the complexity economics revolution

TRANSCRIPT

J. Doyne Farmer Institute for New Economic Thinking at the Oxford Martin School, Math Institute, University of Oxford; Santa Fe Institute

The complexity economics revolution

Economic theory: Assign agents utility function and model of beliefs Maximize utility subject to constraints Solve for equilibrium

Was austerity good for Greece?

Or was austerity like the sacrifice of Ifigenia?

Science makes things that are random become predictable

Complexity Economics offers an alternative

What is the economy?

What is the Economy?

The economy is the metabolism of civilization

The financial system is like the enteric nervous system

Economics=Accounting+Behaviour

1.Health warning: Complexity economics is a young science

Accounting: Balance sheets are interlinked by transactions and liabilities

1.Health warning: Complexity economics is a young science

The economy is vastly complicated

50 million firms 2 billion households

3.3 billion workers trillions of active contracts

1.Health warning: Complexity economics is a young science

Behavior is complicated too

1.Health warning: Complexity economics is a young science

Dominant model for behavior is rational expectations. Alternatives are now being explored

1.Health warning: Complexity economics is a young science

Complexity economics: Be flexible! Model behavior directly

1.Health warning: Complexity economics is a young science

People use heuristics + bounded rationality to solve problems

The economy can be simulated

1.Health warning: Complexity economics is a young science

“Standard” complexity economics model: Assign agents decision making rules or learning algorithms Simulate collective interactions Observe economic phenomena

1.Health warning: Complexity economics is a young science

Why does the economy change?

1.Health warning: Complexity economics is a young science

Mainstream economics says the economy changes because of “shocks”

Exogenous Dynamics

1.Health warning: Complexity economics is a young science

DSGE = rocking horse economy

But the weather changes all by itself Endogenous Dynamics

The economy also changes by itself

In economics the future strongly influences the present. Rational utility maximizers are unduly static.

Bounded rationality naturally creates endogenous dynamics

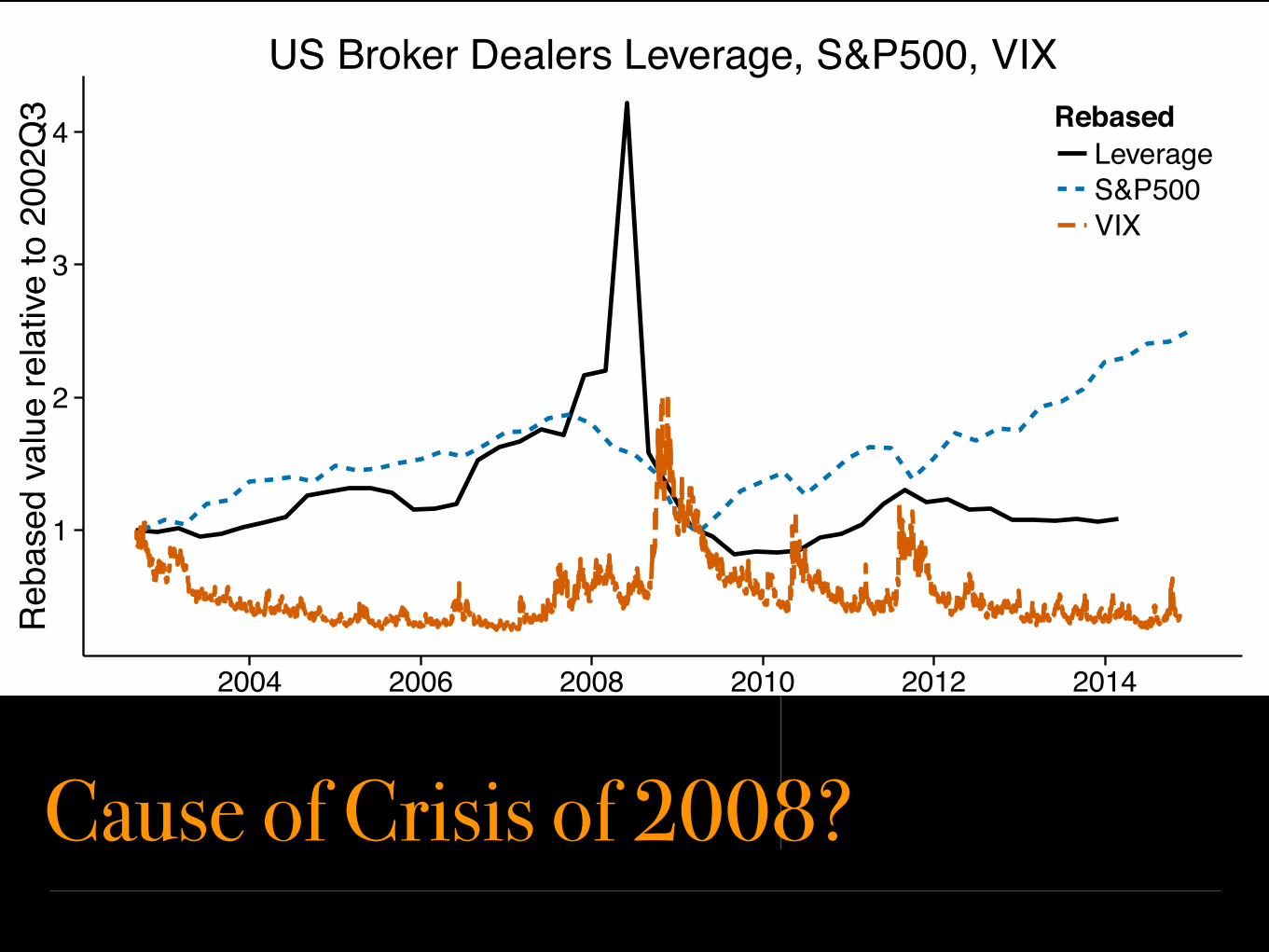

Cause of Crisis of 2008?

