theory versus practice: what is the cost of my mobile ...€¦ · theory versus practice: what is...

TRANSCRIPT

Theory versus Practice:

What is the cost of my mobile

employees?

Yvonne Brazil, CEP – TubeMogul

Jennifer Kirk – Google

Laura Verri, CEP – E*Trade Financial Services Inc.

Marlene Zobayan, CEP – Rutlen Associates LLC

-2-

DISCLAIMER

This presentation contains general information only and the respective speakers and represented firms are not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. The respective speakers and firms shall not be responsible for any loss sustained by any person who relies on this presentation.

-3-

Agenda

Cost and Effect of mobility

Timeline complexities for mobile employees Taxation

Finance and accounting

Timeline of events and cost associated Equity plans compensation costs

Tax equalization

Social tax

Tax advice

Timeline of transactions

Audits and controls

-4-

Google/Alphabet background

Over 60,000 employees in approx. 60 countries; broad-based grants of Google Stock Units (“GSUs”); used to grant stock options (stopped in 2010)

Over 5,000 permanent transfers are part of our gMobility Program

– Launched in April 2011

– Jan 2016 we launched state to state mobility

– We provide 1 year of tax services post-transfer

Fewer than 200 Googlers are on expat packages and tax-equalized but only do hypothetical tax withholding for equity for US inbounds

-5-

TubeMogul background

TubeMogul is an enterprise software company that offers a self-serve platform for digital branding

Located in 11 countries, with approximately 100 employees overseas and 500 employees in the US

Currently a small number of expats, though we had a much larger expat population a year ago. Moving toward localization of our expats

We provide unlimited tax assistance while on assignment and 1 year of tax assistance post localization

-6-

Types of mobile employees

Types of mobile employees covered in today’s presentation:

Assignees (including expatriate, inpatriate, foreign national, third-country national)

Permanent transfers

Business traveler

Can be domestic or global

Individuals may have more than one type of mobility during their careers

Not all costs we will discuss will apply to all types of mobile employee

-7-

POLL QUESTION:

How do you feel about your mobile employees’ records and processes?

We have a good tracking system and technology in place. We have no major issues

We have ‘procedures’ in place and track with the use of spreadsheet. We feel this could be an issue

We don’t have (track) mobile employees. Is this area a major risk?

-8-

Cost of mobile employees

-9-

Cost of mobile employees – Stakeholders

-10-

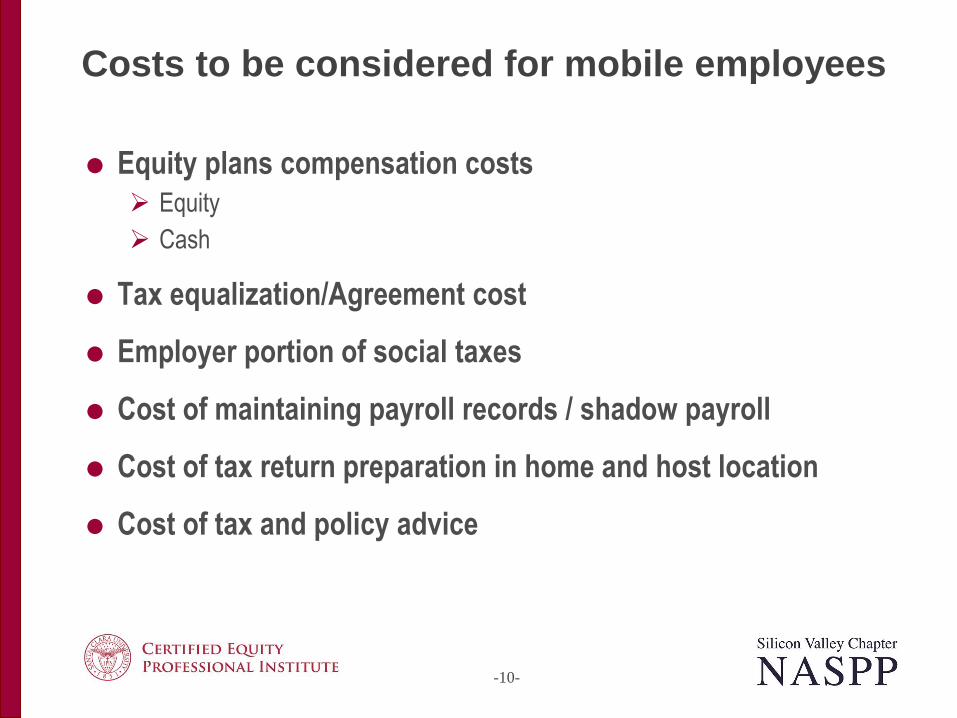

Costs to be considered for mobile employees

Equity plans compensation costs

Equity

Cash

Tax equalization/Agreement cost

Employer portion of social taxes

Cost of maintaining payroll records / shadow payroll

Cost of tax return preparation in home and host location

Cost of tax and policy advice

-11-

Example of mobility costs overtime

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7

-12-

Issues arising from events

Timing of event

Taxable year vs. Fiscal Year

Unpredictability of costs

Share price fluctuation

Foreign exchange

Tax rates /rules changes

Tax bracket

Inability to “close the books” for a mobile employee for long period of time

-13-

Equity plans expense - considerations to be applied

Allocation of the equity expense

Allocation of expense > Recharge to subsidiary

Equity settled awards > Grant date to vest date

Cash settled awards > Trailing liability spans multiple years

Accrual of deferred tax asset

Benefit spans multiple years

Expense allocation ≠ current cost center

ASC718 accrual vs. IFRS2 accrual

Impact of transfer pricing and recharge agreement

Impact on local and home country budget

-14-

POLL QUESTION:

Do you provide, or plan to provide any tax support to your mobile employees?

