the strategic corporate investments handbook

TRANSCRIPT

i

The Strategic Corporate Investments Handbook

The Strategic Corporate Investments Handbook

David Whittaker

EUROMONEY

BOOKS

Published byEuromoney Institutional Investor PLCNestor House, Playhouse YardLondon EC4V 5EXUnited Kingdom

Tel: +44 (0)20 7779 8999 or USA 11 800 437 9997Fax: +44 (0)20 7779 8300www.euromoneybooks.comE-mail: [email protected]

Copyright © 2014 Euromoney Institutional Investor PLC

ISBN 978 1 78137 267 8

This publication is not included in the CLA Licence and must not be copied without the permission of the publisher.

All rights reserved. No part of this publication may be reproduced or used in any form (graphic, electronic or mechanical, including photocopying, recording, taping or information storage and retrieval systems) without permission by the publisher. This publication is designed to provide accurate and authoritative information with regard to the subject matter covered. In the preparation of this book, every effort has been made to offer the most current, correct and clearly expressed information possible. The materials presented in this publication are for informational purposes only. They reflect the subjective views of authors and contributors and do not necessarily represent current or past practices or beliefs of any organisation. In this publication, none of the contributors, their past or present employers, the editor or the publisher is engaged in rendering accounting, business, financial, investment, legal, tax or other professional advice or services whatsoever and is not liable for any losses, financial or otherwise, associated with adopting any ideas, approaches or frameworks contained in this book. If investment advice or other expert assistance is required, the individual services of a competent professional should be sought.

The views expressed in this book are the views of the author and do not reflect the views of Euromoney Institutional Investor PLC. The author alone is responsible for accuracy of content.

Note: Electronic books are not to be copied, forwarded or resold. No alterations, additions or other modifications are to be made to the digital content. Use is for purchaser’s sole use. Permission must be sought from the publisher with regard to any content from this publication that the purchaser wishes to reproduce ([email protected]). Libraries and booksellers and ebook distributors must obtain a licence from the publishers ([email protected]). If there is found to be misuse or activity in contravention of this clause action will be brought by the publisher and damages will be pursued.

Typeset by Phoenix Photosetting, Chatham, Kent

v

Contents

Acknowledgements xiiiAbout the author xivIntroduction xv

1 Strategy and corporate growth 1Strategic planning 1Efficient strategic planning approach 1

Mission, goals and objectives 1Position audit 3Corporate appraisal 3Environmental analysis 5Competitor analysis 5Options available 6Evaluation 6Performance measurement 7Conclusion 7

Marketing strategies 7Product positioning 8

Post-investment financial and performance management 10Capital budgeting 13Other areas of investment appraisal 17

Monthly cash flows 17Capital rationing 17Unequal project lives 20Weighted average cost of capital 22Post-monitoring the corporate investment 23

Review and control 29Organic versus acquisitive growth 29Organic growth 31The new product or business development process 32

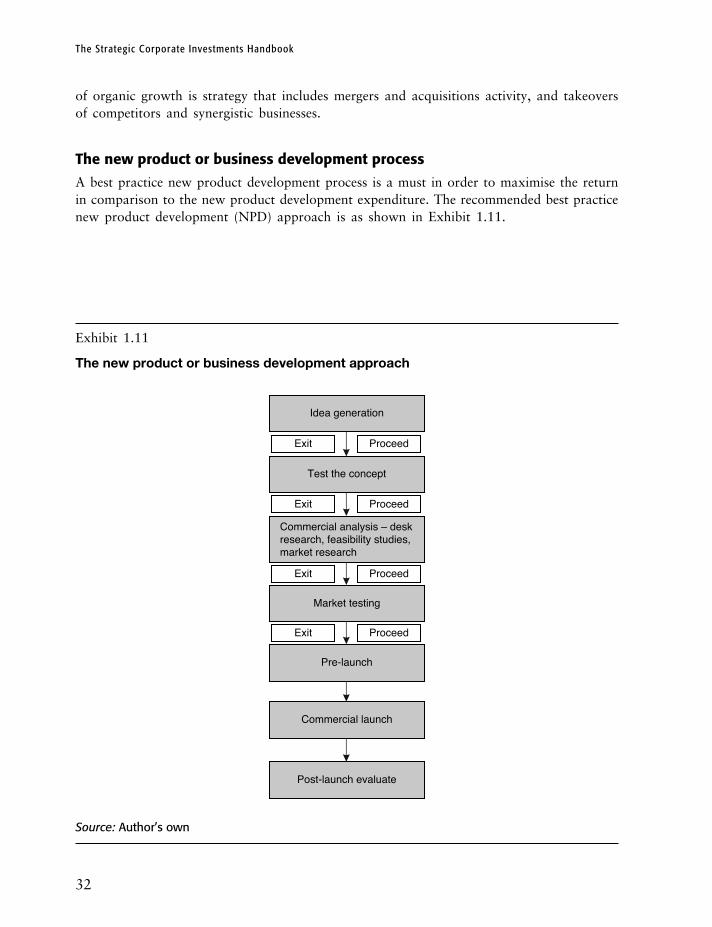

Idea generation 33Test the concept 33Commercial analysis 33Market testing 34Pre-launch 34Commercial launch 35Post-launch evaluation 35

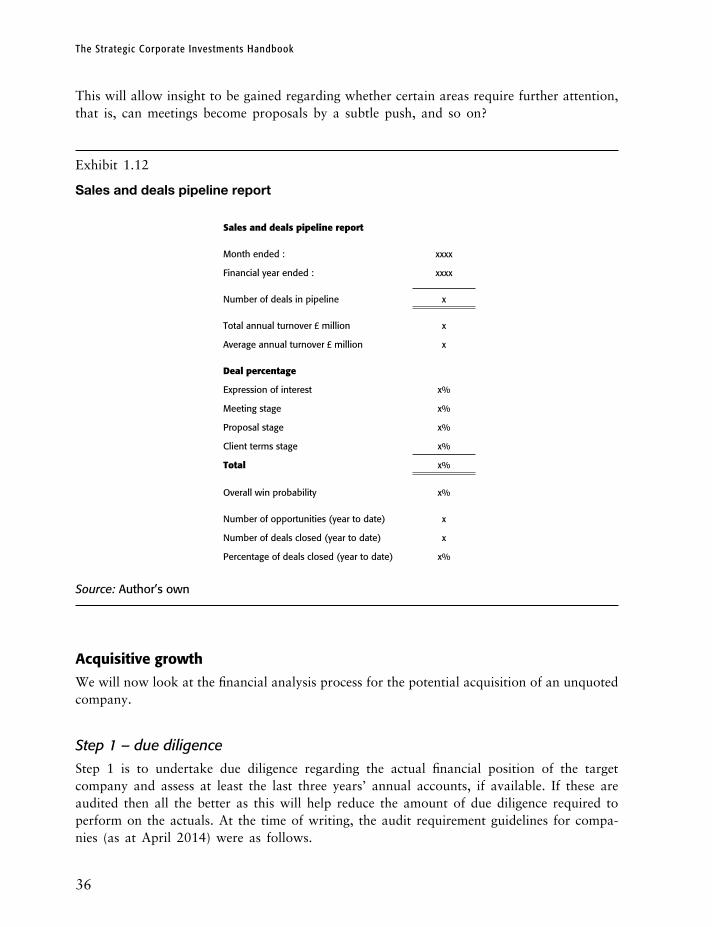

Sales pipeline management 35

vi

Contents

Acquisitive growth 36Step 1 – due diligence 36Step 2 – acquisition value 37

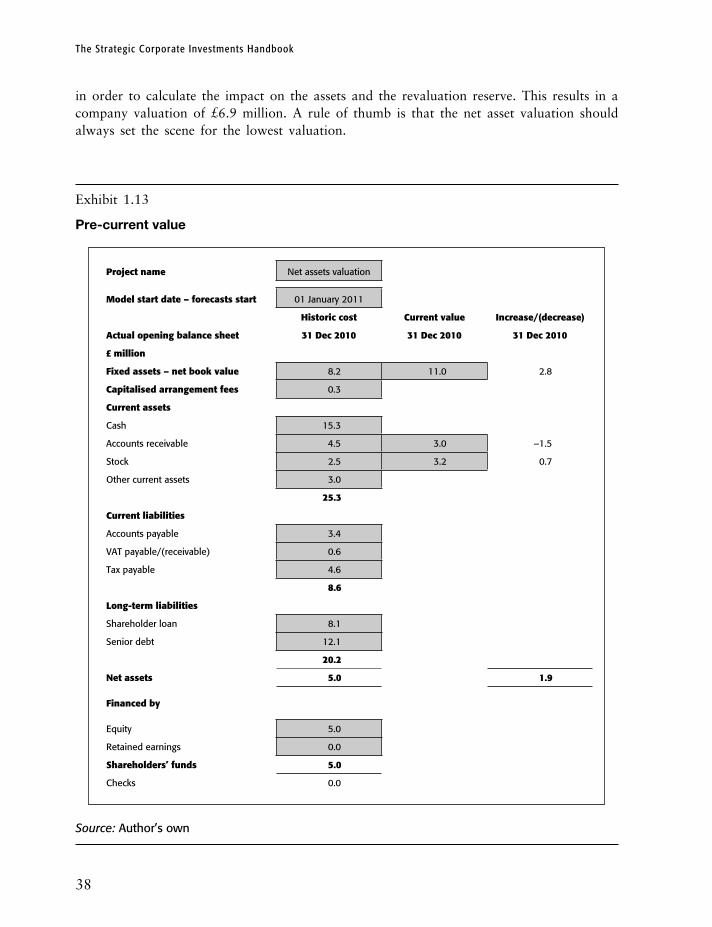

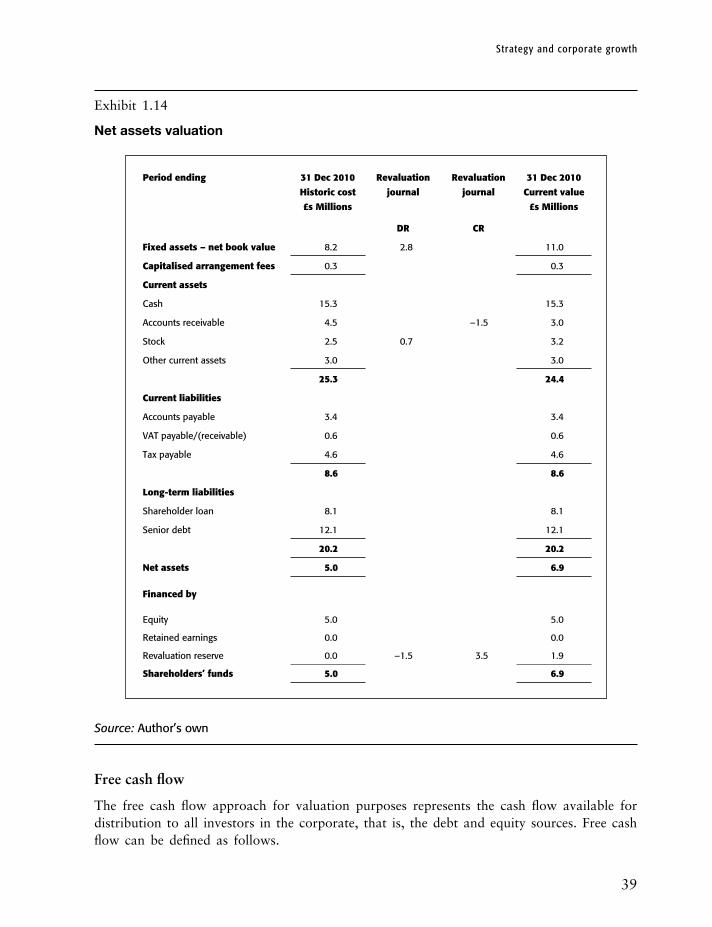

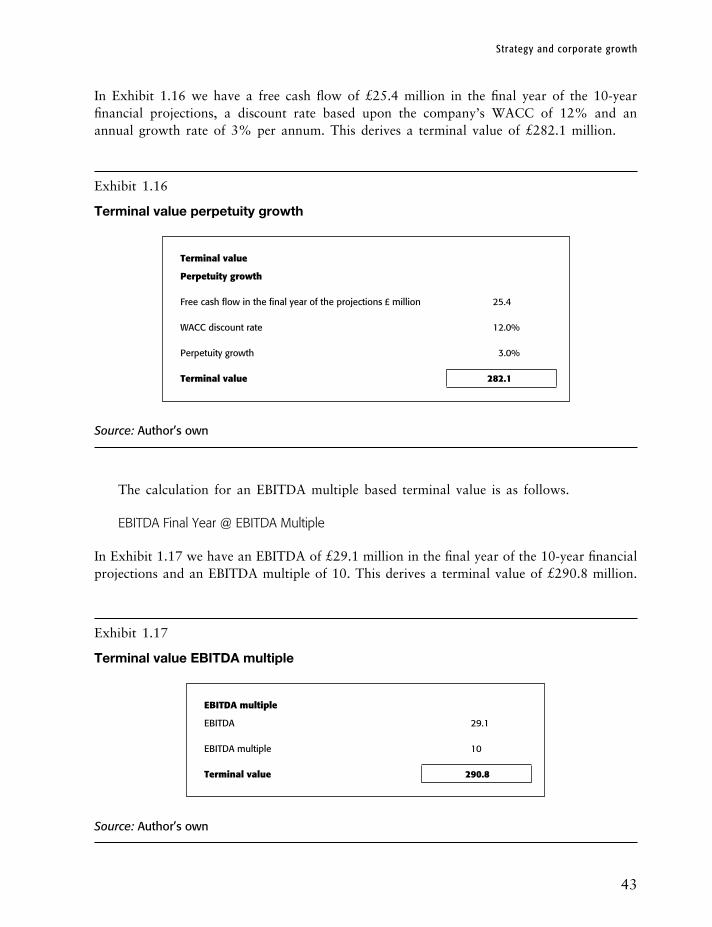

Asset-based valuations 37Free cash flow 39Multiples-based approaches 40Terminal value 42Enterprise value 44

Step 3 – acquirer actuals and projections 45Step 4 – combined actuals and projections 45

Price earnings ratio approaches 45Dividend models 45

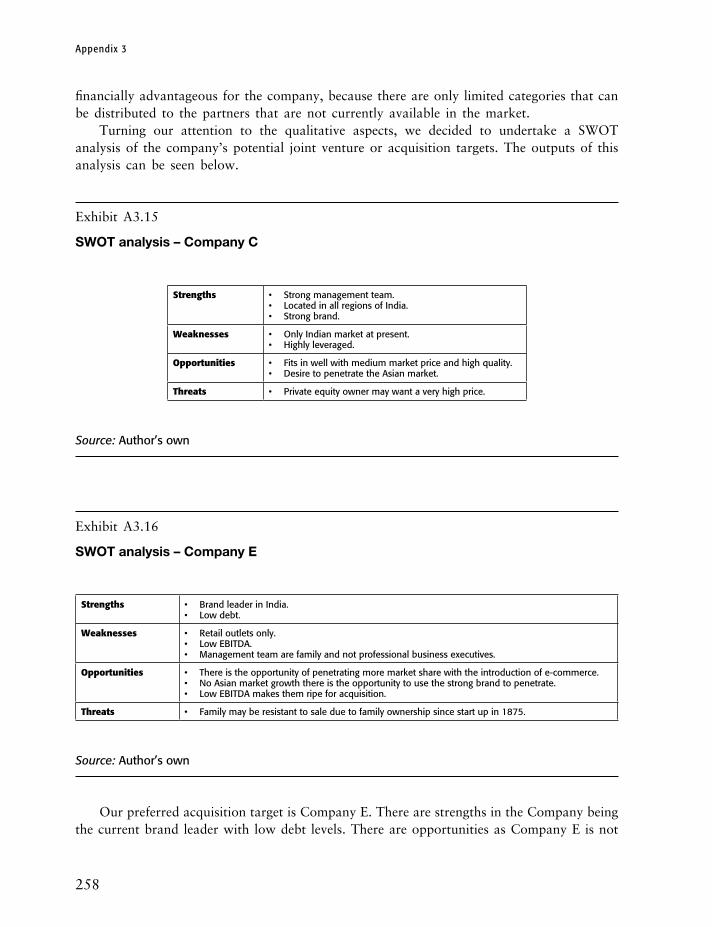

Company mergers 46Joint ventures 52Diversification 52Due diligence 54

Due diligence for mergers and acquisitions decisions 54Appoint legal and accountancy professionals 54Assess information about the business and its relationships 54

Market research 56Market testing 58Desk research 59

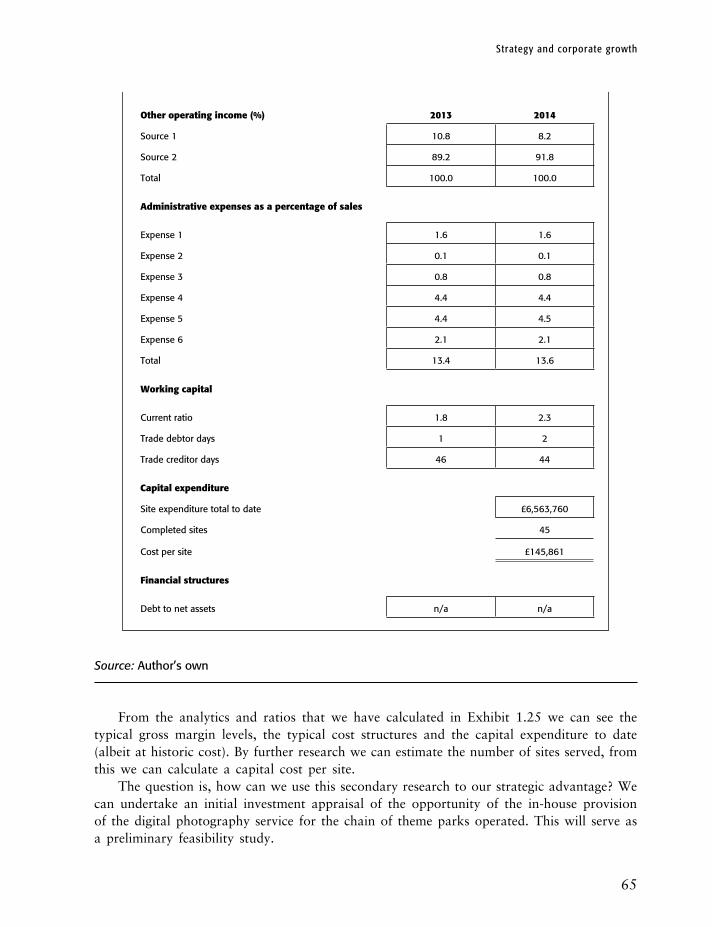

Market reports as a source of secondary research 59Published accounts as a source of secondary research 59Journals and subscription websites as a source of secondary research 66Government published data as a source of secondary research 66Customer desk research as a source of secondary research 66

Business plans 66Executive summary 67The nature of the business 67The mission statement 67The résumés of the senior team 67Short, medium and long-term objectives 68Operational plan 68Market size and opportunity 68Market segmentation 69Investment required and financial projections 69

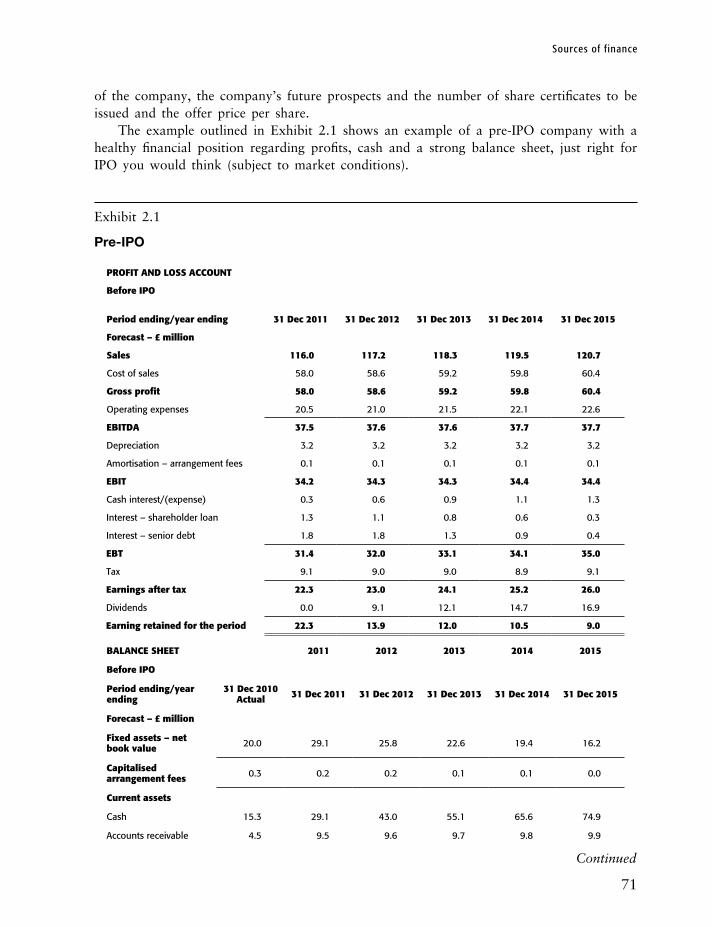

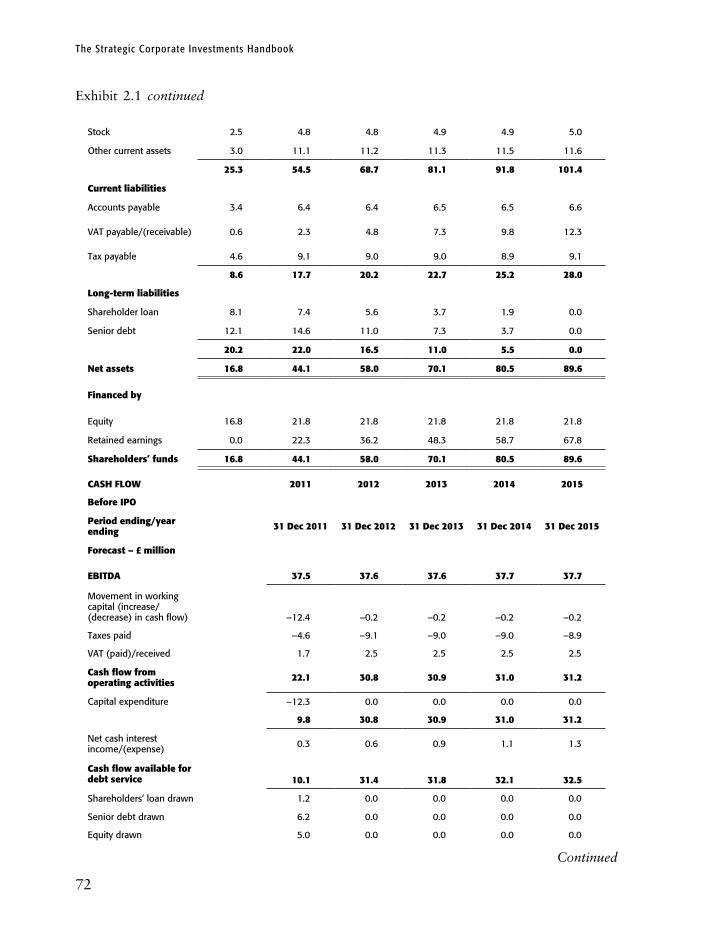

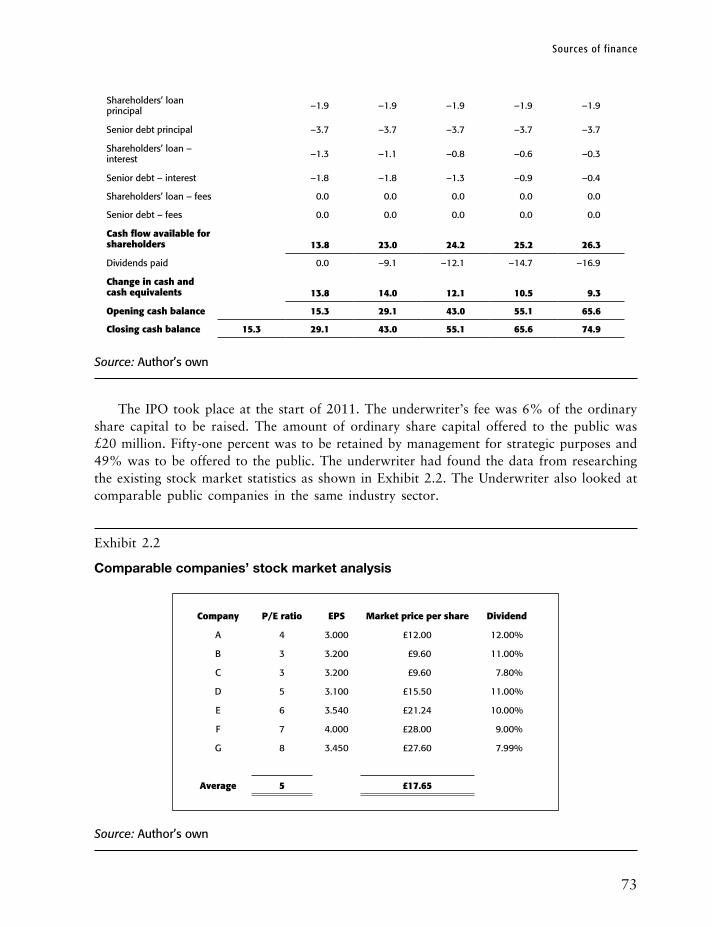

2 Sources of finance 70Initial public offering 70

London Stock Exchange – main listing 75London Stock Exchange – AIMS listing 75Pre-IPO preparation 75

