the imf and the developing countries: evolving relations ... · the paper concentrates on relations...

TRANSCRIPT

WORKING PAPER

Overseas Development Institute 10-11 Percy Street London W1 P OJB Tel: 01-580 7683

9 m

ODI WORKING PAPER

No. 2

THE IMF AND THE DEmOPING COUNTRIES; EVOLVING RELATIONS, USE OF RESOURCES AND THE DEBATE OVER CONDITIONALITY

Graham B i r d *

*Research A s s o c i a t e , ODI and Senior L e c t u r e r , U n i v e r s i t y of Surrey

ODI Working Papers present i n p r e l i m i n a r y form work r e s u l t i n g from research undertaken under the auspices of the I n s t i t u t e . Views expressed are those of the authors and do not n e c e s s a r i l y r e f l e c t the views of ODI. Comments are welcomed and should be addressed d i r e c t l y to the authors.

March 1981

0 35003 0749

This paper d i v i d e s i n t o three main s e c t i o n s . The f i r s t examines r e l a t i o n s between the IMF and the developing c o u n t r i e s from an h i s t o r i c a l p e r s p e c t i v e . The second describes and analyses the use of Fund resources by Idcs, while the t h i r d presents the various arguments I'Tiiich have been r a i s e d concerning c o n d i t i o n a l i t y . The paper concentrates on r e l a t i o n s between the IMF and Idcs through the operation of the General Account and ignores the S p e c i a l Account.

1. i\nalyses of the S p e c i a l Account and i t s relevance to Idcs have been undertaken by the author and are a v a i l a b l e elsewhere, see f o r instance B i r d (1973) (1979).

I - A HISTORY OF IMF IIsVOLVF,T^HT V7ITII ECONOMIC STALILISATION IN DEVELOPING COUNT?ilES

The I n s t i t u t i o n a l framework

-Jhile Idcs exerted only a minimal i n f l u e n c e at the 1944 Brett o n Woods conference which l e d to the c r e a t i o n of the IMF, they were not completely excluded from i t and there was some debate on the problems of development. In d r a f t i n g the A r t i c l e s of Agreement, India.„ f o r instance, pushed hard f o r a reference to Idcs against the o p p o s i t i o n of the USA and there was an element of compromise i n the f i n a l v e r s i o n . Thus, while the A r t i c l e s d i d not make any d i s t i n c t i o n between developed and l e s s developed c o u n t r i e s , there was a d i r e c t reference to development, although whether the p r e c i s e wording of the A r t i c l e s has made any d i f f e r e n c e i n Fund a t t i t u d e s towards Idcs i s unclear. C e r t a i n l y the uniform l e g a l p o s i t i o n of a l l member countries has not prevented i t from adopting p o l i c i e s which have p r i m a r i l y favoured Idcs. Even soj a more s p e c i f i c commitment to development may have encouraged greater s e n s i t i v i t y to the problems which face Idcs (Marquez (1970)).

During i t s f i r s t years the Fund showed l i m i t e d concern w i t h the problems of developing c o u n t r i e s , regarding development as a r e l a t i v e l y unimportant i s s u e which was, i n any case, outside i t s terms of reference. In 1947-49 Western Europe accounted f o r three-quarters of t o t a l drawings from the IMF and Idcs f o r well under a q u a r t e r , ever, though post-war r e c o n s t r u c t i o n i n Europe was then being financed by Mar s h a l l A i d , the con d i t i o n s o f which l i m i t e d recourse to the IMF to 'ex c e p t i o n a l and unforeseen circumstances

Even s o , c e r t a i n changes i n the e a r l y 1950s x-tere b e n e f i c i a l to Idcs. Drawings on the gold tranche were made automatic and the f i r s t c r e d i t tranche became more e a s i l y a v a i l a b l e . In 1952 the stand-by concept was introduced. Upon the acceptance of a package of economic p o l i c i e s , stand-bys provided c o u n t r i e s w i t h an assured l i n e of c r e d i t . In the same year i t was announced that an agreed par value vrould no longer n e c e s s a r i l y be a p r e c o n d i t i o n of Fund a s s i s t a n c e .

1. Schleiminger (1970) has argued that i t would have been harmful to i n t e r n a t i o n a l monetary co-operation and thus to Idcs had the Fund d i f f e r e n t i a t e d betvreen various groups of c o u n t r i e s .

I t s annual reports during the e a r l y and mid 1950s, hor-jever, confirm that the Fund had l i t t l e s p e c i f i c i n t e r e s t i n the p a r t i c u l a r problems of Idcs as such. Fund p o l i c y continued to r e s t on the no t i o n that monetary s t a b i l i s a t i o n and free trade were i n the i n t e r e s t s of a l l members a l i k e .

In the l a t e 1950s and through the 1960s there was a s i g n i f i c a n t s h i f t i n the Fund's a t t i t u d e towards development. This r e s u l t e d i n innovations intended to a l l e v i a t e the monetary aspects of economic problems faced by Idcs. F i r s t , quotas were increased, e s p e c i a l l y small quotas. Second, the geographical d i s t r i b u t i o n of Fund lending s h i f t e d towards Idcs. T h i r d , i n 1961 the Managing D i r e c t o r s t a t e d that the IMF had a p o s i t i v e r o l e to p l a y i n promoting development through the p r o v i s i o n of short-term finance to co u n t r i e s e x p e r i e n c i n g ten^orary payments d i f f i c u l t i e s . Monetary s t a b i l i t y was s t i l l viewed as being the Fund's main o b j e c t i v e but t h i s was nox/ presented as necessary f o r s t a b l e development. Fourth, and a f t e r some i n i t i a l r e s i s t a n c e , the Fund accepted that export i n s t a b i l i t y c o n s t i t u t e d a s p e c i a l problem f o r developing countries that was not covered by e x i s t i n g f a c i l i t i e s and i n 1963 the Compensatory Financing F a c i l i t y (CFF) was introduced. Although open to a l l members, the CFF was of greatest b e n e f i t to primary product e x p o r t i n g c o u n t r i e s , and represented perhaps the f i r s t i n s t i t u t i o n a l response to the demands of Idcs. I n i t i a l l y compensation was a v a i l a b l e only on r e s t r i c t i v e terms, but i n 1966 lobbying by Idcs r e s u l t e d i n a l i b e r a l i s a t i o n , although the Fund continued to r e s i s t making the f a c i l i t y a u t o m a t i c a l l y a v a i l a b l e . As a f i f t h i nnovation the B u f f e r Stock Financing F a c i l i t y (BSFF) was set up i n 1969 to a s s i s t members f a c i n g payments d i f f i c u l t i e s as a r e s u l t of p a r t i c i p a t i o n i n i n t e r n a t i o n a l b u f f e r stock schemes. A l s o during the mid-1960s the Fund began to show concern over Idc indebtedness and p a r t i c i p a t e d i n n e g o t i a t i o n s concerning the debts of s e v e r a l Idc members (de V r i e s (1976) (1977)).

W r i t i n g i n 1967, Scott was able to conclude that "the overwhelming evidence i s that the Fund i s c u r r e n t l y doing a l l i t p o s s i b l y can to a s s i s t developing n a t i o n s w i t h i n i t s t r a d i t i o n a l sphere of ope r a t i o n s , but that i t i s r e s i s t i n g w i t h equal v i g o u r any s u b s t a n t i a l m o d i f i c a t i o n of t h i s very l i m i t e d sphere \ The s h i f t s i n a t t i t u d e occurred only w i t h i n what the Fund considered to be the c o n s t r a i n t s inposed by i t s A r t i c l e s of Agreement. Lending to Idcs remained constrained by quotas and the short term nature of the as s i s t a n c e (Mookerjee, 1966).

Perhaps, not c o i n c i d e n t a l l y , as the Fund was beginning to show greater awareness of Idc problems, i t s i n f l u e n c e over i n t e r n a t i o n a l monetary reform i n general v/as d i m i n i s h i n g . The General Arrangement to Borrow, the Basle Agreements and a system of b i l a t e r a l swap agreements were a l l e s t a b l i s h e d i n the 1960s and these m o d i f i c a t i o n s were organised by i n d u s t r i a l countries largel}' o u t side the IJIF. Even the e a r l y n e g o t i a t i o n s which e v e n t u a l l y l e d to the i n t r o d u c t i o n of the S p e c i a l Drawing Rights scheme were l a r g e l y conducted outside the IIIF, though i t was as a r e s u l t of pressure from the Fund that developing c o u n t r i e s were u l t i m a t e l y included i n i t (de V r i e s , 1976; Southard, 1979).

An apparently growing f e e l i n g w i t h i n the Fund that Idcs warrant s p e c i a l treatment continued i n t o the 1970s. During the d o l l a r c r i s i s of 1971, however, i n t e r n a t i o n a l monetary n e g o t i a t i o n s again took place l a r g e l y outside the IIIF and the voice of developing countries was f a i n t . The f a i l u r e of these moves to shore up the Bretton Woods system l e d to an attempt to make a f u l l assessment of the i n t e r n a t i o n a l monetary system and to produce a reform T-^hich virould cover a l l aspects of that system. This d i s c u s s i o n took place under the auspices of the Fund i n the Committee on Reform of the I n t e r n a t i o n a l Monetary System and Related Issues (The Committee of Twenty or C-20). The i n t e r e s t s of Idcs were w e l l represented, w i t h nine out of the twenty members. Two t e c h n i c a l groups set up by C-20 looked at is s u e s of s p e c i f i c concern to Idcs, namelj' the SDR/aid l i n k and the t r a n s f e r of r e a l resources. The Committee's report and 'Outline of Preform' ^ urged that future i n t e r n a t i o n a l monetary arrangements be organised so as, "to give p o s i t i v e encouragement to economic development and to promote an i n c r e a s i n g net floTJ of r e a l resources to developing countries'".

The report and 'Outline of Reform' of C-20 are s i g n i f i c a n t landmarks i n the e v o l v i n g r e l a t i o n s beti'/een the IMF and Idcs. For the f i r s t time Idcs p a r t i c i p a t e d f u l l y i n an attempt to remalce the i n t e r n a t i o n a l monetary system, and the proposed changes envisaged that the i n t e r n a t i o n a l monetary system should s p e c i f i c a l l y c a t e r f o r the problems of development. Some distance had been t r a v e l l e d from B r e t t o n Woods.

1. Committee on Reform of the I n t e r n a t i o n a l Monetary System and Related Issues, I n t e r n a t i o n a l Monetary Reform; Documents of the Committee of Twenty, IMF, Washington, 1974.

Although, subsequent to the G-20 d i s c u s s i o n s , the IMF has maintained i t s concern f o r Idcs' problems, the move towards f l e x i b l e exchange r a t e s and the i n c r e a s i n g s i g n i f i c a n c e of p r i v a t e f i n a n c i n g has eroded the c e n t r a l p o s i t i o n of the Fund i n the i n t e r n a t i o n a l monetary system (Crockett and H e l l e r (1978)) and Idcs have probably l o s t as a r e s u l t of t h i s .

