the online purchase experience in china: local champions...

TRANSCRIPT

LUXURY GOODS

The Online Purchase Experience in China: Local Champions Dominate

25 JANUARY 2017 at 06:01* We continue our analysis of how the luxury goods brands perform online. We shift our focus to

China, after having tested the Italian and US markets The Online Purchase Experience Ranking,

The Online Purchase Experience Ranking: From Milan to New York City

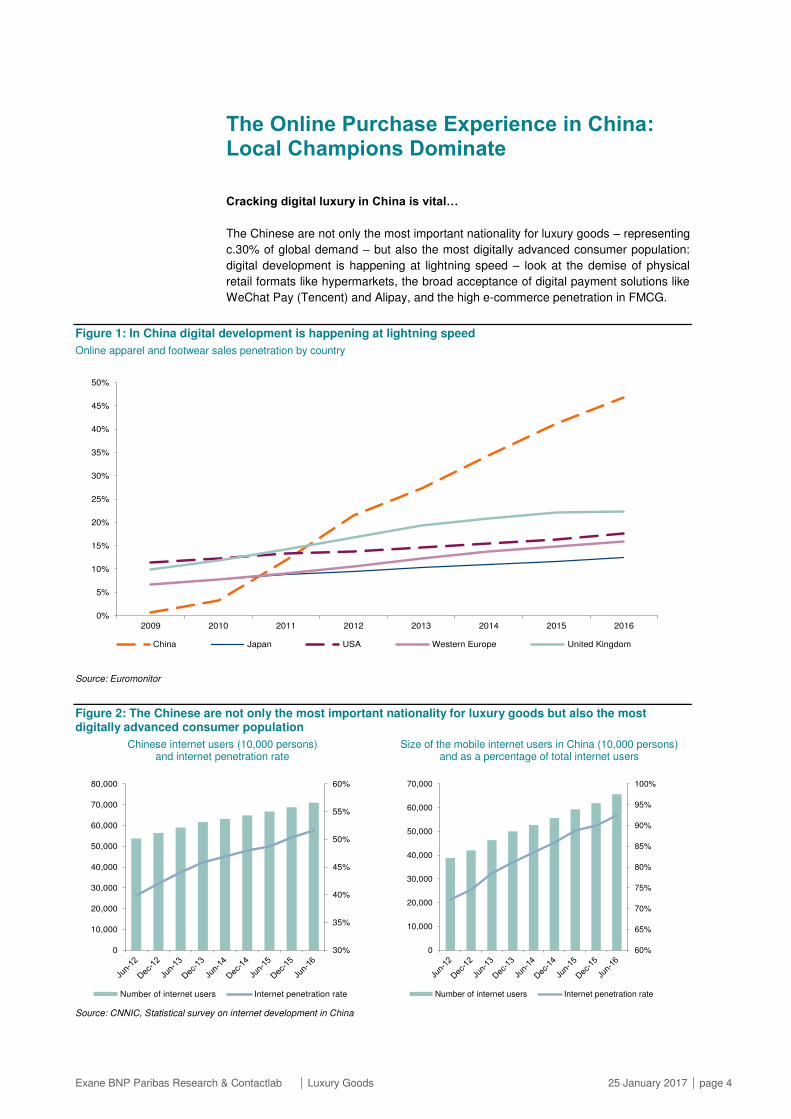

Cracking digital luxury in China is vital…

The Chinese are not only the most important nationality for luxury goods but also the most digitally

advanced consumer population: digital development is happening at lightning speed – look at the

demise of physical retail formats like hypermarkets, the broad acceptance of digital payment

solutions like WeChat Pay and Alipay, and the high e-commerce penetration in FMCG.

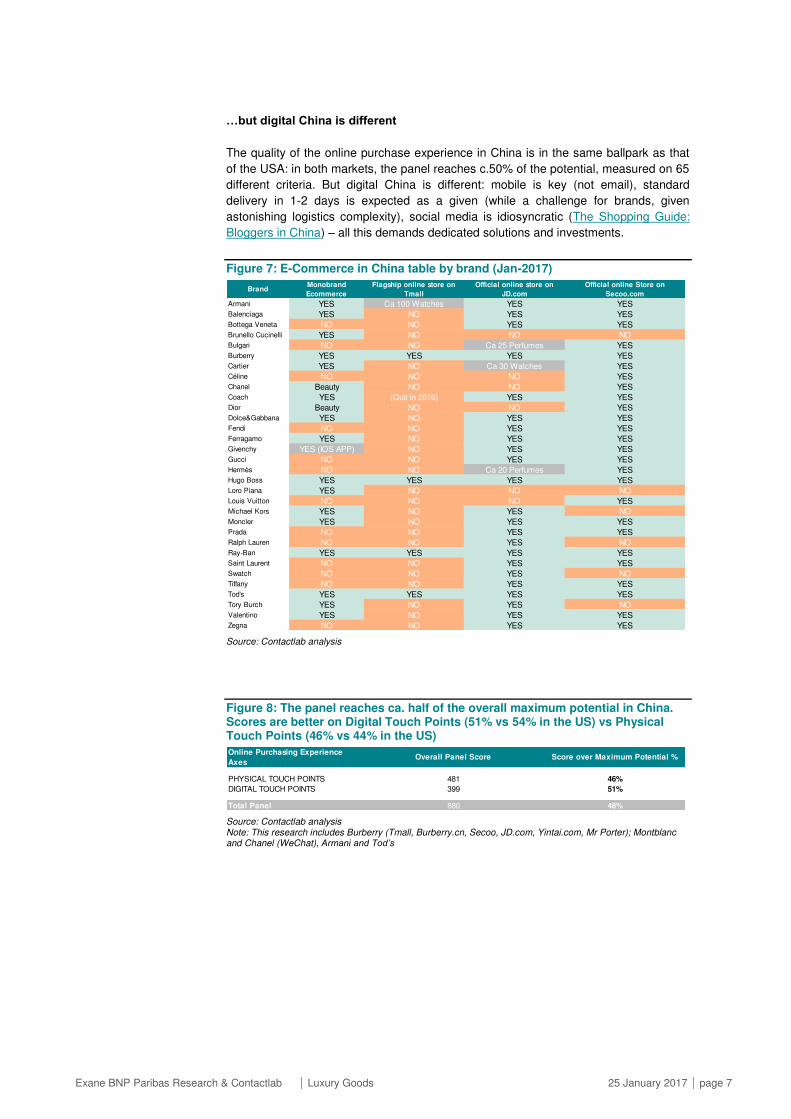

…but digital China is different The quality of the online purchase experience in China is in the same ballpark as that of the USA.

But digital China is different: mobile is key (not email), standard delivery in 1-2 days is expected as

a given, social media is idiosyncratic (The Shopping Guide: Bloggers in China) – all this demands

dedicated solutions and investments.

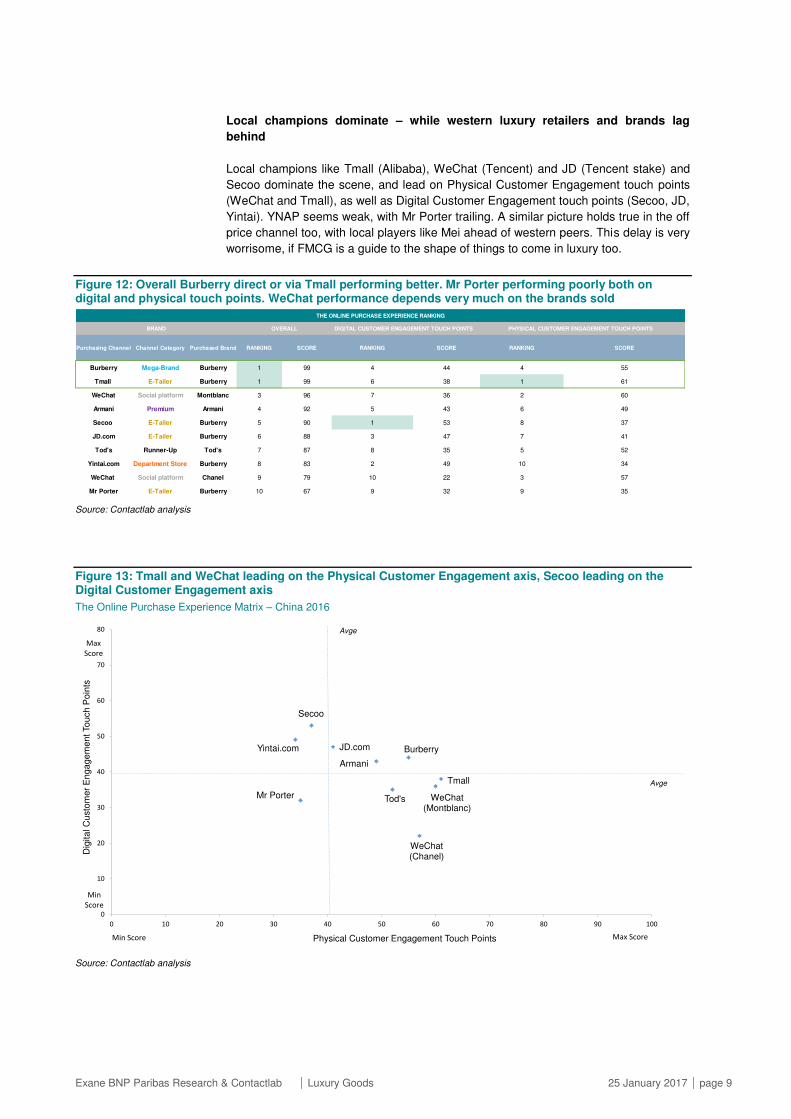

Local champions dominate – while western luxury retailers and brands lag behind

Local champions like Tmall (Alibaba), WeChat (Tencent) and JD (Tencent stake) and Secoo

dominate the scene, and lead on Physical Customer Engagement touch points (WeChat and

Tmall), as well as Digital Customer Engagement touch points (Secoo, JD, Yintai). YNAP seems

weak, with Mr Porter trailing. A similar picture holds true in the off price channel.

Local champions converting to authenticity would put pressure on the sector to shape up

The practice of local daigous mixing foreign sourced authentic products and fakes has prevented

digital luxury from taking off in earnest. Issues remain, as our field research has confirmed, and

Chinese consumers remain concerned (China Reality Check: Luxury and the Online Boom). A

more convincing transition to authenticity by local champions would confront luxury brands with

tough choices, making digital essential and unavoidable.

Luca Solca

(+44) 203 430 8503

Melania Grippo

(+39) 02 89 63 1724

Guido Lucarelli

(+39) 02 89 63 1726

Specialist sales

David Tovar

(+44) 203 430 8677

Contactlab

Marco Pozzi

(+39) 02 28 31 181 [email protected]

Francesca Borgonovo

(+39) 02 28 31 181 [email protected]

Xian Zhang

(+39) 02 28 31 181 [email protected]

Kuiling Song

(+39) 02 28 31 181 [email protected]

* Date and time (London Time) on which the investment recommendation was finalised. It may differ from the date and time of broad dissemination on the website.See Appendix (on p65) for Analyst Certification, Important Disclosures and Non-US Research Analyst disclosures.

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 2

Contents

Executive Summary _______________________________________ 3

The Online Purchase Experience in China: Local Champions Dominate _______________________________________________ 4

Detailed Results _________________________________________ 13

Digital Touch Points __________________________________________________ 13

Ordering ___________________________________________________________ 13

Purchasing Communications ___________________________________________ 31

Return Communications _______________________________________________ 34

Physical Touch Points ________________________________________________ 36

Delivery ___________________________________________________________ 36

External Packaging __________________________________________________ 39

Internal Packaging ___________________________________________________ 44

Documents inside Packaging ___________________________________________ 48

Return Procedures ___________________________________________________ 53

Methodology ___________________________________________ 56

Appendix ______________________________________________ 59

Websites __________________________________________________________ 59

About the collaboration with Contactlab ___________________________________ 64

Contactlab presentation _______________________________________________ 64

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 3

Executive Summary

We continue our analysis of how the luxury goods brands perform online. We shift our

focus to China, after having tested the Italian and US markets The Online Purchase

Experience Ranking, The Online Purchase Experience Ranking: From Milan to New

York City. In this research we have focused our attention on the purchase experience

for sales channels rather than brands. We have analysed the main Chinese e-tailers

operators and a few brands that own a proprietary e-commerce websites in China.

Cracking digital luxury in China is vital…

The Chinese are not only the most important nationality for luxury goods – representing

c.30% of global demand – but also the most digitally advanced consumer population:

digital development is happening at lightning speed – look at the demise of physical

retail formats like hypermarkets, the broad acceptance of digital payment solutions like

WeChat Pay and Alipay, and the high e-commerce penetration in FMCG.

…but digital China is different

The quality of the online purchase experience in China is in the same ballpark as that

of the USA: in both markets, the panel reaches c.50% of the potential, measured on 65

different criteria. But digital China is different: mobile is key (not email), standard

delivery in 1-2 days is expected as a given (while a challenge for brands, given

astonishing logistics complexity), social media is idiosyncratic (The Shopping Guide:

Bloggers in China) – all this demands dedicated solutions and investments.

Local champions dominate – while western luxury retailers and brands lag

behind

Local champions like Tmall (Alibaba), WeChat (Tencent) and JD (Tencent stake) and

Secoo dominate the scene, and lead on Physical Customer Engagement touch points

(WeChat and Tmall), as well as Digital Customer Engagement touch points (Secoo, JD,

Yintai). YNAP seems weak, with Mr Porter trailing. A similar picture holds true in the off

price channel too, with local players like Mei ahead of western peers. This delay is very

worrisome, if FMCG is a guide to the shape of things to come in luxury too.

Local champions converting to authenticity would put pressure on the sector to

shape up

The practice of local daigous mixing foreign-sourced authentic products and fakes has

prevented digital luxury from taking off in earnest. Issues remain, as our field research

has confirmed, and Chinese consumers remain concerned (China Reality Check:

Luxury and the Online Boom). A more convincing transition to authenticity by local

champions would confront luxury brands with tough choices, making digital essential

and unavoidable. While this seems far away today, things in China change quickly.

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 4

The Online Purchase Experience in China: Local Champions Dominate

Cracking digital luxury in China is vital…

The Chinese are not only the most important nationality for luxury goods – representing

c.30% of global demand – but also the most digitally advanced consumer population:

digital development is happening at lightning speed – look at the demise of physical

retail formats like hypermarkets, the broad acceptance of digital payment solutions like

WeChat Pay (Tencent) and Alipay, and the high e-commerce penetration in FMCG.

Figure 1: In China digital development is happening at lightning speed

Online apparel and footwear sales penetration by country

Source: Euromonitor

Figure 2: The Chinese are not only the most important nationality for luxury goods but also the most digitally advanced consumer population

Chinese internet users (10,000 persons) and internet penetration rate

Size of the mobile internet users in China (10,000 persons) and as a percentage of total internet users

Source: CNNIC, Statistical survey on internet development in China

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2009 2010 2011 2012 2013 2014 2015 2016

China Japan USA Western Europe United Kingdom

30%

35%

40%

45%

50%

55%

60%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Number of internet users Internet penetration rate

60%

65%

70%

75%

80%

85%

90%

95%

100%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Number of internet users Internet penetration rate

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 5

Figure 3: Age structure of Chinese internet users

Source: CNNIC, Statistical survey on internet development in China

Figure 4: Chinese digital growth is causing the demise of physical retail formats like hypermarkets (1/2)

Quotes from meetings in China

In offline FMCG, 25 out of 28 categories are declining. Only few of them recover online. EUR 2.3trn to be generated, over the next five years. This increase in consumption is driven mostly by the upper middle class; young people and services and low tier cities. Social media is key in purchasing. Hypermarkets are very negative. Brick & Mortar logistics are down, even more Hypermarkets are shutting down. Local retailers pay with 120 days delay (!). There is no liquidity. Ferrero derives c.15-20% of online sales in China; product personalization is key. The range on Digital is different from the range offered in the physical stores.

Source: Exane BNP Paribas proprietary field research in China

0%

5%

10%

15%

20%

25%

30%

35%

<10 10-19 20-29 30-39 40-49 50-59 >60

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 6

Figure 5: Chinese digital growth is causing the demise of physical retail formats like hypermarkets (2/2)

Urban FMCG market value (RMB bn)

2012-2015 CAGR 2012-2015 market share (RMB bn)

Source: Bain, Kantar Worldpanel Note: Notes: Hypermarket refers to stores with more than 6,000 square meters; the hypermarket channel includes only the top 72 named hypermarket retailers, representing 80% of total hypermarket channel (based on 2015 revenues); super/mini refers to stores from 100-6,000 square meters; CVS includes chain and individual convenience stores and is defined by being open for more than 16 hours a day; grocery refers to stores with less than 100 square meters; other includes department stores, free market, wholesales, work unit, directsales, specialty store, overseas shopping and others

Figure 6: There is a broad acceptance of digital payment solutions like WeChat Pay (Tencent) and Alipay (Alibaba)

China’s mobile-payment market

Source: iResearch, The Wall Street Journal 22/05/2016

(5%)

0%

5%

10%

15%

20%

25%

30%

35%

40%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015

Super/Mini Hypermarket Grocery CVS E-Commerce Other

1,068 1,146 1,209 1,251

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 7

…but digital China is different

The quality of the online purchase experience in China is in the same ballpark as that

of the USA: in both markets, the panel reaches c.50% of the potential, measured on 65

different criteria. But digital China is different: mobile is key (not email), standard

delivery in 1-2 days is expected as a given (while a challenge for brands, given

astonishing logistics complexity), social media is idiosyncratic (The Shopping Guide:

Bloggers in China) – all this demands dedicated solutions and investments.

