 3,349 6,022

Average Club Revenue, Financial Year 2011 (USD m) 186 301

European rank (based on total league revenue) 4 1

Average spend on wages as % of revenue 52% 68%

Player Data

Total Player Transfer Value (USD m) 2,468 4,388

Average squad value (USD m) 137 219

Foreign player % 49% 65%

Average age 24.80 27.00

Football Performance Data

Champions League Titles 12 7

UEFA Country Coefficient 2012/13 79.328 82.677

European rank (based on UEFA coefficient) 3 2

Attendance Data’

Average Ticket Price 2011/12 (USD) 29.81 43.15

Average Attendance (2011/12) 45,116 34,600

Total Attendance (2011/12) 13,805,462 13,148,133

Largest Attendance (2011/12) 80,521 75,387

European rank (based on UEFA coefficient) 1 2

clubs to concentrate on leveraging their brand elsewhere. German clubs historically have formed close relationships with local businesses and as the German economy has grown these businesses have become huge global corporations, better able to support their sponsored team. Bayern München has the highest reported commercial revenues of any club in the world.

Broadcasting is the only revenue stream where the Bundesliga serious lags behind its English counterpart and, unlike the slight hit to match-day revenue from cheap tickets, this is not by choice. The EPL derives a third of its viewers from Asia and a quarter from Africa and the Middle East, allowing the league to distribute over €1.3bn in broadcasting

revenue to its clubs. By comparison the Bundesliga only generated €519m last year.

If trends continue, German club football will become better recognised on the global stage. The all German Champions League final and an internationally renowned, foreign coach, in the shape of Pep Guardiola, entering the league are early indicators of the step change in global perceptions to come. With this increasing recognition comes an opportunity to patch up poor broadcasting deals with foreign markets. Once this is fixed and incorporated into the financially responsible model of German football, the Bundesliga will truly be able to challenge the EPL on a level playing field.

16 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

How many people do you have working in your marketing/brand team? Do you have more than one office?Juventus: We have no specific marketing team but rather a commercial team of nine people, covering a range of areas from merchandise to marketing the stadium to the brand. At Juventus we do all our marketing activities in house, unlike most other Italian clubs. We feel this gives us greater control and a better connection with our fans.Tottenham: There are eight members of the marketing team, including two digital specialists. The team are all based at the stadium.

Do you benchmark your brand value in any way?Juventus: We feel it would be too subjective to do it ourselves; we rely on information from Brand Finance and the market.Tottenham: Yes. Our main benchmarks are based around tangible indicators of brand value, i.e. growth in commercial revenues, merchandising and licensing, fan base development, global TV audiences for our matches, estimated size of our fan base in key territories, volume of engaged fans across all our channels globally and the level of reach and increase in transacting supporters.

Branding: What the Clubs Say Commercial and on-pitch are intertwined, so in order to remain competitive football clubs must understand the significance and value of the brands they control. We spoke to Juventus’ Commercial Director Francesco Calvo, Tottenham’s Head of Marketing Emma Taylor and a spokesperson from Arsenal on how they monitor, leverage, protect and plan to extend their brands.

‘10 years ago sponsors and partners were primarily concerned with buying visibility. Today sponsors are more concerned with gaining access to content and fans.’Francesco Calvo, Juventus FC Commercial Director

MAY 2013 | BRANDFINANCE® FOOTBALL 50 | 17

Do you have a documented set of brand guidelines/values?Juventus: In 2006/07 we changed the logo; we are continually trying to adapt the brand to keep it modern. In terms of intellectual property it is Nike who is reliant on us to protect the IP through our role as ‘Guardians of the brand’.Tottenham: Yes. The Club has a comprehensive set of guidelines that set out our brand proposition, values and tone of voice and outline a clear narrative of what our brand stands for. Our brand’s visual identity has comprehensive guidelines around the use of our badge as well as how we achieve a cohesive brand look and feel across every club touch point. This is combined with a clear brand protection strategy that ensures our marks and IP are protected and where any potential infringements are carefully monitored.Arsenal: Arsenal Football Club is synonymous with history, tradition and success. We believe that the Club exists to make our fans proud wherever they are in the world and however they choose to follow us. Everyone that works for the Club understands that we will fulfil our goal of making fans proud by being together, always moving forward and doing things ‘The Arsenal Way’. This final element is a key ingredient of who we are. It’s about thinking about others, getting the detail right and going above and beyond expectations.

What do you view as key territories for further brand growth?Juventus: The focus has always been Italy, however we can now look to engage new markets in new ways. In the

future we will be looking to local partners in Japan, China, India, Australia, Indonesia and the USA. This summer we will be competing in the Guinness International Champions Cup in the USA along with Milan and Inter. This allows us to promote the Serie A league together as opposed to one club going to China, one club going to Australia and the message being lost. We work with Serie A to improve the image of the league overall. In my opinion the Italian league remains an entertaining league due to the number of top sides that compete. The German Bundesliga and the Spanish La Liga are dominated by two teams whereas in Serie A you have Juventus, Inter, Milan, Roma, Lazio and Napoli who all compete for top honours.Tottenham: Our primary focus outside the domestic market is the USA and Asia. We have seen significant growth in the USA following our 2012 Tour. Our supporters’ club network has grown by around 40% in the last season.Arsenal: As a genuinely global club with millions of fans all over the world, we have a major focus in a number of different overseas territories, with our most notable growth currently across Africa and Asia.

