the retail tsunami: a perspective on recent chapter 11 ... retail tsunami bcca media... · the...

TRANSCRIPT

Bruce S. Nathan, Esq.LOWENSTEIN SANDLER LLPTel: (212) 204-8686

@BruceSNathan

The Retail Tsunami: A Perspective on Recent Chapter 11 Cases, Including Payless ShoeSource and Toys R Us

49165305

PRESENTATION FOR:

BCCA Media Credit SeminarLocation: Lowenstein Sandler LLP

New York office

November 7, 2017

PRESENTED BY:

Wanda Borges, Esq.BORGES & ASSOCIATES, LLCTel: (516) 677-8200, x 225

ALL TYPES OF

RETAILERS AT RISK

Page 1

2

Major Risk

�Department Stores

�Electronic Retailers

�Retail Operations

Page 2

RECENT DEVELOPMENTS

IN RETAIL BANKRUPTCIES

Page 3

44

Latest Retail Chapter 11

4

Toys “R” Us – 9/19/017

Page 4

55

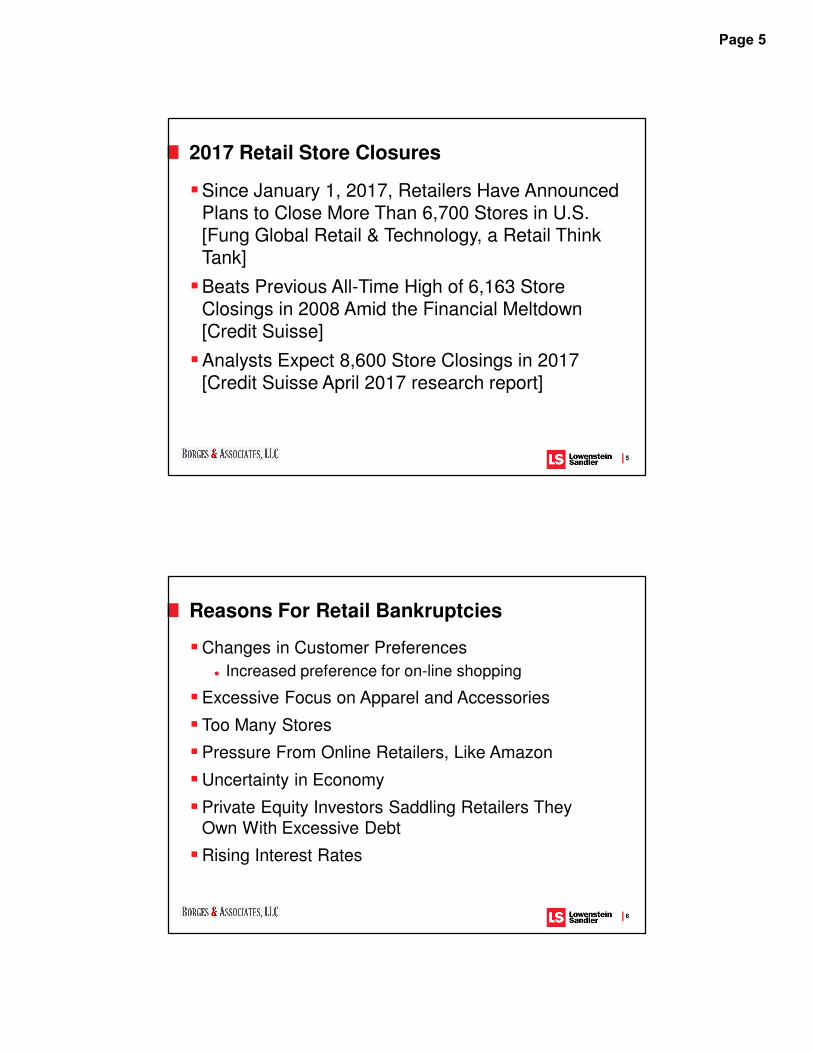

2017 Retail Store Closures

�Since January 1, 2017, Retailers Have Announced Plans to Close More Than 6,700 Stores in U.S. [Fung Global Retail & Technology, a Retail Think Tank]

�Beats Previous All-Time High of 6,163 Store Closings in 2008 Amid the Financial Meltdown [Credit Suisse]

�Analysts Expect 8,600 Store Closings in 2017 [Credit Suisse April 2017 research report]

66

�Changes in Customer Preferences

● Increased preference for on-line shopping

�Excessive Focus on Apparel and Accessories

� Too Many Stores

�Pressure From Online Retailers, Like Amazon

�Uncertainty in Economy

�Private Equity Investors Saddling Retailers They

Own With Excessive Debt

�Rising Interest Rates

Reasons For Retail Bankruptcies

Page 5

77

The Next Stores To Fall According to Predictions of Future Retail Bankruptcies Within Next 12 Months

�Sears/Kmart

�Claire’s Stores

�J Crew

�99 Cents Only Stores

�Forever 21

�Bon Ton Stores

88

� As of 8/31/017, 4 Retailers filed Chapter 11 Cases during Prior Year

for the Second Time: Chapter 22

� American Apparel

● First Chapter 11 filing date: 10/5/15

● Date of emergence from first Chapter 11: 2/5/16

● Date of second Chapter 11 filing: 11/14/16

● Time between filings: 9.3 months

� Radio Shack

● First Chapter 11 filing date: 2/25/15

● Date of emergence from first Chapter 11: 10/7/15

● Date of second Chapter 11 filing: 3/8/17

● Time between filings: 17 months

Retailers That Emerged From Chapter 11 Only to File Again – Chapter 22

Page 6

99

� Wet Seal

● First Chapter 11 filing date: 1/15/15

● Date of emergence from first Chapter 11: 12/31/15

● Date of second Chapter 11 filing: 2/2/17

● Time between filings: 13.1 months

� Bob’s Stores/EMS

● First Chapter 11 filing date: 4/18/16

● Date of emergence from first Chapter 11: 7/18/16

● Date of second Chapter 11 filing: 2/5/17

● Time between filings: 6.6 months

Retailers That Emerged From Chapter 11 Only to File Again – Chapter 22

1010

A New Phenomenon: Reorganizing Retailers

�Retailers With Confirmed Chapter 11 Plans of Reorganization That Call for Most Stores to Remain Open

● Payless ShoeSource

● True Religion Apparel

● rue 21

● Gymboree Corp.