Figure 7: E-Commerce in China table by brand (Jan-2017)

Source: Contactlab analysis

Figure 8: The panel reaches ca. half of the overall maximum potential in China. Scores are better on Digital Touch Points (51% vs 54% in the US) vs Physical Touch Points (46% vs 44% in the US)

Source: Contactlab analysis Note: This research includes Burberry (Tmall, Burberry.cn, Secoo, JD.com, Yintai.com, Mr Porter); Montblanc and Chanel (WeChat), Armani and Tod’s

BrandMonobrand

Ecommerce

Flagship online store on

Tmall

Official online store on

JD.com

Official online Store on

Secoo.com

Armani YES Ca 100 Watches YES YES

Balenciaga YES NO YES YES

Bottega Veneta NO NO YES YES

Brunello Cucinelli YES NO NO NO

Bulgari NO NO Ca 25 Perfumes YES

Burberry YES YES YES YES

Cartier YES NO Ca 30 Watches YES

Céline NO NO NO YESChanel Beauty NO NO YES

Coach YES (Quit in 2016) YES YES

Dior Beauty NO NO YES

Dolce&Gabbana YES NO YES YES

Fendi NO NO YES YES

Ferragamo YES NO YES YES

Givenchy YES (IOS APP) NO YES YES

Gucci NO NO YES YES

Hermès NO NO Ca 20 Perfumes YESHugo Boss YES YES YES YESLoro Piana YES NO NO NO

Louis Vuitton NO NO NO YES

Michael Kors YES NO YES NO

Moncler YES NO YES YES

Prada NO NO YES YES

Ralph Lauren NO NO YES NO

Ray-Ban YES YES YES YES

Saint Laurent NO NO YES YES

Swatch NO NO YES NOTiffany NO NO YES YES

Tod's YES YES YES YES

Tory Burch YES NO YES NO

Valentino YES NO YES YES

Zegna NO NO YES YES

PHYSICAL TOUCH POINTS 481 46%

DIGITAL TOUCH POINTS 399 51%

Total Panel 880 48%

Online Purchasing Experience

AxesOverall Panel Score Score over Maximum Potential %

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 8

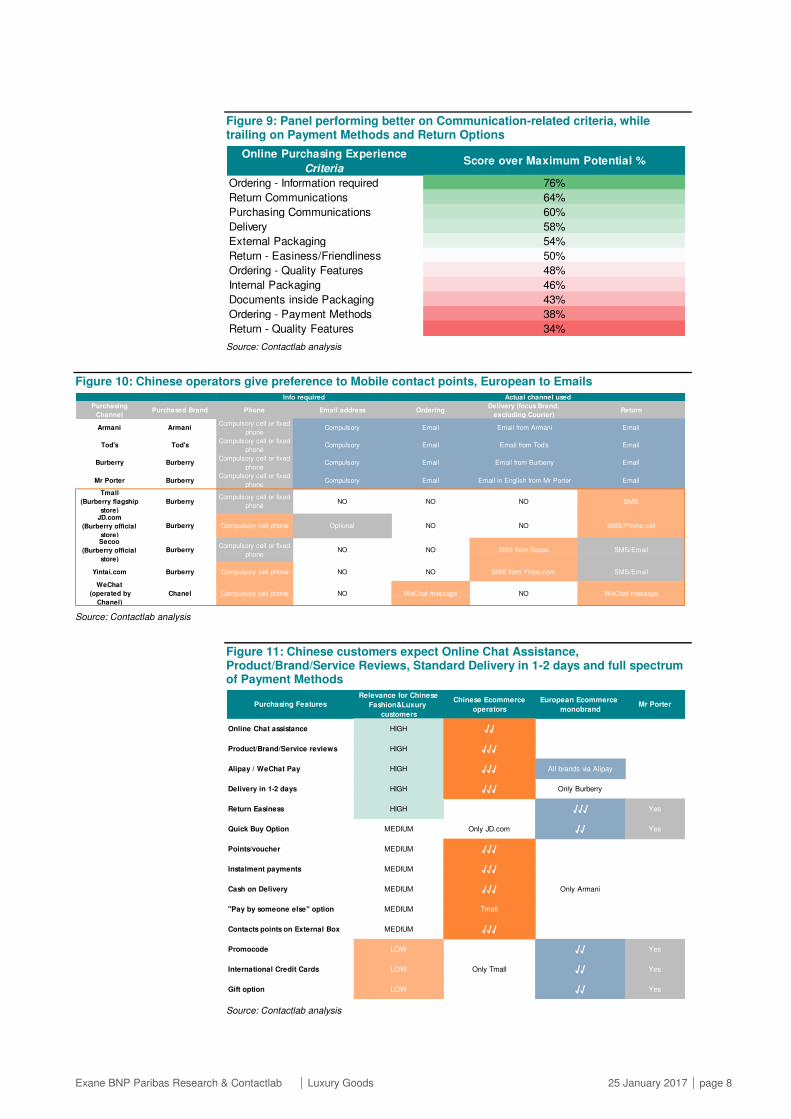

Figure 9: Panel performing better on Communication-related criteria, while trailing on Payment Methods and Return Options

Source: Contactlab analysis

Figure 10: Chinese operators give preference to Mobile contact points, European to Emails

Source: Contactlab analysis

Figure 11: Chinese customers expect Online Chat Assistance, Product/Brand/Service Reviews, Standard Delivery in 1-2 days and full spectrum of Payment Methods

Source: Contactlab analysis

Ordering - Information required 76%

Return Communications 64%

Purchasing Communications 60%

Delivery 58%

External Packaging 54%

Return - Easiness/Friendliness 50%

Ordering - Quality Features 48%

Internal Packaging 46%

Documents inside Packaging 43%

Ordering - Payment Methods 38%

Return - Quality Features 34%

Online Purchasing Experience

CriteriaScore over Maximum Potential %

Purchasing

ChannelPurchased Brand Phone Email address Ordering

Delivery (focus Brand,

excluding Courier)Return

Armani ArmaniCompulsory cell or fixed

phoneCompulsory Email Email from Armani Email

Tod's Tod'sCompulsory cell or fixed

phoneCompulsory Email Email from Tod's Email

Burberry BurberryCompulsory cell or fixed

phoneCompulsory Email Email from Burberry Email

Mr Porter BurberryCompulsory cell or fixed

phoneCompulsory Email Email in English from Mr Porter Email

Yintai.com Burberry Compulsory cell phone NO NO SMS from Yintai.com SMS/Email

Info required Actual channel used

Tmall

(Burberry flagship

store)

BurberryCompulsory cell or fixed

phoneNO NO NO SMS

SMS/Phone call

Secoo

(Burberry official

store)

BurberryCompulsory cell or fixed

phoneNO NO SMS from Secoo SMS/Email

JD.com

(Burberry official

store)

Burberry Compulsory cell phone Optional NO NO

WeChat message

(operated by

Chanel)

Chanel Compulsory cell phone NO WeChat message NO

Online Chat assistance HIGH √√Product/Brand/Service reviews HIGH √√√Alipay / WeChat Pay HIGH √√√ All brands via Alipay

Delivery in 1-2 days HIGH √√√ Only Burberry

Return Easiness HIGH √√√ Yes

Quick Buy Option MEDIUM Only JD.com √√ Yes

Points/voucher MEDIUM √√√Instalment payments MEDIUM √√√Cash on Delivery MEDIUM √√√ Only Armani

"Pay by someone else" option MEDIUM Tmall

Contacts points on External Box MEDIUM √√√Promocode LOW √√ Yes

International Credit Cards LOW Only Tmall √√ Yes

Gift option LOW √√ Yes

Purchasing Features

Relevance for Chinese

Fashion&Luxury

customers

Chinese Ecommerce

operators

European Ecommerce

monobrand Mr Porter

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 9

Local champions dominate – while western luxury retailers and brands lag

behind

Local champions like Tmall (Alibaba), WeChat (Tencent) and JD (Tencent stake) and

Secoo dominate the scene, and lead on Physical Customer Engagement touch points

(WeChat and Tmall), as well as Digital Customer Engagement touch points (Secoo, JD,

Yintai). YNAP seems weak, with Mr Porter trailing. A similar picture holds true in the off

price channel too, with local players like Mei ahead of western peers. This delay is very

worrisome, if FMCG is a guide to the shape of things to come in luxury too.

Figure 12: Overall Burberry direct or via Tmall performing better. Mr Porter performing poorly both on digital and physical touch points. WeChat performance depends very much on the brands sold

Source: Contactlab analysis

Figure 13: Tmall and WeChat leading on the Physical Customer Engagement axis, Secoo leading on the Digital Customer Engagement axis

The Online Purchase Experience Matrix – China 2016

Source: Contactlab analysis

Burberry Mega-Brand Burberry 1 99 4 44 4 55

Tmall E-Tailer Burberry 1 99 6 38 1 61

WeChat Social platform Montblanc 3 96 7 36 2 60

Armani Premium Armani 4 92 5 43 6 49

Secoo E-Tailer Burberry 5 90 1 53 8 37

JD.com E-Tailer Burberry 6 88 3 47 7 41

Tod's Runner-Up Tod's 7 87 8 35 5 52

Yintai.com Department Store Burberry 8 83 2 49 10 34

WeChat Social platform Chanel 9 79 10 22 3 57

Mr Porter E-Tailer Burberry 10 67 9 32 9 35

RANKING SCORE RANKING SCORE

THE ONLINE PURCHASE EXPERIENCE RANKING

BRAND OVERALL DIGITAL CUSTOMER ENGAGEMENT TOUCH POINTS PHYSICAL CUSTOMER ENGAGEMENT TOUCH POINTS

Purchasing Channel Channel Category Purchased Brand RANKING SCORE

Armani

Tod'sMr Porter

Tmall

JD.com

Secoo

Yintai.com

WeChat (Montblanc)

WeChat(Chanel)

0 10 20 30 40 50 60 70 80 90 100

0

10

20

30

40

50

60

70

80

Physical Customer Engagement Touch Points

Dig

ita

l C

usto

me

r E

nga

ge

me

nt To

uch

Po

ints

Min Score Max Score

Min

Score

Max

Score

Burberry

Avge

Avge

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 10

Figure 14: Overall, Chinese operators are performing better on the digital side while lagging behind on the physical side. Digital ecommerce experience is still basic on WeChat

Source: Contactlab analysis

Chinese Ecommerce

channels1 90 1 47 3 43

WeChat 2 88 3 29 1 59

European Ecommerce

channels3 86 2 39 2 48

AVERAGE SCORE

THE ONLINE PURCHASE EXPERIENCE RANKING

OVERALLDIGITAL CUSTOMER ENGAGEMENT

TOUCH POINTS

PHYSICAL CUSTOMER ENGAGEMENT

TOUCH POINTS

RANKING AVERAGE SCORE RANKING AVERAGE SCORE RANKING

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 11

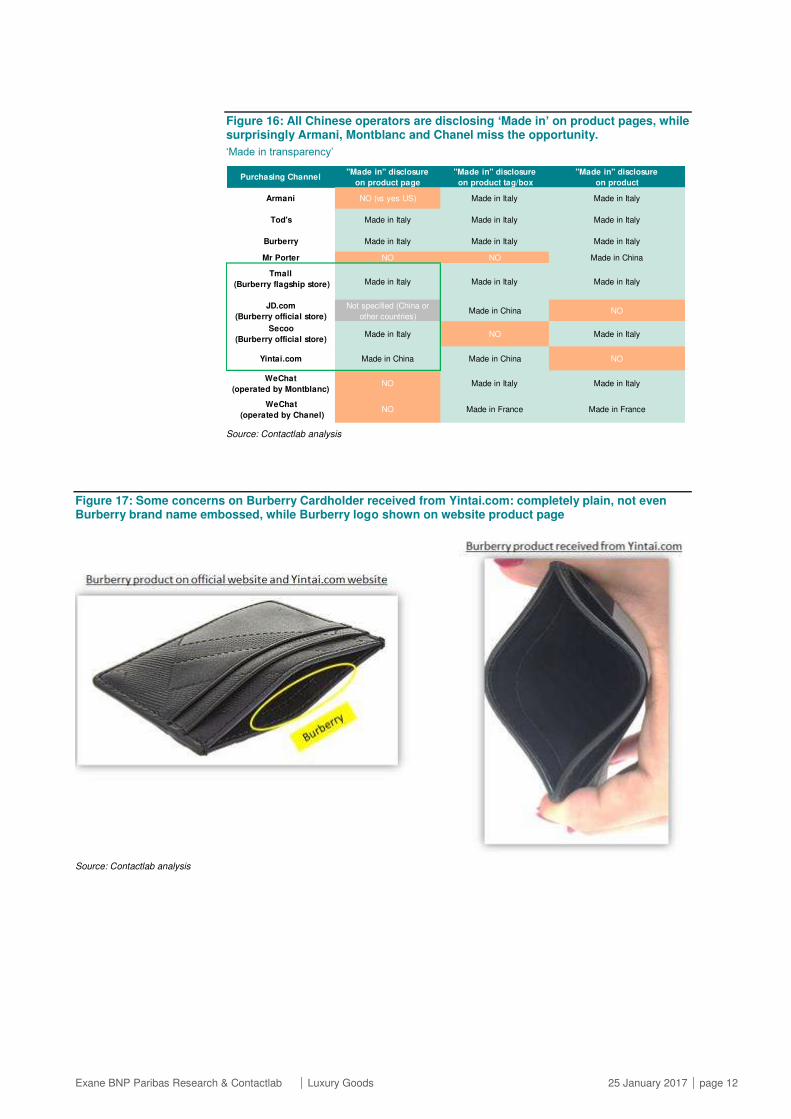

Local champions converting to authenticity would put pressure on the sector to

shape up

The practice of local daigous mixing foreign-sourced authentic products and fakes has

prevented digital luxury from taking off in earnest. Issues remain, as our field research

has confirmed, and Chinese consumers remain concerned (China Reality Check:

Luxury and the Online Boom). A more convincing transition to authenticity by local

champions would confront luxury brands with tough choices, making digital essential

and unavoidable. While this seems far away today, things in China change quickly.

Figure 15: All Chinese operators pay significant attention to authenticity on product pages and include brand product tags

Authenticity assurance

Source: Contactlab analysis

Purchasing ChannelGuarantee of Authenticity on

product pageBrand product tag Security tag for return

Armani Official brand website YES YES

Tod's Official brand website YES NO

Burberry Official brand website YES YES

Mr Porter NO NO NO

JD.com

(Burberry official store)Remark on product page

YES

(Burberry and JD.com)NO

Secoo

(Burberry official store)Icon on product page

YES

(Burberry and Secoo)NO

Yintai.com Remark on product page YES NO

(operated by Chanel)Official brand website YES

YES

(Plastic wrap should not be

opened)

(operated by Montblanc)Official brand website YES NO

Tmall

(Burberry flagship store)

Official brand website plus

authenticity remark on product pageYES YES

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 12

Figure 16: All Chinese operators are disclosing ‘Made in’ on product pages, while surprisingly Armani, Montblanc and Chanel miss the opportunity.

‘Made in transparency’

Source: Contactlab analysis

Figure 17: Some concerns on Burberry Cardholder received from Yintai.com: completely plain, not even Burberry brand name embossed, while Burberry logo shown on website product page

Source: Contactlab analysis

"Made in" disclosure "Made in" disclosure "Made in" disclosure

on product page on product tag/box on product

Armani NO (vs yes US) Made in Italy Made in Italy

Tod's Made in Italy Made in Italy Made in Italy

Burberry Made in Italy Made in Italy Made in Italy

Mr Porter NO NO Made in China

JD.com

(Burberry official store)

Not specified (China or

other countries)Made in China NO

Yintai.com Made in China Made in China NO

Purchasing Channel

Tmall

(Burberry flagship store) Made in Italy Made in Italy Made in Italy

(operated by Chanel)NO Made in France Made in France

Secoo

(Burberry official store)Made in Italy NO Made in Italy

(operated by Montblanc)NO Made in Italy Made in Italy

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 13

Detailed Results

Digital Touch Points

Figure 18: Overall, Chinese operators leading on digital touch points, with Secoo first followed by Yintai.com and JD.com

Digital touch points – Ranking China 2016

Source: Contactlab analysis

Ordering

Figure 19: Significantly different approaches between Chinese operators, asking compulsory cell phone, and Europeans, asking compulsory Email address

Ordering – Information required

Source: Contactlab analysis

Information

RequiredQuality Features

Payment

Methods

Secoo E-Tailer Burberry 53 1 8 2 1 6 6

Yintai.comDepartment

StoreBurberry 49 2 6 1 5 6 1

JD.com E-Tailer Burberry 47 3 1 4 4 9 1

Burberry Mega-Brand Burberry 44 4 1 5 6 1 5

Armani Premium Armani 43 5 1 7 3 2 1

Tmall E-Tailer Burberry 38 6 8 2 6 9 7

WeChatSocial

platformMontblanc 36 7 6 9 2 2 7

Tod's Runner-Up Tod's 35 8 1 6 8 2 7

Mr Porter E-Tailer Burberry 32 9 1 7 10 2 1

WeChat Social

platformChanel 22 10 10 9 9 6 7

DIGITAL TOUCH POINTS – RANKINGS CHINA 2016

Purchasing

Channel

Channel

Category

Purchased

BrandSCORE

OVERALL

RANKING

ORDERINGPURCHASING

COMMUNICATIONS

RETURN

COMMUNICATION

S

Purchasing Channel Purchased Brand Ranking

Physical address

automatically

retrieved from

account

Phone Email address

Armani Armani 1 YES Compulsory cell or fixed phone Compulsory

Tod's Tod's 1 YES Compulsory cell or fixed phone Compulsory

Burberry Burberry 1 YES Compulsory cell or fixed phone Compulsory

Mr Porter Burberry 1 YES Compulsory cell or fixed phone Compulsory

JD.com Burberry 1 YES Compulsory cell phone Optional

Yintai.com Burberry 6 YES Compulsory cell phone NO

WeChat Montblanc 6 NO Compulsory cell phone Compulsory

Tmall Burberry 8 YES Compulsory cell or fixed phone NO

Secoo Burberry 8 YES Compulsory cell or fixed phone NO

WeChat Chanel 10 NO Compulsory cell phone NO

YES Compulsory cell phone Compulsory

Compulsory cell or fixed phone Optional

NO Not required Not required

ORDERING - INFORMATION REQUIRED

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 14

Figure 20: Chinese operators giving high relevance to Support via Chat, Customers Reviews and Guarantee of Product Authenticity on Product Pages

Ordering – Quality Features

Source: Contactlab analysis

Figure 21: Example of Yintai.com offering receipt preview with and without price

Gift option

Source: Contactlab analysis

Yintai.com Burberry 1 Free (no price tag) Remark on product page Made in China Products NO NOVisual aid for product

dimensionsYintai Voucher

YES (Personal or

Company)5

Official brand website plus

authenticity remark on

product page

Secoo Burberry 2 NO Icon on product page Made in Italy Products / Brands NO YES, web / app Secoo VoucherYES (Personal or

Company)4

JD.com Burberry 4 NO Remark on product pageNot specified (China or

other countries)Products NO YES, web /app JD points

YES (Personal or

Company or VAT)4

Burberry Burberry 5

Free (no price tag,

gift packaging, gift

message card)

Official brand website Made in Italy NO Only for gift NO NOYES (Personal or

Company)5

Tod's Tod's 6 NO (vs Yes US) Official brand website Made in Italy NO NO NO Promocode YES 5 (vs 3 US)

Armani Armani 7Free (no price tag,

gift message card)Official brand website NO (vs yes US) NO NO NO Promocode NO 7 (vs 4 US)

Mr Porter Burberry 7

Free (gift

packaging, gift

message card)

NO NO NO YES NO Promocode NO 5

WeChat Montblanc 9 NO Official brand website NO NO NO NO NOYES (Personal or

Company or VAT)

