the impact of dividend initiation on the information ... 1989.pdf · initiation on the information...

TRANSCRIPT

http://www.jstor.org

The Impact of Dividend Initiation on the Information Content of Earnings Announcementsand Returns VolatilityAuthor(s): P. C. VenkateshSource: The Journal of Business, Vol. 62, No. 2, (Apr., 1989), pp. 175-197Published by: The University of Chicago PressStable URL: http://www.jstor.org/stable/2353225Accessed: 26/06/2008 14:21

Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at

http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless

you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you

may use content in the JSTOR archive only for your personal, non-commercial use.

Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at

http://www.jstor.org/action/showPublisher?publisherCode=ucpress.

Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed

page of such transmission.

JSTOR is a not-for-profit organization founded in 1995 to build trusted digital archives for scholarship. We work with the

scholarly community to preserve their work and the materials they rely upon, and to build a common research platform that

promotes the discovery and use of these resources. For more information about JSTOR, please contact [email protected].

P. C. Venkatesh University of Houston

The Impact of Dividend Initiation on the Information Content of Earnings Announcements and Returns Volatility*

I. Introduction

A rationale often provided for the payment of cash dividends, despite their tax disadvantage, is that they provide a signaling mechanism. This is indeed the conclusion of two recent articles on the subject. Asquith and Mullins (1983) examine the impact of initiation of a cash dividend by a firm and find a strong positive stock-price reac- tion. They interpret this to mean that investors welcome the initiation of dividends because it establishes a mechanism by which management can communicate private information about fu- ture cash flows. Richardson, Sefcik, and Thomp- son (1986) arrive at a similar conclusion.

This article examines another implication of this "dividend-signaling" argument: are divi- dends and earnings announcements substitutes or complements in terms of the information they convey? This article provides evidence on this question by studying the empirical consequences of the introduction of dividends on the informa- tion content of earnings announcements. Prior to the introduction of dividends, investors presum-

This article provides some evidence on the empirical consequences of initiating dividends. First, it documents that the information content of quarterly earnings announcements de- creases after the in- troduction of cash divi- dends. This suggests that dividends and earnings are partial "information substi- tutes." The second finding is that the vol- atility of total daily re- turns decreases after the initiation of divi- dends and that most of this decrease is attrib- utable to a decrease in the firm-specific volatil- ity. A possible reason for this is that, in the postdividend period, investors place less weight (relative to the predividend period) on other "information sig- nals," and, hence, ob- served volatility may be lower.

* I would like to thank my colleagues at the University of Houston, in particular, John Easterwood, Palani-Rajan Kadappakam, and Rich Pettit, for their unstinting criticism, patience, and encouragement. Illuminating discussions with Sarab Seth and Ron Singer have led to considerable improve- ment in the paper. I would also like to thank Kose John and Joe Williams for their comments. The onus for any errors, of course, rests with me.

(Journal of Business, 1989, vol. 62, no. 2) ? 1989 by The University of Chicago. All rights reserved. 0021-9398/89/6202-0003$O1 .50

175

176 Journal of Business

ably relied quite heavily on earnings figures to estimate future cash flows. After the introduction of dividends, investors can use dividend figures as well as earnings figures to estimate future cash flows. My hypothesis, therefore, is that the average information content of earn- ings announcements in the predividend period is greater than that in the postdividend period, ceteris paribus.1 A finding in favor of this hypothesis would suggest that the two announcements are substitutes, and this finding could also be construed to mean that investors place more reliance on dividend announcements than on earnings.2 The op- posite evidence would indicate that the two announcements convey different information.3 As part of this investigation, I also study whether dividend initiation has an impact on the characteristics of daily returns. Finally, hypotheses relating the change in information content of earnings announcements to firm-specific factors are examined.

As hypothesized, I find that the average price reaction to earnings announcements is smaller in the postdividend period, regardless of whether earnings precede or follow dividend announcements; the re- duction is statistically significant.4 Dividend initiation also appears to affect the characteristics of daily returns. Specifically, the volatility of raw (total) returns is lower in the postdividend period, primarily "due" to a decrease in the "firm-specific" (nonmarket) component of volatil- ity. A possible explanation for this is that, in the postdividend period, investors accord less importance to pieces of "information" (an- nouncements/rumors) that could have induced price reactions in the predividend period. Hence, there may be fewer large price changes (in magnitude) in the postdividend period, and observed volatility may be lower. This evidence supports the notion that investors view dividends as an information-transmission mechanism.

Finally, in examining whether the change in earnings information content and the change in volatility are related to firm-specific charac- teristics, I find only weak evidence of an exchange-listing effect. There is a slightly larger reduction in earnings information content for New York Stock Exchange (NYSE) firms as compared to American Stock Exchange (AMEX) firms, suggesting that the information role of divi-

1. This is, of course, the alternative hypothesis in the empirical tests. The null hy- pothesis is that there is no change in information content.

2. The latter conclusion would be justified unless dividend announcements were made systematically before the corresponding earnings announcements. I show later that this is not the case.

3. Previous studies (Aharony and Swary 1980; Kane, Lee, and Marcus 1984) suggest that the two announcements convey different information. These articles are discussed subsequently.

4. Healy and Palepu (1988) find that the stock price responsiveness to annual earnings announcements is generally smaller after dividend initiation; however, the reduction is statistically significant only in the year of the initial dividend. My results suggest a permanent reduction in earnings information content. Their work is discussed subse- queotly.

Impact of Dividend Initiation 177

dends is more important for NYSE firms. This runs counter to the standard argument that more "information" is available about NYSE firms (more analysts, more news items, etc.), so that an additional information source such as dividends should be less important, ceteris paribus.

This article is organized as follows. Section II provides a brief re- view of the literature. The data and methodology are discussed in Section III. Section IV contains the major results, and the exchange- listing effect is described in Section V. Concluding comments are of- fered in Section VI.

II. Literature Review

A. Research on Initial Dividends

Asquith and Mullins (1983) were the first to examine the impact on stockholders' wealth of the initiation of dividends. They observe that the initiation of dividends may mark an important turning point in the history of a corporation. Research on trading behavior around this date can provide fresh insights into the dividend-policy question as well as the dividend-signaling argument. If the initiation of dividends induces clientele shifts (imposing costs on old stockholders), then the stock price may decrease. An increase in stock price is consistent with the view that investors welcome the establishment of a mechanism whereby managers will communicate their inside information. They document that the positive excess returns accompanying announce- ments of initial dividends are larger than those accompanying subse- quent dividend increases. (However, this is no longer the case once an adjustment is made for the size of the dividend.) They conclude from this that dividends convey unique, valuable information to investors.

