the effect of annual earnings announcements on the chinese stock markets

TRANSCRIPT

The Effect of Annual EarningsAnnouncements on the Chinese

Stock Markets

SHUHONG KONG* AND MAJID TAGHAVI**

AbstractThis paper examines the annual earnings announcement effect of the stock markets

in China. The investigation is based on events analysis and carried out by modeling thedaily changes of stock returns using the M-EGARCH approach, by testing the newseffects of annual earnings announcement on the conditional mean of abnormal returnand the variance of the returns. It is found that a higher than expected earningsannouncement leads to a rise in the conditional mean of stock returns on days before thenews announcement and a fall afterwards. The conditional volatility of the changes aresignificantly reduced by bigger absolute values of reported earnings before the newsannouncement and increased afterwards, supporting the rejection of semi-strong-formefficiency. (JEL G10, G12, G14)

Introduction

Many studies on the semi-strong-form efficiency of stock market are focused on theanalysis of the information content of annual earnings and dividend announcements.The purpose of these public disclosure announcements is to provide information thatmeets investors’ needs for decision-making. According to Fama [1991], in a sub-efficientmarket, the share price may fail to fully reflect all relevant information, and abnormalreturns may be obtained by taking advantage of public information because there is asignificant time lag between announcement and full incorporation of the information.

Previous empirical studies on annual earning announcements in the Chinese stockmarket largely concentrate on the drift effect on the overall market attributed toinformation disclosure [Zhao, 1998; Chen and Liu, 1999; Chen and Yang, 1999; Chen andChen, 2002], without considering the precise quantitative relationship between yieldchange and earnings change given new information disclosure. We investigate theseeffects using the M-EGARCH model. We intend to discover the precise quantitativerelationship between the earnings and the yield shift. Specifically, the daily changes ofstock prices are modeled by M-EGARCH to ascertain the existence and the nature of theannual earning announcement effects on the conditional mean and variance of thechanges. In the European and the U.S. markets, most such news announcements affectstock prices on the days of the information disclosure and the effect would not continueafter the day of disclosure. This means that the European and American markets arebasically semi-strong-form efficient stock markets. In contrast, we will show that theChinese markets are not as efficient as the western markets.

International Advances in Economic Research (2006) 12:318Y326 * IAES 2006

DOI: 10.1007/s11294-006-9020-8

*University of International Business and Economics—Beijing, China and ** University ofNorthumbria—Newcastle upon Tyne NE3 5AJ, UK.

318

This paper will find evidence of the sub-efficient character of Chinese markets bymeans of an EGARCH model. The EGARCH model is based on exponential generalisedautoregressive conditional heteroskedastic model, which was first put forward by Nelson[1991]. This model is more apt to explain the asymmetric changes of the conditionaldeviation, and the extent of yield change due to information disclosure. The estimatedcoefficients of the model would provide us with answers to our questions. This type ofmodeling is important in our research because of the following reasons.

First, the model used here is based on the conditional heteroskedasticity property ofthe daily changes, so that the results of empirical study are more coincident with actualcondition. Many researchers of Chinese stock markets using other models have oftenignored the adverse consequences of heteroskedasticity.

Second, the model will estimate the exact value of the mean of daily changes of stockprices in the events window, and the elasticity relating to EPS (earning per share) overtime. This empirical result describes more exactly the effect of annual earningsannouncement. Other studies, on the other hand, only distinguish the difference betweenthe good and the bad news.

Finally, and more importantly, using the model we can examine and evaluate theeffects of announcement news on the conditional volatility of the abnormal returnchanges in the events window. The exact value of the variance in response to the news,higher volatility due to good news or bad news and the asymmetric reactions towards goodand bad news are also offered by the model.

The rest of the paper is organized as follows. The next section offers a literature reviewof the empirical investigations in this area. The following section discusses the nature ofthe data and the modeling issues. Then, the paper presents the empirical results. Finally,the last section concludes the paper.