4 WeChat payment / Alipay, 9 other

banks

WeChat Chanel 9 NO Official brand website NO NO NO NO NOYES (Personal or

Company)6

YES - FreeYES, icon/remark on

product pageYES

YES, products,

services and brandsYES YES YES YES Yes 3 or less pages

YES - Extra cost YES, products Only for gift 4-5 pages

NO NO NO NO NO NO NO NO NO 6 or more pages

Tmall Burberry 2 NO

ORDERING - QUALITY FEATURES

Purchasing

Channel

Purchased

BrandRanking Gift Option

Guarantee of Authenticity

on product page

"Made in" disclosure

on product pageCustomer reviews

Packaging

info

Support via chat

during purchasing

Made in Italy 3

Extra touch in

purchasing process

Special price

optionReceipt Option

Number of webpages from product

page to purchase confirmation

NO YES, web /app Tmall points NOProducts / Services

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 15

Figure 22: Example of Mr. Porter offering gift message and personalized label option

Gift option

Source: Contactlab analysis

Figure 23: Guarantee of authenticity on product page

Example Tmall

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 16

Figure 24: Guarantee of authenticity on product page

Example JD.com

Source: Contactlab analysis

Figure 25: Guarantee of authenticity on product page

Example Secoo

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 17

Figure 26: Guarantee of authenticity on product page

Example Yintai.com

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 18

Figure 27: ‘Made in’ disclosure

Example Tmall declaring ‘Made in’ origin on product page

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 19

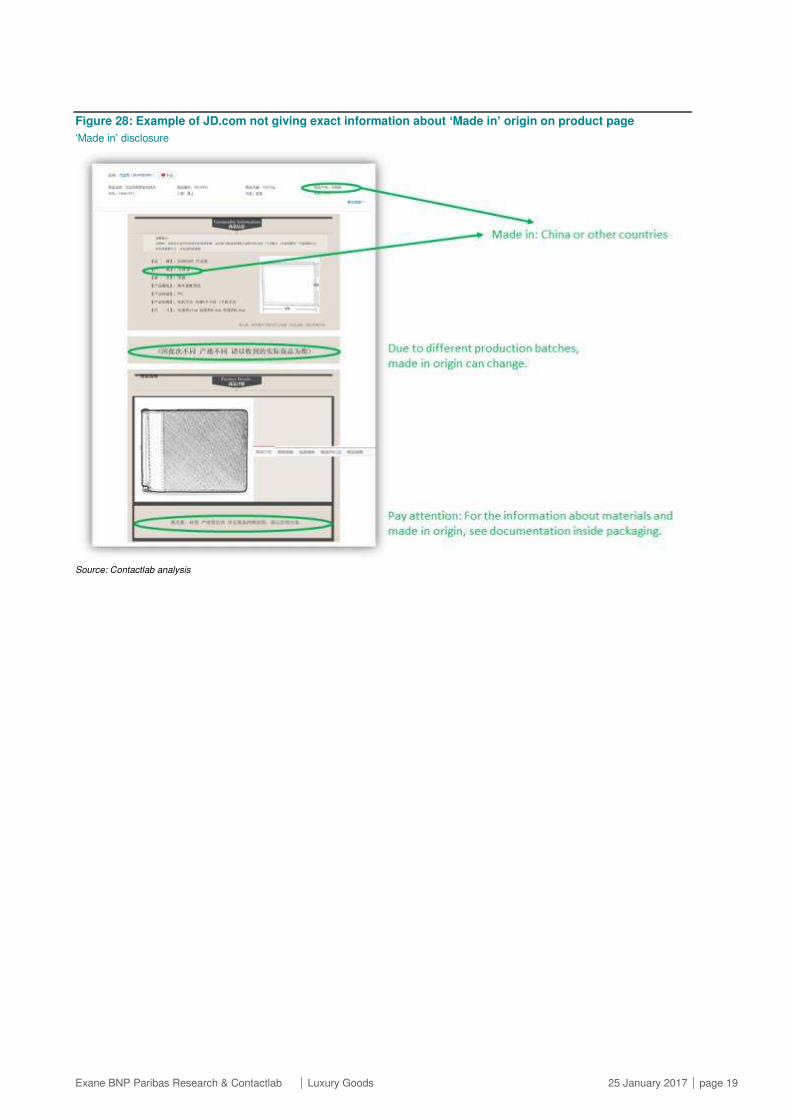

Figure 28: Example of JD.com not giving exact information about ‘Made in’ origin on product page

‘Made in’ disclosure

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 20

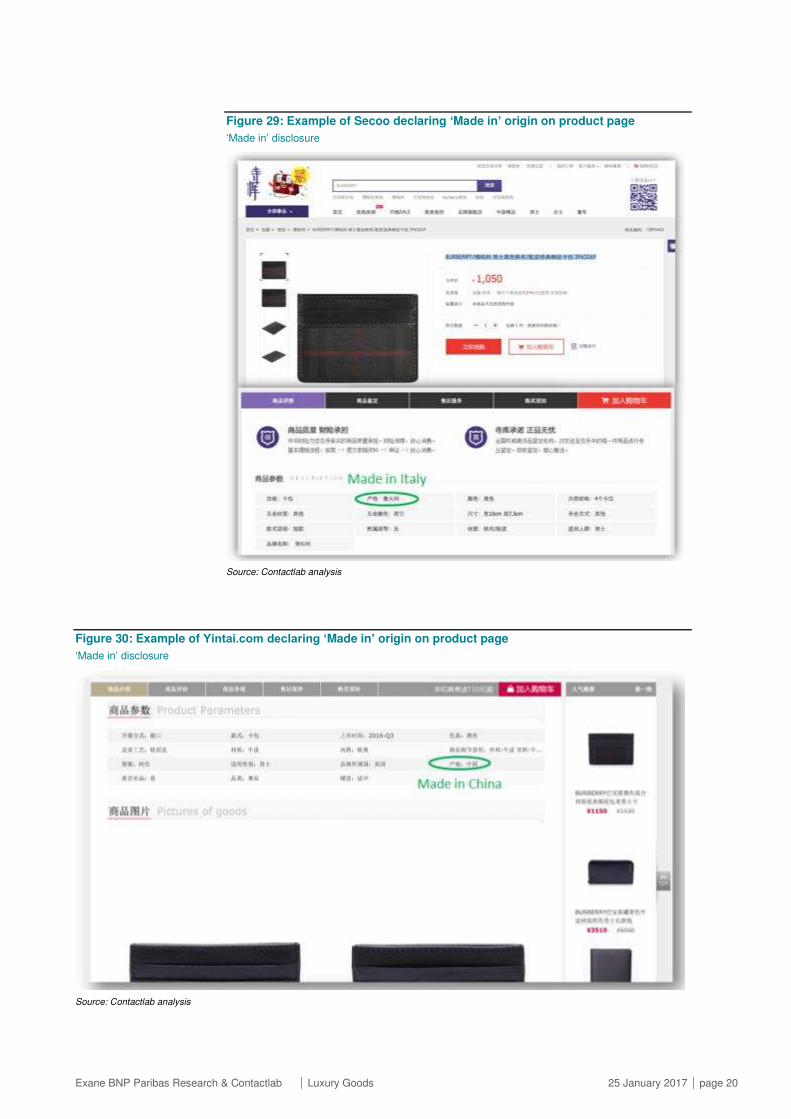

Figure 29: Example of Secoo declaring ‘Made in’ origin on product page

‘Made in’ disclosure

Source: Contactlab analysis

Figure 30: Example of Yintai.com declaring ‘Made in’ origin on product page

‘Made in’ disclosure

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 21

Figure 31: Example of Tmall offering both product and service reviews

Customer reviews

Source: Contactlab analysis

Figure 32: Example of Tmall product reviews on product page with brand reply

Customer reviews

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 22

Figure 33: Example of JD.com including product reviews on product page

Customer reviews

Source: Contactlab analysis

Figure 34: Example of Secoo includes reviews both on products and brands

Customer reviews

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 23

Figure 35: The example of Mr Porter

Packaging info

Source: Contactlab analysis

Figure 36: Example of Aliwangwang Messenger on Tmall

Support via chat during purchasing process

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 24

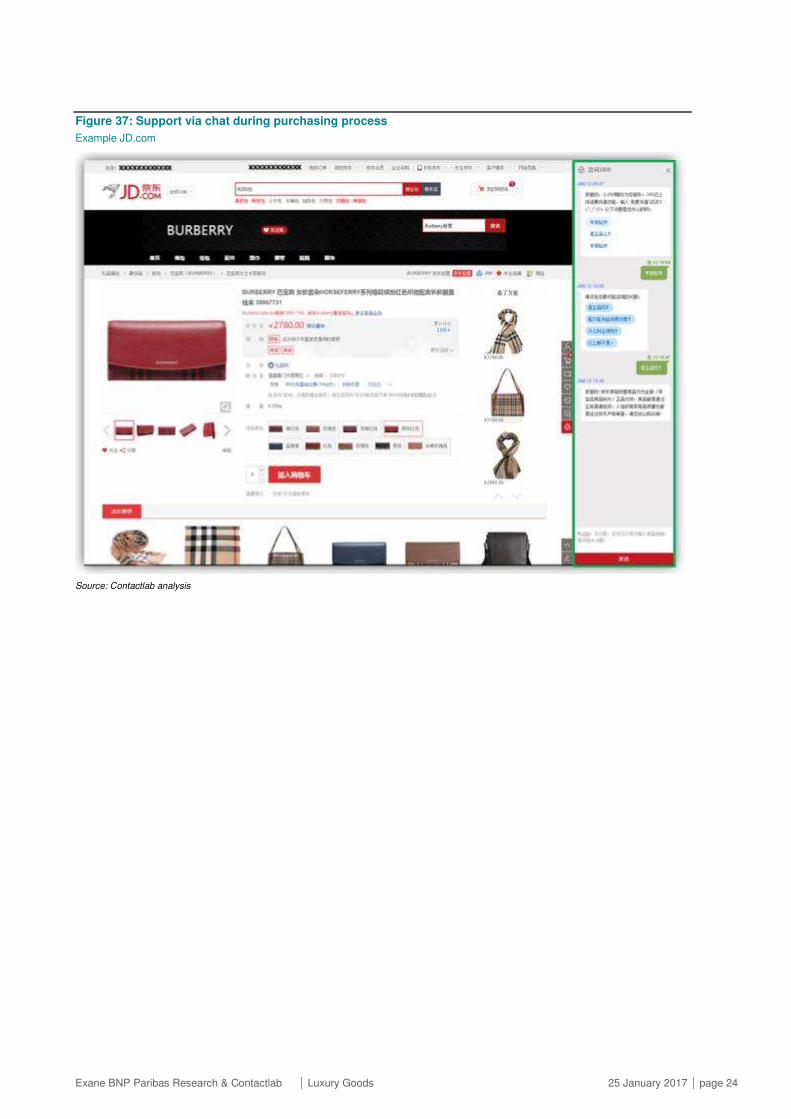

Figure 37: Support via chat during purchasing process

Example JD.com

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 25

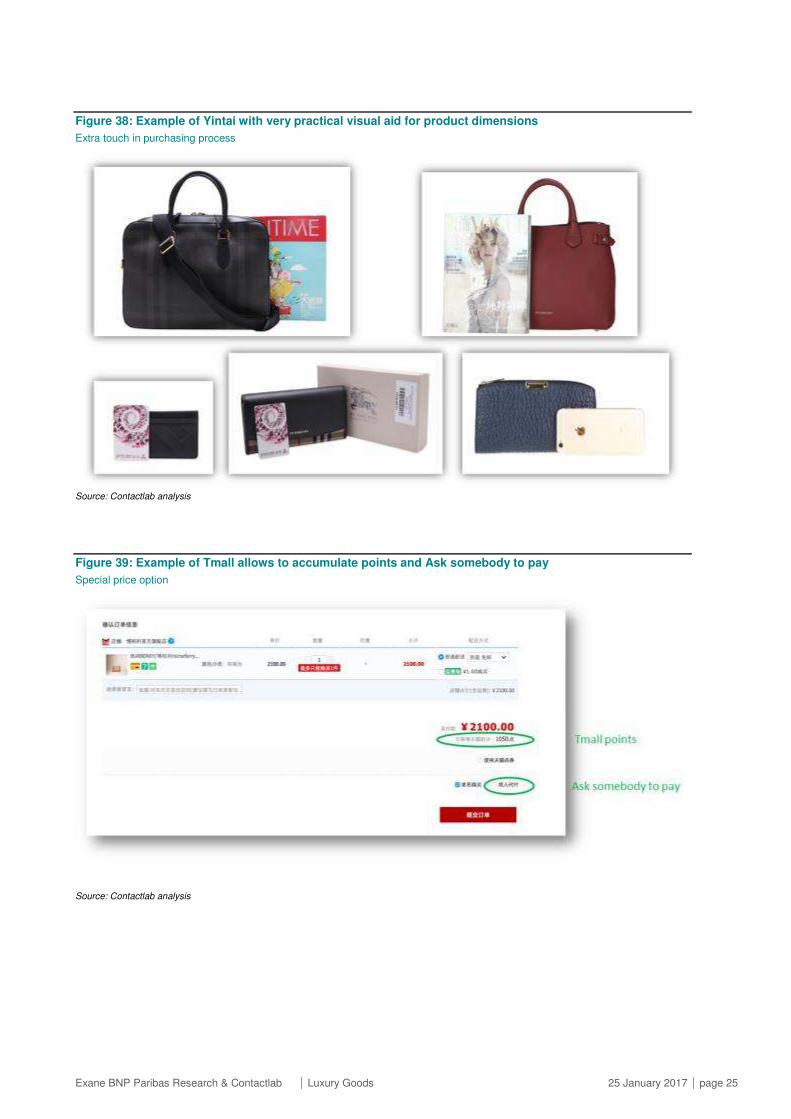

Figure 38: Example of Yintai with very practical visual aid for product dimensions

Extra touch in purchasing process

Source: Contactlab analysis

Figure 39: Example of Tmall allows to accumulate points and Ask somebody to pay

Special price option

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 26

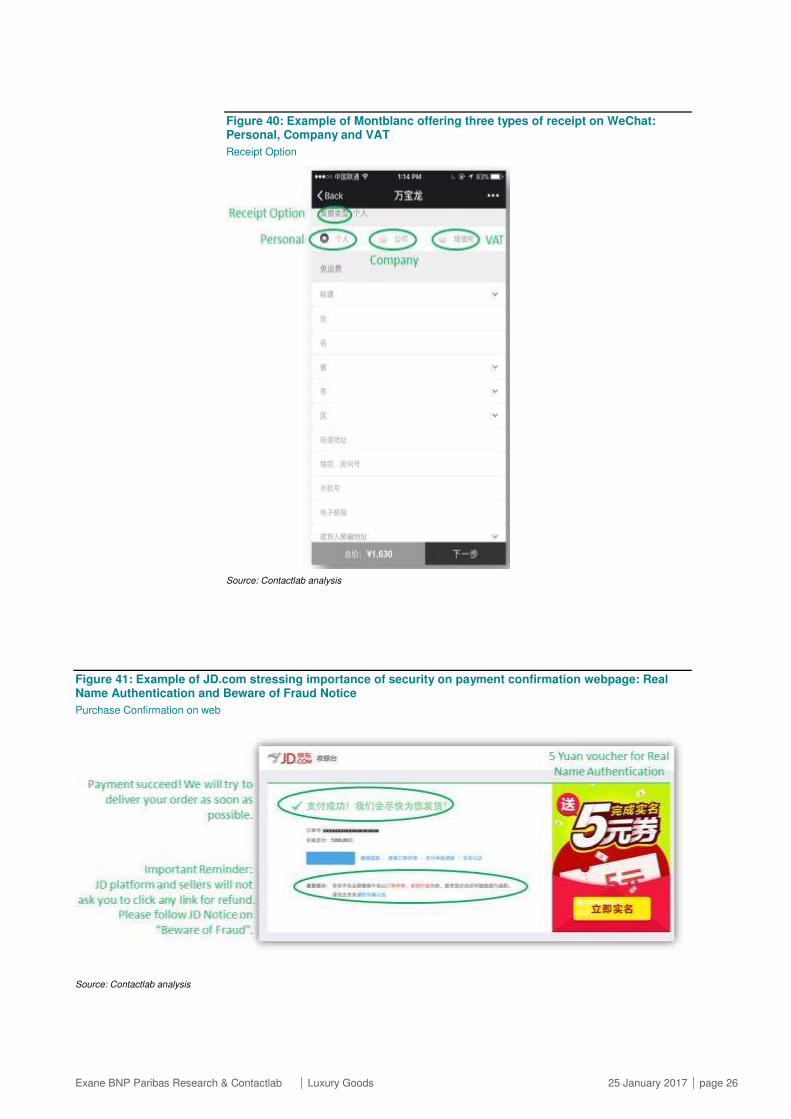

Figure 40: Example of Montblanc offering three types of receipt on WeChat: Personal, Company and VAT

Receipt Option

Source: Contactlab analysis

Figure 41: Example of JD.com stressing importance of security on payment confirmation webpage: Real Name Authentication and Beware of Fraud Notice

Purchase Confirmation on web

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 27

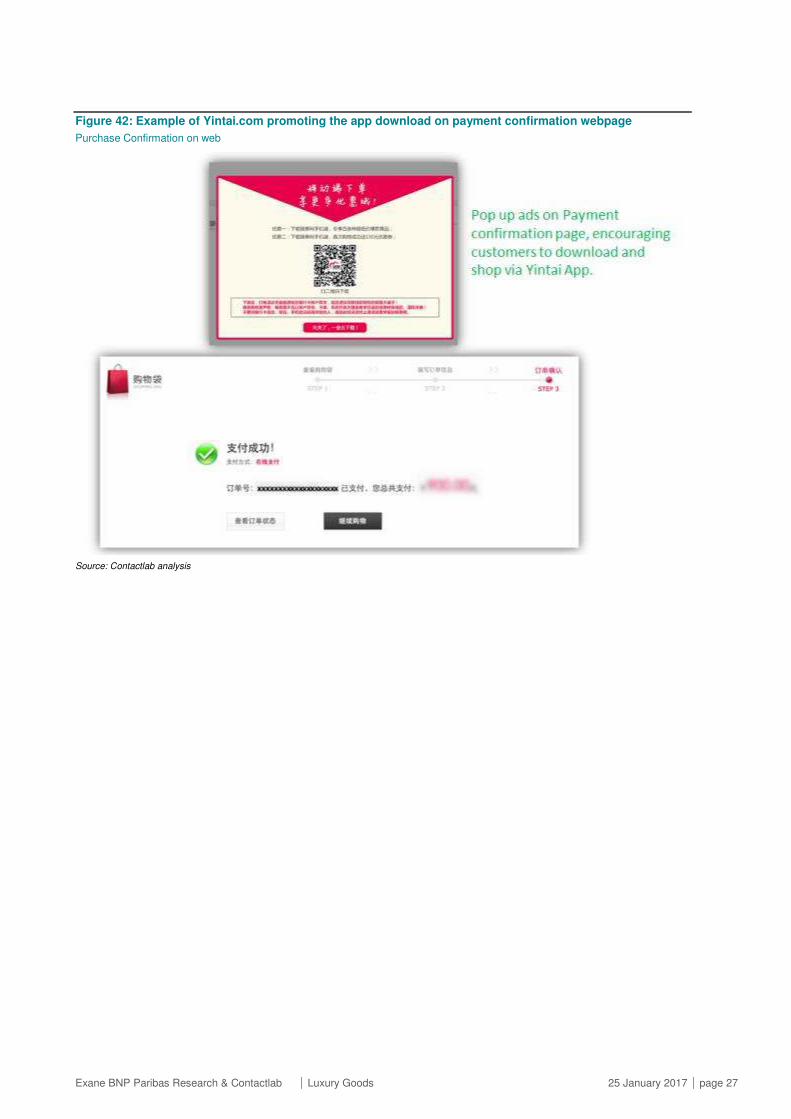

Figure 42: Example of Yintai.com promoting the app download on payment confirmation webpage