Richardson et al. (1986) observc that dividend-clientele theories pre- dict a shift in clienteles, and hence an increase in trading volume, when a firm changes its dividend policy. They find that trading volume in- creases around the declaration of initial dividends, but they conclude that this increase stems primarily from the signaling aspect of the initial dividend. They suggest that some evidence of clientele trading exists but that this motive is of secondary importance.

There is little by way of theoretical work to indicate when and why firms might initiate regular cash dividends. Preliminary work by John and Nachman (1987) provides some promise. They consider a sequen- tial signaling model where managers choose optimal dividend and fi- nancing strategies. Hence, there might arise a point in time when it is optimal for a firm to initiate dividends. From a somewhat different standpoint, Marsh and Merton (1987) argue that firms may change dividends, at least partly, for reasons other than to signal firm-specific

178 Journal of Business

information. In their view, firms may calibrate their dividend policies relative to their peer firms (e.g., firms in the same industry). Hence, we may observe cross-sectional dependence in dividend changes. This contrasts with Asquith and Mullins (1983) in that firms may initi- ate dividends for reasons other than to establish a signaling mecha- nism. The evidence in Healy and Palepu (1988), which suggests that dividend-initiating firms experience higher earnings growth in their dividend-initiating year than do their industry peers, tends to support traditional signaling arguments (e.g., John and Williams 1985; Miller and Rock 1985). That is, better firms try to distinguish themselves via higher dividends.

B. The Information Content of Earnings and Dividend Announcements

With a few exceptions, there now appears to be a consensus that both types of announcements have information content. One nettlesome issue in the past was that, since the two announcements may be made close together, it was difficult to attribute an observed price reaction to any one announcement. With the appropriate data, Aharony and Swary (1980) were able to establish that each announcement has infor- mation content, after controlling for the potential contamination from the other. Kane, Lee, and Marcus (1984) find a corroboration effect between the two announcements. For instance, an increase in earnings as well as in dividends (separate announcements) produces a more favorable reaction than an increase in only one of them. The results in these studies suggest that the two types of announcements are not perfect substitutes in terms of the information they convey. This article examines this question for a sample of firms that have recently in- troduced dividends (possibly for the purpose of information transmis- sion). This should enable an especially sharp test of dividends-earnings substitutability.

Theoretical models differ in their description of the exact nature of the information conveyed by dividend announcements. In general, div- idends may convey information about the expected value and/or the risk of future cash flows; however, since the literature on this subject is not well developed, I focus on two works with implications for divi- dends-earnings substitutability. In Miller and Rock (1985), dividends are determined as a residual (i.e., "after" the investment decision), and unanticipated dividend changes primarily reflect earnings shocks; dividend and earnings announcements would be fairly close substitutes in their model. John and Nachman (1987) consider a multiperiod model of dividend and financing strategies and explicitly allow for "smooth- ing" of dividends by management. The optimal dividend in their signal- ing equilibrium is the product of a "current-liquidation" term and a "relative-value" term. Neither of these terms is intended to signal

Impact of Dividend Initiation 179

current or future earnings. In their words, "dividends are a coarse signal of earnings" (p. 5). In their model, earnings are revealed through a costless public audit. Thus, theoretical models are divided about the role of dividends vis-a-vis earnings. As summarized above, the empir- ical evidence to date seems to suggest that the two announcements are complements rather than perfect substitutes.

Asquith and Mullins (1986) discuss some reasons why both managers and investors might prefer to convey information via dividends rather than through other means. Earnings figures, in particular, are subject to the criticisms that they are "manipulable" and that they may not be future oriented. However, the empirical fact that earnings announce- ments produce price reactions suggests that they have more than short- term information content.5

A recent paper by Healy and Palepu (1988) is similar to this article in that it also examines the relation between dividend initiation and earn- ings. Although the primary focus of their paper is the nature of earnings changes around dividend initiation, they also have results on stock- price responsiveness to annual earnings announcements (before and after dividend initiation). They document that dividend-initiating firms experience earnings growth in the year of the dividend announcement and for two subsequent years, but not thereafter. However, the initial dividend announcement conveys no information on future annual earn- ings changes beyond the first year. They find that stock-price respon- siveness to the "unexpected" component of annual earnings an- nouncements is generally smaller in the postdividend period; however, the reduction is statistically significant only in the year of the initial dividend.

Although the work by Healy and Palepu and this article are both concerned with the relation between dividend initiation and earnings, there are also substantial differences. Healy and Palepu (1988) primar- ily examine how much information the initial dividend announcement alone conveys about future earnings. In this article, the approach tends to emphasize the viewpoint that the initial dividend also puts in place an information-transmission mechanism; that is, investors learn from the initial dividend as well as from subsequent dividends. Thus, whether or not the information content of postdividend earnings an-

5. Two other recent studies are relevant to the discussion here. Kormendi and Lipe (1987) document that price reactions to earnings surprises are related to the estimated impact of a current earnings shock on future cash flows (as implied by a univariate time- series model of earnings). Ofer and Siegel (1987) provide empirical evidence that market participants use unexpected dividend changes to form earnings expectations. They find that security analysts revise their earnings forecasts following unexpected dividend changes and that the magnitude of the revision is related to the dividend change. The latter discussion provides additional evidence that investors use both earnings and divi- dends to estimate future cash flows.

180 Journal of Business

nouncements is smaller may also depend on the information in nearby dividend announcements. The analysis in this article accounts for this by grouping the postdividend quarterly earnings announcements ac- cording to whether they precede or follow the associated quarterly dividend announcement. I also relate the change in earnings informa- tion content to firm characteristics. In addition, this article also docu- ments that dividend initiation is followed by a reduction in the volatility of daily returns. Healy and Palepu (1988) provide important evidence, which is not contained in this article, on the nature of earnings-changes around dividend initiations and omissions. The results, with respect to the change in earnings information content, are similar in some re- spects but not in others. The differences are discussed in note 4 above and Section IV below.

