tiner insurance report

DESCRIPTION

gTRANSCRIPT

Financial Services Authority

Insurance SectorBriefing:Delivering the TinerInsurance Reforms

April2005

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 1

Foreword 3

1. Introduction and executive summary 5

2. A fair deal for consumers 11

3. Soundly managed insurance firms with adequate financial resources 19

4. Smarter regulation of insurance firms 29

Annex: relevant FSA Publications 38

Page 1

Contents

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 3

In autumn 2001, the FSA Board asked me to initiate a programme of reform to overhaulthe way in which insurance companies were regulated to address the deficiencies of theregime we had inherited. To do so, it was clear to me that wholesale and systematic changeacross all fronts was needed.

The modernisation of the insurance regime has been all encompassing. But in addition, theindustry has had to respond to other commercial and strategic challenges in this period. For lifeinsurers, these include a deep bear market in equities, the continuing shift from public toprivate pension provision, the erosion of consumer confidence in the long-term savings industryand with it the increasing unpopularity of the with-profits product, greater marketconcentration and the emergence of closed with-profits funds consolidators. For generalinsurers, the period has included the aftermath of the tragic events of 9/11, catastrophes such asthe hurricanes in the US and the floods closer to home, significant consolidation in thereinsurance industry and the implementation of a new conduct of business regime followingthe Insurance Mediation Directive. This is to name but a few. In short, since 2001 the operatingenvironment for the insurance industry has undergone nothing short of a seismic shift.

Once thought of as the poor cousin of financial services regulation, insurance regulation inthe UK is now holding its own and is broadly consistent with the regulation of othersectors. In particular, the newly-introduced requirement for all insurance companies toassess how much capital they actually need to support the risks of their business, and thenhold commensurate financial resources, is a radical departure from the previous one-size-fits-all model. It also marks the very welcome much closer alignment of economic andregulatory capital.

For life insurers, we have also fundamentally reviewed the framework within whichdiscretion is exercised in the management of with-profits funds and how their financialcondition is reported. We have issued new rules and guidance on the information madeavailable to with-profits policyholders in both open and closed funds. More generally, ourwork to modernise the disclosure regime for all investment products continues. And welook forward to working with the industry and other stakeholders to introduce practicablerequirements that address the shortcomings of the current regime.

We have also radically altered our regulatory approach to Lloyd’s of London, bringing itinto line with the way in which other non-life insurers are regulated. And we haveimplemented the Insurance Mediation Directive bringing retail and wholesale generalinsurance brokers within FSA regulation for the first time. We hope that these newconstituents will seize on the advent of statutory regulation as a catalyst for modernisingtheir processes and business models. In addition, we have introduced a new conduct ofbusiness regime for general insurers, thereby enhancing the protection for consumers.

Foreword

Change has also been apparent within the FSA as well. We have taken a long hard look atthe way in which we regulate the insurance sector. True to our form as an integratedregulator, over the last few years we have focused on ensuring that supervisors give the rightlevel of attention to a firm’s financial condition, the way it is managed and the interactionwith its customers throughout the product or policy life-cycle. Our new risk assessmentprocess has now become a fixed point on the regulatory landscape, with some internationalregulators looking to follow our lead. All but the smallest insurance firms have now beenthrough the risk assessment process and through this recognise that the relationship with ushas become more proactive and challenging than under the previous regulatory system.Importantly, the last few years have also seen something of a cultural change among ourinsurance staff. As well as increasing numbers by recruiting from the industry, there has beena greater push to help ensure that our staff have the correct skills and experience.

This report marks the transition from design to delivery in respect of our original set ofreforms. It seeks to compare and contrast the old with the new requirements and in doing soillustrate how the individual reforms interlock to reinforce a regime that should inspireconfidence in the sector. Collectively, the reforms mark change of the highest order in theinsurance industry. Once fully embedded, they will make for an industry that is collectivelyin stronger financial health and much better positioned to prosper in a world in whichconsumers wield increasing power.

Three and half years on in 2005, it is clear the enormous progress that has been achievedhas been possible only through the partnership approach that we adopted from the outset.But there is still more to be done to complete the implementation of the new regime. Wealso continue to be fully engaged in developments on the European and wider internationalfronts that will impact on the UK insurance sector. The impact of other initiatives we havetaken since we started our modernisation programme will also be keenly felt in theinsurance sector – especially our work on Treating Customers Fairly and the depolarisationof the investment advice market. And, of course, our initiatives on contract certainty andthe management of conflicts of interest in the general insurance market are providing newchallenges and opportunities as well. We recognise fully the commitment that the industryhas shown in helping us develop a modernised regime and, now that the foundations havebeen laid, we look forward to a continuing constructive partnership as the reforms bed inand become a reality.

John TinerApril 2005

Insurance Sector Briefing: Delivering the Tiner Insurance ReformsPage 4

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 5

Background

1.1 In October 2001 the Economic Secretary to the Treasury asked the FSA to report on theactions we intended taking to implement the recommendations set out in the Baird Reportinto the FSA’s regulation of Equitable Life. The Baird Report, which had been commissionedby our Board, made several recommendations about the regulation of the insurance sector.1

1.2 In addition to the concerns surrounding the regulation of Equitable Life, other issuespointed to the stark need for change in the regulation of the insurance industry. Theseincluded instances of mis-selling, the problems surrounding Independent Insurance and thelow ebb of consumer confidence. In addition to this, the creation of a single unifiedregulator highlighted the significant differences between the regulation of insurance andother parts of the financial services industry.

1.3 So the case for reforming the regime that we had inherited was therefore very clear; notonly in terms of the specific rules for the sector but also in relation to the way in whichthese were applied by the regulator. The programme to modernise the regulatory regimewas led by the then Managing Director, John Tiner, and had three distinct but interrelatedcomponent parts designed to help ensure:

• a fair deal for consumers;

• soundly managed insurance firms with adequate financial resources; and

• smarter regulation of insurance firms.

1.4 Collectively, these became known as the Tiner Reforms, and were initially set out in Thefuture regulation of insurance (November 2001) and The future regulation of insurance: aprogress report (October 2002). 2005 is the year in which a critical mass of these reformsis being implemented – from the integrated Prudential Sourcebook being switched on andchanges to the role of actuaries in life offices, through to new reporting requirements and anew regime for with-profits.2 As such, this report marks the move from policydevelopment to implementation and delivery, and sets out what has been achieved undereach of the three broad headings above. The report also provides details of other policydevelopments and changes to the way we regulate the insurance sector.3 Although notstrictly part of the Tiner Reforms, these illustrate further the scope and depth of thetransformation that has taken place since 2001.

1.Introduction and executive summary

1 The Regulation of Equitable Life: an independent report, Ronnie Baird (September 2001).

2 Some of the specific reforms described in this report – notably changes to the prudential regime and the with-profits review,predated 2001 but were taken forward as part of the package of reform for insurers.

3 Some of these, such as our approach to financial capability, Treating Customers Fairly and the risk assessment process, clearlyhave an application that goes well beyond insurance.

Insurance Sector Briefing: Delivering the Tiner Insurance ReformsPage 6

1.5 Since the launch of the reform programme in 2001, a number of additional industryreports have been published, including Sandler and Penrose.4 We have taken full accountof the recommendations of these reports in developing and taking forward the individualcomponents of the Tiner Reforms.

A fair deal for consumers

1.6. Two of our four statutory objectives are directly associated with securing a fair deal forconsumers: promoting public understanding of the financial system; and securing theappropriate degree of protection for consumers. Consequently, the fair treatment ofcustomers is a central tenet of our regulatory approach across the financial services industry.

1.7 Reforms to help deliver these objectives for insurance have centred on three mainoutcomes:

• firms treat their customers fairly before, during and after the point of sale;

• consumers make better informed decisions; and

• a liberalised framework for financial advice.

1.8 The majority of these reforms have mainly affected life insurance firms. However, we havealso introduced a new conduct of business regime for non-life insurance and intermediariesfrom January 2005 (along with the implementation of the Insurance Mediation Directive(IMD)), benefiting general insurance customers as well.