Even so, the momentum generated by the C-20 has not been t o t a l l y d i s s i p a t e d . Indeed concern w i t h the problems f a c i n g Idcs has been enhanced by the r i s i n g p r i c e of o i l and i t s i m p l i c a t i o n s f o r o i l i n p o r t i n g Idcs. The economic s i t u a t i o n of the developing c o u n t r i e s and ways o f p r o t e c t i n g t h e i r economic growth from the e f f e c t s of vjorld i n f l a t i o n and r e c e s s i o n have become dominant themes at recent annual meetings, and have r e s u l t e d i n m o d i f i c a t i o n s to the operation of the IMF.

Fol l o w i n g a suggestion of C-20, a J o i n t M i n i s t e r i a l Committee of the Boards of Governors of the Bank and the Fund on the Tran s f e r of Real Resources to Developing Countries (Development Committee) was set up,^P^usyi^in£iug^Intemational monetary reform to economic development. The Committee has been concerning i t s e l f w i t h the t r a n s f e r of r e a l resources to Idcs, paying p a r t i c u l a r a t t e n t i o n to the l e a s t developed c o u n t r i e s and those Idcs most s e r i o u s l y a f f e c t e d by pajnnents d i f f i c u l t i e s .

F urther suggestions made by C-20 r e s u l t e d i n the establishment, i n 1974 f o r a two year p e r i o d , of an o i l f a c i l i t y the s p e c i f i c purpose of which was to a s s i s t c o u n t r i e s to cope vrith the pas^nents i m p l i c a t i o n s of the increased cost of o i l . To reduce the i n t e r e s t r a t e burden as s o c i a t e d w i t h OF drawings the Fund a l s o e s t a b l i s h e d a Subsidy Account to make concessionary a s s i s t a n c e a v a i l a b l e to low-income Idcs that had been most s e r i o u s l y a f f e c t e d by the o i l c r i s i s . The p a r t i a l i n s u l a t i o n from the i m p l i c a t i o n s of increases i n iiiq)ort p r i c e s provided by the OF and s u b s i d i s a t i o n of i n t e r e s t r a t e s were s i g n i f i c a n t changes i n the r e l a t i o n s h i p between the DIF and developing c o u n t r i e s .

As a f u r t h e r response to the d e t e r i o r a t i o n i n the world economic s i t u a t i o n the CFF was l i b e r a l i s e d i n 1975 and again i n 1979, and the percentage of quota that may be draxm from the Fund, e x c l u s i v e of CFF and BSFF drawings, has been r a i s e d to 600 per cent.

Other i n s t i t u t i o n a l changes w i t h i n the IMF, but not d i r e c t l y r e l a t e d to the world economic s i t u a t i o n , have been the i n t r o d u c t i o n of the Extended Fund F a c i l i t y (EFF) and the Trust Fund. The EFF, e s t a b l i s h e d i n September 1974, represented a response to another proposal put forti^ard by the C~20. I t i s designed to be of p a r t i c u l a r b e n e f i t to developing c o u n t r i e s , w i t h the purpose of p r o v i d i n g medium-term ass i s t a n c e to co u n t r i e s f i n d i n g themselves i n d i f f i c u l t i e s r e q u i r i n g p o l i c i e s o f a longer-term nature than those normally supported by ordi n a r y tranche dratd-ngs on the Fund. The EFF provides a s i g n i f i c a n t e x t r a dimension to Fund involvement w i t h the formulat i o n of economic p o l i c y i n member co u n t r i e s s i n c e , p r i o r to i t s i n t r o d u c t i o n the Fund had appeared to be d i r e c t l y and e x c l u s i v e l y i n t e r e s t e d i n short-term f i n a n c i a l s t a b i l i s a t i o n p o l i c i e s . The EFF gives some r e c o g n i t i o n to the f a c t that payments d i f f i c u l t i e s may c o n s t i t u t e the monetary m a n i f e s t a t i o n of s t r u c t u r a l m i s a l l o c a t i o n , and s p e c i f i c a l l y views the balance of payments i n the context of development p o l i c y .

The main purpose of the Trust Fund, e s t a b l i s h e d i n May 1976, i s to provide e l i g i b l e Idcs, b a s i c a l l y the l e a s t developed c o u n t r i e s , w i t h c o n d i t i o n a l but concessionary balance of payments a s s i s t a n c e . The Trust Fundus resources are derived l a r g e l y from gold s a l e s by the IMF but a l s o from loans and voluntary c o n t r i b u t i o n s . A s i g n i f i c a n t feature of the Trust Fund i s that i t s establishment has demonstrated a w i l l i n g n e s s by the IMF to use i n t e r n a t i o n a l monetary reform, i n t h i s case a reduction i n the r o l e of gold, as a way of b e n e f i t t i n g the poorest c o u n t r i e s i n the xrorld.

A f u r t h e r a d d i t i o n a l f a c i l i t y , which began to operate i n 1979, i s the Supplementary Fina n c i n g F a c i l i t y , the purpose of which i s to provide 'supplementary f i n a n c i n g , i n conjunction w i t h the use of the Fund's o r d i n a r y resources, to members of the Fund f a c i n g s e r i o u s pajnnents infcalances that are large i n r e l a t i o n to t h e i r quotas'. The SFF i s a h i g h - c o n d i t i o n a l i t y f a c i l i t y (as i s the extended f a c i l i t y ) and i s designed to support upper-tranche stand-bys or drawings under the extended f a c i l i t y . The repayment p e r i o d on SFF drat'/ings, however, i s longer than t h a t associated w i t h conventional stand-bys and t h i s may be of p a r t i c u l a r help to developing c o u n t r i e s i n which adjustment i s r e l a t i v e l y slow. A l a r g e r concessionary element to drawings under SFF w i l l be provided to low income c o u n t r i e s by the i n t r o d u c t i o n of a Subsidy Account designed to reduce the a s s o c i a t e d i n t e r e s t r a t e .

The Fund and s t a b i l i s a t i o n p o l i c y

As noted, s i n c e 1952 ord i n a r y drawings on the IMF have c o n v e n t i o n a l l y been made under stand-by arrangements which guarantee a l i n e of c r e d i t f o r a p e r i o d of time, u s u a l l y twelve months. The c r e d i t i s over and above the reserve tranche drawing and i s renewable. The gr a n t i n g of a stand-by arrangement depends on agreement between the Fund and the member about domestic economic p o l i c i e s .

F o l l o w i n g c o n s u l t a t i o n w i t h a Fund mission the member country signs a ' l e t t e r of i n t e n t ' which sets out the o b j e c t i v e s of i t s economic programme and the p o l i c i e s i t intends to pursue to r e a l i s e these o b j e c t i v e s . I f the s t a t e d i n t e n t i o n s meet the Fund's c o n d i t i o n s , the member i s assured by the stand-by arrangement that i t w i l l be able to purchase a s p e c i f i e d amount of f o r e i g n currency d u r i n g the l i f e of the arrangement. The stand-by guarantees that the f i r s t c r e d i t tranche w i l l be a v a i l a b l e i n f u l l and w i l l not depend on a c t u a l economic performance. The a v a i l a b i l i t y of subsequent c r e d i t tranches, hoxrever, depends on the observance of 'performance c r i t e r i a ' . These have been defined as 'aspects of a member's p o l i c i e s , formulated i n the l e t t e r of i n t e n t i n q u a n t i f i e d and other o b j e c t i v e terms, that are of c r u c i a l importance f o r the success of the programme, so that i f any of them i s not observed there i s a s i g n a l that the member of the Fund should c o n s u l t on any necessary adaptation of the programme before the member resumes purchases under the stand-by arrangement". The finance i s thus i n e f f e c t 'phased'•

Members may a l s o draw on the s p e c i a l f a c i l i t i e s already described. Again access t o each of these i s c o n d i t i o n a l and r e s t s on the acceptance and r e a l i s a t i o n of s p e c i f i e d o b j e c t i v e s and p o l i c i e s . In the case of the CFF and RSFF the c o n d i t i o n s are not very harsh and are comparable w i t h the c o n d i t i o n s t h a t apply to drawings under the f i r s t c r e d i t tranche. Drawings under the EF and SFF are subject to much harsher c o n d i t i o n s , s i m i l a r to those attached to upper c r e d i t tranche drawings.^

1. F u r t h e r d e t a i l s of the range of Fund f a c i l i t i e s may be found i n IMF Annual Reports, IMF Survey and Chapter 1 of t h i s study.

D i r e c t e d by i t s own A r t i c l e s of Agreement to concentrate on the short term c o r r e c t i o n o f the balance of payments, the management of i n t e r n a l demand has always been an i n p o r t a n t component of Fund programmes w i t h bank c r e d i t used as the p r i n c i p a l i n d i c a t o r of o v e r a l l demand. A l l programmes include a c e i l i n g f o r t h i s v a r i a b l e even though t h i s does not always i n v o l v e a d e c e l e r a t i o n i n the growth of c r e d i t . C o n t r o l s on c r e d i t expansion i n v o l v e c e i l i n g s on the growth of net domestic c r e d i t by the c e n t r a l bank or the banking system and sometimes i n v o l v e a s p e c i f i c c e i l i n g on the amount of c r e d i t to be extended to the p u b l i c s e c t o r . C e i l i n g s on domestic c r e d i t to government c l e a r l y have f i s c a l i m p l i c a t i o n s and Fund programmes o f t e n i n v o l v e r a i s i n g p u b l i c e n t e r p r i s e p r i c e s and reducing s u b s i d i e s . Rather l e s s f r e q u e n t l y they i n v o l v e a dev a l u a t i o n of the exchange r a t e . Removal of exchange and trade r e s t r i c t i o n s i s a l s o a frequent component of Fund programmes and more r e c e n t l y p o l i c i e s r e l a t i n g to e x t e r n a l indebtedness, such as a c e i l i n g on the a c q u i s i t i o n of new e x t e r n a l debt, have been i n c l u d e d . Less f r e q u e n t l y included are p r i c e s and incomes p o l i c i e s . Examination of published evidence on stand-bys (Reichmann and S t i l l s o n (1978), Reichraann (1978)), suggests that the Fund has viewed over-expansionary domestic demand p o l i c y as the s i n g l e most important cause of payments imbalances i n developing c o u n t r i e s .

Any informed assessment of the e v o l u t i o n of the Fund's approach to s t a b i l i s a t i o n i s made d i f f i c u l t by the c o n f i d e n t i a l i t y w i t h which much of the m a t e r i a l i s t r e a t e d . Observations can however be made from published m a t e r i a l . C e r t a i n l y the whole t h r u s t of stand-by arrangements from t h e i r i n c e p t i o n has been to b r i n g about a reasonably prompt improvement i n the e x t e r n a l p o s i t i o n of the borrowing country.