● Perfumania Holdings (Prepackaged Chapter 11 plan

approved – general unsecured claims to receive

payment of 100% of their claims)

● Toys R Us?

Page 7

1111

Recent Chapter 11 Proceedings

� Gymboree: The children's clothing retailer filed for bankruptcyon June 11, 207 saying it may close 375 of its 1,300 stores under the Gymboree, Crazy 8 and Janie and Jack brands. Chapter 11 plan approved on September 7, 2017 and the plan went effective on September 29, 2017

� rue21: The teen clothing retailer filed for bankruptcy on May 15, 2017 and said it has plans to close about one third of its 1,200 stores. Chapter 11 plan approved on September 8, 2017 and the plan went effective on September 22, 2017

� Gordmans Stores: A century-old regional department store chain, Gordmans had 106 stores in 22 states in the Midwest and western U.S. It filed for bankruptcy on March 13, 2017 and is shuttering all of its stores. Chapter 11 plan approved.

1212

Recent Chapter 11 Proceedings

� RadioShack: The iconic electronics retailer first filed for bankruptcy in 2015, and tried to stay in business through a deal with Sprint in which the wireless provider operated stores within the RadioShack stores. But in March, 2017, the company that now owns RadioShack filed for bankruptcy once again, putting it on the path to close its remaining stores. Chapter 11 plan approved on October 25, 2017

� Wet Seal: The troubled teen clothing retailer, which made a previous trip through bankruptcy in 2015, filed for bankruptcy again in February, 2017. This time it went out of business, closing 171 stores and putting 1,750 employees out of work.

� The Limited: The once popular women's clothing chain filed for bankruptcy in January, 2017 and closed all of its remaining stores.

Page 8

THE SPORTS AUTHORITY

BANKRUPTCY CAST A

SHADOW ON ATHLETIC RETAIL

Page 9

1414

The Sports Authority

�Chapter 11 filing on March 2, 2016

�Many creditors felt comfortable because

majority of inventory was sold to TSA

pursuant to Consignment Agreements

● Most Consignment Agreements turned

about to be “no good”

- Notice was not given or was defective

- UCC Financing Statement was not filed

1515

The Sports Authority

�Demise began as a leveraged buyout

● A financial transaction in which a company is

purchased with a combination of equity and debt, such

that the company's cash flow is the collateral used to

secure and repay the borrowed money.

�Recall the many failed leverage buyouts of the 1980’s and 1990’s

�Minimizing Risk

● Watch for Leveraged Buyouts

Page 10

1616

The Sports Authority

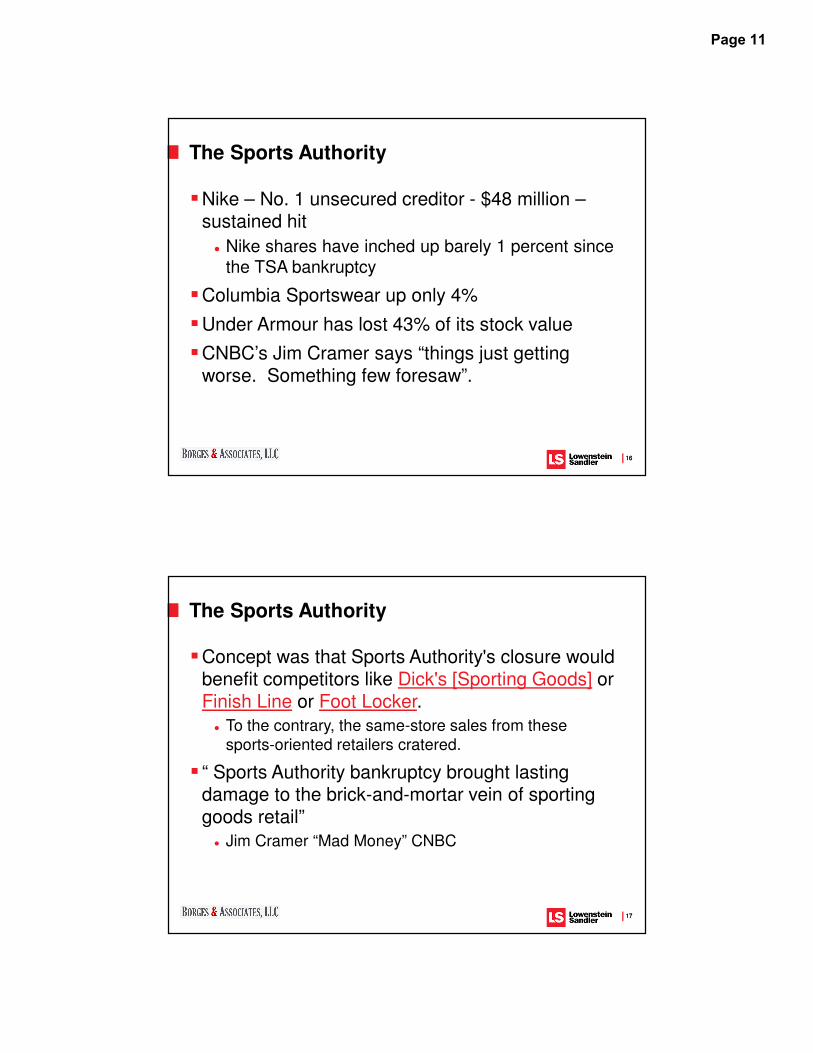

�Nike – No. 1 unsecured creditor - $48 million –sustained hit

● Nike shares have inched up barely 1 percent since

the TSA bankruptcy

�Columbia Sportswear up only 4%

�Under Armour has lost 43% of its stock value

�CNBC’s Jim Cramer says “things just getting worse. Something few foresaw”.

1717

The Sports Authority

�Concept was that Sports Authority's closure would benefit competitors like Dick's [Sporting Goods] or Finish Line or Foot Locker.

● To the contrary, the same-store sales from these

sports-oriented retailers cratered.