Soundly managed insurance firms with adequate financial resources

1.9 Consumers need to have confidence that the insurance firm they deal with is soundly managedand has sufficient resources to honour any commitment it makes. But as well as supportingour consumer protection objective, financial soundness is also key to securing confidence inthe market. Complementing the reforms to help ensure that consumers get a fair deal, thesecond key area for change concerns the prudential regulation of insurance firms.

1.10 Change has been wholesale, focusing on three outcomes:

• adequate financial resources;

• sound management; and

• streamlined financial reporting.

1.11 Delivery on each of these three fronts has required a sustained effort from us and theregulated community, both in terms of developing the new approaches and also inimplementing them. We believe that once fully embedded the new prudential requirementswill make for a much fitter and financially sounder industry.

4 Sandler Review of Medium and Long-term savings in the UK (July 2002) and Report of the Equitable Life Inquiry (2004).

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 7

Smarter regulation of insurance firms

1.12 Supporting the new regulatory requirements, the reform programme has also modernisedthe ways in which we go about the business of insurance regulation. Here, the reformprogramme has sought to:

• implement a proactive, risk-based regulatory approach, including deploying resourcesto areas of greatest risk;

• consolidate the structural changes already made within the FSA to deliver anintegrated approach to regulating insurance firms, that encompasses both prudentialand conduct of business issues;

• develop more effective working relationships with those firms posing a greater risk toour statutory objectives; and

• deliver insurance supervisors who operate effectively in the new environment.

1.13 The delivery of these reforms has radically altered the relationship between the regulatorand the regulated, resulting in a much more cohesive and integrated regulatory frameworkthat is underpinned by a challenging and proactive risk-based approach.

Cost benefit analysis and consultation

1.14 In line with the requirements set out in the Financial Services and Markets Act 2000(FSMA), and our commitment to openness and transparency, we have publicly consultedon all of the rule changes and guidance that form part of the Tiner Reforms. Weacknowledge that the volume of consultation material the modernisation programme hasgenerated has been significant. We appreciate the efforts of the industry and otherstakeholders in reading, digesting and responding to this material. It was important to usthat the changes we planned would be workable, minimise unintended consequences onmarket structure and be proportionate to the risks identified. Since 2001, we also havemade increasing use of detailed consumer testing of our proposals and have founddialogue with the industry to be extremely valuable and on the whole constructive.

1.15 FSMA also requires that the benefits of the reform programme outweigh the costs. And, assuch we have carried out full and rigorous cost benefit analyses for each change to theregime. Examples of where the CBA process has resulted in us altering our proposalsinclude:

• the way in which we modified the definition of ‘customers’ in the Insurance Conductof Business sourcebook (ICOB);

• permitting co-mingling of client and insurer monies by general insuranceintermediaries;

• limiting the requirement for firms to report on the realistic basis to those with with-profits liabilities in excess of £500m; and

• our decision not to require firms to send Consumer Friendly PPFMs to existing with-profits policyholders who do not receive annual statements.

Insurance Sector Briefing: Delivering the Tiner Insurance ReformsPage 8

Conclusion

1.16 Together, the Tiner Reforms have transformed the regulatory regime for insurers. Theimpact of each individual reform will be significant and far-reaching: changes to the wayin which insurers interact with their customers; changes to the way in which companiescalculate how much capital they need to support the risks of their business; and changes tothe way in which insurance companies manage their business. Combined with changes tothe way in which regulation is carried out and the collective impact of the reformsbecomes immense.

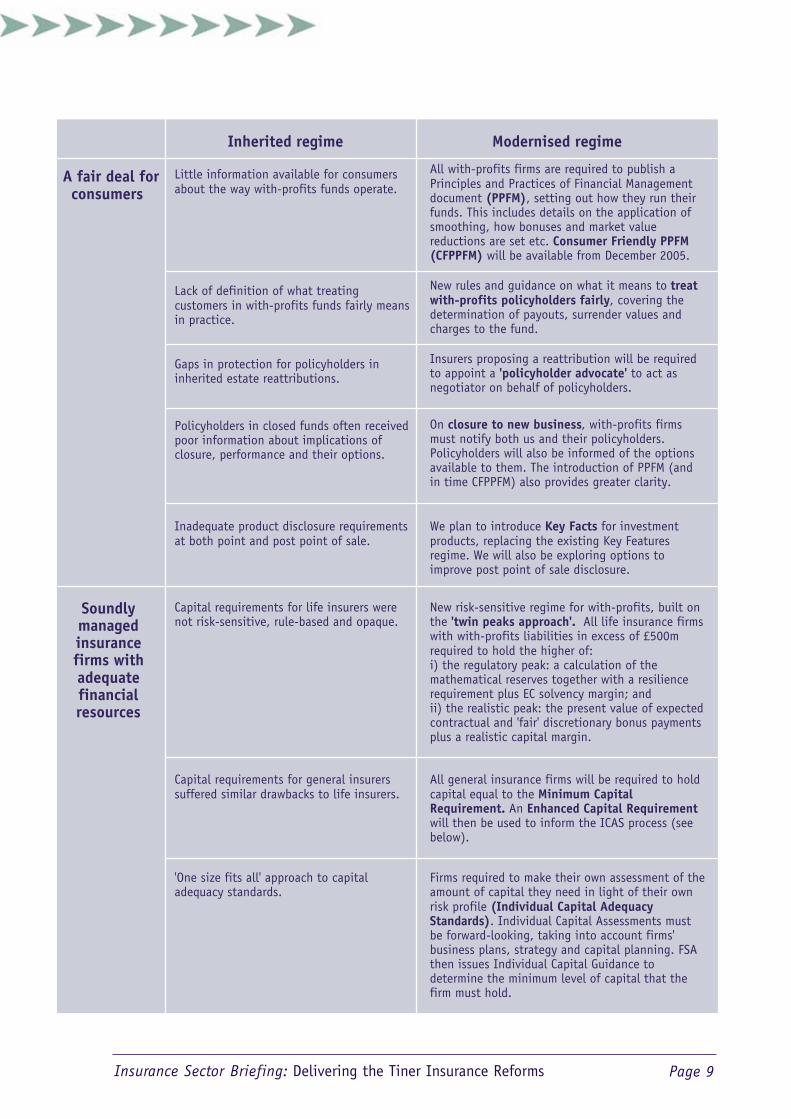

1.17 This report marks the transition from policy development to implementation and, as such,it is too early to pass judgement on how the industry will assimilate and embed thereforms. Our objective was to modernise the regime so it will deliver an industry that isfinancially sounder and that serves both its investors and customers well, withoutinterfering with market forces such as competition, innovation and choice.5 We believethe Tiner Reforms will achieve this. The table overleaf summarises the key reforms,illustrating the stark differences between the regime that we inherited and the modernisedregime that is now being delivered.

1.18 Regulation must necessarily evolve to keep pace with market developments, and thisapplies equally to insurance regulation as to any other sector. In addition to keeping a keeneye on developments in Europe and beyond, we will continue refining our own regulatoryprocesses and monitoring the ways in which the industry responds to the new regulatoryenvironment. If further changes are deemed necessary, we will take these forward in aproportionate and risk-based manner.

5 Both our prudential and conduct of business rules aim to deliver an appropriate degree of protection. But they do not attempt todeliver a zero-failure regime.

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 9

Inherited regime Modernised regime

Little information available for consumersabout the way with-profits funds operate.

All with-profits firms are required to publish aPrinciples and Practices of Financial Managementdocument (PPFM), setting out how they run theirfunds. This includes details on the application ofsmoothing, how bonuses and market valuereductions are set etc. Consumer Friendly PPFM(CFPPFM) will be available from December 2005.

Lack of definition of what treatingcustomers in with-profits funds fairly meansin practice.

New rules and guidance on what it means to treatwith-profits policyholders fairly, covering thedetermination of payouts, surrender values andcharges to the fund.

Gaps in protection for policyholders ininherited estate reattributions.

Insurers proposing a reattribution will be requiredto appoint a 'policyholder advocate' to act asnegotiator on behalf of policyholders.

Policyholders in closed funds often receivedpoor information about implications ofclosure, performance and their options.

On closure to new business, with-profits firmsmust notify both us and their policyholders.Policyholders will also be informed of the optionsavailable to them. The introduction of PPFM (andin time CFPPFM) also provides greater clarity.

A fair deal forconsumers

Inadequate product disclosure requirementsat both point and post point of sale.

