the role of state and market in economic development · the role of the state and the market in...

TRANSCRIPT

The Interaction of the State and the Market

In a Developing Transition Economy:

The Experience of China

Chunlin Zhang1

Senior Enterprise Restructuring SpecialistThe World Bank Office BeijingEmail: [email protected]

Revised Version June 20, 2002

Abstract

This paper assesses how the particular form of interactions between the state and themarket may have had its impact on China’s overall success in the past two decades ineconomic reform and development. In doing so, the question of development economics,i.e., the role of the state and the market in development, is discussed in a context oftransition economics. Some key components of China’s reform experience are examinedto illustrate the way the state interacts with market forces, including ownershiptransformation of people’s communes and state owned enterprises, regionaldecentralization, price reform, financial sector reform and capital market development,and bankruptcy regime. In interacting with market forces in some “transitioninstitutions”, the state seemed to have played positive roles in ensuring political andsocial feasibility of reform measures, supporting the market to achieve initialimprovement in efficiency, and maintaining the momentum of reform.

1 The author wishes to thank the organizers and participants of the workshops“Promoting growth and welfare: the role of institutions and structural change in Asia”held in Santiago and Rio de Janeiro in May 2002 for their valuable comments. The viewsexpressed in this paper are entirely that of the author and should be in no way interpretedas the views of the World Bank.

2

I. Introduction

The role of the state and the market in economic development has been constantly asubject of debate. While the debate is far from concluded, it seems clear that at least inthe field of economic policy making, the meaningful question is not one of “state ormarket”. Instead, it is very much about how the two can interact in such a way thateconomic development is promoted. From this point of view, China’s experience oftransition and development in the last two decades provides an interesting case to studywith. China differs from most other transition economies in that it is still a developingcountry, and from most developing countries in that it has experienced a transition from aSoviet-style central planning economy to a market economy, or more precisely, a“socialist market economy with Chinese characteristics”. Since the transition in Chinahas been a process of “crossing the river by touching the stones”, in which both the oldand new mechanisms are partial but have a role to play, it is interesting to see how thestate and the market interact during the transition process and how such interactionsimpact on development.

China’s modern history started in 1840 when the door of the closed empire was brokenup by British warships. In the following one hundred years or so, China sufferedmiserably from great internal strife and foreign exploitation. When the ChineseCommunist Party (CCP) succeeded in its revolution and came to power in 1949, China’sshare in global GDP was only about 5%, down from 33% in 1820 (Dahlman and Aubert,2001, p1). Blaming private ownership, market forces and international capitalism for thehardship, the CCP decided to rebuild the country by adopting a Soviet-style centralplanning model based on public (state and collective) ownership. From 1950-56, thewhole urban economy (accounting for around half of GDP and less than 15% ofpopulation) was nationalized, while the rural economy was collectivized. Marketmechanism was no longer allowed to exist in any significant sense. A wide range ofcentral planning mechanisms was transplanted from the Soviet Union, which also assistedChina to start its post-war industrialization with 156 key investment projects in early1950s. Despite the seemingly cooperative relationship with the Soviet Union in early1950s, overall international environment was such that the country’s door was closedagain to most parts of the world, from both inside and outside. In terms of the role of stateand market in development, China went to one of the extremes: only state, no market.

3

The implementation of this model, however, was never straightforward. Mainstreamcommunists led by late Chairman Mao Zedong had to engage in political and ideologicalcampaigns year after year to crackdown oppositions and fight against human nature. The“Cultural Revolution” in 1966-76 marked the extreme of such efforts. The “DisastrousTen Years” awakened those communists who put the welfare of the people anddevelopment of the nation before ideology, such as Deng Xiaoping, the paramount leaderof China in 1978-1997. It was recognized that economic development is not going to beachieved before the traditional communist ideology is abandoned to allow a role ofmarket forces and private initiatives. The philosophy that later guided China’s reformwas expressed by Deng in late 1970s using a thousand-year old Chinese proverb: “ a catis a good one so long as it catches mice, never mind it is white or black”.

The reform and opening up launched by Deng in 1978 has proved a phenomenal success.As Stiglitz (1999) noted, China’s growth record since 1978 is nearly unparalleled inhuman history. As shown in Figure 1 and Figure 2, during a period of 23 years since1978, China’s GDP increased by more than 26 times, from RMB362.4 billion (USD43.66billion) to RMB9593.3 billion (USD1155.82 billion). Per capita GDP in 2001 reachedRMB7537 (USD908.07), 19 times higher than that of 1978 (RMB379 or USD45.66).More importantly, China’s long period of rapid growth has been achieved withoutmaking dramatic inroads into poverty. It managed to reduce the number of people livingin absolute poverty (defined as living on USD1 a day or less) by over 200 million in aperiod of two decades (Stiglitz, 1999). The improvement of living standard of ordinaryChinese has been unprecedented in Chinese history.

In 2000, 51% of China’s GDP was produced by secondary industry, 33% by tertiaryindustry, and 16% by primary industry. In terms of employment, however, primaryindustry accounted for 50%; secondary industry and tertiary industry shared the rest(22.5% and 27.5%, respectively). China is clearly on its way in the transition from anagricultural economy to an industrial and service economy. The ownership structure ofthe corporate sector is shown in Table 1. The roughly equal shares of state ownedenterprises (SOEs) sector and private sector highlighted the fact that China is about halfway in its transition from a central planning economy to a market economy. The extent towhich China has integrated into the world economy is indicated by a 44.5% ratio of totalvalue of imports and exports to GDP in 2000, a sharp contrast to a ratio of 9.8% in 1978.Totally USD40.7 billion foreign direct investment (FDI) was utilized in China in 2000,equivalent to 10.3% of its total fixed assets investment.

[Insert Table 1 here]

China’s success is undoubtedly a success of the market: the reform and opening up havebeen a constant movement from the state to the market. Indeed, since the pre-reformsystem was at one extreme of state-market spectrum, the reform had to be market-oriented. The important fact, however, is that China is not the only economy that hasundertaken such a movement, but seems to have been more successful than others interms of economic development. This suggests that the direction of the movement is not

4

the only determinant of success. In the past decade or so, a huge body of literature hasbuilt up as economists tried to find out what are the others. For example, many tend toattribute China’s success to its gradualist approach of reform, while others emphasizedifference of initial conditions between China and other transition economies.

Without intending to be involved in this ongoing debate, this paper will try to assess howthe particular form of interactions between the state and the market may have had itsimpact on China’s overall success. In doing so, the question of development economics,i.e., the role of the state and the market in development, is discussed in a context oftransition economics, which is all about the transition from the state to the market.Specifically, some key components of China’s reform experience are examined toillustrate the way the state interacts with market forces, including ownershiptransformation of people’s communes and state owned enterprises (section II),decentralization (section III), price reform (section IV), financial sector reform andcapital market development (section V) and bankruptcy regime (section VI). Keyfindings are summarized in Section VII.

II. Partial Transformation of Ownership

At the outset of reform, the Chinese economy was dominated by public ownership. Inthe rural economy, land and other production assets were owned by People’s Communes(based in townships) and Production Brigades (based in villages). Each People’sCommune (PC) consisted of dozens of Production Brigades. Party secretaries andmanagers of Production Brigades were selected from local peasants by PCs, while that ofPCs themselves were appointed by county Party organs and governments. ProductionBrigades organized production activities according to government plan received fromPCs, sold their outputs to and bought their inputs from distribution entities run by PCs orother levels of the government. This system enabled the state to fully control the ruraleconomy, in particular, to set both amounts and prices of agricultural outputsprocurement to support its overall development goals.