� “ Sports Authority bankruptcy brought lasting damage to the brick-and-mortar vein of sporting goods retail”

● Jim Cramer “Mad Money” CNBC

Page 11

1818

The Sports Authority

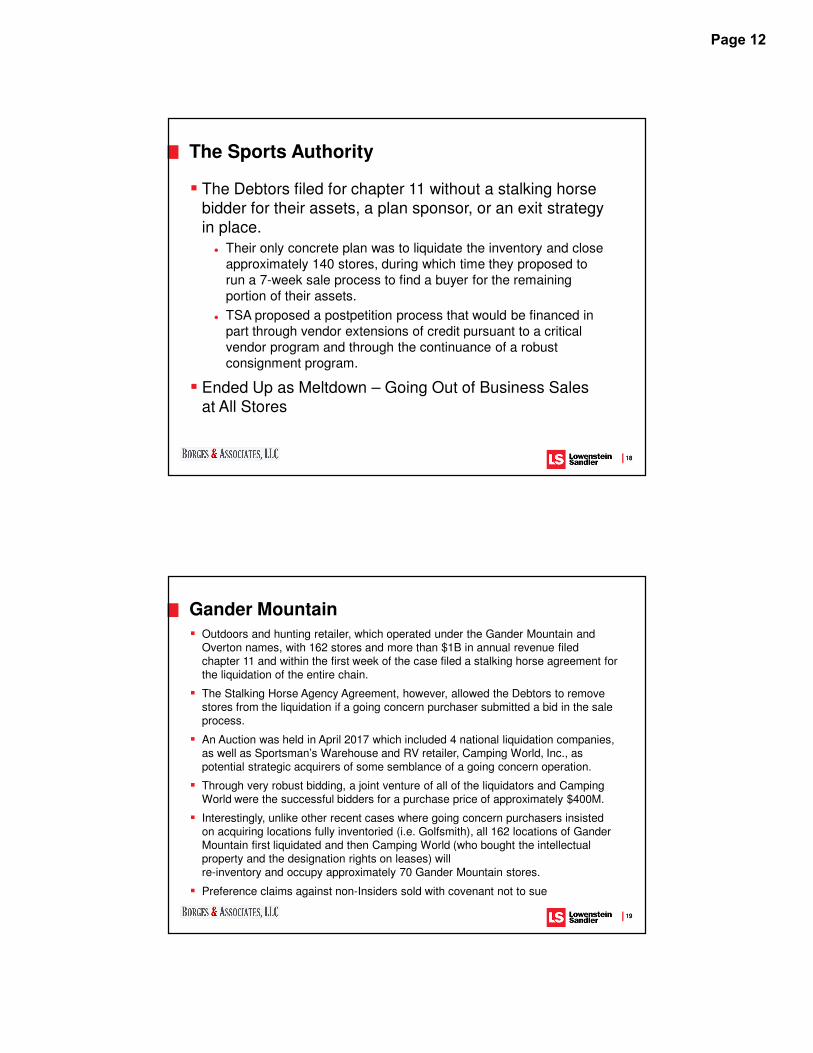

� The Debtors filed for chapter 11 without a stalking horse

bidder for their assets, a plan sponsor, or an exit strategy

in place.

● Their only concrete plan was to liquidate the inventory and close

approximately 140 stores, during which time they proposed to

run a 7-week sale process to find a buyer for the remaining

portion of their assets.

● TSA proposed a postpetition process that would be financed in

part through vendor extensions of credit pursuant to a critical

vendor program and through the continuance of a robust

consignment program.

� Ended Up as Meltdown – Going Out of Business Sales

at All Stores

1919

Gander Mountain

� Outdoors and hunting retailer, which operated under the Gander Mountain and Overton names, with 162 stores and more than $1B in annual revenue filed chapter 11 and within the first week of the case filed a stalking horse agreement for the liquidation of the entire chain.

� The Stalking Horse Agency Agreement, however, allowed the Debtors to remove stores from the liquidation if a going concern purchaser submitted a bid in the sale process.

� An Auction was held in April 2017 which included 4 national liquidation companies, as well as Sportsman’s Warehouse and RV retailer, Camping World, Inc., as potential strategic acquirers of some semblance of a going concern operation.

� Through very robust bidding, a joint venture of all of the liquidators and Camping World were the successful bidders for a purchase price of approximately $400M.

� Interestingly, unlike other recent cases where going concern purchasers insisted on acquiring locations fully inventoried (i.e. Golfsmith), all 162 locations of Gander Mountain first liquidated and then Camping World (who bought the intellectual property and the designation rights on leases) will re-inventory and occupy approximately 70 Gander Mountain stores.