Iifhile the range of p o l i c i e s supported by the Fund does not seem to have a l t e r e d d r a m a t i c a l l y over the years, the i n c r e a s i n g i n t e r e s t i n f i n a n c i a l programming shown by the Fund si n c e the l a t e 1960s has brought w i t h i t an increase i n the degree of p r e c i s e q u a n t i t a t i v e s t i p u l a t i o n (de V r i e s (1976)). ^

In the e a r l y 1970s Executive D i r e c t o r s began to show a keen i n t e r e s t i n the ways i n which programmes were formulated, the models on which they were based, and the e f f e c t s they had on key economic v a r i a b l e s .

1. With regards e q u i t y of treatment between developed and developing c o u n t r i e s , and since the Review of Stand-bys i n 1968 the terms

cont'd over...

This l e d the Fund to study a nuniber of questions: 'Was a monetarist a n a l y s i s e q u a l l y a p p l i c a b l e to both developed and developing c o u n t r i e s ? Were there not i n p o r t a n t d i f f e r e n c e s between c o u n t r i e s i n respect of the t r a n s m i s s i o n mechanism e x p l a i n i n g how monetary i n f l u e n c e s a f f e c t r e a l output, employment and the p r i c e l e v e l ? ... To v/hat extent d i d programmes based on c r e d i t c e i l i n g s a f f e c t domestic employment and the d i s t r i b u t i o n of income? Were aggregative techniques u s e f u l f o r i n f l u e n c i n g the newly emerging socio-economic o b j e c t i v e s of enhancing employment and r e d i s t r i b u t i n g income?' (de V r i e s (1976)). In the e a r l y 1970s, then, there seemed to be the beginning of a r e a p p r a i s a l of the Fund's involvement i n economic s t a b i l i s a t i o n . The outcome of t h i s r e a p p r a i s a l , -t ^ i c h was made more necessary by events i n the 1970s i s , one suspects, being r e f l e c t e d by the changes i n p o l i c y w i t h regards both the content of programmes and the p e r i o d of repayment, t h a t have been made more r e c e n t l y .

In the past the Il'lF has tended to respond to pressures from developing c o u n t r i e s by e n l a r g i n g the range of i t s f a c i l i t i e s r a t h e r than by changing i t s p o l i c y c o n d i t i o n s . In the l a t e 1970s and e a r l y 1980s,

cont'd from previous page

of stand-bys do not seem t o have r a i s e d the c r i t i c i s m t hat they are of themselves harsher f o r developing than f o r developed c o u n t r i e s , though there i s the c r i t i c i s m that the a l l e g e d standard package may be l e s s appropriate f o r developing c o u n t r i e s . The Review f o l l o w e d a drawing by the United Kingdom which took the Fund's h o l d i n g of s t e r l i n g to almost 200 per cent of the UK quota. There can be l i t t l e doubt that the c o n d i t i o n s attached to t h i s p a r t i c u l a r upper tranche drawing were s i g n i f i c a n t l y and uniquely more l e n i e n t than those which had been attached to stand-bys negotiated between the Fund and various developing c o u n t r i e s , (de V r i e s (1976), Southard (1979)). There were no q u a n t i t a t i v e performance ta r g e t s set and no phasing. The Fund defended i t s p o s i t i o n by p o i n t i n g to the importance of s t e r l i n g as an i n t e r n a t i o n a l currency.

Developing c o u n t r i e s at t h i s stage endeavoured to persuade the Fund to move towards the uniform adoption of the type of stand-by arrangement that had been negotiated w i t h the UK, i n c o r p o r a t i n g as i t d i d an emphasis on general p o l i c y measures and c o n s u l t a t i o n r a t h e r than p r e c i s e q u a n t i t a t i v e t a r g e t s . Instead the Review confirmed what, i n e f f e c t , had been standard p r a c t i c e p r i o r to the 1967 UK episode. Q u a n t i t a t i v e performance c r i t e r i a were r e t a i n e d f o r drav/ings beyond the f i r s t c r e d i t tranche, and the emphasis remained on the c o n t r o l of c r e d i t , though performance clauses were t o be l i m i t e d to " s t i p u l a t i n g c r i t e r i a necessary to evaluate the implementation of the member's f i n a n c i a l s t a b i l i s a t i o n programme." Phasing was a l s o r e t a i n e d f o r such drawings except when the purpose of the stand-by was to maintain confidence i n a member's currency.

Thus although developing c o u n t r i e s d i d not achieve the l e s s onerous terms that they i d e a l l y wanted they d i d ensure that they would not be r e q u i r e d to meet r e l a t i v e l y harsh c o n d i t i o n s as compared w i t h developed c o u n t r i e s .

however, p o t e n t i a l l y s i g n i f i c a n t changes have talcen place i n the form of lengthening the p o s s i b l e p e r i o d of repayinent f o r stand-bys (to three years) and the extended f a c i l i t y drawings (to ten y e a r s ) , and i n the form of the 1979 Review of the Guid e l i n e s on C o n d i t i o n a l i t y . These changes could turn out to be s t r a t e g i c . The lengthening o f the repayment p e r i o d may enable countries to pursue r a t h e r longer-term balance of payments p o l i c i e s and t h i s may a l l o w the Fund to put greater emphasis on s t r u c t u r a l l y o r i e n t e d p o l i c i e s , and on supply, as opposed to demand, management. Indeed the Fund i s c u r r e n t l y i n the process of studying how i t s adjustment p o l i c i e s can be best designed and implemented, " t T i t h a view to enhancing the supply side of ... menibers' economies and t h e i r long term p o t e n t i a l f o r growth.^ The nature of the r e l a t i o n s h i p between s t a b i l i t y and development w i l l t h e r e f o r e become an i s s u e of great s i g n i f i c a n c e f o r the Fund as the movement towards longer term c r e d i t s continues.

^{'hile the 1979 Review of Guidelines on C o n d i t i o n a l i t y endorses the Fund's b e l i e f i n c o n d i t i o n a l i t y , i t includes changes from the previous p o s i t i o n . F i r s t , the Review encourages c o u n t r i e s to turn to the Fund 'at an e a r l y stage of t h e i r balance of payments d i f f i c u l t i e s or as a precaution against the emergence of such d i f f i c u l t i e s ' . Second, there i s a cautious move towards extending the time over which stand-by drawings may be made, though the normal p e r i o d remains twelve months. S i g n i f i c a n t l y Gold maintains t h a t , 'a reason f o r c a u t i o n about longer periods as a more normal p r a c t i c e i s the u n d e s i r a b i l i t y of b l u r r i n g the d i s t i n c t i o n between balance of pajrments a s s i s t a n c e and development f i n a n c i n g . ' T h i r d , the Review st a t e s t h a t , 'the Fund w i l l pay due regard to the domestic s o c i a l and p o l i t i c a l o b j e c t i v e s , the economic p r i o r i t i e s , and the circumstances of members, i n c l u d i n g the causes of t h e i r balance of payments problems.' I t seems to have been accepted then that c e r t a i n p o l i c i e s may be necessary to maintain p o l i t i c a l and s o c i a l s t a b i l i t y and that t h i s should be taken i n t o account i n d e v i s i n g an economic programme. However, an e l u c i d a t i o n of the phrase 'economic p r i o r i t i e s ' by Gold makes i t c l e a r t h a t , while the Fund i s aware of the p o t e n t i a l l y adverse e f f e c t s V7hich p o l i c i e s d i r e c t e d p r i m a r i l y towards short term macroeconomic s t a b i l i t y may have on long term development, and i s anxious to avoid these,

1. Thus Gold (1979) p o i n t s out that w h i l e 'most of the d e c i s i o n i s d e c l a r a t o r y of the p r a c t i c e that has emerged i n the years since 1968 ,.. the d e c i s i o n i n c l u d e s c e r t a i n new or c l a r i f i e d elements, l a r g e l y i n deference to the viev/s of developing members', who f e e l that the Fund's c o n d i t i o n a l i t y has been, 'too severe i n r e l a t i o n to them.' Subsequent quotations i n t h i s s e c t i o n are a l s o from Gold (1979) unless otherwise s t i p u l a t e d .

i t r u l e s out the use of Fund resources to help s t r u c t u r a l change. The Fund s t i l l f e e l s unable to provide a s s i s t a n c e unless adjustment can be achieved w i t h only the tenq?orary use of i t s resources. The emphasis remains on what are e s s e n t i a l l y short term p o l i c i e s . Although the reference to the causes of payments probleiris represents some r e c o g n i t i o n that payments d i f f i c u l t i e s i n developing c o u n t r i e s may r e s u l t from f a c t o r s beyond t h e i r c o n t r o l , the Fund r e t a i n s the view that 'members must adjust t h e i r balance of pajnnents whatever may be the o r i g i n of t h e i r problems.' There i s no formal r e c o g n i t i o n that d i f f e r e n t causes r e q u i r e d i f f e r e n t p o l i c i e s , even though i n f o r m a l l y the Fund does c l a i m to take account of the sources of balance of payments d i f f i c u l t i e s and t o be somewhat l e s s s t r i c t where these are e x t e r n a l l y generated. Fourth,the Review suggests that the Fund continues to want to avoid becoming h e a v i l y i n v o l v e d i n a country's economic, and by i m p l i c a t i o n p o l i t i c a l and s o c i a l l i f e , c o n c e n t r a t i n g on aggregate macroeconomic v a r i a b l e s r a t h e r than the mechanisms by which t a r g e t s are achieved.

F i n a l l y the Review s t a t e s that the Fund intends to keep a l l aspects of stand-bys and t h e i r r e l a t e d c o n d i t i o n a l i t y under s c r u t i n y . Some research on c o n d i t i o n a l i t y has already been undertaken both w i t h i n the Fund and elsewhere (Reichmann (1978), Reichmann and S t i l l s o n (1978), Connors (1979)) and i t would seem l i k e l y t h a t , i n p a r t , i t was as a

t h a t r e s u l t of t h i s research/tHe 1979 r e a p p r a i s a l was made. The evidence suggests that w h i l e Fund p o l i c i e s have caused economies t o move i n the d i r e c t i o n s intended there has been r e l a t i v e l y l i t t l e success i n r e a l i s i n g s p e c i f i c u l t i m a t e t a r g e t s . Thus although i n the c l e a r m a j o r i t y of cases intermediate targets on c r e d i t expansion, f o r i n s t a n c e , have been r e a l i s e d , and the p r i n c i p a l purpose of the stand-by achieved, i n terms of trade l i b e r a l i s a t i o n f o r example, the e f f e c t of stand-by programmes on u l t i m a t e t a r g e t s such as economic growth, i n f l a t i o n and the balance of payments has been much l e s s marked.