We plan to introduce Key Facts for investmentproducts, replacing the existing Key Featuresregime. We will also be exploring options toimprove post point of sale disclosure.

Capital requirements for life insurers werenot risk-sensitive, rule-based and opaque.

New risk-sensitive regime for with-profits, built onthe 'twin peaks approach'. All life insurance firmswith with-profits liabilities in excess of £500mrequired to hold the higher of:i) the regulatory peak: a calculation of themathematical reserves together with a resiliencerequirement plus EC solvency margin; andii) the realistic peak: the present value of expectedcontractual and 'fair' discretionary bonus paymentsplus a realistic capital margin.

Capital requirements for general insurerssuffered similar drawbacks to life insurers.

All general insurance firms will be required to holdcapital equal to the Minimum CapitalRequirement. An Enhanced Capital Requirementwill then be used to inform the ICAS process (seebelow).

Soundlymanagedinsurancefirms withadequatefinancialresources

'One size fits all' approach to capitaladequacy standards.

Firms required to make their own assessment of theamount of capital they need in light of their ownrisk profile (Individual Capital AdequacyStandards). Individual Capital Assessments mustbe forward-looking, taking into account firms'business plans, strategy and capital planning. FSAthen issues Individual Capital Guidance todetermine the minimum level of capital that thefirm must hold.

Insurance Sector Briefing: Delivering the Tiner Insurance ReformsPage 10

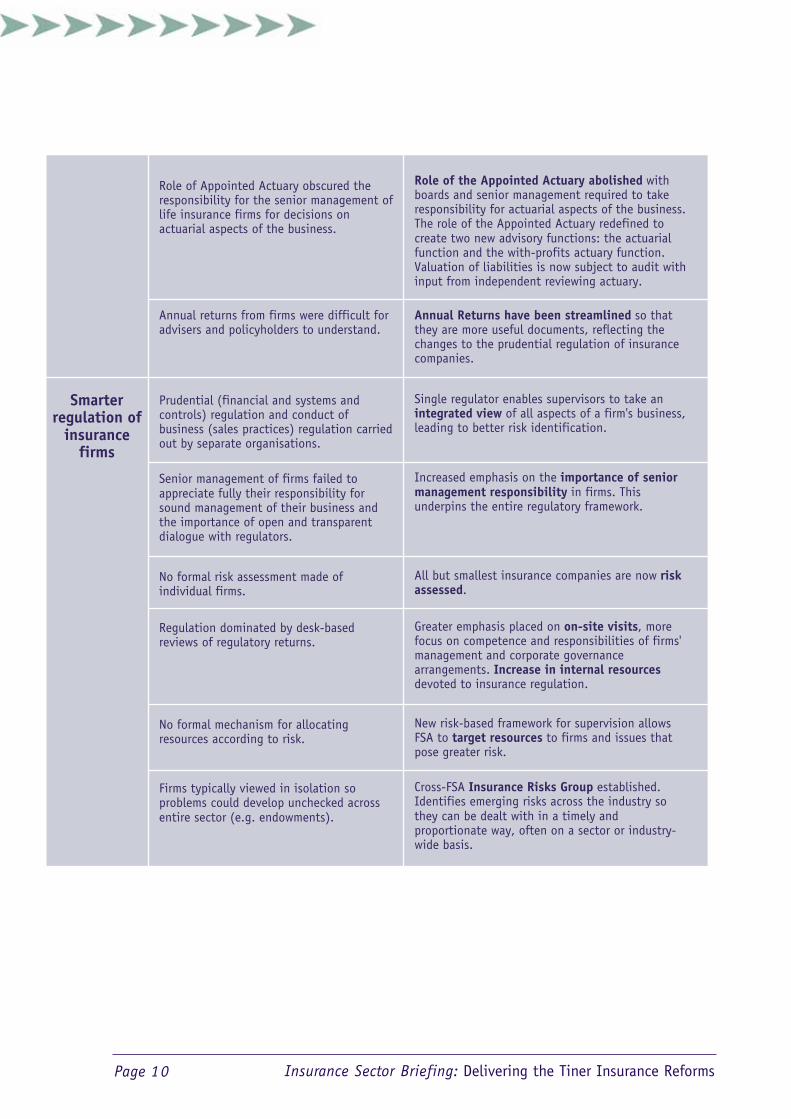

Role of Appointed Actuary obscured theresponsibility for the senior management oflife insurance firms for decisions onactuarial aspects of the business.

Role of the Appointed Actuary abolished withboards and senior management required to takeresponsibility for actuarial aspects of the business.The role of the Appointed Actuary redefined tocreate two new advisory functions: the actuarialfunction and the with-profits actuary function.Valuation of liabilities is now subject to audit withinput from independent reviewing actuary.

Annual returns from firms were difficult foradvisers and policyholders to understand.

Annual Returns have been streamlined so thatthey are more useful documents, reflecting thechanges to the prudential regulation of insurancecompanies.

Prudential (financial and systems andcontrols) regulation and conduct ofbusiness (sales practices) regulation carriedout by separate organisations.

Single regulator enables supervisors to take anintegrated view of all aspects of a firm's business,leading to better risk identification.

Senior management of firms failed toappreciate fully their responsibility forsound management of their business andthe importance of open and transparentdialogue with regulators.

Increased emphasis on the importance of seniormanagement responsibility in firms. Thisunderpins the entire regulatory framework.

No formal risk assessment made ofindividual firms.

All but smallest insurance companies are now riskassessed.

Regulation dominated by desk-basedreviews of regulatory returns.

Greater emphasis placed on on-site visits, morefocus on competence and responsibilities of firms'management and corporate governancearrangements. Increase in internal resourcesdevoted to insurance regulation.

No formal mechanism for allocatingresources according to risk.

New risk-based framework for supervision allowsFSA to target resources to firms and issues thatpose greater risk.

Smarterregulation of

insurancefirms

Firms typically viewed in isolation soproblems could develop unchecked acrossentire sector (e.g. endowments).

Cross-FSA Insurance Risks Group established.Identifies emerging risks across the industry sothey can be dealt with in a timely andproportionate way, often on a sector or industry-wide basis.

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 11

2.1 With two of our statutory objectives directly associated with consumers (promoting publicunderstanding and securing the appropriate degree of consumer protection), it isabsolutely clear that much of our time should be spent on helping them to secure a fairdeal. In this respect, the Tiner Reforms have concentrated principally on issuessurrounding disclosure and transparency. In addition, there have also been importantdevelopments that go well beyond the insurance sector, most notably in our work onfinancial promotions, and the broader Treating Customers Fairly (TCF) initiative.6

2.2 As well as new rules and guidance to help ensure that consumers get a fair deal, there is aclear need for a greater push on financial capability to help redress the imbalance ofinformation that typically characterises the relationship between the financial servicesindustry and its customers.7 For insurance, this is particularly important given thecomplex nature of products such as with-profits policies.

2.3 The reforms described in this chapter were designed to help deliver the following threeoutcomes:

• firms treat their customers fairly before, during and after the point of sale;

• consumers make better informed decisions; and

• a liberalised framework for financial advice.

2.4 In addition, we have also recently introduced a new conduct of business regime for generalinsurers and intermediaries. Although not part of the Tiner Reform’s original scope (theregime was implemented as part of the IMD), these new requirements will help deliver afair deal for general insurance customers also.

2.5 It is early days to see the impact of these reforms. But we would expect that once fullyembedded they will contribute to restoring consumer confidence in the industry.

Firms treat their customers fairly before, during and after the point of sale

2.6 One of the principal concerns we had over the inherited regime related to the opacity andcomplexity of with-profits and some aspects of the way in which with-profitspolicyholders were being treated. The inadequacy of the existing disclosure requirements

2.A fair deal for consumers

6 Treating Customers Fairly – progress and next steps (July 2004)

7 We made clear in the original report on the Tiner Reforms that, as set out in FSMA (s. 5(2)), we support the general principle thatconsumers should take responsibility for their own decisions. That position remains unchanged.

Insurance Sector Briefing: Delivering the Tiner Insurance ReformsPage 12

was another catalyst for reform. Consequently, key deliverables have included the radicaltransformation of the way in which with-profits funds are regulated, including makingmore information available to consumers. In addition, we continue to develop a newdisclosure regime encompassing both point of sale and post sale.