Comprehensive business plan 76

Contents

vii

Suitability for an IPO 76Assess the management team 76Board appointments 77Internal controls 77Improving operational efficiency 77Financial performance 77

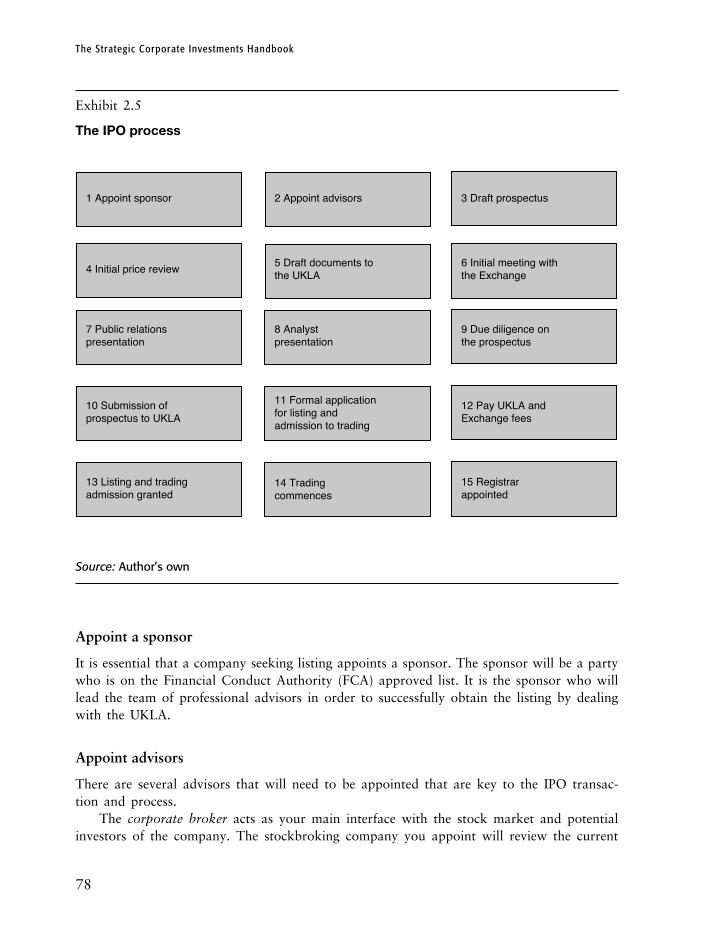

The IPO process 77Appoint a sponsor 78Appoint advisors 78Draft prospectus 79Initial price review 80Draft documents to the UKLA 80Initial meeting with the exchange 80Public relations presentation 80Analyst presentation 81Due diligence on the prospectus 81Submission of the prospectus to the UKLA 81Formal application for listing and admission 81Payment of UKLA and exchange fees 81Listing and trading admission granted 81Trading commences 81Registrar appointed 81

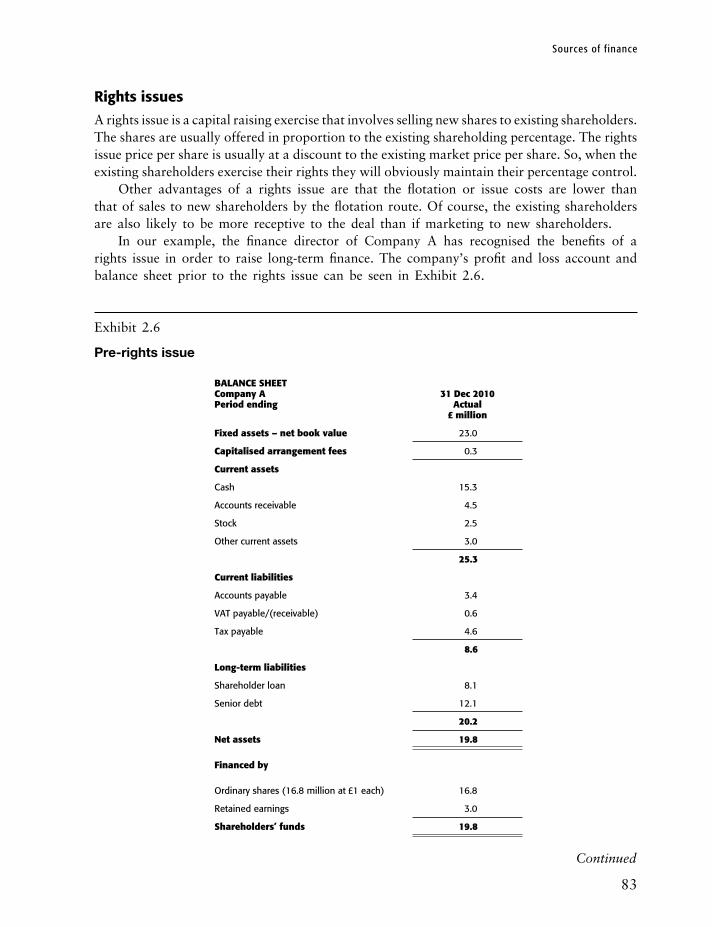

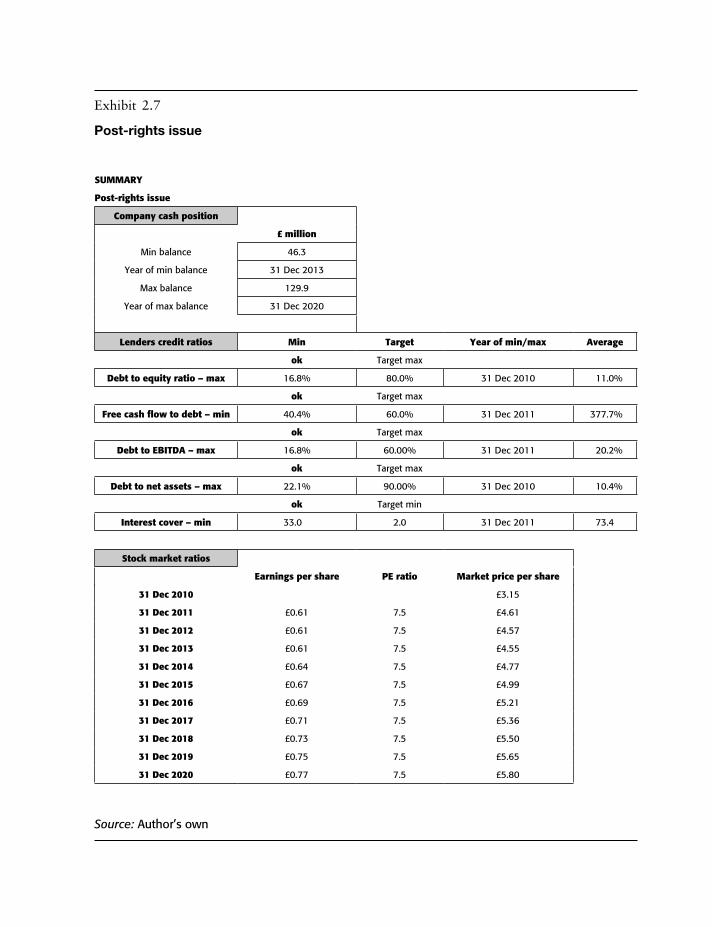

Post-IPO compliance 81Rights issues 83Debt capital 86

Planning different debt structures 87Corporate investment funds 87Infrastructure fund governance and controls 87

Introduction 88Investment fund structure 88Corporate governance and the investment process 89

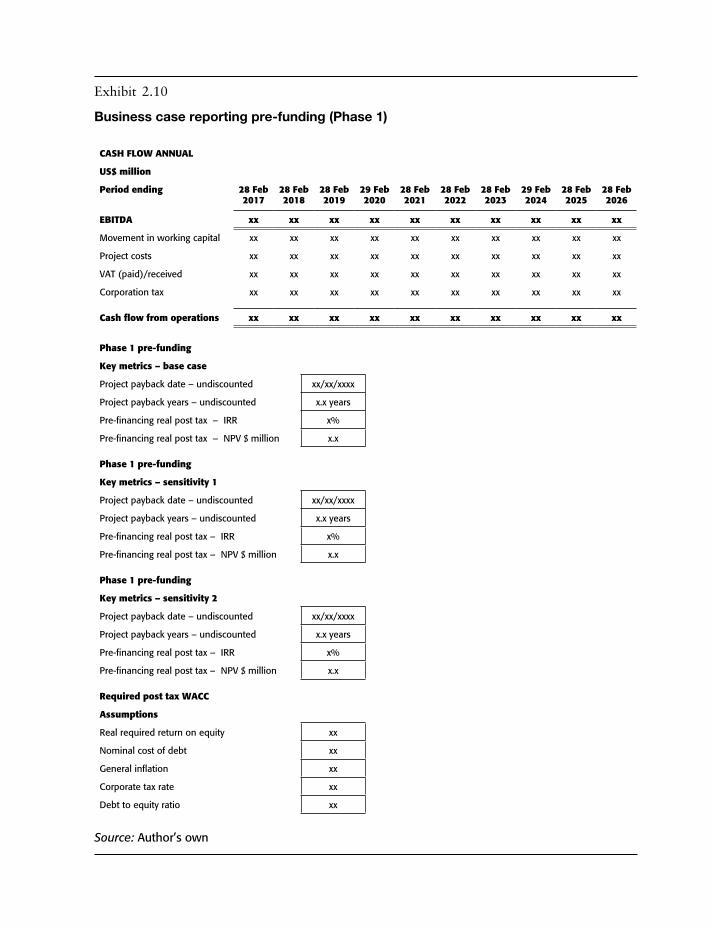

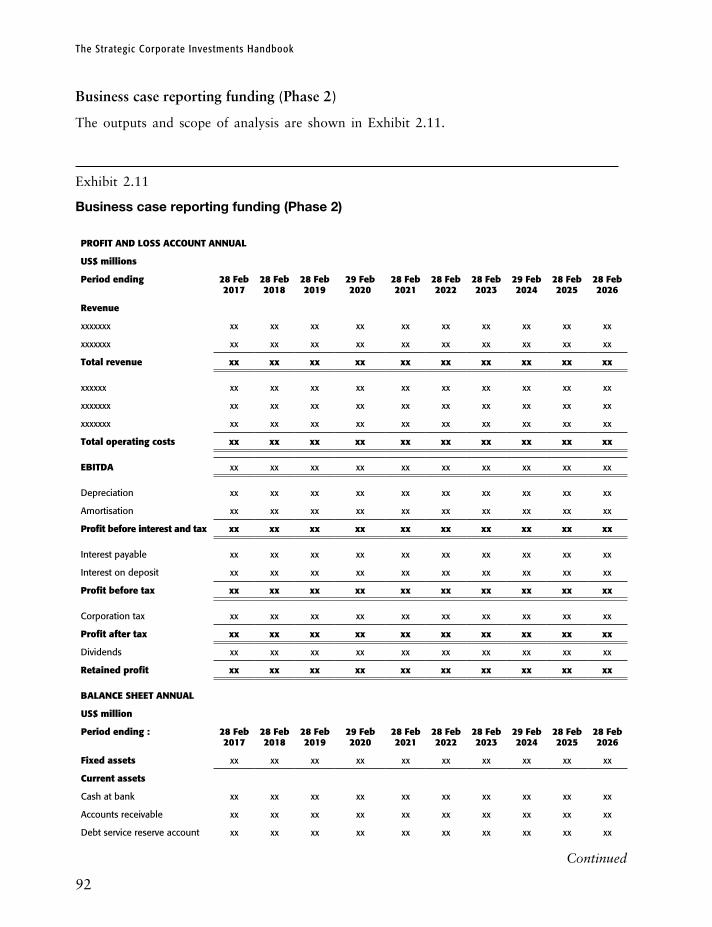

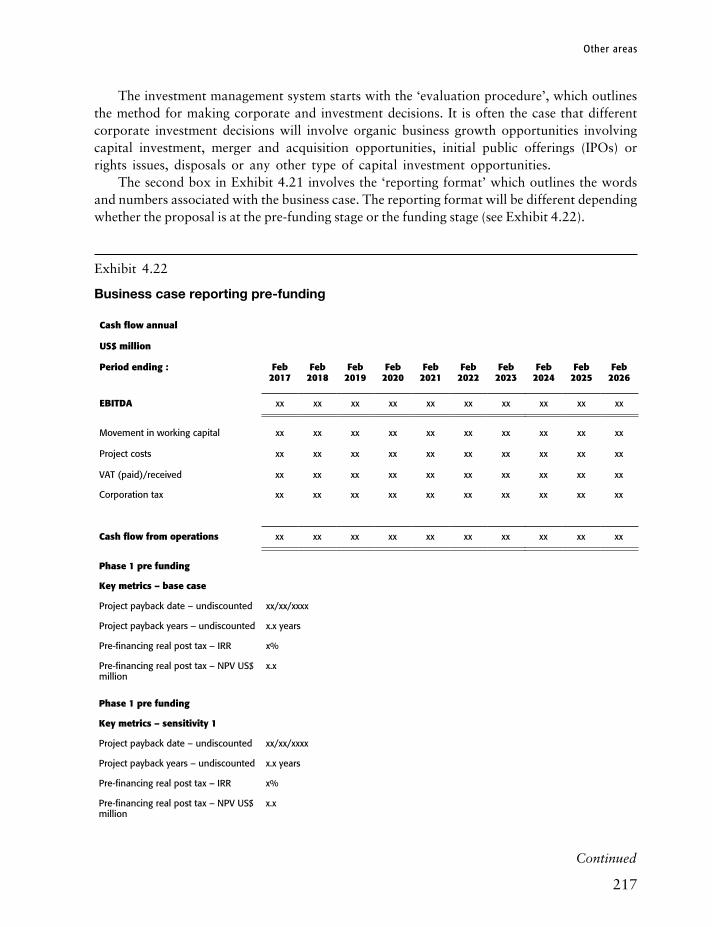

Business case reporting pre-funding (Phase 1) 90Business case reporting funding (Phase 2) 92Authorisation levels 95

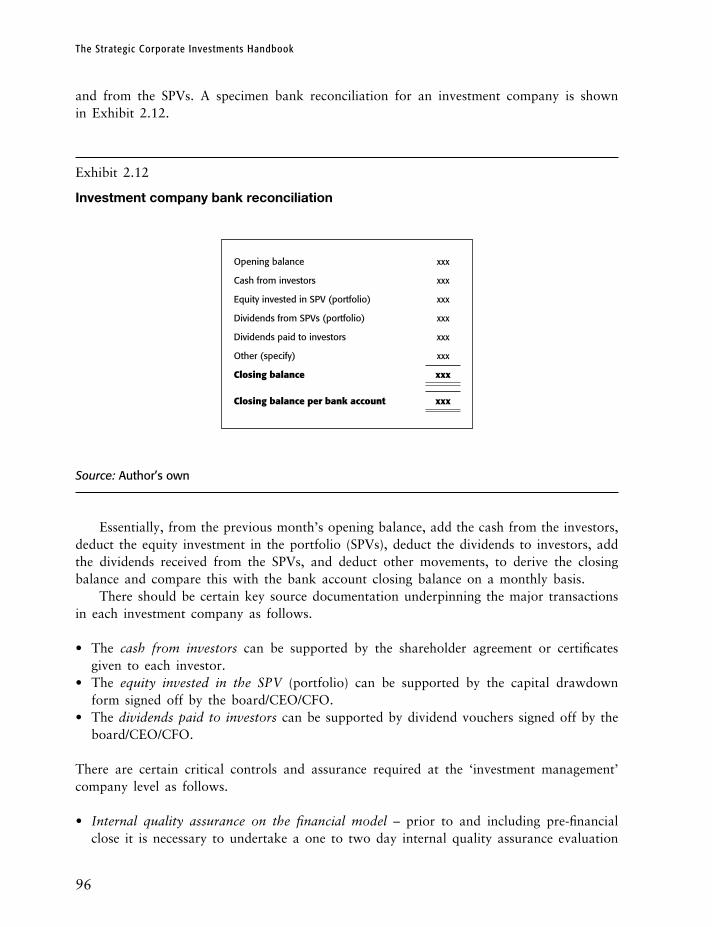

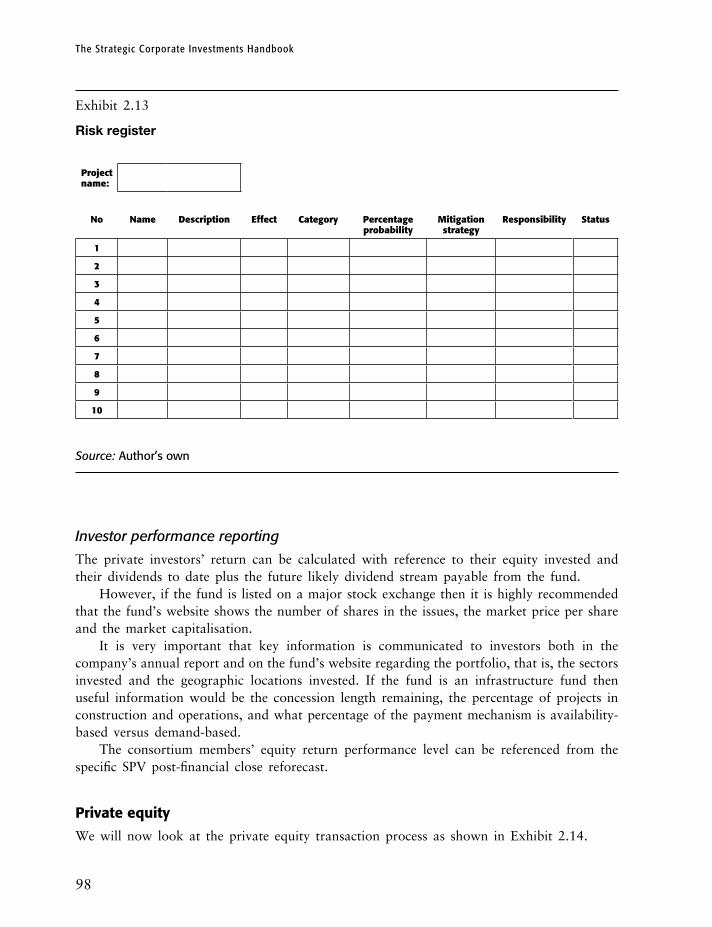

Internal controls and assurance 95Risk management 97Investor performance reporting 98

Private equity 98Different types of private equity transaction 101

Buyout 101Development capital 101Growth capital 101Venture capital 101Turnaround capital 102

viii

Contents

Buyout capital financial analysis implications 102Development capital financial analysis implications 102Growth capital financial analysis implications 102Venture capital financial analysis implications 103Secondary private equity transaction 103Recapitalisation 103

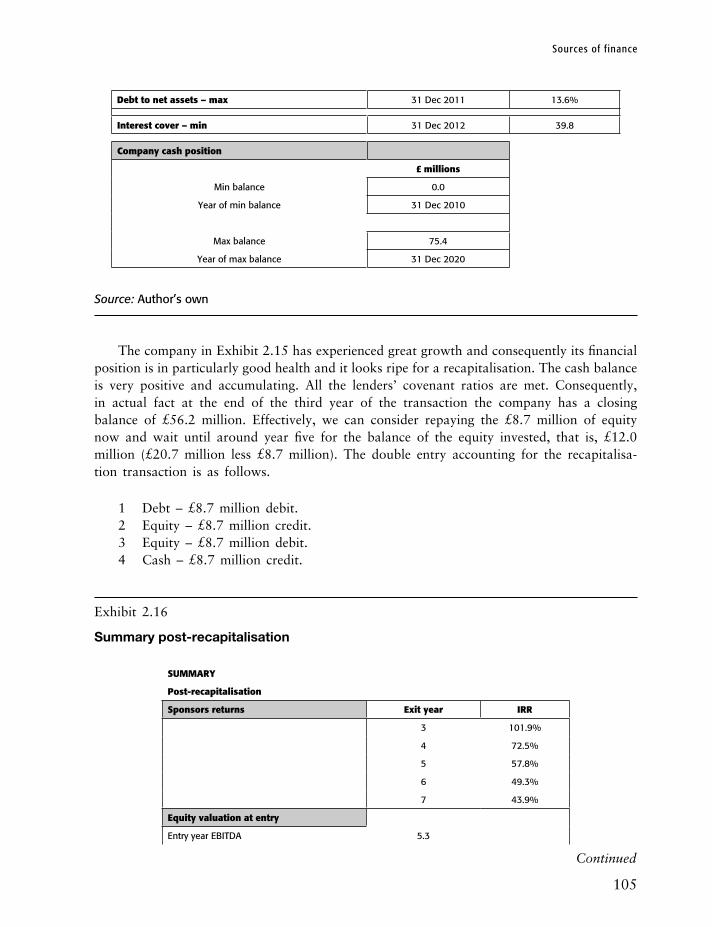

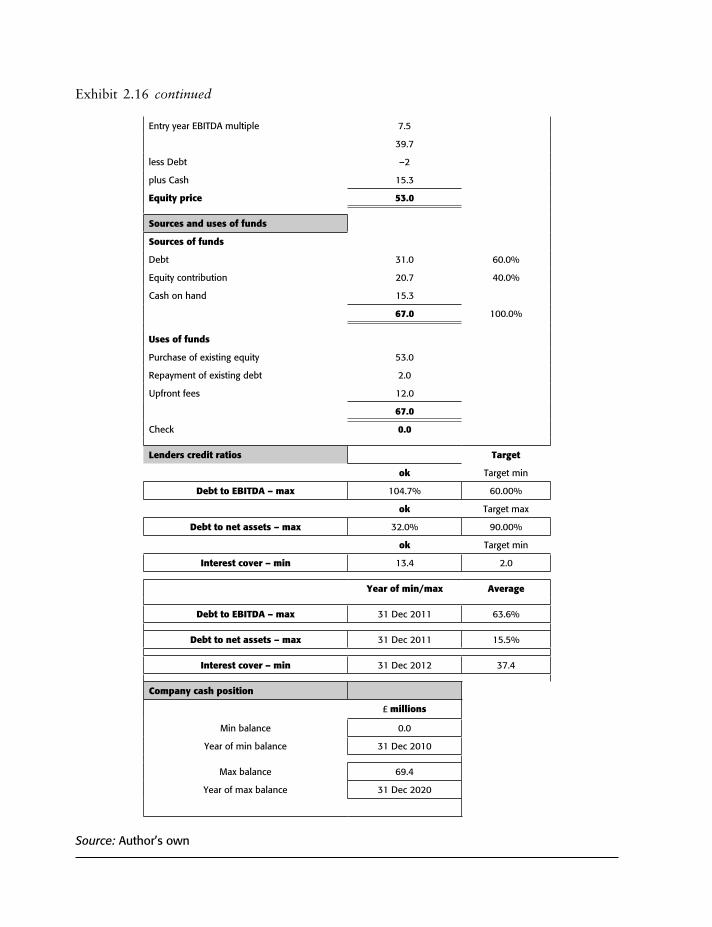

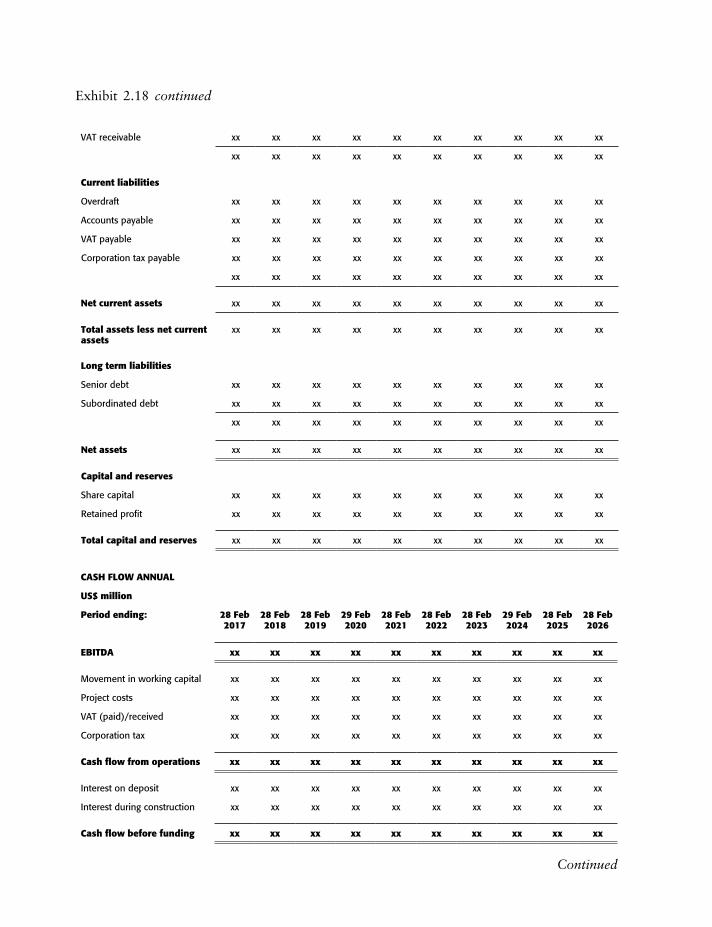

Project finance as a source of funding 107Material and key project finance areas 113