III. Data and Methodology

A. Data I first identified a sample of firms that paid initial quarterly dividends for the years 1972-83 (inclusive) by scanning the Center for Research in Security Prices (CRSP) monthly master files (1987). Then I collected earnings and dividend information for each of the 14 quarters that preceded and succeeded the quarter of the initial dividend. Thus, a firm with complete data would have information on 29 quarterly earnings announcements and 15 quarterly dividend announcements. The spe- cific requirements for inclusion in the sample are given below.

i) The firm's first cash dividend ever is designated a quarterly pay- ment by CRSP, and this announcement is made sometime during the period 1972-83. This eliminates some firms whose subsequent divi- dends were to be paid on other than a quarterly basis (e.g., monthly or semiannually).

ii) Daily returns data are available for the 3-year period preceding and the 3-year period succeeding the year of the initial dividend. Thus, I require that at least 3 years elapse between the date of a firm's initial listing on the exchange and the date of its initial dividend.6

iii) Earnings announcement dates and earnings-per-share figures are available in the quarterly Compustat (1987) files and/or the Wall Street Journal Index (1969-86).

iv) Dividend announcement dates and dividends per share for the 14 quarters following the initial dividend are available on the CRSP files and/or the Wall Street Journal Index.

6. This criterion may induce a selection bias if the time interval between initial listing and the initial dividend is genuinely associated with firm-specific characteristics or leads to perceived differences across firms.

Impact of Dividend Initiation 181

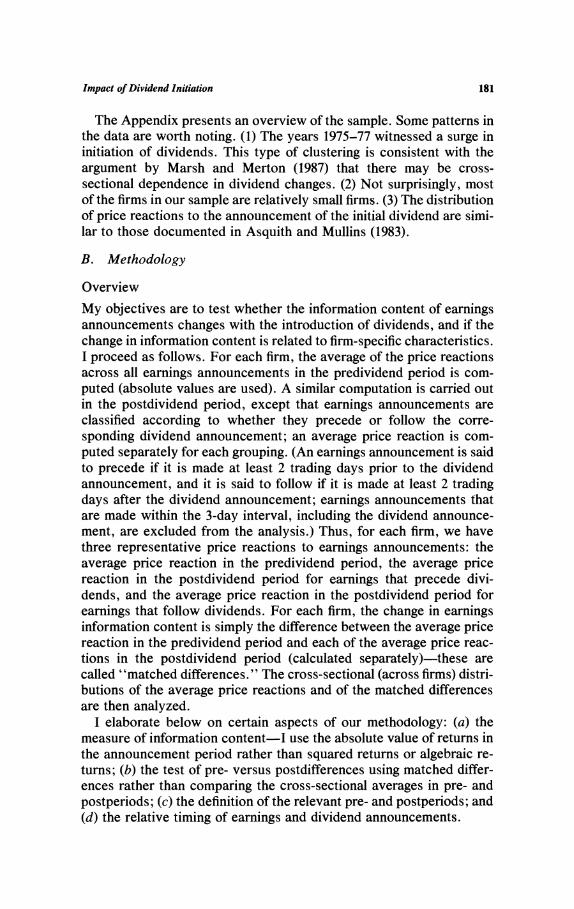

The Appendix presents an overview of the sample. Some patterns in the data are worth noting. (1) The years 1975-77 witnessed a surge in initiation of dividends. This type of clustering is consistent with the argument by Marsh and Merton (1987) that there may be cross- sectional dependence in dividend changes. (2) Not surprisingly, most of the firms in our sample are relatively small firms. (3) The distribution of price reactions to the announcement of the initial dividend are simi- lar to those documented in Asquith and Mullins (1983).

B. Methodology

Overview

My objectives are to test whether the information content of earnings announcements changes with the introduction of dividends, and if the change in information content is related to firm-specific characteristics. I proceed as follows. For each firm, the average of the price reactions across all earnings announcements in the predividend period is com- puted (absolute values are used). A similar computation is carried out in the postdividend period, except that earnings announcements are classified according to whether they precede or follow the corre- sponding dividend announcement; an average price reaction is com- puted separately for each grouping. (An earnings announcement is said to precede if it is made at least 2 trading days prior to the dividend announcement, and it is said to follow if it is made at least 2 trading days after the dividend announcement; earnings announcements that are made within the 3-day interval, including the dividend announce- ment, are excluded from the analysis.) Thus, for each firm, we have three representative price reactions to earnings announcements: the average price reaction in the predividend period, the average price reaction in the postdividend period for earnings that precede divi- dends, and the average price reaction in the postdividend period for earnings that follow dividends. For each firm, the change in earnings information content is simply the difference between the average price reaction in the predividend period and each of the average price reac- tions in the postdividend period (calculated separately)-these are called "matched differences." The cross-sectional (across firms) distri- butions of the average price reactions and of the matched differences are then analyzed.

I elaborate below on certain aspects of our methodology: (a) the measure of information content-I use the absolute value of returns in the announcement period rather than squared returns or algebraic re- turns; (b) the test of pre- versus postdifferences using matched differ- ences rather than comparing the cross-sectional averages in pre- and postperiods; (c) the definition of the relevant pre- and postperiods; and (d) the relative timing of earnings and dividend announcements.

182 Journal of Business

Details of the Methodology

Measure of information content. First, letting day 0 be the an- nouncement day, the absolute value of the sum of the algebraic returns on days - 1, 0, and + 1 is taken to be representative of the information content/price reaction of that announcement. For each firm, the aver- age of the price reactions across all announcements in the predividend period is computed. In the postdividend period, an average price reac- tion is computed separately for earnings announcements that precede and those that follow the corresponding quarterly dividend announce- ment (alternative definitions of pre- and postdividend periods and the relative timing of earnings and dividend announcements are discussed below). I conduct and report separately analyses using raw returns (i.e., observed returns without any risk or mean adjustment) and mar- ket-adjusted, excess returns.7

Absolute returns are used for two reasons: (i) under the assumption that the algebraic returns are normally distributed, the statistical the- ory for the absolute transformation is well developed (Johnson and Kotz 1970, pp. 81-83, 90; Leone, Nelson, and Nottingham 1961); and (ii) we are interested in the magnitudes of returns, abstracting from the signs of the returns-since the absolute return provides this, it is easier to interpret than, say, squared returns.