Purchase Confirmation on web

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 28

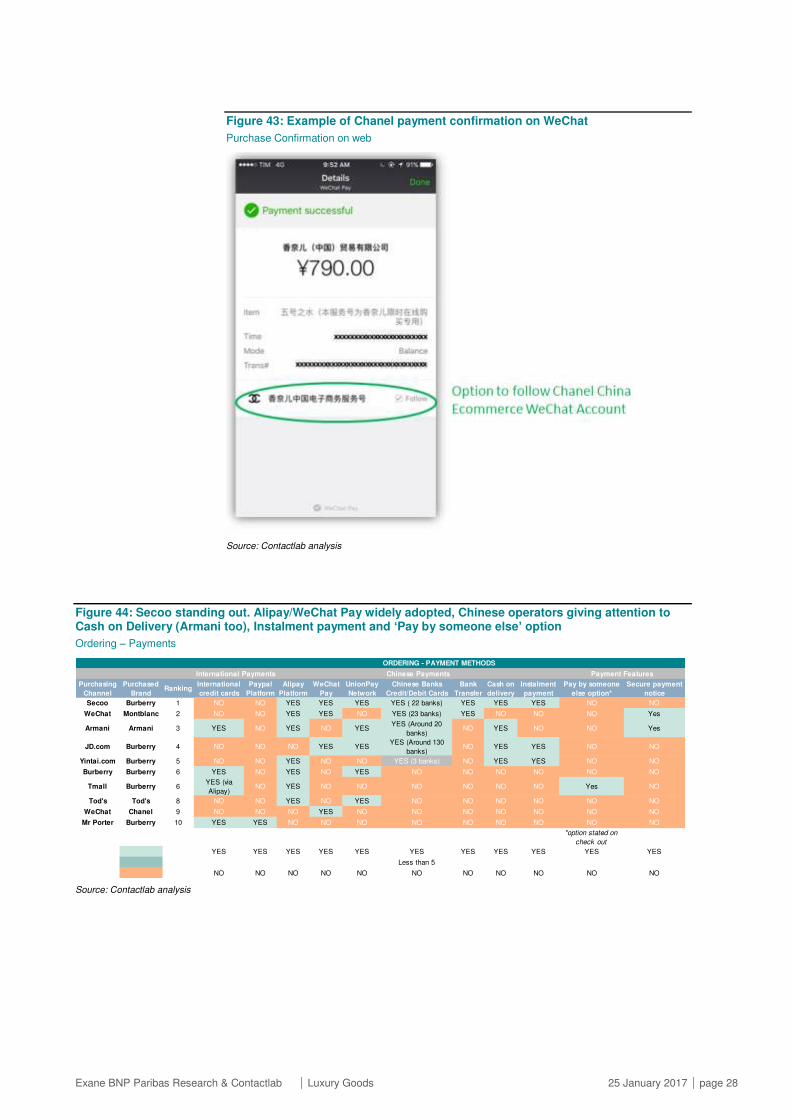

Figure 43: Example of Chanel payment confirmation on WeChat

Purchase Confirmation on web

Source: Contactlab analysis

Figure 44: Secoo standing out. Alipay/WeChat Pay widely adopted, Chinese operators giving attention to Cash on Delivery (Armani too), Instalment payment and ‘Pay by someone else’ option

Ordering – Payments

Source: Contactlab analysis

Purchasing

Channel

Purchased

BrandRanking

International

credit cards

Paypal

Platform

Alipay

Platform

Pay

UnionPay

Network

Chinese Banks

Credit/Debit Cards

Bank

Transfer

Cash on

delivery

Instalment

payment

Pay by someone

else option*

Secure payment

notice

Secoo Burberry 1 NO NO YES YES YES YES ( 22 banks) YES YES YES NO NO

WeChat Montblanc 2 NO NO YES YES NO YES (23 banks) YES NO NO NO Yes

Armani Armani 3 YES NO YES NO YESYES (Around 20

banks)NO YES NO NO Yes

JD.com Burberry 4 NO NO NO YES YESYES (Around 130

banks)NO YES YES NO NO

Yintai.com Burberry 5 NO NO YES NO NO YES (3 banks) NO YES YES NO NO

Burberry Burberry 6 YES NO YES NO YES NO NO NO NO NO NO

Tmall Burberry 6YES (via

Alipay)NO YES NO NO NO NO NO NO Yes NO

Tod's Tod's 8 NO NO YES NO YES NO NO NO NO NO NO

WeChat Chanel 9 NO NO NO YES NO NO NO NO NO NO NO

Mr Porter Burberry 10 YES YES NO NO NO NO NO NO NO NO NO

*option stated on

check out

YES YES YES YES YES YES YES YES YES YES YES

Less than 5

NO NO NO NO NO NO NO NO NO NO NO

ORDERING - PAYMENT METHODS

International Payments Chinese Payments Payment Features

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 29

Figure 45: Example of Secoo offering a variety of local payment options: Alipay, WeChat payment and Instalment payment

Chinese Payments

Source: Contactlab analysis

Figure 46: Example of Tmall offering a variety of payments via Alipay platform: local credit cards, local debit cards and International bank cards

Chinese Payments

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 30

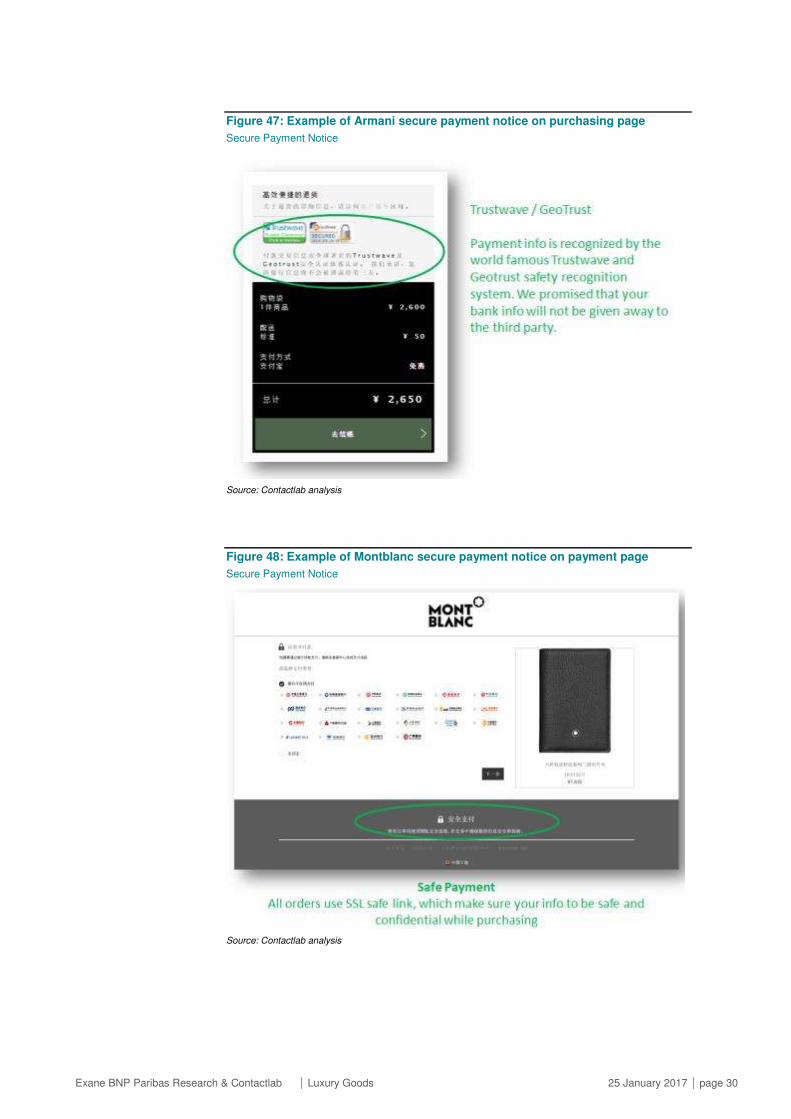

Figure 47: Example of Armani secure payment notice on purchasing page

Secure Payment Notice

Source: Contactlab analysis

Figure 48: Example of Montblanc secure payment notice on payment page

Secure Payment Notice

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 31

Purchasing Communications

Figure 49: Burberry has the most complete set of communications all via email. Chinese operators communicating less and only via SMS/Messages

Purchase communications

Source: Contactlab analysis

Purchasing

Channel

Purchased

BrandRanking

Order confirmation (Email,

SMS...)

Payment confirmation from

brand, not bank

Shipping

confirmationDelivery confirmation

YES YES

(Email, combined with

payment confirmation)

(Email, combined with order

confirmation)

Armani Armani 2 YES (Email) NO YES (Email) Phone call courier before delivery

Tod's Tod's 2 YES (Email) NO YES (Email) Phone call courier before delivery

YES

(SMS /Email/phone call by DHL

before delivery)

WeChat Montblanc 2 YES (Email) NO YES (Email) Phone call courier before delivery

Secoo Burberry 6 NO NO YES (SMS) Phone call courier before delivery

Yintai.com Burberry 6 NO NO YES (SMS)

YES

(SMS for delivery confirmation by

EMS courier)

WeChat Chanel 6 YES (WeChat message) YES (WeChat message) NO NO

Tmall Burberry 9 NO NO NO Phone call courier before delivery

JD.com Burberry 9 NO NO NO Phone call courier before delivery

YES YES YES YES

NO NO NO NO

YES (Email in

English)

PURCHASING PROCESS - COMMUNICATIONS

Burberry Burberry 1 YES (Email) Phone call courier before delivery

Mr Porter Burberry 2 YES (Email in English) NO

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 32

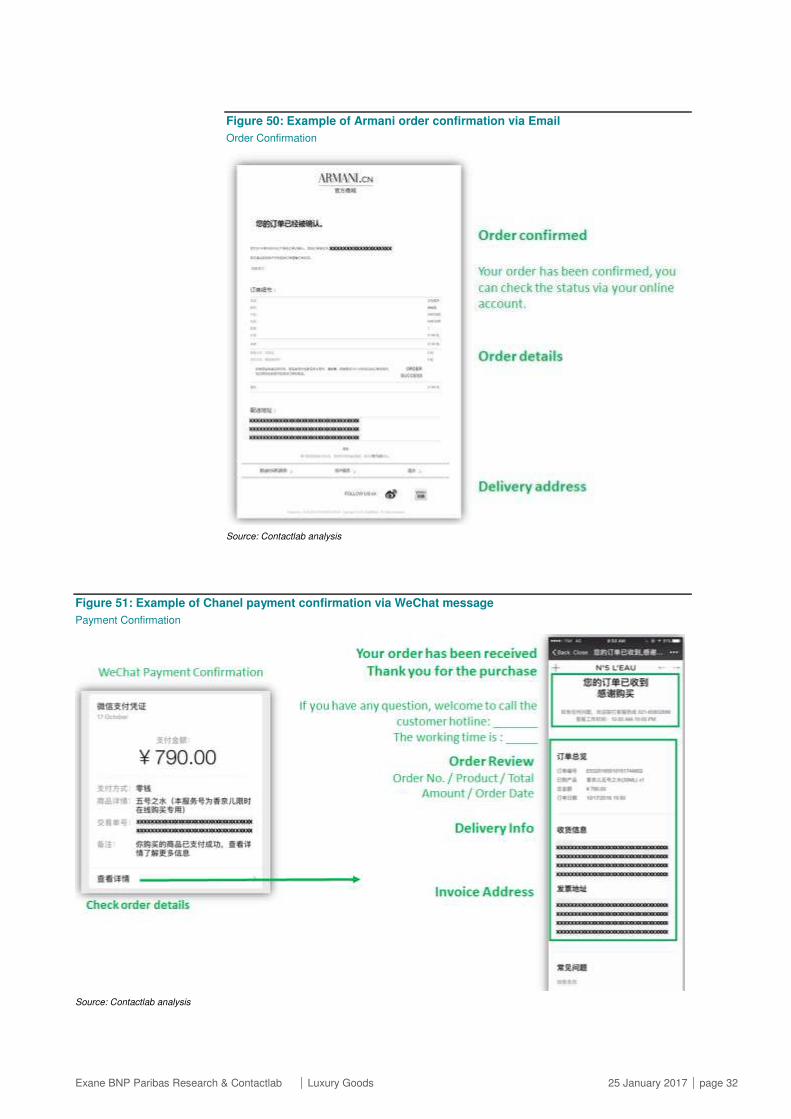

Figure 50: Example of Armani order confirmation via Email

Order Confirmation

Source: Contactlab analysis

Figure 51: Example of Chanel payment confirmation via WeChat message

Payment Confirmation

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 33

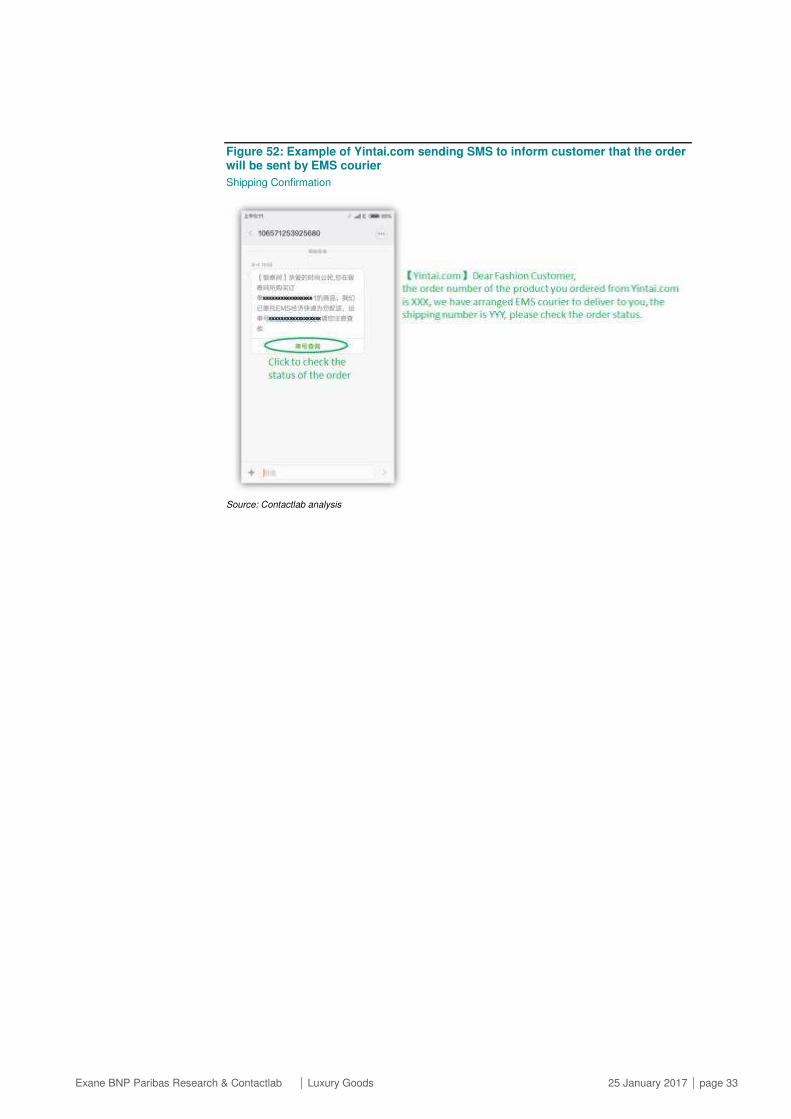

Figure 52: Example of Yintai.com sending SMS to inform customer that the order will be sent by EMS courier

Shipping Confirmation

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 34

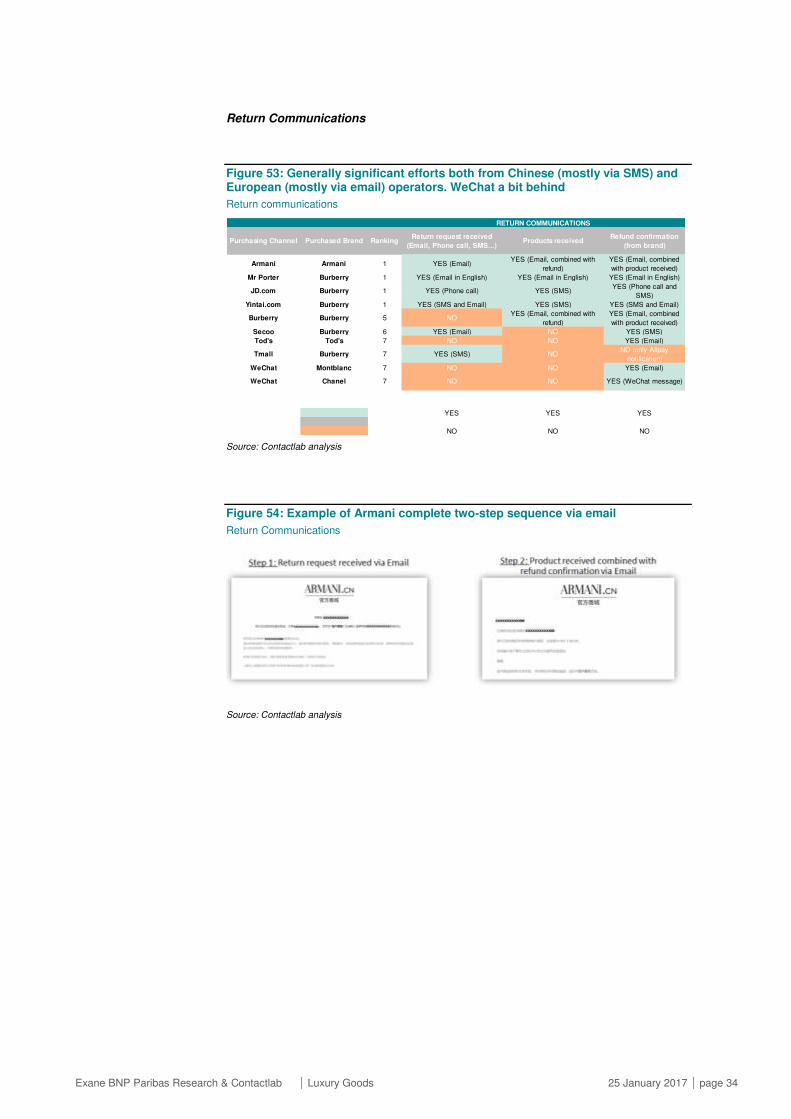

Return Communications

Figure 53: Generally significant efforts both from Chinese (mostly via SMS) and European (mostly via email) operators. WeChat a bit behind