We provide full support, including tax equalization, tax advice, and tax return preparation

We provide some support for tax return preparation

No, not applicable

-15-

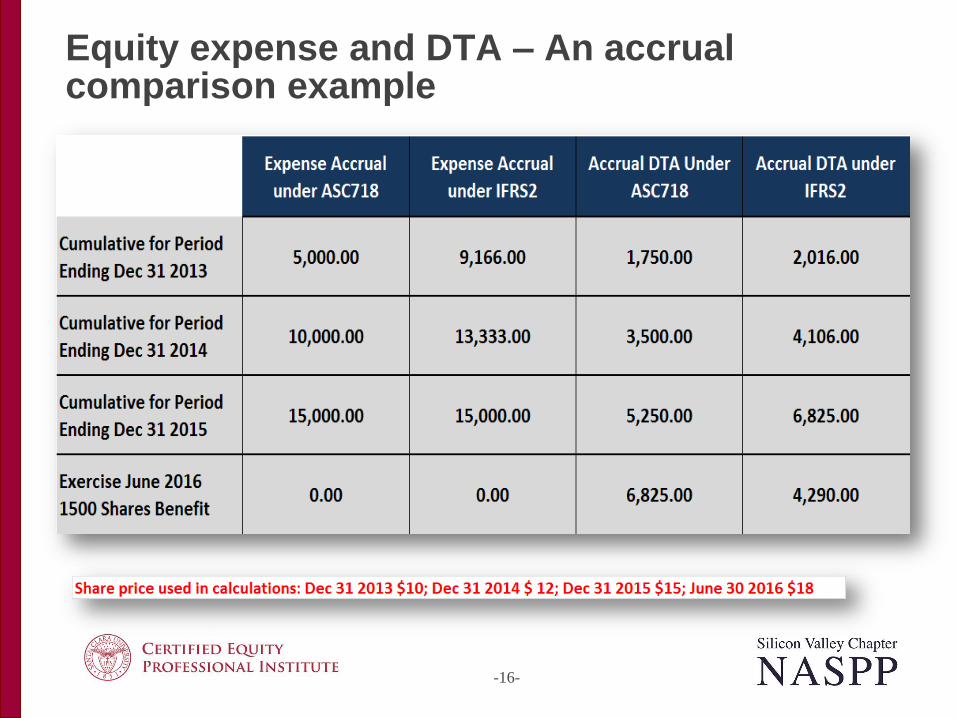

Julie, a U.S. citizen is employed by ACME Co. in the U.S.

On Jan 1, 2013 she is granted NSO for 3,000 shares in ACME which vest over 3 years – 33% per year

On Jan 1, 2014 Julie is transferred to the UK subsidiary

On Jan 1, 2016 the NSO fully vests

ACME recharges NSO costs to its UK entity

Corporate Tax Rate : USA 35% - UK 22%

Case study example

Date Stock price Fair value

1-Jan-13 $10 $5

1-Jan-14 $10 $5

1-Jan-15 $12 $5

1-Jan-16 $15 $5

-16-

Equity expense and DTA – An accrual comparison example

-17-

Tax equalization / agreement cost

What is tax equalization?

Accruals and releases

Post repatriation tax equalization costs

Is cost center still open?

Impact on local budget

-18-

Employer social tax

Certificate of coverage?

Social tax position if no certificate of coverage

Impact of chargeback of cost on employer social tax

Difference in social tax rates

Europe and South America higher rate

Transfer cost/accrual lower than local rate

Trailing employer social tax costs

-19-

Employer social tax – An accrual comparison example

-20-

Progress of social tax and other costs

2013 2014 2015 2016 2017 2018 2019

-21-

Mobility event

Agree tax equalization

Agree certificate of coverage/social tax situation

Agree payroll situation

Tax returns preparation

Tax advice

Impact on equity compensation expense

Impact on deferred tax asset

-22-

Transaction: timing of event

RSU at vest – Option at exercise

Impact of equity compensation expense

Impact of deferred tax asset

Impact of tax equalization

Impact on social tax expense including timing of payments by the internal payroll team

Impact on tax preparation and advice

-23-

Repatriation: what’s next?

-24-

Audit and controls

Keep current records of mobile employees

Detailed information from HR and subsidiary

Where do employee reside and where they work?

Processes and training material for all the parties involved

Ongoing communications between all stakeholders

Keep detailed records of expatriate vs. movers

U.S. and non U.S. regulations at hand

Documentation and controls for mobile employees

-25-

Yvonne Brazil

TubeMogul

510-201-0457

Questions

Jennifer Kirk

650-214-5674

Laura Verri, CEP

E*TRADE FINANCIAL SERVICES INC.

650-331-5514

Marlene Zobayan, CEP

Rutlen Associates LLC

650-868-9282