Tests of pre- versus postdifferences. For each firm, the change in earnings information content is given by the difference between the average price reactions in the pre- and postdividend periods; this dif- ference is taken separately for the two groups of earnings announce- ments (i.e., those that precede and those that follow the dividend announcement) in the postdividend period. They are referred to subse- quently as matched differences. The statistical tests are based on the cross-sectional (across firms) distributions of these matched differences.

Definition of the relevant pre- and postdividend periods. We adopt two definitions. The first definition simply treats the first 14 quarters as the predividend period and the last 14 quarters as the postdividend period. Under this definition, the difference between the average infor- mation content in the first 14 quarters and the average information content in the last 14 quarters forms the basis for our tests. However, it seems possible that the initiation date may be preceded and succeeded

7. To obtain market-adjusted excess returns, I run the following time-series regression for each firm:

Rt = a + b-I * Rm,t-I + b * Rm,t + b+I * Rm,t+I + et. This is the same procedure followed by Richardson et al. (1986). The relation is intended to capture the nonsynchronous dependence between the returns on a security and those on a market index. The excess returns used in the analysis are the "within-sample" residuals from this regression.

Impact of Dividend Initiation 183

by a transition period in which the firm's earnings/cash flows are quite different from their "norm." Since the immediate goal is to investigate the information content under more typical conditions, I use a second definition of pre- and postdividend periods. I subdivide the entire 29 quarters into four "windows" consisting, respectively, of the first 8 quarters (called period Ia), the next 6 (quarters 9-14, called period Ib), the next 6 (quarters 16-21, called period Ila), and the last 8 quarters (22-29, called period Ilb). When using this definition, the first and the last windows are treated as the relevant test periods.

Relative timing of quarterly earnings and dividend announcements in the postdividend period. An earnings announcement is said to pre- cede if it is made at least 2 trading days prior to the nearest dividend announcement and is said to follow if it is made at least 2 days after the nearest dividend announcement. Earnings announcements that are made within this window are treated as "joint" and excluded from the analysis. To compute an average price reaction for any firm, I require that at least three usable earnings announcements be available in each category. Panel A of table 1 gives, for the two-window analysis, the number of firms that meet this condition and hence are used in subse-

TABLE 1 Number of Firms and Announcements in Subsequent Analysis

Total No. of No. of firms for announcements

subsequent analysis represented

A. Two-window analysis: Predividend period (quarters 1-14) 72 939 Postdividend period (quarters 16-

29): a) Earnings precede dividends 55 373 b) Earnings follow dividends 51 243

B. Four-window analysis: Predividend subperiod 1, Ia (quar-

ters 1-8) 72 579 Predividend subperiod 2, lb (quar-

ters 9-14) 72 360 Postdividend subperiod 1, Ila (quar-

ters 16-21) 59 301 Postdividend subperiod 2, Ilb (quar-

ters 22-29) 71 428

NOTE.-Panel A gives, for the two-window analysis, the number of firms used in subsequent analysis and the total number of earnings announcements represented. In the postdividend period, earnings announcements are grouped according to whether they precede or follow dividend an- nouncements. (An earnings announcement is said to precede if it is made at least 2 trading days prior to the dividend announcement and said to follow if it is made at least 2 days after.) To be included in subsequent analysis, a firm must have at least three usable announcements in a particular grouping. Hence, in general, there are fewer firms included in the postdividend groups than in the predividend group. Panel B gives similar information for the four-window analysis. Here, the distinction between earnings preceding/following dividends is dropped: for a given firm, all earnings announcements made outside the 3-day interval containing a dividend announcement are included for analysis. A firm must have at least three such announcements to be included for later analysis.

184 Journal of Business

quent analysis and also the total number of announcements repre- sented. For the four-window analysis, I drop the distinction between earnings that precede and those that follow. All earnings announce- ments that are made outside the 3-day interval containing the dividend announcement are considered for analysis. As before, a firm must have at least three such announcements for it to be included for subsequent analysis. Panel B of table 1 gives the same data as panel A for the four- window analysis.

IV. Results

A. Changes in Information Content

Two-window analysis. Table 2 provides the basic results. Panel A presents the summary statistics from the cross-sectional distributions of the average information content of earnings announcements in the pre- and postdividend periods. Information content measures are com- puted using raw returns as well as market-adjusted, excess returns. As discussed previously, in the postdividend period I distinguish between earnings announcements that preceded the associated dividend an- nouncements and those that followed. The results are based on the "two-window" analysis (i.e., the predividend window includes quar- ters 1-14, the postdividend window includes quarters 16-29, and the initial dividend is made in quarter 15).

Panel A indicates that the cross-sectional mean and median of the average price reaction are noticeably smaller in the postdividend pe- riod. This is true regardless of whether the earnings announcement preceded or followed the dividend announcement. There is little differ- ence between the results using raw returns and those based on the market-adjusted returns.

Panel B provides the summary statistics from the cross-sectional distribution of the matched difference (i.e., the cross-sectional distri- bution of the average predividend information content less the average postdividend information content). For earnings that precede divi- dends, the mean and median indicate that the average price reaction to earnings announcement is smaller by at least 1 percentage point in the postdividend period. Also, the postdividend price reaction is smaller for 80% of the firms (44 of 55). For earnings that follow dividends, the median values indicate a reduction in average price reaction of 0.68% (for market-adjusted returns) and 1.04% (for raw returns). The means are somewhat smaller than the medians primarily because of one large negative value.8 The postdividend price reaction is smaller for 70% of the firms (36 of 51).

8. Notes labeled t and ? in table 2 indicate the means and t-statistics after adjusting for the "outliers." The t-statistics are then significant at the 5% level.

Impact of Dividend Initiation 185

Finally, panel C of table 2 provides the results of statistical tests of the hypothesis that the price reaction to earnings announcements is, on average, smaller in the postdividend period. This amounts to a test of whether the location parameter of the cross-sectional distribution of the change in information content (i.e., the matched diffelence) is posi- tive. The rejection levels from the Wilcoxon and the t-tests clearly support the (alternative) hypothesis that the information content of earnings announcements is smaller in the postdividend period.9

In sum, the results indicate that the average price reaction to earn- ings announcement is generally smaller after the introduction of divi- dends. The results are stronger when earnings precede dividends; that is, earnings announcements that follow dividends (in the postdividend period) tend to produce a larger price reaction than those that precede. Although not reported here, we found a similar result for dividend announcements; that is, price reactions were larger for dividend an- nouncements that followed earnings announcements. This suggests that the two announcements are complements (i.e., partial, not per- fect, substitutes) and is broadly consistent with the evidence in Kane et al. (1984) and Venkatesh and Chiang (1986).

