this webcast will begin shortly - association of corporate...

TRANSCRIPT

This Webcast Will Begin Shortly

If you have any technical problems with the Webcast or the streaming audio, please contact us via email at:

Thank You!

Employee Stock Ownership Plans: Is it the Right Fit for Our Company

in the United States

April 30, 2015

Presented By: Alexander L. Mounts

Partner, Krieg DeVault LLP One Indiana Square, Suite 2800

Indianapolis, IN 46204 (317) 238-6335

Moderated By: Kristen Chittenden

Associate General Counsel Hendry Marine Industries

Is your company publicly traded?

Yes No

Do you have an ESOP or an ESOP component to your 401(k) plan?

Yes, an ESOP Yes, an ESOP component to my 401(k) plan No, neither

5

What is an “Employee Stock Ownership Plan”?

• Tool of CORPORATE FINANCE/SUCCESSION VEHICLE

• Tax-qualified RETIREMENT PLAN • Invests “primarily” in EMPLOYER STOCK • Numerous Federal tax incentives encourage

implementation

Private Company ESOPs

6

7

Advantages of C and S Corporation ESOPs Flexibility • Market for shareholders’ stock • Unlike most buyers, serves as source of funds to purchase minority

blocks • Low marketability discount (typically 5%) on value of shares (private

company) • Succession planning vehicle for gradual transfer of ownership to next

generation (often combined with transfers of ownership to management – “sweat equity”)

• “Financial” buyer with long term perspective • Easily combined with “401(k)” plan – use of “matching” contributions

to fund ESOP; some transactions allow employees to transfer 401(k) funds to ESOP

• Investment option for employees. • Additional fiduciary protection since ESOP are designed to invest

primarily in company stock.

Advantages of ESOPs Tax – C Corporation • If certain requirements in Code Section 1042 are met, selling shareholder(s)

can defer (or even eliminate) taxable gain on sale • All contributions to ESOP (including those used to repay loan) are tax

deductible • Cash dividends are deductible if used by ESOP to:

– repay loan, – distributed to participants, or – Used to buy more shares

• Allocations to participants’ accounts are tax deferred; distributions eligible for tax-free rollover

• Special tax treatment of “net unrealized appreciation” on distribution of stock

8

9

Advantages of ESOPs

Tax – S Corporation • ESOP’s share of company’s income is not subject to

tax • Contributions to ESOP are tax deductible (important if

ESOP owns less than 100%) • ESOP’s share of “tax dividends” can be used to repay

loan, satisfy repurchase liability or pay expenses • Allocations to participants’ accounts are tax deferred;

distributions are eligible for tax-free rollover • Special tax treatment of “net unrealized appreciation”

on distribution of stock

10

Effect on Employees (Well Communicated ESOPs)

• Pride of ownership culture • Recruiting/retention tool • Increased commitment and enthusiasm • Material increase in value of corporation* *See Key Studies on Employee Ownership and Corporate Performance at https://www.nceo.org/articles/studies-employee-ownership-corporate-performance

11

Disadvantages of an ESOP

• Cost and number of service providers • Complexity • Communication • Repurchase liability (private company) • Less diversification of retirement assets (private

company) • Fiduciary responsibility/liability

Fifth Third Bancorp v. Dudenhoeffer • Case involving a public company ESOP. • The Supreme Court ruled that there is no presumption of

prudence to protect fiduciaries of plans designed to invest in company stock, and specifically ESOPs.

• While the decision eliminated the presumption of prudence rule, it replaces it with a pleading requirement that plaintiffs demonstrate the fiduciary acted imprudently.

