three key areas equity analysts look when rating life insurance companies

TRANSCRIPT

Accenture Insurance Equity Analyst Survey

Outperforming the market in uncertain times What life insurers must do to meet analysts’ expectations of risk control, growth and cost reduction

1

IntroductionIn 2008 Accenture commissioned a survey* of insurance equity analysts to find out what they wanted from those insurance companies to which they gave their highest ratings. A lot has happened in the industry since then: many new problems have arisen and the old ones, if anything, have got worse. To learn how events have influenced analysts’ expectations we repeated the survey in 2012**.

Perhaps the most surprising finding of the new survey is that, despite worsening market conditions, analysts have not lowered the growth and profitability targets – they expect the top performers to achieve significantly higher growth in 2012 and virtually the same ambitious return on equity (RoE).

It’s necessary to point out that these expectations apply not to the industry as a whole, but to those carriers which will receive the most glowing valuations. It is also a fact that the most successful companies have comfortably exceeded these levels over the past few years.

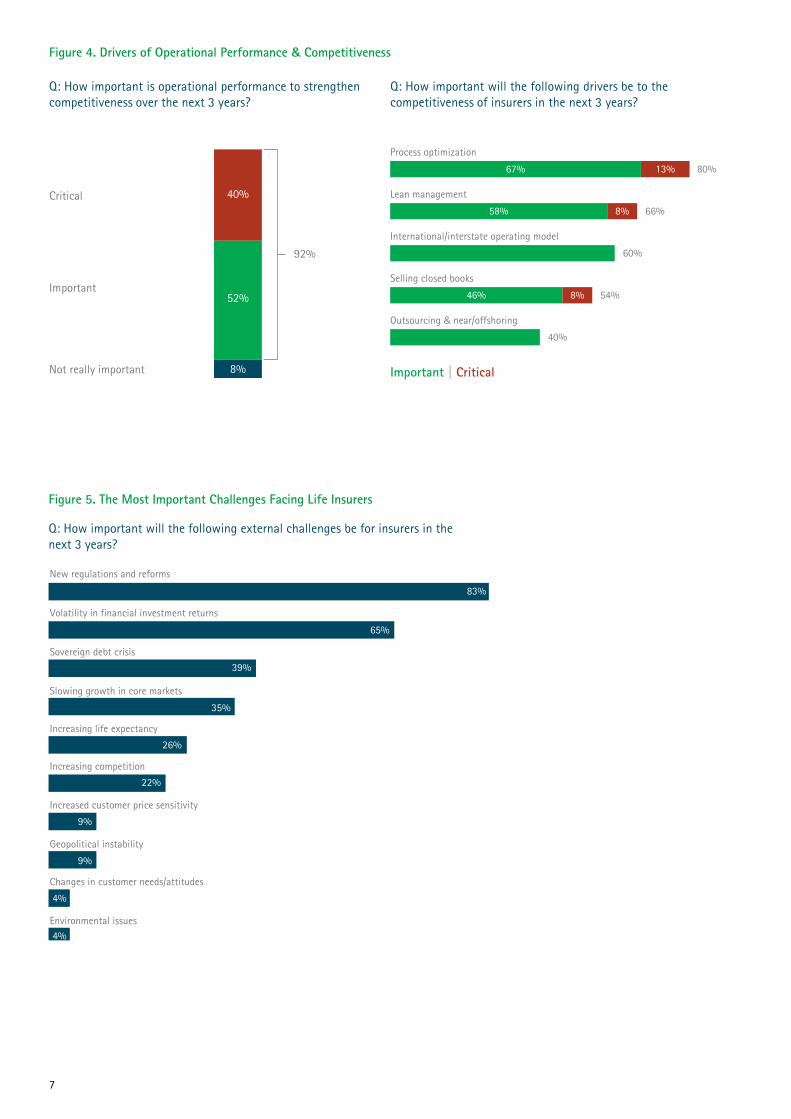

Nonetheless, all but a few life insurers will have their work cut out if they are to satisfy these demanding stakeholders. To do so they will need to focus firstly on risk control – analysts believe the main external challenges facing insurers are new regulations and reforms, and investment volatility. Growth is their next priority, while cost reduction trails in third place.