Reserve accounts 113Dividends 113Financial asset accounting 114Revenue recognition 114

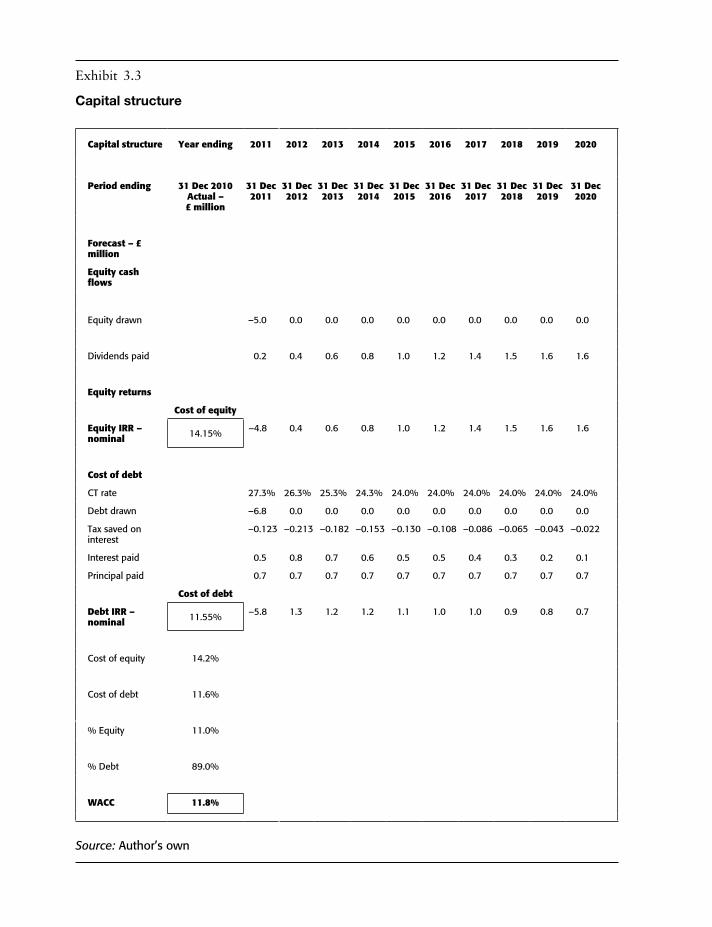

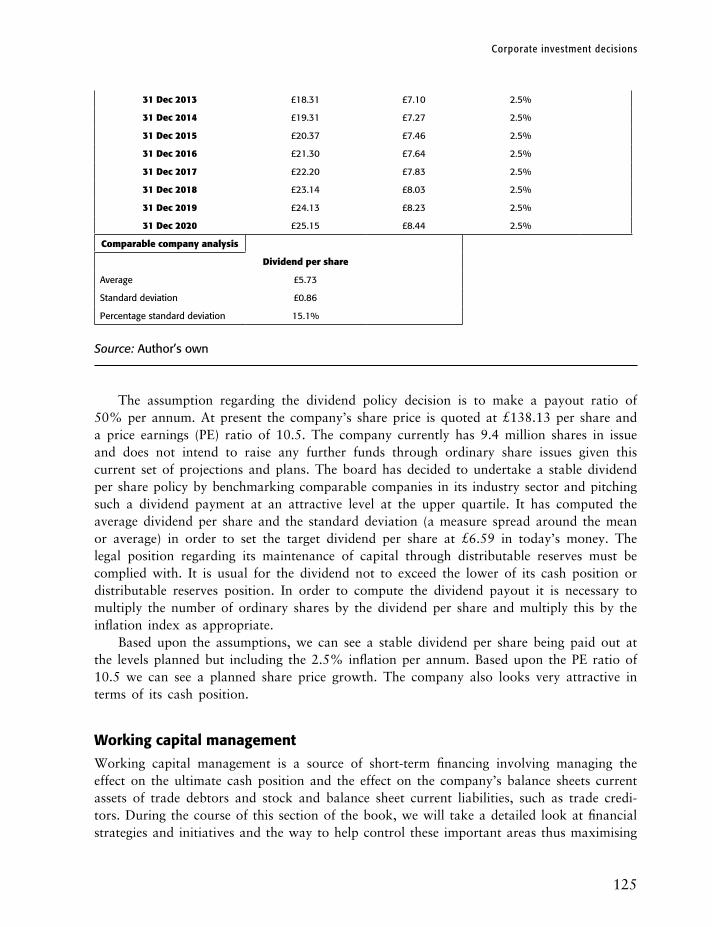

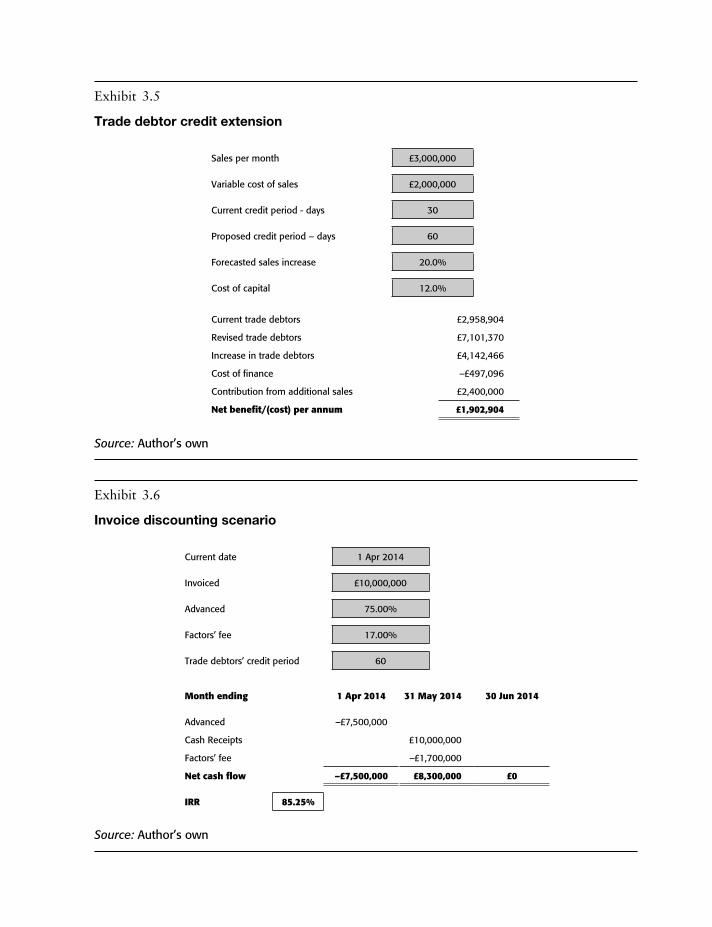

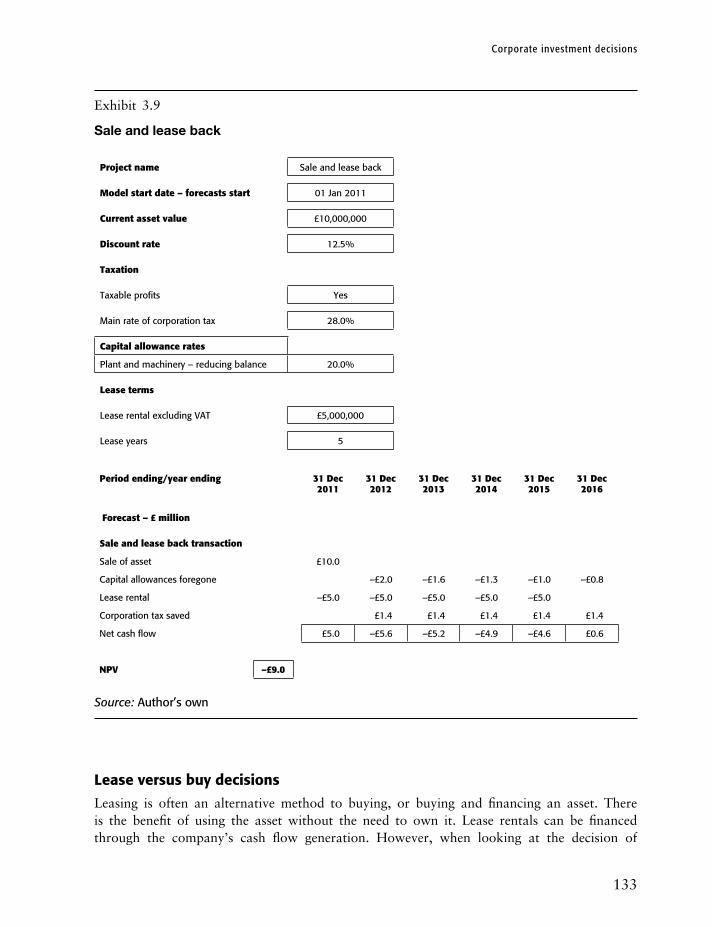

3 Corporate investment decisions 115Disposals 115Refinancing 119Capital structures 121Dividend policy 121Working capital management 125Sale and lease back decisions 132

Advantages of sale and lease back 132Disadvantages of sale and lease back 132Financial evaluation 132

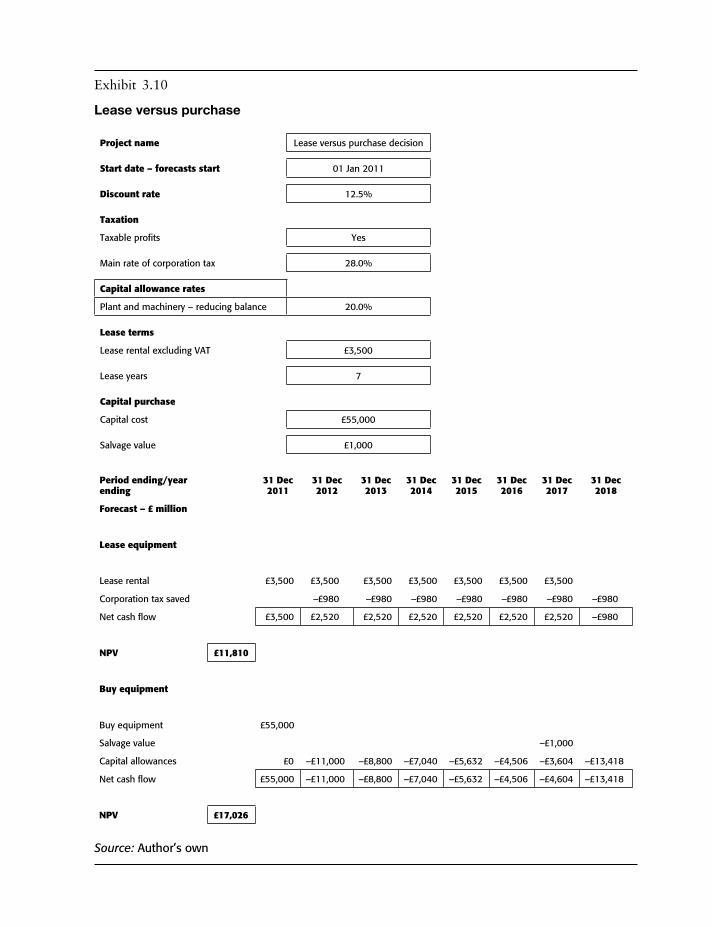

Lease versus buy decisions 133The advantages of leased equipment 134The disadvantages of leased equipment 134Lease versus purchase decisions 134Consider the lease terms before taking the decision 136

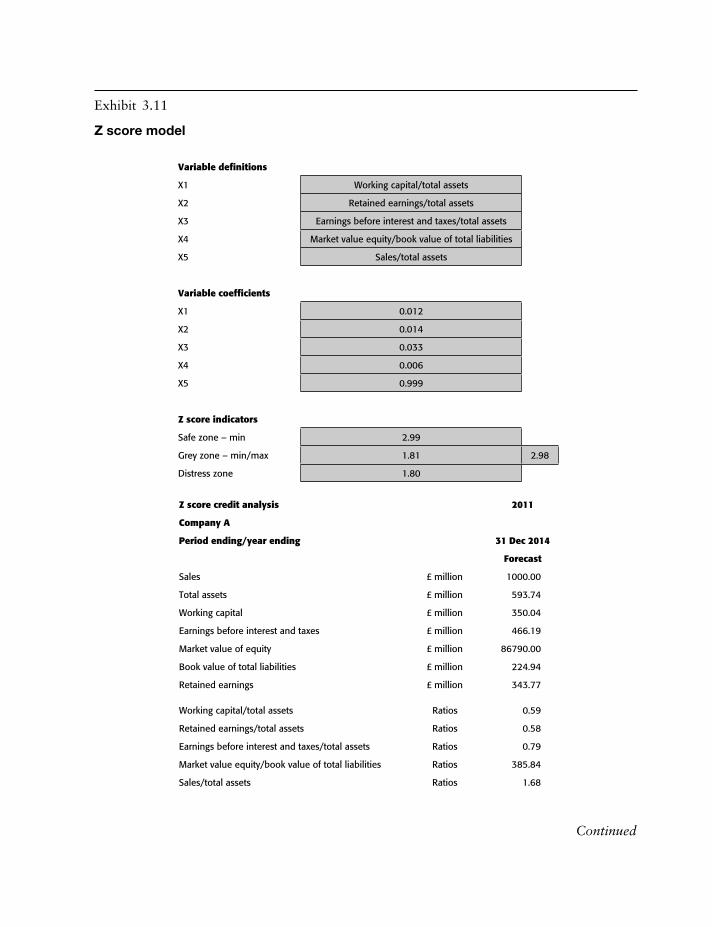

Credit analysis 136Restructuring and distressed debt 138

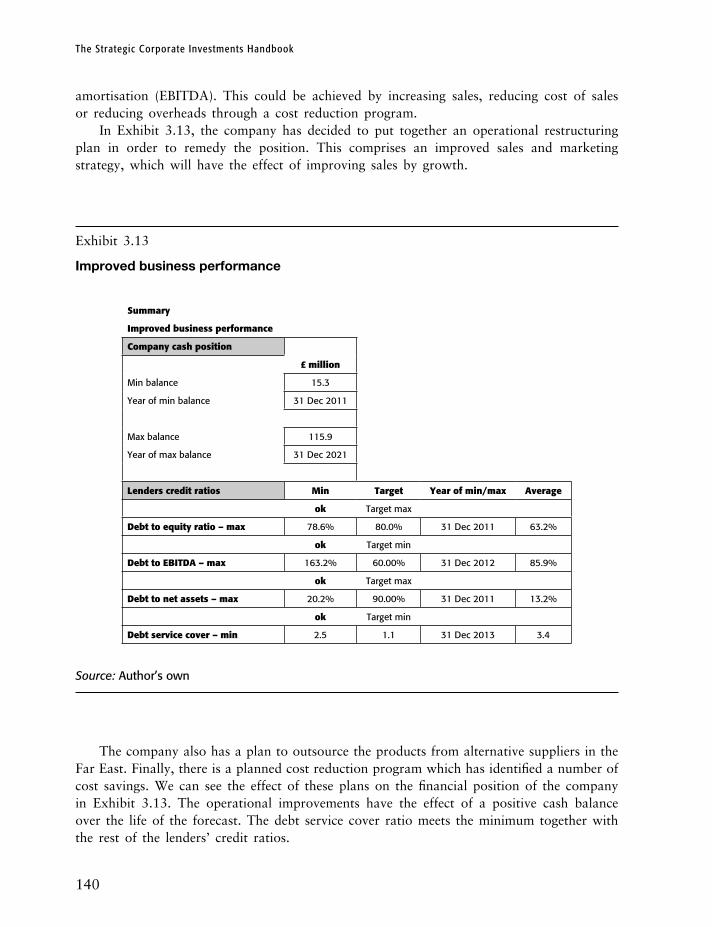

Improve business performance 139Reschedule debts 141Strategic disposals 141Capital reconstruction 145

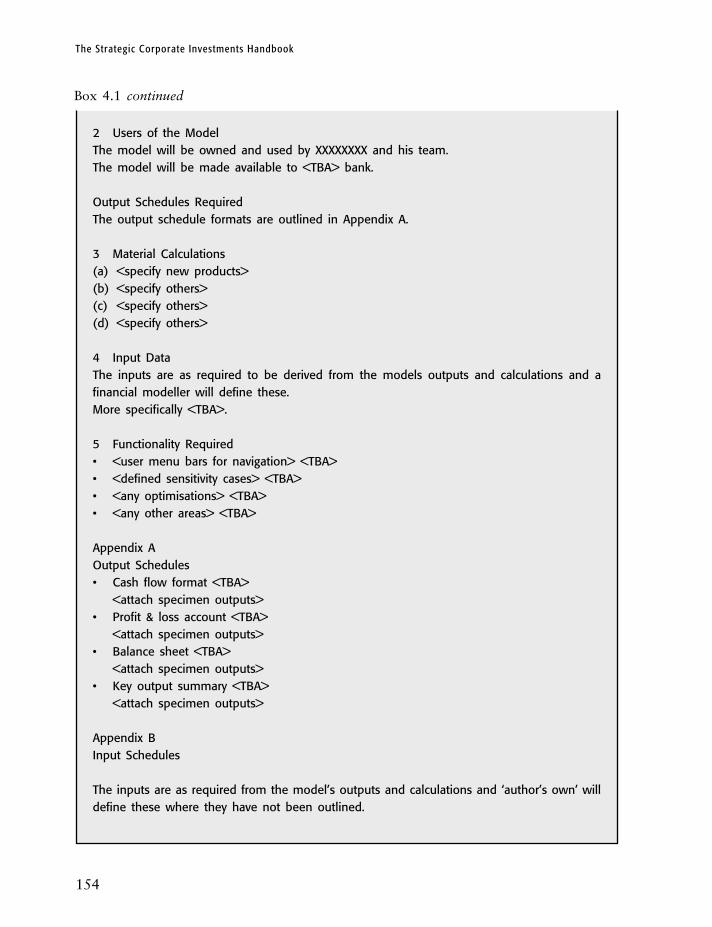

4 Other areas 151Credible business projections 151

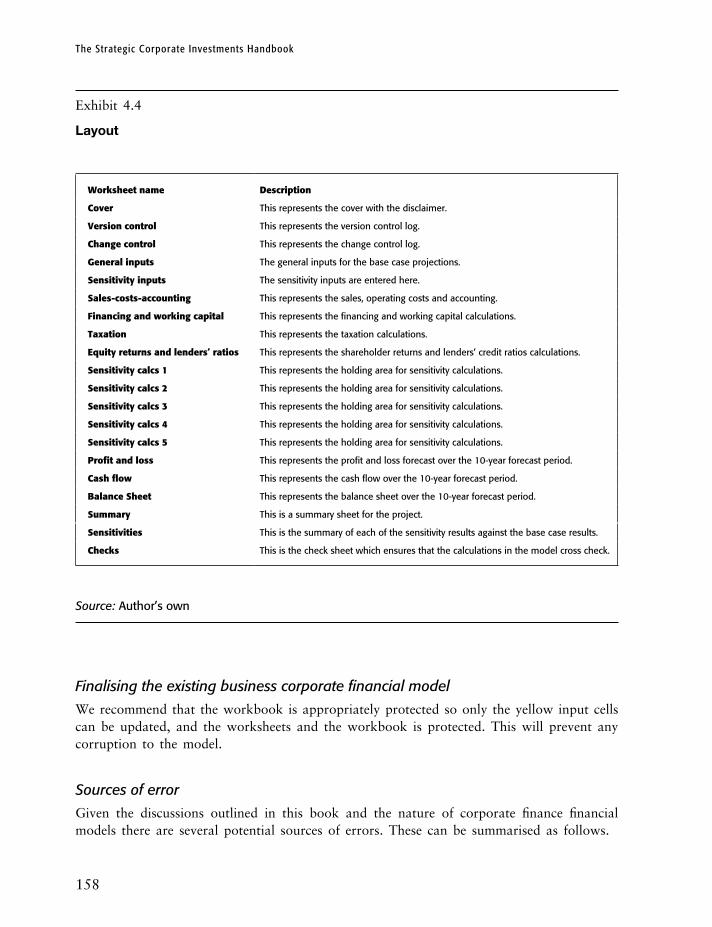

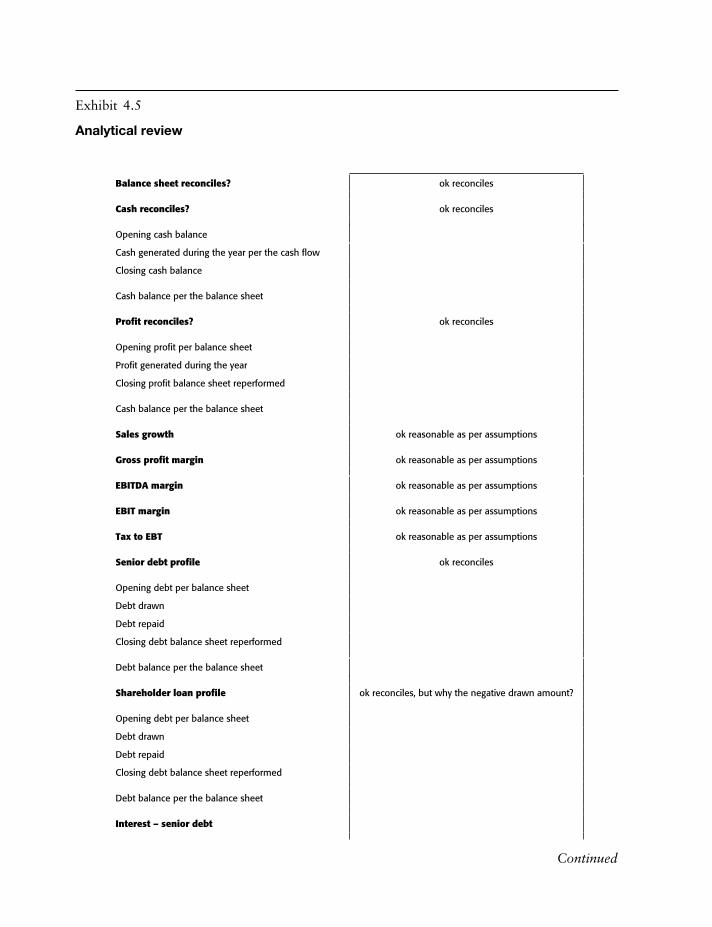

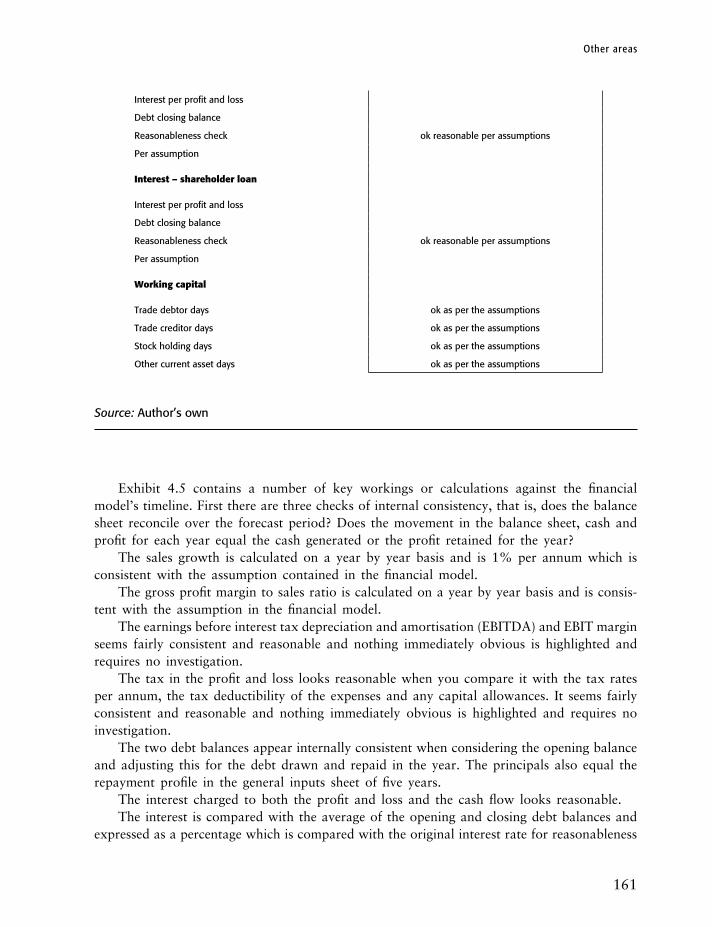

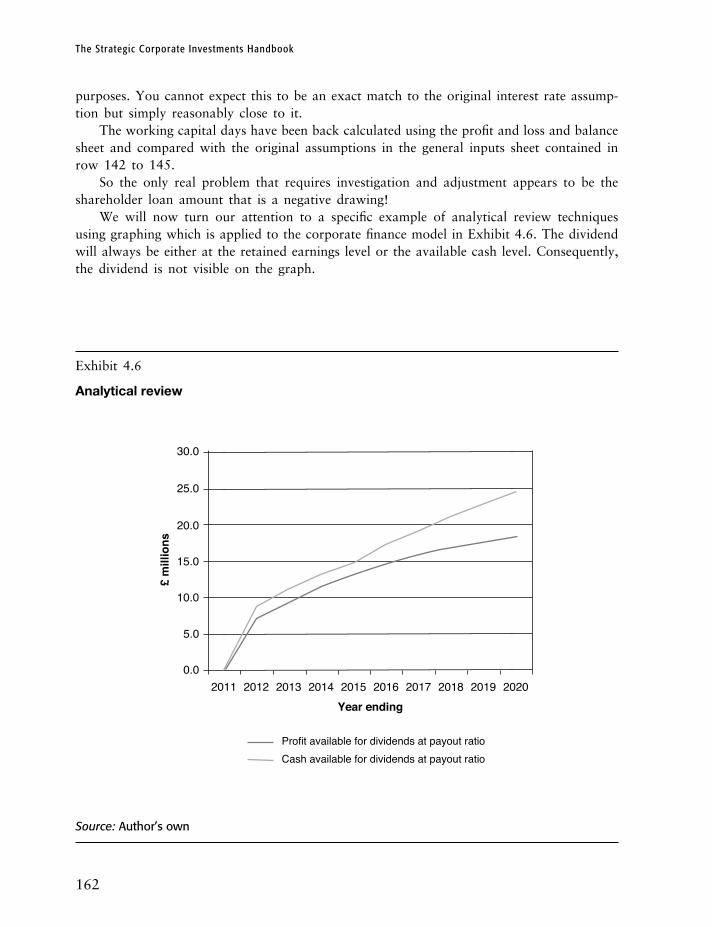

Financial modelling best practice 151Scope 157Designing the financial model 157Layout 157Finalising the existing business corporate financial model 158Sources of error 158Self-testing the model 159