� Preference claims against non-Insiders sold with covenant not to sue

Page 12

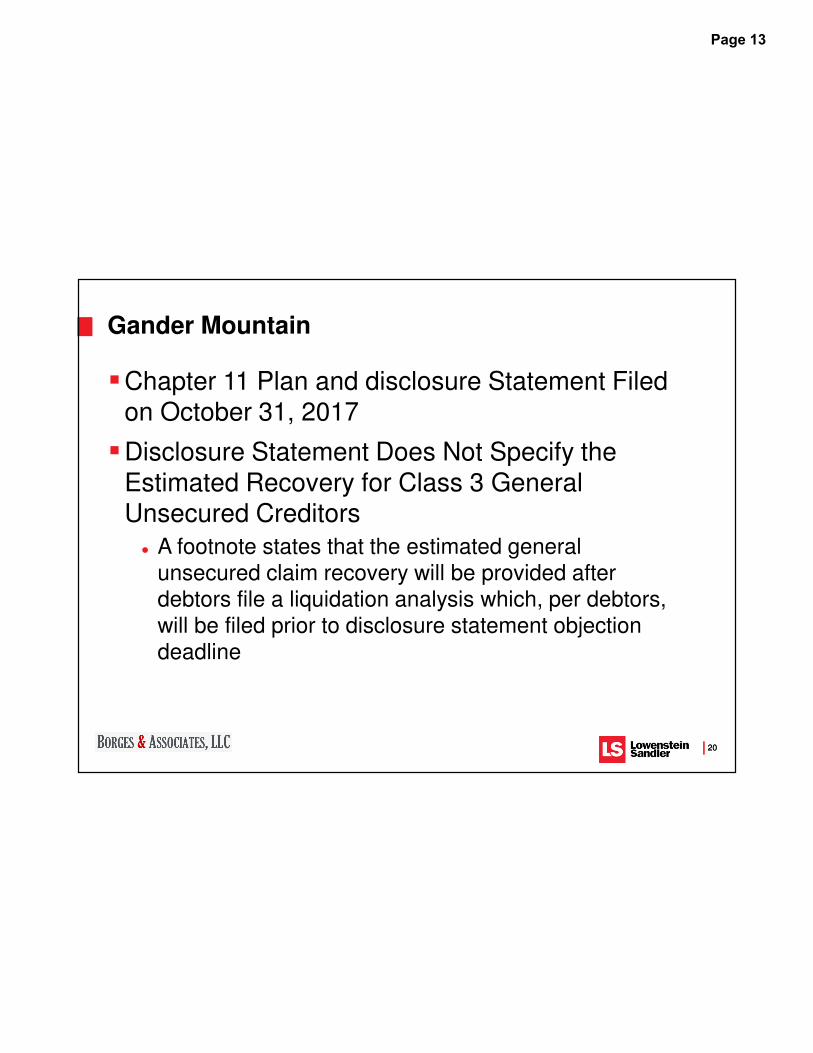

2020

Gander Mountain

�Chapter 11 Plan and disclosure Statement Filed

on October 31, 2017

�Disclosure Statement Does Not Specify the

Estimated Recovery for Class 3 General Unsecured Creditors

● A footnote states that the estimated general unsecured claim recovery will be provided after debtors file a liquidation analysis which, per debtors, will be filed prior to disclosure statement objection deadline

Page 13

PROTECTING/ELEVATING/

INVESTIGATING AND

PROSECUTING CLAIMS

Page 14

2222

Protecting/Elevating ClaimsThe Claims Waterfall

The Bankruptcy Code accords certain debt “priority” in payment over other debt:

i. Carve Out Claims. A portion of a secured claim that is “carved out” for the benefit of professionals and U.S. Trustee fees.

ii. Secured Claims. A debt is “secured” if the holder of the debt is entitled to look to specific property for its satisfaction. Debt may become secured by agreement (i.e., mortgage, security agreement, trust deed) or against the debtor’s will (i.e., attachments, tax liens). A debt is secured to the extent of the value of the estate’s interest in the property securing it. All other debt is “unsecured” debt.

iii. Super Priority Administrative Claims. Administrative claims that are paid ahead of other administrative claims. The Bankruptcy Code permits the court, under certain circumstances, to grant super priority administrative expense status to a debtor’s postpetition lender.

2323

Protecting/Elevating ClaimsThe Claims Waterfall

iv. Administrative Claims. Claims for the actual and necessary costs of preserving the estate, including professional fee claims, postpetition wages and salaries, postpetition taxes, postpetition rent and payment on account of goods received postpetition.

v. Priority Claims. Includes prepetition claims elevated in priority by the Bankruptcy Code, including claims for prepetition wages earned within 180 days of the bankruptcy, contributions to employee benefit plans, consumer deposits held by a debtor, and most taxes and claims arising from capital commitments to federally insured banks and other depository institutions. The Bankruptcy Code establishes a scheme setting forth the relative priorities between these “priority” claims.

vi. General Unsecured Claims. The prepetition claims of trade creditors, landlords, utility service providers.

vii. Equity Interest Holders.

Page 15

2424

Material Case Events Financing, Cash Collateral And The Budget - Continued

Postpetition Trade Credit

� The debtor may incur unsecured debt in the ordinary course of business. If it does so, such debt will be afforded administrative priority.

● When trade vendors ship goods and provide services postpetition,

the credit extended is entitled to administrative priority.

● Note, however, that administrative priority claims will be paid only

after:

i. secured claims,

ii. “super priority” administrative expense claims, and

iii. administrative claims of any superseding chapter 7 case.

� Risk of administrative insolvency – insufficient funds to fully pay all chapter 11 administrative priority claims

2525

Material Case Events Financing, Cash Collateral And The Budget � The First Major Test of Strength of the Parties in a Chapter 11 Case Often

Involves the Debtor’s Request for Approval of Postpetition Financing and/or Use of the Cash Collateral of its Prepetition Secured Lenders.

� The Court will Typically Hold an “Interim” Hearing within a Day or Two of the Bankruptcy Filing and a “Final” Hearing within 30 days after the Filing.

� Trade Vendors Should Pay Particular Attention to the Terms of the Proposed Financing and/or Use of Cash Collateral, because, among other things:

i. the sufficiency of financing will assist in your determination of whether or not to extend credit on a postpetition basis;

ii. you will want to ensure that the creditors’ committee is working to protect the rights of unsecured creditors so that they are not eviscerated in the first month of the case; and

iii. the various documents (orders, agreements, etc.) may include a timeline for the case with triggering events (i.e., sale within a certain number of days from the petition date).

Page 16

2626

Material Case Events Financing, Cash Collateral And The Budget - Continued

Postpetition Financing (a/k/a DIP Financing)

� The DIP lender may receive the following protections if it

can show that unsecured financing was not available:

● a “super priority” administrative claim (i.e., an administrative expense claim with priority over all other administrative expense claims);

● a lien on assets that were previously unencumbered; or

● a junior lien on encumbered assets.

- The Bankruptcy Code seems to indicate that the DIP lender

may receive only one of the above-mentioned protections.

Nevertheless, DIP lenders regularly receive all three.

2727

Material Case Events Financing, Cash Collateral And The Budget - Continued

Postpetition Financing (a/k/a DIP Financing)

� The DIP lender may also receive a “priming” lien (i.e., a security

interest that is “senior or equal” to an existing lien).

� In cases involving a “priming” lien or use of cash collateral, the debtor

will typically seek to provide the lender whose liens are being primed

or whose cash is being used with “adequate protection” (often in the

form of liens, fees and expenses and/or interest payments).

● The creditors’ committee and unsecured creditors generally should

carefully review the proposed adequate protection to ensure that it is

not excessive – after all, each dollar that goes to the prepetition

lender as “adequate protection” may come out of unsecured creditors’

pockets.