1

2

3

4

2004 2006 2008 2010 2012 2014Date

Reb

ased

val

ue re

lativ

e to

200

2Q3 Rebased

LeverageS&P500VIX

US Broker Dealers Leverage, S&P500, VIX

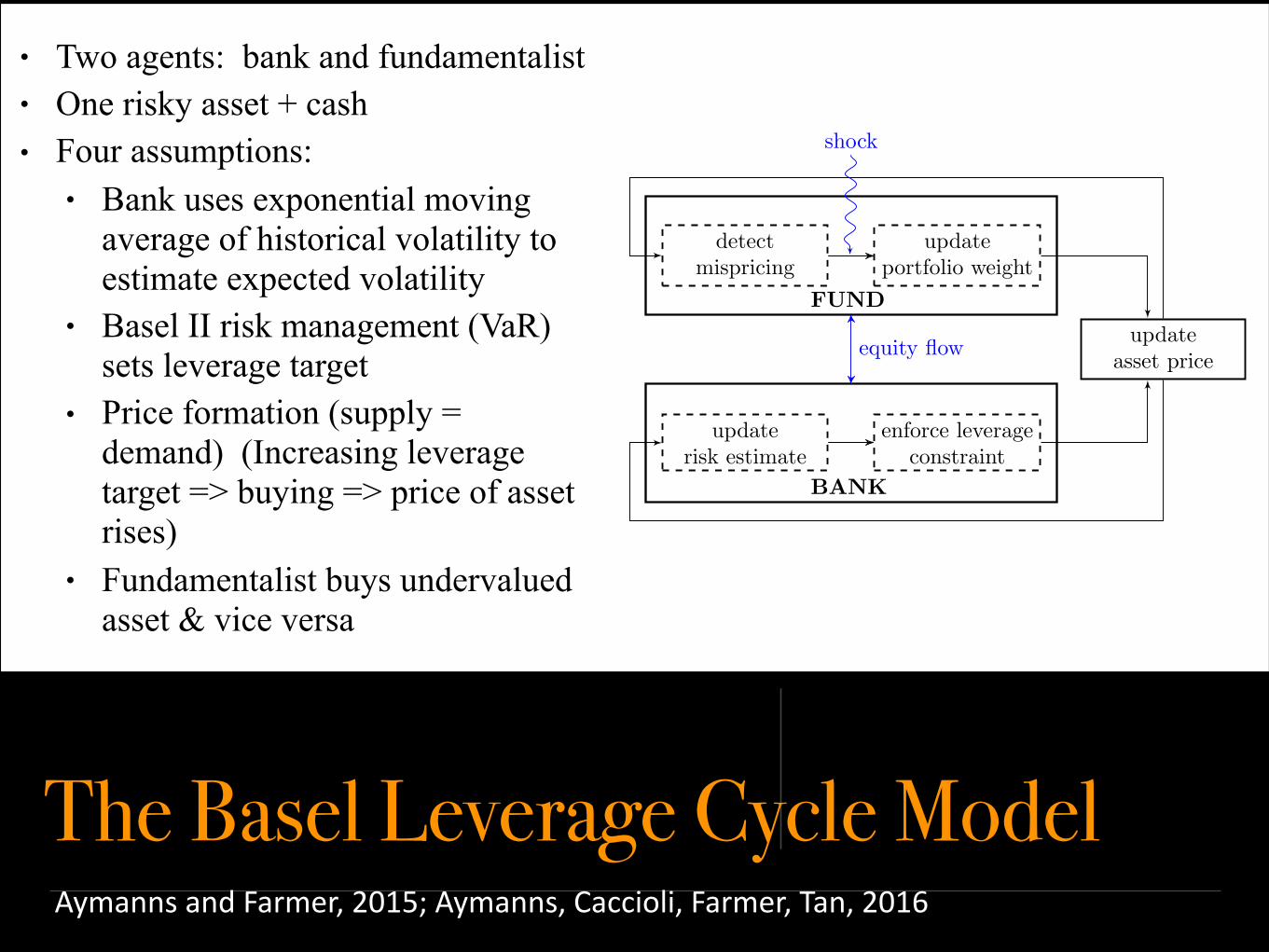

The Basel Leverage Cycle Model

detectmispricing

updateportfolio weight

updaterisk estimate

enforce leverageconstraint

updateasset price

equity flow

FUND

BANK

shock

• Two agents: bank and fundamentalist • One risky asset + cash • Four assumptions:

• Bank uses exponential moving average of historical volatility to estimate expected volatility

• Basel II risk management (VaR) sets leverage target

• Price formation (supply = demand) (Increasing leverage target => buying => price of asset rises)

• Fundamentalist buys undervalued asset & vice versa

AymannsandFarmer,2015;Aymanns,Caccioli,Farmer,Tan,2016

ModelReality

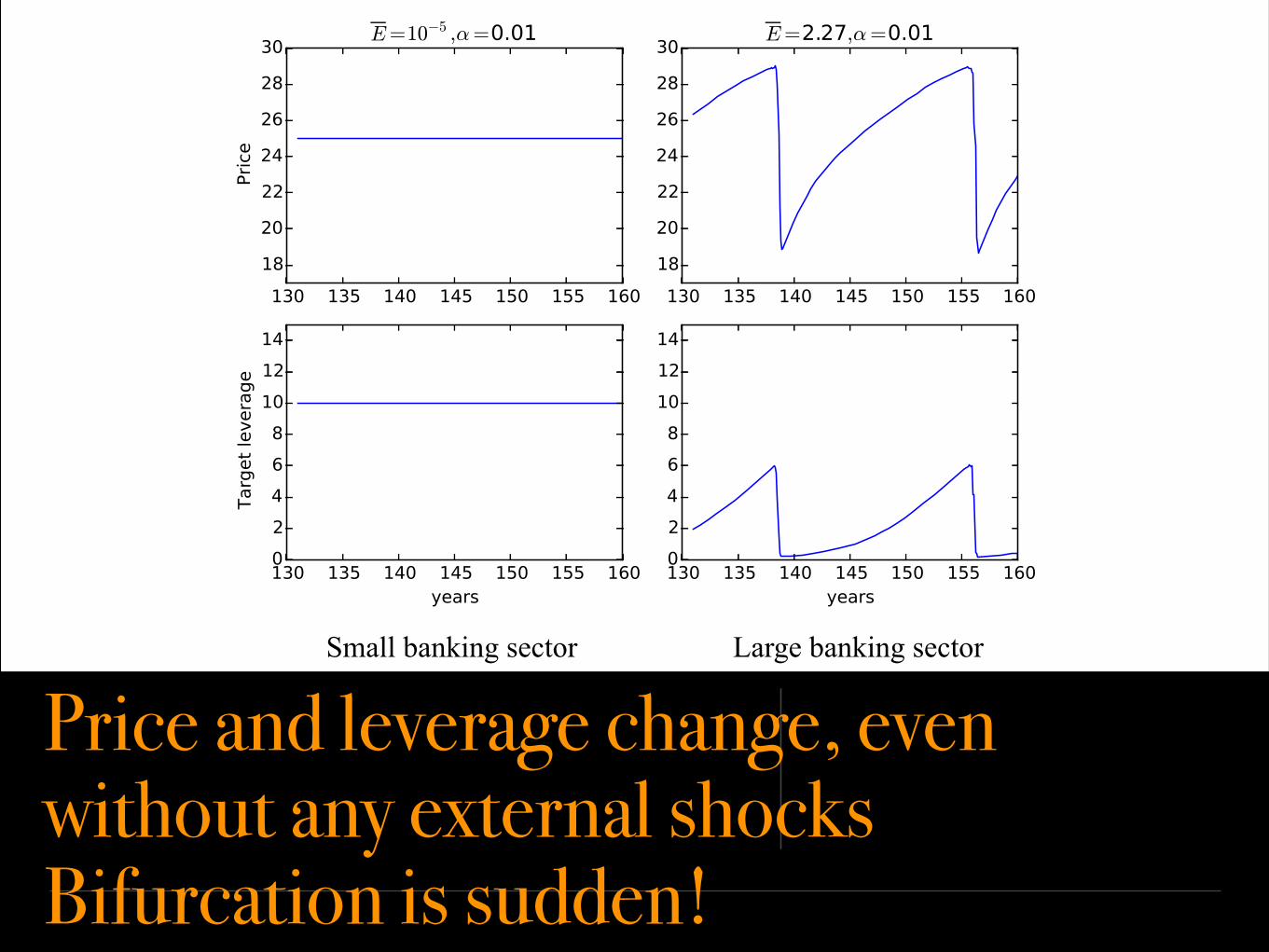

Price and leverage change, even without any external shocks Bifurcation is sudden!

