the indian experience with managing capital flows - … indian experience with managing capital...

TRANSCRIPT

1

The Indian Experience with Managing Capital Flows

SUBIR GOKARN Deputy Governor

Reserve Bank of India

High-level Seminar on Managing Capital Flows to Emerging Markets, Rio de Janeiro

May 26-27,2011

2

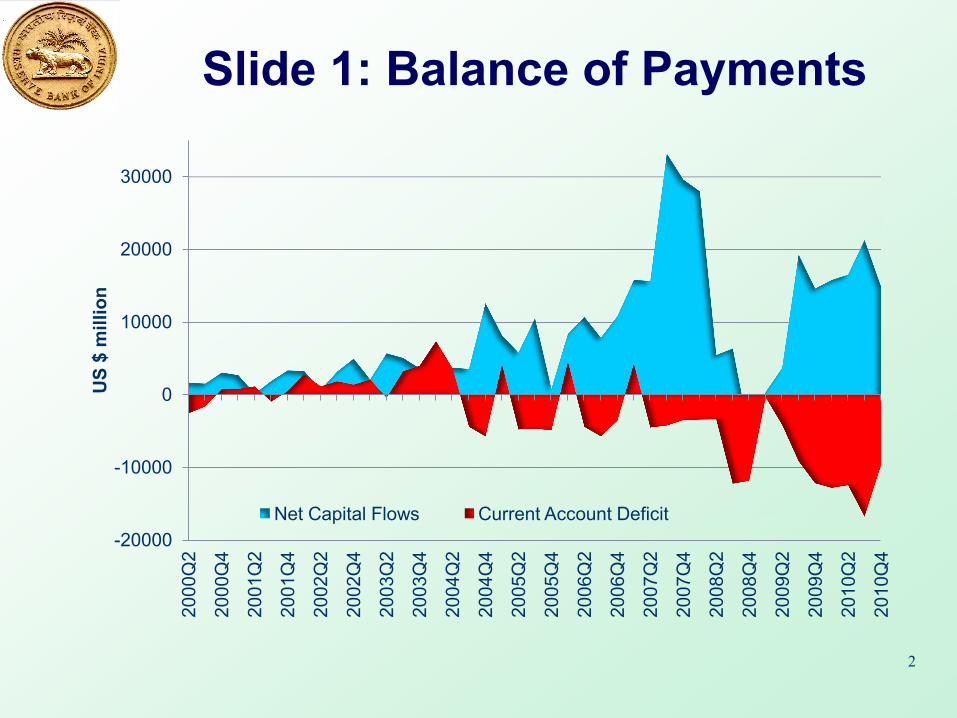

Slide 1: Balance of Payments

-20000

-10000

0

10000

20000

30000 20

00Q

2

2000

Q4

2001

Q2

2001

Q4

2002

Q2

2002

Q4

2003

Q2

2003

Q4

2004

Q2

2004

Q4

2005

Q2

2005

Q4

2006

Q2

2006

Q4

2007

Q2

2007

Q4

2008

Q2

2008

Q4

2009

Q2

2009

Q4

2010

Q2

2010

Q4

US

$ m

illio

n

Net Capital Flows Current Account Deficit

3

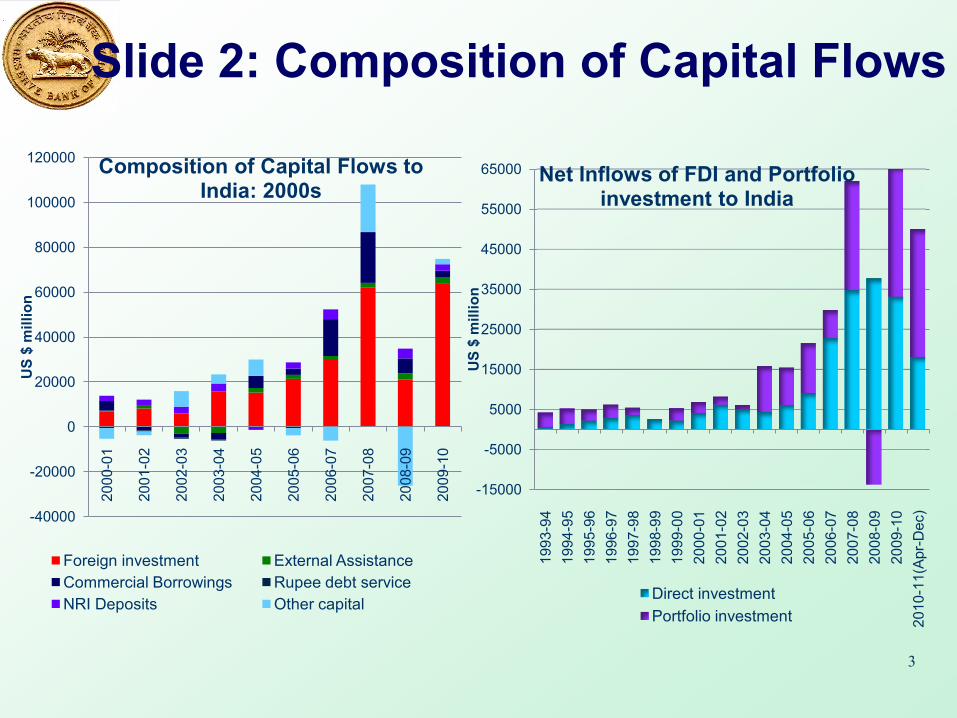

Slide 2: Composition of Capital Flows

-40000

-20000

0

20000

40000

60000

80000

100000

120000

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

US

$ m

illio

n

Composition of Capital Flows to India: 2000s

Foreign investment External Assistance Commercial Borrowings Rupee debt service NRI Deposits Other capital