Literature Review

The theory of rational-informed efficient financial markets has been extensivelytested for nearly a quarter of a century. Although there has recently been an increase inempirical research regarding emerging/developing financial markets, a glance throughthe literature reveals that a significant amount of work needs to be conducted in thisarea. It has been noted by Balaban and Kunter [1996] that research on developingeconomies’ financial markets may offer valuable opportunities for diversification beyondnational markets. Amongst many [Balaban, 1995; Cornelius, 1991, 1993; Muradoglu andMetin, 1995], Keane [1993] has presented a detailed analysis and empirical investigationof the Efficient Market Hypothesis (EMH) in developing markets. In particular, as Chinabecomes more integrated into global financial markets, any examination of and analysisbased on Chinese stock markets should be of significant interest to academics, policymakers, and investors.

Many empirical studies on the European and American capital markets tend to focuson the reaction speed of the market to important events or other new information.Particular use has been made of event studies, which examine the extent to whichreturns are abnormal in the time period surrounding a public announcement. Numerousstudies have analysed price reactions following specific information disclosures, such asstock splits, new exchange listings, or earning announcements. Pettengill and Jordan[1990] found overreaction and, hence, abnormal returns for European and Americanmarkets. In contrast, Zarowin [1989] discovered size anomalies, but found no evidencefor overreaction to news announcements. Amihud et al. [1999] found evidence for thesize of shareholders effect on stock price. Bernard and Thomas [1990] went on to point

CHINESE STOCK MARKETS 319

out that new information exerted its full influence on the stock price within 1 h afterdisclosure. There appears, therefore, to be very little evidence for the European and theAmerican markets not being semi-strong-form efficient.

In China, however, event studies based on information disclosure only commenced inthe late 1990s. Zhao [1998] looked at the information content from earnings informationdisclosure in the Shanghai Stock Market by means of accumulated abnormal returns. Hefound evidence of both overreaction and under-reaction. Chen and Liu [1999] examinedthe impact of earnings information disclosure in both the Shanghai and ShenzhenMarkets using the OLS. They concluded that earnings announcements are rich enoughin information content to exert a significant influence on the market. However, there arefew studies on the precise effect of information disclosure on changes in yield. Moreover,the previous empirical studies disregard the non-constancy of the dispersal about themean of yield and stock price. Real markets often disobey the assumption of constantdeviation due to influence of various factors. It is necessary to introduce GARCH orEGARCH models to describe this varying deviation.

There are many other studies where the time varying nature of daily return dispersalabout the mean is modeled using GARCH models. For example, Bollerslev, et al. [1992]and Ritchken and Trevor [1999] applied the GARCH and EGARCH models to dispersalsabout the mean for daily return changes with asymmetric changes of the conditionaldeviation. However, no research in this regard has ever been conducted for the Chinesemarkets. This paper will use the EGARCH model to investigate the daily change of stockprices on Chinese markets and discover the precise quantitative relationship betweenyield change and earnings change given new information disclosure.

Data and Models

In a semi-strong-form efficient market, the yield should adjust instantaneously tounanticipated information. However, new information can also increase or reduce un-certainty in the market. Therefore, it would be expected that volatility (and, hence, theappropriate risk adjusted return) would also change. There are three probable cases.First, announcements have no significant effect on either the mean or the conditionalvolatility of the abnormal return changes on the days of their announcements. Second,announcements significantly affect the value of the abnormal return and the adjustmentprocess takes a significant amount of time. Third, announcements significantly affect theconditional volatility.

The first case indicates that information disclosure has no influence on the market.One could infer from this that the information has already been fully impounded into theprice, and that there is a strong-form efficiency. The second case indicates temporarydeviation from semi-strong efficiency if adjustment is not instantaneous. The third caseindicates that risk/uncertainty associated with a stock may be modified by the in-formation disclosure.

This paper aims to discover which of the above three cases is most likely to occur inthe Chinese stock markets. By establishing the EGARCH model for the data of dailychange of stock prices on the events window and testing for the overall significance of themodel, we will be able to find answers to our questions.