● Creditors’ committee should oppose granting of liens/superpriority

re: avoidance claims, such as preference claims

Page 17

2828

Material Case Events Financing, Cash Collateral And The Budget - Continued

� “Cash Collateral” is a Term Used in the Bankruptcy Code to Describe

Cash or Cash Equivalents in which in the Debtor and Another Party

Have an Interest, Usually a Lien. Cash Proceeds of a Lender’s

Collateral will Almost Always be “Cash Collateral.”

� If the Cash is a Prepetition Lender’s Collateral, the Debtor Needs

Authorization (from the Lender or the Court) to Use the Cash.

� The Party with an Interest in Cash Collateral is often Granted

“Adequate Protection” to Protect Against the Diminution in Value of

the Collateral.

● As with adequate protection provided to DIP lenders, creditors’

committees and unsecured creditors generally should ensure that

lenders are not provided with excessive protections in the form of

adequate protection from assets that would otherwise inure to the benefit

of unsecured creditors, such as preference claims.

2929

Material Case Events Financing, Cash Collateral And The Budget - Continued � Unsecured Creditors Should Carefully Review the Proposed Budget to Ensure

that the Lender is Providing Funding (Whether Through a DIP Loan or

Through the Use of Cash Collateral) Sufficient for the Debtor to Operate in

Chapter 11. This Includes, Among Other Things:

● Funding for administrative obligations, including sufficient funding for postpetition trade purchases and other administrative claims and rent;

● Funding for all professionals to be retained in the case;

● If the debtor seeks authority to make adequate protection payments, sufficient funding to make such payments; and

● Sufficient funding to pay all obligations pursuant to “first day” orders, including amounts owed to critical vendors, PACA/PASA/PPFPA vendors,

employees, etc.

� If the Budget is Ultimately Insufficient to Satisfy the Debtor’s Working Capital

Needs and the Lender has Succeeded in Obtaining a “Section 506(c) Waiver”,

the Debtor Will Not be Able to Surcharge the Lender’s Collateral for the Costs

of the Chapter 11 Case.

Page 18

3030

Protecting/Elevating Claims – Critical Vendors

� Generally, although a debtor may use property of the estate

in the ordinary course of business, it does not have the right

to pay prepetition claims.

� In certain situations, courts have permitted a debtor to pay

pre-petition claims to creditors whose goods and services

are essential to the continuation of the reorganizing

business, but who would refrain from doing future business

with a debtor without payment of their prepetition claims.

� Determination of whether a creditor is critical to a debtor’s

business is made on a case-by-case basis.

3131

Protecting/Elevating Claims – Critical Vendors - Continued

� Debtors often condition inclusion in a critical vendor program on an

agreement by the creditor to continue to provide goods or services on

terms better than or equal to those in effect prepetition.

● Terms are frequently negotiable.

� There are generally 3 factors courts examine to determine whether a

vendor is entitled to critical vendor status:

● It is critical that the debtor continue to deal with the vendor in

question;

● The debtor’s failure to deal with the vendor creates a risk of harm

or loss of economic advantage to the debtor’s estate that is

disproportionate to the vendor’s prepetition claim; and

● There is no practical or legal alternative by which the debtor can

cause the vendor to deal with it other than by payment of its

prepetition claim.

Page 19

3232

Creditors’ Committees – Overview

� Bankruptcy Code provides for the appointment of a

creditors’ committee in Chapter 11 cases.

� As a fiduciary representative of all unsecured creditors,

the creditors’ committee serves in the more substantive

roles of watchdog, consultant, and negotiator of the Plan

and asset purchase agreements.

� Subject to court approval, the creditors’ committee can

select its own counsel and financial advisors to help it

perform those functions, and these professionals are

paid not by the creditors but by the debtor’s estate.

3333

� Creditor is given a seat at the table to determine the debtor’s future

business operations – ability to negotiate sale of assets and/or plan.

� Creditors are provided confidential information with respect to the

debtor and its operations. (Committee members may not share this

information with other creditors or use that information in their role

as a creditor of the debtor).

� Most committees hold regular meetings by telephone if the parties

are geographically widespread.

� All reasonable expenses of Committee membership are paid by the

debtor.

� Participation in a committee provides committee members with a

unique opportunity to network with both the debtor and other

creditors involved in the industry.

Creditors’ Committees – Benefits of Committee Membership

Page 20

3434

� Usually, the creditors holding the largest unsecured claims are appointed (by the United States Trustee) to the creditors’ committee.

� However, U.S. Trustee will take into account other considerations, such as obtaining a diversity of perspectives by appointing different types of claimants: trade claims, landlord claims, governmental claims, employee claims.

� Creditors whose claims are insured or secured by a letter of credit might not be appointed to sit on a Committee.

� If you want to serve on a creditors’ committee, it is important to respond promptly to the solicitation of interest sent by the United States Trustee or otherwise make your interest known to the United States Trustee.

� In large cases an organizational meeting designed to select the committee is often held within the first one to two weeks after the case is filed, and well in advance of the official Meeting of Creditors, commonly referred to as the 341 meeting.

� Creditors may attend the committee organizational meeting by proxy.