-15000

-5000

5000

15000

25000

35000

45000

55000

65000

1993

-94

19

94-9

5

1995

-96

19

96-9

7

1997

-98

19

98-9

9

1999

-00

20

00-0

1

2001

-02

20

02-0

3

2003

-04

20

04-0

5

2005

-06

20

06-0

7

2007

-08

20

08-0

9

2009

-10

20

10-1

1(Ap

r-D

ec)

US

$ m

illio

n

Net Inflows of FDI and Portfolio investment to India

Direct investment Portfolio investment

4

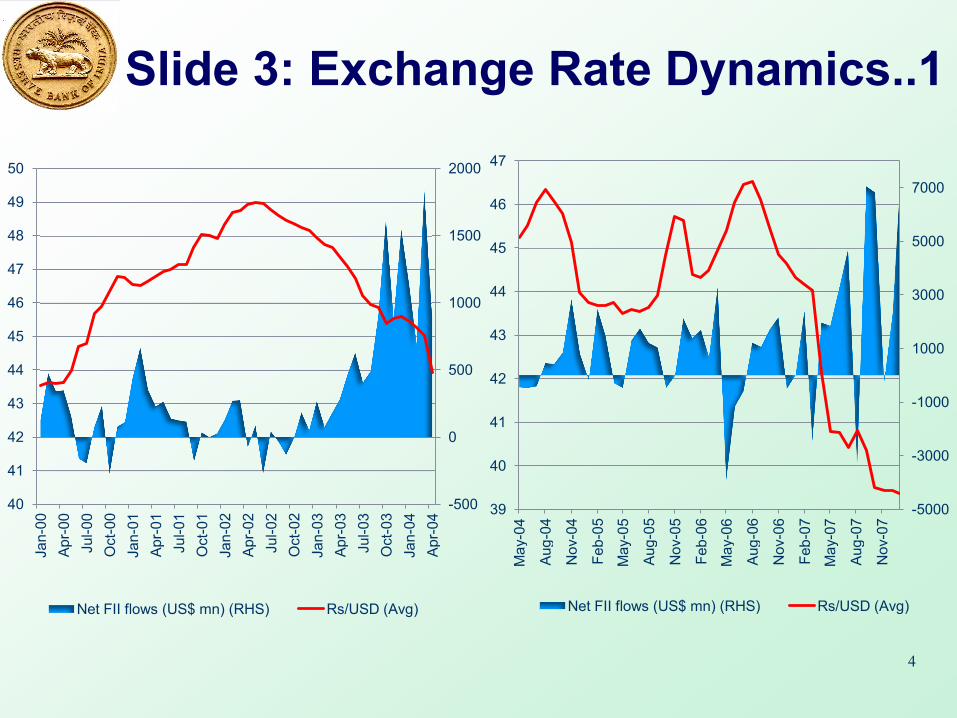

Slide 3: Exchange Rate Dynamics..1

-500

0

500

1000

1500

2000

40

41

42

43

44

45

46

47

48

49

50

Jan-

00

Apr-

00

Jul-0

0 O

ct-0

0 Ja

n-01

Ap

r-01

Ju

l-01

Oct

-01

Jan-

02

Apr-

02

Jul-0

2 O

ct-0

2 Ja

n-03

Ap

r-03

Ju

l-03

Oct

-03

Jan-

04

Apr-

04

Net FII flows (US$ mn) (RHS) Rs/USD (Avg)

-5000

-3000

-1000

1000

3000

5000

7000

39

40

41

42

43

44

45

46

47

May

-04

Aug-

04

Nov

-04

Feb-

05

May

-05

Aug-

05

Nov

-05

Feb-

06

May

-06

Aug-

06

Nov

-06

Feb-

07

May

-07

Aug-

07

Nov

-07

Net FII flows (US$ mn) (RHS) Rs/USD (Avg)