Do you have a unified return on investment (ROI) metric that you use with all commercial partners/sponsors?Juventus: 10 years ago sponsors and partners were primarily concerned with buying visibility. Today sponsors are more concerned with gaining access to content and fans.Tottenham: Yes, in that we commission independent analysis

‘Everyone that works for the Club understands that we will fulfil our goal of making fans proud by being together, always moving forward and doing things ‘The Arsenal Way’.’Arsenal Football Club

18 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

from trusted industry sources in order to put a valuation on both the tangible and intangible elements of a partner’s package of rights. We use current market media, brand valuation data and measures to put values on each element of the partnership, for example; media, hospitality and ticketing, event and facility usage, corporate real estate, merchandise etc. In addition we use accepted industry methodologies to quantify the brand value to a partner through brand awareness and benefit of association impact, brand stand out and rarity value, promotional rights and ‘money can’t’ opportunities.

How do you balance the dual role of fans as both customers from whom you must make money and supporters/brand ambassadors?Juventus: The 1st priority is that the team wins. We work to develop a close relationship with the fans and hope that continued on the pitch success will deliver financial rewards in the future. Tottenham: Our aim is to bring all our fans closer to the club, to provide a sense of belonging and make them feel part of the club. First and foremost it is about creating ways for fans to engage and interact with the club whatever their

desired level of involvement and ultimately aim to nurture a one-to-one relationship with each and every Spurs fan. The growth in social media and digital channels allow us to extend our reach and open up new opportunities to attract new fans and inspire advocacy from existing fans. If we achieve this, the ability to monetise support is a seamless outcome of engagement whether it is direct transactions or value for our partners or broadcasters.Arsenal: We know that as a club we have an avid following all over the world and while the vast majority will never make it to an actual Premier League game, our challenge is to engage with their passion for Arsenal and make all supporters feel a part of the club wherever they are.

The primary objective is to have as many supporters as possible regularly engaging with the club across a number of different platforms, whether that’s directly through fan events and activities tied in to our Tour, or through digital media. Once you have established a conversation with those fans and understand their interests in more detail (something we are developing extensively through investment in our Customer Relationship Management (CRM) system), it is easier for the club to interact on an individual basis and develop potential commercial revenue streams.

‘What we do off the pitch is also important in determining our brand values and gaining new supporters, so on and off-pitch activities are mutually supportive.’Emma Taylor, Tottenham Hotspur FC Head of Marketing

MAY 2013 | BRANDFINANCE® FOOTBALL 50 | 19

How much impact can off-pitch activities have when compared to the effect of on-pitch success?Tottenham: What we do off the pitch is also important in determining our brand values and gaining new supporters, so on and off-pitch activities are mutually supportive. By way of example, we are at the forefront of charitable efforts and CSR through our Tottenham Hotspur Foundation, which is dedicated to utilising the power of football to engage young people and create life changing opportunities. The Foundation runs a vast number of programmes which are fully supported by the players and coaching staff, who attend events on a weekly basis. This has earned the club a reputation for being responsible, caring and inspiring. Our global coaching programmes also take the ‘Tottenham style’ of play to grass roots football at schools and colleges. Everything we do is guided by our core principles. Arsenal: In our opinion, the two need to work in tandem to drive real fan engagement and brand value. We know that supporter pride is driven primarily by success on the pitch and this means winning trophies. At Arsenal, we are also proud that our style of play, our focus on developing youth talent, our magnificent stadium, our broader contribution in the community and our self-financing approach helps us to

stand out amongst the crowd and provide additional sources of pride and recognition.

Players are obviously crucial to your image, how do you manage the risks that they may personally damage the club’s brand?Juventus: There was a Juventus before them and there will be a Juventus after them, the club is more important than any one player.Tottenham: The players have a duty to represent the Club in the best way at all times and all are made aware of this responsibility. We constantly liaise with the players regarding new trends and the best ways to communicate.Arsenal: The players are undoubtedly the club’s primary asset and we work hard to ensure that they, like the rest of the club’s staff, adhere to our vision and values both on and off the pitch. The growth in digital and social media means that many players now interact directly with supporters, and while this presents its challenges, we are able, through consistent engagement and comprehensive media training, to provide the players with clear parameters, whilst using their individual appeal and profile to enhance and support the club’s own initiatives.