The data includes annual earnings announcement in Shanghai and Shenzhen StockMarkets, and the daily stock price returns for each stock where there has been anannouncement. The sample data fulfill two prerequisites. First, they encompass anannual earnings announcement within the period under analysis. Second, the requisitestock market prices are available a year before the annual announcement. In the year

320 SHUHONG KONG AND MAJID TAGHAVI

chosen there were 1,224 listed companies altogether, 698 in Shanghai and 526 inShenzhen. There were also 3,672 observations on the earnings and losses announcementdays and 23,680 observations on daily stock price returns in the period around theannouncement day.

The normal period chosen for studies on the European and American modern capitalmarket is often as long as 10 years, so that the influence of unusual or extraordinaryfactors on earnings information may be reduced or eliminated. Since the Chinesemarkets are still at the early stage of development, it is difficult to find a sample with astable group of member firms. Moreover, the very limited experience of trading on theChinese stock market means that it is much more difficult to explore what reallyconstitutes the regular and normal behaviour from which anomalies can be subtracted.Hence we take the latest year available instead.

The time window wrapped around each annual earnings information disclosure isj10 days to +10 days, for various earnings announcements, taken place in the year 2001in both Shanghai and Shenzhen stock markets. The purpose of the exercise is to analysethe impact of any change in EPS on returns by comparison with the previous year.

Daily returns are defined as follows:

Rt ¼ lnPt � lnPt�1ð Þ � 100 ð1Þ

where Pt is the closing prices of stocks on day t.Abnormal return is defined as follows:

ARjt ¼ Rjt � bRRj ð2Þ

where ARjj is the flow of abnormal return of j, and bRRj is the expected return (normalreturn). The expected return is calculated over all n sample data points, while theabnormal return is calculated over the event period.

bRRj ¼1

n

Xn

t¼1

Rjt ð3Þ

Chen and Chen [2002] show that expression (3) of abnormal return is superiorcompared to other complex models, because it ignores the disturbance noise to theexpected return. It could more effectively examine the stock price’s reaction on variousevents, especially in the case of such events which have weaker influences on stockprices.

The EGARCH model is an appropriate technique for any differentiated deviationmodeling, hence, to explain asymmetric change in the conditional deviation. EGARCHhas already been extensively applied in financial capital sequence analysis. Given thepotential for an increase in deviation, investors would require additional risk premium ascompensation, indicating that the return should be modeled as a function of deviation.Following a test for serial correlation, the M-EGARCH model chosen here would be oforder (1,1) as follows:

ARt ¼ �0 þ �1NEWYt þ �h

ffiffiffiffiffi

ht

p

þ "t ð4Þ

"t ¼ffiffiffiffiffi

ht

p

vt

ln ht ¼ �0 þ �hln ht�1 þ �1 NEWYtj j þ g NEWYtf g ð5Þ

8

>

>

>

<

>

>

>

:

CHINESE STOCK MARKETS 321

The variable ARt is the abnormal return on day t; t = j10, . . . ,+10. The variableNEWYt is �Y

Y , where Y is the stock price on day j10, and DY is the increase margin ofEPS compared to the previous year. In this model, ht is the conditional deviation ofreturn, and vt is a white noise.

Equation (4) represents the conditioned mean of abnormal return, while equation (5)determines the effect of new information on the deviation of the return. The testing ofthe three cases, mentioned earlier, is carried out by examining the sign and thesignificance of the coefficients of the news variables in the conditional mean and varianceequations. The news variables in the conditional mean equation would pick up the newseffects on the mean of the return changes on the days of their announcement. If theannouncements exhibit to have impact on the volatility of the changes, their non-linearinfluence would still be represented in the residuals of the conditional mean equation,after their linear influence have been removed. The coefficients of the news variables inthe conditional mean equation convey information regarding the effects of theannouncement on the price changes, which depend on the equilibrium relationshipbetween the announced economic variable and stocks prices.