Return communications

Source: Contactlab analysis

Figure 54: Example of Armani complete two-step sequence via email

Return Communications

Source: Contactlab analysis

Armani Armani 1 YES (Email)YES (Email, combined with

refund)

YES (Email, combined

with product received)

Mr Porter Burberry 1 YES (Email in English) YES (Email in English) YES (Email in English)

JD.com Burberry 1 YES (Phone call) YES (SMS)YES (Phone call and

SMS)

Yintai.com Burberry 1 YES (SMS and Email) YES (SMS) YES (SMS and Email)

Burberry Burberry 5 NOYES (Email, combined with

refund)

YES (Email, combined

with product received)

Secoo Burberry 6 YES (Email) NO YES (SMS)

Tod's Tod's 7 NO NO YES (Email)

Tmall Burberry 7 YES (SMS) NONO (only Alipay

notification)

WeChat Montblanc 7 NO NO YES (Email)

WeChat Chanel 7 NO NO YES (WeChat message)

YES YES YES

NO NO NO

RETURN COMMUNICATIONS

Purchasing Channel Purchased Brand RankingReturn request received

(Email, Phone call, SMS...)Products received

Refund confirmation

(from brand)

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 35

Figure 55: Example of JD.com Best practice with multiple communications with clients (SMS/Phone call)

Return Communications

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 36

Physical Touch Points

Figure 56: Burberry performing better via Tmall than directly. Apart from Tmall channel, European brands better than Chinese e-tailers/Dept. Stores and Mr Porter

Physical Touch Points – Overall Ranking

Source: Contactlab Analysis

Delivery

Figure 57: Striking performance from JD.com delivering in one day. Burberry also performing very well both directly and via Tmall. E-tailers pickup points widely adopted

Delivery ranking

Source: Contactlab analysis

External InternalDocuments

inside

Quality

FeaturesEasiness/Friendliness

Tmall E-Tailer Burberry 61 1 2 3 3 6 1 3

WeChat Social platform Montblanc 60 2 6 5 2 1 8 8

WeChat Social platform Chanel 57 3 6 1 1 2 10 7

Burberry Mega-Brand Burberry 55 4 2 2 10 2 1 3

Tod's Runner-Up Tod's 52 5 6 8 4 2 3 2

Armani Premium Armani 49 6 6 6 6 5 3 1

JD.com E-Tailer Burberry 41 7 1 10 8 7 3 5

Secoo E-Tailer Burberry 37 8 6 3 6 7 8 5

Mr Porter E-Tailer Burberry 35 9 4 8 5 10 3 8

Yintai.com Department Store Burberry 34 10 4 6 8 7 7 8

PHYSICAL TOUCH POINTS – RANKINGS CHINA 2016

Purchasing

Channel

Channel

Category

Purchased

BrandSCORE

OVERALL

RANKINGDELIVERY

PACKAGING RETURN PROCEDURE

COSTS

Purchasing

Channel

Purchased

BrandRanking

Declared standard delivery

performance during purchasing

Actual delivery performance from

purchase to arrival in Fujian province

Costs for standard

delivery

Delivery to

boutique/pick-up pointExtra effort

JD.com Burberry 1 Next day after payment 1 (from Guangzhou) Free YES, JD spot

Burberry Burberry 2 1-5 days after dispatching 2 (from Shanghai) Free YES, some boutiques

Tmall Burberry 2 Shipped within 3 days 2 (from Suzhou) Free YES, Tmall spot

Mr Porter Burberry 4 3-4 working days 4 (from UK) Free N.A. Signature at delivery option

Yintai.com Burberry 4 Not specified 2 (from Jinhua) Free NO Preferred delivery option

Armani Armani 6 3-5 working days 4 (from Shanghai) Free (promotion) NO

Tod's Tod's 6 1-2 days after dispatching 3 (from Shanghai) Free NO

Secoo Burberry 6 Not specified 4 (from Beijing) FreeYES, Secoo experience

center

WeChat Montblanc 6 Not specified 2 (from Shanghai) Free NO

WeChat Chanel 6 Not specified 2 (from Shanghai) Free NO

YES, declared 1-2 days FREE YES YES

YES, partial information 3 days

Not declared 4 or more Payment NO NO

DELIVERY

TIMING QUALITY FEATURES

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 37

Figure 58: Burberry – Example of pickup in store offering

Delivery to boutique

Source: Contactlab Analysis

Figure 59: Tmall and JD.com – Example of offering pickup points

Delivery to pickup point

Source: Contactlab Analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 38

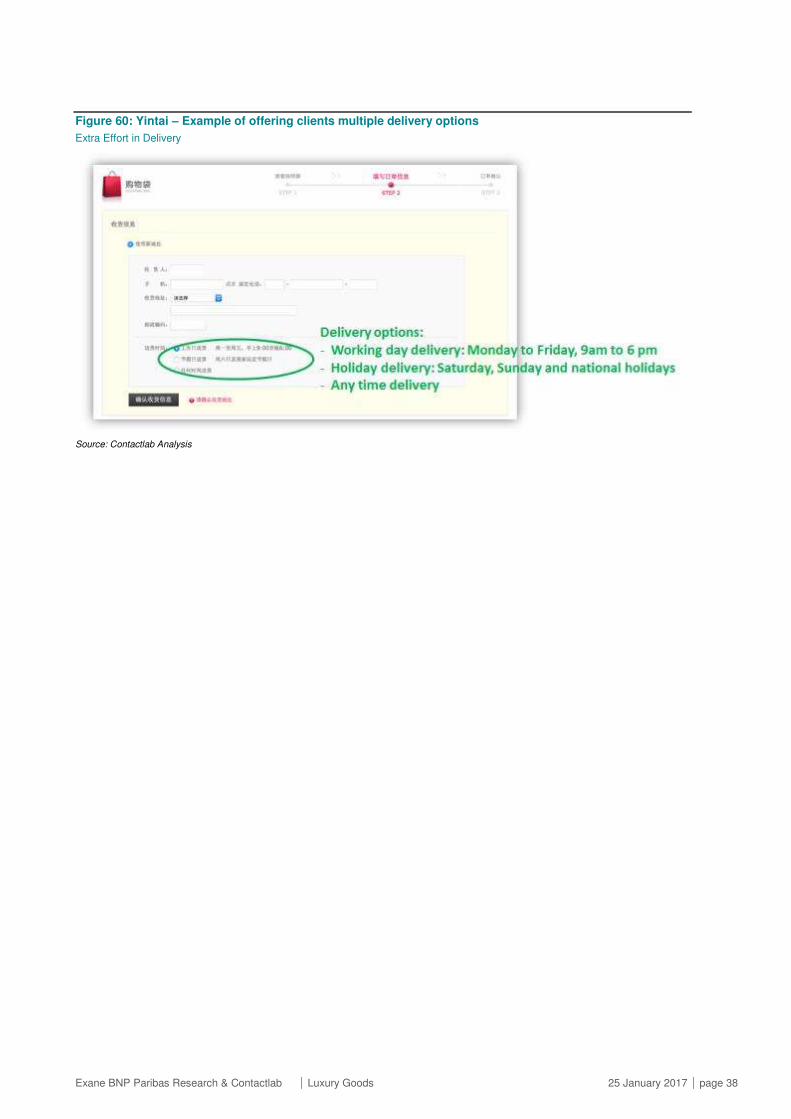

Figure 60: Yintai – Example of offering clients multiple delivery options

Extra Effort in Delivery

Source: Contactlab Analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 39

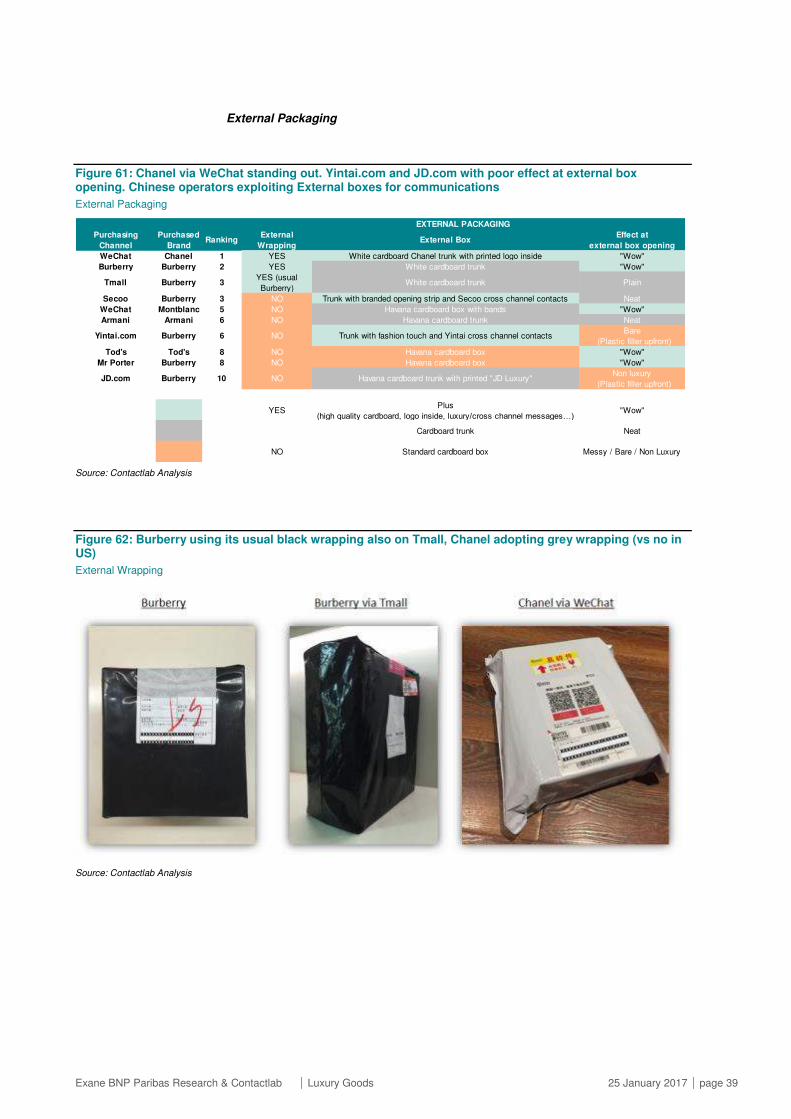

External Packaging

Figure 61: Chanel via WeChat standing out. Yintai.com and JD.com with poor effect at external box opening. Chinese operators exploiting External boxes for communications

External Packaging

Source: Contactlab Analysis

Figure 62: Burberry using its usual black wrapping also on Tmall, Chanel adopting grey wrapping (vs no in US)

External Wrapping

Source: Contactlab Analysis

Purchasing

Channel

Purchased

BrandRanking

External

Wrapping External Box

Effect at

external box opening

WeChat Chanel 1 YES White cardboard Chanel trunk with printed logo inside "Wow"

Burberry Burberry 2 YES White cardboard trunk "Wow"

Tmall Burberry 3YES (usual

Burberry)White cardboard trunk Plain

Secoo Burberry 3 NO Trunk with branded opening strip and Secoo cross channel contacts Neat

WeChat Montblanc 5 NO Havana cardboard box with bands "Wow"

Armani Armani 6 NO Havana cardboard trunk Neat

Yintai.com Burberry 6 NO Trunk with fashion touch and Yintai cross channel contactsBare

(Plastic filler upfront)

Tod's Tod's 8 NO Havana cardboard box "Wow"

Mr Porter Burberry 8 NO Havana cardboard box "Wow"

JD.com Burberry 10 NO Havana cardboard trunk with printed "JD Luxury" Non luxury

(Plastic filler upfront)

YESPlus

(high quality cardboard, logo inside, luxury/cross channel messages…)"Wow"

Cardboard trunk Neat

NO Standard cardboard box Messy / Bare / Non Luxury

EXTERNAL PACKAGING

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 40

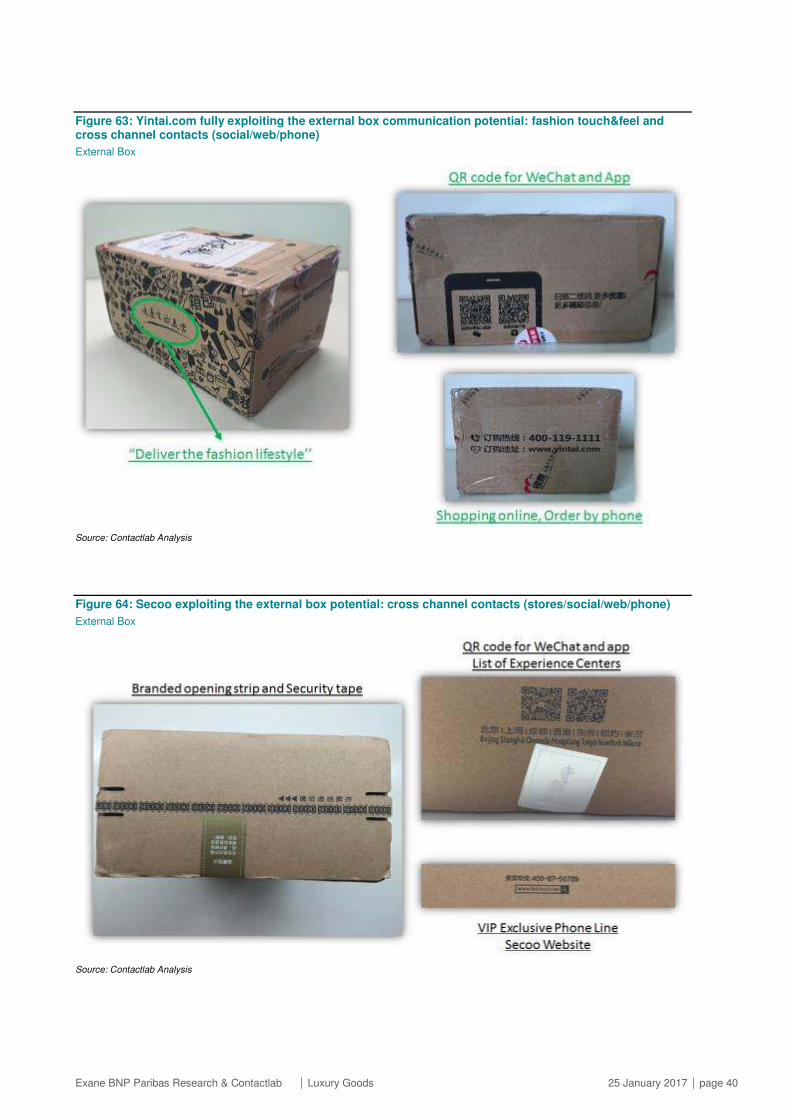

Figure 63: Yintai.com fully exploiting the external box communication potential: fashion touch&feel and cross channel contacts (social/web/phone)

External Box

Source: Contactlab Analysis

Figure 64: Secoo exploiting the external box potential: cross channel contacts (stores/social/web/phone)

External Box

Source: Contactlab Analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 41

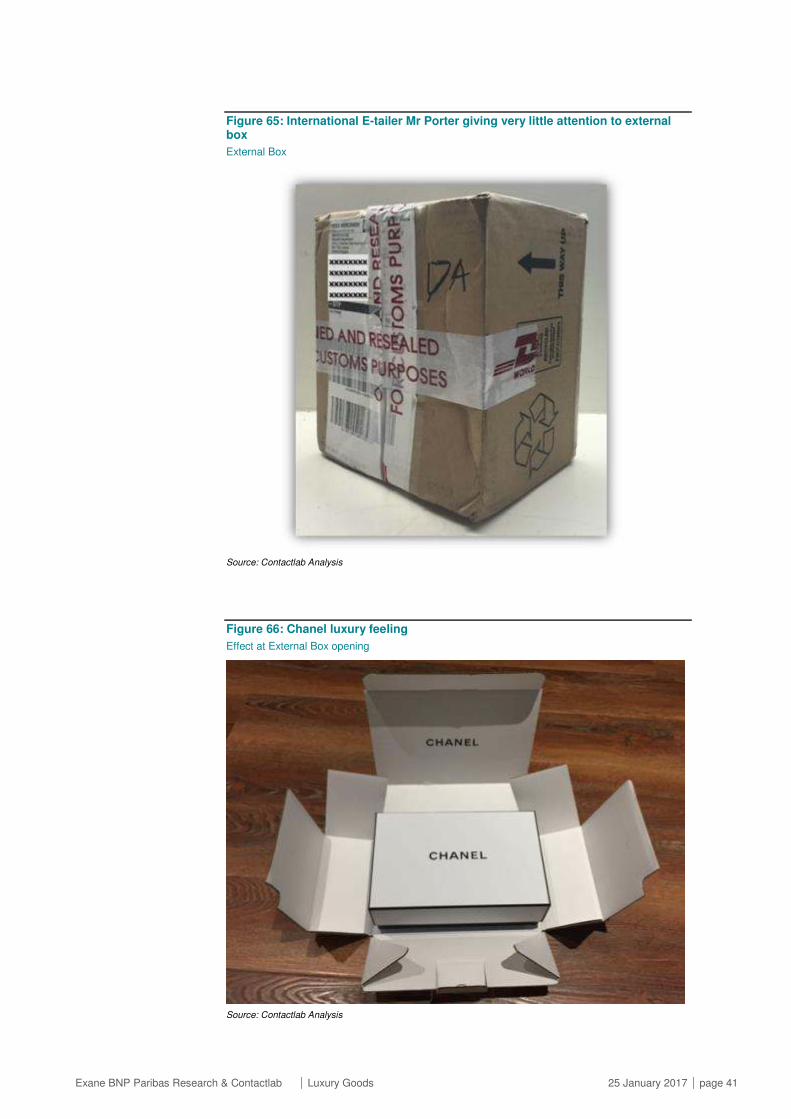

Figure 65: International E-tailer Mr Porter giving very little attention to external box

External Box

Source: Contactlab Analysis

Figure 66: Chanel luxury feeling

Effect at External Box opening

Source: Contactlab Analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 42

Figure 67: Burberry opening experience better directly than via Tmall

Effect at External Box opening

Source: Contactlab Analysis

Figure 68: JD.com poor visual impact

Effect at External Box opening

Source: Contactlab Analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 43

Figure 69: Yintai.com poor visual impact

Effect at External Box opening

Source: Contactlab Analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 44

Internal Packaging

Figure 70: Chanel and Montblanc with a superior attention to Internal Packaging. Burberry via Tmall and Secoo much better than direct

Internal Packaging

Source: Contactlab Analysis

Figure 71: Secoo Best Practice: look and feel similar to Mr Porter, plus cross-channel contacts (Club, APP, customer service number)

Internal Box

Source: Contactlab Analysis

Purchasing

Channel

Purchased

BrandRanking Internal box/bag

Effect at Internal

box/bag openingInternal wrapping Filler to keep product stable Product box Product wrapping and protection Extra touch Shopper bag

WeChat Chanel 1"Chanel luxury box" (white/black

smooth box with embossed logo)"Wow"

"Luxury"

(Chanel white branded tissue paper with sealing

wax for closure)

"Luxury"

(pleated tissue paper, very effective)"Premium branded box" (embossed Chanel logo)

"Plus"

(branded Chanel paperboard wrapping)

Perfume samples in

Chanel branded fabric

bag

NO

WeChat Montblanc 2Montblanc branded box (box with

logo)"Wow"

"Luxury"

(Montblanc branded paper wrap, branded ribbon,

white rigid paper box )

"Luxury"

(black small cut pleated premium paper,

effective)

"Premium branded box" (embossed Montblanc

logo)

"Luxury"

(branded Montblanc fabric bag)"Made in" navigator NO

Tmall Burberry 3

"Burberry luxury shopper bag"

(shopper bag with embossed

logo and ribbon

Neat NOYES

(white tissue paper)

"Luxury"

(made in England box with embossed Burberry

logo and ribbon)

"Luxury"

(tissue paper with branded Burberry sticker

plus branded Burberry fabric bag)

Yes

Tod's Tod's 4 NO n.a.