20 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

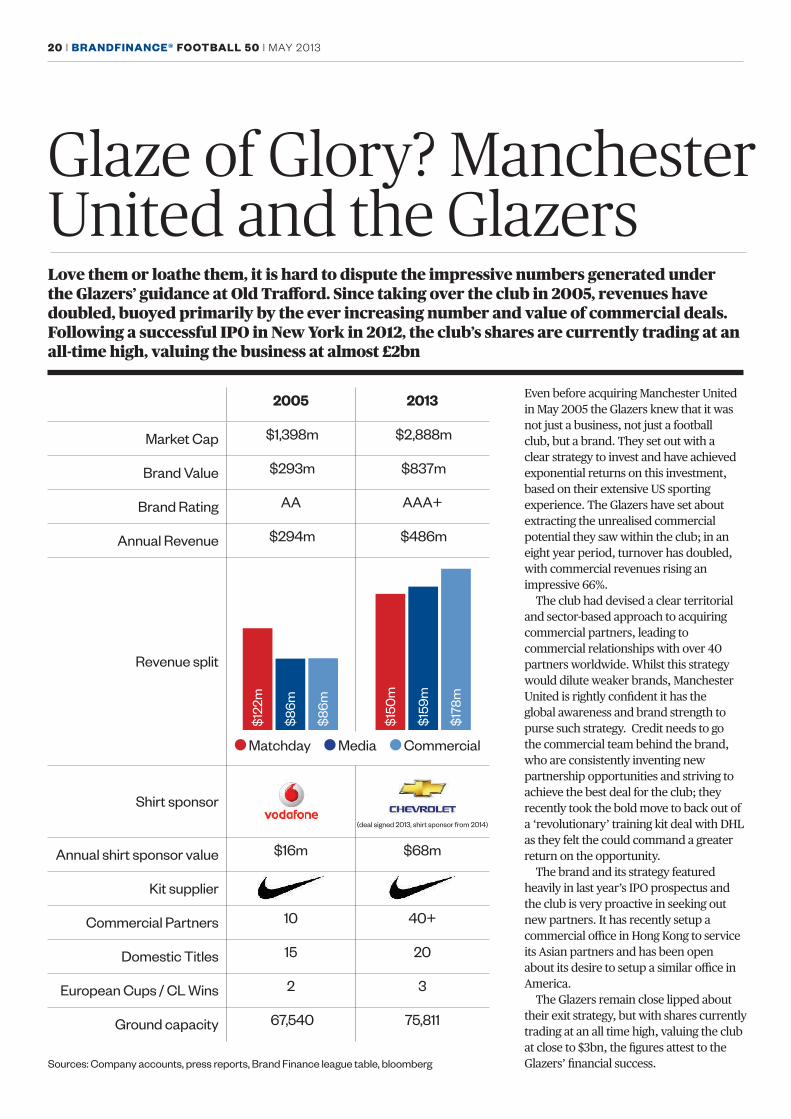

Glaze of Glory? Manchester United and the GlazersLove them or loathe them, it is hard to dispute the impressive numbers generated under the Glazers’ guidance at Old Trafford. Since taking over the club in 2005, revenues have doubled, buoyed primarily by the ever increasing number and value of commercial deals. Following a successful IPO in New York in 2012, the club’s shares are currently trading at an all-time high, valuing the business at almost £2bn

2005 2013

Market Cap $1,398m $2,888m

Brand Value $293m $837m

Brand Rating AA AAA+

Annual Revenue $294m $486m

Revenue split

Matchday Media Commercial

Shirt sponsor(deal signed 2013, shirt sponsor from 2014)

Annual shirt sponsor value $16m $68m

Kit supplier

Commercial Partners 10 40+

Domestic Titles 15 20

European Cups / CL Wins 2 3

Ground capacity 67,540 75,811

Sources: Company accounts, press reports, Brand Finance league table, bloomberg

Even before acquiring Manchester United in May 2005 the Glazers knew that it was not just a business, not just a football club, but a brand. They set out with a clear strategy to invest and have achieved exponential returns on this investment, based on their extensive US sporting experience. The Glazers have set about extracting the unrealised commercial potential they saw within the club; in an eight year period, turnover has doubled, with commercial revenues rising an impressive 66%.

The club had devised a clear territorial and sector-based approach to acquiring commercial partners, leading to commercial relationships with over 40 partners worldwide. Whilst this strategy would dilute weaker brands, Manchester United is rightly confident it has the global awareness and brand strength to purse such strategy. Credit needs to go the commercial team behind the brand, who are consistently inventing new partnership opportunities and striving to achieve the best deal for the club; they recently took the bold move to back out of a ‘revolutionary’ training kit deal with DHL as they felt the could command a greater return on the opportunity.

The brand and its strategy featured heavily in last year’s IPO prospectus and the club is very proactive in seeking out new partners. It has recently setup a commercial office in Hong Kong to service its Asian partners and has been open about its desire to setup a similar office in America.

The Glazers remain close lipped about their exit strategy, but with shares currently trading at an all time high, valuing the club at close to $3bn, the figures attest to the Glazers’ financial success.