As explained earlier, the focus of this paper is on the news effects on the conditionalmean and volatility of the stocks prices changes. Estimated coefficients of the newsvariables will reveal which of the three cases is supported. If there are no news effects oneither the conditional mean or variance of the changes, the news coefficients will not besignificantly different from zero and, hence, case (1) is supported. Case (2) is relevant ifthe news variables are significant only in the conditional mean equation. If the

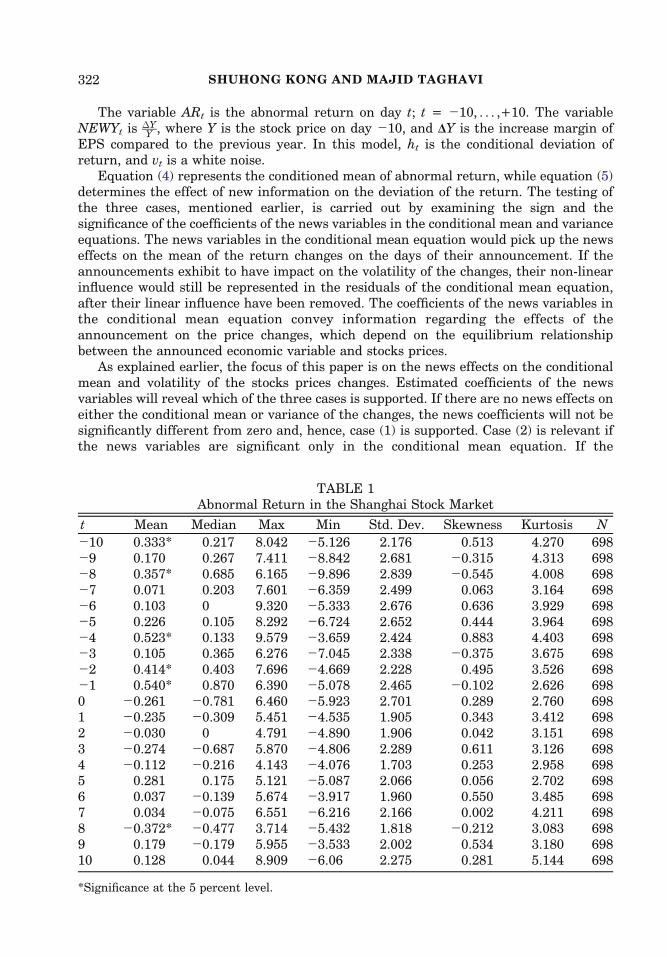

TABLE 1Abnormal Return in the Shanghai Stock Market

t Mean Median Max Min Std. Dev. Skewness Kurtosis N

j10 0.333* 0.217 8.042 j5.126 2.176 0.513 4.270 698j9 0.170 0.267 7.411 j8.842 2.681 j0.315 4.313 698j8 0.357* 0.685 6.165 j9.896 2.839 j0.545 4.008 698j7 0.071 0.203 7.601 j6.359 2.499 0.063 3.164 698j6 0.103 0 9.320 j5.333 2.676 0.636 3.929 698j5 0.226 0.105 8.292 j6.724 2.652 0.444 3.964 698j4 0.523* 0.133 9.579 j3.659 2.424 0.883 4.403 698j3 0.105 0.365 6.276 j7.045 2.338 j0.375 3.675 698j2 0.414* 0.403 7.696 j4.669 2.228 0.495 3.526 698j1 0.540* 0.870 6.390 j5.078 2.465 j0.102 2.626 6980 j0.261 j0.781 6.460 j5.923 2.701 0.289 2.760 6981 j0.235 j0.309 5.451 j4.535 1.905 0.343 3.412 6982 j0.030 0 4.791 j4.890 1.906 0.042 3.151 6983 j0.274 j0.687 5.870 j4.806 2.289 0.611 3.126 6984 j0.112 j0.216 4.143 j4.076 1.703 0.253 2.958 6985 0.281 0.175 5.121 j5.087 2.066 0.056 2.702 6986 0.037 j0.139 5.674 j3.917 1.960 0.550 3.485 6987 0.034 j0.075 6.551 j6.216 2.166 0.002 4.211 6988 j0.372* j0.477 3.714 j5.432 1.818 j0.212 3.083 6989 0.179 j0.179 5.955 j3.533 2.002 0.534 3.180 69810 0.128 0.044 8.909 j6.06 2.275 0.281 5.144 698

*Significance at the 5 percent level.