In the urban area, state owned enterprises dominated. By 1978, SOEs accounted for 80%of China’s industrial output. Unlike a firm in the market economy, a pre-reform SOEassumed multiple functions. It was foremost a political institution, a cell of the party-statethat served as the carrier of the Party’s presence at the grassroots level. It was also a levelof state administration, exercising administrative control on behalf of the party-state. Interms of economic and social functions, a SOE was nothing more than a productionfactory of the super company owned and managed by the central or local planningauthorities, and a state agency providing social welfare to employees. SOEs had littleindependence and no separate legal identity. They received production quotas, guaranteedoutlets for products and the necessary resources from the budget to implement the plan.Whatever “profits” were made had to be remitted to the state budget. As the basic cell ofthe command economy, the SOE was responding to administrative orders. There was adirect state control over factory employees’ salaries, together with permanentemployment. (Tenev, Zhang and Brefort, 2002).

5

The systems of PCs and SOEs were designed to facilitate state planning and suppress therole of market forces. Ubiquitous state control over economic activities in PCs and SOEsmeant practical impossibility for them to respond to price signals in any significant sense.And incentive structures were such that they could not be profit-driven suppliers in themarket. It follows, therefore, that market forces could play no role before ownershiptransformation takes place in PCs and SOEs. The interesting question is what kind ofownership transformation to take place. The simple answer would be privatization.Private ownership would certainly be sufficient to allow market forces to replace thestate. However, political and social constraints that prevailed in China in the 1980sdictated otherwise. Since a complete privatization was simply not acceptable andfeasible, China was thus forced to search for compromise, which must be a kind ofownership transformation that allows a larger role of market forces on one hand, and ispolitically and socially feasible on the other. The reform that did take place in PCs andSOEs in the 1980s was such a kind of ownership transformation that might beconveniently viewed as partial and informal privatization.

Household Contract Responsibility System. In rural China, ownership transformation wasimplemented in early 1980s through a “household contract responsibility system”, inwhich each rural household signed a contract with its Production Brigade to gain therights of using certain pieces of collective land for certain years, and undertook to delivercertain amount of products to the state procurement system. This reform restoredtraditional household farming after two decades of collective ownership and PC system.In the sense of residual claim and residual control, the two key components of ownershipas defined by Grossman and Hart (1986), agricultural production was privatized. Privatefarmers were allowed to decide on what to produce and how, and retain whatever was leftafter costs, taxes, and contractual contributions are deducted from total output. This wasin sharp contrast with the PC system, which was characterized as one of “eating rice in ashared pot”, in which “it makes no difference if one works harder or not”. Given the factthat agricultural production in China was still characterized by heavy labor inputs withtraditional backward technology, such a change in incentive structure was sufficient togenerate enormous increase in output and income. In a matter of four years, China’sagriculture recovered from stagnation and reached historically high level of grain outputin 1984. This allowed a gradual liberalization of agricultural prices and sharp increase ininvestment of farmers in industries, which led to the phenomenal rise of township andvillage enterprises (TVEs). While it is widely noticed that China’s economic growth ismore attributable to new entry of non-state firms, of which TVEs are the most important,than reform of existing firms, the rise of TVEs would be clearly impossible without thesuccess of agricultural reform.

However, despite the success, the privatization of agriculture was, and is still partial: landhas not been privatized. And this is not insignificant. Without legally protected privateownership of land, under-investment by farmers’ in their lands has been an unsolvedproblem for over two decades. The government tried to alleviate the negative impact byextending the contracts to 15 to 30 years, without visible success. Since the populationsof villages are changing, the government has been forced to redistribute land use rightsamong households periodically to reflect the demographic changes, which made it even

6

more difficult to encourage long term investment in land. On the other hand, the absenceof a market for land prevented free flow of land among farmers, which tends to preventtechnological and structural improvement from taking place in private farms. (Wu, 1999,p131-32) However, these distortions and inefficiencies were not large enough to offsetthe positive impact of the reform. In addition, a rigid and government controlleddistribution of land use rights served to limit the scope of competition and its impact onincome distribution by preventing concentration of land ownership to a small number ofhouseholds, which happened frequently in the Chinese history. Politically, privatizationwithout changing land ownership has never been regarded as privatization even by themost conservative fractions of the society, and therefore contributed to political stability.

Managerial Autonomy and Earning Sharing. China’s SOE reform has been the leastsuccessful part of its reform program. In 2000, there were 191,000 SOEs in China, ofwhich 51% was losing money according to official statistics. However, given thedominance of SOEs in the urban economy at the beginning of the reform, and the factthat the pre-reform SOE system did not allow a role of market forces in any significantsense, it is also beyond any doubt that no reform could have succeeded had the SOEreform been a complete failure. So, how did the seemingly unsuccessful SOE reformcontribute to the overall success of the reform?

China’s SOE reform in the 1980s was characterized by managerial autonomy and earningsharing between the state and the “enterprise”, which essentially meant managers andworkers, or insiders, of SOEs. This reform strategy is better known in China as“delegating power and conceding profit (fang quan rang li)”. It was developed with thepolitical and social constraint that no privatization was acceptable. However, the strategywas also derived from the diagnosis that over-centralization of decision making powerand weak incentives of SOE managers and workers were responsible for their poorperformance. It was therefore believed as essential to transfer more decision makingpower to managers, and allow managers and workers to share the economic outcomes oftheir efforts with the state. In terms of changes in incentives, this was of the same natureas the contract responsibility system in the rural economy: part of the residual controlrights and cash flow ownership rights were privatized.

The start of the reform was marked by an experiment of “enlarging enterprisesautonomy” carried out by the CCP Sichuan Provincial Committee in October 1978 in sixSOEs. In May 1979, six central government ministries jointly carried out their ownexperiment in 8 large SOEs, which led to a State Council decision in July to enlargemanagerial autonomy of all SOEs. Together with the “enlargement of managerialautonomy” was a profit retention scheme introduced in July 1979 by the State Council.All SOEs which were “independent accounting units” and profitable were eligible toadopt the scheme. A fixed retention rate was set for three years based on parameters ofpast financial record, and the retained profit was supposed to be split into three envelopes(later known as “three funds”): “production development fund” for re-investment,“employees welfare fund” for public welfare of employees, and “employees reward fund”for bonus and other rewards. Although profit retention was intended to be only a limitedexperiment, it spread rapidly, and by the mid-1980, 6,600 state-owned industrial

7

enterprises, accounting for 60 percent of total industrial output and 70 percent of totalprofit of industrial SOEs, had instituted some form of profit retention.

In late 1986, the government made further decision to implement “contract responsibilitysystem” in SOEs. By the end of 1987, 80% of SOEs adopted one or another form ofcontract responsibility systems. The specific terms of the contracts varied substantiallyfrom case to case. The most commonly used ones are the following, expressed as formulaof total remittance requirement:

• A base amount + a sharing ratio x (total profit realized – target profit)• A base amount x (1 + a progressive annual growth rate)• A base amount fixed for certain years• A fixed target of loss reduction• “ Two guarantees and one linking”: enterprises guarantee a target amount of profit

and tax remittance, guarantee the implementation of technical innovation projects,and their total wage bill can be linked with total profit and tax.

SOE managers were given greater control over enterprise operations in return for meetingprofit remittance targets. Many contracts also gave the enterprises greater autonomy oversales and permitted managers to grant employees bonuses and hire contract workers. Inview of the terms of contracts, the contract responsibility system is an extreme form ofthe managerial autonomy and earning sharing approach. Subject to the legal ownership ofthe state and the desire of government agencies for power, contracting responsibilitysystem probably maximized the independence of SOEs from their owner in terms ofmanagerial autonomy and residual claim.

To the extent that ownership of a firm can be defined as the combination of residualclaim, or cash flow rights, and residual control, what happened in Chinese SOEs in the1980s was indeed privatization. However, it was again partial and informal. It was partialin the sense that what was privatized was only part of the cash flow plus a subset ofcontrol rights; only in rare cases did insiders manage to gain the entirety of cash flowrights and control rights. It was informal in the sense that the cash flow rights and controlrights received by insiders were granted by the other player of the game, the government,through administrative order or contract. The division of cash flow rights and controlrights between the state and insiders has never been explicitly defined by a law as adivision of legal ownership rights. In legal terms, it is still the state that owns the entiretyof the enterprise. Reflecting this fact, no matter how much of cash flow and controlinsiders were allowed to share with the state, the state always had the power to decidewith whom to share, i.e., the state has firmly retained the power of appointing anddismissing managers of SOEs.