The apparent general f a i l u r e of p r e c i s e macroeconomic t a r g e t i n g suggests that the Fund i s becoming i n c r e a s i n g l y s c e p t i c a l of the scope f o r f i n e t u n i n g i n developing c o u n t r i e s and that i t i s beginning to favour a broadly based and longer term macroeconomic p o l i c y approach % i l e the new g u i d e l i n e s on c o n d i t i o n a l i t y permit a s i g n i f i c a n t a l t e r a t i o n i n the nature of Fund involvement i n economic management.

t h e i r e f f e c t w i l l depend c r u c i a l l y on hov; they are i n t e r p r e t e d i n p r a c t i c e . Statements by Fund personnel f a i l to c l a r i f y j u s t how s i g n i f i c a n t a change there has been i n the Fund's adjustment p o l i c y . Monetary s t a b i l i t y s t i l l seems to be viewed as a p r e r e q u i s i t e f o r economic development. In a speech d e l i v e r e d i n 1980 the, Managing D i r e c t o r maintained t h a t , "sound adjustment means, above a l l , implementation of f i s c a l and monetary p o l i c i e s designed to avoid overconsumption i n r e l a t i o n to a v a i l a b l e resources and to prevent waste or mismanagement of those resources. In t h i s connection, there i s one simple t r u t h which must be recognised; when demand i s s t i m u l a t e d by measures which are r a p i d l y d i s s i p a t e d i n higher p r i c e s , t h i s stimulus i s f r u i t l e s s , or counterproductive, from the standpoint of development and growth, as w e l l as dangerous from the standpoint of i n f l a t i o n and balance of payments s t a b i l i t y . A more p o s i t i v e c o n s i d e r a t i o n i s that the adoption and p u r s u i t of s u i t a b l e adjustment programmes i n cooperation w i t h the Fund g e n e r a l l y tends, through enhancement of the c r e d i t w o r t h i n e s s of borrovi;ing c o u n t r i e s , to f a c i l i t a t e the a t t r a c t i o n of p r i v a t e c a p i t a l . The resources of the Fund and adjustment programmes of the type that i t sponsors thus seemm to me to be i n d i s p e n s a b l e elements i n the f o s t e r i n g of investment and economic growth." However he d i d go on to p o i n t out t h a t , "they c l e a r l y do not represent comprehensive s o l u t i o n s f o r the d i f f i c u l t i e s now confronted." Such remarks make i t p l a i n that the s h i f t from demand management towards supply management i s e a s i l y exaggerated. The Fund remains p r i m a r i l y committed to what i t sees as sound i n t e r n a l f i n a n c i a l p o l i c y . I f there has been a change i n emphasis i t seems to be that the Fund now recognises that sound f i n a n c i a l p o l i c y may not be s u f f i c i e n t to ensure development, that the short term costs of some of the p o l i c i e s i t has supported may have been underestimated and that the p o l i c i e s may have concentrated too much on the s o l e o b j e c t i v e of b r i n g i n g about a short run improvement i n the balance of payments. I f t h i s i s an accurate i n t e r p r e t a t i o n the change could indeed be s i g n i f i c a n t .

From being viewed i n i t s e a r l y years an an i n s t i t u t i o n which had no s p e c i a l concern f o r the problems of developing c o u n t r i e s , more recent reviews see the Fund as having become, or at l e a s t as being w e l l on the way to becoming, an i n s t i t u t i o n vrhose only r o l e i s that of a s s i s t i n g the poorer c o u n t r i e s f o r whom the p r i v a t e f i n a n c i a l markets do not provide a f e a s i b l e a l t e r n a t i v e (Southard (1979), Williamson (1979));

A major problem w i t h t h i s apparent t r a n s i t i o n i s , howeverj that the A r t i c l e s of Agreement define the Fund's r e s p o n s i b i l i t i e s as p r o v i d i n g short run balance of payments finance, not longer run development a s s i s t a n c e . Although t h i s d i s t i n c t i o n i s not always c l e a r i n p r a c t i c e , the A r t i c l e s do c o n s t r a i n the Fund's involvement w i t h c o u n t r i e s where balance of payments adjustment i s seen as a long term process. I t i s therefore not c l e a r e x a c t l y how f a r the t r a n s i t i o n w i l l be able t o proceed under the IMF's e x i s t i n g A r t i c l e s and r u l e s . C u r r e n t l y the Fund i s caught i n the awlcward p o s i t i o n of h e l p i n g to deal w i t h problems f o r which i t s cKm r u l e s and procedures may not i d e a l l y equip i t .

1. Fo. a f u l l e r d i s c u s s i o n of the IMF's A r t i c l e s and Agreement and the p o t e n t i a l c o n f l i c t between short term s t a b i l i s a t i o n , the major o b j e c t i v e of the Fund, and long term developn^nt, the major o b j e c t i v e of developing c o u n t r i e s , see B i r d (1978) (1979).

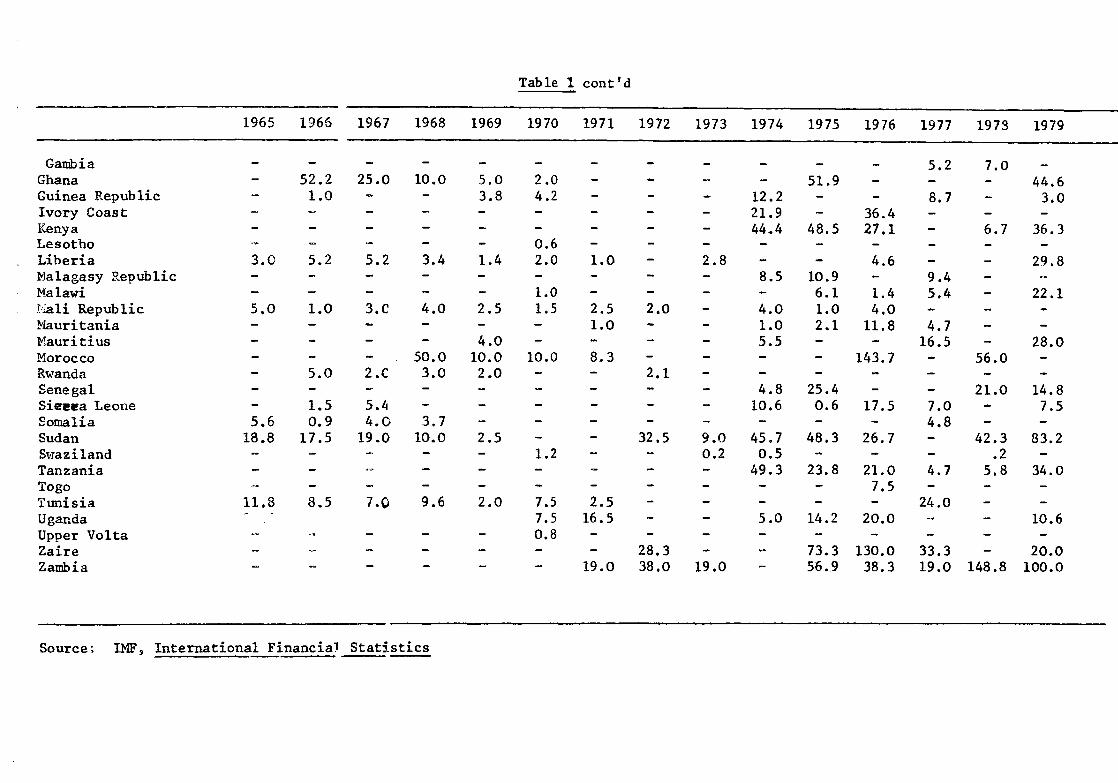

Table 1. T o t a l Idc draxnngs on the Fund, 1965-79 (SDR m i l l i o n s )

1965 19 5C 1967 1968 1969 1970 1971

Less-developed areas 436.5 556.3 410.0 688.6 385.2 326.3 427.0 O i l - e x p o r t i n g c o u n t r i e s - -• 40.0 100.8 65.8 90.8 2.9 Indonesia - - - 45.0 65.8 38.0 2.9 Ira n - - 46.5 - 16.8 -Iraq - 40.0 - - 27,3 -K i g e r i a - - - 9.3 - 3.8 -Other T'Jestern Iiemispherel47.2 174.0 122.7 273.5 177.2 124.1 173.3 A r g e n t i n a - 47.5 - - - - 5.2 i k s l i v i a - - 12.0 11.0 - 4.5 B r a z i l 75.0 - 75.0 " - -C h i l e 35.0 30.0 10.0 43.3 29.0 -- 77.5 GolcJibia -• 37.6 71.4 34.8 33.3 29.3 30.0 Costa Rica 10.0 6.6 2.8 - - 1.8 6.0 Doiriinican Rep. 5.0 S.fe ~ - 14,0 - 7,5 Ecuador 11.0 6.3 - 18.0 10.0 -SI Salvador _ 20,C 5.0 3.0 12.3 - 9.0 Guateu:aia 5.0 7.0 10.0 3.0 6.0 - -7 a i t i 2.5 4.6 2.3 - 1.5 - -Honduras 2.5 - - - 6.3 -Mexico ~ - - - - -Kicaraj^ua - - 19.0 14.0 10,0 3.0 Panama 2.7 - - 3.0 5.4 — 1,0 Paraguay — — — — — Peru - 21.3 46.3 30.0 18,0 16.0 Uruguay - 5.0 29.5 1.8 40,4 9.5 Barbados - — — Grenada - — — — Guyana - - -

_ 4.0 J a E a i c a — 3,8 T r i n i d a d & Tobago . . . — — 4.3 *- 4.8

796.1 315.1 1700 2038.9 2749.0 4.2 - - 80.0 2.7 - - 80.0

1.5 - - - - - - -447.9 89.0 308.9 610.2 1192.6 153.7 177.9 485.1 284,0 - - 311.3 269.5 _ - -