It is clear from analysts’ responses that insurers don’t have the luxury of choosing which of the priorities they should focus on. Three out of three is the minimum requirement.

* Accenture Insurance Equity Analyst Survey, 2008** Accenture Insurance Equity Analyst Survey, 2012

2

To gain insight into the factors driving the ratings of insurance companies, as well as the strategies that insurance CEOs should adopt to improve valuations of their companies, Accenture commissioned Institutional Investor Market Research Group (IIMRG) to conduct a survey of leading insurance equity analysts around the world.

IIMRG conducted telephonic interviews with 68 analysts from North America, Asia Pacific, Europe, Africa and Latin America responsible for researching and rating insurance companies. The interviews, which were carried out in March and April 2012, were guided by a standardized questionnaire designed by in-house industry experts along with external contributions from several equity analysts.

Survey scope & methodology

“What performance do you expect in 2012 from the life insurers to which you give superior ratings?”

“What are the critical value drivers for insurers over the next three years?”

Quality of service

Pricing strategy

Data analysis

“What are the biggest external challenges insurers will face in the coming years?”

New regulations and reforms

Volatile investment returns

“What should insurers’ most important priorities be in the year ahead?”

Risk control

Sustainable growth9.6% 15.1%

50%

44%

50%

38%

83%

65%

21%

Expected meanpre-tax RoE

Expected annual mean growth

3

Key findings – what analysts think

4

In pursuit of high performancePerhaps the most surprising finding of the Equity Analyst Survey is the bullish expectations which analysts have of the life industry’s top performers – they demand strong growth in annual revenue in 2012, as well as a nine-percent increase in pre-tax return on equity over 2011. Buffeted as insurers are by the global economic crisis, and struggling with weak demand and ever-more stringent regulatory requirements, they might have been forgiven for merely maintaining their positions.

A survey question about the impact of the tough market conditions provides insight into analysts’ thinking: no fewer than 55 percent expect the impact to be positive for the industry’s front runners. In other words the weaker players, unable to adapt to the more challenging environment, will lose share or be eliminated. The leaders, on the other hand, will be forced by the prevailing circumstances to strengthen their capabilities. This will equip them to grow.

Organic growth is likely to be more important than inorganic growth, with analysts expecting insurers to concentrate their efforts somewhat more on emerging markets (44 percent say it is critical) than mature markets (25 percent). However, they predict that mergers and acquisitions in emerging markets (20 percent) will contribute to growth – significantly more so than in mature markets (4 percent).

The shifting landscapeLife insurers are operating in a challenging and fast-changing environment. Their businesses are under enormous pressure from a range of external forces. The most demanding of these, the survey found, are new regulations and reforms, volatility in investment returns, the sovereign debt crisis and slowing growth in core markets.

Changes in consumer demand is another source of uncertainty. Whereas at the moment analysts believe the majority of customers prefer differentiated, value-added products rather than standardized, undifferentiated products, in the not too distant future the balance is expected to shift.

5

Opportunities in a tough marketWhile organic growth will be challenging over the next three years, analysts believe that to achieve it insurers will need to better understand and predict customer behavior and needs (36 percent say this is critical), develop and implement a multi-channel distribution strategy (28 percent), and introduce new, relevant products (24 percent). Expanding the business in new markets is regarded as an important opportunity for insurers; even more so are improving risk control and enhancing their asset management capabilities.

Sharpening the competitive edge Competition in the life insurance market, from both traditional and non-traditional players, remains fierce. Analysts expect banks and asset managers, other life insurers and mutual funds to remain a threat. They also foresee a change in the face of competition in the next three years, with 36 percent predicting that new players such as retailers will enter the industry as distributors.

To meet analysts’ expectations of profitability and competitiveness, life insurers must focus on improving their operational performance. Process optimization, lean management, an interstate or international operating model that includes platform consolidation and shared services, and the divestment of closed books are among the actions that analysts believe will drive the competitiveness of top-rated life insurance companies in the medium term.