This partial and informal privatization may have been efficiency enhancing at least in onesense. Suppose there was a strong demand for certain product, and it was surelyprofitable for factories to increase their production because of the potentially high pricegenerated by short supply, as what is typically found in a “shortage economy”. Withoutearning sharing and managerial autonomy, managers and workers of factories wouldnever have the incentives to increase their production, because it would add nothing to

8

their private income under the “sharing big rice pot” system. And even if they had suchincentives, they were handicapped in that they did not have the rights to make thedecision and the access to the needed inputs. The result could be nothing but thecontinuation of shortage economy and loss of income growth. The reform of earningsharing and managerial autonomy made it possible to avoid such efficiency loss. This isprobably the most important success of China’s SOE reform in the 1980s. SOEs couldhave performed much worse in the competition with non-state enterprises, and economicgrowth in China could have been much slower given the large share of resourcesoccupied by SOEs, had the pre-reform system been kept intact.

However, this approach could not have been an end of SOE reform because it wasseriously flawed in some fundamental aspects. First, it could provide incentives formanagerial performance only in an imperfect way. Managerial performance cannot beobserved directly. And commonly available indicators such as profit and sales are not a“sufficient statistic”. They reflect many other factors in addition to managerialperformance, and can be manipulated. Second, this strategy could privatize only profit,not loss. The primary reason for this failure is the wealth constraint of insiders. Variousattempts were made to alleviate this problem in late 1980s to “improve the contractingresponsibility system”. For example, managers and workers were required to providedeposit before being granted a contract. However, it was never sufficient to free the statefrom a situation of “head I win, tail you lose”, because the potential loss of state assetsthat could be brought about by actions of insiders was far too large in comparison withtheir personal wealth. This resulted in a mismatch of residual claim and residual controlwhen insiders were granted substantial control rights, and encouraged insiders toundertake riskier actions that a rational private owner of the enterprise would not.

These problems point to the main dilemma that reformers faced. If the state kept grantingautonomy and sharing profit with insiders, it could lead to insiders control of aconsiderable degree, and in effect an informal and partial privatization of control rightsand profit and a complete socialization of loss. On the other hand, if the state wanted toput insiders under control, the only means it could employ was still the old system, i.e.,re-centralization, or reinforcement of administrative control, because legal ownership wasnot changed. The actual course of reform in China during the period of 1978-93 wasindeed one of “hitting and reflecting” in a corridor of two hard walls: the pre-reformsystem of state run enterprise on one side, and insider control on the other. This gave riseto a corporate governance structure in most SOEs that was characterized by acombination of insider control and administrative intervention (Zhang, 1995, p34).

The informal and partial nature of the privatization of ownership rights, and therefore thepotential economic and social value that could be realized by putting insider controlunder control, has led to a fundamental failure of the SOE reform in the 1980s: thereform has basically failed to address the problem of politicization (in a similar sense asBoycko, Shleifer and Vishny 1993) or the multiple functions of SOEs. Despite all kind ofreform efforts to enlarge the autonomy of managers, SOEs remain cells of the “party-state economy”. Since the managers of SOEs are appointed and dismissed by the Party as“cadres”, it is unrealistic to expect them to concentrate on profit maximization and

9

economic efficiency, even though they themselves are sharing economic profit with thestate. The failure to de-politicize SOEs helped maintain an environment in which eventhose who really have entrepreneurial talents find it difficult to survive until they trainthemselves to become bureaucratic entrepreneurs or entrepreneurial bureaucrats.

To summarize, the ownership transformation of PCs and SOEs can be viewed as one caseof interaction of the state and the market. In the form of partial privatization, it improvedincentives, hardened budget constraints, and unleashed standard market forces, whichcombined to generate growth and raise efficiency. In the meantime, none of them wasdone in a complete way. State ownership and control was retained to certain degree toensure that the reform was acceptable to all fractions of the society, and the political andsocial shocks the reform brought about was within a manageable degree. The partialnature of the reform had its own cost, of course. However, in retrospective, the criticalpoint does not seem to be the fact that there was a cost. Instead, what has been critical isthat on the balance, the net gain from reform was large enough that further reform wasboth justified and supported.

III. Federalism with Political Centralization

As market-oriented reform started from a point of “only state, no market”, there is anatural question of incentives of the state. Given the fact that everything was undergovernment control, reform could only be initiated and carried out by the government, orat least with substantial government support. On the other hand, however, completegovernment control over economic, political and social life meant no reform would bepossible without loss of power on the government side. So, how could the government beexpected to lead a reform? When the government’s utility function is such that marketoriented reform generates net loss of its welfare, what follows logically is that a politicalchange must precede economic reform to put in place a pro-reform government. Thepolitical change China experienced in 1976 when Chairman Mao died and the “Gang ofFour”, the leaders of the left-wing extremelists who were the driving force of the CulturalRevolution, were arrested. However, it was managed as an internal political event withinthe CCP rather than a political revolution of the scale comparable with what happened inlate 1980s in the former Soviet Union and Eastern Europe2.

When reformers led by Deng Xiaoping took the power in 1976-78, the issue of incentivesof government became one of how the central government incentivizes localgovernments (provinces, prefectures, counties, and municipalities at each of the threelevels). Given the size and regional diversity of the country, it is not difficult to see how

2 In retrospective, China might have been more fortunate than other transition countries inthat such an small scale political change was sufficient to put in place a new governmentthat was capable to lead the reform, so that it was able to avoid the heavy economic andsocial cost that many other transition countries had to pay following large scale politicalrevolution. However, one might want to relate this to what the Chinese often call “tuitionfee” paid in the “Disastrous Ten Years”, in which the Party and the whole nation wereeducated.