322 SHUHONG KONG AND MAJID TAGHAVI

announcements significantly affect the stocks prices and raise (lower) the volatility of thedaily changes, the coefficients in the deviation equation will be positive (negative) andsignificant, then case (3) is to be supported.

Empirical Results and Analysis

We have chosen 2,448 observations for EPS: a set of 1,224 for each of the years 2000and 2001. Of these, 698 cases relate to Shanghai and 526 to Shenzhen. The distributionalinformation for the 1,224 stocks is given in Tables 1 and 2.

Table 1 shows that there are five mean daily returns in the Shanghai market relatingto the pre-announcement being significantly and positively signed, whilst only one suchcase can be found being significant and negatively signed after the announcement. InTable 2, we found five cases of significantly positive estimates relating to pre-announcement and two negative cases to post announcement. There is also one case ofsignificant positive post-announcement in the Shenzhen market. However, these basicstatistical inferences are largely consistent with our basic hypothesis.

The estimated findings for the M-EGARCH model [equations (4) and (5)] are given inTables 3 and 4. Table 3 shows that in the Shanghai market the mean of a1 is positive andsignificant (at the 5 percent level) five days before the announcement, while it is positiveand significant (at the 10 percent level) two days after the announcement. Thus, a 1percent increase in EPS should on average lead to a 0.1102 percent increase in abnormal

TABLE 2Abnormal Return in the Shenzhen Stock Market

T Mean Median Max Min Std. Dev. Skewness Kurtosis N

j10 0.243 0.203 8.542 j7.600 2.928 0.003 4.119 526j9 0.461* 0.359 9.564 j8.106 3.066 0.560 4.122 526j8 0.292 0.279 8.156 j5.129 2.541 0.458 4.067 526j7 0.386* 0.170 8.058 j7.933 2.735 0.080 3.693 526j6 0.420* 0.256 5.988 j6.266 2.551 0.005 2.648 526j5 j0.230 j0.135 9.573 j5.711 2.349 0.398 5.261 526j4 0.545* 0.378 7.923 j6.589 2.338 0.262 3.925 526j3 0.292 0.264 8.464 j8.324 2.431 j0.047 5.359 526j2 j0.038 0.104 4.871 j5.135 2.278 j0.018 2.654 526j1 0.439* 0.142 8.358 j3.326 1.866 0.861 5.221 5260 0.442* 0.064 8.369 j4.953 2.801 0.535 3.187 5261 j0.054 0 5.283 j3.439 1.998 0.488 2.718 5262 0.231 0.189 9.592 j3.564 2.036 1.003 6.337 5263 j0.053 j0.120 7.080 j5.145 1.983 0.462 4.116 5264 j0.143 j0.149 9.531 j5.147 2.038 1.184 8.416 5265 0.134 0.279 5.446 j6.772 2.049 j0.404 3.845 5266 j0.389* j0.196 3.279 j5.291 1.829 0.214 2.740 5267 j0.015 0 7.031 j6.760 2.208 j0.056 4.078 5268 j0.381* j0.325 6.436 j6.519 2.483 0.729 5.292 5269 0.350* 0.135 6.259 j5.512 2.035 0.056 3.372 52610 j0.037 j0.168 7.648 j3.695 1.944 0.905 4.645 526

*Significance at the 5 percent level.