No fewer than 39 percent of analysts say it is critical for insurers to increase the value of their products and services. They believe service quality, an effective pricing strategy and an advanced data analytics capability will also be crucial value drivers. Product innovation will be important since analysts foresee a shift in demand over the next three years from differentiated, value-added products and advice to more standardized products. In both cases innovation will need to meet the requirements of relevance to customer needs, and understandability.

Technology and profitability The effective use of technology will be a key point of differentiation for the top-rated players in the life insurance sector – 20 percent of analysts say it will be critical to profitability over the next three years. Risk management (including underwriting), investment risk management and pricing are not only the three areas which analysts believe will generate the greatest return on technology investment; they are also the areas which have grown the most in importance since the 2008 survey.

Fifty-six percent of analysts regard insurers’ technology performance as “good” and nine percent rate it “excellent”. However, no fewer than 91 percent believe improvement is needed.

Organic growth in emerging markets

54% 25%

M&A growth in emerging markets

44% 44%

Organic growth in mature markets

48% 20%

M&A growth in mature markets

40% 4%

Important | Critical

Q: How important is it for an insurance company to take the following actions in the next 3 years?

6

Q: How important will each of the following be to support organic growth over thenext 3 years?

88%60% 28%

Develop and implement a multi-channel distribution strategy

Develop new products

60% 24% 84%

Enter new lines of business

44% 4% 48%

56% 36%

Understand and predict customers' behavior & needs

92%

Important | Critical

Figure 1. Sources of Future Growth

Figure 2. Actions & Capabilities Likely to Support Organic Growth

Q: What are the most important value drivers for insurers over the next three years?

88%50% 38%

Pricing strategy

Data analytics

58% 21% 79%

Product innovation

75% 4% 79%

46% 50%

Quality of service

96%

Important | Critical

Figure 3. Service & Pricing the Primary Value Drivers

7

Q: How important will the following external challenges be for insurers in the next 3 years?

Increasing competition

22%

Increasing life expectancy

26%

Slowing growth in core markets

35%

Sovereign debt crisis

39%

Volatility in financial investment returns

65%

New regulations and reforms

83%

Changes in customer needs/attitudes

4%

Geopolitical instability

9%

Increased customer price sensitivity

9%

Environmental issues4%

Figure 5. The Most Important Challenges Facing Life Insurers

80%67% 13%

Process optimization

66%58% 8%

Lean management

60%

International/interstate operating model

54%46% 8%

Selling closed books

40%

Outsourcing & near/offshoring

Q: How important will the following drivers be to the competitiveness of insurers in the next 3 years?

Q: How important is operational performance to strengthencompetitiveness over the next 3 years?

Important | Critical

92%

Important

Critical

Not really important

52%

40%

8%

Figure 4. Drivers of Operational Performance & Competitiveness

8

Q: What are the 3 most important areas in which insurers should invest in new technologies to improve their business performance?

2012 Survey | 2008 Survey

Ranked within Top Three Choices

Underwriting risk management

Investment risk management

Pricing

Distribution channels

Customer service

Policy administration

Claims management

Underwriting

35%74%

30%22%

41%17%

19%26%

26%30%

33%39%

33%48%

65%44%

Figure 7. Technology Investment & Business Performance

80%

Important

Critical

Poorsignificant improvement required

Good some improvement required

Excellentno significant improvement required

Not really important35%

56%

9%

40%

40%

16%

Q: How would you rate the importance of technology in the insurance industry over the next 3 years?

Q: How would you rate the current level of technology performance among most insurers?

Not important at all 4%

Figure 6. Perceptions of Insurers’ Technology Performance

9

Comparing the 2008 and 2012 surveys

A lot of water under the bridge

The 2012 Equity Analyst Survey is a follow-up to a similar study conducted in 2007/8. The fieldwork was completed in December 2007, when the current recession had begun but well before markets crashed and the depth of the crisis became apparent. At that point, analysts predicted that the highest-performing life insurers would grow at an average annual rate of 10.9 percent over the ensuing three years. In the 2012 survey they report that the companies to which they gave the highest ratings grew by 9.6 percent in 2011. Not surprisingly, they have set their sights somewhat lower, forecasting growth of 9.2 percent for 2012.