10

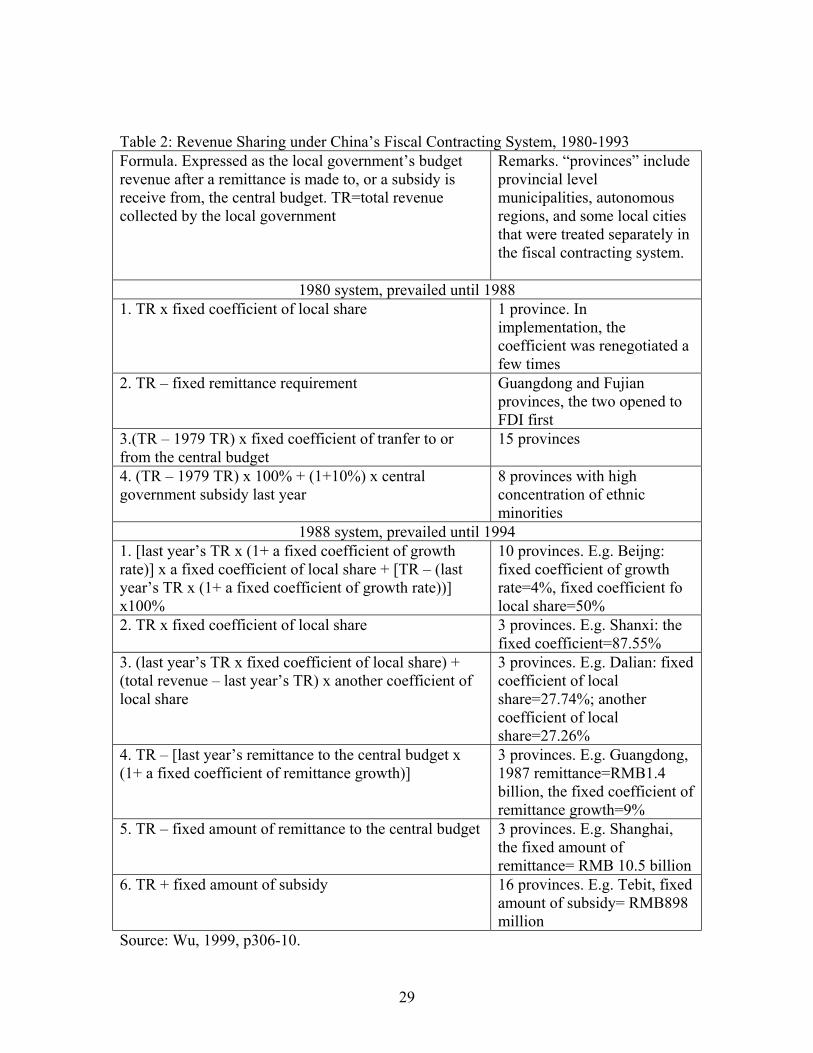

crucial this is to the success of reform. China’s approach to this problem was similar tothe one to ownership transformation of PCs and SOEs. A “fiscal contracting system” wasimplemented in 1980s to make local governments residual claimants, while moredecision making power was delegated to them as part of the decentralization process.This reform led to the emergence of a system of “federalism with politicalcentralization”, as Blanchard and Shleifer (2000) put it. Under the fiscal contractingsystem, better known in China by the nickname of “eating from separate kitchens” asopposed to the pre-reform system of “eating from a shared pot”, local governmentsentered into long-term fiscal contracts with higher level governments (Qian, 1999). Thenature of the contract varied across regions and over time. Table 2 shows the mainvariants of the contracts between central and provincial governments. All the formulawas applied after the division of expenditure responsibilities and the scope of “currentyear total revenue” were clarified. Despite the complexity in some cases, there is clearly acommon feature that local governments were made responsible for the revenueconsequence of their economic policies. This is especially comparable with the system ofmanagerial autonomy and earning sharing that the government implemented in SOEs.

[Insert Table 2 here]

This system is believed to have had positive impact on economic growth in the followingaspects. In terms of efficiency of decision-making, local governments have informationadvantage over the central government. This is so because a large part of the informationthat is needed in making economic decisions is idiosyncratic in the sense that it is aboutchanges in “particular circumstances of time of place” and by its nature cannot enter intostatistics and be conveyed to the central authority (Hayek, 1945). In the sense ofincentives, the reform strengthened local governments’ incentives and hardened theirbudget constraints, in a similar way as the managerial autonomy and earning sharingsystem did in the case of SOEs. With decentralized decision-making and strengthenedincentives, inter-jurisdictional competition was generated (Qian, 1999). In other words,market forces were brought into play.

The contribution of local governments to China’s economic success has been widelyrecognized. One of the most significant aspects has been its role in promoting andfacilitating the growth of non-state enterprises. China’s rapid economic growth has beenmade possible largely by new entry of non-state firms, especially TVEs. From 1978 to1997, China’s industrial output grew 27 times, while that of SOEs grew only 9 times.More than three quarters of the output growth was attributable to non-SOEs. In the sameperiod, China’s total employment and urban employment increased by 294 million and107 million, of which the contribution of non-state sector was 89% and 67%, respectively(NBS, 1998). While SOEs and PCs dominated Chinese economy at the outset of thereform, in 1998, the non-state sector accounted for 63% of GDP (IFC, 2000, p?).

However, inter-jurisdictional competition could not have had such a positive impactwithout the interaction with the state. A recent comparative study of China and Russia(Blanchard and Shleifer, 2000) highlighted this issue. It is recognized that the differencein economic growth between the two countries has come mostly from the growth of the

11

new private sector, and the behavior of local governments in both countries are importantto explain the difference. In China, local governments have actively contributed to thegrowth of new firms, while in Russia, local governments have typically stood in the way,be it through taxation, regulation, or corruption. What made Chinese local governmentsbehave differently, according to this study, was political centralization. In China, the CCPand the central government has been in a strong position both to reward or to punish localgovernments, as all the senior local officials are de facto appointed by the centralauthority. By contrast, transition in Russia has come with the emergence of a partlydysfunctional democracy, in which the central government has been neither strongenough to impose its views, nor strong enough to set clear rules about the sharing of theproceeds of growth. In this sense, inter-jurisdictional competition has been more like acontest, in which the state acts as a referee. Reward and punishment were not exercisedautomatically by market forces, as is the case in competition among firms. They wereexercised by the central authority of the state. Without such a role of the state, marketforces might have led local governments to maximize their welfare through differentmeans, such as blocking the development of private sector. In the words of Blanchard andShleifer (2000), “for federalism to function and to endure, it must come with politicalcentralization”.

However, even in China, federalism with political centralization has come with such aheavy cost that it has been criticized by some prominent Chinese reform economists andpublic finance experts. And indeed the criticisms are well justified. For example, despitepolitical centralization, inter-jurisdictional competition has led to strong local protectionand fragmented domestic market, even when the country is opened to internationalmarket. Fighting against local protection is still high on the agenda of the centralgovernment, as is evidenced in its report to the National Peoples’ Congress (theparliament) in early March 2002. The fiscal decentralization was also seen as highlyproblematic and dysfunctional by public finance experts, who believed that it distortedresource allocation, generated regional inequality, and undermined the centralgovernment’s fiscal policy (Qian, 1999). In 1994, a major package of comprehensivereform changed the central-local fiscal relationship again. However, although eight yearshas passed since then, China’s fiscal system reform remains an unfinished agenda. Fromthis point of view, federalism with political centralization is best viewed as a “transitionalinstitution” rather than “best practice”. The crucial point to note is that the particular wayof interaction between the state and the market made it fit much better to “the particularcircumstances of time and place” than any other best practice institution.

IV. Dual-Track Pricing: “Growing out of the State”

In terms of interaction of the state and the market, China’s unique approach to marketliberalization, the dual-track pricing, provides another interesting case, in which the formof interaction can be characterized as “growing out of the state”, following BarryNaughton’s (1995) famous book “Growing out of the Plan”.

In the absence of market, it was the state that set prices in the central planning economy.In the case of China, state pricing accounted for 94.4% of agricultural products and 97%

12

of total retail sales in 1978 (NBS, 1998b, p71). Obviously, market forces would not playany role despite of ownership transformation in PCs and SOEs, and decentralization, ifthe pricing mechanism remained the same. However, similar to complete privatization,given the distortions in relative prices resulted from decades of government pricing, theconstant threat of inflation, and limited progress in terms of ownership transformation inPCs and SOEs, a complete and quick price liberalization in early 1980s was regarded aspolitically unacceptable and economically unachievable, mostly for fear of inflation.Instead of totally abandon the old regime, reform had to be initiated from somewhere init. During 1978-84, while agricultural reform was the top priority of the government, andSOE reform was in the early stage, the government concentrated its efforts in “adjusting”prices, i.e., to reduce distortion within the framework of government pricing. Forexample, as part of the agricultural reform, state procurement prices of agriculturalproducts were raised by 25% on average in 1979. However, as ownership transformationand decentralization unleashed the natural forces of growth especially in the non-statesector, by mid-1980s, it became clear that mere adjustment of prices was not adequate.From 1978 to 1984, the share of non-SOEs in industrial output increased from 22% to31%. Even SOEs found it increasingly difficult to operate with administratively setprices, as the managerial autonomy and earning sharing arrangement injected profitmotivation, albeit limited, into SOEs, which tended to drive them to buy and sell inresponse to changes of market supply and demand.

Started from 1985, a dual track pricing system was implemented. In the rural sector, thefarming household was assigned the obligation to sell a fixed quantity of grain to the stateprocurement agency under the contracting responsibility system, and the price remainedadministratively determined. However, subject to fulfilling this obligation, it was free toproduce and sell whatever it considered profitable, at prices determined in the market.Thus, two prices were created for one product: one determined by the state, another bythe market.