Contents

ix

Top level analytical review 159Key output review 163Flex and sensitivity review 163

Using the model 163Disclaimers 163Sales documents 164

Reviewing and auditing financial models 164Limited scope financial model reviews 164

Design review 165Analytical review 165Degree of integration and reconciliation of financial statement forecasts 165Flex testing and sensitivity review 166Parallel or shadow modelling 166Macro review 167

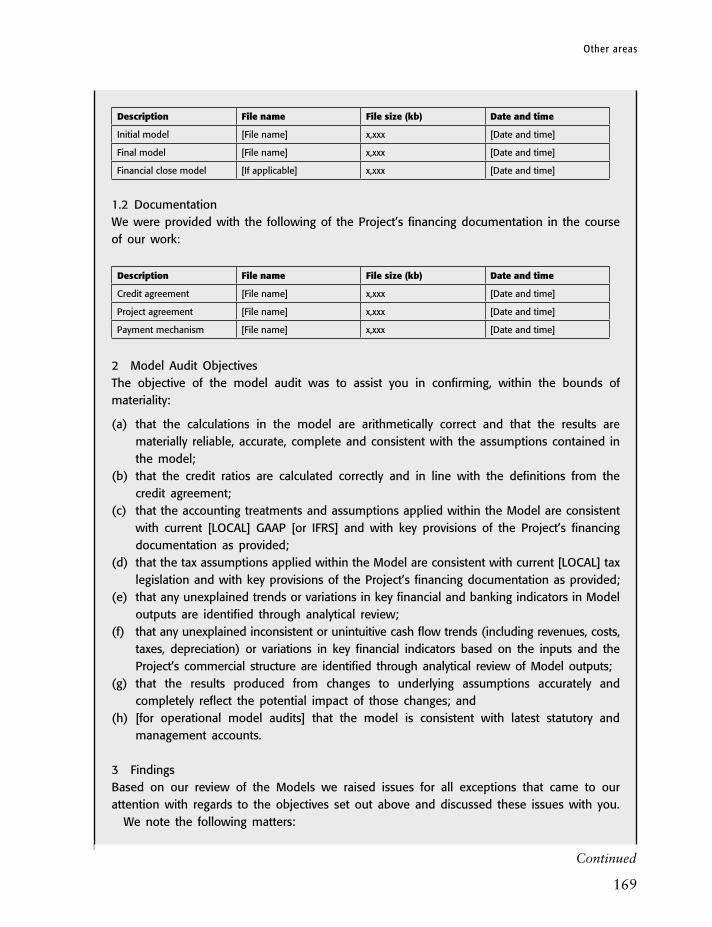

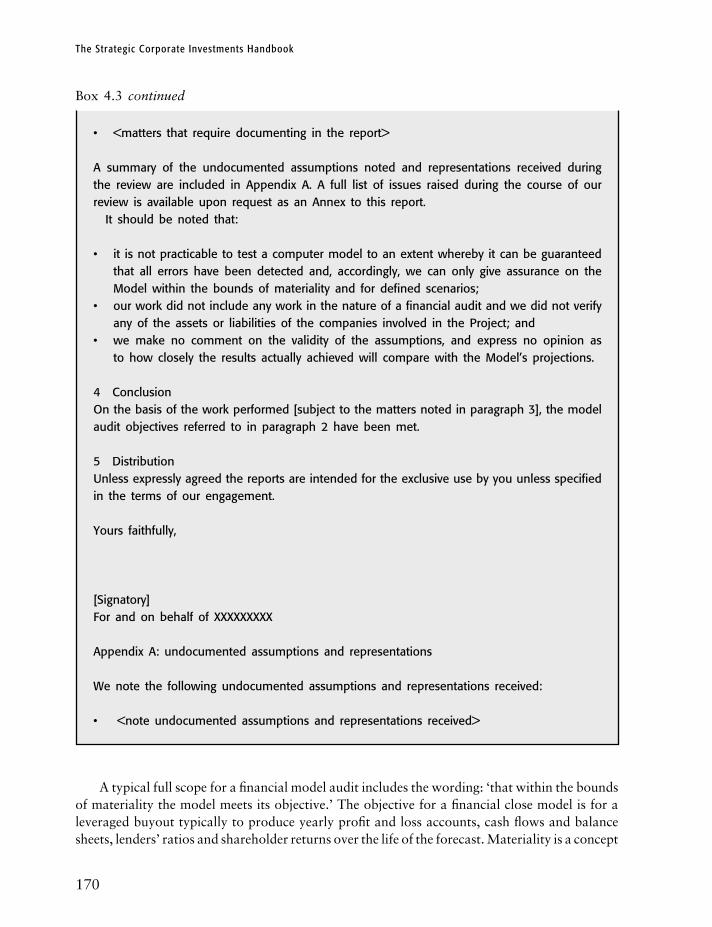

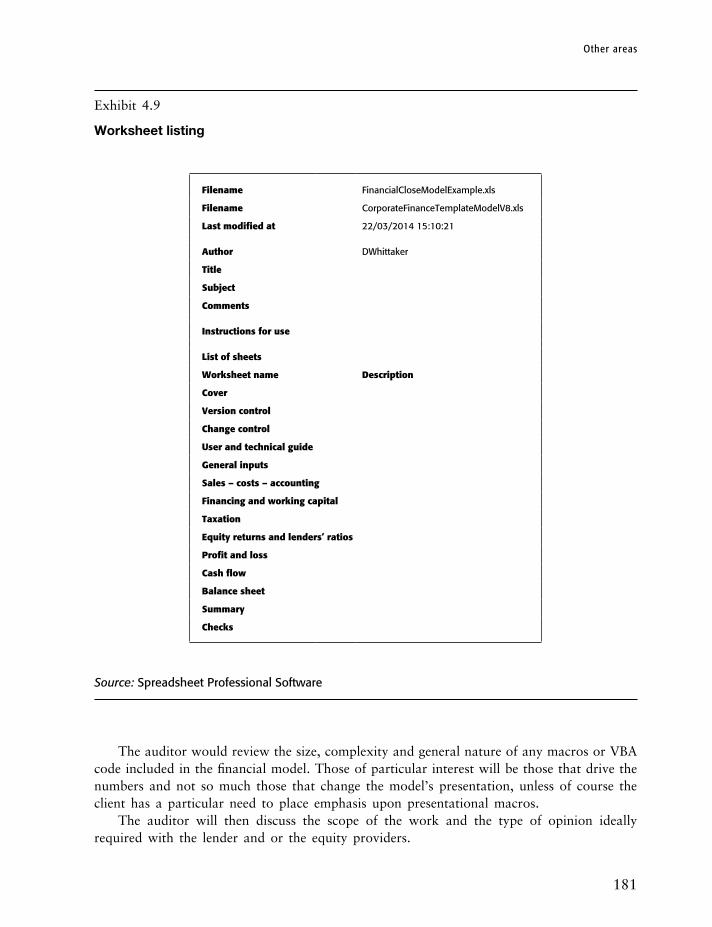

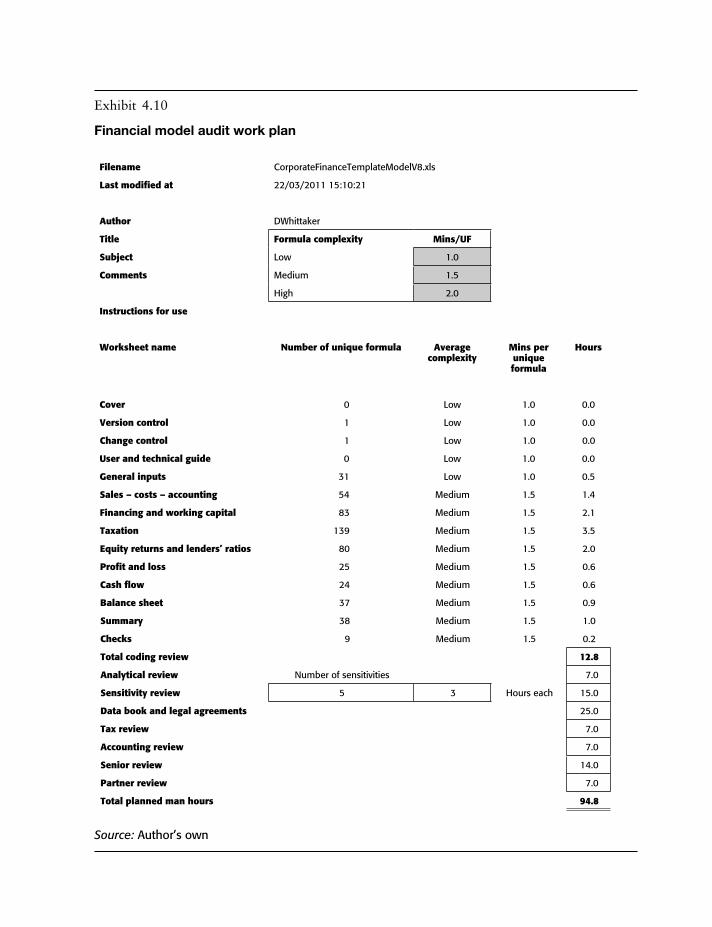

Financial model audits – corporate finance models 168Scoping 171Work plan 182Coding review 182Analytical review 186Data book and legal documentation 186Tax 186Accounting 186Review comments 186Iterations and base case clearance process 187Sensitivities 187Second senior review 187Partner sign off 187

Project information memorandum 187Well-structured 188Professionally presented and well-written 188

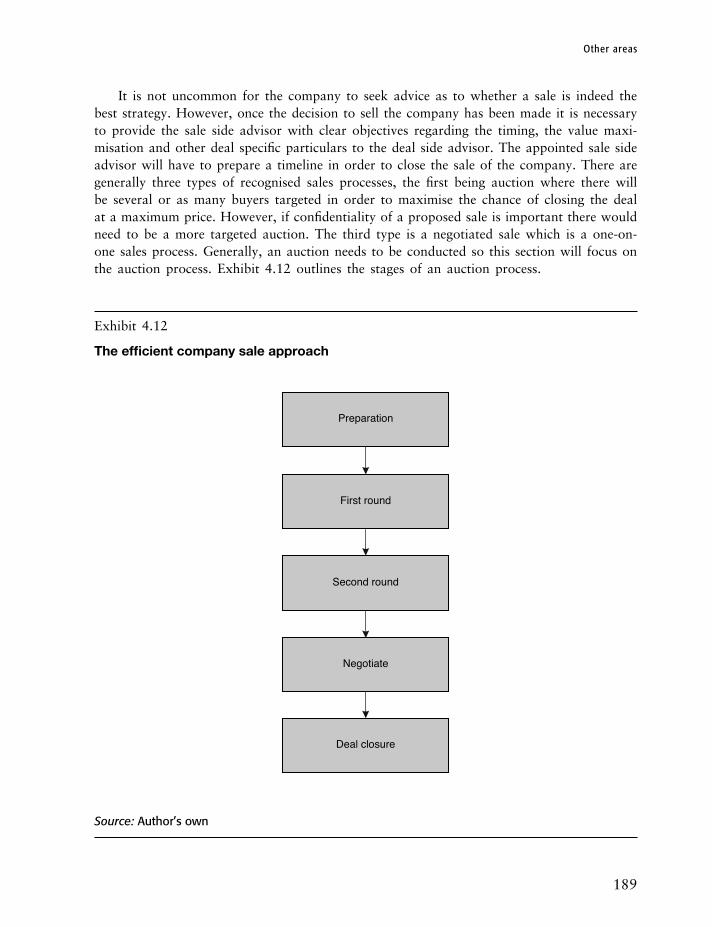

Offering memorandum 188The company disposal process 188

Preparation 190First round 190Second round 192Negotiate 193Deal closure 193

Internal controls 193The sales cycle 194The purchases cycle 194Payroll 195The stock cycle 195Bank account and cash 195

Corporate governance 195

x

Contents

The UK Corporate Governance Code 196Comply or explain 197The main principles of the Code 197

Section A: Leadership 197Section B: Effectiveness 197Section C: Accountability 198Section D: Remuneration 198Section E: Relations with shareholders 198

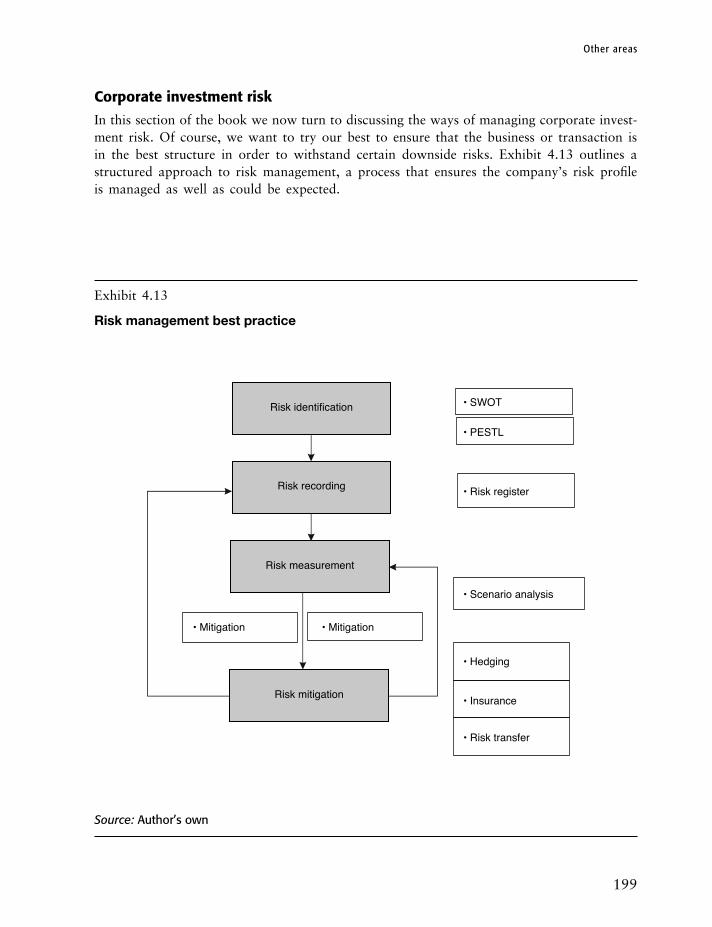

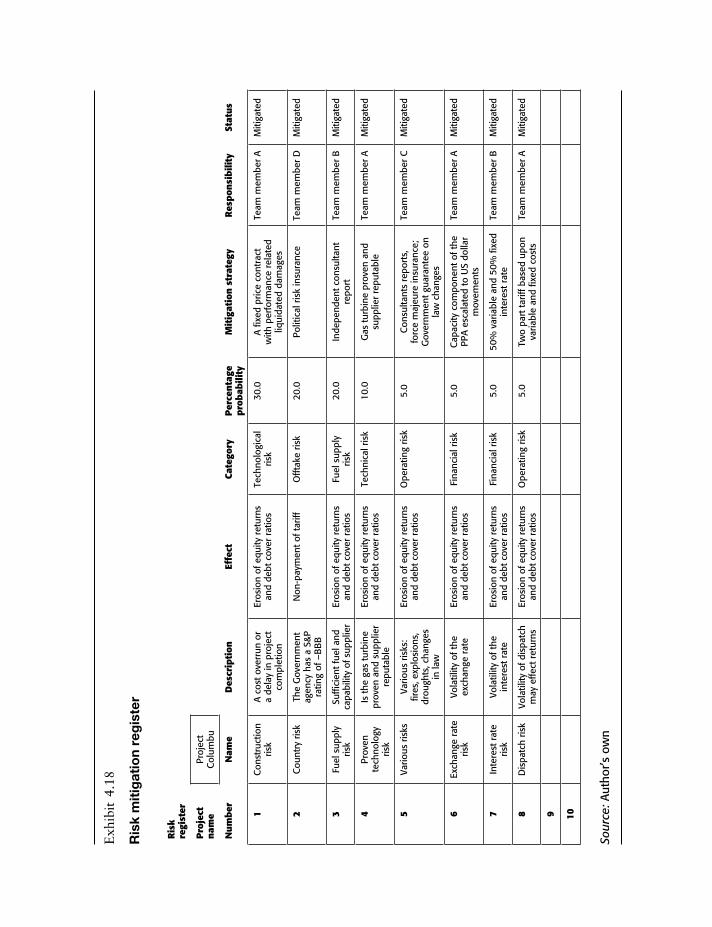

Corporate investment risk 199Examples of risk management techniques 200

SWOT 200PESTL 200Risk register 201Scenario analysis 201

Excel’s scenario manager 202Interest rate risk management 202

Fixed versus floating rate debt 203Forward rate agreements 203Interest rate futures 203

Interest rate options 203Interest rate swaps 204Exchange rate risk management 204

Forward exchange rates 204Other exchange rate hedging strategies 204

Insurance 205Political risk insurance 205

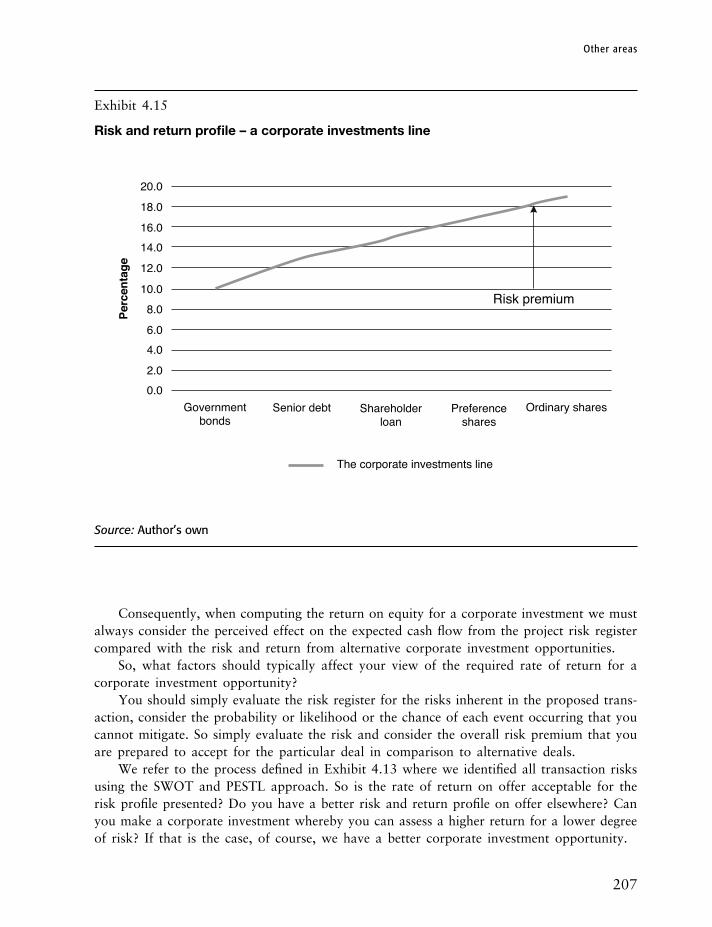

Risk transfer 206Risk and return 206Risk management best practice case study 208

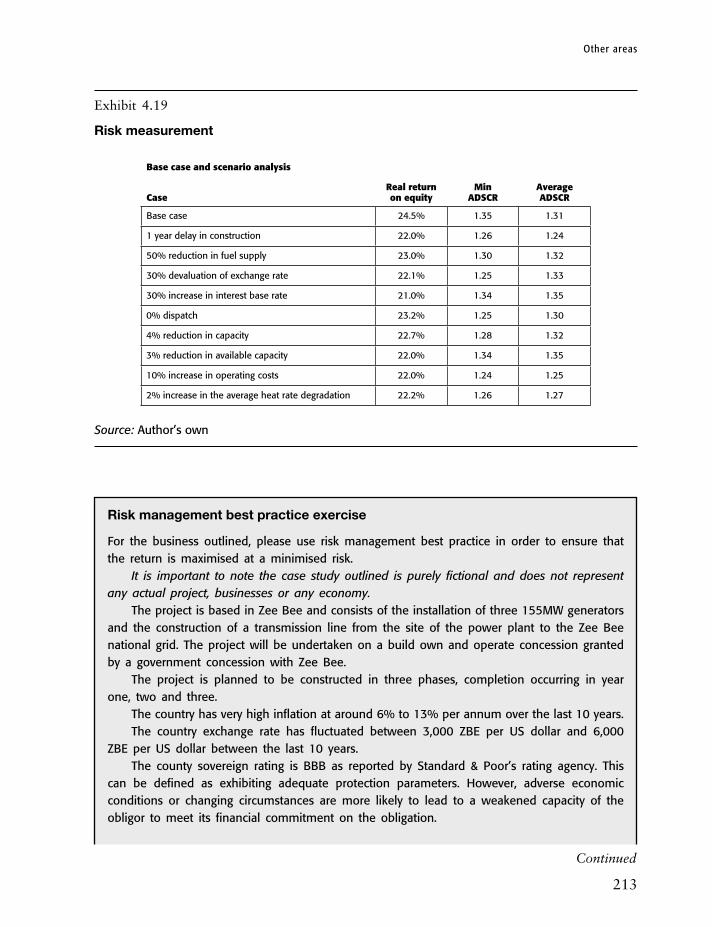

Risk identification and risk recording 209Risk measurement 212

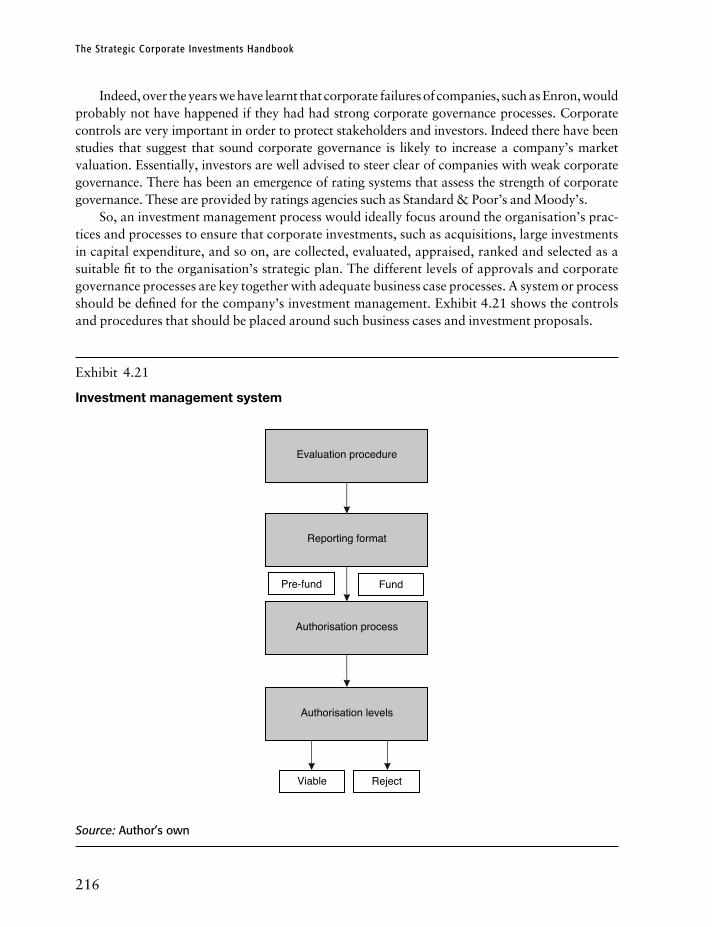

A critical evaluation of business plans 214Business case proposals – controls and processes 215