2.7 Although we have indicated that TCF is a principles-based initiative, we have also madeclear that if necessary we will consult on adding to the Handbook with rules and guidanceon specific areas that require attention. With-profits was one such area where it was clearthat there was a need for greater definition on what treating policyholders fairly meant.

Reforming with-profits

2.8 In response to increasing concerns over with-profits products, we announced a wide-ranging review of with-profits business in February 2001. Although this began prior to thelaunch of the wider Tiner Reforms, the changes that the With-Profits Reviewrecommended have been folded into the broader modernisation programme.8

2.9 The main step that we have taken to increase transparency in how with-profits funds areoperated is through introducing publicly-available documents known as PPFM (Principlesand Practices of Financial Management). Designed to set out how an insurer manages itswith-profits business, the PPFM covers key information, including how policy payouts aredetermined, the investment strategy and charges and expenses. Since April 2004 insurerscarrying on with-profits business have been required to produce these documents and tomake them freely available to policyholders.

2.10 Although still in their infancy, it is clear that PPFMs have proved a valuable governancediscipline. However, to help ensure that consumers read and understand the most importantinformation that is contained in them, we are also requiring firms to produce a consumer-friendly version by December 2005.9 We will be working closely with the industry to helpintroduce higher quality documents and greater consistency of format. We will also beexploring ways to promote their use by the advisory sector and other external stakeholders.

2.11 All with-profits companies are now also required to report to policyholders on whetherthey have complied with the PPFM obligations. The with-profits actuary will be requiredto report publicly on whether, in their opinion, the insurer’s report to policyholders andthe discretion it has exercised may be viewed as having taken policyholders’ interests intoaccount in a reasonable and proportionate manner.10 In addition, new guidance ongovernance standards supports the desirability of bringing independent judgement to bearon the assessment of an insurer’s compliance with its PPFM and how it has handledconflicts of interests between different groups of policyholders and, if relevant, betweenpolicyholders and shareholders.11

8 Full details of the With-Profits Review can be found on the FSA website: www.fsa.gov.uk/pubs/other/with_profits/

9 PS05/01: Treating with-profits policyholders fairly – feedback on CP04/14 and made text (Jan 2005)

10 Reform to the role of actuaries in life offices is covered in more detail in the next chapter, paragraphs 3.33 – 3.40.

11 A survey that we carried out in November 2004 indicated that in response to this guidance, a number of with-profits insurers arenow introducing With-profits Committees of the Board.

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 13

2.12 New rules and guidance on treating with-profits policyholders fairly will also beintroduced later this year. Codifying good practice in the industry, these address how thefirm determines payouts, surrender values, charges to the fund and terms for newbusiness.12 Going forward, when a fund closes to new business it will be required to notifyboth us and its policyholders promptly. Further, it must inform policyholders of optionsavailable to them and submit a run-off plan to us.

2.13 We have also introduced new rules and guidance to improve the process for thereattribution of inherited estates to ensure that policyholders’ interests are adequatelyrepresented. These take account of concerns voiced over the processes followed in anumber of reattributions carried out between 1985 and 2000, including some confusionabout the regulator’s role. The central plank of our new requirements is to require insurersproposing a reattribution to appoint a ‘policyholder advocate’ to act as negotiator onbehalf of policyholders.

Treating Customers Fairly

2.14 We have described above the specific measures we have taken to help ensure with-profitspolicyholders are treated fairly. But, more broadly, TCF in its generic sense is a key priorityfor the FSA that we see as helping tackle the range of market failings of recent years. Ifsuccessful, TCF will contribute to restoring confidence in the financial services sector.

2.15 Most importantly, we want to ensure that firms’ senior management take responsibility fortheir obligation to treat their customers fairly.13 In many cases, this is likely to involvegreater or more effective disclosure and transparency, consistent with the specificallytargeted work on with-profits as described above. Evidence of positive steps that someregulated firms, including insurers, are taking to ensure they are treating their customersfairly is starting to emerge. However, progress is not uniform across the insurance sectorand it is clear that some firms need to do much more than others. We recognise thevaluable contribution that organisations such as the Association of British Insurers (ABI)are already making in this area and will continue to work with the trade associations andconsumer bodies to bring about the standards we expect of the firms we regulate.

2.16 As we have no current plans to introduce additional rules on TCF in the wider sense, tohelp firms understand what we expect of them we have begun publishing material on ourwebsite giving examples of good and bad practice. In June, we will publish a progressreport on work that has been completed and set out our priorities for the coming year. Atthat stage, we also plan to publish a series of case studies which we hope will further helpcompanies implement their strategies.

2.17 Assessing TCF will be built into the normal supervisory process, but at this stage our focushas been to establish whether companies are evaluating where they are and taking steps toimplement TCF strategies. As time goes on, we will increasingly want to look at moredetailed aspects of individual businesses. Given our new responsibility for insuranceintermediation and a new conduct of business regime for general insurers, we will bestarting to consider the application of TCF in this market.

12 PS05/01: Treating with-profits policyholders fairly – feedback on CP04/14 and made text (Jan 2005)

13 Principle 6 requires firms to pay due regard to the interests of their customers and treat them fairly.

Insurance Sector Briefing: Delivering the Tiner Insurance ReformsPage 14

Disclosure review

2.18 It is clearly in consumers’ (and the industry’s) interests that the disclosure regime is aseffective as possible so that consumers can make more informed decisions about what theyare buying and understand better the consequences of their purchase. But our research hasshown that consumers often find the information they receive difficult to understand. Theymay also be put off by the length or not even read the material at all. Having alreadyimplemented Key Facts for buyers of mortgages and general insurance products, in 2005 wewill launch Key Facts as the main disclosure vehicle for buyers of investment products,replacing the existing Key Features regime.14 This will bring significant benefits, withconsumers seeing clear, concise and consistent information (including on costs) about theproducts they are buying.

2.19 In addition to the literature that is given to consumers at the point of sale, it is also clearlyimportant that policyholders are kept informed of how a product or service is performingthroughout its life cycle, so they can manage their finances effectively. The existing post-sale requirements do not apply to all packaged products.15 We recognise that the ABI’sRaising Standards initiative has made a valuable contribution in this area by requiringaccredited firms to provide their customers with yearly statements on the progress of theirinvestment, but it is clear that more needs to be done.

2.20 The Disclosure Review therefore continues to focus on improving the quality ofinformation on packaged products provided to customers both at, and after, the point ofsale. Our aim is to publish a Consultation Paper later this year, setting out:

• feedback from our initial consultation on disclosure (CP170) on the consumerinformation supplied at the point of sale for packaged products and on furtherresearch and policy work we have conducted in light of that consultation;

• new proposals for Key Facts for investment products, to replace Key Features. Theseproposals will include our response to the Treasury Select Committee’s recommendationsthat we develop a summary box for key information on investment products and explorethe viability of a standardised consumer-friendly risk rating system;

• feedback on our Discussion Paper on projections (DP 04/01) and proposals for a newapproach to projections; and

• new proposals for information after the point of sale on packaged products.

Financial promotions

2.21 Again, despite having a wider application than just insurance, our work on financialpromotions is critical in helping us ensure that consumers get a fair deal. In particular, we want firms to be clear on how they think about customers from the product designstage onwards.

14 This is the principal disclosure vehicle to date for packaged products. Packaged products include: life policies with an investmentelement; personal pensions, including stakeholder pension schemes; units or shares in collective investment schemes; andinvestment trust savings schemes.

15 In addition, for some products (such as pensions) there is a requirement for firms to produce annual statements, whereas for lifepolicies no similar requirement exists.

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 15

2.22 Our role involves:

• reviewing promotions in a variety of media;

• investigating complaints made to us by members of the public and firms;

• assessing firms’ systems and controls through visits;

• communicating with the industry and consumers about the work we are doing andexplaining what they can do to help themselves and us; and

• taking appropriate regulatory action where firms do not comply with our rules.

2.23 To encourage both consumers and firms to report promotions that seem misleading orunbalanced, we now have a Financial Promotions Hotline and an online reporting form.The Hotline was launched in July 2004 and has proved a valuable source of intelligencefor our monitoring work.