ESOP Valuation Requirements

• Publicly traded companies use the current stock value. • IRC Section 401(a)(28)(C) – “ . . . All valuations of

employer securities which are not readily tradeable on an established securities market . . .” must be the subject of an independent appraisal

• ERISA Section 3(18) – if there is no “…generally recognized market…” for the shares (i.e., they are not traded on a “national securities exchange”), they must be the subject of a valuation which meets the requirements of the statute and regulations

13

ESOP Valuation Considerations (private company)

• ESOP Valuation vs. “Multiple of Book” – How should ESOP shares be valued? – Independent appraisal firm qualified and experienced with

ESOP valuations – Appropriate methods of valuing companies – Weighting of methods – Use of publicly available information regarding non-publicly

traded companies • Financial performance • Merger and acquisition activity

– Effect of cash and stock dividends on value – Effect of repurchase obligation on value

14

How does Company Stock get in an ESOP in a Public Company? • Purchase in the market or from the company with

employee deferrals, profit sharing contributions or matching contributions.

• Matching or profit sharing contributions made in the form of shares of stock.

Basic Structure of a Private Company ESOP Transaction (Bank Financing)

16

4. Cash

5. Employer Stock

Employer Bank

1. Bank Loan

2. Pledge of Collateral

Step 1

Shareholders ESOP

Basic Structure of a Private Company ESOP Transaction (Bank Financing)

17

Employer Bank 3. Loan Payments

1. Contributions

Dividends

Step 2

ESOP

Stock

18

Company

Basic Structure of a Private Company ESOP Transaction (Seller Only Financing)

“Short Term” Subordinated

Note & Warrant

Redeem Shares

“Long Term” Note

Subscribe for Newly

Issued Shares

Step 1 Shareholder

ESOP

1

2

19

Basic Structure of a Private Company ESOP Transaction (Seller Only Financing)

Note Payments

Contributions (Including 401(k) “Match”) Distributions

Note Payments

Step 2 Company Shareholder

(Warrant)

Stock

ESOP

20

Examples of Benefits of “S” Corporation ESOP Structure

Net Income of $5,000,000 with No ESOP

Corporate Tax -0-

Individual Shareholder Tax:

on $5,000,000 @ 45% = $2,225,000

Total “Tax Dividends” = $2,225,000

Net Income of $5,000,000 with 50% ESOP

Corporate Tax -0-

Individual Shareholder Tax:

on $2,500,000 @ 45% = $1,125,000

ESOP Shareholder Tax on $2,500,000 = $0

Total Tax Dividends = $2,225,000

ESOP’s Share = $1,125,000

Net Income of $5,000,000 with 100% ESOP

Corporate Tax -0-

ESOP Shareholder Tax on $5,000,000 = $0

Additional cash flow = $2,225,000

21

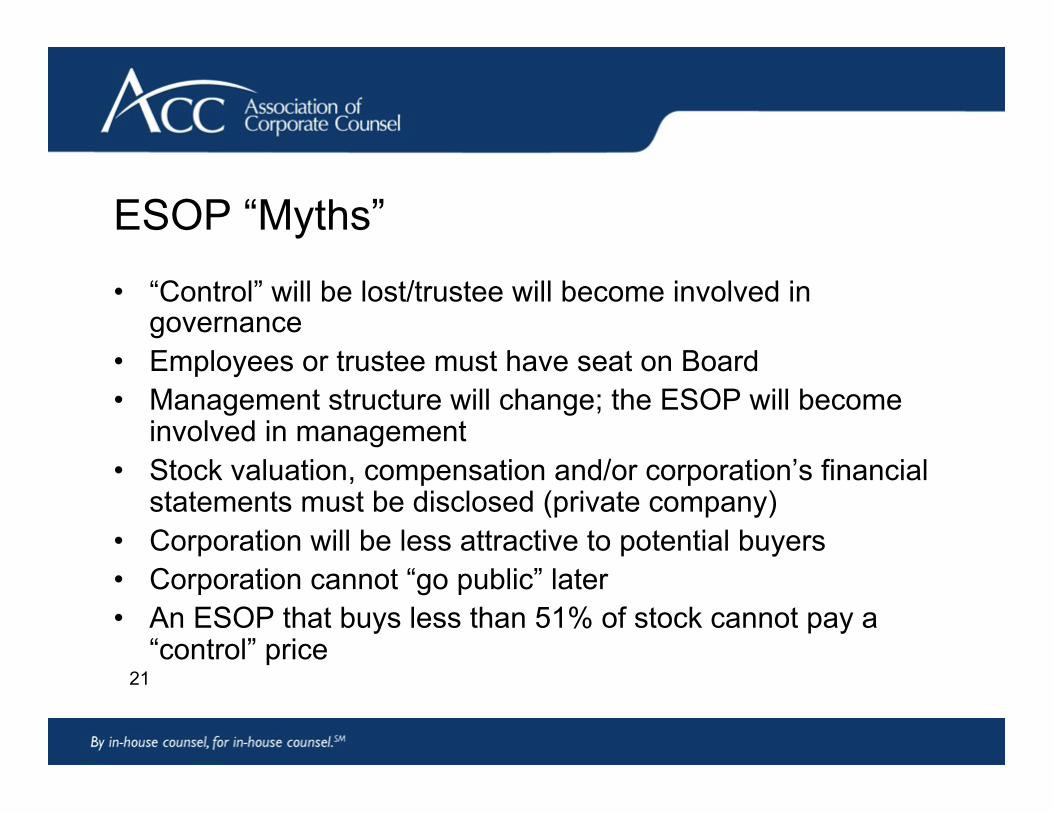

ESOP “Myths” • “Control” will be lost/trustee will become involved in

governance • Employees or trustee must have seat on Board • Management structure will change; the ESOP will become

involved in management • Stock valuation, compensation and/or corporation’s financial

statements must be disclosed (private company) • Corporation will be less attractive to potential buyers • Corporation cannot “go public” later • An ESOP that buys less than 51% of stock cannot pay a

“control” price

22

Characteristics of Well-Designed and Implemented ESOPs

• “Sanity check” approach to implementation a. Stock valuation b. Feasibility c. Financing d. Commitment of key managers

• Independent, experienced advisors to ESOP a. Counsel b. Financial Advisor c. Trustee

• Well-educated ESOP “Committee” • Well-prepared feasibility analysis

a. Projections based on history b. “Cushion” for economic downturn

• Repurchase Liability Study (private company)

23

• Carefully designed ESOP distribution provisions a. Forms (e.g. lump sums vs. installments) b. Times (after loan paid vs. current)

• Non-dilutive “sweat-equity” plan for key management (or outright buy-in)

• Employment and non-compete agreements for key management

• Effective employee communications program (“Employee as Owner”)

Characteristics of Well-Designed and Implemented ESOPs (Cont’d)

The “1042 ESOP Rollover”

• The business owner can elect to defer the recognition of long-term capital gain on the sale of C corporation stock to an ESOP if certain requirements are satisfied: – Owner must sell “qualified securities” - “best common

stock” of a non-publicly traded C corporation – Holding period must be at least three years at time of

sale

24

The “1042 ESOP Rollover” (cont’d)

• Immediately after sale, ESOP must own at least: – 30% of the total number of shares of each class of

stock, or – 30% of the value of all outstanding stock of the

corporation

• Selling shareholder, members of family and 25 percent or greater shareholders cannot receive allocations of shares on which gain is deferred

25

Disclaimers

• These slides are for educational purposes only and are not intended, and should not be relied upon, as legal or accounting advice.

• Pursuant to Circular 230 promulgated by the Internal Revenue Service, please be advised that these slides were not intended or written to be used, and that they cannot be used, for the purposes of avoiding federal tax penalties unless otherwise expressly indicated.

26

7218450.1

Thank you for attending another presentation from

ACC’s Webcasts

Please be sure to complete the evaluation form for this program as your comments and ideas are helpful in planning future programs.

If you have questions about this or future webcasts, please contact ACC at [email protected]

This and other ACC webcasts have been recorded and are available,

for one year after the presentation date, as archived webcasts at http://www.acc.com/webcasts