"Luxury"

(rigid Tod's branded textured cover, plus orange

tissue paper with ochre branded texture sticker)

"Luxury"

(crinkled orange paper, effective)

"Luxury"

(branded ochre box with Tod's branded ribbon)

"Luxury"

(brown fabric wrapping with embossed

Tod's logo)

NO

Mr Porter Burberry 5

"Mr. Porter luxury box"

(branded box with nice texture,

Mr.Porter signature)

"Wow"

(including client name on

sticker)

NOYES

(black tissue paper, effective)NO box

"Luxury"

(branded Burberry fabric bag)NO

Armani Armani 6"Armani luxury box"

(branded box with magnetic lock)Bare

"Tissue paper"

(white with black stickers)NO

"Premium branded box"

(grey textured box with embossed Armani logo)

"Plus"

(branded Armani tissue paper wrapping)NO

Secoo Burberry 6

"Secoo luxury box"

(box with nice texture,

embossed logo, cross channel

contacts)

Messy"Bare"

(trasparent plastic wrap)

YES

(plastic bubble wrap with Secoo logo,

effective)

NO box

(replaced by Burberry branded plastic bag)

"Luxury"

(branded Burberry fabric bag)NO

JD.com Burberry 8 NO n.a."Bare"

(trasparent plastic bag)

YES

(plastic bubble wrap with JD logo,

effective)

NO box

(replaced by Burberry branded plastic bag)

"Luxury"

(branded Burberry fabric bag)

Sunglasses as gift in

additional boxNO

Yintai.com Burberry 8 NO n.a. NOYES

(anonymous plastic bubble wrap)

NO box

(replaced by Burberry branded plastic bag)

"Luxury"

(branded Burberry fabric bag)Discount coupon NO

Burberry Burberry 10 NO n.a. NOYES

(white tissue paper cushion)

"Premium branded box"

(made in England box with embossed Burberry

logo)

"Plus"

(tissue paper with branded Burberry

sticker)

NO

Luxury feeling "Wow" Luxury feeling / Wow effect Luxury feeling / Wow effect Luxury/Wow effect Luxury/Wow effect - branded bag YES Yes

Brand name Neat Tissue paper Yes Premium (branded box) Plus - branded tissue paper

No box/bag Bare Bare / None None No boxPlain - plastic wrapping, unbranded tissue

paper NO NO

INTERNAL PACKAGING

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 45

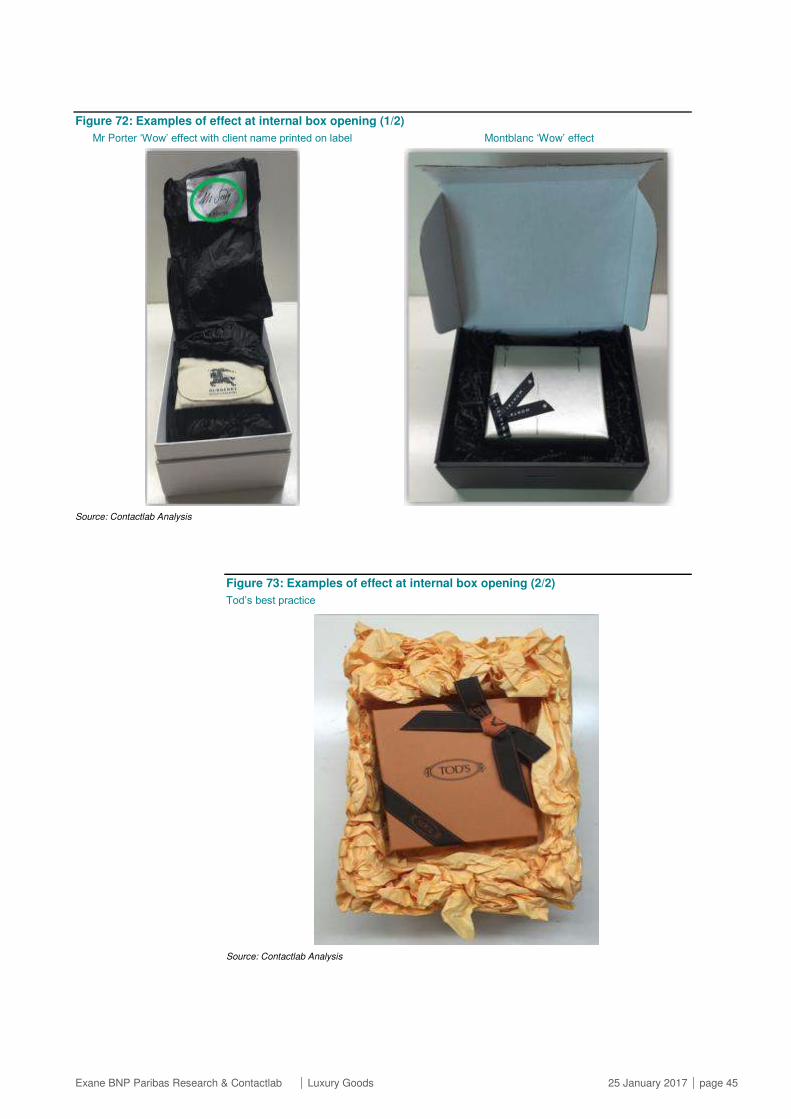

Figure 72: Examples of effect at internal box opening (1/2)

Mr Porter ‘Wow’ effect with client name printed on label Montblanc ‘Wow’ effect

Source: Contactlab Analysis

Figure 73: Examples of effect at internal box opening (2/2)

Tod’s best practice

Source: Contactlab Analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 46

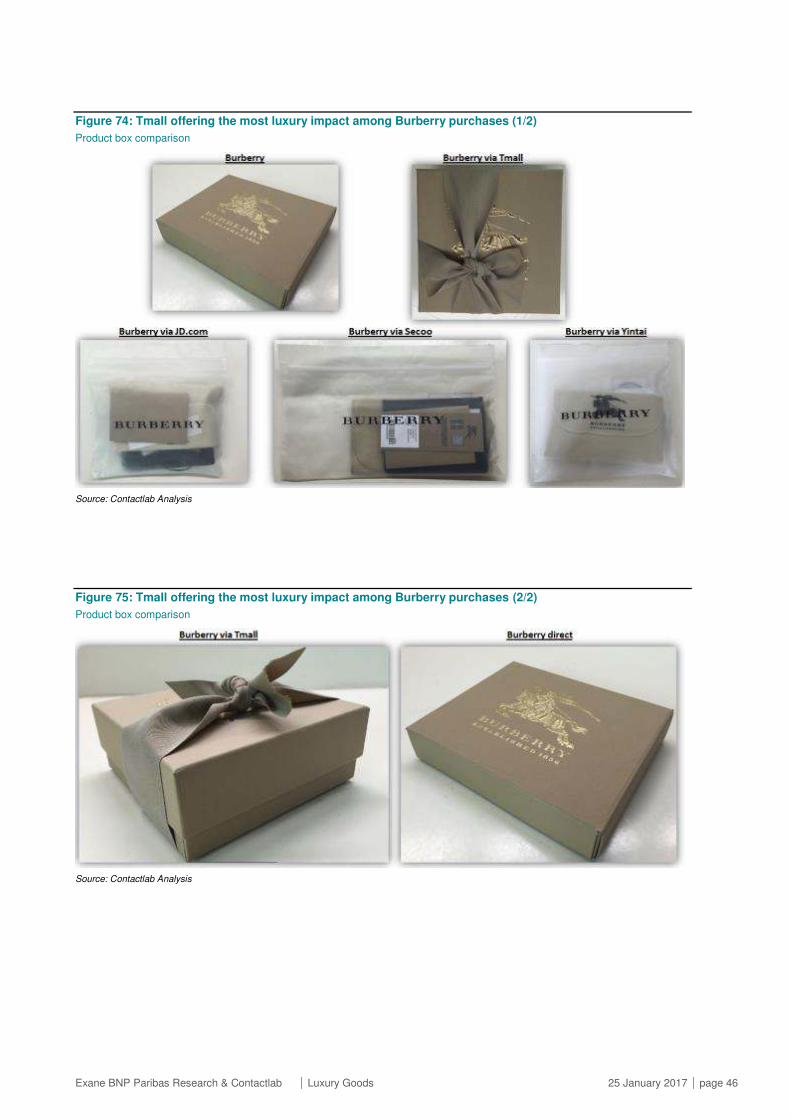

Figure 74: Tmall offering the most luxury impact among Burberry purchases (1/2)

Product box comparison

Source: Contactlab Analysis

Figure 75: Tmall offering the most luxury impact among Burberry purchases (2/2)

Product box comparison

Source: Contactlab Analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 47

Figure 76: Tmall best practice, including both tissue paper and fabric bag

Product wrapping and protection

Source: Contactlab Analysis

Figure 77: Extra touch in Internal packaging (1/2)

Chanel including perfume samples JD.com including sunglasses as gift

Source: Contactlab Analysis

Figure 78: Extra touch in Internal packaging (2/2)

Montblanc ‘Made in’ navigator to facilitate the understanding of Made in origin

Yintai.com promotion of Yintai Intime Retail with 30% off on first order

Source: Contactlab Analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 48

Documents inside Packaging

Figure 79: Montblanc standing out. Burberry direct better than via JD.com, Secoo, Yintai.com and Mr Porter

Documents inside packaging

Source: Contactlab Analysis

Figure 80: Examples of Thank you message

Montblanc dedicated card Chanel dedicated card

Source: Contactlab Analysis

WeChat Montblanc 1Yes, dedicated

cardNO "Luxury"

"Luxury"

(branded premium paper, neatly

folded)

YESYES

Montblanc warranty cardMade in Italy Made in Italy NO

Tod's Tod's 2 NO NO "Luxury"

"Luxury"

(branded premium paper, neatly

folded)

YES NO Made in Italy Made in Italy NO

Burberry Burberry 2 NO NO "Luxury""Plus"

(branded good quality paper)YES NO Made in Italy Made in Italy YES

WeChat Chanel 2Yes, dedicated

card inside folderNO NO

"Plus"

(branded good quality paper)YES NO Made in France Made in France

YES

(Plastic wrap should

not be opened)

Armani Armani 5

YES

(Mentioned in

order recap)

NO NO"Basic"

(loose and plain documents)YES

YES

Armani "Certificato di

autenticita"

Made in Italy Made in Italy YES

Tmall Burberry 6

YES

(Mentioned in

receipt)

NO "Plus""Basic"

(low quality paper and print)YES NO Made in Italy Made in Italy YES

JD.com Burberry 7 NO NO NO"Very basic"

(just return tag)

YES

(Burberry and

JD.com)

NO Made in China NO NO

Secoo Burberry 7 NO NO NO"Basic"

(plain one page document)

YES

(Burberry and

Secoo)

NO NO Made in Italy NO

Yintai.com Burberry 7 NO NO NO"Basic"

(plain one page document)YES NO Made in China

NO

(not even Burberry logo

on product)

NO

Mr Porter Burberry 10 NO NO NO"Basic"

(loose and plain documents)NO NO NO Made in China NO

Yes, dedicated

letterYes

Luxury

feelingLuxury feeling YES YES YES YES YES

Mention in other

docPlus Plus

No No No/plain Basic/very basic NO NO NO NO NO

Security tag for

return

DOCUMENTS

Purchasing

Channel

Purchased

BrandRanking

Thanks

messageGift card

Documents

EnvelopeShipping documents Brand product tag Authenticity certificate

"Made in" disclosure

on product

"Made in" disclosure

on product tag/box

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 49

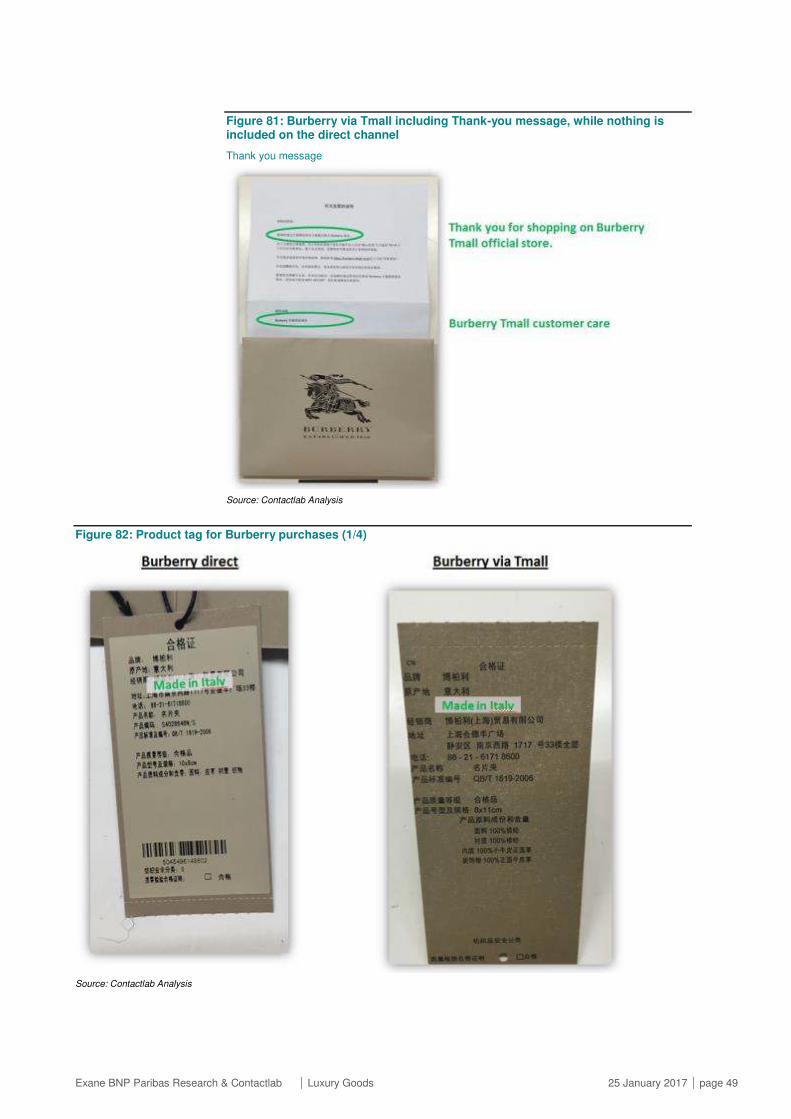

Figure 81: Burberry via Tmall including Thank-you message, while nothing is included on the direct channel

Thank you message

Source: Contactlab Analysis

Figure 82: Product tag for Burberry purchases (1/4)

Source: Contactlab Analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 50

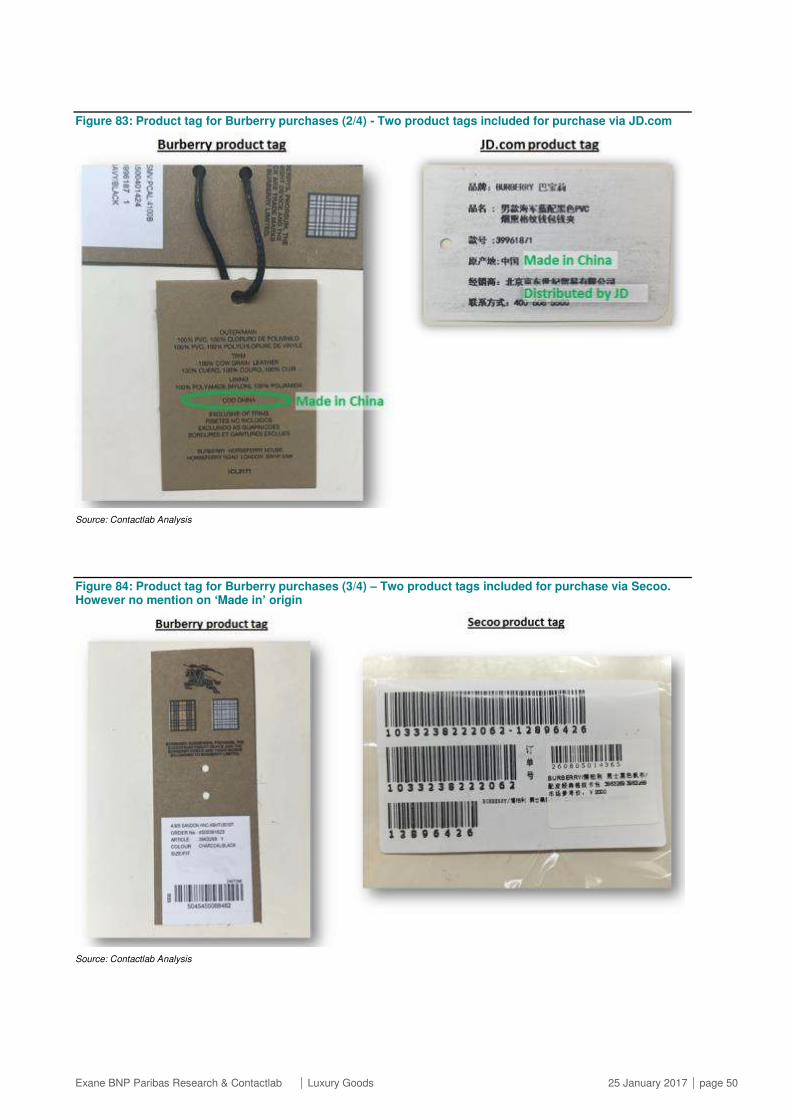

Figure 83: Product tag for Burberry purchases (2/4) - Two product tags included for purchase via JD.com