In the urban sector, a quota of production materials of industrial enterprises was set upbased on 1983 actual. SOEs were secured to receive production materials supply from thestate at planned prices so long as their demand was within the quota. For any above quotademand, they had to purchase in the market at prices determined by supply and demand.For producers, the same regime applied. Within-quota output was purchased by the stateat planned prices, and above-quota output could be sold in the market. The emergence ofthis “market track” made it possible for non-SOEs to survive and grow without beingcovered by the state-run distribution network. What happened in the following years wasthat the coverage of the “planned track” stayed the same, while that of the market trackgrew. For example, the state procurement of domestically produced grains between 1978and 1988 remained essentially fixed, while there was almost a one-third increase in grainoutput. In the industrial sector, the same thing happened. For coal, the principal energysource, the planned delivery was increased somewhat from 329 million tons in 1981 to427 tons in 1989, but the market track increased from 292 million tons to 628 tons in thesame period. In case of steel, the share of planned allocation fell from 52% in 1981 to30% in 1990. Since the planned track was more or less frozen, the economy was able to

13

grow out of the plan on the basis of market track expansion fueled by both non-state andstate sector growth. (Qian, 1999).

While dual track pricing was adopted, full liberalization was also implemented whereverit was feasible. For example, prices for meats, seafoods, eggs and vegetables wereliberalized in 1985, though the degree of liberalization varied across regions andproducts. For some product in some region, price ceiling was imposed to curb inflation.In 1986, prices for 7 major industrial consumer goods, including bicycle, black-&-whileTV set, refrigerator, washing machine, and textile products were also liberalized. (NBS,1998b, p68-69).

The most significant advantage of dual track pricing was that it introduced real marketprices and market allocation of resources in the very early stage of reform, and createdconditions that allowed rapid growth of the non-state sector, without incurring the cost ofpolitical and social shocks that would be brought about by a complete and quick priceliberalization. While economic growth was generated, the dual track system itselfevolved as the market track outgrew the planned track.

However, again, this benefit did not come as free lunch. The cost of long lasting dualtrack system was particularly high in that it created a vast hotbed for corruption in the1980s. The opportunities of corruption is obvious, as the plan track for inputs conferredinstant profits upon the favored purchaser upon reselling quota inputs in the free market(Woo, 2002). For example, at some point of time in late 1980s, the market price for steelwas six times higher than the planned one, which made some storekeepers of steelcompanies millionaires. In 1988, Deng Xiaoping himself attempted to “crash through thegate of price reform” by liberalizing prices in a big-bang manner, but was forced to abortit by panic purchases in the market. The widespread corruption contributed to thedeterioration of the political and social atmosphere of reform, which eventually led to thetragic event in June 1989. After reform was re-launched in 1992, price liberalization wasimmediately implemented in 1993-94. By 1997, 85% of agricultural outputs, 95% ofretail sales, and 96% of production materials had been traded at fully liberalized marketprices. (NBS, 1998b, p71).

V. The Financial System with the State as a Primary Intermediary

The combined reform efforts in the field of ownership transformation, regionaldecentralization, and price reform, together with the growth of the non-state sector led tothe emergence of a market for goods and services (goods market). Even SOEs changedtheir behavior in 1990s from “going to the mayor” (asking government for help) to“going to the market” (finding a market niche to survive). However, goods market alonedoes not make a market economy. For market forces to allocate resources, goods marketmust function jointly with factor markets, for example, capital and labor markets. In thisregard, interaction of the state and the market is again an important feature of China’sreform. While the goods market has been largely developed, though not fully yet, theallocation of financial resources is still dominated by the state. China’s financial systemis characterized by the strong role of the state as a primary intermediary.

14

In a simple setting, a market economy can be viewed as two sectors, households andfirms, linked by three markets: goods market, labor market and capital market. Capitalmarket in particular is responsible to mobilize and distribute savings from the householdsector to the most efficient usages in firms. The central planning economy eliminated thethree markets but could not eliminate the two sectors. While firms were all publiclyowned, households remained private. A natural challenge to the central planning systemwas therefore the mobilization and allocation of savings by the state. In the case of China,the solution was found within the question. Since neither goods market nor labor marketexisted, the state took their place in allocating goods and labor, which enabled it tonationalize savings and replace the capital market.

Firstly, the replacement of the goods market by the state enabled it to distort the relativeprices of agricultural and industrial products. The distorted relative price became thus amajor vehicle to transfer savings from the rural household sector to the state ownedindustrial sector (World Bank 1997, p9). When the state purchased agricultural productsfrom PCs at lower prices and sold industrial products at higher prices, the so called“scissors difference” resulted in an implicit transfer of income from rural households tothe state. Part of the income that could have become private savings of rural householdshad relative prices not been distorted was transferred to the state sector in forms of lowercost and higher revenue of SOEs. Thus, as Lardy (1983, p101) observed, in the pre-reform era, prices were set by the government “largely to generate industrial profit, andthus government revenue”. His study found that after early 1950s, agriculturalprocurement and retail price policy were used to enable the state to generate significantresources through the profits of light industry, which was a source of 29% of all statebudgetary revenue during 1950-77(Lardy, 1983, p127, 126). The low relative prices offood grains he found (Lardy, 1983, p114, 119) also imply lower labor cost and higherprofit in the whole SOE sector.

Secondly, the replacement of the labor market by the state also enabled it to distort theprices of urban labor. This was done in the form of suppressed wage rates of SOEemployees. It has been well known that workers in the state sector before the reformreceived only very low and hardly changed wages (Table 3), which left them unable tobuild up long-term savings. The part of income that could have been distributed toworkers and added to their private savings was collected by the government in the formof profit remittances from SOEs, which increased the government budget revenue andsavings. Of course, various social services provided by the government or SOEs, such ashousing, pension, medical care, education, job security, etc., tended to increase budgetexpenditure, decrease budget revenue and thus reduce government savings. However, thissystem also served to maximize government savings since it enabled the government toeffectively control the level of expenses of social services and keep it as low as politicallyfeasible.

[Insert Table 3 here]

15

In doing so, the state played a role of intermediary in that it raised funds from householdsector through distortion of prices of products and labor, and allocated funds throughcentral planning and budget allocation. Private savings were suppressed to the minimum.In 1978, per capita bank deposit, by far the dominant form of private financial assets, wasonly RMB21.9, equivalent to 50 kg rice. The share of the government and enterprises innational savings, according to one statistical study (Guo and Han, 1991), was as high as88% in 1978.

However, the market-oriented reform in the 1980s undermined the foundation of thissystem. Ownership transformation in PCs and SOEs and price reform substantiallyeliminated the distortion in goods and labor market, by allowing a sharp increase inagricultural prices in relation to prices for industrial products on one hand, and looseninggovernment control over wages and particularly bonus on the other. The pattern ofnational income distribution among government, enterprises and households was changedin favor of households. In particular, budgetary income from SOEs kept falling,contributed to the overall decline of the share of fiscal revenue in GDP. From 1978 to1995, fiscal revenue as a percentage of GDP dropped by 24 points, from 31.2% to ahistorical low of 10.7%. Of which about 15 points can be attributed to the decline ofbudgetary income from SOEs (NBS, 2000, pp256-7). As a result, savings were privatizedin the sense that the share of private households in national savings rose sharply, from12% in 1978 to 56% in 1995, according to some estimate (Wu, Xiaoling and others,1998).