Small banking sector Large banking sector

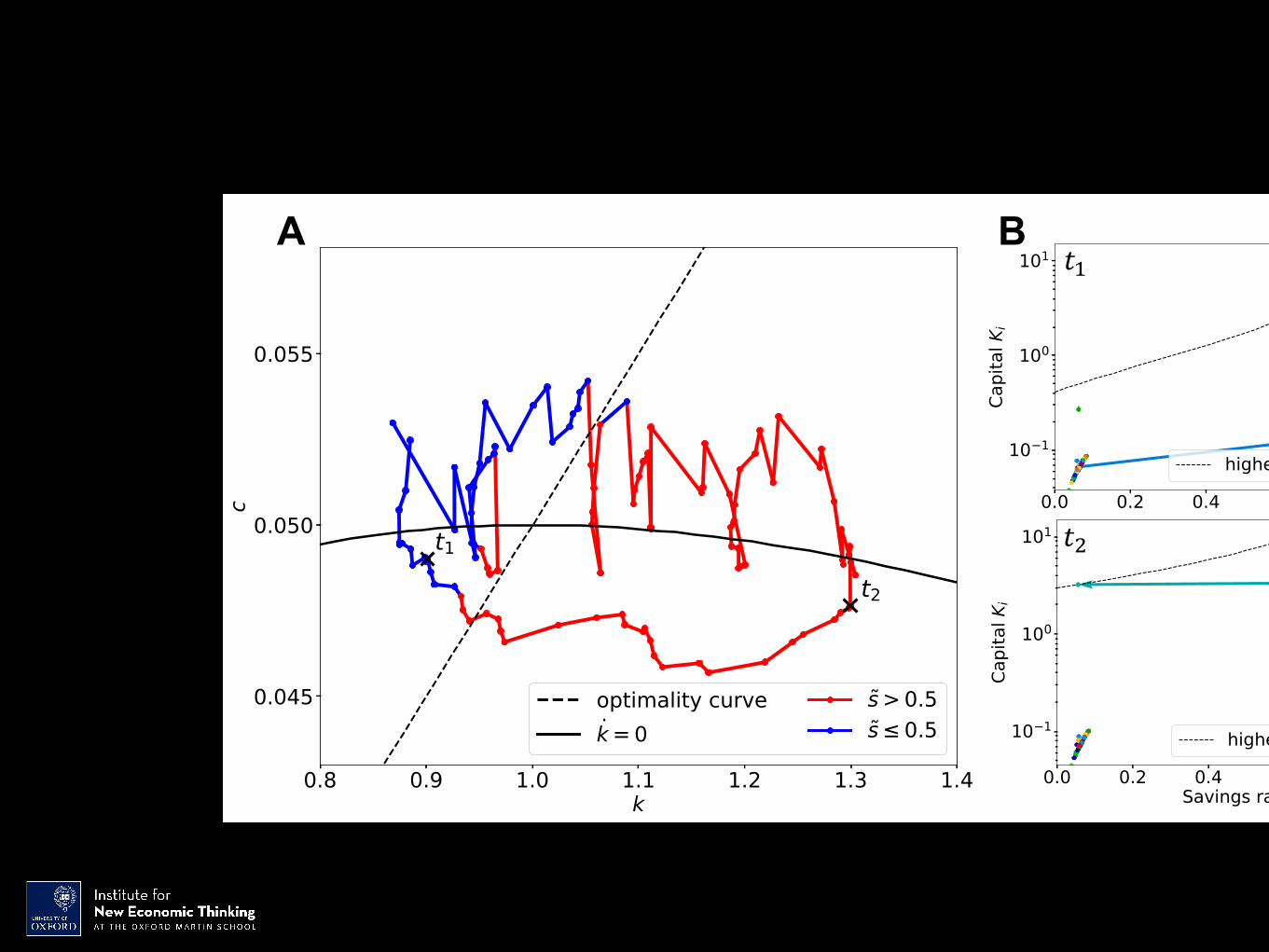

• Standard RCK model: Rational, representative household chooses savings rate to maximize discounted consumption

• Invests savings in representative firm- compromise between consumption and investment

• Our version: Heterogeneous households have social network. At intermittent intervals of average length tau, each copies savings rate of neighbor with highest consumption.

Standard macro model with bounded rationalityYuki Asano, Jakob Kolb, JDF, Jobst Heitzig