5 Conclusions 220

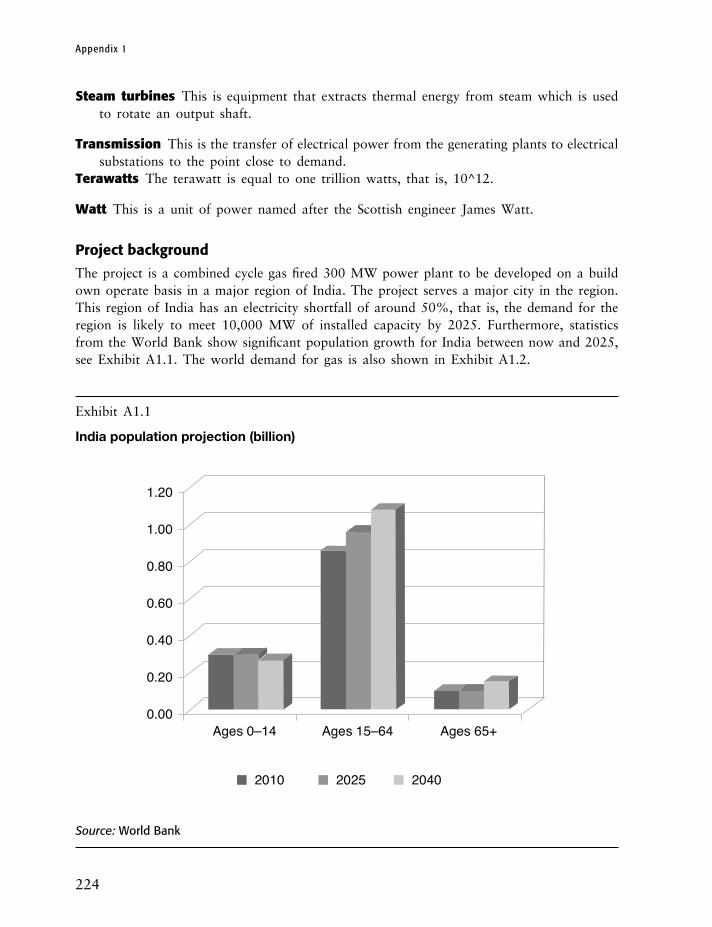

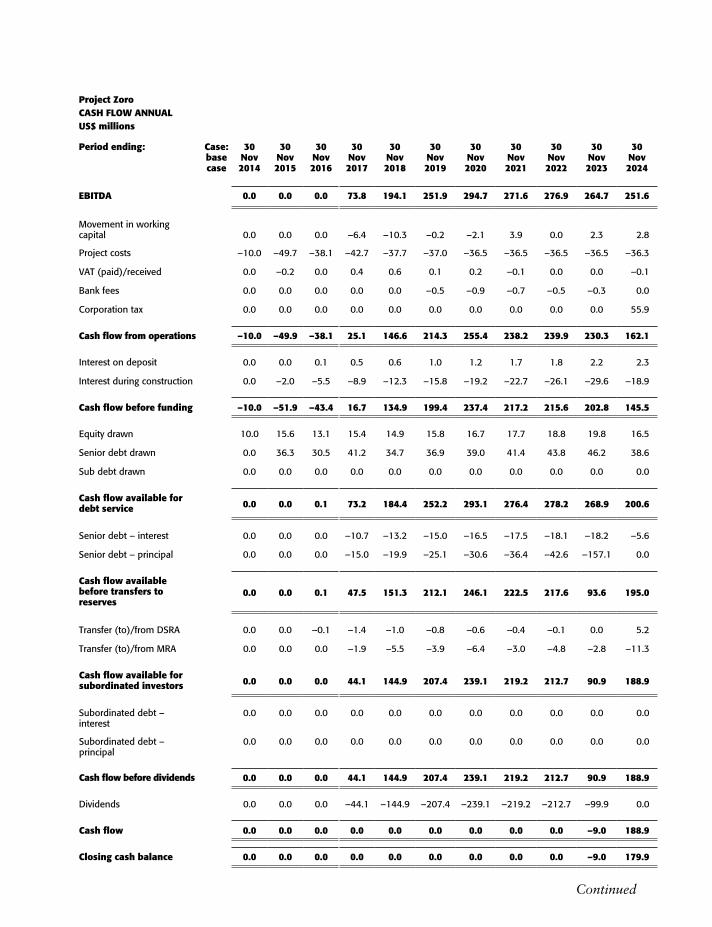

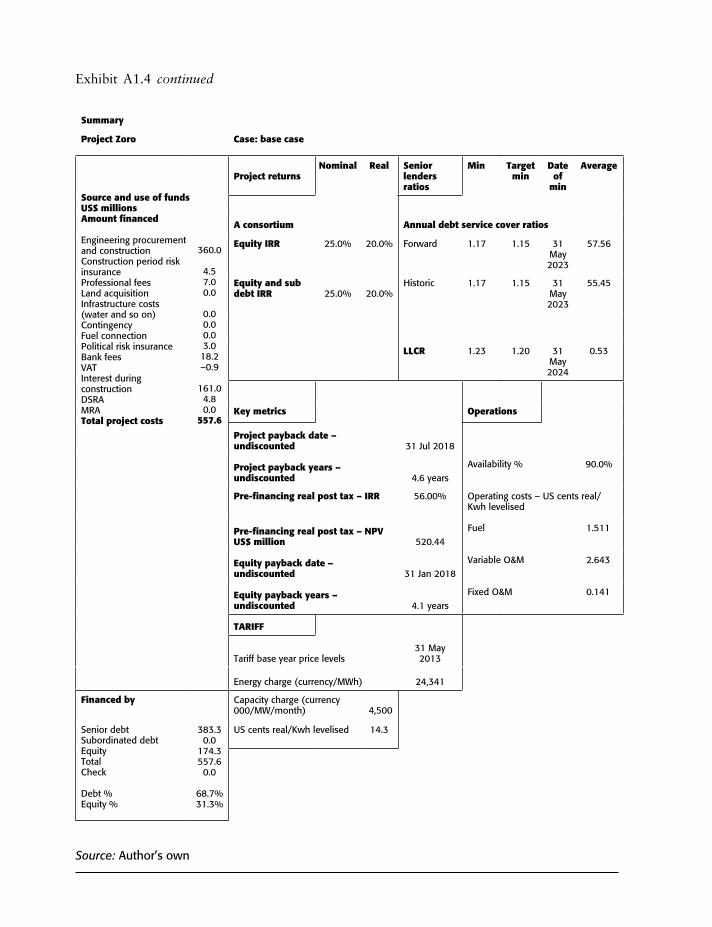

Appendix 1 Project information memorandum 221Disclaimer 221Table of contents 222Glossary of terms 222Project background 224Transaction overview 225

Introduction 225Project structure 225

Contents

xi

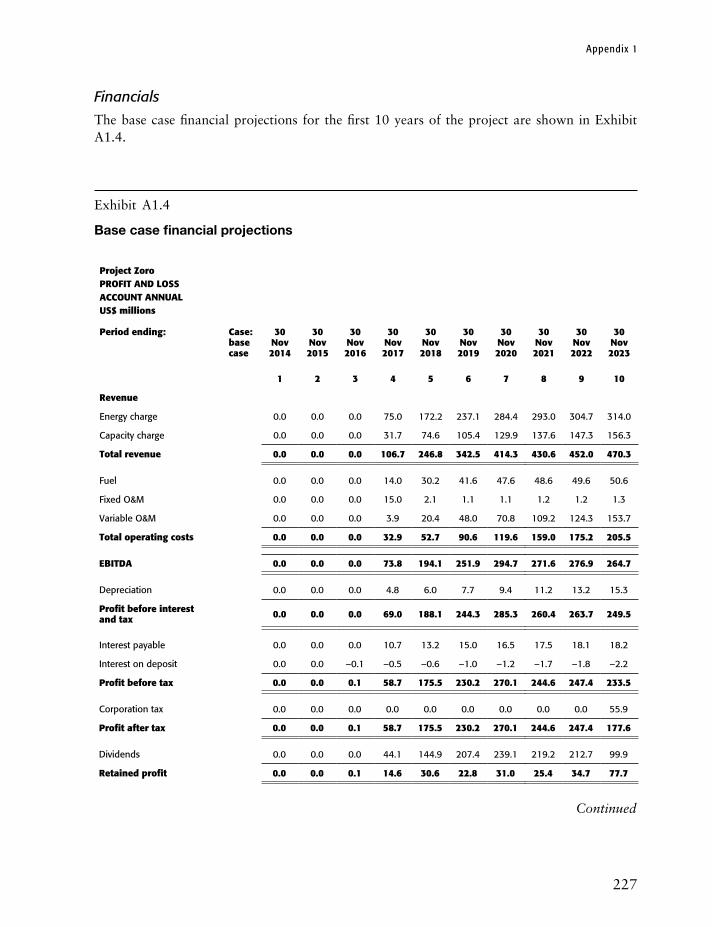

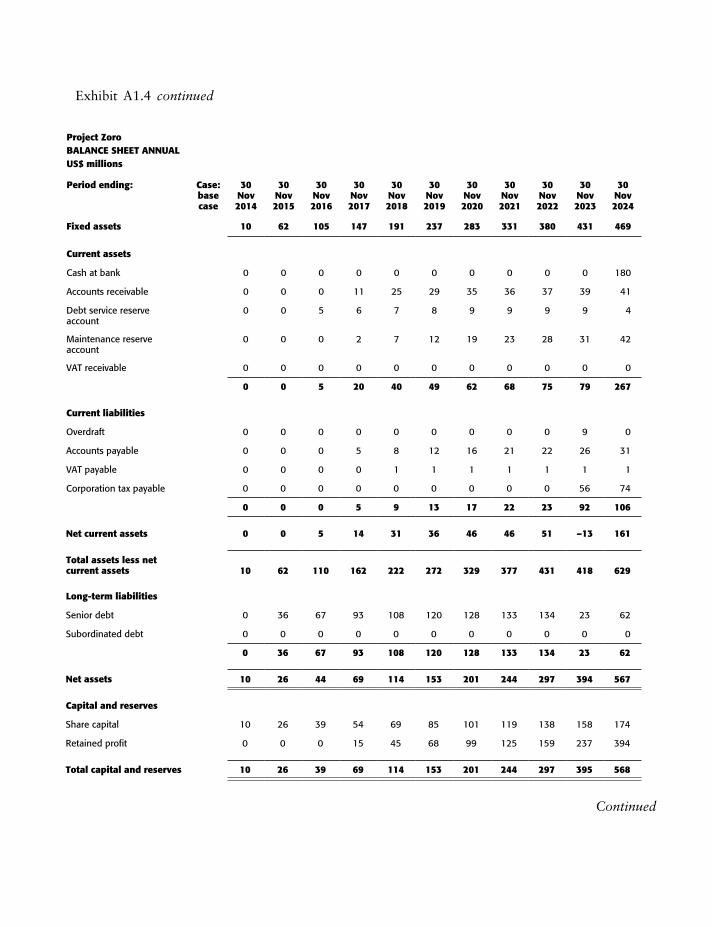

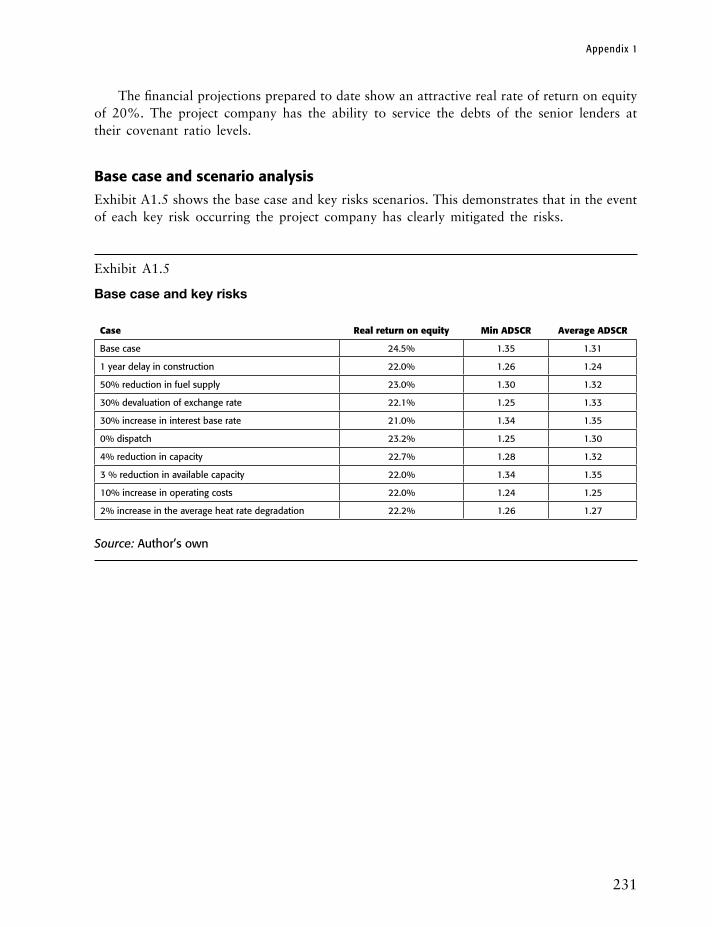

Financials 227Base case and scenario analysis 231Location 232Project risks and mitigation 232

Construction risk 232Fuel supply risk 232Offtake risk 232Technological risk 232Operating risk 232Environmental and licensing risk 233

Contact us 233

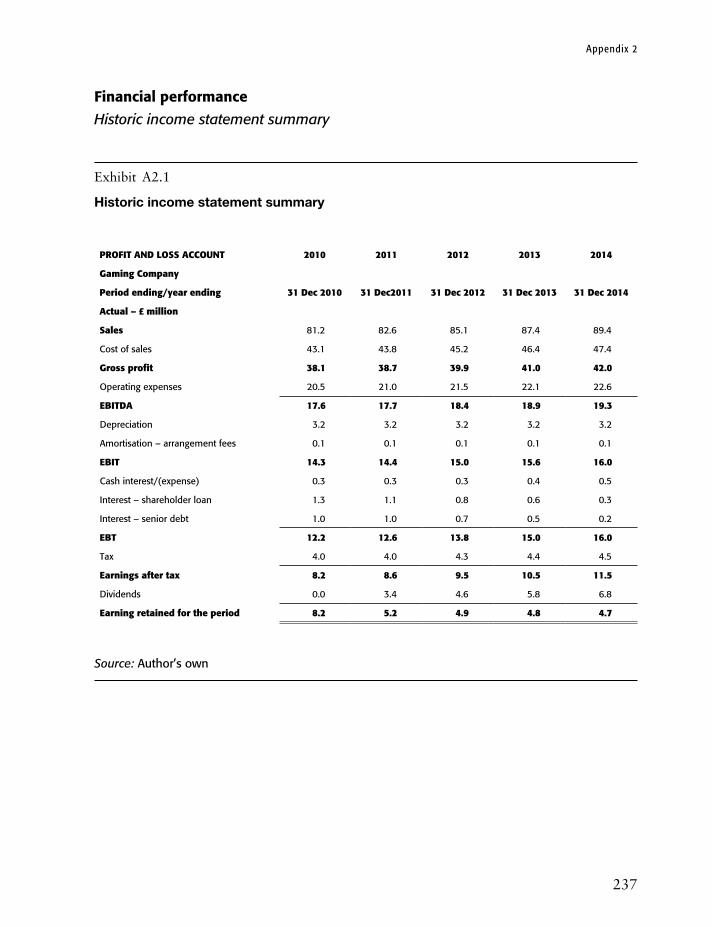

Appendix 2 Confidential offer memorandum 234Cover 234Table of contents 234Disclaimer and notice 234Industry overview 235Overview of the business 235Ownership and control 235Strategy and business model 235Products and services 236Market segmentation 236Management and employees 236Facilities and premises 236Information systems 236Proprietary technology and intellectual property 236Legal, regulatory and environmental 236Financial performance 237

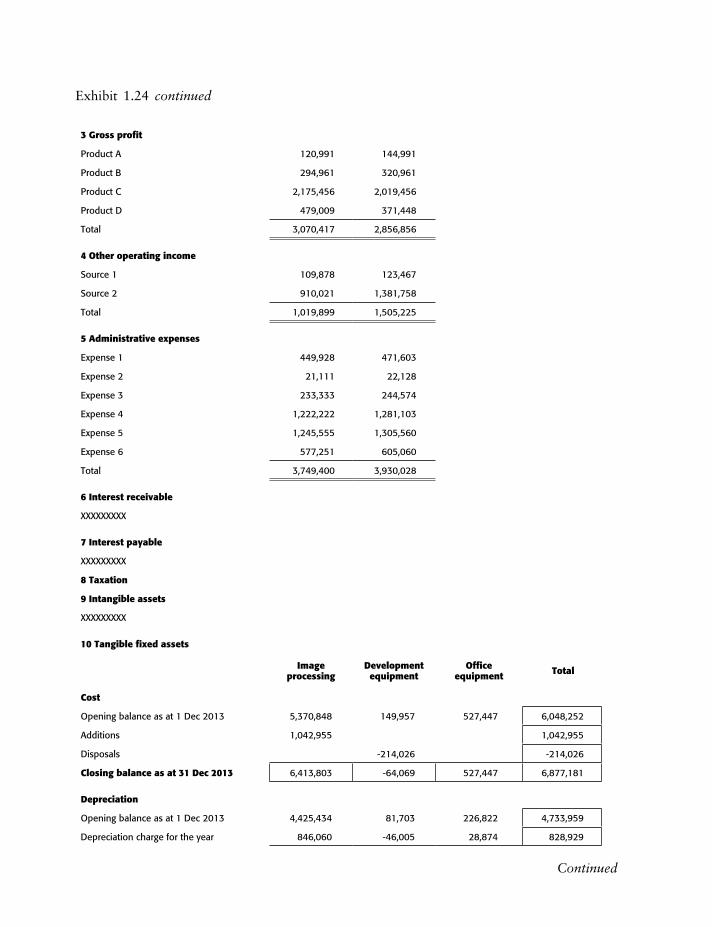

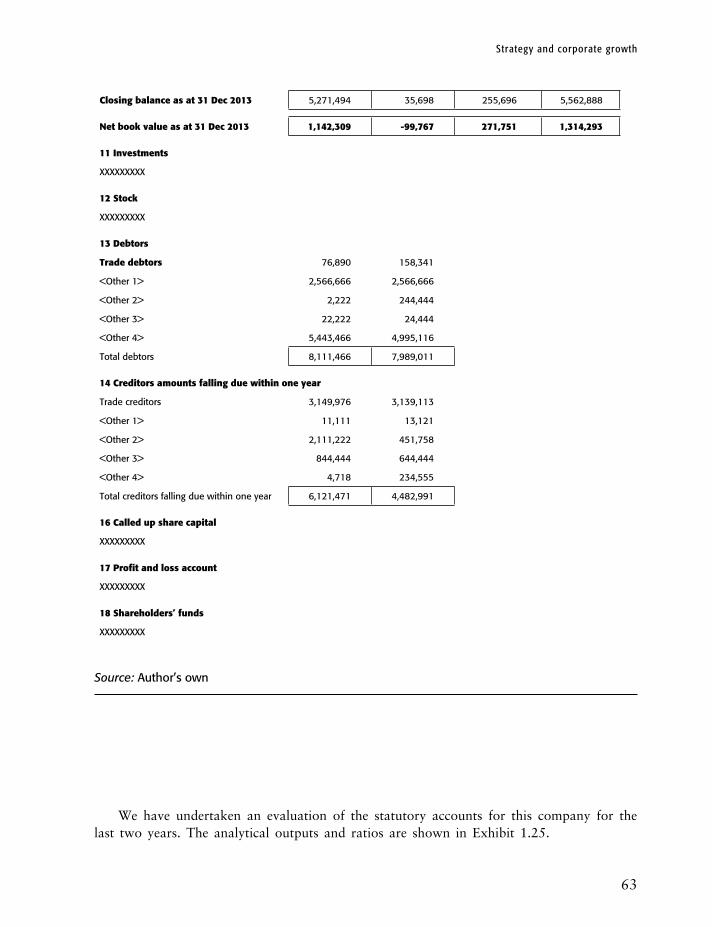

Historic income statement summary 237Historic balance sheet 238Historic cash flows 239Historic financial ratios 240

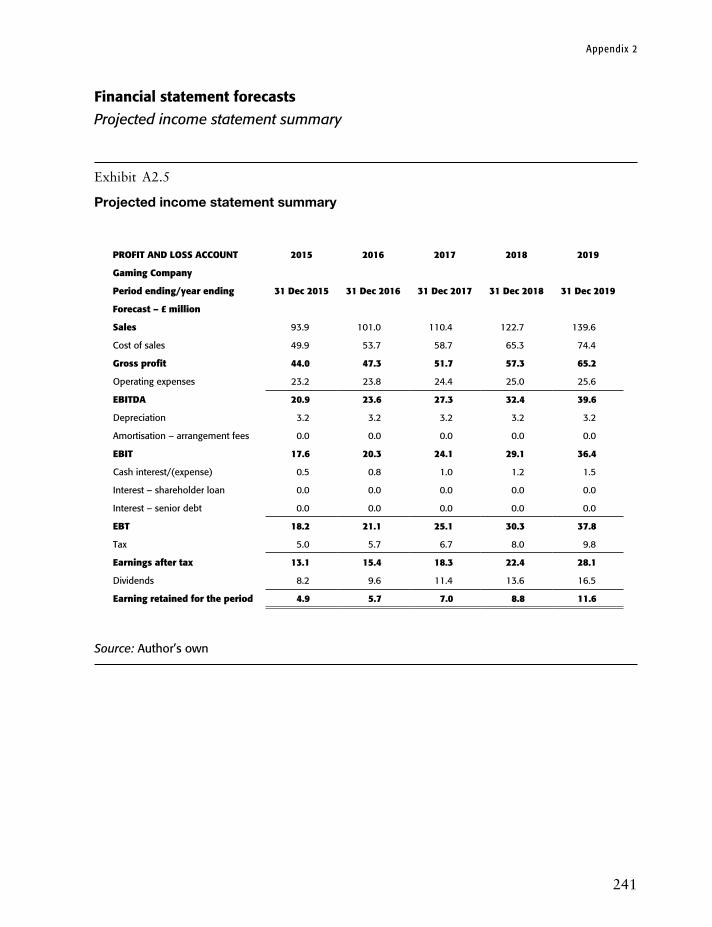

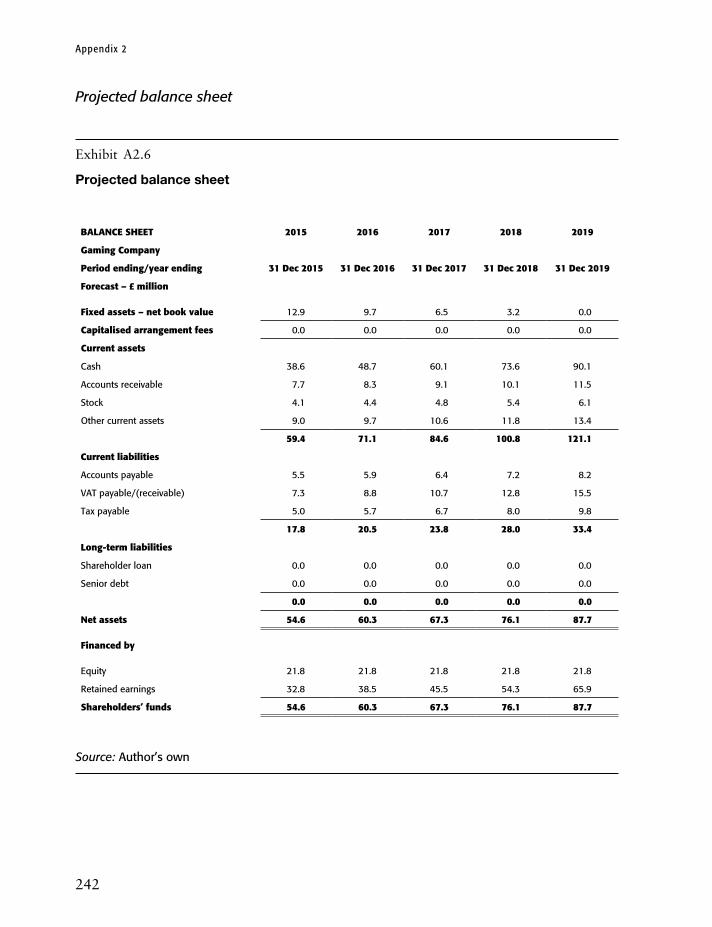

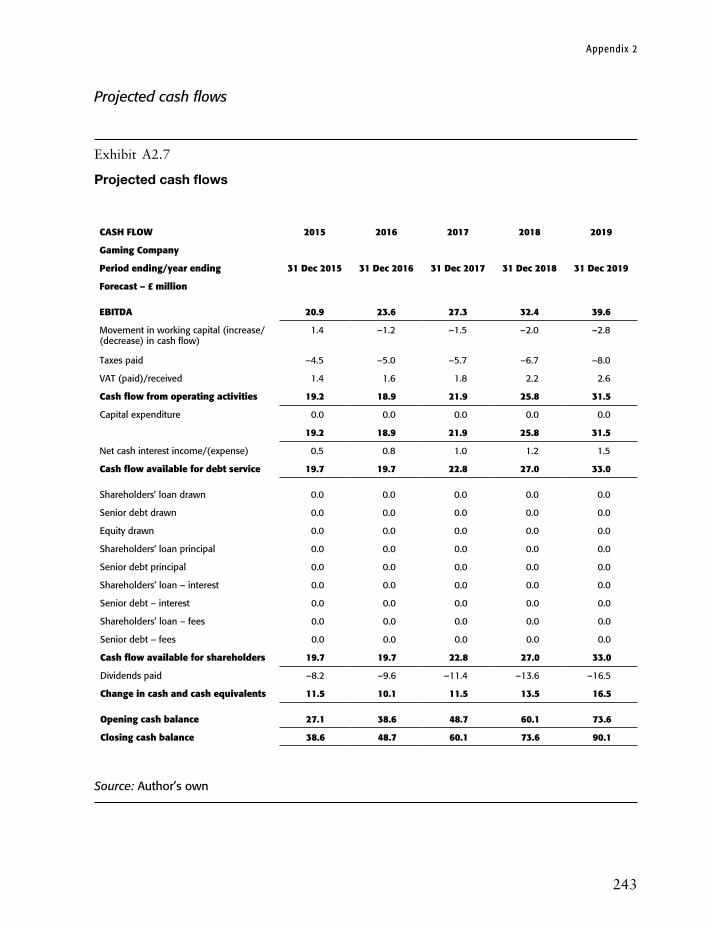

Financial statement forecasts 241Projected income statement summary 241Projected balance sheet 242Projected cash flows 243Projected financial ratios 244