CHINESE STOCK MARKETS 323

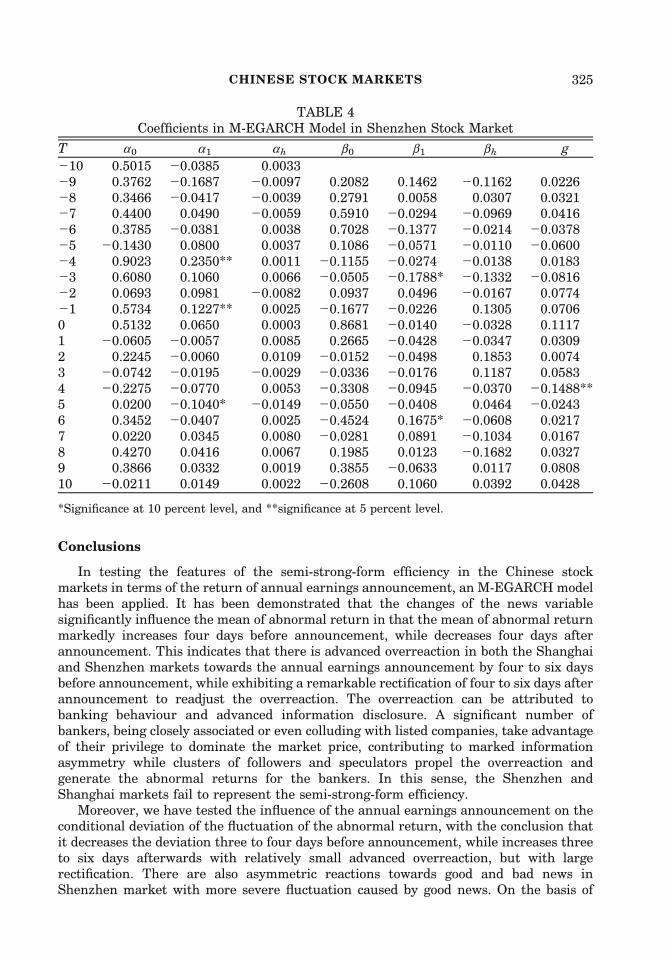

return five days before the announcement, followed by a further 0.0797 percent increasetwo days afterwards. There is no evidence here for retrenchment. From Table 4 it isevident that in the Shenzhen market the mean of a1 is positive and significant (at the 5percent level) four days and one day before the announcement, while it is negative andsignificant (at the 10 percent level) five days after the announcement. Thus, a 1 percentincrease on EPS should on average lead to 0.235 percent and 0.123 percent increases,respectively, on abnormal return four days and one day before announcement and onaverage 0.1 percent decrease after announcement.

The results are indicative of strong impact of NEWYt on the conditional volatility ofthe abnormal return via parameter b1. In the Shanghai market, the estimates of b1

suggest that volatility is increased by new information three and four days after theannouncement. In the Shenzhen market, by contrast, volatility is reduced three daysbefore the announcement and increased six days after announcement.

The parameter ah is not significantly different from zero for all periods in bothmarkets, which indicates that the conditional deviation does not significantly influencethe return. This may give rise to the extent of inappropriateness measure of risk, and,hence, suggesting that a Beta based measure of risk would be more appropriate thanindividual volatility. The parameter bh is found not to be significant, indicating thatthere is no persistence or autocorrelation in conditional deviation. The parameter g issignificant in only one case out of four, indicating a rather weak effect of news onconditional returns.

TABLE 3Coefficients in M-EGARCH Model in Shanghai Stock Market

T a0 a1 ah b0 b1 bh g

j10 0.2627 j0.0526 0.0013j9 0.1348 j0.0265 j0.0006 0.7326 j0.0978 j0.0609 0.0544j8 0.3667 0.0074 0.0052 0.7826 0.0195 j0.1002 j0.0282j7 0.1143 0.0328 0.0013 0.1154 0.0805 j0.1942 j0.0496j6 0.0590 j0.0331 j0.0028 0.2371 0.0447 j0.2502 j0.0118j5 0.3724 0.1102* 0.0063 0.4840 j0.0300 j0.2458 0.0866j4 0.6903 0.0503 0.0049 0.2178 0.0827 0.0016 0.0423j3 0.1687 0.0215 j0.0074 0.0244 0.0786 j0.0104 0.0350j2 0.5208 0.0053 j0.0018 j0.0831 j0.0177 0.1740 j0.0223j1 0.6458 0.0045 0.0056 0.4949 0.0716 j0.0475 0.05940 j0.3297 j0.0503 0.0031 1.1655 j0.0716 0.0026 j0.02901 j0.2133 0.0147 0.0072 j0.1843 0.0261 j0.0901 j0.06072 0.0710 0.0797* j0.0058 j0.3350 0.0109 j0.1899 0.00383 j0.2214 0.0400 0.0076 0.0374 0.1098* j0.0992 0.02524 j0.1090 j0.0020 j0.0016 j0.6297 0.1229* j0.0193 0.03855 0.3220 0.0310 j0.0027 0.1234 0.0622 j0.1826 0.05446 0.0236 j0.0100 0.0028 j0.5515 0.0862 0.1006 j0.01387 j0.0411 j0.0567 0.0083 j0.2135 0.0103 0.0552 j0.02638 j0.3293 0.0325 0.0055 0.0085 j0.0160 j0.0019 0.03359 0.0930 j0.0647 j0.0091 j0.2739 0.0524 j0.0914 j0.029010 0.1882 0.0453 j0.0078 0.1673 0.0185 j0.1406 j0.0249