4.3 18.2 - 4.7 - - 15.0 8.7

41.0 - 120.5 176.8 124.4 ^ ^ -

21.5 12.0 6.8 - - 20.5 10.8 10.8 21.5 15.0 - 68.3

8.9 8.9 - - 17.6 - - -8.8 - 22.4

3.7 7.5 4.5 4.9 3.0 23.0 - - -

- - - - 416.9 100.0 4.0 12.0 3,3 12.2 - - 6.8 43.1

16.4 10.2 25.1 -- - 6.0

61.5 - ~ - 189.5 10.0 $.5 177.0 22.3 16.4 65.3 53.2 38.0

6.5 ~ 1.3 0.4 - - .7

4.6 5.0 - 22.3 - 12.'; 12.9 13.3 13.7 13.3 13.3 55.7 19.2 57.8 145.8

6.6 -

1955 196 5 1967 1968 1969 1970 1971 1972 1973 1974 1975 1976 1977 1978 1979

Other l i i d d l e East 15.0 11.7 9.5 63.0 54.5 21,0 56.5 25.0 49.9 131.0 191.8 255.8 117.5 147.4 Bahrain 15.0 11.7 S.5 63.0 54.5 21,0 56.5 25.0 49.9 131.0 191.8 255.8 117.5 147.4 -Cyprus - 0.9 - - - - - - - 12.9 1.7 35.0 - 9.9 Egypt 15.0 7,5 - 63.0 - 17.5 32.0 47.0 40.0 - 125.7 105.0 75.0 -I s r a e l - - - 45.0 - 20.0 - - 65.0 175.8 77.0 - 72.4 -Jordan - - - - -- 4,5 - 2.9 - - - - - -S y r i a 3,3 9.5 9.5 3.0 - 25.0 - - - - 12.5 - -Yemen Arab S a p u b l i c - - - - - 0.5 - - - - - - - - -Yemen, Peopl3's Dem Rep. - - - - - - - - 13.1 14.3 13.2 - - -Other A s i a 278.2 273.8 162.3 152.6 61,0 53.5 140,8 215.2 145.4 1025.9 782.8 776.4 295.7 334,9 355.7 Afg h a n i s t a n 1.7 9.1 4.0 4.8 13.0 4.0 - - 7.5 2,5 8.5 - - - -Bangladesh .„ - - - - - - 62.5 0.8 71.2 58.8 97.2 -- - 57.0 Burma - - l i . O 4.5 - 12.0 6.5 -- 13.5 29,5 9.5 - 25.0 25.0 15.0 Cambodia - - - - - 6.3 6.3 6.3 - - - — — — China, Per. of - - - - - - 59.9 - - - 59.9 - - - -I n d i a 200.0 225,0 9( .0 - - - - - - 573.2 201.3 - - - -Korea - - 12.5 - - 7.5 - - 130.0 107.3 104.4 - - -Laos - - - - - 0.5 - - - - 6.5 3.3 - 4.0 -M a l a y s i a - - • - - - 11.7 - - - - 93.0 - - -Nepal - ~ • - - - - - - - - 7.6 - 8.5 -P a k i s t a n 53.5 9,5 - 40.0 35.0 - - 84.0 60.0 129.9 161.4 107.2 67.0 40.0 21.2 S r i Lanka 23.0 30.3 2! .8 35.3 13.0 9.5 14.0 25.3 18.6 46.9 42.1 28.2 55.0 38.0 80.0 T h a i l a n d - - • - - - 2.2 - - - 67.0 - 101.3 45,3 Vietnam - - • - - - - - - - - 15.5 31.0 22.5 -F i j i - • — - - — — _ 2,6 _ _ 8.4 „ „

Papua New Guinea - - • - - - - - - - - 29.8 Uestem Samoa — • — — - — - - - 1.6 0.7 .5 1.6 ,7

Other A f r i c a 45.1 96,8 75.6 98.7 36.7 36.9 53.6 103.8 31.0 235.0 374.2 524.2 1035.2 1210.7 ; 1769.9 Burundi 2.0 3,9 5.0 5.0 3.5 2.5 1.5 - - 2.0 1.3 — — _ — Cameroon - • - - - - - - 11.5 7.5 21.8 — — C e n t r a l A f r i c a n Empire - - • - - 1.3 - - 3.2 2.3 6.1 - - — Chad - - - - 3.8 - - - 5.0 - 6.5 — - — Congon People's Republic - - - - - - - - - - - 13.2 3.3 2,0 E q u a t o r i a l Guinea - - - - - - 1.0 - - - - 1.8 - -

1965 1965 1967 1968 1969 1970 1971 1972 1973 1974 1975 1976 1977 1973 1979

Gaidbia _ _ — _ 5.2 7.0 Ghana - 52.2 25.0 10.0 5.0 2.0 - - - - 51.9 - — — 44.6 Guinea R e p u b l i c 1.0 - - 3.8 4.2 - - - 12.2 - - 8.7 - 3.0 Iv o r y Coast - - - - - - - - 21.9 - 36.4 - - -Kenya - - - - - - - - - 44.4 48.5 27.1 - 6.7 36.3 Lesotho - - - - - 0.6 - - - - - - - - -L i b e r i a 3.0 5.2 5.2 3.4 1.4 2.0 1.0 - 2.8 - - 4.6 - - 29.8 Malagasy R e p u b l i c - - - - - - - - - 8.5 10.9 - 9.4 - --Malawi - - - - - 1.0 - - - - 6.1 1.4 5.4 - 22.1 M a l i R e p u b l i c 5.0 1.0 3.C 4.0 2.5 1.5 2.5 2.0 - 4.0 1.0 4.0 - - -M a u r i t a n i a -- - - - - - 1.0 - - 1.0 2.1 11.8 4.7 - -M a u r i t i u s - - - - 4.0 - - - - 5.5 - - 16.5 - 28.0 Morocco - - - 50.0 10.0 10.0 8.3 - - - - 143.7 - 56.0 -Rwanda - 5.0 2.C 3.0 2.0 - - 2.1 - - - - - - -Senegal - - - - - - - - - 4.8 25.4 - - 21.0 14.8 Sieeea Leone - 1.5 5.4 - - - - - - 10.6 0.6 17.5 7.0 - 7.5 Somalia 5.6 0.9 4.0 3.7 - - - - - - - - 4.8 - -Sudan 18.8 17.5 19.0 10.0 2.5 - - 32.5 9.0 45.7 48.3 26.7 - 42.3 83.2 Swaziland - - - - 1.2 - - 0.2 0.5 - - - .2 -Tanzania - - - - - - - - 49.3 23.8 21.0 4.7 5.8 34.0 Togo - - - - - - - - - - 7.5 - - -T u n i s i a 11.8 8.5 7.0 9.6 2.0 7.5 2.5 - - - - - 24.0 - -Uganda 7.5 16.5 - - 5.0 14.2 20.0 -- - 10.6 Upper V o l t a -- - - - - 0.8 - - - - - - - - -Z a i r e -- - - - - - 28.3 - -- 73.3 130.0 33.3 - 20.0 Zambia - - - - - 19.0 38.0 19.0 - 56.9 38.3 19.0 148.8 100.0

Source: IMF, I n t e i m a t i o n a l F i n a n c i a l S t a t i s t i c s

I I - DRAVIINGS ON THE IMF BY DEVELOPHIG COUNTRIES: EMPIRICAL EVIDENCE AND ANALYSIS'^

Evidence of the general n a t t e r n of drawings

Developing countries have made considerable use of the IMF as a source of i n t e r n a t i o n a l finance. The general p a t t e r n of t o t a l drawings i s shown i n Table 1, which also i l l u s t r a t e s the marked f l u c t u a t i o n s i n y e a r l y drawings. Amongst developing c o u n t r i e s there has been a considerable range of experience. While some have made frequent and la r g e drax^ings others have had l i t t l e or no recourse to the Fund. The mid~1970s5 hox\/everp stand out as a pe r i o d when the m a j o r i t y of developing c o u n t r i e s did draw on the Fund, w i t h 1976 as a peak year f o r drawings. These f e l l q u i t e d r a m a t i c a l l y i n 1977 and 1973 and i n 1978 developing c o u n t r i e s a c t u a l l y made a net repayment to the Fund, althoug net drawings became p o s i t i v e again i n 1979, and seem to have r i s e n s t i l l f u r t h e r i n 1980.

The geographical breakdown given i n Table 1 r e v e a l s that i n general the developing c o u n t r i e s of L a t i n America and the Caribbean have drawn most from the Fund, though since 1976 they have not c o n s t i t u t e d the s i n g l e l a r g e s t group of borrowers. In 1977 and 1979 t h i s r o l e was assumed by A f r i c a n countries and i n 1978 by Asian c o u n t r i e s . I'Jhile p r i o r to 1973 o i l e x p o r t i n g developing c o u n t r i e s made f a i r l y r e g u a l r use of the Fund, only one drawing was made by t h i s group i n 1973-79. However, there i s no c l e a r cut r e g i o n a l p a t t e r n to drawings. Although s i m i l a r i t i e s may be found between some r e g i o n a l l y proximate c o u n t r i e s i t i s not d i f f i c u l t to f i n d counter-examples. Thus u n t i l 1976 Argentin a made f a i r l y continuous draw'.ngs on the Fund, w h i l e B r a z i l has made no drawings since 1968. Jamaic. drew from the IMF every year i n 1970-78, while Barbados has only once dvaim from the Fund, i n 1977. Geographical l o c a t i o n alone, then, cannot e x p l a i n the p a t t e r n of drawings. 3y the end of 1979, of the 101 developing c o u n t r i e s belonging to the Fund, 87 had made a drawing. Drav/ings have, however, been h e a v i l y concentrated i n a much narrower group of c o u n t r i e s . The l a r g e s t f i v e users, I n d i a , Argentina, the P h i l i p p i n e s , C h i l e and P a k i s t a n , alone accounted f o r 29% of t o t a l drawings by developing countries to end 1979, the l a r g e s t ten accounted f o r 45% and the l a r g e s t twenty f o r 52%.

1. Space c o n s t r a i n t s preclude a f u l l p r e s e n t a t i o n of a l l the s t a t i s t i c a l m a t e r i a l which forms the background f o r and s u b s t a n t i a t e s the claims made i n t h i s s e c t i o n . A more d e t a i l e d s t a t i s t i c a l annex may however be obtained from the author, see Appendix,

From amongst the Fund's range of f a c i l i t i e s the c r e d i t tranches have represented the s i n g l e l a r g e s t source of finance to Idcs. About h a l f as important as these has been the CFF, follov/ed by the o i l f a c i l i t y and reserve tranche. The extended f a c i l i t y , , the supplementary f i n a n c i n g f a c i l i t y and the b u f f e r stock f a c i l i t y have been of l i m i t e d q u a n t i t a t i v e importance, although we should remember that the EF and SFF were only r e c e n t l y introduced. I-Jhen dramngs are averaged over t h e i r l i f e t i m e s , the s i g n i f i c a n c e of both the EFF and SFF increases c o n s i d e r a b l y , and the SFF moves i n t o second place as a source of f i n a n c e . This aggregate p i c t u r e i s , however, not rep r e s e n t a t i v e of a l l developing c o u n t r i e s . Some have r e l i e d more h e a v i l y on the compensatory and/or o i l f a c i l i t i e s than on ordinary dravdngs under the reserve and c r e d i t tranches, though no country from the Western Hemisphere f a l l s i n t o t h i s categorj'^. Regional group averages emphasize the r e l a t i v e importance of the CFF to A f r i c a n c o u n t r i e s and of the OF to Asian c o u n t r i e s .

The p a t t e r n of drawings under the va r i o u s Fund f a c i l i t i e s has a l s o v a r i e d over time. Ordinary tranche dravrings represented e a s i l y the l a r g e s t source of finance u n t i l 1972. In only f i v e of the years between 1963 and 1976 d i d CFF drawings account f o r more than 10% of t o t a l Idc drawings. In 1976, however, there was a major change i n the r e l a t i v e use of the various IMF f a c i l i t i e s and f o r almost a l l developing c o u n t r i e s drawings under the OF and CFF became l a r g e r than those under the c r e d i t tranches. Since 1976 the OF has been discontinued and ordinary tranche drawings have again been the s i n g l e l a r g e s t source of Fund finance f o r n o n - o i l Idcs.