With regard to profitability, their expectations in 2008 were that the top performers would achieve an average pre-tax return on equity, over the next three years, of 15.3 percent. In the latest survey they report that 13.9 percent was achieved in 2011, and they predict 15.1 percent for 2012.

Considering the upheaval of the past four years, it is not surprising that the external challenges which analysts believe confront life insurers have changed to some degree. Investment risk, number one on the list in 2008, has slipped to second place while new regulations and reforms (previously fourth) takes the top spot. The third- and fourth-ranked challenges, the sovereign debt crisis and slowing growth, did not feature in the 2008 survey.

The perceived importance of technology to the industry over the next three years has declined from a high of 93 percent (“important” and “critical”) in 2008 to 80 percent. At the same time, analysts are more impressed than before with the performance of insurers’ IT: whereas 61 percent rated it as “poor” in the first survey, this has dropped to 35 percent in the second.

10

Figure 8. Risk is a Greater Priority for Equity Analysts in North America than Those in Other Regions

The companies that analysts rated most favorably achieved average growth rates in 2011 of 6 percent in NA, 7.4 percent in Europe and 13.6 percent in APAC. They expect, in 2012, the same of NA insurers (6.1 percent) and somewhat less of European (6.7 percent) and APAC insurers (11.0 percent).

Profitability, however, is forecast to rise. The average pre-tax return on equity of the leading NA insurers is expected to increase from 12.1 percent in 2011 to 13.7 percent in 2012, in Europe from 15.5 to 16.4 percent, and in APAC from 13.1 to 13.8 percent.

While the challenges facing insurers worldwide are similar, their relative importance varies. Analysts believe investment volatility (71 percent) and new regulations and reform (52 percent) are the biggest threats to NA carriers. For European companies, regulations come first (61 percent) and investment volatility second (57 percent). In APAC, regulations are by far analysts’ greatest concern: they score 92 percent, compared to 67 percent for slow growth in core markets and 50 percent for investment volatility.

NA insurers, if analysts are right, will achieve most of their growth organically in mature markets; their other priorities should be organic growth and M&A in emerging markets. For European companies, organic growth in emerging markets is by far the most promising source of growth. In APAC, M&A and organic growth in emerging markets are viewed as marginally more important than organic growth in mature markets.

Analysts are undecided as to the actions that insurers in NA should take to support their quest for organic growth – they assign similar priority to developing new products, implementing a multi-channel distribution strategy, and gaining a better understanding of customer needs and behavior. In Europe, however, understanding the customer is significantly more important, while in APAC a multi-channel distribution strategy is clearly the first priority, followed by new, relevant products.

The greatest opportunities for NA insurers, analysts believe, are to revisit their pricing strategies and to improve their risk management capabilities. It’s no surprise, therefore, that the most important value drivers over the next three years are considered to be pricing strategy and data analytics.

For European carriers the biggest opportunities are to reduce costs and improve pricing – the value drivers are the same as for their NA counterparts. In APAC, expanding business in new markets is the most important opportunity, followed by implementing a multi-channel distribution strategy and de-risking the investment portfolio. Pricing and service quality are the key value drivers.

Across all three regions, analysts believe insurers need to invest in technology to improve their performance. The key areas for NA carriers to consider are risk management and pricing; in Europe it is claims management followed by risk management; and in APAC it is risk management and controlling investment risk.

Comparing findings for North America, Europe and Asia Pacific

Different priorities in the global villageGiven the markedly different conditions which confront insurers in North America (NA), Europe and Asia Pacific (APAC), no one would be surprised to learn that equity analysts in the different regions have different expectations of the insurance firms which they rate. Notwithstanding the fact that many analysts rate companies which operate in multiple countries, the data bears this out*.

Q: What should be the most important priority for insurers in the year ahead?

