tim richison chief financial officer cas catastrophe seminar october 7 - 8, 2002 the challenges of...

TRANSCRIPT

Tim RichisonChief Financial Officer

CAS Catastrophe Seminar

October 7 - 8, 2002

The Challenges of Dealing with Natural Catastrophes

AGENDA

BACKGROUND

FINANCIAL OVERVIEW

RATING PLAN

MARKETING PLAN

Background

IntroductionIntroduction

CEA created by Statute during 1995/1996 in wake of Northridge Earthquake

• Voluntary coverage for consumers

• Carriers may elect to join the CEA and offer CEA coverage or their own policy

• CEA authorized to sell “Basic Residential Earthquake Insurance”

• Rates are required to remain actuarially sound

Mission Statement:The California Earthquake Authority is a privately funded, publicly managedorganization that provides Californians the ability to protect themselves, their homes, and their loved ones from earthquake loss.

In support of this mission, the CEA is committed to: Provide actuarially sound insurance coverage, while striving to make policies available

and competitively priced; Assure the Authority’s readiness and capability to handle claims promptly, fairly, and

consistently; Educate Californians about earthquake risk and options available to them to reduce that

risk; Provide tools and incentives for earthquake loss reduction and retrofitting; Use the best science available; Collaborate with organizations operating in the public interest that can help achieve

the CEA’s goals.

Allstate Insurance CompanyArmed Forces Insurance Exchange

Automobile Club of Southern CaliforniaCalifornia FAIR Plan

CSAAEncompass Insurance (formerly CNA)

Farmers GroupHomesite Insurance of California

Liberty MutualMerastarMercury

PrudentialState Farm

USAAWorkmen’s Auto Insurance

Current CEA Member CompaniesCurrent CEA Member Companies

Financial Overview

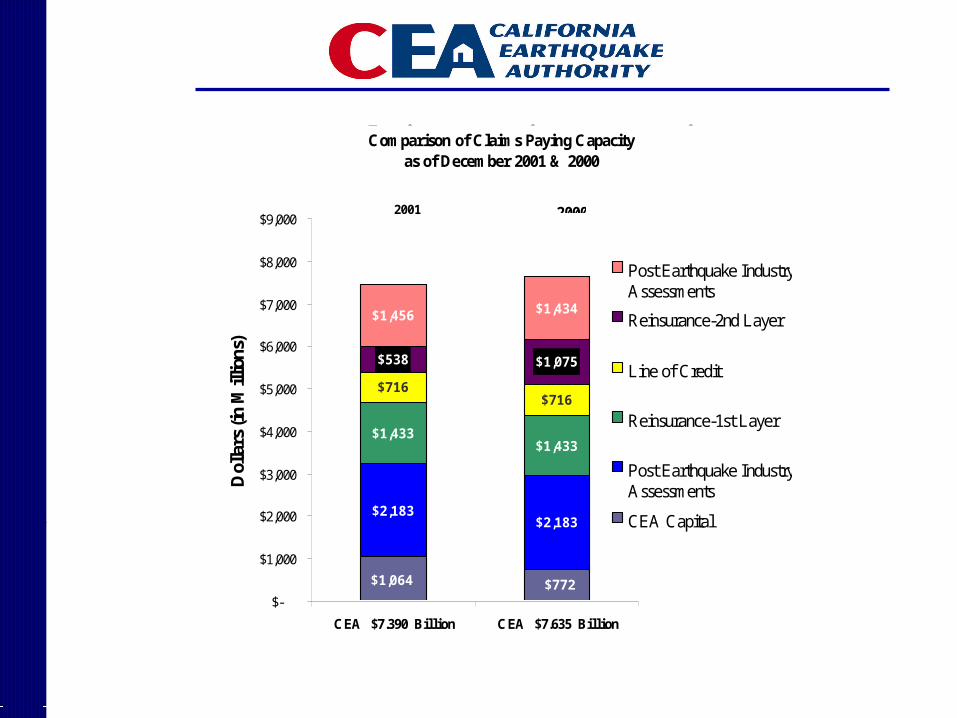

Claims Paying Capacityas of December 31, 2001

Comparison of Claims Paying Capacity as of December 2001 & 2000

$1,433

$716

$1,456

$1,064 $772

$2,183$2,183

$1,433

$716

$1,075$538

$1,434

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

CEA $7.390 Billion CEA $7.635 Billion

Dol

lars

(in

Mill

ions

)