Drawings under s p e c i a l f a c i l i t i e s

1) CFF Before i t s l i b e r a l i s a t i o n i n 1966 only B r a z i l , Egypt and Sudan had made use of the CFF. Fo l l o w i n g the l i b e r a l i s a t i o n seven Idcs drev; on the CFF i n 1967 but during the remainder of the decade the CFF was l i t t l e used. Record drawings t o t a l l i n g almost SDR 300m were made by ten Idcs i n 1972, but t h i s was an exception to the general p a t t e r n . Up to 1976 the CFF had been used by r e l a t i v e l y few Idcs, and w i t h only l i m i t e d exceptions such as Arge n t i n a , the s i z e of drawings had been r a t h e r s m a l l . Thus, during 1963-75 51 drax-.iings were made by 30 Idcs? a t o t a l of SDR 1097 m was used, w i t h an average drawing of SDR 21.5m.

In 1976, f o l l o w i n g a f u r t h e r l i b e r a l i s a t i o n , there occurred a dramatic change; 37 Idcs drew a t o t a l of SDR 1454 m, g i v i n g an average drax<ring of SDR 39.3 m. As conqiared w i t h the previous record year of 1972, the s i z e of the average drawing almost doubled and the number of Idcs using the CFF almost quadrupled. Amongst n o n - o i l - e x p o r t i n g Idcs, L a t i n American and Caribbean c o u n t r i e s , w i t h drawings of SDR 975 m, have made the greatest use of the CFF; Middle Eastern Idcs have drawn SDR 290 m; A s i a n Idcs have drawn SDR 823 m and A f r i c a n Idcs have drawn SDR 446 m. Compared w i t h the peak year of 1976 CFF drawings f e l l d r a m a t i c a l l y i n 1977, but rose i n both 1978 and 1979. I t i s too e a r l y to say what the impact of the 1979 l i b e r a l i z a t i o n has been.

2) The B u f f e r Stock F a c i l i t y This f a c i l i t y has been l i t t l e used by developing c o u n t r i e s . Over i t s e n t i r e l i f e t i m e u n t i l A p r i l 1980 draxd.ngs by Idcs had t o t a l l e d a mere SDR 37 m, and only ten developing c o u n t r i e s ha^^'^A^is f a c i l i t y . A f t e r zero drawings under the BSFF i n 1976 and 1977 and one drawing i n 1978, four were made i n 1979 f o l l o w i n g the c o n c l u s i o n of the I n t e r n a t i o n a l Sugar Agreement.

3) The O i l F a c i l i t y By c o n t r a s t , during i t s short existence the OF was e x t e n s i v e l y used by Idcs. By the end of 1976 45 Idcs had dra\m a t o t a l of SDR 2539 m under the OF. N o n - o i l - e x p o r t i n g A s i a n Idcs made greatest use, w i t h drawings t o t a l l i n g SDR 1227 m by the end of 1976. Western Hemisphere Idcs had drawn SDR 618 m, w h i l s t Middle Eastern and A f r i c a n Idcs had drawn SDR 229 m and SDR 465 m r e s p e c t i v e l y . The large Asian d r a w i n g s h o w e v e r , do not mean that many cou n t r i e s used the f a c i l i t y ; i t r e f l e c t s r a t h e r the l a r g e s i z e of the drawings made by those that d i d use i t , e s p e c i a l l y I n d i a , Korea and P a k i s t a n .

4) The Extended F a c i l i t y The EF has been l i t t l e used by developing c o u n t r i e s s i n c e i t came i n t o being i n 1975. In 1975-79 there was a t o t a l of only eleven drawings by ei g h t c o u n t r i e s , t o t a l l i n g SDR 605 m. However, there has been some increase i n the number of drawings over time, w i t h four during 1979.

5) Ihe Supplementary F i n a n c i n g F a c i l i t y This f a c i l i t y only became operative i n 1979, during which year s i x c o u n t r i e s drew a t o t a l of SDR 307m, to supplement stand-bys under the c r e d i t tranches or extended f a c i l i t y .

6) The Trust Fund Trust Fund loans have been made over two p e r i o d s . During J u l y 1976 to June 1978 SDR 841 m were disbursed to 43 low income Idcs. During the twelve months ending J u l y 1979, SDR 350 m was a l l o c a t e d to 27 Id c s , w i t h f u r t h e r a l l o c a t i o n s due during the f o l l o w i n g twelve months. For many of the l e a s t developed countries the Trust Fund has been an important source of f i n a n c e . The loans are a d d i t i o n a l to normal drawings, c a r r y a low i n t e r e s t r a t e , have r e l a t i v e l y long repayment periods and i n v o l v e minimal c o n d i t i o n a l i t y . However, t o t a l loan disbursements are l i m i t e d by the p r o f i t s obtained from s a l e s by the Fund of p a r t of i t s gold s t o c k s . ^

Trends i n drawings on the Fund

Iilhile there i s no obvious o v e r a l l trend i n terms of developing c o u n t r i e s ' drawings on the Fund, by examining the years 1965-79 a number of sub-periods do emerge. In 1965-69 drawings were r e l a t i v e l y h i g h , they were low between 1970 and 1973, higher during 1974-76, and low again during 1977-79. Given the d i v e r s i t y of Idc experiences i t i s d i f f i c u l t to provide a s a t i s f a c t o r y e x p l a n a t i o n of these v a r i a t i o n s , but world economic developments, as w e l l as i n s t i t u t i o n a l changes, are c o n s i s t e n t w i t h the p a t t e r n of drawings.

The drop i n drawings during 1970-73, f o r example, c o i n c i d e d w i t h a sharp d e c l i n e i n the number of Idcs e x p e r i e n c i n g pajraients d e f i c i t s , as compared w i t h 1965-69. Less than 30% of Idcs recorded d e f i c i t s i n 1970-73, as compared vrLth 48% i n 1969. This improvement occurred d e s p i t e a d e t e r i o r a t i o n i n the terms of trade of primary producing c o u n t r i e s i n 1971 and a near doubling i n the aggregate current account d e f i c i t of developing c o u n t r i e s . These developments were, however, o f f s e t by l a r g e net c a p i t a l i n f l o w s . The poor trade performance of Idcs i n 1971 l e d to lar g e compeiiaatory drawiiigs the f o l l o w i n g year, although i n 1972 i t s e l f , as w a l l as i n 1973, there was an upturn i n the voliraie of world trade, an increase i n coffiiiiodi;;y p r i c e s and a f u r t h e r r i s e i n net c a p i t a l i n f l o w s . During 1974-76, by c o n t r a s t , the p r o p o r t i o n of developing c o u n t r i e s r e c o r d i n g d e f i c i t s increased. In 1974 a r i s e i n export p r i c e s plus an increase i n net capr.tal i n f l o w s eased the Idc payments p o s i t i o n

1. de S i l v a (1979) has argued that r i c h c o u n t r i e s have gained f a r more from recent IMF p o l i c y on gold v i a c a p i t a l gains than have poor c o u n t r i e s through the o p e r a t i o n a l Trust Fund. Fu r t h e r d i s c u s s i o n of t h i s i s s u e may be found i n B i r d (1979b)(1981a).

and only 39% of them recorded d e f i c i t s , but i n 1975 export p r i c e s f e l l v;hile import p r i c e s continued t h e i r r a p i d a c c e l e r a t i o n and 52% of developing covmtries went i n t o d e f i c i t .

The i n t r o d u c t i o n of the OF a l s o c o n t r i b u t e d to the increase i n drawings during 1974-76, as d i d the l i b e r a l i s a t i o n of the CFF i n 1975. Indeed, i t has been estimated that had the r u l e s governing the CFF remained unchanged drawings under t h i s f a c i l i t y i n 1975 would only have been 20% of the a c t u a l amount (Goreux (1977)). Thusthis l i b e r a l i s a t i o n combined w i t h the world economic r e c e s s i o n seem to provide a major explanation of the sharp r i s e i n drawings under the CFF i n 1976. As the r e l a t i v e importance of the OF and CFF increased so the share of drawings under the or d i n a r y tranches diminished. Furthermore, there was a s i g n i f i c a n t and apparently growing r e l u c t a n c e to make drav/ings which extended i n t o the upper tranches. P r i o r to 1974 58% of t o t a l net purchases i n the c r e d i t tranches went i n t o the upper tranches, against only 19% i n 1974-76. Over 1976-78 only 8 c r e d i t tranche drawings by developing c o u n t r i e s went beyond the f i r s t tranche. This was no doubt p a r t l y due to the greater use that was made of other Fund f a c i l i t i e s and the growing importance of commercial sources of f i n a n c e . I t i s c e r t a i n l y not the case that Ides' balance of payments have been s u f f i c i e n t l y strong as not to r e q u i r e a s s i s t a n c e . U l t i m a t e l y , however, i t seems l i k e l y that the r e l a t i v e l y l a r ge drawings under the OF and CFF are the r e s u l t of the low c o n d i t i o n a l i t y attached t o them, w h i l e the small drawings under the upper c r e d i t tranches r e s u l t from the s e v e r i t y of the p o l i c y c o n d i t i o n s attached to them.

However, f o r 1977-79 the problem i s one of e x p l a i n i n g the g e n e r a l l y s l i g h t usage made of almost a l l sources of Fund f i n a n c e . Ldcs showed considerable reluctance to draw on any of the Fund's f a c i l i t i e s , which r e s u l t e d i n the Fmd possessing considerable excess l e n d i n g c a p a c i t y . Hot'jever, there was a major r e v i v a l i n Idc drawings during 1980.

I t i s d i f f i c u l t to c a l c u l a t e the p r e c i s e q u a n t i t y of Fund resources a v a i l a b l e to developing c o u n t r i e s and excess l e n d i n g c a p a c i t y since a v a i l a b i l i t y depends on the existence of a payments need. At any time there may be a number of co u n t r i e s that cannot j u s t i f y using Fund resources i n terms of t h e i r balance of payments p o s i t i o n , and they w i l l be i n e l i g i b l e f o r Fund finance. Furthermore i n order to use such f a c i l i t i e s as the CFF co u n t r i e s have to meet c e r t a i n other e l i g i b i l i t y c r i t e r i a .

Thus a developing country which has a pajnnents problem but i s not expe r i e n c i n g an export s h o r t f a l l w i l l not be e l i g i b l e to draw under the CFF- n e i t h e r w i l l a country which, even though experiencing an export s h o r t f a l l , has no balance of pajnnents need.

As regards the SFF, the purpose of t h i s f a c i l i t y i s to remove the s t r i c t quota l i m i t s on a country's drawings and the amount of finance a v a i l a b l e to a country under the SFF i s open-ended. In the case of a very l a r g e d e f i c i t the resources a v a i l a b l e under the SFF could be as much as f i v e or s i x times the country quota.