Acquisition and transaction information 244

Appendix 3 Strategic planning case study 245Exercise 245

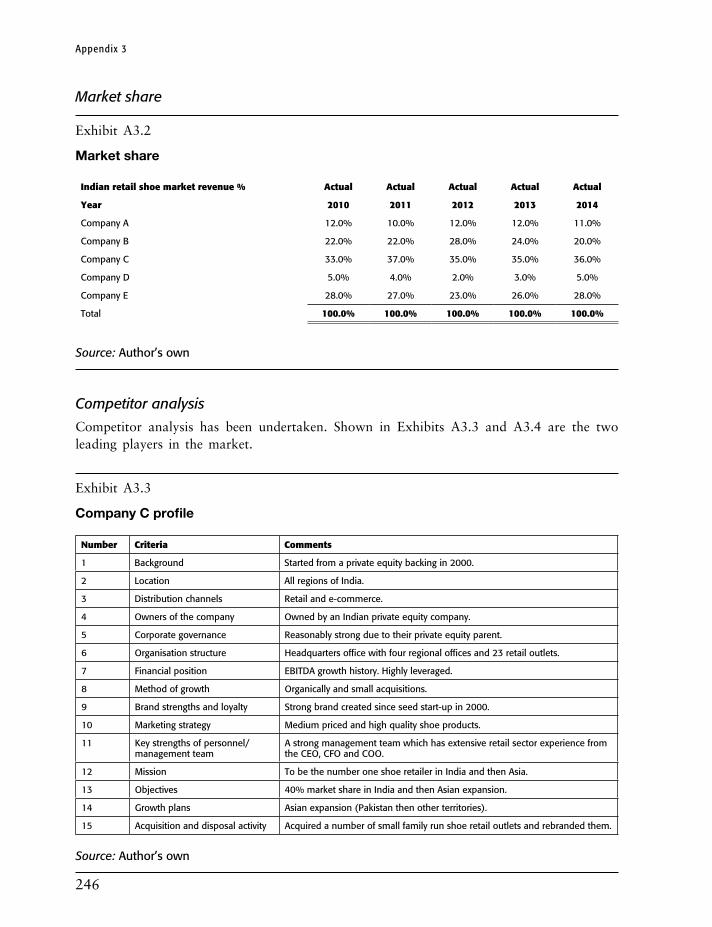

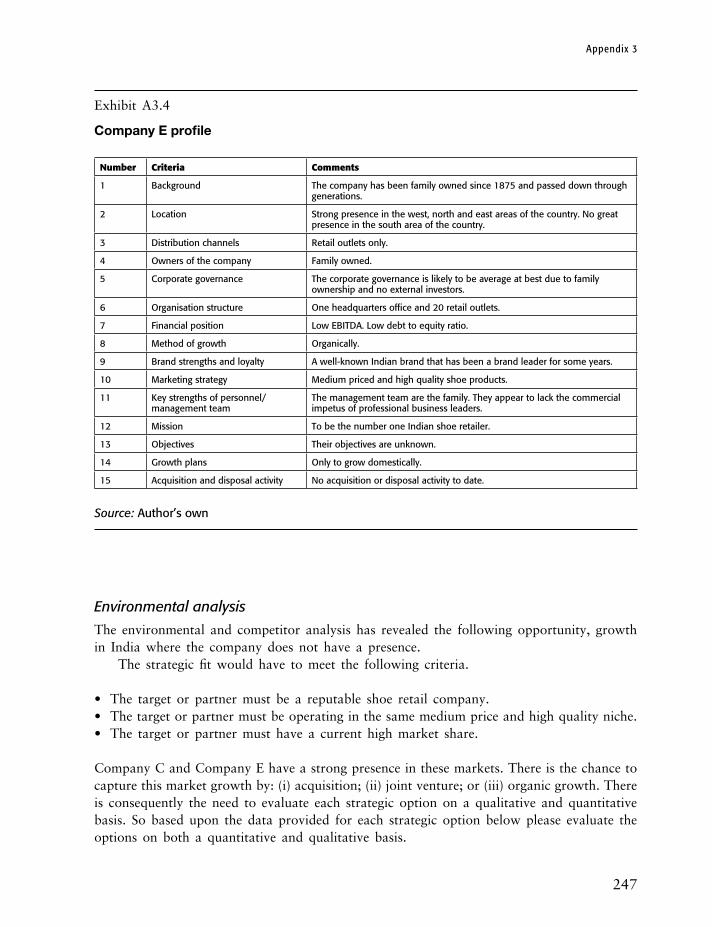

Market size/growth 245Market share 246Competitor analysis 246

xii

Contents

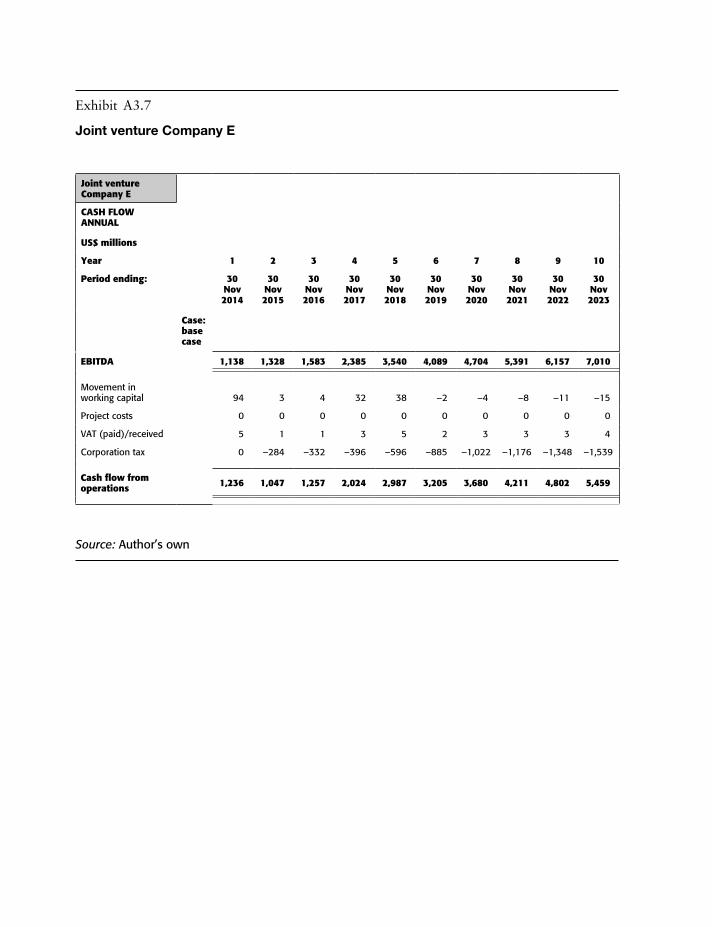

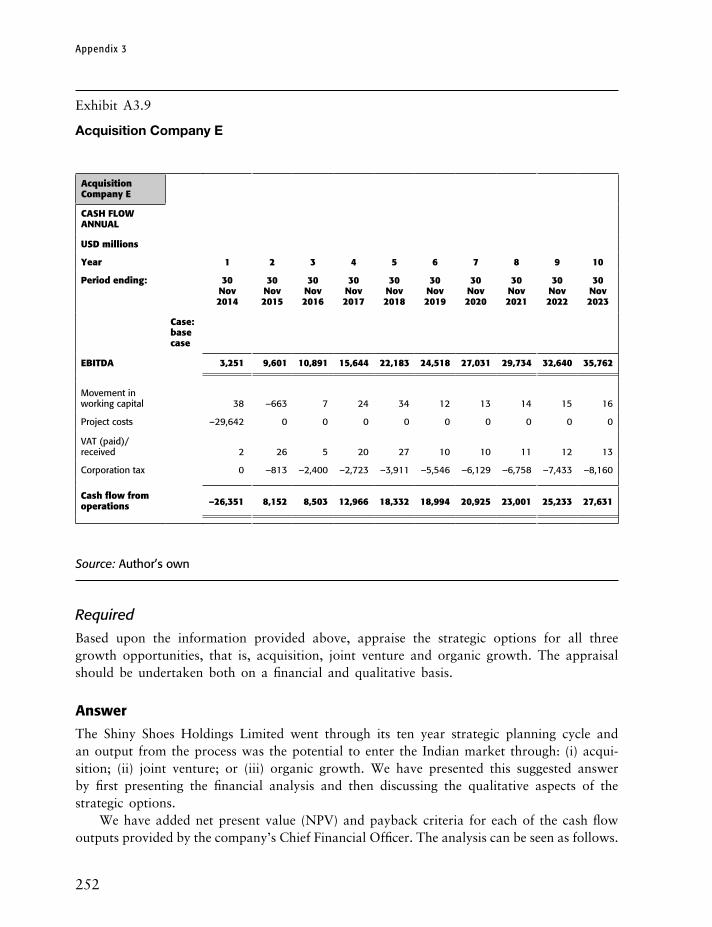

Environmental analysis 247Financial analysis 248Required 252

Answer 252

Glossary 260

xiii

Acknowledgements

I would like to dedicate this book to all the people who have been influential in my career. I would also like to make a special acknowledgement to my family for their support.

xiv

About the author

David Whittaker is an experienced finance and commercial professional who has supported and added value to strategic, financial and commercial decision making in corporations for over two decades. He is a business school graduate and a chartered management accountant. He has led several seminars and training courses. He has published four other successful Euromoney titles.

xv

Introduction

This book has been written in order to give readers the opportunity to gain skills and knowledge which integrate corporate strategy with finance. Furthermore, this book will assist readers to enhance the business value creation process in a more controlled and less risky way.

It addresses the areas of corporate strategy and growth supported by a methodology of maximising value at minimal risk. The sources of finance that can support the corporate strategy and growth are discussed. Other investment decisions to increase the value of the corporate over the corporation’s life cycle are discussed. Other areas are addressed including the key documentation for engaging with potential investors or buyers, the necessity to prepare credible projections, how to manage risks and critically evaluate corporate invest-ment opportunities.

It is important to note that the figures, illustrations or the case studies used in this book do not represent any past, current or indeed future corporate finance transactions or projects of any kind. The numbers and results contained herein are purely fictional.

David WhittakerAugust, 2014

1

Chapter 1

Strategy and corporate growth

Strategic planning

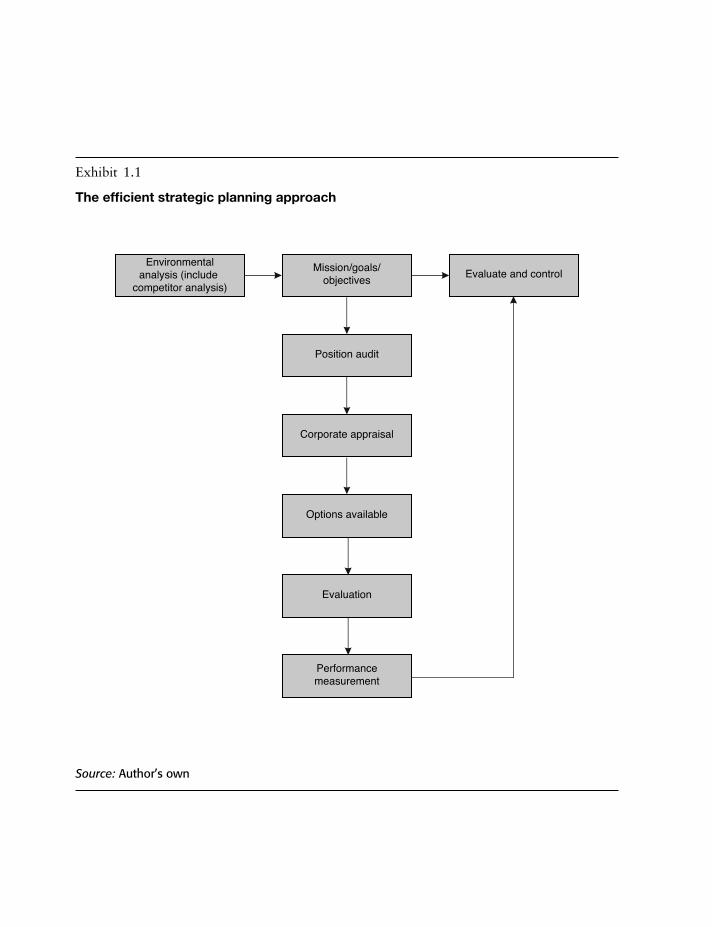

Strategic planning can be defined as an organisation’s process which defines its strategic direction and decision making in order to fulfil its goals, mission and vision. We will now discuss the efficient strategic planning approach. This is a framework that allows a company to achieve its goals, mission and vision in an efficient and effective manner.

Efficient strategic planning approach

The efficient strategic planning approach shown in Exhibit 1.1 outlines a basis for sustain-able corporate growth and competitive advantage. We will discuss this approach in more detail below.

Mission, goals and objectives

The mission statement outlines the fundamental purpose of the organisation. For example, an engineering, procurement and construction (EPC) contractor may have the mission of providing quality infrastructure at competitive prices thus maximising the value of its share-holders. The objectives may be to grow the company organically and by acquisition in the Eastern European market achieve a goal by the end of year five of 200% growth in both turnover and earnings before interest taxation depreciation and amortisation (EBITDA). Objectives need to be supported by measurable goals with a clearly defined timescale to achieve them. In summary, all objectives should be specific, measurable, agreed, realistic and time (SMART) deliverable.

Exhibit 1.1

The efficient strategic planning approach

Environmentalanalysis (include

competitor analysis)

Mission/goals/objectives Evaluate and control

Position audit

Corporate appraisal

Options available

Evaluation

Performancemeasurement

Source: Author’s own

Strategy and corporate growth

3

Position audit

The position audit will allow senior management to have a clear view of where the business is today. The important areas that will have to be addressed include the following.

• Have the organisation’s goals and objectives been achieved? • How does the turnover versus profitability look?• How well is the working capital being managed?• How well is the company able to service the debt levels of lenders and provide returns

to shareholders or investors? • How do employee performance management issues look? That is, are key management

team members performing against their objectives?• How good are the organisation’s information systems? • What critical management information is lacking?• How efficient are the sales processes and how strong are the order book and contract

pipeline?• Does the organisation have any future business development opportunities?• How well is the organisation performing financially and what is the financial strategy and

is it suitable to support the future growth plans?

It is inevitable that a list of actions will come from the position audit. These actions will be necessary in order to take advantage of opportunities and the potential impact of threats. It is important that the list of actions is translated into a managed and planned execution program.

In summary, a business position audit provides a clear snapshot of a business as it stands at the present moment. It represents a systematic assessment of the current strength and weaknesses of an organisation as a pre-requisite for future strategic planning.

Corporate appraisal

Corporate appraisal is often referred to as strengths, weaknesses, opportunities and threats (SWOT) analysis. This process is a critical evaluation of the strengths and weaknesses, opportunities and threats in relation to the internal and environmental variables impacting an organisation in order to evaluate the organisation’s position prior to drafting the long-term strategic plan.

In summary, strengths and weaknesses are normally variables within the organisation and opportunities and threats are normally outside the organisation.

Examples of potential sources of strengths, weaknesses, opportunities, and threats are as follows.

• Strengths. # The advantages of the business or product proposition. # The product capabilities given the customer’s needs. # The competitive advantages in terms of competitors, for example, better distribution

channels, better technology. # The innovative aspects of the product/business.

The Strategic Corporate Investments Handbook

4

# Any unique selling points. # The resources, assets, people, for example, a team with critical mass. # The experience, knowledge and data. # The processes, systems, IT and communications.

• Weaknesses. # The disadvantages of the business or product proposition. # The gaps in capabilities or market needs. # The competitive weakness versus other similar businesses. # The financial constraints such as a high debt capacity. # Any poor processes and systems. # A lack of necessary accreditations. # Any restrictions on IT, systems or communications.

• Opportunities. # The market developments. # The competitors’ weaknesses or vulnerabilities. # Any geographical or export opportunities. # Any seasonal influences or trends. # The current styles or trends. # Any niche markets or specialist segments of existing markets.

• Threats. # The political factors which may affect the company. # The legislative changes such as taxation. # The environmental pressure such as emissions, pollution and so on. # The IT or computer technology that may reduce the demand for the company’s prod-

ucts and services. # Any new competitors entering the market with attractive and competitive offerings. # The consumer demand decrease due to recessionary impacts. # The technological threats such as new methods of distribution such as e-commerce

which may act as an alternative to retail outlet distribution.

An ideal way to tackle potential opportunities is to match the organisation’s core strengths or competencies where possible. For example, a livestock farm has the opportunity of using its chicken pieces for fried chicken fast food outlets in developing markets where fast food demand is likely to grow as the lower middle class or the socio-economic profile is increasing and has the disposable income to purchase such goods and services. The know-how required to grow from the core skills of a chicken producer to a strategy of forward vertical integra-tion into the fast food outlets is lower than that required to organically grow into something totally unrelated to the organisation’s core skills. Indeed, the development costs and time associated with such a business strategy are also likely to result in lower organic growth in a totally unrelated business. A further example of organic growth from a company’s core business is a commercial airline that may have a growth opportunity of expanding into freight markets by offering international air cargo services. This will obviously involve the use of existing assets (that is, aircraft) in order to generate further business prosperity and cash flows.

Strategy and corporate growth

5

Threats can often be avoided by utilising the organisation’s strengths.The organisation’s weaknesses can often be addressed in the form of an opportunity.

Their weaknesses must be minimised in order to avoid the potential threats.

Environmental analysis

Environmental analysis is a process which is required in order to draft the strategic plan for the organisation. Approaches such as political-economic-social-technological-legal (PESTL) can be used to undertake environmental analysis.

Looking specifically at the PESTL approach, we will now address each of the following areas.

• Political risk – this can relate to government instability or non-payment of government obligations.• Economic risk – this can relate to interest rate, exchange rate and inflation amongst other areas.• Social risk – this can relate to social unrest, labour disputes, changes in consumer tastes

and behaviour.• Technological risk – this can relate to the introduction of new technology as a substi-

tute product, for example, Wi-Fi internet connection replacing cable-based technology or e-commerce replacing some retail outlets.

• Legal risk – this can relate to the change in laws affecting the business or project. An example of this is where a change in tax legislation may adversely affect the taxation cash flows for a business.

Competitor analysis

Competitor analysis is also a very useful technique which is often overlooked by most corporates. Competitor analysis can be defined as a strategic and marketing evaluation of both strengths and weaknesses of both current and potential competitors in the market. It will help to identify both opportunities and threats to the company. It will allow the corpo-rate to fine-tune its marketing strategy in terms of the price, product, promotion and place (distribution) elements of the marketing mix. Corporate strategy can also be re-addressed in terms of acquisition opportunities, disposal opportunities, joint venture opportunities, organic growth opportunities and so on.

The most common approach is to provide a detailed profile of each of the company’s major competitors. This will include background, that is, the location of premises, offices and distribution channels. Ownership will include who owns the company, their corporate governance and organisation structure. Also included is the financial position of the company, that is, its financial structures, profitability and liquidity. The company’s method of growth (organic, acquisitive or collaborative) will be included, together with the products offered by the company and their features, brand strength and loyalty, and the company’s patents and licences. The marketing strategy of each company should be considered – the kind of advertising themes, promotional mix, market segments, market shares, growth rates, distri-bution channels, joint ventures, geographic regions, pricing and discounting. The company’s personnel should be understood. What are the key strengths of the management team and the management style? It would of course be useful to understand the corporate strategy of

The Strategic Corporate Investments Handbook

6

each of the competitors, that is, their mission, objectives, growth plans and their acquisition and disposal activity.

Options available

There are a number of strategic options that are available which could be used in order to respond to an opportunity or a threat. These options can include organic growth, acquisition or merger, joint ventures, franchising or licensing, exporting, divestment, do nothing, withdraw from the market or consolidate or rationalise. Each of these areas will be discussed in detail.

Organic growth strategies are business development techniques that promote corporate growth by increased output and larger sales volume of the existing business or a start-up which requires assembling the management team, planning and promoting the business. The opposite of organic growth strategies includes mergers and acquisitions activity, and takeovers of competitors and synergistic businesses.

An acquisition is the purchase of one company by another for a certain consideration package. This consideration package can be made up of cash, shares and debt according to how the parties see fit. The acquirer obviously has a controlling interest over the target company.

A merger represents a business combination of two companies bringing together their operations on certain financing terms, that is, share exchanges, debt or cash financing.

A joint venture is a business arrangement whereby two or more parties agree to work together to undertake a certain opportunity or project. Often each party will contribute an agreed amount of equity. The parties to the joint venture are responsible for the profits and losses arising from the venture often through a specifically incorporated vehicle such as a limited company.

A divestment is the opposite of making an investment. It represents the action of disposing of a company’s asset through a sale.

The doing nothing option obviously equates to a course of action that involves not changing one’s strategic position.

A strategic option may be considered which involves leaving the market. For example, an airline which is experiencing a very poor business performance for a certain route or set of routes may withdraw its service from that particular market and redeploy its aircraft and staff to alternative routes and destinations which may lead to more business prosperity.

The strategic option of rationalisation may involve a restructuring or turnaround of an underperforming business. A cash negative business can be transformed into a cash generative business. Where a restructuring decision is required there is a need to plan the initiative in both words and numbers. Ideally a restructuring or cost reduction plan needs to be included in the budget and certainly the five or 10-year strategic plan of the organisation. The stra-tegic option of undertaking a restructuring should then be performance managed in terms of feedback and control against the planned financials and any non-financial key performance indicators (KPI) identified.

Evaluation

The evaluation stage involves the evaluation of each of the strategic options that a company may consider. Each strategic option should be evaluated both in terms of the qualitative

Strategy and corporate growth

7

advantages and disadvantages of the proposed strategy and the quantitative effect on the forecast financial position of the organisation.

Performance measurement

The post-investment financials and performance is where the management team are running the company with a primary objective of providing an adequate return to its shareholders by maximising the value of the company, servicing the debts of its lenders, and remaining financially viable. It is important that optimal processes and controls are evident in the organisation. Consequently, a unique edge which this book seeks to address is the process for ensuring optimal planning and control of the corporate investment.

Conclusion

We strongly recommend that all businesses undertake a five to 10-year plan on an annual basis. This will ensure that the organisation is both strategically and financially prepared to grow sustainably and it can pre-empt and react against any opportunities or threats appropriately. This will involve going through the efficient strategic planning approach as outlined in Exhibit 1.1. It would be necessary to revisit the mission statement, evaluate the last strategic plan’s objectives and targets, undertake an environmental analysis, a position audit and a corporate appraisal, consider the options appraisal and evaluate this. The plan should be put in action by the key directors and senior executives with targets. The targets should be measurable in the form of KPIs.

Marketing strategies

The concept of marketing and the application of marketing strategies to your business is an extremely useful tool kit in order to fine-tune your business offerings. The marketing concept can be defined as follows.

The management process responsible for identifying, anticipating and satisfying customer requirements profitably.1

The tool kit that is used in order to meet this is called the marketing mix of product, price, promotion and place (4 P’s). This is a set of variables an organisation can use to influence a customer’s purchase decision for goods or a service.

• Product: this represents the product or service’s package of benefits, including guarantees, warranties and after sales service.

• Price: the pricing element includes price promotions, discounts and periods of credit, interest free credit and payment terms offered for the goods or services.

• Promotion: the promotional mix or promotional plan is comprised of four subcategories: advertising, personal (or direct) selling, sales promotion and public relations.

The Strategic Corporate Investments Handbook

8

• Place: place is where the product can be purchased from, for example, channels of distri-bution, such as retail outlets and online e-commerce. Typical distribution channels today include the internet, email, shops/branches, post, telephone, catalogues, other distributors and so on.

The primary goal of any marketing strategy is to satisfy the strategic goals of the company, for example, competitive strategy must support the corporate strategy, mission and the goals of the company.

The mission statement and corporate objectives should be reviewed in conjunction with the organisation’s five or 10-year plan.

It would be necessary to audit the external marketing environment by using the PESTL approach. Competitive benchmarking of ‘marketing mix’ practices would need to be under-taken of both your own company and in comparison with your competitors. The company must obtain regular market intelligence, evaluate this and make recommendations. It is recommended that the company formulates and evaluates its own competitive strategy. The strategic marketing process should lead to the production of a detailed action plan. The marketing strategy should be reviewed and feedback obtained periodically. It would be necessary to undertake a regular marketing audit in order to maintain a competitive position in the market.