Healy and Palepu (1988) find that stock price responsiveness to an- nual earnings announcements is generally smaller in the postdividend period, but the reduction is significant only in the year of the initial dividend. Our results suggest a permanent, significant reduction in the information content of quarterly earnings announcements. The results may not be directly comparable because of differences in statistical procedures and the use of annual versus quarterly earnings. It is also possible that other corporate announcements (dividends, other plans, etc.) are made along with annual earnings announcements; this is prob- ably less likely for quarterly announcements.

Four-window analysis. As discussed in the previous section, it is possible that the quarters immediately adjacent to the initial dividend quarter constitute a transition period and are not typical. In particular, it is conceivable that the results in table 2 were influenced by the inclusion of atypical announcements. For example, if earnings an- nouncements immediately preceding the initial dividend were "un- usually" informative (presumably, positive surprises), followed by "unusually" uninformative earnings announcements in the immediate postdividend period, we may mistakenly conclude that initiation of dividends reduces the information content of earnings announcements over longer periods. I account for this possibility by subdividing the pre- and postdividend periods as described in Section III. It is assumed

9. The t-statistics for the group "earnings follow dividends" does not appear to be significant; however, as indicated in notes labeled t and ? in table 2, the t-statistics, after adjusting for what appear to be outliers, are significant at the 5% level.

186 Journal of Business

>.

.E~~~~~W oo C\

CD CD 00"I r

Y ~ ~ ~ ~ ~ ~ ~ ~ ~ ~~~~~ rA CD W) It

U E N ce om be cO~~~~~~~~~"I

tD ~ ~ ~~~~~W ct CDs 00 -4 11 N m t

*

l C) W) W) It

sX~~~~~~~0 r0 C)0 \0 I I

O .

fl 3 ' @z a', ''b3t''b&^ R~~~~~~~~~> Z

Impact of Dividend Initiation 187

=0 110, I 2 r.

4+ CIC*

4

C: 4.4 4-4 > 0 0 0

> cd >,,= > - -j t V Cd Cd 7:1,-1 Cd 4., 0

Cd Cd 4-4

o 0 0 0 ,, 4) 7:1 E --- < > > 4-i 4) O lz cn Cd 4-4

7:1 Cd 'al 7 > 0

0.4 4:1 cd 0 >

u Cd Cd 7:$ 7:1 > 0 4) 0 u Cd Cd + 7:1

C's Cd Cd 7:$ 0 >

cd .- 7:1

7:1 -tzl 7:1 Cd 7:$ 7:$ cn cn 7:$ 0 Cd Cd

lz Cd

Cd Cd Cd J., cd

0 7:$ Cd 'C 0 o 0 0 0 4-4

cd O'D cd 0 -al V _5

Cd cn Cd 4- 03 cd cn "I0 0 0 j::j 0 cd al F-4 x P4 C) C) > 7:$ 7:$ CD 0 0 0 -t:l Cd

W) cd 110 en 00 00 14-4

4-4 7:$ 0 0

0 + cd Cd 0 2:: C Cd Cd 7 cd

0 E E $_4 0 Cd Cd

7 7:$ lz

0 'al Cd

0 cd Cd cd

cd 0 %-W 7:$ ,U >

cd 7:$ Cd ,::j

00

0 7:$

Cd cd 'Z = 0

A E-4

4;4 O ml

4) 4-t Ml 0 Ei 4) 4) 4-4 Ei 0 o o '8 cd cd cn >

> C's up

0 lal 0 4;4

c d V 0 F" R cd > > 0 ., - -al 0 M CZ

0 0 Cd

Ei cd 64 40, C id U

4) Ei Ei cd 'O' =., 4) > 4m,

(A 4.4 4.4 0 0.4.- P4 P4 ,. 11 " " O>.,,. , Cd Z 4+

U

188 Journal of Business

that the earnings announcements in the periods more distant from the initial dividend, namely those in periods Ia (quarters 1-8) and Ilb (quarters 22-29), are more representative or typical than the announce- ments in periods lb (quarters 9-14) and Ila (quarters 16-21). To keep the tables short (and in view of the relatively mild differences between them), I drop the distinction between whether the earnings announce- ment preceded or followed the dividend announcement. All earnings announcements that are made outside the 3-day interval bracketing a dividend announcement are used. The results of this analysis using raw returns are presented in table 3-the results with excess returns are virtually the same and not reported here.

Panel A contains the summary statistics from the cross-sectional distributions of the average information content in each of the sub- periods. The mean and median price reactions in the predividend sub- periods (i.e., Ia and Ib) are generally higher than those in the post- dividend subperiods (i.e., Ila and Ilb) and are clearly largest in the first predividend subperiod (Ia). This reaffirms the results of the two- window analysis (in table 2). Price reactions in the two postdividend subperiods, Ila and Ilb, are very similar to each other. The mean price reaction in the second predividend subperiod, Ib, is lower than that in the first predividend subperiod, Ia, but higher than those in the post- dividend subperiods Ila and Ilb. These observations are confirmed by the results in panel B, which presents summary statistics for the matched differences, and also by the statistical tests in panel C of table 3.

In summary, the results of the four-window analysis indicates that the two-window analysis is quite robust with respect to the definition of the relevant pre- and postdividend periods. That is, the conclusion that earnings announcements are more informative in the predividend pe- riod is not simply due to a few "unusual" earnings announcements in the quarters immediately surrounding the initial dividend. In view of this, I report only the results for the two-window analysis in the subsequent tests.