$122

m

$86m

$86m

$150

m

$159

m

$178

m

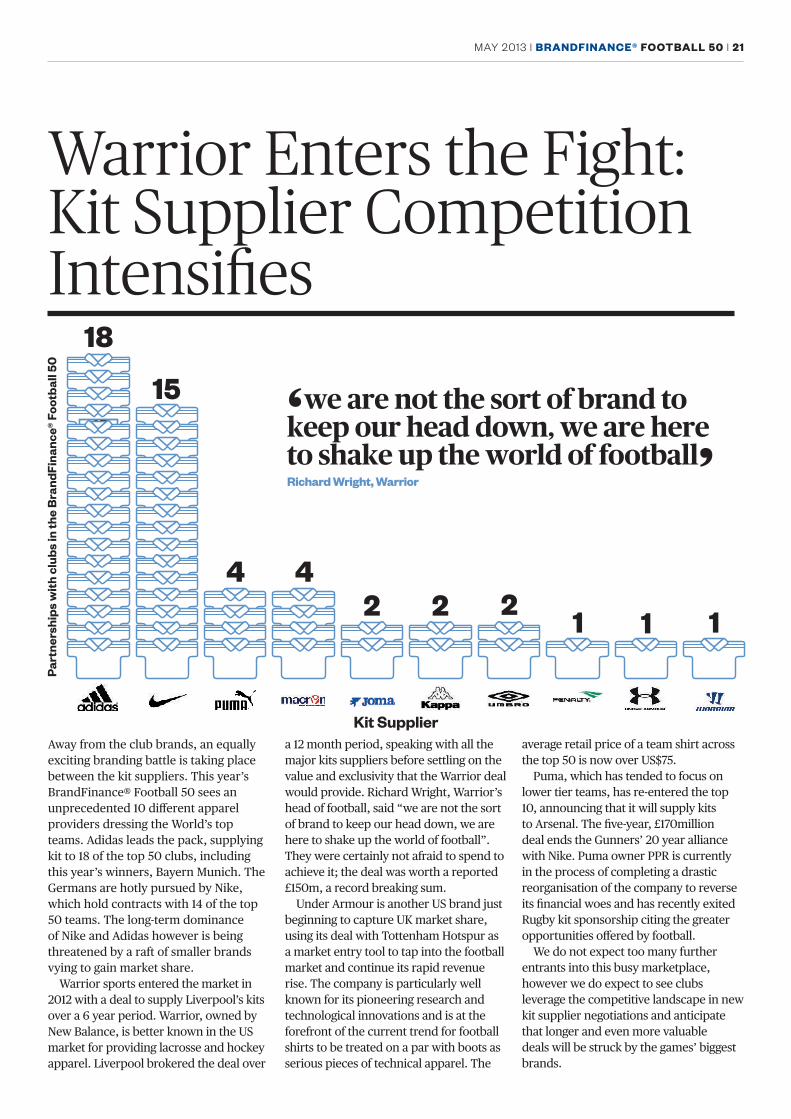

Away from the club brands, an equally exciting branding battle is taking place between the kit suppliers. This year’s BrandFinance® Football 50 sees an unprecedented 10 different apparel providers dressing the World’s top teams. Adidas leads the pack, supplying kit to 18 of the top 50 clubs, including this year’s winners, Bayern Munich. The Germans are hotly pursued by Nike, which hold contracts with 14 of the top 50 teams. The long-term dominance of Nike and Adidas however is being threatened by a raft of smaller brands vying to gain market share.

Warrior sports entered the market in 2012 with a deal to supply Liverpool’s kits over a 6 year period. Warrior, owned by New Balance, is better known in the US market for providing lacrosse and hockey apparel. Liverpool brokered the deal over

a 12 month period, speaking with all the major kits suppliers before settling on the value and exclusivity that the Warrior deal would provide. Richard Wright, Warrior’s head of football, said “we are not the sort of brand to keep our head down, we are here to shake up the world of football”. They were certainly not afraid to spend to achieve it; the deal was worth a reported £150m, a record breaking sum.

Under Armour is another US brand just beginning to capture UK market share, using its deal with Tottenham Hotspur as a market entry tool to tap into the football market and continue its rapid revenue rise. The company is particularly well known for its pioneering research and technological innovations and is at the forefront of the current trend for football shirts to be treated on a par with boots as serious pieces of technical apparel. The

average retail price of a team shirt across the top 50 is now over US$75.

Puma, which has tended to focus on lower tier teams, has re-entered the top 10, announcing that it will supply kits to Arsenal. The five-year, £170million deal ends the Gunners’ 20 year alliance with Nike. Puma owner PPR is currently in the process of completing a drastic reorganisation of the company to reverse its financial woes and has recently exited Rugby kit sponsorship citing the greater opportunities offered by football.

We do not expect too many further entrants into this busy marketplace, however we do expect to see clubs leverage the competitive landscape in new kit supplier negotiations and anticipate that longer and even more valuable deals will be struck by the games’ biggest brands.

MAY 2013 | BRANDFINANCE® FOOTBALL 50 | 21

Warrior Enters the Fight: Kit Supplier Competition Intensifies

Kit Supplier

Part

ners

hips

wit

h cl

ubs

in th

e B

rand

Fina

nce®

Foo

tbal

l 50

18

15

4 42 2 2 1 1 1

‘we are not the sort of brand to keep our head down, we are here to shake up the world of football’Richard Wright, Warrior

22 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

Treasure Chests: The Growing Value of Shirt SponsorshipSponsorship is a huge investment opportunity for corporate brands seeking to expand their global reach and raise awareness amongst new customers in new markets. In World football, the value of these sponsorships has grown dramatically in recent years, with some of the top clubs now generating more than $70m per year from shirt & kit sponsorship alone. This should not be surprising; shirts are worn by both players and fans and televised to a global audience of 4.7 billion making them prime real estate for sponsors.

Bayern Munich, generate $37million per year from its deal with Deutsche Telekom.The 2014/15 English Premier League (EPL) season will see Manchester United begin a $79 million per year shirt sponsorship deal with Chevrolet, making it the largest deal of its kind to date. In recent years even Catalonian

giants Barcelona have chosen to emblazon their traditionally plain shirt with a lucrative sponsorship deal. The Qatar Foundation reportedly agreed to pay €30 million a year to become the club’s first kit sponsor in its 113 year history. The top 10 most valuable brands in this year’s report generate an impressive $266m from their shirt sponsorship alone, not taking into account the raft of secondary deals and kit partnerships.

Corporate brands seeking a platform for building, strengthening and maintaining their brand image see partnerships with football brands as the ideal vehicle. Brands seeking to develop in new markets will look to clubs with the strength to raise awareness. Manchester United represents the gold standard in this regard; its new deal with Chevrolet signals the car manufacturer’s desire to drive its appeal up

MAY 2013 | BRANDFINANCE® FOOTBALL 50 | 23

in the European market by using the well developed United brand. At the same time the Glazers are attempting to grow the United brand in the US, as shown by the United’s annual stateside tours, so the partnership with an iconic American brand is likely to boost both United brand as well as its balance sheet.

Clearly sponsors must also fit with their target audience and brands must have synergy with viewers and supporters alike. A look at the top sponsorship deals in world football shows huge investment from brands that believe they share the same ideals that make a football club successful; the pursuit of perfection, hard work and passion.