Product positioning

Indeed there are different ways of fine-tuning a company’s marketing mix. Competitive positioning is about the company’s role in the competitive marketplace. Undifferentiated (or homogenous) positioning is the targeting of an entire market with a single marketing mix (the 4 P’s). Differentiated targeting is the targeting of different market segments and a specific marketing mix for each segment. Concentrated positioning is the targeting of a single market segment only with a single marketing mix, for example, single segment focus.

The product life cycle illustrates the succession of stages that a product goes through in terms of its sales or market share. The market environment in which a product is sold is always changing and, therefore, must be managed as it moves through a succession of different stages. A product or service typically goes through the stages of introduction, growth, maturity and decline. There would need to be different marketing strategies applied at different stages of the product’s life cycle.

Branding means a trade name, symbol or logo synonymous or identifiable to an organ-isation, or its product or service, for example, Adidas and its associated logo. Branding has certain advantages of marketing, such as the ability to support new products and services that are launched, as consumers associate with and know the brand that has strong loyalty and recognition. If a product or service has a strong brand it is possible to sell your products or services at a premium price than less well-branded products. Strong branding can have the benefit of being able to grow the business by franchising or licensing, an example of this is McDonalds. It is often the case that branded products and services have a longer life cycle.

Indeed brands can be used to a company’s advantage in order to increase the value of a company. A line extension strategy may be used in order to launch new sizes or flavours of

Strategy and corporate growth

9

a product under the same brand name. A brand extension strategy can be adopted whereby a new product can be launched using the same brand name.

Market segmentation is the grouping of customers, with each sub-group or segment of customers having a common need, want or value. Each sub-group or segment will be affected by different targeting strategies; they will behave differently and respond differently to vari-able ‘tailored’ marketing mixes. There are certain advantages that can be associated with a market segmentation strategy, such as the ability to match closely features of a product or service to certain customer groupings or niches. Thus, the company may be able to produce a greater level of customer satisfaction. It may be possible that by segmenting the market that the company will be able to create better brand and customer loyalty. A segmenta-tion marketing strategy may lead to the more efficient use of marketing resources such as advertising. However, on the other side of the coin, there are a number of disadvantages and indeed reasons not to engage in a market segmentation strategy. The first reason is that the segment may not be profitable enough to serve. It may be that there is not sufficient promotional media that can economically create consumer awareness. The segment may already be very competitive. Also, there may be circumstances where the company lacks the competencies to deliver the product or service but an acquisition is uneconomic.

Relationship marketing is about devoting marketing resources to the maintenance of the company’s existing customer base, as well as trying to attract new customers. Customer loyalty and retention has become critical to the long-term survival of companies; relationship marketing aims to build excellent relationships with customers in order to retain their loyalty.

Below are a number of management accounting methods that could be used in order to add value to the marketing process. These methods can help to create strategies to improve customer or product profitability in areas such as changing the price of the products, stimu-lating the volume sold, reducing the amount of support that incurs specific customer or product cost. It may help to make the decision to stop selling a certain product or to sell it to a certain customer grouping.

Customer profitability analysis involves relating specific costs to serving customers or groups of customers, so that their relative profitability can be assessed. It would be usual to use a closely correlated driver of the costs for allocation purposes, that is, similar to an activity-based costing approach. Customer profitability analysis focuses on cost reduction by understanding how customers consume different support resources, for example, processing, delivery, sales visits, telephone support and internet support. It allows an organisation to concentrate on the most profitable of its customers.

Direct product profitability analysis is a decision making tool that helps a company by providing a better indication of the profitability of products. The process allocates direct product costs to individual products. It would be usual to use a closely correlated driver of the costs for allocation purposes, that is, similar to an activity-based costing approach. These costs are subtracted from the gross profit to derive direct product profitability for each product. The normal indirect costs attributed to products would be distribution, warehousing and retailing. Direct product profitability would ignore indirect costs such as head office overheads, only product specific fixed (indirect) cost would be analysed.

Distribution channel profitability is about relating specific distribution costs to serving customers or groups of customers, so that their relative profitability can be assessed. Typical

The Strategic Corporate Investments Handbook

10

distribution chain channels today include the internet, email, shops/branches, post, telephone, catalogues, other distributors and so on.

Post-investment financial and performance management

Exhibit 1.2 shows a post-investment financial and performance management process model that seeks to maximise the value of the company invested in along the way of the investment period and throughout the corporate life cycle. Essentially this involves the process of strategic planning, budgeting and target setting, monitoring against the actual performance and the management. We can define strategic planning as the process that sets out where the company is likely to want to go in terms of its strategic vision. This is often defined through the use of a mission statement, which summarises the fundamental purpose of an organisation.

Exhibit 1.2

Post-investment financial and performance management

Strategic plan

Budgets and targets

Actuals Performancemanagement

Source: Author’s own

Strategy and corporate growth

11

Strategic planning also involves the process of looking at the business in terms of its SWOT analysis. A SWOT analysis can help a business to understand how it is positioned relative to its market and competition as discussed above.

Another area in which to attain a competitive advantage is through leading edge budgeting techniques. Budgets and targets can be set by traditional budgeting techniques, such as zero-based budgeting and activity-based costing/management (ABC/M). The purpose of budgeting is to help the organisation to provide a forecast of revenues, expenditures, profit and loss, cash flow and balance sheet over the next accounting year usually on a monthly basis. The budgeting process will seek to set targets on a functional and departmental level that links to the overall financial goals of the company. It is important that the first budget year ties up with the forecast of the company’s deals, financial projections or financial model, which is translated into budgetary terms for the organisation. The financial model should be used for reforecast purposes by the organisation.

It is advantageous for the organisation to promote efficient budgeting approaches that avoid being non-incremental and are more aligned to a zero-based budgeting. This is a method of budgeting in which all expenses must be justified for each budget period. Zero-based budgeting starts from a ‘zero base’ and each department within the company is evaluated for its needs and costs. Budgets are then forecast around what is needed for the forthcoming budget period. It is irrelevant whether the budget is higher or lower than what has been spent historically or allocated as budgets for previous years. The clear advantage is that a very lean and efficient budget is set for the organisation which will obviously help to improve the EBITDA year on year and plan the overall financial position.

A further area to gain a great advantage and improve EBITDA, which we know is a critical target for corporate financial success, is the use of ABC/M techniques.

ABC/M is a management accounting technique that identifies activities in an organisation and assigns the cost of each activity with resources to all products and services according to the actual consumption of the resources. This technique attributes more indirect costs or overheads to the direct costs compared with conventional costing models. Consequently, ABC/M allows an organisation to have the following strategic advantages.

• To allocate more resources on profitable products, departments and activities.• To control the costs at any per product level and on a departmental level.• To find unnecessary costs that may be eliminated.• To set the price of a product or service more strategically and realistically. • To identify the profitability of customers.

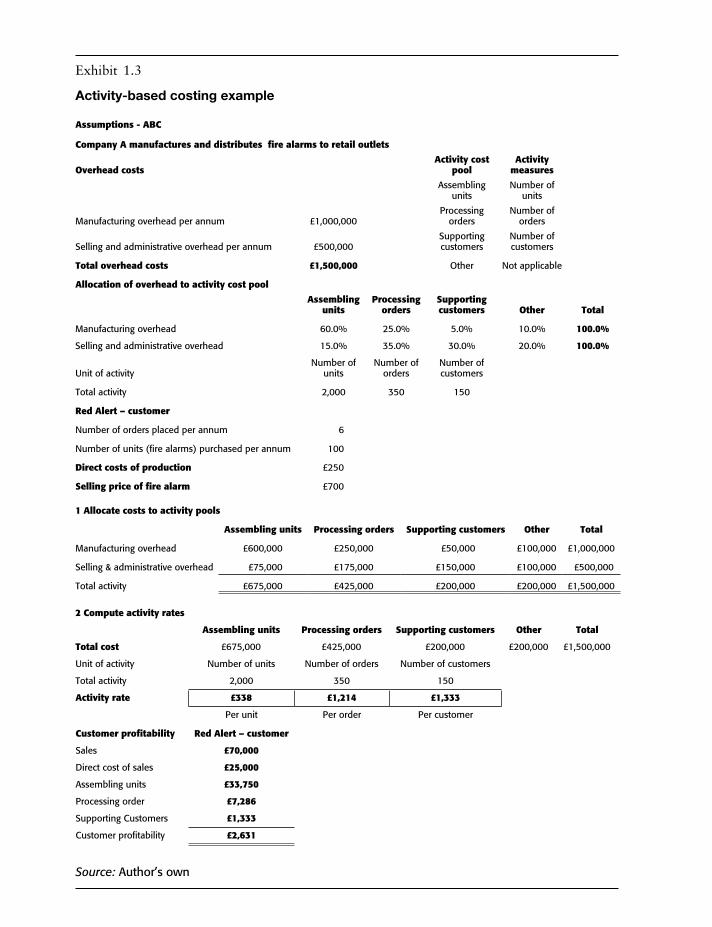

An example of the use of ABC/M can be seen in Exhibit 1.3. This shows the use of activity-based costing techniques for customer profitability purposes. The general process that it adopted is as follows.

• To allocate costs to activity pools.• To compute activity rates.• To measure customer profitability.

Exhibit 1.3

Activity-based costing example

Source: Author’s own

Assumptions - ABC

Company A manufactures and distributes fire alarms to retail outlets

Overhead costs Activity cost

poolActivity

measures

Assembling

unitsNumber of

units

Manufacturing overhead per annum £1,000,000 Processing

ordersNumber of

orders

Selling and administrative overhead per annum £500,000 Supporting customers

Number of customers

Total overhead costs £1,500,000 Other Not applicable

Allocation of overhead to activity cost pool

Assembling

unitsProcessing

ordersSupporting customers Other Total

Manufacturing overhead 60.0% 25.0% 5.0% 10.0% 100.0%

Selling and administrative overhead 15.0% 35.0% 30.0% 20.0% 100.0%

Unit of activityNumber of

unitsNumber of

ordersNumber of customers

Total activity 2,000 350 150

Red Alert – customer

Number of orders placed per annum £006

Number of units (fire alarms) purchased per annum £100

Direct costs of production £250

Selling price of fire alarm £700

1 Allocate costs to activity pools

Assembling units Processing orders Supporting customers Other Total

Manufacturing overhead £600,000 £250,000 0£50,000 £100,000 £1,000,000

Selling & administrative overhead 0£75,000 £175,000 £150,000 £100,000 0£500,000

Total activity £675,000 £425,000 £200,000 £200,000 £1,500,000

2 Compute activity rates

Assembling units Processing orders Supporting customers Other Total

Total cost £675,000 £425,000 £200,000 £200,000 £1,500,000

Unit of activity Number of units Number of orders Number of customers

Total activity 2,000 350 150

Activity rate £338 £1,214 £1,333

Per unit Per order Per customer

Customer profitability Red Alert – customer

Sales £70,000

Direct cost of sales £25,000

Assembling units £33,750

Processing order £7,286

Supporting Customers £1,333

Customer profitability £2,631

Strategy and corporate growth

13

This approach is demonstrated in Exhibit 1.3 for a company that manufactures and distributes fire alarms to retail outlets. There is a requirement to find the profitability of the Red Alert customer. Each activity in the process is allocated an ‘activity cost pool’, that is, assembling units, processing orders and supporting customers. The activity cost pools are then given an activity measure which most closely correlates or drives the cost, that is, the number of units for assembly, the number of orders for processing and the number of customers needing support. These are often called ‘cost drivers’.

The first part of the process is to allocate costs to activity pools. From researching a significant amount of historic data it has been found that a certain percentage of time is attributable to certain tasks that drive the manufacturing, selling and administration overheads. The activities that drive these costs are assembling units, processing orders and supporting customers. The section ‘1 Allocate costs to activity pools’ shows the allocation of overheads to the activity pools. This is simply the allocation of the overhead costs to the activity cost pool by multiplying the percentages.

The next step is to compute the activity rates, that is, the cost per activity unit. This involves calculating the costs of each of the cost drivers or activity pools, that is, assembling units, processing orders or supporting customers. By referencing the next section ‘2 Compute activity rates’, we find the total cost of each activity pool is linked in. The total activity for each pool is also linked in order to compute the activity rate in pounds. In summary, we have activity rates for assembling units of £338 per unit assembled. We have an activity rate of £1,214 per order for the processing of orders. We have an activity rate of £1,333 per customer for support.

The ‘customer profitability’ output shows the calculation of the customer profitability. Sales are equal to the number of units purchased per annum at the selling price per fire alarm. The direct cost of production is equal to the rate per unit at the number of units purchased. The ‘Assembly unit’ cost is equal to the number of orders placed by Red Alert at the activity rate for assembling units. The processing order cost is equal to the number of orders placed by Red Alert at the activity rate for processing orders. The cost of supporting customers is the activity rate per customer. Customer profitability is simply calculated by sales less total costs.

ABC exercise

Using Exhibit 1.3 inflate the overhead costs by 25% and assign the costs to the activity pools, compute the activity rates and derive the customer profitability for the Red Alert customer.

Capital budgeting

The ability for a company to make financially viable incremental business decisions involving large amounts of capital investment is critical and can be managed and controlled through adequate capital budgeting processes and techniques.

The Strategic Corporate Investments Handbook

14

Capital investment appraisal techniques can be used when a company has incremental business opportunities or projects to appraise. Capital investment appraisal typically involves the use of discounted cash flow techniques (DCF) to undertake the financial evaluation of an incremental capital expenditure decision and the benefits and costs associated with that investment opportunity. Capital investment appraisals involve the entire process of plan-ning expenditures whose returns are expected to extend beyond one year. The very obvious examples of capital expenditures are plant and machinery, buildings and land. The less obvious types of investments are research and development projects, advertising and promo-tional campaigns.

Before we start to look at the example of a capital investment appraisal shown in Exhibit 1.4, it is best to consider the main definitions used in capital investment appraisals.

The payback period for a capital investment decision can be either expressed in undis-counted terms or discounted cash flow terms. It is simply the amount of time in years and months that it takes to breakeven in cash flow terms either discounted or undiscounted.

The internal rate of return (IRR) for a capital investment decision can be defined as the discount rate at which the net present value (NPV) of the future stream of net cash flows equal zero. This rate can be linked to the company’s weighted average cost of capital (WACC) for financial evaluation purposes. Therefore, ignoring any qualitative factors if the project’s IRR exceeds the company’s WACC, the project will incrementally add value to the company as a whole.

The NPV for a capital investment decision can be defined as the value of a series of cash flows discounted at the required rate of return to derive a value in today’s money. It accounts for the time value of money in the discounting process, that is, the opportunity cost of the rate of return is considered. Therefore, ignoring any qualitative factors, if the project’s NPV exceeds zero then the project will incrementally add value to the company as a whole.

In Exhibit 1.4, a retail company has raised £300 million of capital which it is now free to invest in a number of retail outlets, that is, buying the properties’ leases of 10 years and opening and running stores in certain areas. The project’s economic life is 10 years and the timeline and period of analysis reflect this.

Strategy and corporate growth

15

Exhibit 1.4

Capital investment appraisal

Cash flow 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Capital investment appraisal

Period ending 31 Dec 2011

31 Dec 2012

31 Dec 2013

31 Dec 2014

31 Dec 2015

31 Dec 2016

31 Dec 2017

31 Dec 2018

31 Dec 2019

31 Dec 2020

Forecast – £ million

EBITDA 28.0 28.1 28.1 28.1 28.2 28.2 28.2 28.2 28.2 28.2

Movement in working capital (increase/(decrease) in cash flow) –14.5 –0.1 –0.1 –0.1 –0.1 –0.2 –0.2 –0.2 –0.2 –0.2

Taxes paid 0.0 –5.2 –5.7 –5.8 –5.8 –5.9 –6.0 –6.1 –6.2 –6.3

VAT (paid)/received –3.8 1.9 1.9 1.9 1.9 1.9 1.9 1.9 1.9 1.9

Cash flow from operating activities 9.8 24.6 24.1 24.1 24.1 24.1 23.9 23.8 23.7 23.7

Capital expenditure –84.4 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

–74.5 24.6 24.1 24.1 24.1 24.1 23.9 23.8 23.7 23.7

Net cash flow –74.5 24.6 24.1 24.1 24.1 24.1 23.9 23.8 23.7 23.7

Summary

Capital investment appraisal

Project results Base case Capital evaluation criteria

Net present value £48.1 >£0

IRR 29.2% >12%

Discounted payback period

Payback year 2016 2014

Payback month 1 1

Payback period

Payback year 2015 2013

Payback month 1 1

NPV/£ invested £0.57 >£1.2

Source: Author’s own

For the purpose of evaluating these incremental projects the finance director of the company in conjunction with the board of directors has formulated some capital investment appraisal criteria as follows.

The Strategic Corporate Investments Handbook

16

A discount rate has been set at 12%, this represents the company’s WACC and effectively the hurdle rate for discounted cash flow (DCF) analysis purposes. The investment appraisal criteria or benchmarks such as NPV, IRR discounted and undiscounted payback years can be seen in the Summary.

Further criteria are made regarding the NPV per pound sterling invested. This is a useful metric when a company has several capital investment appraisals to consider and has raised limited funds for investment. In financial speak we call this capital rationing and the organisa-tion will seek to maximise the NPV per pound sterling of capital invested. This can be used as a ranking mechanism for the allocation of capital subject to other evaluation criteria both quantita-tive and qualitative.

It is because we are looking at cash investments, that the investment appraisal model will not include accounting adjustments, and the key outputs will be based upon cash flow forecasts. However a ‘profit and loss’ extract is included in the profit and loss output. The profit and loss extract is required in order to compute the cash flow timing effects of the working capital in the cash flow output.

Turning our attention to the cash flow we can see that the EBITDA is linked from the profit and loss account. The movement in working capital, taxes paid for both corporation tax and VAT are included in order to derive a cash flow from operating activities. The capital expenditure is also included in order to derive the net cash flow for the project which is pre funding.

First, the NPV is shown, which represents the stream of cash flow over the 10-year period discounted at the 12% discount rate. Excel’s NPV function can assume that the cash flows arise either at the beginning of the period or at the end of the period. In this particular example the cash flows arise at the end of the period. If we wanted to make the assumption that the cash flows arise at the beginning of the period we would simply add a ‘1’ after the cash flow stream in the NPV formula.

Second, the IRR is shown. The calculation simply takes the stream of cash flows over a 10 year period and uses the discount rate as a guess to find the discount rate at which the NPV equals zero. In order to compute the discounted payback period metric the cash flows are discounted using first principles; the cash flow for each year is multiplied by (1(/(1+r)^n)) where r is the discount rate and n is the year number.

The payback period takes the previous period’s negative cumulative cash flow and the next period’s positive cash flow and assumes equal timings of cash flow throughout the year and calculates the months required to breakeven. The payback period is the same as the logic above except that the cash flows are not discounted.

The NPV per pound sterling invested is calculated by taking the NPV and simply dividing by the capital expenditure.

The results show the base case business compared with the qualitative capital evalua-tion criteria.

Capital investment appraisal exercise

Based upon the a stream of net cash flows arising in Exhibit 1.4, please increase each number by 45%, add logic to the cash flow outputs, and increase the capital expenditure. Develop the analysis further so that you calculate the payback, IRR and NPV for capital investment appraisals.

Strategy and corporate growth

17

Other areas of investment appraisal

There are other areas of investment appraisal that are worthy of our attention. We shall discuss these now with reference to relative examples.

Monthly cash flows

An example of the use of monthly cash flow timing can be seen in Exhibit 1.5. Excel’s ‘XNPV’ formula can be used to calculate the NPV by accessing the discount rate, the net cash flows and the monthly dates. Similarly, the IRR is calculated in cell B12, by using Excel’s ‘XIRR’ formula. The net cash flows are accessed and the range of monthly dates, together with a given discount rate.

The example also includes a cross check to prove that our monthly logic is indeed mate-rially correct. We calculate the number of days per month. We can see the discount factor per month is simply the number of days per month divided by 365 days per year. This is shown cumulatively. The cash flows are discounted by making the following calculation.

Net Cash Flow multiplied by 1/(1+Discount Rate) ^ Discount factor cumulative

The sum of the discounted cash flow gives a very minor difference to the Excel formula.

Monthly cash flows exercise

Based upon the figures used in Exhibit 1.5 use Excel and increase the net cash flow by 25% and the project by 20 years at 1% growth per month, then calculate the NPV, IRR using the XNPV and XIRR formulas and also calculate the NPV from first principles as a cross check.

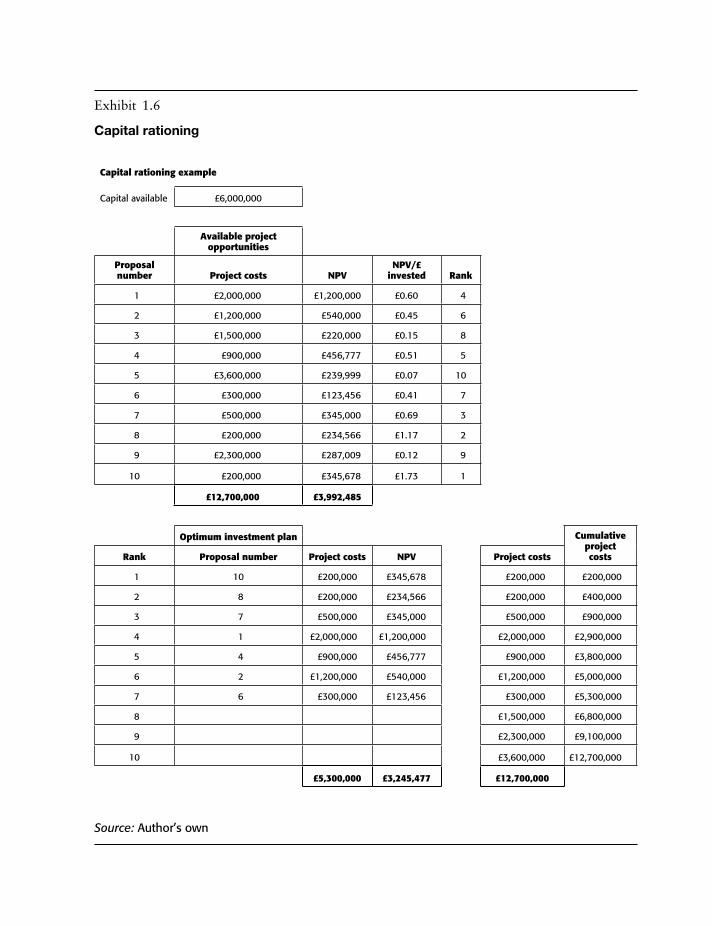

Capital rationing

An example of the use of capital rationing can be seen in Exhibit 1.6 and shows a meth-odology for the available project opportunities given that the company has a limit of £6 million to invest. The illustration shows the available project opportunities available from 1 to 10. The project costs, NPV, and the NPV per pound sterling invested is shown. The projects have been shown by relative ranking in terms of the greatest NPV per pound sterling of capital.

Exhibit 1.6 shows the ranking by project which maximises the NPV for the company given its £6 million capital availability. The project costs are allocated on this basis, together with the NPV.

We can see the optimum investment plan is to invest £5.3 million which will give a £3.2 million NPV. It is important to note that the eighth most attractive investment proposal would take us over the £6 million capital limit and is thus not selected.

Exh

ibit

1.5

NP

V m

ont

hly

exam

ple

CASH

FlO

w

Mon

thly

cas

h fl

ows

Per

iod

/mon

th e

nd

ing

31 D

ec 2

010

31 J

an 2

011

28 F

eb 2

011

31 M

ar 2

011

30 A

pr

2011

31 M

ay 2

011

30 J

un

201

1

Fore

cast

- £

mil

lion

Net

cas

h fl

ow

–1

08,0

00.0

48.3

50.7

53.2

55.9

58.7

Net

pre

sen

t va

lue

£19,

441.

2

IRR

14.4

%

Mon

thly

cas

h fl

ows

firs

t p

rin

cip

les

Day

s p

er m

onth

3128

3130

3130

Dis

coun

t fac

tor

per

mon

th

0.08

490.

0767

0.08

490.

0822

0.08

490.

0822

Dis

coun

t fa

ctor

cum

ulat

ive

0.

0849

0.16

160.

2466

0.32

880.

4137

0.49

59

Year

Net

pre

sen

t va

lue

Dis

coun

ted

cash

flow

s£1

9,25

5.0

–106

,965

.547

.449

.351

.353

.355

.5

Chec

k£1

86.2

0.

96%

Sour

ce: A

utho

r’s o

wn

Exhibit 1.6

Capital rationing

Capital rationing example

Capital available £6,000,000

Available project

opportunities

Proposal number Project costs NPV

NPV/£ invested Rank

1 £2,000,000 £1,200,000 £0.60 4

2 £1,200,000 £540,000 £0.45 6

3 £1,500,000 £220,000 £0.15 8

4 £900,000 £456,777 £0.51 5

5 £3,600,000 £239,999 £0.07 10

6 £300,000 £123,456 £0.41 7

7 £500,000 £345,000 £0.69 3

8 £200,000 £234,566 £1.17 2

9 £2,300,000 £287,009 £0.12 9

10 £200,000 £345,678 £1.73 1

£12,700,000 £3,992,485

Optimum investment plan CumulativeprojectcostsRank Proposal number Project costs NPV Project costs

1 10 £200,000 £345,678 £200,000 £200,000

2 8 £200,000 £234,566 £200,000 £400,000

3 7 £500,000 £345,000 £500,000 £900,000

4 1 £2,000,000 £1,200,000 £2,000,000 £2,900,000

5 4 £900,000 £456,777 £900,000 £3,800,000

6 2 £1,200,000 £540,000 £1,200,000 £5,000,000

7 6 £300,000 £123,456 £300,000 £5,300,000

8 £1,500,000 £6,800,000

9 £2,300,000 £9,100,000

10 £3,600,000 £12,700,000

£5,300,000 £3,245,477 £12,700,000

Source: Author’s own

The Strategic Corporate Investments Handbook

20

Capital rationing exercise

Using Exhibit 1.6 add 25% to each NPV and 22% to each project cost for each of the proposal numbers. Please complete the optimum investment plan based upon the available investment opportunities. Please compute the NPV/pound sterling invested and the relative rank, and prepare the optimum investment plan that maximises the company’s NPV.