10 1 100 101 102 1030.0

0.2

0.4

0.6

0.8

1.0Sav

ings

rat

e s i

s *

sgold

s

10 2

10 1

100

prob

abili

ty

0 500 1000 1500 2000 2500 3000 35000.00

0.25

0.50

0.75

1.00Sa

ving

s ra

te si

Time evolution

s

0 500 1000 1500 2000 2500 3000 35000

5

10

15

Cap

ital

Ki

0 500 1000 1500 2000 2500 3000 35000.4

0.5

0.6

s

0.0 0.5 1.0

Histograms

si

10 1 101

Ki

10 12

Y

9

10

11

Out

put

Y

!"A B

!#

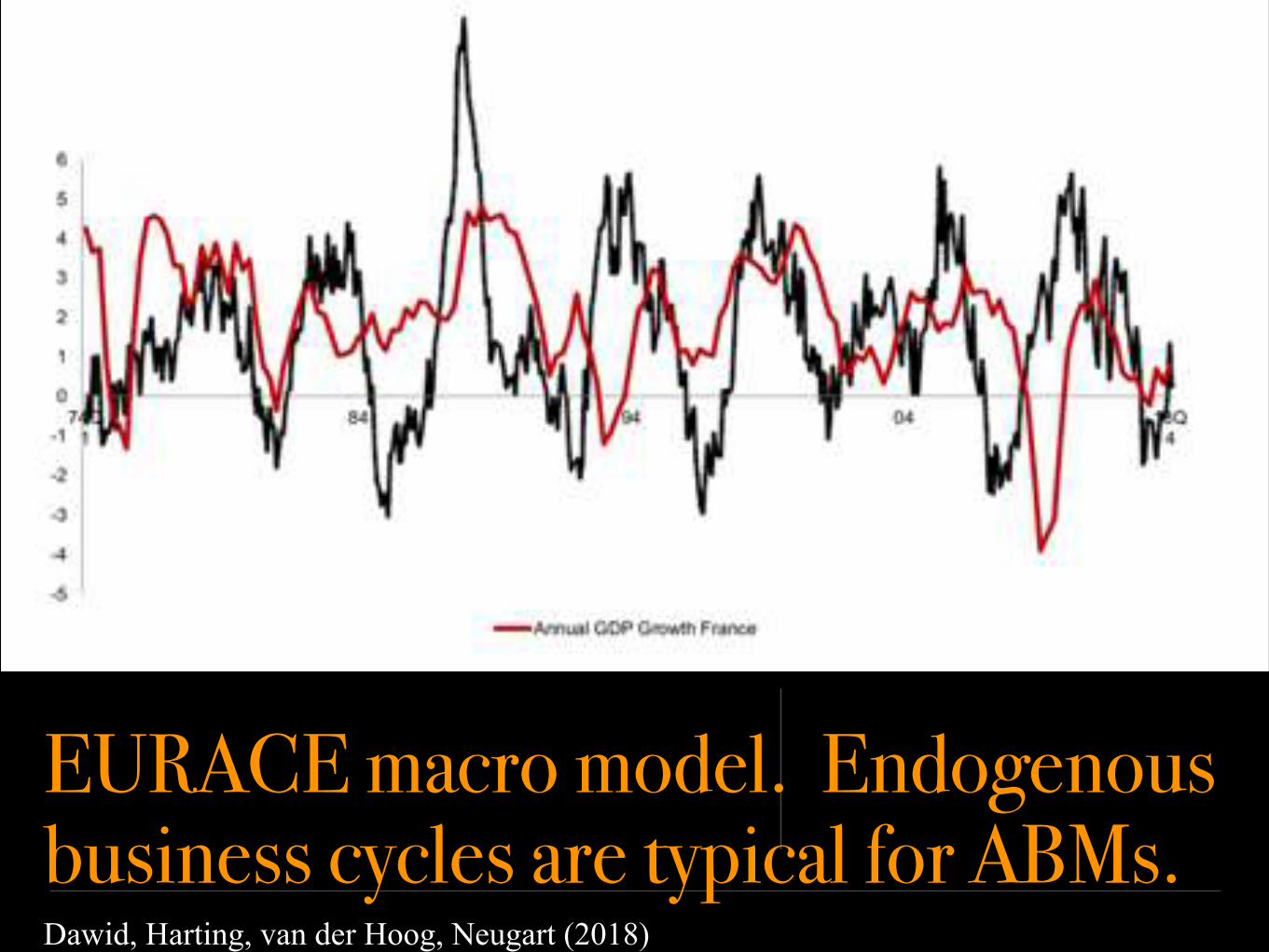

EURACE macro model. Endogenous business cycles are typical for ABMs.Dawid, Harting, van der Hoog, Neugart (2018)

Simulation of Washington DC Housing MarketAxtell, Carella, Farmer, Geanakoplos, Goldstein, Howitt and others.

And hot off the press…

The economy is an ecology of specialists

Adam Smith, Wealth of Nations, 1776.

“It is not from the benevolence of the butcher, the brewer, or the baker that we expect our dinner, but from their regard to their own interest.”