5

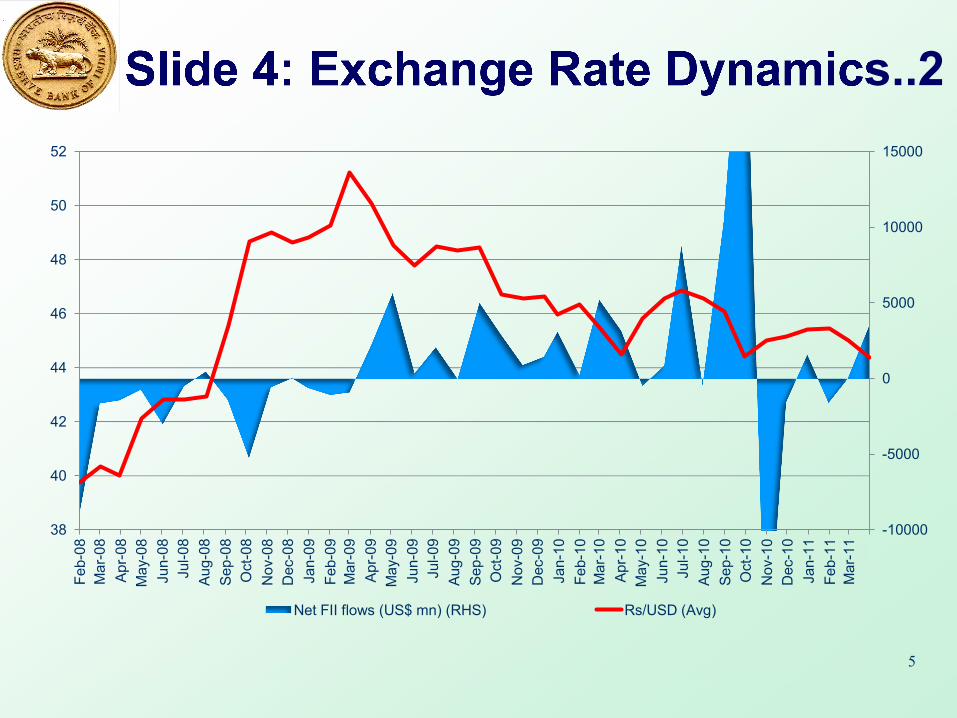

Slide 4: Exchange Rate Dynamics..2

-10000

-5000

0

5000

10000

15000

38

40

42

44

46

48

50

52

Feb-

08

Mar

-08

Apr-

08

May

-08

Jun-

08

Jul-0

8 Au

g-08

Se

p-08

O

ct-0

8 N

ov-0

8 D

ec-0

8 Ja

n-09

Fe

b-09

M

ar-0

9 Ap

r-09

M

ay-0

9 Ju

n-09

Ju

l-09

Aug-

09

Sep-

09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr-

10

May

-10

Jun-

10

Jul-1

0 Au

g-10

Se

p-10

O

ct-1

0 N

ov-1

0 D

ec-1

0 Ja

n-11

Fe

b-11

M

ar-1

1

Net FII flows (US$ mn) (RHS) Rs/USD (Avg)

6

Slide 5: An Evolving Approach: The Exchange Rate

• Transition from balance to net surplus in the early 2000s

• Phase 1 Response (until Jan 2007): Intervention with sterilization • Design and use of Market Stabilization

Bonds • Phase 2 Response (Feb 2007 onwards): Essentially no intervention

7

Slide 6: An Evolving Approach: Capital Controls

Preference Ordering Foreign Direct Investment Foreign Portfolio Investment in Equities Long-term Debt Short-term Debt

Barring some sector-specific constraints, FDI flows are unconstrained

Equity investments are unconstrained for institutions; new channels have been created for individuals

Debt flows are subject to approval relating to end-use Some quantitative and pricing controls are in effect on

debt flows

8

Slide 7: A Conceptual View…1 Co-existence between capital controls and effectively

floating exchange rate since 2007

Strategic vs. Tactical Controls Preference Ordering reflects a strategic view of

macroeconomic benefits and risks of different channels Once controls are in place, they stay for some time,

making rules of the game stable and predictable “Reform” then implies a change in the risk-benefit

assessment of specific channels

Intervention and controls such as URR are tactical in nature

Issues of predictability and monetary management

9

Slide 8: A Conceptual View…2 Intervention and controls such as URR are tactical in

nature Issues of predictability and monetary management Assessment Non-intervention has facilitated monetary policy

operations It has made stakeholders sensitive to exchange rate

risk, resulting in more effective hedging “Reform” implies development of market-based

hedging instruments and better regulation of OTC instruments

10

Slide 9: Concluding Thoughts The Indian capital flow management framework has

evolved in response to challenges in maintaining macroeconomic stability

Even as intervention has been stopped, controls on some forms of inflows are still considered necessary

A balance has been sought through the conceptual distinction between strategic and tactical controls

Country circumstances differ and should determine the approach

However, this distinction might provide a useful input into the thought process