Unfair contract terms

2.24 Under the Unfair Terms in Consumer Contracts Regulations 1999, we consider complaintsabout clauses in particular contracts and carry out thematic reviews to identify terms thatcause significant consumer detriment. One output of this work will be a Statement ofGood Practice on premium review clauses. This will set out our views on what firms needto do to ensure that terms giving firms the power to vary the premiums payable for certainlife and long-term health-related policies are fair and operated fairly.

Complaints handling

2.25 Across the FSA we have been examining the ways in which firms handle customercomplaints and the use they make of complaints data to improve the quality andsuitability of their products and advice. As we set out in a ‘Dear CEO’ letter issued at theend of 2004, one area of particular concern in the insurance sector related to mortgageendowments. Through supervision – and enforcement action if necessary – we willcontinue working to ensure that insurers take the necessary steps to review their processesand comply with our requirements.

Consumers make informed decisions

Financial capability

2.26 We believe that increased public understanding and awareness will deliver more capableand confident consumers who will be better equipped to: manage their financial affairssuccessfully; exercise a greater influence in the retail market; be in a position to takegreater responsibility for their own actions; and be better able to protect themselvesthrough less mis-buying and by being less susceptible to mis-selling.

2.27 The National Strategy for Financial Capability is a long-term project involving a range ofpartners – Government, the financial services industry (including some insurers), tradeassociations (including the ABI), employers’ organisations and trade unions, the media,consumer organisations and the voluntary sector. Launched in November 2003, theStrategy aims to deliver a step change in financial capability, through a combination ofinformation, education and generic advice. A Steering Group, led by John Tiner butdrawing on expertise from across the financial services industry and beyond, will drive theStrategy forward.

2.28 Although the Strategy is clearly relevant to all consumer-facing financial services sectors,delivering greater financial capability would have a tangible impact on the insurancesector, given the broad exposure that consumers have to the sector, through productsranging from household and motor insurance through to critical illness and annuities.

2.29 The Strategy’s work has been split into seven priority areas. These are: schools, young adults,families, workplace, borrowing, generic advice and retirement. Key deliverables include:

• the launch of the schools project by the end of the third quarter in 2005, which aimsto enhance resources for teaching personal finance education in schools;

• the publication during the second quarter of 2005 of good practice research on how toraise financial capability among young adults;

• developing the business case for rolling out financial capability initiatives in theworkplace, during the third quarter of 2005;

• launching a financial healthcheck tool on websites (including our website) in thesecond quarter of 2005. This will help consumers to identify and understand theirfinancial needs, identify possible priorities and next steps and identify other relevantsources of information and advice;

• a credit self-assessment tool will be launched during the third quarter of 2005, whichwill allow users to gain an understanding of whether they are at risk of becoming over-indebted; and

• establishing a modest innovation fund for the voluntary sector to support new ideasfor, and ways of, increasing financial capability.

2.30 In addition we are carrying out a comprehensive ‘baseline survey’ to measure levels offinancial capability. This is the first time that such a survey has been conducted and it willallow us to measure improvements in financial capability in the future. We will publish theresults of this survey in the first quarter of 2006.

Consumer information provided by the FSA

2.31 We continue providing consumer information and services through our consumer website,publications and contact centre, including a range of materials on insurance-related issues.Most recently, addressing specific concerns over consumer understanding of with-profitsproducts, we published a list of ten questions designed to help with-profits policyholders

Insurance Sector Briefing: Delivering the Tiner Insurance ReformsPage 16

think through the types of issues that they need to consider when making decisions abouttheir investments. We will be looking at other ways of improving consumer understandingof with-profits.

2.32 Since their launch in 2001, our comparative tables now cover a wide range of products -including personal and stakeholder pensions, investment bonds and pension annuities.16

This is a web-based service to help consumers compare the features of a range of financialproducts, giving data on 220 different products from around 60 different providers. Wewill also be looking at incorporating meaningful measures of with-profits insurance firms’financial strength in the tables, once the new realistic reporting regime (as described in thenext chapter) has bedded down.

Liberalised framework for financial advice2.33 The final major component of this aspect of the reform programme relates to the delivery

of a liberalised framework for financial advice.

Depolarisation and the new basic advice regime for stakeholder products

2.34 At the end of 2004 we introduced new measures to reform the way in which retail financialproducts are sold to consumers.17 Improved disclosure, transparency and greater consumerchoice under the new regime should bring significant benefits. Following a six monthimplementation period, all companies will need to comply with new rules on 1 June 2005.

2.35 The introduction of the new basic advice regime for ‘Sandler’ products in April 2005 willalso contribute to the changing dynamic of the distribution of retail investment products inthe UK. The new regime for basic advice will offer a simpler, quicker and lower-cost formof advice to consumers interested in buying the new stakeholder products. In developingthis, our aim has been to ensure it will provide adequate protection to consumers.

2.36 We recognise that the move from policy development to implementation may impact on thestructure of the retail market and we remain alert to any risks that may emerge. We willmonitor developments closely to determine whether depolarisation and basic advice havedelivered the intended benefits of enhanced competition and consumer choice.

2.37 As part of depolarisation, we have introduced requirements for firms to produce two newdisclosure documents to increase transparency and to help consumers gain a betterunderstanding of the choices available to them.

2.38 The Initial Disclosure Document sets out the scope of advice that a firm can offer and willinclude information about its product range. In addition, firms will also be required toproduce a fees and commission statement upfront. Commonly known as the ‘menu’ thiswill disclose a firm’s cost of advice and will help consumers to identify, understand andcompare key information before buying financial products.

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 17

16 Comparative data on mortgage endowments was withdrawn in August 2004 due to the low number of product providers.

17 This was the culmination of a fundamental review of financial advice, which concluded that the old polarised regime hinderedcompetition.

A new conduct of business regime for general insurers 2.39 Although not included in the scope of the Tiner Reforms, another key change to the

regulatory regime for insurers has been the introduction of a new conduct of businessregime for general insurers and intermediaries.

2.40 Following two years of extensive consultation, on 14 January 2005 we started regulatingthe sale and administration of non-investment insurance contracts by insurers andintermediaries. This extension of our remit stemmed from the Government’s decision toimplement the Insurance Mediation Directive (IMD) through FSA rules and to introduce alevel playing field by applying conduct of business regulation to insurers. It involves around40,000 firms and Appointed Representatives in all including around 14,000 firms that wereauthorised for the first time. We hope that those new to regulation will seek to capitalise onthe advent of statutory regulation to modernise their processes and business models.

2.41 Much of the new regime reflects EU directive requirements. Where we have gone beyonddirective requirement we have tailored our approach so that it is proportionate to the risksassociated with insurance mediation and reflects the diverse and complex nature of the market.

2.42 The requirements of the new regime include the following:

• High-level standards, including the Principles for Businesses and the need for firms tohave adequate systems and controls.

• The Insurance: conduct of business sourcebook (ICOB), which sets out the standardsfirms must meet when selling insurance – including the information they must givecustomers about insurance policies and the mediation service they are providing. TheICOB rules also set standards insurers must follow when handling claims. Many of theserules reflect various directive requirements. Different rules apply to commercial and retailcustomers, with the rules for the latter providing a greater degree of protection.

• Financial resource requirements, including a requirement for intermediaries to holdprofessional indemnity insurance and to operate segregated trust accounts if they holdclient money (both of which reflect requirements of the IMD).

• Complaints and compensation arrangements. We have extended the compulsoryjurisdiction of the Financial Ombudsman Service (FOS) to insurance intermediaries andbrought them within the scope of the Financial Services Compensation Scheme (FSCS).

2.43 The new regime will benefit consumers through: clearer product information in the formof a Key Facts policy summary that sets out any significant and unusual exclusions;standards to ensure that any policy recommended to them is suitable for their needs; andaccess to the FOS if the firm does not resolve their complaint and to the FSCS if the firmgets into financial difficulty or becomes insolvent.

Insurance Sector Briefing: Delivering the Tiner Insurance ReformsPage 18

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 19

3.1 The previous chapter sets out what we have done to help ensure that consumers get a fairdeal. Principally, these reforms focus on the interface between the customer and theinsurance firm or intermediary. However, insurance firms also need to be soundly managedand have adequate financial resources. This chapter describes the changes that have takenplace since 2001 to support sound management practices and to place the industry on amore robust financial footing.