Aspirational brands from the aviation and the automotive industries, as well as some of the World’s most valuable banking and telecoms brands can be found on the shirts of the most successful clubs. Away from the top global brands, betting has become a major source of football sponsorship. The synergy between these areas is clear with TV, mobile, online and pitch-side advertising invested in heavily by betting businesses such as Bet 365, Bet Fred and 32 Red amongst others. Shirt sponsorship by betting brands in the Football 50 is now worth US$47 million per annum.

Sponsorship in football is not without its risks however, with on-pitch success by no means guaranteed. Corporate sponsors can risk aligning their brand with a sinking ship or paying tens of millions of dollars only to have their sponsored club miss out on vital UEFA Champions League qualification and the awareness that comes with global television broadcasting. Wolverhampton Wanderers’ sponsor Sporting Bet must be bitterly disappointed following the club’s relegation in consecutive seasons. Unexpected success is the flip-side of

this, with the potential for sponsors to reap rewards for far in excess of a relatively modest deal. Swansea City sponsors 32 RED will no doubt have been extremely happy with the club’s promotion from the Championship, the securing of a 9th place finish in this year’s EPL as well as a first major trophy, the Capital One Cup, in February this year. This uncertainty is however reflected in the size of deal a club can command, those that can guarantee European football consistently will attract the best sponsors for the best money.

Sponsors must not forget that through their partnerships with the club as an entity they are also associating themselves with the individual stars. Footballers as individuals are notoriously difficult to control at the best of times, for example Luis Suarez poses a difficult dilemma for Liverpool’s head sponsor Standard Chartered. The Uruguayan’s silky skills are vital to the success of the Merseyside club on the pitch which can in turn become off-pitch brand success, but his propensity to grab headlines for what we might euphemistically call unsportsmanlike behaviour is no doubt causing headache at Standard Chartered.

Sponsorship revenues are a key component of any club’s income and are often driven by on-pitch success. The problem faced by many clubs is that in order become successful on the pitch they must first attract the big sponsors to fund the best players and staff. Many clubs have found this leap difficult, leaving an imbalance in football where the smaller clubs cannot challenge the big boys on or off the pitch. The increasing emphasis on running clubs as viable businesses creates an opportunity for traditionally smaller teams who, with shrewd a commercial operation, will be able to break this cycle through innovation and value for money.

24 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

Brand Finance Services

Brand Finance sponsorship servicesAdvising, implementing and measuring sponsorship

1 Opportunity Analysis

2 Brand Alignment

3 Negotiation Strategy

4 Evaluation

5 Brand & Business uplift

What opportunities are available and how feasible are they?

How strongly do our brand values align with those of our current or potential sponsored organisation?

Brand Finance is highly experienced in the technical issues surrounding sponsorship agreements.

Did the sponsorship achieve the objectives set?

What was the impact on both business performance and the value of the brand?

• Selecting the right partner• Market research• Competitor research• Budget setting• Stakeholder mapping• Sponsorship objective• Fundraising• Business case modelling

• Brand audit• Brand due diligence

• Royalty rate setting• Structure of charges• Length of agreement• Termination conditions• Transfer pricing• Tax structuring• Naming rights

• ROI• Sponsorship objectives

• ROI• Sponsorship objectives

MAY 2013 | BRANDFINANCE® FOOTBALL 50 | 25

Brand Finance Services

Brand Finance services for rights holdersReviewing, managing and improving business performance for sports brands

1 Revenue Analysis

2 Fundraising

3 Brand Strategy

4 Negotiation Strategy

5 Brand & Business

Valuation

Are we extracting the maximum value from all three revenue streams?

What are the various options open to us when attempting to raise funds? How can we implement these options?

Which strategy will provide the greatest return from the budget allocated?

Brand Finance is highly experienced in the technical issues surrounding sponsorship and stadium naming rights agreements.

What was the impact on both business performance and the value of the brand?

• ROI• Market research• Competitor research

• Naming rights• Financing• Licensing • Royalty rate setting

• Business case modelling• Brand audit• Brand due diligence• Selecting the right partner• Budget setting• Stakeholder mapping

• Royalty rate setting• Structure of charges• Length of agreement• Termination conditions• Balance of power analysis• Documented evidence• Negotiation support• Naming rights

• Pre & post business valuation• Pre & post brand valuation• Brand Value tracking