A fundamental mismatch then emerged. On one hand, private households became themain source of external finance for the corporate sector, on the other hand, a substantialpart of the corporate sector and the whole financial sector were owned by the state. Howcould the private savings be channeled to the corporate sector? One option would beprivatization of SOEs, state owned banks and non-bank financial institutions, incombination with a complete liberalization of capital market. Again, this was not whathappened. The government chose to maintain its ownership monopoly in the financialsector, mainly through state owned commercial banks (SOCBs), which accounted forover 70% of financial assets in China in 1990s. In the meantime, stock market wasallowed to develop under extensive government control. As a result, allocation of capitalin China since early 1990s has been done by a combination of government orders andmarket forces.

Project approval. As a legacy of the central planning economy, government approval ofinvestment projects has been one of the key instruments for the state to allocate capitalamong competing usages. In the pre-reform era, since almost all investments werefinanced by budget funds, the government was able to completely control the allocationof capital by review and approval of almost all large investment projects. Despite twodecades of reform, government review and approval has not been phased out. The StateDevelopment and Planning Commission and its local counterparts are the key agencies inreviewing and approving investment projects. Large projects are approved by the StateCouncil. In comparison with the pre-reform system, there are two key changes though.First, the government decision now is based on information collected from a better

16

functioning goods market as well as the international market. Second, depending on thesource of finance, investors are now given more power to decide. This is often describedas the government “digs the holes” and investors “plant the trees”. Banks, localgovernments, enterprises and foreign investors are not supposed to invest in projects thatare disapproved by the government, however, they do not have to invest in those that areapproved by the government.

Bank lending. Since SOCBs controlled the bulk of household savings, intervention inbank lending decisions has been another key instrument the state holds in allocatingcapital. In 2000, RMB471.1 billion household income, or 5.3% of GDP was depositedwith banks. Total medium and long term lending increased by RMB396.3 billion,equivalent to 12% of total fixed assets investment. Formal credit plan used to be the keychannel through which the government exercised control over bank lending decisions. Inan annual credit plan, the government laid out guiding principles of lending for banks tofollow. This system was not abolished until 1998. Government appointment of bankmanagers is also a critical channel of government intervention. Before 1998, managers oflocal bank branches were all appointed by local party committee and government, whichwas a major reason why loans were often lent to loss making local enterprises, mostlySOEs. To the extent that SOCBs are commercialized and lending decisions areindependent, market forces have played an increasingly significant role in guiding banklending decisions. However, there are other constraints. For example, most lendingdecisions, esp. those made by local branches, are still collateral-based. Good projectswithout collaterals are unlikely to receive bank loans. The key reason for this is thathuman resources of SOCBs are such that they do not have the adequate institutionalcapacity to make lending decision based on cash flow projection.

Stock market. China established its stock market in 1990 by opening two stock exchangesin its two major southern cities, Shanghai and Shenzhen. Table 4 shows where theChinese stock market was at its ten- year anniversary. The small amounts of total fundsraised in the market and market capitalization of listed companies in comparison withGDP and fixed assets investment indicated its limited role in capital allocation. Furthermore, government control over the market has been so severe that it is hard to say thatcapital has been allocated by market forces. Until recently, all initial public offerings(IPOs) had to be approved by the government. In the earlier stage of development, IPOquotas were allocated to central government ministries and local governments. It wasmade explicit that the stock market was supposed to “support SOE reform”. In late 1990s,companies who applied for IPOs were even required to take over a loss making SOEbefore being approved. Most companies listed in the market were formerly SOEs. Whena SOE conducts an IPO, it is corporatized first, with the state holding the majority stake.The state shares are not sold in the IPO; instead, new shares are subscribed by newinvestors. Only new shares issued to individual investors are tradable in the market. Othershares, including state owned shares and shares owned by legal entities such as otherSOEs are non-tradable.

[Insert Table 4 here]

17

While banks and the stock market are the two main channels through which householdsavings are transferred to the corporate sector, a substantial part of household savingswent to the corporate sector as direct investment. The main form is equity investment inprivately owned enterprises, mostly small and medium ones. Since investments of privateenterprises tend to be in small size and therefore less regulated by the government,market forces play a much more significant role in terms of capital allocation.

Apart from household savings, the next most important part of national savings is savingsof enterprises, mainly retained earnings. According to one estimation, enterprises savingsaccounted for 17.2% of GDP or 42% of national savings in 1995 (Wu, Xiaoling andothers, 1998). SOE managers and their immediate supervisors in the government jointlyhold the power to allocate their retained earnings, subject to constraints such as projectapproval.

Putting together, capital allocation in China is dominated by a financial systemcharacterized by the role of the state as the primary intermediary, as shown in figure 1.There are five basic channels for savings to be transferred to the corporate sector:

• Channel (1): A part of the national income that could have been distributed amonghouseholds was retained by the state with the help of administratively determinedprices and wage rates and became budget revenue. It was then invested in enterprisesand resulted in state owned equity (L1), which are essentially assets owned by thestate budget on behalf of all Chinese citizens (A1).

• Channel (2): Households deposit part of their savings with state banks and thusbecome holders of debt claims against the state banks (L2), which are their privateassets (A2).

• Channel (3): Households invest part of their savings in equities of enterprises that aretransformed from wholly state owned enterprises into joint stock companies (L3),these equity holdings become their private assets too (A3).

• Channel (4): Overseas investors participate in the ownership structure of former SOEs(L4) by acquiring shares or forming joint ventures (A4).

• Channel (5): Households invest their savings in private firms, TVEs, acquire smallSOEs and turn them into joint stock cooperatives in which all employees hold sharesof their firm. These investments are recorded as equity on the balance sheets of thosenon-state enterprises (L5) and become another form of private assets (A5).

The role of the market has been increasing, but is still limited. Such a halfway house hascreated a number of serious problems for the economy. First, the financial system isburdened with huge amount of non-performing loans. According to an estimation madeby a central bank researcher, the total cost of restructuring China’s financial sector couldbe as high as RMB2.5 trillion3, or 22% of 2001 GDP. Since the state monopolizes thefinancial sector, it has to bear the entirety of this cost. As a result, the sustainability ofgovernment debts is affected. Second, the dominance of state ownership has resulted inan unbalance between debt finance and equity finance. While the state is the owner of

3 South China Morning Post, October 24, 2000

18

191,000 enterprises, it does not have the financial resources to make substantial equityinvestments. On the other hand, private savings cannot be channeled into theseenterprises as equity investment due to the under development of capital market andinstitutional capacity. As a result, they are forced to rely on bank loans to finance thoseinvestments that would have been supported by equity finance in a more developedcapital market. Under-development of capital market has also negatively affected thegrowth of those private enterprises which need equity capital to grow but do not haveaccess to the stock market. In 2000, China’s bank deposits were equivalent to 151% of itsGDP, much higher than countries such as Korea (66.6%), Thailand (85.4%), Brazil(15.5%) and Chile (45.7%). (World Bank, 2001).

The existing combination of the roles of the state and the market in allocating capital is areflection of current status of reform. Why has the state kept such a large role in capitalallocation while it has basically allowed the goods market to play a full role? There aregood reasons to argue that capital market development and financial reform could havebeen much faster had the government adopted different policies. For example,commercialization of the banking sector could have been faster had the party and thegovernment allow the management of state owned commercial banks to concentrate oncommercial objectives such as profit and risk, and pay less attention to politicalobjectives. The stock market development could have been healthier had the governmentnot required it to serve the need of SOEs.

However, even with perfect government policies, the development of capital market, andtherefore the withdrawal of the state, could not have been much faster, due to somepractical constraints. One of such constraints is the development of a social safety net.The efficiency of capital allocation can not achieved without serious social consequencesin a transition economy such as China, and when the social safety net is not adequate, it ispractically difficult for the government to manage the transition if market forces areallowed to play a much larger role than they have been. We will come back to this pointin the next section.