3.2 Our reforms seek to deliver the following outcomes:

• adequate financial resources;

• sound management; and

• streamlined financial reporting.

3.3 The rules and guidance on prudential standards and systems and controls for insurers arenow incorporated in the Prudential Sourcebook, which came into effect on 31 December2004. For large firms with with-profits liabilities in excess of £500m this introduced therequirement to produce a realistic balance sheet – including provisions for discretionarybenefits and a risk-based capital requirement. For general insurance business an EnhancedCapital Requirement (ECR), again on a risk-based approach, must now be calculated andreported to us. Addressing concerns over the role of actuaries in life insurers, we have alsointroduced an entirely new framework, which has involved abolishing the role ofAppointed Actuary. Our reporting requirements, which remain in the Interim PrudentialSourcebook for insurers, have also been updated to reflect the new regime.

3.4 In addition, we have overhauled the way we regulate the Lloyd’s of London market,bringing this into line with the way we regulate the rest of the insurance sector.

Adequate financial resources

New capital requirements

3.5 It is widely recognised that the existing capital requirements for insurance companies as setout by the European Directives are inadequate and not sufficiently risk-sensitive. Andalthough the EU’s Solvency 2 programme to reform the current directives is ongoing, theframework has not yet been determined and implementation is still some years away. For lifeinsurers writing with-profits business, the previous capital requirements effectively allowed

3.Soundly managed insurance firmswith adequate financial resources

Insurance Sector Briefing: Delivering the Tiner Insurance ReformsPage 20

insurance firms to ignore some significant non-contractual promises – including policyholders’expectations that they would receive a fair terminal or final bonus. Even for contractualoptions or guarantees to pay minimum benefits, firms’ measurement approaches were not asrobust as might have been expected. Previous provisioning and capital requirements forgeneral insurers were also generally too low and not sufficiently risk-responsive.

3.6 Regulators in the UK and a number of other EU member states have recognised theshortcomings of the current directives, but in practice have adopted differing approaches toimprove prudential regulation. In the UK, for example, historically we have typicallyexpected with-profits life insurers to hold a minimum of around two times the EU solvencymargin requirement. A similar ‘rule of thumb’ applied to non-life firms depending on theirlines of business. In comparison, other EU regulators expect insurers to include margins forprudency in provisions for claims. Despite the plans for Solvency 2, which are discussed inmore detail below, we felt it was essential to reform our domestic capital adequacyframework without delay. This is because of the significant weaknesses in the statutoryregime for life insurers that were exposed in the bear market of recent times, and the increasein the number of non-life insurers going into run-off due to their inability to raise newcapital. As such, we moved ahead of the Solvency 2 timetable to introduce a new solvencyregime for the UK. Our new regime provides a framework which facilitates the systematic,risk-sensitive and more transparent consideration of the adequacy of a firm’s financialresources. We also think it will have a positive impact on the way in which general insurancefirms manage the underwriting cycle, as the ECR is less sensitive to falls in premiums.

3.7 We have also introduced new rules for insurance groups, including implementing theFinancial Groups Directive. These cover the calculation of the group solvency position forgroups headed by an insurance holding company, as well as the calculation of the adjustedsolo position. For insurance groups headed by an EEA insurance holding company, a‘hard’ group solvency test will apply from the end of 2006 with public disclosure of theresult from the end of 2005.

Life insurers

3.8 For with-profits life insurers, the new regime is built upon what we term the ‘twin peaks’approach. This requires life firms that have with-profits liabilities in excess of £500m tomake a realistic assessment of their with-profits liabilities (including discretionary benefits)and of the associated risk-based capital based on specified stress and scenario testing (the‘realistic peak’), to determine whether they need additional capital to that determined bythe regulatory basis, excluding any allowance for future annual or final bonuses (the‘regulatory peak’ based on current directives).18

3.9 Since June 2002, firms have been preparing for this fundamental change by submitting tous realistic numbers on a six-monthly basis. Our regulatory requirement to adopt marketconsistent modelling of assets and liabilities has required with-profits firms to enhance

18 Life offices with liabilities in excess of £500m make up around 97% of the market. Those with-profits firms with liabilities of lessthan £500m have the option of adopting the ‘twin peaks’ approach, but are not obliged to do so. They are, nevertheless, stillrequired to hold capital to the EU minimum and meet our threshold conditions.

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 21

their systems and processes significantly. Firms have risen to this challenge and as result wenow have in place a more appropriate measurement of the liabilities of with-profits lifeinsurers. In line with the three pillar Basel structure, we have also introduced arequirement for full disclosure of the methods and assumptions used by firms for theirrealistic asset and liability calculations. As we go to print, the new realistic balance sheetsare due to be published, but data for end-June 2004 showed that all with-profits firms hadmet the new requirements, with an aggregate realistic surplus across the sector of £23bn.

3.10 In moving to realistic reporting, many firms recognised they had not quantified someliabilities accurately in the past and so had failed to establish appropriate levels of capitalto match all their liabilities.19 Consequently, a number of funds needed additionalfinancial resources. If a firm is unable to raise additional capital in such a situation, it mayhave to consider reducing benefits to policyholders. Sometimes known as ‘managementactions’ this can take a number of forms including, for example, cutting allocations orpayouts, reducing the equity backing ratio, or charging policyholders explicitly for theguarantees given. Such management actions are an acceptable part of the running of awith-profits fund, so long as the firm continues to treat its policyholders fairly. In 2004,we did a significant amount of work to ensure that realistic balance sheets were fair topolicyholders and consistent with firms’ PPFM. How firms ensure they hold adequatecapital is for them to decide. However, we are properly concerned that firms have an assetmix and capital resources which enable them to meet their commitments to policyholders.

3.11 We will review whether to extend the realistic approach to non-profit business and whetherto make it compulsory for small firms to adopt a ‘twin peaks’ approach at a later stage.

Case study: regulatory pragmatism in response to market conditions

Although we planned to introduce realistic reporting to all with-profits firms withliabilities in excess of £500m for the end of 2004, when markets fell in 2002 and again in2003 many life offices were feeling the pressure to engage in ‘forced’ selling of equities. Soin January 2003, we wrote to all chief executives of life insurance firms to explain ourproposals to move to the realistic method of reporting and pointing to the optionsavailable. In particular, we indicated that for well-managed and strong firms, we wouldconsider favourably applications for a waiver or modification to the rules on thecalculation of certain liabilities. This was provided that firms continued to meet the EUsolvency requirements and the minimum requirements of the realistic approach. In doingso, we effectively accelerated the introduction of realistic reporting, giving firms greaterflexibility in the face of volatile market conditions.

19 Notwithstanding this, the industry has largely welcomed the new regime, with a number of the larger insurance companiespublicly supporting the FSA’s moves to develop and introduce realistic reporting.

Insurance Sector Briefing: Delivering the Tiner Insurance ReformsPage 22

General insurers and reinsurers

3.12 For general insurers and reinsurers the new regime is similarly more risk-sensitive, withcompanies required to calculate an ECR. This aims to take account of the levels of riskinherent in different types of assets. The ECR will remain a ‘soft test’ for the time being.20

3.13 The ECR forms part of our considerations in setting Individual Capital Guidance (ICG). ICGmay be set at a higher level than a firm’s Solvency 1 capital requirement (the MinimumCapital Requirement, or MCR). For some, there may be no impact because the companyalready holds capital at, or above, the level at which ICG is set. Others will need to respond,for example by raising new capital or by reducing the risks they face or underwrite.

Individual Capital Adequacy Standards (ICAS) framework

3.14 Our individual capital adequacy framework recognises that a standardised approach todetermining capital requirements may provide an appropriate treatment of a typicalpresentation of risks. But it cannot adequately reflect each firm’s individual risk profile. SoICAS provides a framework for systematically considering the individual financial resourcesrequirement of each insurer. In essence, the senior management of an insurer must carry out itsown assessment of how much capital the firm needs given its business model and risk appetite.This is submitted to the FSA and we then make our own assessment of whether this is anappropriate level of capital for the company. We then issue ICG reflecting our own assessmentof how much capital is required to support an insurer’s individual risk profile.