26 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

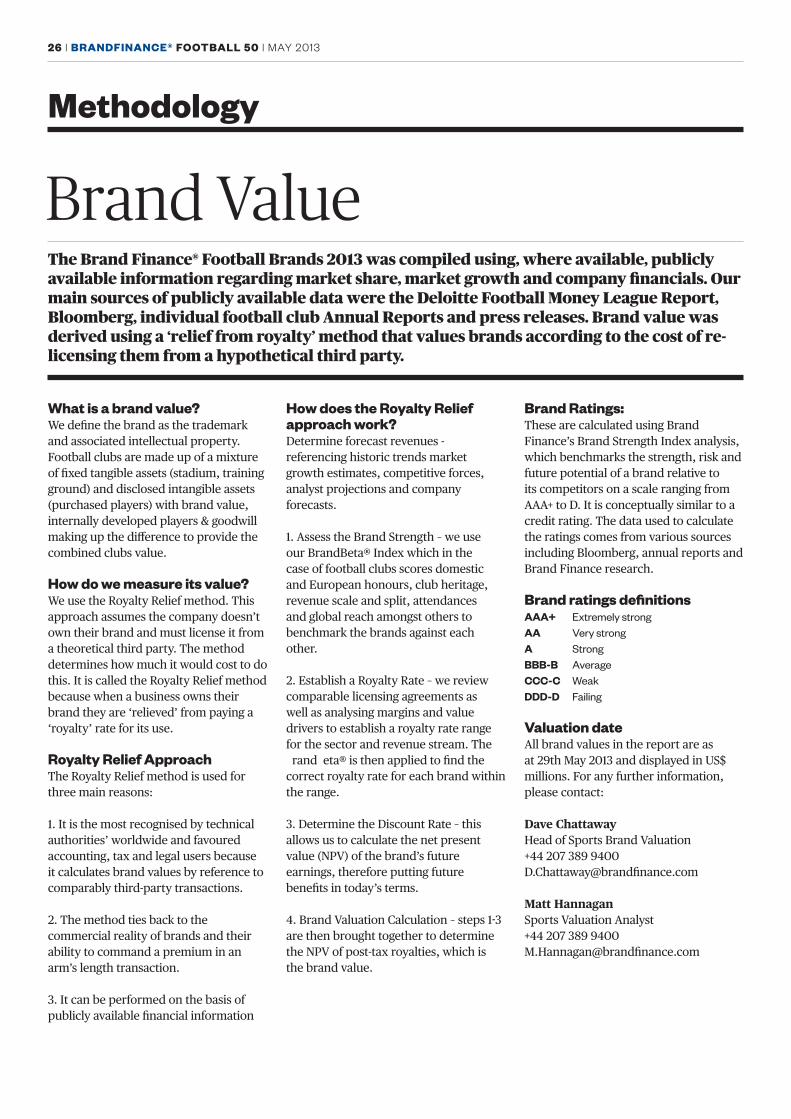

Methodology

What is a brand value?We define the brand as the trademark and associated intellectual property. Football clubs are made up of a mixture of fixed tangible assets (stadium, training ground) and disclosed intangible assets (purchased players) with brand value, internally developed players & goodwill making up the difference to provide the combined clubs value.

How do we measure its value?We use the Royalty Relief method. This approach assumes the company doesn’t own their brand and must license it from a theoretical third party. The method determines how much it would cost to do this. It is called the Royalty Relief method because when a business owns their brand they are ‘relieved’ from paying a ‘royalty’ rate for its use.

Royalty Relief ApproachThe Royalty Relief method is used for three main reasons:

1. It is the most recognised by technical authorities’ worldwide and favoured accounting, tax and legal users because it calculates brand values by reference to comparably third-party transactions.

2. The method ties back to the commercial reality of brands and their ability to command a premium in an arm’s length transaction.

3. It can be performed on the basis of publicly available financial information

How does the Royalty Relief approach work?Determine forecast revenues - referencing historic trends market growth estimates, competitive forces, analyst projections and company forecasts.

1. Assess the Brand Strength – we use our BrandBeta® Index which in the case of football clubs scores domestic and European honours, club heritage, revenue scale and split, attendances and global reach amongst others to benchmark the brands against each other.

2. Establish a Royalty Rate – we review comparable licensing agreements as well as analysing margins and value drivers to establish a royalty rate range for the sector and revenue stream. The βrandβeta® is then applied to find the correct royalty rate for each brand within the range.

3. Determine the Discount Rate – this allows us to calculate the net present value (NPV) of the brand’s future earnings, therefore putting future benefits in today’s terms.

4. Brand Valuation Calculation – steps 1-3 are then brought together to determine the NPV of post-tax royalties, which is the brand value.

Brand Ratings:These are calculated using Brand Finance’s Brand Strength Index analysis, which benchmarks the strength, risk and future potential of a brand relative to its competitors on a scale ranging from AAA+ to D. It is conceptually similar to a credit rating. The data used to calculate the ratings comes from various sources including Bloomberg, annual reports and Brand Finance research.

Brand ratings definitionsAAA+ Extremely strongAA Very strongA StrongBBB-B AverageCCC-C WeakDDD-D Failing

Valuation dateAll brand values in the report are as at 29th May 2013 and displayed in US$ millions. For any further information, please contact:

Dave ChattawayHead of Sports Brand Valuation+44 207 389 [email protected]

Matt HannaganSports Valuation Analyst+44 207 389 [email protected]

Brand ValueThe Brand Finance® Football Brands 2013 was compiled using, where available, publicly available information regarding market share, market growth and company financials. Our main sources of publicly available data were the Deloitte Football Money League Report, Bloomberg, individual football club Annual Reports and press releases. Brand value was derived using a ‘relief from royalty’ method that values brands according to the cost of re-licensing them from a hypothetical third party.

MAY 2013 | BRANDFINANCE® FOOTBALL 50 | 27

Below is a sample of the Key Performance Indicators we look at when accessing the strength of a football brand.

• Star playersStar players win matches and sell merchandise – they can be the key component of strengthening the brand. A club can have the heritage, the staff and the stadium, but if they don’t have the fundamental product – the players – to win and be successful on-pitch then it is all for naught.

• HeritageHistory is something you cannot buy. The oldest clubs tend to have the most successful histories and a loyal fan base stretching back generations that will stick with the club through thick and thin.

• TrophiesUltimately history only remembers winners, the runner-up is rarely given a shout. Fans and sponsors alike want to be associated with these winners. Every fan, player, manager and owner talks in terms of trophies, they are the raison d’etre for any club.

• StadiaA vital revenue generator and brand “touch point”, stadia are where the clubs “product” is showcased. Creating an enjoyable experience for fans is a must to make them part with their hard earned money as well as being large enough to fit all their fans in, easily accessible and well maintained.

• ManagerThe single most important person at any club and the single hardest job. Without their successful stewardship no club can rise to the top of our rankings.