Creditors’ Committees – Eligibility Requirements for Membership

3535

Creditors’ Committee – Powers

� Investigates the Acts and Financial Affairs of the Debtor

� Consults with the Trustee or Debtor Concerning

Administration of the Case

� Involvement Chapter 11 Financing/Use of Cash Collateral

� Involved in 363 Sale of Business Assets

� Participation in Formulation/Negotiation of Chapter 11 Plan

� Requests Appointment of a Chapter 11 Trustee based

upon Debtor Misconduct

Page 21

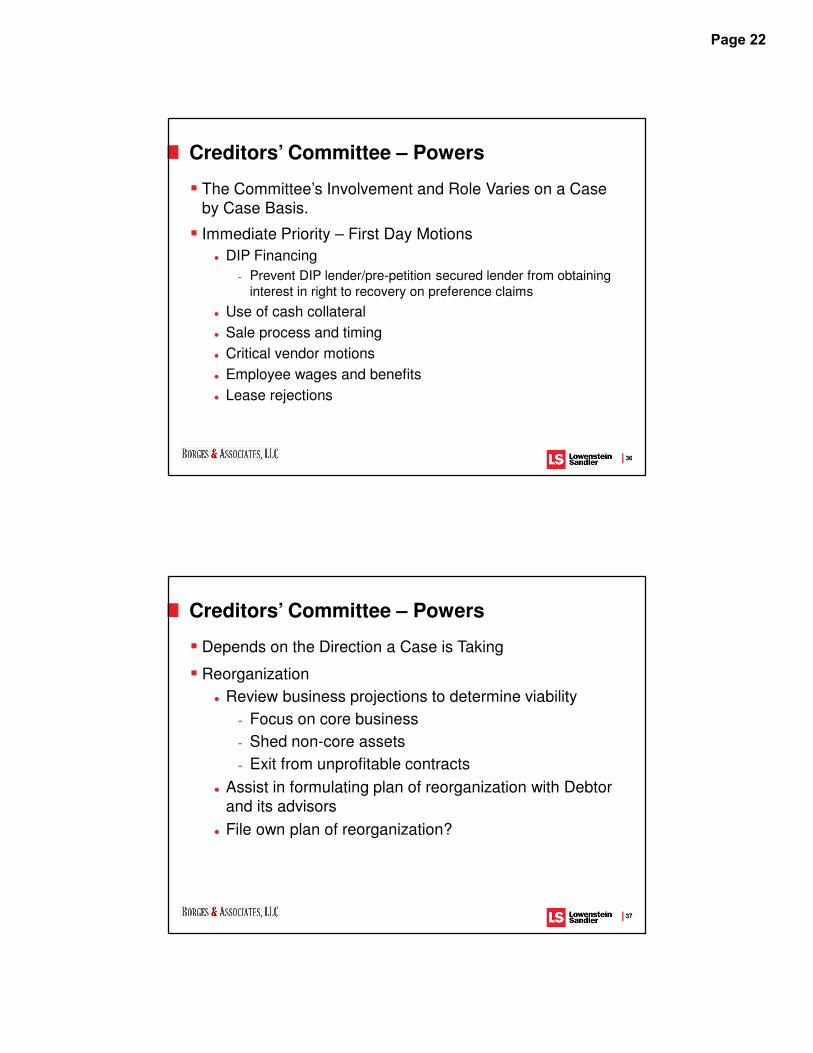

3636

Creditors’ Committee – Powers

� The Committee’s Involvement and Role Varies on a Case

by Case Basis.

� Immediate Priority – First Day Motions

● DIP Financing

- Prevent DIP lender/pre-petition secured lender from obtaining

interest in right to recovery on preference claims

● Use of cash collateral

● Sale process and timing

● Critical vendor motions

● Employee wages and benefits

● Lease rejections

3737

Creditors’ Committee – Powers

� Depends on the Direction a Case is Taking

� Reorganization

● Review business projections to determine viability

- Focus on core business

- Shed non-core assets

- Exit from unprofitable contracts

● Assist in formulating plan of reorganization with Debtor

and its advisors

● File own plan of reorganization?

Page 22

3838

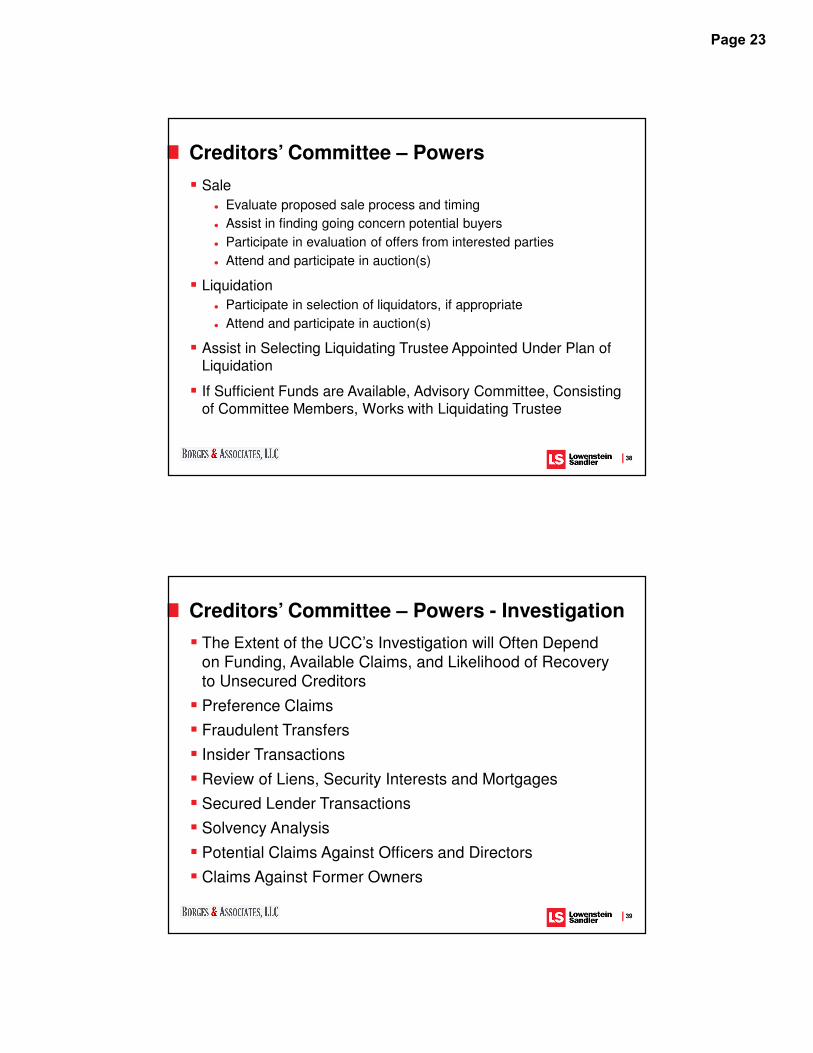

Creditors’ Committee – Powers

� Sale

● Evaluate proposed sale process and timing

● Assist in finding going concern potential buyers

● Participate in evaluation of offers from interested parties

● Attend and participate in auction(s)