42% 42%

European equity analysts

Asia Pacific equity analysts

43% 43%

25% 69%

North American equity analysts

Improve operational efficiency | Sustain growth | Control risk

16%

14%

6%

* Whereas the survey findings contained elsewhere in this report refer to life insurers only, in this regional comparison the data for life, P&C and multiline insurers has been aggregated.

11

Implications for insurers Equity analysts are clear: notwithstanding difficult market conditions, they expect the leading life insurers to achieve strong growth in the next few years. This is probably because the largest firms* have grown at an average 6.5 percent between 2007 and 2011, with the top four** life performers achieving no less than an average 17.9 percent. The mean annual return on equity (RoE) for the largest companies was 12.5 percent since 2008, with the four most profitable life insurers averaging 18.5 percent.

What is certain is that analysts expect the companies they evaluate to achieve an RoE in excess of 15 percent. Growth will go some way toward delivering this profitability, as will cost reduction, but the primary focus will be on controlling risk. They list a number of other important considerations, such as asset management, service quality, pricing strategy and product innovation, but these are all contributors to their three priorities.

Achieving these goals will not be easy. The industry is facing more severe headwinds than most insurance executives have ever experienced. Demand is low and volatile, at least in mature markets, due to customers’ financial straits, their lack of confidence in equity-based investments, and their general mistrust of financial institutions. Low interest rates have decimated investment returns. Stock market volatility has made high-return guarantee products a risky proposition – repricing would help but the market resists this. Solvency II and Dodd-Frank, together with a steady stream of other new regulations, are forcing insurers to hold larger capital reserves and incur greater sales and other costs.

In emerging markets, conditions are more promising. Consumer demand is stronger, due to more buoyant economies as well as the rapid growth of affluent, under-insured middle classes. But to capitalize on this opportunity, global carriers need to equip themselves for success in unfamiliar environments while grappling with complex regulatory regimes and confronting local competitors which, in recent years, have become a lot more sophisticated.

Another opportunity is the retirement market, a traditional life insurance segment but one which has been under-exploited by the majority of carriers. A new global survey by Accenture***, of more than 8,000 consumers in 15 countries, has found that most people realize they need to save more now to provide for their retirement – but life insurers are not their preferred provider of retirement products. Eighty-six percent have little or no knowledge of insurers’ products, with half of these saying they have never received comprehensible retirement information from a life carrier. More than 60 percent have never been contacted by a life insurer or a broker to discuss their retirement needs. If insurers can improve their engagement with consumers they should be well placed to take advantage of this huge opportunity.

* All insurance companies with annual gross written premiums in excess of $50 billion.** Excluding Chinese insurance companies*** Accenture Retirement Services Survey, 2012

12

Controlling riskIt is hardly surprising, in the light of the growing regulatory and economic pressures to which insurers are subjected, that equity analysts place such a high premium on risk control. Even when underwriting is excluded, insurers are more exposed to different types of risk than companies in many other sectors – new regulations and reforms, and investment volatility are the risks that analysts believe pose the greatest danger.

They certainly agree that effective risk management is a more important contributor to profitability than cost reduction. Without the stability which risk control brings, investment in growth and cost reduction is discouraged. The appointment of a dedicated risk manager, supported by actuaries and reporting quarterly to the financial director, may achieve compliance but is insufficient to realize the significant value that risk management can generate.

It is worth bearing in mind that many of the new regulations affecting insurers are intended either to improve the stability of the organization or to ensure fair treatment of its customers. A good case can therefore be made for aiming beyond compliance. Risk should be a more important consideration in operational planning than it currently is. It should involve more than an understanding of the mechanics of risk, and should become a preoccupation of everyone in the company. It needs to be managed not quarterly, but daily, weekly and monthly.

By aligning risk management with their overall business strategy, and integrating it with their key business processes, insurers will not only ensure compliance but will enhance operational performance, reduce costs and deliver distinctively superior customer service.

For many carriers, the reliance on a complex array of diverse, aging platforms is an obvious risk to the business. Where risk cannot be avoided – the decision to exclude defined benefit schemes may not be feasible – better ways of sharing it need to be found. Investment volatility can be addressed by de-risking the assets on the balance sheet, a step which most companies will already have taken.