Brand StrengthBrand ratings’ are calculated using Brand Finance’s Brand Strength Index analysis, which benchmarks the strength, risk and future potential of a brand relative to its competitors on a scale ranging from AAA+ to D. It is conceptually similar to a credit rating. The data used to calculate the ratings comes from various sources including Bloomberg, annual reports, websites such as transfermrkt.co.uk and Brand Finance original research.

BRAND STRENGTH INDEX

BSI Rank Club

BV2013USD

BrandRating

Key Performance Indicators

Founded League Titles

CL Titles

UEFA 5y coefficient

Squad Value USD

Stadium Size Utilsation Manager (12/13 season)

Managerial Assessment

Manager Career Win %

1 621 AAA+ 1902 31 9 137 798 Santiago Bernabéu 80,354 91% José Mourinho Extremely Strong 67%

2 837 AAA+ 1878 20 3 131 562 Old Trafford 75,957 99% Sir Alex Ferguson Extremely Strong 63%

3 572 AAA 1899 22 4 158 806 Camp Nou 99,354 80% Tito Vilanova Good 70%

4 860 AAA 1900 23 4 145 578 Allianz-Arena 69,901 99% Jupp Heynckes Very Strong 52%

5 180 AAA- 1897 29 2 71 433 Juventus Stadium 41,000 93% Antonio Conte Good 50%

6 263 AAA- 1899 18 7 94 281 Giuseppe Meazza 80,065 58% Massimiliano Allegri Good 49%

7 151 AA+ 1908 18 3 106 274 Giuseppe Meazza 80,065 75% Andrea Stramaccioni Satisfactory 52%

8 410 AA+ 1886 13 0 114 380 Emirates Stadium 60,355 99% Arsène Wenger Extremely Strong 56%

9 56 AA+ 1905 1 0 55 110 Ramón Sánchez Pizjuan 45,500 79% Unai Emery Satisfactory 46%

10 81 AA 1892 4 0 32 155 St. James Park 52,387 91% Alan Pardew Satisfactory 40%

11 103 AA 1910 5 1 0 94 Estádio do Pacaembu 40,199 63% Tite Good 48%

12 361 AA 1858 18 5 79 327 Anfield Road 45,522 93% Brendan Rodgers Satisfactory 42%

13 82 AA 1927 3 0 53 145 Olimpico di Roma 72,698 42% Aurelio Andreazzoli Satisfactory 53%

14 65 AA 1912 8 3 0 79.5 Estádio Urbano Caldeira 16,798 48% Muricy Ramalho Extremely Strong 47%

15 418 AA 1905 4 1 136 517 Stamford Bridge 41,841 99% Rafael Benítez Strong 54%

16 219 AA 1882 2 0 70 357 White Hart Lane 36,257 99% André Villas-Boas Good 59%

17 260 AA 1909 8 1 62 342 Signal Iduna Park 81,264 97% Jürgen Klopp Strong 48%

18 162 AA 1900 31 4 65 123 Amsterdam ArenA 52,960 89% Frank de Boer Strong 63%

19 144 AA 1887 6 1 56 141 Imtech Arena 57,274 95% Thorsten Fink Good 55%

20 61 AA- 1913 21 1 65 88 Philips Stadion 35,500 94% Dick Advocaat Very Strong 55%

Methodology

28 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

Brand Finance

A global brand strategy consultancy helping clients to measure, manage and maximise the value of their brands and branded businesses.

Brand Finance connects brands to business performance and help clients to solve their strategic brand challenges using robust financial analysis.

Our unique range of skills has been put to work on a wide range of projects including; brand and branded business valuation, patent and other intangible asset valuation, brand equity and brand strength drivers analysis, brand architecture & portfolio management, investor relations & IPOs, brand tracking and brand scorecards for some of the world’s strongest and most valuable brands.

About Brand FinanceBrand Finance is an independent global business focused on advising strongly branded organisations on how to maximize value through the effective management of their brands and intangible assets.

The Brand Finance network of 20 international offices gives us the breadth of expertise and local knowledge required to work with clients on every continent.

Since it was founded in 1996, Brand Finance has performed thousands of branded business, brand and intangible asset valuations worth trillions of dollars.

Brand Finance’s services support a variety of business needs:• Technical valuations for accounting, tax and legal purposes• Valuations in support of commercial transactions (acquisitions, divestitures, licensing and joint ventures) involving different forms of intellectual property• Valuations as part of a wider mandate

to deliver value-based marketing strategy and tracking, thereby bridging the gap between marketing and finance. Our clients include international brand owners, tax authorities, IP lawyers and investment banks. Our work is frequently peer-reviewed by the big four audit practices and our reports have also been accepted by various regulatory bodies, including the UK Takeover Panel.

Brand Finance is headquartered in London and has a network of international offices in Amsterdam, Bangalore, Barcelona, Cape Town, Colombo, Dubai, Helsinki, Hong Kong, Istanbul, Lisbon, Madrid, Moscow, New York, Paris, Sao Paulo, Seoul, Sydney, Singapore, and Toronto.

David HaighCEO

Edgar BaumMD, North America

Xander Bird, MD, Australia

Samir Dixit MD, Singapore

Gilson NunesMD, Brazil

Joao Pinto Goncalves MD, Portugal

Hany MwafyMD, Middle East

Muhterem Ilguner MD, Turkey

Unni KrishnanMD, India

Marc Cloosterman MD, Netherlands

Dave Chattaway Head of Sports Valuation, UK [email protected]

MAY 2013 | BRANDFINANCE® FOOTBALL 50 | 29

Contacts

The Team

BUSINESS ENQUIRIESFor further information on Brand Finance’s services, please contact your local representative.