Some estimate of the approximate magnitude of the Fund's spare lending c a p a c i t y w i t h regard to Idcs may, however, be made. As of end May 1980 the maximum Fund resources a v a i l a b l e to developing c o u n t r i e s might, i n p r i n c i p l e , have been as piuch as SDK 15 -20 I; i f not r a t h e r more. EScn^

_ allowance making / f o r the p o i n t s r a i s e d e a r l i e r , the a c t u a l drawings of only SDR 6.5b support the view that the Fund possessed considerable u n u t i l i s e d l e n d i n g c a p a c i t y . This u n d e r - u t i l i s a t i o n w r r - i n t s s c r u t i n y . The p r i o r problem i s one of i n c r e a s i n g the use of resources already a v a i l a b l e , r a t h e r than the f u r t h e r c r e a t i o n of nev? f a c i l i t i e s .

The economic c h a r a c t e r i s t i c s of user-countries

Given the evidence already presented a question a r i s e s as to whether drawings by developing c o u n t r i e s d i s p l a y any d i s c e r n i b l e economic p a t t e r n . I f so, what are the economic c h a r a c t e r i s t i c s both of those c o u n t r i e s that do draw on the Fund, and of those that do not; and i s i t p o s s i b l e to p r e d i c t which Idcs are l i k e l y to draw on the Fund and i n what amounts?

In an attempt to shed some l i g h t on these questions an econometric a n a l y s i s was undertaken on the b a s i s of a model which regressed drawings on country economic c h a r a c t e r i s t i c s such as the balance of payments p o s i t i o n , the debt s e r v i c e r a t i o , the rate of i n f l a t i o n , per c a p i t a income, the l e v e l of reserves, and access to eurocurrency c r e d i t s . ^

1. For a f u l l e r e x p l a n ation of the model used and r e s u l t s obtained see B i r d and Orme (1980(a)).

From both a s t a t i s t i c a l and a l s o economic point of view the model was s a t i s f a c t o r y when t e s t e d w i t h 1976 data. The estimated c o e f f i c i e n t s were c o n s i s t e n t w i t h a p r i o r i reasoning f o r a l l the explanatory v a r i a b l e s except e x t e r n a l debt, f o r which the c o e f f i c i e n t was, i n any case, not s i g n i f i c a n t l y d i f f e r e n t from zero. On the b a s i s of t h i s evidence i t would seem that the IMF and the Eurocurrency market provide coit5>lementary r a t h e r than competing sources of finance and that reserve use and drawings on the Fund are, i f anything, complementary a c t i v i t i e s . Developing c o u n t r i e s seem to draw more from the Fund as t h e i r payments s i t u a t i o n , and t h e i r general economic performance d e t e r i o r a t e s , but tend to draw l e s s as they become r i c h e r . However, when re-estimated f o r 1977 i n order to t e s t f o r the s t a b i l i t y of the f u n c t i o n the model broke down, thus reducing confidence i n the 1976 r e s u l t s . The model was a l s o t e s t e d s e p a r a t e l y f o r OF and CFF drawings. I'Jhile p r o v i d i n g a poor explanation of the former i t provided a good explanation of the l a t t e r . An attempt to d i s t i n g u i s h between low and high c o n d i t i o n a l i t y draidngs was f r u s t r a t e d by lack of data.

I t was a l s o p o s s i b l e to analyse the behaviour of those c o u n t r i e s that d i d not draw on the Fund i n 1976. On the b a s i s of the model drawings were p r e d i c t e d f o r the 27 developing which d i d not a c t u a l l y draw on the Fund and f o r x^hich data were a v a i l a b l e . I t was discovered that only 8 of these had p r e d i c t e d drawings of zero. The remaining 19 would a l l have been expected to draw on the Fund given t h e i r economic s i t u a t i o n . Attempts to e x p l a i n the r e t i c e n c e of these c o u n t r i e s i n terms of the c o n d i t i o n a l i t y that would have been attached to drawings and exchange rate p o l i c y proved g e n e r a l l y unsuccessful. I t thus appears that drawings are not a p u r e l y economic phenomenon. P o l i t i c a l , s o c i a l and i n s t i t u t i o n a l f a c t o r s a l s o no doubt need to be taken i n t o account.

The s i g n i f i c a n c e of Fund finance to developing c o u n t r i e s

In order to gain an a p p r e c i a t i o n of the q u a n t i t a t i v e importance of drawings from the Fund Table 2 shows the c o n t r i b u t i o n that r e s e r v e - r e l a t e d c r e d i t f a c i l i t i e s , i n c l u d i n g the use of Fund c r e d i t , have made towards meeting n o n - o i l developing c o u n t r i e s ' current account balance of payments d e f i c i t s , as con^jared w i t h other sources of f i n a n c e . For most of the p e r i o d since 1973 the IMF emerges as a r e l a t i v e l y i n s i g n i f i c a n t source of finance f o r developing c o u n t r i e s , and during the 1970s the r e a l value of Fund c r e d i t s to Idcs has a c t u a l l y f a l l e n . Even assuming that they were to draw to t h e i r

f u l l p o t e n t i a l the q u a n t i t a t i v e s i g n i f i c a n c e of Fund finance to developing c o u n t r i e s would remain l i t d t e d as compared w i t h other f i n a n c i a l i n f l o w s . I t a l s o appears that over time the IMF became l e s s s i g n i f i c a n t r e l a t i v e to other sources of f i n a n c e , accounting f o r a d e c l i n i n g share of t o t a l f i n a n c i a l flows.

Care has to be e x e r c i s e d i n i n t e r p r e t i n g these f i g u r e s , however. I t i s not n e c e s s a r i l y v a l i d to conclude that the Fund's r o l e has been small and of d e c l i n i n g importance. F i r s t , Fimd finance i s s p e c i f i c a l l y d i r e c t e d towards the balance of payments and i t s s i g n i f i c a n c e should t h e r e f o r e o nly be judged against the s i z e of the payments problem. Even evidence that the r a t i o between the IMF quotas of developing c o u n t r i e s and the value of t h e i r trade has f a l l e n may be m i s l e a d i n g i f there has simultaneously been an increase i n the s t a b i l i t y of trade. However, evidence f o r 1967-76 reveals that drawings on the Fund have on average covered a d e c l i n i n g p r o p o r t i o n of recorded d e f i c i t s , d e s p i t e the growing tendency to use more than one f a c i l i t y at a time. While the evidence shows that the p r o p o r t i o n of a d e f i c i t that i s covered r i s e s w i t h the number of f a c i l i t i e s under which drawings are made, the share of d e f i c i t s covered by the combined use of c r e d i t tranche and conqpensatory drawings f e l l from 1967-73 to 1974-76. Whereas i n the e a r l i e r p e r i o d t h e i r combined use covered more than h a l f the d e f i c i t i n a l l cases and more than three quarters of i t i n 86% of the cases, i n the l a t t e r p e r i o d t h e i r use covered more than h a l f the d e f i c i t i n only 40% of cases and there was not a s i n g l e country i n which more than three-quarters of the d e f i c i t was covered (Burke D i l l o n (1978)).

While the current account d e f i c i t of n o n - o i l Idcs aiMunted to $233 b, net Fund c r e d i t financed l e s s than $10b of t h i s i n 1974-79. Although such evidence seems to confirm that the d i r e c t importance of the Fund as a source of finance i s d e c l i n i n g , at l e a s t three r i d e r s to t h i s statement are a p p r o p r i a t e . F i r s t , the IMF may provide a d i r e c t l y s i g n i f i cant q u a n t i t y o f a s s i s t a n c e i n p a r t i c u l a r cases. Thus, w h i l e drawings on the Fund covered only 3.2% of the cond)ined balance of trade d e f i c i t of a l l n o n - o i l Idcs taken together i n 1978 (coin)ared w i t h 3.9% a decade e a r l i e r ) , drawings covered more than 40 per cent of the d e f i c i t s of Peru, Jamaica, Burma and S r i Lanka.

Table 2. Hon-oil developing c o u n t r i e s : current account f i n a n c i n g , 1973-79 ( i n b i l l i o n s of U.S. d o l l a r s )

1973 1974 1975 1976 1977 1978 1979 1973-79 11.5 36.9 45.9 32.9 28.6 35.8 52.9 244.5

9.8 13.2^ 11.7 12.1 14.4 16.2 19.4 96.8

4.9 6.92 7.4 7.6 8.3 8.0 10.7 53.8 0.6 0.8 -1.0 -0.2 1.0 2.0 0.8 4.0 4.3 5.5 5.3 4.7 5.1 6.2 7.9 39.0 1.7 23.7^ 34.2 20.8 14.2 19.6 33.5 147.7

-9.3 -1.2- 2.0 -12.7 -11.9 -18.2 -11.0 -62.3 11.0 24.92 32.2 33.5 26.1 37.0 44.5 210.0 5.5 11.4 10.2 12.!: 13.3 15.9 78.3 3.7 6.52 7.1 6.6 8.7. P.? 10.7 51.4 1.8 3.1 4.3 3.6 4.3 4.6 5.2 26.9 6.6 10.2 14.7 17.6 15.8 25.1 23.4 113.4 4.0 8.6 9.2 10.9 15.6 19.3 17.3 84.9 0.5 0.3 0.2 1.1 2.G 3.0 2.0 9.7 2.1 1.3 5.3 5.6 -2.4 2.8 4.1 18.8 0.3 1.6 2.4 0.7 0.2 9.9

- 5.1 6.5 3.9 -0.0 c n -1.4 -1.6 -2.8 -2.5 -1, 7 3.0

Current account d e f i c i t ^ F i nancing through t r a n s a c t i o n s th£t do not a f f e c t net debt p o s i t i o n s Net unrequited t r a n s f e r s r e c e i v e d by governments of n o n - o i l developing c o u n t r i e s SDR a l l o c a t i o n s , gold monetization, and v a l u a t i o n adjustments D i r e c t investment flows, net

3 Net borrowing and use of reserves

Reduction of reserve assets (accumulation, -) Net e x t e r n a l borrowing^

Long-term from o f f i c i a l sources, net^ On concessionary terms^ On nonconcessionary terms^

Other long-term borrowing from nonresidents, net From f i n a n c i a l i n s t i t u t i o n s ^ Through bond i s s u e s ^ Other sources'

Use of r e s e r v e - r e l a t e d c r e d i t f a c i l i t i e s , net Other short-term borrowing, net Residual e r r o r s and omissions

Source! JIIF Annual ?.eport, 1980, Table 10. Notes: 1. Net t o t a l of balances on goodsa s e r v i c e s , and p r i v a i s traii-;j: t s , as d e f i n e d f o r Balance r--^ Py/ments Yearbook -.Vith sign i-^versed) 2. Excludes the e f f e c t of a r e v i s i o n of the terms of the dispos-tion of economic aisistsn.-> loans made by the 'Oniu-ti States zo I n d i a

and repayable i n rupees, and of rupees already acqiiirod by the U.S. Government i n vef>cyz:::^n^ c-f. sv.c:- lo^ns :.: f: r e v i s i o j i hz-^s the e f f e c t of i n c r e a s i n g government t r a n s f e r s by at.^cvt i'1$2 b i l l i o n s w i t h an o f f s e t i n not o f f i c i a l l-.-;v.5-.