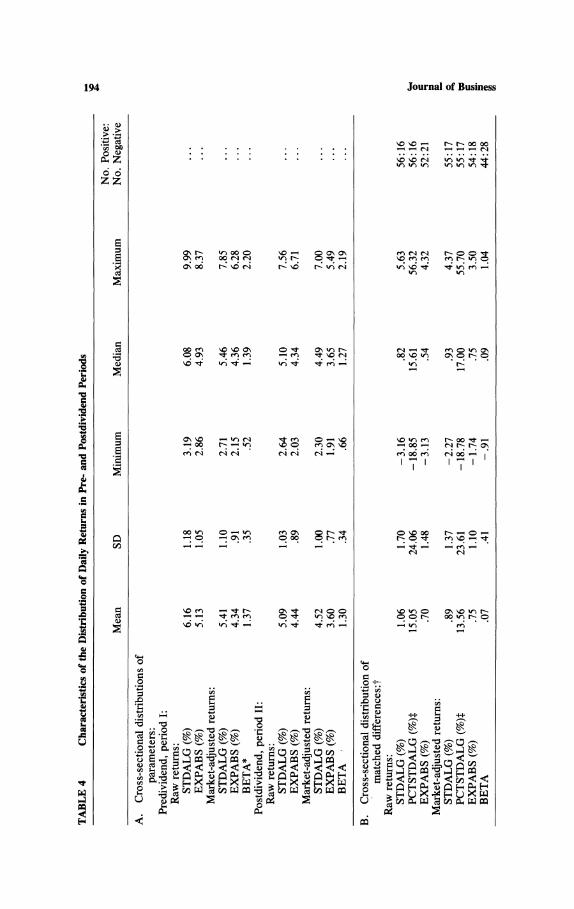

B. Characteristics of the Distributions of Daily Returns in the Pre- and Postdividend Periods

In this section, I document that dividend initiation has an impact on the characteristics of daily returns (i.e., nonannouncement, "typical" trading days). I find that the volatility of daily returns falls after divi- dend initiation. This is true for raw returns as well as excess returns and for different measures of volatility. Furthermore, most of the de- crease in the volatility of raw/total returns is attributable to a decrease in the nonmarket or "firm-specific" component of volatility. The aver- age change in the market-sensitivity coefficient (i.e., BETA) is rela- tively quite small.

Impact of Dividend Initiation 189

Although such a result is not predicted by any theory, I can offer an explanation that is consistent with the "dividend-information/ dividend-signaling" argument. Quite simply, with the dividend-infor- mation mechanism in place (i.e., in the postdividend period), it is con- ceivable that investors accord less importance to other pieces of information that could have induced price reactions in the predividend period. Thus, there may be fewer large-magnitude price changes in general in the postdividend period, and observed volatility may be lower.

Computations-overview. The computations are carried out as fol- lows. For each firm, I compute two parameters that characterize the volatility/variability of daily returns. Estimation is carried out sepa- rately over all days (nonannouncement as well as announcement days) in the pre- and postdividend periods. The parameters are computed for raw (total) returns as well as market-adjusted, excess returns. The cross-sectional distributions of these parameters and of the matched differences in the parameters are used to evaluate whether the charac- teristics of returns are different between pre- and postdividend periods.

Computations-details. Recall that the price reaction around an announcement date was computed as the absolute value of the sum of the algebraic returns on the 3 days bracketing the announcement date. To maintain comparability (and, if desired, to standardize announce- ment price reactions), I continue to use the sum of the algebraic returns on 3 successive days as the basic unit of return; denote this 3- day summed return by RALG3 and the absolute value of RALG3 by RABS3.10 In the predividend period, the distribution of RALG3 and RABS3 is computed over the interval from quarter l's first earnings announcement date to the initial dividend date; this includes all 3-day intervals with nonmissing returns. In the postdividend period, the dis- tributions are generated over the interval from the initial dividend date to the last earnings date for quarter 29. From these distributions, I compute for each firm the following parameters (separately for pre- and postdividend periods): (i) the standard deviation of the distribution of RALG3, denoted by STDALG-this measure is the same as conven- tional measures of return volatility, except that it is based on 3-day returns; and (ii) the mean of the distribution of RABS3, denoted by EXPABS-this can be interpreted as the magnitude of the price change (i.e., absolute value) over a "typical" 3-day interval and hence can be used to "standardize" announcement price reactions, if so desired.

All of the above computations are repeated using market-adjusted excess returns; that is, distributions of RALG3 and RABS3 are gener- ated using excess returns rather than raw returns, and the parameters

10. Qualitatively similar results are obtained when using 1-day returns rather than the 3-day-summed return.

190 Journal of Business

>~~~~~~ e> 'rs ON -

c,o . : : : : N. . . . ^ N

S o o . . . . -

t Nt 0 0

et z z

S

= ? o ~~~t co

0~~~~~~~~0

. . r '" 1 : . oC o-I 0 0 N N

: S m ~~~~t t Nt

- 00 'IC

41.1 ON -l r - 00 00 - ~C CiN

cn 1\ N o ^t --- N

44 "0 -- ' ON C - N ON C-~

.~ 0 0 e~~C "t ' e

Cu~~~~~~~~~~~I

> 64 6 t t

- Z

_ x C- ON ON - "3

o C:t, 0 l ON 0 E Ao e

_ 5> f g bi *5 r Cr~r r, r-, >r 1r

Y~~ - - e. C 't C- 'rl

-4 C1-sggs .. U U 4

0 0 0CON~

_ 3 c = r =r=r=r=r3 r~ 0 o 0 ON

~~' 444 ~~4),00000 0

6- - " - el O -z ON - ONz

Impact of Dividend Initiation 191

+..- , 0 , 0 m I.. cn

7 0 > 0 e s F- C:

0 cn

---4 'IC ---4 Nt 0 0 00 00 INC W)

R -,0 U 0 r. 0 0

Ei 0

P4 .2 0 Ei

cd cd

P4 0 0 4) r. , > I., cd 0

Cd > u 40.

u Cd 0 -, 0 0

4mo

Ei 0 0 ll 0.> C! t

OWM0 r.00 Cd

0 15 >, O.- 0 0 cd 6

Cd .0 r. 0 0

0 0

0 0 : = x P4 00 " -1 -1 0 Cd Ei

Cd C) W) Nt INC C) 0 r. Cd

-4 : m w W) ,C ,C 4f 4 t 0

o cd V cn .- 10. 0 0 > 0

Ei OC .40Z Cd cd 0 -

r- Ei Ei 0 CZ 0

Cd cd Ei -u5 r. 00

> 45- 0

r. cd

Cd " 4- 0

cd = -5 , 7; Cd

Cd r. , 0 = 0 cd .44 Ei :.5 ,

4 0

0 (5 - ll

64

40, 0 r. o Cd

0 M 0 7 Ei >1 r. r. Ei

Cd 0 o o 0 4;4 -

--z Cd 0-4 a , > 7 C$ cq r. o Ei

0 4

C$ C$ 4-i 0 -Z 0 o -4 0-4 0-4 0

Cd -4 r4 -4 r r r r r E Cd > > -4 -4 ., q -8 E -, x

4 -4 0-4 0 4) Ei cd 0 `C$ C$ `C$ 4) . > cd 4) Ei

Ei cl 0 0 0 0

04 t CZ 4--,

cd > 0 .-

to 84 Ei 0, Cd

0 C$ cd = Ei 0 0 Ei m o Ei

Cd 0 iz

Cd c cd 0 Ei -i Ei "u go 4)