Further international contacts;

Alexander Eremenko (Russia) [email protected] Oliver Schmitz (South Africa) [email protected] Min Jae Son (South Korea) [email protected] Ruchi Genewardene (Sri Lanka) [email protected]

For enquires from territories not mentioned above, please contact Richard Yoxon (UK Managing Director) [email protected].

MEDIA ENQUIRIESRobert Haigh, Communications ManagerTel: +44 (0)207 389 9400 Mobile: +44 (0)776 2211 267 Email: [email protected]

METHODOLOGY ENQUIRIESDave Chattaway, Head of Sports Brand ValuationTel: +44 (0)207 389 9400 Email: [email protected]

Matt Hannagan, Sports Valuation AnalystTel: +44 (0)207 389 9400 Email: [email protected]

GENERAL ENQUIRIESFor any other enquiries, please email us at [email protected], call +44 (0)207 389 9400 or visit our websites; www.brandfinance.com, www.brandirectory.com and www.brandfinanceforum.com.

30 | BRANDFINANCE® FOOTBALL 50 | MAY 2013

The BrandFinance® Football 50 USDT

HE

BR

AN

DFI

NA

NC

E® F

OO

TB

ALL

50

1-2

5

20

13

ra

nk2

01

2

rank

Clu

bC

ount

ry2

01

3U

SD2

01

2U

SDch

ange

Bra

ndR

atin

gM

ain

Spo

nsor

sK

it S

uppl

ier

Foun

ded

Leag

ue

Tit

les

CL

Tit

les

Squ

ad

Val

ue*

Sta

dium

Siz

eU

tils

atio

nM

anag

erW

in %

12

FC B

ayer

n M

unic

hG

erm

any

86

07

86

9%

AA

AD

euts

che

Tele

kom

Adi

das

19

00

23

45

78

Alli

anz-

Are

na 6

9,9

01

9

9%

52

%

21

Man

ches

ter U

nite

d FC

Engl

and

83

78

53

-2%

AA

A+

Aon

Nik

e1

87

82

03

56

2O

ld T

raffo

rd 7

5,9

57

9

9%

63

%

33

Rea

l Mad

rid C

FSp

ain

62

16

00

4%

AA

A+

bwin

Adi

das

19

02

31

97

98

Sant

iago

Ber

nabé

u 8

0,3

54

9

1%

67

%

44

FC B

arce

lona

Spai

n5

72

58

0-1

%A

AA

Qat

ar F

ound

atio

nN

ike

18

99

22

48

06

Cam

p N

ou 9

9,3

54

8

0%

70

%

55

Che

lsea

FC

Engl

and

41

83

98

5%

AA

Sam

sung

Adi

das

19

05

41

51

7St

amfo

rd B

ridge

41

,84

1

99

%5

4%

66

Ars

enal

FC

Engl

and

41

03

88

6%

AA

+Em

irate

sN

ike

18

86

13

03

80

Emira

tes

Stad

ium

60

,35

5

99

%5

6%

77

Live

rpoo

l FC

Engl

and

36

13

67

-2%

AA

Stan

dard

Cha

rter

edW

arrio

r1

85

81

85

32

7A

nfiel

d R

oad

45

,52

2

93

%4

2%

88

Man

ches

ter C

ity F

CEn

glan

d3

32

30

21

0%

AA

-Et

ihad

Airw

ays

Um

bro

18

80

20

57

8Et

ihad

Sta

dium

47

,72

6

97

%5

5%

99

AC

Mila

nIta

ly2

63

29

2-1

0%

AA

A-

Emira

tes

Airl

ines

Adi

das

18

99

18

72

81

Giu

sepp

e M

eazz

a 8

0,0

65

5

8%

49

%

10

11

Bor

ussi

a D

ortm

und

Ger

man

y2

60

22

71

5%

AA

Evon

ikPu

ma

19

09

81

34

2SI

GN

AL

IDU

NA

Par

k 8

1,2

64

9

7%

48

%

11

10

FC S

chal

ke 0

4G

erm

any

25

92

66

-3%

AA

-G

azpr

omA

dida

s1

90

47

02

20

Vel

tins-

Are

na 6

1,4

82

1

00

%5

6%

12

12

Tott

enha

m H

otsp

ur F

CEn

glan

d2

19

22

5-3

%A

AA

uton

omy

Und

er A

rmou

r1

88

22

03

57

Whi

te H

art L

ane

36

,25

7

99

%5

9%

13

16

Juve

ntus

FC

Italy

18

01

60

12

%A

AA

-Fi

at-J

eep

Nik

e1

89

72

92

43

3Ju

vent

us S

tadi

um 4

1,0

00

5

2%

50

%

14

14

AFC

Aja

xN

ethe

rland

s1

62

18

4-1

2%

AA

AEG

ON

Adi

das

19

00

31

41

23

Am

ster

dam

Are

nA 5

2,9

60

8

9%

63

%

15

13

FC In

tern

azio

nale

Mila

noIta

ly1

51

21

5-3

0%

AA

+Pi

relli

Nik

e1

90

81

83

27

4G

iuse

ppe

Mea

zza

80

,06

5

75

%5

2%

16

17

Ham

burg

er S

VG

erm

any

14

41

53

-6%

AA

Emira

tes

Adi

das

18

87

61

14

1Im

tech

Are

na 5

7,2

74

9

5%

55

%

17

NEW

Gal

atas

aray

AŞ

Turk

ey1

16

NEW

NEW

A+

Turk

Tel

ekom

Nik

e1

90

51

90

19

0Tü

rk T

elek

om A

rena

52

,69

5

64

%4

8%

18

15

Oly

mpi

que

de M

arse

ille

Fran

ce1

11

16

8-3