Post Earthquake IndustryAssessments

Reinsurance-2nd Layer

Line of Credit

Reinsurance-1st Layer

Post Earthquake IndustryAssessments

CEA Capital

20002001

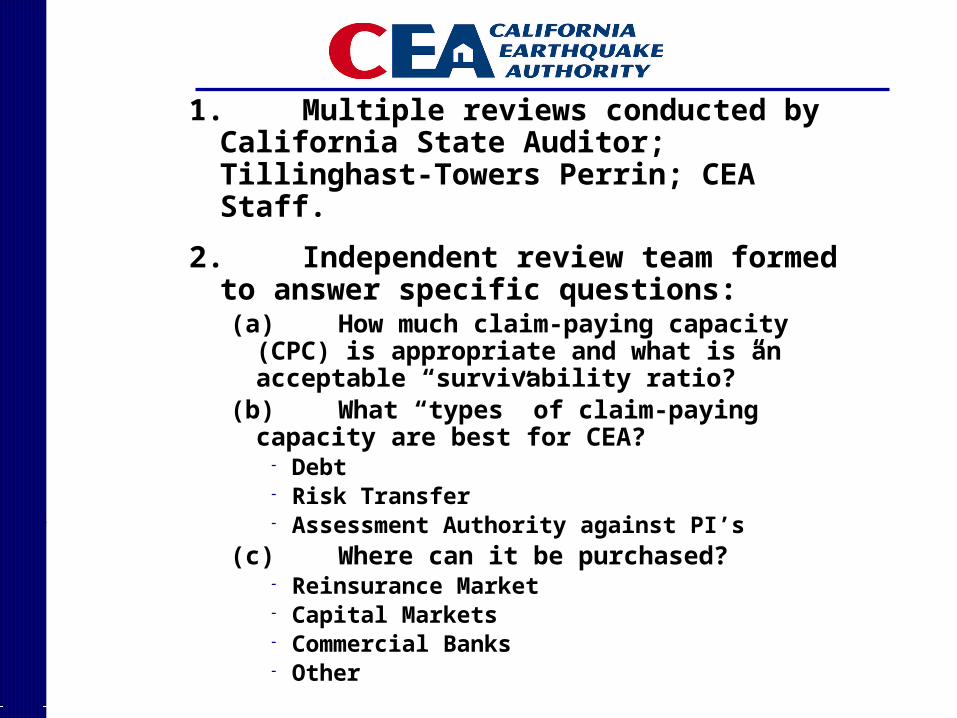

1. Multiple reviews conducted by California State Auditor; Tillinghast-Towers Perrin; CEA Staff.

2. Independent review team formed to answer specific questions:(a)How much claim-paying capacity (CPC) is

appropriate and what is an acceptable “survivability ratio?”

(b) What “types” of claim-paying capacity are best for CEA?

Debt Risk Transfer Assessment Authority against PI’s

(c)Where can it be purchased? Reinsurance Market Capital Markets Commercial Banks Other