7 It:$ cq a$ cq 0 cd Cd 0 Ei Ei C$ C$ C$ C$ C$ IZ >

a$ 0 ,t:s 0 0 0 0 0 0 0 " -4 .-4.,-4 O'.- Cd . > e, Z.,

C) -4 -4 -4 .

r > > > > > -S u Ei

Q.-4 0 -4 0 0

0 t CZ 0 = - 0 Z m " Cd O.

0 u 0 Cd cr Cd 0 "I

192 Journal of Business

computed accordingly. I also provide data on the "market-sensitivity" coefficient, denoted by BETA in the table."

Results. Panel A of table 4 provides summary statistics from the cross-sectional distributions of STDALG, EXPABS, and BETA for the pre- and postdividend periods. Panel B contains the summary statistics for the matched differences. The volatility of raw returns, as measured by STDALG, is distinctly lower in the postdividend period; the aver- age magnitude of reduction in STDALG is 1.06 percentage points. The percentage reduction (relative to the predividend value) is given by PCTSTDALG; the mean and median of PCTSTDALG indicate that, on average, the postdividend STDALG is about 15% lower than the pre- dividend value. The behavior of EXPABS is very similar to that of STDALG.

Similar patterns are observed with market-adjusted excess returns; on average, the postdividend volatility (STDALG) is lower by .89 per- centage points and about 14% lower in percentage terms. The changes in the market-sensitivity coefficient, BETA, are much less marked. Although the BETA in the predividend period tends to be higher (44 decreases and 28 increases), the magnitudes are quite small; the aver- age decrease in BETA is only 0.07.

Panel C of table 4 reports the results of statistical tests of whether the parameters are equal in the 2 periods. We can conclude with a high degree of confidence that the parameters STDALG and EXPABS are higher in the predividend period. The data also suggest that BETA is slightly higher in the predividend period but only at a significance level greater than the 5% level.

For each firm I also computed the ratio of the change in the volatility of excess returns to the change in volatility of raw (total) returns. This gives an approximate idea of how much of the change in volatility of total (raw) returns is "due" to a change in the firm-specific volatility (proxied by volatility of excess returns); I interpret a ratio value close to 1.0 as indicating that most of the change in total volatility arises from a change in firm-specific volatility. 12 Panel D gives the cross-sectional distribution of the ratio. The median and mean of 0.83 and 0.84, respec- tively, suggest that change in firm-specific volatility is primarily re- sponsible for the change in total volatility.

V. Relationship to Firm-specific Characteristics

I examined whether the change in earnings information content and the change in volatility are related to firm-specific characteristics. I tested

11. Beta is equal to the sum of the three market-sensitivity coefficients in the regres- sion described in n. 7 above.

12. Similar results are obtained when using the ratio of the change in the variance of excess returns to the change in the variance of total returns.

Impact of Dividend Initiation 193

for a relationship between the change in the information content of earnings announcements and (a) market value of equity, (b) number of years elapsed between initial listing and the initial dividend, YRDFF, and (c) exchange listing. A number of studies have documented that earnings-information content is negatively related to firm size (e.g., Atiase 1985) and is smaller for NYSE firms as compared to over-the- counter (OTC) firms (Grant 1980). 13 The authors explain the results on the grounds that "more information" may be available for large firms and NYSE firms (as compared to AMEX and OTC firms). If this is true, dividends may be less important as an information mechanism for such firms, and, by extension, the reduction in earnings-information content should be very small. A negative relationship with the variable YRDFF is likely because for firms with larger values of YRDFF, the market may have sought out other means of uncovering inside informa- tion, or management may have established other forms of com- munication. 14

In running a regression, I find no (linear) relationship between the change in earnings information content, equity value, and YRDFF. Surprisingly, I do find that the decrease in earnings-information con- tent is somewhat larger for NYSE firms as compared to AMEX firms. This suggests that the information role of dividends may be more im- portant for NYSE firms. There is also weak evidence that the reduction in volatility is greater for NYSE firms.

VI. Conclusions

This article investigates the empirical consequences of initiating quar- terly cash dividends. One of my principal objectives is to examine the impact of the introduction of an alternative information vehicle (namely, dividends) on the information content of earnings announce- ments. I find that the information content of earnings announcements is substantially lower after the introduction of quarterly cash dividends. This is true regardless of whether the earnings announcements precede or follow the associated dividend announcements. The results are gen- erally consistent with the notion that dividends and earnings are par- tial, but not perfect, information substitutes.

I also find that the volatility of daily returns is lower in the post- dividend period. Most of the decrease in the volatility of total (raw) returns stems from a decrease in firm-specific volatility. A possible explanation for this result is that in the postdividend period investors

13. The definition of information content used by these authors is not the same as mine, but those results are not likely to be very sensitive to the definition.

14. Firms with large YRDFF may have attracted a clientele that prefers low-payout stocks. If so, the price reactions at the announcement of the initial dividend may be negative (perhaps in the short-run) rather than positive. I propose to investigate this with a larger sample of firms (for which earnings announcement dates are not required).