3.15 All insurance firms are now required to have completed their Individual CapitalAssessment (ICA), and we will be reviewing these in a risk-based sequence over the comingtwo and half years. The new framework allows us to be proactive in monitoring thefinancial soundness of individual insurers, with the introduction of ICG providing us witha clear regulatory intervention point. We recognise that this is a developing field and lookforward to the benefits the new regime will bring.

European directives and International Accounting Standards

3.16 The Tiner Reforms focus exclusively on modernising the domestic regulatory regime forinsurers. However, the new prudential requirements must be seen against a widerbackground of relevant European insurance directives and international developments,many of which could have major implications for the UK regime. Many of these will notbe resolved in the short term. Now that the domestic regime is largely in place, much ofour focus will be directed at EU and international developments to help secure outcomesthat are not incompatible with the new UK regime.

Solvency 2

3.17 Of all these developments, Solvency 2 could potentially have the greatest impact for theinsurance sector. We take this very seriously and have committed significant resource tothe Committee for European Insurance and Occupational Pensions Supervisors and insupport of HM Treasury.

20 As a soft test, the ECR is reported to us on a private basis. Clearly though, firms are still required to meet our threshold conditions.

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 23

3.18 As described above, the case for a thorough root-and-branch reform of solvency in Europeis clear. The existing regime is not sufficiently risk-sensitive and market developments havehighlighted the framework’s inadequacies. Our decision to introduce a more risk-sensitivesolvency regime in the UK underlines the importance and urgency we attach tomodernising insurance regulation.

3.19 As with our domestic regime, we believe that the three-pillar framework adopted in Baselfor banking is also suitable for the insurance sector. As such, we advocate the importance ofrisk responsive pillar 1 capital requirements, the pillar 2 supervisory review (including theability to set individual capital requirements above the pillar 1 requirement as necessary)and the pillar 3 disclosures to harness market discipline. We strongly support thedevelopment of Solvency 2 as a crucial step in securing adequate consumer protection andstable markets. We are pleased to be able to share our experiences of introducing a risk-based capital regime with our European partners through the Solvency 2 working groups.

3.20 Although a Commission proposal for a Framework Directive is not expected until 2006(with implementation anticipated in 2010), the pace of developments is starting to pick up.As such, it will become increasingly important that firms also begin engaging with theproposals to introduce a revised pan-European solvency framework.

Reinsurance Directive

3.21 The Reinsurance Directive is intended to create a single market in reinsurance (similar tothat which already exists for direct insurance) and to remove remaining barriers to tradewithin the EU, such as supervisor-imposed collateral requirements. This would allow purereinsurers to write business cross border within the EU, based on home country prudentialsupervision. The directive is intended to be an interim measure, generally applying therequirements of the current Solvency 1 Directives for direct insurers to reinsurers. A fullre-examination of reinsurers’ solvency requirements is expected as part of Solvency 2.

3.22 As one of the member states which already supervises pure reinsurers in essentially the sameway as direct insurers, and in the light of the interim nature of the directive, our intention inthe negotiations has been to establish a sound and prudent regime which does not imposeadditional requirements on pure reinsurers which are not justified on prudential grounds.We will continue advising HM Treasury and UKREP as required and, if the Directive isadopted, will consult on implementation within the UK. It is possible that we will consulton implementation in the first half of 2006, with implementation at the end of 2007.

International Accounting Standards (IAS)

3.23 The International Accounting Standards Board (IASB) has issued an interim standard onaccounting for insurance contracts (IFRS 4) while it continues to develop a robust long-term solution. The interim standard permits insurers moving to IASs to continue with theirexisting accounting policies for insurance contracts (with some exceptions) or to changethem so long as the changes are consistent with the IASB’s declared long term objectives.Following the Penrose Report, the UK Accounting Standards Board rapidly developed and

issued a new accounting standard on life insurance contacts (FRS 27), to apply in 2004.This would roll forward as existing GAAP when insurers moved to IASs in 2005. FRS 27was based on our realistic reporting regime for with-profits business.

3.24 The IASB has been working on long-term solution for insurance contracts since 1997. Inview of the continuing controversy over accounting in the financial services sector, theIASB has recently announced it will go back to first principles on insurance and has set upa new advisory committee. Although any standard is unlikely to be introduced before2009, it is expected to reflect the time value of money. We will continue to monitordevelopments very closely.

Sound management3.25 As well as delivering capital adequacy, the new prudential rules impose requirements on

firms to maintain effective risk management practices. Identifying, assessing and managingrisk is a fundamental part of good business management and features strongly in all of ourrequirements for insurance firms. It is greatly encouraging that even at this early stage ofthe new regime, the industry also recognises the commercial benefits of developing goodrisk management practices.21 These are essential for responding to emerging risks, such aschanges in longevity and legislative outcomes.

3.26 There is, however, plenty of scope for improving current risk management practices. In2003, we carried out our own research into the risk management practices and proceduresin the UK insurance industry.22 It is clear that, since we began carrying out riskassessments in 2001, many insurers have improved the way they manage risk. The reviewidentified a number of positive developments – for example, most firms had made goodprogress in putting in place processes that will enable better identification, assessment andcontrol of risk, such as senior management committees, risk assessment functions andmanagement information. Against this steady improvement, however there were, pocketsof weakness. These included: lack of independent and objective assessment of risks; under-developed or in some cases un-defined risk appetites; poor quality of managementinformation; a lack of consideration of risks arising from the operations of other groupcompanies; and a lack of co-ordination between internal audit, risk assessment functionsand those responsible for assessing capital requirements.

3.27 We plan to repeat the study of risk management practices in 2006 to ascertain the impact thatour reforms have had on this important aspect of the management of an insurance company.

Systems and controls

3.28 The Interim Prudential Sourcebooks for insurers and friendly societies (IPRU) and the Lloyd’ssourcebook (LLD) included less detailed guidance on some aspects of systems and controls in

Insurance Sector Briefing: Delivering the Tiner Insurance ReformsPage 24

21 In a recent survey of European Property and Casualty insurers, an overwhelming 95 per cent of respondents agreed that effectiveand competent risk management can reduce solvency capital requirements (Risk and Capital Management for Insurers: a KPMGInternational Survey of Capital Assessment Practice, November 2004).

22 Review of UK Insurers’ risk management practices (October 2003).

comparison with the sourcebooks for other financial services sectors. As a consequence, wehave introduced new and more extensive guidance for insurance companies on:

• high-level controls (including the composition and role of the governing body,apportionment and definition of management responsibilities, and the audit committee);

• responsibilities of the risk assessment function;

• internal audit (including its mandate and reporting lines, audit plans and reports, andoutsourcing);

• management information needed to identify, measure and control risks in the business;

• outsourcing (including issues to consider, contracts with suppliers and service levelagreements); and

• risks arising from a company’s relationship with the rest of the group to which it belongs.

These have now been incorporated into the Prudential Sourcebook.

3.29 High-level operational risk systems and controls requirements, where the risks areorganisational rather than prudential, have been relocated to SYSC 3A. Theserequirements came into force for insurers at 31 December 2004 and cover:

• people;

• processes and systems;

• external events and other changes;

• outsourcing; and

• insurance.

Financial engineering

3.30 In 2002, we consulted on our regulatory approach to insurers’ use of financial engineering.We indicated that, if properly constructed and presented, financial engineering can be avalid method of strengthening a firm’s solvency position so long as there is a genuine andmaterial transfer of risk to an unconnected counterparty. We also made clear that financialengineering could potentially be used to obscure the underlying financial condition of acompany, thereby misleading consumers and/or regulators.

3.31 For life insurers, the introduction of realistic reporting and other changes to the AnnualReturns (such as the Valuation Report) help make more transparent the extent to whichthe balance sheet is supported by such arrangements and the nature of the arrangementsput in place. We have amended our rules and guidance to reflect the phasing out ofimplicit items by the end of 2009, in line with the Solvency 1 changes to the ConsolidatedLife Directive.

3.32 We are currently establishing the extent to which general insurers engage in financialengineering (for example through the use of finite reinsurance) and what systems andcontrols they impose over this type of business. We will be doing more targeted thematicwork on this in the coming period and considering enhanced disclosure.