� Liquidation

● Participate in selection of liquidators, if appropriate

● Attend and participate in auction(s)

� Assist in Selecting Liquidating Trustee Appointed Under Plan of Liquidation

� If Sufficient Funds are Available, Advisory Committee, Consisting of Committee Members, Works with Liquidating Trustee

3939

Creditors’ Committee – Powers - Investigation

� The Extent of the UCC’s Investigation will Often Depend

on Funding, Available Claims, and Likelihood of Recovery

to Unsecured Creditors

� Preference Claims

� Fraudulent Transfers

� Insider Transactions

� Review of Liens, Security Interests and Mortgages

� Secured Lender Transactions

� Solvency Analysis

� Potential Claims Against Officers and Directors

� Claims Against Former Owners

Page 23

PAYLESS SHOESOURCE

A BANKRUPTCY

SUCCESS STORY

Page 24

4141

Payless – A Bit of History

�Founded in 1956

�Built for the budget conscious family

�2016 sales - $2.3 billion

● North America - $1.9 billion in sales

- Down from 2015 sales of $2 billion

�2016 EBITDA - $95 million

�Franchise stores exist only in Africa, Asia and the Middle East

4242

Payless ShoeSource

�Publicly traded since 1962

�Taken private in 2012

�April 4, 2017 Payless Holdings LLC and 28 affiliated debtors filed for chapter 11 protection

�Not a Surprise!

�February, 2017 Moody’s Investor Services downgraded its outlook to “negative”

Page 25

4343

Payless – Chapter 11 Proceeding

�Attempted a “quick” turnaround without general

unsecured creditor support

� Initial Plan proposed de minimis distributions to

general unsecured creditors and substantial

releases to Plan Sponsors which included

lenders

● Creditors’ Committee opposed initial plan

4444

Payless – Chapter 11 Proceeding

� Creditors’ Committee Asserted Claims in the Hundreds of

Millions of Dollars Against Debtors’ Private Equity

Sponsors, Golden Gate Capital and Blum Capital and The

Debtors’ Directors and Officers

� Committee’s Allegations:

● Debtors’ payment of dividends to Golden Gate and Blum in 2013 and 2014 and related financing transactions that funded such payments

- After the 2012 LBO, the sponsors “siphoned over $400 million

out of the Debtors”

● Potential fraudulent conveyance and other claims

Page 26

4545

Payless – Successful Reorganization

� Negotiation among Plan Sponsors, Pre-Petition Lenders,

Debtors and Committee lead to consensual 5th Amended

“Pot” Plan

� Fifth Amended Plan Provides:

● Sponsors contributed more than $20 million

● Total Cash Pool to be distributed to creditors: $32.316 million

- Releases granted to Sponsors, individuals, lenders, etc.

● General Unsecured Creditors will receive cash payments of between 18% and 22%

● All preference claims against General Unsecured Creditors Waived

● Canadian Unsecured Creditors will receive 100%

4646

Payless Emerges

� AUGUST 10, 2017 – Payless emerged from bankruptcy

court protection

● More than 67- stores closed

● First of 14 retail companies who filed since the start of 2016 to successfully emerge from chapter 11

● Will continue “brick and mortar” stores

- Canada, U.S., Asia, Central America, South America and the

Caribbean

● Will continue online stores

● Expanding its Asia presence through franchise agreements

Page 27

TOYS R US

Page 28

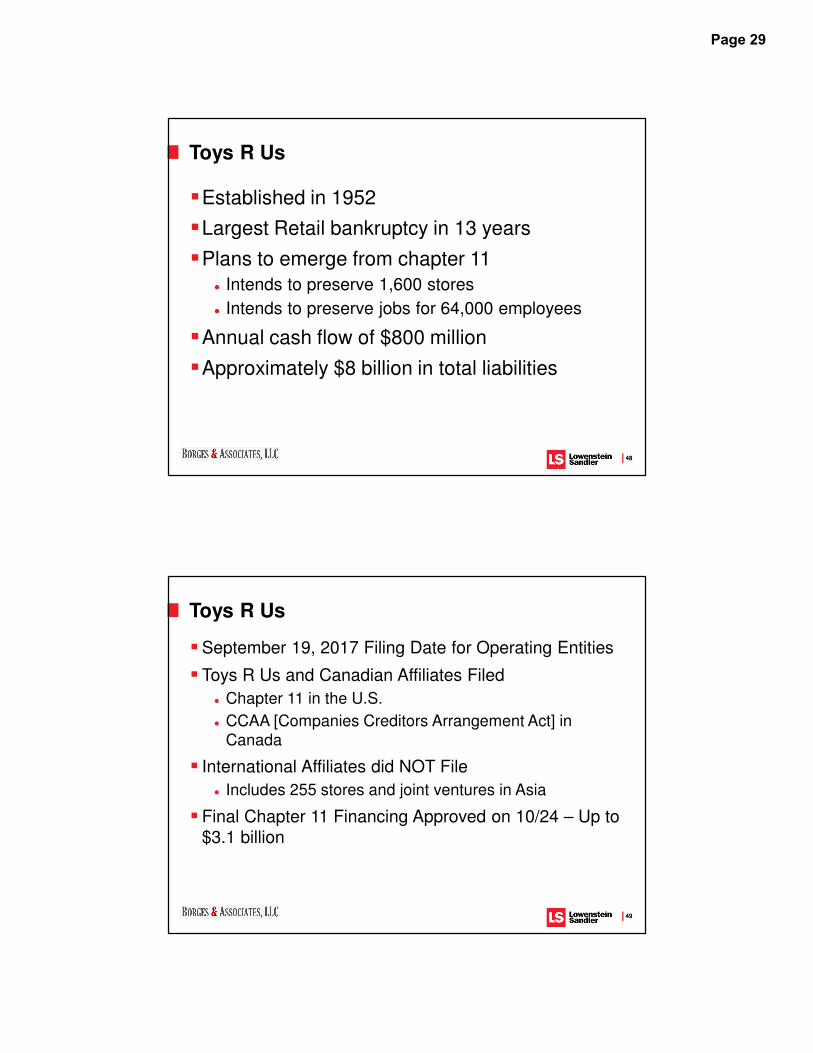

4848

Toys R Us

�Established in 1952

�Largest Retail bankruptcy in 13 years

�Plans to emerge from chapter 11

● Intends to preserve 1,600 stores

● Intends to preserve jobs for 64,000 employees

�Annual cash flow of $800 million

�Approximately $8 billion in total liabilities

4949

�September 19, 2017 Filing Date for Operating Entities

� Toys R Us and Canadian Affiliates Filed

● Chapter 11 in the U.S.