Another practical constraint of great significance is institutions. The speed of capitalmarket development simply cannot be accelerated without limit, because buildinginstitutions takes time. Even writing new rules takes a great deal of time. China did nothave a company law until 1994, commercial banking law until 1995, and securities lawuntil 2000. However, even more time consuming is capacity building. Take theaccounting and law professions as an example, departments of accounting and law wereabolished in universities during the Cultural Revolution. And even when they existedbefore that, they were supposed to train accountants and law workers serving the need ofthe central planning economy and its political system. Chinese universities started to re-establish these two departments only in mid-1980s, and courses were restructured toserve the need of a market economy much later. While the demand soared as thetransition went on, the growth of supply was constrained. As a result, the services ofthese two professions have been in constant shortage both in terms of quantities andqualities. For example, until recently, one did not need a law degree in order to be ajudge. Many judges were retired members of the People’s Liberation Army. The first

19

national exam for qualification of judges took place only in March 2002. Existinglawyers were required only recently by the government to read for master degree in law,or to quit the profession in five years. The accounting industry is also constrained by lackof qualified accountants. This contributed to a creditability crisis when scandals involvingaccounting professionals were disclosed one after another by the media in the past twoyears. In some cases, for example, fabricated financial statements were produced byyoung and educated accountants but signed by their old colleagues who wereapproaching retirement and apparently had no future in the market. A recent surveyconducted by the National Accounting Institute covering 102 accounting firms found thatonly 17.7% of the firms believe their recent auditing reports did not include falseinformation.

The under-development of institutional investors provides another example. A few yearsago, the government realized difficulty to develop a more efficient stock market with aninvestor based dominated by retail investors, most of whom for example could hardlyunderstand financial statements of companies. It was then decided that “extra-ordinarymeasures” should be taken to allow institutional investors develop at “extra-ordinaryspeed”. However, despite the government efforts, the role of institutional investorsremains small in international standard. In 2000, for example, the total assets ofinstitutional investors as a percentage of GDP was only 5.6% in China, compared with18% in Thailand, 42.7% in Brazil and 84.2% in Chile (World Bank, 2001). And role ofthe nascent fund management industry in promoting capital market development has beenunder question when its involvement in market manipulation and other frauds weredisclosed by the media.

Of course, the constraints of capital market development do not automatically justify thecontinuation of a large role of the government. It could be the case that the governmentdoes even worse than what the nascent capital market would have done. In a moretheoretical sense, even the constraints of institutional capacity building can be by-passedif the government allows foreign control in banks and opens the capital markets toforeign investors. However, it is hard to predict what would have happened in thisparticular time and place should the government have adopted such policies.

VI. Industrial Restructuring: the Government-led Bankruptcy Process

One of the functions of the goods market is to divide enterprises into winners and losers.In the central planning economy, every enterprise produced in response to governmentorder, and there was not such an issue as being unable to sell its products. Accordingly,SOE managers did not need to worry about the market of their products. Even when dualtrack pricing system was implemented in the 1980s, the economy was still one of“shortage economy” and most enterprises did not find difficult to sell their extra-quotaoutputs. However, all these were changed by the development of goods market in late1980s and early 1990s. By mid-1990s, competition in goods market had beensignificantly intensified. More and more products were found over supplied, and the“shortage economy” was widely regarded as a history. Reflecting this change, theperformance of SOEs deteriorated substantially, calling for major scale industrial

20

restructuring. As shown in figure 2, total loss made by loss-making industrial SOEs hadnever exceeded 10% of total profit made by their profit-making counterparts before 1988.However, this ratio climbed to 66% in 1997.

In a well functioning market economy, when inefficient enterprises are singled out bygoods market competition, the capital markets and labor market will work together tomake sure these enterprises are either liquidated or restructured. Bankruptcy process,including liquidation and reorganization, plays a key role in this regard. In China, theunbalanced development of goods market and capital markets have meant that nobankruptcy of SOEs could be possible before the government played a central role.

Compared with laws such as the company law and securities law, China was quite earlyto establish its bankruptcy law. A Trial Bankruptcy Law for State-Owned Enterprises waspassed in 1986 and became effective in 1988. To cope with bankruptcy cases of non-stateenterprises, the Civil Procedures Law introduced in 1991 rudimentary provisions on thebankruptcy of legal persons in general, and the Company Law in 1994 added provisionson voluntary liquidation. However, the period from 1988-1993 saw only 277 bankruptcycases per annum, negligible in comparison with the total number of SOEs, which stoodover 300,000 at that time. By the time the new round of reform was launched in 1993,bankruptcy remained a subject government officials, managers and workers all feared totalk about. “Birth without death” was identified by the government as one of theobstacles that blocked the way for SOEs to transform themselves into players of a marketeconomy.

Bankruptcy of SOE was difficult mainly for two reasons. First and the most importantone was of course its social impact. However, the social impact of bankruptcy is, to alarge extent, a function of two variables, the mindset of workers and adequacy of thesocial safety net. In early 1990s, both variables were extremely unfavorable. For decades,workers had been educated that bankruptcy is something specific to capitalism, and theyare guaranteed lifetime employment under socialism. None of them had ever thoughtabout the possibility of being laid off, not to mention to get themselves prepared. Neitherdid the government. Unemployment insurance system did not exist until mid-1980s, andwas hardly functional in early 1990s. In such an environment, for bankruptcy of any SOEto take place, the government had to make sure employees are well consulted andfinancial resources are made available for compensation. Indeed, the 1986 bankruptcylaw requires the government to take responsibility in securing the living standard ofunemployed workers before they find new jobs, leaving the question of how for thegovernment to answer.

The second difficulty was also related to the availability of financial resources, but for adifferent reason, i.e., recapitalization of banks. When a SOCB lent to a SOE, and the loanhas turned into non-performing, everything could remain fine if the SOE stays there. Tothe bank, it was good enough to tell the government in its balance sheet that so muchmoney was lent to certain SOE, though not repaid. However, if the SOE is liquidated, theamount of the loan has to be deducted from the bank’s total assets, which leaves a hole tobe filled with new money. In particular, when bankruptcy of SOEs takes place in a large

21

scale, banks themselves may run into bankruptcy if they are not recapitalized, given theirlow capital adequacy ratio. However, since banks are state owned and no privatization isacceptable, it has to be the government who makes available sufficient financialresources to recapitalize banks, before bankruptcy of SOEs becomes a real option. In1995, 37% of the 300,000 SOEs were reported as insolvent in accounting terms in thatthe book value of their assets fell short of liabilities. This provides a rough indication howlarge the scale of bankruptcy could be. Before mid-1990s, there was no regular source offinance within the fiscal system that could be used for recapitalization of SOCBs.

In 1994, realizing the urgency of implementing the bankruptcy law among SOEs, thegovernment formulated a set of policies to deal with the two difficulties mentionedabove. First, it was stipulated that the proceeds of assets sales in liquidation must be usedto pay a specified amount of compensation to unemployed workers before any payment ismade to creditors. Second, the loss SOCBs incurred in SOE bankruptcies was allowed tobe written off with their own reserves. Given the ad hoc nature of these policies, theirimplementation was restricted to selected SOEs in selected cities, and a ceiling wasimposed on the amount of debt write-off. Starting from 1994, the government organizedan experiment, known as “capital structure optimization program (CSOP)” in over 100industrial cities. The write-off ceiling was translated into quota, which was distributed toeach city.

Such a policy-based bankruptcy regime gave rise to a dominant role of the government.A World Bank (2001) report described the typical steps of a government-led bankruptcyprocess under this regime.

(i) The management of a distressed SOE jointly with the relevant sector bureau underthe local government and in agreement with the mayor’s office comes to considerbankruptcy as a potential option. Several factors figure prominently in theirdeliberations:

• The firm’s inability to pay workers and pensioners, increasing difficulty in getting itsbanks to roll over credit, and its losses and consequent lack of tax payments;

• Whether worker and retiree entitlements could be settled from liquidation proceedswithout substantial municipal contribution, or whether another firm has been or willlikely be found that is willing, with some moral suasion and incentives, to take overthe assets as well as the workers and their entitlements;

• The likely militancy of the employees, in light of the local social strains throughalready high unemployment;

• Whether the firm uses land that could serve attractive development purposes; and

• Whether approval of debt write-off can likely be obtained from Beijing for the localbranch of the main creditor bank, given the write-off ceiling.