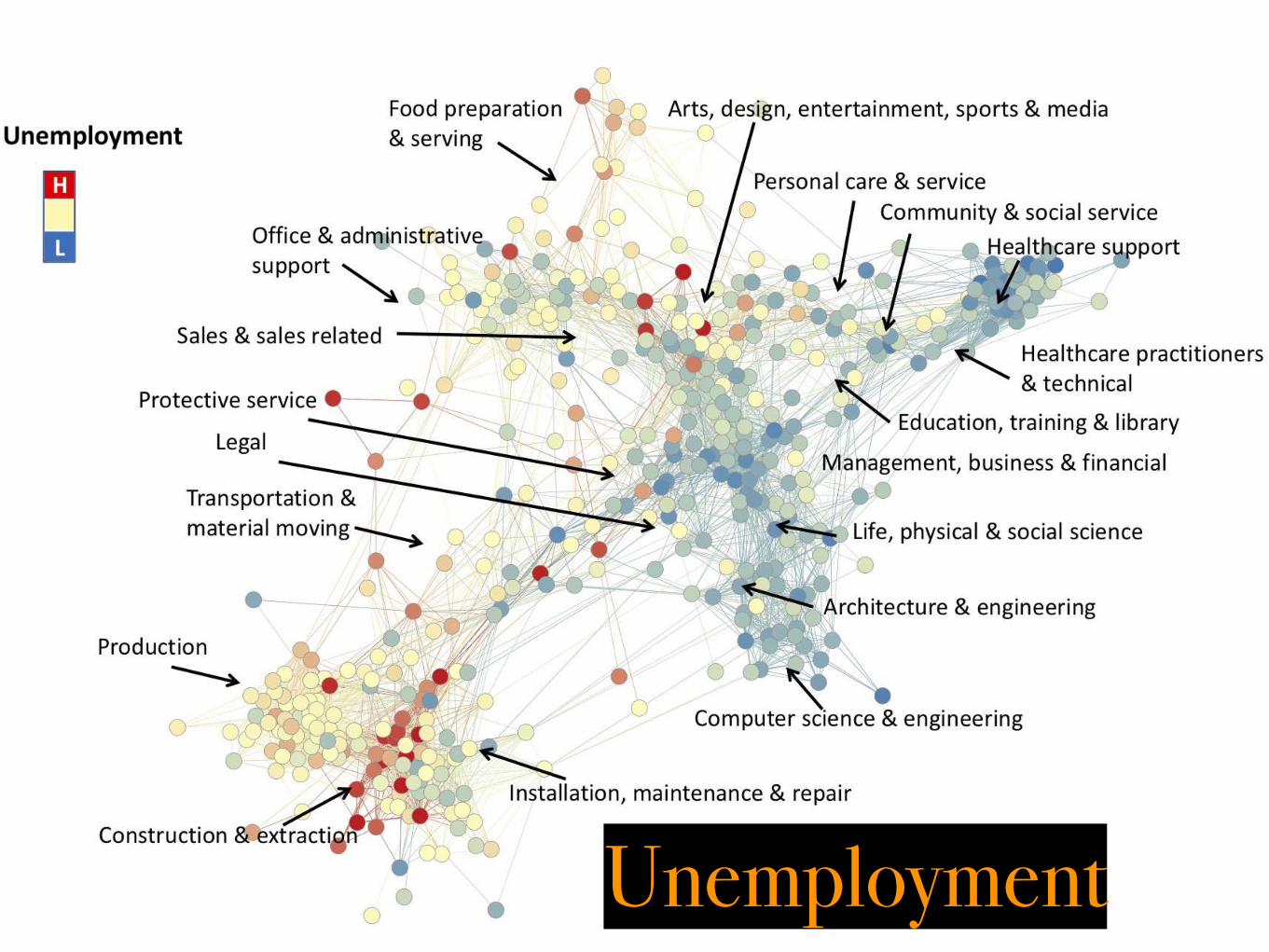

Unemployment

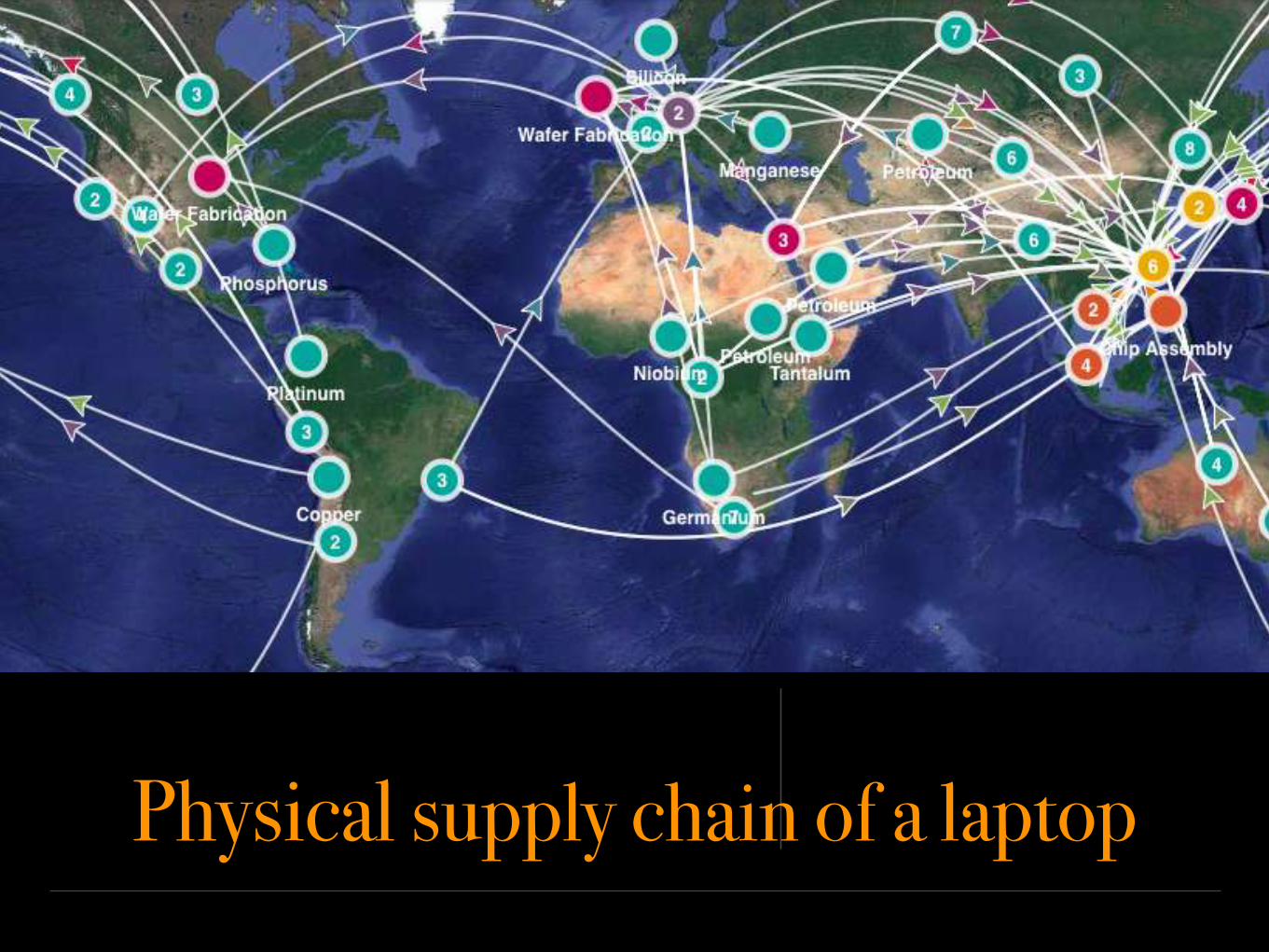

Physical supply chain of a laptop

Production Network of the USAMcNerney and Silverberg

WassilyLeontief

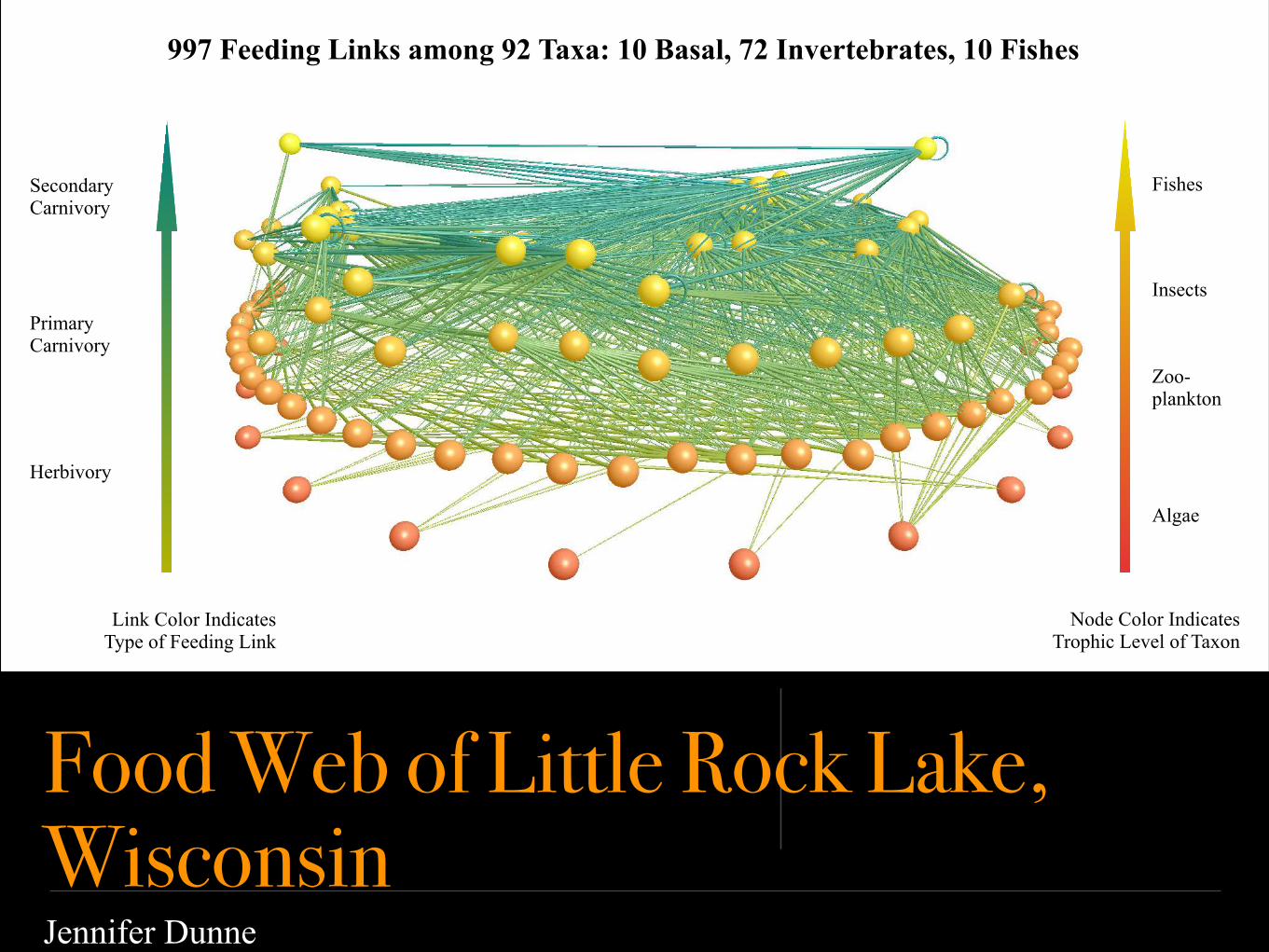

Food Web of Little Rock Lake, Wisconsin

Fishes

Insects

Zoo- plankton

Algae