● CCAA [Companies Creditors Arrangement Act] in Canada

� International Affiliates did NOT File

● Includes 255 stores and joint ventures in Asia

� Final Chapter 11 Financing Approved on 10/24 – Up to $3.1 billion

Toys R Us

Page 29

5050

�9 person Creditors’ Committee Appointed 9/26/17● 4 Toy companies (including 1 specializing in

baby toys & products)

● 2 landlords

● 1 insurance company (credit insurer?)

● 1 bank

● 1 paper, packaging, office solutions company

Toys R Us

5151

� “Business as Usual”

● On-line sales continuing both “Toys-R-Us” and “Babies-R-Us”

● Per Toys R Us’ Counsel: “vendors back on normal terms”; “49 of top 50 vendors have returned to ‘normalized trade terms’”

● “ …transform the experience of coming into a Toys R Us bricks and mortar store and turn it into something that’s quite different and a lot more fun…”

� Cross-Border Protocol approved

● Harmonize and coordinate efforts

● Promote orderly and efficient administration

● Joint hearings may be conducted

Toys R Us

Page 30

5252

Toys R Us – Approved First Day Motions

�Pay shippers

�Pay Critical Vendors up to $325 million

�Pay 503(b)(9) Vendors● Up to $200 million on a final basis

�Pay Foreign Vendors up to $56 million

�Pay outstanding pre-petition orders to be delivered post-petition

�Nothing for Media Providers (unless Critical Vendors)

5353

Q & A

QUESTIONS?

Page 31

Wanda Borges, Esq.Borges & Associates, LLC

WANDA BORGES, ESQ. is the principal member of Borges & Associates, LLC, a law firm based in Syosset, New York. For more than thirty-five years, Ms. Borges has concentrated her practice on commercial litigation and creditors rights in bankruptcy matters, representing corporate clients and creditors’ committees throughout the United States in Chapter 11 proceedings, out of court settlements, commercial transactions and preference litigation. She is a member and Past President of the Commercial Law League of America and has been an Attorney Member of its National Board of Governors, a Past Chair and current member of the Bankruptcy Section, a past member of the executive council of its Eastern Region and is currently the Immediate Past Chair of its Creditors’ Rights Section. She is a member of several bar associations, including the American Bar Association and the American Bankruptcy Institute. Ms. Borges serves on its Board of Directors of the International Association of Commercial Collectors, of which her firm is an associate member. She is an internationally recognized lecturer and author on various legal topics including Bankruptcy Issues such as 503(b)(9) claims and preferences, the Uniform Commercial Code, ECOA, FCRA, antitrust law, and current legal issues such as Credit Card Surcharge issues and current proposed legislation that may impact trade credit grantors. Ms. Borges has authored, edited and continues to contribute to numerous publications including Thomson West’s Enforcing Judgments and Collecting Debts in New York, NAB’s book Out of the Red and into the Black, the BCCA’s Credit & Collection Handbook, The Financial Manager, the CLLA’s Commercial Law World Magazine. She has authored the treatise “Hidden Liens, Who is Entitled to What?” and NACM’s Antitrust, Restraint of Trade and Unfair Competition: Myth Versus Reality. She is a contributing author to NACM’s Manual of Credit and Collection Laws and Principles of Business Credit. She has co-authored The Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 – An Overhaul of U.S. Bankruptcy Law, also published by the NACM and her article has “Uniform Voidable Transactions Act (US) has been published by the British Law Journal Insolvency Intelligence. In November, 2010, Ms. Borges received the “Robert E. Caine Award for Leadership” from the Commercial Law League of America. In April 2015, Ms. Borges received a “Woman of Distinction” award from St. Catharine Academy, her high school alma mater. Ms. Borges has been included in the New York Super Lawyers – Metro Edition list (Bankruptcy & Creditor/Debtor Rights) each year since 2009..

Tel: (516) 677-8200, x 225 E-mail: [email protected]

Bruce S. NathanPartner, New York

Bruce S. Nathan is a partner in Lowenstein Sandler’s

Bankruptcy, Financial Reorganization & Creditors'

Rights Department. Bruce has over more than 35

years' experience in the bankruptcy and insolvency

field, and is a recognized national expert on trade

creditor rights and the representation of trade creditors

in bankruptcy and other legal matters. Bruce has

represented trade and other unsecured creditors,

unsecured creditors' committees, secured creditors,

and other interested parties in many of the larger

Chapter 11 cases that have been filed. Bruce also

handles letters of credit, guarantees, security,

consignment, bailment, tolling, and other agreements

for the credit departments of institutional clients.

Among his various legal recognitions, Bruce received

the Top Hat Award in 2011, a prestigious annual award

honoring extraordinary executives and professionals in

the credit industry. He was co-chair of the Avoiding

Powers Committee that worked with the American

Bankruptcy Institute’s Commission to Study the Reform

of Chapter 11 and also participated in ABI's Great

Debates at their 2010 Annual Spring Meeting, arguing

against repeal of the special BAPCPA protections for

goods providers and commercial lessors, and was a

panelist for a session sponsored by the American

Bankruptcy Institute. He is a frequent presenter at

industry conferences throughout the country, as well as

a prolific author regarding bankruptcy and creditors’

rights topics in various legal and trade publications.

Tel. 212.204.8686

Fax. 973.422.6851 E-mail: [email protected]

Education

� University of

Pennsylvania School

of Law (J.D., 1980)

� Wharton School of

Finance and

Business (M.B.A.,

1980)

� University of

Rochester

(B.A., 1976),

Phi Beta Kappa

Bar Admissions

� 1981, New York

© 2017 Borges & Associates, LLC and Lowenstein Sandler LLP