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 25

The role of actuaries in life offices

3.33 The With-profits Review, and the Baird investigation into our regulation of Equitable Life,identified a number of significant weaknesses in the appointed actuary regime. These weresubsequently confirmed by the Penrose Report. These included ambiguity about seniormanagement responsibilities, the potential for conflicts of interest to arise and theexclusion of the valuation of policyholder liabilities from the external audit.

3.34 To address these weaknesses, we have made significant changes to the role of actuaries inlife offices. These improvements were recently endorsed by Sir Derek Morris in his reviewof the Actuarial Profession.23

3.35 The key reform has been abolishing the role of Appointed Actuary at the end of 2004, andreplacing it with two new advisory functions:

• the actuarial function (applicable to life insurers); and

• the with-profits actuary function (only for firms carrying on with-profits business).24

3.36 Holders of these roles require prior approval from the FSA and are subject to thewhistleblowing requirements that previously applied to appointed actuaries. Individualsholding these roles are prohibited from being chairman or chief executive of the firm orfrom holding any other position that could give rise to a significant conflict of interest –including, in the case of the With-Profits Actuary, from being a board member.

3.37 The actuarial function has a range of specified responsibilities, which include: advising thegoverning body on the firm’s ability to meets its policyholder liabilities and the methodsand assumptions for the valuation of these liabilities; calculating these liabilities andreporting the results to the governing body; and monitoring the insurer’s financial positionand advising on how much capital is needed to support its business.

3.38 Complementing this, the with-profits actuary is responsible for advising the governingbody on its use of discretion within the with-profits fund as this relates to the fairtreatment of policyholders. This is an area where there may be particular tensions betweenpolicyholder interests and those of management and any shareholders. The with-profitsactuary is required to make a formal report to the governing body at least once a year onkey aspect of the firm’s use of discretion. In an important improvement in transparency,the with-profits actuary is also required to make an annual public report on whether thefirm has taken proper account of policyholders’ interests when exercising discretion.25

3.39 Policyholder protection has also been augmented by broadening the scope of the audit toinclude the valuation of policyholder liabilities as well as the firm’s assets. Auditors arerequired to seek actuarial advice on the valuation of liabilities from a reviewing actuarywho is independent of the firm, relating both to the regulatory and realistic peaks.

Insurance Sector Briefing: Delivering the Tiner Insurance ReformsPage 26

23 Morris Review of the Actuarial Profession (March 2005).

24 Both of these are controlled functions as defined by the Supervision manual.

25 Please also see paragraph 2.11 on the with-profits actuary.

3.40 The reviewing actuary is required to give advice on, amongst other things, whether in theiropinion the firm’s methods and assumptions for calculating reserves for liabilities werereasonable; the calculations of reserves have been conducted in line with our requirements;and the capital requirements have been determined in line with our requirements.

Streamlined financial reporting

Regulatory and public reporting

3.41 The publicly available Annual Return for insurers is an important document which we useto help assess the financial condition of insurers and, particularly in the case of long-termbusiness, how they are meeting their obligation to treat customers fairly. It is also heavilyused by market analysts (including the rating agencies), consumer organisations, financialcommentators and others with an interest in insurance. The current format of the AnnualReturn has evolved over the years and has become complex and unwieldy, so much so thatit is difficult even for expert users to understand. The amendments we are introducing seekto make the returns more useful, as well as reflecting the changes that took effect on 31December 2004 with the introduction of the Prudential Sourcebook.

3.42 Specifically, the changes that took effect at end 2004 or are due to take effect from end2005 will:

• reduce the number of disclosures that firms have to make by, for example, notrequiring repeat disclosure of product terms from life insurers, and fewer businessclasses for non-life insurance firms;

• turn the life insurers’ Valuation Report into a mainly narrative document with a clearstructure;

• amend materiality criteria for reporting business to reduce the burden, in particular forsmaller companies;

• introduce standard classification of business to improve sector analysis;

• reflect the new realistic balance sheet requirements and capital calculation for with-profits (new forms 18 and 19 and the realistic valuation report); and

• require disclosures of pay-outs on specimen with-profits policies.

3.43 From December 2004, the Directors’ Certificate will contain statements regarding thepremiums for contracts entered into and mathematical reserves.

3.44 Mindful of the costs of regulation, we have not proposed more far reaching reportingchanges at this time due to the possible impact of the International Accounting Standards.As described above, these could affect the balance sheet information reported on theannual return. We will keep under review the information we collect using these returns toensure it remains appropriate.

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 27

3.45 The revised returns mark an important step in a longer-term programme to make the FSAeasier to do business with and to increase regulatory efficiency. We have begun a phasedreview of reporting requirements for all regulated activities, resulting in the revisedinsurance return. We have also introduced Mandatory Electronic Reporting (MER) ofregulatory data as FSA policy, which is being applied as the revised reporting requirementsare being rolled out or later if appropriate. For insurers the revised reporting requirementswhich took effect at end 2004 or are due to take effect from end 2005 will be submittedusing existing methods. We will announce the timetable for the application of MER in theautumn, but giving at least 12 months’ notice before introducing it.

Regulating Lloyd’s of London 3.46 As set out in the two previous reports on the Tiner Reforms, we decided to exercise more

directly some of our responsibility for the prudential regulation of insurance businessconducted at Lloyd’s, as we extended the risk-based approach to regulating insurance tocover the Lloyd’s market as well. Our two main areas of focus over the last two years havebeen to revise the prudential regime applying to Lloyd’s and to apply our risk assessmentframework to the managing agents operating in the Lloyd’s market, as well as to theSociety of Lloyd’s itself. The aim of these changes was to ensure that our rules and oursupervisory effort are directed at where risks are being managed.

3.47 In developing a new prudential regime for the Lloyd’s market, we sought to bring Lloyd’swithin the scope of the Prudential Sourcebook, taking into account the market’s structure andoperation. In particular, we introduced risk-based capital requirements for both the Society andthe managing agents, consistent with the approach we took for non-life insurance firms. Finalrules were published in December 2004 and the new regime became effective on 1 January2005 (with some rules having a delayed implementation date of January 2006 in response toconsultation). In the coming period we will consult on changes to the Lloyd’s return to reflectthe policy changes. The new prudential regime will help ensure that senior management at boththe Society and at managing agents focus effectively on their responsibilities and on the level ofcapital needed to support the risks of the insurance businesses they manage.

3.48 The second strand of the changed approach to Lloyd’s was to apply our risk assessmentprocess directly to the managing agents as well as to the Society. Having completed thefirst round of risk assessments of the managing agents, we are now re-assessing firms on arisk-based cycle. Assessing the risks at managing agency level, rather than just at a marketlevel, allows us to have a better understanding of them and to put in place remedial actionat the most effective level. In carrying out the risk assessments we have identified a numberof common risks across the market and have adopted a thematic approach to tacklingthese, such as managing the underwriting cycle.

3.49 In addition we also made an important step in improving policyholder protection bybringing Lloyd’s within the compensation arrangements under the Financial ServicesCompensation Scheme.

3.50 In making these changes, we have liaised with the Society to minimise any duplication ofeffort. The Society has made a number of significant changes to the way it operates. Webelieve the changes we have made to reflect the division of responsibility better, with theSociety managing the risks to the franchise and the FSA carrying out regulatory oversight.

Insurance Sector Briefing: Delivering the Tiner Insurance ReformsPage 28

Insurance Sector Briefing: Delivering the Tiner Insurance Reforms Page 29

4.1 The creation of a single regulator highlighted significant and untenable differencesbetween the regulation of insurance and of other sectors, both in terms of how regulationwas carried out and in terms of resourcing. In our first report on the Tiner Reforms, werecognised that, in addition to reforming the regulatory requirements for the insuranceindustry, there was a clear need to modernise the way we discharged our regulatory duties.Consequently, the reform programme has focused on delivering four key outcomes:

• implementing a proactive risk-based regulatory approach, including the deployingresources to areas of greatest risk;

• consolidating structural changes already made within the FSA to deliver an integratedapproach to the regulation of insurance firms, encompassing both prudential andconduct of business issues;

• developing more effective working relationships with those firms posing a greater riskto achieving our statutory objectives; and

• delivering insurance supervisors who operate effectively in the new environment.