Node Color Indicates Trophic Level of Taxon

Secondary Carnivory

Primary Carnivory

Herbivory

Link Color Indicates Type of Feeding Link

997 Feeding Links among 92 Taxa: 10 Basal, 72 Invertebrates, 10 Fishes

Jennifer Dunne

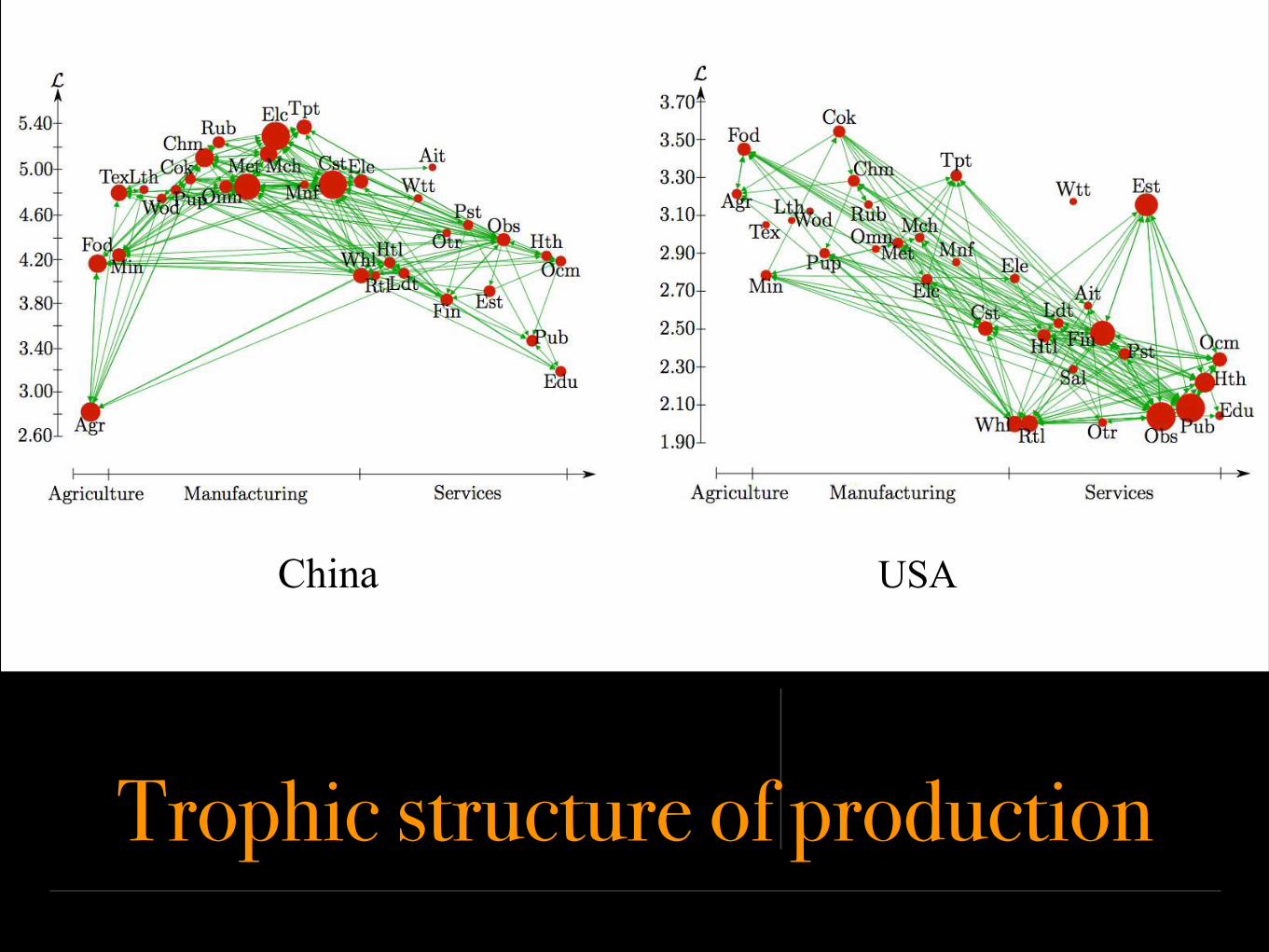

Trophic structure of production

China USA

L̄ = 1 L̄ > 1

44