3. i . e . , f i n a n c i n g through changes i n net debt pc31 (aet borrowing, le^.s net accumul^sricj - or ulss net l i r a i d a t i c n - of o f f i c i a l reserve a s s e t s ) .

4. Includes any net use of nonreserve claims on .-lo-.tr-fiidarits, i n d i v i d u a l c o u n t r i e s , and minor d e f i c i e n c i e s i n cov?r>;'ge.

5. P u b l i c and p u b l i c l y guaranteed borrowing oriiy. 6. Loans on "concessionary terms'' era defined to include a l l Icms c o n t a i n i n g a graiit element: greater than 25 p?:; cent. 7. I n c l u d i n g s u p p l i e r s ' c r e d i t s , a c q u i s i t i o n of long-term e x t e r n a l assets, and e r r o r s and r e s i d u a l s a r i s i n g from mismatching

of data taken from c r e d i t o r and debtor records. 8. Comprises use of Fund c r e d i t anc short-term borrowing by monetary a u t h o r i t i e s from other monetary a u t h o r i t i e s . 9. E r r o r s and omissions i n reportec balance of payments statements f o r i n d i v i d u a l c o u n t r i e s , p l u s minor am i s s i o n s i n coverage.

errors and omissions i n rsporrca balance, of piyzuGuts st.iteHierts f o r

Second, even where only a small p r o p o r t i o n of the d e f i c i t has been covered, the a v a i l a b i l i t y of Fund resources i s such t h a t a much l a r g e r p r o p o r t i o n might have been covered. Further increases i n quotas, along w i t h the 1930 d e c i s i o n by the Executive Board to permit drawings on the Fund to expand to 600 per cent of quota mean that a p o t e n t i a l l y s i g n i f i c a n t p r o p o r t i o n of Idcs' f i n a n c i n g needs may i n p r i n c i p l e be met by the IMF.

T h i r d , even though the absolute amounts of finance provided by the IMF may be small they may r e s u l t i n much l a r g e r i n f l o w s from other sources, p a r t i c u l a r l y the Eurocurrency market. There i s some evidence f o r t h i s . In the r e g r e s s i o n a n a l y s i s mentioned e a r l i e r , there was a p o s i t i v e c o r r e l a t i o n between Fxmd drawings and Eurocurrency drawings and t h i s was supported by a t e s t which gave a Spearman's rank c o r r e l a t i o n c o e f f i c i e n t between drawings on the Fund and Eurocurrency c r e d i t s over the p e r i o d 1971-79 of 0.64. However i t i s al s o c l e a r that drawings from the Fund and the acceptance of the r e l a t e d c o n d i t i o n a l i t y i s , i n i t s e l f , n e i t h e r a necessary nor s u f f i c i e n t c o n d i t i o n f o r access to commercial loans. B r a z i l , f o r i n s t a n c e , borrowed h e a v i l y from the Eurocurrency market during the 1970s w h i l e making no use at a l l of the Fund; at the same time I n d i a , which i n absolute terms made the l a r g e s t cumulative drawings on the Fund up to ond 1979 borrowed only $165 m from the Eurocurrency market; Bangladesh, which ranked 16th i n terms of drawings on the Fund, borrowed nothing from the Eurocurrency market. Examination of the nine stand-by arrangements concluded during 1975-77 where no agreement had e x i s t e d during at l e a s t the previous 2 years confirms the v a r i e t y of experience amongst Idcs. In terms of the i n f l o w of Eurocurrency c r e d i t s a f t e r c o n c l u s i o n of the stand-bys no c l e a r p a t t e r n emerges. In some cases such as Uruguay, Congo and Costa R i c a f y i n c f l a t e i n the i n f l o w of Eurocurrency c r e d i t s , w h i l e i n others, such as Egypt, Nepal and Tanzania, there was not. This r e s u l t i s c o n s i s t e n t w i t h evidence c o l l e c t e d by Kapur (1977). Undert a k i n g a cross country r e g r e s s i o n a n a l y s i s of data from 25 Idcs that borrowed from the Eurocurrency market during 1972-74 he found s u b s t a n t i a l c o n f i r m a t i o n f o r the view that the flow of c r e d i t i s p o s i t i v e l y r e l a t e d to a country's economic growth and export performance, and n e g a t i v e l y r e l a t e d to p r o j e c t e d i n c r e a s e s i n the debt burden and the degree of p r i v a t e banking exposure. I t i s d i f f i c u l t to see how the IMF could have much i n f l u e n c e on these v a r i a b l e s . Having s a i d t h i s , i t i s a l s o true that bankers f r e q u e n t l y s t a t e that they put great s t o r e by IMF involvement when co n s i d e r i n g t h e i r own lending s t r a t e g y towards developing c o u n t r i e s ( I n s t i t u t e of Bankers (1979)).

1. I t may be noted that the IMF may i n c e r t a i n cases impose r e s t r i c t i o n s on a country's e x t e r n a l borrowing as a c o n d i t i o n of Fund a s s i s t a n c e .

I I I - A REVIEW OF CRITICISMS AND DEFENCES OF CONDITIONALITY

There are of course sound reasons why the DlF's lending should be . . ' 2

c o n d i t i o n a l . Banking prudence r e q u i r e s t h a t those making loans should make reasonably sure that borrowers w i l l be able t o repay. In f a c t , the A r t i c l e s of Agreement r e q u i r e adequate safeguards to ensure the ' r e v o l v i n g and temporary character' of the use of Fund resources. When IMF loans to a member are large the country's a b i l i t y to repay may w e l l depend on i t s macro-economic p o l i c i e s . C o n d i t i o n a l i t y might furthermore seem appropriate as a r a t i o n i n g device i f , at the sub-market i n t e r e s t rates charged by the IMF, there was excess demand f o r fi n a n c e . C o n d i t i o n a l i t y might then be used as a way of keeping the demand w i t h i n the c e i l i n g of Fund resources.

While f o r these reasons most would agree w i t h the p r i n c i p l e of c o n d i t i o n a l i t y , developing c o u n t r i e s have f r e q u e n t l y argued t h a t the co n d i t i o n s used are too harsh, too wide-ranging, f r e q u e n t l y misguided, and i n s e n s i t i v e t o the economic, s o c i a l and p o l i t i c a l problems which many fafthem face.

1. This s e c t i o n deals w i t h Fund c o n d i t i o n a l i t y as i t a p p l i e s t o drawings under the upper c r e d i t tranches, the EFF and the SFF. W h i l s t some of iss u e s r a i s e d are a l s o r e l e v a n t to the Fund's low c o n d i t i o n a l i t y f a c i l i t i e s , i n p a r t i c u l a r the CFF, a more s p e c i f i c a p p r a i s a l of these f a c i l i t i e s and t h e i r r e l a t e d c o n d i t i o n a l i t y may be found i n B i r d (1978)(1979)(1981). B r i e f l y the major c r i t i c i s m s that have been l e v e l l e d at the CFF are: (a) t h a t i t i s q u a n t i t a t i v e l y inadequate t o deal w i t h the problem

of export i n s t a b i l i t y as encountered by Idcs, (see f o r example, UNCTAD (1977));

(b) that since i t a p p l i e s only to s h o r t f a l l s i n export r e c e i p t s caused by e i t h e r a f a l l i n p r i c e or q u a n t i t y s o l d i t does not compensate f o r those payments d i f f i c u l t i e s caused by e x t e r n a l l y generated increases i n inqjort p r i c e s or by bad harvests which f o r c e a country to make a d d i t i o n a l o u t l a y s on food imports, (see, f o r example. B i r d (1971));

(c) that i t i m p l i c i t l y assumes that export s h o r t f a l l s w i l l be reversed w i t h i n three years (see, f o r example Corea (1979));

(d) that i t s trade basis r e s u l t s i n a skewed d i s t r i b u t i o n of b e n e f i t s (see, f p r example, de V r i e s (1975));

and (e) th a t i t f a i l s to deal w i t h the longer term and more fundamental causes of export i n s t a b i l i t y such as the heavy concentration on one or two exports (see, f o r example, Goreux (1971)).

2. I t i s important to r e i t e r a t e at t h i s stage that not a l l the Fund's f a c i l i t i e s are subject to s t r i n g e n t p o l i c y c o n d i t i o n s ; about 40 per cent of the hjr p o t h e t l c a l c r e d i t maximum a v a i l a b l e t o a member country I s f r e e from s t r i c t c o n d i t i o n a l i t y . For f u r t h e r d e t a i l s and a discu s s i o n ; of the nature of the c o n d i t i o n s t h a t apply t o the v a r i o u s Fund f a c i l i t i e s , see, f o r i n s t a n c e . B i r d (1978).

A statement of c r i t i c i s m s that have been made of Fund c o n d i t i o n a l i t y

One argument i s that c o n d i t i o n a l i t y r e s u l t s i n asymmetrical adjustment. Under the e x i s t i n g i n t e r n a t i o n a l monetary system l i t t l e pressure i s exerted on c o u n t r i e s to adjust i n order to remove surpluses. Again, reserve-currency countries l i k e ^ t ^ l * ^ 7 " ^ ^ ^ f be able to finance d e f i c i t s by i n c r e a s i n g t h e i r e x t e r n a l l y h e l d l i a b i l i t i e s . Other d e f i c i t c o u n t r i e s may be i n a p o s i t i o n to finance d e f i c i t s through p r i v a t e , o f t e n u n c o n d i t i o n a l , borro^d-ng which allows them freedom to ehoose doitsestic p o l i c i e s . The l e s s economically strong n a t i o n s , however, are o f t e n f o r c e d to tuim to the IMF where they become subj e c t to the d i s c i p l i n e of c o n d i t i o n a l i t y . Of course, i t might be maintained that i t i s j u s t these c o u n t r i e s that most need guidance i n t h e i r economic a f f a i r s s i n c e t h e i r poverty and l a c k of c r e d i t - w o r t h i n e s s i l l u s t r a t e a l a c k of e x p e r t i s e i n economic management. While there may be something i n t h i s , i t need not always be the case. The evidence suggests that over recent years many Idcs have been faced w i t h severe payments d i f f i c u l t i e s which have been caused p r i m a r i l y by e x t e r n a l f a c t o r s r a t h e r than by domestic mismanagement ( D e l l and Lawrence

(1980)). I t i s one of the inescapable consequences of a zero-sum i n t e r n a t i o n a l monetary system that d i s e q u i l i b r i a i n the form of surpluses i n one p a r t of the system imply d e f i c i t s elsewhere.