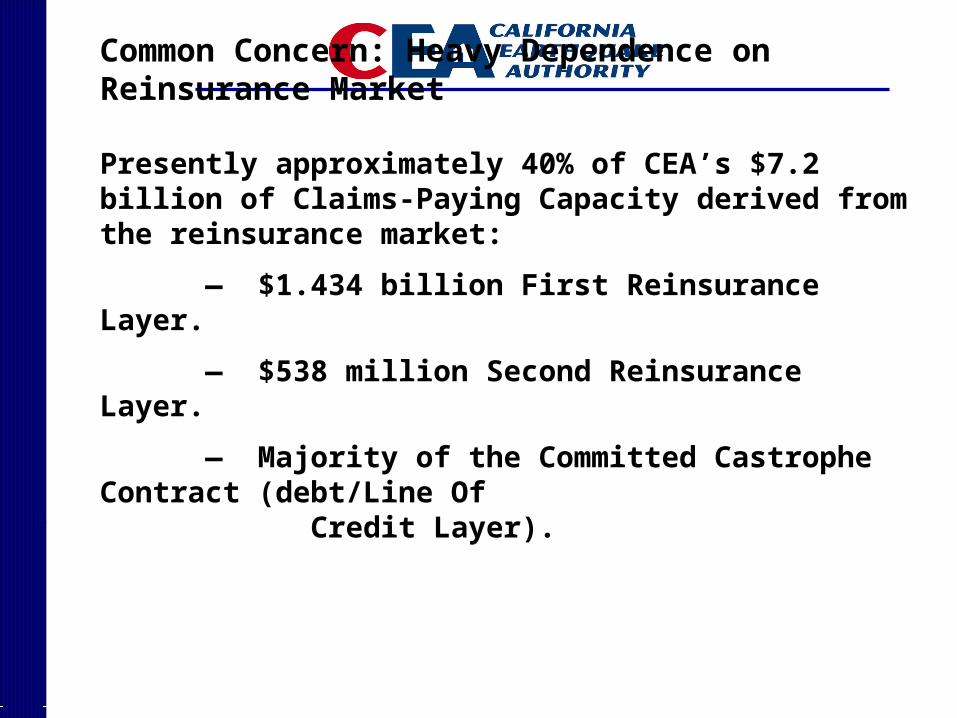

Common Concern: Heavy Dependence on Reinsurance Market

Presently approximately 40% of CEA’s $7.2 billion of Claims-Paying Capacity derived from the reinsurance market:

— $1.434 billion First Reinsurance Layer.

— $538 million Second Reinsurance Layer.

— Majority of the Committed Castrophe Contract (debt/Line Of Credit Layer).

Second Industry Assessment Layer

$1,456M$338M Fourth Reinsurance Layer

$616M Line of Credit – Interim GRB Financing

$600M First Reinsurance Layer

$100M Pre-Event General Revenue Bond Layer

$400M Second Reinsurance Layer

First Industry Assessment Layer

$2,183M

$1,110M Capital and Retained Earnings

$350M Minimum Statutory Capital

$5,547M

$717M***

$4,393M

$4,293M

$3,893M

$3,293M

$7,003M*

$5,009M

$200M Transformer Reinsurance Layer

$5,209M

CEA Financial Structure - Proposed at 1/1/03Second Industry Assessment Layer

$1,456M

$538M Second Reinsurance Layer

$717M CCC Layer** - Interim GRB Financing

First Reinsurance Layer$1,434M

$844M Capital and Retained Earnings

$350M Minimum Statutory Capital

$7,172M*

First Industry Assessment Layer

$2,183M

$5,716M

$4,461M

$5,178M

$3,027M

$844M

CEA Financial Structure - at 12/31/01

*Excluding the $350 million Minimum Statutory Capital, total claim-paying capacity at 12/31/01 is $7.172 billion; proposed claims-paying capacity at 1/1/03 is $7.003 billion.

Rating Plan

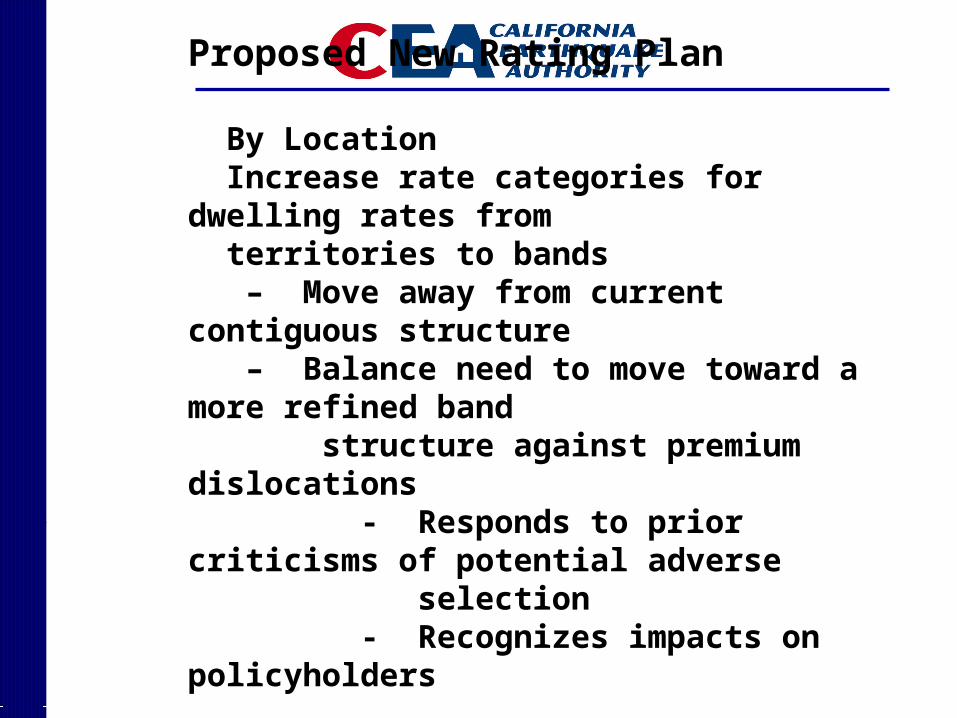

Proposed New Rating Plan

By Location Increase rate categories for dwelling rates from territories to bands – Move away from current contiguous structure – Balance need to move toward a more refined band structure against premium dislocations - Responds to prior criticisms of potential adverse selection - Recognizes impacts on policyholders