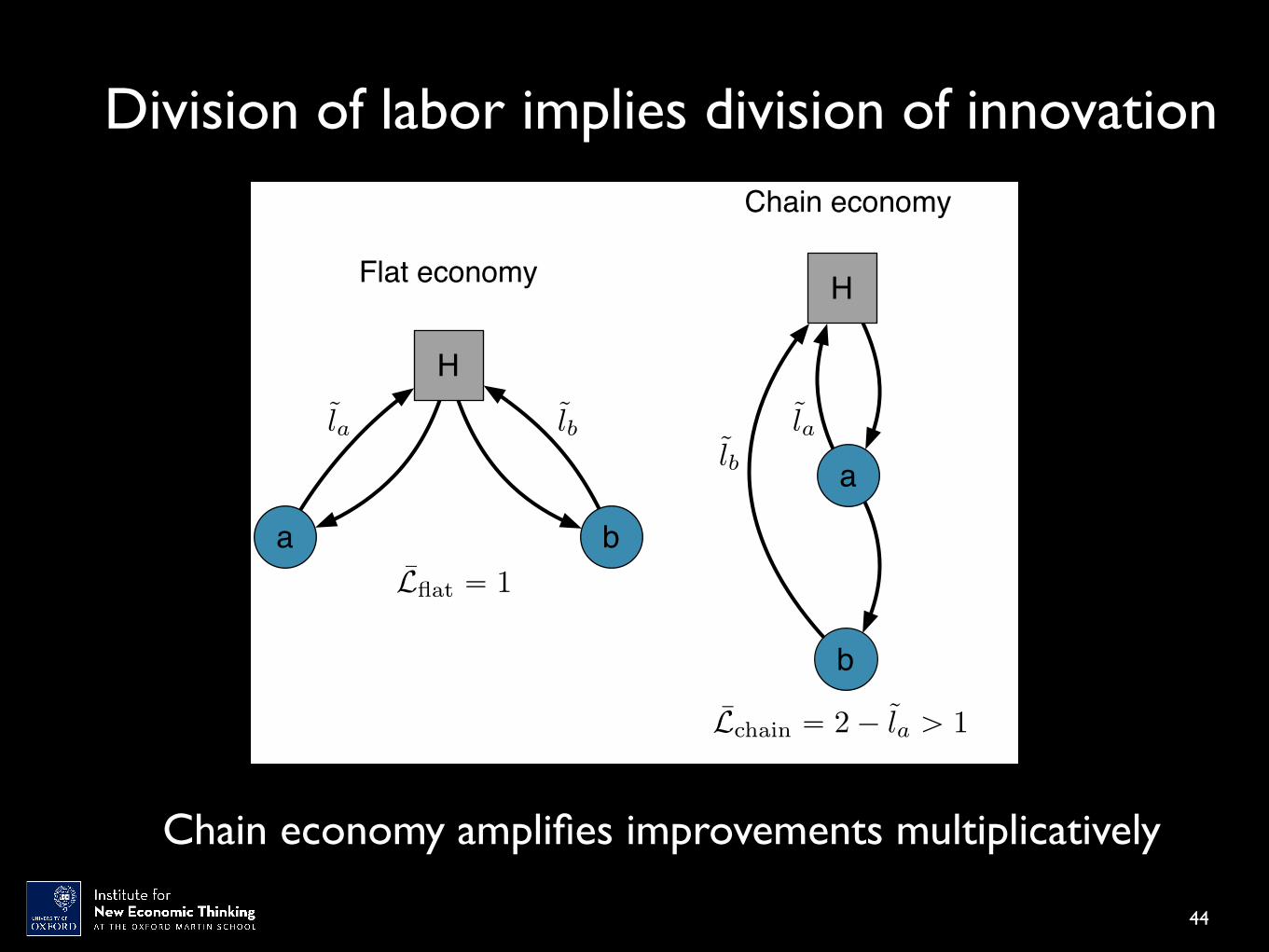

Chain economy amplifies improvements multiplicatively

Division of labor implies division of innovation

Flat economy

Chain economy

H

a b

H

b

a

L̄chain “ 2 ´ l̃a ą 1

L̄flat “ 1

l̃a l̃b l̃al̃b

Trophic level predicts economic growthMcNerney, Savoie, Caravelli, Carvalho and Farmer