Source: Contactlab Analysis

Figure 84: Product tag for Burberry purchases (3/4) – Two product tags included for purchase via Secoo. However no mention on ‘Made in’ origin

Source: Contactlab Analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 51

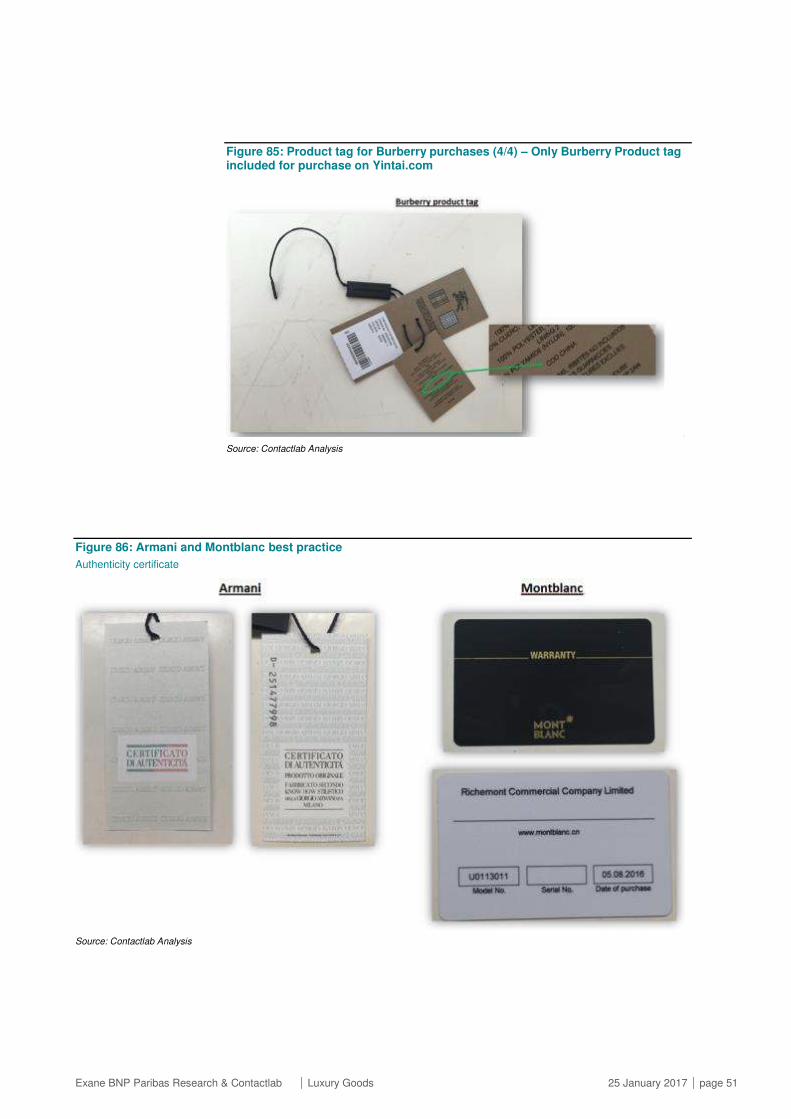

Figure 85: Product tag for Burberry purchases (4/4) – Only Burberry Product tag included for purchase on Yintai.com

Source: Contactlab Analysis

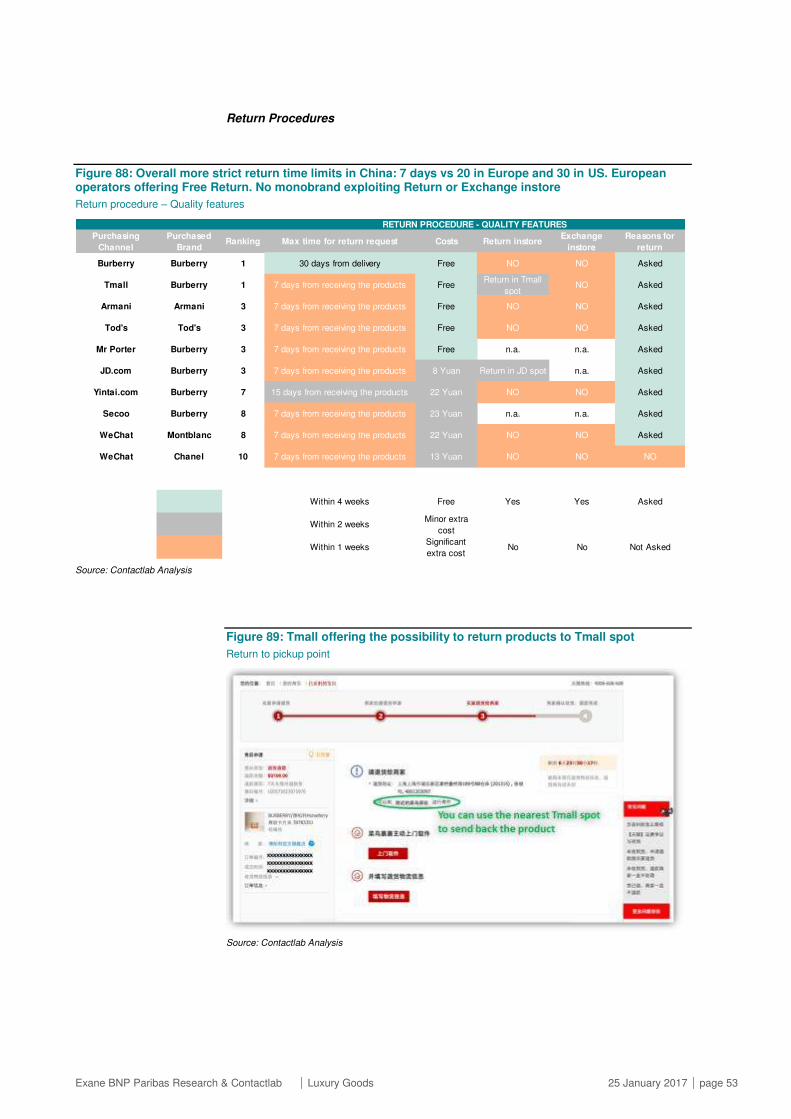

Figure 86: Armani and Montblanc best practice

Authenticity certificate

Source: Contactlab Analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 52

Figure 87: Secoo giving very confusing price information: 1,050 RMB on product page vs. 2,000 RMB on tag attached to the product. Incidentally, Burberry officially says 1,500 RMB!

Pricing information

Source: Contactlab Analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 53

Return Procedures

Figure 88: Overall more strict return time limits in China: 7 days vs 20 in Europe and 30 in US. European operators offering Free Return. No monobrand exploiting Return or Exchange instore

Return procedure – Quality features

Source: Contactlab Analysis

Figure 89: Tmall offering the possibility to return products to Tmall spot

Return to pickup point

Source: Contactlab Analysis

Purchasing

Channel

Purchased

BrandRanking Max time for return request Costs Return instore

Exchange

instore

Reasons for

return

Burberry Burberry 1 30 days from delivery Free NO NO Asked

Tmall Burberry 1 7 days from receiving the products FreeReturn in Tmall

spotNO Asked

Armani Armani 3 7 days from receiving the products Free NO NO Asked

Tod's Tod's 3 7 days from receiving the products Free NO NO Asked

Mr Porter Burberry 3 7 days from receiving the products Free n.a. n.a. Asked

JD.com Burberry 3 7 days from receiving the products 8 Yuan Return in JD spot n.a. Asked

Yintai.com Burberry 7 15 days from receiving the products 22 Yuan NO NO Asked

Secoo Burberry 8 7 days from receiving the products 23 Yuan n.a. n.a. Asked

WeChat Montblanc 8 7 days from receiving the products 22 Yuan NO NO Asked

WeChat Chanel 10 7 days from receiving the products 13 Yuan NO NO NO

Within 4 weeks Free Yes Yes Asked

Within 2 weeksMinor extra

cost

Within 1 weeksSignificant

extra costNo No Not Asked

RETURN PROCEDURE - QUALITY FEATURES

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 54

Figure 90: European operators make the return procedure more friendly: instructions inside box (Secoo too), pre-printed labels

Return procedure – easiness / friendliness

Source: Contactlab Analysis

Figure 91: Secoo best practice with visual aid

Instructions for Return

Source: Contactlab Analysis

Purchasing

ChannelPurchase Brand Ranking

Instructions for return

(inside packaging)

Return label

pre-printedCourier pick-up booking

Pick-up

location

Armani Armani 1 Within the recap order YES Phone call courier Home

Tod's Tod's 2 Only web YES Phone call courier Home

Burberry Burberry 3 Within the recap order NO via Customer Care Home

Tmall Burberry 3 Within the recap order NO via Customer Care Home

JD.com Burberry 5 Only web NO via Customer Care Home

Secoo Burberry 5 Form with visual aid NO Phone call courier Home

WeChat Chanel 7 Within the recap order NO Phone call courier Home

Mr Porter Burberry 8 Only web NO Phone call courier Home

Yintai.com Burberry 8 Only web NO Phone call courier Home

WeChat Montblanc 8 Only web NO Phone call courier Home

Extra effort YESSame step

(Online / Customer care)

Courier c/o

Customer

Within the recap order

Only web instruction NOExtra step

(Phone call courier)

Post office /

other location

RETURN PROCEDURE - EASINESS / FRIENDLINESS

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 55

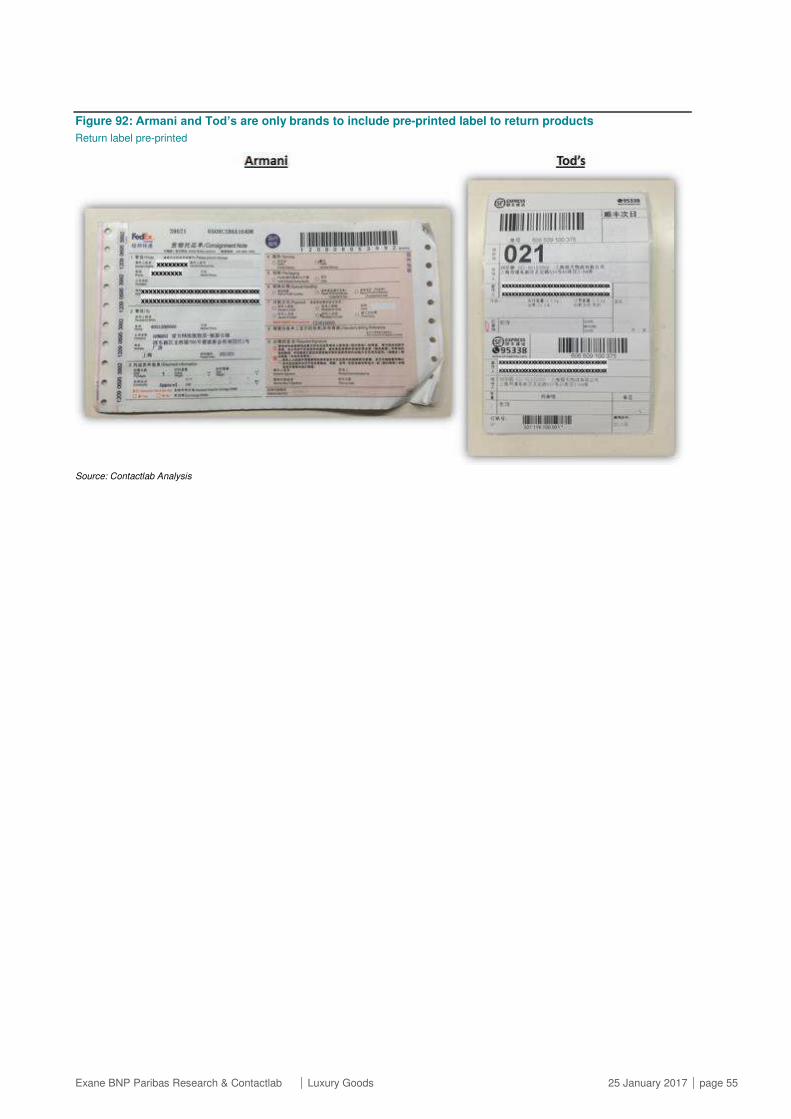

Figure 92: Armani and Tod’s are only brands to include pre-printed label to return products

Return label pre-printed

Source: Contactlab Analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 56

Methodology

Figure 93: Methodology

Source: Contactlab analysis

Figure 94: Scope of the Online Purchasing Process tested in China

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 57

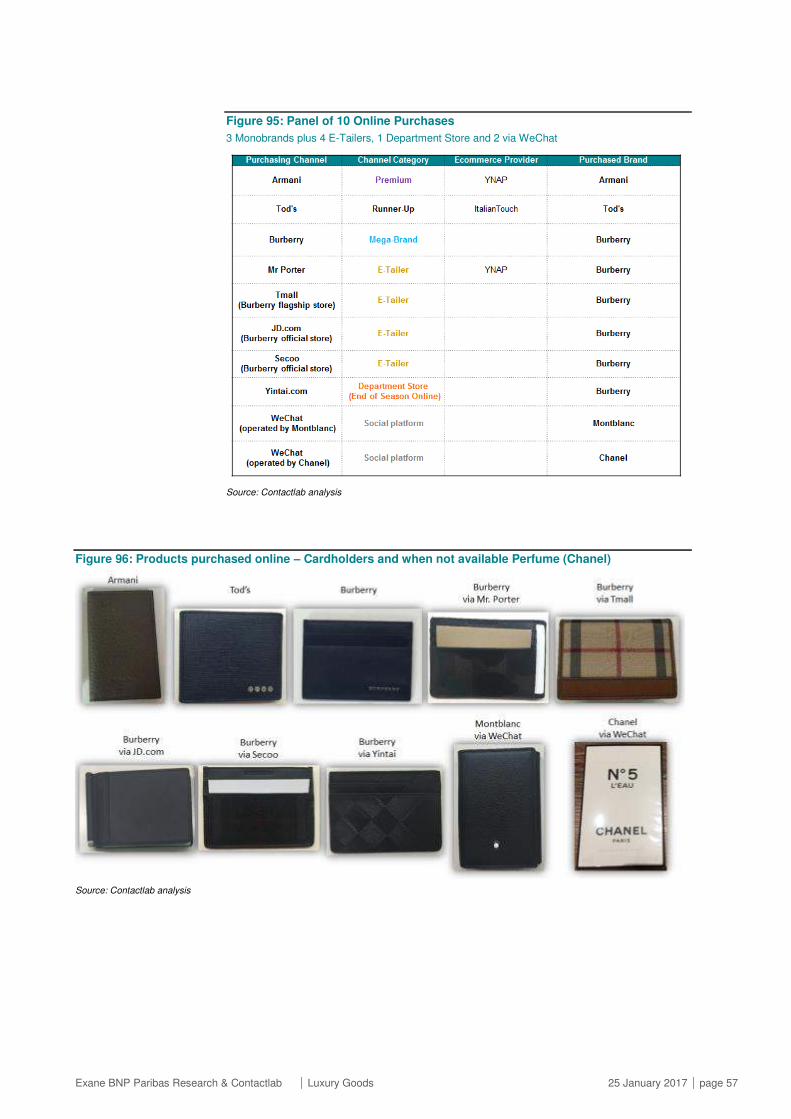

Figure 95: Panel of 10 Online Purchases

3 Monobrands plus 4 E-Tailers, 1 Department Store and 2 via WeChat

Source: Contactlab analysis

Figure 96: Products purchased online – Cardholders and when not available Perfume (Chanel)

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 58

Figure 97: Majority of European brands offering Quick Buy option in China, only JD.com among Chinese players

Quick Buy option (Buy as guest, no Account Registration required)