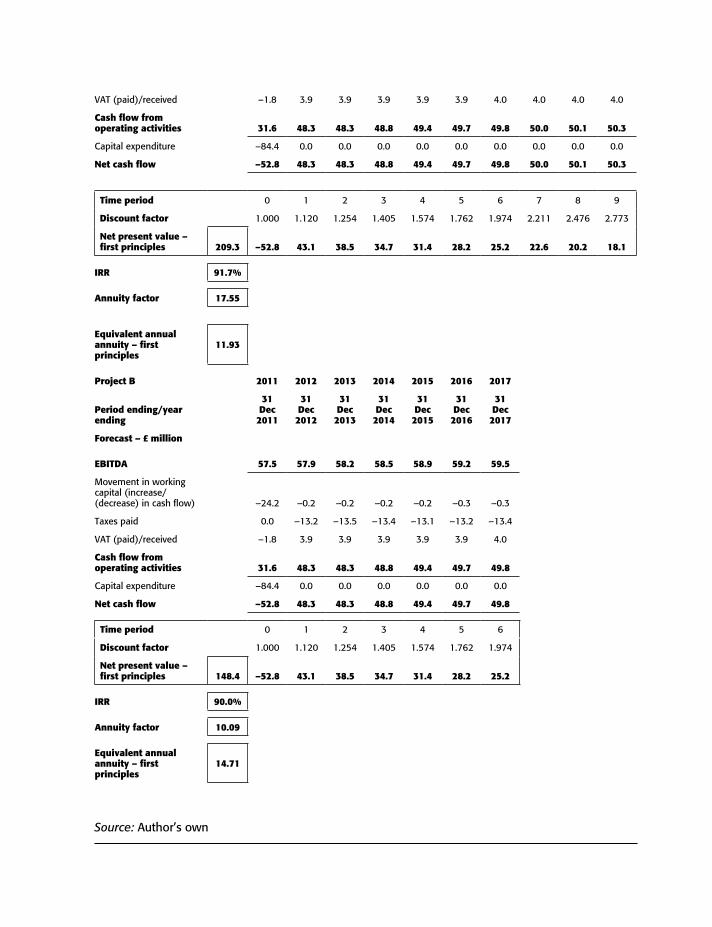

Unequal project lives

An example of the use of unequal project lives can be seen in Exhibit 1.7. Here we show the evaluation technique that outlines comparing two projects with unequal lives. At the top are the discount rates and the relative project lives.

In the summaries ‘Project A’ and ‘Project B’ we can see the net cash flow being discounted in order to arrive at the NPV for each project alternative. The annuity factor is calculated for each project. The different variable being the project life of each. The NPV is divided by the annuity factor in order to find the equivalent annual annuity. Project B has the highest and should therefore be selected. A useful cross check for an annuity factor is the NPV less the annuity which should always equal zero. The annuity factor is calculated as follows.

= (((1+Discount Rate) ^ Project Years)–1)/Discount Rate

The above calculation will allow you take account of the time value money component in order to make a comparison between the two investment proposals.

Exhibit 1.7

Unequal project lives

Discount rate 12.00%

Project A years 10

Project B years 7

Project A 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Period ending/ year ending

31 Dec 2011

31 Dec 2012

31 Dec 2013

31 Dec 2014

31 Dec 2015

31 Dec 2016

31 Dec 2017

31 Dec 2018

31 Dec 2019

31 Dec 2020

Forecast – £ million

EBITDA 57.5 57.9 58.2 58.5 58.9 59.2 59.5 59.8 60.1 60.4

Movement in working capital (increase/(decrease) in cash flow) –24.2 –0.2 –0.2 –0.2 –0.2 –0.3 –0.3 –0.3 –0.3 –0.3

Taxes paid 0.0 –13.2 –13.5 –13.4 –13.1 –13.2 –13.4 –13.6 –13.8 –13.9

Continued

VAT (paid)/received –1.8 3.9 3.9 3.9 3.9 3.9 4.0 4.0 4.0 4.0

Cash flow from operating activities 31.6 48.3 48.3 48.8 49.4 49.7 49.8 50.0 50.1 50.3

Capital expenditure –84.4 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Net cash flow –52.8 48.3 48.3 48.8 49.4 49.7 49.8 50.0 50.1 50.3

Time period 0 1 2 3 4 5 6 7 8 9

Discount factor 1.000 1.120 1.254 1.405 1.574 1.762 1.974 2.211 2.476 2.773

Net present value – first principles 209.3 –52.8 43.1 38.5 34.7 31.4 28.2 25.2 22.6 20.2 18.1

IRR 91.7%

Annuity factor 17.55

Equivalent annual annuity – first principles

11.93

Project B 2011 2012 2013 2014 2015 2016 2017

Period ending/year ending

31 Dec 2011

31 Dec 2012

31 Dec 2013

31 Dec 2014

31 Dec 2015

31 Dec 2016

31 Dec 2017

Forecast – £ million

EBITDA 57.5 57.9 58.2 58.5 58.9 59.2 59.5

Movement in working capital (increase/(decrease) in cash flow) –24.2 –0.2 –0.2 –0.2 –0.2 –0.3 –0.3

Taxes paid 0.0 –13.2 –13.5 –13.4 –13.1 –13.2 –13.4

VAT (paid)/received –1.8 3.9 3.9 3.9 3.9 3.9 4.0

Cash flow from operating activities 31.6 48.3 48.3 48.8 49.4 49.7 49.8

Capital expenditure –84.4 0.0 0.0 0.0 0.0 0.0 0.0

Net cash flow –52.8 48.3 48.3 48.8 49.4 49.7 49.8

Time period 0 1 2 3 4 5 6

Discount factor 1.000 1.120 1.254 1.405 1.574 1.762 1.974

Net present value – first principles 148.4 –52.8 43.1 38.5 34.7 31.4 28.2 25.2

IRR 90.0%

Annuity factor 10.09

Equivalent annual annuity – first principles

14.71

Source: Author’s own

The Strategic Corporate Investments Handbook

22

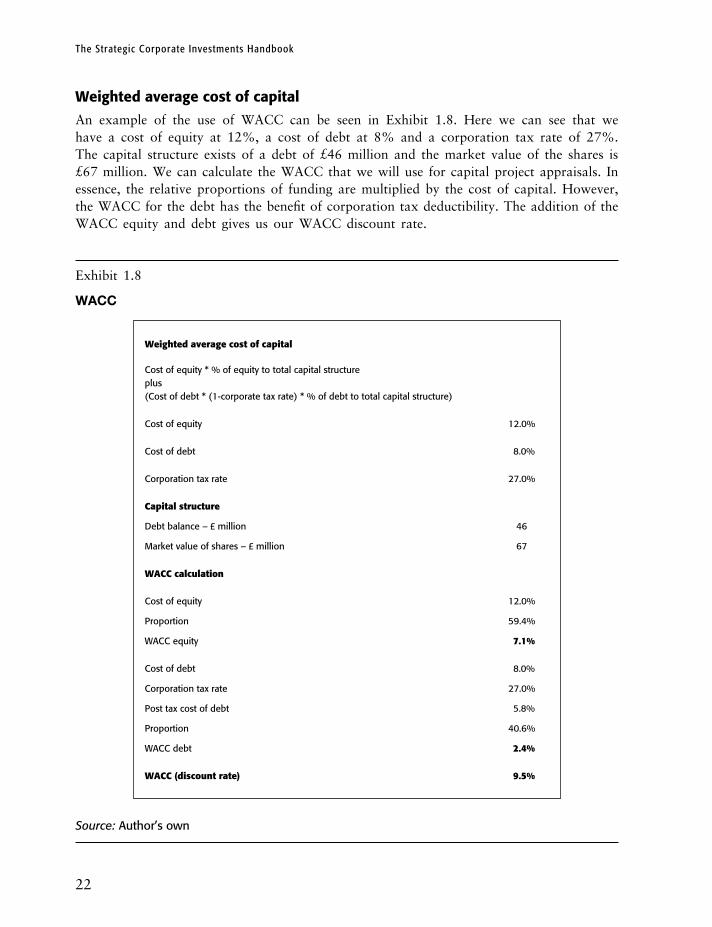

Weighted average cost of capital

An example of the use of WACC can be seen in Exhibit 1.8. Here we can see that we have a cost of equity at 12%, a cost of debt at 8% and a corporation tax rate of 27%. The capital structure exists of a debt of £46 million and the market value of the shares is £67 million. We can calculate the WACC that we will use for capital project appraisals. In essence, the relative proportions of funding are multiplied by the cost of capital. However, the WACC for the debt has the benefit of corporation tax deductibility. The addition of the WACC equity and debt gives us our WACC discount rate.

Exhibit 1.8

WACC

weighted average cost of capital

Cost of equity * % of equity to total capital structureplus(Cost of debt * (1-corporate tax rate) * % of debt to total capital structure)

Cost of equity 12.0%

Cost of debt 8.0%

Corporation tax rate 27.0%

Capital structure

Debt balance – £ million 46

Market value of shares – £ million 67

wACC calculation

Cost of equity 12.0%

Proportion 59.4%

WACC equity 7.1%

Cost of debt 8.0%

Corporation tax rate 27.0%

Post tax cost of debt 5.8%

Proportion 40.6%

WACC debt 2.4%

wACC (discount rate) 9.5%

Source: Author’s own

Strategy and corporate growth

23

WACC exercise

Using Exhibit 1.8 vary the assumptions by 20% and calculate the WACC for equity and WACC for debt leading to the WACC discount rate.

Post-monitoring the corporate investment

In order to control and post-monitor the investments there is a key issue to address the problem at the highest level first. Consequently, it will be necessary to control the annual total company key financial statements, that is, profit and loss, cash flow and balance sheet. Consequently, if we freeze these outputs as at the close of the transaction and compare the ongoing re-forecast we can undertake variance analysis to this original plan. The re-forecast would comprise the actual to date plus the forecast. The forecast would have similar logic as per the original plan.

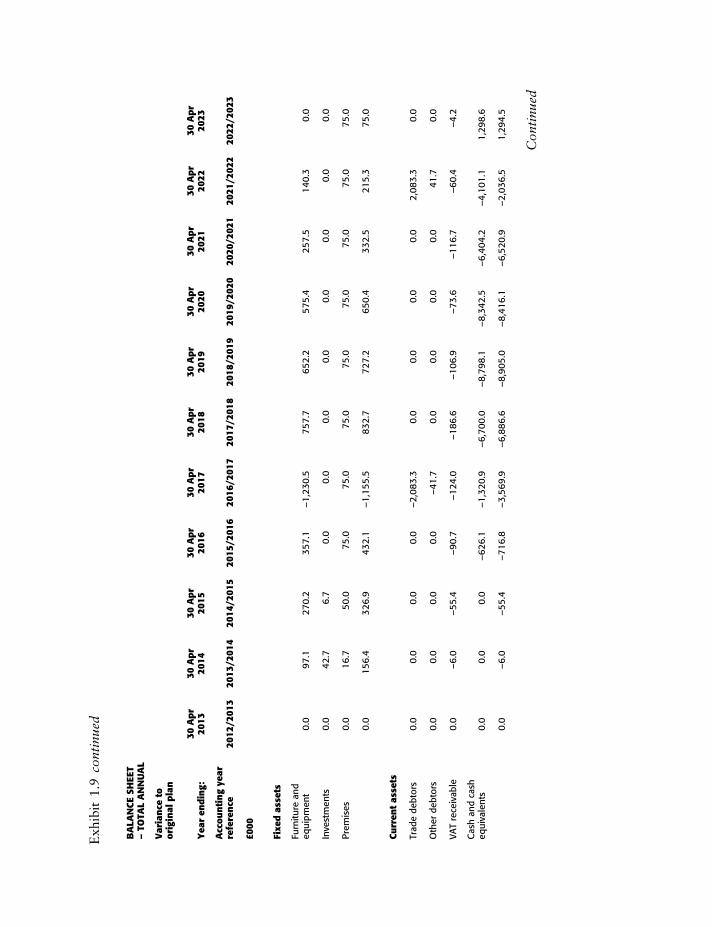

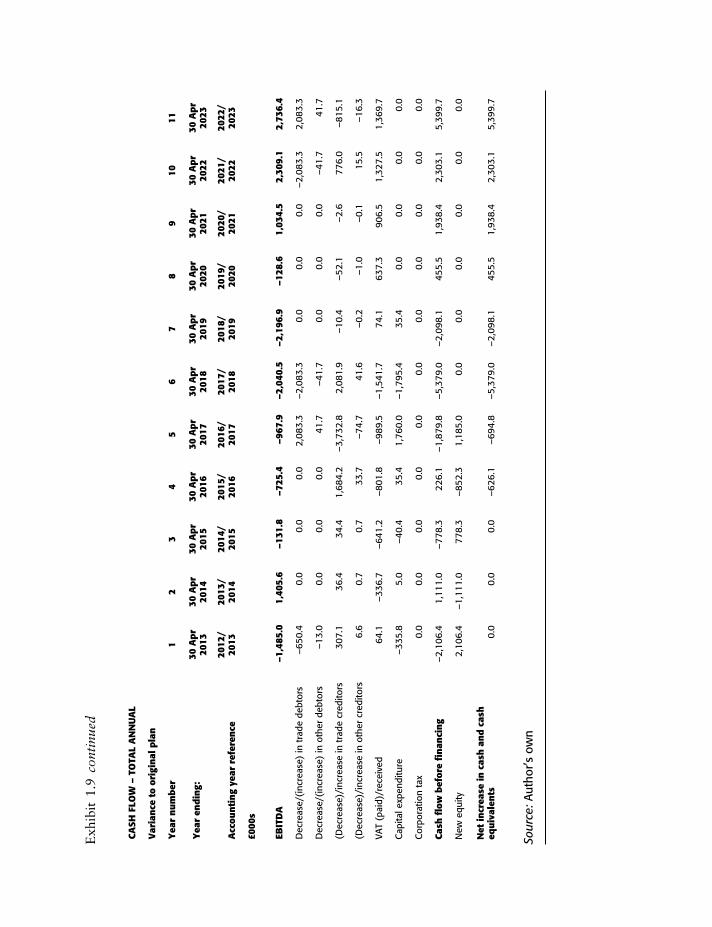

It is normally straightforward to make the comparison at such a high level for control purposes. So for the purposes of our post-monitoring we will keep matters at this level and demonstrate an example of the use of post-monitoring in Exhibit 1.9.

PR

OFI

T A

ND

lO

SS A

CCO

uN

T –

TOTA

l A

NN

uA

l

Var

ian

ce t

o or

igin

al p

lan

Yea

r n

um

ber

12

34

56

78

910

Yea

r en

din

g:30

Ap

r 20

1330

Ap

r 20

1430

Ap

r 20

1530

Ap

r 20

1630

Ap

r 20

1730

Ap

r 20

1830

Ap

r 20

1930

Ap

r 20

2030

Ap

r 20

2130

Ap

r 20

22

Acc

oun

tin

g ye

ar

refe

ren

ce20

12/

2013

2013

/ 20

1420

14/

2015

2015

/ 20

1620

16/

2017

2017

/ 20

1820

18/

2019

2019

/ 20

2020

20/

2021

2021

/ 20

22

£000

s

Turn

over

Cor

e m

anag

ed

serv

ice

cont

ract

0.0

–3,9

73.3

–6,6

66.7

–7,5

00.0

–11,

250.

0–1

1,25

0.0

3,33

3.3

6,66

6.7

8,14

0.0

11,2

50.0

Out

of s

cope

–

core

man

aged

se

rvic

e co

ntra

ct0.

00.

00.

00.

00.

00.

00.

00.

00.

00.

0

Oth

er in

com

e0.

0–1

08.4

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

Tota

l tu

rnov

er0.

0–4

,081

.7–6

,666

.7–7

,500

.0–1

1,25

0.0

–11,

250.

03,

333.

36,

666.

78,

140.

011

,250

.0

Turn

over

gro

wth

p

er a

nn

um

0.0

–0.9

0.5

0.1

0.0

0.0

0.1

0.0

0.0

0.0

Dir

ect

man

aged

se

rvic

e co

sts

Staf

f cos

ts0.

0–2

,493

.2–2

,785

.4–3

,162

.1–4

,903

.7–4

,476

.32,

567.

33,

315.

13,

498.

04,

328.

4

Serv

ice

prov

ider

co

sts

–583

.8–1

,872

.3–3

,069

.4–3

,266

.7–4

,883

.3–4

,529

.22,

564.

63,

313.

53,

291.

14,

331.

3

Gen

eral

cos

ts0.

0–1

42.9

0.0

0.0

–30.

060

.00.

00.

011

2.9

0.0

Bad

deb

ts0.

00.

00.

00.

00.

00.

00.

00.

00.

00.

0

Exh

ibit

1.9

Po

st-m

oni

tori

ng o

utso

urci

ng c

om

pan

y

Con

tinu

ed

Amor

tisat

ion

and

depr

ecia

tion

0.0

–112

.7–4

0.8

–88.

1–1

17.3

–140

.370

.176

.894

.711

7.3

Tota

l dir

ect

man

aged

ser

vice

co

sts

–583

.8–4

,621

.1–5

,895

.6–6

,516

.8–9

,934

.4–9

,085

.75,

201.

96,

705.

46,

996.

78,

777.

0

Gro

ss m

argi

n58

3.8

539.

4–7

71.1

–983

.2–1

,315

.6–2

,164

.3–1

,868

.6–3

8.8

1,14

3.3

2,47

3.0

Gro

ss m

argi

n %

13.0

%0.

7%–1

.5%

–0.6

%–0

.3%

–0.5

%–1

.0%

–0.7

%–0

.4%

–0.3

%

Cen

tral

cos

ts

Staf

f cos

ts41

7.2

–595

.9–2

88.8

–121

.4–1

65.8

–101

.80.

00.

00.

00.

0

Con

sulta

ncy

102.

0–8

0.8

–26.

70.

00.

00.

080

.80.

00.

00.

0

Adm

inis

trat

ion

0.0

–81.

0–1

5.0

–12.

0–1

8.0

–6.0

132.

00.

00.

00.

0

Gen

eral

cos

ts0.

0–9

5.9

–37.

30.

00.

00.

035

.30.

00.

00.

0

Insu

ranc

e0.

00.

0–2

70.7

–187

.5–2

81.3

–281

.283

.316

6.7

203.

528

1.3

Bus

ines

s de

velo

pmen

t–2

50.0

–125

.3–4

1.7

–25.

00.

012

5.0

67.0

0.0

0.0

0.0

Fina

nce

cost

s0.

00.

00.

00.

00.

00.

00.

00.

00.

00.

0

Amor

tisat

ion

and

depr

ecia

tion

0.0

–48.

7–8

9.2

–52.

6–5

5.1

–52.

50.

00.

022

3.2

0.0

Tota

l cen

tral

co

sts

269.

2–1

,027

.6–7

69.3

–398

.5–5

20.1

–316

.639

8.4

166.

742

6.7

281.

3

Taxa

tion

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

Pro

fit/

(los

s)

314.

61,

567.

0–1

.8–5

84.7

–795

.5–1

,847

.7–2

,267

.0–2

05.4

716.

62,

191.

8

EBIT

DA

314.

61,

405.

6–1

31.8

–725

.4–9

67.9

–2,0

40.5

–2,1

96.9

–128

.61,

034.

52,

309.

1

Con

tinu

ed

Exh

ibit

1.9

con

tinu

ed

BA

lAN

CE S

HEE

T –

TOTA

l A

NN

uA

l

Var

ian

ce t

o or

igin

al p

lan

Yea

r en

din

g:30

Ap

r 20

1330

Ap

r 20

1430

Ap

r 20

1530

Ap

r 20

1630

Ap

r 20

1730

Ap

r 20

1830

Ap

r 20

1930

Ap

r 20

2030

Ap

r 20

2130

Ap

r 20

2230

Ap

r 20

23

Acc

oun

tin

g ye

ar

refe

ren

ce20

12/2

013

2013

/201

420

14/2

015

2015

/201

620

16/2

017

2017

/201

820

18/2

019

2019

/202

020

20/2

021

2021

/202

220

22/2

023

£000

Fixe

d a

sset

s

Furn

iture

and

eq

uipm

ent

0.0

97.1

270.

235

7.1

–1,2

30.5

757.

765

2.2

575.

425

7.5

140.

30.

0

Inve

stm

ents

0.0

42.7

6.7

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

Prem

ises

0.0

16.7

50.0

75.0

75.0

75.0

75.0

75.0

75.0

75.0

75.0

0.

015

6.4

326.

943

2.1

–1,1

55.5

832.

772

7.2

650.

433

2.5

215.

375

.0

Curr

ent

asse

ts

Trad

e de

btor

s0.

00.

00.

00.

0–2

,083

.30.

00.

00.

00.

02,

083.

30.

0

Oth

er d

ebto

rs0.

00.

00.

00.

0–4

1.7

0.0

0.0

0.0

0.0

41.7

0.0

VAT

rece

ivab

le0.

0–6

.0–5

5.4

–90.

7–1

24.0

–186

.6–1

06.9

–73.

6–1

16.7

–60.

4–4

.2

Cas

h an

d ca

sh

equi

vale

nts

0.0

0.0

0.0

–626

.1–1

,320

.9–6

,700

.0–8

,798

.1–8

,342

.5–6

,404

.2–4

,101

.11,

298.

6

0.

0–6

.0–5

5.4

–716

.8–3

,569

.9–6

,886

.6–8

,905

.0–8

,416

.1–6

,520

.9–2

,036

.51,

294.

5

Con

tinu

ed

Cred

itor

s: a

mou

nts

fal

lin

g d

ue

wit

hin

on

e ye

ar

Trad

e pa

yabl

es0.

036

.470

.81,

755.

0–1

,977

.810

4.2

93.8

41.7

39.1

815.

10.

0

Oth

er p

ayab

les

0.0

0.7

1.4

35.1

–39.

62.

11.

90.

80.

816

.30.

0

Cor

pora

tion

tax

paya

ble

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

VAT

paya

ble

0.0

–342

.7–1

,033

.3–1

,870

.3–2

,893

.1–4

,497

.5–4

,343

.8–3

,673

.1–2

,809

.7–1

,425

.90.

0

Shor

t-te

rm

borr

owin

gs0.

00.

00.

00.

00.

00.

00.

00.

00.

00.

00.

0

0.

0–3

05.6

–961

.1–8

0.2

–4,9

10.4

–4,3

91.3

–4,2

48.1

–3,6

30.6

–2,7

69.8

–594

.50.

0

Net

cur

rent

ass

ets

0.0

299.

690

5.7

–636

.61,

340.

5–2

,495

.4–4

,656

.9–4

,785

.5–3

,751

.0–1

,441

.91,

294.

5

Tota

l ass

ets

less

cu

rren

t li

abil

itie

s0.

045

6.0

1,23

2.5

–204

.418

5.0

–1,6

62.6

–3,9

29.6

–4,1

35.1

–3,4

18.5

–1,2

26.7

1,36

9.5

Cred

itor

s:

amou

nts

fal

lin

g d

ue

afte

r on

e ye

ar

Long

-ter

m

borr

owin

gs0.

00.

00.

00.

00.

00.

00.

00.

00.

00.

00.

0

Net

ass

ets

0.0

456.

01,

232.

5–2

04.4

185.

0–1

,662

.6–3

,929

.6–4

,135

.1–3

,418

.5–1

,226

.71,

369.

5

Shar

ehol

der

s’

equ

ity

Shar

e ca

pita

l1,

583.

7–1

,111

.0–3

32.7

–1,1

85.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

Reta

ined

pro

fit–1

,583

.71,

567.

01,

565.

298

0.5

185.

0–1

,662

.6–3

,929

.6–4

,135

.1–3

,418

.5–1

,226

.71,

369.

5

Tota

l sh

areh

old

ers’

eq

uit

y0.

045

6.0

1,23

2.5

–204

.418

5.0

–1,6

62.6

–3,9

29.6

–4,1

35.1

–3,4

18.5

–1,2

26.7

1,36

9.5

Con

tinu

ed

CASH

FlO

w –

TO

TAl

AN

Nu

Al

Var

ian

ce t

o or

igin

al p

lan

Yea

r n

um

ber

12

34

56

78

910

11

Yea

r en

din

g:30

Ap

r 20

1330

Ap

r 20

1430

Ap

r 20

1530

Ap

r 20

1630

Ap

r 20

1730

Ap

r 20

1830

Ap

r 20

1930

Ap

r 20

2030

Ap

r 20

2130

Ap

r 20

2230

Ap

r 20

23

Acc

oun

tin

g ye

ar r

efer

ence

2012

/ 20

1320

13/

2014

2014

/ 20

1520

15/

2016