*Significance at 10 percent level, and **significance at 5 percent level.

324 SHUHONG KONG AND MAJID TAGHAVI

Conclusions

In testing the features of the semi-strong-form efficiency in the Chinese stockmarkets in terms of the return of annual earnings announcement, an M-EGARCH modelhas been applied. It has been demonstrated that the changes of the news variablesignificantly influence the mean of abnormal return in that the mean of abnormal returnmarkedly increases four days before announcement, while decreases four days afterannouncement. This indicates that there is advanced overreaction in both the Shanghaiand Shenzhen markets towards the annual earnings announcement by four to six daysbefore announcement, while exhibiting a remarkable rectification of four to six days afterannouncement to readjust the overreaction. The overreaction can be attributed tobanking behaviour and advanced information disclosure. A significant number ofbankers, being closely associated or even colluding with listed companies, take advantageof their privilege to dominate the market price, contributing to marked informationasymmetry while clusters of followers and speculators propel the overreaction andgenerate the abnormal returns for the bankers. In this sense, the Shenzhen andShanghai markets fail to represent the semi-strong-form efficiency.

Moreover, we have tested the influence of the annual earnings announcement on theconditional deviation of the fluctuation of the abnormal return, with the conclusion thatit decreases the deviation three to four days before announcement, while increases threeto six days afterwards with relatively small advanced overreaction, but with largerectification. There are also asymmetric reactions towards good and bad news inShenzhen market with more severe fluctuation caused by good news. On the basis of

TABLE 4Coefficients in M-EGARCH Model in Shenzhen Stock Market

T a0 a1 ah b0 b1 bh g

j10 0.5015 j0.0385 0.0033j9 0.3762 j0.1687 j0.0097 0.2082 0.1462 j0.1162 0.0226j8 0.3466 j0.0417 j0.0039 0.2791 0.0058 0.0307 0.0321j7 0.4400 0.0490 j0.0059 0.5910 j0.0294 j0.0969 0.0416j6 0.3785 j0.0381 0.0038 0.7028 j0.1377 j0.0214 j0.0378j5 j0.1430 0.0800 0.0037 0.1086 j0.0571 j0.0110 j0.0600j4 0.9023 0.2350** 0.0011 j0.1155 j0.0274 j0.0138 0.0183j3 0.6080 0.1060 0.0066 j0.0505 j0.1788* j0.1332 j0.0816j2 0.0693 0.0981 j0.0082 0.0937 0.0496 j0.0167 0.0774j1 0.5734 0.1227** 0.0025 j0.1677 j0.0226 0.1305 0.07060 0.5132 0.0650 0.0003 0.8681 j0.0140 j0.0328 0.11171 j0.0605 j0.0057 0.0085 0.2665 j0.0428 j0.0347 0.03092 0.2245 j0.0060 0.0109 j0.0152 j0.0498 0.1853 0.00743 j0.0742 j0.0195 j0.0029 j0.0336 j0.0176 0.1187 0.05834 j0.2275 j0.0770 0.0053 j0.3308 j0.0945 j0.0370 j0.1488**5 0.0200 j0.1040* j0.0149 j0.0550 j0.0408 0.0464 j0.02436 0.3452 j0.0407 0.0025 j0.4524 0.1675* j0.0608 0.02177 0.0220 0.0345 0.0080 j0.0281 0.0891 j0.1034 0.01678 0.4270 0.0416 0.0067 0.1985 0.0123 j0.1682 0.03279 0.3866 0.0332 0.0019 0.3855 j0.0633 0.0117 0.080810 j0.0211 0.0149 0.0022 j0.2608 0.1060 0.0392 0.0428

*Significance at 10 percent level, and **significance at 5 percent level.