Trophic level in 19951 1.5 2 2.5 3 3.5 4 4.5 5 5.5

Realprice

return

1995-2009

-0.15

-0.1

-0.05

0

0.05

0.1

0.15regressionbin average

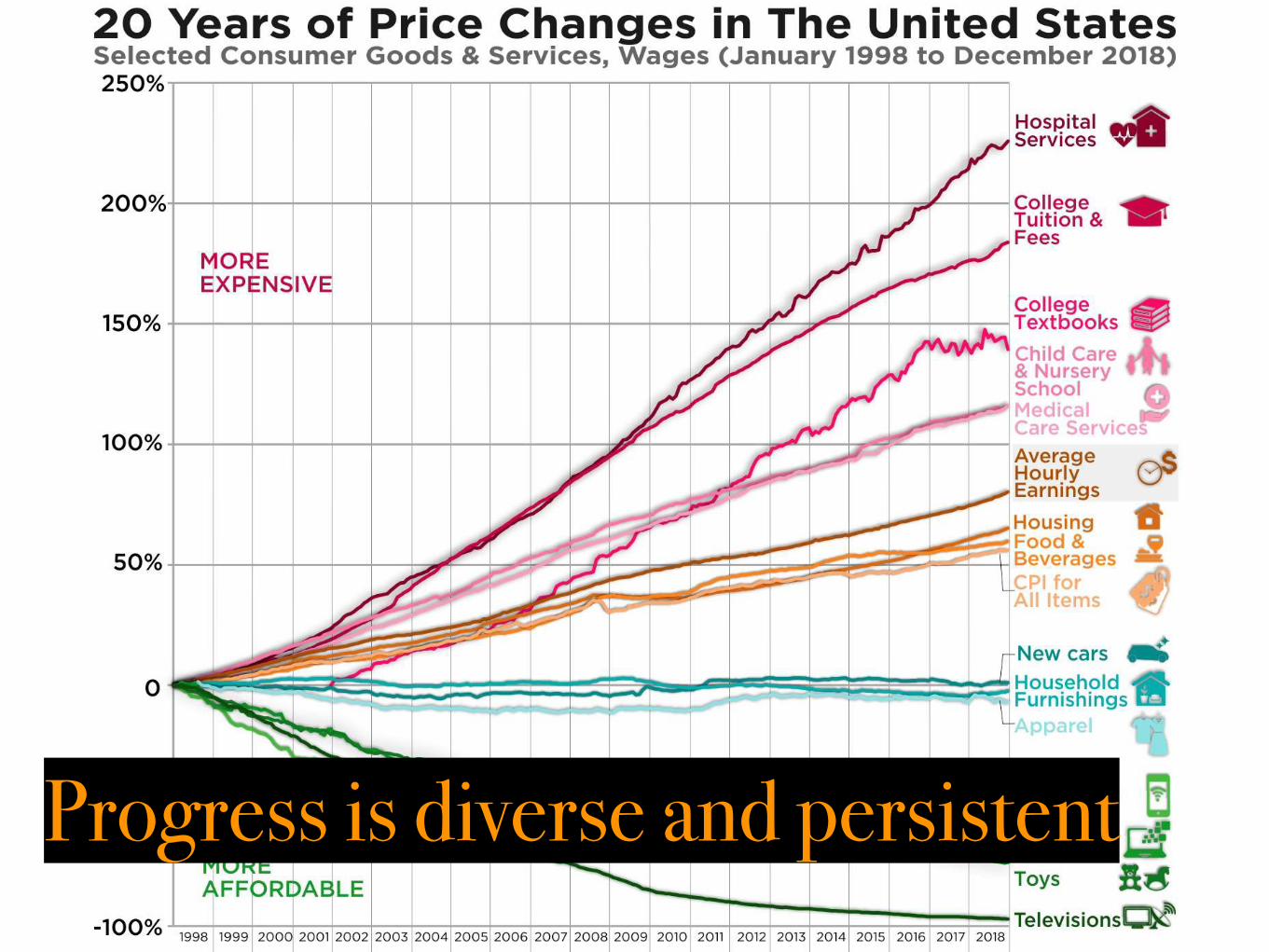

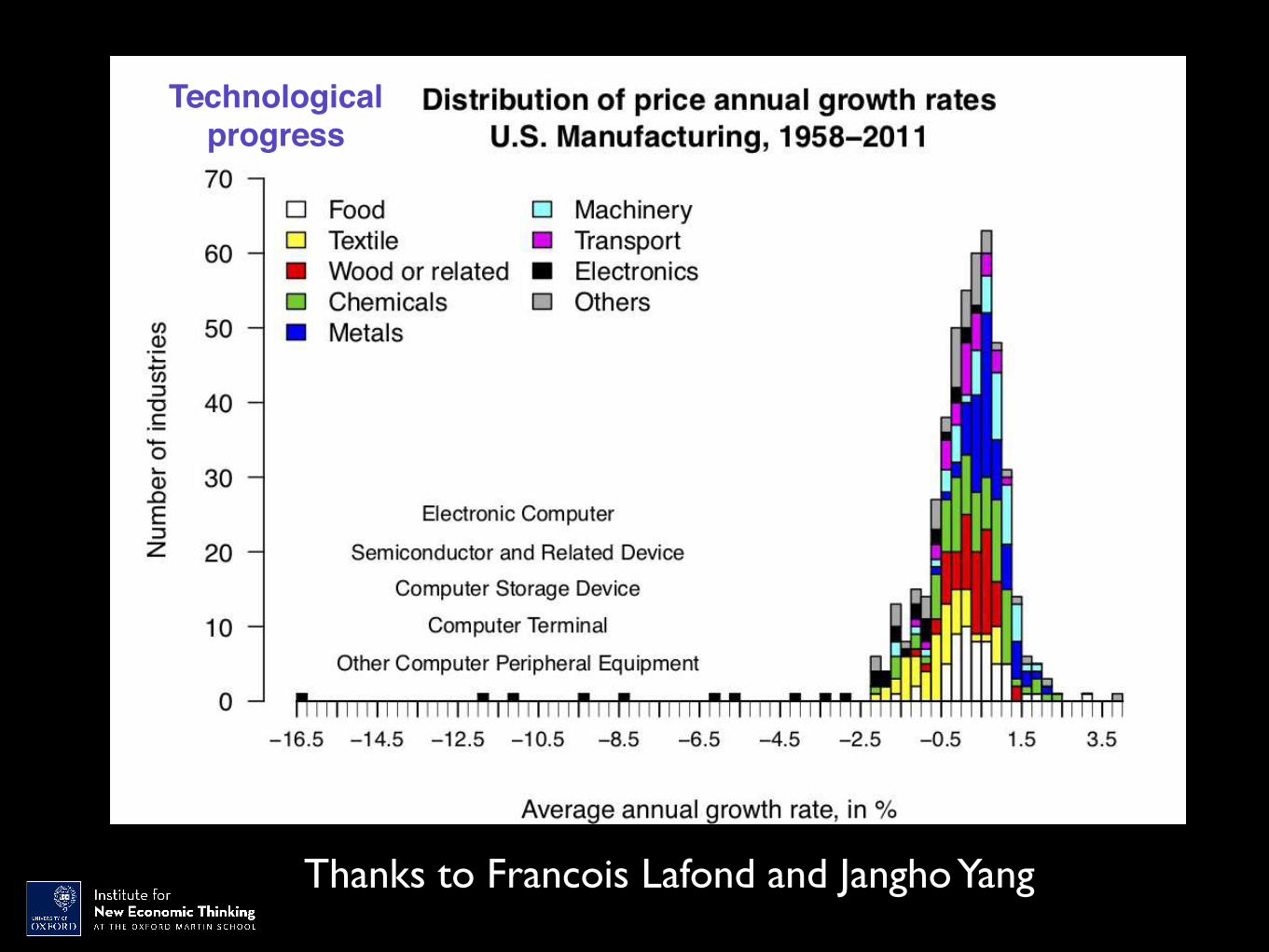

Progress is diverse and persistent

Thanks to Francois Lafond and Jangho Yang

Technologicalprogress

Can use this to forecast prices of technologiesFarmer and Lafond, 2016, Lafond et al. 2018

PV m

odul

e pr

ice

in 2

013

$/W

p

1980 1986 1992 1998 2004 2010 2016 2022 2028

0.02

0.05

0.12

0.33

0.9

2.46

6.69

± 1σ± 1.5σ± 2σ

What about Climate Change?

Bill Nordhaus says optimal warming is 3.5 degrees…

Prices and production of energy technologiesWay, Mealy and Farmer, 2020.

Cost Production

Direct-use primary energy resources

End-use sectors

Nuclear

Coal

Crude oil

Gas

Hydropower

Wind

Biopower

Solar PV

Transport

Industry

Buildings

Energy sector Energy carriers and conversions

Coal

Gas

Electricity

Batteries (daily)

Batteries (multi-day)

Electricity generation

Oil

Coal

Gas

Hydrogen

Batteries (daily)

Technology

Sector

Key:

Carrier

Energy (self-use)

Electrolysers

(for hydrogen)

(for sectors)

Components of the energy system

Scenarios for the green energy transition

Climate Catastrophe Fast Transition Slow Transition Slow Nuclear Transition

Predicted cost of the green energy transition under different scenariosWay, Mealy and Farmer, 2020.

Net present value Distribution of NPV

Fast renewable green energy transition is cheaper than business as usual!

We need a better map of the economy

• Our understanding of the economy and our ability to predict on many levels will become dramatically better when we are able to map out and simulate the production network at fine scale and link to financial markets

• Ultimately we want to link to other social models, e.g. to predict how an epidemic will affect supply chains

Hypothesis

Complexity Economics is a young science

• Parameter estimation (Platt)• Initial condition estimation• Data (data, data, data, …)

Key problems to be solved for ABM to be predictive time

series models

Proof of principle — just a start

Global microeconomicsLet macro emerge from micro

Takes advantage of heterogeneity Much more data at microscale Better statistical significance

Endogenous dynamics Can model emergence Predicts more things

We are facing serious problems: financial crises

inequality climate change

Complexity economics offers new solutions