Proposed New Deductibles

20% deductible – 25% discount from base policy 25% deductible – 44% discount from base policy

Marketing Plan

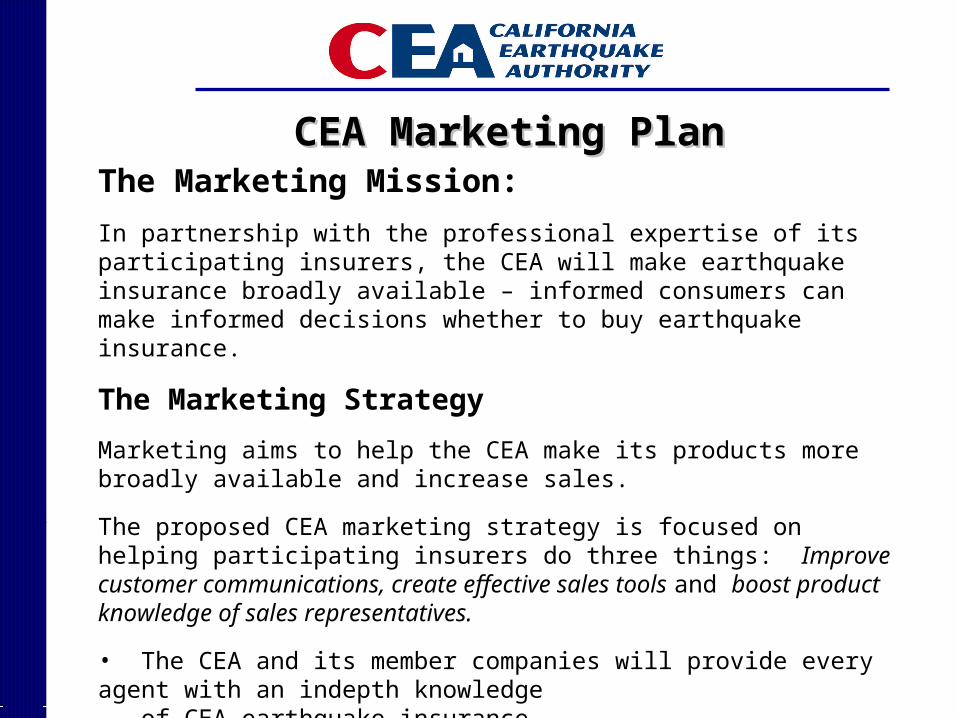

CEA Marketing PlanCEA Marketing PlanThe Marketing Mission:

In partnership with the professional expertise of its participating insurers, the CEA will make earthquake insurance broadly available – informed consumers can make informed decisions whether to buy earthquake insurance.

The Marketing Strategy

Marketing aims to help the CEA make its products more broadly available and increase sales.

The proposed CEA marketing strategy is focused on helping participating insurers do three things: Improve customer communications, create effective sales tools and boost product knowledge of sales representatives.

• The CEA and its member companies will provide every agent with an indepth knowledge of CEA earthquake insurance.• Every customer should have ample information to decide whether they should purchase earthquake insurance. The goal: To reach a point where no customer can say, “I wish I had known about earthquake insurance.”

CEA Marketing PlanCEA Marketing PlanObjectivesObjectives

1. In the 12 months beginning October 2002, each participating insurer will increase its earthquake market penetration rate* by two percent.

2. Secure from each participating insurer a written commitment that it will make earthquake insurance broadly available, increase the marketing of CEA products and target growth.

3. Hands-on help so that each participating insurer can develop an effective marketing plan.

4. Develop and distribute monthly reports to track participating insurer sales results.

*Market penetration rate is defined as the percent of CEA earthquake policies written, relative to the total number of residential properties in force.

CEA Marketing Plan (continued)CEA Marketing Plan (continued)

5. Create sales materials that participating insurers can use to educate consumers and increase earthquake insurance sales.

6. Expand training programs and make them Web-based to enhance sales reps’ and agents’ sales expertise.

7. Formally evaluate CEA products and analyze their pricing.

8. Contact non-CEA-member companies for possible inclusion in the CEA.

Questions