CHINESE STOCK MARKETS 325

our empirical investigation, it can be said that this paper supports the conclusion thatthe Chinese stock markets fail to represent a semi-strong-form efficient towards annualearning announcement.

References

Amihud, Y.; Mendelson, H.; Uno J. BNumber of Shareholders and Stock Prices: Evidence fromJapan,^ Journal of Finance, 3, 1999, pp. 1169Y83.

Balaban, E. BDays of the Week Effects: New Evidence from an Emerging Stock Market,^ AppliedEconomics Letters, 2 (5), 1995, pp. 139Y44.

Balaban, E.; Kunter, K. BFinancial Market Efficiency in a Developing Economy: The TurkishCase,^ Central Bank of Turkey, Discussion Paper 9611, 1996.

Bollerslev, Tim; Chou, Ray; Kroner, Kenneth. BGARCH Modeling in Finance: A Review of theTheory and Empirical Evidence,^ Journal of Econometrics, 52, 1992, pp. 1Y59.

Bernard, Victor; Thomas, Jacob. BEvidence that Stock Prices Do not Fully Reflect the Implicationsof Current Earnings for Future Earnings,^ Journal of Accounting and Economics, 13, 1990,pp. 305Y40.

Chen, Hanwen; Chen, Xiangmin. BEvent Reaction of Stock Price: Methodology, Background andApplication in the Chinese Stock Market,^ Economic Study, 1, 2002, pp. 8Y23.

Chen, Wei; Yang, Yuanxin. BEmpirical Study on the Policy Information Transmission Effect inShanghai Stock Market,^ Chinese Management Science, 3, 1999, pp. 18Y33.

Chen, Xiao; Liu, Zhao. BFeasibility Study on Stock Earning Report: Empirical Evidence fromShanghai and Shenzhen Stock Markets,^ Economic Study, 6, 1999, pp. 112Y36.

Cornelius, P. K. BMonetary Policy and Price Behaviour in Emerging Stock Markets,^ IMF WorkingPaper, 27, 1991.

V. BA Note on the Informational Efficiency of Emerging Stock Markets,^ Weltwirthschaftliches,129, 1993, pp. 820Y28.

Fama, Eugene F. BEfficient Capital Markets II,^ Journal of Finance, 46, 1991, pp. 1575Y617.Keane, S. BEmerging Markets: The Relevance of Efficient Market Theory,^ Occasional Research

Paper, 15, Chartered Association of Certified UK Accountants, 1993.Muradoglu, G.; Metin, K. BEfficiency of the Turkish Stock Exchange with Respect to Monetary

Variables,^ European Journal of Operational Research, 3, 1995, pp. 12Y34.Nelson, D. BConditional Heteroscedasticity in Asset Returns: A New Approach,^ Econometrica, 59,

1991, pp. 347Y70.Pettengill, G. M.; Jordan, B. D. BThe Overreaction by Hypothesis, Firm Size Stock Market

Seasonality,^ Journal of Portfolio Management, Spring, 1990, pp. 33Y62Ritchken, P; Trevor, R. BPricing Options Under Generalized GARCH and Stochastic Volatility

Processes,^ Journal of Finance, 1, 1999, pp. 377Y402.Zarowin, P. BDoes the Stock Market Overreact to Corporate Earnings Information?,^ Journal of

Finance, December, 1989, pp. 1385Y99.Zhao, Yulong. BInformation Content of Accounting Earning Information Disclosure: Empirical

Evidence from Shanghai Stock Market,^ Economic Study, 7, 1998, pp. 121Y44.

326 SHUHONG KONG AND MAJID TAGHAVI