Source: Contactlab analysis

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 59

Appendix

Websites

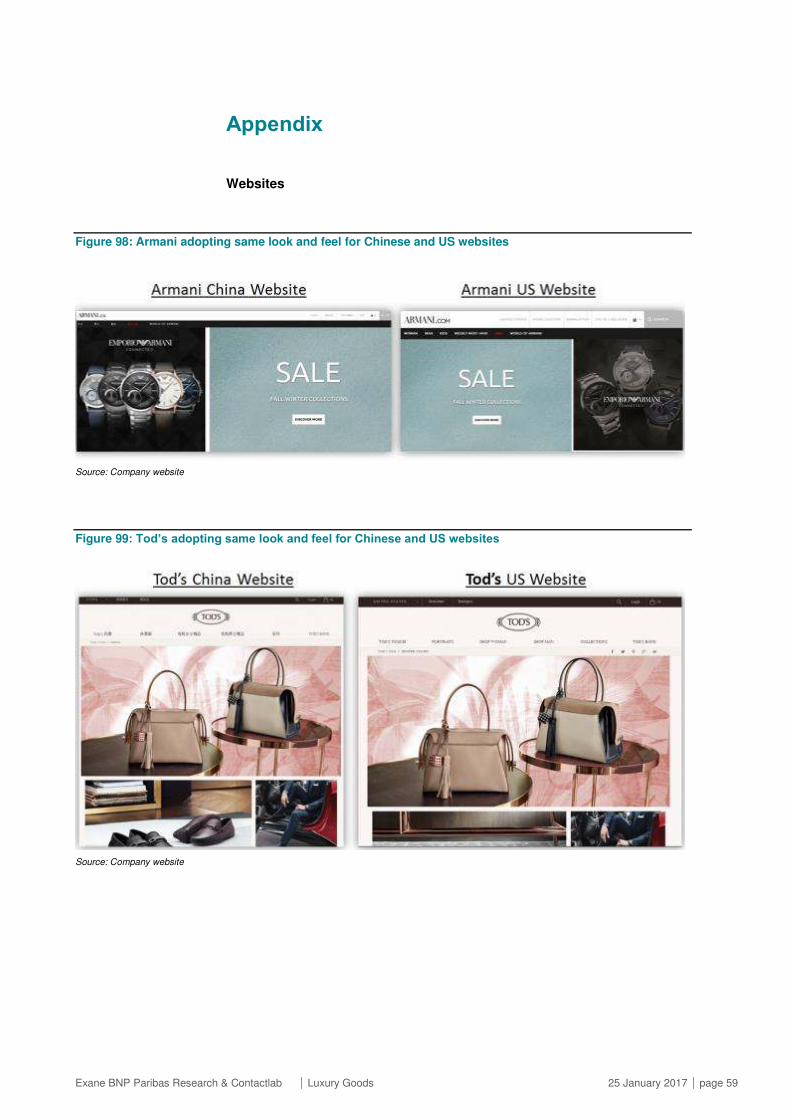

Figure 98: Armani adopting same look and feel for Chinese and US websites

Source: Company website

Figure 99: Tod’s adopting same look and feel for Chinese and US websites

Source: Company website

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 60

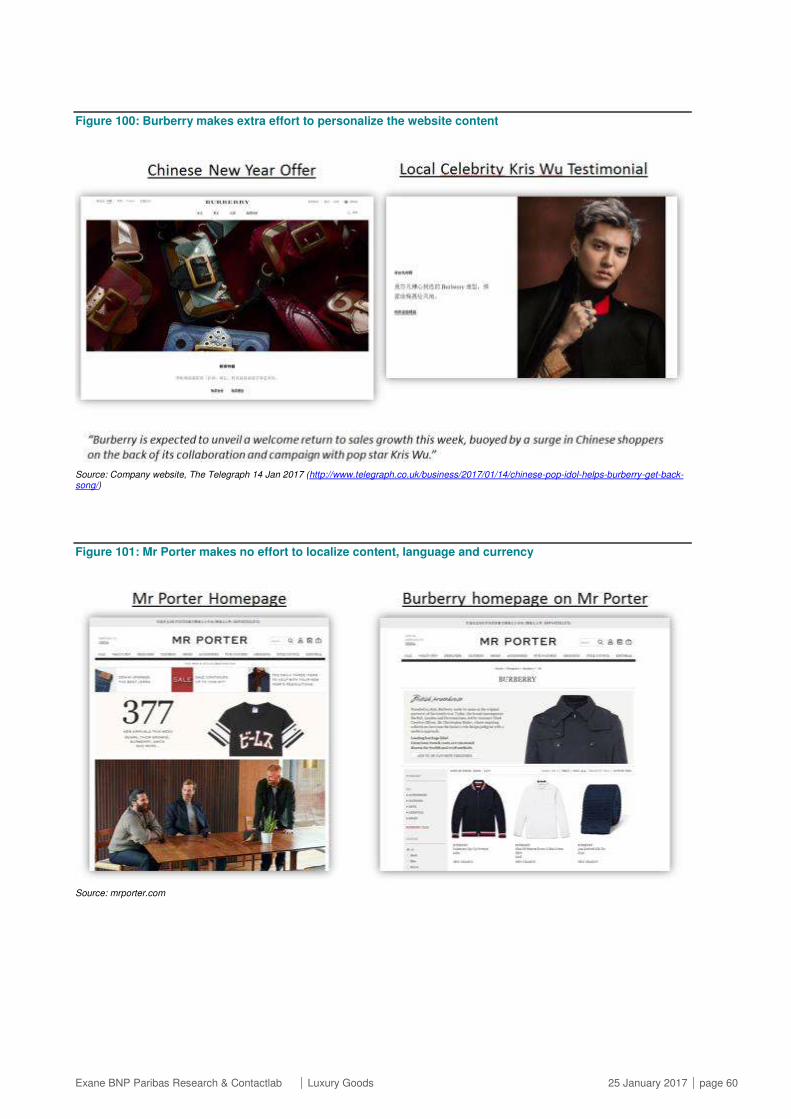

Figure 100: Burberry makes extra effort to personalize the website content

Source: Company website, The Telegraph 14 Jan 2017 (http://www.telegraph.co.uk/business/2017/01/14/chinese-pop-idol-helps-burberry-get-back-song/)

Figure 101: Mr Porter makes no effort to localize content, language and currency

Source: mrporter.com

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 61

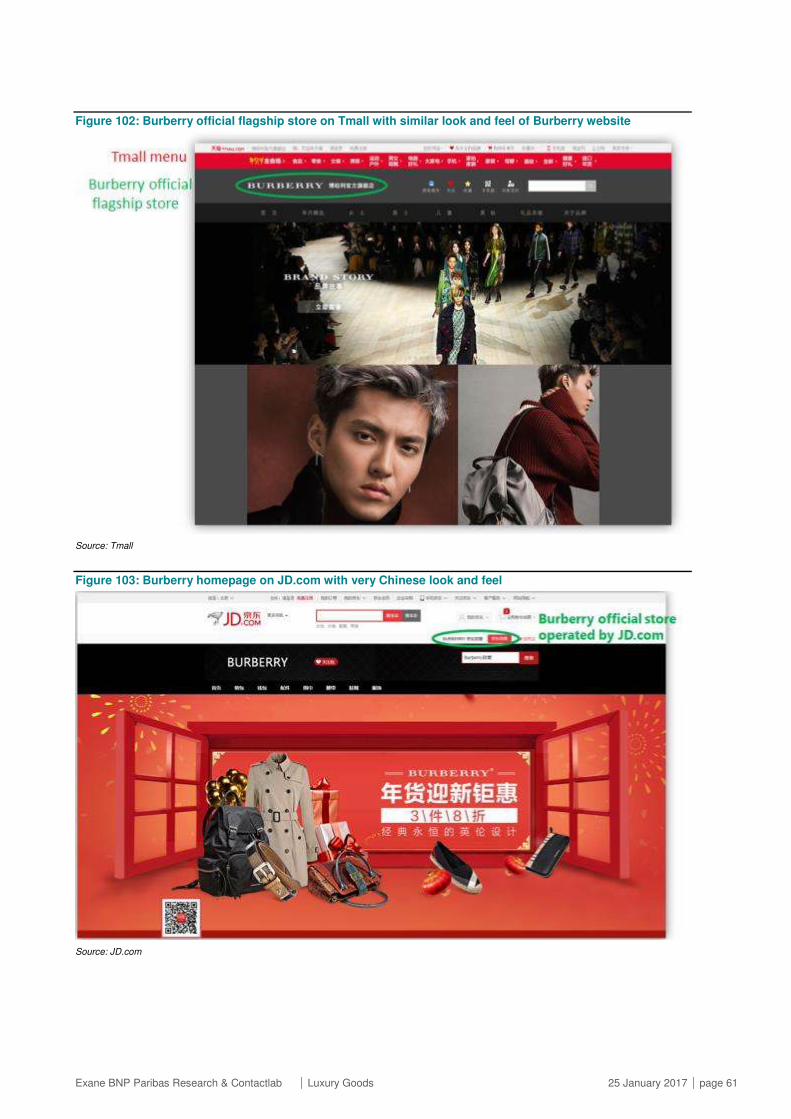

Figure 102: Burberry official flagship store on Tmall with similar look and feel of Burberry website

Source: Tmall

Figure 103: Burberry homepage on JD.com with very Chinese look and feel

Source: JD.com

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 62

Figure 104: Burberry homepage on Secoo pretty basic

Source: secoo.com

Figure 105: Burberry homepage on Yintai.com looks pretty basic

Source: Yintai.com

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 63

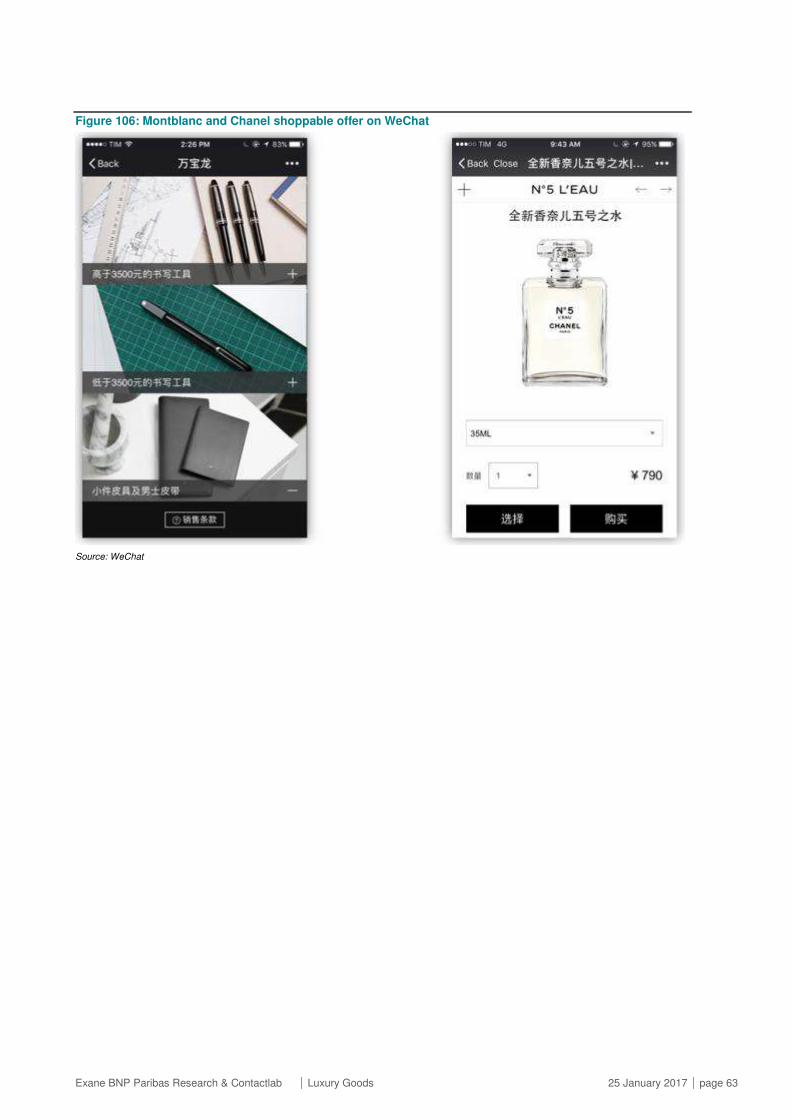

Figure 106: Montblanc and Chanel shoppable offer on WeChat

Source: WeChat

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 64

About the collaboration with Contactlab

Exane has worked in collaboration with Contactlab on this report and the sections provided by Contactlab are clearly highlighted. The

contributors from Contactlab are Marco Pozzi, Francesca Borgonovo, Xian Zhang and Kuiling Song.

Contributors from Contactlab are not Research analysts and are not FCA or AMF registered. They have only shared their expertise on

clearly delineated sections of the report and did not have access to the full report or its conclusions prior to publication.

Contactlab presentation

Contactlab provides the leading engagement marketing platform for commerce-focused companies and fashion & luxury brands to

develop successfully digital communication programs that enable personalized marketing to unlock demand and build lasting customer

preferences. Founded in 1998, Contactlab is led by its founder Massimo Fubini, an internet industry veteran and opinion leader in the

marketing field since 1995.

Thanks to our own enabling PaaS technology and to the experience of our navigated professionals, we enable brands to achieve a

deeper understanding of customers, to deliver uniquely relevant messages at every touchpoint of the customer journey and to measure

performances with real-time dashboards that display all the relevant data. Our enterprise-grade platform is built with the highest security

level, reliability, management, scalability.

Our solutions enable brands to gain insights into the context of each customer and deepen the retail experience by delivering highly

individualized digital contact plans across channels based on events, preferences and product lifecycle.

Today, we work with more than 1000 clients in different industries across the world and serve most of the world-class brands in the

Luxury and Fashion sectors

Disclosures All stock-specific commentary and recommendations in this report are solely based on Exane Research.

Contactlab Contactlab does not make investment recommendations, in this report or otherwise, and nothing in this report should be interpreted as an

opinion by Contactlab either on market forecasts or on the prospects of specific companies.

This report and all of its content are strictly confidential. It may not be circulated or otherwise reproduced in whole or in part.

The analyses set out in the Report are the result of the aggregation of public materials and data coming from a sample of industry players.

Use of this report by any person for whatever purpose should not, and does not, absolve such third party from using due diligence and care in

verifying the report’s contents. Any use which a person makes of this document, or any reliance on it, or decisions to be made based on it, are the responsibility of such

person.

Contactlab, its affiliates and representatives accept no duty of care or liability of any kind whatsoever to any person, and no responsibility for

damages, if any, suffered by any person as the result of decision made, or not made, or actions taken, or not taken, based on this document..

Exane BNP Paribas Research & Contactlab Luxury Goods 25 January 2017 page 65

DISCLOSURE APPENDIX

Analyst Certification We, Melania Grippo, Guido Lucarelli, Luca Solca, (authors of or contributors to the report) hereby certify that all of the views expressed in this report accurately reflect our personal view(s) about the company or companies and securities discussed in this report. No part of our compensation was, is, or will be, directly, or indirectly, related to the specific recommendations or views expressed in this research report.

Non-US Research Analyst Disclosure The research analysts named below were involved in preparing this research report. Research analysts at Exane Limited and Exane SA are not associated persons of Exane Inc. and thus are not registered or qualified in the U.S. as research analysts with the Financial Industry Regulatory Authority (FINRA) or the New York Stock Exchange (NYSE). These non-U.S. analysts are not subject to the NASD Rule 2241 and NYSE Rule 472 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account. Melania Grippo Exane SA Guido Lucarelli Exane SA Luca Solca Exane SA Exane SA is regulated by the Autorité des Marchés Financiers (AMF) in France, Exane Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom, and Exane Inc. is regulated by FINRA and the U.S. Securities and Exchange Commission in the United States.

Research Analyst Compensation The research analyst(s) responsible for the preparation of this report receive(s) compensation based upon various factors including overall firm revenues, which may include investment banking activities.

Disclosure of the report to the company/ies Companies Disclosures

NONE 1 – Sections of this report, with the research summary, target price and rating removed, have been presented to the subject company/ies prior to its distribution, for the sole purpose of verifying the accuracy of factual statements. 2 – Following the presentation of sections of this report to this subject company, some conclusions were amended.

Commitment to transparency on potential conflicts of interest: BNP Paribas While BNP Paribas (“BNPP”) holds a material ownership interest in the various Exane entities, Exane and BNPP have entered into an agreement to maintain the independence of Exane's research reports from BNPP. These research reports are published under the brand name “Exane BNP Paribas”. Nevertheless, for the sake of transparency, we separately identify potential conflicts of interest with BNPP regarding the company/(ies) covered by this research document.

The latest company-specific disclosures, valuation methodologies and investment case risks for all other companies covered by this document are available on http://cube.exane.com/compliance.

LONDON Exane Limited 1 Hanover Street London W1S 1YZ UK Tel: (+44) 207 039 9400 Fax: (+44) 207 039 9440

PARIS Exane S.A. 6 Rue Ménars 75002 Paris France Tel: (+33) 1 44 95 40 00 Fax: (+33) 1 44 95 40 01

FRANKFURT Branch of Exane S.A. Europa-Allee 12, 3rd floor 60327 Frankfurt Germany Tel: (+49) 69 42 72 97 300 Fax: (+49) 69 42 72 97 301

GENEVA Branch of Exane S.A. Rue du Rhône 80 1204 Geneva Switzerland Tel: (+41) 22 718 65 65 Fax: (+41) 22 718 65 00

MADRID Branch of Exane S.A. Calle Génova, 27 7th Floor Madrid 28004 Spain Tel: (+34) 91 114 83 00 Fax: (+34) 91 114 83 01

MILAN Branch of Exane S.A. Via dei Bossi 4 20121 Milan Italy Tel: (+39) 02 89 63 17 13 Fax: (+39) 02 89 63 17 01

NEW YORK Exane Inc. 640 Fifth Avenue 15th Floor New York, NY 10019 USA Tel: (+1) 212 634 4990 Fax: (+1) 212 634 5171

SINGAPORE Branch of Exane Limited 20 Collyer Quay #07-02 Tung Centre Singapore 049319 Tel: (+65) 6212 9059 Fax: (+65) 6212 9082

STOCKHOLM Branch of Exane Limited Nybrokajen 5 111 48 Stockholm Sweden Tel: (+46) 8 5629 3500 Fax: (+46) 8 611 1802

CONTACTLAB MILAN Contactlab Italy, S.p.A Via Natale Battaglia, 12 20127 Milan Italy Tel: (+39) 02 28 31 181 Fax: (+39) 02 70 03 02 69

PARIS Contactlab France, Sarl 5 Rue du Helder 75009 Paris France Tel: (+33) 1 53 24 53 88 Fax: (+33) 1 74 18 05 55

MUNICH Contactlab Deutschland, GmbH Landwehrstrasse 61 80336 Munich Germany Tel: (+49) 89 41 11 23 444 Fax: (+49) 89 41 11 23 111

All Exane research documents are available to all clients simultaneously on the Exane website (http://cube.exane.com). Most published research is also available via third-party aggregators such as Bloomberg, Thomson Reuters, Factset and Capital IQ. Exane is not responsible for the redistribution of research by third-party aggregators. Important notice: Please refer to our complete disclosure notice and conflict of interest policy available on http://cube.exane.com/compliance This research is produced by one or more of EXANE SA, EXANE Limited and Exane Inc (collectively referred to as “EXANE") . EXANE SA is authorized by the Autorité de Contrôle Prudentiel et de Résolution and regulated by the Autorité des Marchés Financiers ("AMF"). EXANE Limited is authorized and regulated by the Financial Conduct Authority (“FCA”). Exane Inc is registered and regulated by the Financial Industry Regulatory Authority ("FINRA"). In accordance with the requirements of Financial Conduct Authority COBS 12.2.3R and associated guidance, of article 313-20 of the AMF Règlement Général, and of FINRA Rule 2241, Exane’s policy for managing conflicts of interest in relation to investment research is published on Exane’s web site (cube.exane.com). Exane also follows the guidelines described in the code of conduct of the Association Francaise des Entreprises d'Investissement ("AFEI") on managing conflicts of interest in the field of investment research. This code of conduct is available on Exane’s web site (http://cube.exane.com). This research is solely for the private information of the recipients. All information contained in this research report has been compiled from sources believed to be reliable. However, no representation or warranty, express or implied, is made with respect to the completeness or accuracy of its contents, and it is not to be relied upon as such. Opinions contained in this research report represent Exane's current opinions on the date of the report only. Exane is not soliciting an action based upon it, and under no circumstances is it to be used or considered as an offer to sell, or a solicitation of any offer to buy. While Exane endeavours to update its research reports from time to time, there may be legal and/or other reasons why Exane cannot do so and, accordingly, Exane disclaims any obligation to do so. This report is provided solely for the information of professional investors who are expected to make their own investment decisions without undue reliance on this report and Exane accepts no liability whatsoever for any direct or consequential loss arising from any use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose. Any United States person wishing to obtain further information or to effect a transaction in any security discussed in this report should do so only through Exane Inc., which has distributed this report in the United States and, subject to the above, accepts responsibility for its contents. BNP PARIBAS has acquired an interest in VERNER INVESTISSEMENTS the parent company of EXANE. VERNER INVESTISSEMENTS is controlled by the management of EXANE. BNP PARIBAS’s voting rights as a shareholder of VERNER INVESTISSEMENTS will be limited to 40% of overall voting rights of VERNER INVESTISSEMENTS.