(ii) The plan to pursue bankruptcy by using part of the write-off quota that themunicipality expects to get this year is then discussed with the local branch of therelevant SOCB. The application for write-off quota under the CSOP is launched to the

22

central government. The application is reviewed together with more than a thousandothers by a temporary taskforce. The taskforce takes into account the merits of the caseand also seeks a certain balance of quota in terms of provinces, sectors, banks, andcurrent policy prerogatives. The emerging list gets fine-tuned in discussion with theSOCBs, and formally approved.

(iii) The firm who made it into the list then files for bankruptcy at the local People’sCourt with formal endorsement by the local sector bureau, as required by the bankruptcylaw. The court applies a somewhat flexible balance sheet test, and verifies the sectorbureau consent prior to starting bankruptcy proceedings. In larger cities, the local courtcommonly has a group of judges that handle all bankruptcy cases and have thus gainedsubstantial experience. The role of the court is largely limited, however, to pronouncingdecisions taken by the Liquidation Commission (LC), the counterpart of liquidator in theChinese bankruptcy law. The court-appointed LC consists usually of representativesfrom various municipal government agencies and the central bank branch. An official ofthe local government often heads the LC. The old SOE management commonlycontinues managing the SOE or maintaining its assets until liquidation is completed.

(iv) After the bankruptcy declaration, substantial creditors are notified and invited topresent their claims. Next, valuations are done by valuation enterprises sponsored bylocal government agencies, including land valuations by a valuator affiliated with theLand Bureau. It seems that the value of the land use right often happens to be foundroughly commensurate with the worker and retiree entitlements. (In this case, the localacquirer of the land use right will not be burdened, beyond the local social needs, bypayments to the estate that end up with a nationwide bank and other out-of-towncreditors.) Eventually a creditor meeting is held, with typically few if any trade creditorsshowing up and the main purpose being to confirm officially the consent of the localbranch of the relevant state bank. Although the Bankruptcy Law has some clauses oncourt-supervised reorganization, they are rarely used. The Law allows application forsuch reorganization only to the SOE or its owner organs, and those parties had anywayalready upfront decided in favor of bankruptcy and against merger despite the fact thatthe latter is also eligible to debt write-off quota.

(v) Liquidation commonly takes one of two forms:

• “Whole takeover” is a bulk sale of the assets. In this case, all the assets including theland use right, together with most workers, “rehabilitation” costs of laid-offemployees, and pension claims are taken over by another firm. Since the acquirer isseen as taking over the burdens of employing these workers and paying the retirees,the value of their total entitlements is subtracted from the asset value upon purchase.Since the land use right is often valued comparable to these entitlements, and otherassets are of little value, little cash changes hands.

• In the case of unbundling the assets, the city takes back the land use right and sells itin some way or another, for example, to a local development company. The proceedsare used to pay pensions and labor rehabilitation costs. Again reflecting priorvaluations, often little additional cash is obtained. Other assets are offered at auction,

23

for instance at a local Property Rights Transaction Center. Often, though, they get nooffer at or above their valuation and hence remain unsold for years, until a specialpetition is launched to higher authorities for permission to sell such a state assetbelow valuation.

It is not difficult to find out how flawed this regime is. With strong presence of localgovernments, which are the parents of debtor SOEs, and given the priority granted toemployees over creditors, the bankruptcy process provides little protection to creditors.To debtor SOEs, on the other hand, bankruptcy became a temptation rather than a threat.Local governments and SOEs found it a convenient way of getting rid of heavy debtburdens. Since the SOCBs owned by the central government are always the largestcreditors (2/3 in typical cases), bankruptcy was often used as one tool to extract implicitsubsidy from central budget by local governments and their SOEs.

However, the point here again is that this regime has been a transitional institution ratherthan a best practice. It has achieved two results. First, SOE bankruptcy has since thenbecome part of normal economic life in China. Table 5 shows the recent data. Second, themindset of SOE workers has been changed. Being laid off is no longer somethingunusual. Indeed the total labor force of the state sector has been downsized by 28% from1995 to 2000, while the size of the total labor force increased by 14%, as shown in table6. Although these have been achieved at heavy cost in terms of distortion of thebankruptcy system, it is again not so clear if there was better alternative. However, it isnow much more clear that this transitional institution should be phased out as soon aspossible. On one hand, the growth of the non-state sector has created a strong and urgentdemand for a unified bankruptcy regime. On the other hand, social security systemreform has made substantial progress in the past few years that a standard bankruptcysystem can be implemented in the SOE sector without major social risk. China starteddrafting a new bankruptcy law in 1995 when the ad hoc policies were implemented. Thenew law is scheduled to go to first reading in mid-2002 by the National People’sCongress.

[Insert Table 5 and Table 6 here]

VII. Concluding Remarks: Role of the State in a Transition to Market

From the point of view of development, China’s success in the past two decadesdemonstrates the scale of gains an economy may obtain when market forces are allowedto play a fundamental role in allocating resources. The shift from the state to the market,or the transition from a central planning economy to a market economy, however, is notsimply shift to “less state, more market” or “no state, only market”. Instead, its successrequires an active role of the state. The first and simplest thing for the state to do in thetransition is to take active actions to stop doing certain things it did before. Market forcescould not play any role before private individuals replace the state in a wide range ofeconomic activities. Second, the state needs to transform its role from a replacement ofthe market to a supporter of the market. At the minimum, the state must provide some

24

basic public goods such as protection of property rights and regulation of the financialmarket in order for the market to play a role.

This paper adds a new dimension to this issue. In a transition economy such as China,where the general environment of reform is such that a gradualist approach is inevitable,the state can play an important role in making some transitional institutions functioningby interacting with the market. In view of the examples provided in this paper, it seemsthe state plays the following roles in these transitional institutions.

(i) Ensure political and social feasibility of reform measures. Many thesetransition institutions are results of political compromise. A significant role isreserved for the state partly to make the reform measures acceptable to mostor all fractions of the society.

(ii) Support the market to achieve initial improvement in efficiency. Compromiseor political and social feasibility would be pointless if the role of the state issuch that no improvement can be achieved in terms of economic efficiency.Therefore, the interaction between the state and the market in thesetransitional institutions must ensure that the functioning of market forces issupported, or at least not blocked, by the state. Once initial improvement isachieved, urgency and conditions are often created for further reform, orfurther withdrawal of the state.

(iii) Maintain the momentum of the reform. One of the largest risks of thegradualist approach is that the transitional institutions are turned intopermanent. This is because transitional institutions create their ownconstituencies, i.e., the vested interest groups whose welfare lies in theimperfection of the transitional institutions. When the reform is entrenched inthe halfway house, the heavy cost that is always associated with transitionalinstitutions becomes net loss because the time in which the transitionalinstitutions are useful has passed. In this context, the state must play theleading role in pushing forward the reform by introducing more market forcesand abandon the transitional institutions.

In a developing transition economy such as China, the central issue of economic policymaking lies in the balance among policy goals of three dimensions: reform, development,and stability. Reform, or the transition from the state to the market, is of course thefundamental source of momentum for development, and stability is maintained onlywhen economic efficiency is raised and development is promoted. However,development and stability also have their impact on reform. No rational reform issustainable without a minimum degree of social and political stability and a minimumspeed of development and growth. This entails difficult tradeoffs: from time to time onegoal has to be sacrificed in favor of another. Transitional institutions such as thosediscussed in this paper are all this kind of compromises.

In a tradeoff situation where reform is sacrificed to serve goals of development andstability, policies often appear to be inconsistent with basic principles of economics andundermining fundamental elements that make a market economy functioning. This often

25