194 Journal of Business

z z

*-N V)o C.- O \O\ C A O o c 0: O : : : : . . . . . N

,^ . o b e r 'e o o oOOr \O o^N Nboo .E ~~~~o cn \0 \0 a \?^^

c ' oo ? N 0 e O\. CIc \ VI) a C - ,CD

E

E

~~~~~~o - V' a\ \0 co r- r- a\ X

a

oOVo 0-Vm er~O\ N> 0oCe 0 ; 0- - o

V OI)C 0ooo\

\0 o reC-

D~~~~~~~~~~a cn c

~~~~~~~~~~~~~~~~c4 ) S X>c) , e )v rv-v

Cdcn- . - - . X r 0~~~~~~~~~~~~~

0~~~~~~~~

0

.0~~~~~~~~~~~~~~~~d1

0 0~~~~

Impact of Dividend Initiation 195

ce !Z 0 -0 u

ce

cd Cd

Z! > 4, 0 0 9 0 0 0

00 ce u 0 0 0 4) O 4) 4-t

> 0 4, u

Cd Cd r

ce C) 0

Cd >

10 cd !:i 0 >

4) COO cn

0 Cd

C's ce O >1.10 ce cd

-S 0 72 0

E- ce >

0 cd ce =3 P4 0 M 0 = C)

.-

0u llc 4-, "u > P4 0 0

"u 0 r- 00 'IC 4-4

0 Cd

C) ce , O np 0 co r. r- 0 0

0 ce

4-4

0 Cd 4-t .,000 000io

cn > cd lz 0 cd 0 15

-C 4- O >

Cd 4-t O 0

0 Cd 0 0 ce $-. ce Cd ce = > >

.14 . .4 4-t 4 O > 0 4, O .4 ce

O -C Cd Cd Cd O B u S-4 S-4 ce Cd Cd 4-t cn 0 - = ce 0 0 .0 04

ce X Cd 0

00 C S 42, S :Z 0 J 0 4-t cd

ce 0 0 > Cd O .0 s. 0 'O 0 O O ce 0;

O 0 en ce >

4-4 0

ce 4-4 s.. cd (U (U

Cd =3 0 O (U

cd Cd

4-4 C) C) Cd .r Co (u 0 > 0

(U Cd 0 .0 Cd cd(u (u

(U 1.4 0

O U

Z 4- 4+ OM O 0

4C." O.. U) > >

196 Journal of Business

give less weight to information cues (other than dividends and earn- ings) than they do in the predividend period.

Finally, there is mild evidence that the reduction in earnings infor- mation content is larger for NYSE firms as compared to AMEX firms. This suggests that the information role of dividends may be more im- portant for NYSE firms. In summary, the evidence in this article sug- gests that the initiation of dividends is an important economic event that results in visible impacts on the characteristics of stock price behavior.

Appendix

Overview of the Sample

A. Number of Firms That Initiated Cash Dividends by Year

1972 1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 Total

3 7 6 9 12 19 4 5 3 0 1 3 72

B. Years Elapsed between Listing (on Exchange) and Initiation of Dividend

Years 3 4 5 6 7 8 9 10 11 12 13 14 15 16+

No. of firms 9 10 6 8 2 7 6 1 4 3 3 5 3 5

(C. Market Value of Equity*

Market Less Value than 20 ($) million 20-50 51-80 80-100 100-150 150-200 200-500 500+

No. of firms 27 15 11 4 5 2 4 4

NOTE.-Median market value: $31 million; mean market value: $145 million; minimum market value: $2.37 million; maximum market value: $2,330 million. All market values show dollars in millions.

* These are average amounts during the year of initial dividend.

D. Cross-sectional Distribution of Price Reactions to Announcement of Initial Dividend; Sum of Returns on Days -1, 0, and + I Where Day 0 Is the Announcement Day

No. Minimum 10% 25% 50% 75% 90% Maximum Mean 50 Positive

Raw returns (%) - 11.04 -5.48 .07 3.36 7.16 10.80 30.74 3.73 6.98 56 of 72 Excess returns (%)* - 11.89 -3.3 .13 2.35 6.6 10.29 31.40 3.46 6.53 55 of 72

* The procedure for computing excess returns is described in table 1.

Impact of Dividend Initiation 197

References

Aharony, J., and Swary, I. 1980. Quarterly dividend and earnings announcements and stockholders's returns: An empirical analysis. Journal of Finance 35 (March): 1-12.

Asquith, P., and Mullins, D. 1983. The impact of initiating dividend payments on share- holders' wealth. Journal of Business 46 (January): 77-96.

Asquith, P., and Mullins, D. 1986. Signalling with dividends, stock repurchases and equity issues. Financial Management (Autumn): 27-44.

Atiase, R. K. 1985. Predisclosure information, firm capitalization and security price behavior around earnings announcements. Journal of Accounting Research 23 (Spring): 21-36.

Grant, E. 1980. Market implications of differential amounts of interim information. Jour- nal of Accounting Research 18 (Spring): 255-68.

Healy, P., and Palepu, K. 1988. Earnings information conveyed by dividend initiations and omissions. Journal of Financial Economics 21 (September): 149-75.

John, K., and Nachman, D. 1987. Multiperiod financing strategies and dividend manage- ment. Working paper. New York: New York University; Atlanta: Georgia Institute of Technology.

John, K., and Williams, J. 1985. Dividends, dilution and taxes: A signalling equilibrium. Journal of Finance 40 (September): 1053-70.

Johnson, N., and Kotz, S. 1970. Continuous Univariate Distributions-i. New York: Wiley.

Kane, A.; Lee, Y.; and Marcus, A. 1984. Earnings and dividend announcements: Is there a corroboration effect? Journal of Finance 39 (September): 1091-1100.

Kormendi, R., and Lipe, R. 1987. Earnings innovations, earnings persistence, and stock returns. Journal of Business 60 (July): 323-45.

Leone, F.; Nelson, L.; and Nottingham, R. 1961. The folded normal distribution. Tech- nometrics 3 (November): 543-50.

Marsh, T., and Merton, R. 1987. Dividend behavior for the aggregate stock market. Journal of Business 60 (January): 1-40.

Miller, M., and Rock, K. 1985. Dividend policy under asymmetric information. Journal of Finance 40 (September): 1031-52.

Ofer, A., and Siegel, D. 1987. Corporate financial policy, information, and market expec- tations: An empirical investigation of dividends. Journal of Finance 42 (September): 889-912.

Richardson, G.; Sefcik, S.; and Thompson, R. 1986. A test of dividend irrelevance using volume reactions to a change in dividend policy. Journal of Financial Economics 17 (December): 313-34.

Venkatesh, P. C., and Chiang, R. 1986. Information asymmetry and the dealer's bid-ask spread: A case study of earnings and dividend announcements. Journal of Finance 41 (December): 1089-1102.

Wall Street Journal Index. 1969-86. New York: Dow Jones.