Other risk management priorities are the upgrading of data collection, analytics and reporting capabilities, and then the definition and implementation of an enterprise-wide framework for data management. Integrating risk and finance management processes throughout the organization is a key step, and a challenging one, but is vital to leveraging compliance initiatives to gain a competitive advantage.

Achieving growthThe demand for life insurance in North America and Europe is weak and penetration levels are declining as hard-pressed customers defer buying and even surrender their policies. In order to grow, analysts believe insurers need to turn this around – but they also need to be in emerging markets. Organic growth is their preferred strategy, but mergers and acquisitions in emerging markets is also important.

Moving into new regions will not be easy. Many countries, like China, are resisting the efforts of global carriers to enter their markets and compete against their local firms. As a result, this approach increases the risk of regulatory complexity – which analysts require insurers to control. What is more, the lack of homogeneity of emerging markets – the cultural differences are more significant than in Europe – makes it difficult for insurers to achieve economies of scale across borders.

While emerging markets may be crucial to the future performance of global groups, they are no panacea. Insurers must continue to do whatever they can to coax growth from their traditional markets. This may entail doing many things differently than they have in the past – their approach to the retirement market is a prime example. There is little doubt that to increase sales at home they will need to be more sophisticated in the ways they manage and engage with their customers.

To achieve organic growth, insurers need to focus on four measures of success: lead generation, close ratios, customer retention and customer penetration. A stronger brand is vital not only to new customer acquisition but also loyalty – which in turn is essential to retention and customer penetration.

The latter is especially important, with insurers needing to direct their creativity to getting more out of their existing customer bases.

To act decisively in a transforming marketplace, rich data, advanced analytics and predictive modeling are invaluable – they help insurers not only understand and segment their markets, but also to develop and continually refine their business and operating models to ensure they are ideally suited to customers’ needs.

The agility to swiftly create and configure new products is a key attribute, especially as the demand grows for more innovative as well as simpler products. In many cases, insurers are prevented by their legacy core platforms from responding effectively. An integrated multi-channel distribution strategy, incorporating innovations like mobility and social media, is also difficult to achieve with older platforms. Yet it is essential to meeting prospects’ engagement preferences and delivering the kind of service experience many customers require today. It can also significantly enhance the effectiveness of advisors.

Strategies for supporting organic growth will vary from region to region. Equity analysts believe that in Europe, an improved understanding of customer needs and behavior is their greatest asset. There is little doubt that in all mature markets, insurers will need to be more sophisticated in the ways they manage and engage with their customers. In Asia, where investment in multi-channel distribution lags the more developed markets, this is regarded as the priority to support growth.

In exploring the potential of emerging markets, life insurers should give careful thought to the suitability of their business model. They need to guard against adding only volume and complexity rather than scale and synergy. A global operating model which allows the insurer to capitalize on its proven assets, processes and capabilities, while adapting to local needs, is essential to geographic expansion.

13

Shared services centers are often viewed as an important component of a successful global operating model. However, Western-style shared services centers often under-deliver in emerging markets. Their focus is invariably on cost-reduction, and there is less redundancy to eliminate and scale is more difficult to attain. A much more powerful investment would be to create a growth-oriented shared services center which supports M&A integration and consolidation, and provides distribution support in the form of customer segmentation and predictive modeling; lead conversion analytics; agent recruitment, training, performance tracking and coaching; and perhaps direct selling.

Many emerging markets are at the stage of maturity where the greatest potential lies not in simply increasing the number of agents, nor in delivering a sophisticated, customized experience, but rather in effective cross-selling to customers who have only one or two products. Anything that helps agents identify and convert cross-sales prospects will contribute to growth in these areas.

Reducing costsThis late in the game, after many years of trimming the fat, there is little to be gained from isolated, piecemeal efforts to cut costs. These are more likely to impair operational performance, and marketing and sales effectiveness, than deliver meaningful savings. What is needed is a thorough review of the cost structure.

Most of the potential for permanently changing the cost structure will be found in old, inefficient and inflexible operating models. Business and product silos from an operations and technology perspective have created an unwanted level of complexity. Portfolio rationalization is, for many life insurers, a major opportunity to reduce costs. So too is business process and other forms of outsourcing, which have shown they can generate savings of up to 40 percent while also enabling a shift from fixed to variable costing.

The introduction of lower cost distribution channels, and their integration with traditional systems, can also drive efficiencies. However, investment decisions need to take cognizance of the fact that traditional channels are still the most productive, and in the short term may yield a greater return – a balanced approach may be appropriate.

While many carriers have transformed their distribution capabilities, fewer have addressed the cost to market of new products. In the current market, few things will have as great an impact on costs and profitable growth as the ability to price efficiently.

Another powerful lever of cost reduction, as discussed above, is scale. Two large companies may have the same gross written premium, but the one whose operations are concentrated on a few markets or in a few geographies is likely to be significantly more profitable than the other which is more widespread. The former affords the opportunity of all sorts of efficiencies, as well as a greater return on investments in marketing and distribution due to a higher concentration of resources.

If their expectations of profitable growth are to be met, insurers will have to significantly improve their use of technology. There is no silver bullet for solving this; it is likely that multiple levers will have to be pulled to simplify the existing legacy administration environment. Platform modernization will address the current high cost of manufacturing while also positioning the organization for future growth by enabling strategic capabilities in areas such as product configuration, analytics, digital marketing, mobility and social media.

14

Meeting analysts’ expectations will not be easy

Equity analysts have set the bar high. To achieve a favorable rating it will not be enough to tread water. Nor will sporadic interventions be sufficient – the market is changing too rapidly, and too fundamentally, for a fragmented approach to deliver the required results.

In order to rank among the high performers of the future, life insurers need to re-evaluate their business models. Some will have the capability, the balance sheet and the appetite to operate as a full-function carrier across multiple lines of business and multiple geographies. Others will realize they need to make some changes to compete at this high level. This may entail expanding the role of the chief financial officer to cut the administration cost of closed books and manage distribution profitability, or improving the balance sheet by selling the closed books and under-performing operating units. Certainly, without an effective presence in one or more high-growth emerging markets, insurers are unlikely to receive a favorable rating.

Other carriers may decide that specialization – achieving scale within a more confined operational, product or geographic footprint – is a surer strategy for success. Whichever approach they choose, the required mindset, operating model, infrastructure and capabilities will differ vastly, and may require far-reaching reorganization.

Change on such a scale is daunting. It need not be undertaken all at once, but it does need to be planned with a clear end-state in mind. Only in this way can every enhancement be a consistent step toward the ultimate goal.

While insurers may choose to target discrete market segments or geographies, or to specialize in specific aspects of the business, they don’t have the luxury of selecting which of the equity analysts’ priorities they will concentrate on. Many carriers are currently achieving effective risk management, growth or cost reduction. To achieve favorable evaluations in the future, however, nothing less than three out of three will satisfy this influential group.

To find out more about the Accenture Insurance Equity Analyst Survey, and how we can help you achieve a superior rating, visit our website at www.accenture.com/insurance.

About Accenture ResearchAccenture Research is Accenture’s global organization devoted to Economic and Strategic Studies. The staff consists of 150 experts in economics, sociology and survey research from Accenture’s principal offices in North America, Europe and Asia/Pacific.

About AccentureAccenture is a global management consulting, technology services and outsourcing company, with more than 249,000 people serving clients in more than 120 countries. Combining unparalleled experience, comprehensive capabilities across all industries and business functions, and extensive research on the world’s most successful companies, Accenture collaborates with clients to help them become high-performance businesses and governments. The company generated net revenues of US$25.5 billion for the fiscal year ended Aug. 31, 2011. Its home page is www.accenture.com.

12-2393/ 14-1012

Copyright © 2012 Accenture All rights reserved.

Accenture, its logo, and High Performance Delivered are trademarks of Accenture.